The Piedmont Perspective: Europe at a Civilizational Crossroads

Europe at the Crossroads: Identity, Drift, and the Fear of a New Dark Age

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – A Broadening Labor Slowdown and a Hawkish Cut Ahead

Highlights of the Week

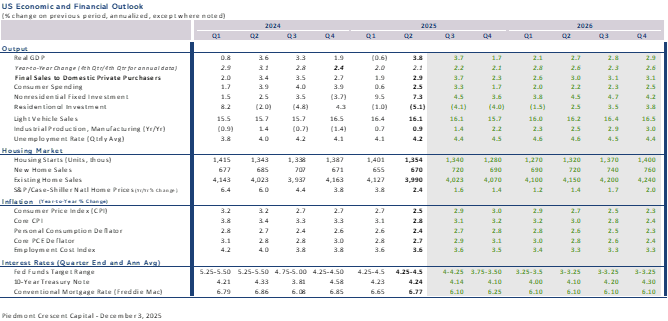

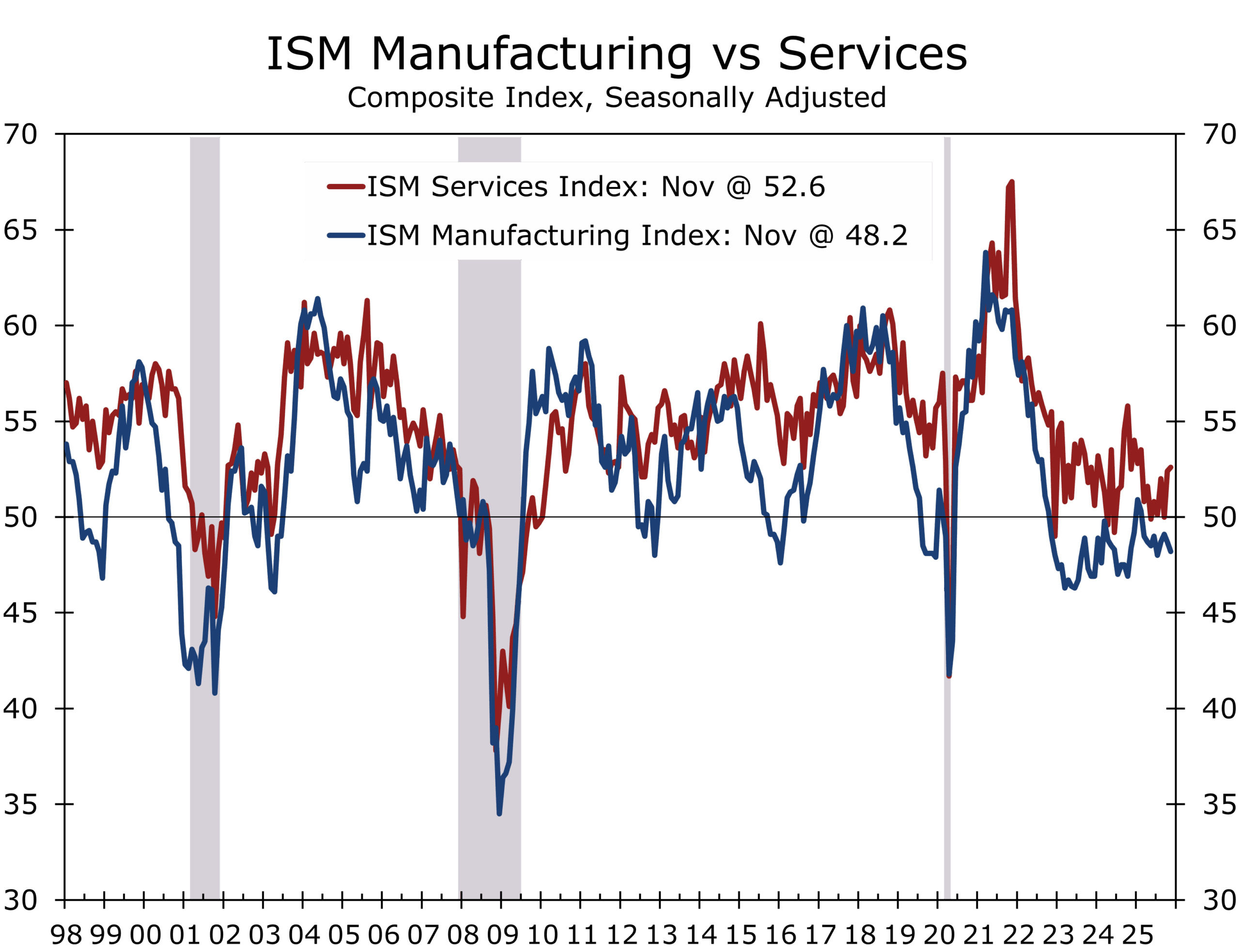

- The U.S. economy is settling into a two-speed pattern—services expanding, manufacturing contracting—keeping growth positive but slowing.

- Labor softening is broadening, and with BLS data delayed, survey-based indicators now carry outsized influence for the Fed.

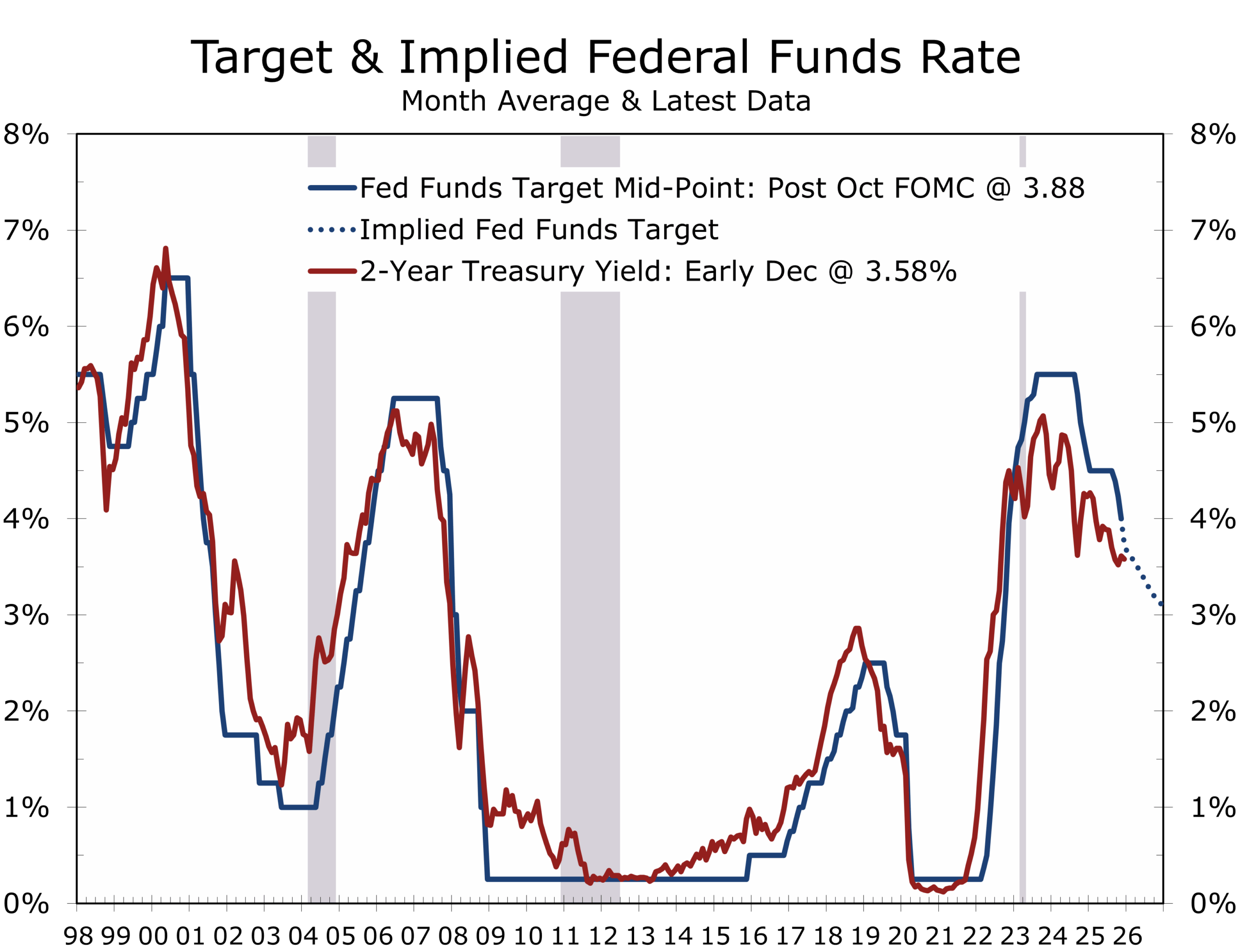

- A December rate cut is widely expected, but the internal dispersion among FOMC members increases the odds of a hawkish cut.

- Treasury markets signal a narrowing easing path for 2026, making optionality critical for financial decision-makers.

- Geopolitical risks remain elevated but contained: Ukraine’s attrition, Middle East fragility, and persistent PLA pressure on Taiwan.

- The new U.S. National Security Strategy frames Europe’s challenges in civilizational terms, signaling a more conditional American posture.

- The coming weeks will test the Fed’s ability to manage a slowing labor market via actions and statements without reigniting inflation expectations, setting the tone for the 2026 policy path and setting the stage for a second half rebound.

A Two-Speed Expansion Enters a Cooling Phase

Financial markets ended the week with a calm that felt slightly at odds with the underlying economic tone. Equity indices hovered near all-time highs, volatility receded, and modestly stronger data from Europe and China offered reassurance that the global soft landing remains intact. Yet beneath the surface, the internal gears of the U.S. economy are turning more slowly. The labor market is softening more sharply and more broadly, the services sector is shedding some of its earlier momentum, and manufacturing remains modestly but firmly in contraction. Stability persists, but with diminishing buffers and a steeper glide path than markets appreciated a few weeks ago.

The soft landing remains alive, but the labor market is cooling in breadth, not just in pockets.

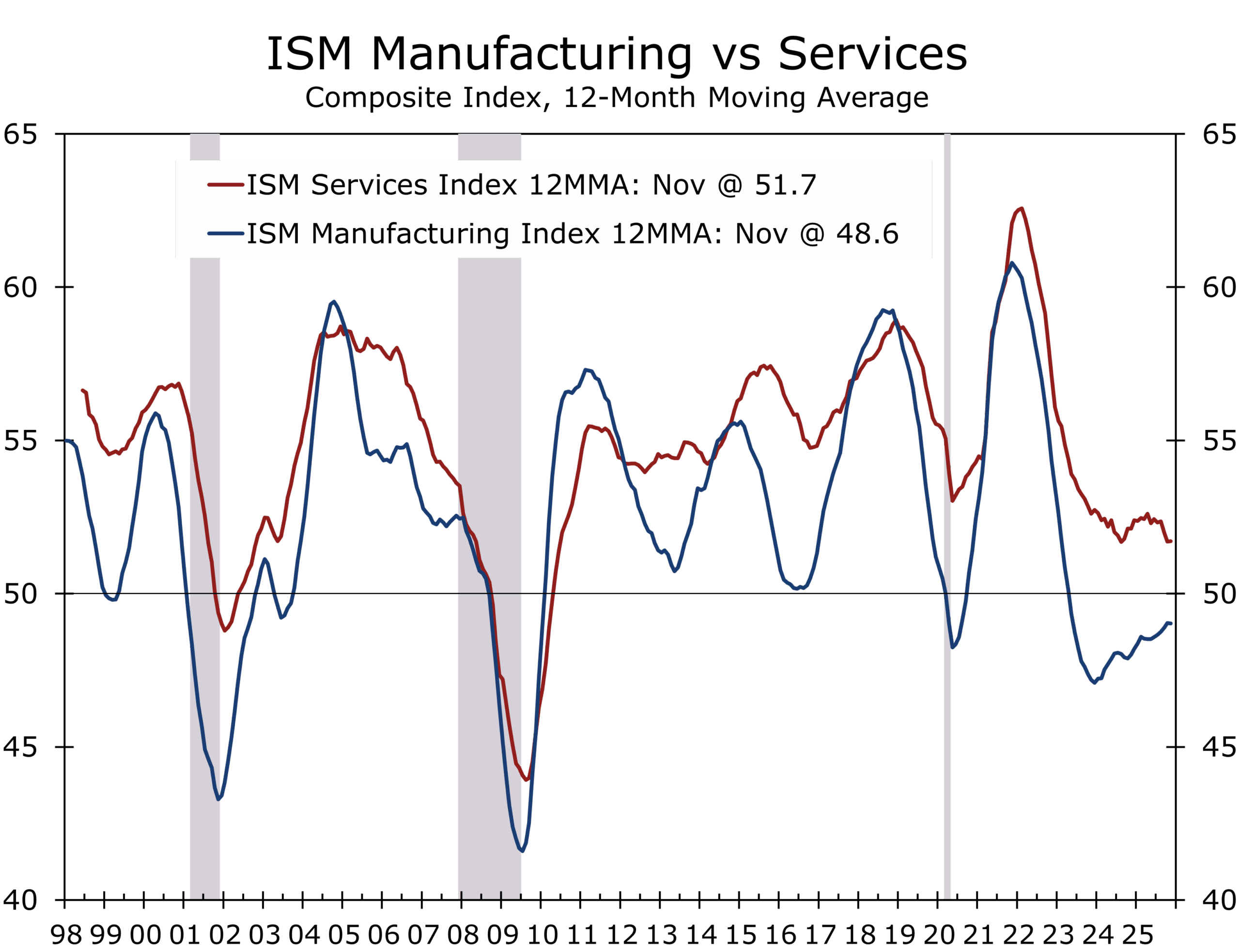

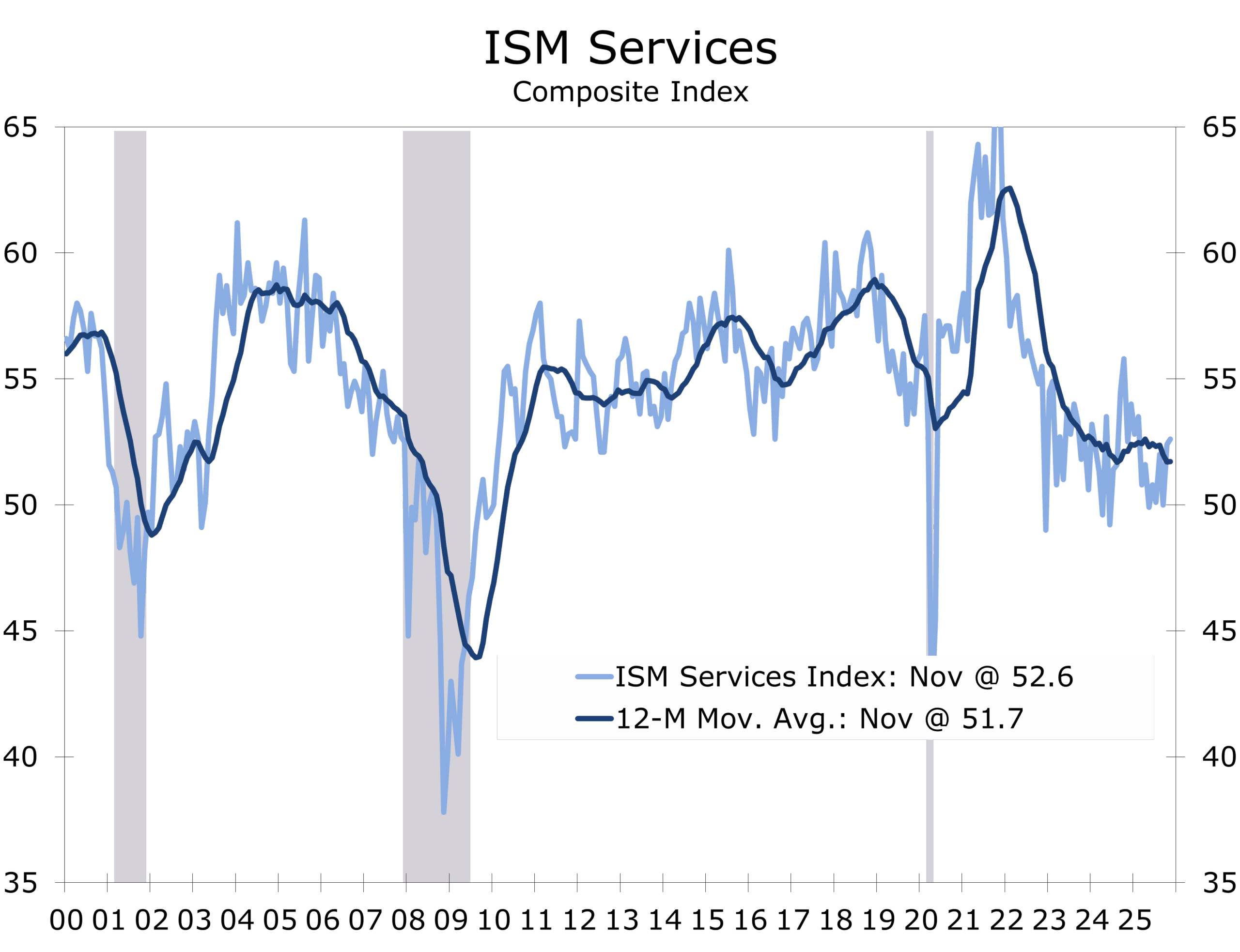

The two-speed economy is now unmistakable. Services remain the dominant engine of the post-pandemic period and continued to expand. The ISM Services PMI rose to 52.6 in November. Business Activity held at 54.5, and backlogs surged to their highest level since early 2025. These indicators collectively point to an economy growing at roughly a 1.3% annualized pace. Yet the deeper trend is drifting downward: the 12-month average of the Services PMI sits at its lowest reading since 2010, evidence of a maturing cycle rather than an accelerating one.

The ISM Survey is consistent with our key call for 2026, which sees the economy getting off to a sluggish start in the New Year but catching its second wind by mid-year.

