The Piedmont Perspective – It Is Not About Oil. It Is About China and Russia and How Venezuela's Oil Wealth Relates to Them

The Move on Venezuela is About Much More than Oil

Executive takeaway

Venezuela’s regime change is not an oil supply shock but a network disruption that weakens Russia-China-Iran-Cuba gray zone operations, trims geopolitical and energy tail risks, and slows sanctions arbitrage at the margin. The result is modest support for the dollar, lower inflation volatility, and a slightly wider monetary policy runway without altering the Federal Reserve’s core reaction function.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 5, 2026

Mark Vitner, Chief Economist

Piedmont Crescent Capital

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Santa Rally, Silver & Gold, and a World That Will Not Sit Still

Highlights of the Week

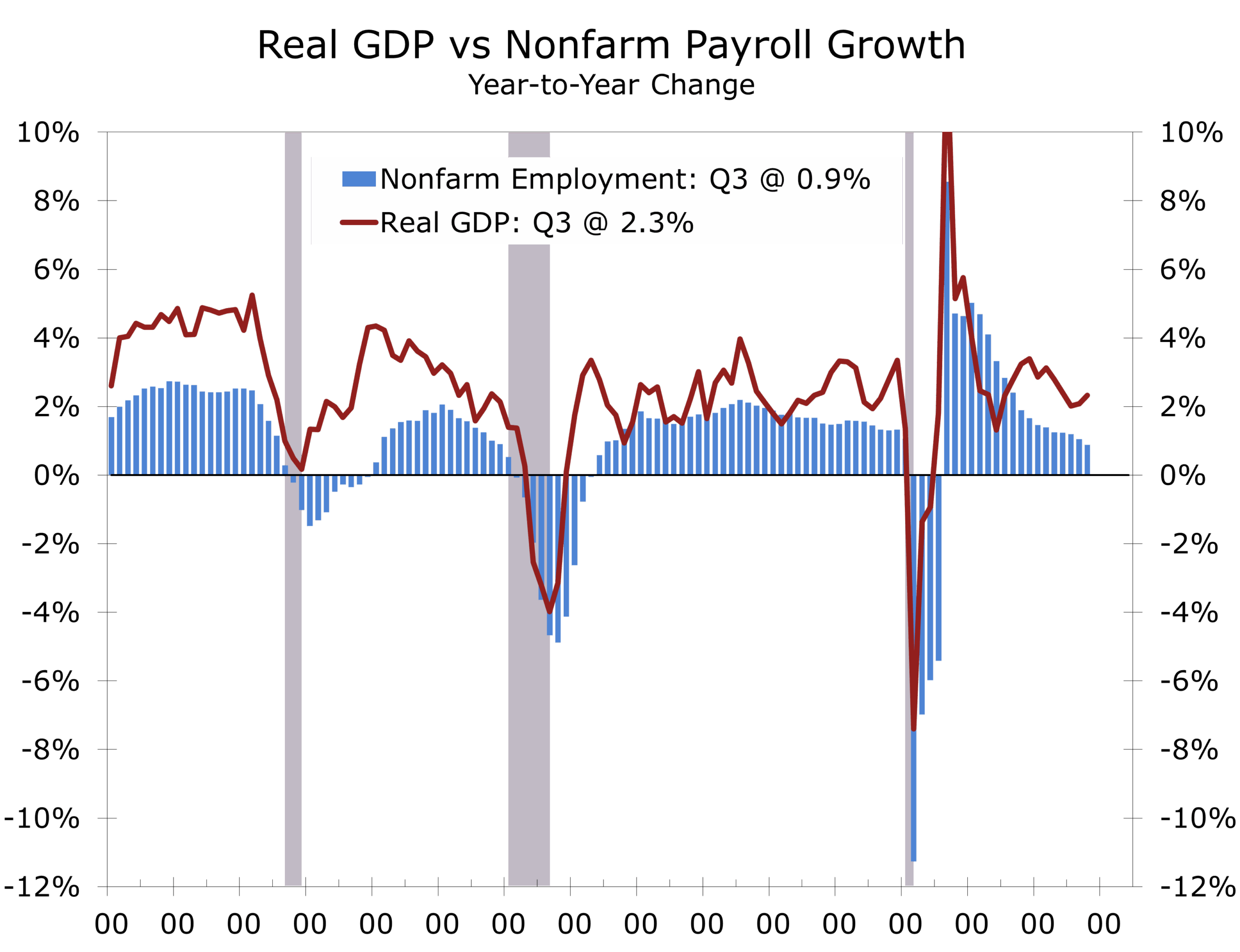

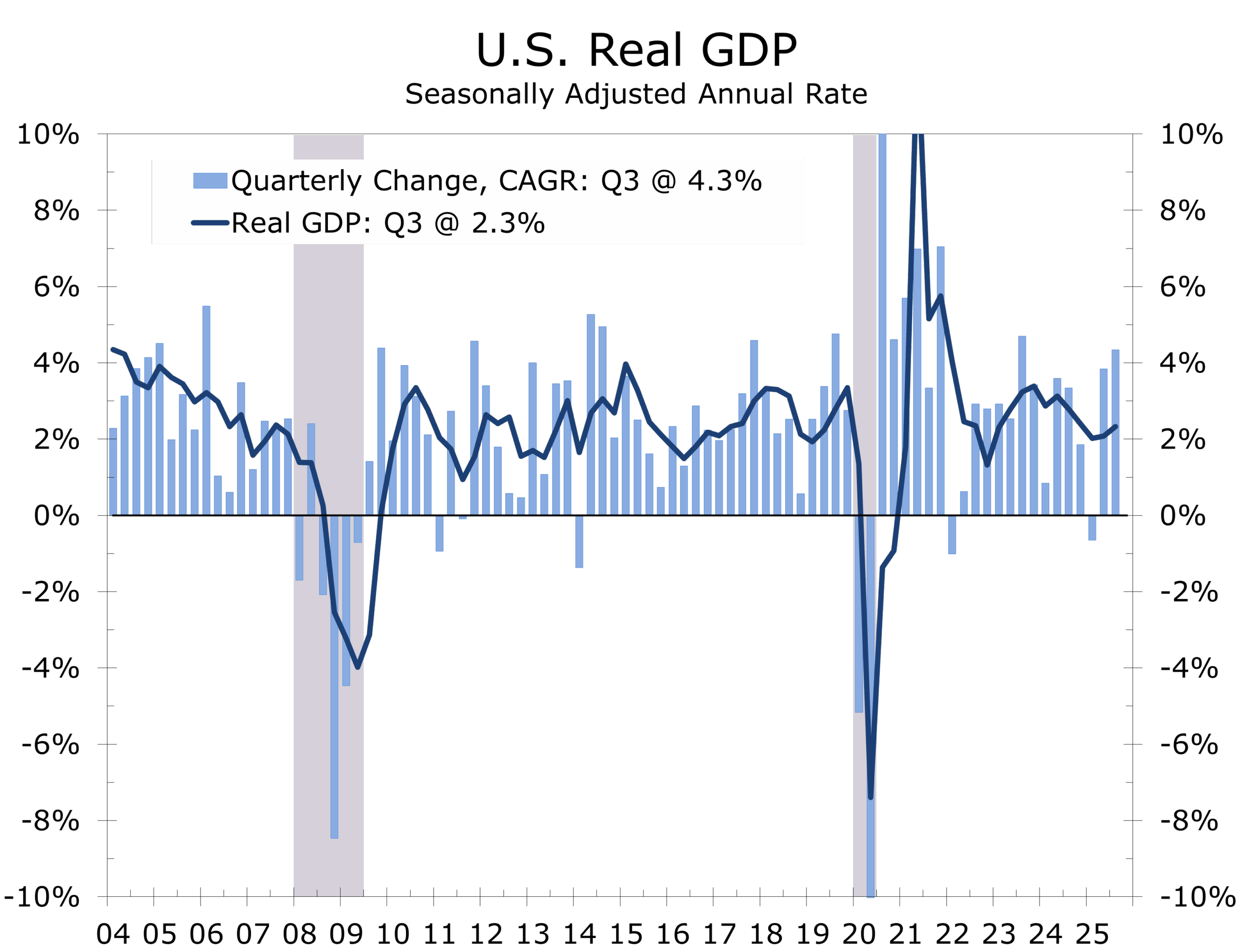

- Q3 GDP printed a robust 4.3% annualized pace, driven by strong consumer spending and AI-related investment.

- The labor market looks stable on the surface, with initial claims at 214k, but lower turnover and cautious hiring point to a more nuanced backdrop.

- Markets are pricing a gradual Fed easing cycle following the recent 25bp cut to 3.5%–3.75%, with CME data signaling a slow-and-steady approach.

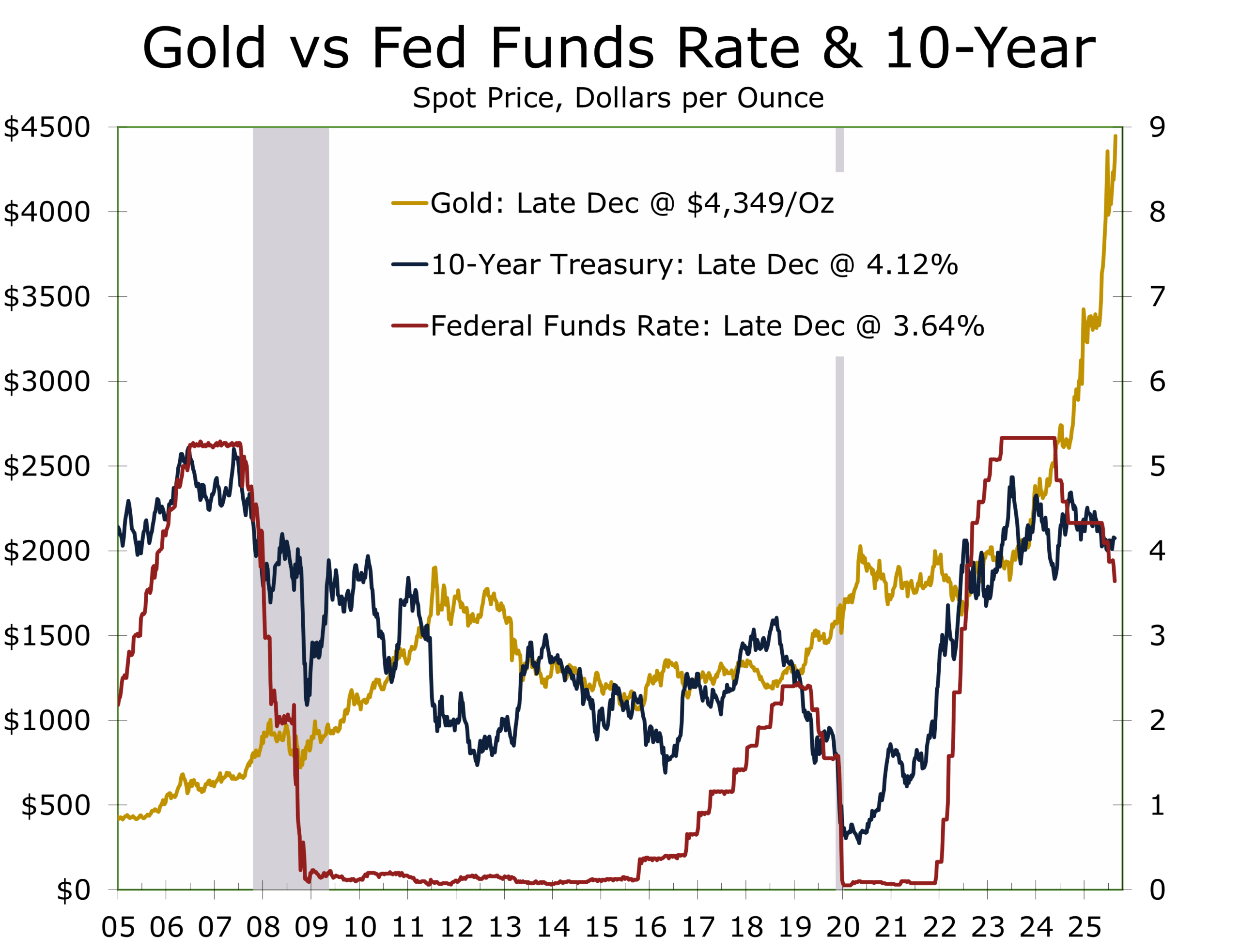

- Silver and gold shone brightly, like a familiar holiday tune, highlighting a shift toward hard asset hedging amid supply concerns and expectations of rate cuts.

- Geopolitical tensions remain front and center, with developments in Ukraine, the Middle East, and Taiwan underscoring a world that is anything but quiet

- 2025 is ending the way many past years have: optimism in the tape, anxiety in the headlines, and history reminding us that “quiet” is usually just a comma, not a period.

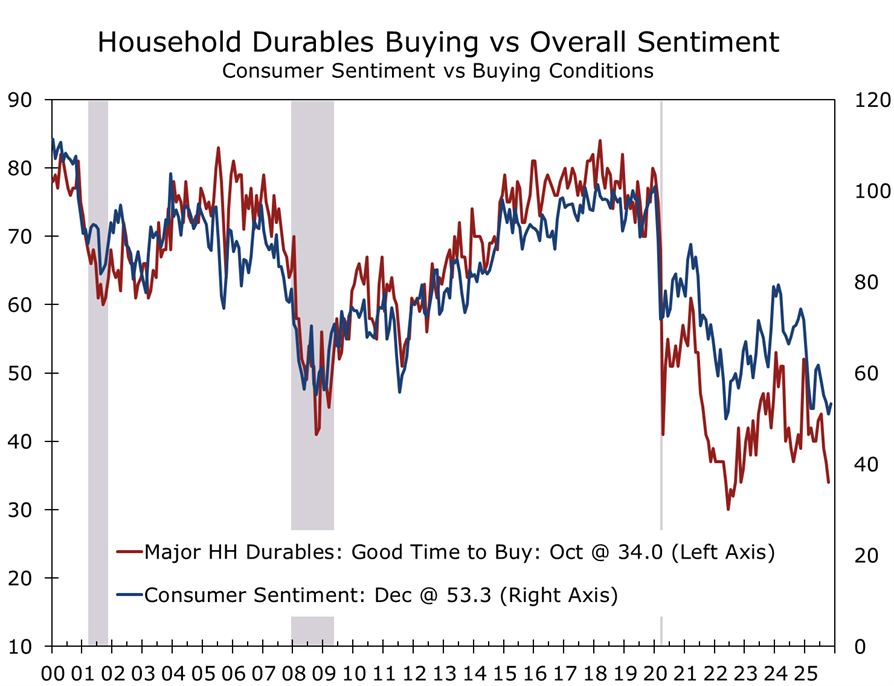

Gold, Growth, and a Job-Light Economy

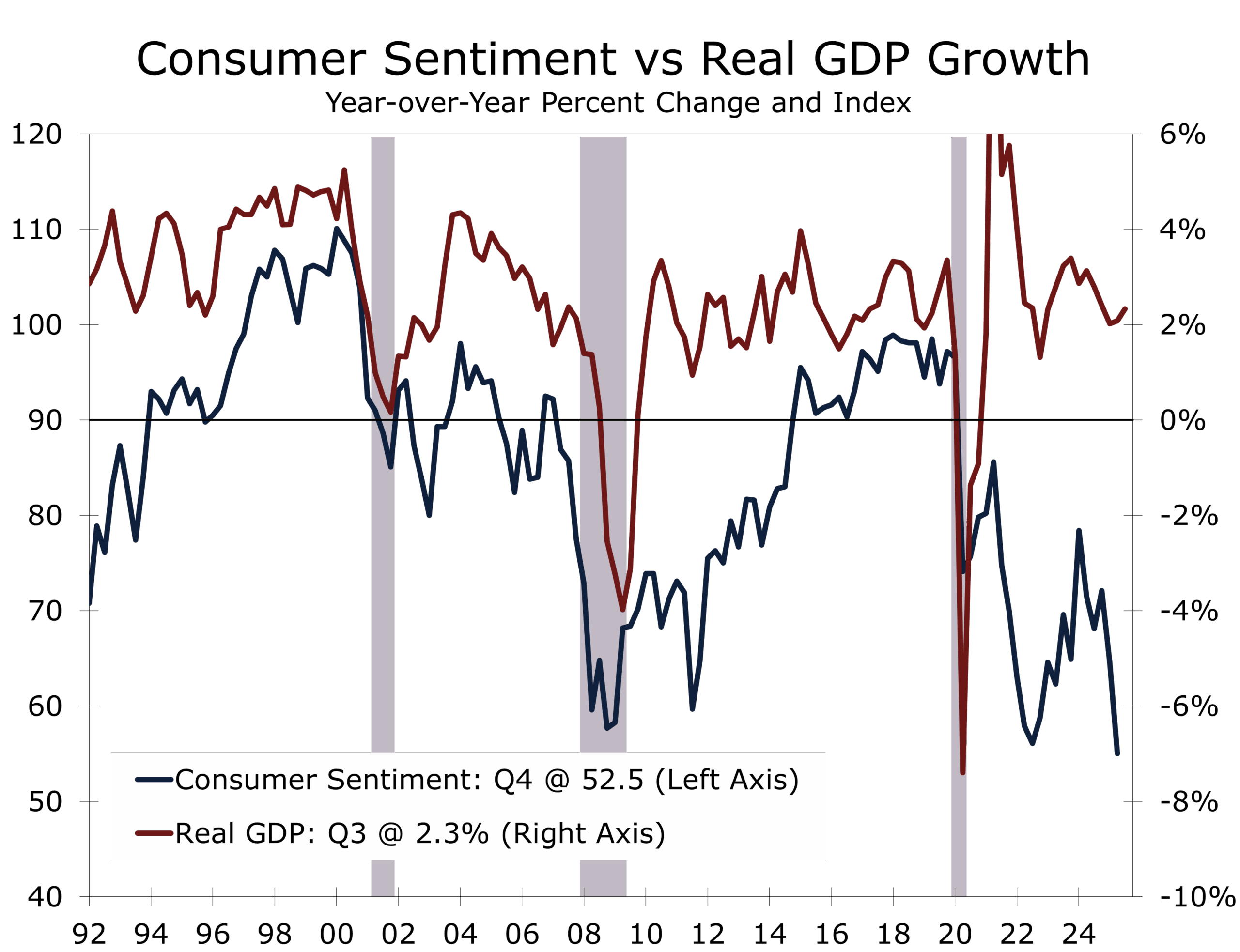

The final full week of 2025 delivered a familiar late-cycle paradox. The macro data still reads like an economy with plenty of altitude, with Q3 real GDP coming in at 4.3% annualized and up 2.3% over the past year, with growth powered by solid consumer spending and an AI-driven investment surge tied to reshoring and technology buildouts. Yet confidence data tells a different story. The economy increasingly feels like one experiencing vertigo.

Things appear to be spinning around the periphery. Consumer confidence fell again in December, with households citing employment and income concerns alongside the usual worries about inflation and politics. The message is not that the expansion is ending. Rather, progress is becoming harder to feel in real time. That disconnect is a defining feature of this job-light, capex-heavy cycle and shows up repeatedly in headlines about how difficult it remains for new entrants and re-entrants to secure employment.

The economy is growing, but the labor market is no longer the messenger.

Under the hood, the labor market is still behaving, at least in the narrow sense that matters for recession risks. Initial jobless claims fell to 214k in the latest week, a historically low level inconsistent with broad-based layoffs. But the labor picture is more nuanced. Turnover remains exceptionally low. With fewer workers voluntarily quitting, firms are hiring less aggressively. Layer in the effects of AI adoption, earlier over-hiring, and lingering reluctance to trim payrolls after the pandemic, and the result is a labor market that looks calm on the surface while quietly adjusting to a more cautious, lower-churn footing.

Labor market uncertainty remains one of the largest open questions for the economy and the 2026 outlook. Revised employment data due early next year are expected to show that job growth slowed sharply in late 2025 and may have briefly turned negative. That would be unusual for an expanding economy. Historically, even modest employment declines have tended to coincide with the onset of recession.

Not every hiring slowdown signals a recession. This job-light expansion appears to be by design.

This cycle may be different, which remains the most dangerous phrase in forecasting. Productivity gains, capital investment, and deliberate talent retention are playing a larger role than broad-based hiring. Rather than an expansion riding a wave of payroll growth, today’s economy is advancing with leaner workforces and stronger productivity, a possible sequel to the “New Economy” dynamics of the late 1990s. Growth is being powered less by headcount and more by automation, efficiency, and strategic staffing, including retaining experienced workers, selectively outsourcing, and relying more heavily on contract and temporary labor.

Markets appear to be reading from the same script. Risk assets are closing the year on a firm note, but the more revealing signals came from hedges rather than headlines. A weaker dollar and a renewed bid for precious metals, specifically silver and gold, echo a familiar holiday refrain from Rudolph the Red-Nosed Reindeer that is now hard to get out of my head. These moves suggest investors are positioning for a sequel economy defined less by labor abundance and more by real constraints, including power availability, debt capacity, and the ability to absorb and deploy rapid gains in artificial intelligence.

Markets are hedging constraints, missing data points, and policy uncertainty—not contraction.

Part of the move reflects rate-cut expectations and renewed questions about Federal Reserve independence. It also points to growing recognition that the industrial economy is colliding with bottlenecks in electrification-era inputs. Data center and power projects are crowding out other industrial projects at the margin. The tape is not signaling a crisis. Instead, it is quietly pricing a regime shift toward hard assets, supply security, and resilience premia in an economy running more on efficiency than expansion. One encouraging signal has been the recent strength in transportation stocks, which may be hinting at an end to the long-running freight recession.

Recent Developments: Signals Beneath the Noise

That resilience theme extends beyond economics into geopolitics. Ukraine is moving toward a negotiation framework, with a revised 20-point peace proposal reportedly under discussion with President Trump, even as the hardest questions around territorial concessions and security guarantees remain unresolved. In the Middle East, Trump and Netanyahu are preparing talks on the next phase of a Gaza plan, though the ceasefire architecture remains fragile, particularly following recent comments from Iranian leadership and the apparent launch of three satellites.

In Asia, China’s largest-ever drills around Taiwan served as a reminder that geopolitical tail risks are no longer confined to the margins. They are part of the main distribution. Trump’s more aggressive posture toward Venezuela and recent arms commitments to Taiwan may also be contributing to Beijing’s willingness to apply pressure on the island.

Looking Ahead

As we turn the page to the first week of the new year, attention will shift back to fresh economic data. The ISM manufacturing index, December’s employment report, and updated readings on consumer sentiment will help set the tone for how 2026 begins.

Before that, the coming week features a lighter calendar, offering a brief pause to recharge and, perhaps, watch a bit more football. Key releases include the FOMC minutes from the December 9–10 meeting on Tuesday, weekly jobless claims on Wednesday, and global and U.S. PMI indices from S&P on Friday. As always, we will be watching for evidence that reinforces or challenges the soft-landing narrative and tests whether the Fed’s cautious easing path remains appropriate. Our preference would be for cuts at alternating meetings, extending the easing cycle without materially lowering the terminal rate.

