Recession Risks Have Eased, Yet Labor Market Momentum Continues to Fade

-

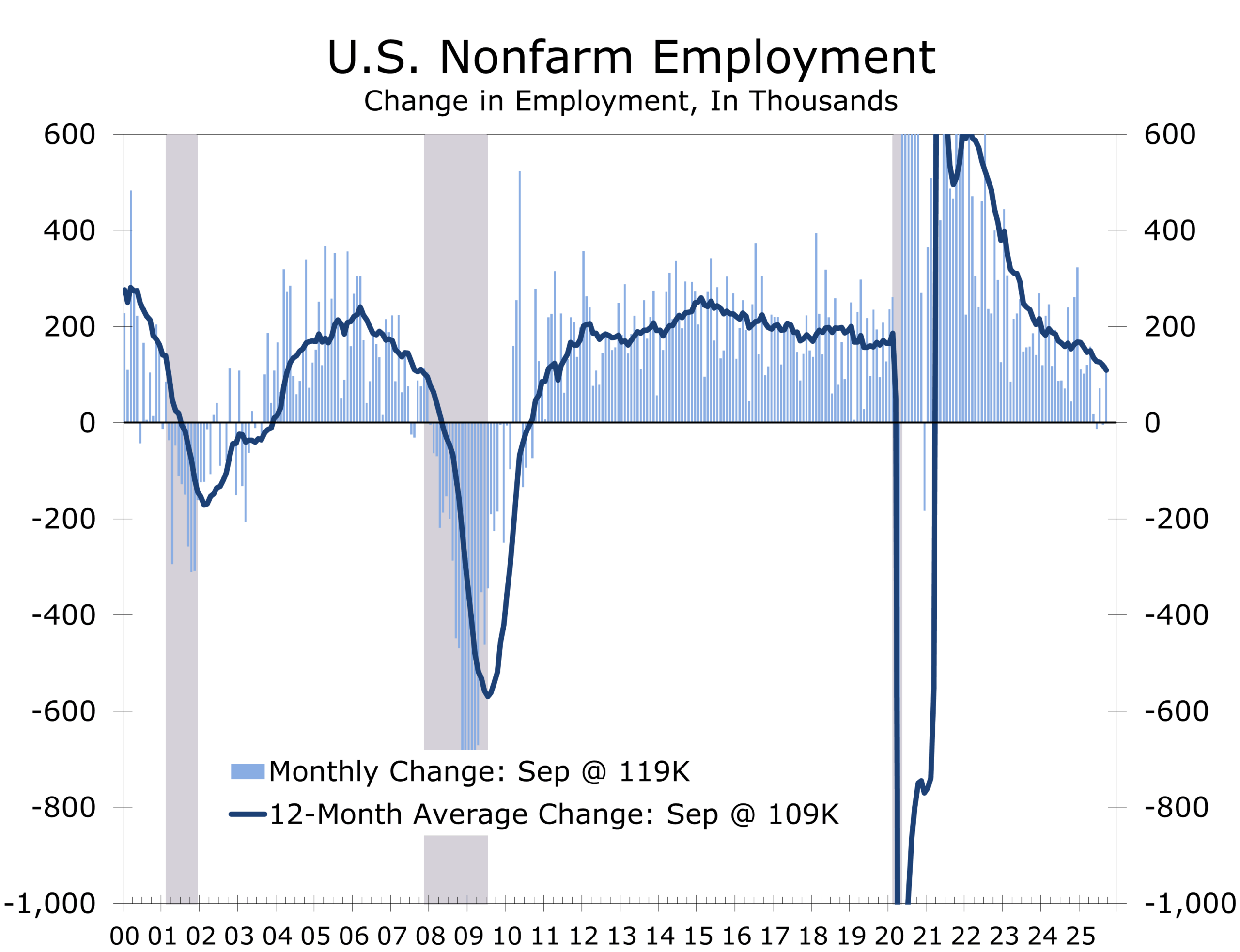

- Nonfarm payrolls rose 119,000 in September; the private sector added 97,000, easing some recession fears.

- Revisions lowered to the two prior months by 33,000; the three-month average improved to 62,000 but remains weak.