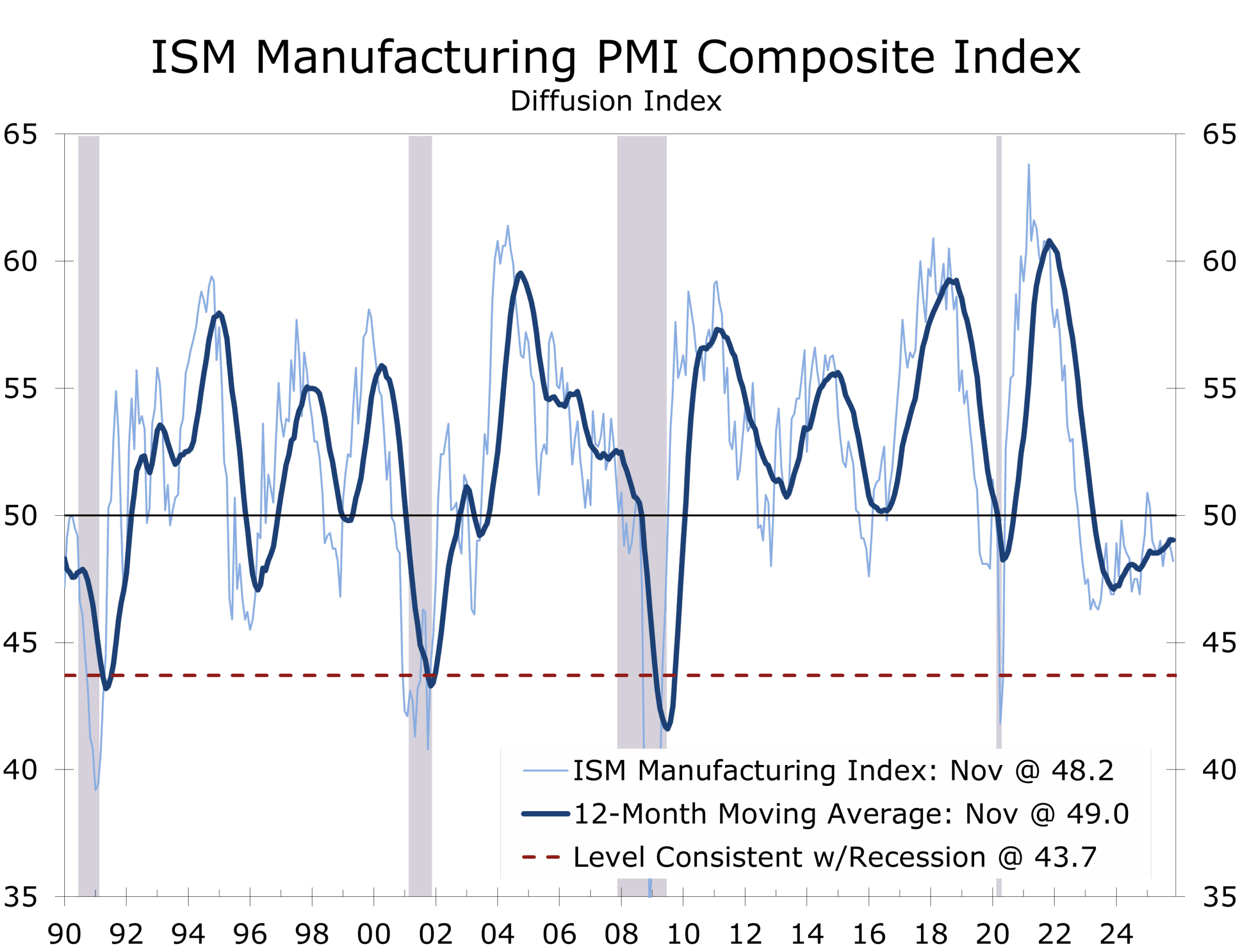

Manufacturing, meanwhile, is charting a different trajectory. The ISM Manufacturing PMI contracted for the ninth consecutive month, slipping to 48.2, with new orders, backlogs, and export demand all under pressure. Producers are not signaling collapse, but rather caution—rooted in tariff volatility, compliance frictions, and lingering effects of the government shutdown. Customer inventories remain unusually lean, a condition that typically precedes a restocking cycle. But managers remain hesitant, preferring liquidity and flexibility over scale until policy uncertainty clears.

Weakness that began in goods production is now visible across the labor landscape.

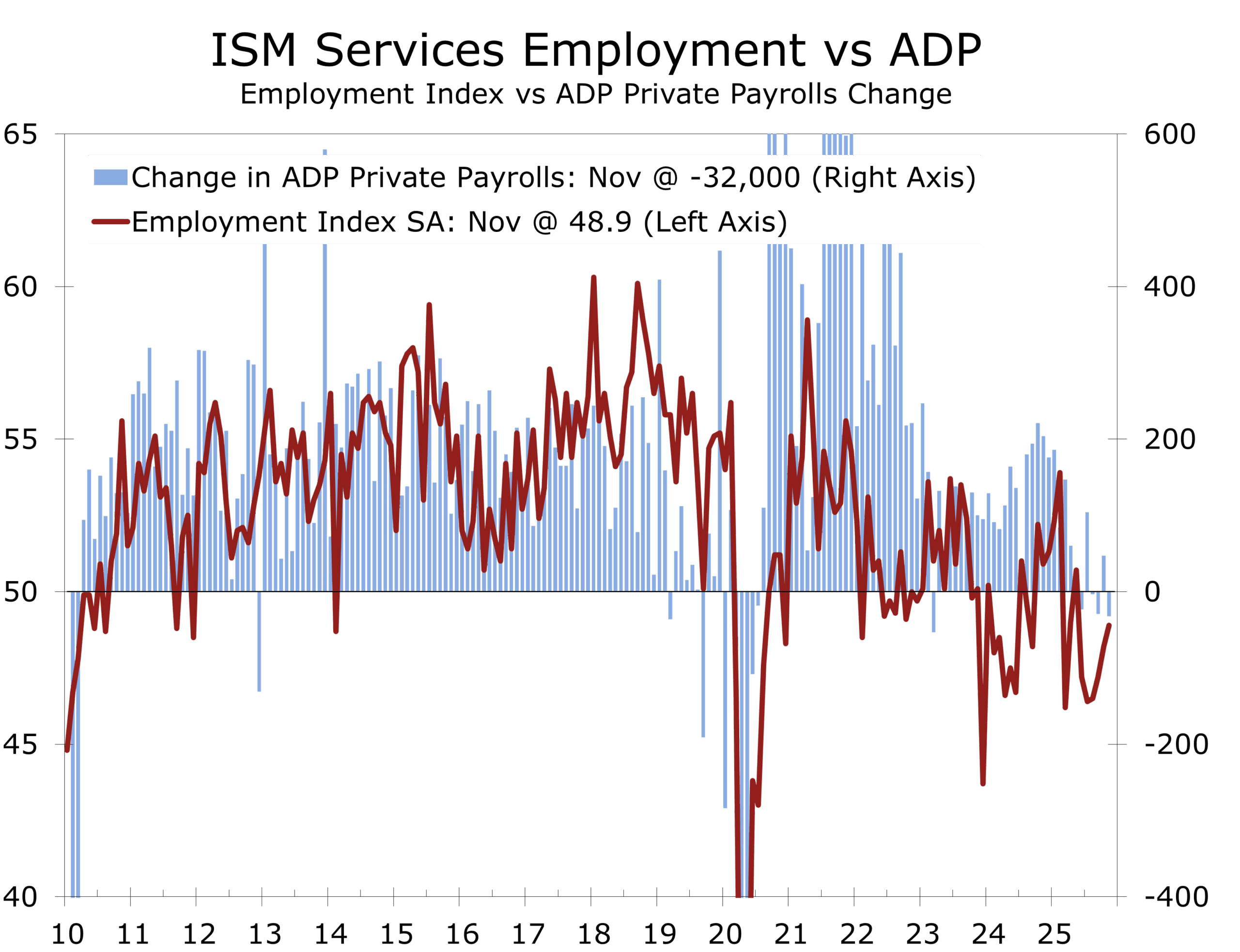

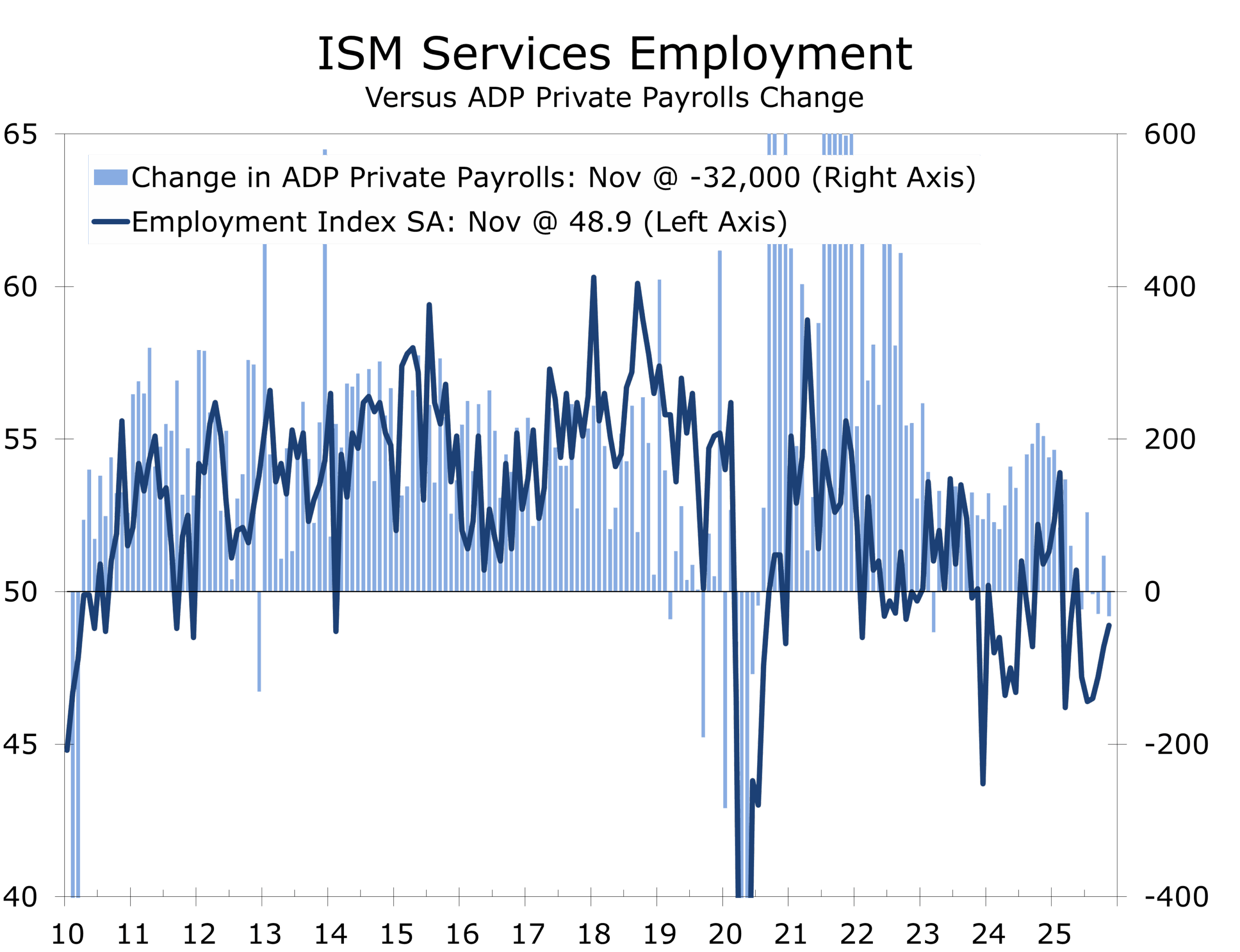

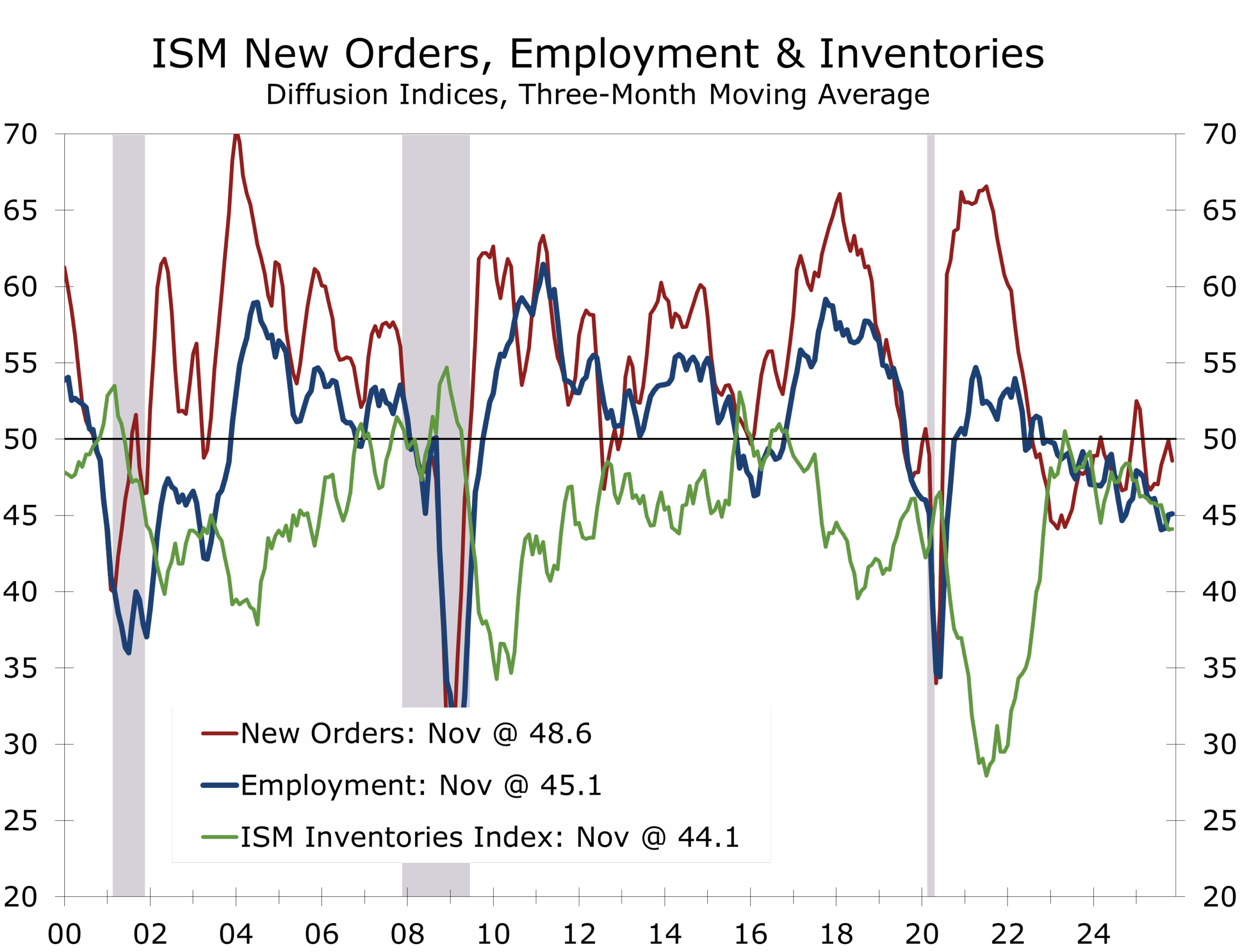

The labor market delivered the most consequential signals of the week. ADP reported a 32,000 decline in private payrolls; Challenger layoffs softened slightly from October’s spike but remain 24% above year-ago levels; and both ISM employment readings remained in contraction—Services at 48.9, Manufacturing at 44.0. Until recently, hiring weakness had been concentrated in rate-sensitive pockets of the economy. Now it is broadening across middle-skill service industries and goods-producing sectors. With the federal shutdown delaying fresh BLS payroll and CPI releases, the Fed must rely more heavily on these forward-looking indicators, which carry decisive weight heading into the December FOMC meeting.

A Hawkish Cut Comes into View

The policy implications are significant. The Fed is almost certain to cut rates this week, but the broader narrative remains unsettled. The dove bloc argues that risks to employment now outweigh risks of lingering inflation and that tariffs represent a one-time shift in price levels rather than a persistent inflationary force. Centrists emphasize careful progress toward the neutral rate. The hawks warn that financial conditions have eased too quickly and that another cut risks weakening the Fed’s credibility. Powell’s challenge is to deliver an easing step that arrests the downward drift in the labor market without signaling a broad pivot.

The Fed must cut to steady hiring but must do so without undermining inflation credibility.

What the market increasingly anticipates is a hawkish cut: one that acknowledges the labor softening while clearly conveying that the Committee is not embarking on a rapid or extended easing cycle.

From a financial management standpoint, this environment requires a more tactical interpretation of the yield curve. The front end remains anchored to the near-certain December cut, but expectations for additional easing have thinned. The long end continues to face upward pressure from Japanese yield dynamics and heavy Treasury issuance. Funding markets remain stable, with abundant liquidity, and tight credit spreads—but duration volatility is still elevated.

This is a moment to preserve optionality: maintain staggered maturity ladders, extend duration opportunistically, and consider timely pre-funding of 2026 obligations. The December cut should be viewed as a calibration of policy, not the beginning of a deeper easing sequence.

Global Dispersion and the Strategic Backdrop

Globally, monetary dispersion has returned. Japan’s upward pressure on yields remains a key undercurrent in global fixed income. Switzerland has not ruled out unconventional measures if the franc strengthens excessively. Australia, Brazil, Canada, and Türkiye all continue to move in divergent directions. The post-tightening era is not synchronized easing but a landscape of increasingly differentiated monetary paths and heightened FX sensitivity.

Geopolitically, the global map remains tense but contained. Ukraine enters winter under considerable strain as Russia employs more sophisticated drone and artillery tactics. The Gaza ceasefire remains fragile but holds for now, with particularly intense fighting around tunnel networks. PLA air and naval activity around Taiwan remains elevated, reinforcing long-term strategic risk in the Indo-Pacific. Markets have absorbed these developments with guarded calm, but that calm depends heavily on diplomatic bandwidth.

A two-speed economy narrows the margin of policy error, particularly in early 2026.

This backdrop echoes in the administration’s newly released National Security Strategy, which employs unusually stark language about Europe’s future. It warns that demographic decline, institutional fragmentation, migration pressures, and insufficient defense investment could leave parts of the continent “unrecognizable in 20 years.” The Strategy reframes Europe less as a postwar project and more as a civilization confronting internal drift. The United States signals continued engagement—but on more conditional terms, emphasizing burden-sharing, energy security, and renewed strategic coherence.

Our view is that the soft landing remains achievable but increasingly delicate. Services continue to provide lift, but with diminishing thrust. Manufacturing remains cautious. Labor is softening more broadly. Inflation continues to ease, but not uniformly. And the Fed must execute a careful recalibration: supportive enough to prevent unnecessary labor weakness, firm enough to preserve credibility, and clear enough to avoid sending markets sprinting ahead of policy.

Private Final Domestic Demand is likely to be weakest at the tail end of 2025 and early 2026. We look for interest-rate-sensitive sectors (housing and consumer durables) to begin to improve by summer and look for inventory rebuilding to add modestly to overall growth.

The economy retains its resilience. But resilience requires continuous adjustment—small corrections made at the right moments to keep the wings level as the air grows thinner. Over the weeks ahead, the skill with which policymakers navigate this narrowing runway will determine whether the economy glides its way into a soft landing or stalls out.

The Week Ahead: December 8-12

The government’s statistical agencies continue to play catch up but the Fed will have to make its decision relying on a mix of private, government and anecdotal reports. The Fed has enough information to make an informed decision.