For now, the economy appears to be staying on script, marked by cautious optimism, an affinity for gold, and a world that never quite sits still.

As we close out 2025, we want to thank our readers and clients for the continued engagement and dialogue. We wish you a healthy, prosperous, and thoughtful New Year, and we look forward to navigating 2026 together.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 29, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

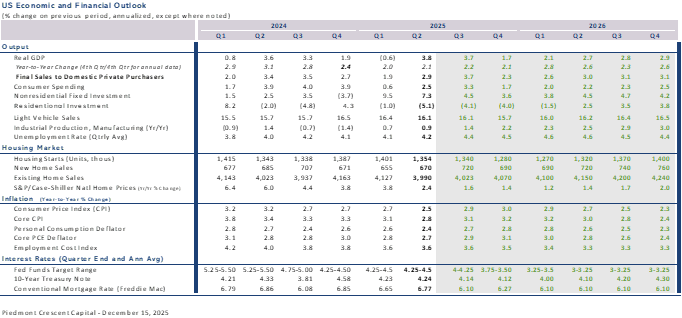

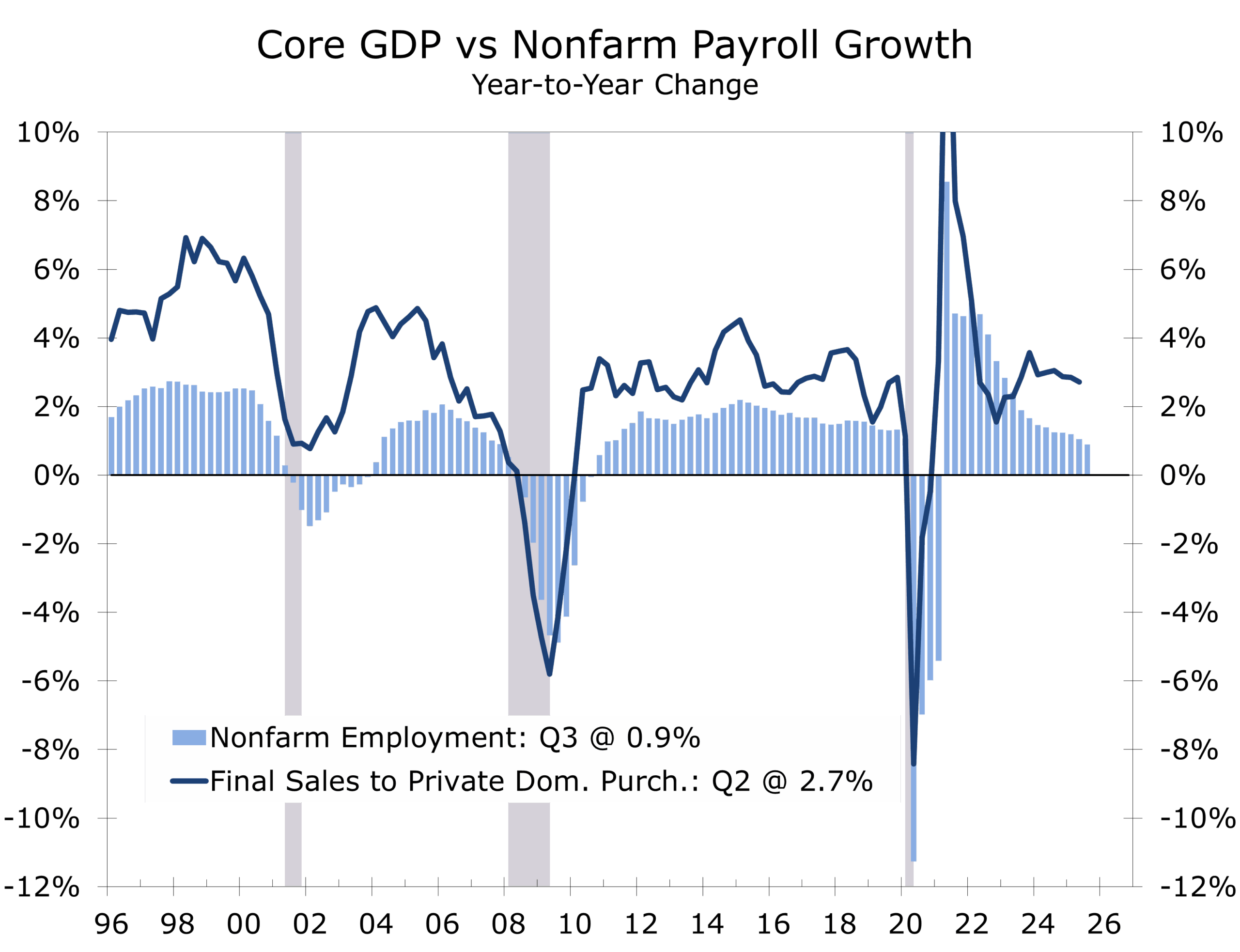

Third Quarter GDP Handily Tops Estimates

Growth Re-accelerates, but the Signal Is Nuanced

-

- Q3 real GDP jumped 4.3%, the fastest pace of 2025, but the headline was amplified by swings in trade, inventories, and government spending rather than a step-change in underlying demand.

- Core private domestic demand grew a solid 3.0%, maintaining its recent strong pace and confirming continued expansion.

- Consumer spending perked up, led by health care, travel, professional services, recreational goods, and prescription drugs, signaling ongoing resilience.

- Investment remained uneven, with further inventory drawdowns weighing on growth, particularly in manufacturing, trucking, and warehousing, while fixed investment held up better than the headline suggests.

- Inflation firmed at the margin, with core PCE rising at a 2.9% annual rate in Q3 and also climbing 2.9% over the past year. With tariff pass-through already visible in price data, the third quarter likely marked the high-water mark for trade-related inflation pressure.

- The third quarter delivered a headline surge in growth, but the signal beneath the noise points to a resilient—rather than overheating—economy, increasingly driven by business fixed investment and value-conscious consumer spending. This emerging mix should prove modestly disinflationary over time, easing the Fed’s balancing act.

A Strong Headline, Filtered Through the Noise

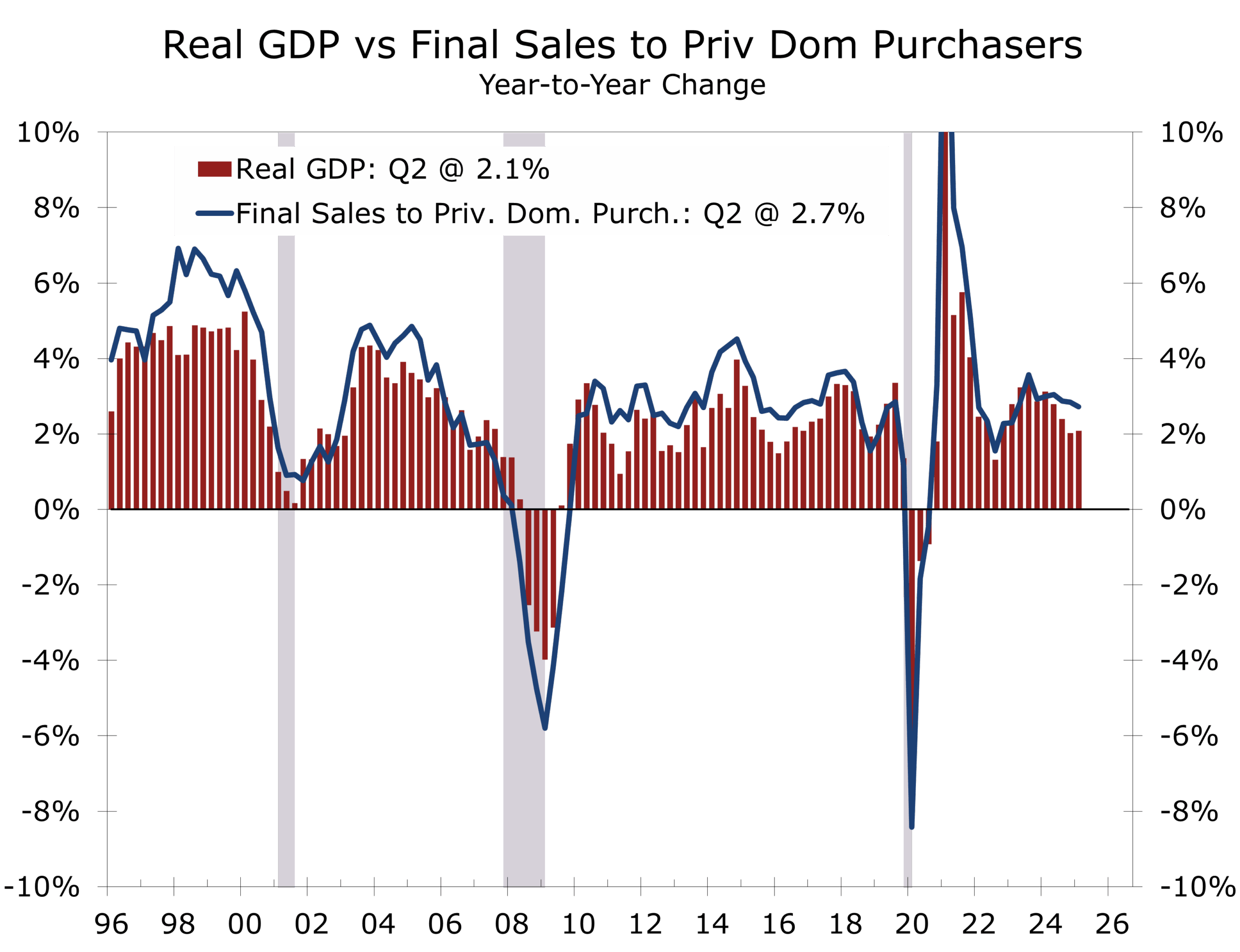

Real GDP accelerated sharply in the third quarter, rising at a 4.3% annualized pace, marking the strongest quarterly growth rate of 2025. On the surface, the report suggests a decisive reacceleration in economic momentum following solid growth in the first half of the year. Beneath the headline, however, the picture is more nuanced. Core private domestic demand advanced at a still-healthy but far less dramatic 3.0%, while the top-line surge was amplified by trade flows, inventory dynamics, and government spending, all measured through a release affected by the recent federal government shutdown.

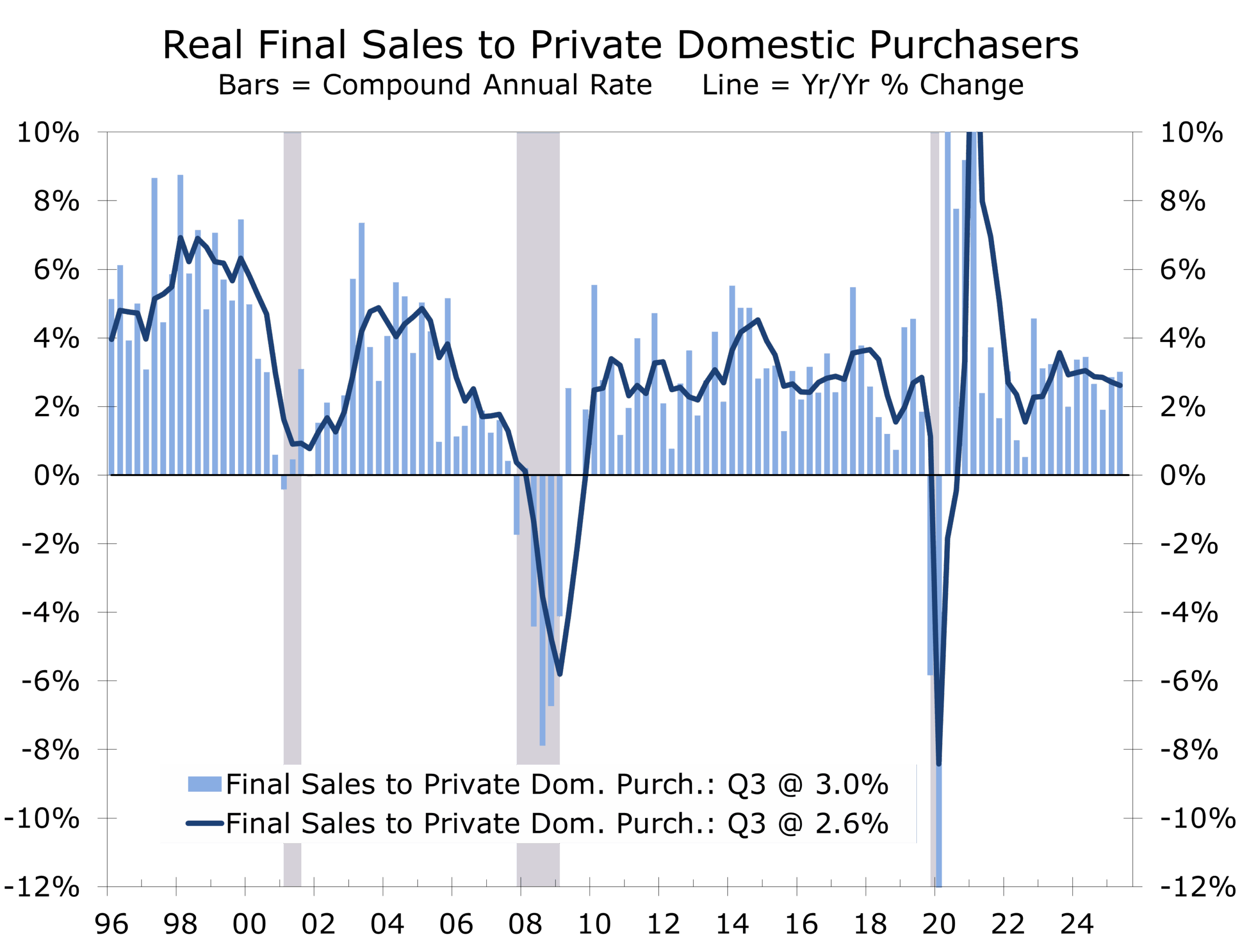

The economy is growing—but not at the breakneck pace the headline implies. We continue to stress that real final sales to private domestic purchasers provide a more reliable assessment of the economy’s underlying momentum.

Income-side measures reinforce this interpretation. Real gross domestic income (GDI) rose at a 2.4% pace, notably below the headline GDP gain and more closely aligned with trend growth in labor income and profits. Because GDI is constructed from wages, salaries, profits, and other income flows, it is typically less sensitive to short-term swings in trade and inventories that can distort GDP in any single quarter. Averaging GDP and GDI, which rose 3.4% in Q3, offers a more balanced read on underlying activity, particularly in a quarter affected by data disruptions.

Q3 growth was lifted by trade, inventories, and defense spending—but the economy’s core continued to expand at a steady, sustainable pace.

Historically, gaps between GDP and GDI tend to emerge late in the cycle, when investment surges, inventory swings, or policy timing inflate measured output even as income growth slows. A comparable episode occurred in late 1999, when headline GDP growth remained strong amid the tech boom, but GDI and labor income growth had already begun to cool, signaling that momentum was becoming increasingly concentrated in investment and asset-driven activity. In that period, GDP continued to look robust even as income-based measures provided an earlier warning that underlying growth was losing breadth.

Averaging GDP and GDI points to growth near the upper end of trend—not a breakout.

Core Domestic Demand Remains the Anchor

The cleanest read on underlying momentum comes from real final sales to private domestic purchasers, which grew at a 3.0% pace, slightly above Q2’s 2.9%. This measure, which strips out inventories, trade, and government spending, confirms that demand driven by households and businesses remains firmly expansionary.

Final sales to private domestic purchasers remain the most reliable signal—and they continue to tell a story of resilience, not acceleration.

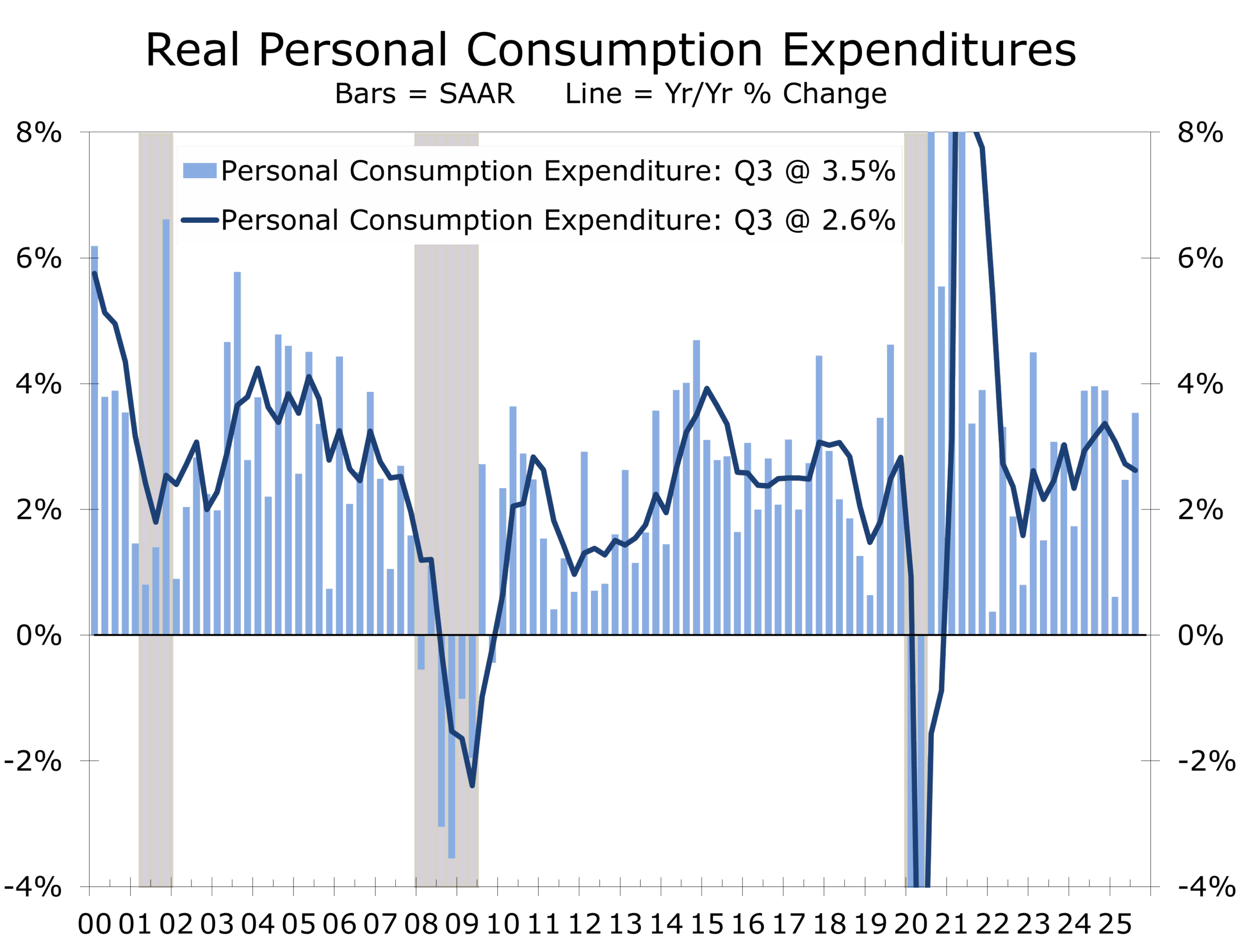

Consumer spending re-accelerated, with gains across both services and goods. Services spending was led by health care, international travel, and professional services, reflecting continued normalization in activity that had lagged earlier in the cycle. Goods spending was supported by recreational goods, vehicles, and prescription drugs, with information processing equipment again playing a notable role.

Real disposable income growth slowed during the quarter, suggesting that recent spending strength is being supported in part by a lower saving rate and wealth effects rather than accelerating labor income. The decline in saving was exacerbated by a spike in light vehicle sales, as households pulled purchases forward ahead of the expiration of attractive electric vehicle tax credits. Together, these dynamics reinforce evidence of a K-shaped consumer, with higher-income households driving discretionary categories such as travel, recreation, and professional services.

Part of the decline in saving reflects timing, not stress—vehicle purchases were pulled forward ahead of expiring EV tax credits.

This is not a consumer-driven boom, but it is a consumer that remains resilient in the face of elevated borrowing costs and ongoing affordability pressures.

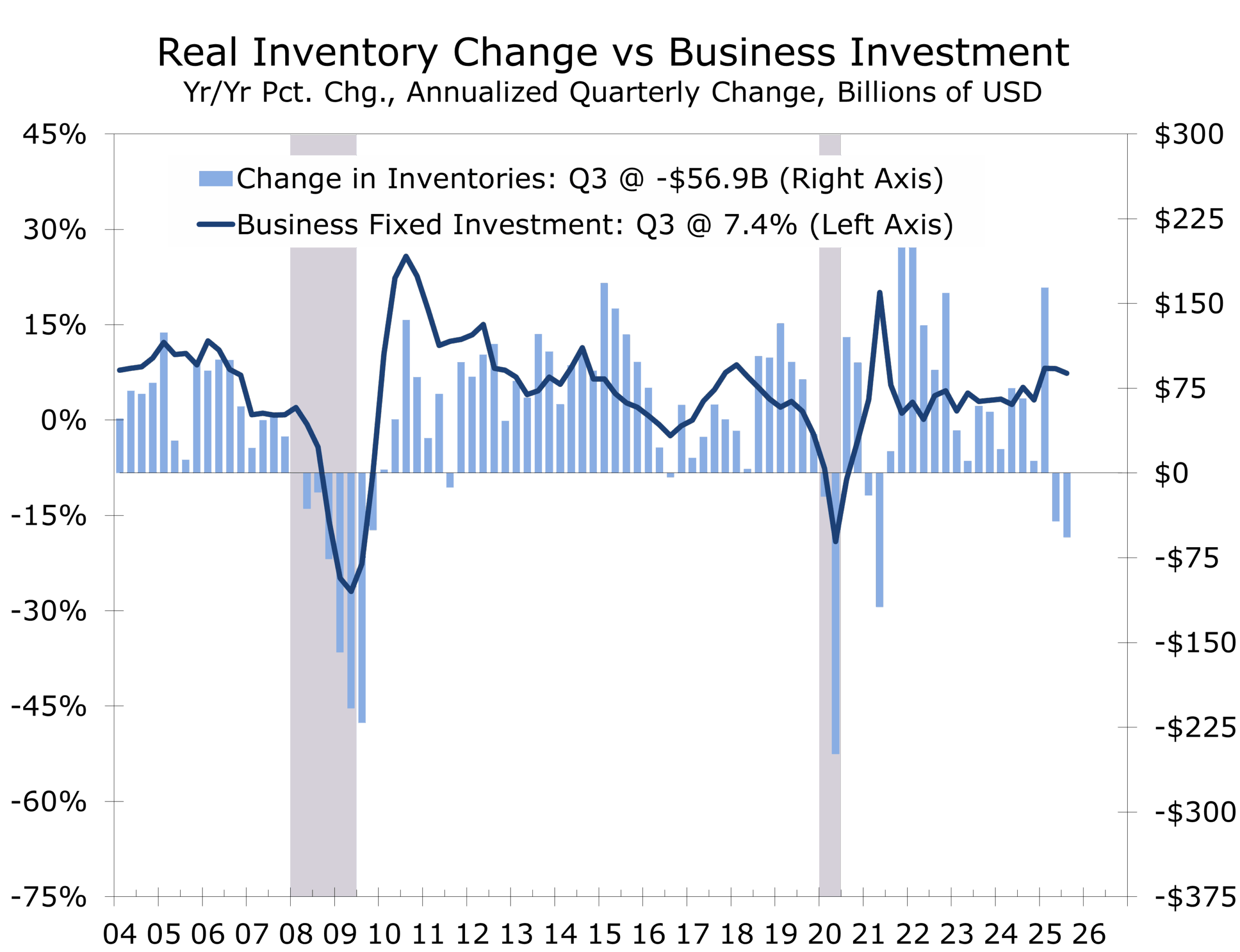

Investment: Inventory Noise Masks a Steadier Core

Private investment remained a modest drag on growth, but far less so than in prior quarters. The decline was driven primarily by inventory liquidation, particularly in wholesale trade and manufacturing. Inventories were built up earlier in the year ahead of tariffs, and businesses have since been drawing down stocks as trade relationships are refined and demand patterns normalize.