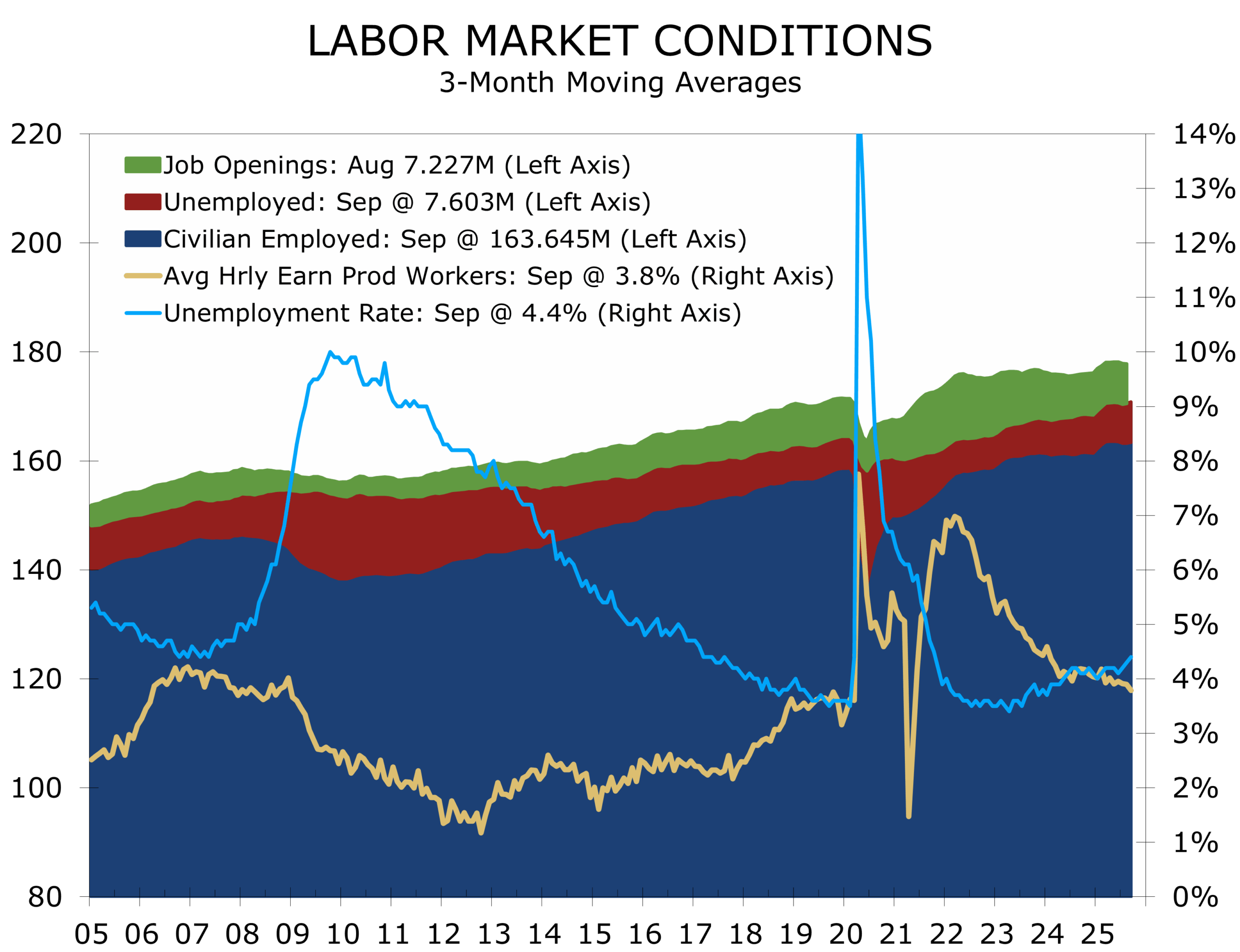

- The unemployment rate rose 0.1 pp to 4.4%, the highest since October 2021, with 7.6 million unemployed.