Tuesday, December 9

NFIB Small Business Optimism (Nov): We are looking for a modest decline in Small Business Optimism, reflecting slowing and uncertain sales and stubborn cost pressures.

JOLTS Job Openings (Sep & Oct): The JOLTS report will provide a much needed update on the labor market. Look for a decline in job openings.

Wednesday, December 10

Employment Cost Index (Q3): We may see slightly more easing on wages, but benefits will likely hold firm. Overall, we look for the ECI to be up 3.6% year-to-year.

FOMC Statement & Powell Press Conference: We are looking for a hawkish quarter point cut, with three and possibly four dissents (one favoring a larger cut and two against any cut at all). Dissents mean less at this time, as a new Fed Chair will likely be announced ahead of the next FOMC meeting in January.

Thursday, December 11

Initial Jobless Claims (week ended Dec 6): Look for a rebound from last week’s holiday-shortened week decline.

Trade Balance (Sep): we are due for a widening in the trade deficit and look for imports to surge on inventory rebuilding and slightly more clarity on tariffs.

Friday, December 12

Fed Speakers: Philadelphia Fed President Paulson (2026 FOMC Voter), Cleveland Fed President Hammack (2026 FOMC Voter), Chicago Fed President Goolsbee (2025 FOMC voter).

Note: while regional Federal Reserve Bank presidents rotate voting roles by year, all members have a voice at every FOMC meeting.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 8, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

November ISM Services: Steady, Not Strong

Key Takeaways from November’s ISM Services Report

-

- Services PMI rose to 52.6, modestly above expectations and the 12-month average of 51.7, marking the ninth month of expansion in 2025 and implying roughly 1.3% annualized real GDP growth.

- Business Activity held at 54.5, its seventh reading above 54% this year, consistent with solid—but not spectacular—underlying demand.

- New Orders fell to 52.9 from 56.2, still above their 12-month average but clearly pointing to a softer fourth-quarter pipeline.

- Employment remained in contraction at 48.9, the sixth straight sub-50 reading, even as the index has edged higher since July.

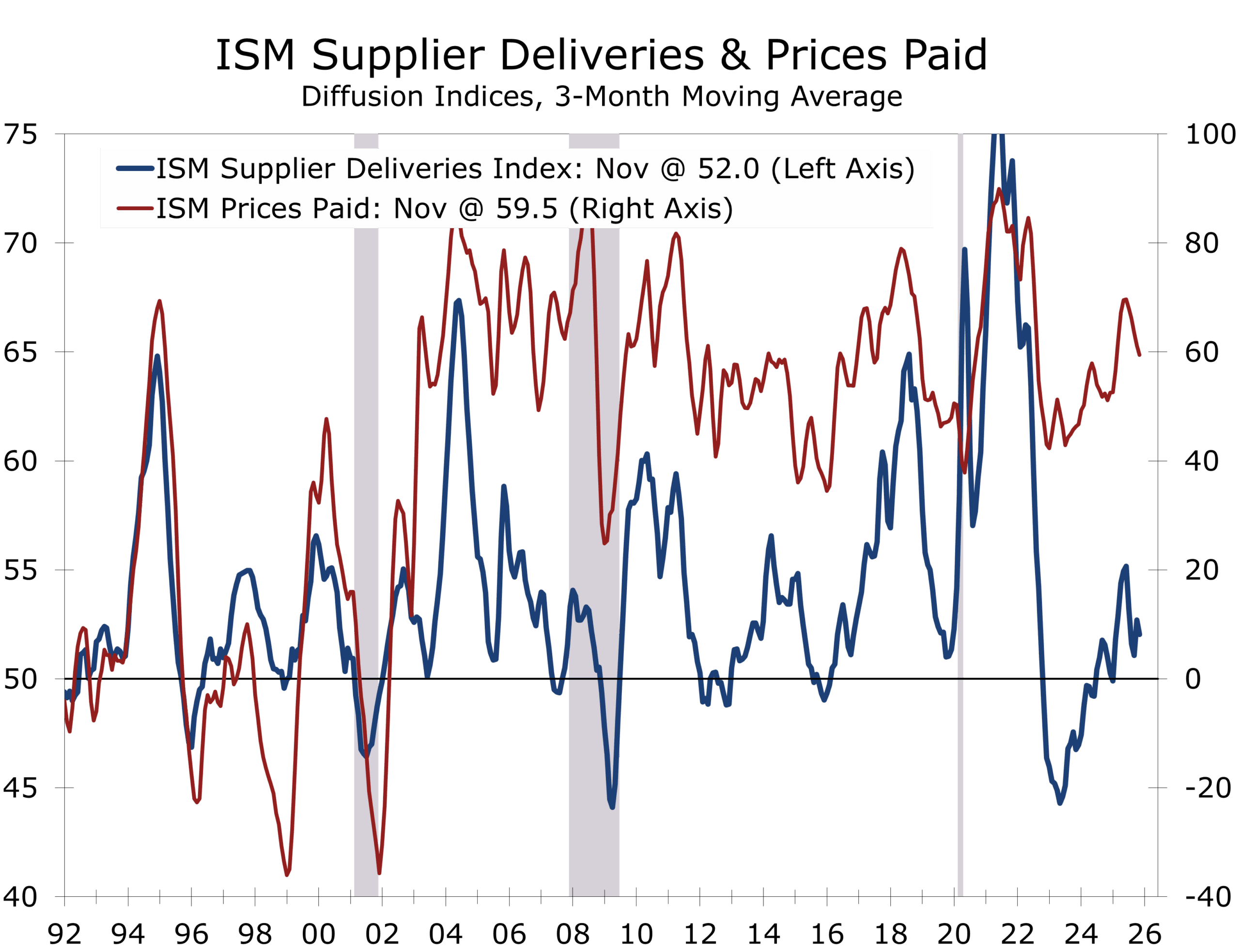

- Supplier Deliveries jumped to 54.1, the highest since late 2024, reflecting slower deliveries tied to tariffs, customs delays, the government shutdown, and air-traffic disruptions.

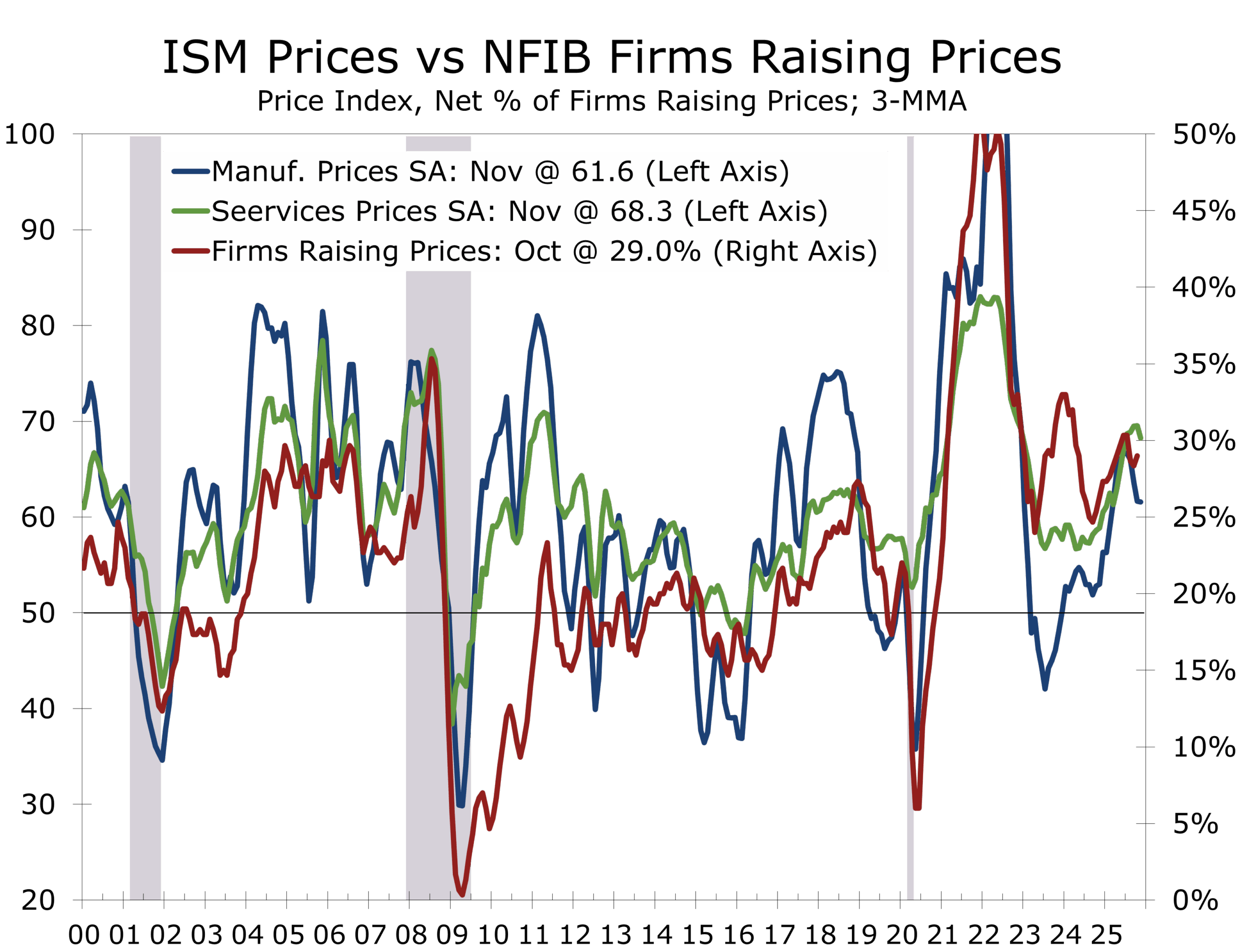

- Prices eased but stayed elevated: the Prices Index fell to 65.4, its lowest since April, but has now been above 60 for 12 straight months.

- Inventories returned to expansion at 53.4, and backlogs rebounded sharply to 49.1, the highest since February 2025, easing fears of a more abrupt slowdown.

- Breadth improved: 12 industries reported growth, while only five reported contraction.

- Overall tone: the services sector is still carrying the expansion, but the 12-month trend in the PMI has dropped more than 10 points since early 2022, underscoring a slower, narrower cycle.

Expansion Endures, Even as Underlying Currents Slow

The November ISM Services PMI® edged up to 52.6 from 52.4, modestly beating expectations and extending the services sector’s expansion for a ninth month this year. Historically, a reading above 48.6 is consistent with overall GDP growth, and November’s figure corresponds to roughly a 1.3% annualized gain in real output. The broader backdrop is less impressive. The 12-month average of the Services PMI remains stuck at 51.7, its lowest level since 2010, and more than 10 points below the 62.6 peak reached in February 2022. The expansion is intact, but the cycle has clearly downshifted from the roaring prints of the early post-pandemic period to something more akin to a late-cycle glide.

Solid activity, softer demand: Business Activity holds at 54.5 while New Orders drop 3.3 points.

Compositionally, the report reinforces that story of “steady, not strong.” The Business Activity Index held at 54.5, up a modest 0.2 point from October and above 54% for the seventh time in 2025, signaling that day-to-day output in the services sector remains in solid expansion. New Orders, however, told a cooler story. The index fell 3.3 points to 52.9. It is still in growth territory and sits nearly a point above its 12-month average, but the step-down points to a softer fourth-quarter pipeline. Respondents describe a split environment: big pharma is spending more aggressively than in the first half of the year, while other customers are pulling back or delaying commitments amid tariff uncertainty and mixed economic signals.

Backward-looking momentum is being cushioned by backlogs. The Backlog of Orders Index rose sharply to 49.1 from 40.8, its biggest monthly gain since mid-2022 and the highest reading since February 2025. Backlogs remain in mild contraction, but the rebound from very weak levels indicates that the worst of the backlog bleed may be behind us. In practice, that means firms still have enough work in the queue to buffer activity as new orders cool. New export orders remained in contraction at 48.7, the fifth straight sub-50 reading and the eighth this year, reflecting slower international demand and tariff-related frictions, even as some respondents reported a relatively strong fourth quarter in Europe.

Services Employment stayed in contraction at 48.9, the sixth straight sub-50 reading

The labor picture continues to transition from tight to merely firm. The Employment Index improved to 48.9 from 48.2, its highest reading since May but still in contraction for the sixth consecutive month. This run of sub-50 readings marks a clear shift away from the earlier era of pervasive labor shortages. Respondents noted that some firms are now “filling vacancies,” yet others still struggle to attract candidates, particularly for roles that require employees to be in the office. Employment increased in retail, accommodation and food services, wholesale trade, agriculture, health care, and utilities, but declined in mining, transportation and warehousing, management of companies and support services, public administration, construction, professional services, finance, and information.

When cross-checked against the November ADP data, which posted a decline of 32,000 private sector jobs in November, the ISM readings reinforce the conclusion that labor-market is softening is gaining momentum and broadening.

Price and cost dynamics remain one of the clearest constraints on policy. The Prices Index fell to 65.4 from 70.0, its lowest level since April and a welcome sign that the most intense pressure is easing. Yet prices have now been above 60 for 12 consecutive months, and 14 industries reported higher input costs in November, with construction the only sector reporting lower prices. Labor, software licensing, copper products, and steel were cited as up in price, while a handful of items—including gasoline, lumber, and engineered wood products—moved lower. On the parallel survey side, the S&P Global services PMI showed declines in both input and output prices, reinforcing a narrative of gradual disinflation rather than outright cost relief.

Prices are cooling at the margins, but firms continue to manage elevated cost

Inventories and inventory sentiment tell a story of cautious normalization. The Inventories Index returned to expansion at 53.4 after two months of contraction, with several respondents reporting that they are drawing down stocks after a quiet storm season or recalibrating inventories as trade deals are resolved. At the same time, the Inventory Sentiment Index stood at 54.8, indicating that many firms still view their inventories as “too high” relative to current business needs. That combination—modest inventory rebuilding alongside a persistent sense of excess—suggests that firms remain reluctant to carry much buffer and will continue to favor lean, just-in-time stock positions as long as demand remains choppy.

Supply conditions, meanwhile, have become more complicated. The Supplier Deliveries Index rose to 54.1 from 50.8, signaling slower deliveries for the 12th consecutive month and the highest reading since October 2022. A reading above 50 indicates worsening delivery performance, and respondents pointed squarely at tariffs and the federal government shutdown. Several noted items being stopped at borders or slowed by customs processing. The tragic UPS cargo plane crash on November 4 loomed in the background of the comments, a sobering reminder of the operational risks facing logistics providers as they move into the holiday shipping season.

Imports remained in mild contraction at 48.9, but the underlying narrative has shifted: rather than purely reflecting weak demand, the survey indicates that many firms are deliberately moving sourcing toward USMCA suppliers to mitigate steep tariffs on food, apparel, and electronics from Asia.

Breadth across industries improved modestly in November. Twelve out of seventeen services industries reported growth, including retail trade, arts and entertainment, accommodation and food services, wholesale trade, health care and social assistance, educational services, public administration, agriculture and related activities, finance and insurance, information, professional and technical services, and utilities. Only five industries—construction, real estate and rental and leasing, mining, management of companies and support services, and transportation and warehousing—reported contraction.

The respondent anecdotes bring this divergence to life. Retailers describe business as “strong, driven by customer traffic,” with stable pricing. Health-care systems report patient volumes leveling off, better fill rates in supply chains, less dependence on travel labor, and an overall optimistic outlook despite still-elevated costs. Construction and real-estate respondents, by contrast, highlight mortgage-rate headwinds and tariff pressures, framing the current slowdown as an “intentional pause” with margins expected to erode as competitors fight harder for fewer projects. In information and management services, tariffs, shutdown effects, and mixed macro indicators are fostering a more defensive stance heading into early 2026. Wholesale trade sits in between: respondents are bracing for margin compression as competition heats up, even as they anticipate higher lumber prices in 2026 due to reduced production.

From a macro perspective, the November report underscores a two-speed U.S. economy. The services sector, with a PMI of 52.6, remains in expansion and is modestly above its 12-month average. Manufacturing, by comparison, shows a PMI of 48.2, pointing to ongoing contraction. The services PMI has now held the line above 50 in nine of eleven months this year, but the trend has drifted steadily downward since early 2022, leaving the 12-month average at its lowest since the early 2010s. That profile is consistent with an expansion that has matured and slowed, yet remains intact.

For the Federal Reserve, the signal is nuanced but broadly supportive of a measured easing path. Growth is clearly slower than in the immediate post-pandemic rebound, but still positive. Labor demand is softening in services and outright weakening in manufacturing, yet there are no clear signs of a hard break. Inflation pressures are easing, but services prices remain elevated enough to keep policymakers wary of cutting rates too quickly. Layered on top of that, tariffs, trade re-routing, and episodic shutdown risk are now regular features of the operating environment rather than one-off shocks.

Against this backdrop, the November ISM Services report suggests that services will continue to carry the expansion into early 2026, but with less thrust than earlier in the cycle. New orders are cooling, employment is contracting modestly, and supply-chain and tariff frictions are still feeding into prices and delivery times. At the same time, business activity remains solid, backlogs have stabilized at more sustainable levels, and the breadth of growth across industries has widened slightly. The bottom line is that the economy is still growing, but the cycle is running at a lower gear—and policy, margins, and capital allocation decisions will need to adjust accordingly.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 3, 2025

Mark Vitner, Chief Economist

(704) 458-4000

November ISM Manufacturing: Demand Weakens Again as Production Advances while Hiring Retreats

Key Takeaways from November’s ISM Report

-

- Manufacturing PMI®: 48.2 (–0.5 pts) — ninth consecutive month of contraction; breadth of softness widened modestly.

- New Orders: 47.4 (–2.0 pts) — third straight contraction as demand remains uneven.

- Production: 51.4 (+3.2 pts) — returned to expansion, supported by improved component flow and backlog conversion.

- Employment: 44.0 (–2.0 pts) — headcount reductions deepened amid ongoing caution.

- Supplier Deliveries: 49.3 (–4.9 pts) — faster deliveries, signaling ample capacity and fewer supply chain constraints.

- Prices Paid: 58.5 (+0.5 pts) — input costs rose again, driven by metals and tariff-affected imports.

- Inventories: 48.9 (+3.1 pts) and Customers’ Inventories: 44.7 — both remain lean, but firms remain hesitant to rebuild.

- Order Backlogs: 44.0 (–3.9 pts) — pipelines remain thin heading into year-end.

- November’s PMI® corresponds with roughly +1.7% annualized real GDP, consistent with continued overall economic expansion.

Supply Chains Steady, Demand Slips, and Managers Remain Guarded

The ISM Manufacturing PMI® slipped to 48.2 in November, marking a ninth month of contraction and reinforcing the sector’s struggle to regain traction. Readings below 50 reflect breadth of deterioration, not magnitude, and the latest figure remains consistent with a manufacturing sector treading water while the broader economy continues to expand.