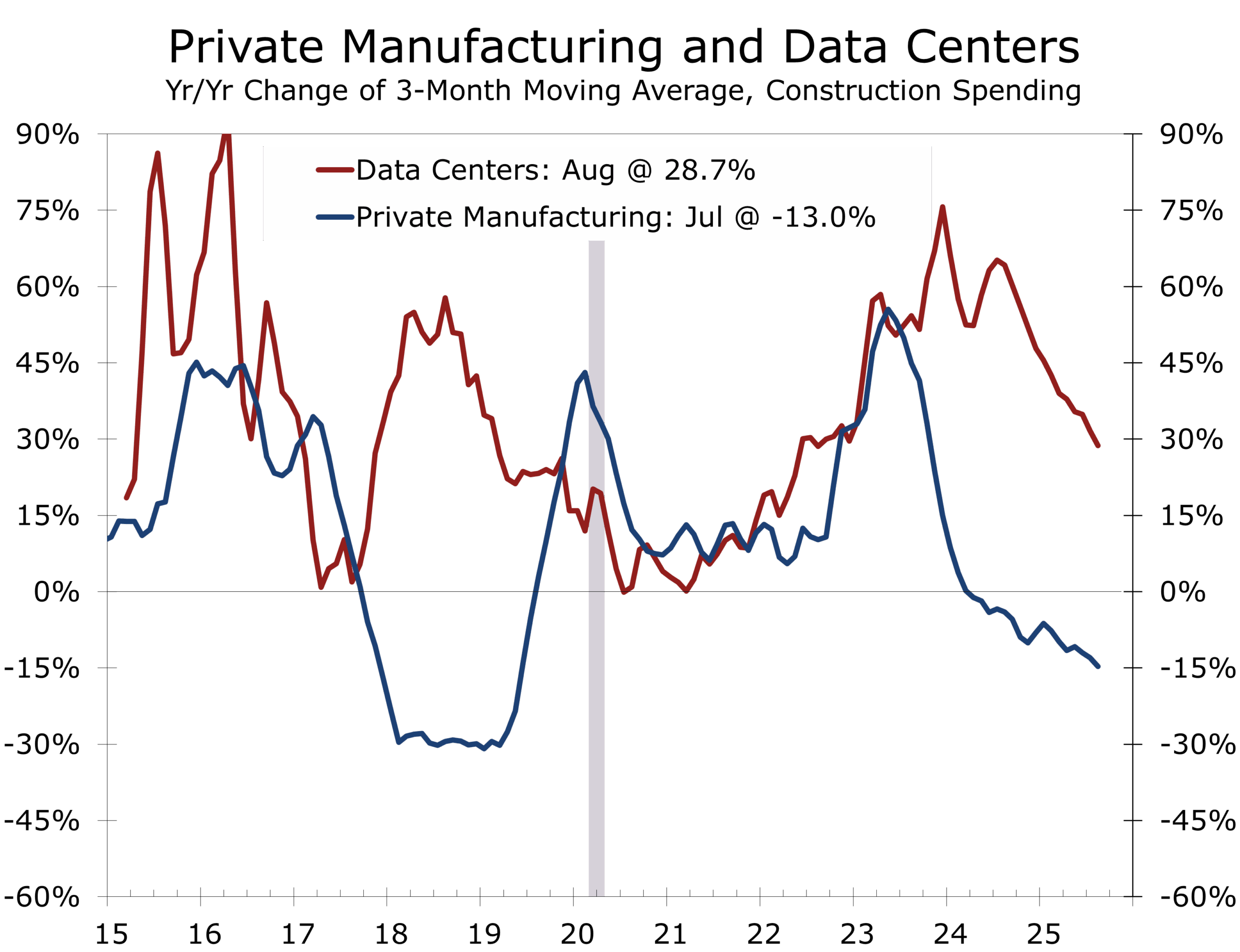

Importantly, gross private fixed investment held up better than the headline suggests, reinforcing the view that businesses remain cautious but not retreating. Growth slowed outside of data-center-related construction, with intellectual property investment cooling modestly and structures investment weakening as factory and mining construction softened following earlier front-loaded buildouts. Firms appear to be managing balance sheets and inventories conservatively while preserving the ability to expand investment once policy uncertainty and financial conditions improve.

Trade and Government Spending Flatter the Headline

Exports rebounded in the third quarter, supported by gains in both goods and services. Imports declined again, boosting measured GDP but complicating interpretation of domestic momentum. These trade dynamics have become a recurring source of volatility in recent quarters and are best viewed as amplifiers rather than drivers of the business cycle.

Government spending also contributed positively, with increases at both the federal and state and local levels. Defense spending led the federal gains, while state and local consumption expenditures also rose. As with trade, these contributions lift the headline but offer limited insight into the sustainability of private-sector growth.

Inflation Moves the Wrong Way at the Margin

Inflation data were less reassuring. The gross domestic purchases price index rose at a 3.4% pace, while PCE inflation accelerated to a 2.8% pace and core PCE increased to a 2.9% pace. While inflation remains well below its 2022 peak, the third-quarter uptick was already apparent in earlier CPI data.

Tariff-related price pressure likely peaked in Q3; broader inflation trends remain contained.

Encouragingly, core capital goods prices remain well behaved, suggesting that underlying investment-related inflation pressures are contained even as headline deflators temporarily firm. With tariff effects now largely reflected in the data, we look for the deflators to follow the CPI lower in coming quarters.

Profits Quietly Improve

Corporate profits from current production increased $166 billion in the third quarter, a sharp rebound from the prior period. Combined with steady income growth, this improvement supports margins, balance sheets, and capital spending optionality heading into 2026. This aspect of the report received less attention than the headline GDP number but remains an important underpinning for medium-term growth.

Policy and the Road Ahead

From a policy perspective, the third-quarter report argues for flexibility rather than urgency. Growth remains above potential, inflation has firmed modestly, and labor income continues to support demand. At the same time, the absence of broadening inflation pressure and signs of cooling outside of AI-related investment argue against renewed tightening.

The most likely outcome is a for the Fed to cut rates more slowly, by perhaps cutting at every other FOMC meeting, which will not only allow for a clearer read of the data but also extend the easing cycle. The expansion remains intact, underlying momentum is moderating gradually. Yet the labor market is still deserving of additional Fed support but without undermining hard-won progress at reducing inflation.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 23, 2025

Mark Vitner, Chief Economist

(704) 458-4000

The Piedmont Perspective: Politics, Perception, and the 2026 Economy

Politics, Perception, and the 2026 Economy

Executive takeaway

Markets price direction. Politics prices memory. By late 2026, the distance between the two may narrow meaningfully.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – A Little Fog, a Resilient Economy, and Positive Momentum into 2026

Highlights of the Week

- Growth is cooling at the margin, not stalling; resilience remains the defining feature of this cycle. We expect growth to handily top consensus estimates.

- Inflation data noise persists, but housing disinflation is increasingly durable and broad-based.

- Lean inventories and a solid holiday season are quietly rebuilding the industrial pipeline.

- Manufacturing and logistics are setting up for a rebound in 2026 driven by normalization, not excess.

- 2026 will be a momentous year for the U.S., marking the nation’s 250th anniversary, the hosting of the World Cup, the expiration of key provisions of the 2017 tax cuts, a scheduled USMCA review, and concluding with midterm elections.

Confidence, Constraints, and Narrowing Margins

The U.S. economy is closing out the year with more resilience than many expected. While the runway is a bit foggy, Santa’s sleigh looks likely to make its rounds with ease. Low inventories, a solid holiday season, and a growing sense that the economy bends rather than breaks are setting the stage for a rebound in manufacturing and logistics as 2026 approaches.

Recent data reinforce that view. Existing home sales remain subdued, but pricing pressure is easing as inventories slowly rebuild. Consumer sentiment has improved modestly, consistent with real income growth continuing to outpace headline inflation. We are also seeing more promotional activity at grocery stores, as food companies reintroduce discounts to support volumes. The picture is not one of acceleration, but of durability.

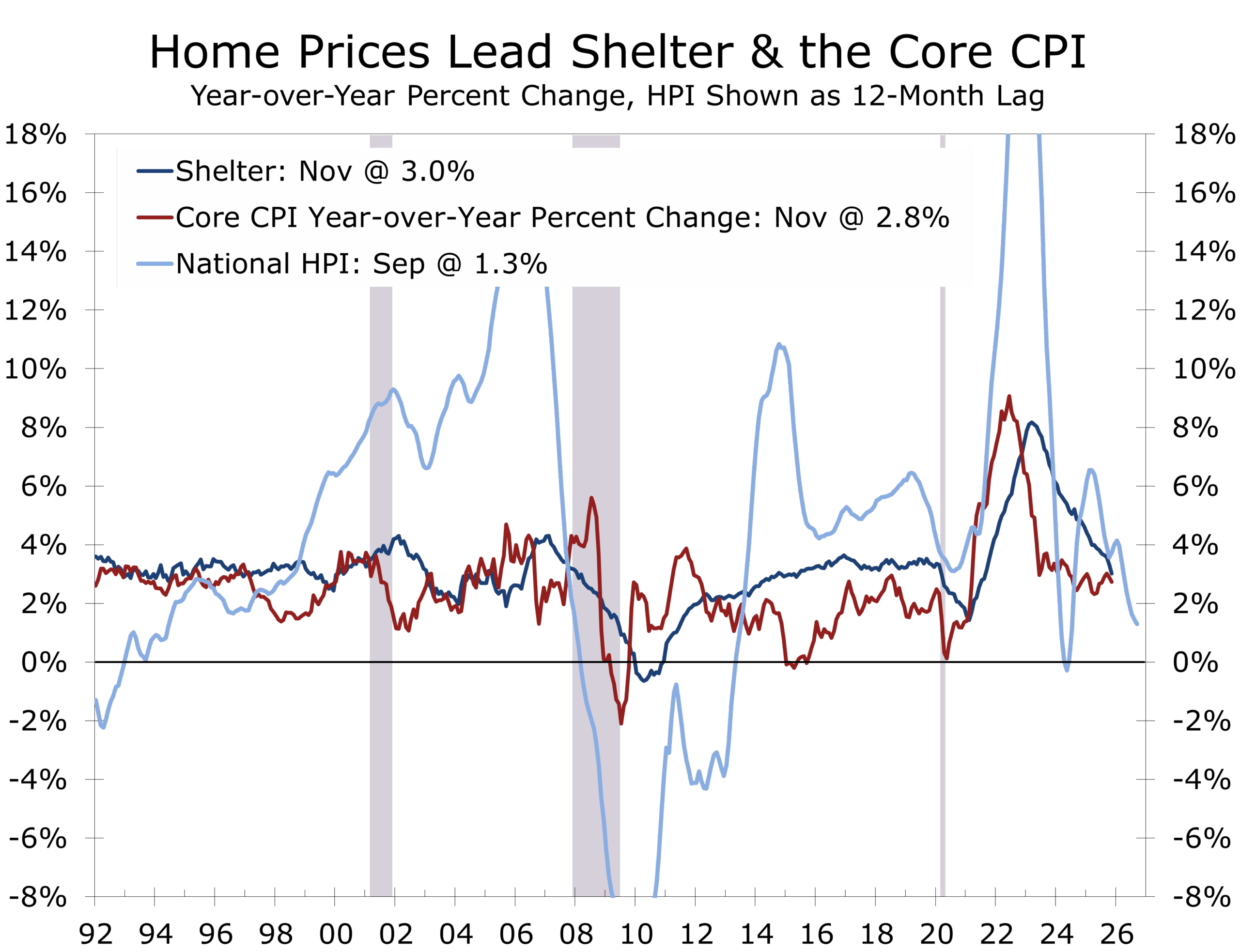

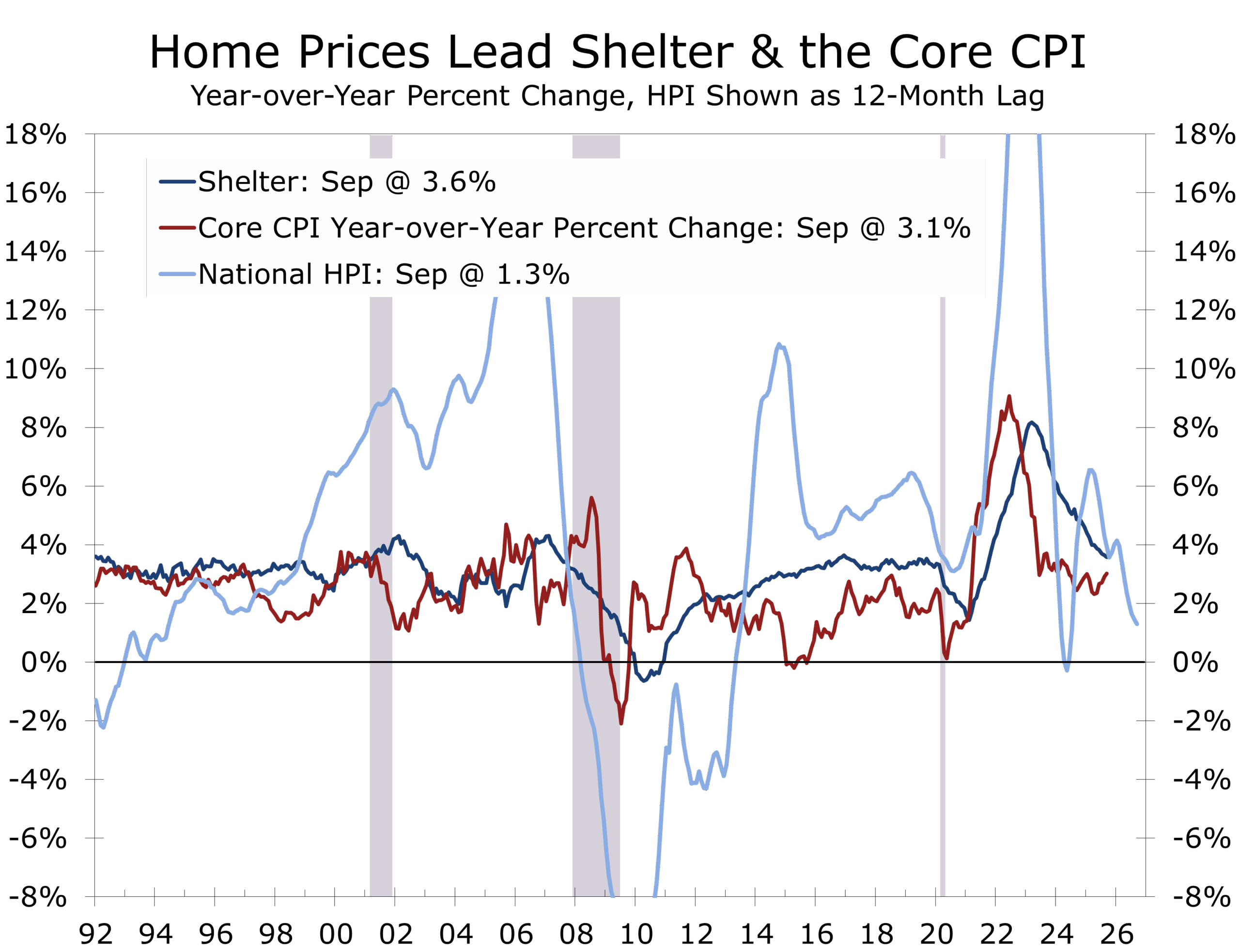

Inflation dynamics continue to evolve in the Federal Reserve’s favor. Housing costs are clearly decelerating, both in market rents and in forward-looking measures embedded in CPI. While debate persists around the precision of the latest CPI report, there is far less disagreement about direction. Housing prices have fallen sequentially in five of the past six months, and the year-over-year increase has slowed to roughly 1.3%. More importantly, inflation is likely to improve more meaningfully in 2026, as changes in home prices and rents filter gradually into official measures.

Inflation is no longer broad-based; it is now concentrated, political, and idiosyncratic.

Consumers may also receive relief on another front. Despite the horrific fires in Los Angeles that opened 2025, the year ultimately saw fewer catastrophic weather events, with no major hurricanes making landfall. As a result, property and casualty insurance costs are likely to ease in 2026. Energy costs are also likely to provide consumers with a meaningful break.

Inflation: data noise versus durable signals

Concerns about persistent data distortions in inflation reports are understandable—but they risk overshooting the runway.

The data may be noisy, but the housing signal is clear—and it points to durable disinflation.

Some CPI and PCE components will remain noisy due to survey timing, seasonal adjustments, and lingering post-shutdown effects. But the most important inflation component—housing—is sending a consistent and reassuring signal across multiple independent measures. Market rents have flattened or declined year over year, new lease growth has cooled materially, and multifamily completions remain elevated. Owners’ Equivalent Rent, slow by design, is now catching up to reality.

The takeaway is straightforward: the instruments may wobble, but the destination is clear. Housing disinflation is real, durable, and likely to continue capping inflation prints well into 2026, making today’s debate about missing data petty and insignificant.

Looking ahead, insurance costs are the next swing factor. Fewer catastrophic storms should ease property and casualty premiums. Health insurance remains the wild card, with policy choices likely to distort pricing regardless of the macro backdrop.

Financial markets reflect this mix. Equities have moved higher with narrow leadership, Treasury yields have drifted lower, and credit spreads remain contained. The message is not exuberance, but confidence that policy tightening has done enough. Markets continue to assume that the Federal Reserve can move from restraint to calibration without triggering a downturn.

Manufacturing and logistics: setting up the rebound

One of the more underappreciated developments this year has been inventory discipline. Firms entered the holiday season lean, and early indications point to solid seasonal demand.

Late-cycle rebounds are often industrial and investment driven, not consumer-led.

Low inventories, improving demand visibility, easing inflation and lower interest rates create fertile ground for a rebound in manufacturing and logistics. Even modest restocking can translate into a meaningful pickup in orders, production, and freight volumes.

Piedmont Perspective: The Election Year Economy

Political handicapping currently point to a decisive midterm outcome. Both traditional forecasters such as the Cook Political Report and market-based indicators like Polymarket reflect today’s dissatisfaction with affordability and inflation.

That view risks underestimating how different the economy may look by November 2026.