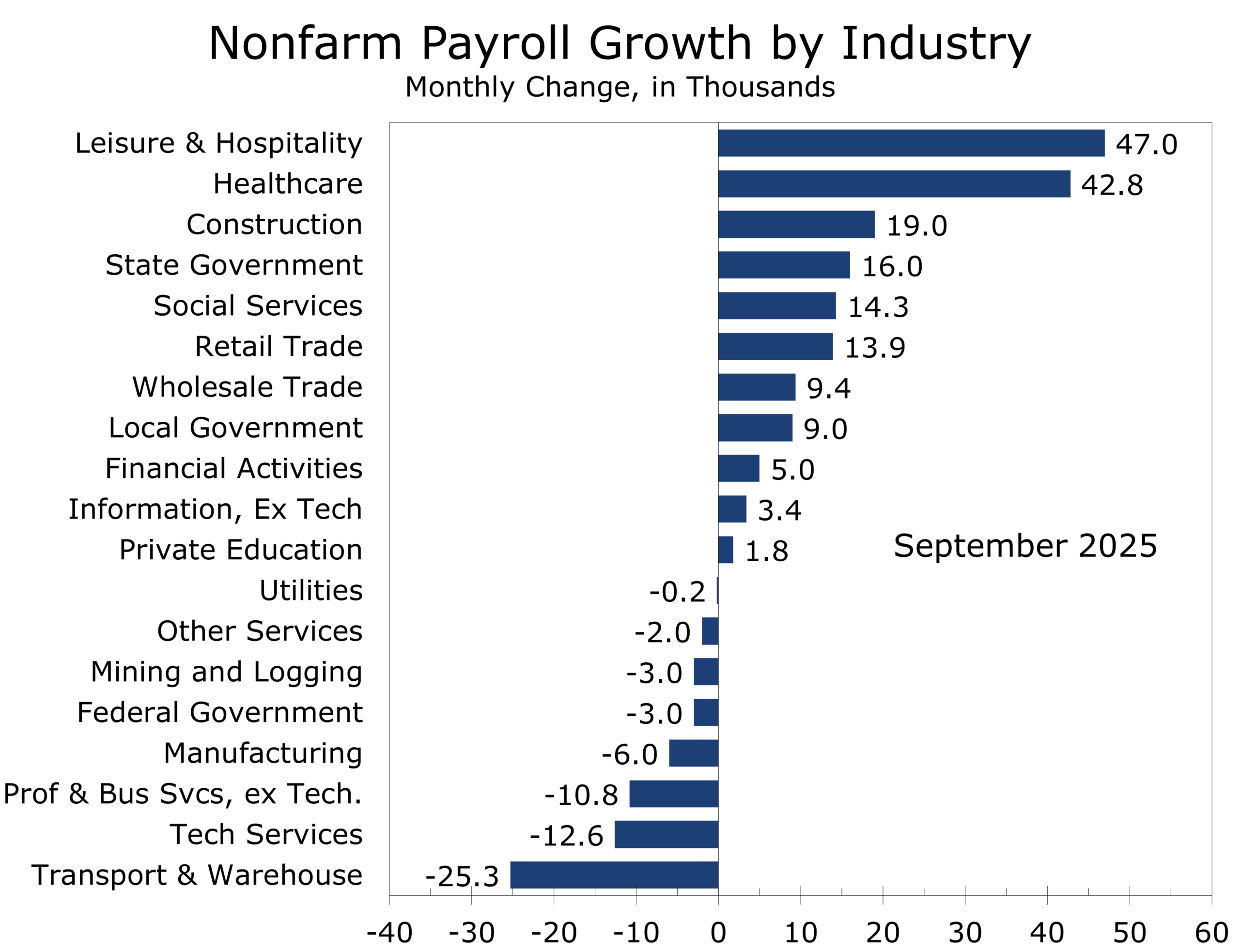

- Hiring remained concentrated in health care, restaurants, and social assistance.

- Wage growth slowed to 3.8% y/y, and hours worked remained flat.

- Rising permanent job losses, narrowing sectoral breadth, and weakening goods-producing momentum point to accumulating slack and diminishing inflationary tailwinds.

- The September employment report supports the case for further Fed easing, though the shutdown-delayed data release schedule complicates the timing. We continue to call for a quarter point cut, as we do not expect to see compelling evidence to suggest otherwise before the Fed meets on December 9-10.

A Labor Market That Stabilized in September—But on Unsteady Footing

September’s employment data delivered a welcome dose of stability at a moment when markets had begun to fear that the U.S. economy was sliding toward recession. Nonfarm payrolls rose 119,000, with the private sector adding 97,000 jobs — both comfortably above expectations and strong enough to reassure investors that the economy had not fallen off a cliff during the prolonged government shutdown. While the report is backward looking it is still reassuring. Employment conditions show no evidence of a pre-shutdown collapse and handily beat the market’s consensus estimates.

This modest strengthening followed another strong earnings report from Nvidia, which reinforced confidence in the AI investment cycle and eased doubts about the durability of the tech-driven productivity boom. Together, the labor data and renewed strength in AI provided just enough breathing room for markets rattled by the Liberation Day tariffs and rising global uncertainty.