November’s report once again displayed the now-familiar pattern: demand softened, production improved, employment contracted, and supplier deliveries accelerated, suggesting that capacity is more than adequate. Input costs remain elevated, with Prices Paid rising to 58.5%, though the tariff-driven run-up appears to be losing momentum, and respondents signaled that cost pressures are starting to ease around the edges.

Production Rebounds, but Orders Slide as Uncertainty Keeps Managers Cautious.

New Orders fell 2 points to 47.4, contracting for a third straight month, while Employment dropped to 44.0, its lowest level since August. Production, however, bounced back into expansion at 51.4, reflecting improved parts availability and execution of previously delayed orders. Inventories rose modestly but remained in contraction, and Customers’ Inventories stayed at “too low” levels, a historically supportive signal once confidence improves.

Despite the weaker PMI, several regional Fed manufacturing surveys report a guarded optimism that 2026 may bring steadier demand and fewer tariff disruptions. For now, manufacturers remain cautious but not pessimistic.

Manufacturers Are Navigating a Two-Speed Cycle

- Demand for goods is weakening, with New Orders, Backlogs, and New Export Orders all in contraction.

- Production is expanding, helped by supply-chain stabilization and conversion of existing orders.

- Employment is contracting faster, as firms preserve liquidity and avoid adding capacity into an uncertain environment.

Panelists again cited tariff volatility, policy uncertainty, shifting international regulations, and inconsistent external demand as central challenges. Nearly two-thirds of manufacturers continue to manage headcount lower, relying on attrition, selective layoffs, and more disciplined labor deployment to boost productivity and protect margins.

Rising jobless expectations signal a softer market for lower-wage and entry-level workers.

Firms continue to operate in a defensive configuration — emphasizing cash-flow discipline, flexible staffing models, streamlined supplier portfolios, and reduced forward commitments. With backlogs thinning further, the sector lacks the “cushion” needed for a near-term snapback in production should orders remain soft.

The uncertainty that defined October became more visible in November. Respondents highlighted:

- Tariff-driven cost volatility in metals, electrical components, and engineered materials.

- Longer import transit times, even as aggregate supplier performance improved.

- Sourcing shifts and planning challenges tied to reciprocal trade actions and compliance changes.

- Lingering shutdown effects in agriculture, transportation equipment, and regulated industries.

- Offshore production adjustments, where firms sought ways to blunt tariff exposure.

The unifying theme: uncertainty, not collapsing demand, remains the dominant headwind and continues to reinforce a “wait-and-see” posture for inventories, hiring, and capital allocation.

Consumers remain cautious—but they’re still spending, prioritizing value and essentials.

The Prices Paid index increased to 58.5, marking the 14th consecutive month of rising costs. Metals (aluminum, copper, hot-rolled steel), critical minerals, and advanced electronics components continue to exert upward pressure. Top of Form

Respondents noted:

- Tighter supplier bases in some materials

- Longer lead times for specialized components

- Elevated landed costs due to tariff structures

- Limited availability of rare-earth magnets and electronic components

While the rate of increase has slowed relative to earlier spikes, cost stickiness remains a challenge, encouraging firms to maintain lean inventories and selective purchasing — a quiet signal to supply-chain teams that diversified sourcing and tighter contract windows may carry outsized strategic value.

Customers’ Inventories rose slightly to 44.7, still firmly in “too low” territory, a condition that historically precedes production upturns once sentiment turns. Inventories increased modestly to 48.9 but remain constrained by caution rather than capacity.

These dynamics mirror the backdrop from October: lean inventories could support a restocking cycle, but policy uncertainty — not supply chains issues — is keeping that demand on hold.

Backlog weakness reinforces that narrative. The Backlog of Orders Index fell to 44.0, its softest reading since spring, signaling minimal near-term lift for production.

Sector Breadth and Structural Takeaways

Four industries expanded in November:

Computer & Electronic Products; Food, Beverage & Tobacco; Miscellaneous Manufacturing; and Machinery.

Eleven contracted, including Apparel, Wood Products, Paper, Nonmetallic Minerals, Fabricated Metals, Chemicals, Petroleum & Coal, Transportation Equipment, and Plastics & Rubber.

The strongest sectors continue to reflect:

- Semiconductor and electronics ecosystems

- Food and beverage, supported by stable consumption

- Machinery and automation, driven by targeted investment in efficiency

Weaker sectors remain concentrated in:

- Construction-related inputs

- Tariff-affected intermediates

- Durables and transportation equipment, where planning visibility remains murky

The breadth of contraction is meaningful but not accelerating, aligning with a sector undergoing incremental adjustment rather than acute decline.

Inventories and Customers’ Inventories Signal Room for Restocking — When Confidence Returns

The November ISM report points to a manufacturing economy navigating a slow-moving adjustment, not a recession. The challenge remains the same as in October: low visibility, variable costs, and policy volatility are suppressing risk-taking at a time when inventories and customer stock levels would ordinarily support a modest rebuild.

The combination of thin backlogs, lean customer inventories, still-elevated input costs, and heightened geopolitical and trade friction, suggests that stabilization is possible in early 2026 if policy clarity improves. Until then, manufacturers are likely to remain defensive, focusing on flexibility over scale and liquidity over expansion.

Implications for the Federal Reserve

The ISM Manufacturing report neither accelerates nor derails the Fed’s path. While the factory sector is contracting at a slightly faster pace, the overall economy is still growing modestly, consistent with our Q4 real GDP forecast at 1.7%. This supports the view that near-term rate cuts should be approached cautiously, not urgently, and that manufacturing will not be a source of renewed inflation pressure without a significant shift in policy or trade conditions.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 1, 2025

Mark Vitner, Chief Economist

(704) 458-4000

The Piedmont Perspective: Societies Fray Gradually, Not Suddenly

A Tragedy in Washington and the Quiet Work of Resilience

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Signals, Softness, and the Shifting Center of Gravity

Highlights of the Week

- The Beige Book confirms softer labor demand, more cautious consumers and producers, and still-resilient capital spending that continues to justify lower rates.

- Investment momentum remains the cycle’s backbone, led by AI infrastructure, aerospace, energy and industrial buildouts.

- Early holiday shopping began with heavy foot traffic but lighter spending per person, suggesting a mixed and highly value-conscious start to the season.

- ADP’s latest high-frequency data show a four-week average loss of private-sector jobs, raising concerns about a faster cooling labor market.

- Russia–Ukraine enters a dangerous winter phase with diminishing diplomatic traction, raising spillovers for Europe, energy and the U.S.–China strategic calculus.

- A new international investment initiative signals a pivot toward “diplomatic deal-making,” turning global capital flows into geopolitical tools.

- Markets remain hypersensitive to incremental data as traders balance falling inflation against uncertainty about how quickly the Fed can ease.

A Market Searching for Confirmation

Financial markets spent the week parsing signals in an environment where the broad story is already understood. Inflation is cooling. The labor market is losing momentum. The Fed is preparing to cut, while remaining cautious about moving too quickly or signaling that it is adopting a more aggressive path. Treasury yields drifted lower following a steady run of dovish remarks from Fed officials. Equities maintained a measured upward bias.

Investors seek confirmation rather than direction. Data continue arriving in fragments—cooler in some places, firmer in others—yielding a narrative that is neither recessionary nor exuberant, but transitional to a lower trajectory. The economy continues to be driven by capital spending, innovation and productivity while households and employers step back from the confidence they carried earlier in the year.

A market in transition: cooling inflation, cooling labor, and investors waiting for proof.

Private data broadly reinforce this more cautious backdrop, with hiring and consumer sentiment slipping further. Anecdotal evidence from the Beige Book and from retail earnings calls echoes the same themes: caution at the register, a sharper tilt toward value, and a resilient core that is carrying more of the load.

The Beige Book’s Quiet Signal: Softer Labor, Cautious Consumers, Capital Still in Command

The Fed’s latest Beige Book strengthened the case for lower rates by underscoring a cooling labor market and a more guarded consumer. Districts reported slower hiring plans, easing wage pressures, and early indications that workers feel less invulnerable than they did in the spring. Retailers and manufacturers noted lighter traffic, thinner order books, and a noticeably defensive posture heading into year-end.

The Beige Book shows a labor market that is cooling, not cracking.

The path forward is not as simple as the data suggests. While the case for easing is convincing, lower rates would almost certainly invigorate financial markets and intensify capital spending—risking a renewed bout of asset inflation at a moment when the Fed is trying to guide the economy toward a softer glide path rather than an upswing in speculative momentum.

Capital investment remains the economy’s stabilizing force. Long-cycle projects—most notably AI infrastructure, energy systems, aerospace, and industrial equipment—continue to provide ballast as other sectors cool. A shift to lower financing costs would likely accelerate this capital-intensive expansion, though potentially at labor’s expense.

A Kansas City contact remarked that it is “a great time to get a tattoo,” because top artists once booked months ahead suddenly have availability. Workers likely feel a little more self-conscious and less secure about the job market. That is certainly what the data show. Consumer confidence is breaking lower and consumers are becoming increasingly selective.

A Mixed Start to the Holiday Shopping Season

Early retailer feedback and high-frequency trackers suggest the holiday season got off to a strong start on Friday and Saturday. Retailers described crowded stores and active browsing, but conversions were uneven and heavily reliant on promotions. While sales came in at the high end of expectations, shoppers leaned into discounts, prioritized essentials and shied away from expensive discretionary purchases.

This year’s holiday shopping season is defined by large crowds and a discerning consumer.

The tone is value-oriented and price-sensitive. Yet retailers are said to be going into the relatively short traditional holiday shopping season with fewer promotions. This unusual discipline will likely prove short-live and we look for promotions to increase, which will boost volume but compress margins.

The shift mirrors the Beige Book message: the consumer is still engaged but increasingly cautious. The economy is no longer consumer-led; momentum has shifted toward investment and productivity.

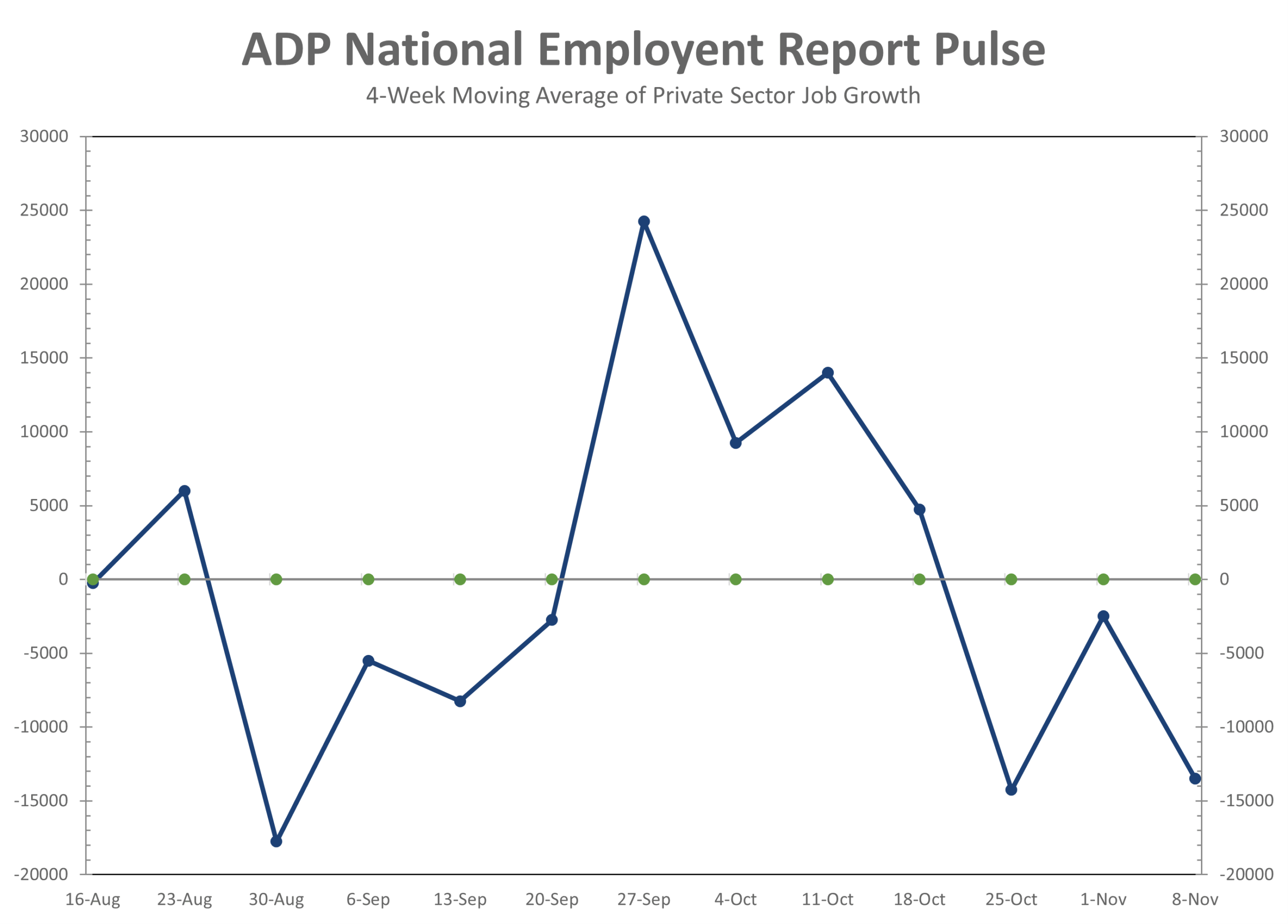

ADP Labor Data: A Clear Warning Signal

ADP’s latest NER Pulse report shows that private-sector employers shed an average of 13,500 jobs per week over the four weeks ending November 8. This four-week moving average is the weakest stretch in many months and suggests that labor-market softening is accelerating beneath the surface.

The contraction was broad-based across goods and services. The decline carries heightened significance given the Fed’s comfort with the ADP series and the lack of fresh BLS data ahead of the December meeting. For investors and policymakers, this is the clearest early-warning signal yet that labor-market cooling may be further along than widely acknowledged.

The government shutdown exerted a larger than expected drag on the economy.