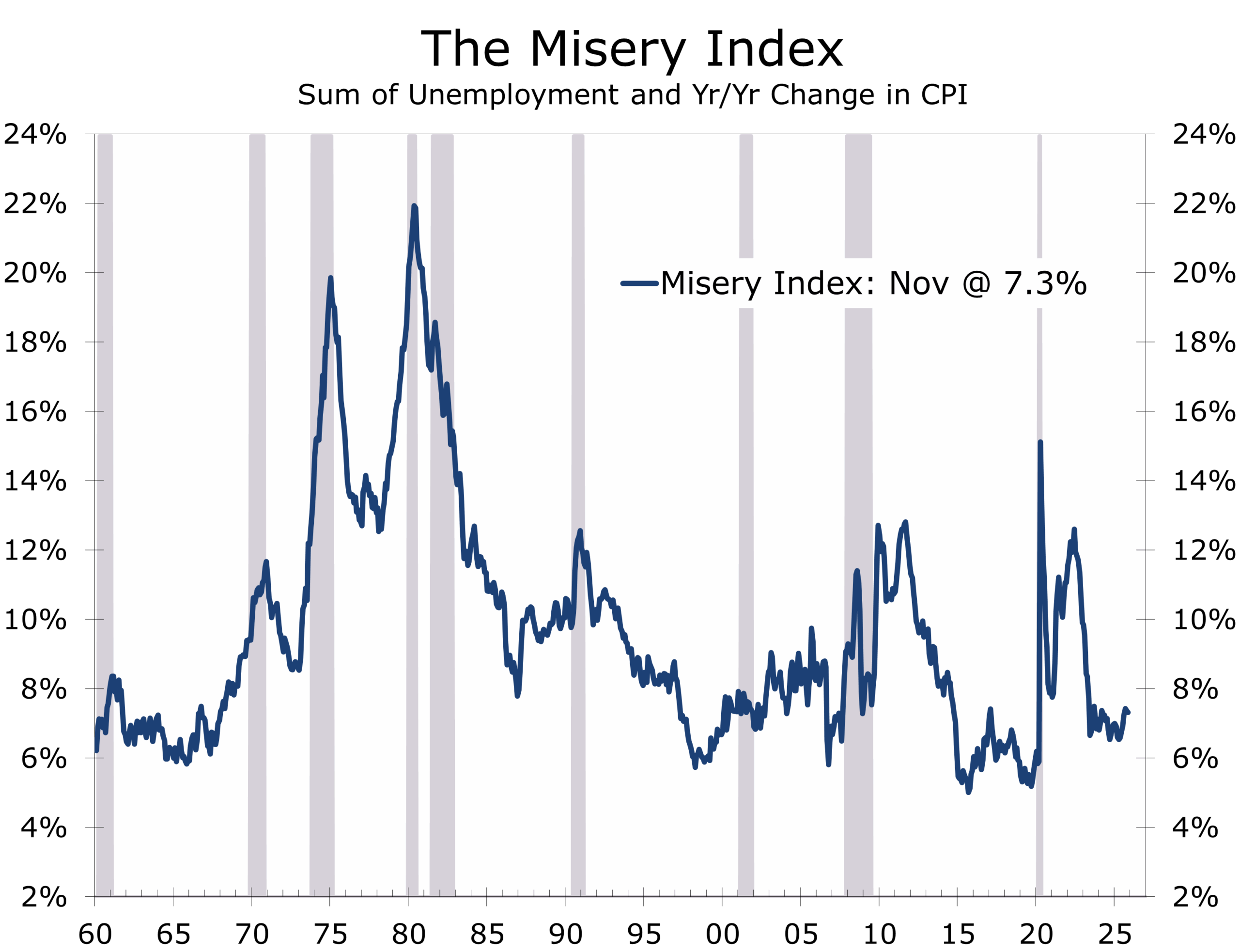

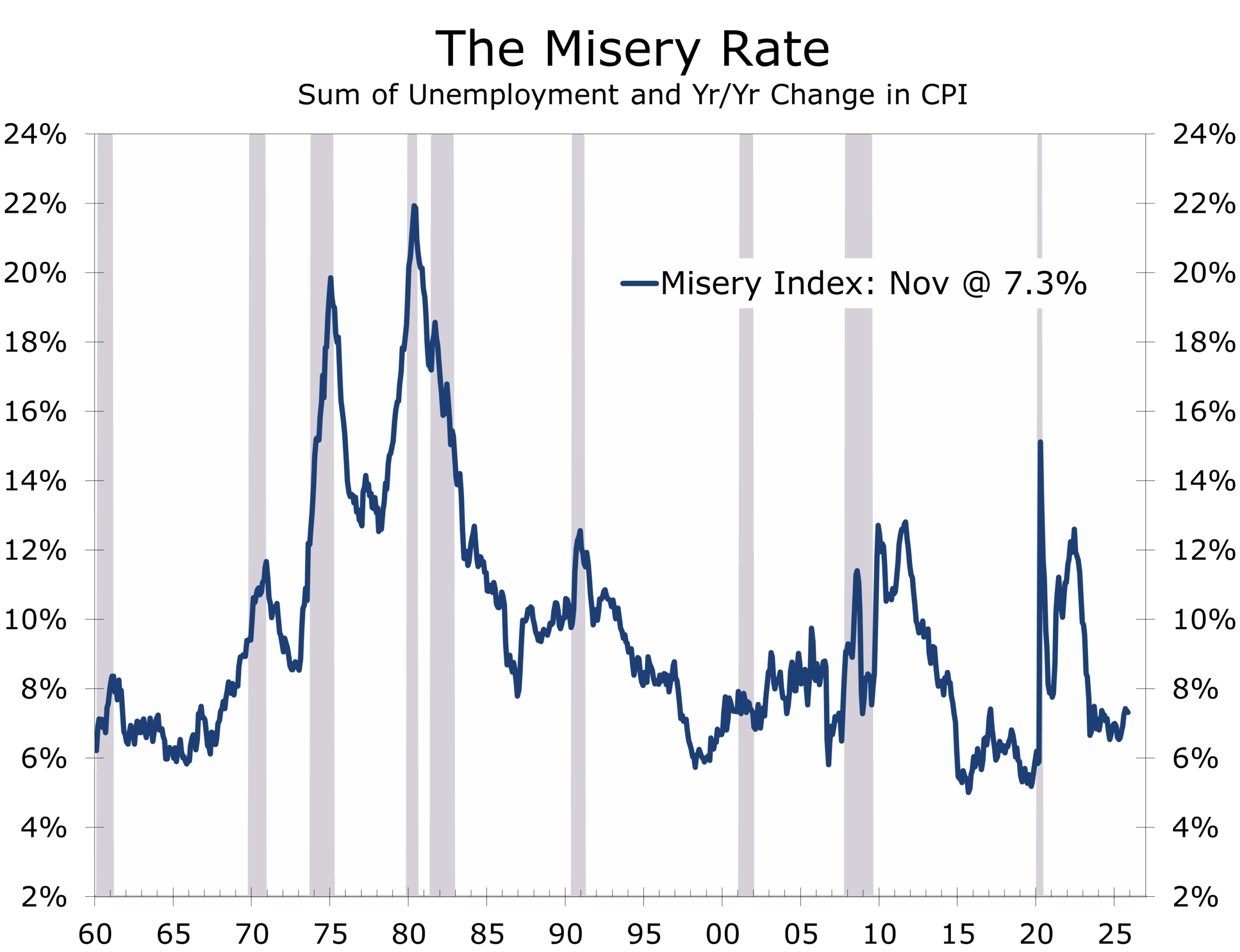

Elections tend to be driven less by economic levels than by economic direction. Several indicators that historically correlate more closely with electoral outcomes are likely to improve over the next year. The Misery Index should decline as inflation cools and labor-market softening remains orderly. Real per-capita disposable income should improve as nominal growth again exceeds inflation.

With Republicans controlling the White House and both chambers of Congress, messaging is likely to emphasize progress—cooler inflation, steadier growth, and rising real purchasing power. Democrats are likely to stress persistent affordability challenges, particularly groceries, housing, and healthcare.

In an era that feels like permanent campaign season, both narratives can coexist. The economy does not need to boom to alter the political landscape; it simply needs to improve. We expect the election outcome to become a closer call as we get closer to November.

Tuesday, December 23

A heavier-than-usual holiday calendar, though most data is shutdown-delayed and backward-looking:

- GDP (Q3, delayed estimate)

- Durable Goods Orders (October, preliminary)

- Industrial Production & Capacity Utilization (November)

- Consumer Confidence (Conference Board)

- New Home Sales (October, delayed)

GDP will attract the most attention, but holiday liquidity and timing limit reaction.

Wednesday, December 24 (Christmas Eve)

Early market close. No major releases. Liquidity thin.

Thursday, December 25 (Christmas Day)

U.S. markets closed.

Friday, December 26

Markets reopen with limited participation. Any releases should be treated cautiously.

Final Thoughts: policy, permanence, and perception

This cycle continues to defy simple labels. Growth is slower but intact. Inflation is cooling, even if the data occasionally obscures the trend. Housing is no longer a drag, inventories remain lean, and investment is quietly reasserting itself as a stabilizing force.

Slower growth, cooler inflation, and a cautious Fed are reshaping the cycle without breaking it.

What distinguishes the current environment is the durability of policy choices shaping it. Trade policy, often framed as tactical, is increasingly being applied with longer horizons in mind—reshaping supply chains, redirecting capital, and reinforcing geopolitical objectives with limited inflationary spillover.

That durability matters in an era that feels like perpetual election season. By the time voters head to the polls in 2026, the economy they experience is likely to look meaningfully different from today’s debate. Cooler inflation, steadier growth, and rising real incomes would complicate prevailing narratives—without requiring an outright boom.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 22, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

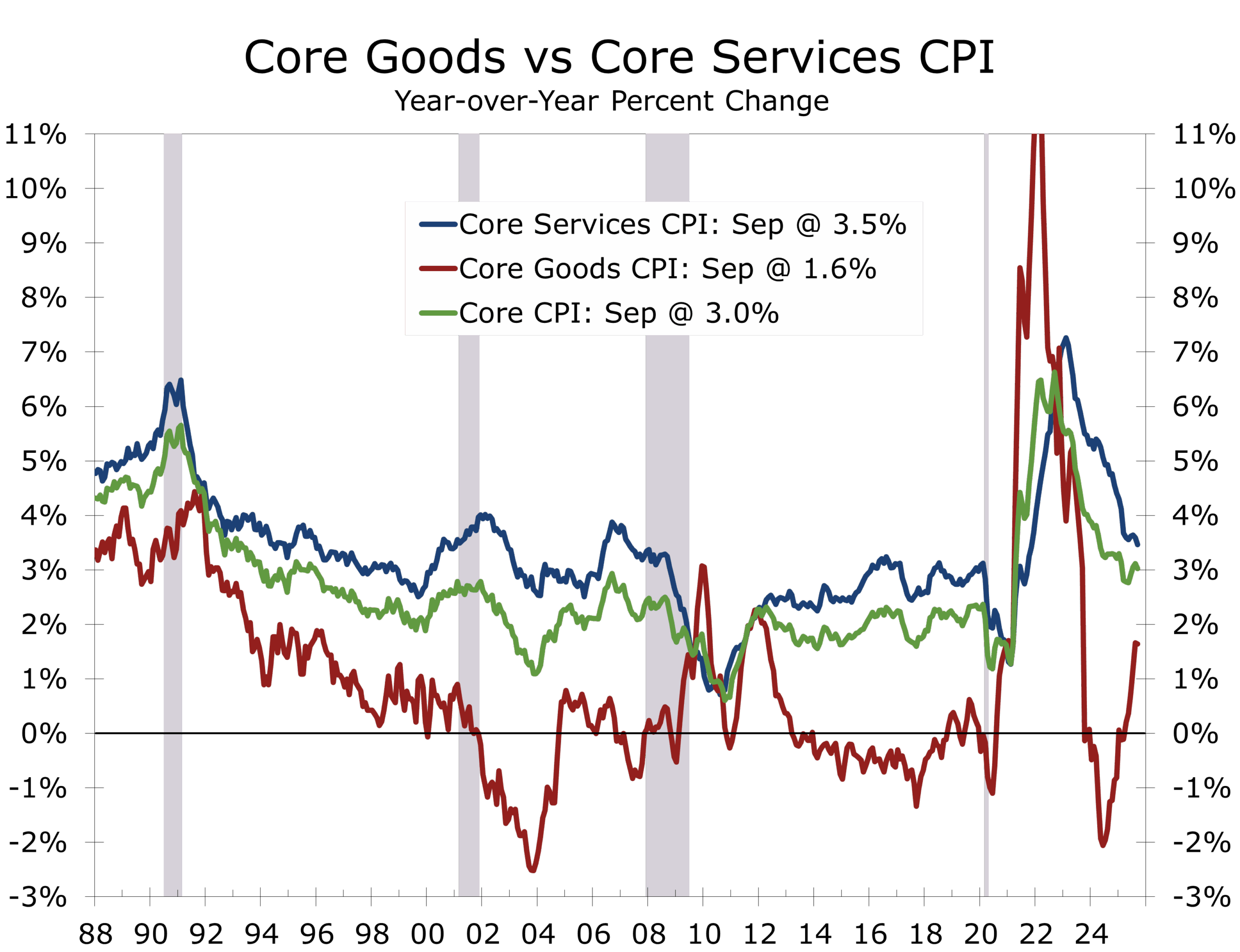

November 2025 Consumer Price Index: Disinflation Resumes Despite Shutdown Distortions

Shelter and Core Inflation Continue to Cool

-

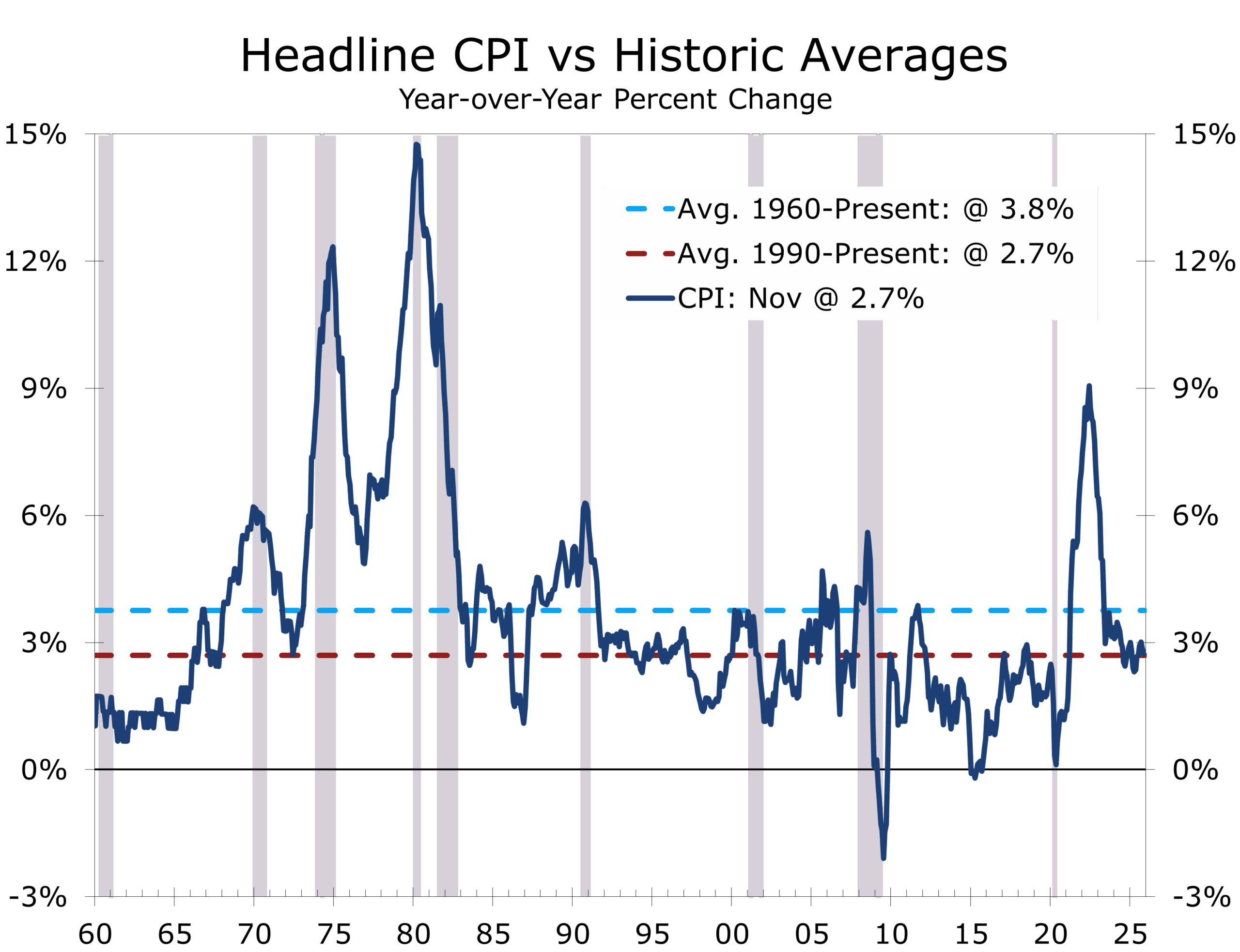

- Headline CPI rose 2% over the two-month period (September–November), with year-over-year inflation slowing to 2.7%, down from 3.0% in September.

- Core CPI increased 0.2% over two months, leaving core inflation at 2.6% y/y, the lowest reading of this cycle.

- Shelter inflation continued to decelerate, rising just 0.2% over two months and slowing to 3.0% y/y.

- Energy prices rebounded, lifting headline inflation, but remain a volatile rather than structural driver.

- Food inflation eased further, particularly at grocery stores, while restaurant inflation remained elevated but stable.

- Data caveat: October CPI data were not collected due to the federal government shutdown, compressing two months of inflation into a single report.

- Policy signal: Despite plenty of data distortions, the direction of travel is clear; inflation is cooling, reinforcing the Fed’s ability to continue easing.

The Big Picture: Two-Months of CPI in One-Month

November’s CPI report is unusual, but its message is unmistakable. Because the federal government shutdown halted data collection in October, the Bureau of Labor Statistics reported two months of price changes in a single release. That complicates month-to-month comparisons, but it does not obscure the underlying trend.

Inflation is moderating.

Headline CPI rose 0.2% from September to November, while year-over-year inflation declined to 2.7%, its lowest level since early 2021. The year-to-year change in the CPI is now back to its average since 1990. Core CPI followed the same trajectory, rising 0.2% over two months and decelerating to 2.6% y/y. Even with imperfect data, the signal is clear: underlying inflation pressures continue to fade.

The CPI was the only major piece of federal government data released during the shutdown; reflecting its outsized influence.

Core Inflation: Cooling, Even Through the Noise

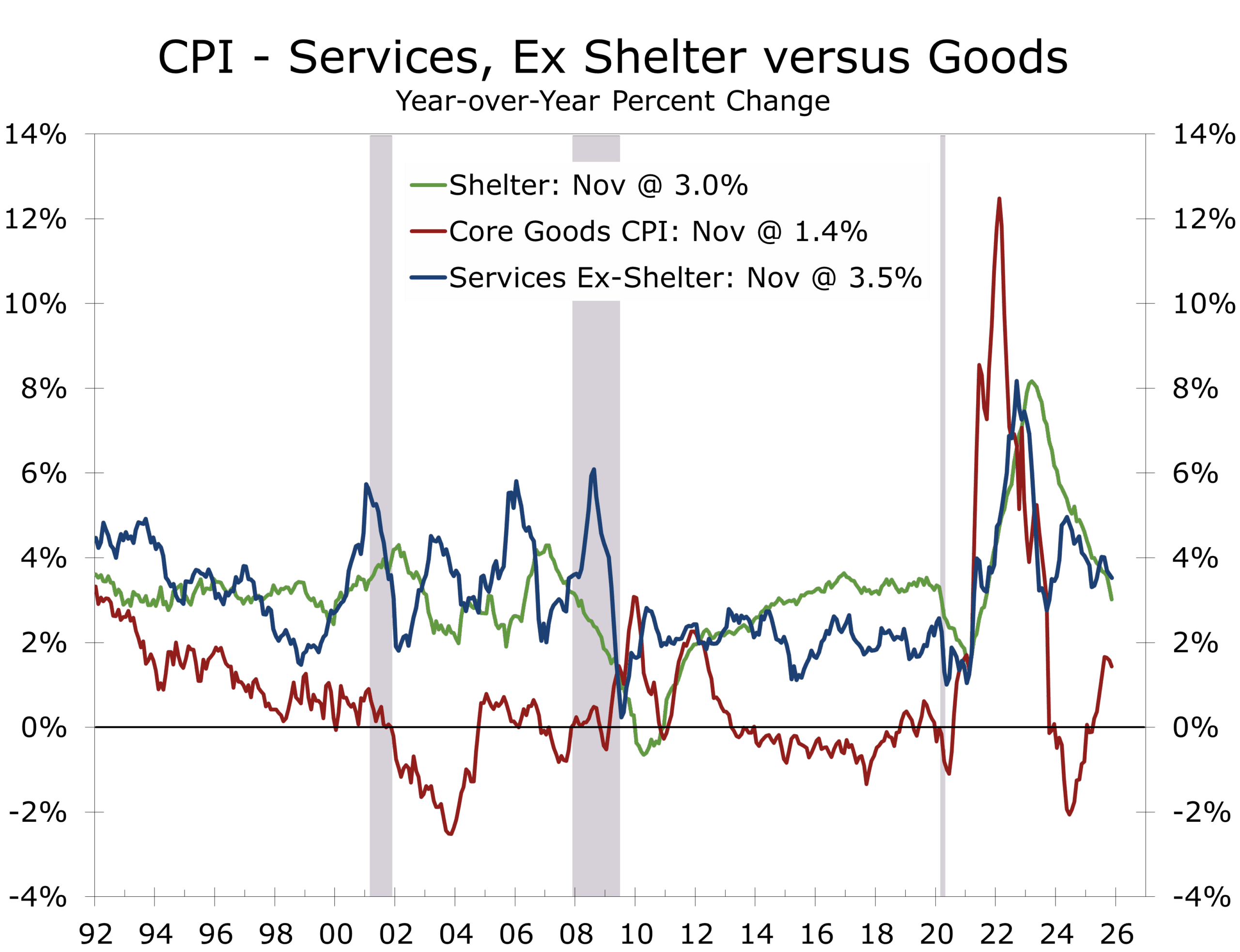

Core inflation rose at an annualized pace well below the Fed’s comfort threshold. A two-month increase of 0.2% implies roughly 0.10% per month, a pace consistent with inflation settling near target once shelter completes its normalization. We have taken a simple average of the September and November data to impute the missing monthly data for October to allow continuity with our charts. This was done all series where no October data was available.

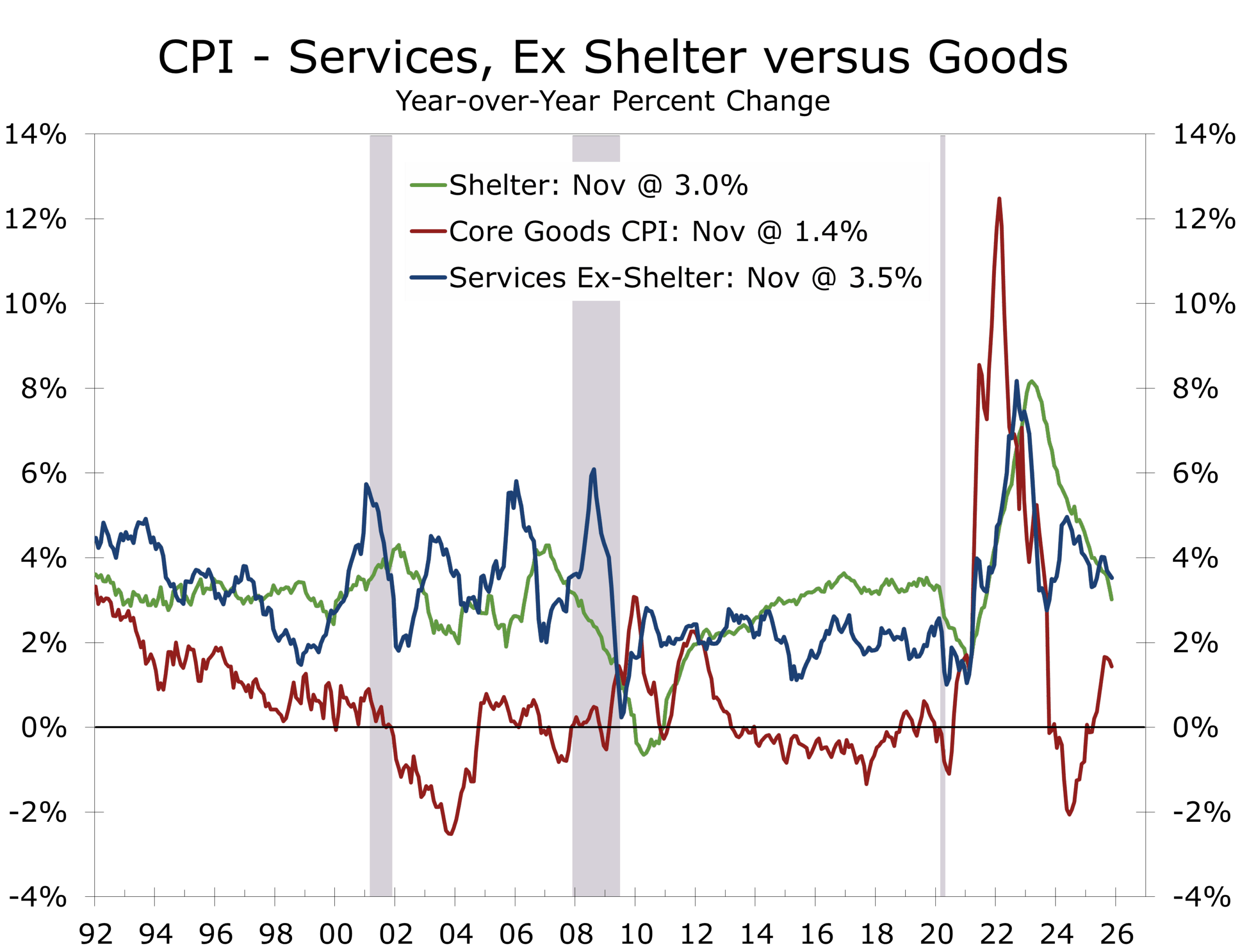

Core services excluding energy rose 3.0% y/y, down materially from earlier in the cycle, while core goods inflation remained contained at 1.4% y/y despite ongoing tariff uncertainty and a weaker dollar. The slight improvement suggests the bulk of the tariff impact is now behind us. Used vehicle prices edged higher but remain far removed from their pandemic-era surge.

