Confidence Breaks Lower

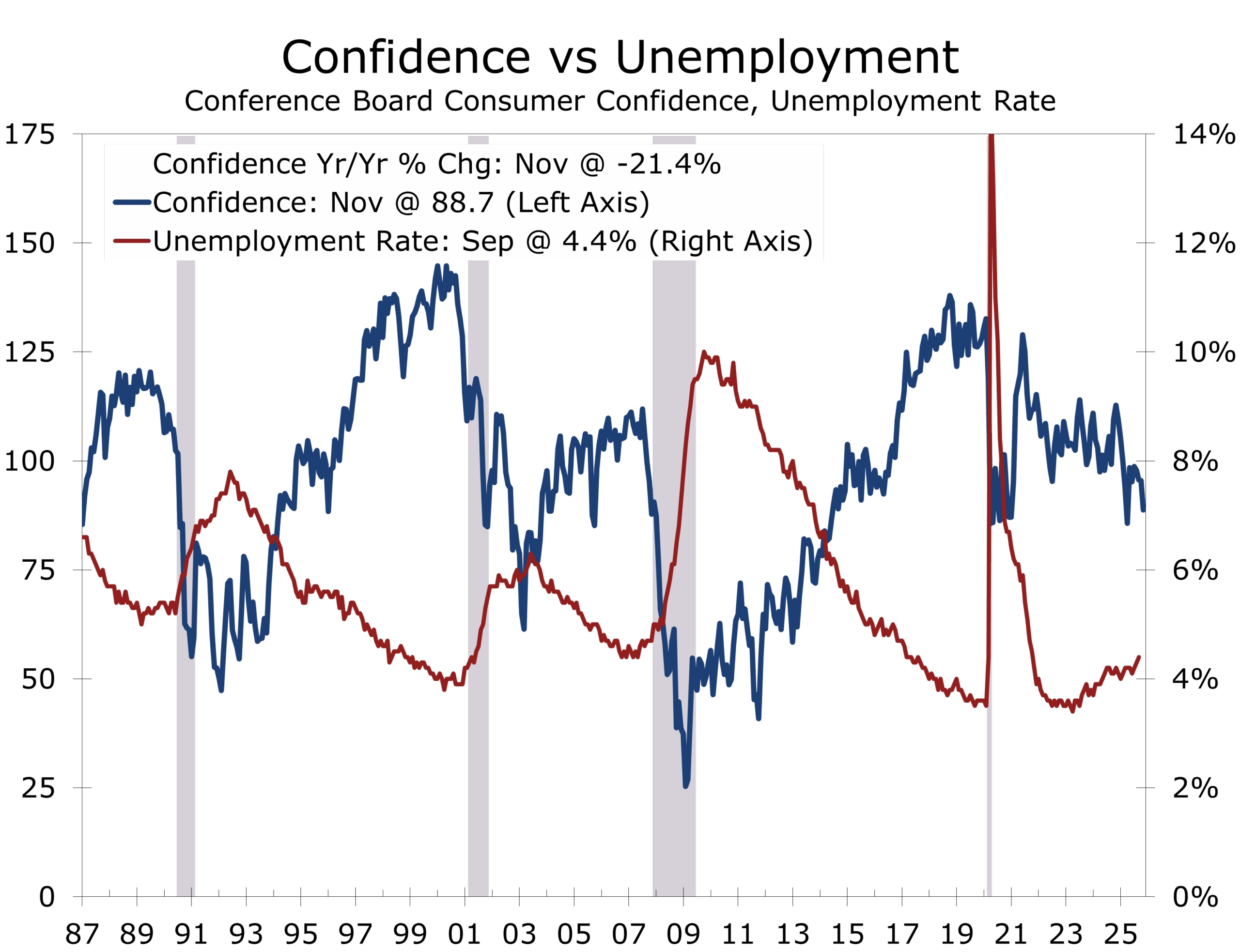

- The Consumer Confidence Index® fell sharply to 88.7 from 95.5, its lowest level since April.

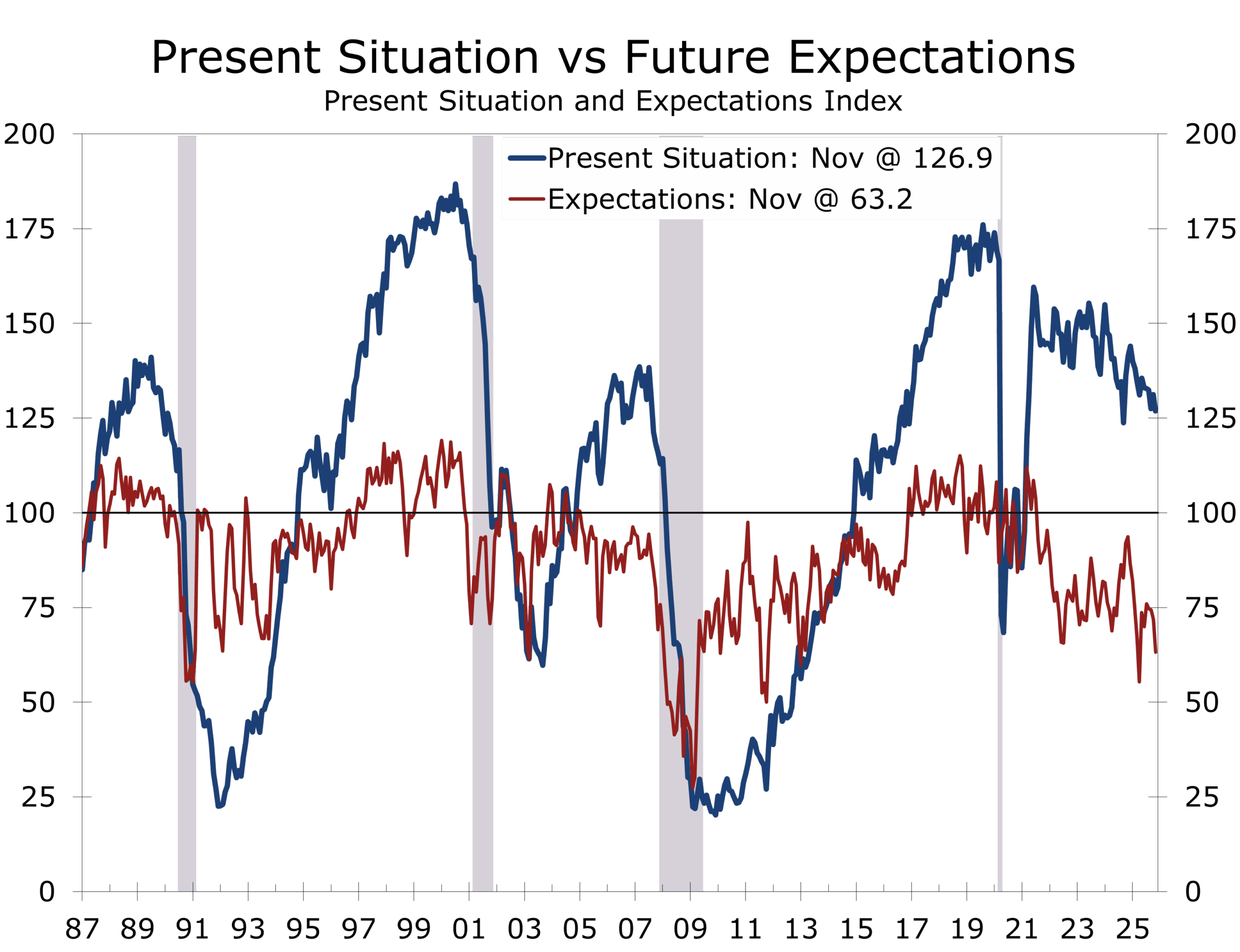

- Both the Present Situation Index and Expectations Index declined, with expectations sinking to 63.2, well below the recession-signaling threshold of 80.

- Confidence deteriorated across nearly all age and income groups, with the steepest pullback among consumers 35 and older and among independent voters.

- Inflation concerns, tariffs, political tensions, and the federal government shutdown dominated write-in responses.

- Household financial assessments weakened materially, and recession perceptions continued to drift higher.

- Layoff announcements surged in October, and the earlier equity-market sell-off weighed on wealth perceptions—both contributing to November’s sharp decline.

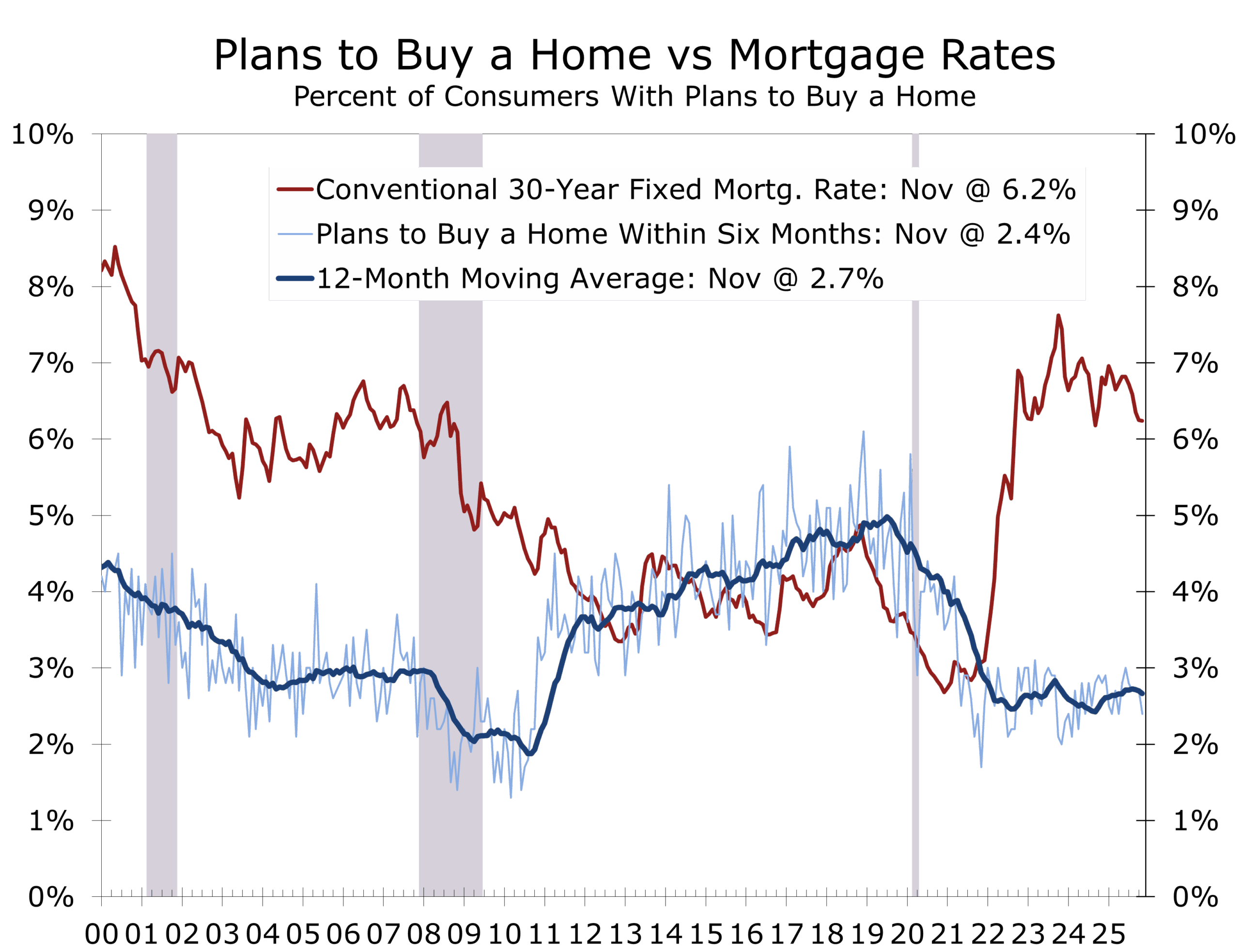

- Big-ticket buying plans slipped across cars, appliances, electronics, and homes, though homebuying intentions relatively stable.

- Service-spending plans softened broadly, with only minor increases in museum and historic-site visits.

- Despite weaker sentiment, consumers’ 12-month inflation expectations remain within its recent range at 4.8%, while stock-price expectations stayed strongly positive.

Households Turn More Cautious

U.S. consumer confidence tumbled in November, with the Conference Board’s Consumer Confidence Index® falling 6.8 points to 88.7, the weakest reading since April. The decline marks a clear break from the sideways pattern of recent months and reflects broad softening across perceptions of the labor market, household finances, and the economic outlook. Importantly, November’s pullback did not occur in a vacuum. The survey period captured the spreading effects of the 43-day federal shutdown, a wave of layoff announcements through October, and an earlier sell-off in the stock market—a combination that weighed heavily on household confidence and future expectations. Shutdown-related disruptions featured prominently in consumer write-ins, joining persistent concerns about inflation, tariffs, and political tensions.

Shutdown fallout and rising layoffs drove confidence to its weakest since April.

The Present Situation Index fell to 126.9, reflecting less favorable assessments of both current business conditions and the labor market. Fewer consumers reported that jobs were plentiful, and while the share calling jobs “hard to get” edged down, the net labor-market differential weakened again after a brief improvement in October. This deterioration aligns with recent labor-market data showing slower hiring, rising unemployment—now 4.4%, a four-year high—and a visible increase in announced job cuts across technology, retail, and media. For many households, especially middle- and lower-income respondents, the labor market is beginning to feel materially less secure.

The larger story lies in the forward-looking Expectations Index, which fell to 63.2, its tenth straight month below the recession-signaling threshold of 80. All components deteriorated. Consumers grew more pessimistic about business conditions six months ahead, and expectations for labor-market improvement retreated further. Expectations for higher household income—which had held firm for six months—fell sharply. This shift is notable given that wage growth remains positive; it suggests households are increasingly concerned about the durability of the expansion, the impact of elevated prices and tariffs on real incomes, and the implications of the recent layoffs and market volatility for future earnings.

The Expectations Index marked its tenth month below the recession threshold of 80.

Sentiment weakened across most demographic groups. Confidence improved only among consumers earning less than $15,000, but they remain the least optimistic overall. The steepest declines were among consumers 35 and older, with those 55+ again the most downbeat. Confidence fell across political affiliations, with independents posting the sharpest retreat. These broad-based declines underscore a national shift in sentiment rather than erosion concentrated in any single group.

Consumers’ views of both their current and expected financial situations worsened markedly. Assessments of current family finances fell to their lowest level since August 2024, while expectations for future finances softened alongside rising recession fears. Inflation expectations increased to 4.8%, and although fewer consumers expect higher interest rates, their expectations for future stock gains moderated slightly—consistent with the equity-market volatility seen during the survey period.

Big-ticket buying plans softened in November after stabilizing through much of the fall. Intentions to purchase new and used vehicles slipped, reversing a modest rebound earlier in the year. Plans to buy appliances, furniture, and electronics declined, though items such as TVs, smartphones, and used cars remain comparatively favored. The recent dip in mortgage rates has done little to lift home buying intentions. Affordability remains strained, and rising concerns about job security are increasingly keeping would-be buyers on the sidelines.

Plans for big-ticket purchases and discretionary services slipped across nearly all categories.

Service-spending plans also weakened across nearly every category. Consumers signaled reduced plans for travel, lodging, entertainment, and personal recreation, with only small increases in planned visits to museums, libraries, and historic sites. Healthcare spending intentions moved sharply higher—rising to the second-most-cited spending category—likely reflecting heightened awareness of insurance costs and subsidies during the shutdown. Overall, service-sector plans continue to shift toward lower-cost, necessary activities, consistent with a late-cycle consumer prioritizing essential rather than discretionary spending.

Vacation intentions fell back in November after October’s surprising surge. Both domestic and international travel expectations edged lower, consistent with reduced plans for hotels, motels, and airfare. This pullback reinforces the broader narrative of a more cautious consumer—particularly around commitment-heavy expenditures such as travel.

Taken together, November’s confidence report portrays a consumer who remains resilient but increasingly guarded. Labor-market softening, rising layoff announcements, the broadening impact of the shutdown, and recent equity volatility all contributed to a broad-based deterioration in sentiment. While confidence has not collapsed, the tenth consecutive month with expectations below 80 underscores a higher-risk environment heading into 2026. The consumer is still spending, but the foundation beneath sentiment is clearly thinning as the cycle matures.

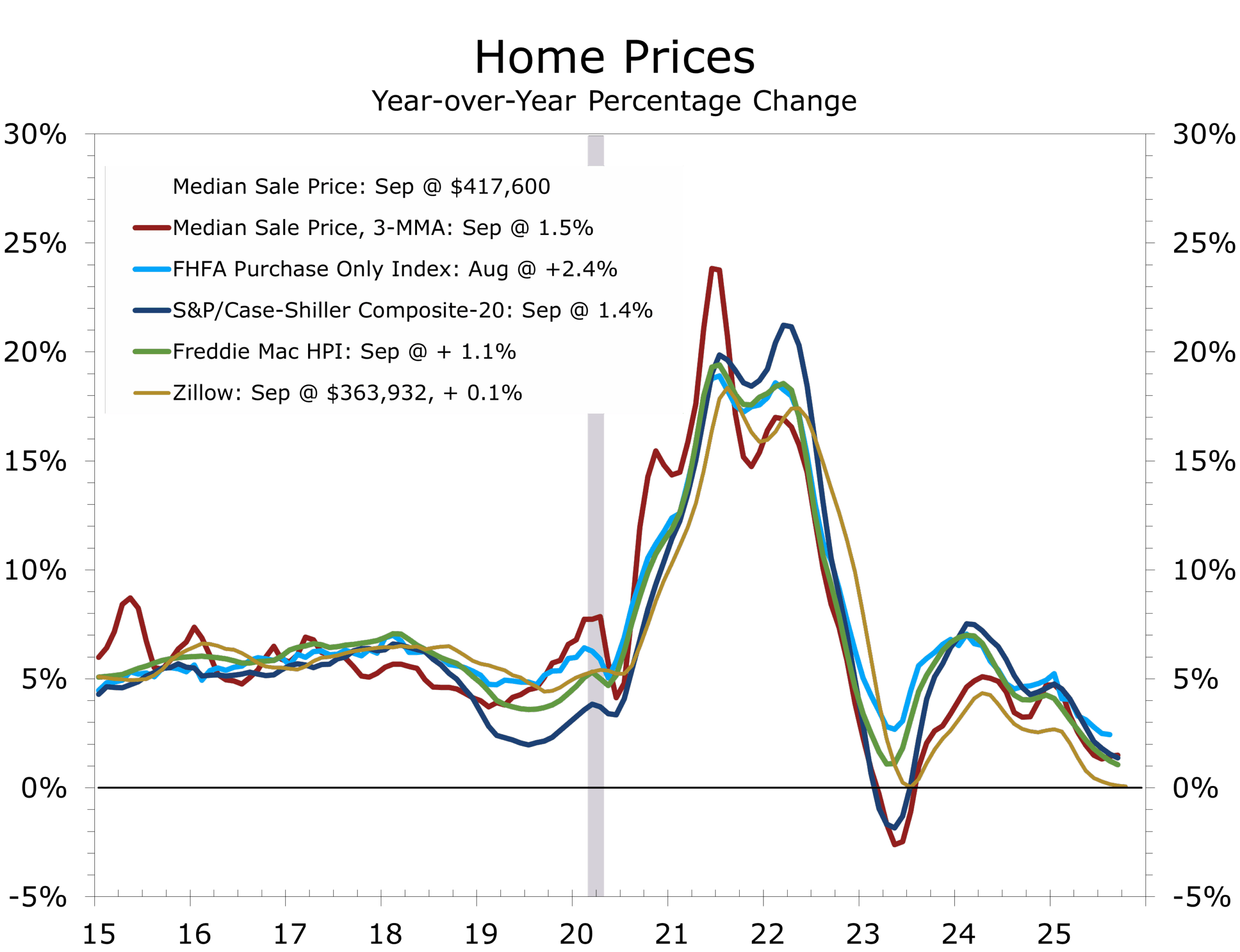

Home Prices: Slower Appreciation and Broadening Monthly Declines

The latest S&P Cotality Case-Shiller release confirms a decisive loss of momentum in housing. National home prices rose just 1.3% year over year in September, down from 1.4% in August and marking the slowest pace since mid-2023. Price growth is now running well below inflation, widening the real-price adjustment underway in many markets.

On a month-to-month basis, national home prices fell 0.3% before seasonal adjustment, the third consecutive monthly decline. Even after seasonal adjustment, the national index managed only a 0.2% gain, reinforcing the steady downshift in momentum. All 20 major metros posted negative NSA monthly readings, a rare and unambiguous sign of broad cooling as affordability pressures and higher rates cut deeper.

Home price growth slowed to its weakest pace since mid-2023 and is running below inflation.

Regional performance continues to invert the pandemic narrative. Chicago (+5.5% YoY), New York (+5.2%), and Boston (+4.1%) led annual gains, supported by tighter inventories and steadier labor markets. At the other extreme, several metros that experienced the largest pandemic-era surges are now retrenching: including Tampa (-4.1% YoY) posted its eleventh straight annual decline, while Phoenix (-2.0%), Dallas (-1.3%), and Miami (-1.3%) also fell year over year.

Month-to-month weakness was widespread, with Tampa (-0.95% NSA), San Diego (-0.92%), Seattle (-0.91%), and Las Vegas (-0.85%) seeing the sharpest drops. Even previously resilient markets—Atlanta (-0.59%), Charlotte (-0.77%), and Denver (-0.70%)—registered meaningful monthly price deterioration.

With the national index still 78% above its 2006 peak, even modest pullbacks carry substantial affordability implications. The combination of slowing appreciation, real-price declines, and broad regional softening provides an important backdrop to the recent stabilization in homebuying intentions amidst declines in consumer confidence in general: rates eased during much of the survey period, supply is gradually improving, and buyers appear increasingly attuned to the shift in pricing power. We remain optimistic about 2026.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 25, 2025

Mark Vitner, Chief Economist

(704) 458-4000