Government Shutdown Ended Just in Time

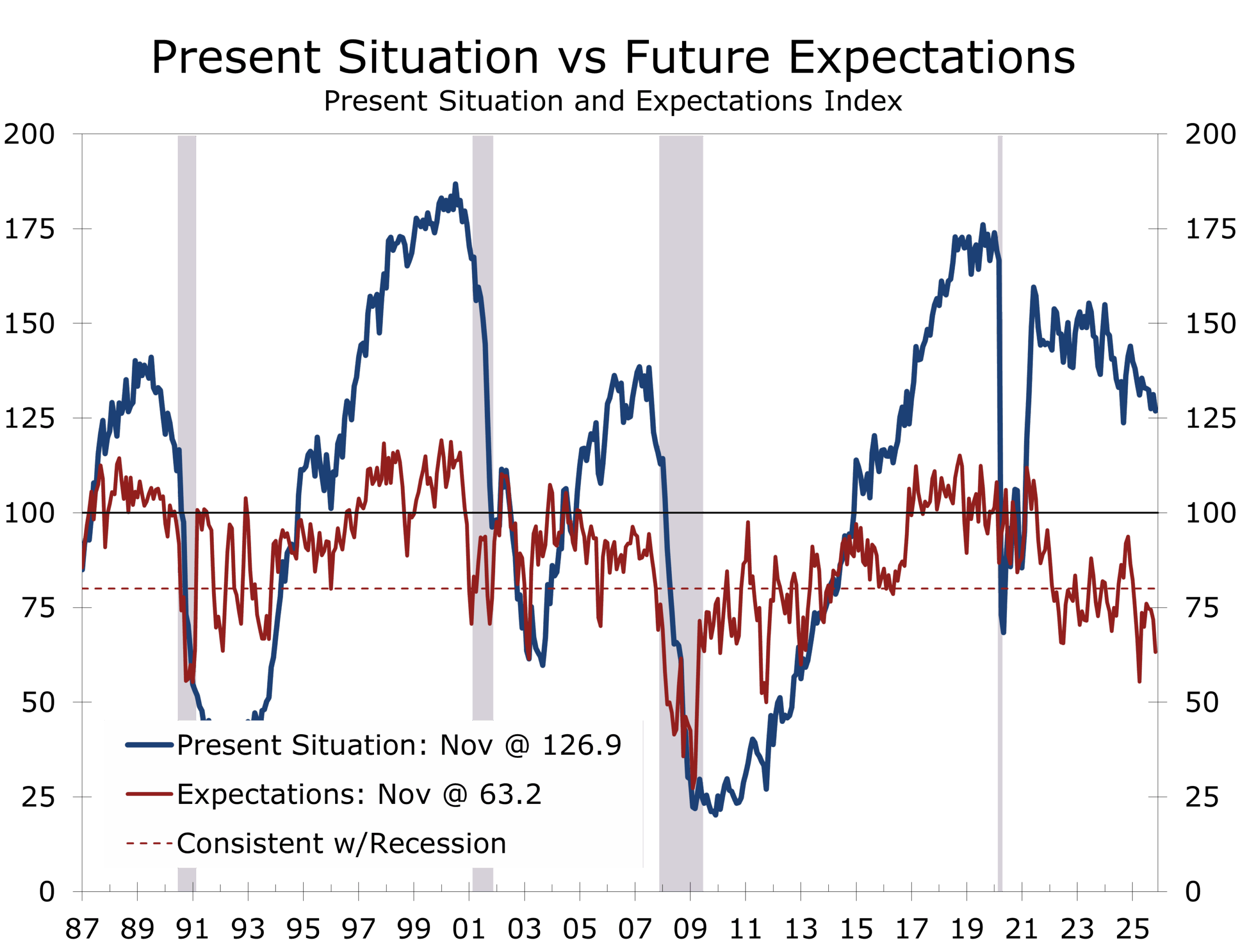

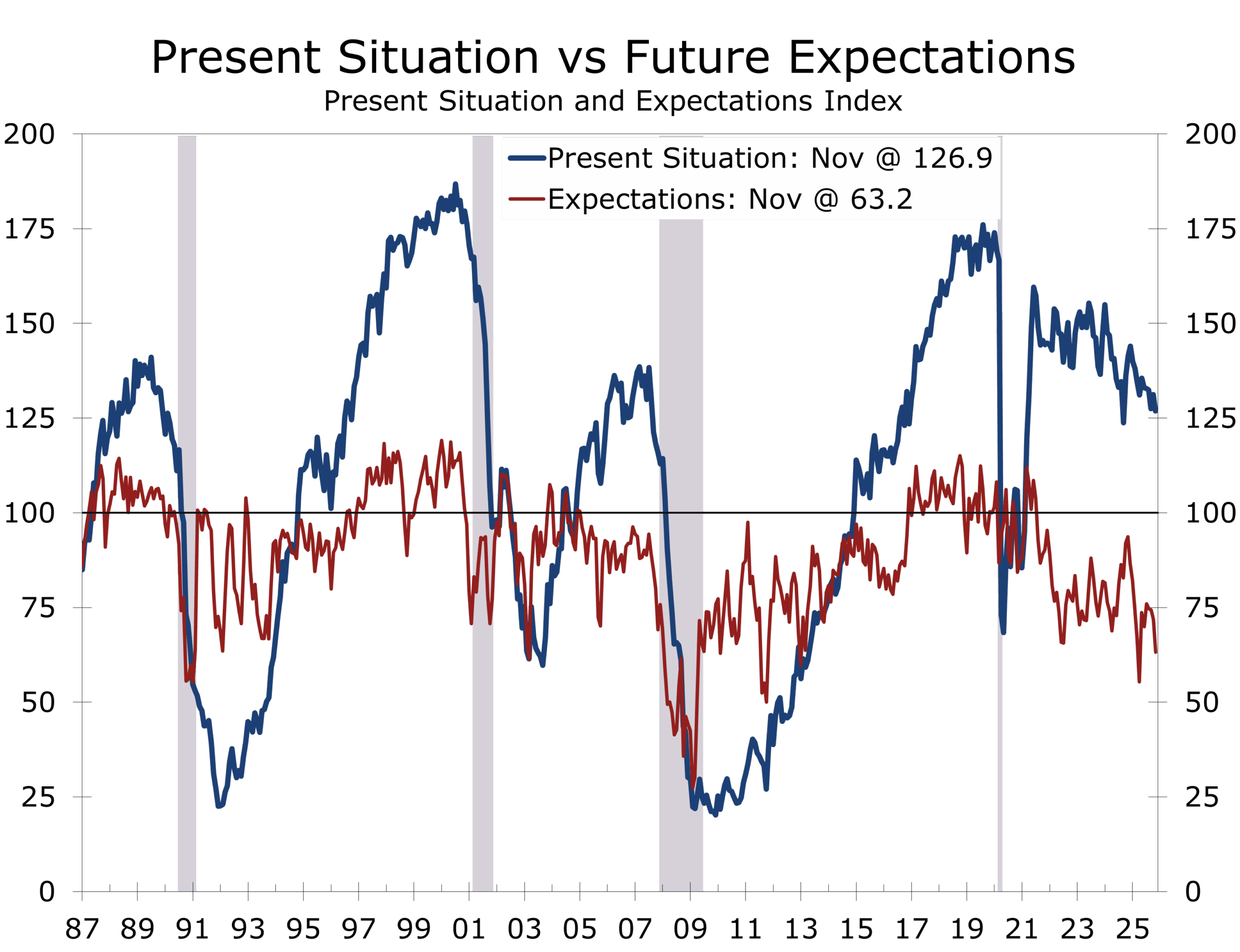

Consumer confidence fell to 88.7, its weakest reading since April. The 43-day federal shutdown, increased layoff announcements, equity volatility, and persistent concerns over inflation dominated write-in responses. The Expectations Index fell to 63.2, its tenth straight month below the recession-signaling threshold of 80.

Sentiment deteriorated across all major demographic and political groups. Big-ticket buying plans slipped, and service-spending intentions weakened. Spending grew solidly in Q3 but now looks more guarded.

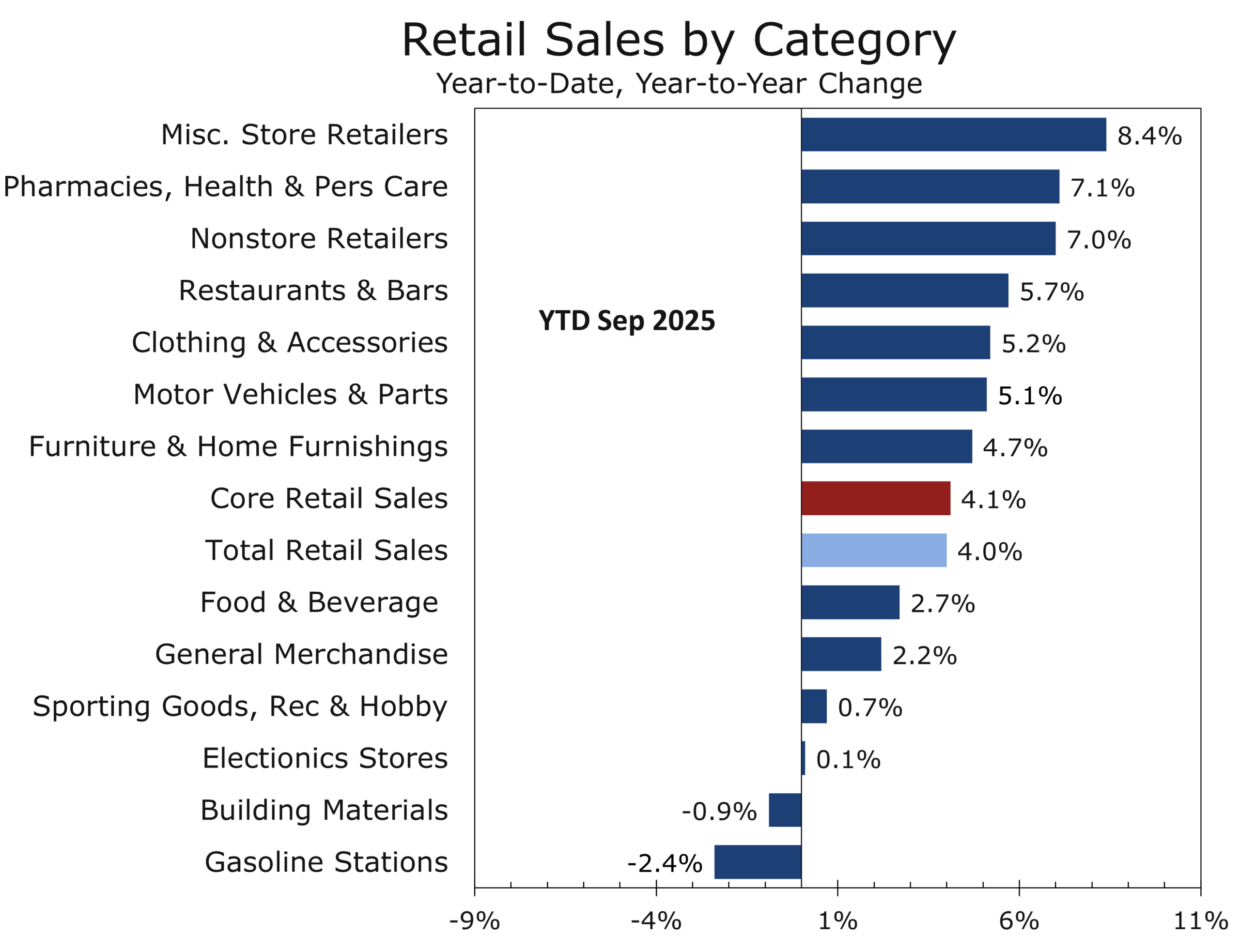

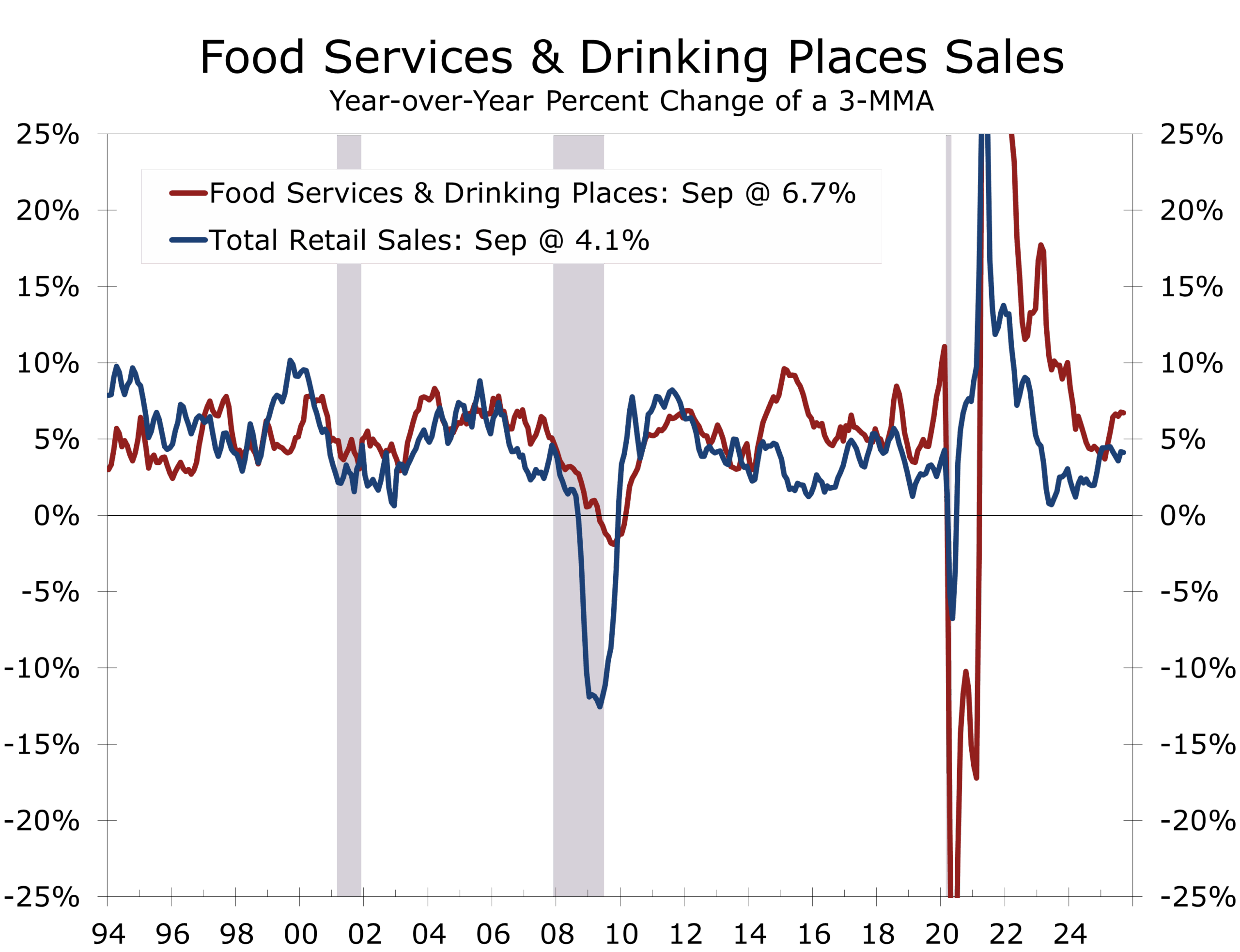

Spending ended Q3 on a weak note, with retail sales rising just 0.2% in September—essentially flat in real terms. Goods categories weakened broadly (electronics, nonstore retail, sporting goods, apparel), while spending in food services (restaurants and bars) rose 0.7%, personal care (+1.1%) and miscellaneous retailers (+2.9%) provided stability.

Control-group sales fell 0.1%, reflecting shifting consumer preferences. The “K-shaped” profile persists. Higher-income households continue to spend mostly on services and experiences, while middle- and lower-income households increasingly ration discretionary purchases. This split extends to restaurant dining as well, with fast food and limited service chains seeing slower sales and diminished pricing power, but sales and prices both rising at full service restaurants, particularly at the upper end.

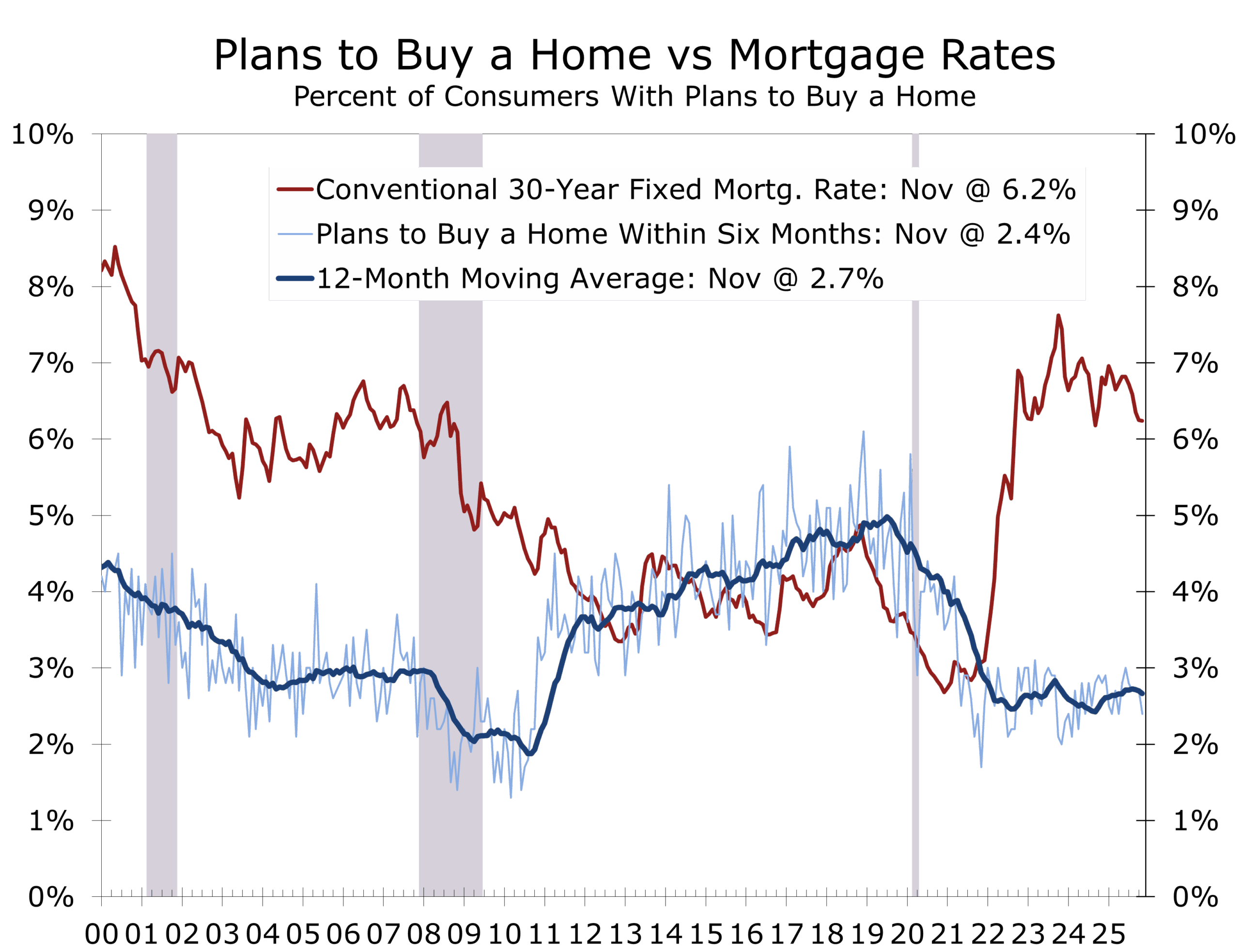

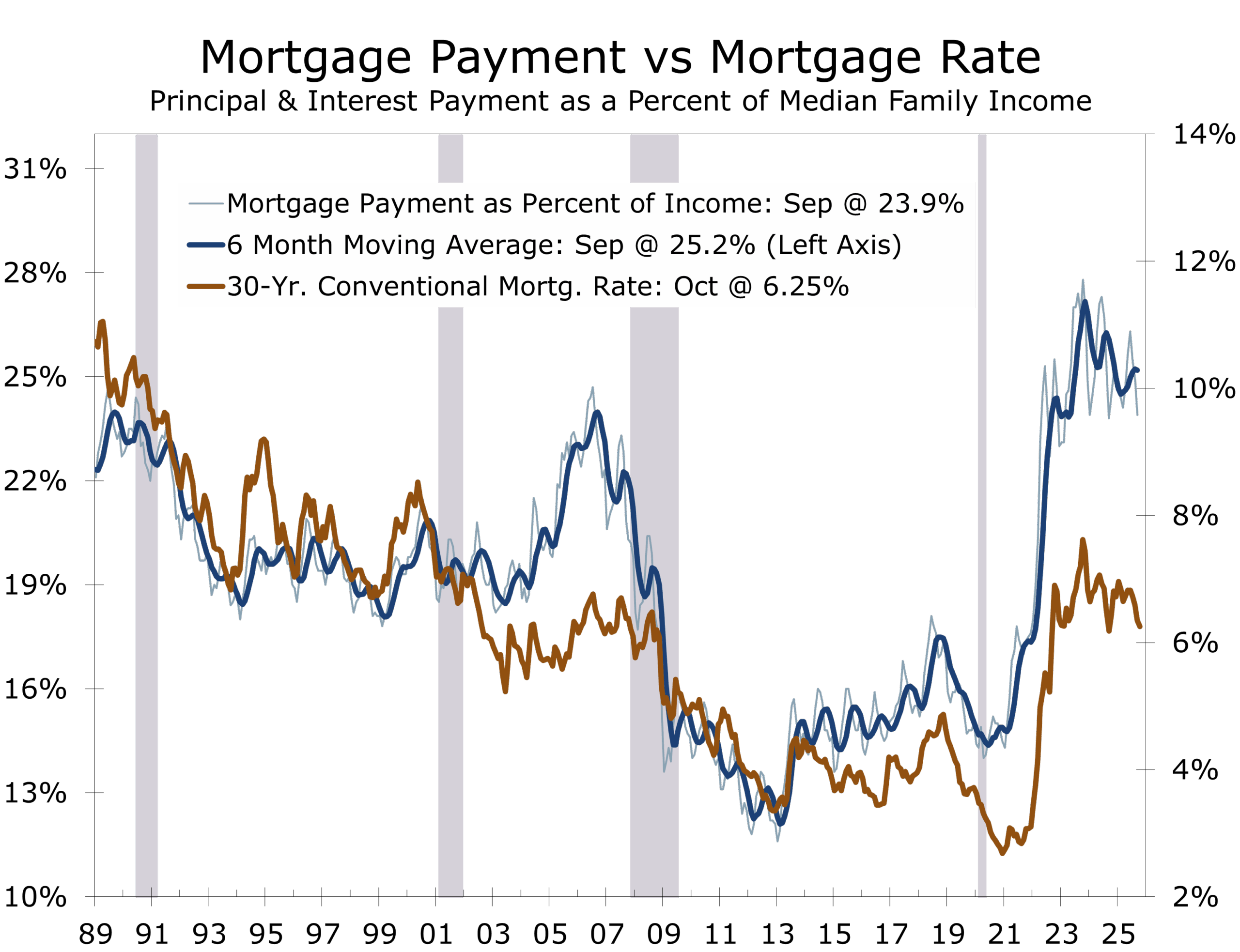

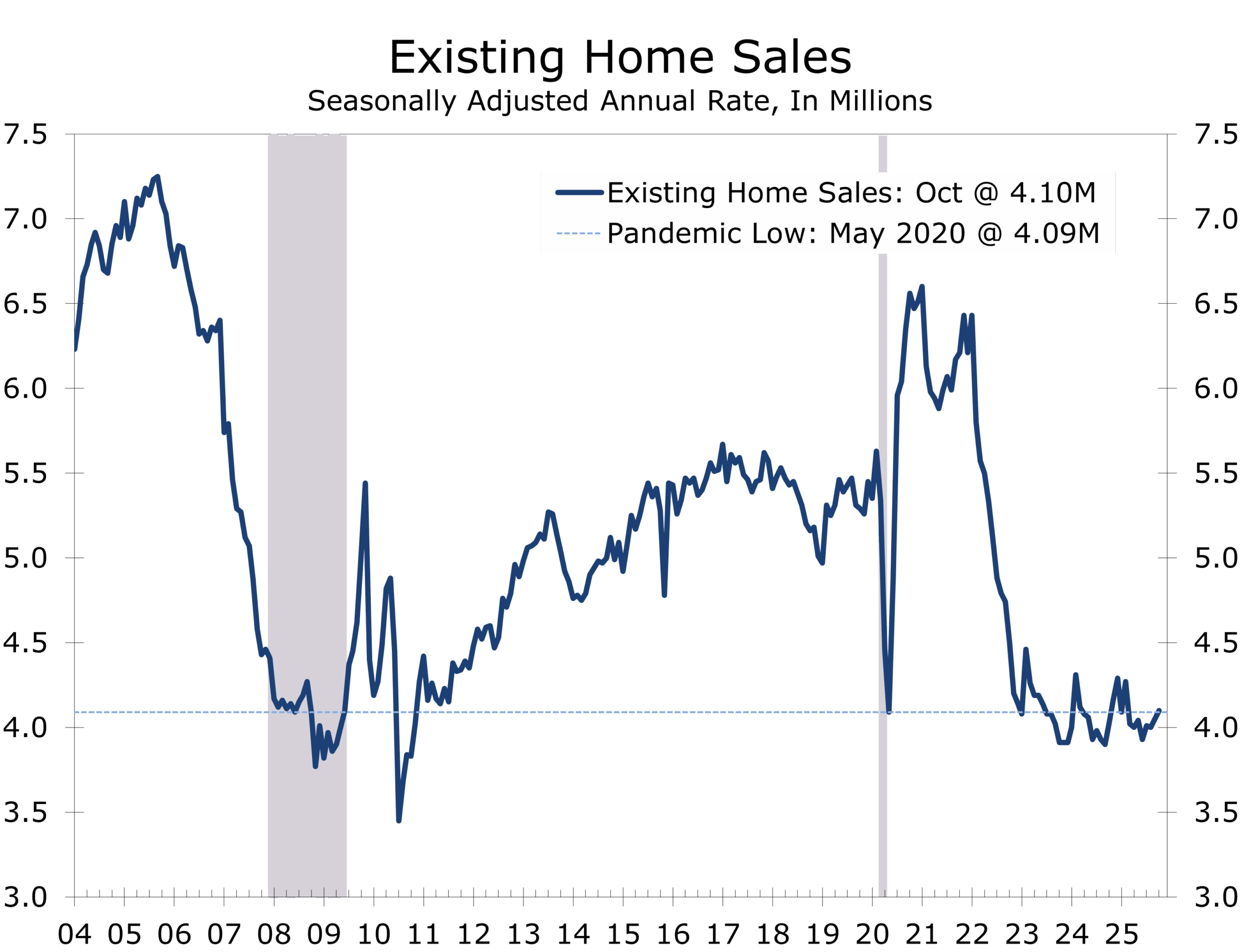

Housing affordability remains stretched, which is keeping a low ceiling on home sales.

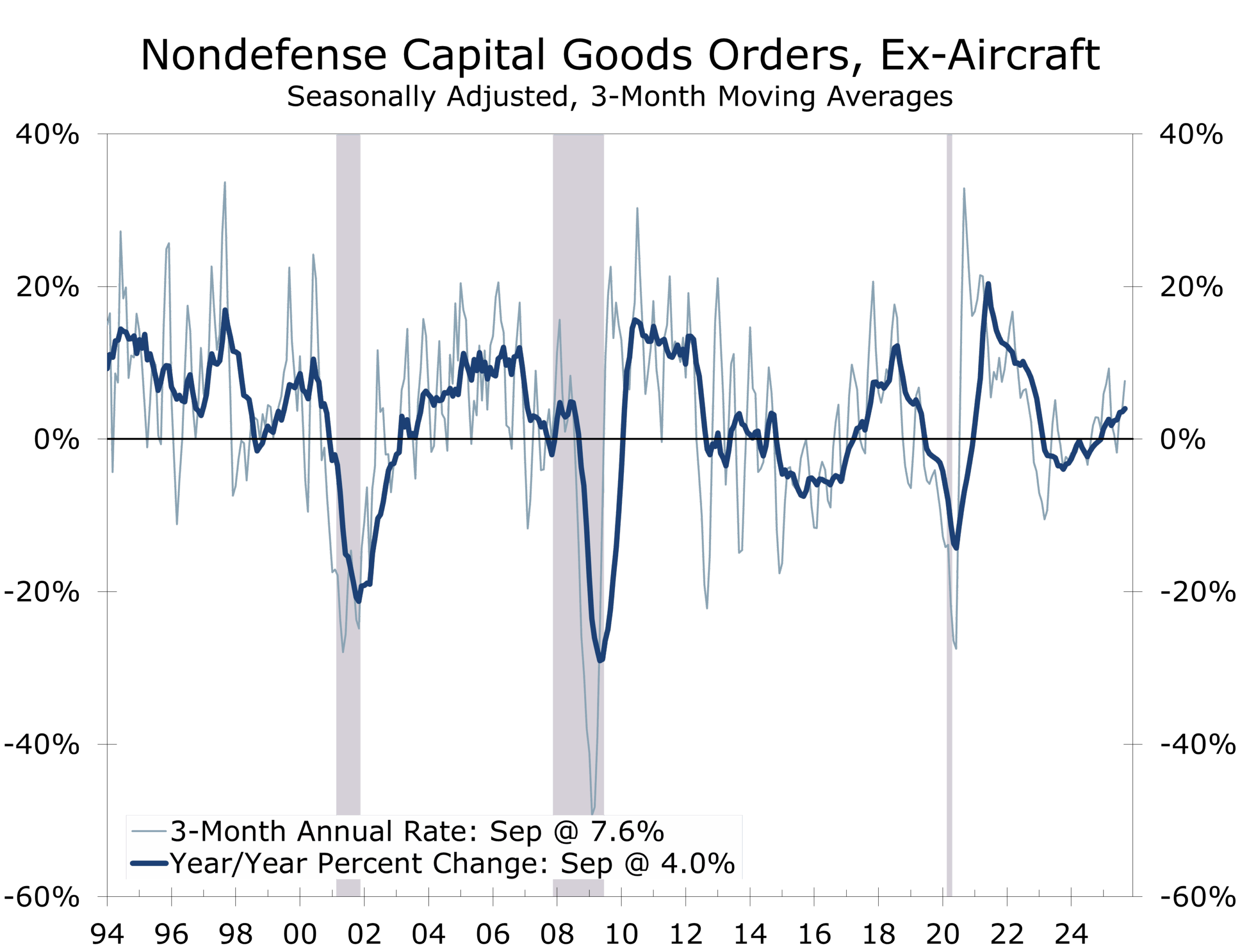

AI-Led Capex Continues, but Shipments Slow

Durable goods orders rose 0.5%, supported by a second consecutive 0.9% increase in core orders. Strength remains concentrated in AI-adjacent categories such as information-processing and electrical equipment. But shipments slowed sharply, pushing Q3 equipment investment growth down to 3.1% from 8.5% in Q2. The slowdown caused many forecasters to trim their Q3 GDP estimates.

Corporations continue to benefit from wide margins and low credit spreads. Now, with interest rates falling and expected to remain lower in 2026, we expect the recent strength to broaden beyond AI. Productivity enhancing investment is likely to be pursued by producers of consumer goods, with reshoring efforts becoming more apparent.

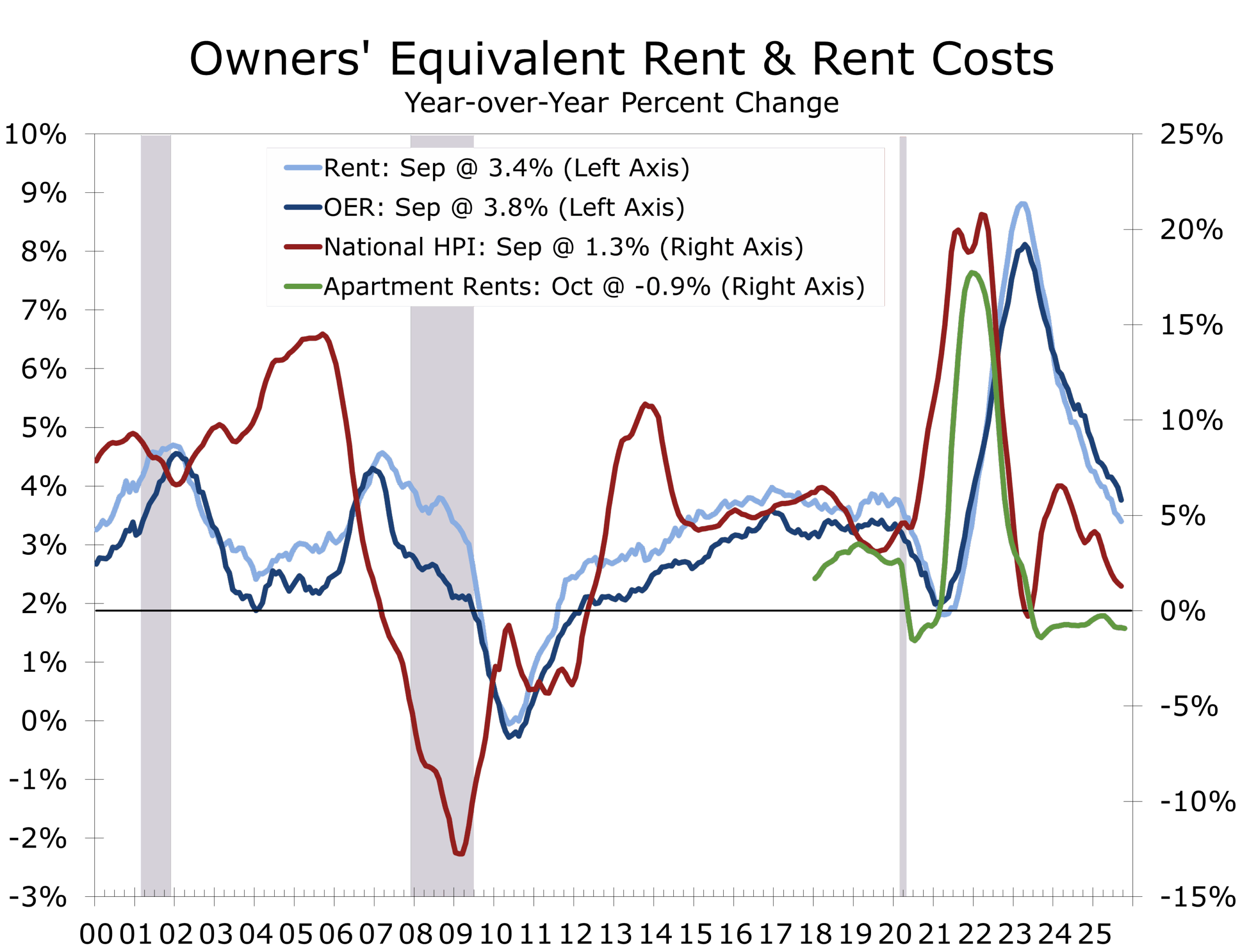

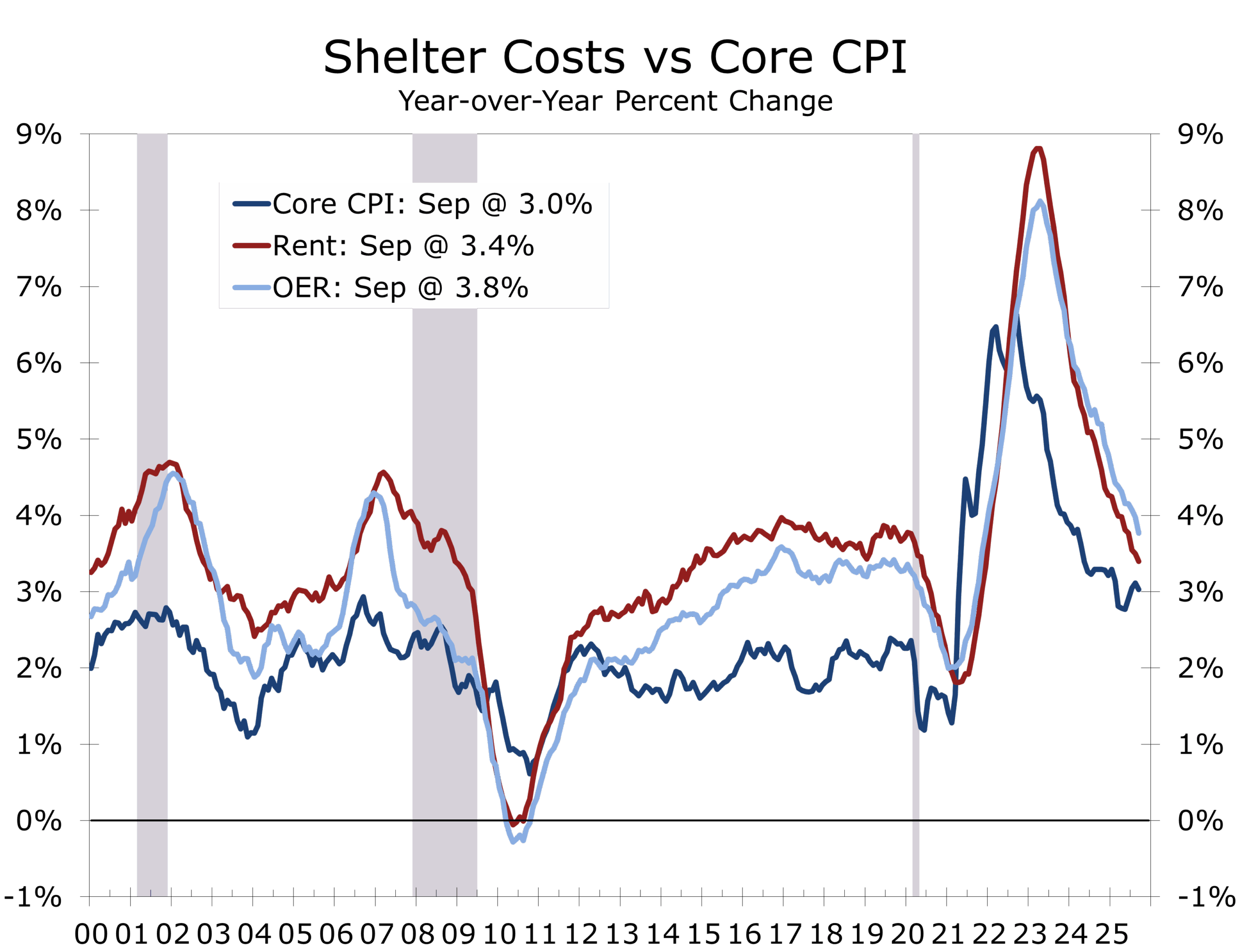

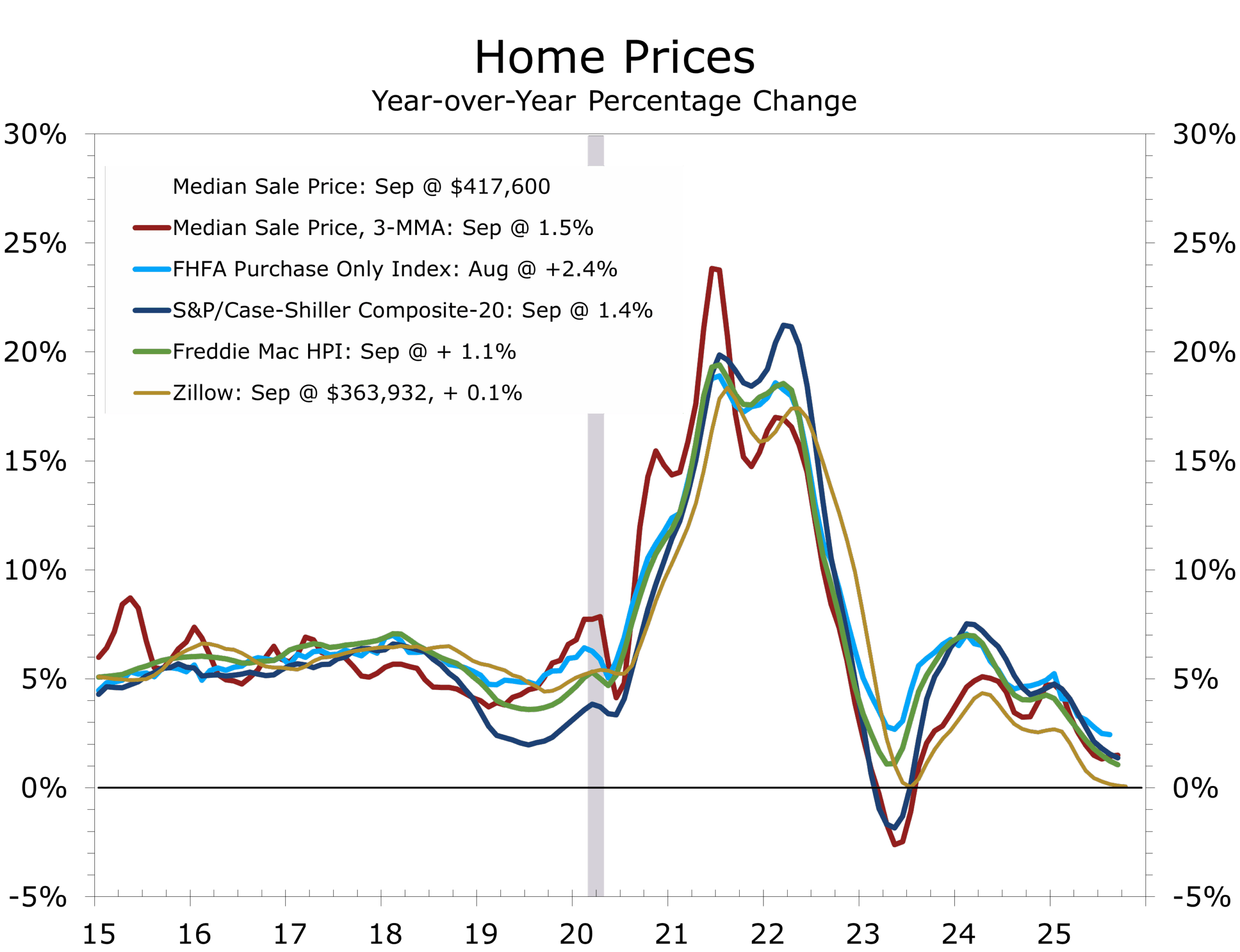

Home Prices: Broad Cooling and Shelter Disinflation

National home prices rose just 1.3% over the past year and fell 0.3% month over month in September. All 20 major metros posted monthly price declines (NSA), with Tampa (-4.1% y/y), Phoenix, Dallas and Miami leading the downturn.

Residential rents tend to follow home prices, which means core inflation is headed lower.

Home price growth is expected to fall below 1% before rebounding in mid-2026 as rates decline. The cooling points to shelter inflation decelerating toward 3% by year-end 2026, a key disinflationary tailwind for the coming year. Shelter accounts for just over 44% of the core CPI, so that deceleration should become readily apparent and help bring headline and core inflation back in line with the Fed’s long-run goal.

PPI: Energy-Driven Rebound, Core Remains Mild

Producer prices rose 0.3% in September as a rebound in wholesale gasoline prices and higher beef prices lifted the headline. Final demand goods advanced 0.9%, the largest gain since February. About 60% of the increase came from gasoline, which surged 11.8%. Energy overall rose 3.5%, food increased 1.1%, and goods excluding food and energy edged up 0.2%. Beef and meats strengthened, along with residential electric power and motor vehicles, while fresh vegetables and nonferrous ores declined.

Final demand services were flat, as a 0.2% drop in retailer and wholesaler margins offset firmer readings in transportation and warehousing (+0.8%) and a modest uptick in services less trade and transportation. Airline fares jumped 4.0%, while margins for machinery and equipment wholesaling fell 3.5%, and portfolio management fees declined 1.2%.

Taken together with the earlier reported CPI, the data imply inflation remain relatively contained in September. The overall PCE deflator likely rose 0.3%, while the core likely rose 0.2%

Fixed Income: Lower Yields, Higher Cut Odds

Treasury yields ended the week 7–9 basis points lower as markets priced in a higher probability of a December rate cut following dovish signals from New York Fed President Williams. Mortgage-backed securities widened on expectations of increased volatility, and primary dealer Treasury holdings climbed to a record $604 billion, highlighting strong demand for duration in a thin-data environment. For funding managers, the message is clear: fixed-income markets remain range-bound heading into the FOMC meeting and a compressed holiday issuance calendar, but positioning is shifting toward rate-cut readiness. Funding conditions are stable, liquidity remains ample, and the window for opportunistic terming-out of debt is still open, although it may narrow quickly once the Fed’s path becomes clearer.

A Winter of Attrition and Narrowing Diplomacy

This winter is shaping up to be one of higher military tempo and shrinking diplomatic opportunity. Ukraine continues to ration artillery and drones, leaning on asymmetric strikes and localized counter-offensives, while Russia presses along multiple fronts and employs increasingly sophisticated Iranian-style drone swarms. President Trump had repeated stated his desire for a peace deal by Thanksgiving and is now probably striving for Christmas or yearend. A poorly structured settlement, however, would risk setting a precedent that could haunt Europe, the United States, and Asia for years to come.

America’s geopolitical bandwidth is fully subscribed, as risks are increasingly intertwined.

Europe’s energy position is stronger than it was in 2022, but its political cushion is notably weaker. Fiscal strains, demographic pressures, and rising populism are chipping away at cohesion. For the United States, the stakes run through two major channels. First, China’s Taiwan calculus: Beijing is studying Ukraine closely as a sandbox for sanctions resistance, supply-chain rerouting, and attrition warfare. Japan is watching with equal urgency. Second, Middle East stability: regional tensions from Syria to the Gulf continue to simmer, with Israel repeatedly disrupting rearmament efforts by Hezbollah and Hamas.

Piedmont Perspective

“Societies fray gradually, not suddenly.” — Tolstoy

The tragic shooting of two National Guard troops in Washington this week is a reminder of how thin the seams of American public life have become. These were young Americans serving in the capital, far from any battlefield, yet caught in the undertow of a society that feels more strained and brittle than it did only a few years ago.

Tolstoy’s A Confession offers an unsettling parallel. Writing in 1882, he warned of a “corrosion of spirit,” a gradual loss of meaning and connection that takes hold as trust erodes. Societies rarely break in a single dramatic moment. They often come apart slowly, thread by thread, as small tears go unattended and the bonds that once held communities together weaken through neglect, fatigue, or indifference.

The erosion of societal norms rarely announces itself. It begins subtly through frayed trust, rising cynicism, and quiet withdrawals from community long before it becomes visible in headlines or data.

The pressures visible today follow that pattern. Economic strains linger even as the broader economy shows resilience. Institutional missteps and political volatility have fed a deeper sense of skepticism. Inequality continues to shape how people experience opportunity and stability. On top of this sits an information environment built for speed and outrage. Social media, partisan echo chambers, and parts of the press often reward provocation over clarity. This dynamic does not cause violence by itself, but it increases isolation, weakens judgment, and makes the cracks in society more difficult to repair.

None of this reduces individual responsibility or simplifies the complexity of a single act. It does, however, form the context in which too many people now struggle with belonging, purpose, and confidence in their institutions. The sense of drift is widespread across demographic, regional, and political lines.

Tolstoy did not write to encourage despair. His goal was to highlight the need for repair and renewal. Resilience comes from the basic ties that make a society work: trust built in small interactions, communities that extend beyond politics, institutions that act transparently and with restraint, and citizens who view themselves as stewards of the wider republic rather than spectators to it.

Resilience is rebuilt the same way it frays: gradually. Small acts of trust, service, and accountability reverse the drift.

A quieter point sits underneath all of this, and it carries economic relevance. Markets may focus on inflation prints, labor data, and the next move from the Federal Reserve, but confidence does not exist in a vacuum. A society that feels strained or disconnected becomes more sensitive to shocks and more reactive to uncertainty. The same “erosion of norms” that weakens civic life also shows up in survey data, consumer behavior, and risk appetite. This past week’s declines in confidence and more selective holiday spending fit that pattern.

As we sift through the latest economic signals, it is worth remembering that the country’s real strength has never been measured only in GDP releases, employment reports or by the shape of the yield-curve. It comes from the people who show up each day. It comes from workers and soldiers, first responders and teachers, public servants and small-business owners, as well as families and communities that create the quiet foundation of civic life.

We honor the two Guardsmen, one who lost her life and one who continues to fight for his, by remembering that our institutions endure because free citizens build them, protect them, and hold them accountable. That commitment to a free society remains the quiet engine of American resilience. It is not the businesses or institutions themselves that define our strength, but rather our capacity to create, renew, and reinvent them. At a time when the headlines lean toward division, it is this shared responsibility that gives the country its greatest advantage and helps steady the broader economy when uncertainty rises.

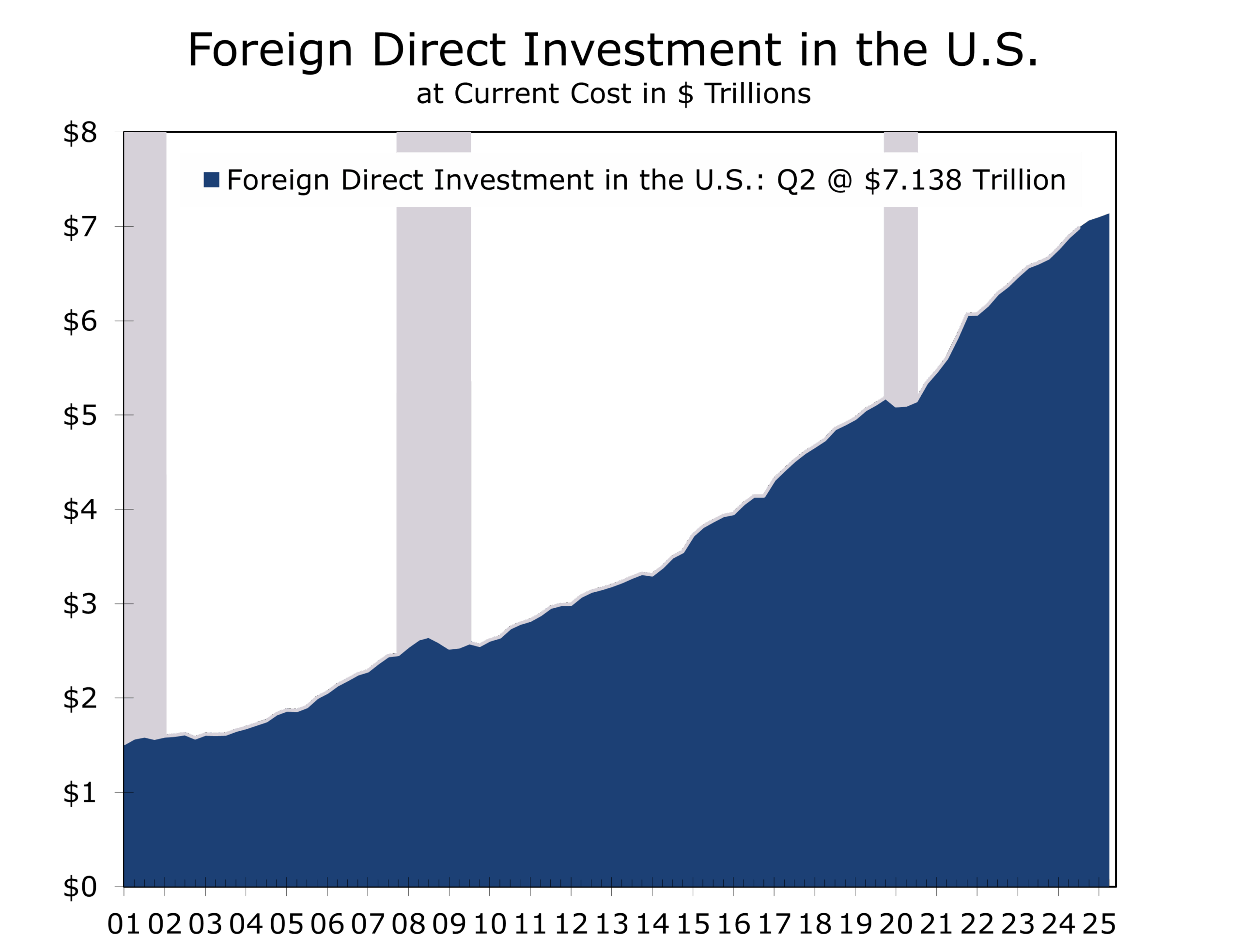

Foreign Direct Investment: Capital as Diplomacy

The Trump administration’s new international investment framework signals a pivot from tariff-centric confrontation toward a more deal-driven form of economic statecraft. The emerging strategy treats access to U.S. capital, corporate partnerships, and investment guarantees as tools of geopolitical influence—leveraging balance sheets where sanctions and tariffs have begun to hit diminishing return.

Recent Bloomberg analysis notes that while headline pledges of a $20-trillion investment boom are materially overstated, identifiable commitments still run into the multi-trillion range and concentrate heavily in advanced technologies, energy systems, and strategic manufacturing. Bloomberg’s more conservative analysis puts the total at closer to $7 trillion, which is still a hefty sum.

A multi-trillion dollar investment push creates upside risk for U.S. capex and long-run growth.

A sustained wave of cross-border projects—even at the lower, independently verified scale—would carry real macroeconomic weight. In a world reshaped by reshoring, friend-shoring, and supply-chain redundancy, expanded U.S. investment from abroad would reinforce the capital-led expansion already underway. Sectors such as AI infrastructure, semiconductors, energy platforms, defense technology, and advanced logistics anchor the current cycle; additional international activity would deepen order books for U.S. suppliers and add upside risk to near-term capex and GDP.

Context matters. The entire stock of foreign direct investment already in the United States stands at roughly $7.1 trillion, at current costs, while U.S. direct investment abroad totals about $6.8 trillion. Even a modest, sustained increase in direct investment flows, well below Trump’s touted figures, would still be large relative to the existing base and could meaningfully support long-run potential GDP. If the Bloomberg analysis is accurate, then $7 trillion in additional foreign direct investment would roughly double the stock of facilities currently in place. To borrow a phrase from president Trump, that would be ‘huge’. The initiative’s emphasis on advanced manufacturing, data-driven systems, and modern energy would also reinforce productivity, raise global demand for U.S. goods and services, and extend the reindustrialization impulse that has defined this cycle.

There are trade-offs. Politically influenced investment flows tend to be lumpy, with project timing and approval tied to negotiations rather than purely economic returns. That increases volatility and makes the growth path more corridor-shaped than smooth. But the broader takeaway is clear: cross-border capital is becoming a strategic asset. Its deployment will be more dynamic and less predictable—but also rich with opportunity for the sectors aligned with the administration’s priorities.

Drifting Toward Easing, Still Waiting for Data

Equities closed the week with a modest gain, helped by a modest decline in Treasury yields and slightly tighter credit spreads. The S&P 500 and Dow ended the month in positive territory, while the Nasdaq slipped fractionally. With no employment report ahead of the FOMC meeting, markets are trading on inference rather than evidence, waiting for data that either validates the soft-landing narrative or complicates it.

With Santa leading the rally, the markets are waiting for confirmation, not direction.

The Fed’s runway for easing remains visible but narrow. A December cut now appears highly likely, yet visibility beyond that is hazy at best. We anticipate clarity on Powell’s successor by yearend, with Kevin Hassett emerging as the leading candidate. Powell, for his part, seems intent on leaving room for his successor to navigate what may become a more complicated early-2025 policy landscape.

The Week Ahead: December 1-5

We continue to wait for federal agencies to catch up with the economic data. Private data continue to offer the best intel of current economic conditions.

Monday, December 1

Look for credit card data and other private high frequency data for an assessment on Black Friday and opening weekend holiday retail sales.

We will also get a couple of readings on the manufacturing sector, with S&P final PMI at 9:45 and ISM Manufacturing Index at 10:00 am. The ISM Manufacturing Index has been stuck at just under 50 but well north of the 43.7 level that is typically consistent with recession. The more leading indicators have recently been hinting at some reacceleration, but it is likely too soon to see that in this report.

Jerome Powell will provide remarks before joining a panel on George P. Shultz and his economic policy contributions at the Hoover Institution at 8:00 pm.

Tuesday, December 2

Michelle Bowman, as Fed Vice Chair for Supervision, is scheduled to testify before the U.S. House Committee on Financial Services.

We will also get data on U.S. light vehicle sales and reports on sales for Cyber Monday.

Wednesday, December 3

We will get the latest update on ADP employment for November. The October report posted an increase of 42,000 private-sector jobs. We are also scheduled to receive reports on import prices, as well as the final S&P Services PMI and the ISM Services Index. The latter will be closely scrutinized for updates on employment and prices.

Thursday, November 26

We will receive weekly first-time unemployment claims and are also scheduled to receive October merchandise trade data.

Friday, November 27

We will close the week with a look at September personal income and spending, as well as inflation data. Personal income is expected to rise 0.4%, while consumer spending should rise 0.2%, or essentially flat after inflation. Services outlays are a bit of wildcard.

We will also get preliminary University of Michigan Consumer Sentiment and Consumer Credit use data for the month of October late Friday afternoon.

An Economy Tilting Toward Capital and Resilience

A consistent pattern emerges across the Beige Book, durable-goods orders, home prices, labor data and capital spending: the U.S. economy is gradually shifting toward a capital-led, innovation-driven expansion. AI infrastructure, industrial construction, aerospace, energy systems, logistics and defense technology are becoming the structural supports of the cycle.

The investment boom is being supported by wide corporate margins, strong order books, reshoring initiatives and a growing pipeline of public and private projects. This shift toward capital deepening and productivity-enhancing investment gives the economy a sturdier foundation than headlines often suggest.

The outlook is not without risk, but also not without promise. Consumers remain under pressure. Labor markets are cooling. The inflation fever has broken but has not fully subsided. Even so, an investment-centric expansion can support stronger long-run growth, greater supply-chain resilience and a healthier balance between consumption and production.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 30, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

October 2025 Consumer Confidence - Layoffs, Shutdown Fallout, and a Softer Job Market Hit Confidence Hard

Confidence Breaks Lower

- The Consumer Confidence Index® fell sharply to 88.7 from 95.5, its lowest level since April.

- Both the Present Situation Index and Expectations Index declined, with expectations sinking to 63.2, well below the recession-signaling threshold of 80.

- Confidence deteriorated across nearly all age and income groups, with the steepest pullback among consumers 35 and older and among independent voters.

- Inflation concerns, tariffs, political tensions, and the federal government shutdown dominated write-in responses.

- Household financial assessments weakened materially, and recession perceptions continued to drift higher.

- Layoff announcements surged in October, and the earlier equity-market sell-off weighed on wealth perceptions—both contributing to November’s sharp decline.

- Big-ticket buying plans slipped across cars, appliances, electronics, and homes, though homebuying intentions relatively stable.

- Service-spending plans softened broadly, with only minor increases in museum and historic-site visits.

- Despite weaker sentiment, consumers’ 12-month inflation expectations remain within its recent range at 4.8%, while stock-price expectations stayed strongly positive.

Households Turn More Cautious

U.S. consumer confidence tumbled in November, with the Conference Board’s Consumer Confidence Index® falling 6.8 points to 88.7, the weakest reading since April. The decline marks a clear break from the sideways pattern of recent months and reflects broad softening across perceptions of the labor market, household finances, and the economic outlook. Importantly, November’s pullback did not occur in a vacuum. The survey period captured the spreading effects of the 43-day federal shutdown, a wave of layoff announcements through October, and an earlier sell-off in the stock market—a combination that weighed heavily on household confidence and future expectations. Shutdown-related disruptions featured prominently in consumer write-ins, joining persistent concerns about inflation, tariffs, and political tensions.

Shutdown fallout and rising layoffs drove confidence to its weakest since April.

The Present Situation Index fell to 126.9, reflecting less favorable assessments of both current business conditions and the labor market. Fewer consumers reported that jobs were plentiful, and while the share calling jobs “hard to get” edged down, the net labor-market differential weakened again after a brief improvement in October. This deterioration aligns with recent labor-market data showing slower hiring, rising unemployment—now 4.4%, a four-year high—and a visible increase in announced job cuts across technology, retail, and media. For many households, especially middle- and lower-income respondents, the labor market is beginning to feel materially less secure.

The larger story lies in the forward-looking Expectations Index, which fell to 63.2, its tenth straight month below the recession-signaling threshold of 80. All components deteriorated. Consumers grew more pessimistic about business conditions six months ahead, and expectations for labor-market improvement retreated further. Expectations for higher household income—which had held firm for six months—fell sharply. This shift is notable given that wage growth remains positive; it suggests households are increasingly concerned about the durability of the expansion, the impact of elevated prices and tariffs on real incomes, and the implications of the recent layoffs and market volatility for future earnings.

The Expectations Index marked its tenth month below the recession threshold of 80.

Sentiment weakened across most demographic groups. Confidence improved only among consumers earning less than $15,000, but they remain the least optimistic overall. The steepest declines were among consumers 35 and older, with those 55+ again the most downbeat. Confidence fell across political affiliations, with independents posting the sharpest retreat. These broad-based declines underscore a national shift in sentiment rather than erosion concentrated in any single group.

Consumers’ views of both their current and expected financial situations worsened markedly. Assessments of current family finances fell to their lowest level since August 2024, while expectations for future finances softened alongside rising recession fears. Inflation expectations increased to 4.8%, and although fewer consumers expect higher interest rates, their expectations for future stock gains moderated slightly—consistent with the equity-market volatility seen during the survey period.

Big-ticket buying plans softened in November after stabilizing through much of the fall. Intentions to purchase new and used vehicles slipped, reversing a modest rebound earlier in the year. Plans to buy appliances, furniture, and electronics declined, though items such as TVs, smartphones, and used cars remain comparatively favored. The recent dip in mortgage rates has done little to lift home buying intentions. Affordability remains strained, and rising concerns about job security are increasingly keeping would-be buyers on the sidelines.

Plans for big-ticket purchases and discretionary services slipped across nearly all categories.

Service-spending plans also weakened across nearly every category. Consumers signaled reduced plans for travel, lodging, entertainment, and personal recreation, with only small increases in planned visits to museums, libraries, and historic sites. Healthcare spending intentions moved sharply higher—rising to the second-most-cited spending category—likely reflecting heightened awareness of insurance costs and subsidies during the shutdown. Overall, service-sector plans continue to shift toward lower-cost, necessary activities, consistent with a late-cycle consumer prioritizing essential rather than discretionary spending.

Vacation intentions fell back in November after October’s surprising surge. Both domestic and international travel expectations edged lower, consistent with reduced plans for hotels, motels, and airfare. This pullback reinforces the broader narrative of a more cautious consumer—particularly around commitment-heavy expenditures such as travel.

Taken together, November’s confidence report portrays a consumer who remains resilient but increasingly guarded. Labor-market softening, rising layoff announcements, the broadening impact of the shutdown, and recent equity volatility all contributed to a broad-based deterioration in sentiment. While confidence has not collapsed, the tenth consecutive month with expectations below 80 underscores a higher-risk environment heading into 2026. The consumer is still spending, but the foundation beneath sentiment is clearly thinning as the cycle matures.

Home Prices: Slower Appreciation and Broadening Monthly Declines

The latest S&P Cotality Case-Shiller release confirms a decisive loss of momentum in housing. National home prices rose just 1.3% year over year in September, down from 1.4% in August and marking the slowest pace since mid-2023. Price growth is now running well below inflation, widening the real-price adjustment underway in many markets.

On a month-to-month basis, national home prices fell 0.3% before seasonal adjustment, the third consecutive monthly decline. Even after seasonal adjustment, the national index managed only a 0.2% gain, reinforcing the steady downshift in momentum. All 20 major metros posted negative NSA monthly readings, a rare and unambiguous sign of broad cooling as affordability pressures and higher rates cut deeper.

Home price growth slowed to its weakest pace since mid-2023 and is running below inflation.

Regional performance continues to invert the pandemic narrative. Chicago (+5.5% YoY), New York (+5.2%), and Boston (+4.1%) led annual gains, supported by tighter inventories and steadier labor markets. At the other extreme, several metros that experienced the largest pandemic-era surges are now retrenching: including Tampa (-4.1% YoY) posted its eleventh straight annual decline, while Phoenix (-2.0%), Dallas (-1.3%), and Miami (-1.3%) also fell year over year.

Month-to-month weakness was widespread, with Tampa (-0.95% NSA), San Diego (-0.92%), Seattle (-0.91%), and Las Vegas (-0.85%) seeing the sharpest drops. Even previously resilient markets—Atlanta (-0.59%), Charlotte (-0.77%), and Denver (-0.70%)—registered meaningful monthly price deterioration.

With the national index still 78% above its 2006 peak, even modest pullbacks carry substantial affordability implications. The combination of slowing appreciation, real-price declines, and broad regional softening provides an important backdrop to the recent stabilization in homebuying intentions amidst declines in consumer confidence in general: rates eased during much of the survey period, supply is gradually improving, and buyers appear increasingly attuned to the shift in pricing power. We remain optimistic about 2026.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 25, 2025

Mark Vitner, Chief Economist

(704) 458-4000

A Cooling Consumer: September Sales Signal a Slower Q4

Retail Sales Hit a Flat Spot…

- Retail sales rose 0.2%, softer than expectations and essentially flat given the Census Bureau’s ±0.4% confidence interval.

- August’s +0.6% gain was unrevised, preserving a strong summer handoff.

- Year-over-year sales increased 4.3%, led by nonstore retail (+6.0%) and food services (+6.7%).

- September’s sectoral shifts showed goods categories cooling while service-oriented and necessity-driven categories strengthened.

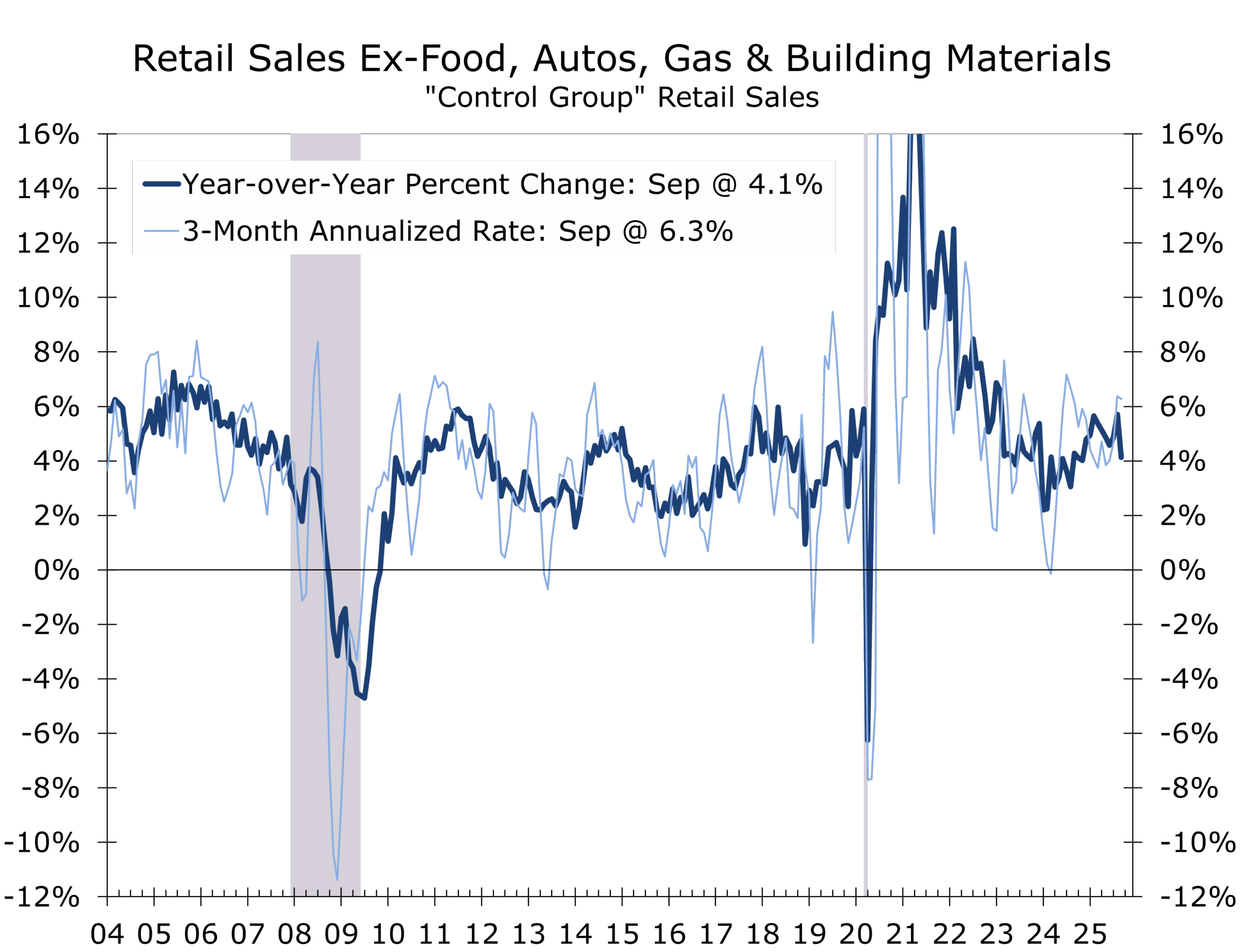

- Control-group sales fell 0.1%, but still rose 6.1% annual rate during Q3

- The unwind of summer EV-driven auto demand began earlier than expected. The EV tax credit expired at the end of September, suggesting supply constraints or early pull-forward effects were behind the drop.

- Nonstore sales’ 0.7% decline may stem partly from seasonal adjustment issues tied to unusually large August online promotions that seasonal factors failed to fully capture.

- The K-shaped consumer remains firmly in place: high-income households continue to spend, while middle- and lower-income households face rising costs for key necessities, weaker job fundamentals and tighter credit.

- Slower retail momentum adds fuel to the growing calls for a December rate cut, particularly as a cooling labor market is now clearly exerting pressure on discretionary categories.

- Despite September’s softness, holiday spending remains on track for its strongest growth since 2021, supported by wealth effects and high-income resilience. We are looking are looking for holiday retail sales to rise 4.5% this year

…As Momentum Rolls into Services

U.S. retail sales rose 0.2% in September, undershooting expectations and marking a meaningful slowdown after a stronger summer. The gain sits entirely inside the Census Bureau’s ±0.4% confidence interval, effectively yielding a flat print.

The report—delayed by the 43-day federal shutdown—follows July and August strength that was amplified by a rush to purchase electric vehicles ahead of the expiring federal tax credit. Curiously, motor vehicle sales softened 0.3% in September even though the credit expired at month-end, suggesting that the strongest models were depleted ahead of the deadline and that the pull-forward was more front-loaded than usual.

September’s soft headline gain masks a shift away from goods to steadier service spending.

The defining feature of September’s report is the sectoral rotation that is becoming more pronounced as the cycle matures. Goods categories that surged earlier in Q3 softened across the board: electronics (–0.5%), clothing (–0.7%), sporting goods (–2.5%), and nonstore retail (–0.7%). Yet all remain positive year-over-year, indicating that part of the decline reflects payback for prior strength rather than an outright deterioration. The weakness in nonstore sales was likely amplified by residual seasonality created when a wider group of online retailers aligned their promotions with Amazon’s expanded Prime Day—an effect not yet fully reflected in seasonal-adjustment factors.

In contrast, service-oriented and necessity-based categories showed ongoing strength. Food services (restaurants and bars) rose 0.7%, health & personal care 1.1%, and miscellaneous retailers 2.9%. Gasoline station sales rose 2.0%, though they remain negative on a year-over-year basis due to lower fuel prices. This rotation away from discretionary goods and toward services and necessities mirrors classic late-cycle behavior, with households becoming more selective but still engaged.

Momentum indicators reinforce this shift, with most retail categories posting softer readings in September. Nonstore retail shows the same pattern: weak sequential momentum despite a 6.0% year-over-year gain. Food services continues to be the most dependable pillar of the consumer, maintaining three-month momentum near 6.2% and 6.7% year-over-year growth.

Control-group softness adds mild downside risk to early Q4 GDP tracking

The weakness in control-group sales, which fell 0.1%, introduces nuance without changing the underlying Q3 story. Core retail sales, which provide a good approximation of the goods portion of personal consumption expenditure, rose at a 6.3% annual rate during the third quarter.

.

Personal spending is tracking a 0.4% nominal gain for the month and a real increase of close to 0.2%, consistent with real consumer spending rising at around a 3.2% annualized in Q3. That aligns closely with our own Q3 real GDP tracking at 3.7%.

Slowing retail momentum increases pressure on the Fed to consider a December rate cut

The larger question now is how sharply spending slows in Q4. The answer increasingly hinges on the labor market. Unemployment has risen to 4.4%, the highest in four years, and hiring has become narrower and more uneven across industries. These dynamics are now showing up in September’s discretionary categories. More broadly, they strengthen the argument—already building in markets—that the Fed should consider an insurance cut in December. While Fed officials have centered their concerns on the labor market, the September retail data show that a cooling job market is clearly pressuring spending at the margin. The marginal deceleration visible in goods categories dovetails with market volatility, softer sentiment, and the increasingly bifurcated consumer landscape.

September’s weaker motor vehicle sales suggest they pullback in October will be less than had been expected. We are looking for real consumer spending to slow to a 1.7% annualized rate in Q4. That said, underlying demand heading into the holiday season remains healthier than September’s headline number suggests. High-frequency indicators continue to look solid, and strong household wealth gains—especially among older and higher-income households—are expected to support a 4.5% year-to-year rise in holiday-related spending this year.

Spending at restaurants and bars remains a notable bright spot, with sales up 6.7% year-over-year, reinforcing that higher-income households are still spending freely on discretionary services even as goods categories cool. This strength, however, masks a widening performance gap across the industry. Many chains, particularly those marketing to middle income households, have reported sluggish traffic and tightening margins, squeezed by higher food and labor costs that remain difficult to fully pass through. Larger national brands—with established marketing platforms, stronger digital engagement, and the scale to offer targeted value—are outperforming smaller operators. September’s results fit this pattern: demand at the upper end remains healthy, but the pressure on operating margins underscores how uneven and income-dependent service-sector momentum has become at this stage of the cycle.

Overall, the September retail sales report points to normalization rather than deterioration: a resilient but increasingly selective consumer navigating a cooling labor market, shifting incentives, and tighter financial conditions. Momentum is easing, the ceiling is lower, and the floor—while still firm—is clearly thinning as the cycle matures. The government will release its full estimate of Q3 GDP on December 23. September’s figures set the tone for Q4 and remain consistent with our early call for a slowdown toward the 1.7% range.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 25, 2025

Mark Vitner, Chief Economist

(704) 458-4000

The Piedmont Perspective: Emerald Cities and Economic Narratives

Oz Revisited 125 Years Later

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Clearer Skies, Uneven Air

Highlights of the Week

- Post-shutdown data confirm an economy that is still expanding but doing so at a noticeably slower pace—fully consistent with our latest CAVU Compass.

- Labor markets continue to soften quietly: Challenger layoff announcements have risen, continuing claims are edging higher, and consumers are increasingly strained by affordability rather than job insecurity.

- Companies are accelerating economic-development announcements as they adapt to rapid tariff adjustments and a more interventionist policy environment.

- Oil and broader commodity prices eased this week as reports surfaced of a potential U.S.–Russia–Ukraine peace framework, reducing the geopolitical risk premium.

- With a slew of projects nearing completion, the coming global LNG supply wave presents a structural disinflation force that will shape energy pricing into 2026.

- Geopolitical risks—including Gaza and Lebanon, the potential Saudi normalization, and possible regime change in Venezuela—remain elevated, even as markets trade with surprising calm.

- The narrative tension developed in the CAVU Compass and extended in our Piedmont Perspective—between official progress and lived experience—continues to define the moment in both the U.S. and globally.

A Clearer View of a Cooling Economy

The past week provided a clearer window into the post-shutdown macro environment, and the data that emerged fit neatly within the framework laid out in the latest CAVU Compass. The economy continues to expand, but its pace has become more deliberate and uneven. Third-quarter GDP still appears stronger than initially expected, supported by a narrower trade deficit and firmer construction activity. Yet the underlying rhythm of domestic demand is clearly more moderate than the headline suggests. As the flow of data normalizes, the picture that emerges is not of an economy accelerating into late 2025 but of one easing gradually onto a slower trajectory.

Following a surprisingly strong Q3, growth remains positive but is no longer accelerating.

Growth remains positive but is no longer accelerating

Labor market developments continue to warrant close attention. Headline payroll gains in September were firmer on the surface, but the downward revisions to August and the softening three-month average are more revealing. Initial jobless claims remain low, but continuing claims have risen steadily—an early sign that job seekers are taking longer to reattach to the workforce

The more consequential development came via the Challenger job-cut announcements, which have now begun to rise after months of relative stability. These are not broad-based layoffs, but targeted reductions across a widening set of industries, signaling a shift from hiring freezes toward more active cost control.

Consumers, meanwhile, remain under pressure. The final University of Michigan Sentiment Index slipped again, reinforcing a theme that has persisted all year: the dominant source of household stress is not fear of unemployment but the cost of living. Elevated rent, insurance, mortgage payments, and utilities continue to weigh on household budgets even as inflation recedes. This gap—between the employer’s view of labor costs and the household’s view of affordability—remains one of the defining tensions of this cycle.

Persistent affordability challenges and a soft job market for recent college graduates is driving anxiety.

The latest Consumer Sentiment data show consumers generally feel more pessimistic about their current financial situation, with buying conditions for durable goods falling to their worst level in more than 40 years, even as year-ahead and long-run inflation expectations eased for a third straight month. Sentiment declined across all income groups, but remains most depressed among lower-income households, reflecting the growing bifurcation of the American consumer.

Monetary policy sits squarely in this middle ground. The October FOMC minutes underscored a divided Committee heading into the December meeting, with members split between the need for additional insurance cuts and the risk of moving too quickly in the absence of fresh official data. Shutdown-delayed payroll and inflation releases mean the Federal Reserve is flying with only partial visibility.

With official economic data still playing catch-up, the Fed will likely err on the side of caution and cut rates at their December FOMC meeting

Market pricing already reflects a multi-quarter sequence of slow, measured rate cuts. The modestly positive slope of the yield curve aligns with this expectation: the curve is not pricing recession, but neither is it pricing acceleration. Rather, it reflects an economy in controlled deceleration with a central bank intent on maintaining credibility.

The curve is modestly positive—and telling a very different story from a year ago

Energy and commodities introduced a notable shift in tone this week. Oil prices eased as reports suggested a potential peace framework between Russia and Ukraine, reducing one of the most important geopolitical risk premia embedded in global commodity markets. Even tentative negotiations can influence pricing when the conflict has disrupted energy flows, shipping routes, and insurance costs for nearly four years. If the diplomatic signals materialize into a more durable arrangement, the corresponding easing in supply risk could prove meaningful for oil, natural gas, wheat, and industrial inputs.

In a major switch, geopolitics appear set to pull prices lower, rather than push them higher