Job growth has slowed to the bare minimum needed to keep unemployment from rising.

Yet beneath the steadier surface, the labor market remains fragile. Growth has slowed markedly since April, and the latest report does not change that overarching narrative. The three-month average for job gains improved to roughly 60,000, but that figure — even when adjusted upward — is barely above the job growth needed each month to keep the unemployment rate from rising . The upward bump is welcome but hardly convincing. Job growth has lost considerable momentum since the spring, and September represents stabilization, not a renewed acceleration.

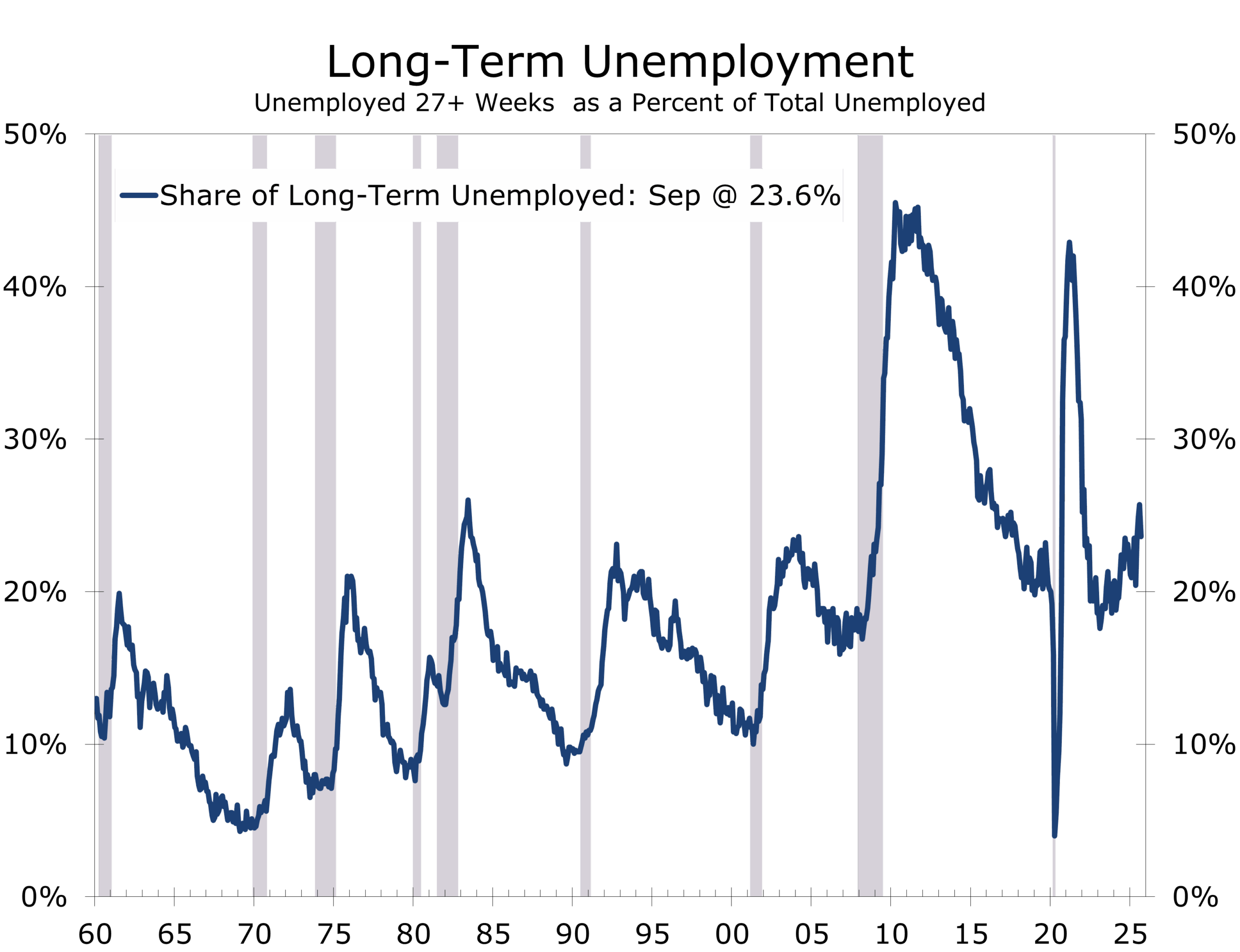

Revisions to July and August subtracted 33,000 jobs from the previous data, reminding us that the prior trend was weaker than first reported. And while the headline unemployment rate held at 4.4%, its highest since October 2021, the increase was driven partly by a surprisingly strong 470,000 jump in labor-force entrants. The influx is a sign that workers are reentering the job market rather than disengaging from it — a positive development. The household survey also showed rising permanent job losses, however, which climbed above 2 million for the first time since late 2021 — an unsettling development when hiring outside of a few industries remains sluggish. The trend has means a growing share of the unemployed have been without a job for 27 weeks or more.