With the worst of tariff impacts behind us, inflation pressures are narrowing.

Shelter: The Heavy Lifting Continues

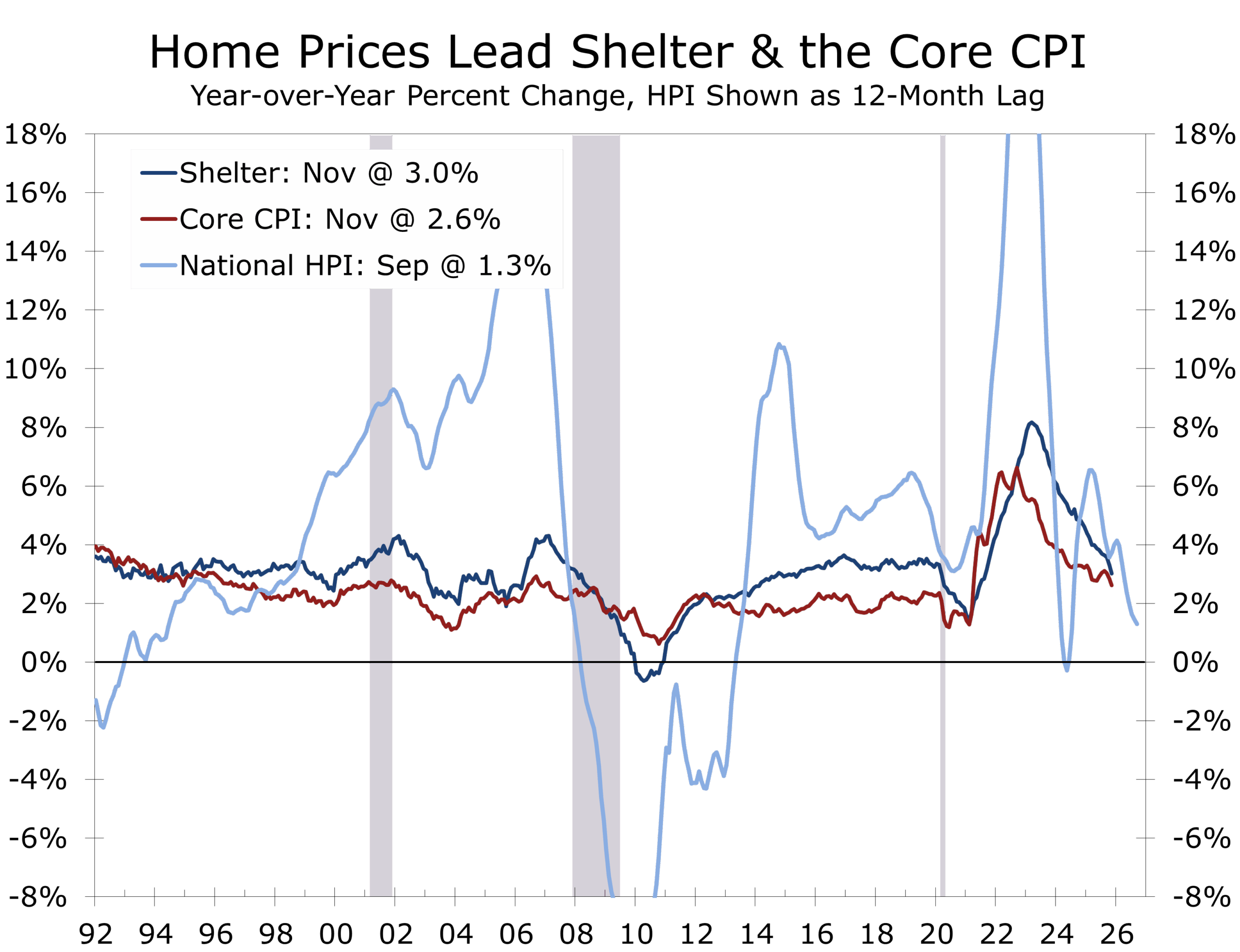

Shelter remains the key variable in the CPI narrative. November delivered further confirmation that this component is finally bending lower, which confirms earlier private sector reports of falling home prices and declining rents.

Shelter prices rose just 0.2% over two months, pulling year-over-year shelter inflation down to 3.0%, a dramatic deceleration from the 6%+ pace seen earlier in the cycle. This reflects a confluence of forces: a surge in multifamily supply, widespread rent concessions, and lease renewals resetting at lower rates, particularly across the Sun Belt. Home prices also declined for five months in a row earlier this year and are currently up just 1.3% year-to-year.

Given that shelter accounts for roughly 44% of core CPI, its deceleration is doing most of the work in pushing inflation lower.

Energy: Volatile, Not Structural

Energy prices rose 1.1% over the two-month period, lifting the energy index to 4.2% y/y. Gasoline prices increased modestly, while electricity and natural gas costs remain elevated on a year-over-year basis.

The inflation problem is shifting from grocery stores to more slowly moderating services.

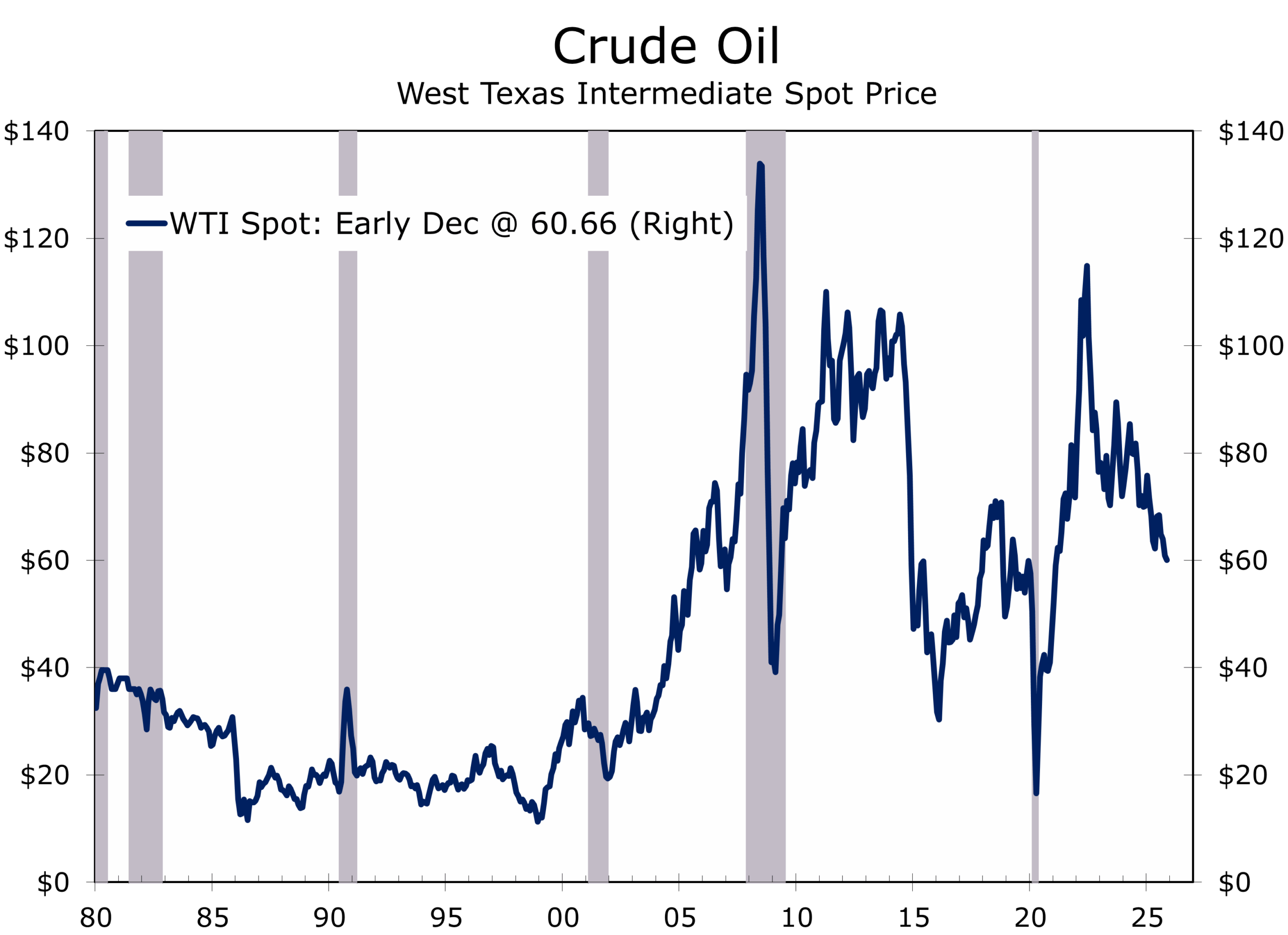

Still, energy continues to behave as a swing factor rather than a structural inflation driver. Absent a sustained surge that feeds into wages or expectations, energy-driven volatility does little to alter the disinflation trend. Moreover, oil prices have weakened recently, and natural gas prices are expected to decline over the next year, slowing gains in electricity costs.

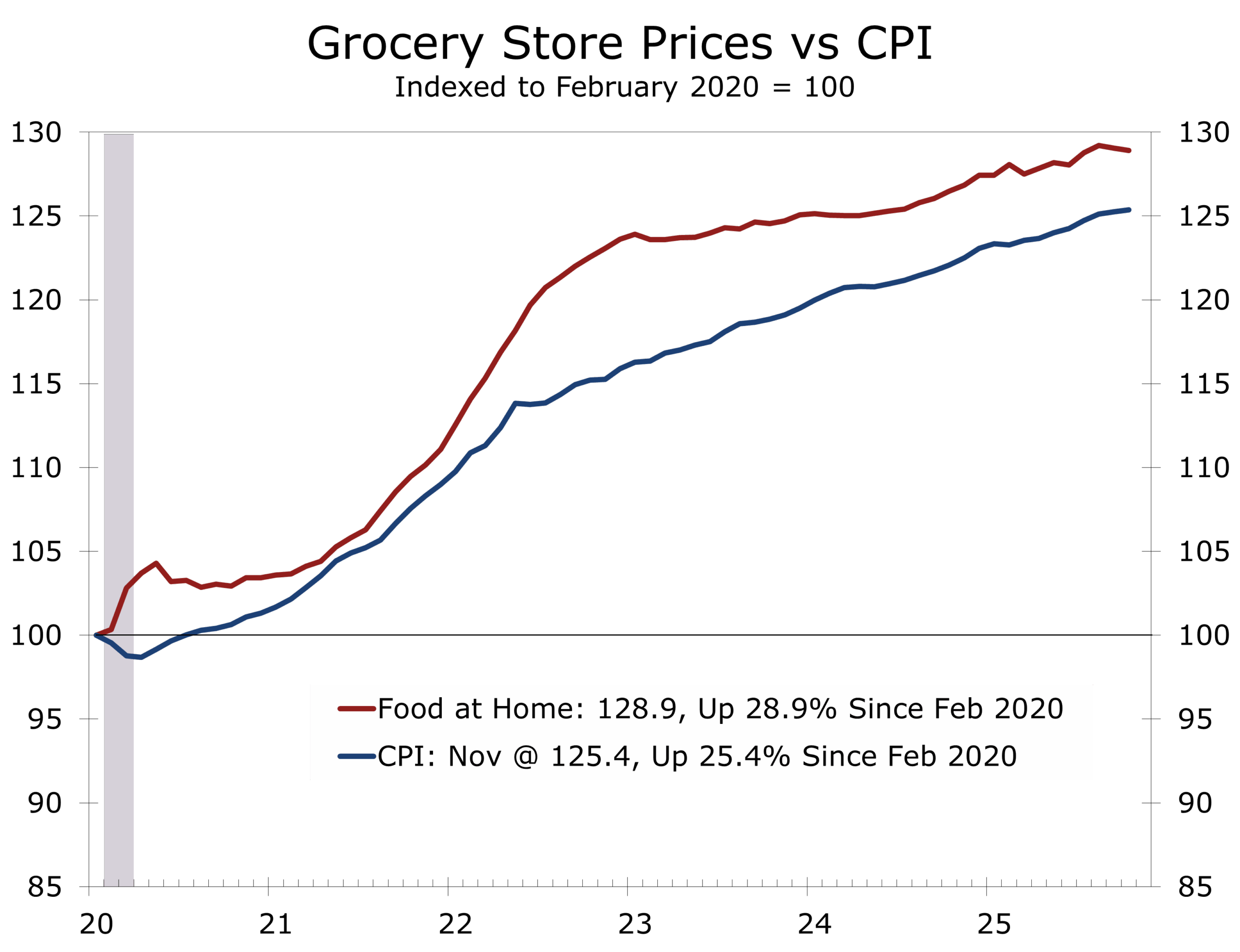

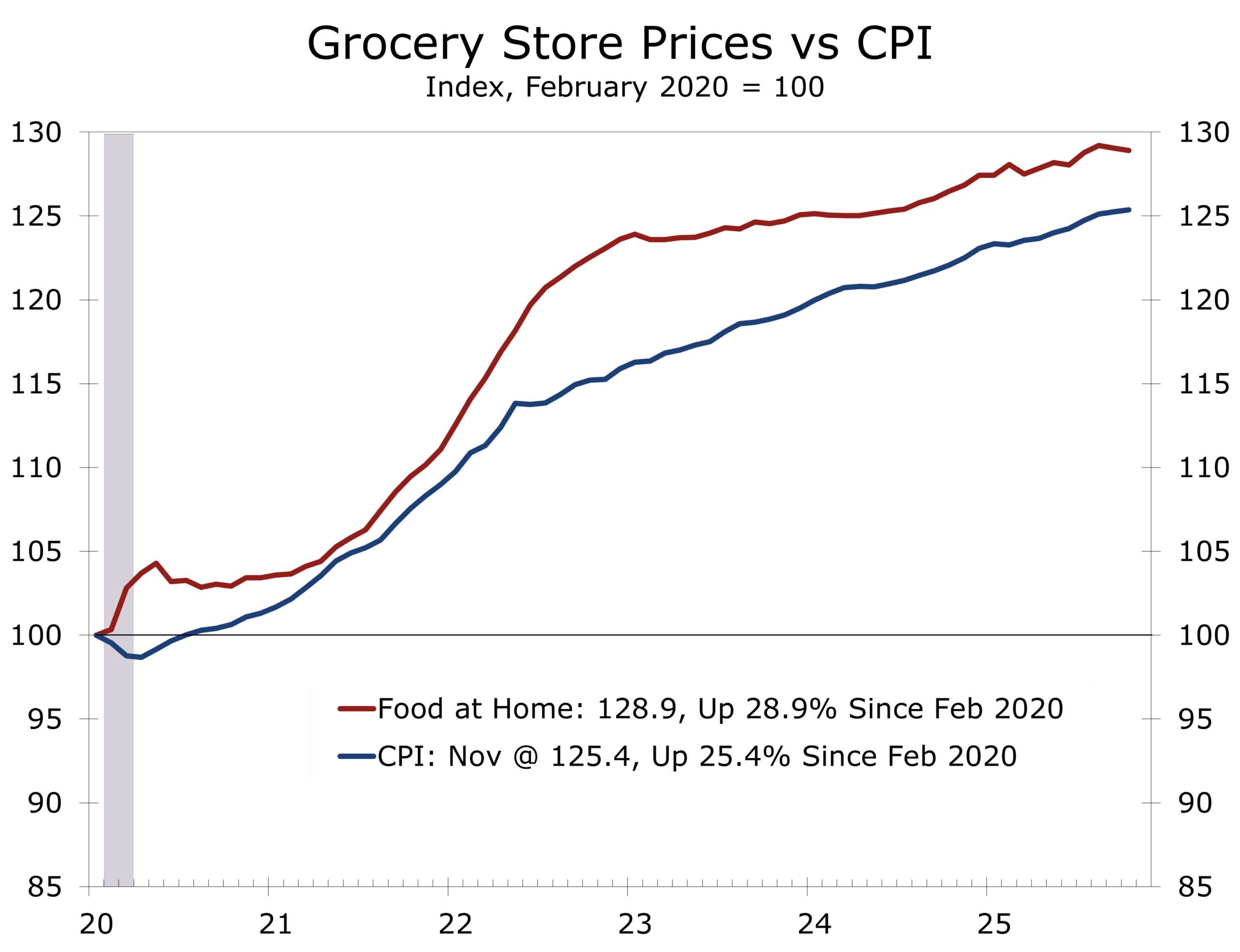

Food: Cooling at Home, less so at Restaurants

Food inflation continues to decelerate, led by groceries. Food at home rose just 1.9% y/y, with dairy prices falling and produce inflation essentially flat. In contrast, food away from home rose 3.7% y/y, reflecting still-elevated labor and occupancy costs.

Restaurant pricing remains one of the last pockets of persistence, but even here momentum is no longer accelerating. Promotions, menu simplification, and growing consumer price sensitivity are limiting further pass-through. Beef is a clear exception to the moderating trend and is rising due to structural factors, not monetary policy. Higher beef prices will slow the moderation in grocery store prices and also squeeze restaurant margins.

Surprise and Doubts

The improvement in CPI may ring hollow for many consumers, particularly those still grappling with elevated grocery bills. While inflation has slowed, prices are not falling. The post-pandemic inflation surge was the product of a policy era marked by massive federal spending and a Federal Reserve that was slow to withdraw accommodation as the economy roared back to life.

Flush with stimulus-era savings, consumers bid up prices for key necessities, including groceries and housing, at a pace well above the overall inflation rate. Although price increases have since moderated, grocery prices remain roughly 29% higher than before the pandemic. Much of that increase is now embedded in labor costs, which rose even faster and are unlikely to reverse. Adding to the strain, beef prices are poised to rise further before improving, reinforcing consumer frustration. Chicken and pork prices should be less affected and may provide some relief at the margins—but for many households, the sticker shock is here to stay.

Shutdown Distortions: Timing Changed, Trend Intact

The federal shutdown introduces important caveats. The BLS did not collect survey data in October and was unable to retroactively recover those observations. As a result, this report reflects a combination of two months of survey-based data and non-survey sources where available.

Even so, the shutdown distorted timing, not direction. Despite compressed reporting and missing seasonal detail, the underlying trend points decisively toward slower inflation.

Policy Implications: The Fed’s Job Has Changed

This report reinforces a clear shift in the Fed’s reaction function. Inflation is no longer the dominant risk. With headline CPI at 2.7%, core CPI at 2.6%, and shelter inflation decelerating rapidly, policymakers have room to pivot their focus toward emerging labor-market softening and broader financial-conditions stability.

The inflation fight is not over, but it no longer requires highly restrictive policy.

Rate cuts at this stage are best viewed as insurance, not stimulus—designed to guard against a policy-induced or needlessly severe downturn in employment while inflation continues its gradual glide lower. Monetary policy is working, and at current levels the federal funds rate remains modestly restrictive. Calls for sharply lower rates are premature unless economic growth weakens materially.

Strip away the shutdown noise, and the message is straightforward: inflation is cooling, shelter is leading the way, and price pressures are becoming increasingly concentrated rather than broad-based. While it is too soon for a victory lap, the latest CPI data provide important confirmation that the disinflation process is durable enough for the Fed to remain focused on stabilizing growth and employment as 2026 approaches, providing the incoming Fed Chair greater policy latitude.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 18, 2025

Mark Vitner, Chief Economist

(704) 458-4000

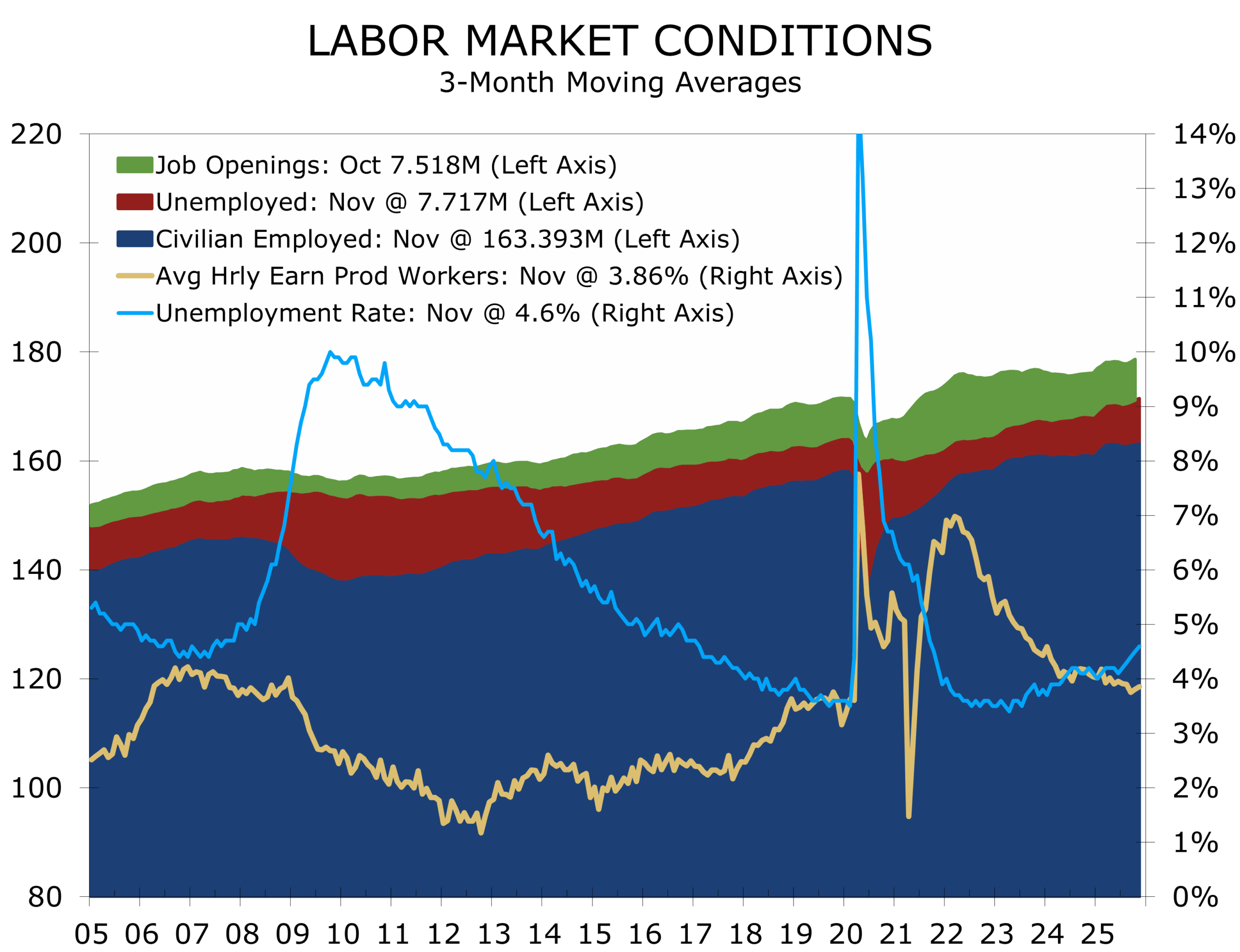

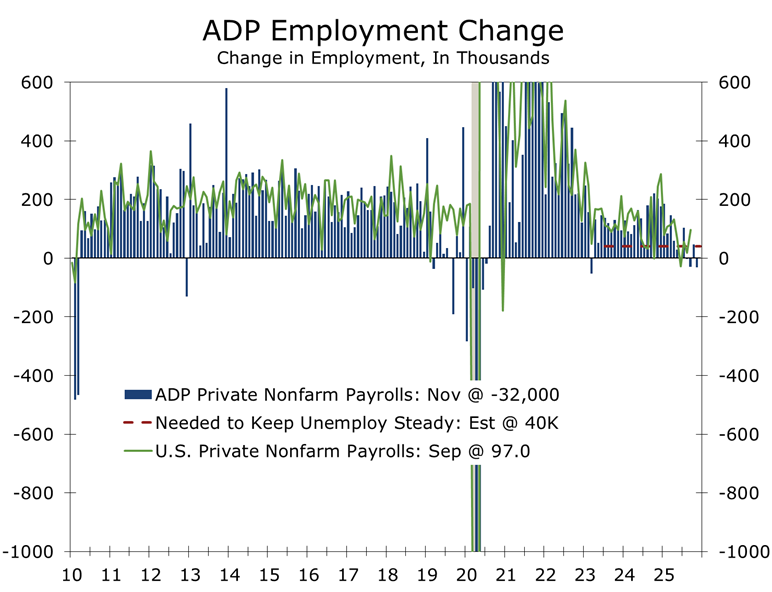

November Employment Report— Stall Speed With Some Slack Building

November Data Provide a Number of Confirming Signals for Policymakers and the Markets

-

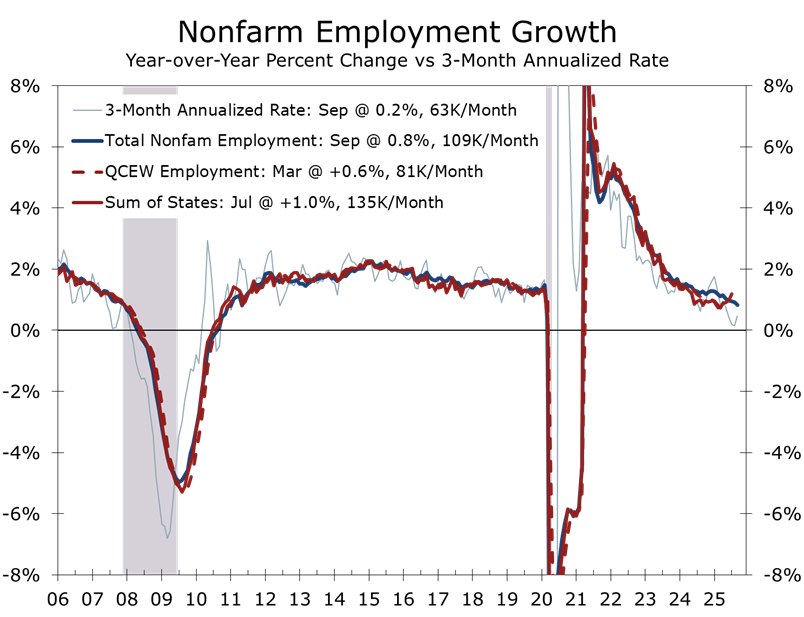

- Payroll growth remains stuck near stall speed. Nonfarm payrolls rose 64,000 in November, extending a pattern of minimal net job growth in place since April.

- Federal job losses are now a material drag. DOGE-related cutbacks have eliminated roughly 271,000 federal jobs year-to-date, distorting headline payrolls and tightening labor conditions in affected regions.

- Hiring is narrow and late-cycle. Job gains remain concentrated in health care, social assistance, and construction, while most other sectors show little or no growth.

- Slack is building beneath the surface. Underemployment surged, with part-time for economic reasons rising by 909,000, and short-term unemployment increasing.

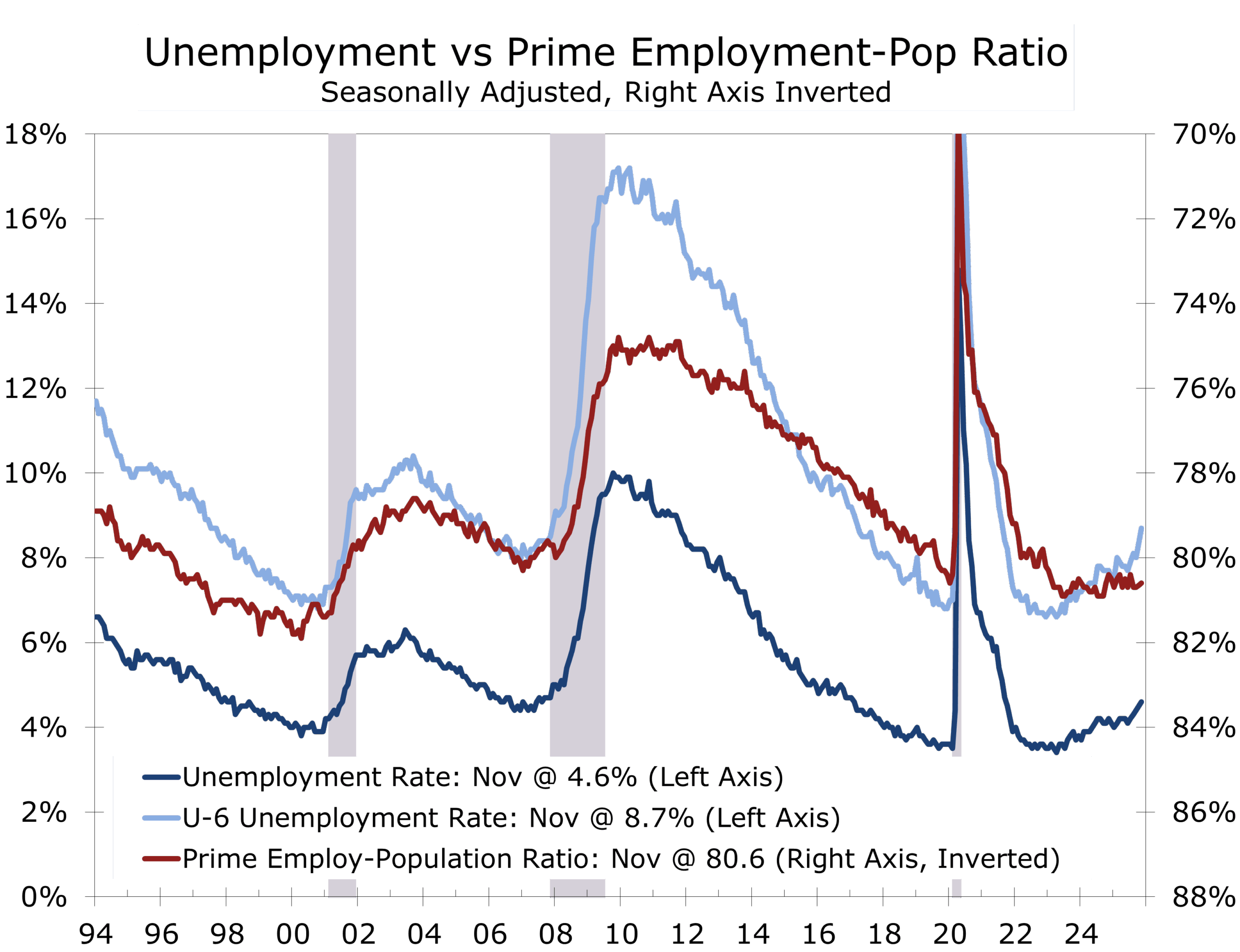

- Unemployment is drifting higher—but unevenly. The jobless rate rose to 4.6%, the highest since October 2021, driven largely by labor-force reentrants and concentrated among younger workers.

- Wage growth continues to cool. Average hourly earnings rose just 0.1% m/m and 3.5% y/y, consistent with the Fed’s inflation objective.

- Policy implications are clear, timing is not. The labor market is no longer tightening, but shutdown-related data gaps complicate the Fed’s near-term decision-making.

Momentum Fades as Slack Gradually Builds

November’s employment report confirms that the U.S. labor market is no longer tightening and is instead operating near stall speed. Nonfarm payrolls rose by 64,000, extending a pattern of muted job growth that has been in place since April. Revisions to August and September again leaned negative, subtracting a combined 33,000 jobs and reinforcing the view that underlying momentum is softer than headline figures initially suggested.

Job growth has slowed to a pace that barely offsets labor force growth, leaving the unemployment rate vulnerable to further drift.

The unemployment rate held at 4.6%, unchanged from September but materially higher than the 4.2% reading a year earlier. With 7.8 million Americans unemployed, labor market conditions now look meaningfully looser than earlier in the cycle. This is not a sudden break, but a gradual accumulation of slack—an economy decelerating rather than contracting.

Two structural forces stand out in this report. First, DOGE-related cutbacks have materially reduced federal payrolls, transforming what had once been a marginal factor into a meaningful drag on employment. Federal government payrolls declined by another 6,000 in November following a sharp 162,000 drop in October, bringing total federal job losses this year to roughly 271,000. These reductions are policy-driven, not cyclical, and will continue to weigh on headline payroll growth into early 2026.

Federal job losses are no longer a footnote—they are a structural headwind for headline employment.

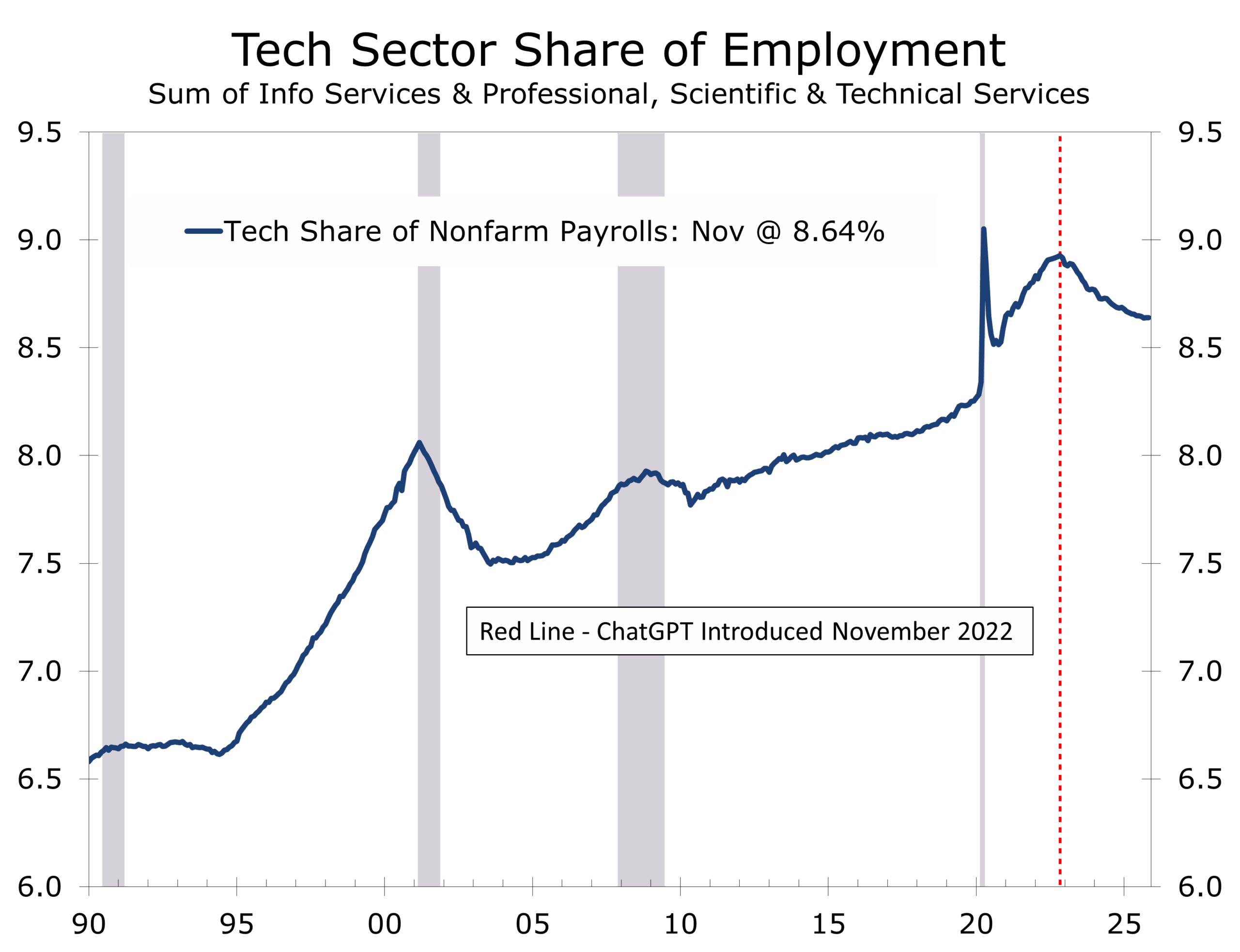

Second, the data increasingly support the view that AI adoption is beginning to suppress employment in certain tech-related sectors, with possible spillovers into parts of the entertainment industry. While AI investment continues to bolster capital spending and productivity, employment in information, professional services, and adjacent creative fields remains soft. Financial services warrants close monitoring as automation, cost discipline, and productivity gains converge over the coming quarters.

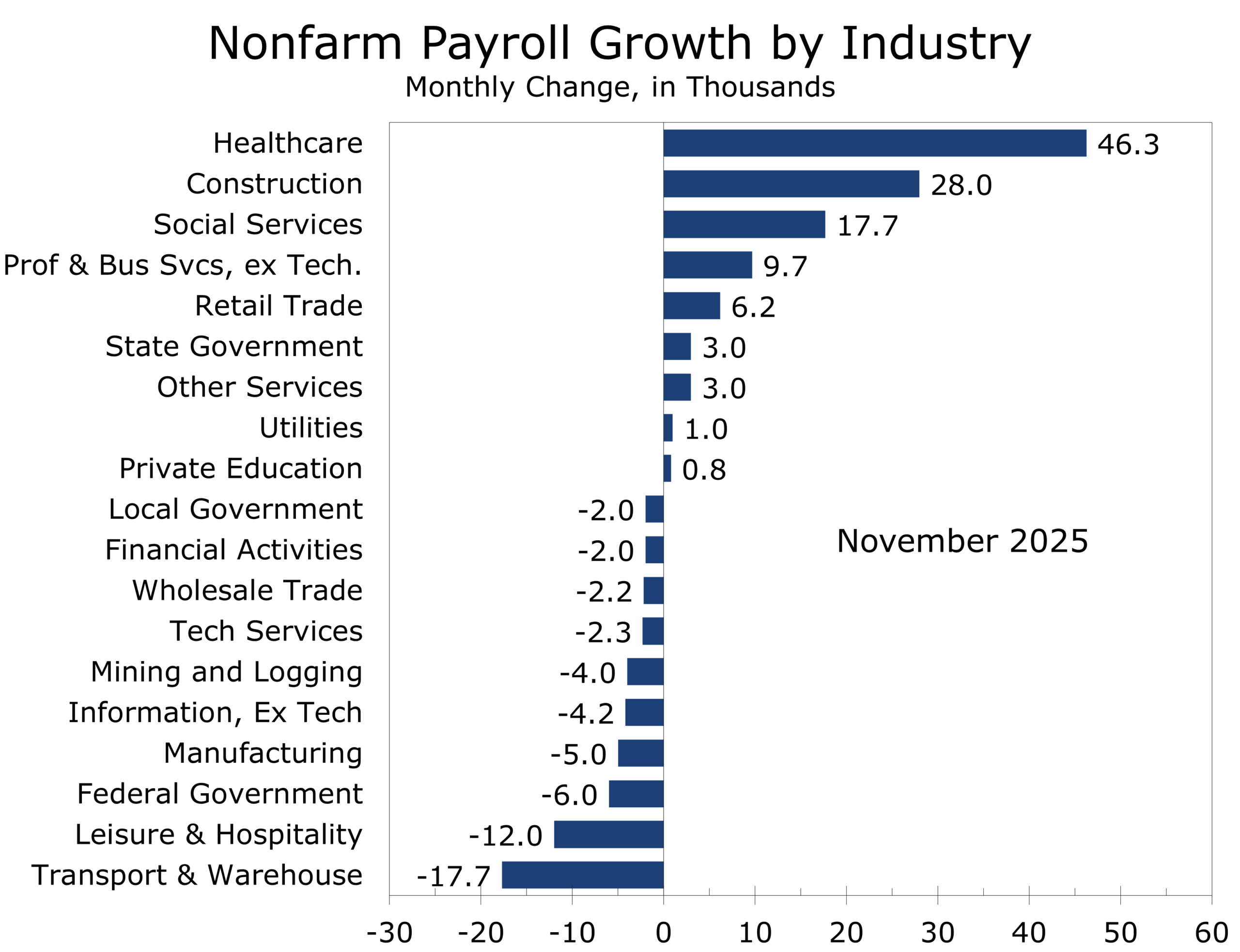

Sectoral detail underscores the late-cycle character of the labor market. Hiring remained concentrated in a narrow set of service industries. Health care added 46,000 jobs, consistent with its longer-run trend, while social assistance rose by 18,000, led by individual and family services. Construction employment increased by 28,000, driven largely by nonresidential specialty trade contractors. While construction employment has been largely flat over the past year, November’s gain suggests backlog completion and infrastructure-related activity are still providing support.

This is not broad-based hiring—it is an economy leaning on a narrow set of labor-intensive services.

Outside these areas, momentum faded. Transportation and warehousing shed 18,000 jobs, entirely due to losses among couriers and messengers. Employment in the sector is now down 78,000 from its February peak, reflecting cooling goods demand. Most other major industries—including manufacturing, retail, wholesale trade, professional and business services, financial activities, and leisure and hospitality—showed little or no change, highlighting the lack of breadth in hiring.

Household survey data reveal additional signs of slack building beneath the surface. While the headline unemployment rate was unchanged on the month, the number of people unemployed for less than five weeks increased by 316,000, suggesting rising job separations or shorter job tenures. More striking was the surge in part-time employment for economic reasons, which jumped by 909,000 to 5.5 million, indicating that firms are increasingly managing labor costs by cutting hours rather than headcount.

This dynamic is also evident in broader measures of labor underutilization. The U-6 unemployment rate, which captures not only the unemployed but also discouraged workers and those working part time for economic reasons, has continued to edge higher, reinforcing the message that underemployment is rising even as the headline unemployment rate appears stable. Historically, sustained increases in U-6 tend to precede more visible deterioration in payroll employment, making this an important late-cycle signal.

Underemployment is rising even as the headline unemployment rate appears stable.

The composition of unemployment has also shifted in a notable way. The rise in the unemployment rate from 4.4% in September to 4.6% in November—the highest level since October 2021—appears to have been driven largely by reentrants to the labor force, potentially including displaced federal workers or their spouses. At the same time, unemployment is increasing disproportionately among younger workers aged 16–24, a group that typically absorbs labor-market adjustments first when hiring slows.

By contrast, labor market conditions for core workers remain comparatively resilient. The prime-age (25–54) employment-population ratio has held relatively steady at historically elevated levels, and the unemployment rate for workers 25 and older has risen by just 0.2 percentage point over the past year to 3.7%. This divergence—rising slack at the margins alongside stability among prime-age workers—is consistent with late-cycle softening rather than a broad-based downturn, suggesting a labor market that is cooling gradually, not breaking.

The composition of unemployment also shifted in a notable way. The rise in the unemployment rate from 4.4% in September to 4.6% in November—the highest level since October 2021—appears to have been driven largely by reentrants to the labor force, potentially including displaced federal workers or their spouses. Unemployment is also increasing disproportionately among younger workers aged 16–24, while the unemployment rate for those 25 and older has risen by just 0.2 percentage point over the past year to 3.7%. This pattern is consistent with late-cycle softening rather than a broad-based downturn.

Wage and hours data reinforce the cooling trend. Average hourly earnings rose just 0.1% in November and are up 3.5% over the past year—well aligned with the Federal Reserve’s inflation objective. The average workweek edged up to 34.3 hours, while manufacturing hours and overtime were unchanged, suggesting that labor demand is easing gradually rather than collapsing.

Wages are no longer the Fed’s key problem, sluggish job growth is.

Taken together, the November report depicts a labor market that has clearly transitioned from expansion to plateau. Hiring remains narrow, underemployment is rising, federal payrolls are shrinking for structural reasons, and wage pressures have faded. Shutdown-related data gaps complicate interpretation, but the direction of travel is unmistakable.

For policymakers, the implication is nuanced. The labor market is no longer generating inflationary pressure, and slack is accumulating at the margins through rising underemployment and cooling wage growth. At the same time, the absence of October data and the distortions embedded in November’s release argue for caution. Policymakers are being asked to make forward-looking decisions with a backward-looking and incomplete dataset. To bridge that gap, we simply averaged the September and November results to approximate October conditions—a method that produces intuitively reasonable results, at least until more complete data become available.

The direction of travel is clear—even if the data are not.

The case for eventual easing remains intact: wage growth has decelerated to a pace consistent with the inflation target, labor-utilization measures are softening, and hiring momentum has narrowed materially. The timing, however, remains less certain. With limited confirmation ahead of the December meeting, the Fed may prefer to wait for cleaner, post-shutdown data early in 2026 before acting, even as the risk of falling behind the curve gradually increases.

While the Fed will receive a substantial amount of new information before its late-January meeting, we believe the odds of a cut at that meeting are higher than current market pricing (just under 25%) suggests. Most of the downside risk to the economy is concentrated in the near term, while the offsetting support from larger tax refunds, capital-spending incentives, and greater clarity on tariffs and trade policy is unlikely to become evident until spring or early summer 2026.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 16, 2025

Mark Vitner, Chief Economist

(704) 458-4000

The Piedmont Perspective: Holiday Violence in a Connected World

Holiday Violence in a Connected World

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Plumbing, Polarization, and the Price of Stability

Highlights of the Week

- Markets are responding less to the Fed’s rate cut and more to its liquidity posture, reinforcing that balance-sheet mechanics now matter as much as policy rates.

- The re-steepening yield curve, led by renewed pressure at the long end, reflects fiscal realities, rising investment demand, and limits on monetary control over long-term capital.

- Transportation stocks are sending a constructive signal that the goods economy is stabilizing beneath headline volatility.

- The labor market is loosening gradually, with cooling wage pressure and declining quits pointing to slower momentum, not collapse.

- AI-driven investment continues to support growth but is becoming increasingly intertwined with credit markets and balance-sheet risk.

- Geopolitical tensions and rising social stress are no longer exogenous risks; they are shaping confidence, behavior, and the macro backdrop.

- The expansion remains intact, but it is increasingly conditional—dependent on careful liquidity management, fiscal credibility, disciplined capital allocation, and the preservation of social and institutional stability. The economy is still moving forward, but the margin for error continues to narrow.

When the Transports Speak, It’s Worth Listening

While markets remain fixated on AI-heavy mega caps, one of the more constructive signals over the past week has come from a far more traditional corner of the tape: the transports.

Transportation stocks—railroads, trucking firms, and logistics providers—have outperformed the broader market. That matters because transports sit closest to real economic activity. They move raw materials, intermediate goods, and finished products. When they strengthen, it often reflects improving expectations for physical demand rather than multiple expansion or liquidity effects.

When transports lead, it’s usually the real economy—not sentiment—that’s turning.

Historically, transports tend to lead at inflection points. Their recent outperformance suggests the goods-producing side of the economy is finding its footing—possibly marking the end of the long-running freight recession. Inventories remain lean, freight volumes have stabilized, and consumer demand—while cooling—is not collapsing.

This is not a signal of reacceleration, nor a late-cycle blowoff. It fits a more nuanced macro narrative: a soft patch, not a hard stop. In a market dominated by intangibles and AI narratives, the steady bid under companies that move goods from Point A to Point B is a reminder that the real economy still anchors the cycle. Demand should firm more visibly this spring and summer as housing and other rate-sensitive sectors respond to lower borrowing costs.

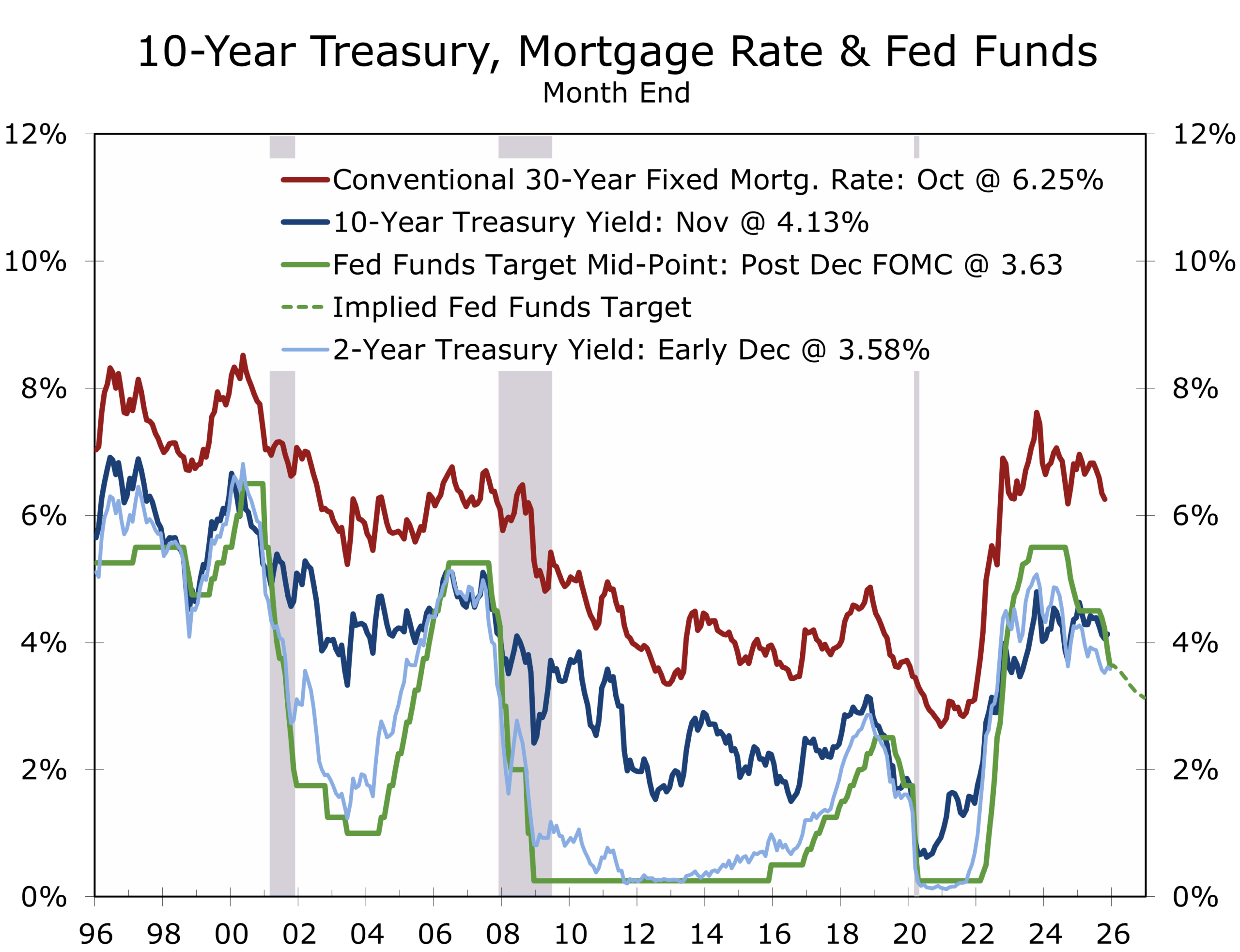

Rates, Fiscal Dominance, and Key Signals

The most revealing story in rates has not been the Fed’s decision to cut, but how markets reacted to how the Fed chose to ease. By moving cautiously, the Fed has preserved a progressively less tight—but still restrictive—policy stance. That approach has cooled inflation pressures without reigniting speculative excess. In that sense, policy has largely done its job.

The rate cut mattered less than how the Fed chose to ease.

The December move marked a subtle inflection.

By meeting day, the cut itself was expected. What mattered was pairing that cut with more aggressive-than-expected near-term Treasury-bill purchases. The modest balance sheet expansion was dubbed QE light by critics and described as reserve management by the Fed. The move was meaningful, which we interpret as an effort to avoid accidentally tipping the economy into recession with a temporary liquidity scare, is meaningful at the margin. Lower policy rates combined with balance-sheet expansion shifted market tone quickly and buoyed risk assets.

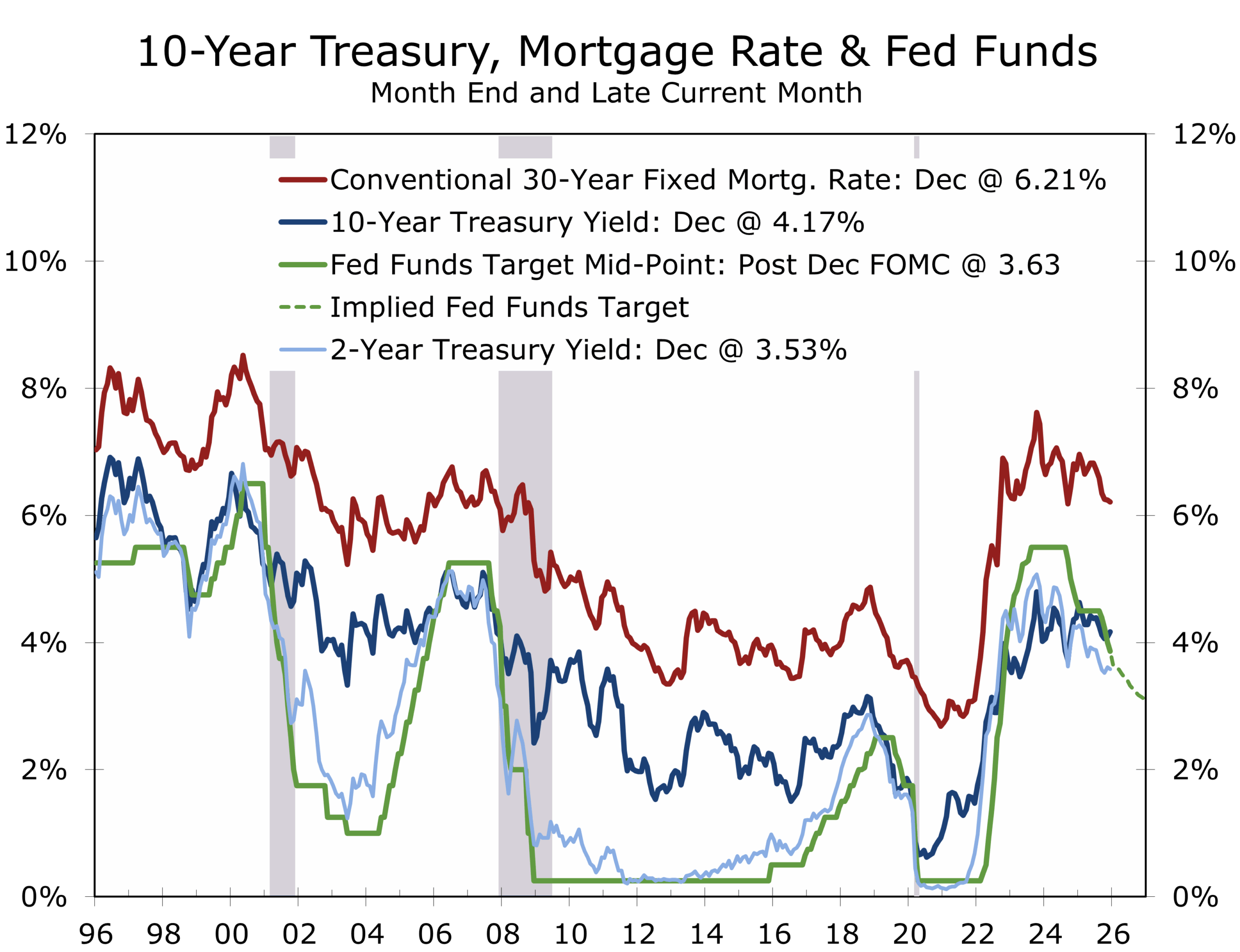

The yield curve responded accordingly. Short rates declined further, but long rates rose. The result was a steeper curve with a more uncomfortable message. The 10-Year Treasury had popped up to 4.20% earlier this month and then fell back under 4.10% and is not back up to around 4.18%.

The 30-year Treasury sent a clearer signal, with yields rising sharply in the days following the Fed’s announcement. The long bond is not trading CPI prints or FOMC rhetoric. It is trading duration risk, supply pressure, and long-run policy credibility.

Higher long rates reflect two beliefs gaining traction simultaneously: growth is likely to strengthen in 2026, and large fiscal deficits and heavy Treasury issuance are set to persist.

The bond market is drawing a distinction between the Fed’s influence over front-end financial conditions and its diminishing control over long-term borrowing costs.

This is fiscal dominance in practice—not a crisis of confidence, but a gradual shift in who sets the marginal price of long-term capital. The curve is not signaling recession, nor celebrating effortless growth. It is delivering a conditional verdict: the economy can move forward, but the cost of long-term capital is rising and the margin for policy error is thin.

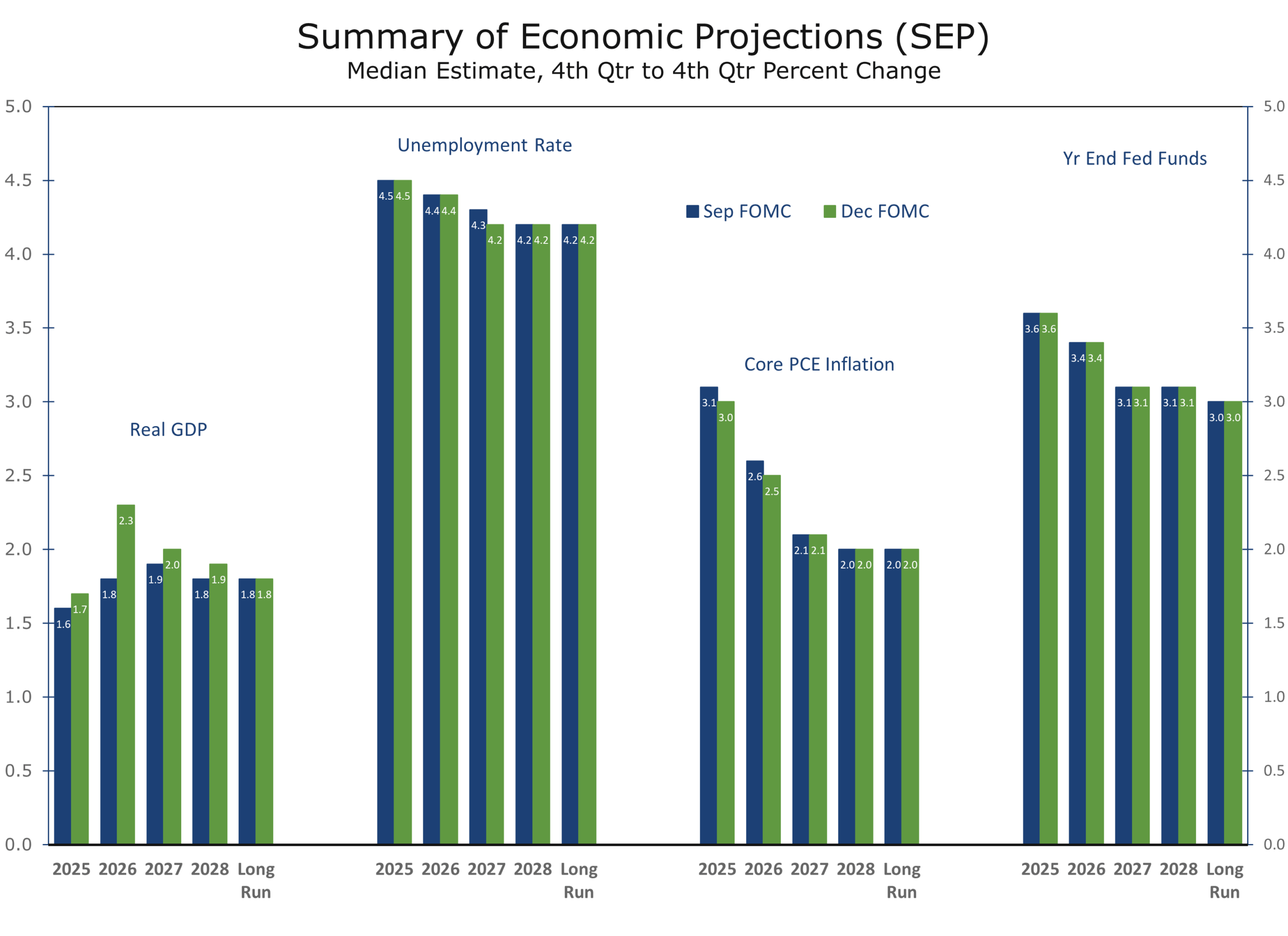

There is also a more fundamental driver behind higher long-term rates. The latest Summary of Economic Projections implies stronger private demand for funds in an increasingly investment-driven economy. The SEP lifted its 2026 GDP growth forecast by a half percentage point to 2.3% while maintaining expectations for decelerating inflation. Investment-led growth should boost productivity and ultimately lift the long-run neutral federal funds rate.

Recent Developments: Signals Beneath the Noise

Recent data reinforce a consistent theme: growth is slowing without stalling out. Small-business sentiment improved modestly. NFIB hiring intentions firmed, suggesting easing policy uncertainty and improved credit conditions may support incremental hiring in 2026. At the same time, inflation remains the top concern and pricing plans strengthened, suggesting that disinflation is uneven.

The labor market is loosening in an orderly way, shifting risk from inflation toward employment.

JOLTS added nuance. Job openings rose but layoffs edged higher. Quits are also off sharply. Job hopping is far less popular this past year and more workers are sending holiday cards to their supervisors this year.

Wage data sharpen that picture. The Q3 Employment Cost Index slowed to a pace consistent with the Fed’s inflation target once productivity is considered. Moreover, wages are rising faster for employees that remain in place than for job switchers. The bottom line is wage pressure is no longer the binding constraint for policymakers; the softening labor-market risk is.

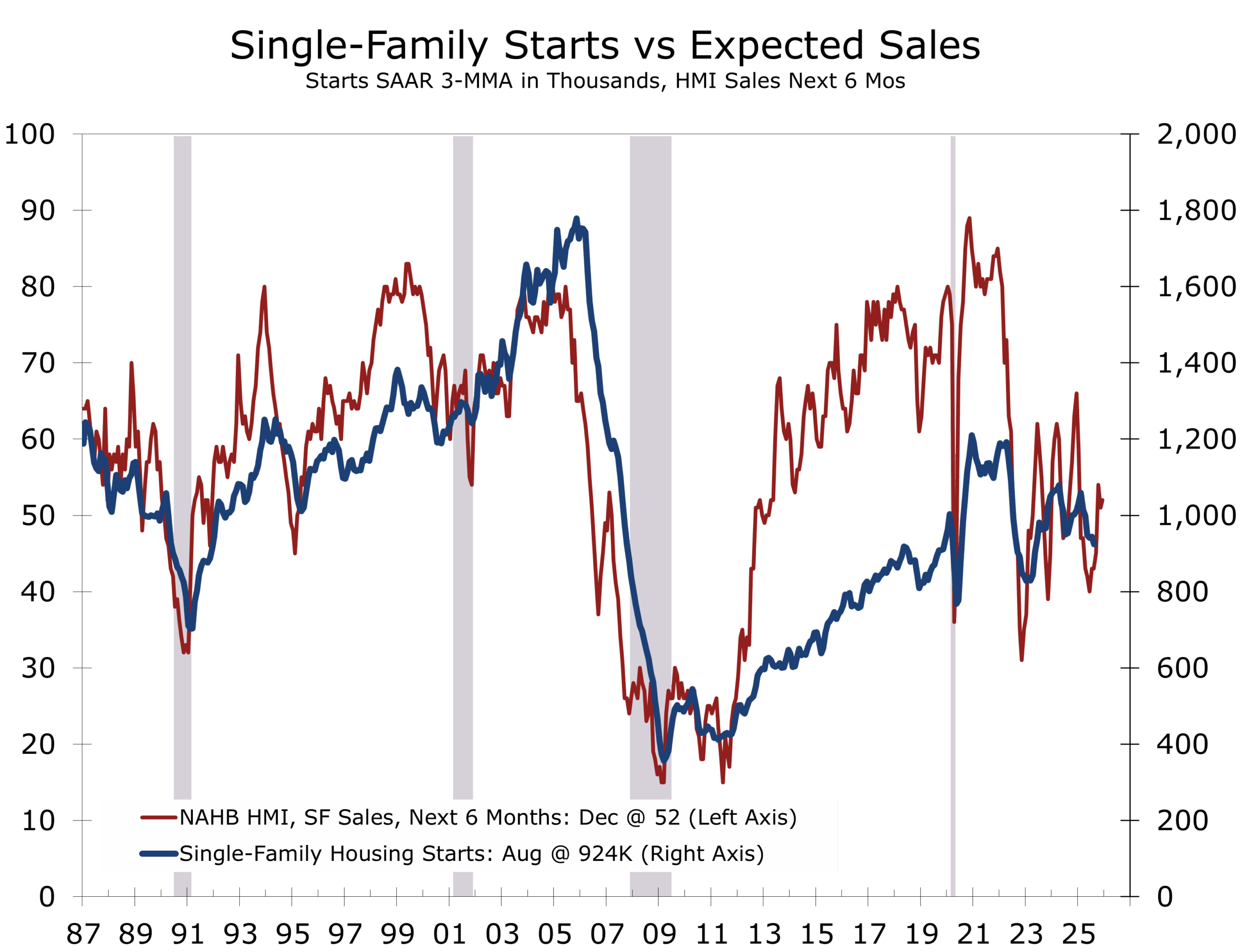

Housing remains soft but forward indicators are improving. Builders continue to rely on incentives to clear elevated inventories and expectations for sale six months ahead have strengthened—suggesting a stabilization in starts before a recovery.

A Dense Calendar at a Sensitive Moment

Monday’s releases set the tone

The Empire State Manufacturing Survey fell sharply into contraction. New orders and shipments weakened materially. Current price pressures eased, but expected prices received rose to their highest level since 2022. The six-month outlook improved notably. Current activity is soft; expectations remain resilient.

The NAHB Housing Market Index ticked higher. Current sales conditions remain subdued, but forward-looking components improved, reinforcing the view that housing is closer to a floor than a cliff.

Tuesday, December 16

The delayed October and November employment reports will be released together. Headline payroll growth should be modest, weighed down by federal displacement and early retirements. Private payrolls will offer a cleaner read on underlying momentum. The unemployment rate is expected to edge higher.

Thursday, December 18

Retail sales, flash PMIs, and CPI will round out the week, testing the Fed’s confidence that disinflation—particularly in shelter—continues into 2026. A heavy slate of Fed speakers will provide additional signal on how policymakers interpret a labor market that may already be near stall speed.

AI Investment: Growth Engine, Growing Side Effects

AI-related investment continues to do extraordinary work for the macro data. Data centers, semiconductors, power infrastructure, and AI-linked software now account for a disproportionate share of incremental business investment.

That concentration is precisely why scrutiny is rising.

AI investment is shifting from an equity narrative to a broader credit and liquidity story.

The concern is not AI’s transformative potential, but the circularity of the current build-out. Hyperscalers fund massive infrastructure projects, sell capacity across the ecosystem, capitalize internally developed software, and increasingly rely on debt structures predicated on sustained high utilization.

Investment shows up immediately in GDP. Productivity gains arrive later. Credit markets are taking note. AI has shifted from a pure equity story to a macro, credit, and liquidity story.

FOMC Statement & Powell Press Conference: We are looking for a hawkish quarter point cut, with three and possibly four dissents (one favoring a larger cut and two against any cut at all). Dissents mean less at this time, as a new Fed Chair will likely be announced ahead of the next FOMC meeting in January.

Geopolitics: Fragile Ceasefires, Shifting Lines

Geopolitical risk resurfaced over the weekend. Ceasefire frameworks in the Middle East were tested again, while developments in Ukraine suggest greater flexibility in pursuit of binding security guarantees. Markets have largely discounted geopolitical risk, but that complacency rests on the assumption that conflicts remain contained—an assumption that carries increasing weight as risk premiums thin.

Piedmont Perspective

Holiday Violence in a Connected World

Recent tragedies in Australia and at Brown University in Rhode Island are first and foremost moments of human loss. They occurred in spaces meant for celebration, learning, and community reflection, making their impact especially profound.

In recent years, violent attacks and unrest during the holiday season have become more frequent, particularly around large public gatherings tied to religious or cultural observance. From shootings and vehicle attacks in the United States to violent protests and security disruptions around Christmas markets in Europe, holidays have increasingly become moments when grievance, symbolism, and visibility converge.

While each incident is unique, many recent attacks and disruptions share a common thread. Grievances, often shaped or intensified by distant geopolitical conflicts, particularly in the Middle East, are increasingly being expressed locally. High-profile holidays and large public gatherings offer symbolism, visibility, and emotional resonance, making them vulnerable soft targets.

Holidays have always concentrated people, emotion, and symbolism. What has changed is the speed of transmission. Global conflicts are now experienced locally and emotionally in real time, amplified through fragmented information channels and absolutist framing. The fact that the FBI announced Monday that it disrupted a terror plot on the West Coast underscores both the persistence of these risks and the degree to which many threats never reach public view.

More troubling still, the language and moral framing of extremist narratives have increasingly bled into mainstream political discourse. While most participants, on the right and the left, reject violence outright, the normalization of absolutist, zero-sum framing lowers the threshold for radicalized individuals to act.

These dynamics matter economically. Social cohesion is a form of capital. When it erodes, confidence becomes fragile. Fragile confidence affects risk appetite, investment horizons, labor mobility, tourism, and, ultimately, growth.

What follows from this is not inevitability, but responsibility. Communities that fare best invest quietly in prevention by coordinating security around major gatherings, maintaining trusted local leadership, and sustaining institutions that identify isolation before grievance hardens into action. Preparedness also means having clear contingencies in place to respond quickly when tragedies occur, with the aim of saving lives and restoring order.

After a tragedy, the response matters. Collective mourning and visible, genuine support for victims and their families help restore confidence in shared spaces and prevent fear from becoming the lasting legacy. Just as importantly, these responses affirm that the overwhelming majority rejects violence, extremism, and the tactics of terror.

Empathy must come first. But resilience—social and economic alike—is sustained by the steady, often unseen work communities do before and after crisis. In that quiet resolve lies a critical source of stability, confidence, and long-term growth.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 15, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

Cooling Cycles, Rebuilding Foundations

Cooling Cycles, Recalibrated Policy, and an Economy Pulling in Different

- Growth becomes increasingly uneven. The expansion continues, but affordability pressures and demographic shifts reshape spending patterns, hiring decisions, and regional performance.

- A virtually jobless start to 2026 is increasingly likely. Payroll gains slow sharply, but tighter immigration enforcement and weaker labor-force growth keeps unemployment from rising significantly.

- Policy calibration expected by spring. Border security tightens, but a “wide door” opens for needed skill sets; tariffs rotate away from broad-based levies toward exemptions for more foodstuffs, raw materials and goods not able to be produced domestically.

- Capital, not labor, remains the cycle’s backbone. AI infrastructure, energy systems, aerospace, defense, biopharma, and advanced manufacturing continue driving investment.

- Housing begins to stabilize. Mortgage rates drift toward 6% (and maybe a little less for short periods of time), inventories rise, and affordability slowly improves—setting the stage for a mid-2026 rebound.

- Lower interest rates and steadier sentiment revive inventory building. Inventory trends were erratic in 2025 as firms first raced to get ahead of tariffs and then paused while waiting for trade policy to settle and supply chains to be reconfigured. With interest rates drifting lower, tariff policy becoming less volatile, and consumer spending and fixed investment holding firm, we expect a modest but meaningful rebound in inventory building in 2026.

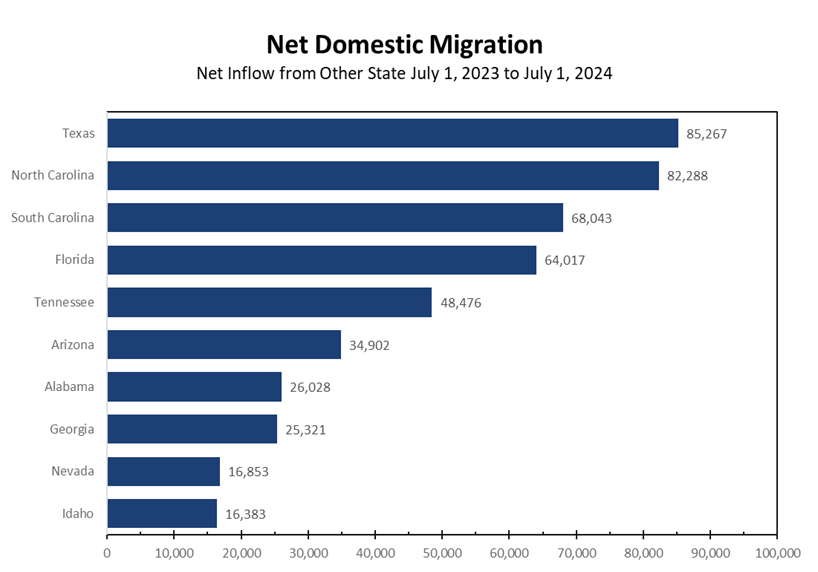

- Regional divergence widens. Two forces drive wider regional gaps in 2026. First, the fuller return to the office bolsters employment in office-adjacent sectors—retail, hospitality, and transportation—across major urban cores, including New York City, Boston, and Washington, D.C. Second, households and businesses continue migrating toward markets with more attainable housing, reinforcing growth in affordable, high-momentum regions. The Carolinas, Tennessee, Georgia, Florida, Alabama, Arkansas, and non-Triangle Texas metros are all notable standouts. Arizona, Utah, Idaho, Missouri, Ohio, and Indiana strengthen further, while Louisiana and Mississippi gain traction. The Texas Triangle, Colorado and Nevada cool as affordability ceilings and slower migration temper demand.

- Geopolitical risks remain elevated but more concentrated. The Russia–Ukraine conflict, instability across the Middle East, and U.S.–China strategic tensions continue to shape energy, trade, and supply-chain dynamics. While broad escalation risks have eased, localized flare-ups and policy missteps still pose outsized market impacts—making geopolitical communication risk a more important market variable.

Cooling Cycles, Rebuilding Foundations

As 2025 draws to a close, the U.S. economy is entering a more uneven, capital-intensive, and policy-sensitive phase of the expansion. The top-line data still points toward a soft landing, but the underlying distribution reveals an economy moving on several different tracks. Growth has cooled yet remains positive. Consumers are more selective rather than retrenching. Capital spending continues to anchor the cycle, while affordability pressures, trade volatility, and tighter immigration enforcement shape decisions in boardrooms and households alike.

The story of 2026 begins with this divergence. Younger households—who consume more relative to income as part of the life-cycle arc—face the sharpest affordability squeeze, particularly around housing, transportation, and services. Middle-income households remain constrained by accumulated price increases. Higher-income households continue to drive discretionary spending through wealth effects and better access to credit. The result is a consumer sector that looks resilient from altitude but is increasingly polarized at ground level.

Geography intensifies the divide. The nation’s growth map is tilting decisively toward affordability and industrial momentum. The Carolinas, Tennessee, Georgia, and Florida remain pillars of the expansion, but the outperforming regions now extend more broadly:

- Alabama’s I-65/I-565 industrial corridor and Gulf Coast—anchored by Birmingham, Huntsville–Decatur–Muscle Shoals, and Gulf Shores—continues to attract aerospace, automotive, defense, and logistics investment.

- Arkansas benefits from an expanding logistics, retail, and advanced-manufacturing ecosystem centered on Northwest Arkansas and the Mississippi River corridor.

- Louisiana and Mississippi gain ground through energy infrastructure, petrochemical capacity, port modernization, and manufacturing expansions from Baton Rouge to Gulfport-Biloxi and North Mississippi’s automotive cluster.

- Arizona and Utah remain two of the strongest performers nationwide, drawing semiconductor, data-center, finance, and tech investment, while consistently ranking among the fastest-growing states demographically.

- Idaho, even after cooling from its pandemic-era surge, remains a net beneficiary of affordability migration from higher-cost western states.

- Missouri, Ohio, and Indiana remain at the center of the rapidly growing EV, battery, aerospace, and defense supply-chain corridor—forming the backbone of a durable industrial renaissance.

- Texas metros outside the Triangle—including the Gulf Coast energy corridor, the Permian Basin, and the emerging industrial crescent between Amarillo, Lubbock, and Wichita Falls—show continued strength.

By contrast, the Texas Triangle (Dallas-Fort Worth-Houston-Austin), Colorado and Nevada have cooled, as affordability ceilings and slowing inbound migration weigh on hiring, housing formation, and broader economic momentum.

Labor-market dynamics tell a similar story. The first months of 2026 are increasingly likely to deliver what amounts to a virtually jobless expansion. High-frequency indicators—from ADP and online postings to diffusion indices—point toward minimal net hiring through late winter. Substantial downward revisions to 2024-2025 payrolls, expected in early February, will likely confirm the softening trend. Yet the unemployment rate is poised to rise only modestly. Slower labor-force growth—driven by demographic constraints, reduced participation among recent arrivals, and tighter immigration enforcement—lowers the break-even level of job creation. Employers remain reluctant to cut staff but equally hesitant to add headcount, producing a labor market that cools sharply without breaking.

These dynamics set the stage for a policy pivot by spring. With the midterms approaching and economic crosscurrents mounting, the Trump Administration is likely to recalibrate at the margins. Border security will remain central, but we expect the Administration to pair a tighter perimeter with a “wide door” for strategically needed skill sets in AI, energy, aerospace, logistics, and advanced manufacturing. A similar adjustment appears likely on tariffs: as negotiations deepen and USMCA deliberations unfold, we expect a rotation away from broad-based levies toward exemptions for foodstuffs, goods and raw materials not produced domestically. That would ease pressure on household budgets and small businesses while preserving strategic leverage against key trading partners.

These economic and policy crosswinds set the stage for evaluating our Top Calls for 2025 and laying out a sharpened and forward-leaning set of Key Calls for 2026. If 2025 was the year the economy cooled without cracking, 2026 is shaping up to be the year the expansion grows with fewer workers, more capital, and increasingly calibrated policy.

Looking Back at our Top Calls for 2025 — Graded and Expanded

- The U.S. Economy Would Enter 2025 with More Momentum Than Consensus Expected

While real GDP swung widely from quarter to quarter, underlying demand remained firm. Real Final Sales to Private Domestic Purchasers—what we refer to as “Core GDP”—likely maintained a better than 2.5% pace into year-end, underscoring stronger momentum than most forecasters anticipated. Private final domestic demand was supported by services spending, business fixed investment, and an unusually long tail of major construction projects. Consumption softened slightly but held up well enough to avoid a more pronounced downshift.

Verdict: Correct.

- Beneath the Surface, Momentum Would Be Softer Than the Headlines

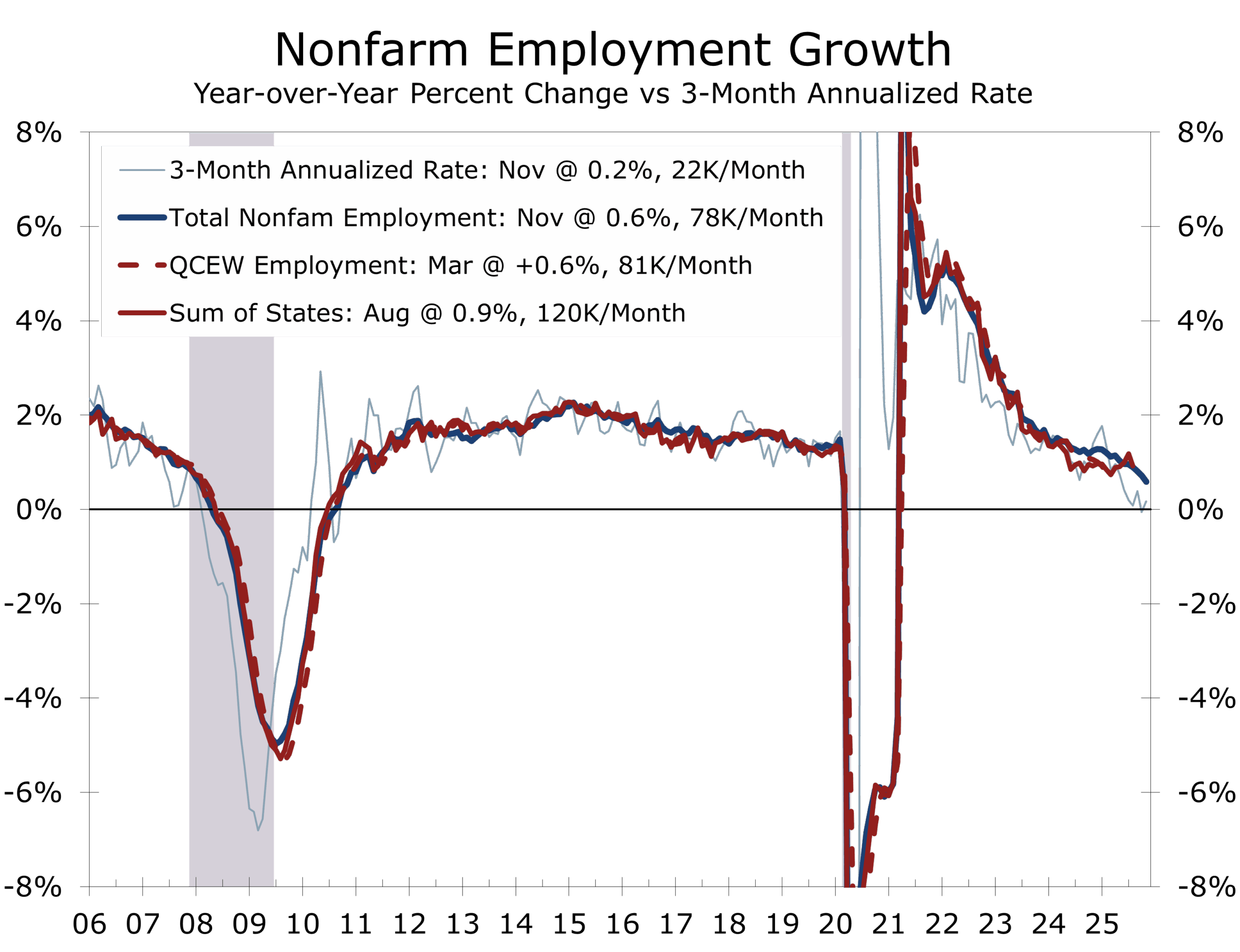

We consistently warned that headline payroll data overstated true labor-market strength. The Quarterly Census of Employment and Wages (QCEW) and state data showed materially slower job creation than the closely watched establishment survey. Diffusion indices narrowed all year, reflecting reduced breadth in hiring.

Verdict: Correct.

- Inflation Progress Would Stall, With Sticky Core Services

Shelter, insurance, and medical services slowed the descent of inflation earlier in the year. Goods disinflation continued, but sticky components of the CPI basket kept overall progress gradual. We expected tariffs to lift goods inflation in the second half, with the impulse peaking around year-end.

Verdict: Correct.

- Fed Easing Would Be Limited — Fewer Cuts Than Markets Expected

The Fed maintained a cautious posture, prioritizing credibility over speed. We argued that the Fed could accomplish more by doing less—and by communicating that conviction (“A December cut is not a sure thing – far from it.”) clearly. The first meaningful rate cuts were delayed until late summer, as uncertainty surrounding tariffs and initially strong reported job growth complicated the easing case.

Verdict: Correct.

- Long-Term Rates Had Moved into a New Structural Range

The 10-year Treasury traded in a 4.20%–4.80% band for most of the year, reflecting a higher term premium, large and persistent fiscal deficits, and firmer potential growth. Markets steadily adjusted to this new equilibrium. Yields drifted toward 4% after the September rate cut and retested that level during the elongated government shutdown, amid concern that the AI boom might grossly misprice risk and inflate asset valuations.

Verdict: Mostly Correct.

- Tariffs Would Rise, But Their Inflation Impact Would Be Modest

We anticipated the effective tariff rate rising from 2.5% to roughly 10%, while the inflation impact remained limited. Even with more aggressive rhetoric and tactics than expected, the actual pass-through to consumer prices proved far more muted than many feared. We consistently argued that consumers would resist meaningful price increases—given slower income growth and depleted excess savings—and that the pandemic-era inflation spike reflected extraordinary factors (stimulus payments, outsized fiscal spending, and an overly accommodative Fed) that were no longer operative. Moreover, unless the Fed accommodated the rise in tariffs, higher import prices would leave consumers with less money to spend on services, which would slow price increases there.

We also went to great lengths to emphasize that tariffs are assessed on the landed value of goods—net of shipping, insurance, and financing costs—not on retail prices, which significantly reduces the consumer-facing inflation impulse. In the end, the largest tariff effect was supply-chain adaptation, not consumer inflation.

Verdict: Correct in Substance.

- Housing Would Be a Drag Through at Least the Second Half of 2025

Elevated mortgage rates constrained resale supply and sidelined buyers. Builder incentives helped lift new-home sales in the fall, but affordability remained the dominant headwind, and rising concerns about job security kept many prospective buyers on the sidelines late in the year. Home prices have been gradually correcting, a necessary step toward restoring affordability and setting the stage for a more durable recovery in 2026.

Verdict: Correct.

- A Late-2025 Mortgage Repricing Window Would Begin to Open

Funding conditions and mortgage spreads showed meaningful early improvement, though not enough to materially shift demand before year-end. The groundwork for a 2026 improvement is clearly in place.

Verdict: Too Early to Call.

- Capital Spending Would Remain the Cycle’s Backbone

AI infrastructure, aerospace, defense, energy systems, and long-lead industrial projects continued advancing even as consumer spending slowed. Investment remained the most reliable engine of growth throughout the year.

Verdict: Correct.

- Market Volatility Would Rise as Growth Remained Firm and Yields Remained High

Equity markets grew increasingly sensitive to long-end yields, and volatility rose as the 10-year moved above 4.5%. Rate dynamics—more than Fed communication—drove the bulk of market repricing.

Verdict: Correct.

- Trump’s Trade Strategy Would Emphasize Negotiation, Not Extremes

Policy signals out of Washington leaned heavily on leverage and renegotiation rather than broad tariff escalation. The unexpectedly large “Liberation Day” tariffs served to strengthen the U.S. negotiating position and enabled more comprehensive trade discussions. Businesses adapted quickly, reducing policy risk.

Verdict: Correct.

- A Russia–Ukraine Framework Would Require NATO/EU Guarantees

Diplomatic readouts confirmed that any workable settlement must be anchored in credible security guarantees. This framework remains central to ongoing negotiations.

Verdict: Correct.

- Middle East Stability Would Hinge on a Ceasefire Plus Abraham Accords Expansion

The region moved incrementally closer to long-term normalization, though progress varied significantly across theaters. While the direction aligned with expectations, timelines slipped. Israel’s geopolitical isolation has increased, complicating any durable peace agreement. Rebuilding Gaza and fully integrating Saudi Arabia into the Abraham Accords will require a credible path to a Palestinian state or autonomy.

Verdict: Mostly Correct.

- China Would Study Ukraine as a Blueprint for Sanctions Resistance

China accelerated efforts to build supply-chain redundancy, develop alternative financial channels, and hedge against sanctions risk. Japan and Southeast Asia undertook similar adjustments.

Verdict: Correct.

- Global Political Turnover Would Raise Market Uncertainty

Elections across major economies introduced new rounds of volatility in currency and bond markets. Investors priced political risk more explicitly, with Japan serving as the most recent example.

Verdict: Correct.

- The U.S. Would Make It Easier for Domestic Energy Producers and Lean on Saudi Arabia to Pressure Oil Toward $60/bbl.

U.S.–Saudi coordination signaled a preference for maintaining higher output to pressure Russia and support broader diplomatic objectives. Oil prices softened substantially during the year—including brief dips near $60/bbl., depending on the benchmark used—though not consistently enough to verify the full thesis.

Verdict: Directionally Correct — Awaiting Full Confirmation.

Key Calls for 2026

- A Softish Landing Early in 2026, Followed by a More Durable Expansion

The government shutdown lasted longer and proved more disruptive than expected, with mounting pressure on air travel finally breaking the stalemate. After a surprisingly strong third quarter, we look for Q4 GDP to slip below 2% and for early 2026 to begin slowly. Business fixed investment remains the cycle’s anchor, led by AI infrastructure, biopharmaceuticals, energy and power, and selected reshoring initiatives. By spring, larger tax refunds and a nascent recovery in home buying should lift growth back toward 2.5%.

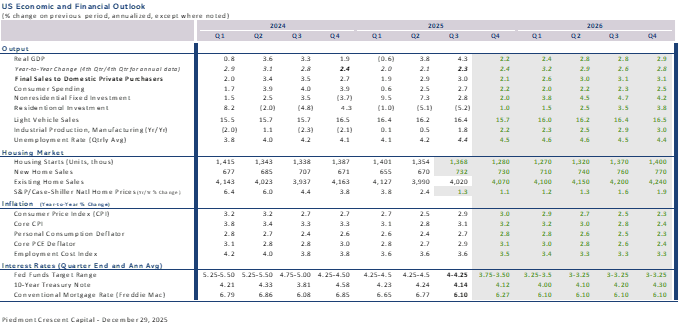

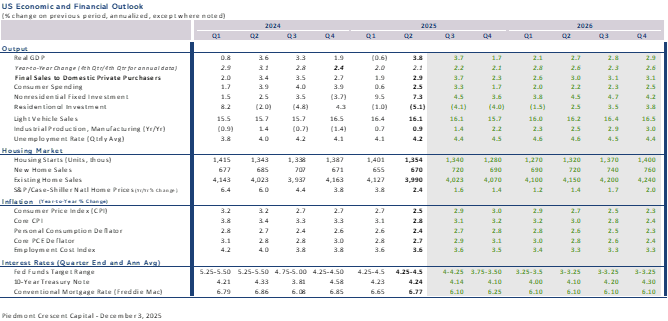

2026 Call: Stronger-than-consensus GDP growth, with real GDP rising at a 2.6% annual rate. The latest Survey of Professional Forecasts pegs 2026 growth at 1.8% and the OECD forecast for the U.S. is currently at 1.6%.

- A Capital-Led Expansion Defines the Cycle

AI infrastructure, power systems, aerospace, defense, biopharma, and advanced manufacturing remain the most durable engines of growth. These sectors are anchored in structural investment cycles and rising foreign direct investment and are far less sensitive to household sentiment.

2026 Call: Private fixed investment posts one of its strongest multi-sector performances in decades.

- The Consumer Reset Takes Hold

Consumers remain constrained by affordability pressures rather than job insecurity. Real wage gains strengthen as inflation cools, supporting firmer spending in the second half. Rising home sales also revive durable-goods spending.

2026 Call: Early caution gives way to a gradual firming in consumer activity by mid-year.

- Housing Rebounds as Inventory Improves and Mortgage Rates Drift Toward 6%

Existing home inventories are rising from historically low levels as market leverage shifts from sellers to buyers. Single-family homebuilding has slowed as pandemic-delayed projects reach completion, and builders have turned toward incentives to clear inventory. Lower mortgage rates and modest price declines should bring more buyers back into the market.

2026 Call: Housing transitions from a drag to a stabilizing force by mid-2026 and becomes a modest positive by late summer and fall.

- Employment Conditions: A Soft Patch Early in the Year, Followed by Gradual Firming

With September still the latest official payroll print, high-frequency indicators—including ADP’s measures—continue to point toward downside risk in private payroll growth, and large downward revisions to 2025 employment expected in early February add further caution. The preliminary QCEW data imply that 911,000 fewer jobs were created from March 2024 to March 2025—roughly 76,000 per month. That slower trend likely extends into the remaining months of 2025. We expect labor-market conditions to remain under pressure early in the year, with monthly nonfarm job growth hovering near zero during the first few months of 2026 before gradually improving to roughly 60,000 per month by year-end. The unemployment rate is likely to rise only modestly, reflecting unusually slow labor-force growth, while wage pressures ease further, with the Employment Cost Index advancing between 3.0% and 3.5%.

2026 Call: The labor market cools sharply early in the year but avoids a deeper contraction, stabilizing by midyear with moderate job creation and easing wage growth.

- Shelter Disinflation Drives Core CPI Toward the Fed’s Comfort Zone