A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Credibility, Capital, and the Quiet Repricing of Risk

Highlights of the Week

- Incoming data continue to support a soft-landing narrative, but the composition of growth is shifting in a more durable direction.

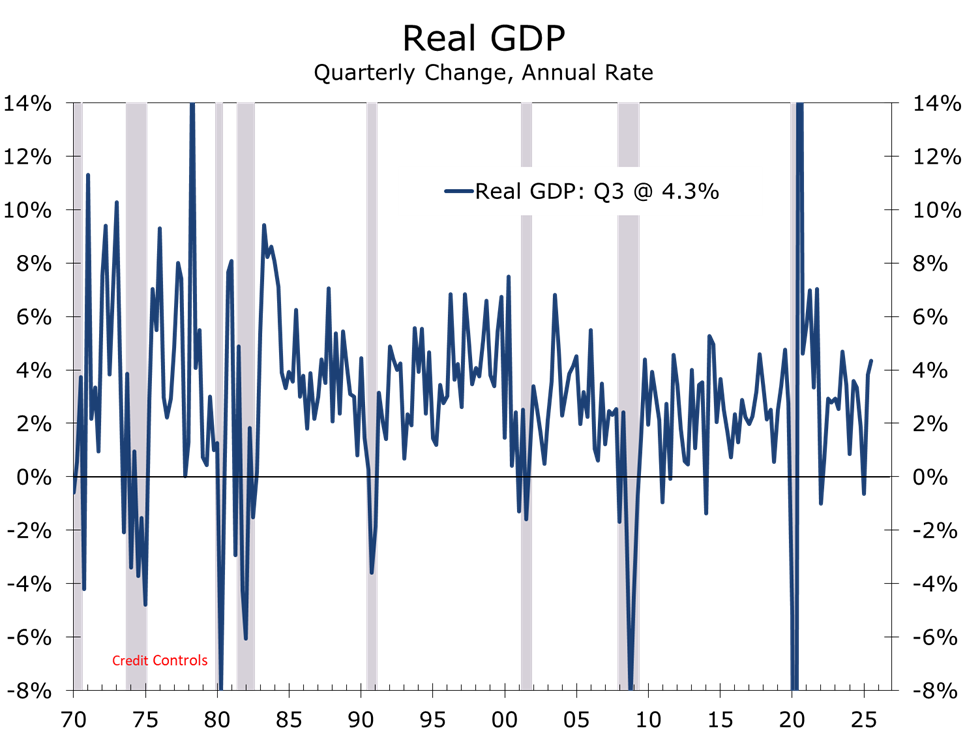

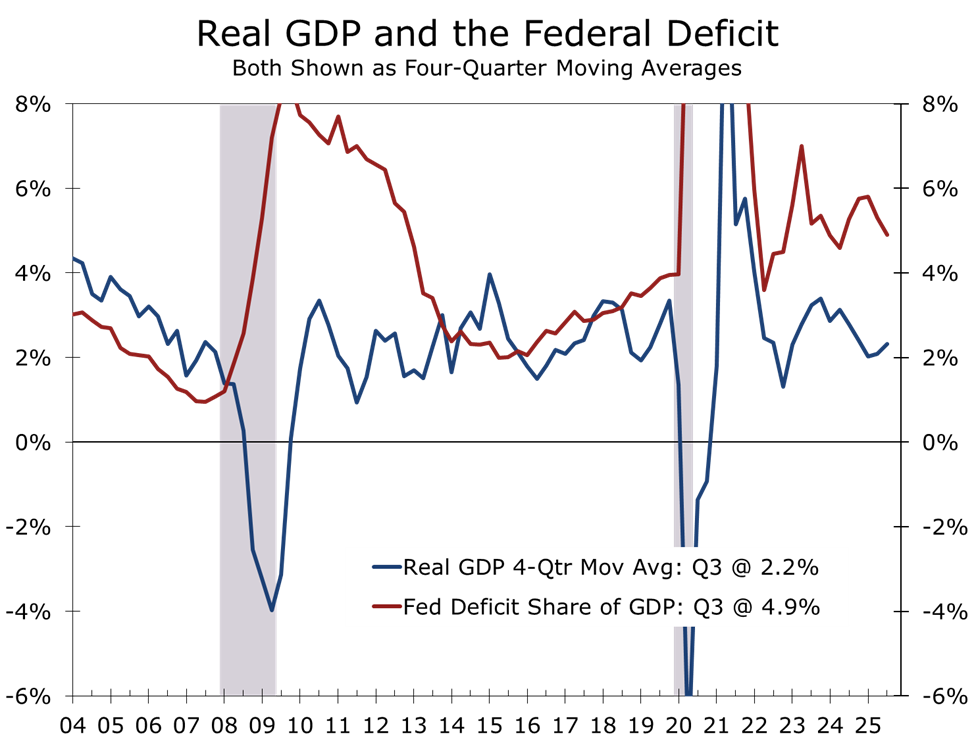

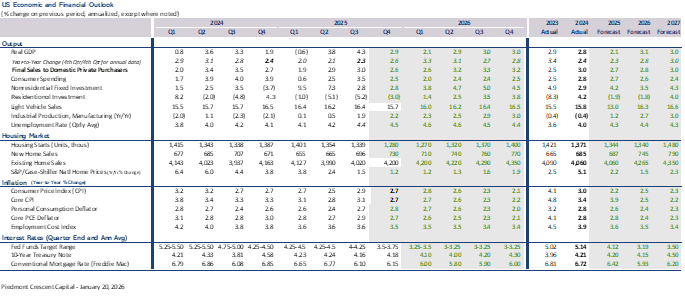

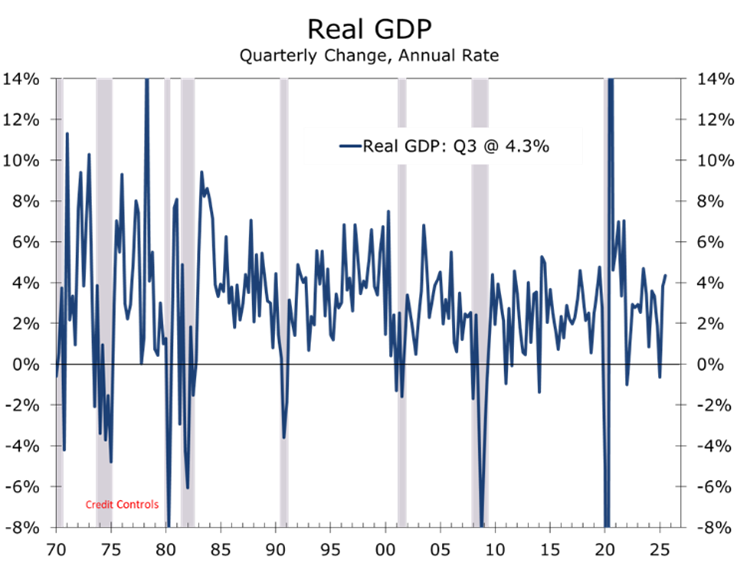

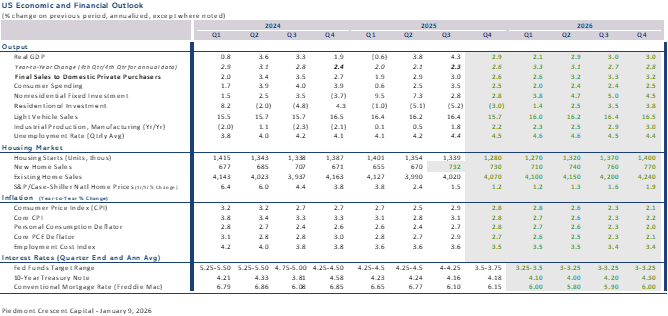

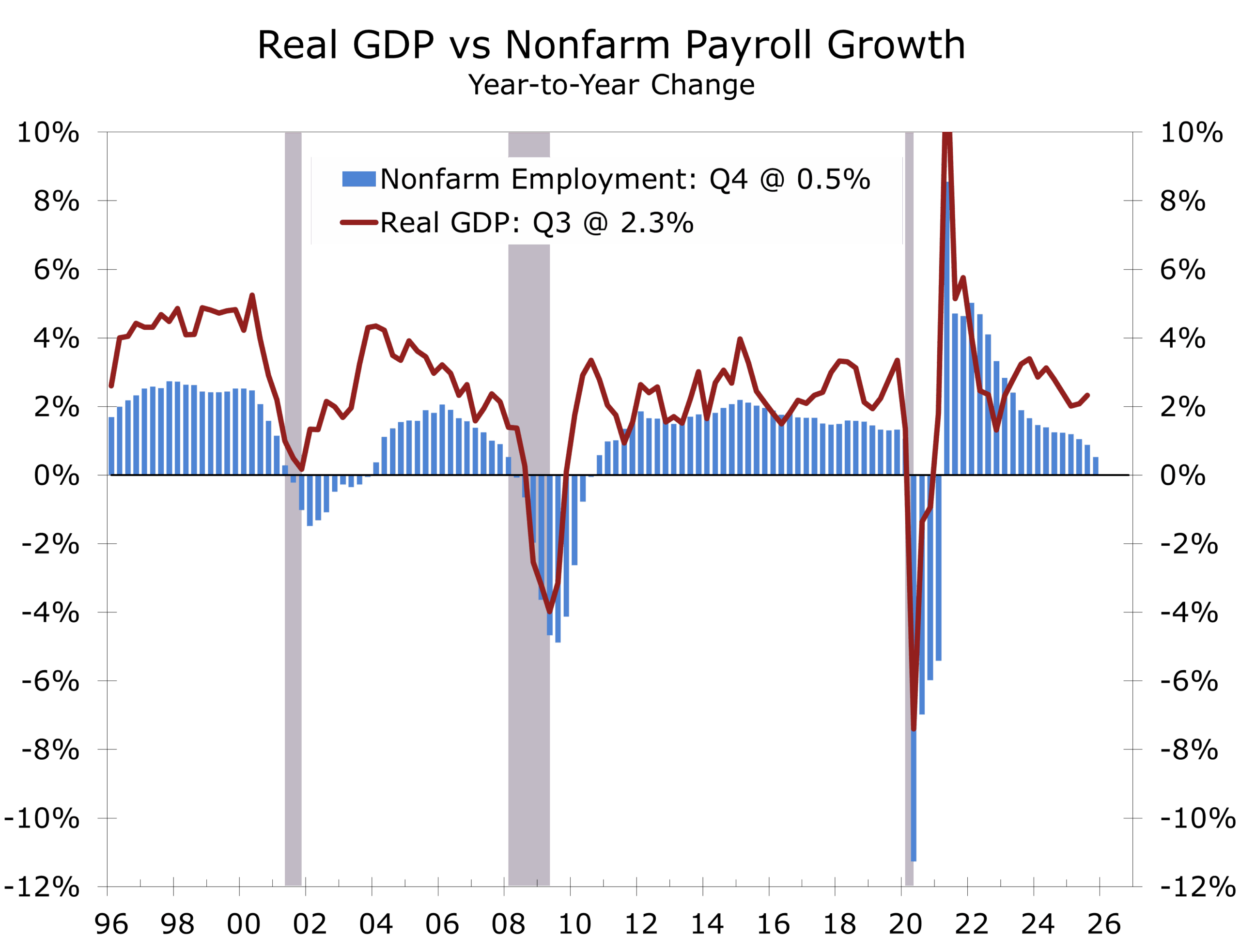

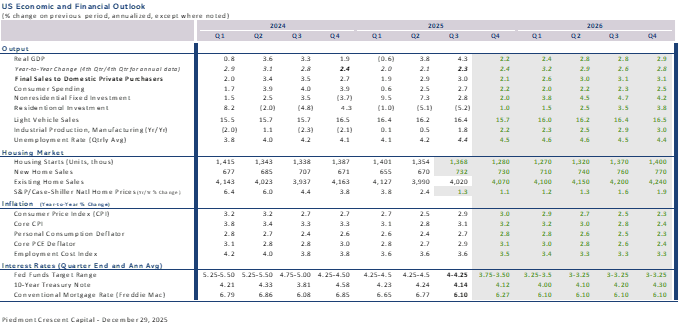

- The latest Atlanta Fed GDPNow projects Q4 real GDP growth at a whopping 5.3% pace, though likely overstated by unusually wide swings in international trade and inventories.

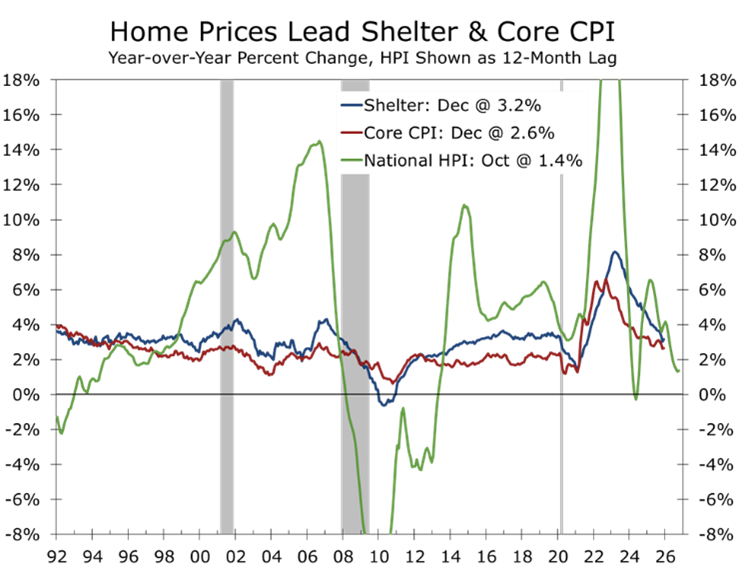

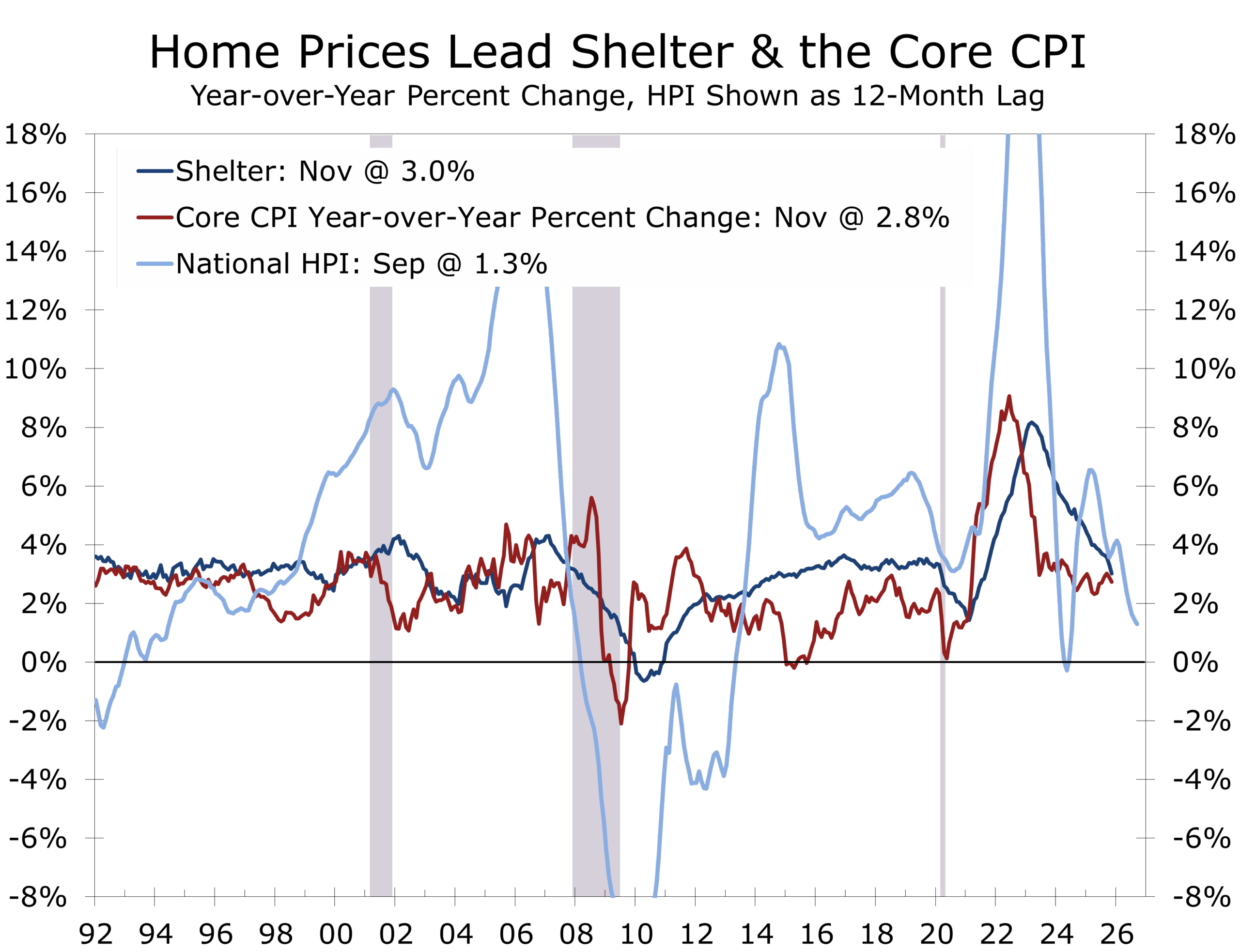

- Inflation is cooling unevenly, with shelter remaining the last mile, yet underlying cost pressures are easing more convincingly.

- Financial markets are repricing term premia and institutional risk, not growth.

- The economic script has flipped toward capital-led growth, pointing to stronger growth, lower inflation, and lower interest rates in 2026.

- U.S. real GDP growth in 2026 now looks likely to run close to 3 percent.

- This week’s Piedmont Perspective revisits credit controls through the lens of Jimmy Carter’s 1980 experiment, with uncomfortable parallels to current policy proposals

Data That Anchored the Narrative

The past week delivered a dense run of economic data that reinforced—rather than altered—the prevailing macro story. Growth is cooling toward trend but remains intact. Inflation continues to ease, though not smoothly. The labor market is adjusting through slower hiring rather than rising layoffs. Against that backdrop, markets spent the week trimming expectations rather than reassessing direction.

Inflation: The Signal Beneath the Noise

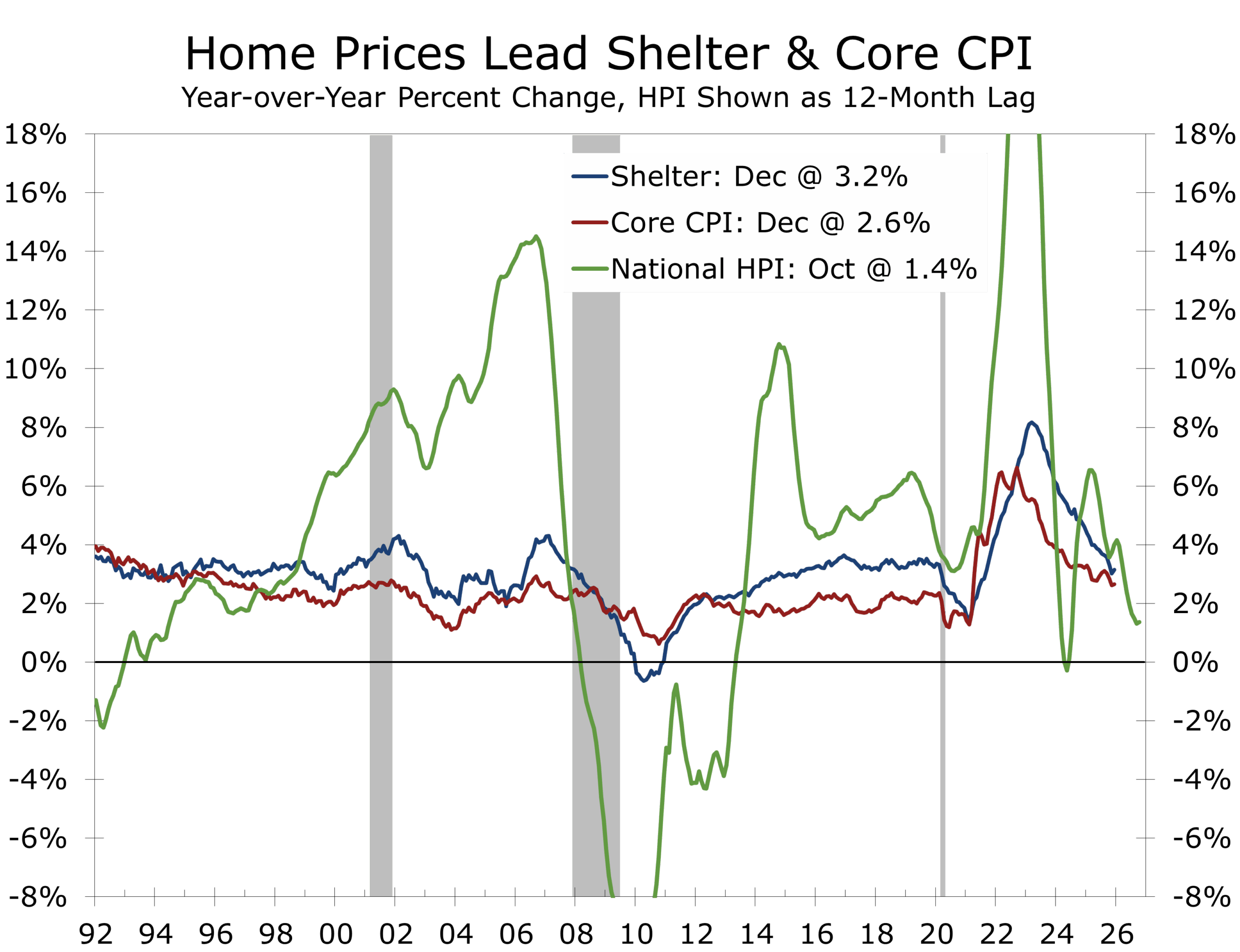

Core CPI rose 0.24 percent month-over-month in December, leaving the year-over-year rate at 2.6 percent. On the surface, the print fits neatly within the soft-landing narrative. Beneath the surface, the trend looks even better.

The three-month annualized change smooths through distortions created by the government shutdown and seasonal noise. On that basis, core CPI is running at roughly 1.8 percent annualized, or closer to 2.0 percent after accounting for the known downward bias in shelter that will not see a full offset until April. In short, the inflation trend is better than the monthly prints imply once shutdown noise and shelter timing are stripped out.

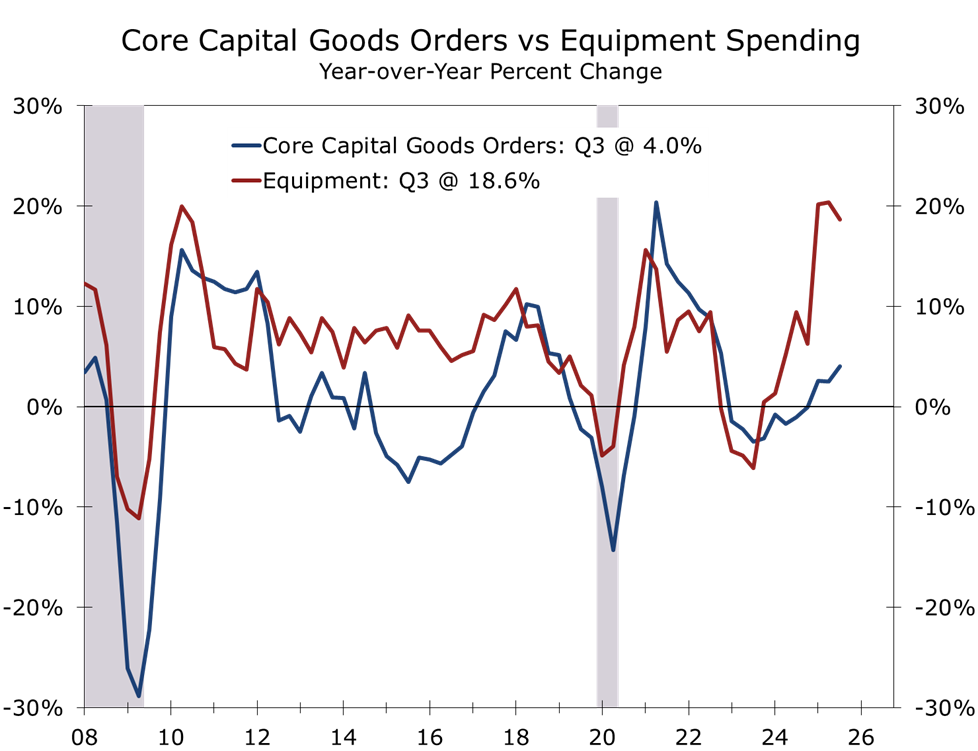

Manufacturing is contracting overall but expanding in capital-intensive segments.

Shelter remains the last mile, but not the obstacle. Outside of housing, inflation continues to cool as goods disinflation persists and services inflation grinds lower alongside improving productivity.

The federal statistical agencies continue to catch up on delayed data releases, including the closely watched personal income and spending figures, with October and November data due this Thursday. The core PCE deflator—the Fed’s preferred inflation gauge—is likely to paint a slightly less optimistic picture, finishing 2025 just under 3 percent year-over-year. The monthly path will be uneven, but the direction remains favorable. We expect core PCE inflation of 0.2 percent in both October and November, followed by a firmer 0.3 percent reading in December, which will be released in February.

Preliminary January consumer sentiment data suggests households increasingly believe the worst of tariff-driven inflation is behind them. Inflation expectations remain elevated relative to recent realized inflation and measures of price breadth, but market-based inflation expectations, which the Fed weights more heavily, remain well anchored just above the 2 percent target.

Revisions suggest underlying demand is cooling beneath still-strong GDP growth.

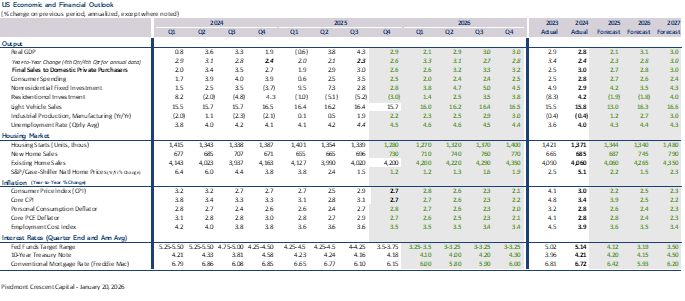

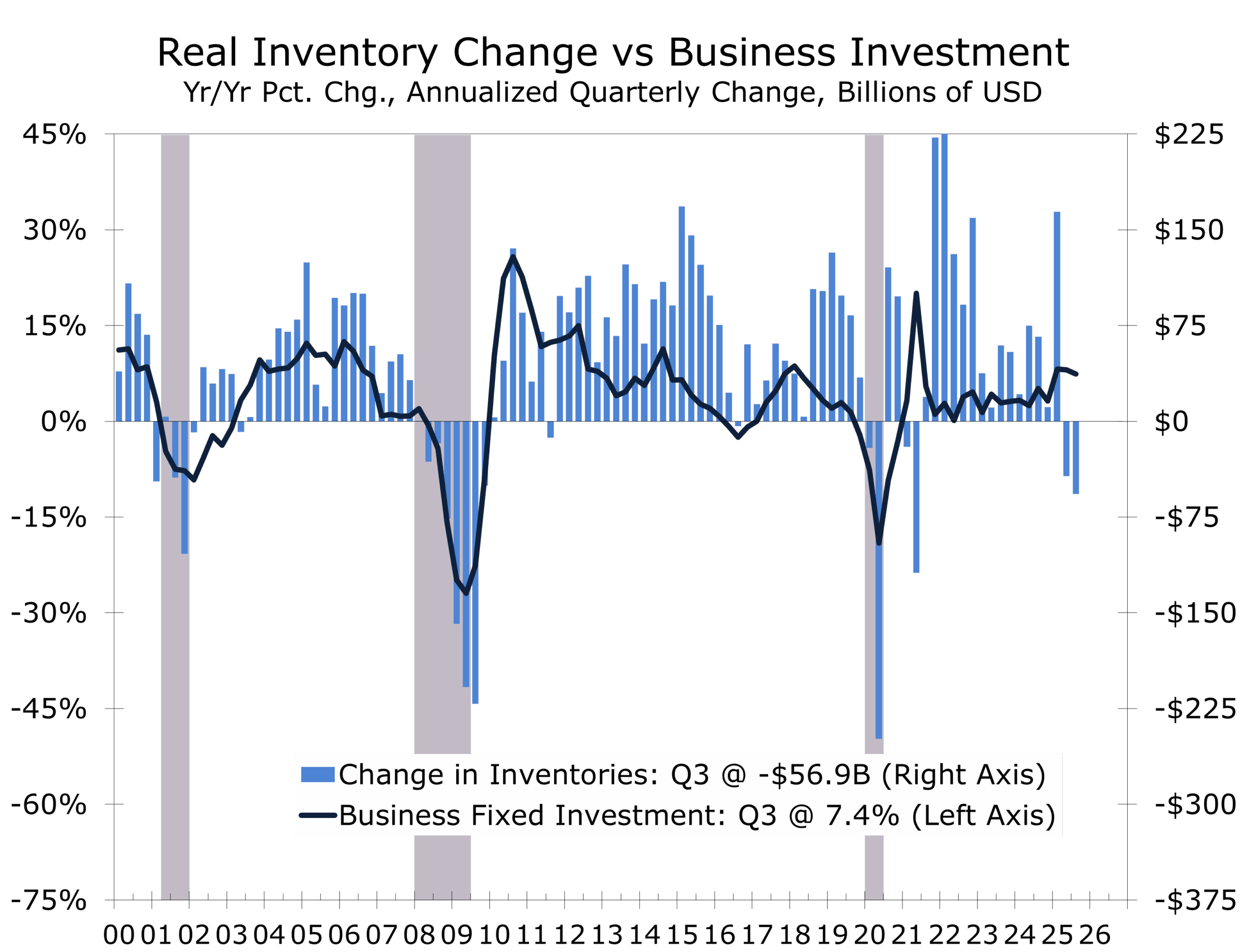

Based on the latest employment and retail sales data, along with revisions to prior months, we estimate personal spending was flat in October and rose 0.4 percent in November. We have trimmed our estimate for fourth-quarter consumption modestly while raising our estimate for inventory accumulation. Our fourth-quarter GDP forecast remains well above consensus, near a 2.9 percent annualized pace.

Industrial production rose 0.4 percent in December, with manufacturing output up 0.2 percent, reinforcing the view that activity remains firm in capital-intensive sectors. Core retail sales rose 0.4 percent in November, but downward revisions to September and October trimmed cumulative momentum. Both the Empire State and Philadelphia Fed manufacturing surveys surprised to the upside in early January, suggesting factory output is stabilizing and potentially gaining traction.

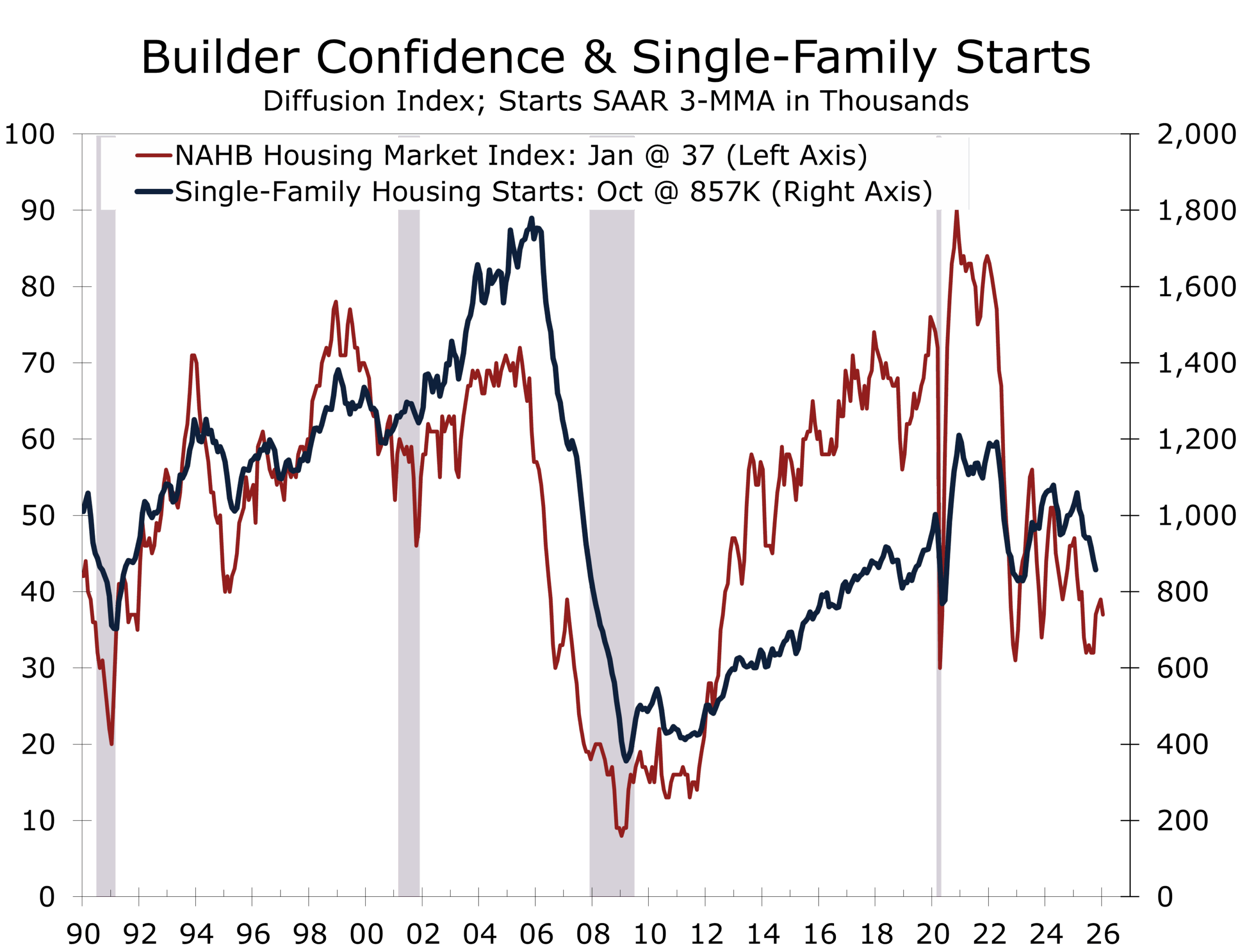

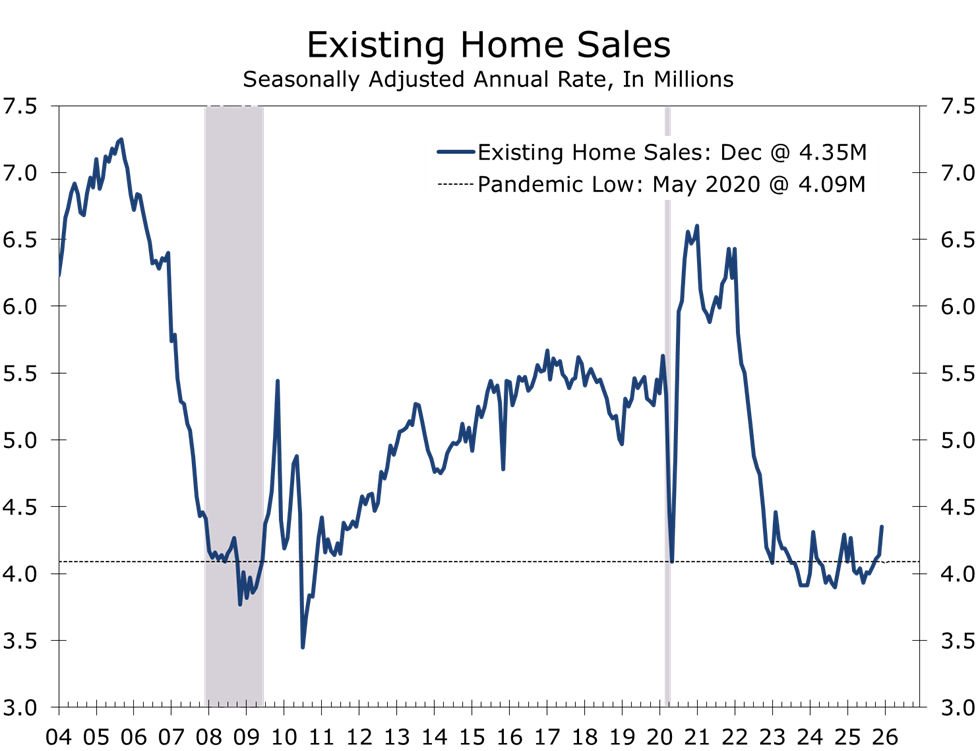

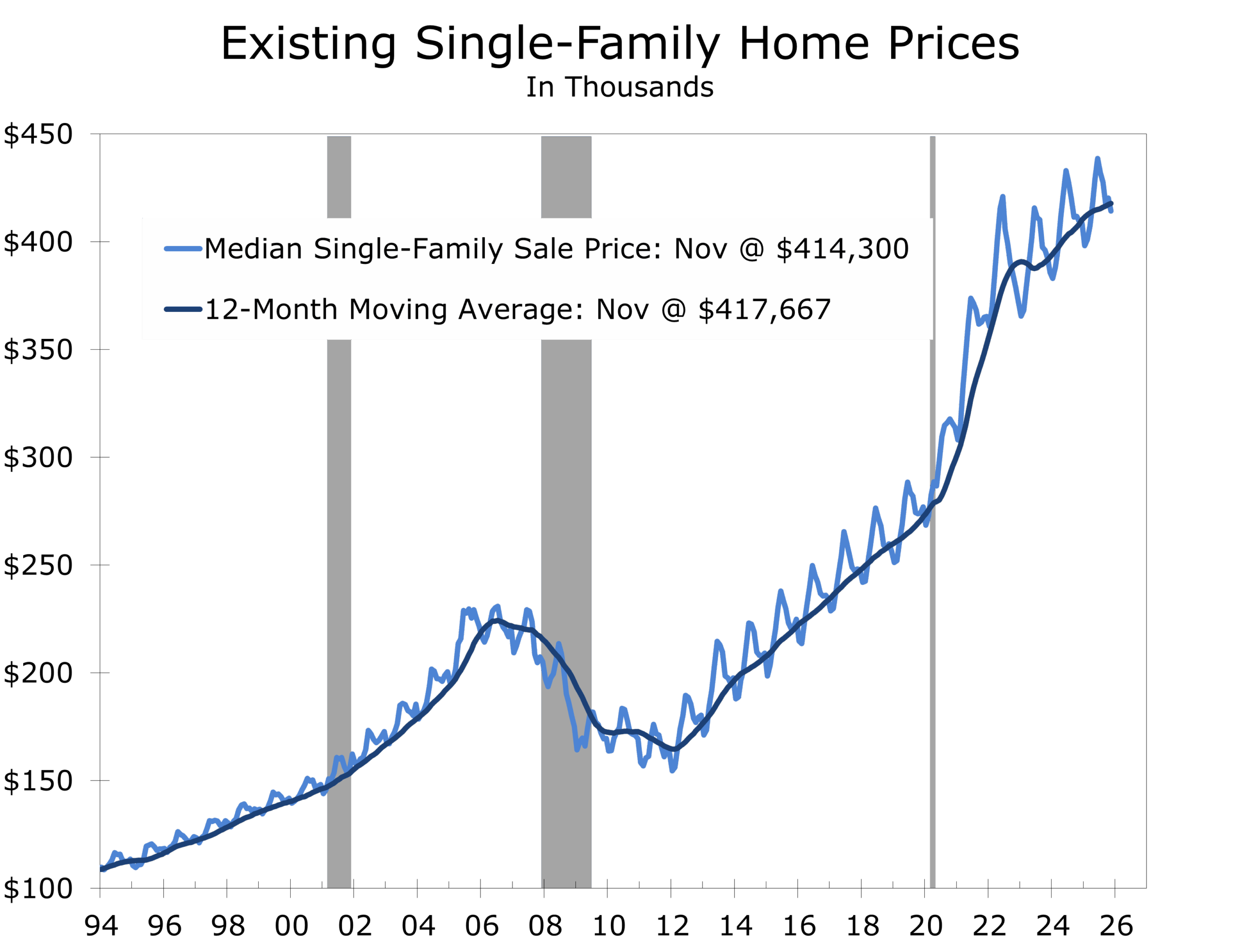

Homebuilder sentiment weakened at the start of the year as inventories of completed homes increased and near-term demand softened. Incentives remain widespread. Lower mortgage rates should provide incremental relief, but housing remains constrained by supply rather than collapsing demand. Existing home sales surprised to the upside, rising to a 4.35-million-unit pace, the strongest reading since early 2023.

Housing is lagging the cycle but no longer leading it lower.

We expect an elongated housing recovery in 2026, with sales improving in the first half of the year as mortgage rates drift back toward the 6 percent range. Elevated inventories of unsold homes are likely to restrain new construction, particularly given repeated bouts of policy uncertainty that have contributed to volatility in bond markets and mortgage rates.

Credibility Risk Replaces Timing Risk

Markets are no longer debating the precise timing of rate cuts. They are increasingly pricing institutional credibility as a balance-sheet risk variable.

The recent market configuration is instructive. Global equities sold off while the dollar weakened and gold rallied. In a conventional risk-off episode, investors would expect dollar strength and falling long-dated yields. That pattern did not materialize. Instead, the price action reflects uncertainty around policy consistency and governance rather than an imminent downturn in demand.

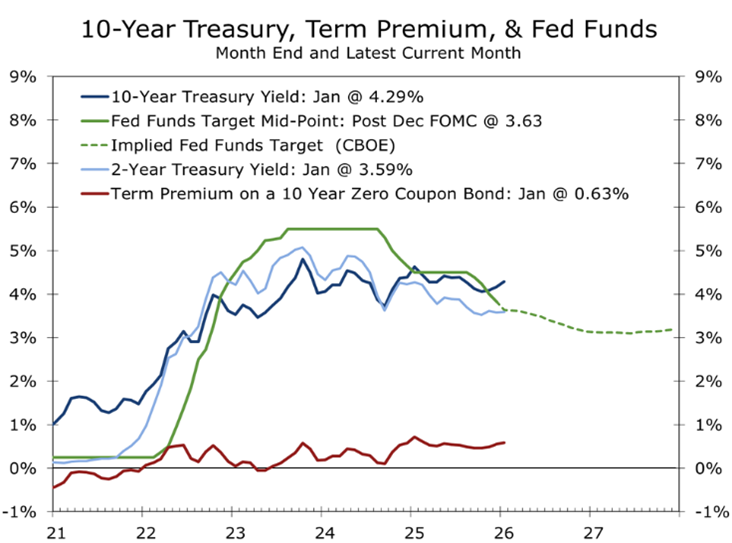

For corporate treasurers, the implication is that long-term funding costs may remain volatile even as inflation cools. Term premia, not short-rate expectations, are driving rate moves. Investors are assigning a small but non-zero probability that political pressure could influence monetary or trade policy at the margin. That risk shows up in the cost of duration, FX hedging, and insurance.

Credit markets remain orderly. Spreads are contained and access to funding is intact. The adjustment is occurring through hedging costs and risk premia, not a withdrawal of liquidity.

This environment favors funding discipline over rate-cut optimism. Opportunistic term issuance, stress-testing of cash and FX hedges, and flexibility in duration exposure matter more than precisely timing the first rate cut.

The Script Has Flipped: Capital Over Calories

For much of the past decade, growth relied on consumption, leverage, and fiscal sugar highs. That model delivered speed, not durability.

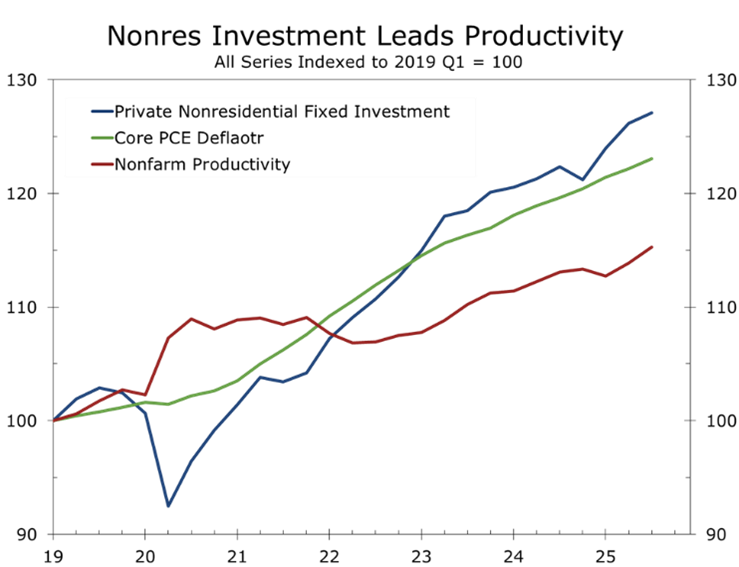

This cycle looks different. Growth is increasingly driven by capital investment in AI infrastructure, power generation, advanced manufacturing, aerospace, biopharma, and defense—long-cycle investments tied to productivity and resilience rather than leverage.

This is a capital-fed expansion, not a credit-fed one. Stronger growth can still be disinflationary.

Productivity has surged, and the multi-year trend since 2019 is consistent with roughly 2 percent annualized growth. Inventory rebuilding and reshoring reinforce the durability of the expansion.

Setting the Stage for 2026

The data and the evolving composition of growth argue for a more constructive 2026 than consensus implies. A capital-led expansion supported by productivity gains and inventory rebuilding is well positioned to deliver stronger real growth with less inflation pressure.

Under this mix, U.S. real GDP growth in 2026 now looks likely to run close to 3 percent. Lower interest rates become the outcome of disinflation, not its precondition.

Policy remains the wild card.

Piedmont Perspective

Echoes of Jimmy Carter: Credit Controls Revisited

President Trump’s proposal to cap credit-card interest rates at 10 percent reflects a familiar impulse. Affordability pressures rise, and policymakers reach for visible solutions.

Credit controls do not make borrowing cheaper. They make credit scarcer.

The closest historical parallel is President Jimmy Carter’s 1980 credit controls. Inflation did not fall. Credit availability collapsed, consumer spending retrenched sharply, and the economy entered a steep recession. Real GDP declined at an 8% annual rate in Q2 1980, marking one of the steepest quarterly drop on record.

A rate cap would operate through the same channel today. Credit would contract most sharply where marginal propensities to spend are highest. History suggests such policies stick briefly, then snap—and make a mess.

Greenland in the Crosshairs

Ukraine and the Middle East continue to add background risk rather than acute shocks. The more consequential geopolitical development for markets this week has emerged from the Arctic. The escalating U.S. push to assert control over Greenland has become a flashpoint, underscoring how trade policy is increasingly being used as geopolitical leverage and why the Arctic is no longer a peripheral theater.

President Trump’s posture has hardened since early January, following what the administration views as a successful assertion of hemispheric control in Venezuela. The Greenland episode fits a familiar strategic pattern: advancing foreign policy objectives through executive action amid domestic legislative gridlock and heightened judicial scrutiny. Trump’s negotiating style has long relied on opening from an extreme position, forcing counterparts to engage from ground they would not otherwise accept.

The centerpiece of the strategy is a tariff ultimatum announced via social media. Beginning February 1, the United States would impose 10 percent tariffs on imports from Denmark and seven European allies—Norway, Sweden, France, Germany, the United Kingdom, the Netherlands, and Finland. Those tariffs would rise to 25 percent by June 1 unless a deal is reached for what the president described as the “complete and total purchase” of Greenland.

Greenland’s strategic value explains the intensity of the standoff. The island occupies a central position in Arctic missile-defense architecture, hosting early-warning radar systems critical to U.S. and NATO detection of ballistic and hypersonic threats from Russia. Control of Greenland also strengthens oversight of North Atlantic and Arctic shipping corridors as melting ice opens new routes between Asia, Europe, and North America. These developments carry commercial promise but introduce new security and surveillance challenges.

Layered on top of defense and shipping is geology. Greenland holds significant rare-earth deposits essential to advanced electronics, renewable energy systems, and defense manufacturing. Any disruption to Arctic cooperation or European alignment would have second-order implications for supply chains already undergoing reshoring and diversification.

European leaders have responded forcefully, warning that the move risks fracturing NATO and triggering a retaliatory trade cycle. U.S. imports from the targeted countries have averaged roughly $360 billion annually over the past three years, while European officials have identified more than $100 billion in potential countermeasures. In Greenland itself, protests underscore local resistance, and Danish officials continue to reaffirm sovereignty.

From a market perspective, the episode matters less because conquest is likely and more because escalation is plausible. The probability that the United States would attempt to seize Greenland by force appears exceptionally low—likely 20 percent or less—given institutional constraints, waning public support, bipartisan opposition in Congress, and legal limits embedded in the National Defense Authorization Act. The odds that emergency tariffs ultimately survive judicial scrutiny have also diminished. In short, checks and balances still matter.

Markets are not pricing certainty. They are pricing tail risk.

That is exactly what they are doing. Volatility has risen, term premia have widened, and classic insurance assets have been bid. The VIX has moved to three-month highs, not because global growth is in doubt, but because alliance stability and policy predictability have become less certain. We do not envision an outcome that materially jeopardizes NATO. Still, markets remember how aggressively Trump has pressed allies in the past—on defense spending and Nord Stream among them—and are struggling to price a negotiating style that deliberately tests institutional boundaries.

Bottom Line

The macro story still reads soft landing. The growth story reads capital led. The market story reads credibility sensitive.

This is a regime adjustment, not a regime break. The repricing is quiet at first and historically modest. The implications are not.

The Week Ahead: Validation, Not Revelation

The coming week is less about new information than confirmation. With the Fed in blackout ahead of the January FOMC meeting, markets will focus on data consistency rather than policy signaling.

What Matters

Construction Spending and Pending Home Sales (Wednesday)

Core PCE inflation (Thursday). We expect monthly gains of 0.2 percent in both October and November, corresponding to year-over-year rates near 2.7–2.8 percent. Confirmation would reinforce confidence that disinflation remains intact despite December noise.

Personal income and spending. Income is expected to rise 0.2 percent in October and 0.4 percent in November, with spending flat in October and up 0.4 percent in November, broadly consistent with recent retail sales data.

Labor market consistency. Initial claims are expected to rebound toward 210k. As long as claims remain at historic lows and continued claims do not trend higher, the labor market will be viewed as cooling, not cracking.

PMIs and sentiment. January preliminary PMIs and final Michigan sentiment will help gauge whether risk headlines are bleeding into real activity.

What Matters Less

Headline rate volatility absent a sustained move in term premia.

Geopolitical headlines that do not disrupt energy flows or trade logistics.

Bottom Line for the Week

The burden of proof remains on downside risks. Absent a negative inflation or labor-market surprise, markets are likely to continue trading the same theme that has defined the start of the year: steady growth, cooling inflation, and rising sensitivity to policy credibility rather than actual cyclical stress.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 20, 2026

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

Protein Over Sugar: Flipping the Script

Protein Over Sugar: Flipping the Script

- 2026 is setting up as a better year than most year-end consensus forecasts projected. The economy continues to shift from a consumption-led to a capital-led expansion with a meaningful assist from inventory rebuilding and a gradually thawing housing market.

- Fiscal policy is still pushing, not pulling. The deficit is large, front-loaded, and additive to demand. CBO estimates the federal deficit totaled $601B in the first quarter of FY2026.

- Inflation is drifting back toward target. Productivity gains and shelter disinflation are doing the heavy lifting, with tariffs now largely in the rear-view mirror rather than a forward shock.

- Rates likely settle lower than feared. The market story is less “cut now” and more “you can cut later without regret” as inflation normalizes. Look for the federal funds rate to undershoot this year as the economy moves to the new next thing.

- Fed leadership is now a market variable. The next Chair choice matters, but the more immediate question is which candidate can preserve credibility, avoid politicization, and keep the inflation-expectations anchored but still allow for capital-intensive economic growth to run well above its past long-run trend.

- Geopolitics continues to have surprisingly little market impact. Pressure on European allies to help craft a deal on Greenland is a negative surprise but we do not expect a material change in relations with NATO nations. Some action against Iran remains likely, which is putting a higher floor under natural gas prices.

The Script Has Flipped

For most of the post-GFC era, economic growth was fueled by cheap credit, asset inflation, and a steady diet of policy sugar. After a sluggish start, that model delivered quick calories through leverage and wealth effects, but it left the economy dependent on low rates and loose financial conditions. Growth was demand-heavy, inflation-prone, and increasingly fragile.

The 2026 playbook looks fundamentally different. The key drivers of growth have flipped, much like RFK Jr. flipped the food pyramid. This expansion is being built on protein rather than sugar. Capital spending, productivity gains, inventory rebuilding, and a housing thaw are the economy’s key drivers this year. Growth is less reliant on consumption pulled forward by credit and more grounded in the economy’s ability to produce.

The next phase of expansion is less about how much consumers can borrow and more about how productively capital is deployed.

These drivers are inherently disinflationary. Productivity expands supply faster than demand. Capital deepening allows firms to raise output without bidding up labor costs. Inventory rebuilding reduces scarcity premiums rather than creating them. A housing recovery driven by volumes instead of prices helps cool shelter inflation rather than reignite it.

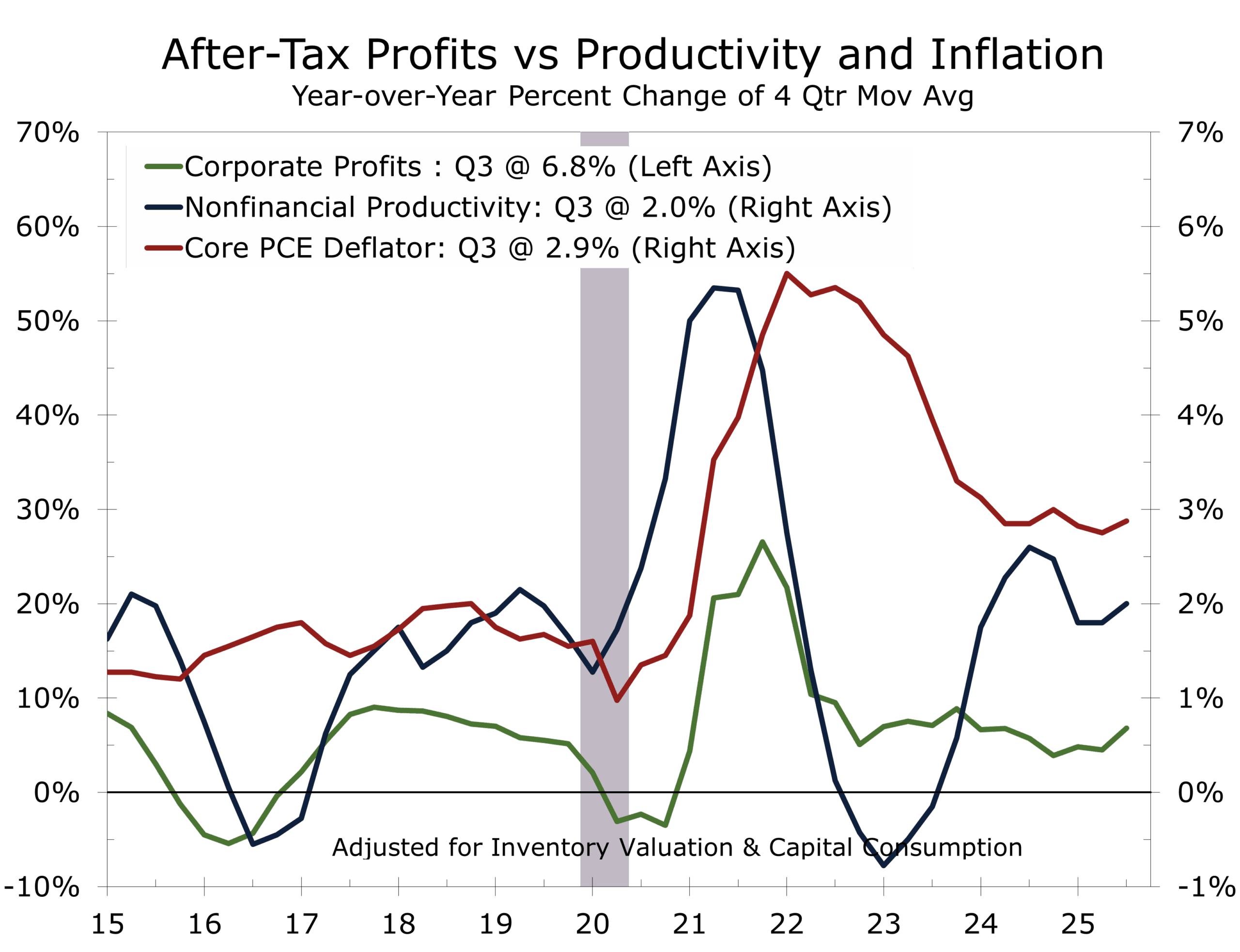

This is also a profit-led expansion, and that distinction is critical. Firms are increasingly generating earnings through efficiency and capital discipline rather than price increases. Margins are being protected by productivity gains even as nominal growth moderates. Profits can grow in a disinflationary environment when costs fall faster than revenues. We are looking for productivity growth to ramp up to a 2.7% pace and look for inflation to fall back toward the Fed’s 2% target by the end of this year. Such a scenario should be good for corporate profits.

Importantly, this does not require a weak consumer. Consumer spending is likely to prove resilient, supported by income growth, balance-sheet repair, and a gradual easing in interest rates. The consumer is no longer the accelerant but will serve more as a stabilizer. Once home buying catches a second wind, we should see notable knock-on effects for furniture, appliances, and related goods and services.

That balance matters for markets. Equity valuations are already full, reflecting confidence that profits continue to compound despite slower headline growth. In this regime, upside is less about multiple expansion and more about execution. The risk is no longer runaway inflation, but whether earnings growth can continue to validate a fully priced market in a capital-driven cycle.

Fiscal Impulse: Still Additive

Fiscal policy remains a tailwind. Even without new legislation, the federal deficit is large enough to support nominal growth and cushion periods of private-sector softness. This is not a tightening environment by any reasonable historical standard.

According to the Congressional Budget Office, the deficit totaled roughly $601 billion in the first quarter of FY2026. The Bipartisan Policy Center notes that the CBO projects a $1.7 trillion deficit for FY2026, equivalent to roughly 5½ percent of GDP. That level of borrowing is inconsistent with austerity and continues to provide meaningful macro support.

The implications are straightforward. First, the economy has a built-in demand buffer, reducing downside risk even as growth moderates. Second, because fiscal restraint is not doing the work, disinflation must come from the supply side—through productivity gains, easing shelter costs, and improved capacity utilization rather than weaker demand.

Washington is not tightening. The private sector is adapting.

Against that backdrop, targeted fiscal initiatives can still matter at the margin. The Big Beautiful Bill (BBB) functions less as baseline support and more as an accelerator, channeling stimulus through higher-multiplier mechanisms. Front-loaded infrastructure spending and expanded middle-income tax credits tend to recycle quickly through local labor markets and construction pipelines, supporting private-sector CAPEX and employment before broader deficit effects fully materialize.

The result is a fiscal environment that is not merely passive, but selectively stimulative. This mix should reinforce growth while leaving the burden of disinflation squarely on productivity and supply-side normalization rather than policy restraint.

Capital Spending: The Cycle’s Anchor

With fiscal policy setting the floor, capital investment is defining the ceiling. Business fixed investment remains the backbone of this cycle. AI infrastructure, power generation and grid upgrades, biopharma, aerospace, defense modernization, and selective reshoring are driving a multi-year capex stack that is far less sensitive to consumer sentiment than typical late-cycle investment.

This investment reflects a reordering of priorities shaped by demographics, energy intensity, national security, and technological scale. Firms are not expanding because demand is overheating, but because capacity, resilience, and productivity matter more in this cycle than marginal labor growth.

Business investment remains the cycle’s anchor, allowing the expansion to regain traction as housing re-engages and seasonal tailwinds lift spring growth.

A near-term accelerant is tax uncertainty. When firms face ambiguity around expensing rules, credits, or corporate rates, they do not typically freeze investment. They pull it forward, especially when balance sheets are healthy and strategic projects are already approved.

Trade data reinforce the point. Capital goods imports have been a clear outlier, supported by high-tech equipment tied to AI infrastructure and data centers, even as other import categories have softened. That divergence underscores how investment demand is being driven by structural needs rather than cyclical exuberance.

This matters for inflation. Capital deepening expands productive capacity, eases bottlenecks, and allows output to grow without proportionate increases in labor or prices. In other words, the same forces lifting capex are also reinforcing disinflation, validating the broader theme of a supply-led, profit-sustaining expansion.

Inventories: A Quiet Tailwind

After a long stretch of lean inventories and cautious ordering, the economy is positioned for incremental inventory rebuilding. That is not glamorous, but it is powerful and will help broaden economic gains beyond the narrow subset that has been driving capital spending.

Think of inventory as the cycle’s flywheel. When inventory moves from drag to neutral, growth accelerates even if final demand merely holds steady. Inventory rebuilding will also help drive demand in transportation and warehousing, which has been noticeable soft since tariffs were introduced in early April of last year.

.

Housing: Thaw First, Then Build

Housing has been the missing transmission mechanism in this cycle. That is beginning to change.

The initial response is showing up in stronger home sales, not a surge in construction. As mortgage rates drift lower and inventories improve at the margin, existing home sales can rebound quickly from depressed levels. Preliminary data suggest sales averaged roughly 4.06 million units in 2025, then firmed late in the year, reaching a 4.35-million-unit pace in December, the strongest reading since early 2023.

That improvement matters, even if conditions remain uneven. Many markets are still buyer-friendly, with easing prices and affordability constraints keeping pressure on sellers. Turnover is the key transmission channel. Rising sales support brokerage income, renovation activity, furniture and appliance demand, and a confidence lift that feeds back into consumption.

Mortgage rates in the 6% range, and occasionally a little under that, appear to be the psychological threshold that re-engages buyers and begins to unlock existing homeowners who have been content to remain in place with sub-4% mortgages. Housing cycles are behavioral as much as financial. Rising activity draws in additional sellers, improves inventory, and reinforces momentum.

The second phase comes later: stronger homebuilding, most likely in the back half of the year. Builders remain focused on managing affordability and elevated inventories of completed homes, while a sizable pipeline of projects under construction continues to work through. That backlog limits the risk of a rapid supply surge even as demand improves. Apartment overbuilding will also keep a low ceiling on multifamily construction.

Housing does not need to boom to matter. It simply needs to improve off recent lows.

This sequencing is critical for the macro-outlook. Housing first supports growth through turnover and consumption; construction follows with a lag. In a capital-led expansion, that delayed response helps extend the cycle rather than cause it to overheat.

Productivity, Inflation, and Rates: The Supply-Side Flywheel

The most underappreciated driver of this cycle is productivity. The third-quarter surge was not a statistical fluke, but an early signal of a broader shift now underway. As output accelerates ahead of hiring, productivity growth is likely to remain elevated over the next several quarters before settling into a higher structural run-rate.

Our expectation is that productivity growth stabilizes between 2.5 and 3.0 percent, materially above the post-GFC norm. That alone is powerful. At that pace, the economy can sustain real GDP growth near 3 percent in both 2026 and 2027 without recreating the inflation pressures that defined earlier expansions.

In this cycle, productivity is doing the heavy lifting that policy usually does.

This is the mechanism that makes the broader 2026 outlook coherent. Capital spending expands supply-side capacity. Productivity rises. Unit labor cost pressure eases. Services inflation moderates. The Federal Reserve gains room to normalize rates without re-accelerating inflation. Growth is no longer dependent on policy stimulus or excess demand. It is being earned through efficiency.

Inflation, in that context, is not collapsing. It is normalizing. The tariff-driven pulse that interrupted disinflation has largely peaked. The next leg lower comes from shelter, where home prices have flattened and rents historically follow with a 12 to 18-month lag. As shelter inflation rolls over and productivity restrains services inflation outside housing, the glidepath back toward the Fed’s target becomes increasingly plausible.

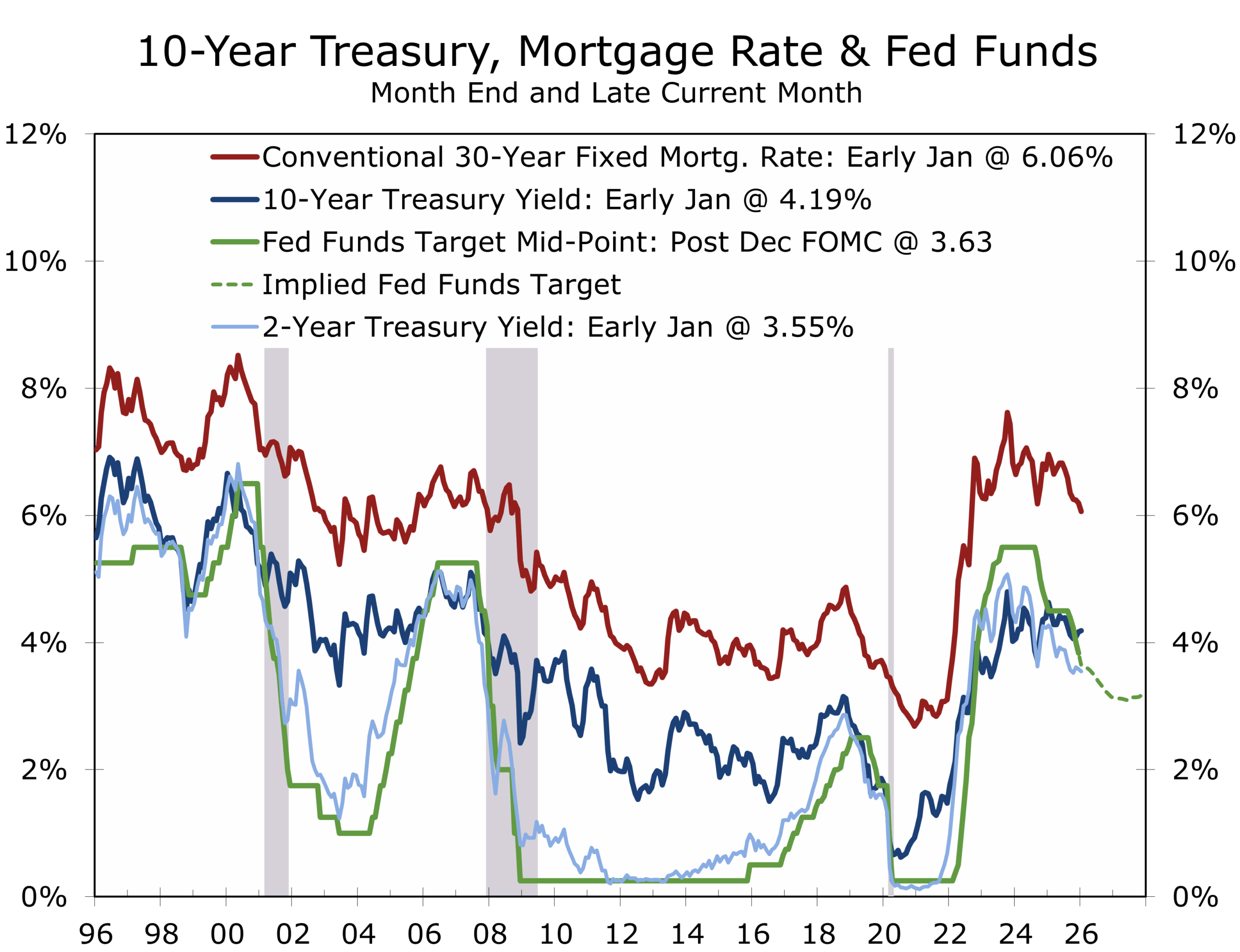

That combination reshapes the interest-rate outlook. Markets remain focused on the timing of the next cut, but the more important question is why rates can be lower. If inflation drifts back toward target while growth holds near trend, the rate regime shifts from restrictive protection to neutral normalization. Historically, that environment supports lower front-end volatility, a gradual decline in real yields, and only modest curve steepening—unless fiscal dynamics force term premia higher.

This backdrop elevates the importance of Federal Reserve leadership. With Chair Powell’s term ending in May 2026, the Chair decision is no longer a distant personnel matter; it is now part of the market narrative. The central issue is not loyalty or ideology. It is credibility.

Markets can accommodate a new Chair. What they cannot accommodate is ambiguity around the Fed’s objective function. The next Chair must be unambiguously committed to the 2 percent inflation target, credible on independence, pragmatic rather than doctrinaire, and experienced in the mechanics of liquidity and market functioning when term premia move. Continuity lowers risk premiums. Perceived regime change raises them.

Recent reporting has highlighted a short list that includes sitting and former Fed officials as well as White House advisers. Our view is straightforward. If the objective is continuity and minimal credibility risk, an experienced Fed leader with a strong inflation-fighting record is the cleanest outcome. If the objective is a sharp break, markets will demand a higher risk premium until credibility is re-established.

In this cycle, growth, disinflation, and lower rates are not in conflict. They are linked by productivity. The forecast rests less on policy easing and more on the economy’s improved ability to grow without overheating. We expect two quarter-point rate cuts this year, most likely in March and June, with a third cut possible if labor market conditions weaken convincingly or inflation returns to target more rapidly than expected.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 20, 2026

Mark Vitner, Chief Economist

704-458-4000

The Piedmont Perspective – Echoes of Jimmy Carter: Credit Controls Revisited

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 20, 2026

Mark Vitner, Chief Economist

Piedmont Crescent Capital

December 2025 Consumer Price Index: Shelter Reaccelerates Modestly, Food Pressures Resurface, Core Inflation Holds Near Target

Inflation Continues to Ease Back to Historic Norms

-

- Headline CPI rose 0.3% in December, while year-over-year inflation held steady at 2.7%, reinforcing evidence that inflation has likely peaked for this cycle.

- Core CPI increased 0.2%, leaving core inflation unchanged at 2.6% y/y, slightly softer than expected once shutdown-related distortions are accounted for.

- Shelter prices rose 0.4%, the largest contributor to the monthly increase, though part of the recent volatility reflects data distortions tied to the federal shutdown rather than a change in trend.

- Food prices surprised to the upside, rising 0.7% on the month, with both grocery and restaurant prices contributing.

- Energy prices increased modestly, driven by natural gas, as unseasonably cold weather offset falling gasoline prices.

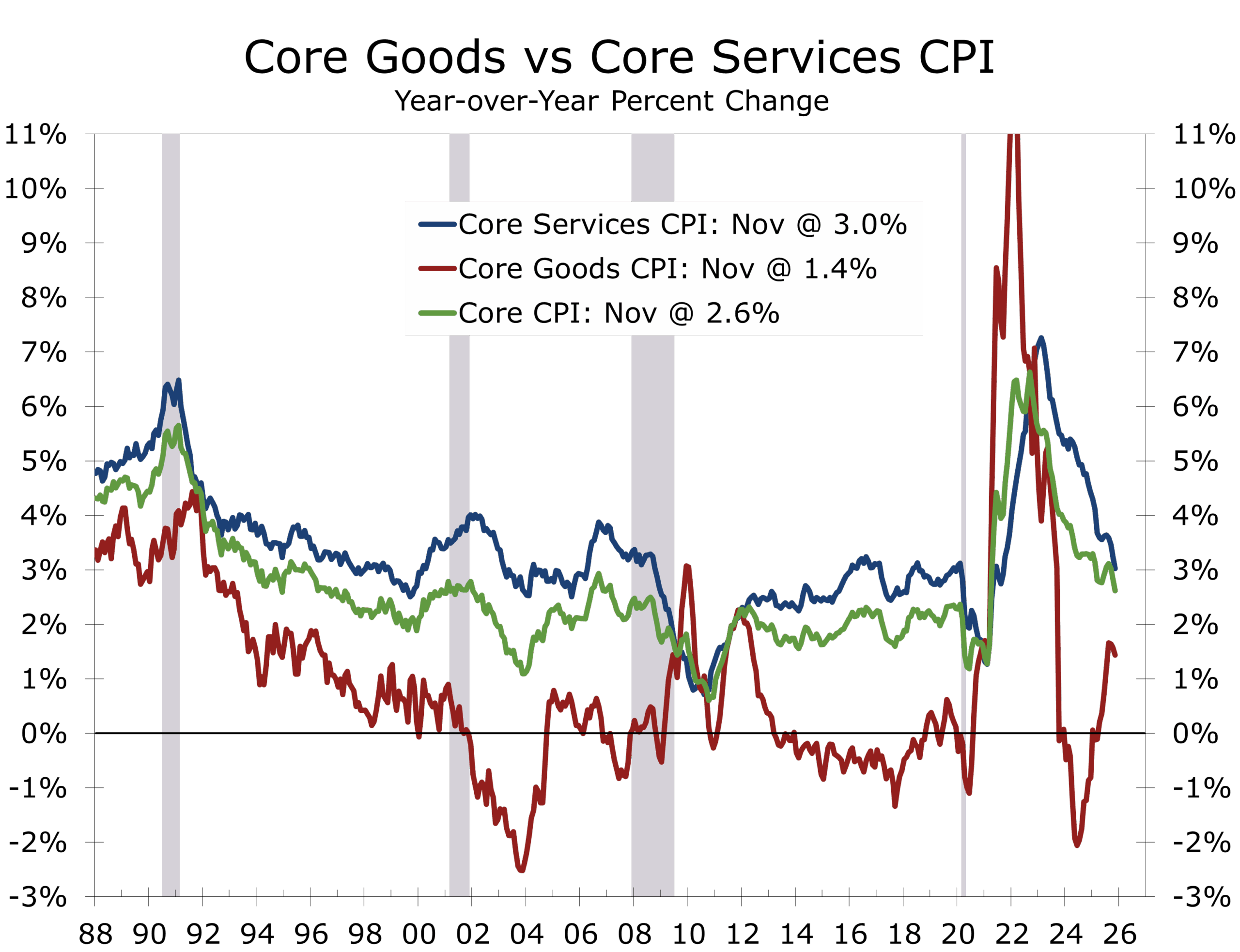

- Core goods inflation appears to have peaked, while services inflation outside of shelter continues to trend lower, supported by improving productivity and easing unit labor costs.

Headline Inflation: A Firm Finish to the Year

Consumer prices rose 0.3% in December, a step up from November, driven primarily by shelter and food. On a year-over-year basis, headline inflation held at 2.7%, confirming that inflation has stabilized at a lower level even as month-to-month readings remain uneven.

December’s report was noisier than usual due to the federal shutdown, which compressed data collection and distorted comparisons with prior months. November prices were collected only for late in the month, exaggerating some December increases, particularly in seasonal and holiday-sensitive categories. Even so, stepping back from the volatility, the broader signal suggests inflation continues to decelerate, and the bulk of the impact from tariffs is now behind us.

Inflation continues to decelerate and is now roughly even with its long-run trend.

Energy prices added modestly to the headline, while food prices delivered an outsized monthly gain. The combination pushed the CPI headline higher even as underlying inflation trends remained broadly consistent with the Fed’s target range.

Core Inflation: Stable, but Not Yet Settled

Core CPI rose 0.2% in December, matching recent monthly averages and keeping core inflation at 2.6% year over year. The rise in the core CPI was slightly softer than expected once shutdown distortions are considered, reinforcing the view that underlying inflation pressures are easing.

Tariffs are most evident in core goods inflation, which now appears to have peaked.

Core goods prices declined again, led by sharp drops in used cars and trucks (-1.1%), communications (-1.9%), and household furnishings (-0.5%). Broader core goods inflation now appears to have peaked, reflecting slower tariff pass-through, easing supply-chain pressures, and growing efforts by the Administration to reduce the sting of tariffs.

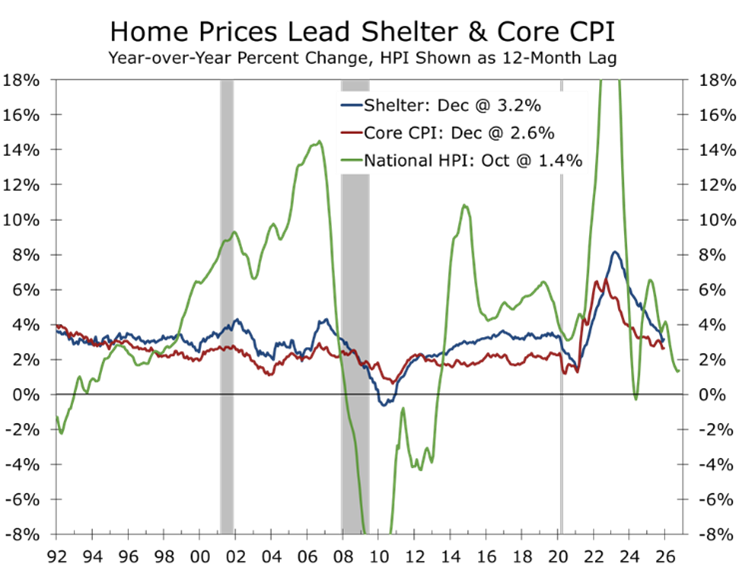

Shelter prices rose 0.4% in December, firmer than in recent months, with both rent and owners’ equivalent rent up 0.3%. The headline was rose more than its two largest components because hotel and other lodging costs surged 3.5%. The spike likely reflects the later survey period, which picked up more holiday season demand. Year-over-year shelter inflation now stands at 3.2%, well below cycle highs but still elevated relative to pre-pandemic norms.

Market-based rent indicators continue to point toward further moderation in 2026 as elevated multifamily supply works through the system. Moreover, home prices, which have reliably provided a leading signal for shelter costs 12 to 18 months ahead, continue to ease.

Shelter costs continue to follow home prices lower and will likely bring the core CPI back to the Fed’s target by year-end.

The message is clear; core inflation is headed lower this year and will likely finish 2026 close to the Fed’s 2% target.

Food prices rose 0.7% in December, marking one of the strongest monthly gains of the year. Grocery prices increased broadly, while restaurant prices continued to reflect elevated labor and operating costs.

Food away from home inflation remains particularly sticky at 4.1% y/y, reinforcing why many consumers remain skeptical of improving inflation data despite easing headline measures. The jump in food and energy prices are the least encouraging elements of the report. We suspect that the later than usual timing of the survey meant that the survey picked up much more of holiday season price hikes. We are looking from more modest gains in grocery prices in 2026.

Higher restaurant prices are likely to weigh on office workers as the return-to-office trend solidifies, with higher beef prices remaining a key upside risk. Restaurants have little room to cut prices, as labor costs are rising along with the minimum wage.

Energy: Volatile but Contained

Energy prices rose 0.3% in December, driven by a sharp increase in natural gas prices amid colder weather, while gasoline prices declined. Over the past year, gasoline prices are down 3.4%.

While falling global oil prices are easing gasoline costs, rising electricity demand, including from data centers, is limiting the pace of disinflation in utilities. Even so, energy continues to behave as a swing factor rather than a structural inflation driver.

We are looking for energy costs to moderate this year, as natural gas prices fall back and restrain electricity prices. The Trump Administration is also likely to lean on utilities this year to avoid passing on the costs of ramping up capacity to serve data center. Finally, the move against Venezuela’s ghost fleet of supertankers will keep oil prices lower.

Services inflation firmed in December, with notable increases in recreation (+1.2%), airline fares (+5.2%), and lodging away from home (+2.9%). These categories remain closely tied to upper-income demand and labor intensity. This past month’s hikes, however, were largely overstated, as the survey took place later than usual and was impacted by holiday season travel.

Goods prices, by contrast, continue to ease, reversing last year’s tariff-driven run-up. Improving productivity growth is helping to slow unit labor costs, which should support further moderation in services inflation outside of shelter in 2026.

Inflation pressure is becoming more concentrated, not widespread.

December’s CPI reinforces a clear shift in the Fed’s reaction function. Both the headline and core CPI have returned to their long-run average of 2.7% and 2.6%, respectively, easing the central bank’s policy dilemma. Inflation is no longer the dominant risk, though residual seasonality and shutdown distortions will complicate interpretation in coming months.

The federal funds rate remains modestly restrictive, and rate cuts are best viewed as insurance rather than stimulus. With inflation fears fading, the Fed has greater flexibility to respond to downside risks in the labor market should conditions weaken.

The inflation data argues for patience rather than urgency. President Trump has gotten the affordability memo and is also likely to use his bully pulpit to pressure firms to restrain price increases, an approach that should prove marginally effective at the margin. With price pressures already easing, we expect both headline and core inflation measures to be near the Federal Reserve’s target by year-end.

December closes the year with inflation lower than a year ago, but still uneven across categories. Shelter is cooling gradually, goods prices are deflating, and services inflation remains the final hurdle. Strip away shutdown distortions, and the evidence increasingly suggests inflation has peaked and is on a slow glide path lower into 2026. Disinflation is intact, but the last mile will remain uneven and politically sensitive as the new year begins.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 13, 2026

Mark Vitner, Chief Economist

(704) 458-4000

The Piedmont Perspective – Institutional Home Buying: Populism Meets the Balance Sheet

Housing politics in a supply-constrained economy

Executive takeaway

Proposals to limit institutional purchases of single-family homes reflect real frustration over housing affordability, but they misdiagnose the problem. Large institutions own only a small share of the U.S. housing stock and cannot explain the national rise in home prices; where they matter is at the margin, in supply-constrained metros where purchase flows can amplify price pressures and reduce entry points for first-time buyers. Even there, institutional activity is a second-order effect layered on top of a much deeper structural shortage driven by years of underbuilding, restrictive zoning, rising construction costs, and strong in-migration. Recent data show institutions already slowing acquisitions and shifting toward build-to-rent, helping expand rental supply rather than crowd it out. Framing affordability as a battle between households and institutions may be politically appealing, but durable relief will come from expanding housing capacity—faster permitting, zoning reform, and infrastructure investment—not from constraining capital in an already undersupplied market.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 12, 2026

Mark Vitner, Chief Economist

Piedmont Crescent Capital

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – An Economy on Parallel Rails

Highlights of the Week

- Growth signals remain bifurcated. Manufacturing continues to contract, services have re-accelerated, and GDP tracking models still point to a very strong fourth quarter. The economy is advancing on parallel rails, not in a straight line.

- The labor market is cooling without cracking. Hiring has slowed materially, wage growth is easing, and productivity is doing more of the work. This is a low-hire, low-fire environment, not a recessionary one.

- Financial conditions remain supportive. Credit markets reopened forcefully, issuance surged, and risk assets are behaving as though policy is restrictive only at the margin.

- Policy risk has shifted from inflation to institutions. Political pressure on the Federal Reserve introduces a new variable that could extend policy restraint even if inflation continues to improve.

- Geopolitics has moved from background noise to event risk, but markets are still treating it as a premium rather than a macro shock.

U.S. macro: mixed signals, durable momentum

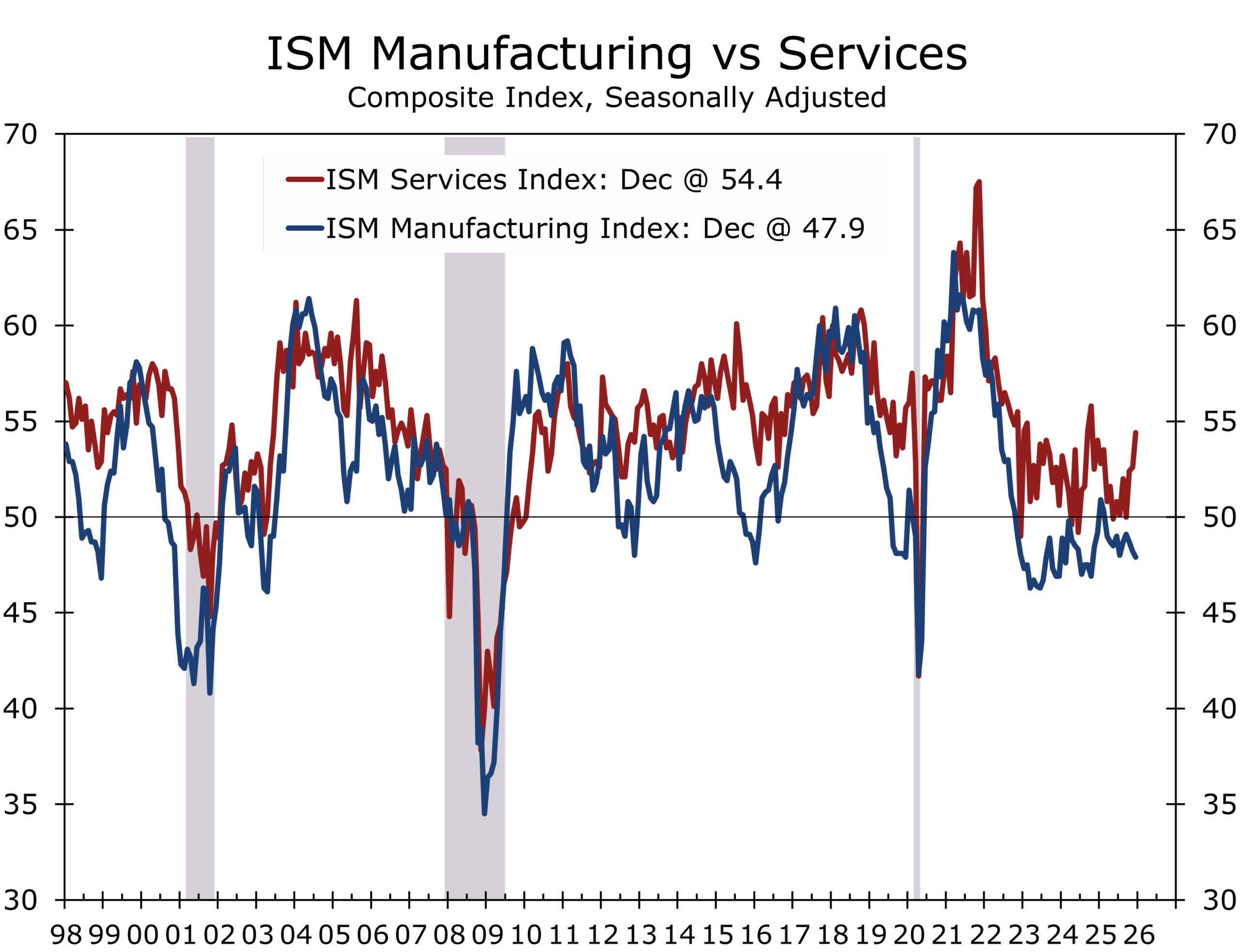

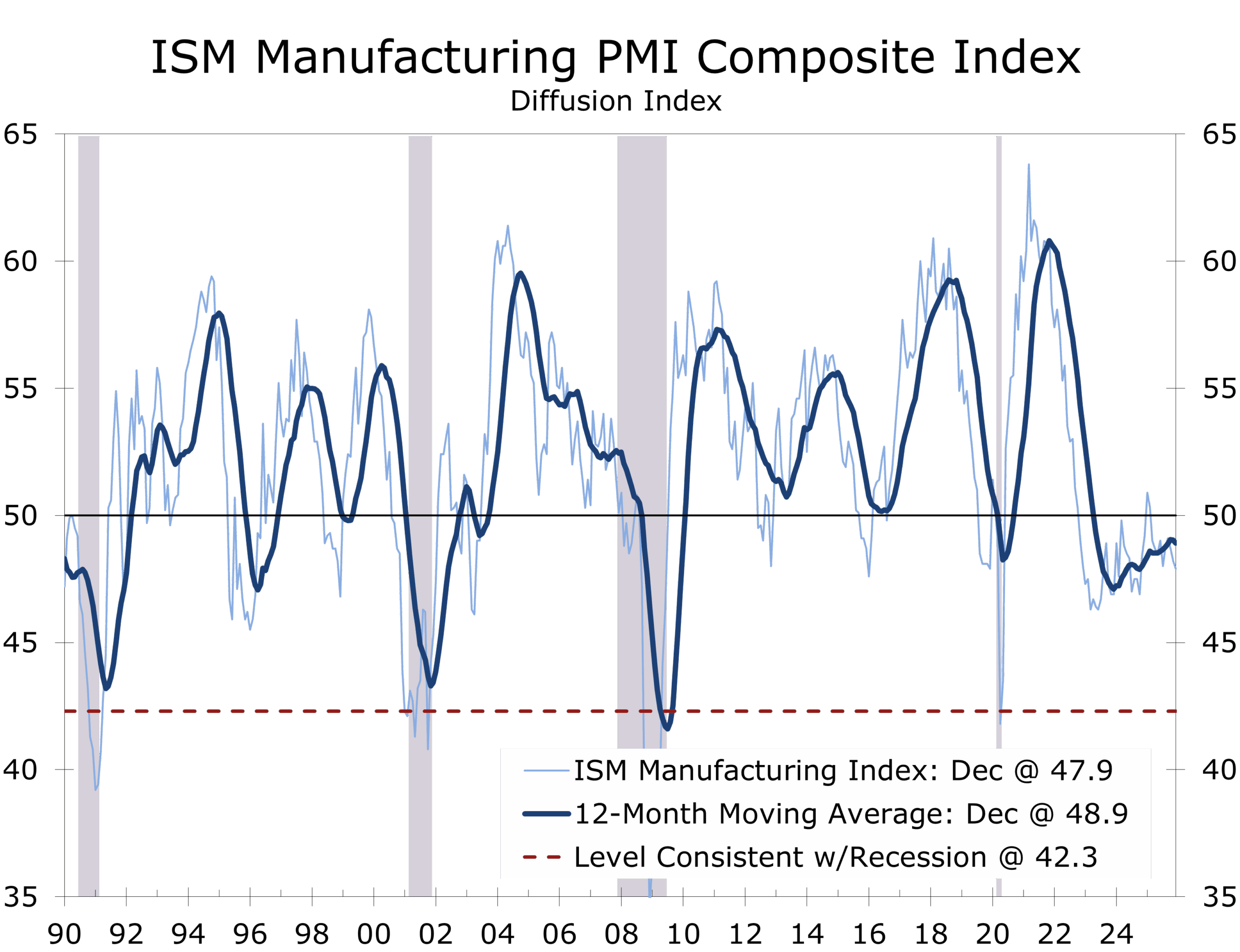

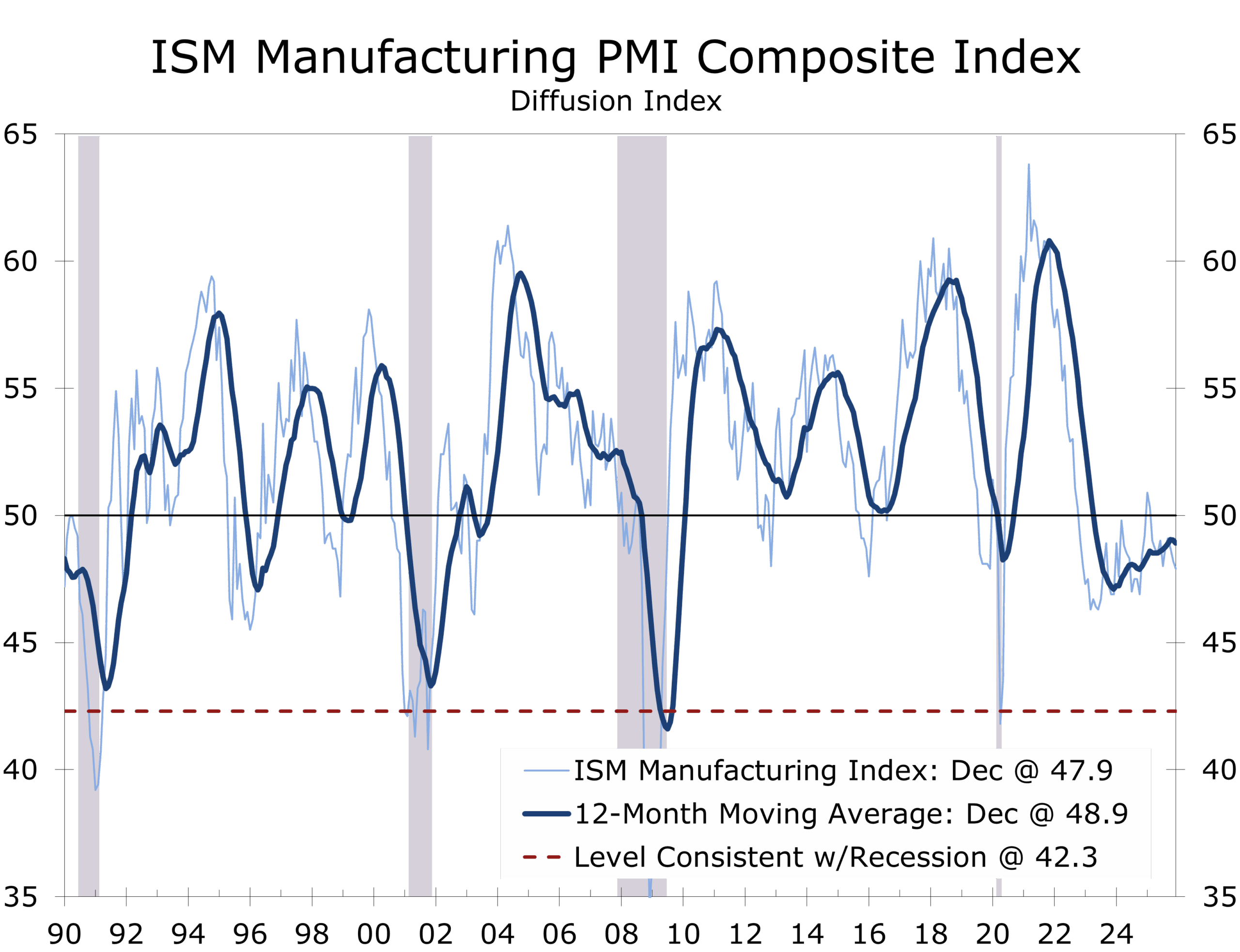

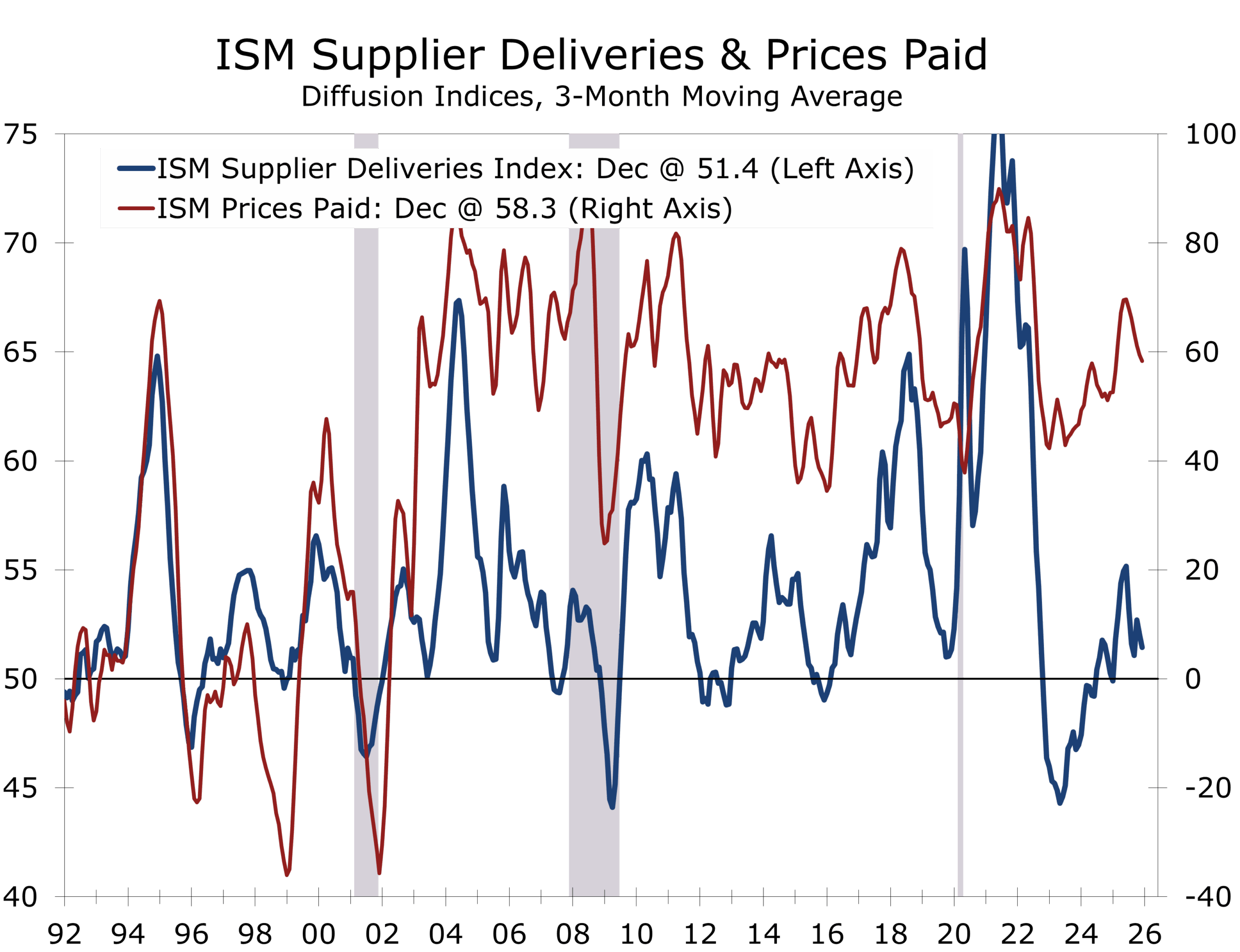

Manufacturing ended 2025 on a softer note. ISM Manufacturing fell to 47.9 in December, pushing further into contraction and underscoring how sensitive the sector remains to policy uncertainty and uneven global demand. But the weakness is not uniform. Manufacturing is increasingly bifurcated.

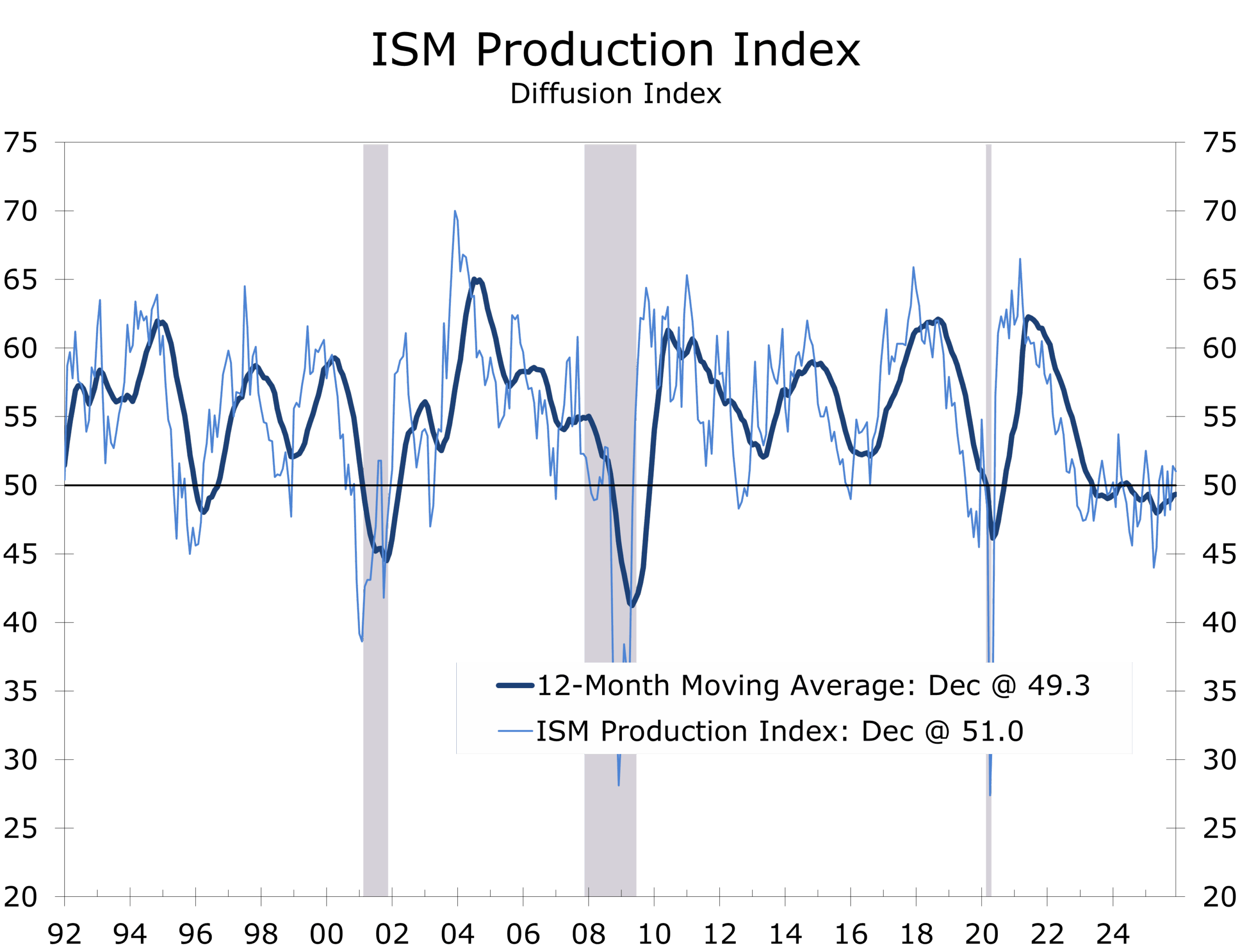

Output of consumer goods rose just 1.4% year over year, while output of business equipment surged 12.5%. That strength is narrowly concentrated in capital-intensive segments—aerospace and miscellaneous transportation equipment, including shipbuilding, where output jumped 25.2%, and semiconductors and related components, up 16.5%. Even within nondurables, pharmaceutical and medicine production stands out, rising roughly 6–7% over the past year.

The signal from industrial production is clear: this is not a consumer-led manufacturing cycle. It is a capital-, defense-, technology-, and innovation-driven expansion operating alongside a still-soft factory backdrop. Reshoring will become more evident during 2026, with pharmaceuticals and steel likely to be two of the earliest beneficiaries.

Manufacturing is contracting overall but expanding in capital-intensive segments.

Services, meanwhile, continue to do the heavy lifting. The Institute for Supply Management Services index climbed to 54.4 in December, signaling sustained momentum in business activity, new orders, and hiring. This is now the economy’s center of gravity. Large, scalable service platforms benefit from recurring demand, pricing power, and operating leverage. Unlike goods production, services are less constrained by inventories and more adaptable to shifts in labor and capital mix.

GDPNow, trade, and the arithmetic of growth

Atlanta Fed GDPNow remains eye-catching. As of January 9, the model was tracking Q4 real GDP growth above 5%, even after a modest pullback. The strength is not coming from housing or consumer excess. It is coming from trade arithmetic and capital spending.

October trade data showed a sharp narrowing of the trade deficit, driven largely by tariff-related timing effects. Pharmaceutical imports reversed abruptly after September front-loading, while capital goods imports surged, reflecting sustained spending on AI infrastructure, data centers, and high-tech equipment. Exports were also boosted by an unusual spike in gold shipments, which flatters the headline trade balance but contributes little to real GDP.

GDPNow captures the arithmetic of the moment; forecasting requires judgment about what lasts.

We adjusted our Q4 real GDP forecast modestly higher following the trade release, but not nearly to the levels implied by GDPNow. The model is deliberately mechanical. When net exports swing sharply and equipment spending remains firm, it upgrades growth aggressively, even if some of that strength is likely to reverse as gold flows normalize and import-timing effects fade. Our 2026 growth forecast remains above consensus, with risks currently skewed to the upside.

Labor market: slow lane, not pile-up

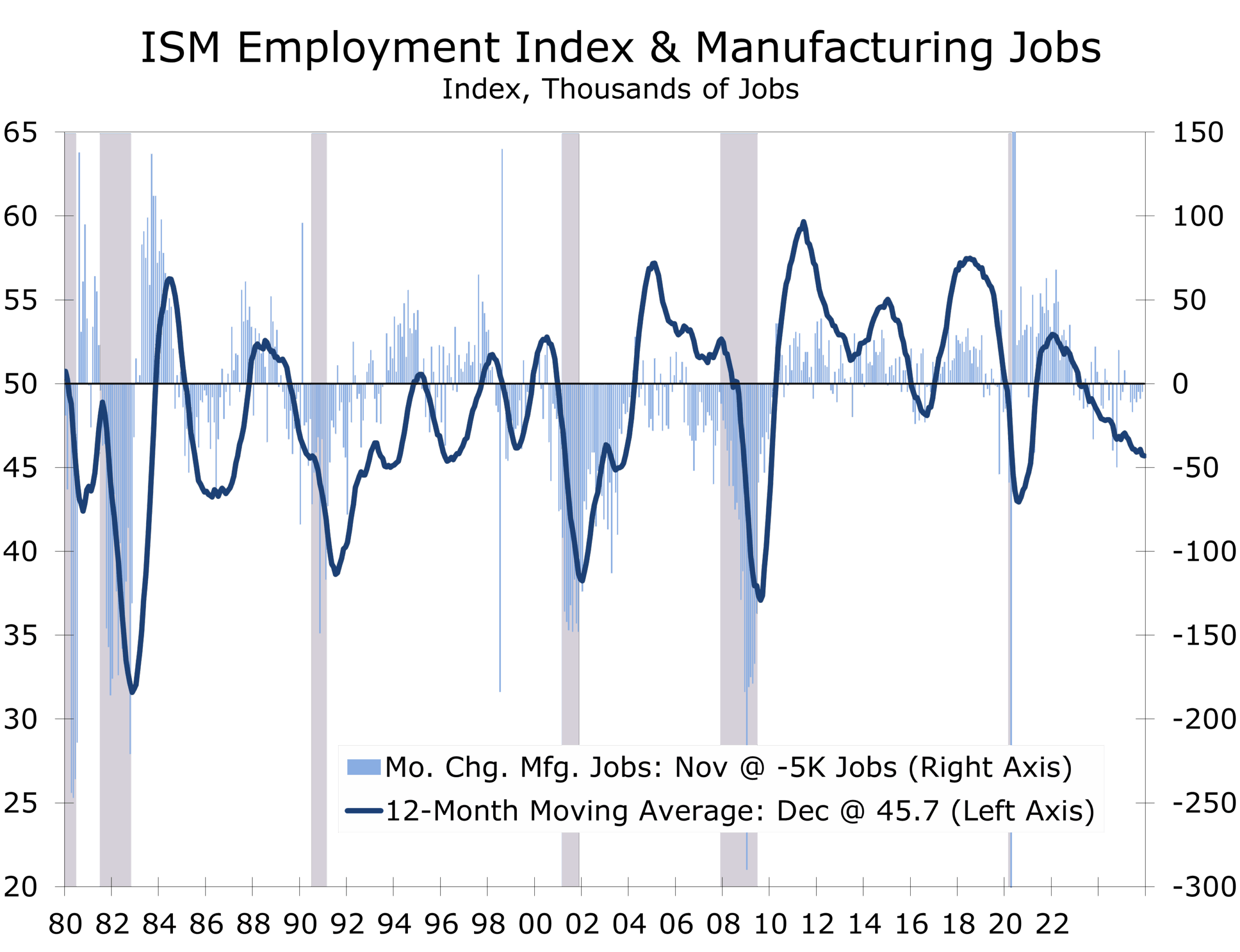

The December Employment Situation capped a notably slower hiring year. Payroll gains averaged roughly 49,000 per month in 2025, a sharp deceleration from prior years, with the unemployment rate ending the year at 4.4%. Wage growth cooled but did not collapse, with average hourly earnings running in the high-3% year-over-year range—firm enough to support consumer spending while remaining consistent with a disinflationary labor backdrop.

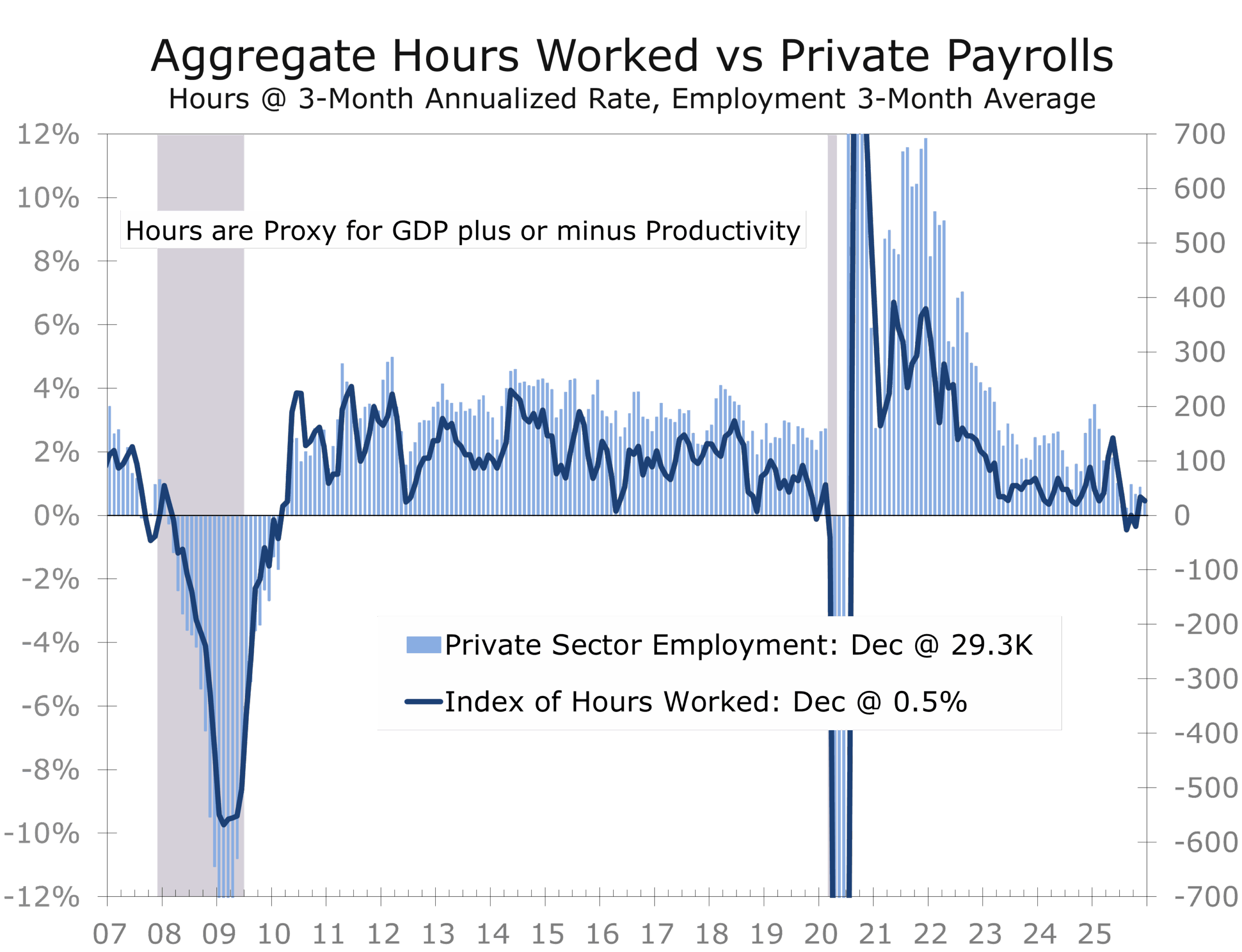

Hiring remains narrowly concentrated, with many cyclically sensitive industries showing little net change. Layoffs remain historically low, however, reinforcing the view that firms are reluctant to shed labor. Adjustment continues to occur primarily through hours rather than headcount, with aggregate hours worked declining modestly and underemployment edging higher at the margin. Productivity is doing more of the work. After a strong third quarter, nonfarm productivity remains up roughly 2% year over year, underscoring a meaningful improvement in output per worker even as hiring slows.

Slower hiring reflects higher productivity and tighter labor supply, not labor-market stress.

Quarterly productivity readings are inherently noisy. The more reliable signal comes from year-over-year trends and multi-year averages, which point to underlying productivity growth closer to 2%, with scope to rise toward 2½%–3% as capital deepening, AI adoption, and the buildout of digital infrastructure shift a larger share of growth toward capital rather than labor. At the same time, businesses are pruning lower-return activities, retaining higher-quality workers, and becoming more selective in hiring; reinforcing the productivity rebound.

This increasingly resembles a low-hire, low-fire equilibrium. Employers are cautious about adding workers but reluctant to cut existing staff. The implication is straightforward: labor costs are becoming more predictable, not more volatile, reducing downside risk to margins even as top-line growth moderates.

Rates, financial conditions, and policy risk

Markets have shifted toward a patient Fed narrative. Rate cuts remain priced for later in 2026 if inflation cooperates, but near-term urgency has faded. Financial conditions reinforce that view. Credit spreads remain contained, issuance has surged, and risk assets are not behaving as though policy is overly restrictive.

A new variable entered the equation this week: direct political pressure on Federal Reserve leadership. The Administration publicly accused Chair Powell of misconduct tied to his prior regulatory decisions and indicated support for potential legal action, an extraordinary step that reframes the policy outlook—not through inflation or employment, but through institutional credibility.

Central Bank independence is a policy tool. Undermining it raises the cost of easing.

Markets have largely discounted immediate consequences, assuming the Fed’s reaction function remains intact. That assumption appears reasonable. Inflation expectations remain well anchored, rate pricing has barely moved, and financial conditions show no signs of credibility shock. Policy is still being set inside the FOMC, not outside it.

History, however, offers an important guide. Episodes of political pressure on central banks rarely result in faster accommodation. More often, they produce the opposite outcome. When independence is questioned, policymakers tend to lean more heavily on process, caution, and institutional legitimacy. Powell’s response fits that pattern. His remarks were institutional, procedural, and deliberately defiant. He made clear that the Federal Reserve’s mandate, framework, and decision-making process remain unchanged. That message was not accidental. It was designed to reinforce credibility at a moment when it was being tested.

Threats to Fed independence rarely hasten easing. They usually reinforce caution.

The irony is that the macro backdrop would otherwise support patience. Growth remains solid, labor markets are cooling without distress, and funding conditions are accommodative. Political pressure risks turning what could have been a benign pause into a longer one, even if inflation continues to drift lower.

This episode is best viewed as a test of norms rather than a transfer of authority. The Federal Reserve’s independence ultimately rests not on rhetoric or statute alone, but on credibility and the willingness of its leadership to hold the line. On that front, Powell has been clear.

Equity and credit: funding windows reopened

Investment-grade credit markets opened the year with force. Roughly $95 billion in U.S. corporate bond issuance marked the busiest first full week since early 2020. This is classic January front-loading, amplified by strong demand and a desire to lock in funding early.

That behavior is inconsistent with a narrative of tightening liquidity. It suggests that access to capital remains available, terms are competitive, and balance-sheet strategies are being executed from a position of relative strength.

Equities have reflected a similar message: growth intact, wage pressure easing, and margins supported by productivity rather than labor expansion.

Geopolitics: risk premium, not shock yet

Venezuela was the headline shock. The U.S.-led capture of Nicolás Maduro sent a clear signal about hemispheric control, inviting comparisons to the 1989 intervention in Panama. Markets have so far treated the episode as a geopolitical risk premium rather than a systemic macro event, with oil prices and broader risk assets largely contained.

Russia intensified strikes on Ukrainian infrastructure during extreme cold, raising humanitarian and energy-system risks. Iran escalated rhetoric toward Israel and the United States, keeping the Middle East risk envelope wide, while renewed movement around Aleppo underscored Syria’s continued volatility. These developments reinforce a backdrop of persistent geopolitical tension without triggering outright disruption.

Geopolitical risk is being priced through volatility and term premia.

The timing matters. Geopolitical assertiveness abroad is coinciding with institutional tension at home, a combination markets typically price with a lag. After a strong start to the year, this raises the likelihood of intermittent volatility, making early-year issuance and proactive funding decisions look increasingly well timed.

Theme: geopolitics, pricing power, and term premia

The common thread across these developments is not immediate disruption but option value. Supply chains remain intact, yet redundancy, inventory buffers, and routing insurance continue to carry a cost. That dynamic keeps a floor under goods inflation even as headline pressures ease. In fixed income, the transmission runs less through near-term rate expectations and more through term premia, as investors demand compensation for geopolitical uncertainty, policy risk, and elevated fiscal supply. The result is a curve that resists flattening and volatility that reappears episodically rather than persistently.

The week ahead: data that can move the narrative

This week’s calendar is dense enough to stress-test the emerging patient-Fed consensus.

Tuesday: December CPI and the NFIB Small Business Optimism Survey. Inflation remains the gatekeeper, particularly core services and shelter. We expect a better-than-feared print, helped by softer grocery prices and easing rent pressure. NFIB sentiment will be closely watched for signs of stabilization.

Wednesday: Retail sales and existing home sales. Control-group sales will shape Q4 GDP tracking and early-year consumer momentum.

Thursday: The Empire State and Philadelphia Fed manufacturing surveys will provide early insight into how manufacturing entered 2026. The data have been volatile, but orders, shipments, and pricing matter more than the headlines.

Friday: Industrial production, capacity utilization, and the NAHB Housing Market Index will round out the week.

The Beige Book will be quietly influential throughout. Confirmation of a low-hire, low-fire labor market would reinforce patience into the spring. With Chair Powell under scrutiny, Fed communication will be parsed less for timing and more for institutional resolve.

Piedmont Perspective

Institutional Home Buying: Populism Meets the Balance Sheet

President Trump’s proposal to limit institutional purchases of single-family homes is best understood as a political signal rather than an economic lever. It speaks to real affordability frustration among younger households, but its economic impact is limited.

Institutional investors hold only 1–3% of single-family homes nationally and under 5% of single-family rentals. Where they matter is at the margin. Purchase flows can amplify price pressure in fast-growing metros during low-inventory periods, particularly in parts of the Sun Belt and Midwest.

Even there, institutions are not the root cause. The binding constraints are underbuilding, zoning restrictions, infrastructure costs, and in-migration. Since 2022, large institutional buyers have slowed acquisitions, shifted toward build-to-rent, and in some cases become net sellers. Restricting their participation risks slowing one of the few scalable sources of new housing supply without materially improving affordability.

Housing responds to capacity. Policies that expand it tend to work. Policies that constrain it tend to reshuffle ownership while leaving prices largely unchanged.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 12, 2026

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

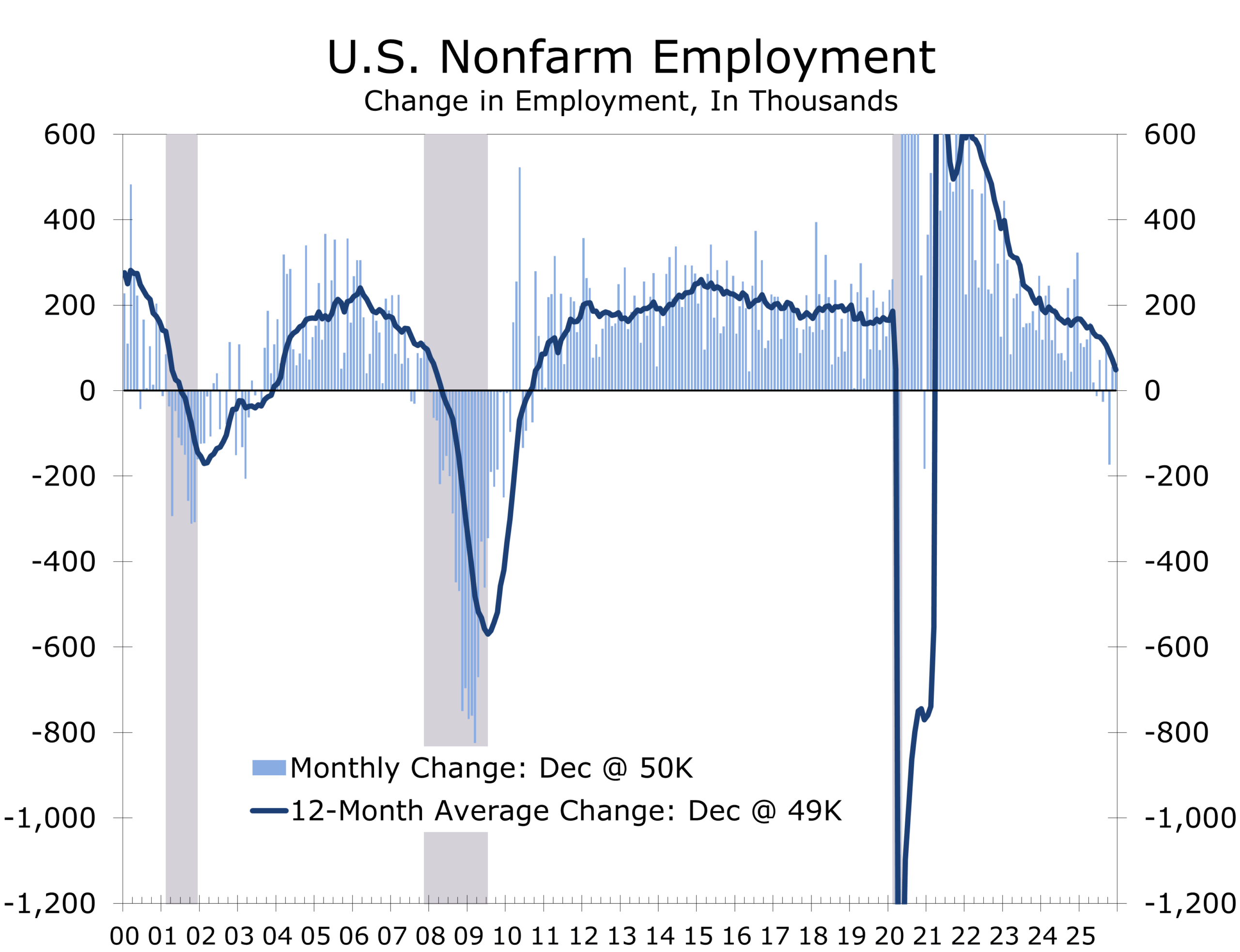

December Employment Report - December Jobs Data Reinforce a Mid-Cycle Rebalance

Cooling Without Cracking

-

- Payroll growth remains subdued. Nonfarm payrolls rose 50,000 in December, extending the stall-speed pace of job growth that has prevailed through much of the second half of 2025.

- Job gains remain narrowly concentrated in health care, social assistance, and food services. Most other major sectors showed little or no change.

- The unemployment rate held at 4.4%, unchanged on the month, but measures of labor underutilization continue to creep higher.

- Wage growth continues to cool. Average hourly earnings rose 0.3% in December and are up 3.8% year over year, consistent with a disinflationary labor market.

- Unemployment is drifting higher—but unevenly. The jobless rate rose to 4.6%, the highest since October 2021, driven largely by labor-force reentrants and concentrated among younger workers.

- Hours worked declined again. Firms continue to manage labor input through hours rather than headcount, a classic late-cycle adjustment.

- The December jobs report supports a policy pause: Federal job cuts and reduced hours mask private-sector resilience, while cooling wages and solid productivity argue for the Fed to hold rates steady in January rather than respond to labor-market stress.

Momentum Fades as Slack Continunes to Gradually Build

December’s employment report confirms that the U.S. labor market is no longer tightening and is instead operating in a lower-growth, mid-cycle equilibrium. Payroll gains of 50,000 were modest, and downward revisions to October and November subtracted a combined 76,000 jobs, reinforcing the view that underlying momentum has been softer than initially reported.

Employers added just 584,000 net new jobs in 2025, a sharp deceleration from the 2.0 million job gain in 2024. Hiring is no longer keeping pace with prior expansionary norms, but neither is it collapsing. This is an economy cooling without breaking.

Job growth has slowed to a pace that barely offsets labor-force growth.

Job Growth Barely Offsets Labor Force Expansion

The unemployment rate remained at 4.4%, with 7.5 million unemployed, little changed on the month. The labor force participation (62.4%) and the employment-population rate (59.7%) were also stable, suggesting that headline labor market conditions remain resilient amidst a lingering hiring slowdown.

Beneath the surface, however, slack continues to accumulate. Long-term unemployment rose to 1.9 million, accounting for 26% of all unemployed, and is up nearly 400,000 over the year. This reflects a labor market where re-employment is becoming more difficult at the margin.

At the same time, part-time employment for economic reasons climbed to 5.3 million, nearly 1 million higher than a year ago, indicating that firms are increasingly trimming hours rather than payrolls.

Underemployment is rising even as the headline unemployment rate remains stable.

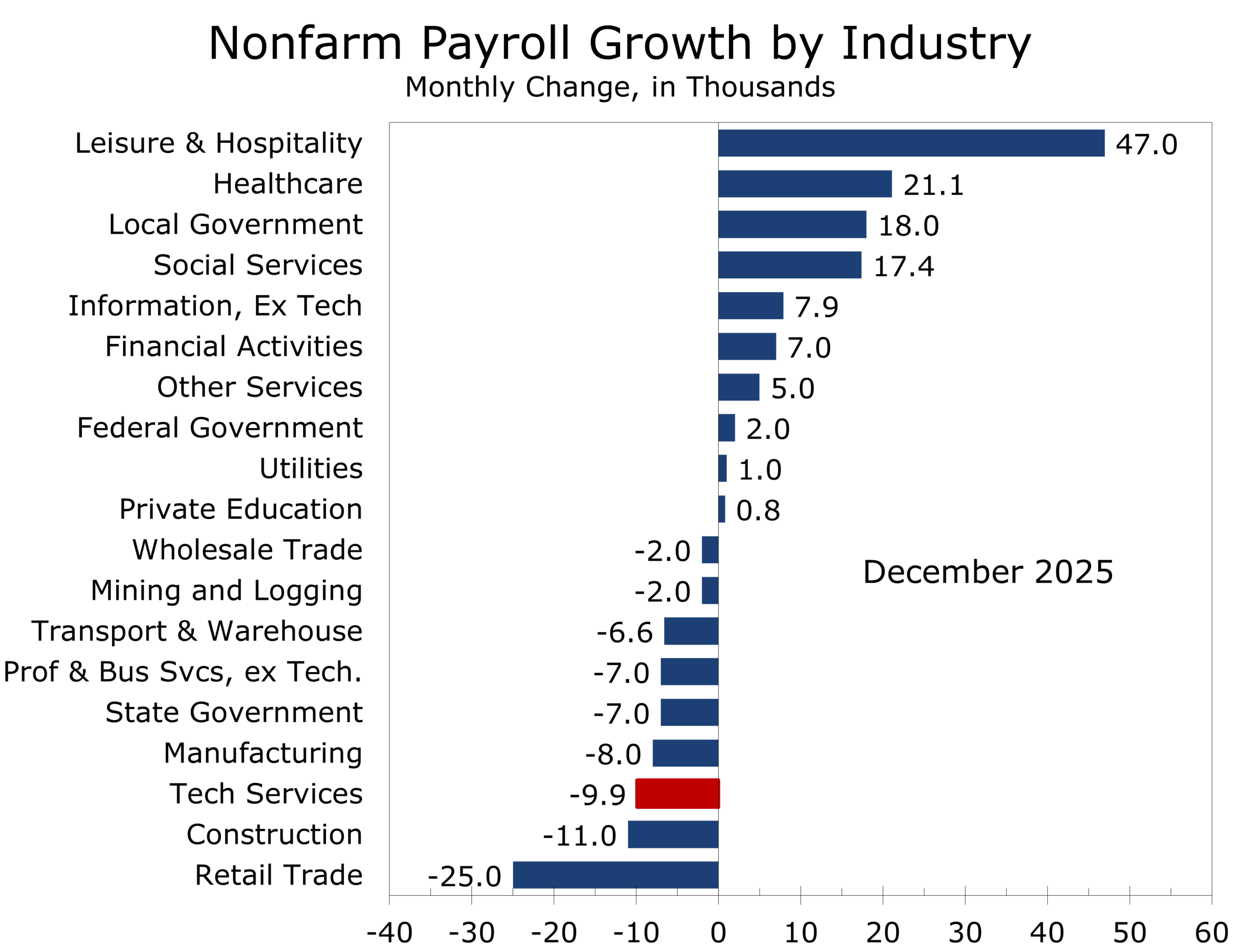

Hiring Remains Narrow and Service-Sector Heavy

Sectoral detail underscores the late-cycle character of the labor market. Food services and drinking places added 27,000 jobs. Health care employment rose by 21,000, led by hospitals. Social assistance increased by 17,000, primarily in individual and family services. These categories account for virtually all net job creation in December.

Elsewhere, hiring stalled. Manufacturing, construction, professional and business services, financial activities, information, wholesale trade, and transportation and warehousing all showed little or no change. Hiring within the tech sector is a notable soft spot, with tech employers cutting 9,900 jobs in December and 61,000 jobs over the past 12 months.

Retail trade lost 25,000 jobs, concentrated in general merchandise and grocery stores. This appears structural rather than cyclical, reflecting productivity gains, automation, and ongoing shifts in retail formats rather than a sudden pullback in consumer demand. The drop was also exaggerated by seasonal factors.

Federal government employment was little changed in December but remains a significant drag. Since peaking in January, federal payrolls are down 277,000 jobs, or 9.2%, reflecting post-pandemic normalization and DOGE-related retirements. These cuts continue to distort headline payroll growth and mask modest private-sector resilience.

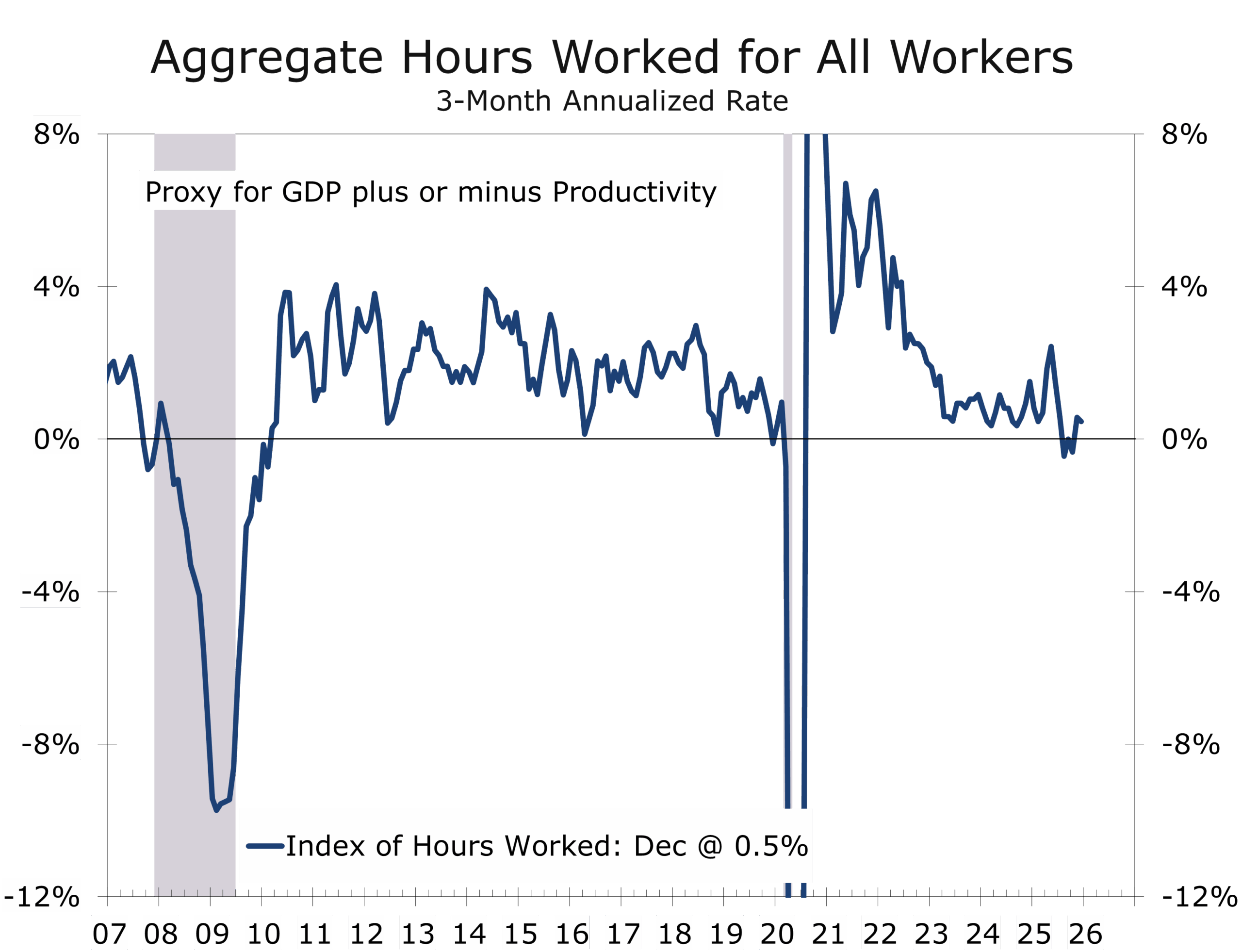

Average hourly earnings rose 0.3% in December and are up 3.8% year over year, a pace consistent with the Federal Reserve’s inflation objective when paired with productivity growth. The average workweek edged down to 34.2 hours, while the manufacturing workweek slipped to 39.9 hours. Overtime hours were unchanged, and aggregate hours worked fell 0.3% in December and rose at just a 0.5% annualized pace in the fourth quarter.

The adjustment continues to occur through hours rather than headcount, signaling caution without distress. Productivity remains sufficient to support real GDP growth near 2.5% in the fourth quarter.

This is not a collapsing labor market. It is a rebalancing one. Hiring has slowed materially, wage growth is cooling, and underutilization is rising at the margins. Yet layoffs remain contained, participation is stable, and service-sector demand continues to absorb labor.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 9, 2026

Mark Vitner, Chief Economist

(704) 458-4000

A Capital-Led Expansion, a Tech-Driven Cycle, and Why Charlotte Stands Out in 2026

Capital Carries the Cycle

- The U.S. economy is slowing, not sliding into recession. Growth is decelerating as hiring cools and consumers become more selective, but underlying demand remains intact.

- The expansion is being carried by capital, not consumption. Private fixed investment in AI infrastructure, power, advanced manufacturing, aerospace and defense, and life sciences remains the primary growth engine.

- Productivity is rising as payroll growth fades. Firms are producing more with fewer workers, signaling a job-light, capital-intensive phase rather than cyclical retrenchment.

- Policy uncertainty is raising the bar, not stopping investment. Capital is still being deployed, but with greater emphasis on scale, execution, and long-term returns.

- Charlotte is positioned to outperform. Its financial services depth, energy and infrastructure advantages, logistics connectivity, and expanding technology ecosystem align well with a capital-heavy, productivity-driven cycle.

A Productivity-Led Expansion

As the U.S. economy enters 2026, growth is cooling but not cracking. The December CAVU Compass captures this phase well: an economy pulling in different directions, with consumer spending becoming more selective, hiring slowing sharply, and policy uncertainty remaining elevated. Beneath those surface frictions, capital spending continues to anchor the expansion. For technology companies, that distinction matters. This is not a demand-driven slowdown. It is a transition toward a more capital-intensive, productivity-led cycle.

This is not a demand problem; it is a productivity shift. The economy is producing more with fewer new workers.

The backbone of the cycle remains private fixed investment. AI infrastructure, power and energy systems, aerospace and defense, biopharma, and advanced manufacturing continue to attract capital at scale. These are not short-cycle bets tied to consumer sentiment; they are long-duration investments driven by returns, resilience, and geopolitical recalibration. Arguments that growth would falter “without AI” miss the point. Capital would still flow to its highest risk-adjusted return. AI is simply where capital is flowing today, as expected risk-adjusted returns remain unusually attractive and AI use shifts from experimental to everyday applications.

Inflation dynamics reinforce this constructive backdrop. Tariffs briefly interrupted the disinflation trend in 2025, but their inflationary impulse has largely passed. More importantly, shelter inflation—which accounts for roughly 44% of core CPI—is now decelerating as home prices flatten and rental supply rises. Our 2026 forecast calls for shelter CPI inflation to slow to 3% or less, pulling core inflation back under 2.5% by year-end. For technology firms, this matters less for headline inflation and more for margin stability and planning certainty.

Labor-market dynamics further underscore the shift underway. Early 2026 is shaping up as a near-jobless expansion, with payroll growth hovering near zero before improving later in the year. Demographics, tighter immigration enforcement, and slower labor-force growth are restraining hiring even as output holds up. Employers are not aggressively cutting staff, but they are increasingly reluctant to add headcount. This divergence is not a warning sign; it is a signal. Demand for automation, AI orchestration, workflow optimization, and data-driven productivity tools tends to rise precisely in this environment.

Businesses are increasingly worried about being left behind as competitors implement AI more effectively.

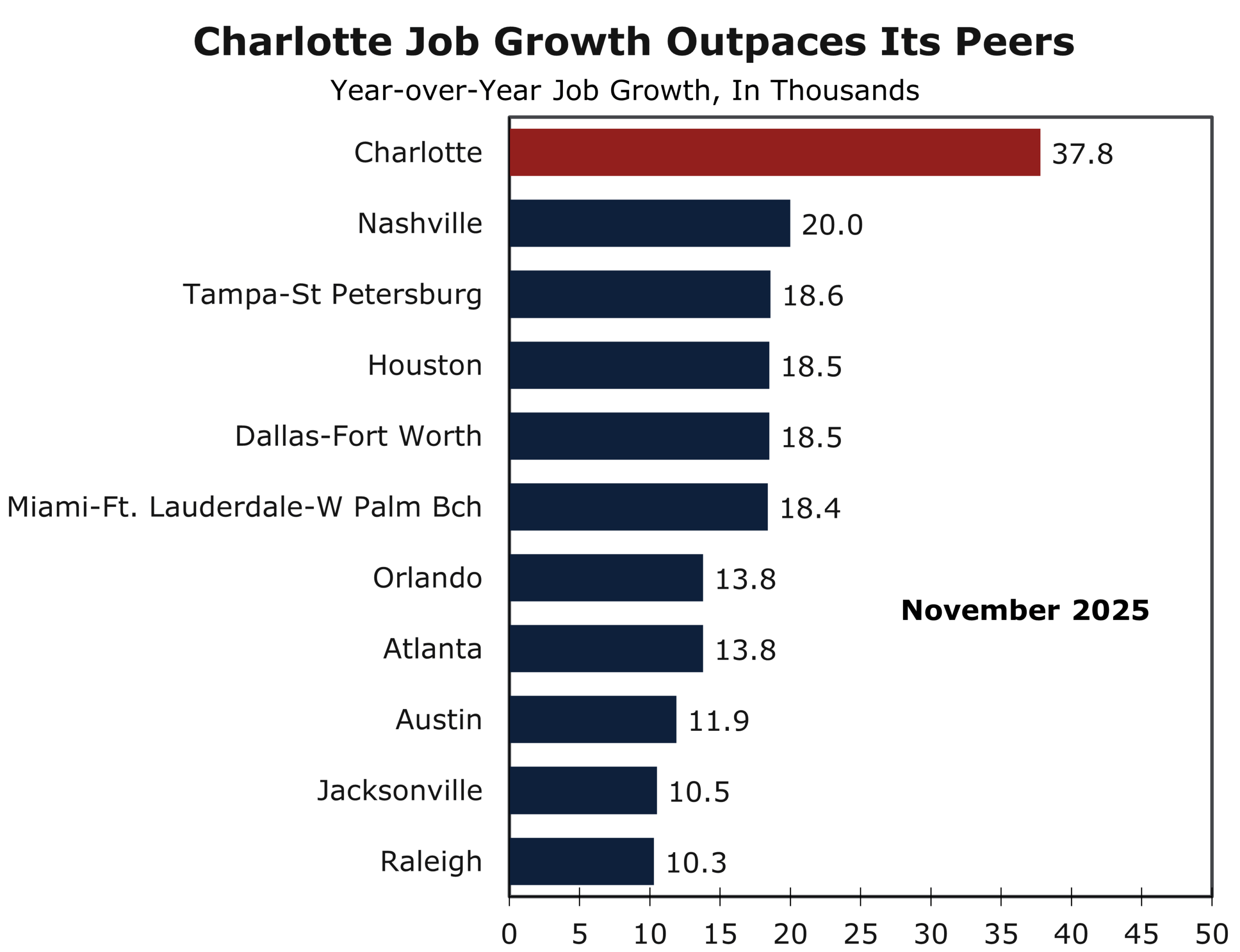

Regional divergence is widening as these forces play out, and this is where Charlotte clearly separates from many of its peers. While job growth has slowed in metros such as Raleigh, Nashville, Tampa, and Austin, hiring accelerated in Charlotte over the past year. Nonfarm employment in the Charlotte metro area increased 2.7% over the past 12 months, as employers added nearly 37,800 net new jobs. That performance places Charlotte among the fastest-growing large MSAs in the country, even as national hiring momentum cools. Net job creation also surpassed that of larger peer metros such as Atlanta, Dallas-Ft Worth, and Miami–Fort Lauderdale–West Palm Beach.

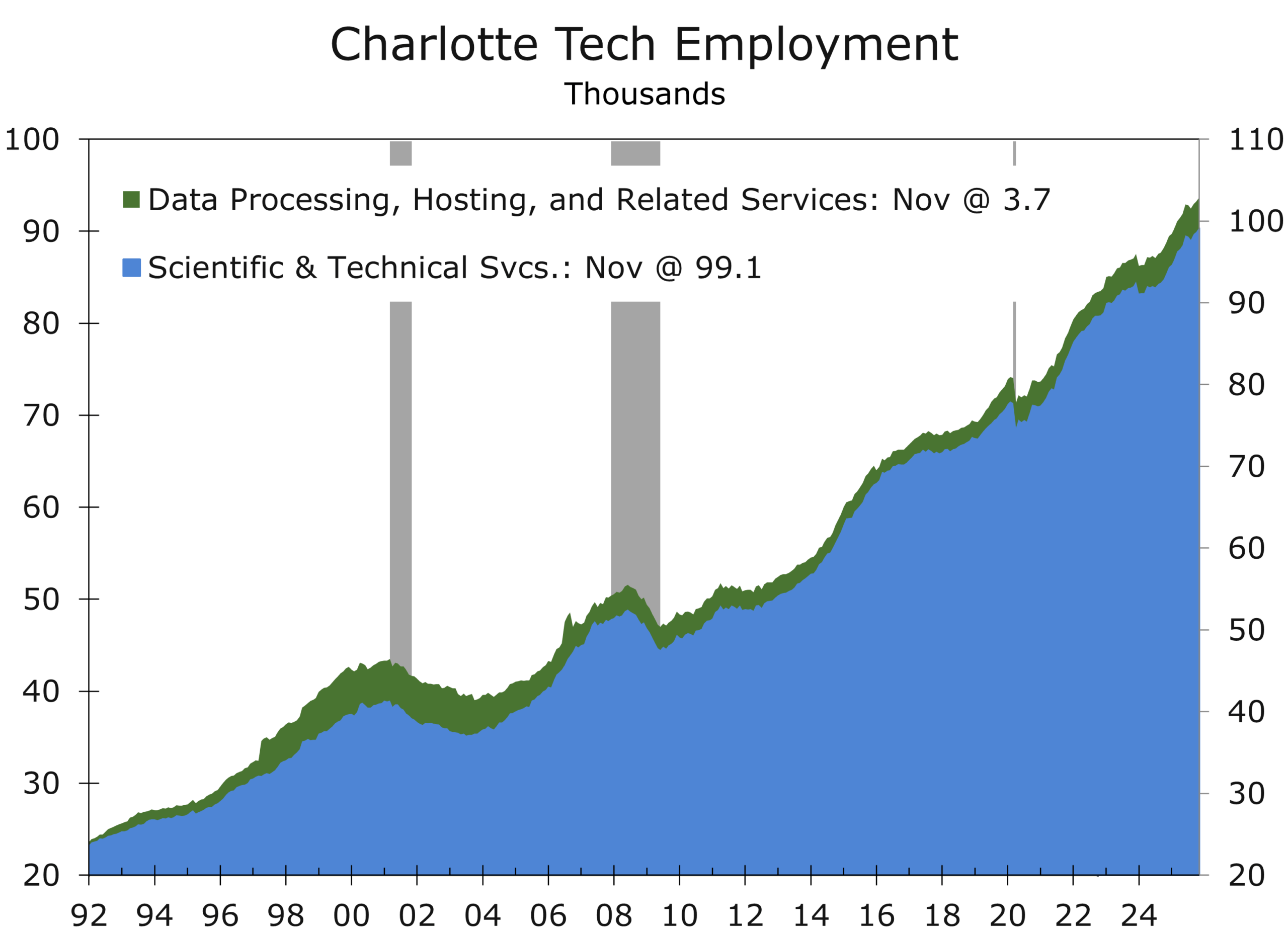

Charlotte’s strength reflects more than favorable timing. The region sits at the intersection of financial services, technology, healthcare, and logistics, supported by sustained population growth and rising capital inflows. Tech and healthcare hiring remain notable bright spots, while investments such as the Wake Forest School of Medicine; and more broadly, The Pearl innovation district, promise to further diversify the region’s economic base. Charlotte also continues to attract corporate and regional headquarters and scored a notable win by landing the new headquarters for Scout Motors. Unlike markets now confronting affordability ceilings and slowing migration, Charlotte continues to benefit from attainable housing, execution speed, and a growing talent pool.

Charlotte is accelerating while many peer tech metros are decelerating. Capital, people, and jobs continue to gravitate toward Charlotte.

While this report draws from discussions with leaders from Charlotte-area technology firms, its conclusions extend well beyond the tech sector. This is not a cycle defined by rapid hiring or outsized top-line growth; it is a capability cycle. Advantages will accrue to organizations that align with capital spending, invest in productivity-enhancing technologies, and operate in regions with durable execution capacity, such as Charlotte. If 2025 was the year the economy cooled without breaking, 2026 is shaping up to deliver growth with fewer workers, more capital, and increasingly calibrated policy. In that environment, discipline, scale, and execution will matter more than speed.

For Charlotte’s tech sector, 2026 is shaping up as a year of opportunity. Firms are accelerating the adoption of AI and automation to boost efficiency, while the sector continues to broaden beyond its historic dependence on the region’s large financial base. Healthcare, life sciences, and MedTech are emerging as particularly strong growth areas. Logistics, long weighed down by a protracted freight recession, is also positioned for a rebound, while financial services and FinTech stand to benefit from lower interest rates and an improving environment for lending and deal flow.

The broader economic outlook remains constructive. While job growth is likely to cool from the pace implied by preliminary data, the Charlotte region is still positioned to outperform the nation and most peer metros. The city’s core advantages remain firmly in place: a diversified economy, a high quality of life, and a well-located major airport hub that consistently ranks as one of the busiest in the world. Population growth continues to be fueled by domestic migration, led by inflows from the Northeast and Midwest, with rising contributions from other Southeast states—particularly Florida—as well as the West Coast. Charlotte also continues to rank among the top U.S. metros for attracting corporate and regional headquarters, reinforcing its long-term growth trajectory.

One of the questions we often get when speaking about the region’s economic performance is: Can this momentum continue, and what could trip Charlotte up? The answer to both is housing affordability. While home prices have risen in Charlotte, the region remains relatively affordable compared to its peers. As long as that remains true, the region’s competitive edge remains intact.

Charlotte is blessed with significant geographical advantages, including abundant land and water resources (including three lakes along the Catawba River). Most metro areas grow predominantly in one direction, typically to the north. In Charlotte, however, growth is roughly evenly split between the north and the south. Furthermore, the east (Cabarrus, Union, and Stanly counties) and west (Gaston and Lincoln) are currently the fastest-growing parts of the metro, benefiting from their own relative affordability.

A key reason these outlying areas remained accessible and affordable for so long is that Charlotte was one of the last major U.S. cities to complete a beltline expressway. The final leg of I-485 did not open until 2015, effectively “unlocking” vast tracts of land for development just as the national migration toward the Sun Belt accelerated. This delayed infrastructure has provided a critical safety valve for housing supply that many of Charlotte’s peers lack.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 9, 2026

Mark Vitner, Chief Economist

(704) 458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Cooling the Cycle, Clarifying the Signal

Highlights of the Week

- Venezuela stirred headlines and sentiment, but ample oil inventories and firm oil fundamentals kept energy prices contained, reinforcing confidence rather than caution.

- Oil and defense stocks rallied, reflecting the prospect of incremental gains to U.S. and Western oil firms, which alone have the expertise needed to boost Venezuelan production.

- Manufacturing is treading water. Production is edging forward modestly, while firms continue to trim labor and run unusually lean inventories as they wait for greater policy clarity.

- The quiet delay of furniture tariffs underscores a broader shift from tariff absolutism to tariff optionality. The switch is important for inflation dynamics, corporate margins, and Federal Reserve timing.

- Policymakers are threading a narrow path as growth stabilizes, inflation cools at the margin, and geopolitical risk rises without yet spilling meaningfully into the macro data.

- The week ahead is unlikely to alter the economy’s direction of travel, but it should clarify the story. Growth is decelerating toward trend, not stalling or rolling over.

Calibrated Power, Calibrated Policy

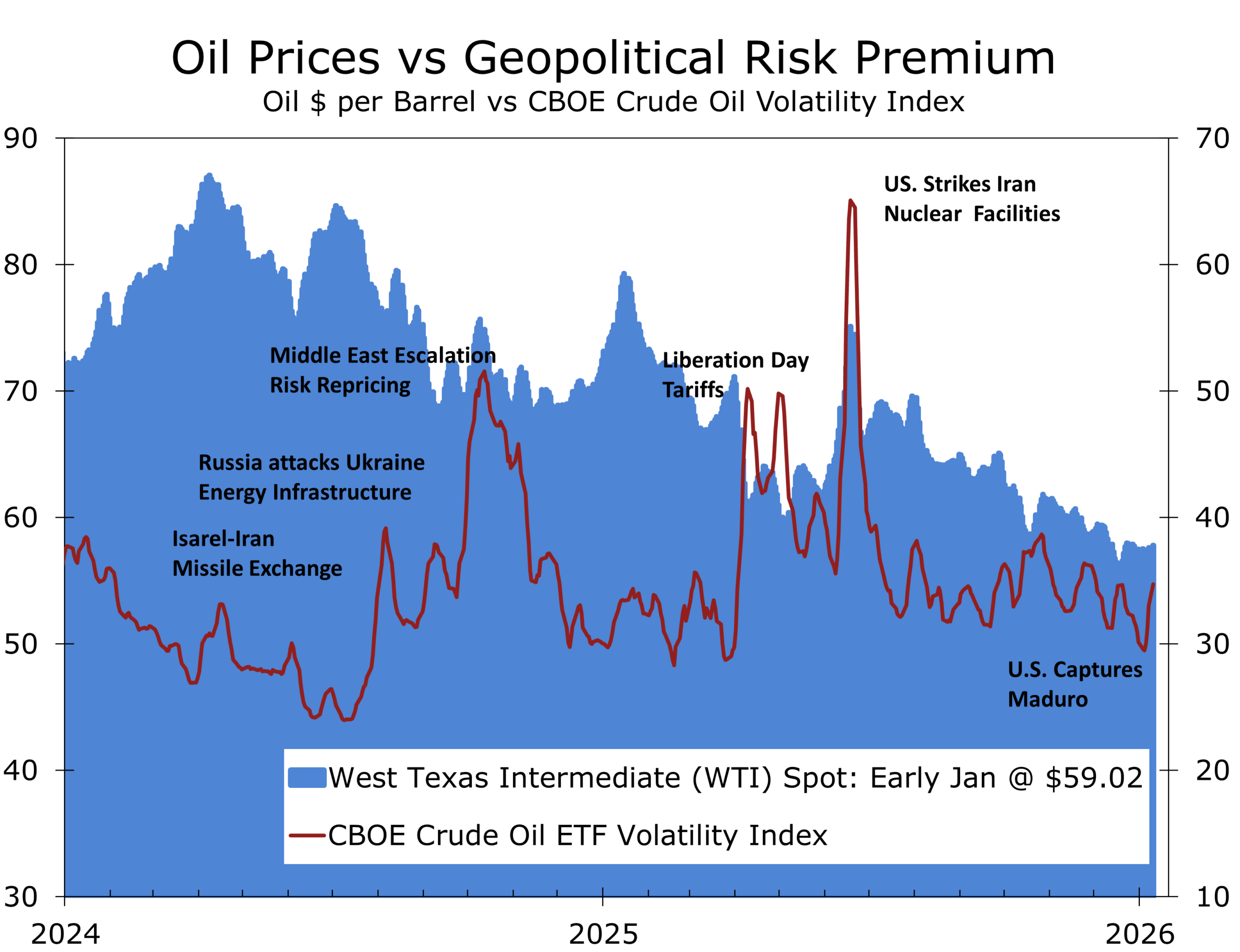

The first full trading week of 2026 offered a familiar lesson dressed in new clothes. Geopolitics can move markets, but fundamentals still write the longer chapters. The arrest of Venezuela’s Nicolás Maduro delivered an early risk-on jolt, pushing equities to record highs and briefly reviving talk of a supply-side oil shock. Yet crude prices barely flinched. Brent and WTI drifted lower, a reminder that global inventories, spare capacity, and demand elasticity still matter more than regime headlines. History rhymes here. Iraq in 2003 changed geopolitics overnight, but oil prices ultimately followed barrels, not banners.

Markets are rediscovering an old truth: geopolitics can move prices in the short run, but fundamentals will anchor them over time.

That same tension between narrative and reality showed up in Monday’s ISM Manufacturing report. The overall PMI fell 0.3 percentage points to 47.9 in December, marking the tenth consecutive month below the expansion threshold and the weakest reading of 2025.

Despite its long run in contraction territory, the weaker ISM index is not a signal of collapse. Instead, it is a picture of a factory sector treading water. Production is eking out modest gains, but manufacturers remain cautious—paring payrolls, preserving liquidity, and holding inventories at unusually lean levels. Capital spending continues, but selectively. Firms are not retreating so much as waiting.

What manufacturers are waiting for is clarity. Trade policy uncertainty and labor availability remain the binding constraints, not demand. On that front, the Trump Administration appears increasingly inclined to oblige. The policy posture emerging early in 2026 is consistent with our central calls for the year: that restoring affordability and momentum ahead of the midterm elections would require easing cost pressures rather than amplifying them. A lighter touch on tariffs and a more pragmatic approach to immigration both fit that playbook.

Manufacturing is not weak because demand has vanished, producers are overly cautious because policy clarity has.

Against that backdrop, trade policy delivered one of the more telling signals of the week. The decision to delay scheduled tariff increases on upholstered furniture, kitchen cabinets, and vanities into 2027 is small in headline terms but meaningful in context. This was not a rollback. Existing tariffs remain in place. But it was a clear acknowledgment of inflation sensitivity and political timing. Furniture is a highly visible, price-elastic category. Allowing tariffs to ratchet higher would have fed directly into consumer prices at a moment when policymakers are trying to declare progress.

Markets understood the message. Home goods and furniture stocks rallied as near-term margin risk eased, and retailers gained a rare commodity in today’s environment: cost visibility. More broadly, the move reinforces a quiet but important evolution in trade strategy. Tariffs are being treated less like permanent fortifications and more like negotiating instruments with built-in off-ramps. That flexibility lowers near-term inflation risk and supports risk assets, even as it raises longer-term planning uncertainty for global supply chains.

Policy restraint is quietly doing some of the Fed’s work for it.

For the Federal Reserve, this matters at the margin. Goods disinflation has been one of the more reliable allies in the fight against inflation. A tariff escalation would have complicated that story just as services inflation shows signs of grinding lower rather than falling cleanly. By delaying the tariff hike, policymakers effectively removed one potential source of renewed price pressure from the 2026 outlook. It does not force the Fed’s hand, but it narrows the set of upside inflation risks the Committee must weigh as it debates the timing and pace of eventual rate cuts.

More broadly, the move reinforces a quiet but important evolution in trade strategy. Tariffs are being treated less like permanent fortifications and more like negotiating instruments with built-in off-ramps. That flexibility lowers near-term inflation risk and supports risk assets, even as it raises longer-term planning uncertainty for global supply chains.

Policy restraint is quietly doing some of the Fed’s work for it, reinforcing the disinflationary trend.

For the Federal Reserve, this matters at the margin. Goods disinflation has been one of the more reliable allies in the fight against inflation. A tariff escalation would have complicated that story just as services inflation shows signs of grinding lower rather than falling cleanly. By delaying the tariff hike, policymakers effectively removed one potential source of renewed price pressure from the 2026 outlook. It does not force the Fed’s hand, but it narrows the set of upside inflation risks the Committee must weigh as it debates the timing and pace of eventual rate cuts.

Geopolitically, the landscape remains unsettled but contained. Venezuela’s future oil contribution is likely measured in quarters, not weeks, and depends on capital, infrastructure, and sanctions mechanics as much as politics. We expect a modest uptick in oil output this year, somewhere around 300,000 additional barrels per day. Gains beyond that will require significant investment and time. What markets seem to be underestimating is U.S. energy know-how, specifically related to Venezuelan crude.

Russia’s war in Ukraine continues to evolve tactically rather than strategically, while China’s tightening grip on dual-use exports to Japan underscores how economic statecraft is becoming more precise, more targeted, and harder to model. None of this has yet bled meaningfully into U.S. macro data, but it continues to shape the risk distribution around the outlook.

The still-growing protests in Iran hold the most promise for the next major geopolitical upheaval. Change may also come sooner than expected in Cuba, but talk about Greenland is most likely a distraction. Unless Greenland becomes a base for Chinese and Russian asymmetric attacks on the U.S., there is no reason for Denmark or other NATO nations to be concerned about an unwanted military takeover by the U.S. Remember that President Trump is always negotiating. The repeated heightened rhetoric on Greenland may be designed to secure a more favorable arrangement with Greenland, such as a lease deal or a mineral rights deal. The U.S. already has the right to operate military bases in Greenland.

Early 2026 is shaping up as a period of calibrated power and calibrated policy. Growth is slower but steadier. Inflation is easing, but has not been vanquished. Manufacturing is waiting, not failing. Tariffs are no longer blunt instruments, and geopolitics is loud without yet being inflationary. The margin for error is thinner than it looks—but the runway remains open, for now.

2026 Top Calls

- Manufacturing treads water, then stabilizes. Production growth remains modest, inventories stay lean, and labor trimming continues into midyear, but conditions improve as policy uncertainty fades.

- Tariffs become more flexible, not more forceful. Expect selective delays, exemptions, and enforcement discretion aimed at containing inflation and protecting politically sensitive consumer categories.

- Immigration pragmatism returns quietly. Incremental easing helps stabilize labor supply, lower service-sector cost pressures, and support affordability without reopening broader political fights.

- The Fed cuts later and by a little less than markets once expected. With goods disinflation intact and services inflation grinding lower, the Fed gains time rather than urgency.

- Geopolitical risk stays elevated but contained. Markets price uncertainty, not disruption, favoring resilience over recession trades.

For a deeper discussion of our macro framework and policy outlook, see the December edition of The CAVU Compass, where these themes were first laid out in detail.

The Piedmont Perspective

The removal of Nicolás Maduro is more than a regime change. It is a stress test of a gray-zone alliance built on opacity, grievance politics, and sanctions arbitrage. For more than a decade, Caracas served as the Western Hemisphere hub of a loose alignment linking Russia, China, Iran, and Cuba. The glue was not ideology but utility: Venezuela offered geography, oil optionality, and permissive terrain for sanctions evasion; its partners provided capital, weapons, intelligence cooperation, and diplomatic cover.