Permanent job losses have quietly risen above 2 million — an early-cycle warning sign.

The shutdown itself added additional noise: the household survey was completed before the funding lapse, but establishment data were compiled using an unusually high 80% electronic reporting rate. October data will not be collected at all, and November will not be published until December 16. This complicates the Fed’s assessment at a critical moment.

Growth Carried by Health Care, Hospitality, and Social Services

Where job growth did appear, it remained concentrated in a narrow slice of the service economy. Health care (+43,000) once again accounted for the largest share of gains, driven by ambulatory centers and hospitals. Restaurants and bars (+37,000) also contributed meaningfully, continuing a steady post-pandemic normalization. Social assistance (+14,000) was propelled by a 20,000 increase in individual and family services.

The top three contributors accounted for the overwhelming majority of net private-sector hiring in September, with most other major industries posting little change . Seasonal patterns related to the start of the school year may have boosted state and local government hiring and partially flattered the gains in leisure and education but do not account for all of the increase.

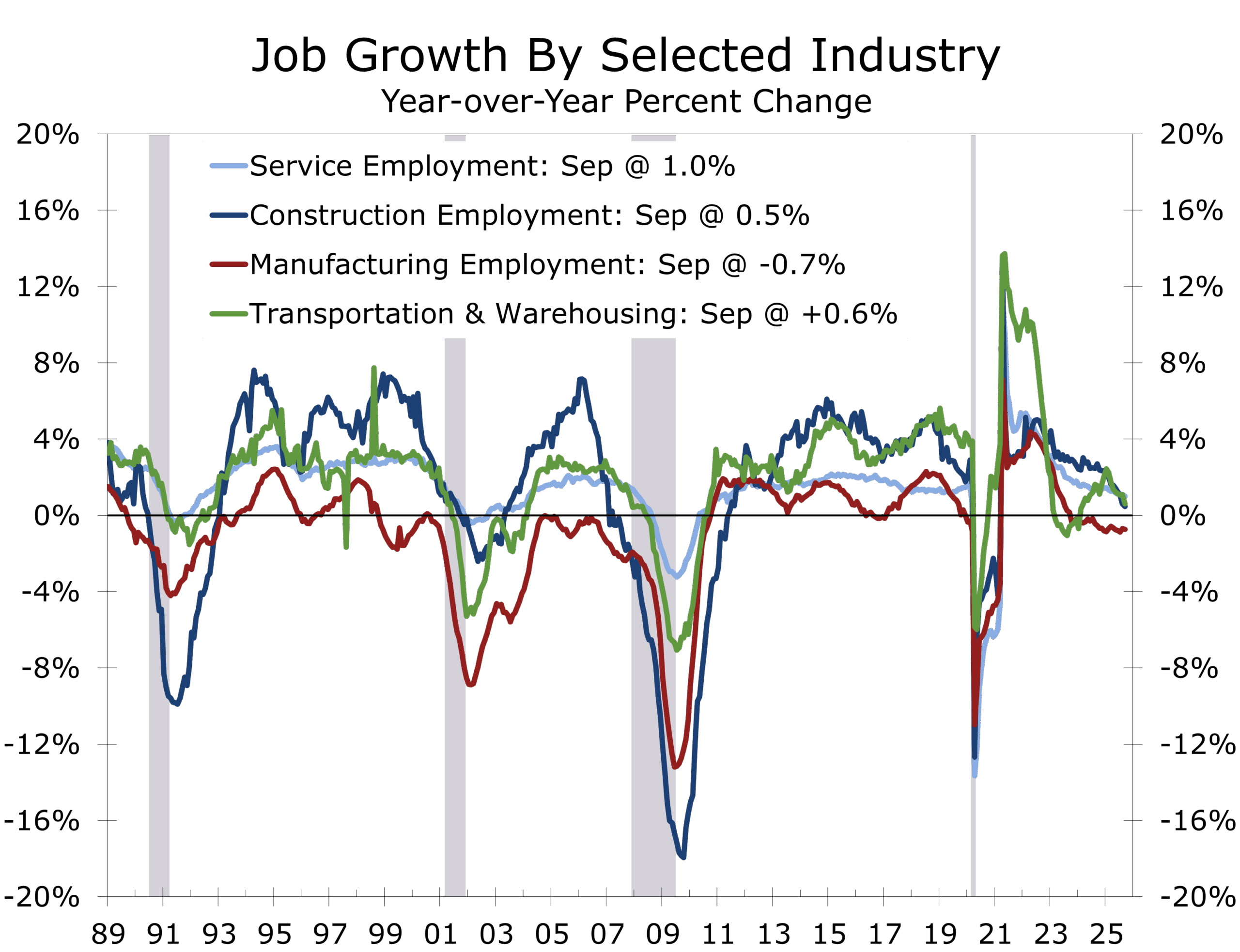

Meanwhile, the soft spots remained firmly in place. Transportation and warehousing shed 25,000 jobs, driven by losses in warehousing (–11,000) and couriers (–7,000). Professional and business services — often a bellwether for white-collar demand — also weakened. Temporary staffing was a notable weak spot but employment also fell in tech-centric industries. And federal employment declined another 3,000 ahead of what is expected to be a huge drop in October and November, as DOGE-related retirements and separations will show up.

One relative bright spot: employment in the most cyclical parts of the economy — construction, manufacturing, and logistics — is holding up better than recessionary patterns would suggest. Construction remains modestly positive; manufacturing is only marginally negative; trucking shows mild year-to-year strength. In a downturn, all three would be sharply negative. This is one of the strongest arguments against the notion that the U.S. is sliding into recession today. Of course, these are preliminary figures and the revised data in February are expected to result in large downward revisions.

Unemployment Is Drifting Higher — and Slack Is Accumulating

The unemployment rate rose 0.1 percentage point 4.4%, but the underlying composition reveals a labor market cooling slowly, not collapsing. The labor force posted an outsized gain of 470,000, while household employment rate by 251,000. The number of unemployed rose by the difference, 219,000. This combination — more people looking for work, but not enough hiring to absorb them — is consistent with a plateauing labor market rather than an economy in free fall.

Participation remained at 62.4%, unchanged over the year. The employment-population ratio slipped to 59.7%, down 0.4 points since last September. And the composition of joblessness continues to shift in a concerning direction: permanent job losers rose above 2 million, while temporary layoffs and job leavers remained relatively stable. The rise in permanent job losses will exert further drag on consumer spending, particularly among middle- and lower-income households.

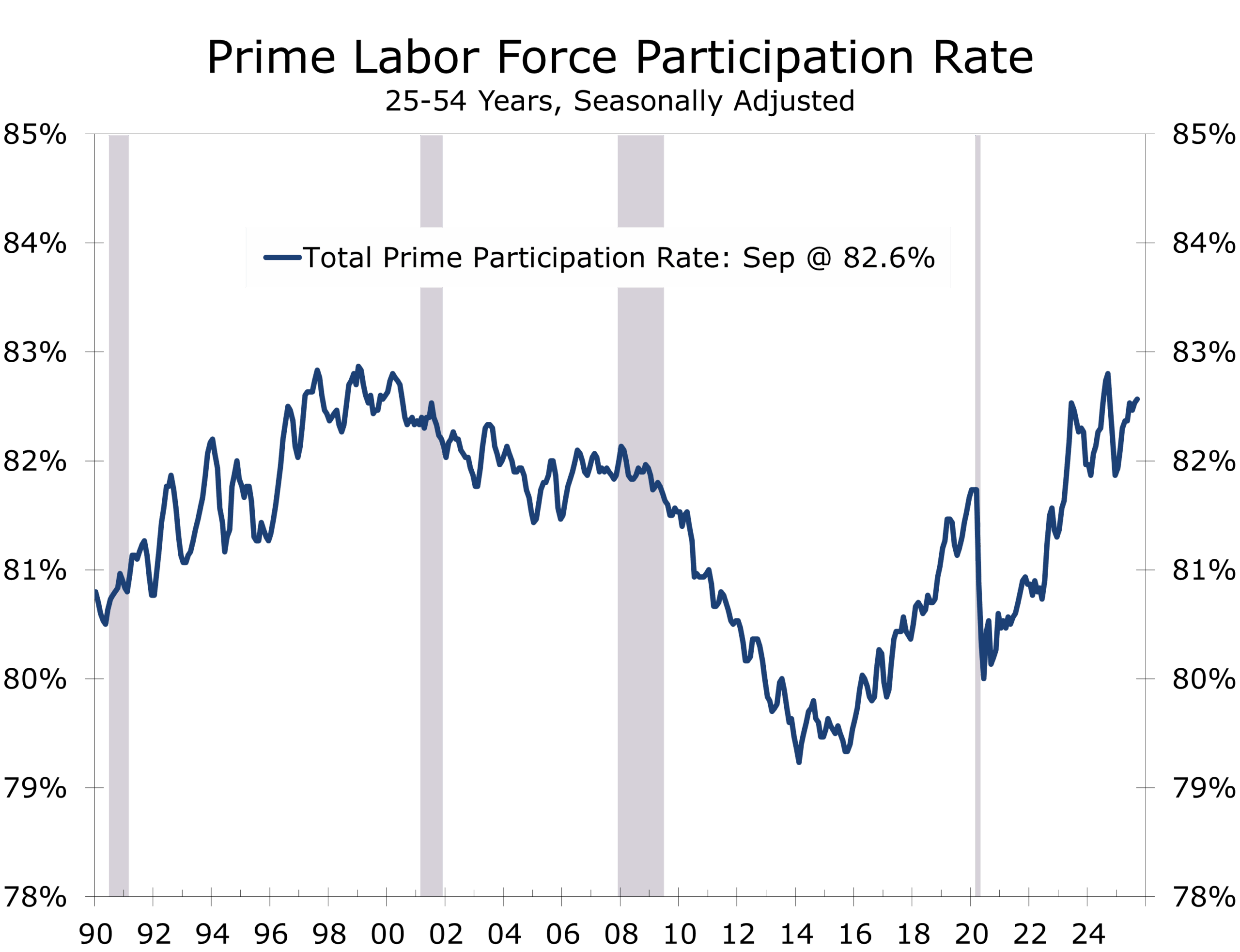

The share of the prime working-age population at work remains high, at just over 80%, and the Sahm Rule remains far from its triggering level, reinforcing that conditions do not yet meet recession thresholds.

Wage Growth and Hours Continue to Moderate

Wage growth slowed to 0.2% m/m and 3.8% y/y, on an overall basis, which is consistent with the Fed’s inflation target. Production and nonsupervisory workers saw slightly stronger gains at 0.3% m/m, but the overall pattern continues to reflect a gradual cooling.

Wage growth has aligned with the Fed’s inflation target — a key precondition for rate cuts.

Hours remained unchanged at 34.2, the average for the past year. Hours worked rose 0.1% in September and were essentially flat during the third quarter, which is well below our forecast of 3.7% GDP growth for the quarter, implying strong productivity growth.

A Late-Cycle Labor Market with Risks Tilting Toward the Downside

Structural indicators point to a maturing business cycle. Hiring is heavily concentrated in health care and services. Goods-producing sectors are flat to mildly negative. Federal employment faces a pending Q4 cliff due to deferred resignations. Permanent job losers are drifting upward. This is classic late-cycle behavior — not recessionary, but not healthy either.

The absence of broad-based deterioration is encouraging, but the accumulation of small points of weakness raises the risk of a slower Q4, especially given the fragile global backdrop and the extension of tariff pressures into fall.

FOMC Implications — A Case for Easing, Delayed by the Data Gap

September’s firmer headline does not change the broader trajectory: the labor market has downshifted from expansion to plateau. The Fed will not have October data and will receive November data only days before its mid-December meeting.

The ingredients for further easing remain in place. Unemployment is drifting higher. Wage pressures have aligned with the inflation target. Hiring is narrow and losing momentum. Goods-producing industries are weakening.

The case for a rate cut is firming — even as the calendar gets messier.

The Fed’s challenge is not the direction of travel — which is clearly softening — but the timing. With the data pipeline disrupted, there may be some reluctance to cut in December but we maintain that in the absence of compelling evidence to suggest otherwise, the Fed will go with the call made on the field and cut rates a quarter point at their December 9-10 FOMC meeting.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 20, 2025

Mark Vitner, Chief Economist

(704) 458-4000