Trade Turmoil Weighs on Manufacturing Activity

Manufacturing Shows Tentative Signs of Stability

- The ISM Manufacturing PMI slipped 0.2 points to 48.5 in May, its third straight sub-50 reading, though underlying data showed signs of resilience.

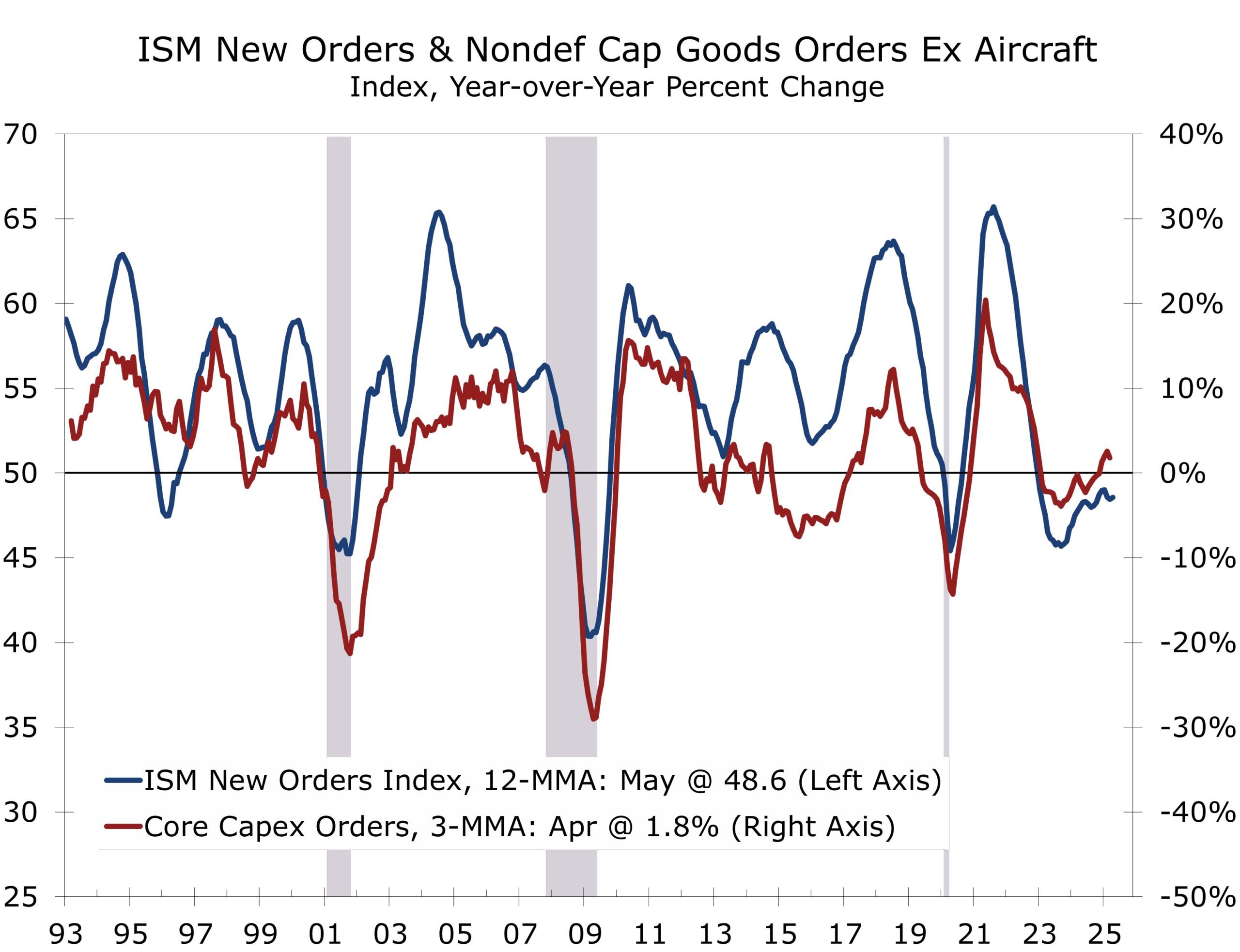

- New orders rose 0.4 points to 47.6—the most forward-looking component of the survey—suggesting early signs of a demand rebound.

- Production ticked up 1.4 points to 45.4, still in contraction but supported by easing backlogs and improving inventory alignment.

- The employment index edged up to 46.8, reflecting fewer layoffs, though hiring remains restrained.

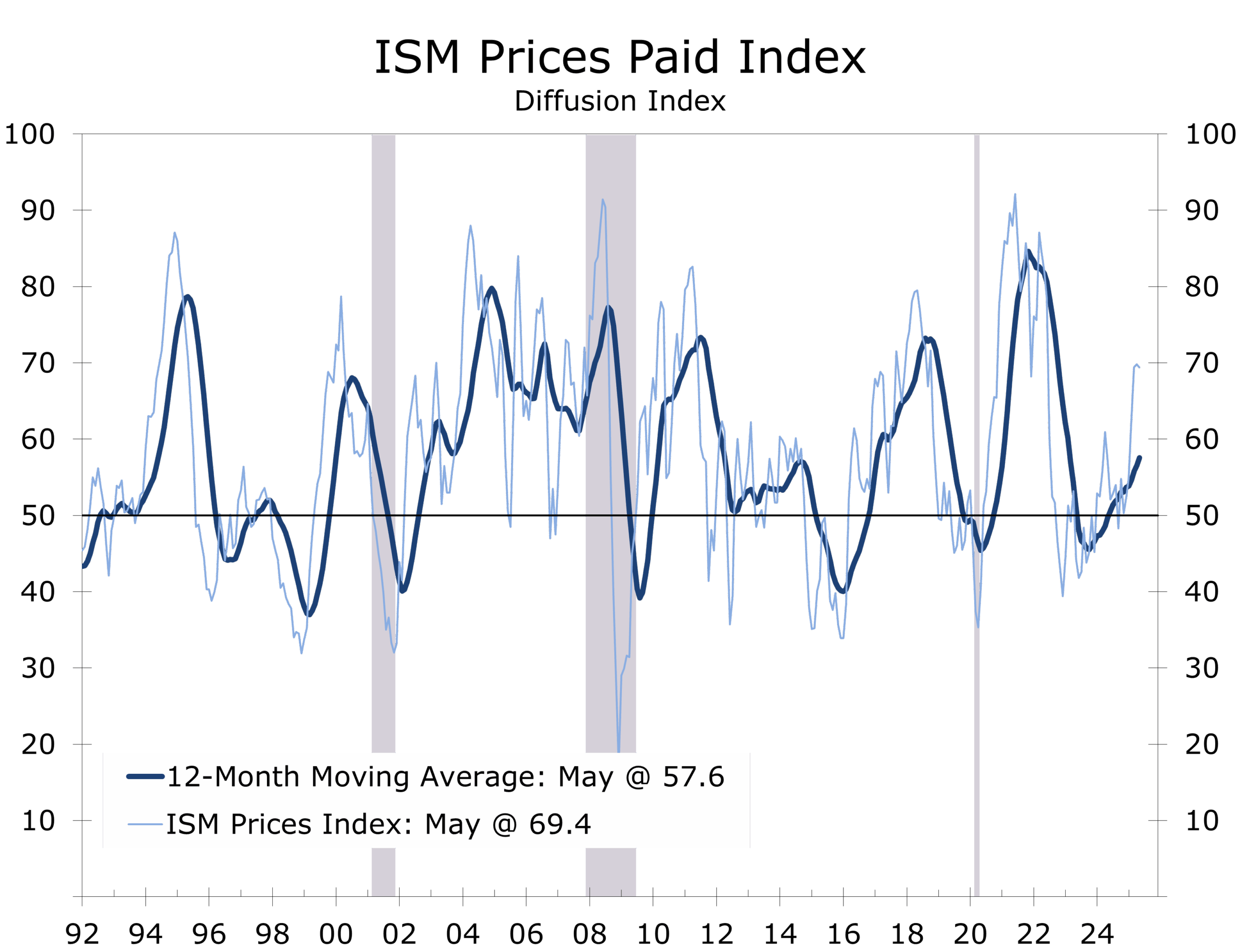

- Prices paid dipped slightly to 69.4 but remain elevated, as tariff pass-throughs continue to compress margins.

- Backlogs rose 3.4 points to 47.1, their highest since January, signaling tentative supply chain normalization and more stable factory schedules.

- Trade turmoil remains a major challenge for supply chain managers, who must navigate inbound material sourcing and outbound logistics amid heightened uncertainty. The fact that the headline index has held near 50 is encouraging and suggest that the recent turmoil has not been enough to derail growth.

While the ISM Manufacturing PMI edged down 0.2 points to 48.5 in May—its third consecutive sub-50 reading—the report offered several signs of underlying resilience. After a brief winter rebound, manufacturing remains in contraction, but forward-looking components suggest the sector may be approaching a turning point.

The New Orders Index rose 0.4 points to 47.6, offering a tentative sign that demand may be stabilizing. Several respondents cautioned that overseas orders remain weak, contributing to ongoing customer hesitation. While buyers are still wary amid pricing volatility and policy uncertainty, the modest improvement in the survey’s most forward-looking component is a welcome development.

The ISM Manufacturing Index remains near 50, highlighting the factory sector’s resilience.

Production rose 1.4 points to 45.4, remaining below the key 50 breakeven threshold, which signals more manufacturers cutting output than increasing it. Firms cited improving customer inventories and selective strength in machinery and electronics, though food processing and transportation continue to lag.

The employment index edged up to 46.8—its second straight gain—suggesting the pace of layoffs is moderating, even as overall hiring remains cautious

Headcount reductions are ongoing but more targeted—some firms are relying on attrition and hiring freezes rather than outright cuts. This aligns with broader labor data showing a plateau in manufacturing payrolls through mid-Q2. Many manufacturers remain chronically short of workers, however, so even the extended lull in activity may not leave them overstaffed.

Input costs remain stubbornly high, with the Prices Paid Index falling just 0.4 points to a still elevated 69.4. The marginal decline reflects slight relief in diesel and natural gas prices, but tariffs continue to complicate cost planning. The index has risen 19.1 points over the past six months. Respondents were explicit: most suppliers are passing through the full burden of tariffs, treating them as taxes.

Most suppliers are passing through the full burden of tariffs, treating them as a tax hike.

Trade remains the weakest link. New export orders plunged to 40.1—the lowest reading outside of COVID since the Great Recession. Imports also cratered, falling to 39.9 amid softer domestic demand and intensifying tariff friction. Multiple panelists described the latest tariff rollouts as more disruptive than COVID, citing shipment delays, canceled orders, and rising customer skepticism around forward pricing.

Inventories contracted sharply, with the index falling 4.1 points to 46.7. The pull-forward strategy that dominated earlier in the year appears to have run its course. Companies are now focused on reducing exposure to policy risk and fortifying balance sheets.

Customer inventories are relatively low, which could drive orders higher in coming months.

The Customers’ Inventories Index fell 1.7 points to 44.5 in May, indicating inventories at the customer level remain too low. While not a direct measure of output, this continued drawdown is typically viewed as a positive signal for future production. Survey respondents noted that products are understocked among customers, suggesting restocking could provide a modest lift to demand in the months ahead.

While the PMI remains in contraction, the broader takeaway from the May report is that recent tariff turmoil is not enough to derail economic growth. At 48.5, the index is consistent with modest GDP expansion—likely near 2%. The underlying details were also constructive: four of the five subcomponents used to calculate the headline PMI improved, including new orders, the most forward-looking of the survey

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Tariffs and Inflation: A Taxing Debate

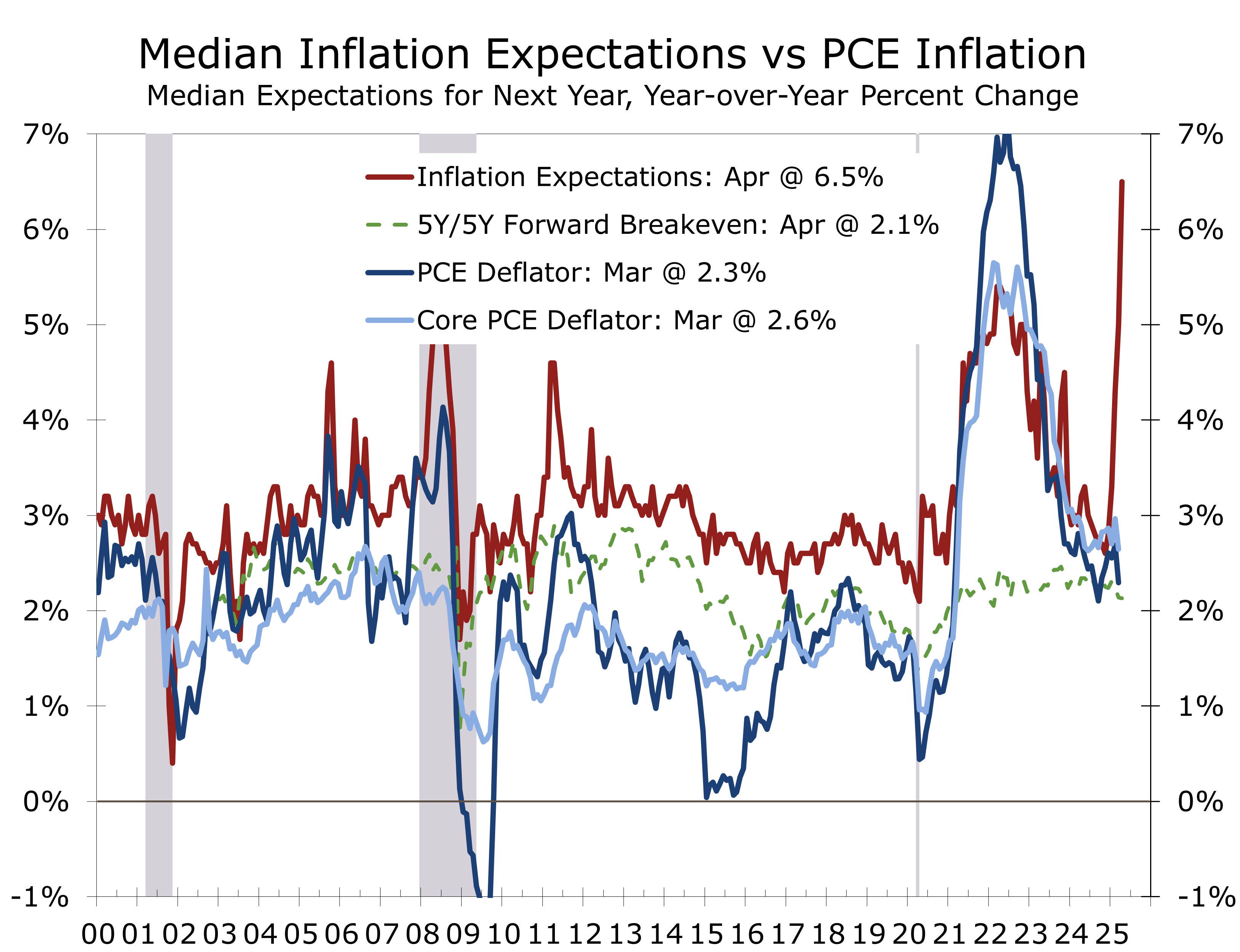

Inflation Remains Well Short of Expectations

- Tariffs continue to dominate the economic discussion and remain the key driver of market volatility.

- Consumer surveys show sharply rising near-term inflation expectations, but data suggest more limited long-term inflation.

- Milton Friedman’s framework supports the idea that tariffs are not inflationary unless the Fed accommodates them.

- April PCE data showed muted inflation, with slowing consumption and a continued moderation in services prices.

- Treasury Secretary Bessant defends tariffs as targeted and non-inflationary; calls for offsetting tax cuts.

- Larry Summers warns of "stagflation-lite" and potential Fed policy missteps.

- Concerns over inflation expectations and supply chain risk are driving the Fed’s cautious stance.

- We expect the Fed to continue unwinding the tightening put in place from early 2022 to mid-2023 and look for two quarter point cuts during the second half of 2025, offsetting some of the drag tariffs have placed on an already slowing economy.

Tariffs and Inflation

Tariffs continue to dominate the economic discussion and remain a key driver of market volatility. One critical question persists: are tariffs inflationary or disinflationary? The most widely followed consumer surveys suggest Americans expect higher prices—both the University of Michigan’s Sentiment Index and the Conference Board’s Consumer Confidence Survey have registered upticks in inflation expectations. But as is typically the case with survey data, the deeper question is what tariffs actually do to inflation. As taxes on imports, they do not expand the money supply. Instead, they distort relative prices—altering the structure of spending more than fueling a rise in the overall price level.

The inflationary impact of tariffs is not as straightforward as it appears at first glance.

One of Milton Friedman’s most famous and defining axioms is that inflation is “always and everywhere a monetary phenomenon.” Within that framework, tariffs are not inflationary unless the Fed allows them to be—either by over-accommodating or by failing to distinguish between one-off price adjustments and persistent cost pressures. That logic underpins the Federal Reserve’s current pause. Despite slowing inflation and a modestly restrictive monetary policy, Chair Jerome Powell has signaled the Fed is not ready to cut interest rates further and will ‘wait and see’ how tariffs ripple through the data.

The latest inflation print supports that stance. The PCE deflator rose just 0.1% in April. Headline inflation eased to 2.1% year-over-year; core PCE slipped to 2.5%. Both are within striking distance of the Fed’s 2% target, particularly with the labor market near full employment. No broad acceleration is evident.

The underlying data are also supportive. Personal income rose 0.8%, driven by a 2.8% surge in transfer payments related to retroactive benefits under the Social Security Fairness Act. Wages and salaries—the core driver of consumer spending—climbed a solid 0.5%. Consumption increased just 0.2%, however, a sharp slowdown from March’s 0.7% gain. Notably, all of April’s increase came from services, reversing the prior month’s strength in goods. Durable goods outlays—particularly on autos and recreational equipment—feel after a March spike, as consumers appeared to front-load purchases ahead of tariff hikes. Since services account for roughly two-thirds of consumer spending, continued price restraint in this category would help limit broader inflation pressures.

The spending spree may have temporarily lifted goods prices and then reversed in April. Overall goods prices fell 0.1% in April, with grocery prices down 0.3% and gasoline prices edging slightly lower. Core goods prices eased as well, although some categories, including motor vehicles (+0.2%), furniture (+0.4%), and recreational goods and RVs (+1.5%) posted gains.

Service prices—largely insulated from import tariffs—rose just 0.1% in April after a 0.2% gain in March. Financial services prices tumbled 1.1%, reflecting the April equity selloff. Prices for recreational services fell 0.7%, driven by lower costs for sporting and cultural events. The closely watched “super core” index—which excludes housing and energy services—was flat in April. The slower pace in services inflation over the past two months may be an early signal of cooling demand in non-tradable sectors.

If consumers are spending more on tariffed imports, they have less to spend elsewhere.

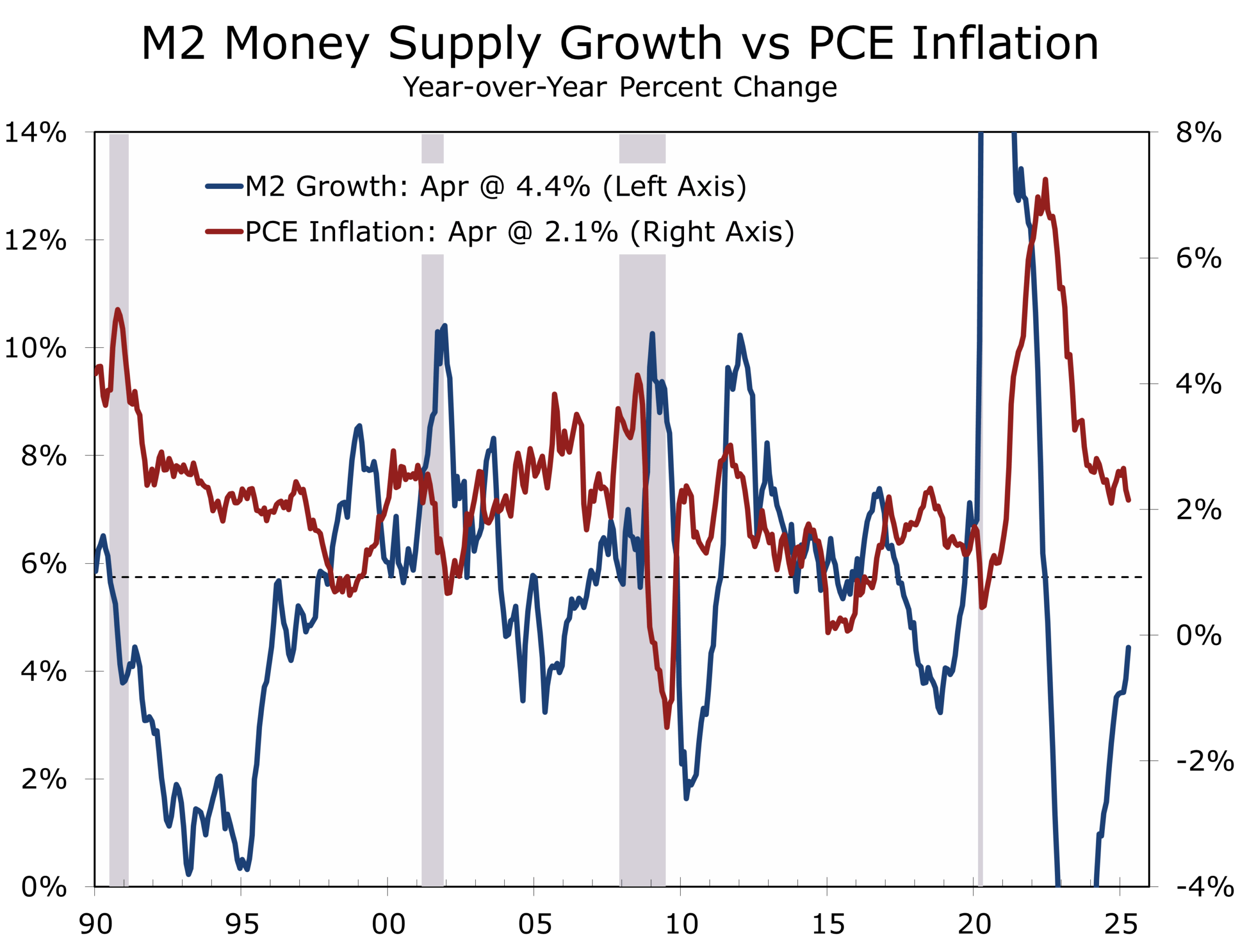

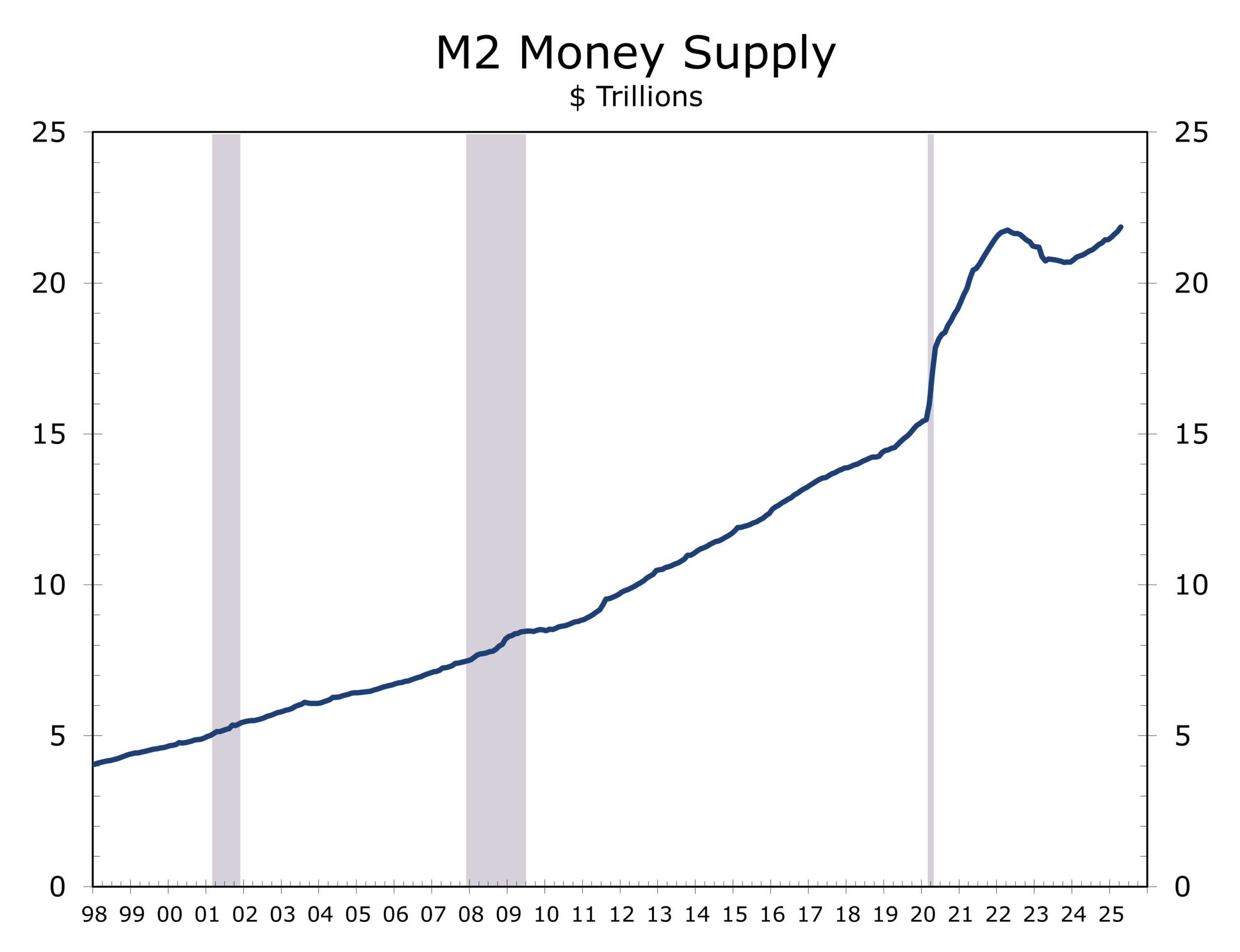

Tariffs raise prices on tradable goods and on goods and services reliant on imported components—they do not increase the money supply. If consumers are spending more on tariffed imports, they may have less to spend elsewhere—unless the Fed injects additional liquidity. This dynamic should limit inflation’s reach. The latest data show the M2 money supply has risen 4.4% over the past year, more than a percentage point below its 5.7% average pace since 1990.

The latest data strengthen the Trump administration’s argument that tariffs will not prove broadly inflationary. While that assessment may be optimistic, tariffs are likely to add less to inflation than consumers currently fear. We expect the economic data to bolster this point in coming months.

Treasury Secretary Scott Bessant appears prescient. He called the tariffs “surgical and necessary,” targeting strategic sectors like electric vehicles, solar panels, and steel. “These measures aren’t hitting staples,” he said on May 30. “We’re not seeing broad inflationary spillovers.” Bessant also suggested that tariff revenues could partially fund offsetting tax cuts. On Meet the Press, he remarked, “If taxes are inflationary, then cutting taxes is deflationary”—a deliberate effort to reframe tariffs not as inflationary fuel, but as a potential fiscal rebalancing tool.

Not all agree. Larry Summers, speaking with Bloomberg in May, warned that tariffs could lead to “stagflation-lite”—weaker growth paired with stickier prices in targeted sectors. He cautioned that mistaking sector-specific pressures for system-wide inflation could provoke a Fed policy error. Research from the Yale Budget Lab estimates that the 2025 tariff rounds—including the recent EU retaliation—could lift the PCE price level by 0.5 percentage points by year-end, relative to where it would otherwise be.

What would Milton Friedman say? Friedman staunchly opposed tariffs in nearly all forms. He would likely have argued that tariffs are primarily a tax that distorts market efficiency, with their inflationary or disinflationary impact depending on context. He would emphasize that tariffs raise the cost of imported goods, potentially increasing prices if domestic substitutes are pricier or supply chains are disrupted. However, he might also note that tariffs act as a tax by reducing consumer purchasing power, which could dampen demand and exert disinflationary pressure elsewhere. Friedman would likely stress that the net effect hinges on market dynamics and the economy’s underlying momentum

Treasury Secretary Scott Bessant appears prescient. He called the tariffs “surgical and necessary,” targeting strategic sectors like electric vehicles, solar panels, and steel. “These measures aren’t hitting staples,” he said on May 30. “We’re not seeing broad inflationary spillovers.” Bessant also suggested that tariff revenues could partially fund offsetting tax cuts. On Meet the Press, he remarked, “If taxes are inflationary, then cutting taxes is deflationary”—a deliberate effort to reframe tariffs not as inflationary fuel, but as a potential fiscal rebalancing tool.

Not all agree. Larry Summers, speaking with Bloomberg in May, warned that tariffs could lead to “stagflation-lite”—weaker growth paired with stickier prices in targeted sectors. He cautioned that mistaking sector-specific pressures for system-wide inflation could provoke a Fed policy error. Research from the Yale Budget Lab estimates that the 2025 tariff rounds—including the recent EU retaliation—could lift the PCE price level by 0.5 percentage points by year-end, relative to where it would otherwise be.

What would Milton Friedman say? Friedman staunchly opposed tariffs in nearly all forms. He would likely have argued that tariffs are primarily a tax that distorts market efficiency, with their inflationary or disinflationary impact depending on context. He would emphasize that tariffs raise the cost of imported goods, potentially increasing prices if domestic substitutes are pricier or supply chains are disrupted. However, he might also note that tariffs act as a tax by reducing consumer purchasing power, which could dampen demand and exert disinflationary pressure elsewhere. Friedman would likely stress that the net effect hinges on market dynamics and the economy’s underlying momentum.

Friedman would fundamentally oppose tariffs for their interference with free trade, predicting long-term inefficiencies—protected industries tend to be less creative and productive—over short-term price effects. This angle remains underappreciated in the current debate.

Tariffs threaten inflation by raising expectations and potentially disrupting supply chains.

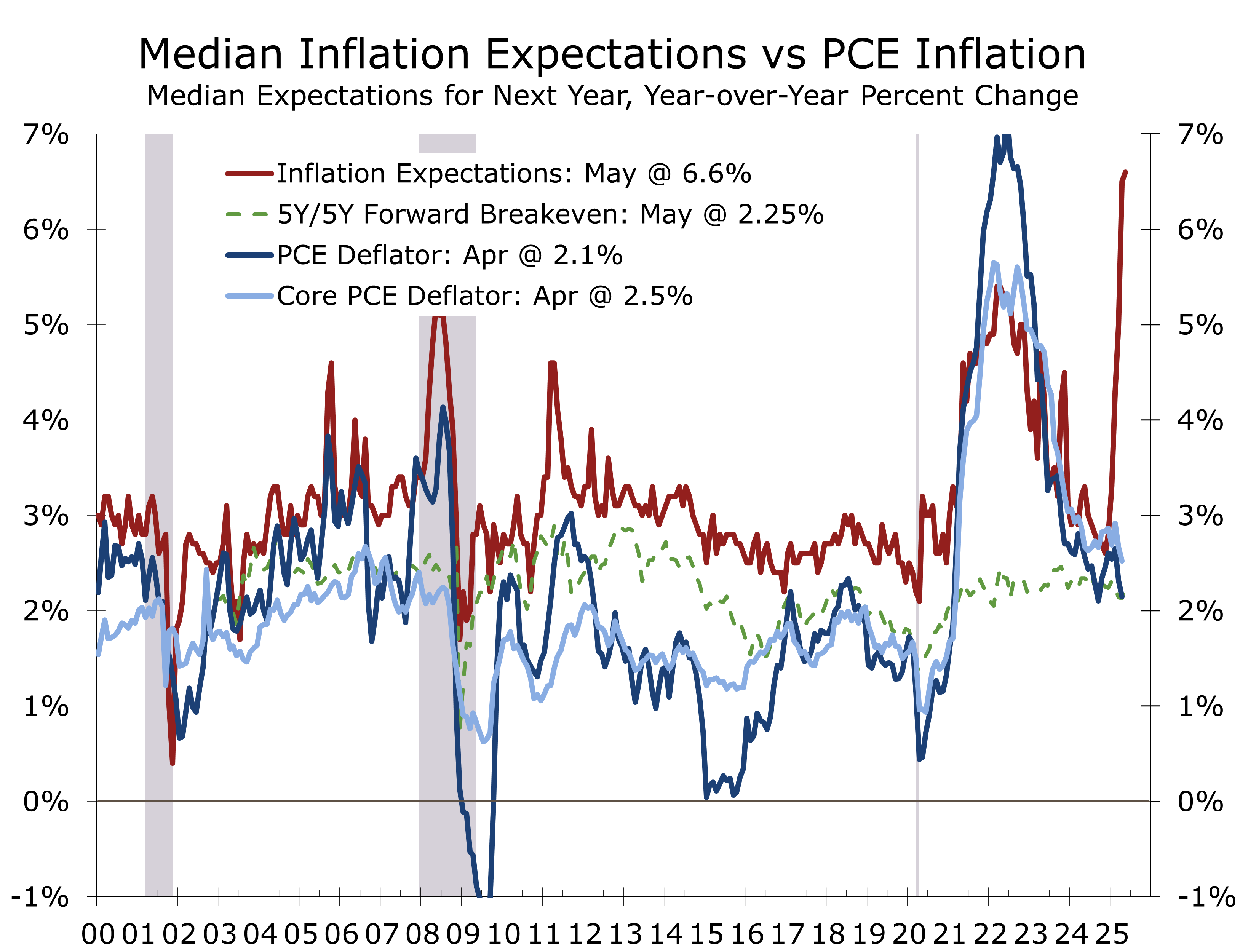

Two key concerns are driving the Fed’s cautious ‘wait and see’ posture: the sensitivity of inflation expectations and the risk of renewed supply chain disruptions. While short-term expectations have spiked, long-term expectations remain mostly anchored. The Fed knows that if businesses and households begin to believe inflation is persistent, it could trigger wage demands and forward-pricing behavior—embedding inflation into economic decisions and pushing rates and volatility higher. Anchoring expectations is critical to maintaining monetary policy credibility.

Supply chain fragility is the other wildcard. Memories of post-pandemic logistics bottlenecks and component shortages are still fresh. With tariffs reinstated and global trade relations under pressure, the Fed is watching closely for signs of renewed stress. Powell and others have pointed to shipping costs, commodity volatility, and reshoring dynamics as potential inflation channels. Many economists in the “Team Transitory” camp still argue that the inflation surge that coincided with the reopening of the economy was driven more by pandemic-era supply snarls than by the 40% jump in M2 that followed the onset of the pandemic.

At its May meeting, the FOMC held rates steady at 4.25% to 4.50%. Minutes revealed most policymakers now see upside risks to inflation. Powell, in his post-meeting press conference, reiterated the Fed’s “wait-and-see” approach. “We can’t say which way this will shake out,” he said, citing the unusual supply-side nature of the risks. Dallas Fed President Lorie Logan noted that it “could take quite some time” before rate cuts are appropriate. New York Fed’s John Williams and Richmond’s Tom Barkin likewise emphasized the need for patience as tariff effects and global trade frictions evolve.

Markets are left parsing a complex signal. Tariffs may not be reigniting inflation as much as feared, but they’re clearly reshaping consumer behavior. The tax burden is real—even if it hasn’t fully registered in the indices. For the Fed, the challenge is distinguishing signal from noise. We still expect two rate cuts before year-end, with the first likely coming in September.

The key question now is whether short-term inflation fears begin seeping into long-term expectations. The University of Michigan’s survey shows a notable uptick, though it has become increasingly politicized. The Fed places more weight on market-based indicators—particularly the five-year forward breakeven. Absent a sustained rise in this measure, we expect the Fed to continue unwinding its 2022–2023 tightening cycle. They will need to proceed cautiously, however, because the noise surrounding the spike in consumer inflation expectations is highly visible and loud. Some reprieve will likely be needed before the Fed moves forward with what we expect to be two quarter point cuts in the federal funds rate, which should help offset the drag tariffs are having on an already slowing economy.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

June 2, 2025

Mark Vitner, Chief Economist

(704) 458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Trade Winds Shift: Q2 Growth Prospects Surge on Import Collapse

Trade Winds Shift: Q2 Growth Prospects Surge on Import Collapse

Highlights of the Week

- The U.S. trade deficit was nearly halved in April as imports collapsed, turning net trade into a major tailwind for Q2 GDP. The Atlanta Fed’s GDPNow model surged in response.

- Durable goods orders fell 6.3% in April due to a sharp drop in commercial aircraft bookings, while core orders and shipments showed modest resilience.

- Q1 GDP was revised slightly upward to a -0.2% contraction, but underlying private domestic demand was revised lower.

- Personal income jumped 0.8% in April, lifted by solid wage growth and retroactive Social Security payments; consumption rose a modest 0.2%.

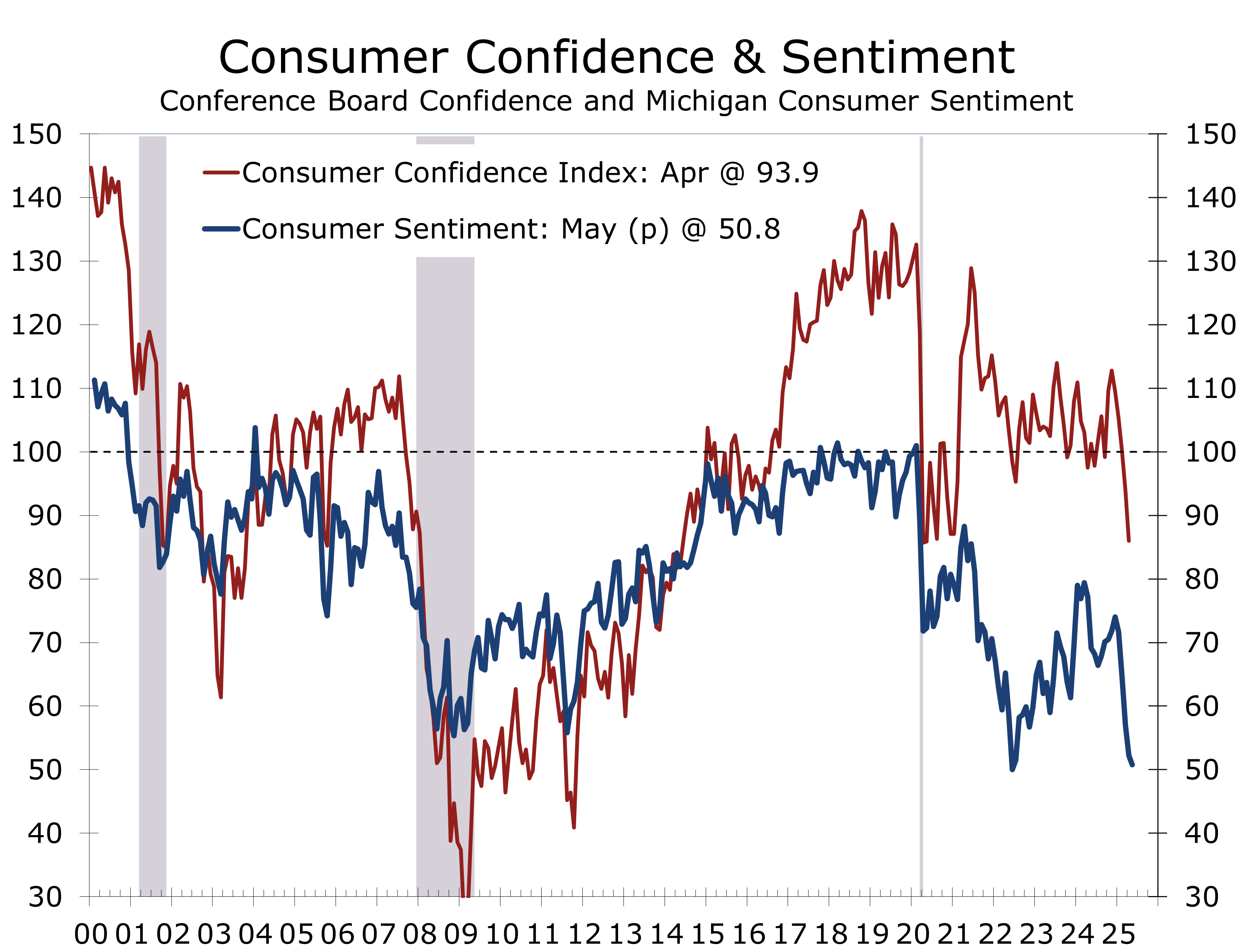

- Consumer confidence rebounded sharply in May, while consumer sentiment improved only modestly and remains historically low.

- Labor market signals continue to soften: the labor differential narrowed for a fifth month and continuing jobless claims hit their highest level since November 2021.

- Russia unleased another brutal attack on Ukraine and is threatening more decisive action, prompting Trump to issue a harsh denunciation of Putin.

- The Fed remains in wait-and-see mode amid sticky inflation and rising employment risks. The markets appear set for a December rate cut but we feel the Fed will move sooner.

Markets Digest Crosscurrents in Trade and Growth

Consumers, businesses and the financial markets continue to grapple with a multitude of macroeconomic and geopolitical crosscurrents. Tariffs and higher interest rates remain the top concern, but there is a growing realization that Trump’s tariffs are designed to bring about trade deals, promote national security and help reshore key parts of the manufacturing sector rather than to severely restrict trade. The extension of the timeline to reach a deal with the European Union is a prime example, as is the President’s post on Truth Social bemoaning China’s unwillingness to comply with the terms of the most recent trade truce. The talk rattled the markets late Friday, as Trump said he was readying new remedies.

The trade deficit appears to be swinging back from its first quarter plunge, boosting Q2 GDP.

New court rulings are adding complexity but not reversing the trade trajectory. On May 28, the U.S. Court of International Trade ruled that several of the administration’s “Liberation Day” tariffs imposed under the International Emergency Economic Powers Act (IEEPA) were invalid. The Trump Administration has already appealed the decision and was granted a temporary stay, allowing the tariffs to remain in effect for now. Legal experts expect the Supreme Court to ultimately hear the case and likely affirm most of the president’s authority under existing national security-based trade statutes. The tariffs most at risk are the reciprocal tariffs applied to U.S. allies, rather than those targeting strategic rivals such as China. Even if the appeals court upholds the lower court’s decision, the president retains other statutory pathways—such as Section 301 and broader national security provisions—to reimpose similar trade barriers. We expect trade negotiations to continue at their recent pace and look for some deals to be announced in coming weeks.

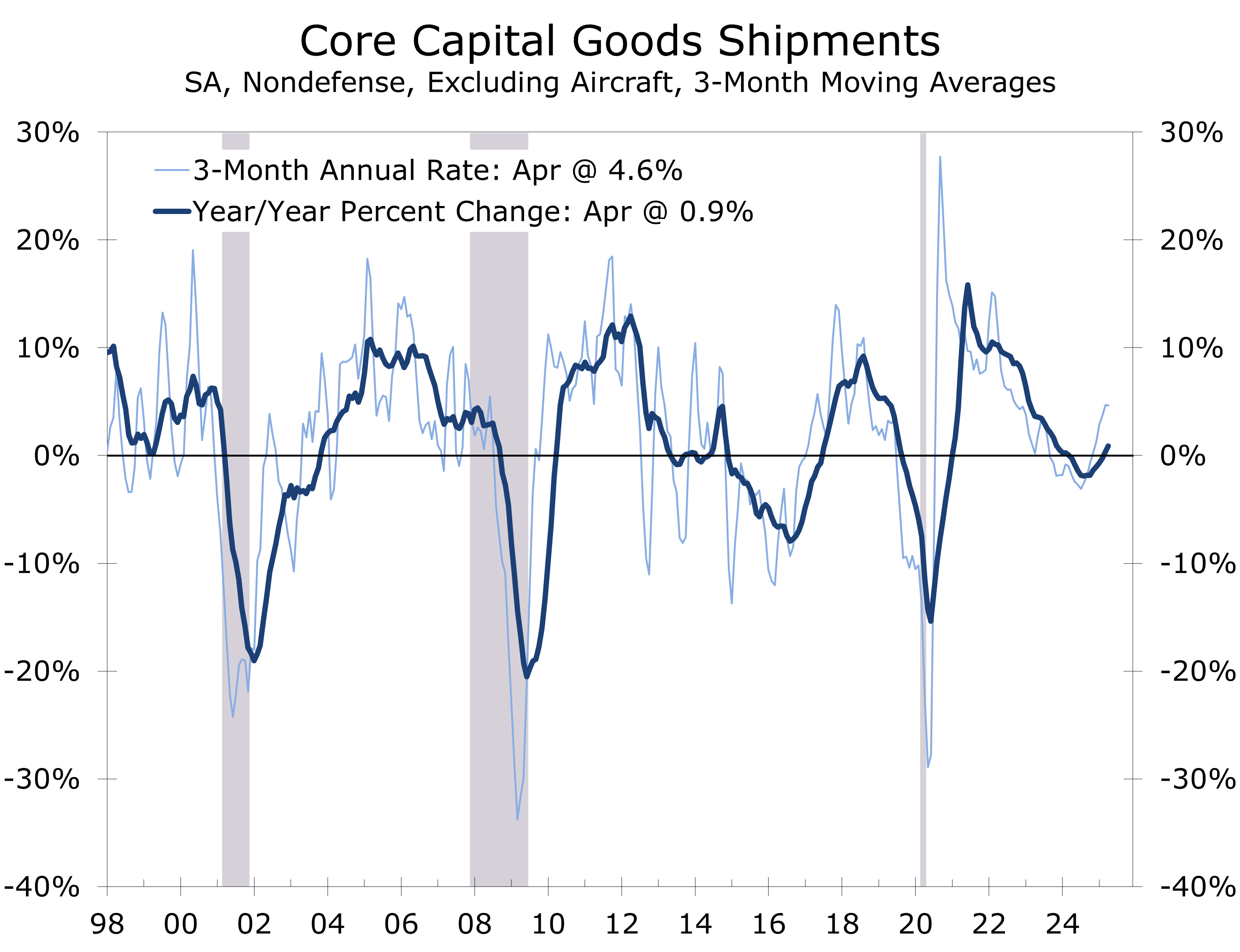

Earlier tariff announcements and efforts to stay ahead of anticipated trade barriers have disrupted recent economic data and are likely to continue doing so into the current quarter. The impact was particularly evident in the April durable goods report. Headline orders plunged 6.3%, largely reflecting a reversal in commercial aircraft bookings, which had surged in March. Commercial aircraft orders are expected to rebound in the coming months following President Trump’s visit to the Middle East and a blockbuster order from Qatar Airways. Excluding transportation equipment, durable goods orders rose 0.2%, indicating some underlying resilience. Orders for nondefense capital goods excluding aircraft—a key proxy for business fixed investment—declined 1.3%, and core shipments edged down 0.1%. These declines follow stronger results in March, as firms pulled forward activity ahead of tariff announcements.

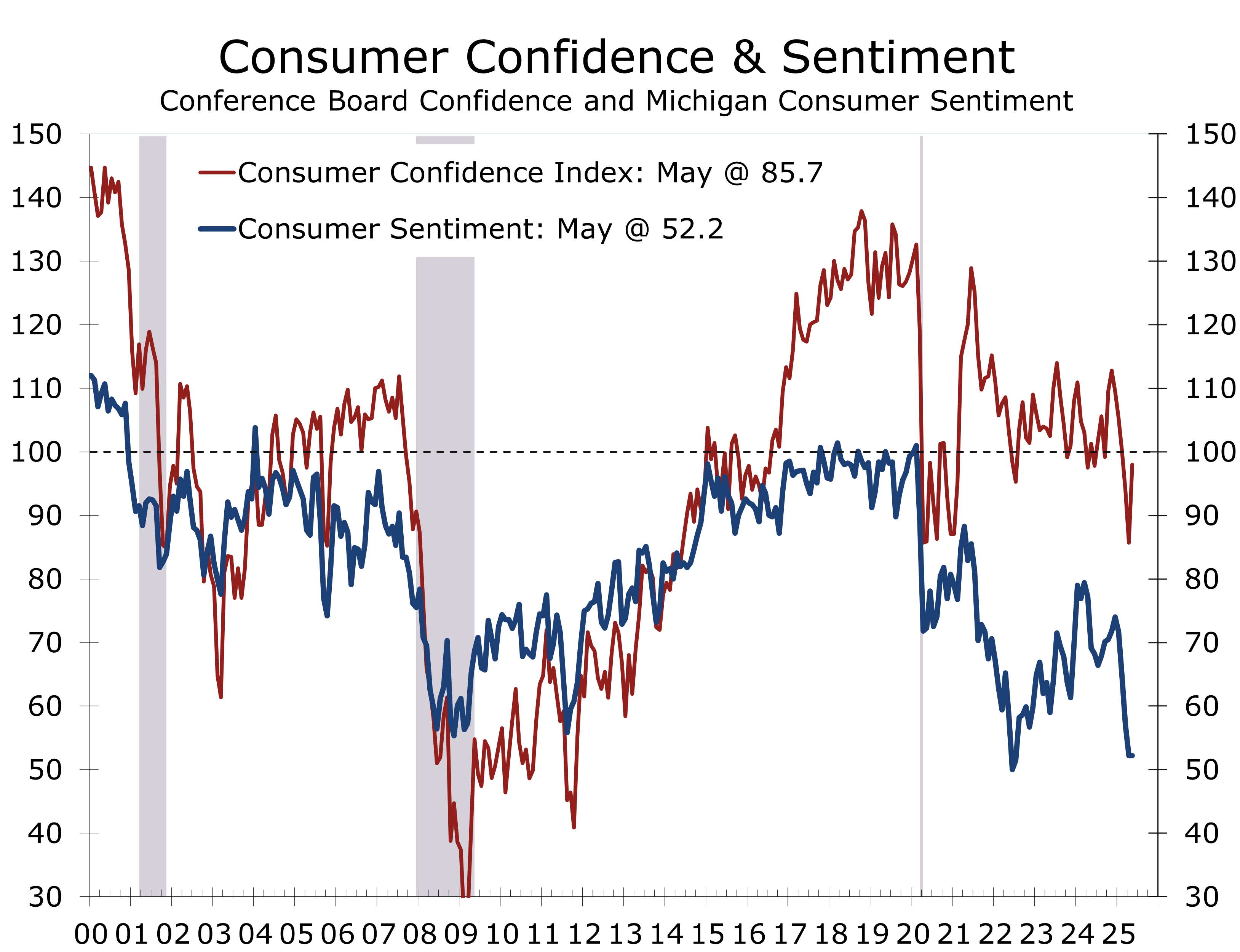

Consumer confidence surged in May, reflecting relief from the partial but significant rollback of earlier tariff hikes on China and a better understanding of how trade policy is likely to evolve. The Conference Board’s Consumer Confidence Index rose 12.3 points to 98.0 in May. Consumers’ assessment of current economic conditions improved modestly, but the expectations component—which tends to influence actual consumer behavior more directly—posted a more substantial rebound. Sentiment was buoyed by equity market gains and a more optimistic outlook for income growth and stock prices. Inflation expectations eased for the first time since late 2024, but labor market perceptions softened slightly, with the labor market differential edging lower. While fears of a recession have subsided, they remain elevated, and policy volatility will likely keep confidence readings choppy in the months ahead.

With tariffs top of mind, businesses have slowed hiring, making it difficult to land a new job.

The Conference Board’s labor market differential —the difference between the share of consumers stating jobs are plentiful versus those saying jobs are hard to get—narrowed in May, falling 0.6 points to 13.2. This marks the fifth consecutive monthly decline and likely signals a further slowdown in hiring. Businesses have become more cautious amid volatility in policy announcements and market swings, contributing to reduced job postings.

While hiring has clearly slowed, layoffs do not appear to have materially increased. Weekly unemployment claims continue to show that initial claims remain historically low, but continuing claims have been trending higher. As of late May, continuing claims reached 1.91 million—the highest level since November 2021—suggesting that job seekers are having a harder time finding new employment. This trend suggests growing friction in labor re-entry, possibly reflecting mismatches in skill sets or simply a reduced hiring appetite in rate-sensitive sectors. Unemployment claims have risen a bit more in the greater Washington D.C. area, reflecting substantial public sector job cuts.

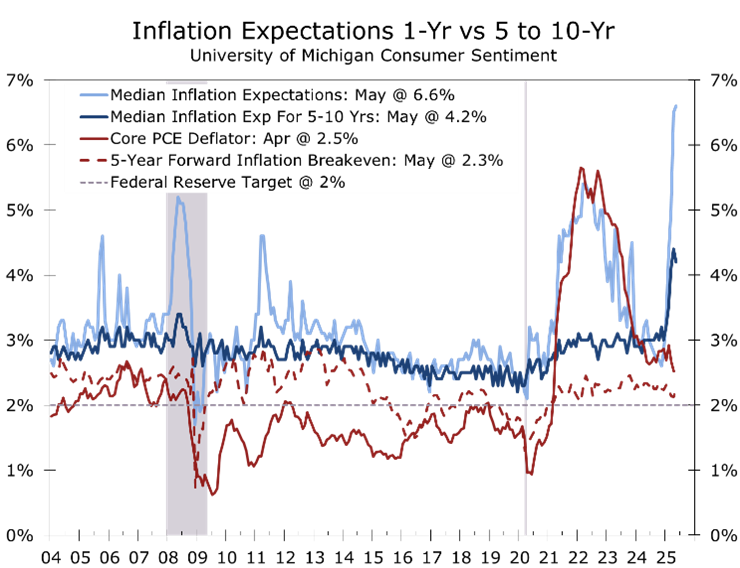

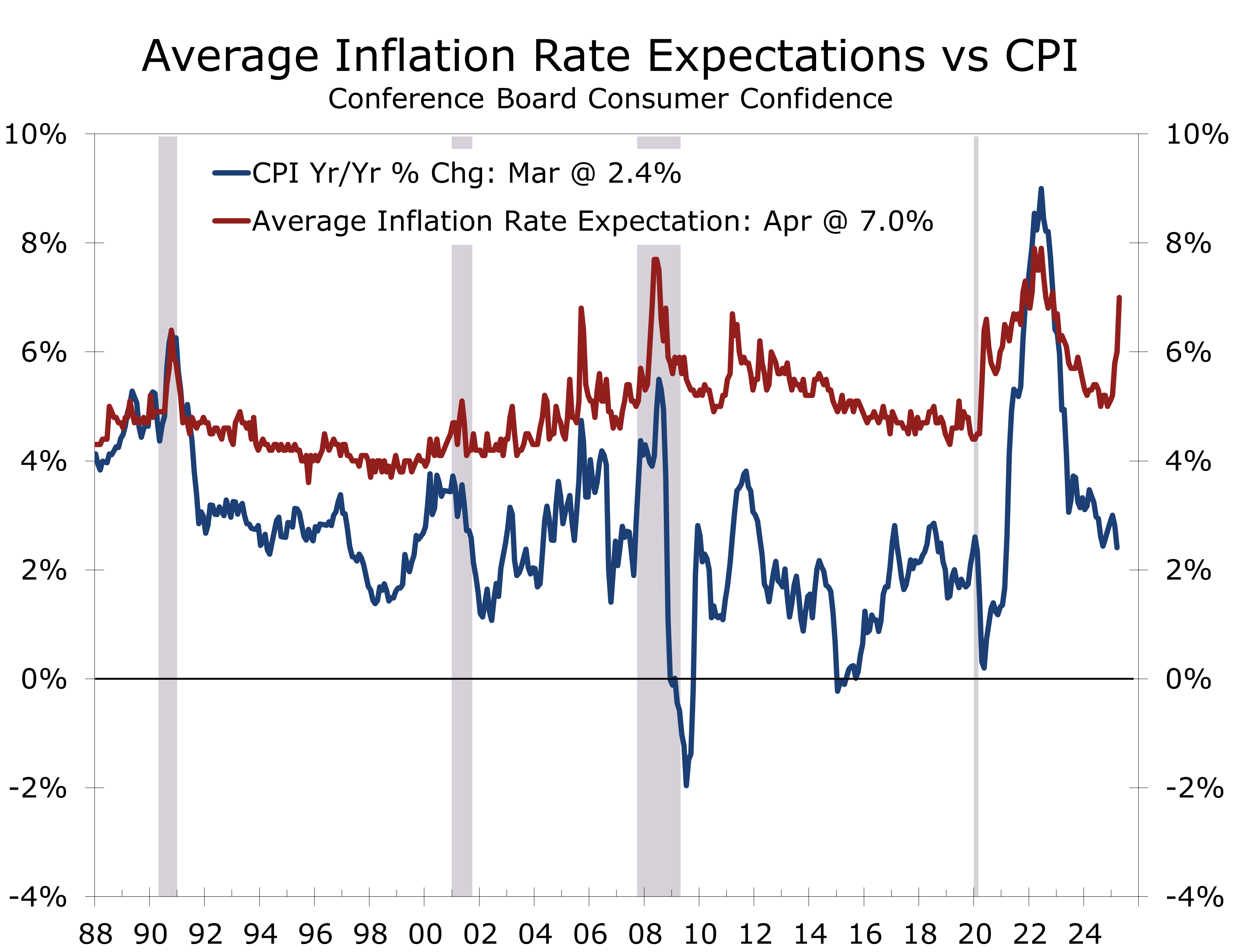

The Conference Board’s results were more pronounced than those released by the University of Michigan on Friday. Consumer Sentiment was revised up only slightly to 52.2 from its early-month preliminary reading. While the revision ended a four-month streak of declines, sentiment remains historically low, and Consumer Sentiment is much further below its historic norms than Consumer Confidence is. The details of the report were more positive, however. Year-ahead inflation expectations were revised down to 6.6%, and long-run expectations fell to 4.2%—the first drop since December 2024. Consumers were more optimistic about future personal finances and buying conditions for big-ticket items, which suggest consumer spending should remain resilient.

Personal income growth has been stellar so far this year, supporting consumer spending.

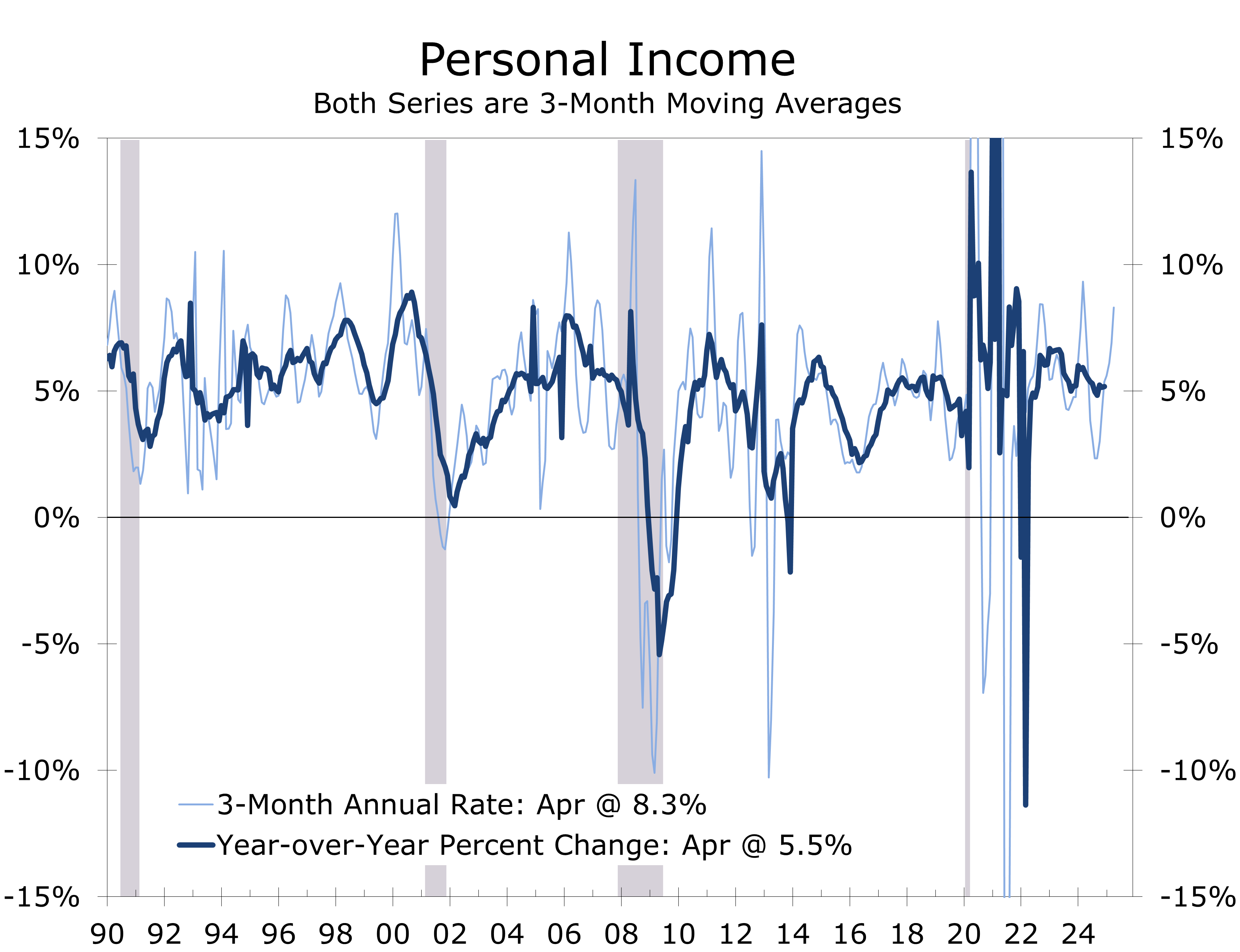

Personal income rose 0.8% in April, beating expectations and reflecting strength across wages and salaries and a significant boost from government transfers, particularly retroactive Social Security payments under the Social Security Fairness Act. Upward revisions to prior months’ data lifted the year-to-date trajectory: on a three-month moving average basis (3MMA), personal income is up 5.5% from last year, while wages and salaries are up 4.2%. Real disposable (after-tax) income rose 0.7% in April alone and is up 1.7% year-to-year, on a 3MMA basis.

Personal consumption rose a modest 0.2% in April, with all of the increase coming from services. Spending on goods fell slightly, driven by declines in durable categories like motor vehicles and recreational equipment, reflecting a partial reversal of March’s front-loading ahead of potential tariffs. Spending on services, particularly restaurant dining, rose solidly during the month. Consumer spending is up a solid 5.5% year-to-year. Given easing inflation expectations and the rebound in equity markets, we suspect spending regained some momentum in May.

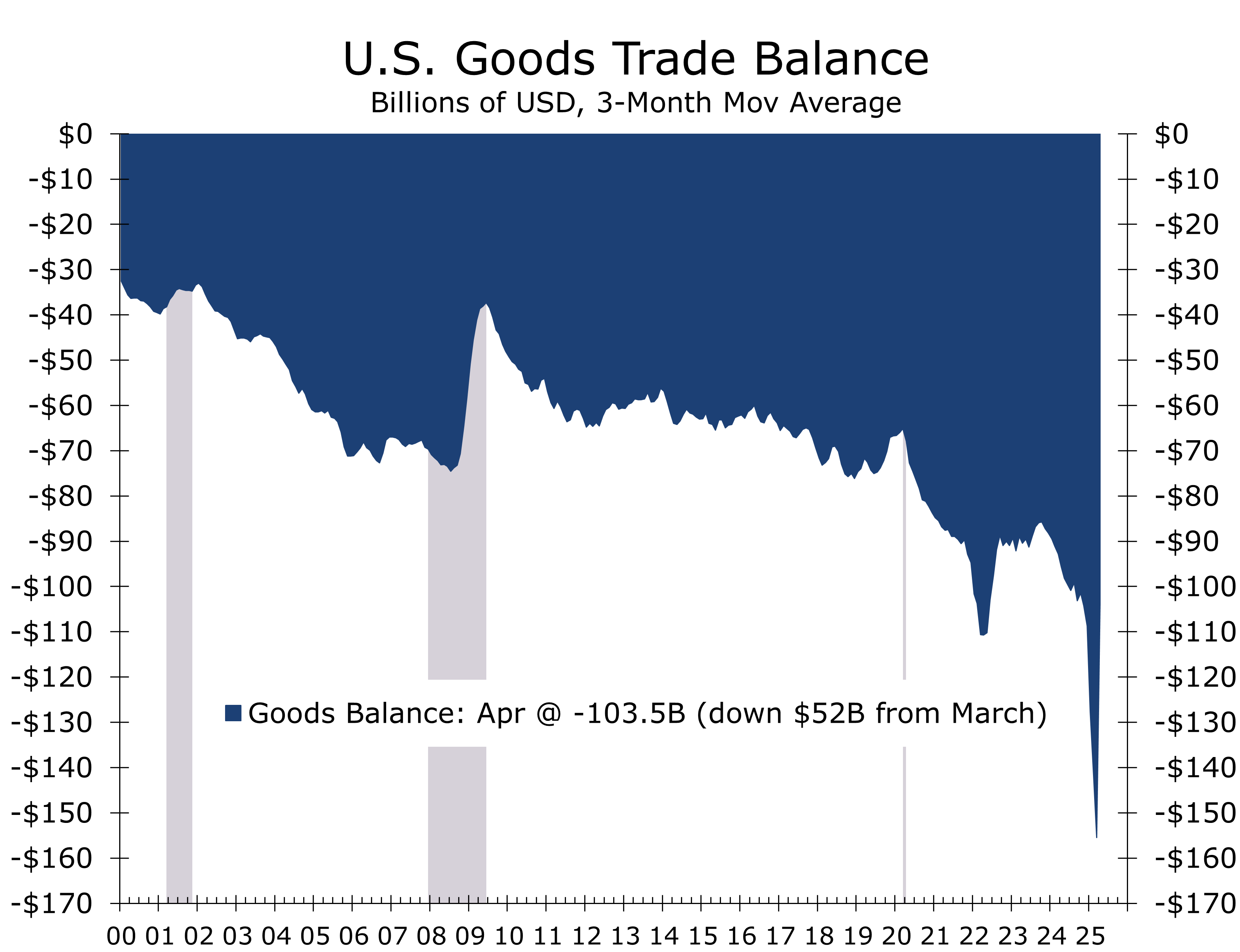

The U.S. goods deficit was nearly halved in April, plunging from $162.3 billion to $87.6 billion, as imports dropped by $68.4 billion—the steepest monthly decline in recent memory. The reversal reflects the unwinding of front-loaded purchases in Q1, collapsing arbitrage in gold flows, and a near standstill in Chinese imports following tariff hikes that temporarily pushed duties above 100%. The sharp import retrenchment—especially in pharmaceuticals, gold, and consumer goods—flipped net trade from a major Q1 drag to a sizable Q2 tailwind. The Atlanta Fed’s GDPNow tracker surged in response, suggesting trade alone may add more than two percentage points to Q2 GDP.

Although net exports are now boosting headline growth, the gains are unlikely to persist into the second half of the year. While some duties have been reduced, uncertainty surrounding future trade deals, retaliatory measures, and procedural constraints continues to cloud the outlook. For now, collapsing imports are alleviating recession fears prompted by the historic widening in the trade gap during the first quarter.

Both the overall and core PCE Deflator—the Fed’s preferred inflation measure—rose 0.1% in April. Inflation is still running well below consumer expectations, which have been hyped by tariff fears.

The May FOMC minutes reiterated that policymakers remain in wait-and-see mode. Although inflation has softened at the margin, the Fed is keenly aware that tariff-induced price pressures may re-emerge. Meanwhile, signs of a softer labor market and a strong dollar are providing room to hold policy steady.

The Fed continues to place a great deal of emphasis on the role inflation expectations play in containing inflation. The recent spike in inflation expectations in the consumer confidence surveys has gotten the Fed’s attention, although more reliable measures, such as the 5-year forward breakeven inflation rate and the New York Fed’s consumer survey, do not suggest expectations have deteriorated nearly as much.

The markets appear set that the Fed will remain on hold until December. We suspect the Fed is leaning toward an earlier rate cut, possibly late this summer but certainly sometime this fall. We feel labor market conditions are weaker than the nonfarm data have indicated and eventually that reality will be reflected in the data.

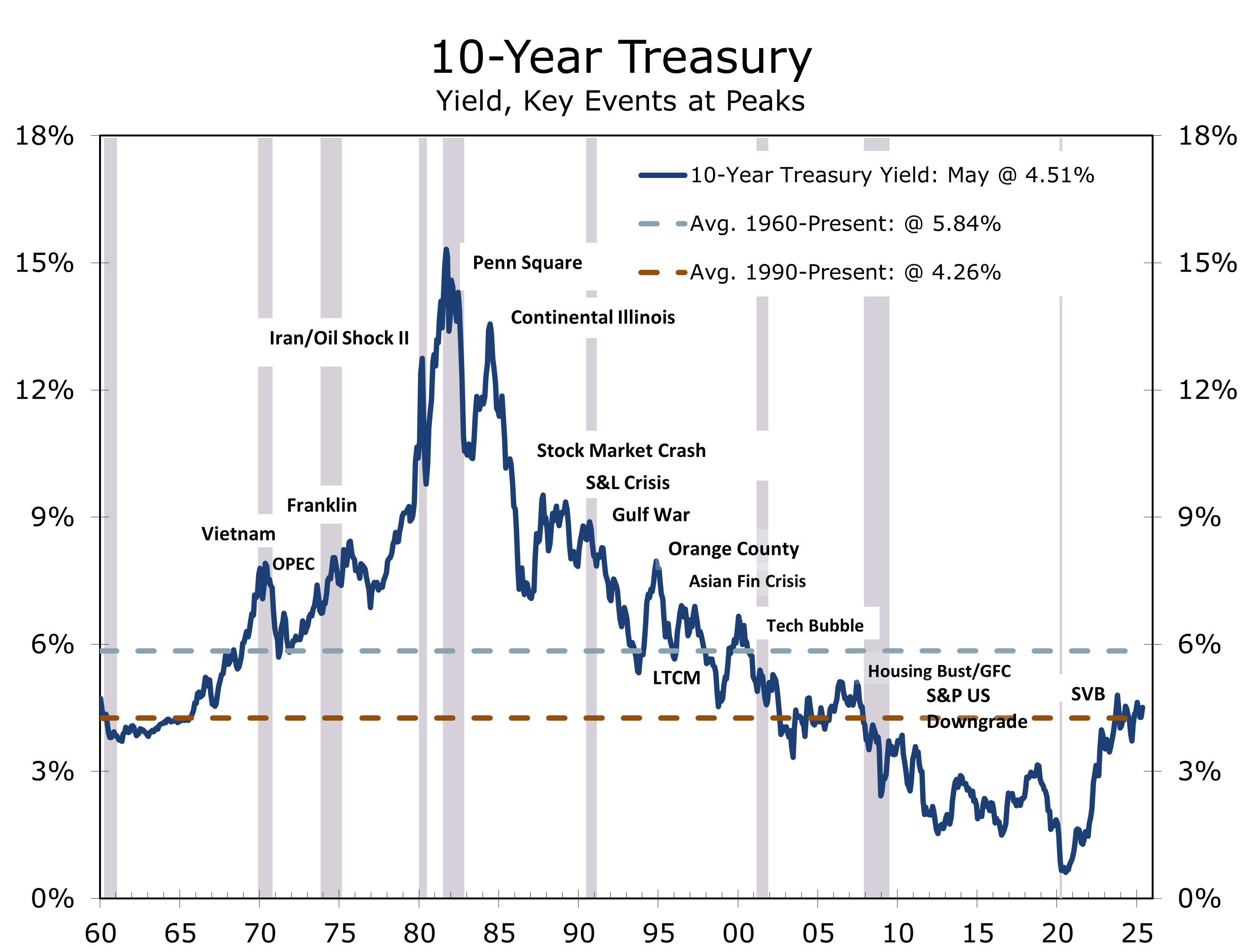

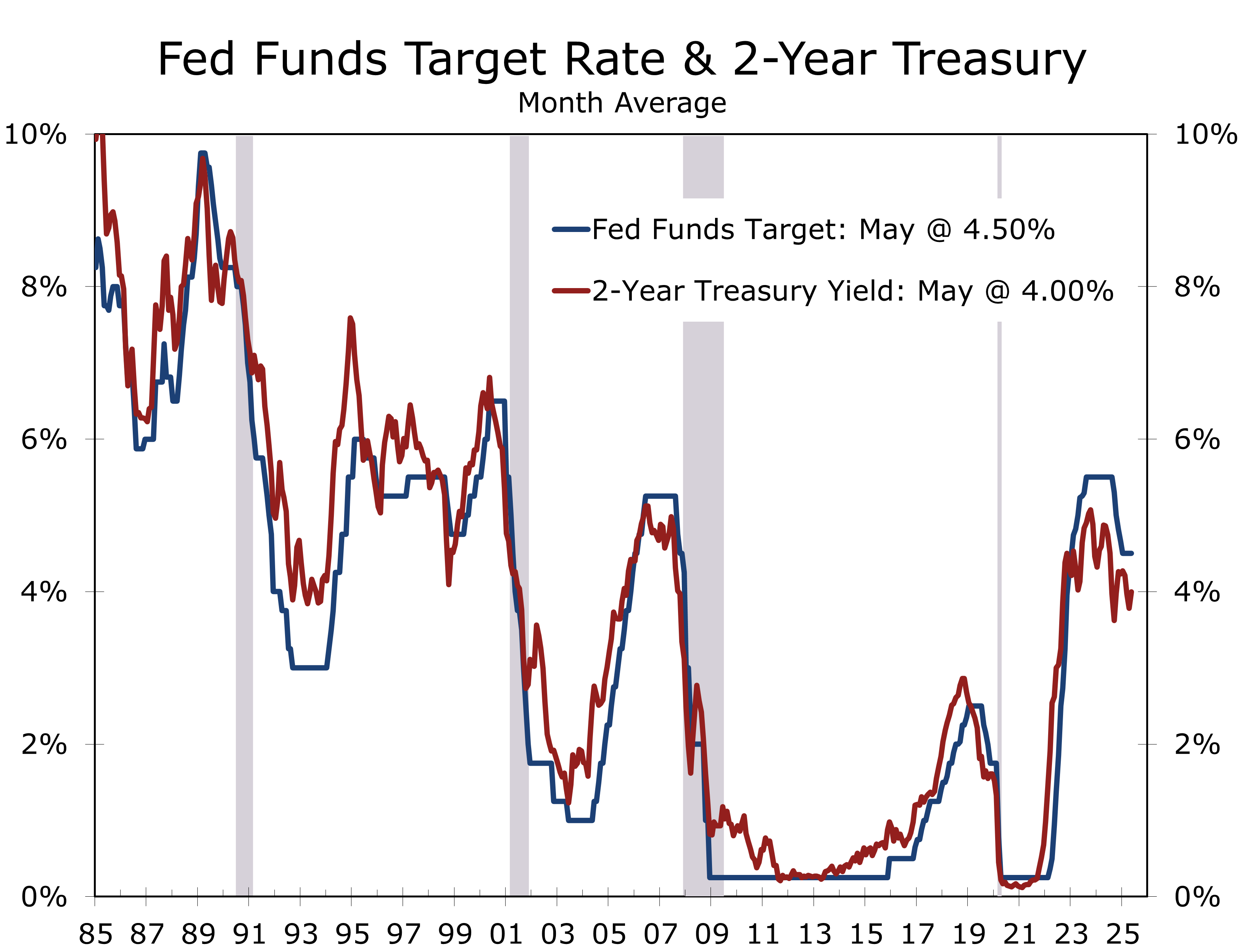

Treasury yields have been unusually volatile. Supply concerns and fiscal uncertainty continue to exert upward pressure on term premiums. The 30-year Treasury briefly rose above 5%, while the 10-Year Note rose above 4.50%, in the aftermath of the Moody’s downgrade and House Reconciliation Bill, which front loads stimulus and pushing budget savings in the out years. Yields peaked following last week’s disappointing 20-Year Treasury auction but have been trending lower ever since. Auctions have also been well bid, including a stellar 7-year Treasury auction this week. Investors appear to be positioning for growth to slow later this year, which aligns with our forecast.

China remains Russia’s economic lifeline but is playing hardball on energy and tech. For Moscow, a ceasefire could lock in territorial gains and stabilize the economy. For Trump, brokering one offers foreign policy clout, a potential market tailwind, and a way to lower NATO tensions.

The war has cost Russia $1.3 trillion, over 100,000 lives, and lasting economic damage. Quiet talks suggest Ukraine’s NATO bid is off the table, and neutrality is assumed. But some affiliation with Western Europe also seems inevitable. We had earlier pondered whether Ukraine could attain some sort of observer status within NATO, allowing for cross training with NATO members but no NATO bases on Ukrainian soil. That prospect seems more remote today. Even a formal peace remains distant, but a tactical ceasefire is increasingly likely.

Europe Pushes Back on Populism

Despite forecasts of a hard-right surge, Europe’s center held. Romania elected pro-European Nicușor Dan over nationalist George Simion. Portugal’s center-right outpaced the far right Chega party in parliamentary elections, which gained seats but not much clout. And Poland’s liberal candidate secured a run-off spot against his nationalist rival.

Looking Ahead: June 2-6, 2025

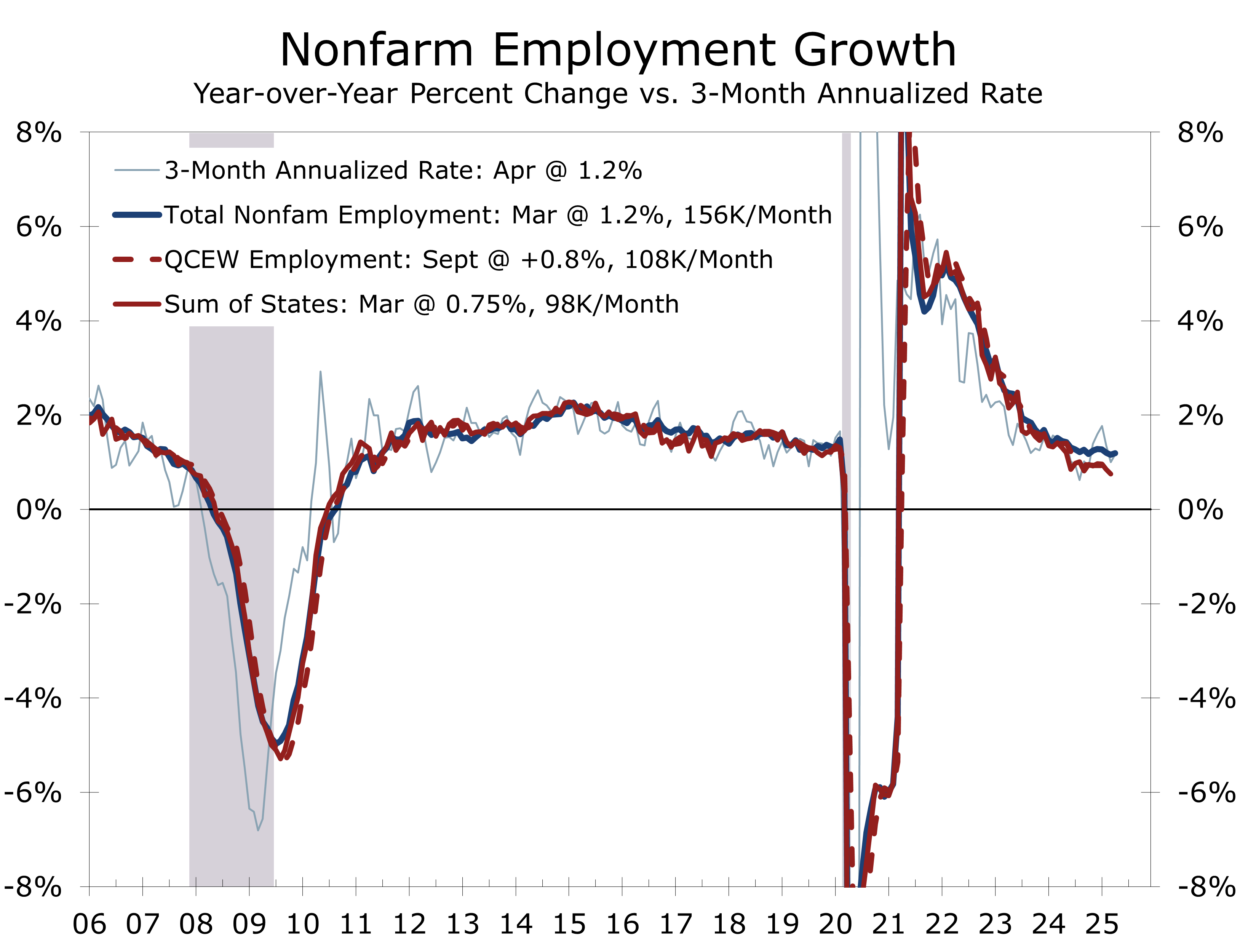

The May employment report will headline another busy week of economic reports. We are projecting a middle-of-the-road 145,000-job gain but are also looking for an 0.1 point uptick in the unemployment rate. The labor data can be unusually volatile in May due to the timing of school year end. With hiring slowing, the seasonals could overcompensate, yielding a much weaker number than expected.

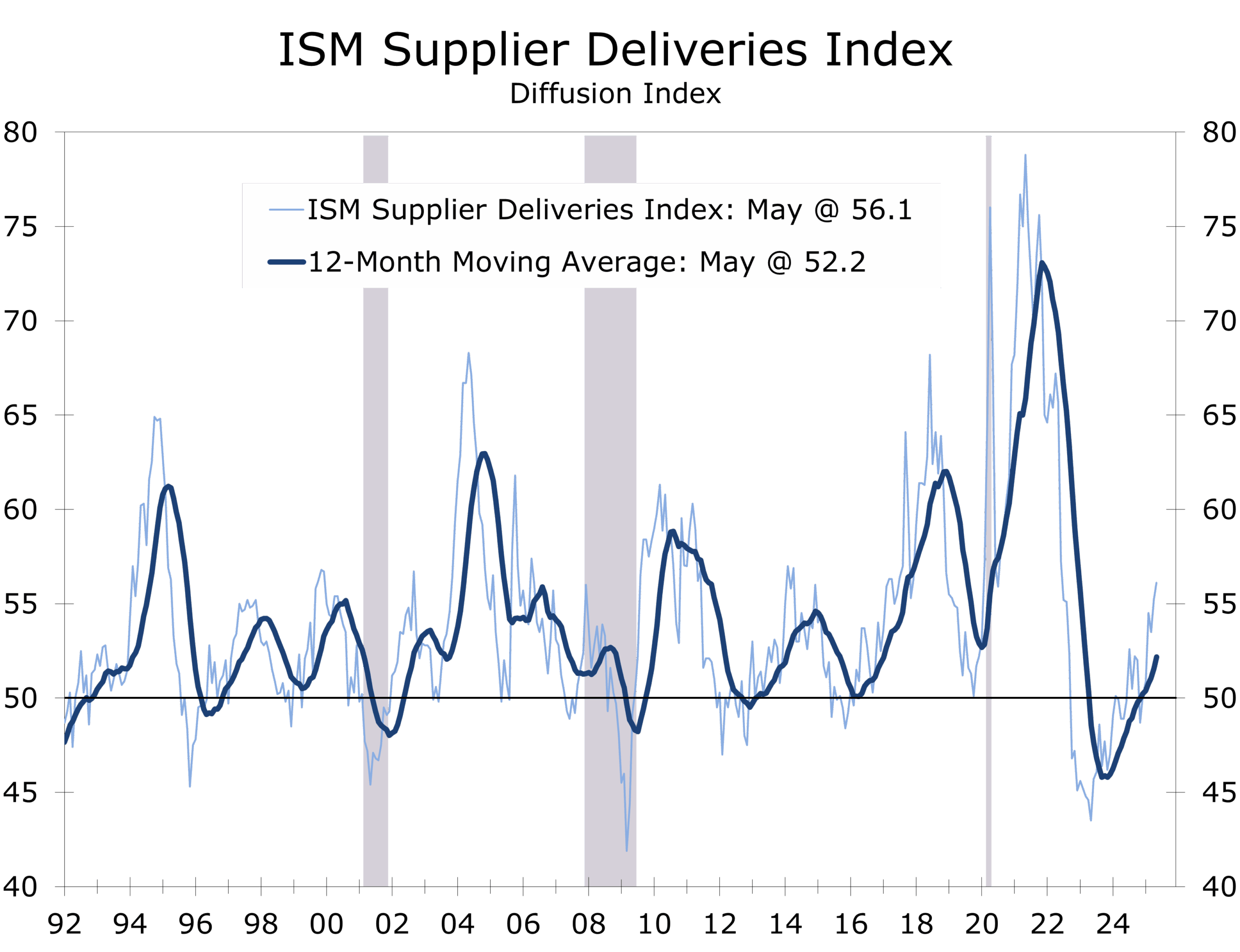

- Monday: ISM Manufacturing Index (May) – is expected to remain in expansionary territory and may surprise to the upside due to lengthening delivery times.

- Tuesday: Factory Orders (April) – look for a decline following weak headline durable goods report.

- Wednesday: ISM Services Index (May) – expected to show modest growth; employment and price indexes in focus.

- Thursday: Jobless Claims – overall claims remain low but continuing claims have been rising and are currently at multi-year highs.

- Friday: Nonfarm Payrolls (May) – we are projecting a 145,000-job rise in nonfarm payrolls; unemployment rate is expected to inch higher to 4.3%.

Market participants will also monitor revisions to productivity and labor costs, plus any policy commentary from Fed speakers. The Fed’s Beige Book will also be released on Wednesday and will be closely reviewed for any fallout from tariffs and changes in consumer behavior.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

May 23, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics

Trade, Tax Cuts & Trump’s Adventures

- The U.S. and China reached a limited trade pact focused on tariff rollbacks and increased access to tech products.

- Moody’s downgraded the U.S. credit rating to Aa1 from Aaa, citing structural fiscal risks and rising debt burdens.

- President Trump’s Middle East trip renewed the U.S.-Saudi strategic partnership, unlocking major IT and defense contracts and a flurry of deals with the UAE, Saudi Arabia, and Qatar.

- Russia’s war with Ukraine appears to be seeing some quiet progress toward a ceasefire, aided by Russia’s faltering economy and growing pressure from China.

- The CPI came in below expectations, while April retail sales were mixed. The tidal wave of tariff announcements slowed industrial production but the recent softening on tariffs has lifted global PMIs.

- Higher interest rates continued to undermine the housing sector. Weekly jobless claims remain mixed, while the early read on consumer sentiment came in weak amidst soaring inflation expectations.

- The tax package (Big Beautiful Bill) is shaping up to be modestly stimulative, while tariffs are expected to produce a drag on growth but modest uptick in government revenues.

Markets opened the week digesting a mix of economic data, trade diplomacy, and geopolitical news. Leading the headlines was a modest U.S.-China trade deal featuring targeted tariff rollbacks and eased restrictions on Chinese chipmakers, in exchange for expanded U.S. access to agriculture and industrial markets. Initial market optimism faded, however, amid lingering high tariffs and persistent uncertainty over summer supply chain disruptions.

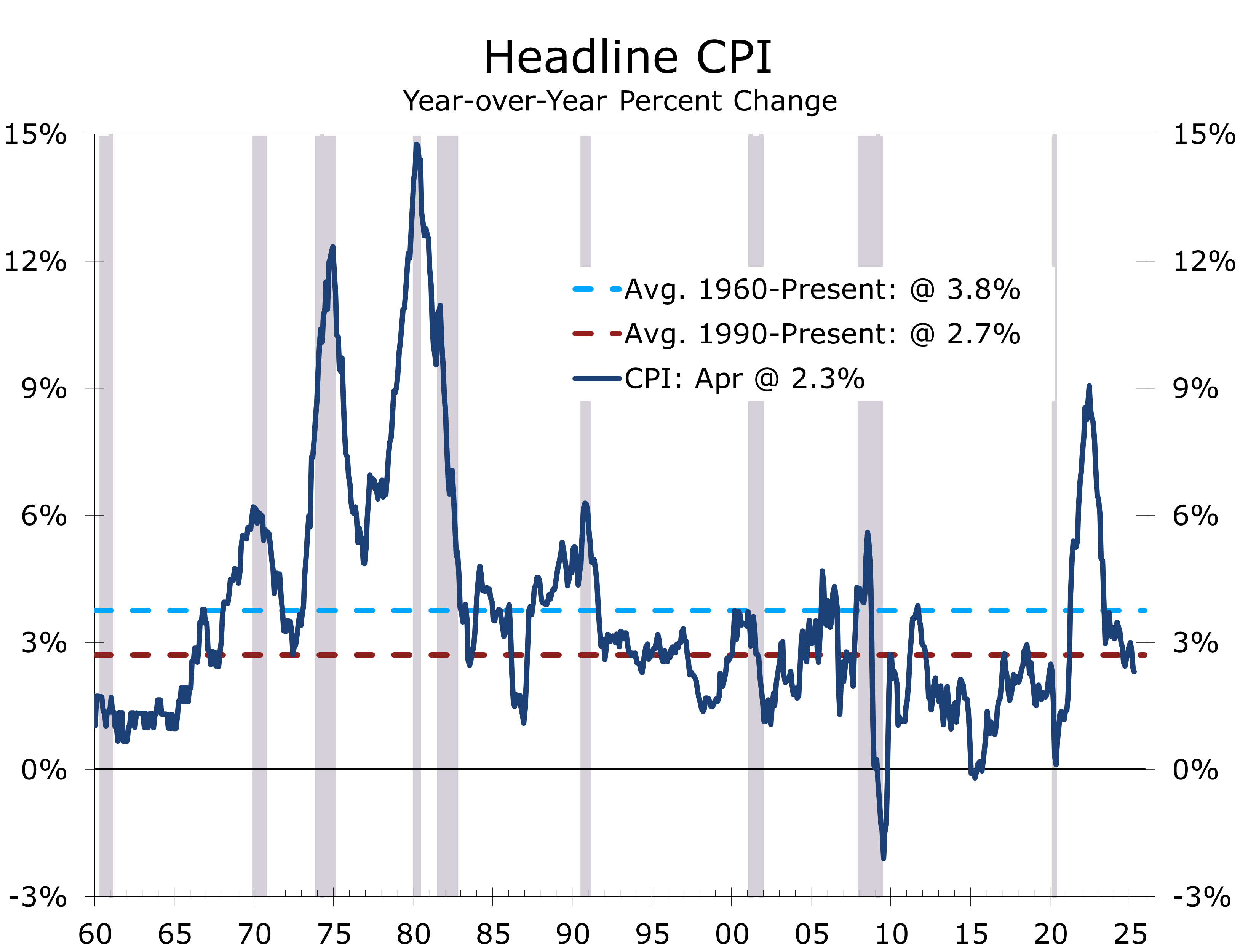

Markets digested a full week of economic data following the trade deal. The April CPI came in cooler than expected, with headline inflation up just 0.2%, bringing the year-over-year rate down to 2.3%. Core inflation held at 2.8%. Goods prices fell 0.2% year-to-year—mainly due to energy—while services stayed firm at 3.7%. Notably, core goods inflation turned positive at 0.1% y/y for the first time since early 2024, suggesting tariff-driven supply shocks may be building.

Tariffs have yet to boost measured inflation. The latest readings came in softer than expected.

Normally, softer CPI readings might nudge the Fed toward easing. However, with inflation expectations rising and supply-side frictions building, policymakers are unlikely to pivot soon.

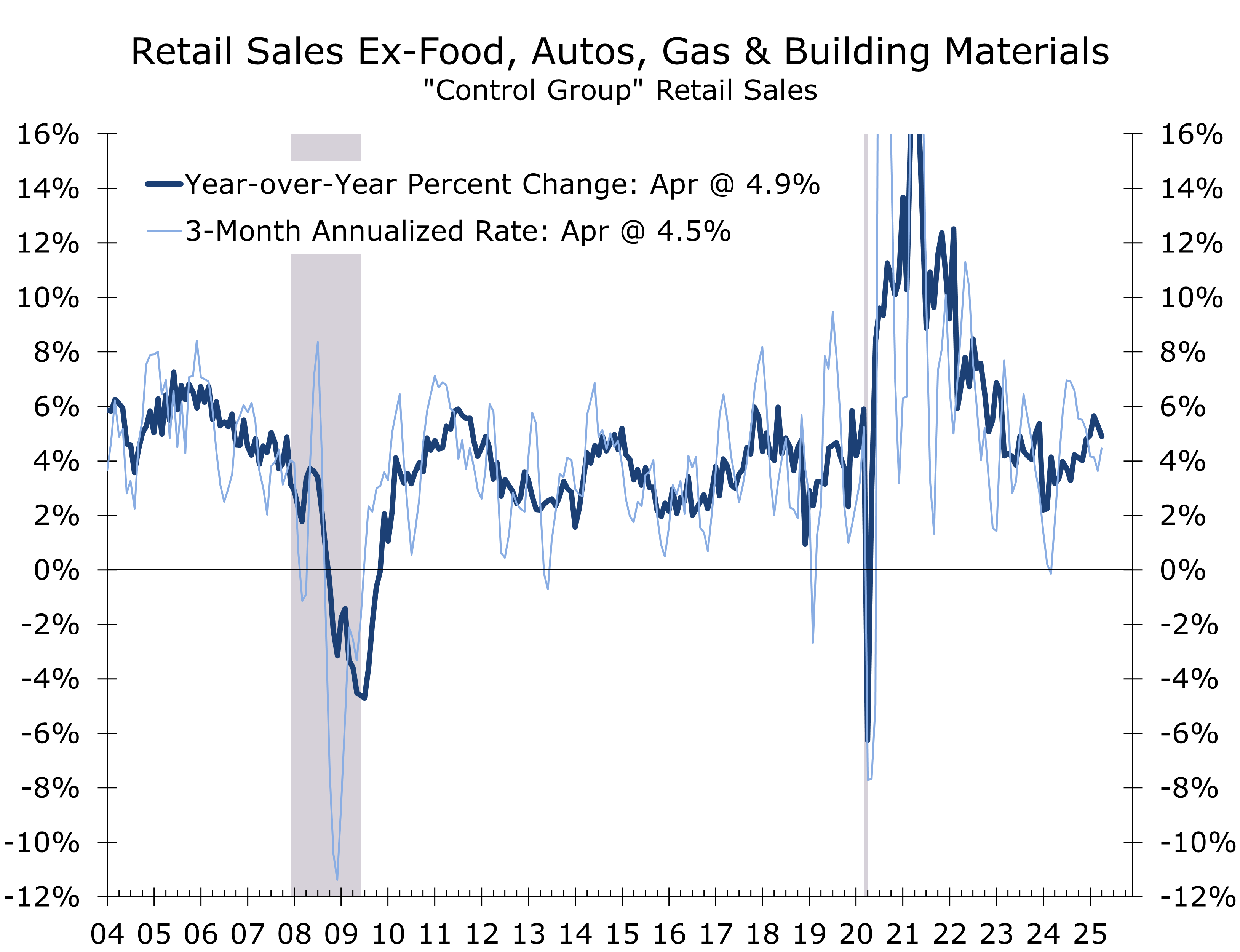

April retail sales pointed to deceleration, not collapse. Headline sales rose 0.1%, beating expectations but well off March’s revised 1.7% surge. Core sales also rose 0.1%, while the control group fell 0.2%, likely due to front-loaded spending in March—particularly autos—and a late Easter shift. Restaurant sales remained firm, countering weak consumer sentiment. On a three-month average basis, spending looks solid, and personal consumption is tracking stronger than expected, supporting our 2.4% upside Q2 GDP call.

Labor market resilience continues. Initial jobless claims edged down 2k to 227,000 for the week ending May 17, in line with expectations. Continuing claims rose 36,000 to 1.79 million—just above consensus—signaling that job seekers are having a harder time landing a new job. Meanwhile, the S&P Global U.S. Manufacturing PMI jumped 2.1 points to 52.3, the highest since 2022, with gains in output (50.7), new orders (53.3), and employment (49.6). Input and output prices surged to two-year highs, driven largely by tariff-related cost pressures. Business sentiment improved following the tariff rollback.

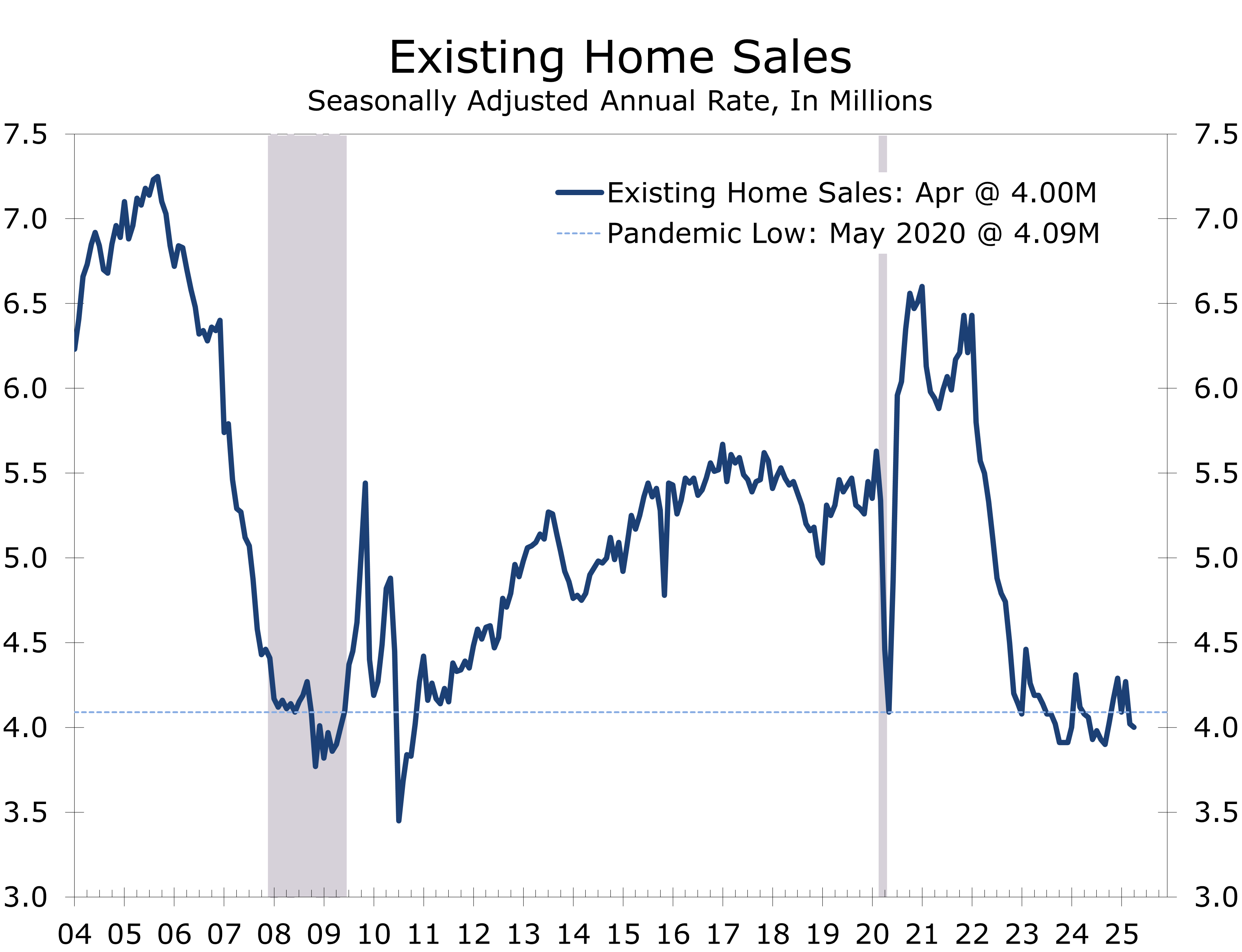

Existing home sales fell 0.5% in April to a 4-million-unit pace. Sales are down 2% year-to-year. Inventory rose 9% to 1.45 million units—the highest since September 2020—and up 21% year-to-year. The months rose to 4.4 months, the highest since May 2020.

While the housing market has needed more inventory, demand is clearly lacking. Homes sat on the market for an average of 29 days in April, up from 26 a year ago, suggesting slower turnover. Anecdotal evidence suggests prices cuts are becoming more common. The median price has slowed to just 1.8% year-to-year.

Earlier reports showed builder sentiment fell to a five-month low in May, and single-family starts declined 2.1% in April, pressured by high mortgage rates and construction costs. With the Fed intent on anchoring inflation expectations—especially after the University of Michigan’s May survey showed 1-year inflation expectations jumping to 7.3%—policy looks likely to stay tight even as growth momentum begins to wane.

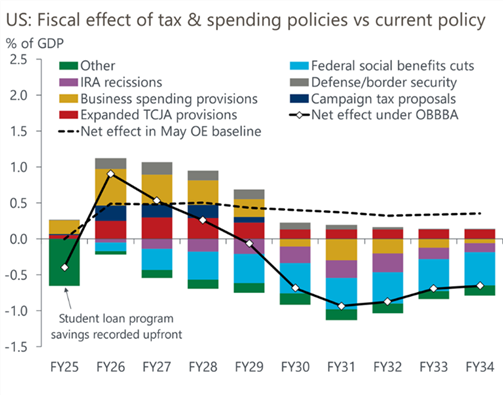

Moody’s downgraded the U.S. sovereign rating to Aa1 from Aaa, citing decades of fiscal drift. Deficits could hit 9% of GDP by 2035, with debt soaring to 134% from 98% in 2024. Rising mandatory spending and interest costs—set to consume nearly a third of federal revenues by 2035—have eroded the ability to service debt, pushing the interest burden above that of other Aaa peers. Though markets shrugged, the downgrade warns that America’s fiscal credibility is unraveling. Moody’s stable outlook rests on the U.S. economy’s scale, institutional strength, and the dollar’s reserve status—but these pillars no longer fully offset fiscal deterioration. Tough decisions loom ahead.

Tax Cuts vs. Tariffs: A Lopsided Battle

Republicans advanced a reconciliation package with slightly larger tax cuts than expected. Deductions for tips and overtime were expanded, along with enhancements to the 2017 tax law—totaling about 0.2% of GDP. SALT deductibility was also broadened. For corporations, full expensing for domestic factory construction was reinstated, but cuts to green subsidies and offsetting tax hikes left net corporate relief smaller than anticipated.

The fiscal impulse—+0.1pp of GDP in Q4 2025 and +0.3pp in Q4 2026—is no match for Trump’s new tariffs, which will subtract 0.8pp and 0.5pp from GDP over the same period.

A modestly stimulative budget bill passed the House but will likely be tightened in the Senate.

Trump’s Global Pivot: Silicon Diplomacy

President Trump’s successful Middle East tour strengthen alliances and struck a number of new deals. The U.S.-Saudi reset includes a 411k bpd oil output increase in June, defense deals, and over $18 billion in tech and military contracts—Microsoft, Oracle, Palantir, Lockheed, and Raytheon among the winners.

Qatar followed with $4.2 billion in LNG, 5G, and semiconductor JVs. A U.S.-Qatar sovereign tech fund is in the works, positioning Doha as the Gulf’s digital hub.

Progress continued on expanding the Abraham Accords, with Saudi Arabia signaling interest contingent on U.S. defense guarantees, civilian nuclear cooperation, and a more active U.S. role in Palestinian peace efforts. A breakthrough remains possible.

On tour, Trump cast the region’s realignment as a bulwark against Iranian aggression and China’s digital expansion, pitching a “NATO for Networks” concept—tying together cybersecurity, missile defense, and data sovereignty. The pitch speaks to 21st-century threats in a multipolar digital battlefield.

Back home, with the “Big Beautiful Bill” squeaking through the House, Senate Republicans are eyeing changes to mitigate its impact on businesses and find more immediate savings.

Russia-Ukraine: Ceasefire Odds Rise as Costs Mount

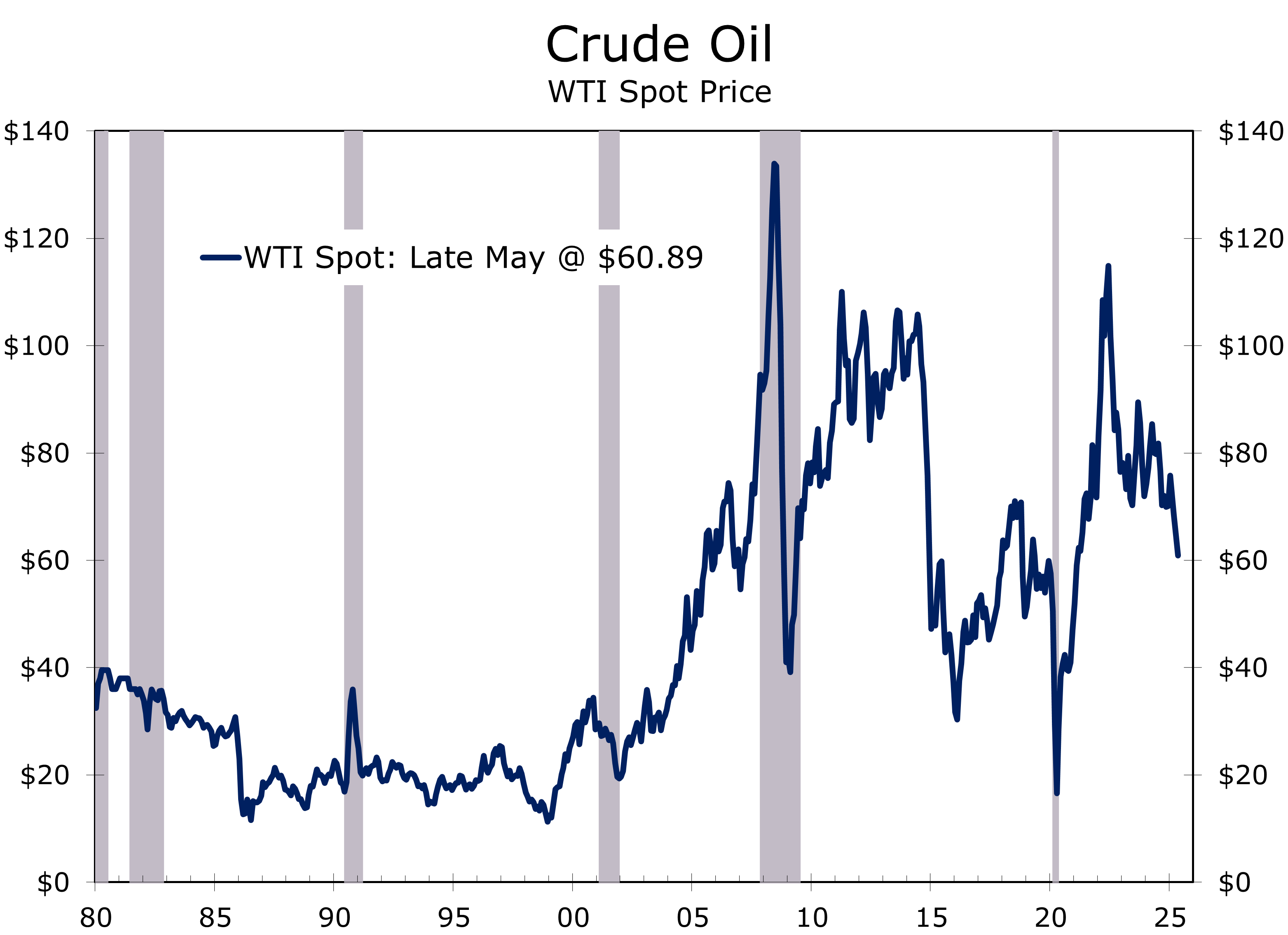

Russia’s war with Ukraine war has become a costly war of attrition. Russia’s economy is buckling—defense spending now outpaces oil and gas revenue, and Brent crude has slipped to $62/barrel. The National Wealth Fund has lost $67B since 2022, debt is nearing one-third of GDP, and interest rates are at 21%. Demographics are another threat: fertility is plunging, and the workforce is shrinking.

Despite widening deficits, Putin is betting on Western war fatigue. Ceasefire momentum may be building, but fresh sanctions could be required to bring Putin to the negotiating table and contain Kremlin ambitions.

China remains Russia’s economic lifeline but is playing hardball on energy and tech. For Moscow, a ceasefire could lock in territorial gains and stabilize the economy. For Trump, brokering one offers foreign policy clout, a potential market tailwind, and a way to lower NATO tensions.

The war has cost Russia $1.3 trillion, over 100,000 lives, and lasting economic damage. Quiet talks suggest Ukraine’s NATO bid is off the table, and neutrality is assumed. But some affiliation with Western Europe also seems inevitable. We had earlier pondered whether Ukraine could attain some sort of observer status within NATO, allowing for cross training with NATO members but no NATO bases on Ukrainian soil. That prospect seems more remote today. Even a formal peace remains distant, but a tactical ceasefire is increasingly likely.

Europe Pushes Back on Populism

Despite forecasts of a hard-right surge, Europe’s center held. Romania elected pro-European Nicușor Dan over nationalist George Simion. Portugal’s center-right outpaced the far right Chega party in parliamentary elections, which gained seats but not much clout. And Poland’s liberal candidate secured a run-off spot against his nationalist rival.

Europeans remain wary of populist instability. Trump’s low favorability and skepticism over U.S. reliability have reinforced centrism. Anti-immigrant rhetoric polls well across the continent, but hard nationalism still spooks mainstream voters.

Trade policy took a volatile turn: President Trump outlined a sweeping tariff overhaul targeting more than 150 countries earlier in the week, with formal notices expected soon. But markets were rattled Friday after he threatened a 25% tariff on imported iPhones unless Apple relocates production to the U.S. He also floated a 50% tariff on EU goods to break the logjam in trade talks. The White House moved quickly to calm markets, which remain cautiously positioned heading into the long weekend.

The 10-Year Treasury yield is ending the week just below its highs after a brief spike triggered by soft demand at Wednesday’s 20-Year bond auction—a less liquid, awkwardly placed maturity. In contrast, Thursday’s 10-Year TIPS auction was well received, helping stabilize yields.

Moody’s downgrade and the budget deal had only muted market impact, with investors positioned for worse. The more significant development may be structural: a surge in capital demand from emerging markets positioning as alternatives to China in global supply chains. Investor interest in EMs is now at its highest level since the early 1990s, and this shift could exert upward pressure on U.S. rates over time. We expect the 10-Year yield to trend higher and remain above its average for the past 35 years but well below its longer term average dating back to 1960, which was influenced by the runaway inflation of the late 1970s.

Looking Ahead

(Holiday-Shortened Week)

A full slate of data is due next week despite the Memorial Day holiday. Tuesday brings April Advance Durable Goods Orders and the May Consumer Confidence report. On Wednesday, the Fed will release minutes from the May FOMC meeting. Thursday follows with revised Q1 GDP, April Pending Home Sales, and weekly jobless claims. Friday rounds out the week with April Personal Income and Spending and the final University of Michigan Consumer Sentiment Index.

Key Variables to Watch:

- Core Capital Goods Orders: Watch for continued strength—these have remained resilient through trade headwinds.

- Sentiment Readings: Consumer Confidence and UMich sentiment should rebound from April’s drop, which reflected market turmoil following Trump’s “Liberation Day” tariff rhetoric.

- GDP Revision: Expect a modest upward revision in Q1 GDP, potentially to -0.1%.

- Consumer Spending: April Personal Consumption Expenditures could surprise to the upside. Unlike the Census Bureau’s retail sales, the BEA does not adjust for holiday calendar effects. We believe retail sales—particularly the control group—understated the underlying strength of consumer demand.

- Inflation Data: Core PCE deflator is likely to come in soft. Inflation expectations may ease slightly after their tariff-driven surge.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

May 23, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

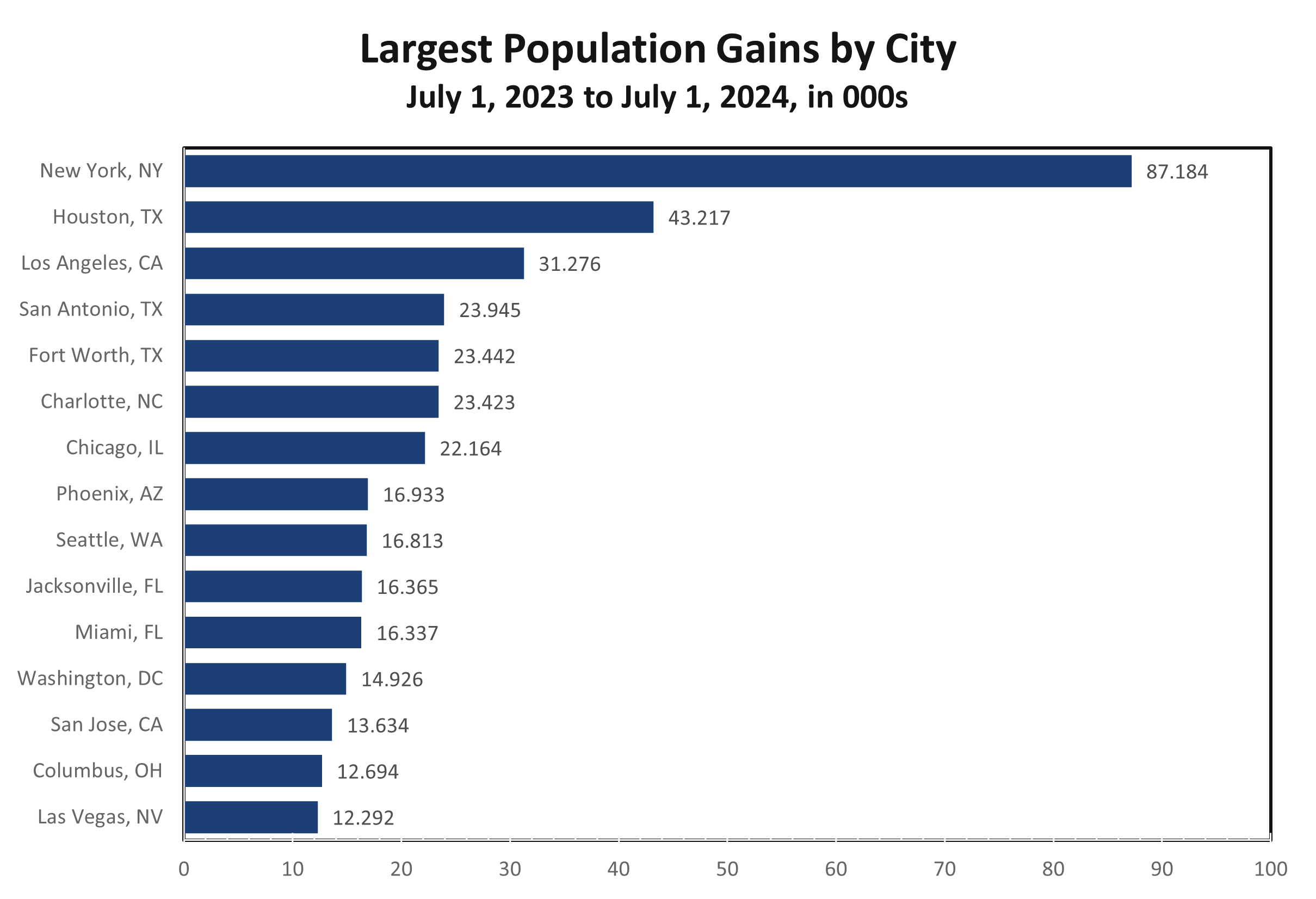

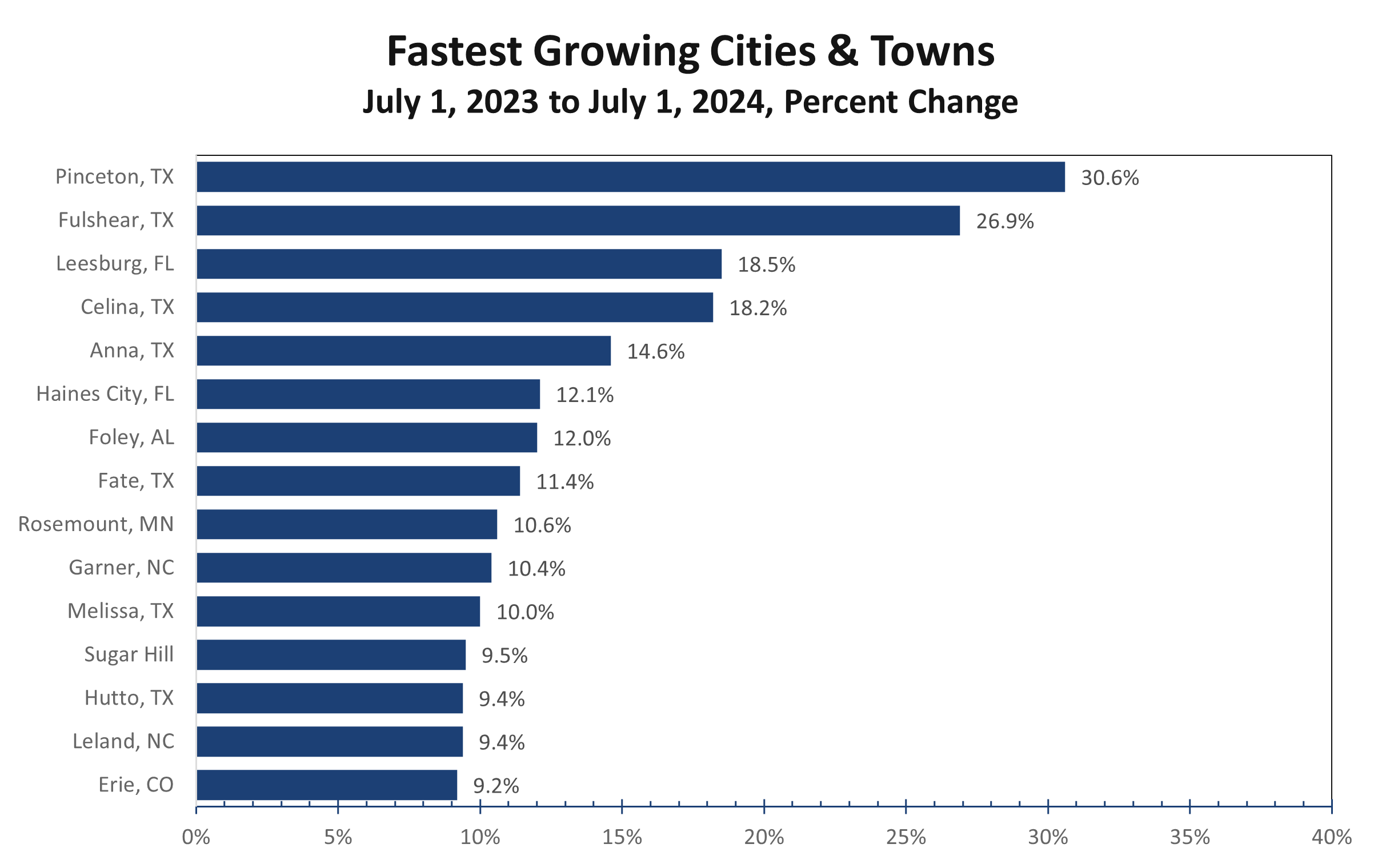

Sun Belt Momentum Accelerates Amid Nationwide Urban Area Turnaround

Return to Office Revives Urban Growth

- Large cities from New York to Los Angeles saw population growth in 2024, reversing multi-year declines amid a stronger return to the workplace and a surge in immigration from mid-2023 to mid-2024.

- The South and Mountain West continue to grow fastest, led by Princeton, TX (+30.6%) and major gains in Fort Worth, Jacksonville, and Charlotte.

- Like the inflationary late ’70s, the nation’s population is reorienting toward the Sun Belt—but this time, California is losing residents rather than gaining them.

- Office-adjacent sectors like restaurants and retail are rebounding, while business travel is steadily reviving in major markets, including NYC, LA, Houston, Atlanta, Miami, and Charlotte.

- The U.S. added 1.4 million new housing units (+1.0% YoY), but construction still lags population growth in key migration corridors.

- The urban rebound is increasingly broad-based and signals renewed opportunity in multifamily, infrastructure, and urban retail across both high-growth Sun Belt metros and stabilizing legacy cities.

Sun Belt Momentum Accelerates Amid Nationwide Urban Area Turnaround

The U.S. Census Bureau’s “Vintage 2024” estimates confirm the reversal: after years of decline or stagnation, American cities—large and small—are growing again. While metros like New York, Los Angeles, and Houston led in numeric population gains, Princeton, Texas secured the title as the fastest growing city, surging +30.6% in one year.

This rebound is being driven by three key trends: the return to the office, rising immigration, and the continued affordability migration—primarily toward the Sun Belt. Cities across all regions saw improved growth from 2023 levels, except for a handful of small Southern towns, which essentially held steady. There has been significant movement within the South, with residents pushing further out into suburban areas in search of more affordable housing. Economic development and retirees are also boosting growth, particularly around Savannah and the Carolinas.

The Return-to-the-Office is helping revive population growth in major cities.

Large urban centers are benefitting from a fuller return to office work. Cities like New York, Chicago, Washington D.C., and Los Angeles, once written off, are seeing a demographic comeback. