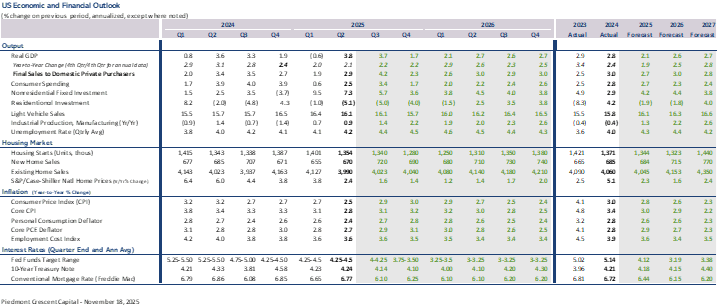

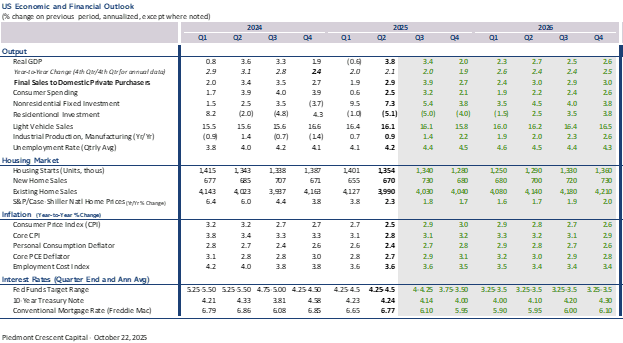

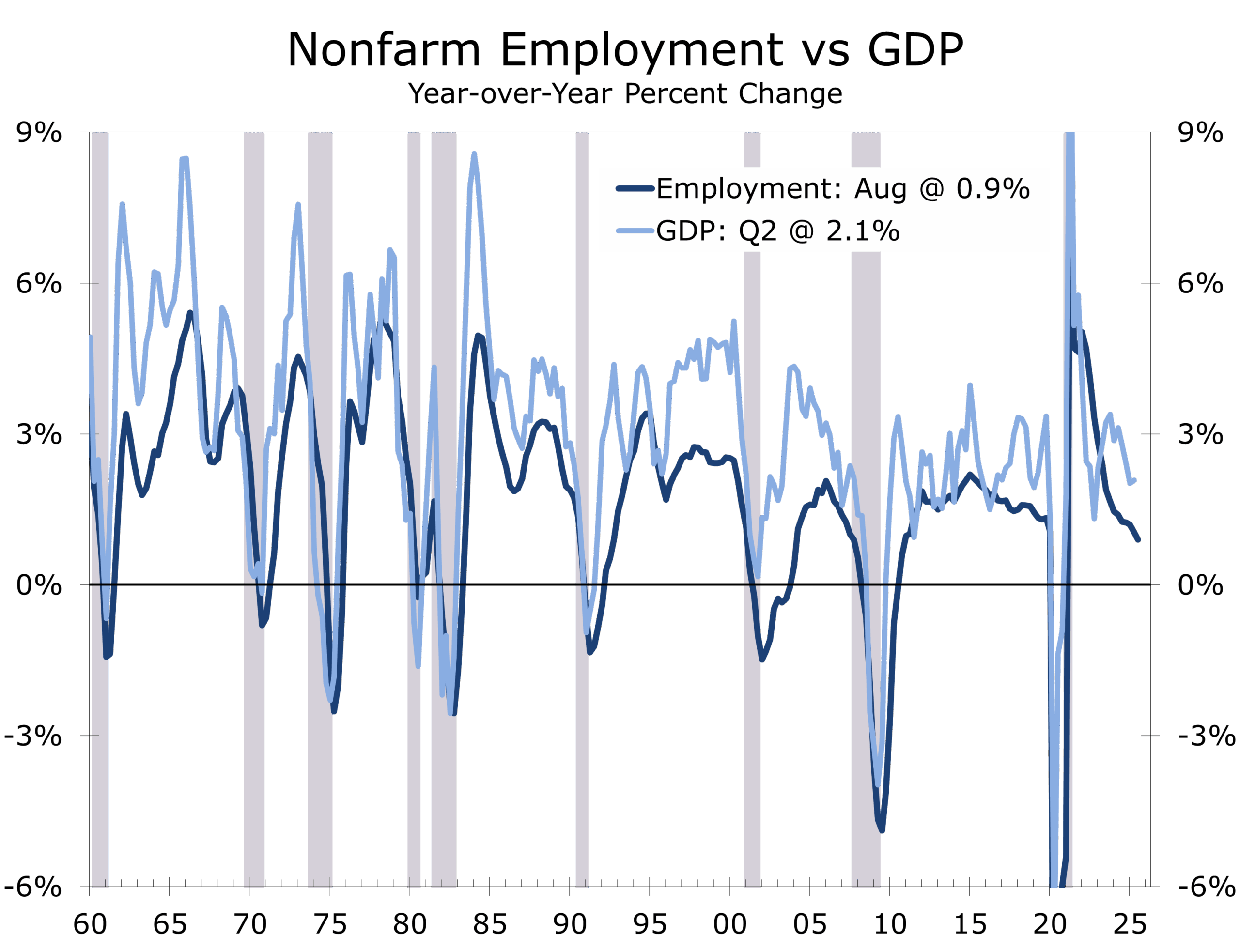

September Employment Report— A Labor Market Drifting Sideways

Recession Risks Have Eased, Yet Labor Market Momentum Continues to Fade

-

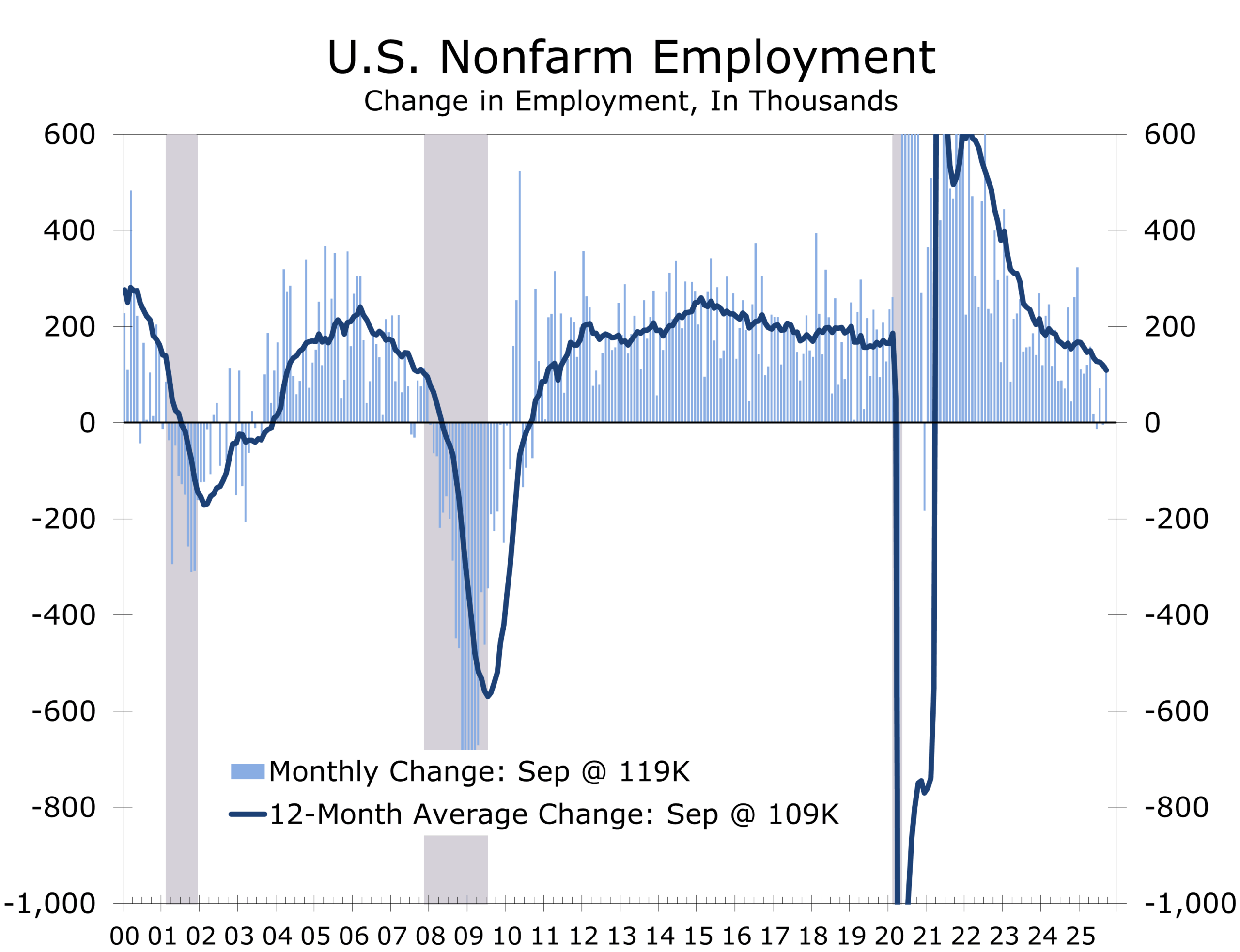

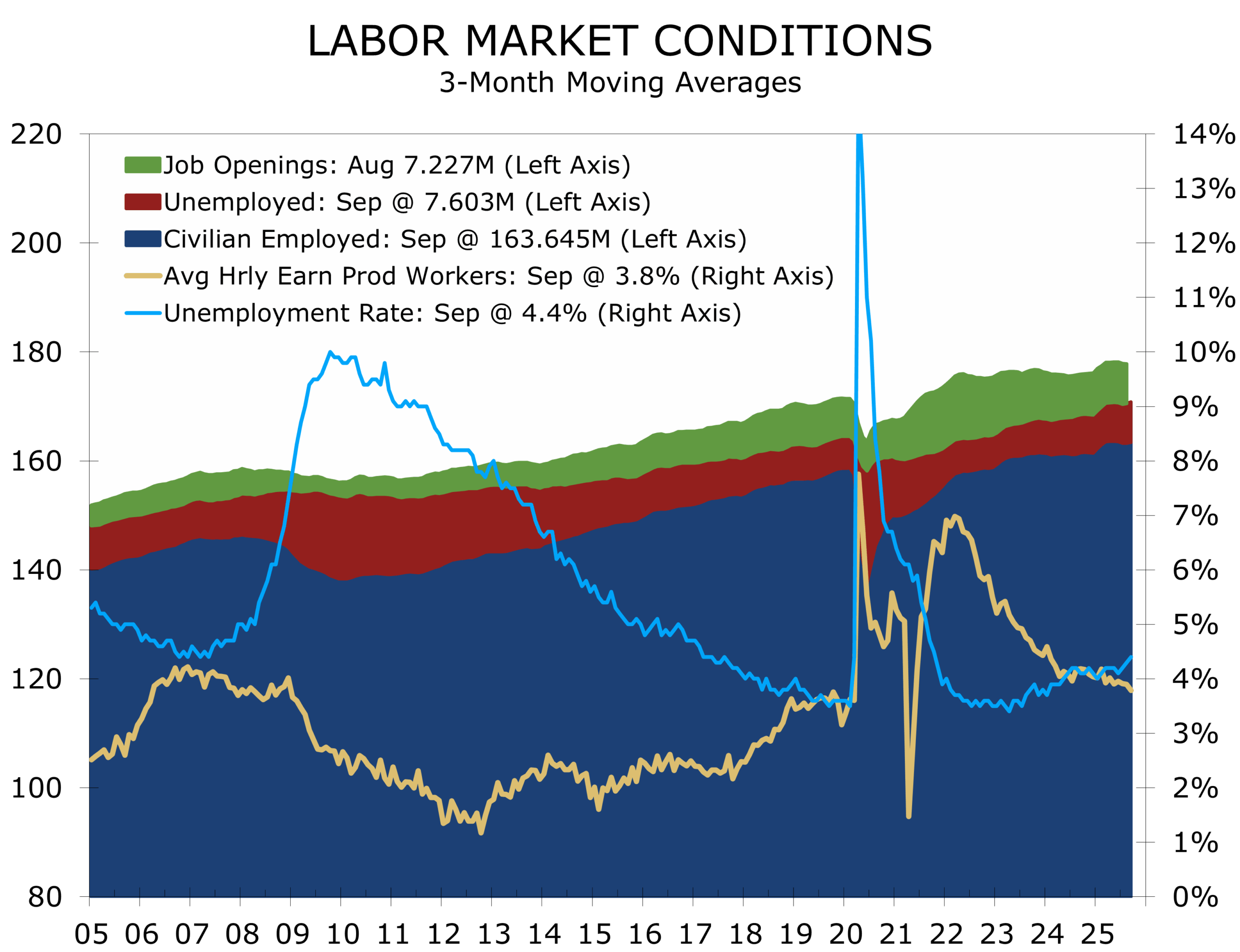

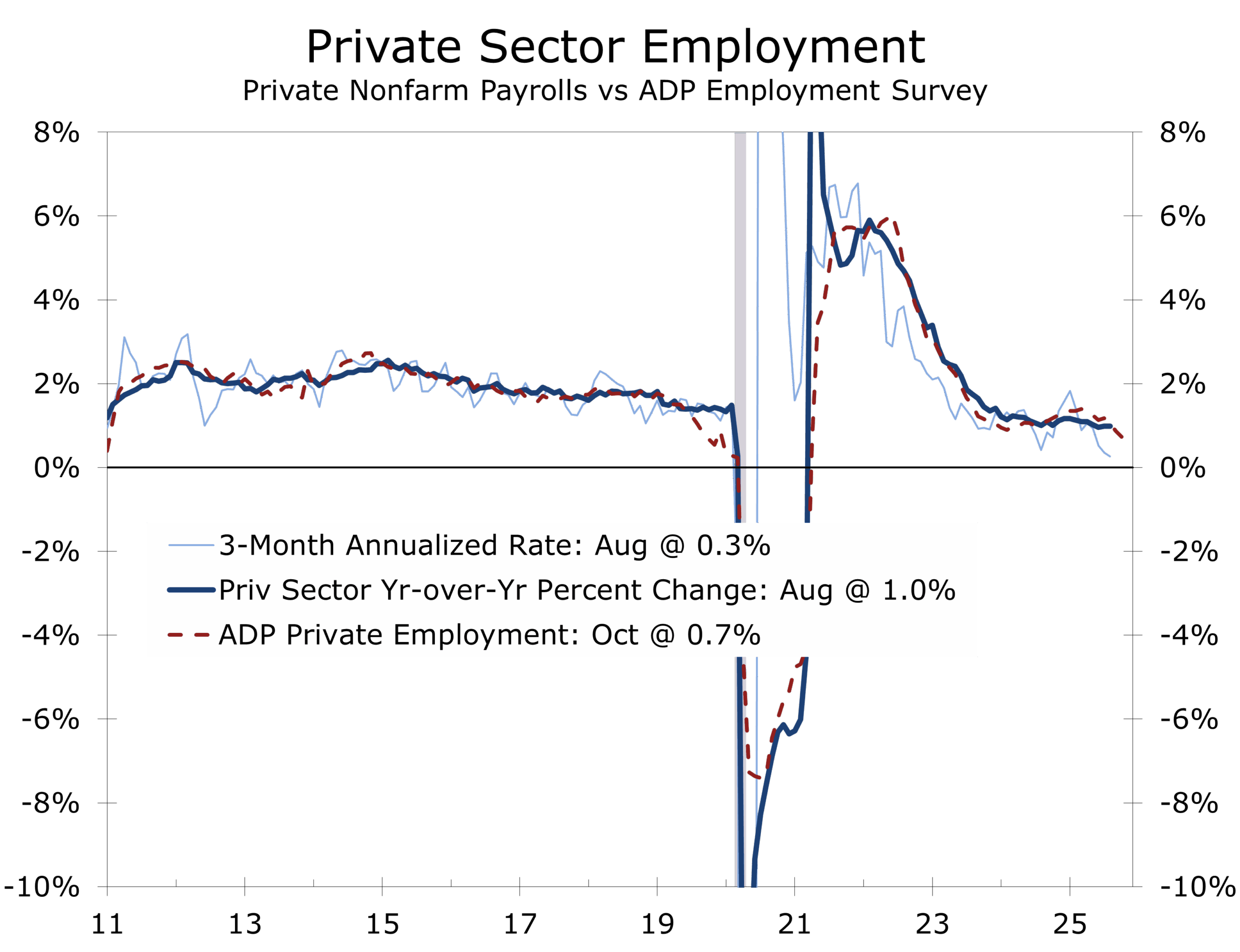

- Nonfarm payrolls rose 119,000 in September; the private sector added 97,000, easing some recession fears.

- Revisions lowered to the two prior months by 33,000; the three-month average improved to 62,000 but remains weak.

- The unemployment rate rose 0.1 pp to 4.4%, the highest since October 2021, with 7.6 million unemployed.

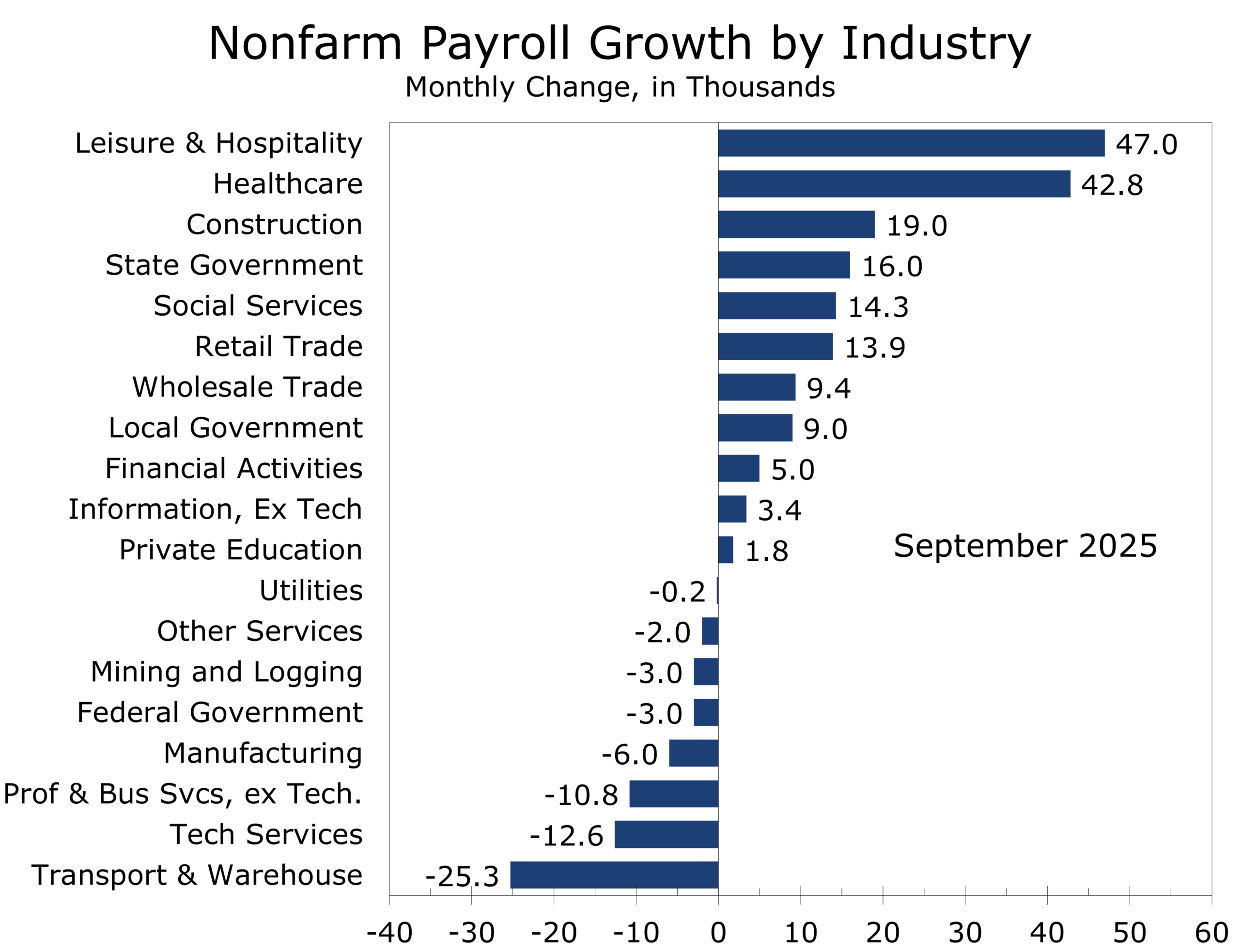

- Hiring remained concentrated in health care, restaurants, and social assistance.

- Wage growth slowed to 3.8% y/y, and hours worked remained flat.

- Rising permanent job losses, narrowing sectoral breadth, and weakening goods-producing momentum point to accumulating slack and diminishing inflationary tailwinds.

- The September employment report supports the case for further Fed easing, though the shutdown-delayed data release schedule complicates the timing. We continue to call for a quarter point cut, as we do not expect to see compelling evidence to suggest otherwise before the Fed meets on December 9-10.

A Labor Market That Stabilized in September—But on Unsteady Footing

September’s employment data delivered a welcome dose of stability at a moment when markets had begun to fear that the U.S. economy was sliding toward recession. Nonfarm payrolls rose 119,000, with the private sector adding 97,000 jobs — both comfortably above expectations and strong enough to reassure investors that the economy had not fallen off a cliff during the prolonged government shutdown. While the report is backward looking it is still reassuring. Employment conditions show no evidence of a pre-shutdown collapse and handily beat the market’s consensus estimates.

This modest strengthening followed another strong earnings report from Nvidia, which reinforced confidence in the AI investment cycle and eased doubts about the durability of the tech-driven productivity boom. Together, the labor data and renewed strength in AI provided just enough breathing room for markets rattled by the Liberation Day tariffs and rising global uncertainty.

Job growth has slowed to the bare minimum needed to keep unemployment from rising.

Yet beneath the steadier surface, the labor market remains fragile. Growth has slowed markedly since April, and the latest report does not change that overarching narrative. The three-month average for job gains improved to roughly 60,000, but that figure — even when adjusted upward — is barely above the job growth needed each month to keep the unemployment rate from rising . The upward bump is welcome but hardly convincing. Job growth has lost considerable momentum since the spring, and September represents stabilization, not a renewed acceleration.

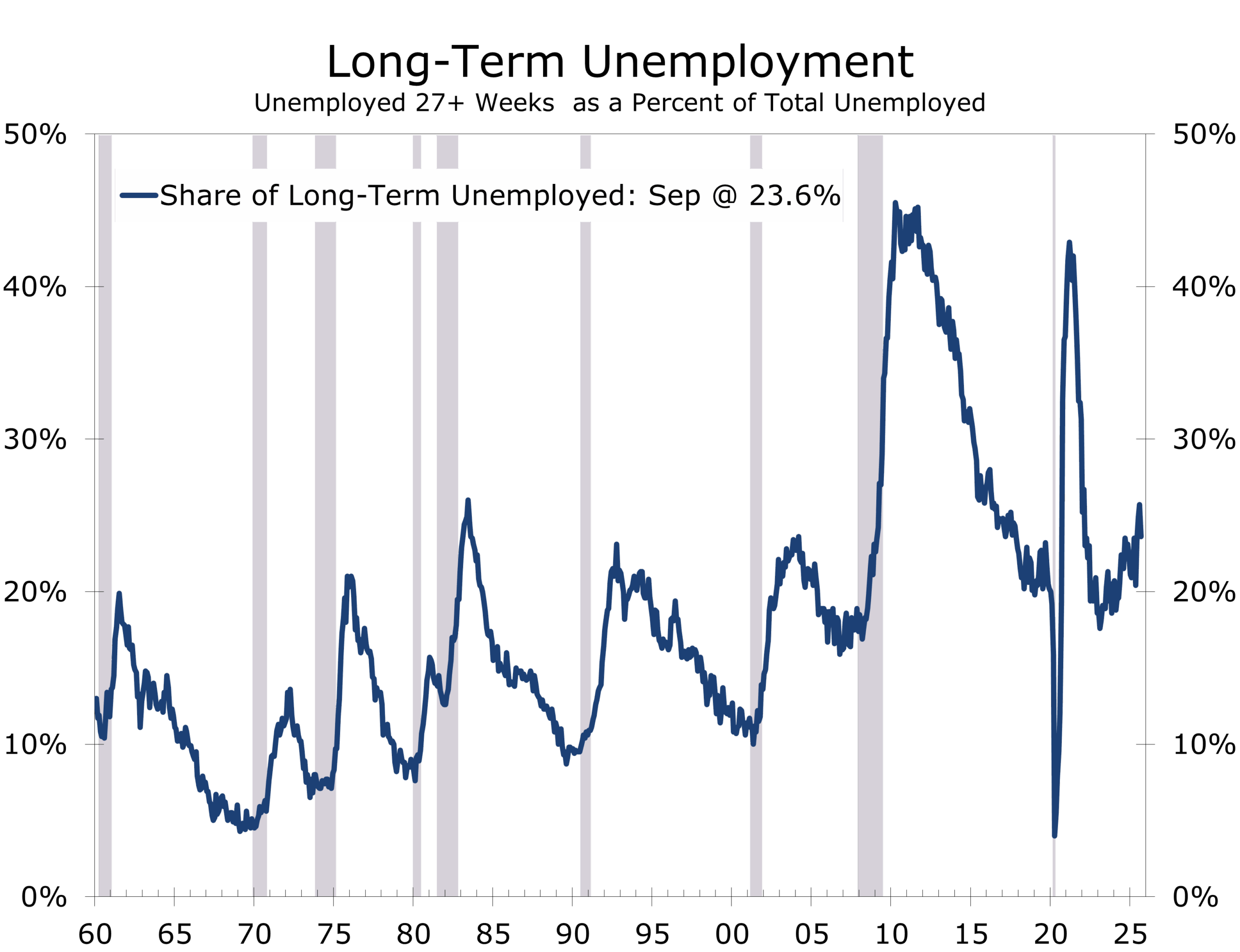

Revisions to July and August subtracted 33,000 jobs from the previous data, reminding us that the prior trend was weaker than first reported. And while the headline unemployment rate held at 4.4%, its highest since October 2021, the increase was driven partly by a surprisingly strong 470,000 jump in labor-force entrants. The influx is a sign that workers are reentering the job market rather than disengaging from it — a positive development. The household survey also showed rising permanent job losses, however, which climbed above 2 million for the first time since late 2021 — an unsettling development when hiring outside of a few industries remains sluggish. The trend has means a growing share of the unemployed have been without a job for 27 weeks or more.

Permanent job losses have quietly risen above 2 million — an early-cycle warning sign.

The shutdown itself added additional noise: the household survey was completed before the funding lapse, but establishment data were compiled using an unusually high 80% electronic reporting rate. October data will not be collected at all, and November will not be published until December 16. This complicates the Fed’s assessment at a critical moment.

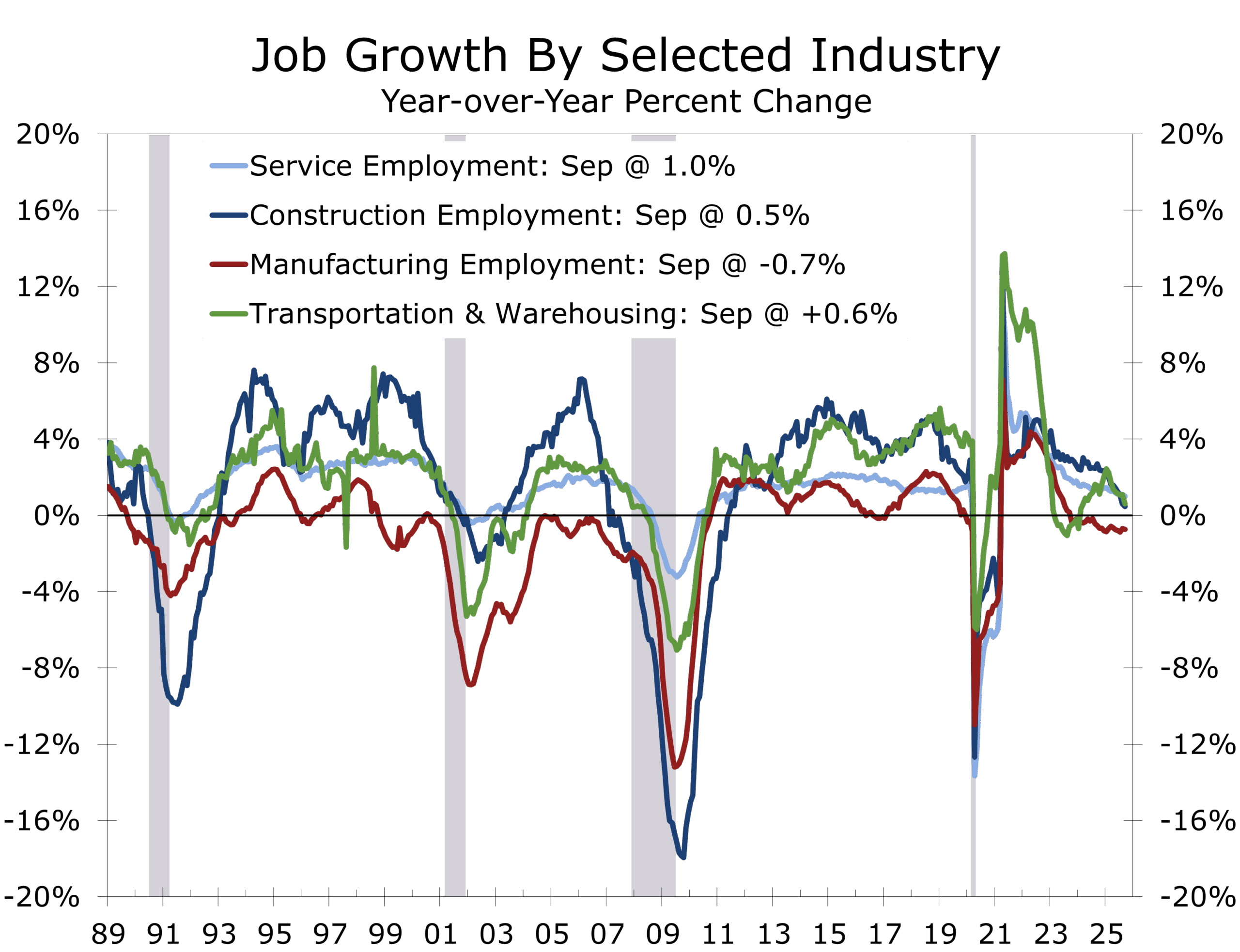

Growth Carried by Health Care, Hospitality, and Social Services

Where job growth did appear, it remained concentrated in a narrow slice of the service economy. Health care (+43,000) once again accounted for the largest share of gains, driven by ambulatory centers and hospitals. Restaurants and bars (+37,000) also contributed meaningfully, continuing a steady post-pandemic normalization. Social assistance (+14,000) was propelled by a 20,000 increase in individual and family services.

The top three contributors accounted for the overwhelming majority of net private-sector hiring in September, with most other major industries posting little change . Seasonal patterns related to the start of the school year may have boosted state and local government hiring and partially flattered the gains in leisure and education but do not account for all of the increase.

Meanwhile, the soft spots remained firmly in place. Transportation and warehousing shed 25,000 jobs, driven by losses in warehousing (–11,000) and couriers (–7,000). Professional and business services — often a bellwether for white-collar demand — also weakened. Temporary staffing was a notable weak spot but employment also fell in tech-centric industries. And federal employment declined another 3,000 ahead of what is expected to be a huge drop in October and November, as DOGE-related retirements and separations will show up.

One relative bright spot: employment in the most cyclical parts of the economy — construction, manufacturing, and logistics — is holding up better than recessionary patterns would suggest. Construction remains modestly positive; manufacturing is only marginally negative; trucking shows mild year-to-year strength. In a downturn, all three would be sharply negative. This is one of the strongest arguments against the notion that the U.S. is sliding into recession today. Of course, these are preliminary figures and the revised data in February are expected to result in large downward revisions.

Unemployment Is Drifting Higher — and Slack Is Accumulating

The unemployment rate rose 0.1 percentage point 4.4%, but the underlying composition reveals a labor market cooling slowly, not collapsing. The labor force posted an outsized gain of 470,000, while household employment rate by 251,000. The number of unemployed rose by the difference, 219,000. This combination — more people looking for work, but not enough hiring to absorb them — is consistent with a plateauing labor market rather than an economy in free fall.

Participation remained at 62.4%, unchanged over the year. The employment-population ratio slipped to 59.7%, down 0.4 points since last September. And the composition of joblessness continues to shift in a concerning direction: permanent job losers rose above 2 million, while temporary layoffs and job leavers remained relatively stable. The rise in permanent job losses will exert further drag on consumer spending, particularly among middle- and lower-income households.

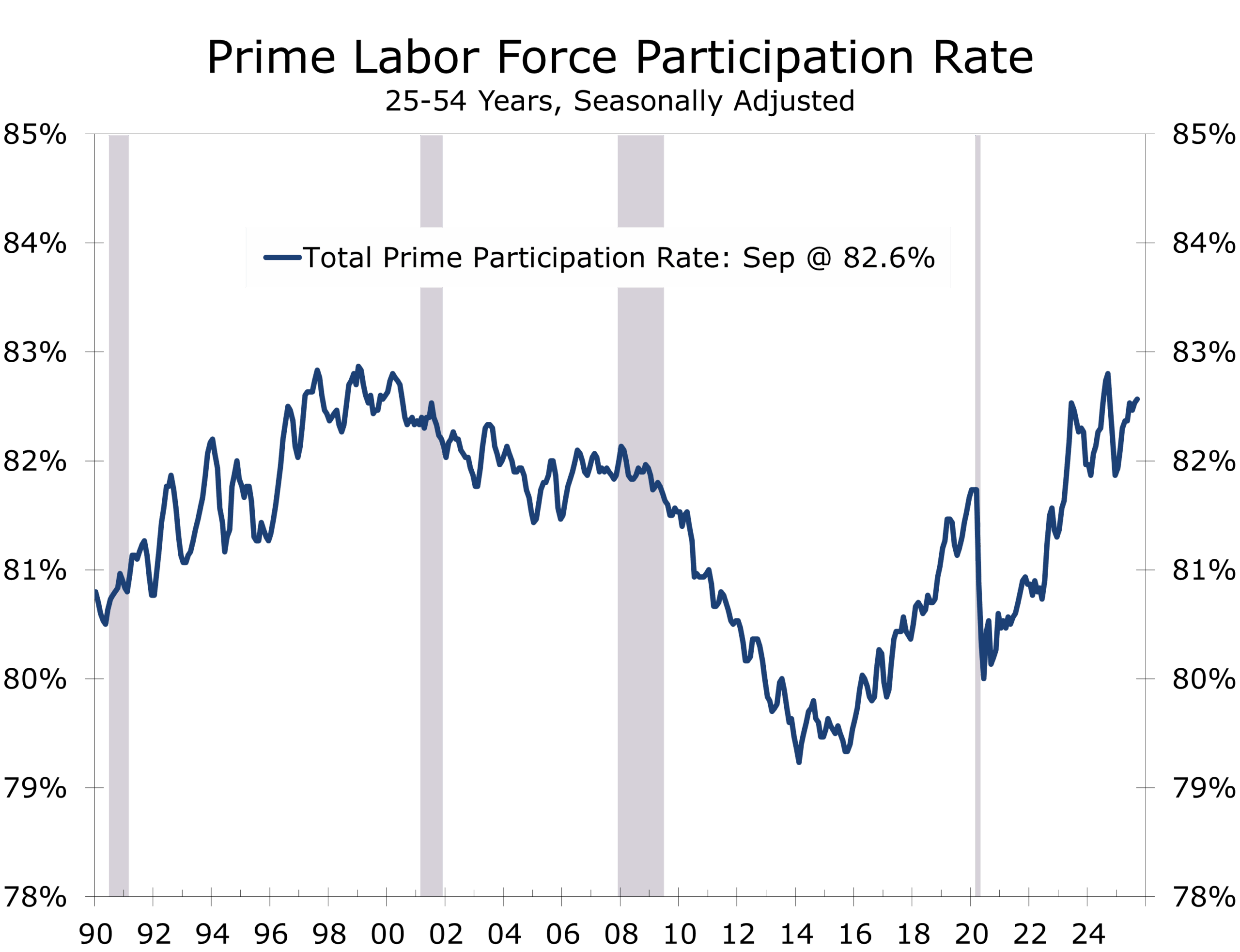

The share of the prime working-age population at work remains high, at just over 80%, and the Sahm Rule remains far from its triggering level, reinforcing that conditions do not yet meet recession thresholds.

Wage Growth and Hours Continue to Moderate

Wage growth slowed to 0.2% m/m and 3.8% y/y, on an overall basis, which is consistent with the Fed’s inflation target. Production and nonsupervisory workers saw slightly stronger gains at 0.3% m/m, but the overall pattern continues to reflect a gradual cooling.

Wage growth has aligned with the Fed’s inflation target — a key precondition for rate cuts.

Hours remained unchanged at 34.2, the average for the past year. Hours worked rose 0.1% in September and were essentially flat during the third quarter, which is well below our forecast of 3.7% GDP growth for the quarter, implying strong productivity growth.

A Late-Cycle Labor Market with Risks Tilting Toward the Downside

Structural indicators point to a maturing business cycle. Hiring is heavily concentrated in health care and services. Goods-producing sectors are flat to mildly negative. Federal employment faces a pending Q4 cliff due to deferred resignations. Permanent job losers are drifting upward. This is classic late-cycle behavior — not recessionary, but not healthy either.

The absence of broad-based deterioration is encouraging, but the accumulation of small points of weakness raises the risk of a slower Q4, especially given the fragile global backdrop and the extension of tariff pressures into fall.

FOMC Implications — A Case for Easing, Delayed by the Data Gap

September’s firmer headline does not change the broader trajectory: the labor market has downshifted from expansion to plateau. The Fed will not have October data and will receive November data only days before its mid-December meeting.

The ingredients for further easing remain in place. Unemployment is drifting higher. Wage pressures have aligned with the inflation target. Hiring is narrow and losing momentum. Goods-producing industries are weakening.

The case for a rate cut is firming — even as the calendar gets messier.

The Fed’s challenge is not the direction of travel — which is clearly softening — but the timing. With the data pipeline disrupted, there may be some reluctance to cut in December but we maintain that in the absence of compelling evidence to suggest otherwise, the Fed will go with the call made on the field and cut rates a quarter point at their December 9-10 FOMC meeting.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 20, 2025

Mark Vitner, Chief Economist

(704) 458-4000

Amid Unevenly Clearing Fog: Nervous Markets, Missing Data, and the New Age of Deficits

Amid Unevenly Clearing Fog: Nervous Markets, Missing Data, and the New Age of Deficits

- The fog is finally lifting, but visibility remains uneven. The return of federal data should re-anchor expectations, and early releases appear likely to confirm what private indicators already signaled: a cooling yet still resilient economy.

- Markets remain choppy, with narrow leadership, rising volatility, and investors on edge. Headlines like The Economist’s “How the markets could topple the global economy” resonate sharply with investors who still carry memories of the GFC.

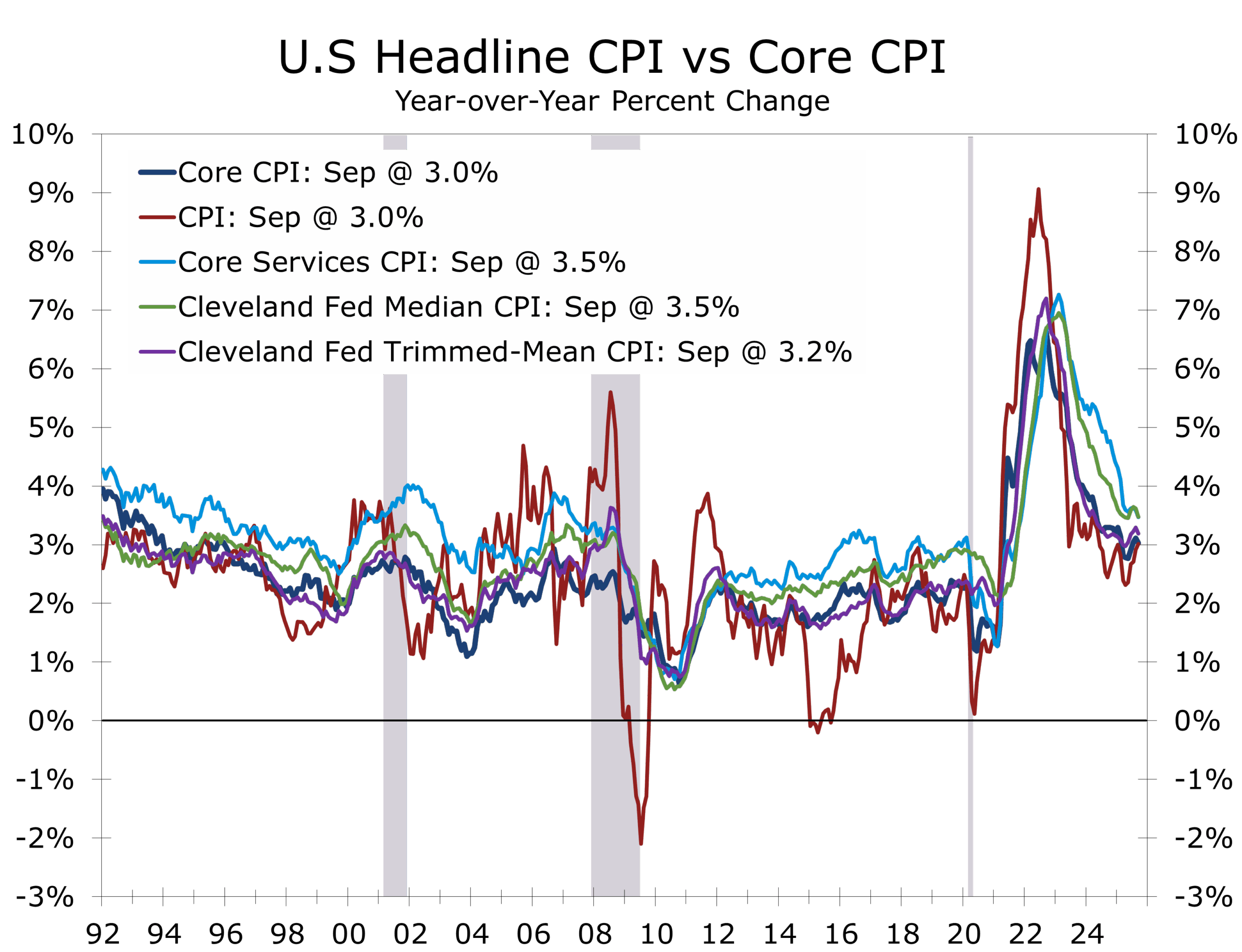

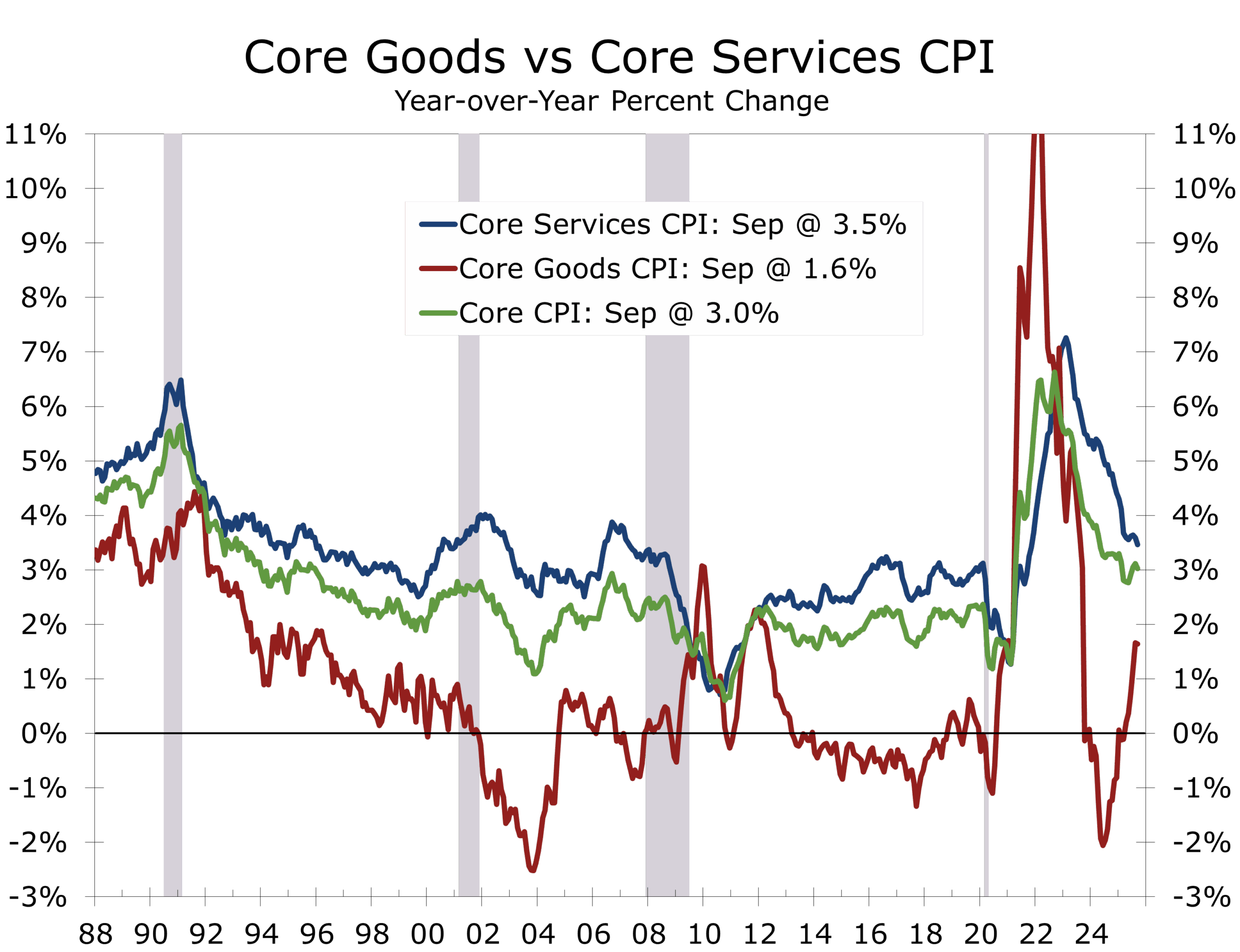

- Inflation continues to ease beneath the surface, with goods prices softening and core services showing further deceleration. Private trackers suggest official CPI will confirm a continued—if uneven—disinflation. The relaxation of several tariffs may support further goods disinflation.

- The labor market is bending, not breaking, as hiring slows and layoff announcements rise, but weekly initial claims remain low. The gig economy and surging Baby Boomer retirements continue to cushion the adjustment.

- Consumers are far more worried about affordability than employment, explaining the widening divergence between deeply pessimistic Sentiment readings and the still-resilient Confidence measure.

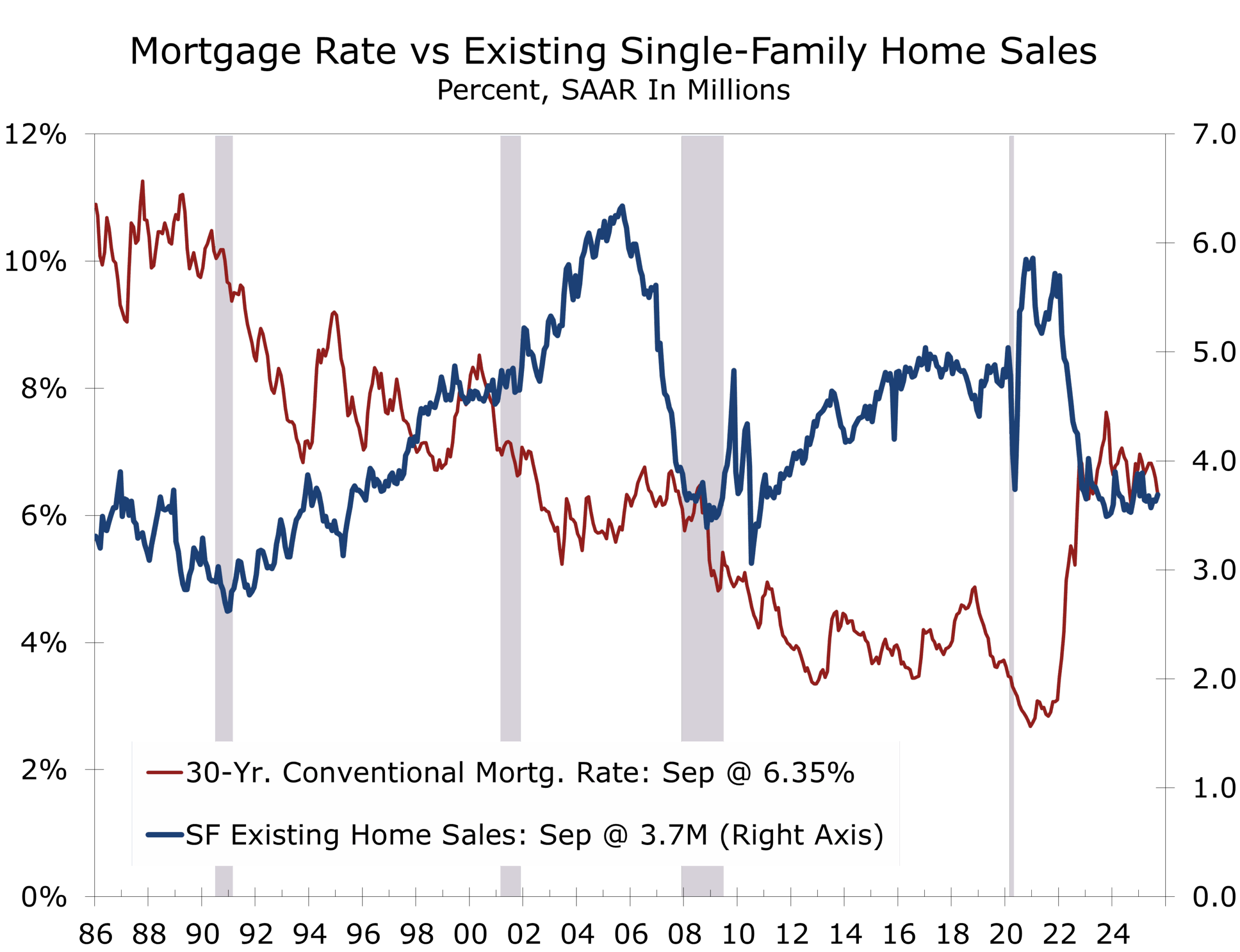

- Housing remains a paradox, with resale supply historically tight while new-home inventories climb. Lock-in dynamics, regional overbuilding, and demographic tailwinds support prices despite intense affordability pressures.

- AI skepticism reflects more dot-com trauma than current fundamentals. Today’s data show strong earnings, clean balance sheets, limited leverage, and capex aligned with real compute demand—conditions inconsistent with a speculative bubble.

- Gold is signaling deep doubts about fiscal sustainability, institutional credibility, and the viability of aging, deficit-heavy advanced economies.

- Fed Nears End of Runoff: Powell’s tone suggests a pivot to growth management, with two more rate cuts likely this year.

- Seven Years’ War fiscal dynamics are reemerging, with major powers overspending into demographic headwinds, rising tax burdens, and broadening generational doubts about capitalism. Stalin’s line—“There are decades where nothing happens, and weeks where decades happen”—feels uncomfortably relevant.

- Geopolitics remain tense but contained, with slow-motion diplomacy between Saudi Arabia and Israel, persistent risks around Iran, and a fragile equilibrium across the China–Taiwan Strait. Russia continues pressing against Ukraine, increasingly targeting civilian infrastructure to break morale or provoke retaliation that could erode Western support for Zelensky.

- Domestic political undercurrents are shifting, with cities such as New York and Seattle electing young, inexperienced Democratic Socialist mayors—reflecting rising generational discontent. This dynamic is already shaping early 2026 political currents, including left-wing pressure on Minority Leader Hakeem Jeffries within his Brooklyn district.

THE FOG BEGINS TO LIFT

The six-week government shutdown severed the economy from its statistical nerve center. Without the jobs report, inflation, income, spending, or productivity data, markets were forced to navigate with one eye closed. For much of that period, the absence of data created more uncertainty than any single release likely would have.

Now, the fog is beginning to thin. The return of the September employment report offers the first hard anchor in more than a month, and expectations point to modest job gains—precisely what private-sector trackers indicated before the shutdown. September is likely to show an economy that lost some momentum but remained fundamentally consistent with its pre-shutdown profile.

October will be murkier. Survey windows were missed, responses were delayed, and parts of the dataset may require reconstruction. Private-sector proxies, including ADP’s 42,000 job gain, slowing weekly job data, and rising layoff announcements—indicate softer conditions with higher downside risks, but not an unraveling.

A newly published ADP weekly series paints a more cautious picture: in the four weeks ending October 25, firms shed an average of 11,250 jobs per week, suggesting that job growth was inconsistent and late-month momentum faded. Layoff announcements continue to rise, and other proxies point to softer hiring, higher downside risk—but at this stage, the signal is of deceleration, not collapse. Still, early estimates for the October employment data call for a net decline in payrolls, as DOGE-era retirements lead to a drop in federal payrolls that will easily swamp what now looks like a modest rise in private payrolls.

Inflation appears to be following a similar arc. Tariffs pushed some goods prices higher, but broader pricing power is fading. Rents and home prices are decelerating. Core services inflation, while elevated, shows renewed signs of slowing. When CPI and PCE return, they are likely to confirm that the tariff-driven bump has largely run its course and that underlying inflation continues to cool.

The fog is clearing—but as it lifts, long-standing vulnerabilities that were hidden in the haze are coming back into view. The softer pace of job growth and easing underlying inflation will inevitably shape policy, increasing the likelihood of selective tariff rollbacks and reinforcing the case for additional interest-rate cuts.

MARKETS: A CORRECTION AND A REORIENTATION, NOT A BUST

Markets remain cautious. The AI complex—once a runaway locomotive—is now moving more like a heavily loaded freight train cresting a grade: powerful, but deliberate, and increasingly sensitive to inclines. Recent selling has been concentrated in mega-cap tech, while cyclicals and defensives have held up better, signaling rotation rather than retreat.

AI skepticism has resurfaced, driven less by current fundamentals and more by the long shadow of the dot-com bust. The comparison, however, is superficial. Balance sheets are strong, leverage is minimal, earnings are rising, and capex remains tightly linked to real demand for computing power rather than speculative excess. IPO volumes are modest, and valuation expansion has been concentrated, not universal. A bubble requires broad exuberance and financial overextension; while markets have shown pockets of enthusiasm—especially as indices pushed to new highs—the underlying numbers do not support the excesses that typify true bubbles.

Even so, investors are on edge. The Economist’s warning that “the markets could topple the global economy” sharpened anxieties—especially among those who lived through 2000–2002 and 2008–2009. In this environment, sentiment reacts violently to uncertainty, even when fundamentals argue for a normal correction and continued sector rotation away from the most fully valued parts of the tech complex.

This market is undergoing a pivot—part correction, part rotation, part repricing—not a systemic breakdown. The path forward will depend on how quickly the data restore visibility. As the economic fog lifts and the trajectory of growth becomes clearer, we expect markets to stabilize and leadership to broaden beyond the narrow handful of AI-driven names that have dominated much of the past year.

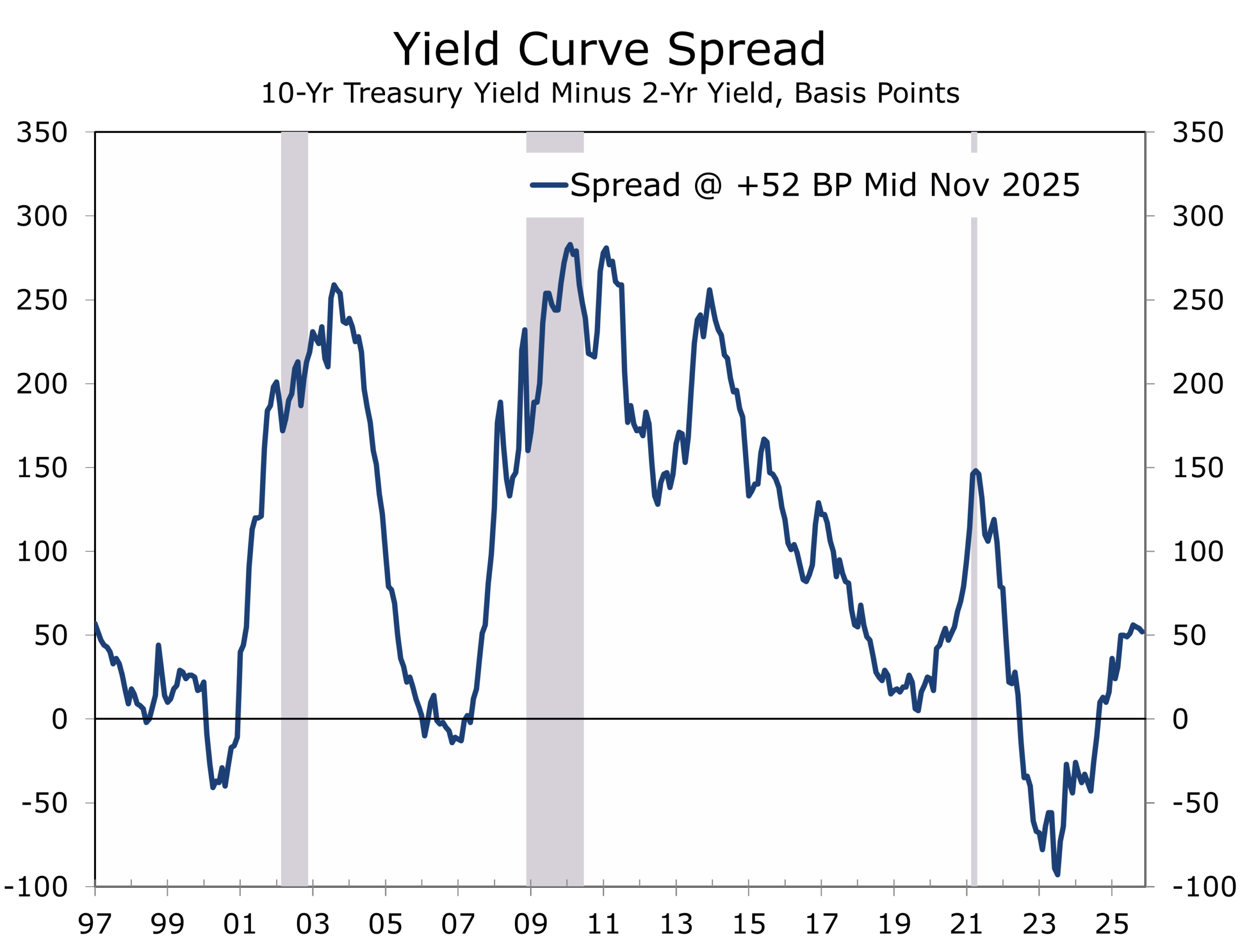

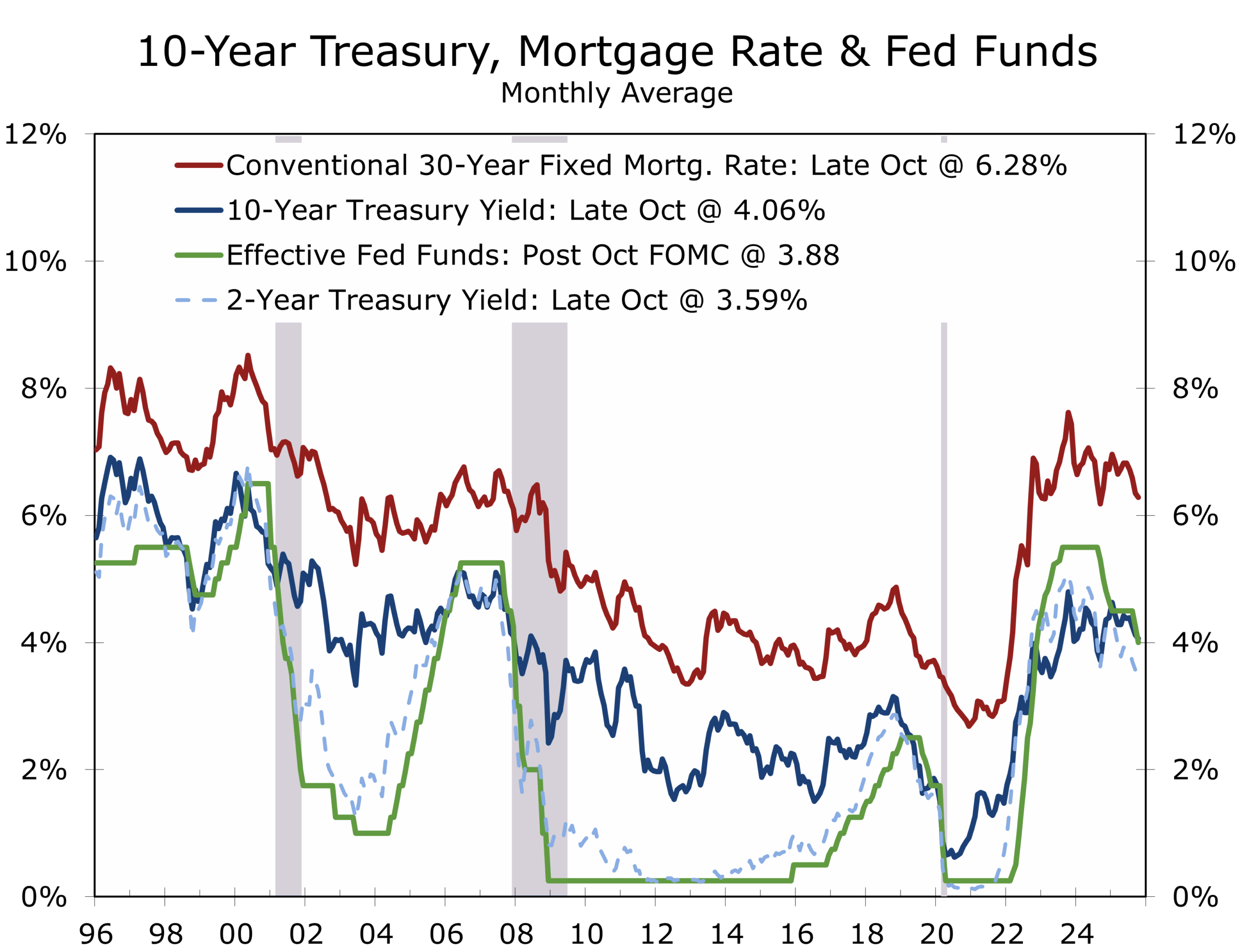

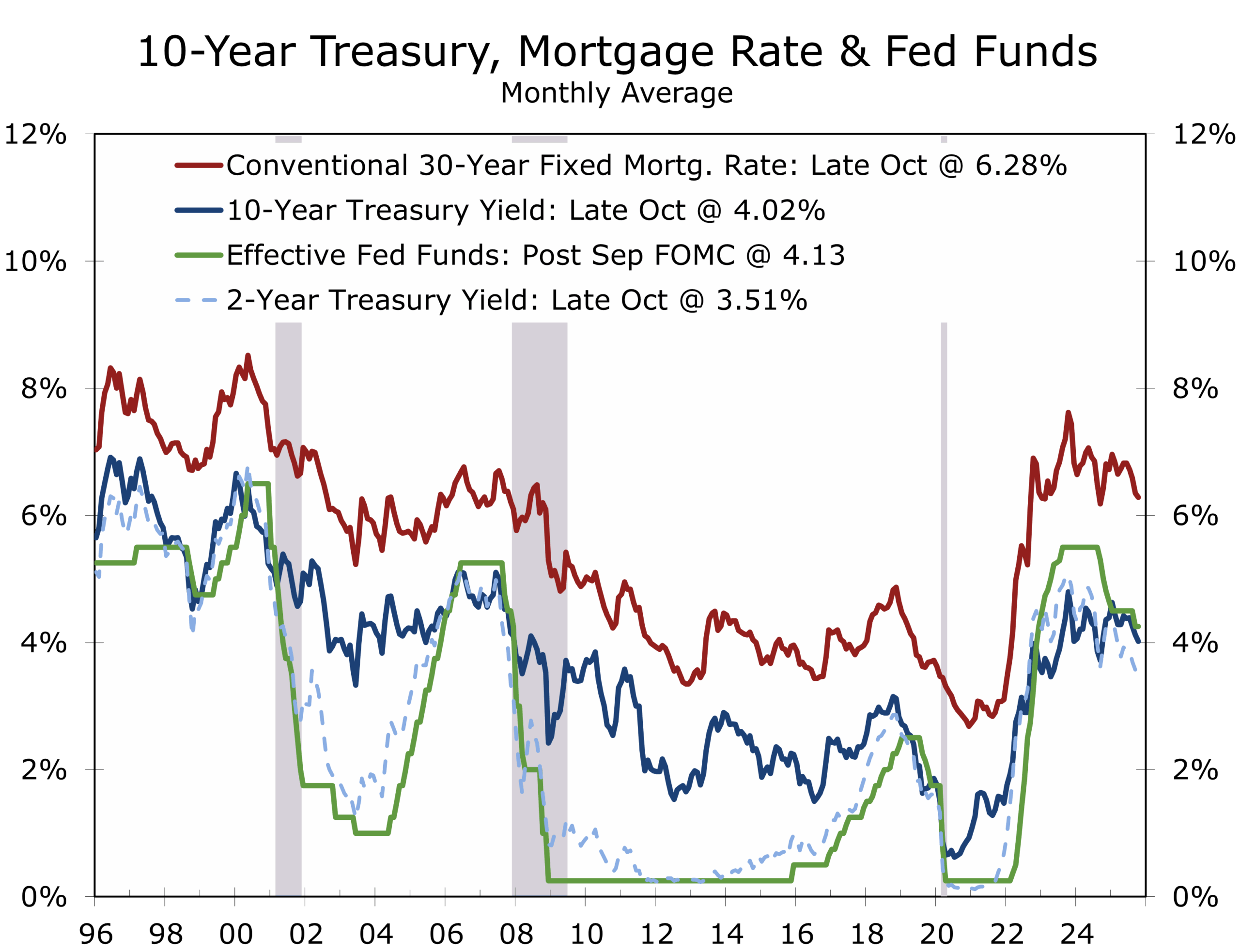

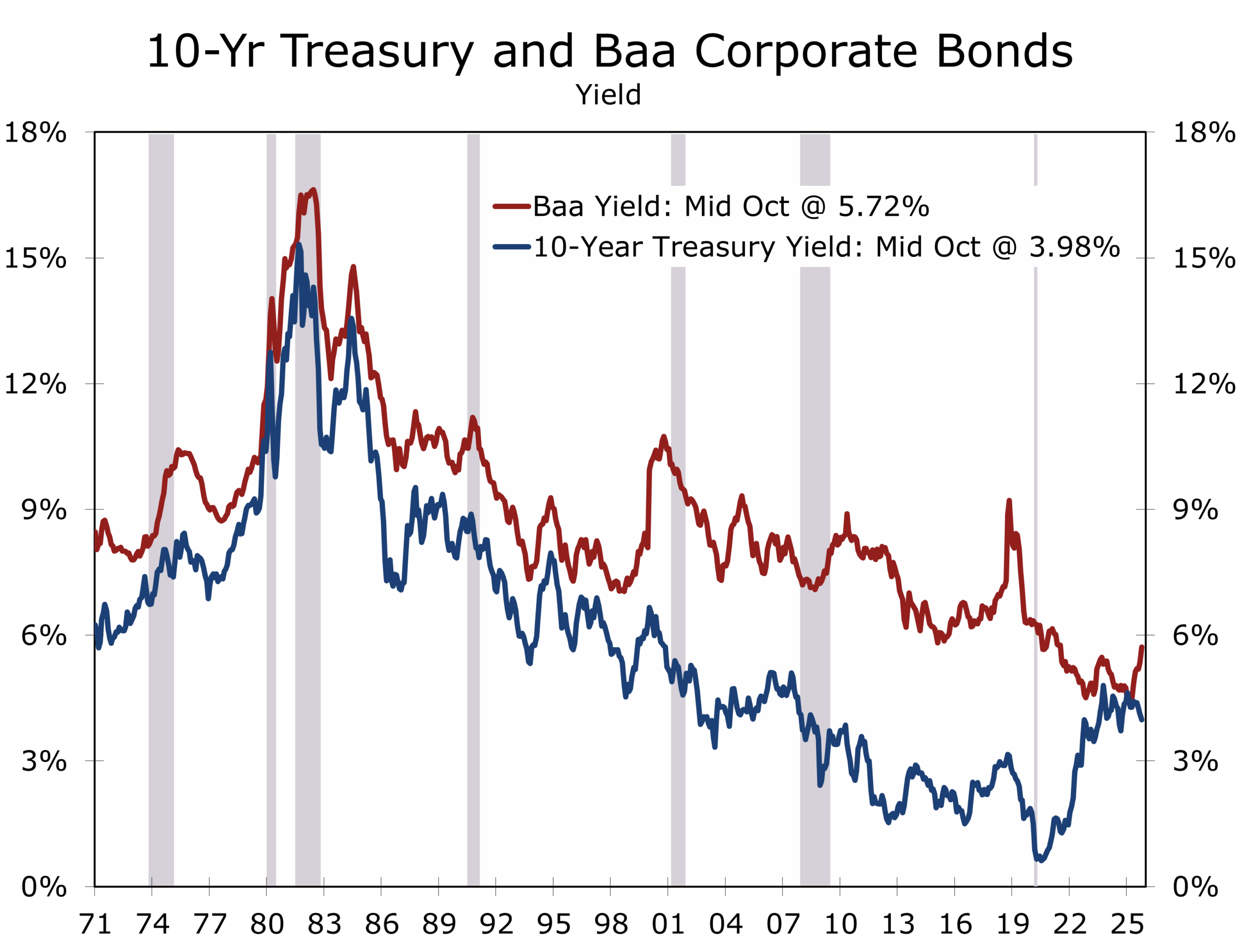

RATES & THE CURVE: ORDERLY NORMALIZATION, LATE-1990s PARALLELS

The yield curve has remained modestly positive for much of the year—a stark departure from the deep and persistent inversions of 2022–23. A drifting lower 2-year reflects expectations for at least one more cut in the federal funds rate, while the 10-year remains elevated due to firmer term premiums and large Treasury issuance. Together, they point to normalization rather than stress and reinforce our forecast for stronger growth in the second half of 2026 following a near pause in growth during the current quarter and Q1 2026.

Kevin Warsh and Kevin Hassett argue that today’s macro backdrop echoes aspects of the late 1990s: an early-stage productivity upswing driven by AI, hardened supply chains, and an investment-led expansion that could ultimately allow short-term rates to settle below what the forward curve implies. They view the present moment as closer to Internet 1.0 and the Y2K investment cycle than to any inflationary replay of the 1970s.

Christopher Waller—now widely seen as a leading contender for Fed Chair—takes a more incrementalist approach. He argues for refining the current framework rather than redesigning it and has signaled that another quarter-point cut in December will likely be appropriate. Waller has underscored that “easier financial conditions” reflected in markets earlier this fall were not being felt by middle-income households facing intense affordability pressures. He has also noted that the labor market is losing momentum and that tariff-related inflation noise is already fading, leaving core inflation “close to 2 percent.”

This debate highlights a deeper reality: high structural deficits are narrowing the Fed’s room to maneuver. Interest expense is consuming a growing share of federal revenues, Treasury issuance is lifting term premiums, and fiscal policy is exerting a growing pull on the long end of the curve. Monetary and fiscal tools—long treated as separate levers—are beginning to intersect in ways not seen in decades.

LABOR MARKETS: SOFTENING, BUT STRUCTURALLY SUPPORTED

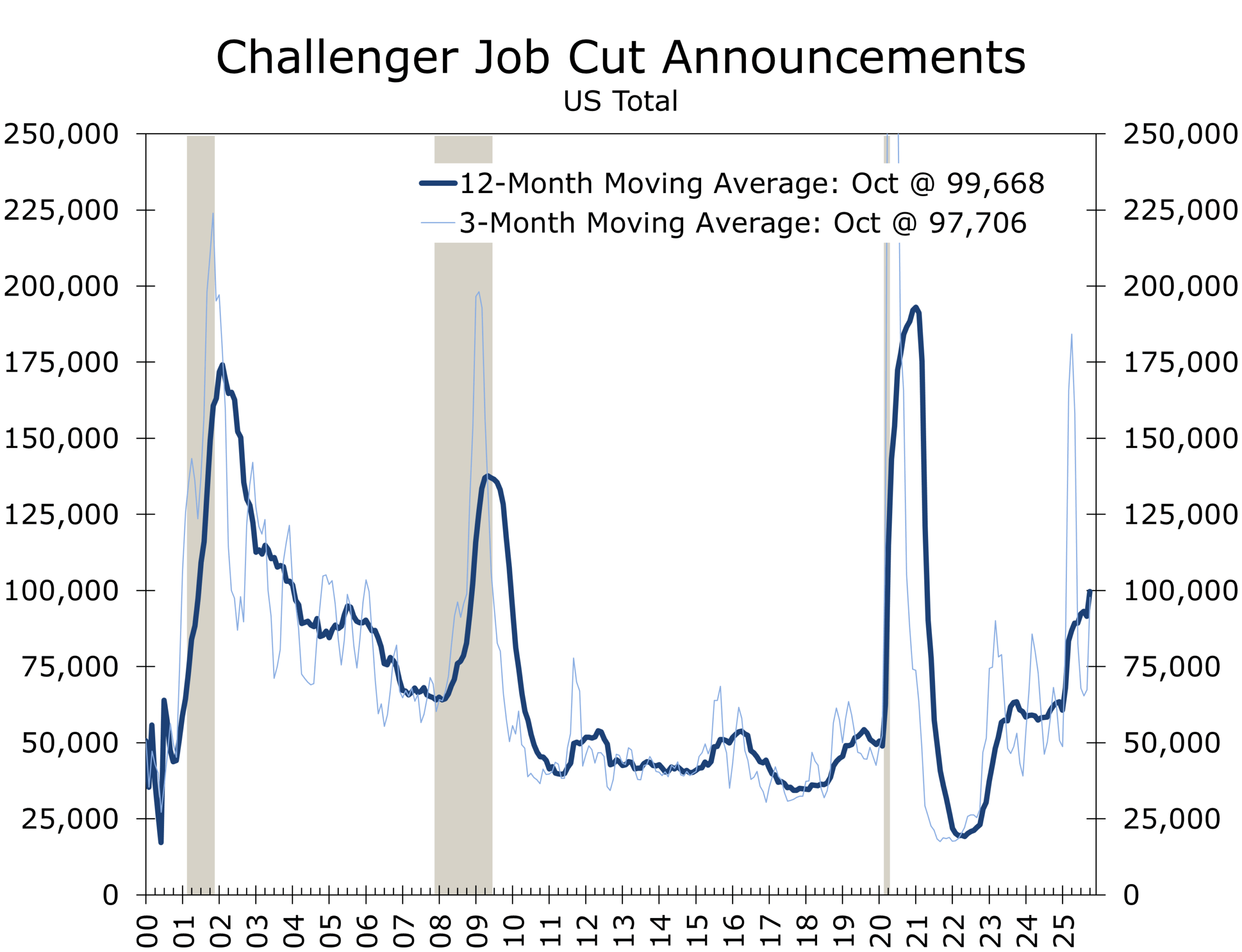

Labor markets continue to cool. Hiring has slowed, job postings have eased, and layoff announcements are rising. Challenger’s October tally was the highest for that month since 2003 and WARN notices in several large states have moved higher. The pattern is eerily similar to the early stages of past recessions, where firms begin trimming headcounts well before claims rise. The trend is also broadening. Verizon announced the largest layoff in its history this past week, with plans to eliminate 13,000 positions—an unusually large move for a company that typically adjusts costs more gradually.

Despite the tide of announcements, weekly jobless claims remain low. Two structural dynamics explain the apparent contradiction. First, the gig economy now acts as a shock absorber, allowing displaced workers to pivot quickly into rideshare, delivery, freelance, or digital task-based income. This was evident during the shutdown, when furloughed federal workers immediately turned to gig work to bridge income gaps. The availability of flexible, on-demand earnings blunts the impact of layoffs and suppresses claims.

Second, accelerating Baby Boomer retirements continue to thin the labor force even as demand softens. This demographic shift reduces measured slack, supports wage stability, and prevents the kind of sharp unemployment spikes seen in previous downturns. Many firms are eliminating positions that might previously have gone to younger workers rather than laying off incumbents.

Labor markets are bending, not breaking. The still low unemployment rate likely overstates strength, while the surge in layoff announcements likely overstates weakness. The truth lies somewhere in between—a cooler, more cautious labor market with meaningful pockets of resilience, with payroll gains averaging 75,000 a month.

CONSUMERS: AFFORDABILITY IS THE PRESSURE POINT

Consumers remain far more anxious about affordability than about job loss. Rents, insurance, utilities, medical services, auto repairs, and debt service continue to compress budgets. This explains why the University of Michigan’s Index of Consumer Sentiment remains historically weak while the Conference Board’s Consumer Confidence Index remains consistent with moderate growth.

High-frequency spending data show a cooler but still expanding consumer backdrop. Lower-income households face the most intense pressure, with rising delinquencies, heavier Buy Now–Pay Later usage, thinning liquidity buffers—but overall spending remains positive.

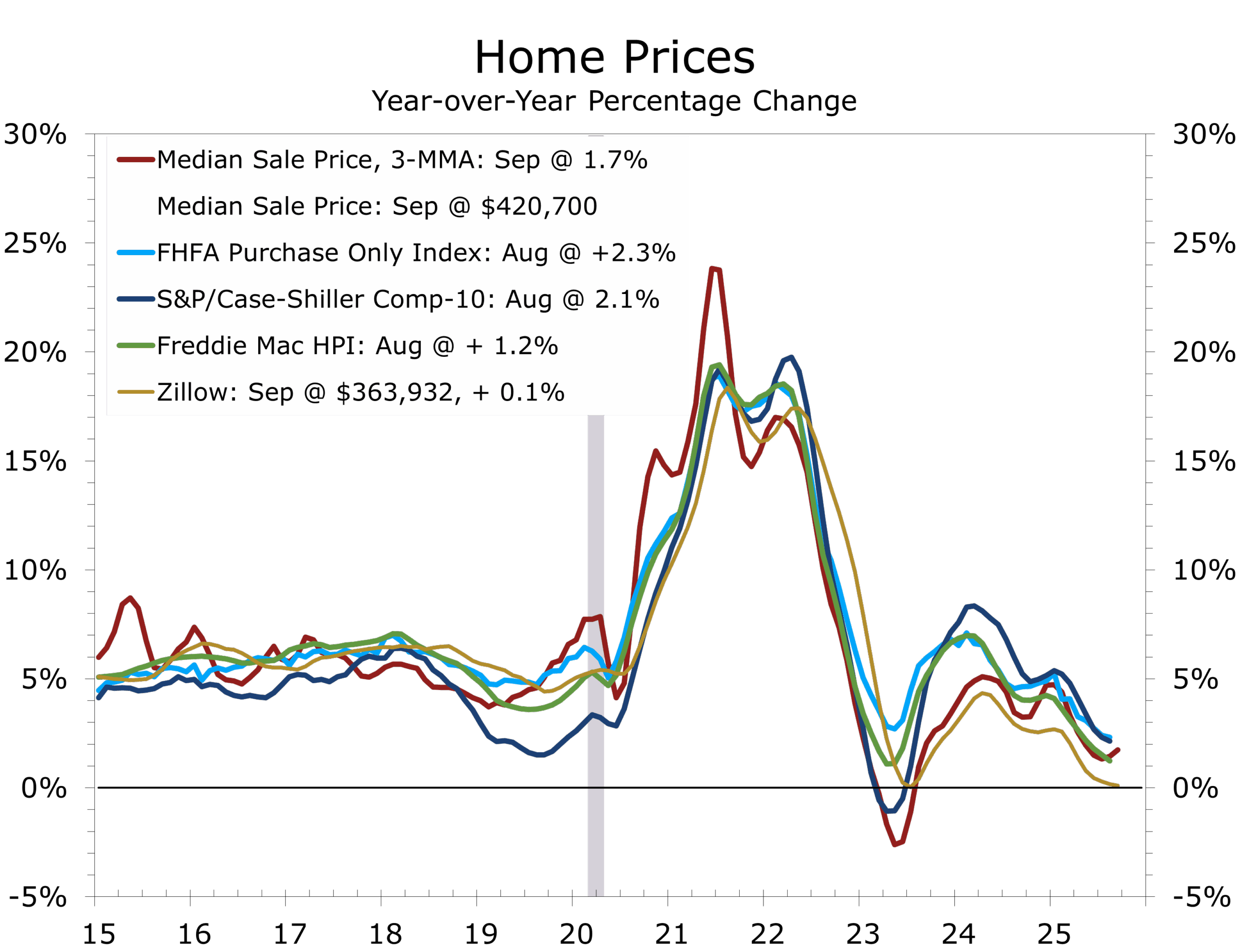

HOUSING: THE PARADOX THAT DEFINES THE CYCLE

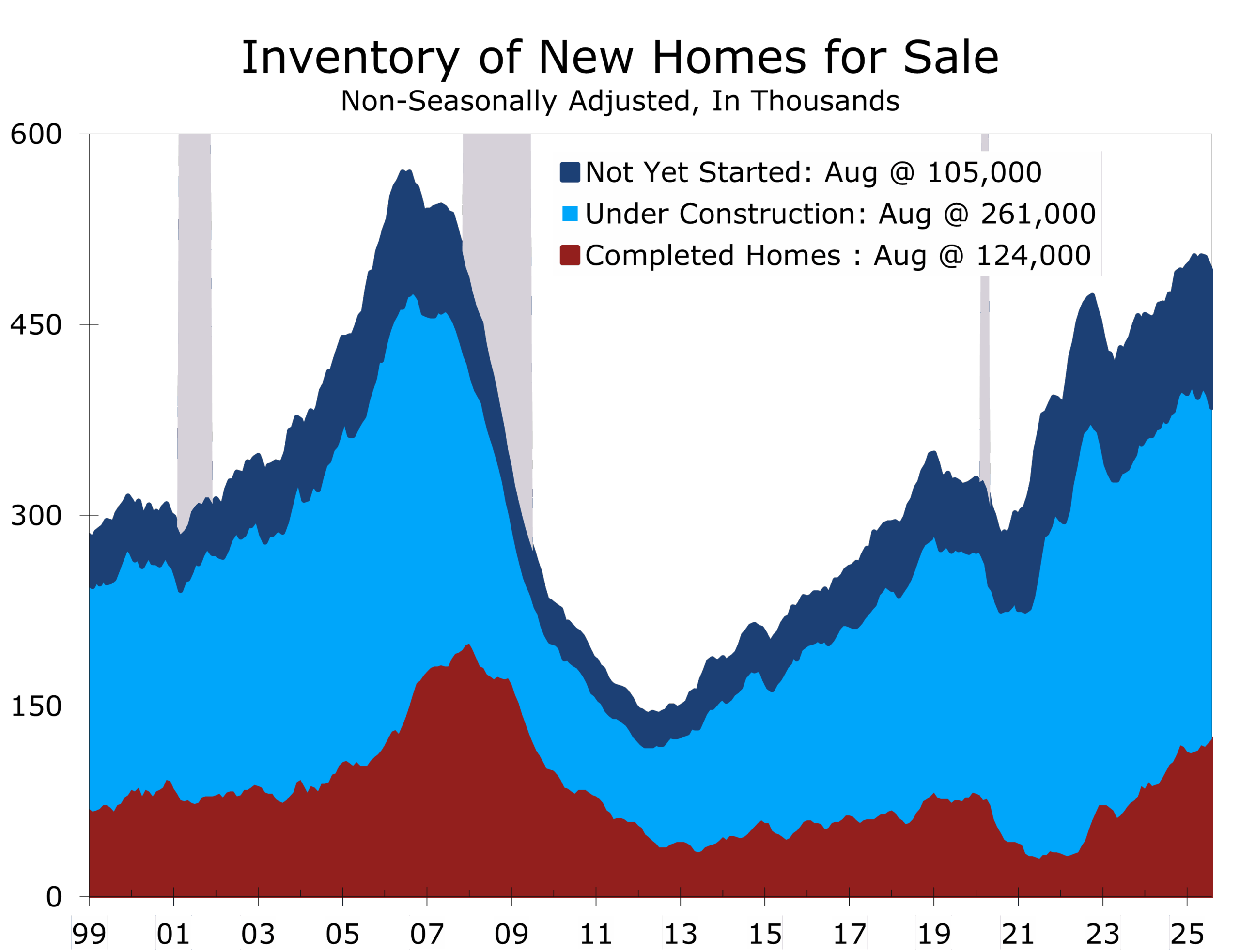

Housing remains the clearest example of structural imbalance. The existing home market is historically undersupplied. Millions of owners with sub-5% mortgages remain unwilling to list, creating structural scarcity and a durable price floor. By contrast, the new home market is working through the tail end of the pandemic-era pipeline. Builders in the Southeast and Mountain West are sitting on elevated completed inventories, the highest since the housing bubble—leading to aggressive incentives and rate buydowns to support absorption.

While new home inventories are the highest since the housing bust, this is not a replay of 2005–2007. While some formerly red-hot markets, most notably Central and Southern Florida, are seeing widespread declines, most markets are seeing only modest price adjustment and overall home prices are still running about 1.5% above their year ago level. The tight resale market prevents builders from slashing prices too much without triggering appraisal failures, cancellations, and margin deterioration. Moreover, Millennials and Gen Z continue to age into peak household-formation years, supporting underlying demand.

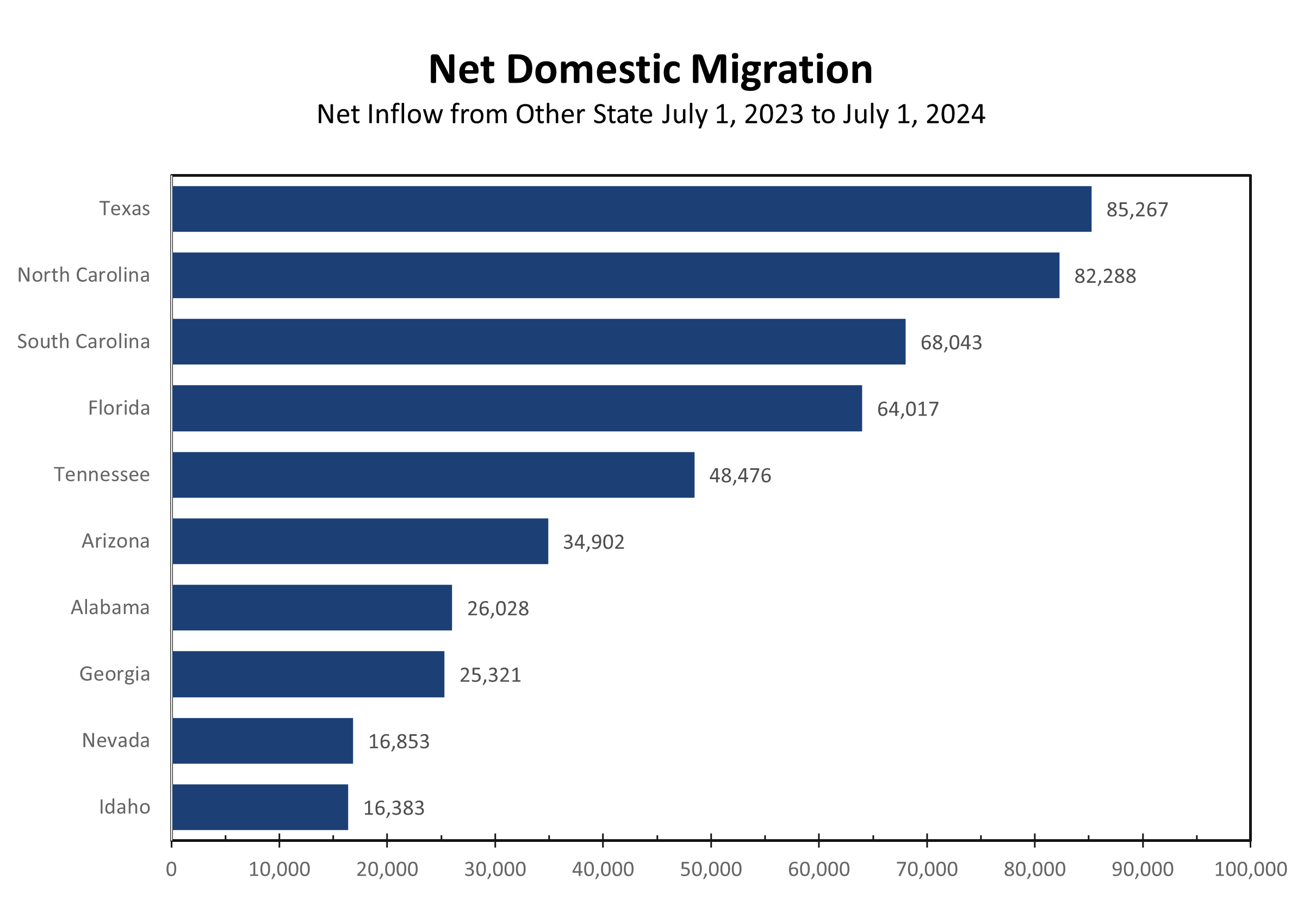

One way that consumers are adjusting is by migrating to parts of the country where housing is relatively more affordable. Texas, the Carolinas, Georgia, Tennessee, Arizona and Alabama are the big winners in this trend.

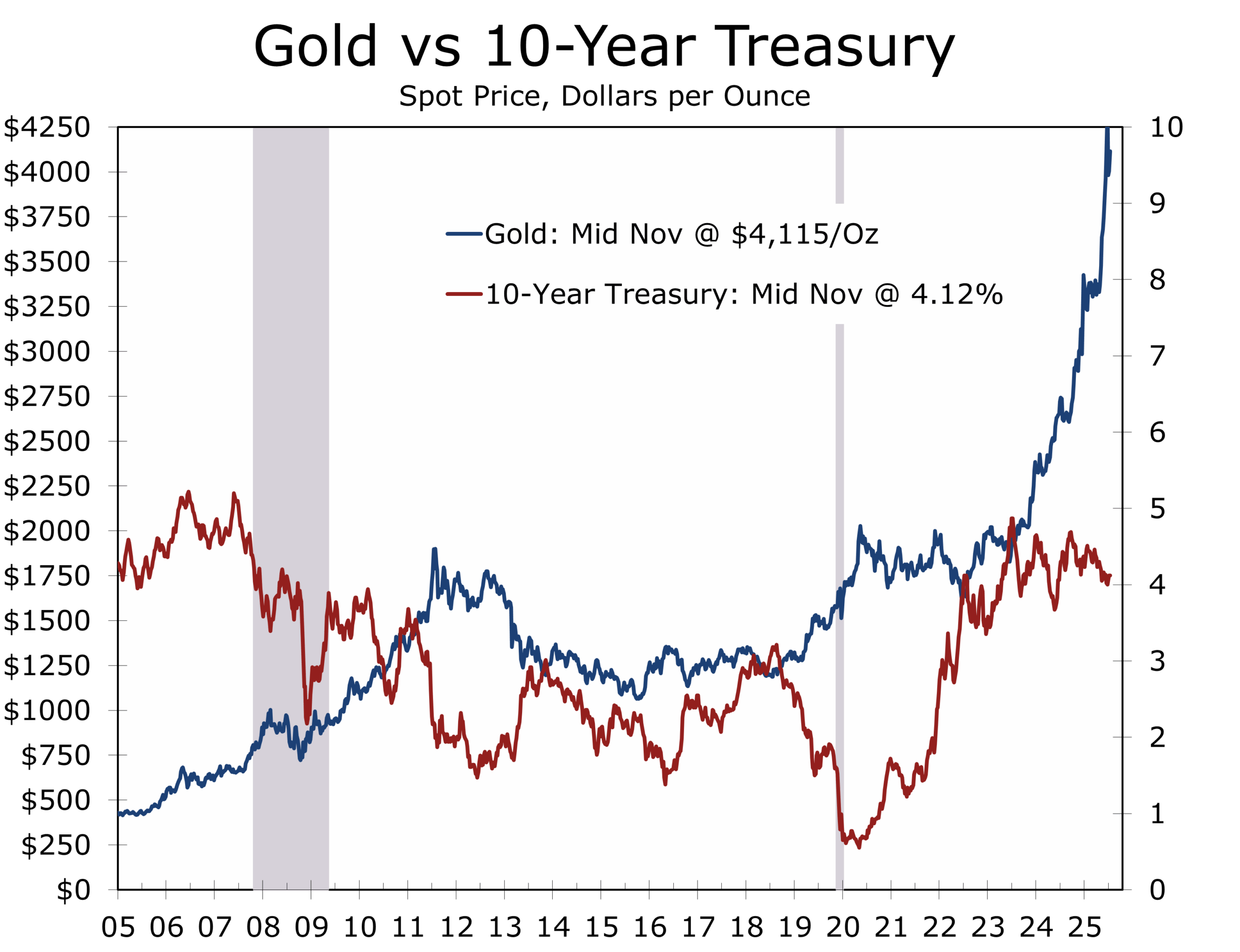

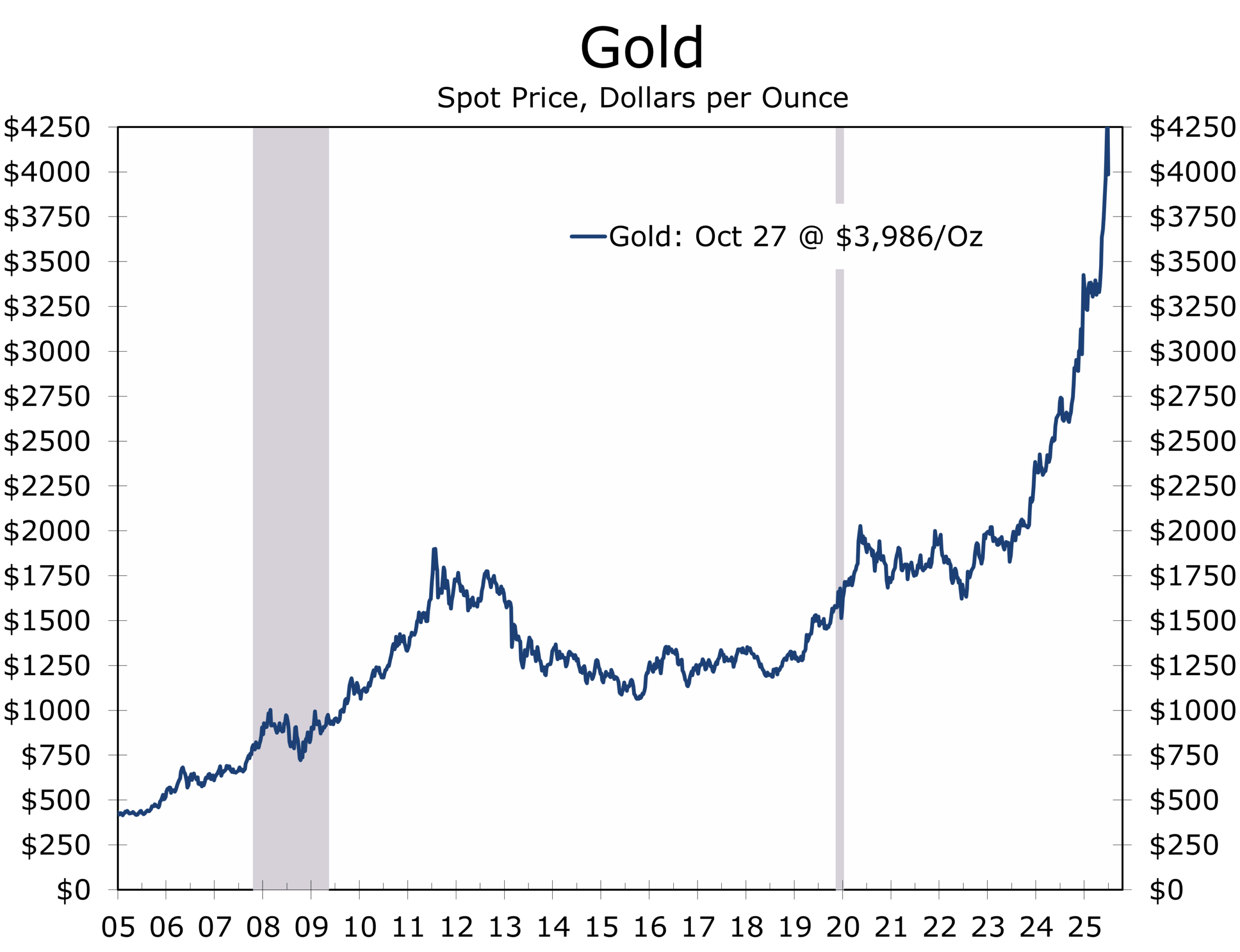

Gold, Deficits, and the New Age of Policy Doubt

Gold is rallying not because of near-term inflation jitters but because investors are questioning the durability of fiscal and geopolitical strategy itself. Structural deficits continue to widen, aging populations are colliding with rising interest burdens, and political systems across advanced economies remain unwilling—or unable—to confront basic fiscal arithmetic. The result is a growing search for assets immune to policy drift. Gold has become less an inflation hedge and more a hedge against eroding fiscal capacity across the U.S., Europe, Japan, and increasingly China, where demographic decline and debt saturation present challenges just as severe.

Layered onto these pressures is the intensifying U.S.–China microchip rivalry—a technological arms race reshaping global power dynamics and straining national budgets. Washington’s CHIPS incentives and export controls, combined with Beijing’s massive state-backed subsidies, have set off a costly contest for semiconductor self-sufficiency. That competition is cascading through the rest of the world: developed economies in Europe and East Asia are being pulled into subsidy battles to protect their own chip ecosystems, while developing economies—from Vietnam and Malaysia to Mexico and India—are absorbing new investment flows as supply chains reroute. The race for technological sovereignty is becoming a fiscal challenge as much as a strategic one, amplifying the sense that traditional policy frameworks are no longer fit for the era.

The historical rhyme is unmistakable. The Seven Years’ War drained the treasuries of the world’s major powers as they chased geopolitical advantage, triggering fiscal crises, heavier taxes, and rising public frustration—conditions that helped set the stage for the American Revolution. Today’s environment carries a similar echo: mounting fiscal stress, institutional fatigue, and a generational skepticism that the existing economic model can still deliver upward mobility or broad-based prosperity.

Stalin’s stark warning captures the moment: “There are decades where nothing happens; and there are weeks where decades happen.” After years in which deeper structural issues could be deferred, the combination of deficits, demographics, and dual-use technology competition has pushed them to the forefront. Gold’s strength is not about the next CPI print—it reflects rising concern over what the next decade will demand from fiscal and monetary systems already stretched to their limits.

GEOPOLITICS: SLOW MOVES, SHARP UNDERCURRENTS

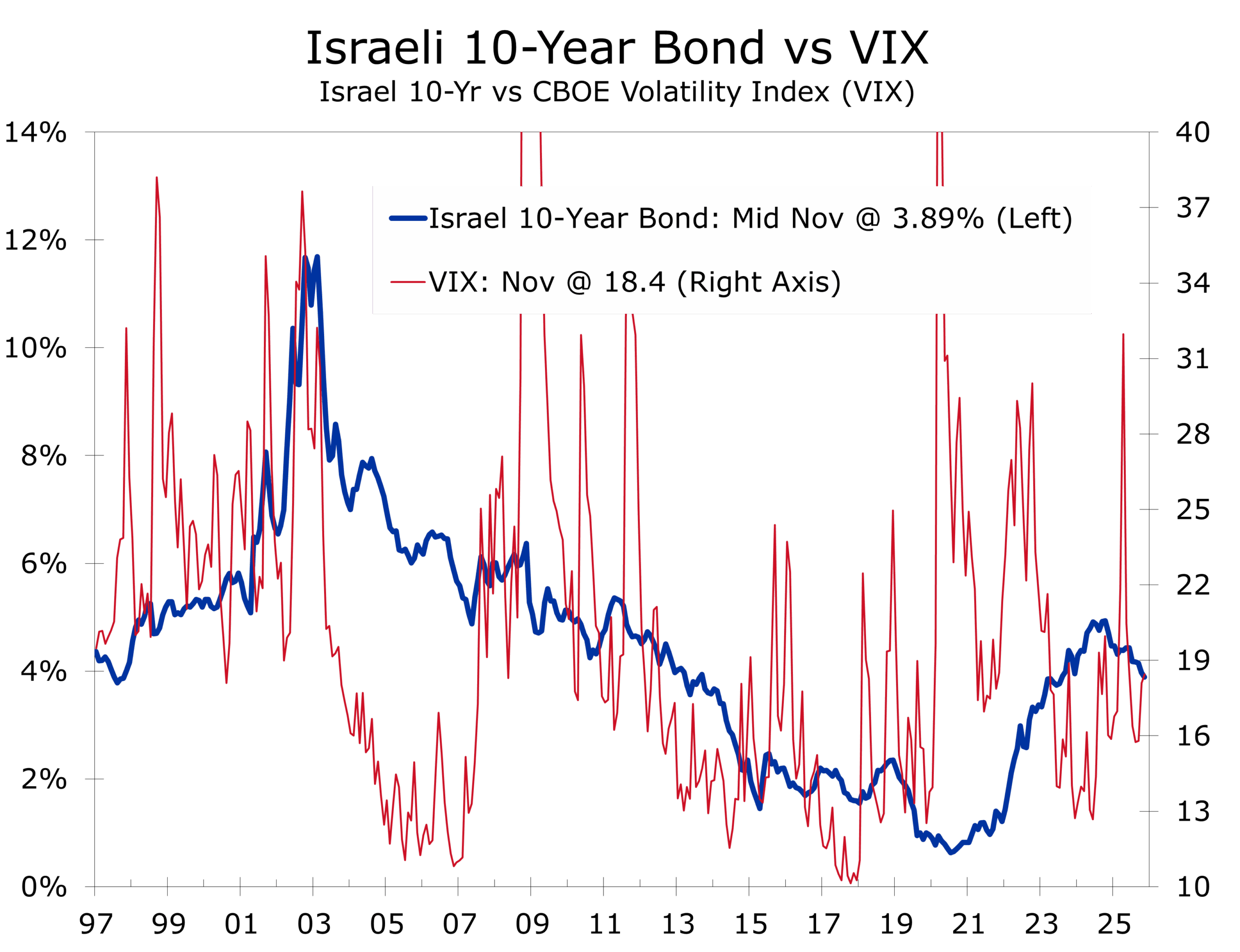

The Middle East tail risk has fallen sharply. The decisive ceasefire that took effect on October 10 has held and the UN Security Council’s unanimous November 17 endorsement of the Trump 20-point Gaza plan—backed by Saudi Arabia and the UAE—has dramatically raised the odds of Saudi-Israeli normalization at some point in 2026. Riyadh’s asks (U.S. defense treaty, civilian nuclear program, tangible Palestinian progress) are steep but now within reach. Credit markets have already responded: S&P shifted Israel’s outlook to stable on November 7, Israeli 10-year yields have dropped 45 bps since early October, and Gulf sovereign spreads are at two-year tights.

Iran remains the principal residual wildcard. Proxy forces are subdued but not disarmed, missile and cyber programs advance unchecked, and domestic pressure could still trigger asymmetric retaliation if Tehran feels encircled by a formal anti-Iran axis. Base case is further de-escalation.

China continues tightly calibrated gray-zone pressure on Taiwan while closing the military gap at pace. TSMC-centric exposures carry explicit invasion pricing—keep rotating to on-shored and diversified-node semis.

Russia systematically strikes Ukrainian civilian infrastructure while baiting Kyiv into responses on Russian soil that would erode international support. European utilities, grains, and freight remain vulnerable; energy prices appear too low given the risk set—stay long hard-currency energy.

U.S. generational backlash is accelerating, amplified by documented PRC, Russian, and Iranian social-media influence operations. DSA mayors hold New York and Seattle; Hakeem Jeffries and Governor Kathy Hochul face credible 2026 left-wing primaries. Favor investments in red states, particularly Texas; raise hurdles for duration and illiquid credit in progressive jurisdictions.

Mexico’s Gen Z protests have escalated into the most sustained and geographically widespread unrest since 1994. Triggered by collapsing real wages, cartel violence spilling into urban areas, and anger at perceived judicial capture under the outgoing administration, demonstrations have paralyzed major cities and forced repeated highway blockades. President-elect Sheinbaum has responded with a mix of concessions and force, but confidence in public security remains at multi-decade lows. Near-shoring beneficiaries with more than 30% Mexico revenue exposure (auto parts, electronics assembly, logistics) now trade with a visible political-risk discount. Selectively underweight or hedge that exposure; favor exporters with U.S.-centric or multi-Latin American footprints.

Risk premiums are easing but not gone. Favor gold, short-dated T-bills, defense, energy, commodity-exposed investment, and a neutral-to-modest overweight on Israeli and Gulf credits. Watch Saudi normalization triggers closely—upside surprises are now the higher-probability outcome. Position defensively but opportunistically.

Outlook – The Fog is Thinning, Albeit Unevenly

U.S. growth has proven far more resilient than nearly anyone expected at mid-year. The Atlanta Fed GDPNow has consistently tracked at or above the high end of consensus, and even after the prolonged government shutdown shaved Q4 estimates, the underlying pace remains robust. Beneath the noise lies the same structural shift we have highlighted all year: an economy increasingly powered by capital-intensive, high-productivity sectors—AI infrastructure, aerospace, defense, and advanced manufacturing—rather than traditional labor-driven expansion. Productivity is quietly rebuilding the foundation for durable growth.

Layoffs have spiked but remain concentrated in a handful of over-extended sectors and have not yet triggered broader contagion. Housing continues to restrain momentum yet does not pose systemic risk; new-home inventories are rising, existing-home supply remains tight, and prices are adjusting modestly. The housing drag is now unambiguously disinflationary, giving the Fed additional latitude to ease.

We still expect the Fed to accomplish more by doing less—no more than three additional 25 bp cuts in the base case. A weakening labor market, the recent equity correction, and the Fed’s upcoming leadership transition introduce modest downside risks, but nothing that derails the expansion. Markets have begun pricing exactly this scenario. Not a boom, nor a bust, but a resilient gradual reacceleration that becomes visible by mid-2026.

The shutdown and layoff headlines generated fog, yet the core pillars: innovation, secure property rights, and trusted capital markets remain unshaken. The fog is thinning, unevenly but unmistakably. We expect growth to surprise to the upside once again in 2026.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 18, 2025

Mark Vitner, Chief Economist

704-458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – The Expansion Goes Jobless

Highlights of the Week

- The Government shutdown appears likely to end as a bipartisan Senate vote approaches; market uncertainty may ease.

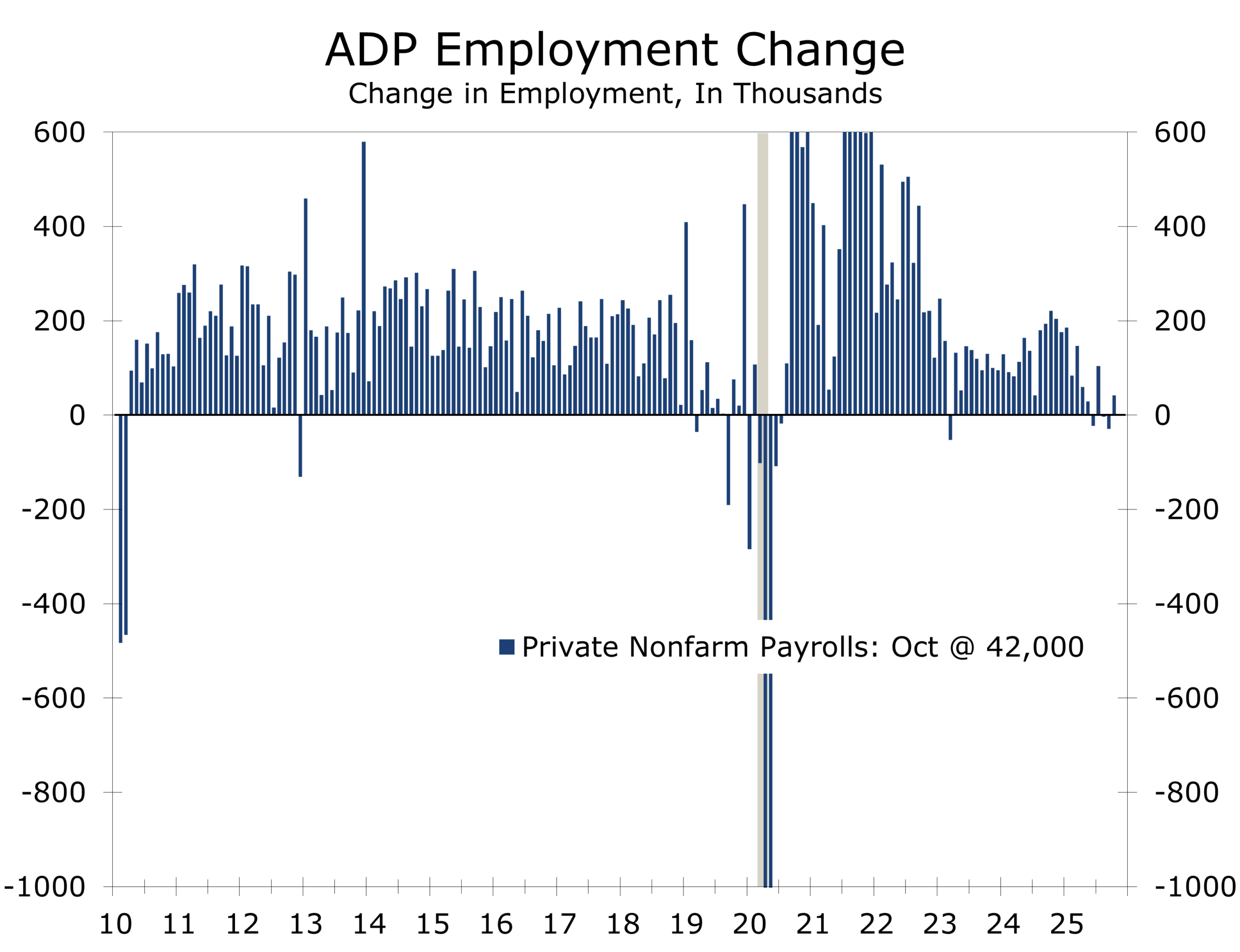

- Private payrolls rose 42,000 in October per ADP, while Challenger layoffs surged 183% from September and jobless claims held near 228,000.

- The data reinforce a picture of a cooling but not collapsing labor market—one where hiring slows, layoffs rise selectively, and firms sustain output through productivity gains rather than adding staff. We may be entering a "jobless expansion".

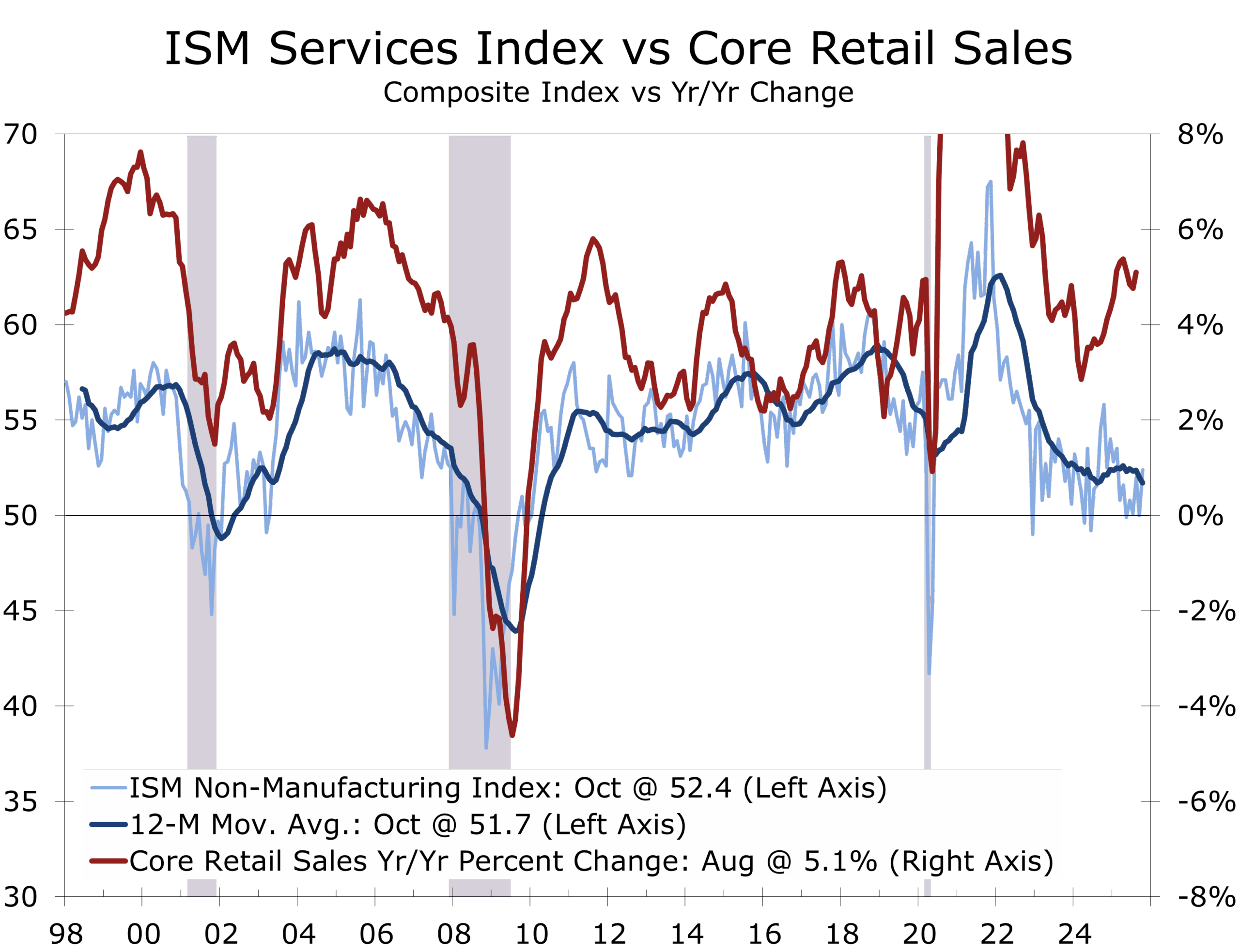

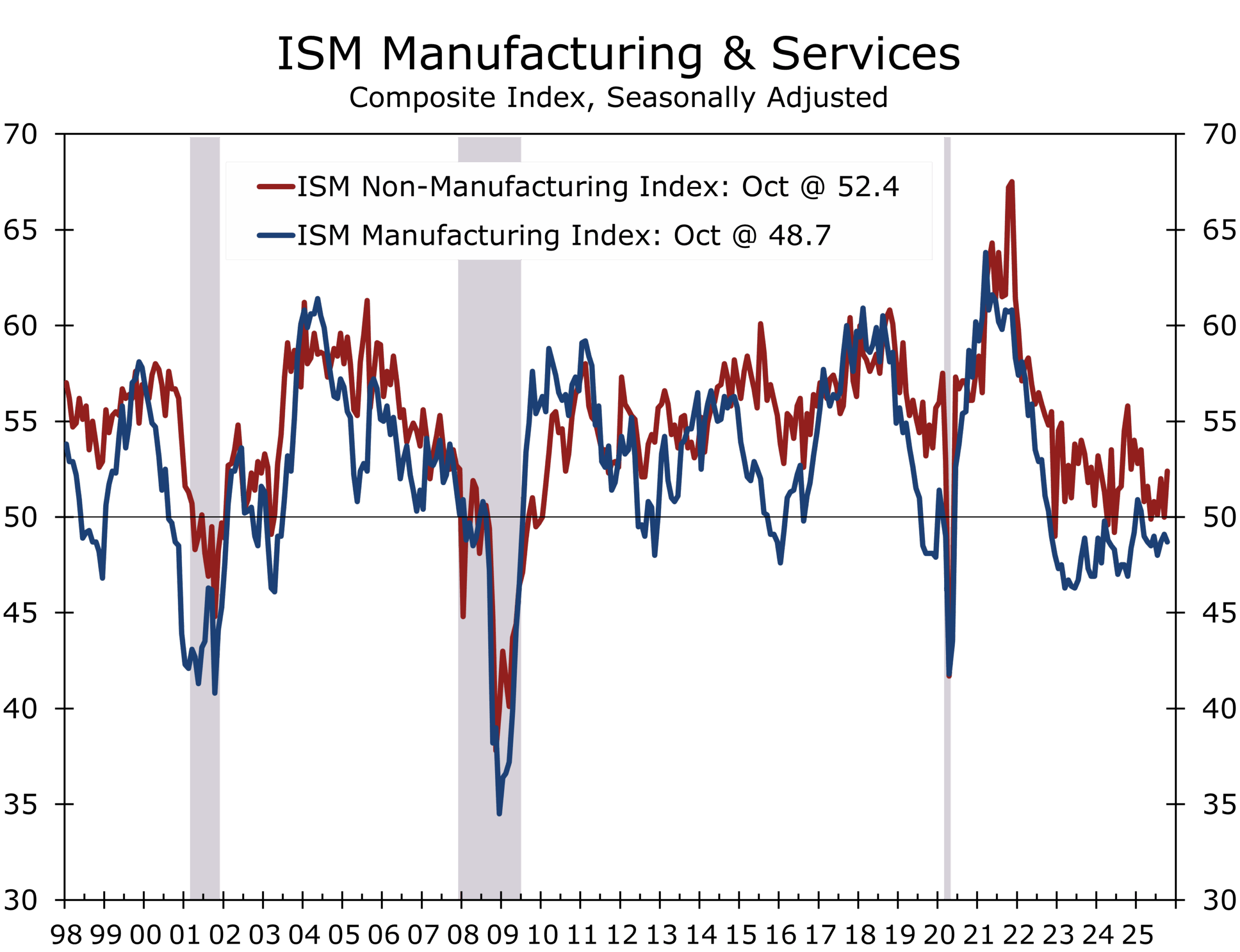

- ISM Services rebounded while manufacturing remains mired in

- Fed officials remain divided as data blackout clouds the December policy decision.

- Stocks suffered their sharpest weekly loss since April; yields remain steady near 4 percent.

- Off-year U.S. elections deepened fiscal gridlock, while Russia escalated winter strikes on Ukraine’s power grid and Israel expanded operations against Hezbollah. Local politics—from New York to Beirut—are now reverberating globally, shaping fiscal policy, supply risk, and energy markets more than central banks.

U.S. ECONOMY & FINANCIAL MARKETS

This week’s commentary assesses the macro and policy landscape, focusing on persistent fiscal uncertainty, labor market bifurcation, and global flashpoints impacting risk assets and corporate strategy. As the government shutdown extends to historic length, prospects for a resolution are improving, with a pivotal Senate vote scheduled Sunday evening and Democrats signaling willingness to support a deal to reopen the government. Macro data visibility remains diminished, creating tactical challenges for allocators and policymakers.

An apparent resolution of the government shutdown appears to be in the works.

The longest government shutdown on record is finally moving toward a resolution. The Senate advanced a bipartisan funding bill on Sunday by a 60–40 vote, clearing the key procedural hurdle to reopen the government. The measure—backed by eight Democrats—would fund most federal agencies through late January and provide retroactive pay to furloughed workers. Negotiations continue over health-care subsidies and longer-term spending caps. The CBO estimates the shutdown has already shaved 1–2 percentage points off Q4 GDP, or roughly $14 billion. A final Senate vote is expected early this week, potentially allowing agencies to resume operations and easing mounting economic strains.

While discussions remain fluid and no deal is finalized until the vote is taken, the mood in Washington has shifted and a breakthrough appears increasingly likely—potentially ending weeks of fiscal drag and market volatility.

Federal contractors and air-traffic controllers remain unpaid, forcing the FAA to cut flight schedules at major hubs. Beyond the fiscal drag, the shutdown has created a data fog for the Federal Reserve just weeks before its December policy meeting. Key inflation and labor reports have been delayed, leaving policymakers to navigate without their usual instruments and relying on private data, experience and instincts.

Labor Market: Cooling, Not Collapsing

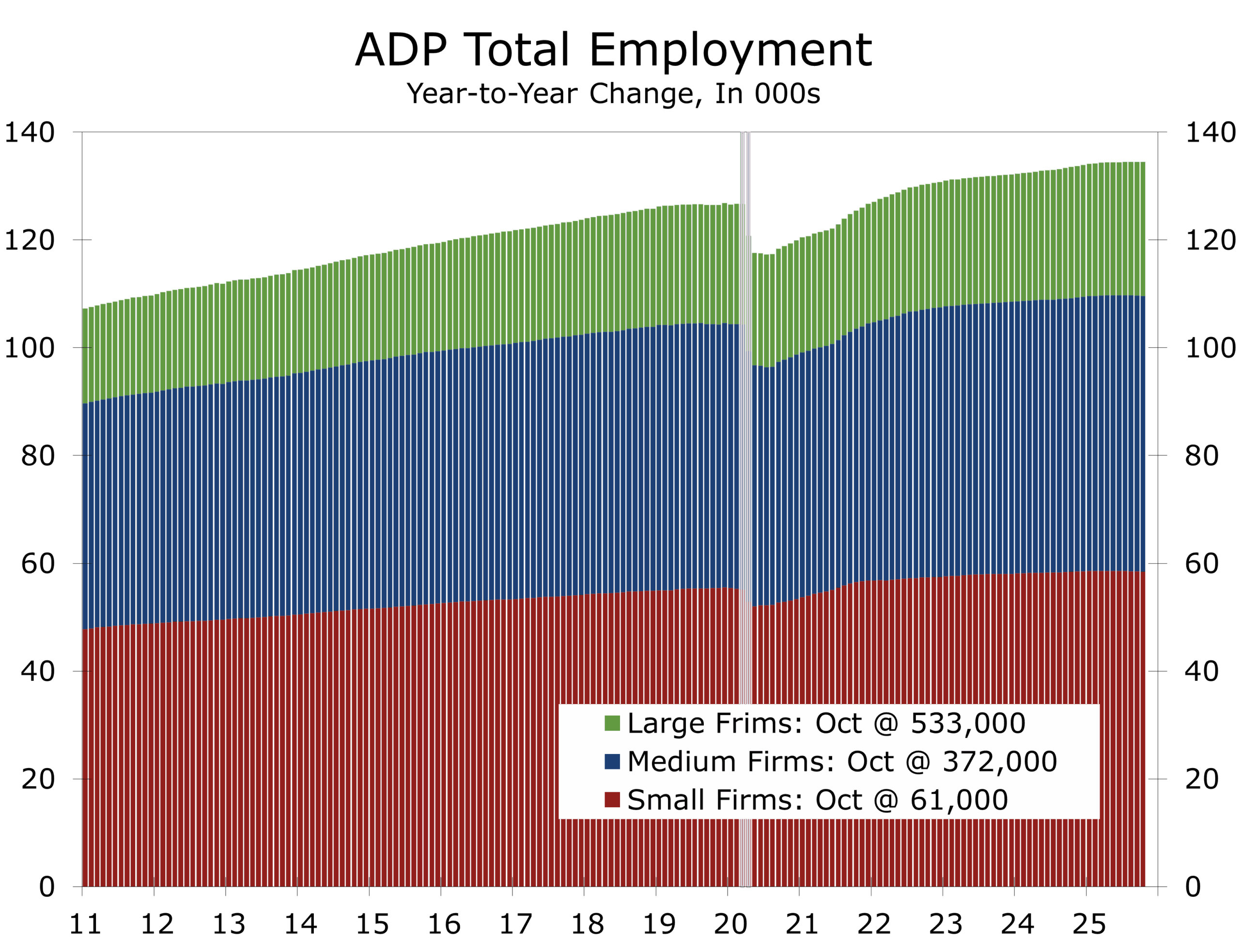

The October ADP report showed a modest 42,000 private-payroll gain—a rebound from two months of declines but well below the pre-pandemic trend. Hiring remains concentrated in healthcare, hospitality and travel-related services while professional and information industries continue to shed jobs. Small and medium sized firms have cut payrolls in five of the past six months, while large companies continue to add staff.

Depictions of a low-hire, low-firm environment may be slightly optimistic; recent data may be overstating net job growth. Productivity gains and AI-driven efficiencies are enabling firms to sustain output with fewer hires. The primary risk is not mass layoffs, but a prolonged period of stagnant hiring and more intense debate over inequality.

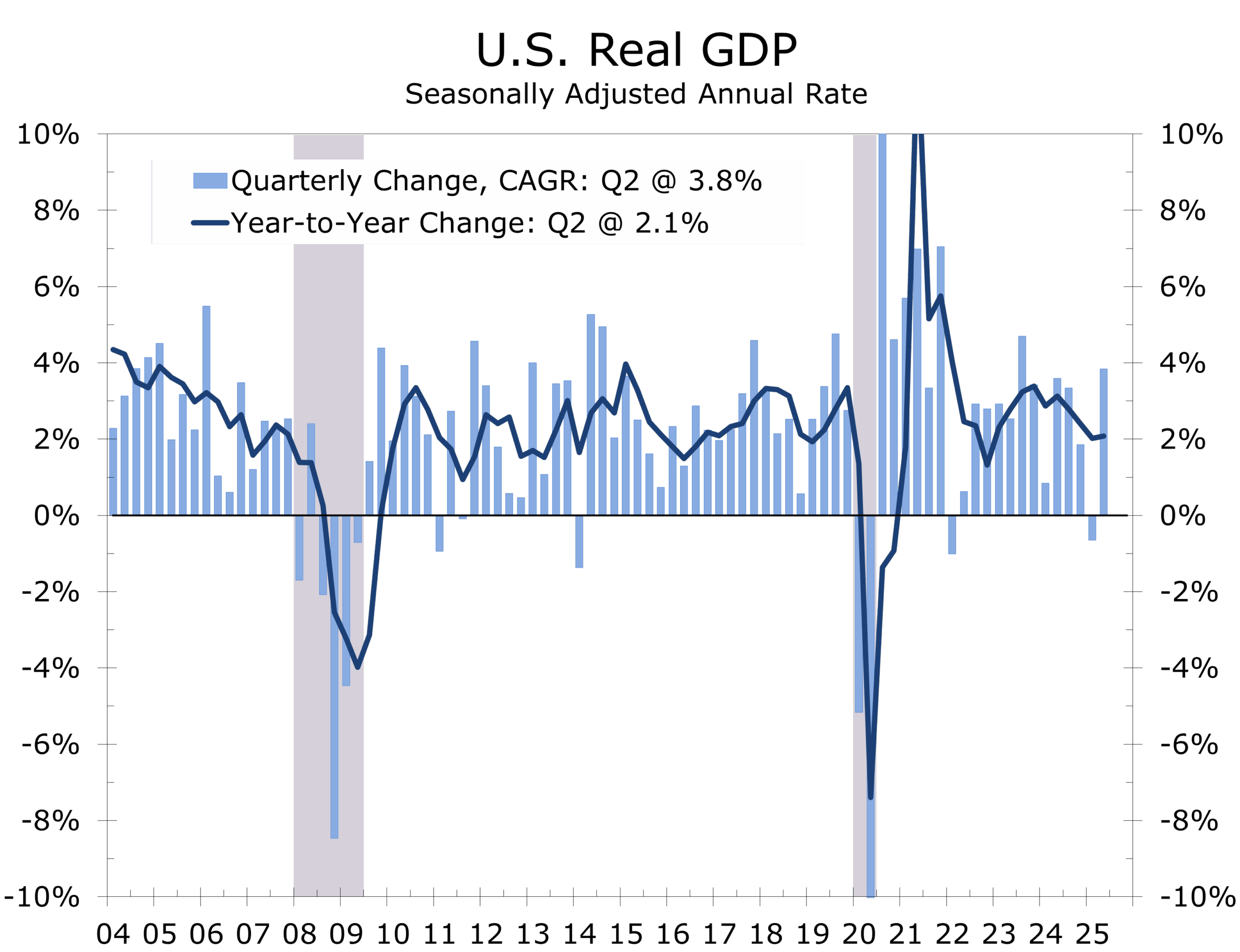

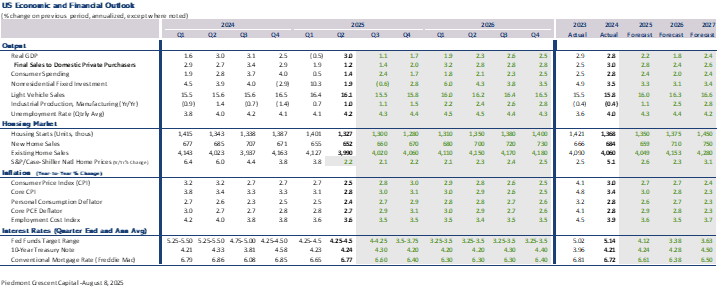

Real GDP is estimated to have risen at a 3.4 percent annual rate during Q3, while nonfarm payrolls averaged just 45,000 per month in July and August. Productivity growth is strong, but labor-force participation is slipping as attractive job opportunities become scarce, immigration slows, and policy uncertainty rises. The threshold for job growth to keep unemployment stable has fallen to roughly 45,000 per month, implying GDP can grow without meaningful job creation.

While layoff announcements spiked in October, state-level unemployment insurance filings do not reflect a generalized uptick. State-level jobless claims remain subdued at around 228,000 per week, consistent with a labor market that is cooling but not cracking. Layoff announcements typically take months to translate into job losses.

The gig economy, meanwhile, provides displaced workers opportunities to generate income while searching for a new position, reducing the impact on headline unemployment statistics.

Consumer Mood Sours

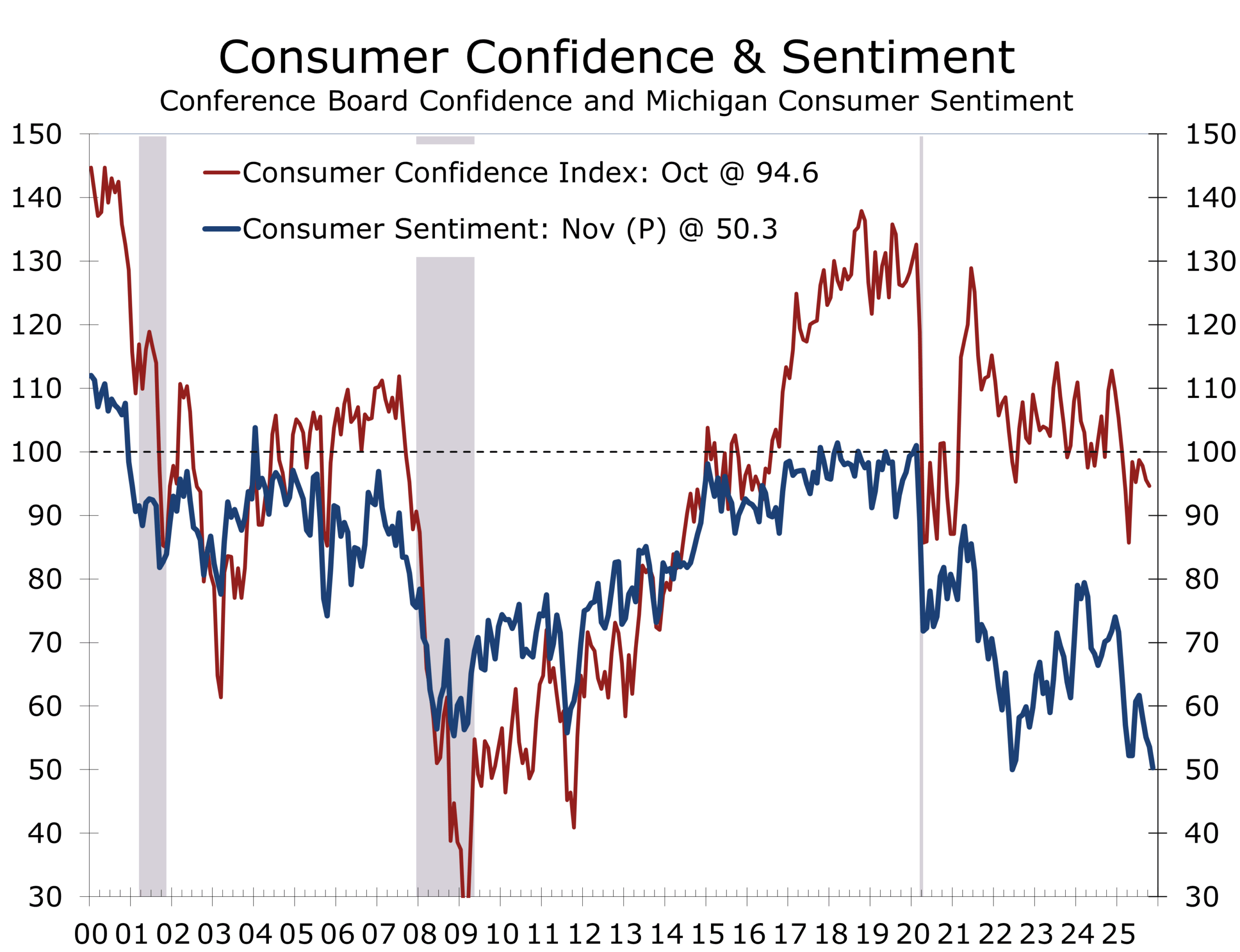

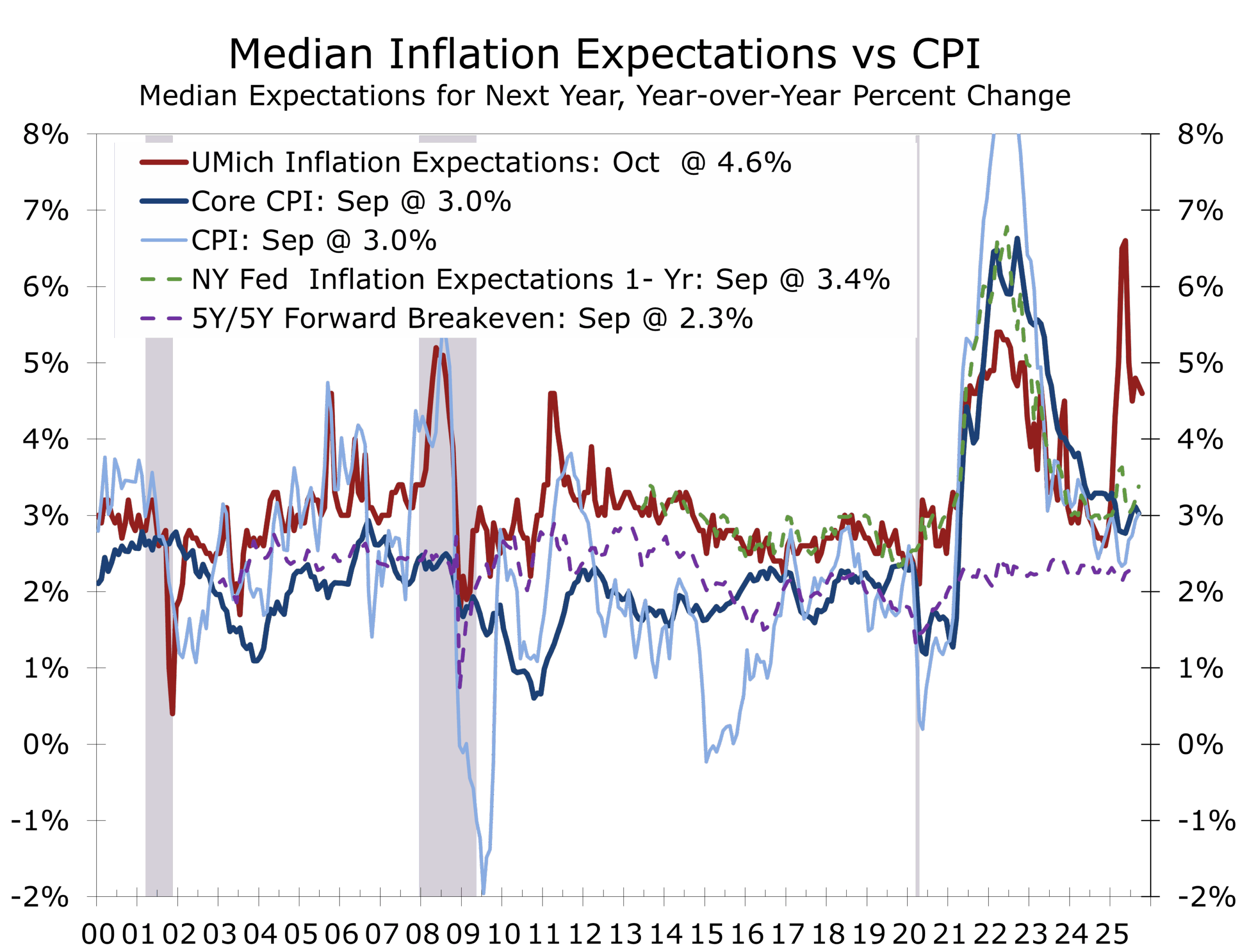

Consumer sentiment fell sharply in early November. The University of Michigan Index dropped 3.3 points to 50.3, the lowest since 2022. The decline reflects growing pessimism after the off-year elections and a deepening divide over the government shutdown. Inflation expectations remain elevated at 4.7 percent for one year and 3.6 percent over five to ten years. Notably, gasoline prices—normally inversely correlated with sentiment—fell in late October and early November.

Wealth effects sustain overall spending, even as confidence and credit use sag.

Despite weaker sentiment, the link between confidence and spending remains loose. Wealthier households, buoyed by strong equity holdings, continue to spend, while middle- and lower-income consumers face tighter credit and shrinking real incomes. Consumer credit rose $13.1 billion in September, driven primarily by student and auto loans. Revolving credit remains negative year over year, underscoring the uneven consumer base and the growing bifurcation of the U.S. household sector.

Manufacturing Still Contracting, Services Rebound

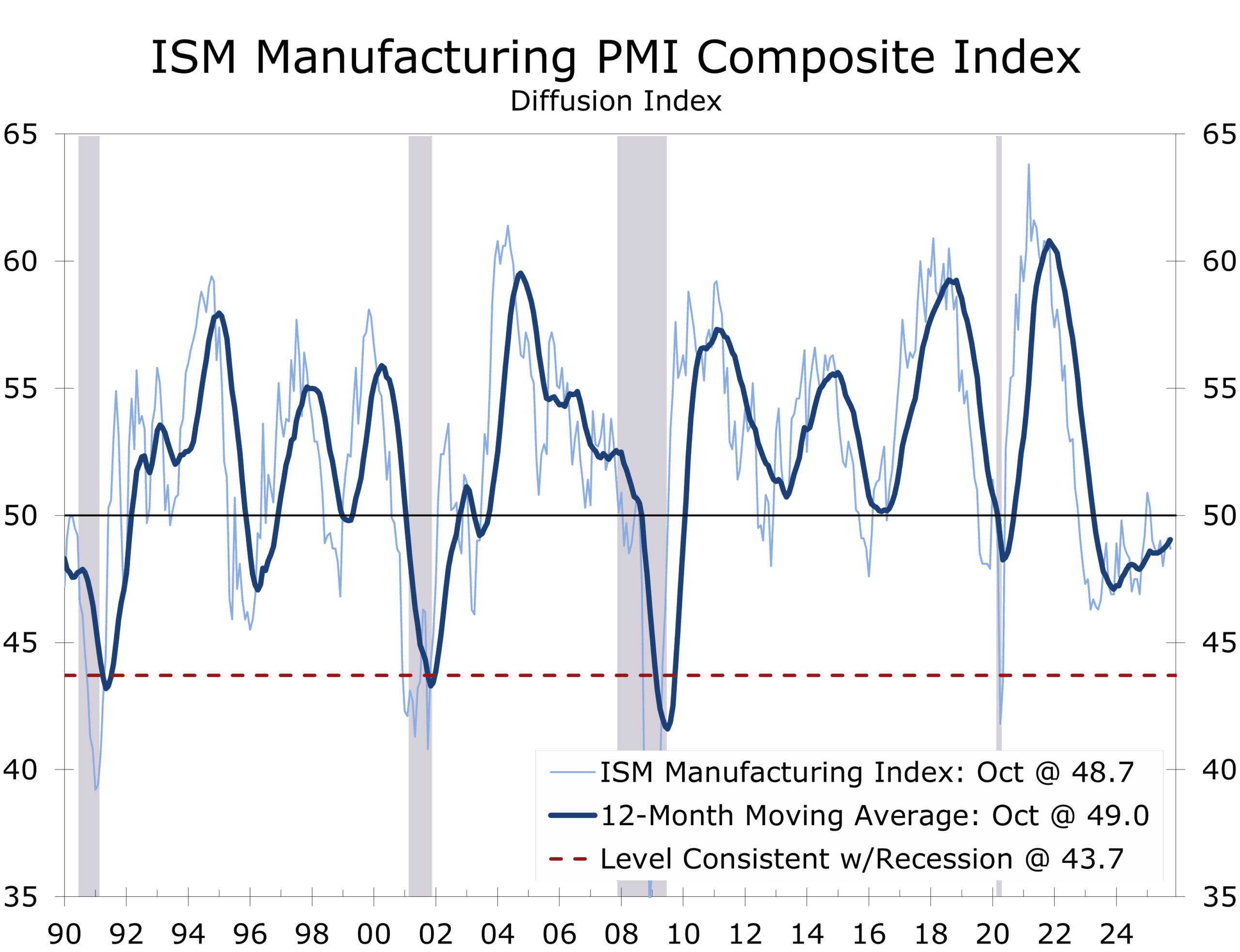

The October ISM Manufacturing Index improved modestly but remained in contraction at 48.7, its fourteenth straight month below 50. Production and new orders are still contracting, as manufacturers trim inventories. ISM Services rebounded to 52.4, driven by business activity and new orders, even as employment stayed soft. The Prices Paid Index rose to 70.0, its highest in nearly three years—a reminder that inflation pressures remain entrenched in services.

The economy appears stuck between resilient services and slowing manufacturing.

The mid-December FOMC meeting remains live, with futures markets assigning a 72 percent probability of a 25-basis-point cut. The December meeting resembles a “booth review” in football—a rate cut is the call on the field, and policymakers will need decisive evidence to overturn it, which would unsettle markets, businesses, and consumers.

With official data frozen, the Fed must weigh a softening labor market against potential inflationary effects from tariff pass-throughs. While inflation expectations have firmed, underlying measures continue to moderate. Rents are likely to remain soft through mid-2026. The jobs and hiring outlook has weakened more than expected, keeping risks weighted toward the employment side of the Fed’s mandate.

Markets: Stocks Snap Streak, Bonds Hold Ground

The stock market endured its worst week since April. The S&P 500 fell 1.8 percent, the Nasdaq lost 2.8 percent, and the Russell 2000 declined 2 percent. Selling was broad, led by technology and consumer discretionary sectors, as weak manufacturing data and mounting policy uncertainty weighed on investor sentiment. Stretched valuations in AI-related names and the worsening government shutdown contributed to a long-anticipated pullback.

Treasuries rallied sharply mid-week before yields retraced. The 10-year ended near 4.10 percent and the 2-year at 3.56 percent. Credit spreads widened modestly, and rate volatility remained high as investors moved into quality.

Gold remains around $4,100 per ounce, near its all-time high, supported by safe-haven demand and growing conviction the Fed will cut rates further. Brent crude slipped toward $64 per barrel, the lowest since early spring, after OPEC+ paused production increases amid softening global demand indicators.

Tariffs and the Court

The Supreme Court’s review of Trump-era tariffs may reshape inflation and trade dynamics. Oral arguments last week revealed most justices are skeptical of presidential authority under IEEPA to impose tariffs without Congressional approval.

Prediction markets now place the odds of the Court upholding IEEPA tariffs at 30 percent, down from 40 percent pre-argument. A decision is expected in December or January, with a closely split result probable. Our take is that the Court will rule the president overstepped, but the Administration could shift tariffs under other statutes or preserve international agreements.

Refunds to U.S. importers will likely be less than originally remitted, with payments delayed and requiring legal follow-up. The net deflationary impact may emerge gradually, via lower import costs and modest relief to corporate margins.

Alternative tariff authorities include:

- Section 122 of the Trade Act of 1974—temporary tariffs up to 15 percent

- Section 301 of the Trade Act—retaliatory tariffs for unfair trade practices

- Section 232 of the Trade Expansion Act of 1962—tariffs on national security grounds

A ruling invalidating tariffs would slightly reduce near-term inflation risk, offering some cushion for policymakers heading into 2026. Renewed use of alternative authorities could reintroduce friction, sustaining supply chain and price volatility. The decision, expected late this year or early 2026, will add another twist to the Fed’s calculus.

Geopolitics: Off-Year Elections and Global Flashpoints

Off-year elections injected more volatility into Washington’s fiscal environment. Democrats gained ground in several key states, underscoring voter frustration with living costs, affordability, and the shutdown. The results strengthen Democrats’ negotiating position in the budget impasse, increasing pressure on House Republicans to act before the economic fallout widens.

Zohran Mamdani’s upset win in New York City on a platform of rent stabilization, transit breaks, and progressive taxation sent shockwaves, prompting immediate White House response—even threats to withhold funding. The federal-local confrontation highlights tangible risks for businesses tied to contracts, infrastructure, or transit systems.

The broader political takeaway is voter fatigue with dysfunction and an emphasis on affordability and stability over ideology. Markets have noticed: the sell-off in equities and rally in Treasuries reflect the view that fiscal disarray, not inflation, is the principal near-term risk.

Russia and Ukraine

Russia’s winter offensive intensified, launching the largest strike on Ukrainian energy infrastructure since the 2022 invasion.

- 458 drones and 45 missiles struck 25 sites across four regions.

- National generating capacity temporarily dropped to zero; outages of up to 12 hours daily in Kyiv

- Civilian casualties rose; Zelenskyy appealed to allies for more Patriot air defense systems

Sanctions waivers for Hungary and continued energy purchases further strain Ukraine’s resilience. Markets remain insulated so far, with energy prices subdued. But escalation risks remain if supply disruptions resurface.

Israel, Hezbollah, and Gaza

Conflict along Israel’s northern border flared, with strikes on Hezbollah in southern Lebanon targeting elite Radwan forces. Disarmament under UN Resolution 1701 remains critical but unfulfilled, complicating prospects for lasting peace. Lebanese and Israeli experts emphasize that failure to disarm Hezbollah undercuts incentives for Hamas and impedes regional stability.

The U.S. Treasury has sanctioned Hezbollah facilitators for funneling funds from Iran. Lebanon’s economic stability now hinges in part on progress toward disarmament.

Meanwhile, Gaza remains volatile. Hezbollah’s claim of success in resistance strategy and inter-group connectivity heighten the risk of north-south escalation. For markets, the status quo is baked in, but any misstep could quickly revive regional risk premiums across energy and defense assets.

OPEC+ and Energy Politics

OPEC+ opted to hold output increases through March 2026, raising only 137,000 barrels per day in December. Weak demand—especially in Asia—drives the decision. Oil prices reflect the freeze, with Brent crude in the low-$65 range and WTI at $61–62. The cartel’s strategy favors stability over spikes, aligning with fiscal stress and rising inventories.

Other Global Flashpoints:

- China: The Fifteenth Five-Year Plan signals more regulation over stimulus, weighing on equities.

- Iran: Intensified uranium enrichment sets the stage for future negotiations.

- Taiwan/Pacific: U.S. naval patrols continue, but risk of confrontation remains muted.

Strategy Watch: For CFOs and Treasurers

- Liquidity and Funding: Volatility in equities and steady Treasury yields present an opportunity to term out short-term debt before year-end. Curve remains slightly upward-sloping; locking in spreads provides insurance ahead of potential rate cuts.

- Cash and Investment Policy: Money-market yields have eased to 3.8–3.9 percent. Ladder Treasury bills and short-duration agencies to preserve liquidity and reduce reinvestment risk.

- Credit and Counterparty Risk: Spreads have widened modestly but remain tight by historical standards. Reassess supplier and customer credit exposure, especially for small or trade-exposed counterparties.

- FX and Commodities: Unwind euro hedges partially; maintain yen protection and update commodity-linked hedges for current price levels.

- Capital Spending and Planning: Expect slower Q4 cash flow, reflecting delayed federal contract payments. Maintain caution on discretionary capex until visibility improves in later this year and in early 2026.

The Week Ahead: November 10–16

Key indicators will remain limited by delayed federal releases. Focus on NFIB small business optimism, Fed speeches, weekly jobless claims, and pre-meeting remarks from Atlanta Fed President Bostic and Kansas City’s Schmid for insight into the Fed’s December outlook.

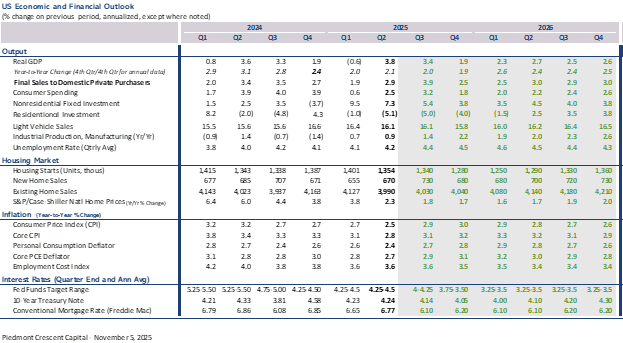

The economy is expected to post 3.4 percent real GDP growth for Q3 and to slow to just under 2 percent in Q4, with momentum increasingly reliant on consumer services and exports as hiring and credit conditions tighten.

Markets begin the week on a firmer footing. The 10-year Treasury yield jump back up to 4.15 percent on optimism that the government shutdown is nearing resolution before settling back in at 4.10. Equities look set to rebound, and the dollar remains mixed, reflecting improved fiscal sentiment but ongoing uncertainty about the Fed’s next move.

For CFOs, treasurers, and other decision makers: liquidity first, duration second, discipline always. Use near-term optimism around a fiscal resolution to lock in funding and reassess exposures—while remembering that the underlying structural issues remain unsettled.

The economy is still moving forward, but the composition of growth is shifting. Productivity, not payrolls, is now driving the expansion. The Fed faces a complex policy decision on a short timetable, and markets and business leaders are adjusting to a slower, leaner phase of growth.

In this environment, balance-sheet discipline and liquidity flexibility are the best tools—and staying opportunistic will be the edge as the market recalibrates around the next policy turn.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 10, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

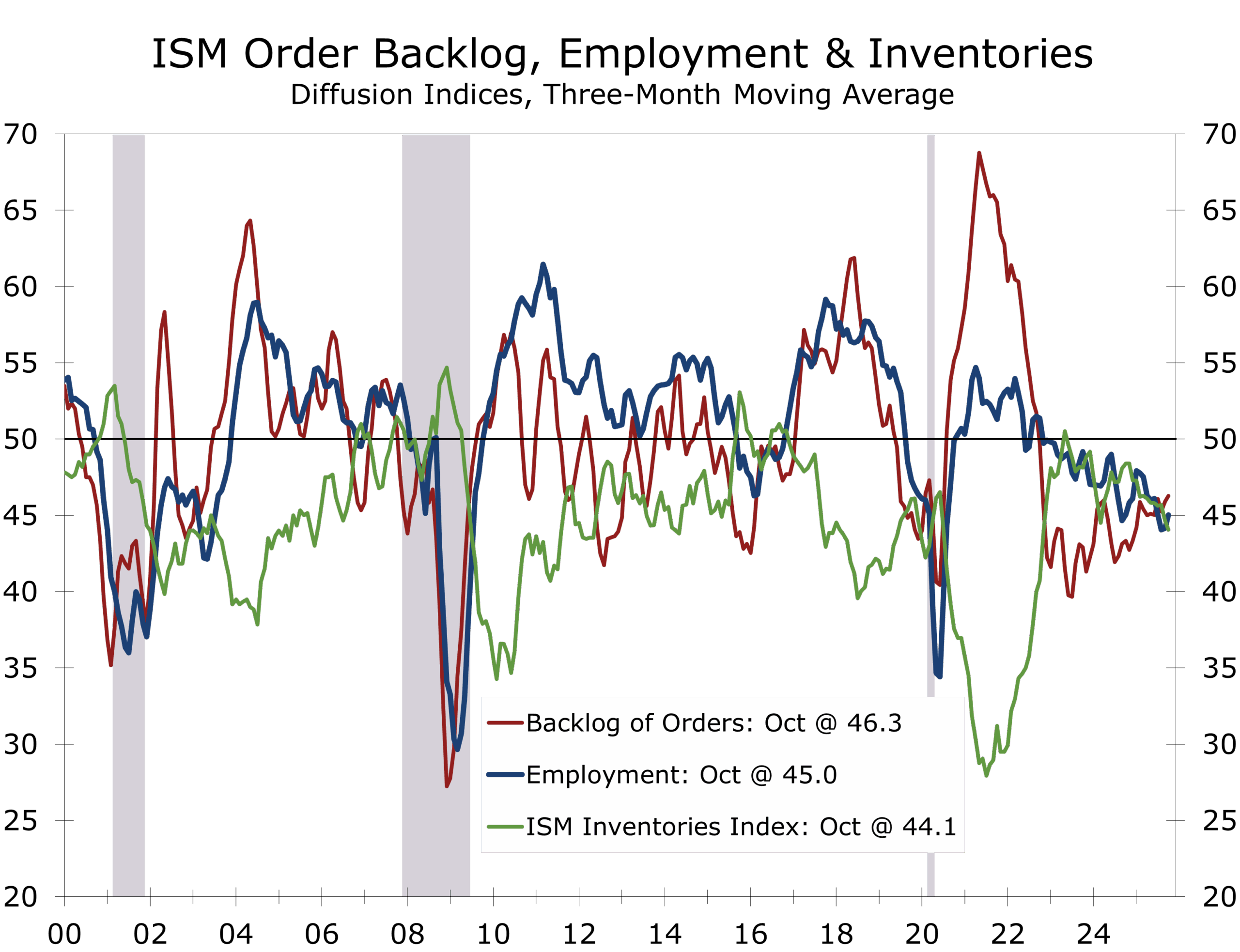

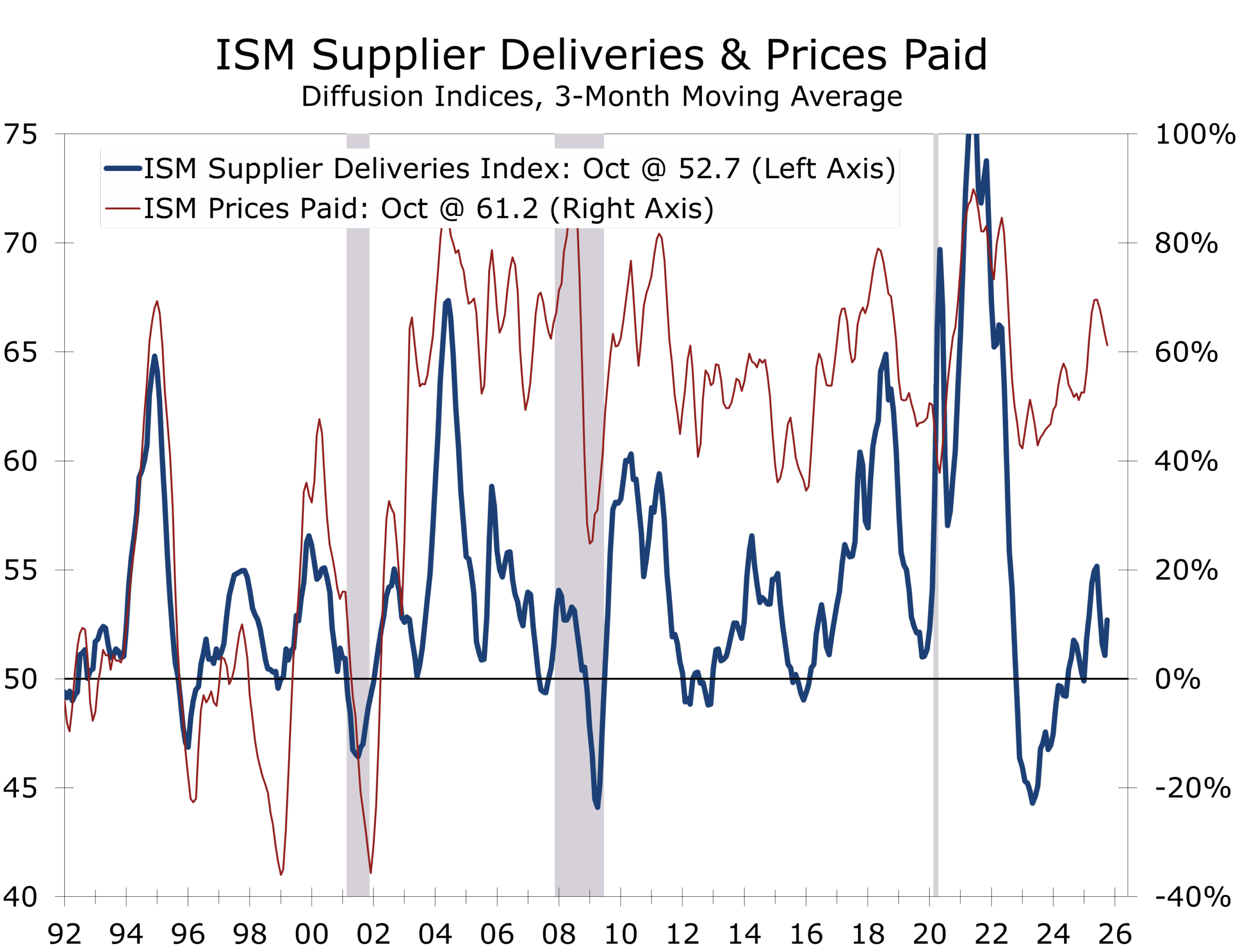

October ISM Manufacturing: Uncertainty Is Increasingly Weighing on Manufacturers

Manufacturers Are Playing Defense

-

- ISM Manufacturing Index: 48.7 (–0.4) — signals the eighth straight month of contraction and a widening breadth of weakness across U.S. manufacturing.

- Production: 48.2 (down from 51.0) — slipped back into contraction after a brief September rebound.

- New Orders: 49.4 (up from 48.9) — second straight month below 50, still reflecting soft demand.

- Employment: 46.0 (+0.7) — ninth month of contraction as manufacturers continue managing headcount leanly.

- Supplier Deliveries: 54.2 (+1.6) — slower deliveries for a third month, consistent with stabilized but subdued activity.

- Customers’ Inventories: 43.9 (+0.2) — still “too low,” implying potential for restocking once confidence improves.

- Prices Paid: 58.0 (–3.9) — still elevated but easing from September’s 61.9, indicating slower input cost inflation.

- Exports: 44.5 (+1.5) — contracting for an eighth consecutive month.

- Imports: 45.4 (+0.7) — seventh month of contraction as tariff pricing dampens activity.

- Backlog of Orders: 47.9 (+1.7) — modest improvement, but still in contraction.

The ISM Manufacturing PMI® registered 48.7 in October, down 0.4 points from September, marking the eighth consecutive month of contraction following a brief reprieve earlier this year. As a diffusion index, readings below 50 mean that more firms report worsening rather than improving conditions — a measure of breadth, not magnitude.

Production fell 2.8 points to 48.2, returning to contraction territory—meaning more firms reported output decelerating rather than accelerating—after just one month of growth. New Orders (49.4) and Employment (46.0) both edged higher but remained below 50, indicating continued weakness in order flow and hiring. Inventories were drawn down more sharply, while supplier deliveries lengthened modestly. Notably, all four demand components—New Orders, New Export Orders, Order Backlogs, and Customers’ Inventories—improved slightly, though each remains in contraction. Overall, the index remains consistent with modest economic growth, and we believe it is uncertainty, more than demand softness, that is weighing on manufacturer sentiment.

The Uncertainty and policy volatility, not collapsing demand, continue to weigh on manufacturing.

Manufacturing weakness in October was broad-based but not especially severe, with about 58% of manufacturing GDP contracting and 41% in strong contraction (PMI® ≤ 45).

Panelists repeatedly described a cautious tone. Two-thirds of respondents indicated they are still managing headcount, not hiring. Most are adjusting production schedules to match slower demand and are reluctant to rebuild inventories or add capacity. Even as backlogs ticked up, they remain historically low — a sign that order pipelines are not refilling.

Firms are operating in risk-management mode, focused on flexibility, liquidity, and cost control.

Tariffs and Policy Volatility Weighing on Risk Taking

Uncertainty appears to be weighing on a growing proportion of manufacturers. ISM respondents cited the tariff environment, the recent government shutdown, and heightened geopolitical and policy uncertainty as key factors shaping business behavior.

Companies report cancelled or reduced orders due to shifting trade policies and reciprocal actions from China, such as export controls on rare earths and semiconductors. Firms in machinery, chemical products, and fabricated metals highlighted how the unpredictability of tariffs is disrupting cost planning, margin management, and investment decisions.

This climate has fostered a “wait-and-see” mindset. As one respondent put it, “Money is sitting tighter, and geopolitical changes add to the uncertainty/risk factor.” Across multiple industries, that sentiment is translating into leaner operations, reduced overtime, and tighter working-capital discipline.

.

Input Prices Remain Elevated but Easing

The Prices Paid Index fell 3.9 points to 58.0, marking the 13th consecutive month of increases but at a slower rate. Price pressure remains concentrated in metals — particularly steel, aluminum, and copper — and in tariff-affected imports. Fewer respondents reported rising costs (27 percent versus 33 percent in September), suggesting that input inflation is decelerating, even as overall price levels remain high.

This backdrop supports ISM’s observation that cost stickiness and margin compression continue to weigh on capital spending and hiring. Manufacturers are prioritizing balance sheet preservation over expansion.

Manufacturers are preserving liquidity and awaiting policy clarity before restocking or rehiring.

Inventories and Demand Indicators: “Too Low,” Yet Still Too Risky to Rebuild

Customer inventories stayed in “too low” territory at 43.9, which historically signals potential for future restocking. However, panelists remain hesitant to respond — instead choosing to operate lean amid uncertain end-market demand.

Inventories fell more sharply (45.8), and order backlogs, while modestly higher, remain in contraction. These dynamics reinforce a theme of defensive stock management rather than preparation for renewed growth. Until confidence strengthens, restocking may continue to lag underlying consumption.

Sector Breadth and Structural Takeaways

Only Food, Beverage & Tobacco Products and Transportation Equipment expanded in October, reflecting stable consumer demand, and solid aerospace activity and defense orders. Most other industries — including machinery, chemicals, fabricated metals, and electronics — saw broad-based declines, confirming that the softness is systemic rather than isolated.

The ISM estimates that the October PMI corresponds to roughly +1.8% annualized real GDP growth, indicating that while manufacturing is contracting, it has not dragged the broader economy into decline. Still, the diffusion of weakness across 12 industries warrants close monitoring as policymakers balance corralling inflation with sustaining growth momentum.

The October ISM Manufacturing Index reinforces our assessment that policy uncertainty—not just soft demand—is the primary headwind facing U.S. manufacturing. The latest data show a sector leaning hard on cost control and liquidity preservation as confidence remains clouded by tariffs, fiscal volatility, and geopolitical friction.

Customers and producers alike are running lean and deferring restocking or rehiring until visibility improves. While the index does not point to a collapse in output, the breadth of contraction has widened, signaling a slow, grinding adjustment phase rather than an outright downturn.

The combination of lean inventories, early signs of easing price pressures (-3.9 points to 58.0 in October), and pent-up replacement demand suggests the groundwork for eventual stabilization. For now, however, the prevailing mood is caution. Unless the policy environment steadies, manufacturers are likely to remain defensive through year-end, waiting for clearer signals before committing to renewed production growth.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 3, 2025

Mark Vitner, Chief Economist

(704) 458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Balancing Diligence and Stability

Highlights of the Week

- The Fed cut the funds rate by 25 bps to 3.75–4.00%, but Powell’s warning that “a December rate cut is not a foregone conclusion” caught markets off guard.

- Front-end yields rose 10–12 bps as traders recalibrated expectations; the dollar firmed and equities ended mixed.

- The latest CPI print continues to germinate across markets and policy circles, with shelter costs and core inflation moderating.

- Consumer confidence held steady at 94.6, showing households are adapting rather than retreating.

- Labor markets continue to cool: initial claims hover near 219,000, while ADP’s new weekly series shows modest but positive hiring.

- Across the Piedmont and the broader South, AI infrastructure, aerospace, shipbuilding, pharmaceuticals and energy investment keep regional growth above trend.

- In Texas, factory activity expanded modestly in October while service and retail sectors contracted further, highlighting the uneven nature of the slowdown.

- Globally, Trump’s Southeast Asia tour and the Busan APEC summit produced a fragile U.S.–China truce — a pause in tariff and rare-earth escalation, not a durable peace — while global central banks signal policy stability.

U.S. ECONOMY & FINANCIAL MARKETS

The Federal Reserve’s October 29 decision marked a shift from momentum to management. Policymakers trimmed the funds rate by 25 bps to 3.75–4.00% and emphasized that policy “is not on a preset course,” reflecting both the committee’s divisions and the information gaps created by the continuing government shutdown.

A measured cut, anchored yields, and a reminder: policy is not on a preset course.

The shutdown itself, now the longest on record, has had limited near-term market impact. Senate leaders have rejected calls to repeal the filibuster rule, virtually guaranteeing its survival and ensuring that fiscal legislation will remain constrained. While the shutdown is likely to end before Thanksgiving, its political fallout has kept Washington’s focus narrow, limiting fiscal risk in the near term.

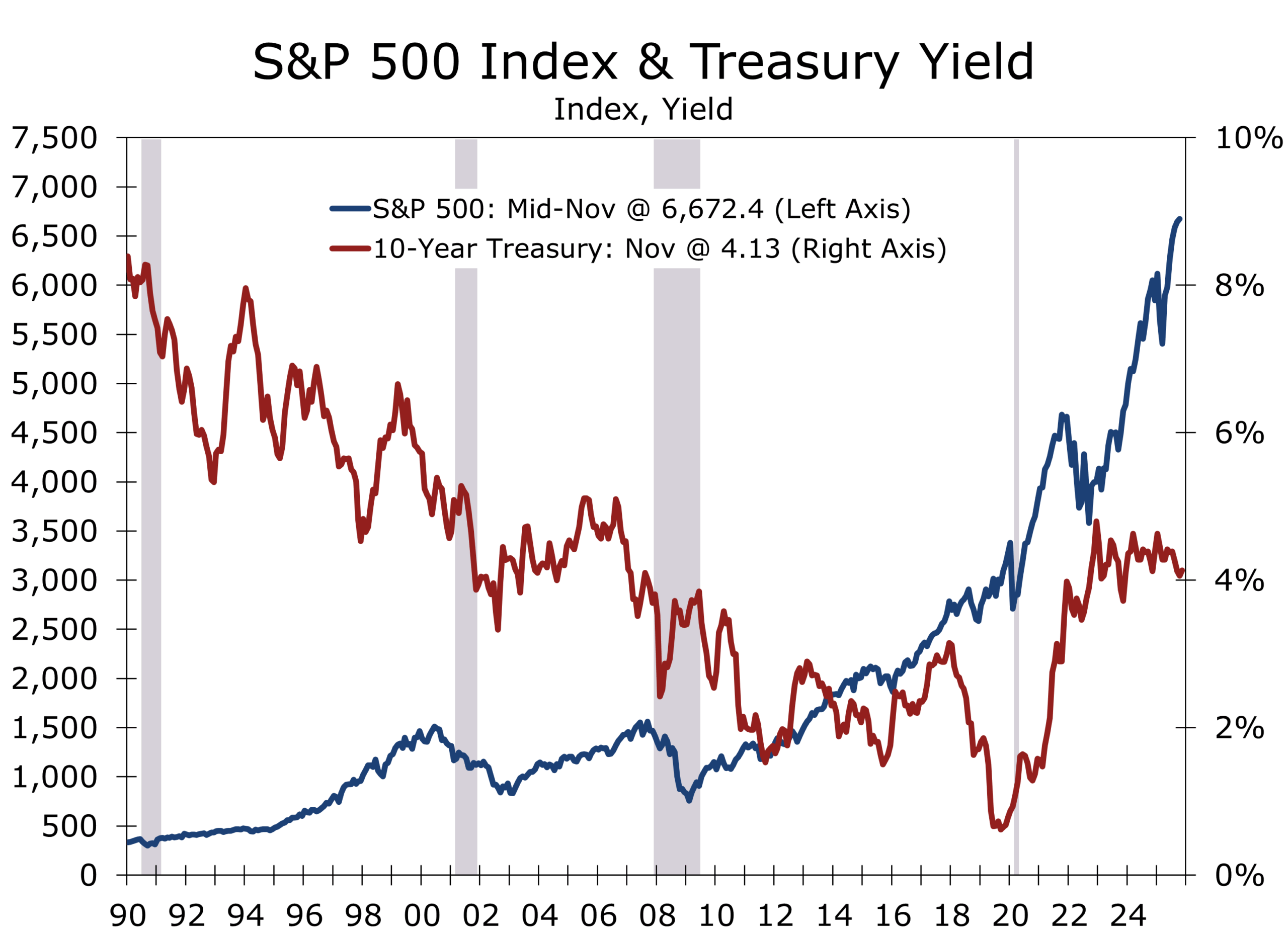

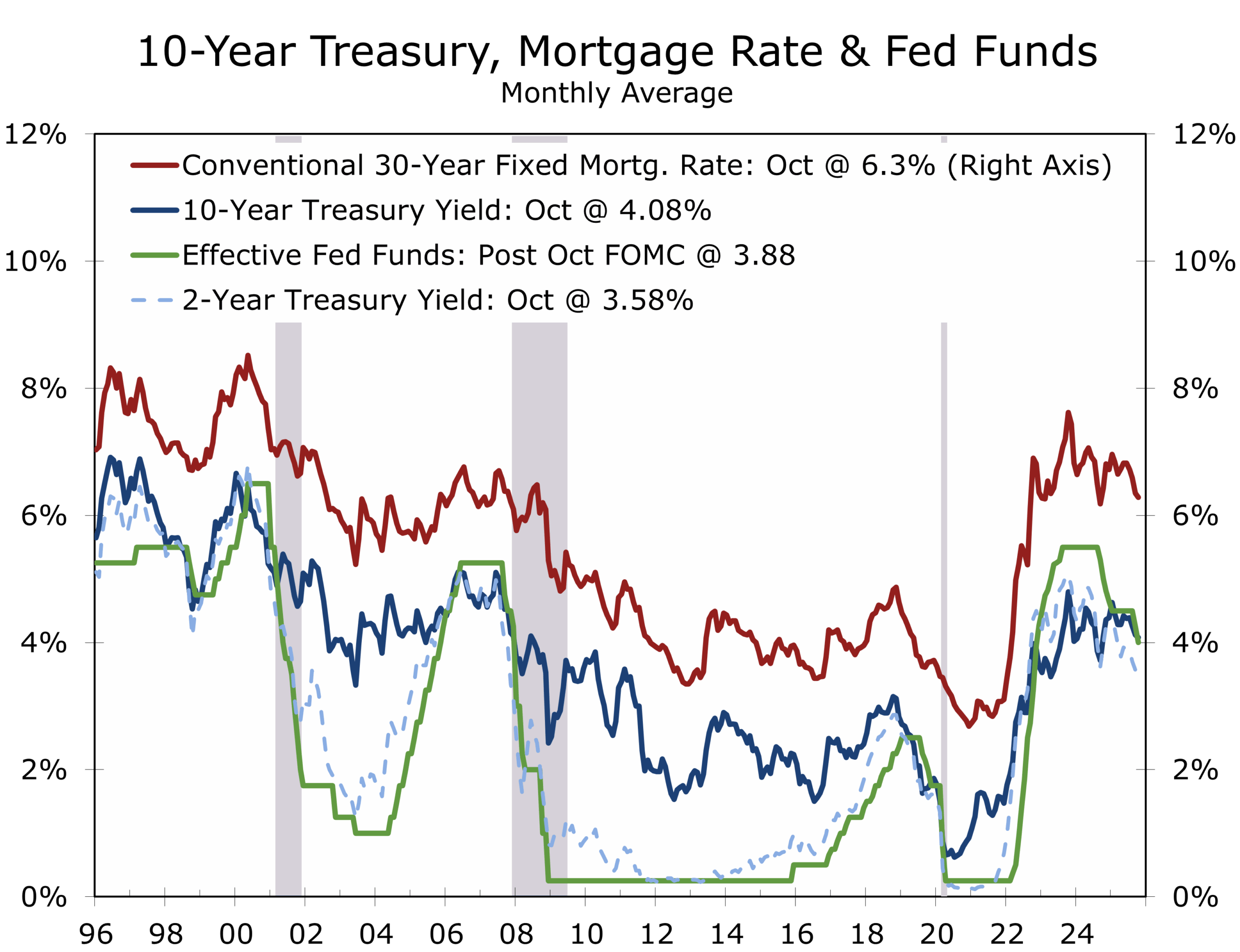

Markets reacted swiftly: the two-year Treasury yield rose to about 3.6%, the ten-year moved back above 4% and ended the week near 4.10%. The S&P 500 gained roughly 0.5%, supported by solid Q3 earnings and increased capex guidance from the major AI and cloud “hyperscalers.”.

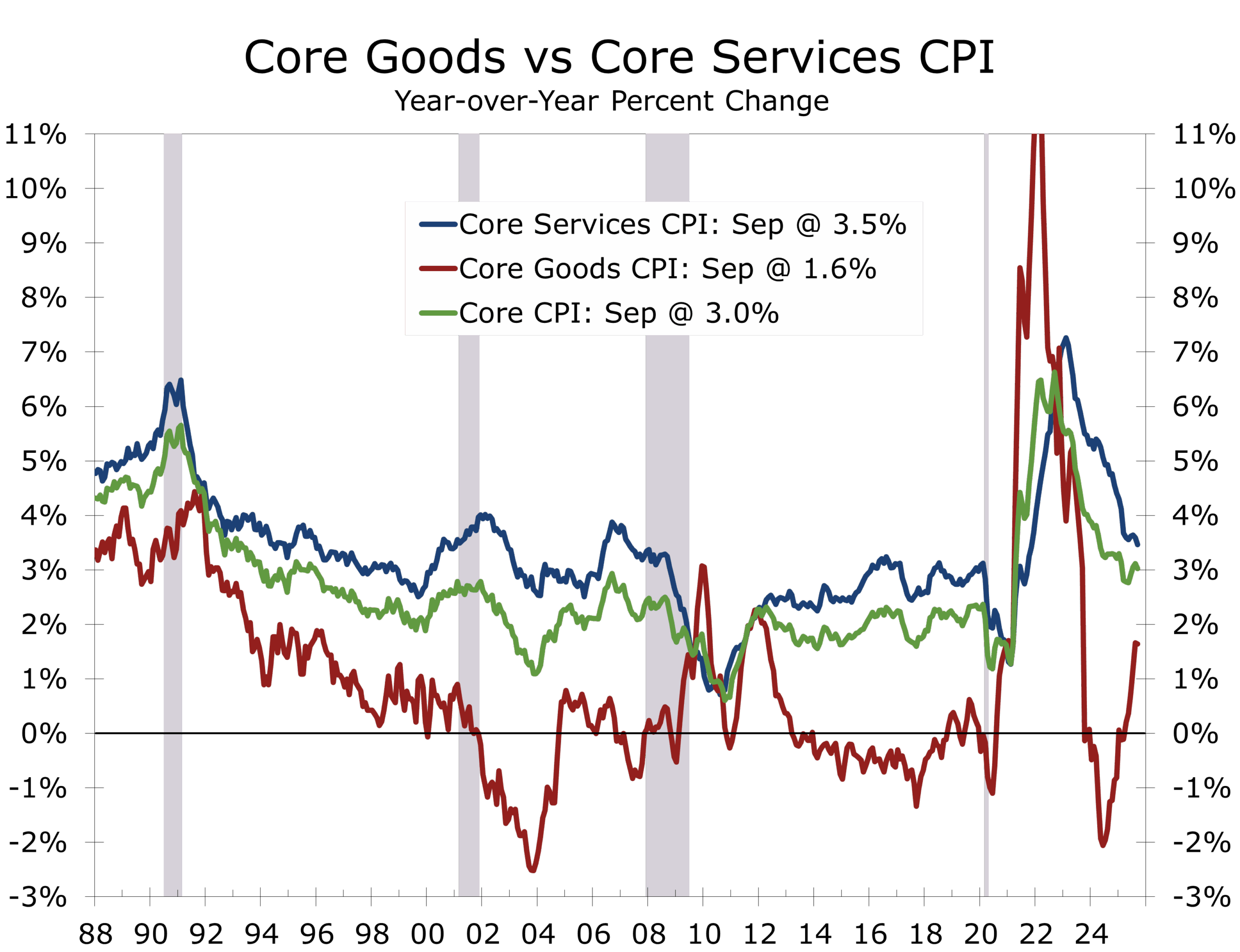

The latest CPI print continues to germinate across markets and policy circles. Core CPI rose 0.2% in September, with shelter’s contribution the smallest since 2021. While some worry the softening may be temporary, private-sector data show rent concessions rising, especially in the South. Headline CPI and core PCE are on pace to finish the year near 3% and to ease toward 2½% by late 2025, giving the Fed room to cut gradually without re-igniting demand.

Consumers remain resilient. The Conference Board confidence index held at 94.6 despite the shutdown, and the “jobs plentiful minus jobs hard to get” spread stabilized — a sign of adaptation, not collapse.

Labor data confirm that cooling, not collapse, is underway. Jobless claims hover just above 219 k, the Chicago Fed’s real-time unemployment measure sits near 4.35%, and ADP’s weekly series shows modest private-sector gains — all consistent with a soft landing.

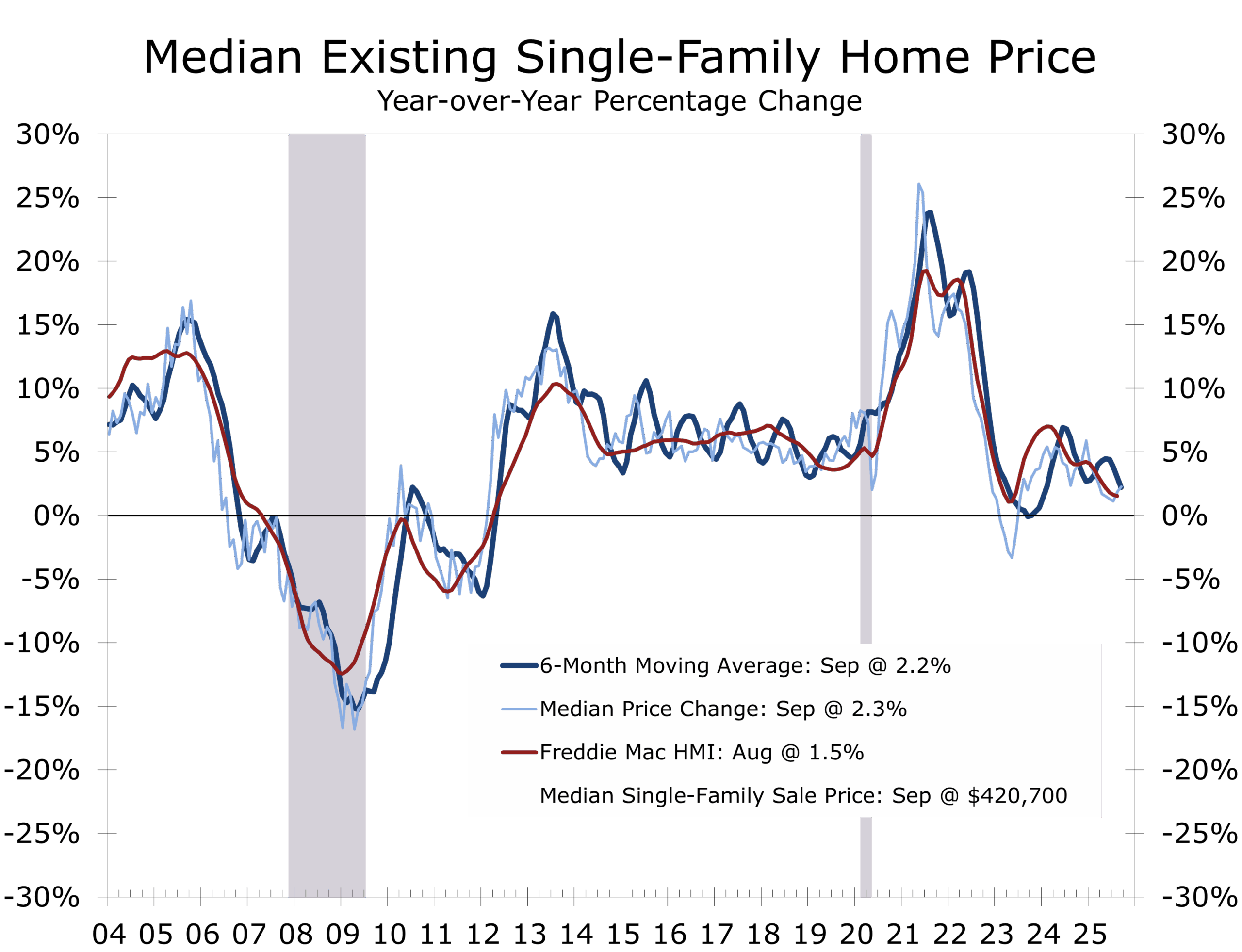

Housing is showing tentative signs of revival. The Case-Shiller index rose 0.2% in August — its first monthly gain since winter — as inventories normalized and sellers re-entered the market. Price growth has slowed to 1½% y/y but appears stable through year-end.

Dallas Fed surveys show a mixed regional picture — steady factory output but service and retail weakness. Manufacturing’s production index held at 5.2 with new orders (–1.7) and capacity utilization (–1.1) softening. Business sentiment remained slightly negative (–5.0) while employment rose marginally (2.0) and hours worked fell (–5.5). Services contracted again (revenue –6.4, employment –5.8), and retail sales fell sharply (–23.5). Overall, industrial and capital-intensive sectors remain firm while consumer-facing industries absorb the slowdown.

The Piedmont Crescent

The Piedmont Crescent — stretching from Birmingham and northern Alabama through Atlanta and up through the Carolinas and Virginia to the D.C. area — continues to outperform the nation.

Atlanta’s logistics and technology corridors are expanding, Charlotte’s finance and manufacturing bases remain steady, and Raleigh–Durham’s research and biotech clusters attract sustained venture capital. Greensboro and the Triad are emerging as electric-vehicle and aerospace hubs, while Richmond and Northern Virginia benefit from defense and data-infrastructure investment.

Migration, population growth, and corporate relocations keep housing active even as national demand cools. Infrastructure upgrades and energy-grid projects continue to anchor industrial expansion.

The Broader South

The South remains the nation’s growth engine. Texas leads in energy and semiconductors, Florida’s tourism and construction expand despite affordability strains, and Tennessee and Alabama capitalize on EV and aerospace investment.

South Carolina’s ports and manufacturing hubs run near capacity, Louisiana and Mississippi advance grid-modernization and petrochemical projects, and shipbuilding along the Gulf Coast — from Mobile to Pascagoula and into New Orleans — is gaining momentum on Navy, Coast Guard, and commercial orders. Together, these trends keep Southern output well above national averages even as the broader economy slows.

Outside the Region

The Midwest’s industrial renaissance continues through chip fabrication and EV supply-chains. The West Coast is stabilizing after a year of tech layoffs as AI capex revives growth from Seattle to San Jose.

Major markets in the Northeast received a boost this year from the return to the office, which also boosted retail trade and the hospitality sector. Financial services have also had a strong year. Divergences across regions are widening, however, a classic late-cycle phenomenon.

Outside the Country — The APEC and ASEAN Circuit

President Trump’s Southeast Asia trip dominated the week’s geopolitical landscape. Visits to Thailand, Malaysia, Cambodia, and Vietnam produced agreements on critical-minerals cooperation and supply-chain diversification.

At the APEC summit in Busan, the U.S. and China announced a one-year truce without teeth — the U.S. cut tariffs tied to fentanyl from 20% to 10% in exchange for Beijing committing to reduce precursor shipments and crack down on the fentanyl trade in general. In addition, China will resume soybean and energy purchases, and suspend rare-earth export curbs for a year. Tariffs on most other goods remain high, and no progress was made on Taiwan or Russia ties.

A fragile détente steadies markets but leaves rivalries intact.

The U.S.–South Korea defense accord was another notable development, allowing Seoul to purchase or jointly develop a nuclear-powered submarine using U.S. technology to be built in a U.S. yard with Korean investment — a move anchoring the peninsula more firmly within the Indo-Pacific security framework. An added plus: Korean investment might also help bolster the U.S. shipbuilding industry.

Europe appears to be settling into a soft landing. The ECB kept rates at 2% for a third meeting, while the Bank of Canada also paused after its cut. The Bank of Japan remains on track to raise to 0.75% by year-end, though Prime Minister Takaichi may delay if data soften. Global policy tone is one of hawkish stability — fine-tuning after a year of adjustment.

Risk tone brightened as Washington and Beijing reached a provisional framework pausing threatened 100% tariffs and rare-earths export curbs—pending Trump–Xi leader sign-off later this week. President Trump said he expects to “come away with a deal,” with China delaying export bans and boosting U.S. soybean purchases—tactically easing AI supply-chain stress and trimming term-premium risk.

Oil prices have stabilized near the low-$60s for WTI and mid-$60s for Brent as higher U.S. output offsets Middle-East risk and sluggish European demand. Argentina’s Javier Milei scored a decisive election victory that reinvigorated market-friendly reform momentum across Latin America. Globally, the backdrop remains one of managed fragility — diplomacy buying time for markets without resolving underlying rivalries.

Policy and Market Wrap-up

Regional Fed surveys paint a mixed picture: Richmond at –2, Dallas and Kansas City showing softer orders, and Atlanta’s business-inflation expectations slipping to 2.5%. Markets now price one more 25-bp cut by January, consistent with a soft-landing baseline.

Private-credit markets are also entering a more discerning phase as the “ghosts of 2020–2021 vintages” resurface. Select distress is emerging in legacy loan books, while AI-linked direct-lending remains active. Alternatives investors are turning more defensive — upgrading infrastructure and ports, re-entering senior housing, and keeping hedge-fund allocations tilted toward global macro.

Credit spreads remain tight, volatility subdued, and equity leadership concentrated in capital-intensive sectors — AI, energy, aerospace, and defense. Next week’s ISM and NFIB surveys will test whether late-year momentum can carry into 2026.

Bottom Line

The U.S. economy continues to evolve rather than erode. Inflation is cooling, labor markets are rebalancing, and policy is shifting from restraint to fine-tuning. Across the Piedmont and the South, industrial investment and migration remain core drivers. Abroad, diplomacy has bought calm but not certainty. Another showdown awaits.

Markets Exhale Amid Persistent Rivalry

The headlines out of Busan were celebratory, but the subtext was cautionary. The temporary U.S.–China thaw — the cut in fentanyl-related tariffs to 10% in exchange for Beijing reducing precursor shipments, the resumption of soybean trade, and a one-year suspension of rare-earth export restrictions — amounts to a cease-fire, not reconciliation.

The U.S. and China have stepped back from escalation, not rivalry.

Behind the smiles and handshakes lies a strategic recalibration rather than surrender. Both nations are buying time: Washington to shore up domestic supply chains through ASEAN partnerships, Beijing to manage capital flight and maintain export leverage. The détente narrows downside risk for AI-driven capex and commodity markets yet underscores how interdependence remains both weapon and weakness.

History suggests that pauses like this often precede a new phase of competition. The world’s two largest economies have stepped back from escalation but not from rivalry. For now, markets can exhale — but they would be wise not to forget to keep their running shoes on.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 2, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

October 28-29 FOMC Meeting Recap: The Fed Cuts Again — Balancing Diligence and Destination

The Fed’s Mission: Find a Way to Balance Rising Risks at Both Ends of the Mandate

- Decision: The Federal Reserve cut the target range for the federal funds rate by 25 bps to 3.75–4.00%, marking a second consecutive reduction as policymakers sought to buffer a cooling labor market and maintain financial stability.

• Liquidity Management: The Fed announced it will halt balance sheet runoff on December 1 and begin reinvesting proceeds from maturing MBS into Treasury bills, effectively restarting limited Treasury purchases to preserve market liquidity.

• Tone: The statement acknowledged that “downside risks to employment rose in recent months,” while inflation “remains somewhat elevated.”

• Context: The decision was complicated by the federal government shutdown, which limited access to official data and forced reliance on private-sector indicators.

• Dissents: Governor Stephen Miran favored a 50 bp cut; Kansas City Fed President Jeffrey Schmid preferred no change. The split underscores the uncertainty about how much economic activity and job growth have slowed and how much more tariffs will add to headline inflation.

• PCC View: We expect quarter-point cuts in both December and January, with the funds rate bottoming at 3.125% in Q1. The Fed may opt to skip a meeting, however, which would extend the duration of the easing but not the depth. Core PCE inflation should end 2025 near 2.5%, down from around 3% this year. Economic growth is expected to strengthen next year, eliminating the need for a more dramatic easing.

Policy Decision and Statement

The Federal Reserve lowered the federal funds rate by 25 basis points to 3.75–4.00%, citing a “shift in the balance of risks” toward weaker employment. The statement described economic activity as expanding at a “moderate pace,” but noted that job gains have slowed and the unemployment rate has edged higher.

Inflation was said to have “moved up since earlier in the year and remains somewhat elevated,” language suggesting concern about price stickiness but confidence that inflation pressures will subside over time. The Committee acknowledged elevated uncertainty and reaffirmed it would “carefully assess incoming data” ahead of any further adjustments.

The Fed needs to find a way to balance rising risks at both ends of its mandate.

The policy statement also confirmed that the Fed will conclude its balance sheet runoff on December 1, marking the end of quantitative tightening and a shift to full reinvestment of maturing securities, primarily into short-dated Treasuries. This reflects concern about tightening liquidity conditions and the Fed’s longstanding commitment to maintaining “ample reserves.”

The operational shift is a technical but meaningful adjustment. By reinvesting MBS proceeds into Treasury bills, the Fed will maintain the size of its balance sheet while subtly improving liquidity in the front end of the curve

Recent strains in money markets—compounded by the government shutdown’s disruption of Treasury issuance—prompted the move. Powell and key officials have been explicit that this is not a return to quantitative easing, but rather a precautionary step to stabilize short-term funding markets and prevent another repo-style disruption.

This balance-sheet decision complements the rate cut: one addresses the cost of money; the other ensures the availability of money.

FOMC members will likely have a wider range of forecasts for growth, inflation and rates.

The 10–2 vote revealed the most ideologically divided Committee since the pandemic era.

- Governor Stephen Miran, who again dissented in favor of a 50 bp cut, is effectively playing the role once held by the Vice Chair—serving as the public voice of the Administration and advocating a faster easing pace to support employment.

- Kansas City Fed President Jeffrey Schmid, who voted against any rate cut, reflects the Kansas City Fed’s long-standing hawkish tradition, shaped by its historic focus on price stability and commodity-related inflation risks.

This dual dissent—from opposite ends of the policy spectrum—highlights the Fed’s internal balancing act: navigating slowing job growth without reigniting inflation or appearing politically influenced.

The government shutdown has limited official data, forcing policymakers to rely on alternative sources such as ADP, Homebase, and private job postings, which collectively suggest the labor market is weakening faster than the headline numbers imply.

At the same time, business investment remains firm, supported by AI infrastructure, defense technology, and reshoring of critical manufacturing. These conflicting signals—resilient capital spending versus softening labor demand—make this one of the most complex policy environments of Powell’s tenure.

Inflation from recent tariffs has been milder than anticipated. The Fed now sees price pressures easing back toward target over the next 18 months, assuming no renewed supply disruptions.

Powell’s Press Conference: Key Themes

Powell struck a measured, data-dependent tone at his press conference, reinforcing the Fed’s pivot from a rules-based framework to one guided by “discretion, diligence, and destination.”

Key themes:

- Labor risk management: “We cannot declare victory on inflation, but we must acknowledge the emerging risks to employment.”

- Liquidity assurance: Reinvesting MBS into T-bills is about function, not stimulus.

- Data limitations: Powell emphasized the difficulty of policymaking amid a statistical blackout. “What do you do when you are driving in a fog? You slow down.”

- December outlook: Powell also noted that a December cut was not a sure thing, even adding “far from it”. He also noted that “policy is not on a preset course” Powell emphasized this point repeatedly and is keeping his options open while implying that another 25 bp cut remains on the table.

- Neutral Rate and the next move: We are now back in the range of where most FOMC participants believe the neutral funds rate is. “There is a growing course that maybe we should wait a cycle.”

- Equity Markets: “We do look at any particular asset, we look at the overall financial system and ask whether it can withstand a shock.”

- The AI Boom: It is different from the 1980s. The companies driving the boom are earning money. These are investments not just ideas.

Piedmont Crescent Capital’s baseline scenario now assumes:

- We still see two additional 25 bp cuts — most likely in December January — bringing the funds rate to a cycle low of 3.125% in Q1 2026. The markets are pricing in less than that, with the 2-Year Treasury rising to 3.59%—essentially pricing in one more cut by the middle of next year.

- Core PCE inflation ending 2025 at around 2.5%, down from 3% this year, as supply normalization and tighter credit cool demand.

- The Fed may opt to skip a meeting and wait for more hard data on inflation and employment. That would essentially extend the duration of the easing cycle without making it any deeper.

- We see the long-run neutral rate around 3% but it is likely edging higher as the buildout of AI infrastructure boosts productivity and long-run potential growth.

We see the Fed nearing the end of its easing cycle, shifting from active accommodation to sustained vigilance. Cutting rates while headline inflation remains “elevated” demands precise messaging. Lower short-term rates and a stable balance sheet should gradually support credit-sensitive sectors in early 2026, fostering a modest pickup in activity without reigniting inflation. If markets perceive the Fed as easing too aggressively, however, long-term yields could rise and offset much of the intended benefit.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

October 29, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

October 2025 Consumer Confidence - Consumer Confidence Holds Steady Amid Data Drought

Anecdotes Provide Some Guidance

-

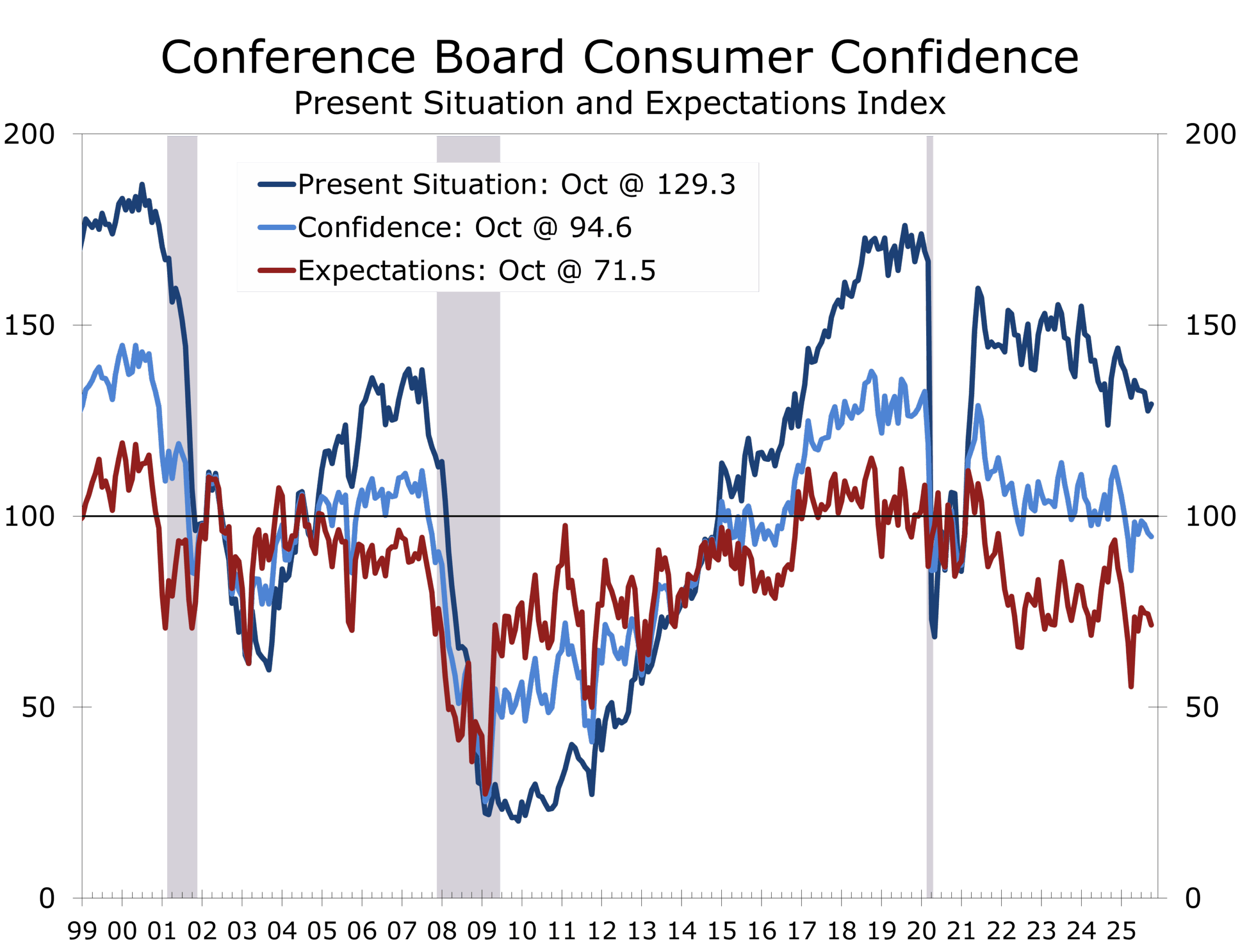

- The Conference Board’s Consumer Confidence Index® slipped 1.0 point in October to 94.6 (1985=100), essentially unchanged from September’s upwardly revised 95.6.

- The Present Situation Index rose 1.8 points to 129.3, while the Expectations Index declined 2.9 points to 71.5 — remaining below the key 80 threshold that historically signals recession risk.

- With most federal data releases delayed by the government shutdown, the Consumer Confidence report provides one of the few real-time signals on household sentiment and labor trends.

- Write-in comments continue to focus on prices, inflation, and the shutdown itself — though mentions of tariffs declined further.

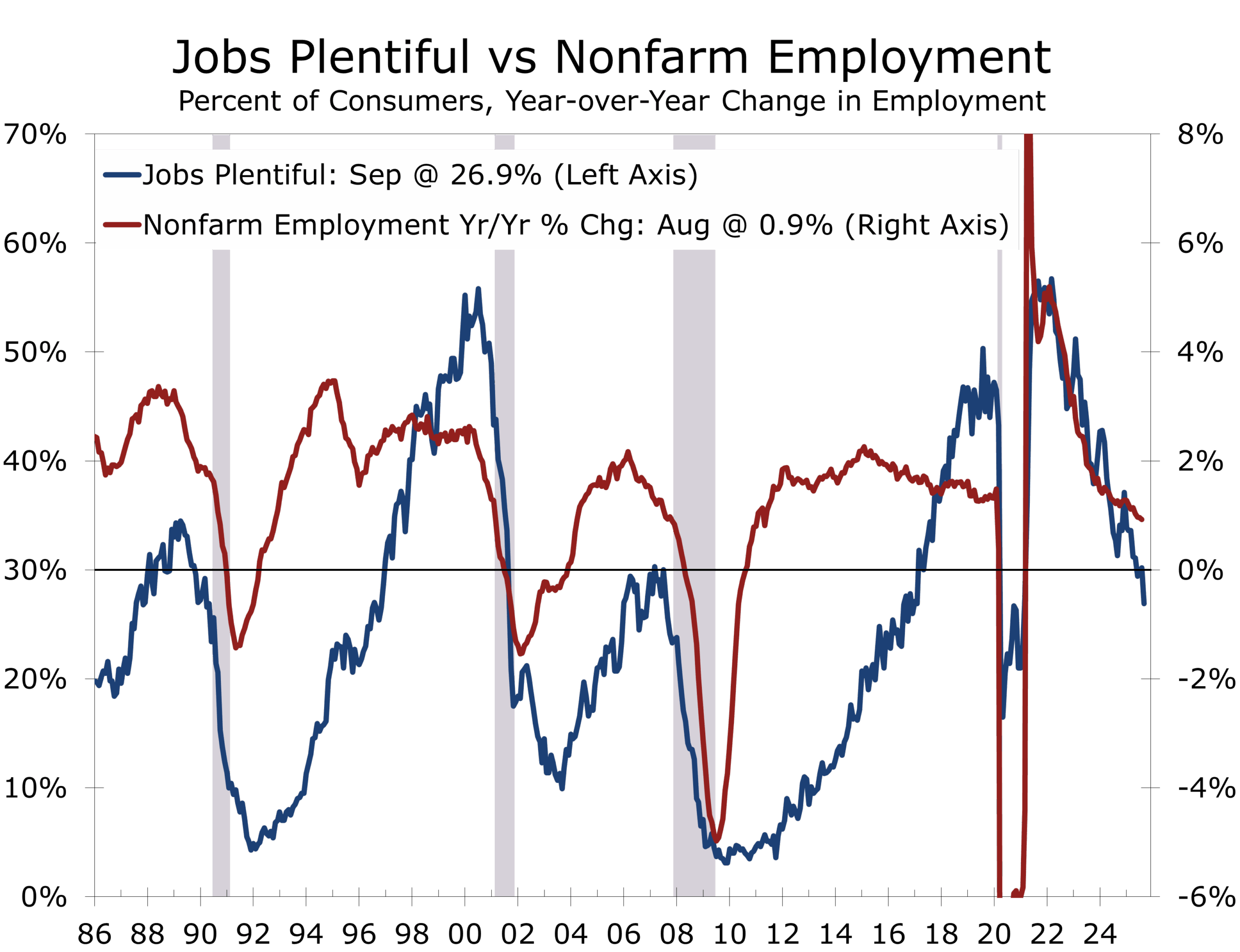

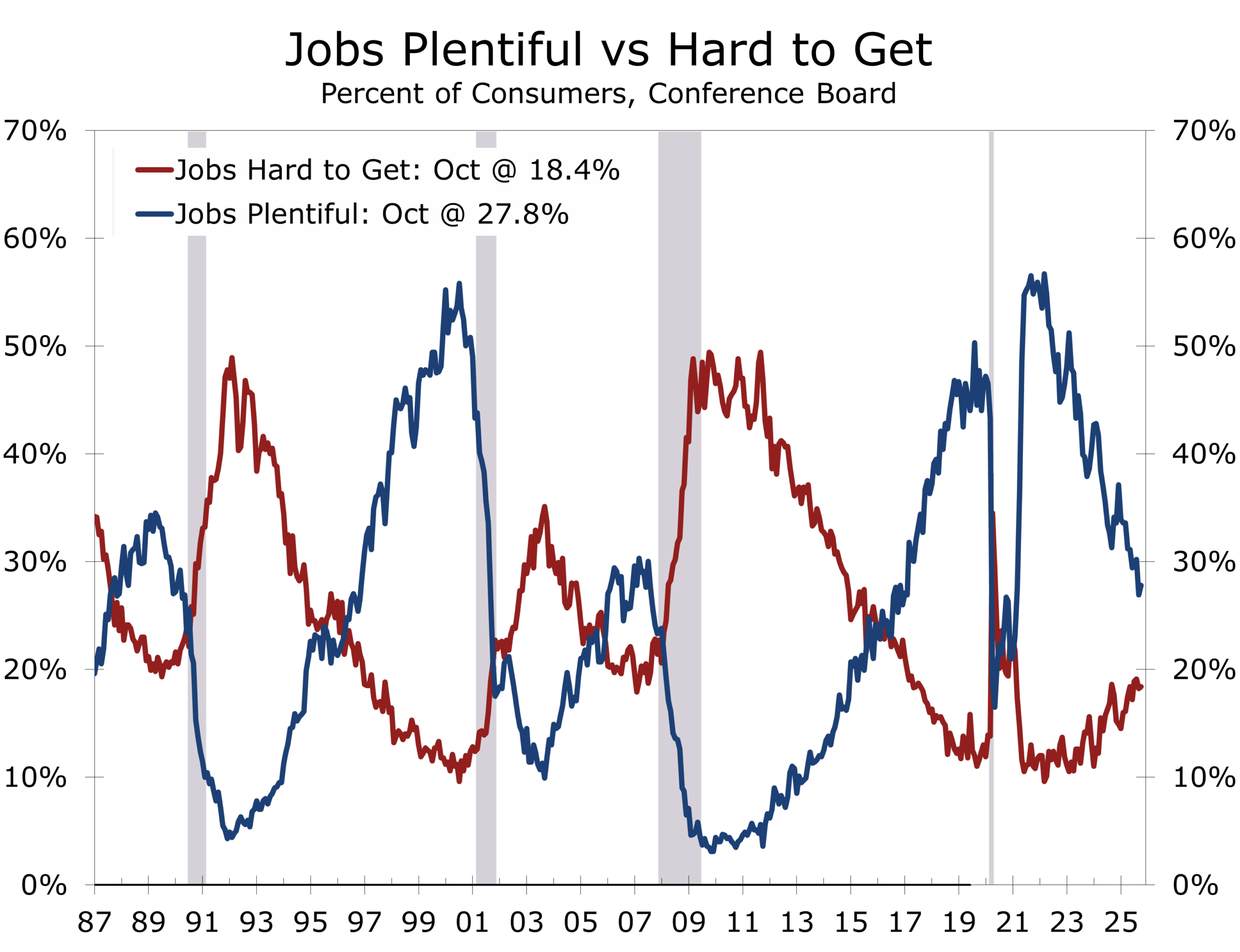

- Views of the job market improved slightly: 27.8% of consumers said jobs were “plentiful,” up from 26.9% in September.

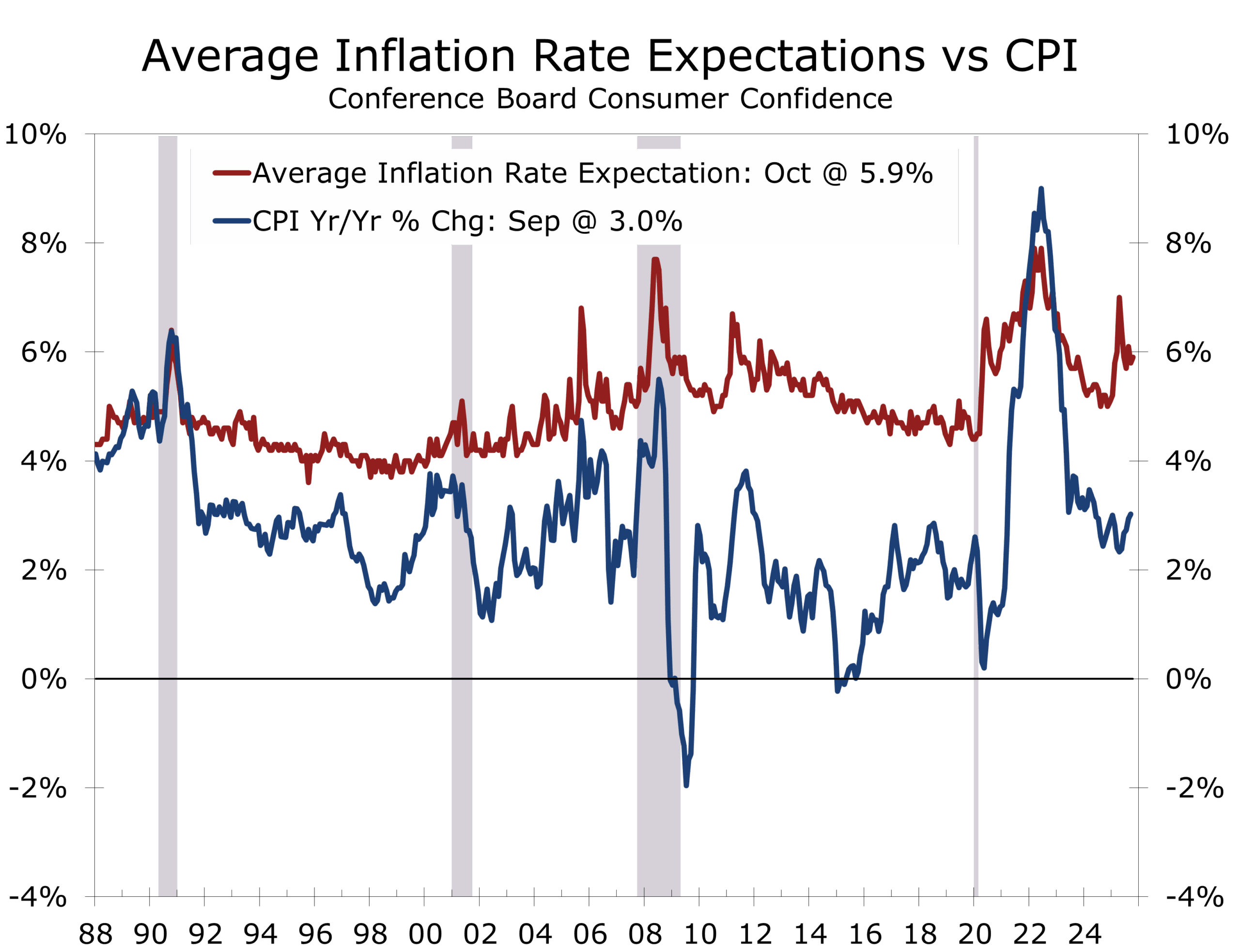

- Inflation expectations edged up to 5.9%, while the share expecting higher interest rates rose to 52.8%.

- October’s confidence readings are consistent with other private data (including this morning’s new weekly ADP report) showing modest payroll growth and a gradual rise in the unemployment rate. The Chicago Fed’s labor market indicator pegs October’s unemployment rate at 4.35%.

Confidence Holds Ground as Data Remains Scarce

With much of the federal statistical system offline during the ongoing government shutdown, this month’s Consumer Confidence report carries unusual weight. In the absence of payroll, retail sales, and inflation updates, the Conference Board survey offers rare, consistent insight into how households perceive current and future conditions. Historically, shifts in its labor market components — particularly the “jobs plentiful” and “hard to get” series — have led changes in nonfarm payrolls by one to two months.

Confidence edged lower, but revisions point to stronger underlying sentiment.

In October, confidence effectively moved sideways. The headline index dipped just one point to 94.6, from an upwardly revised September reading, with stronger views of current conditions offset by weaker expectations. The Present Situation Index gained 1.8 points to 129.3, while the Expectations Index fell nearly three points to 71.5. That measure has now been below 80 since February — a duration consistent with past pre-recession readings. On net, Consumer Confidence was slightly higher than was previously reported for September, despite falling 1 point from the revised reading.

Labor Sentiment Offers Early Clues

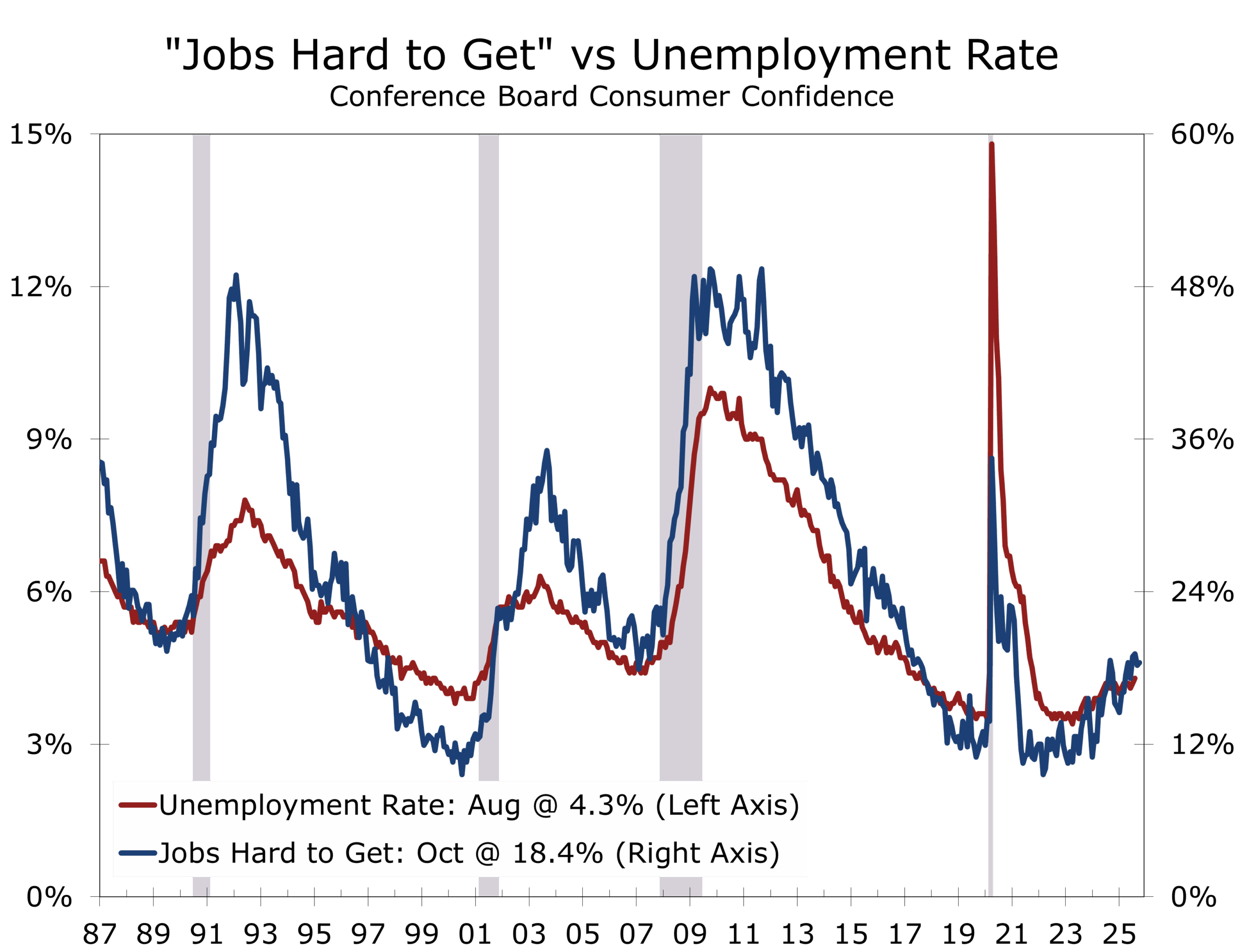

Consumers’ appraisal of the job market improved slightly for the first time since December 2024. The share calling jobs “plentiful” rose to 27.8%, while those calling jobs “hard to get” edged up to 18.4%. The resulting labor differential remains near 9 points — a level consistent with below-trend hiring and a modest uptick in unemployment.

Given the survey’s track record as a leading indicator, the October readings reinforce expectations that the labor market continues to cool, especially in lower-wage and entry-level positions. The latest official unemployment rate for the U.S. is 4.3% for August 2025.

Rising jobless expectations signal a softer market for lower-wage and entry-level workers.

Due to the ongoing government shutdown, however, more recent official data are unavailable. A model from the Federal Reserve Bank of Chicago estimates the jobless rate at around 4.35% for October 2025 and we see the jobless rate eventually rising to 4.5%.

Prices, Shutdown, and Political Fatigue

Consumers’ write-in responses again centered on inflation, which remains the most frequently mentioned concern, followed by the government shutdown and political uncertainty. References to tariffs declined further but remain elevated. Average 12-month inflation expectations edged up to 5.9%, and more than half of respondents expect higher interest rates ahead.

Confidence fell among younger consumers and lower-income households but improved for middle-aged respondents and those earning above $75,000, especially at the top end of the income spectrum. By political affiliation, the Conference Board noted that confidence increased among Independents but slipped among Democrats and Republicans alike.

Spending Signals Mixed but Holding Up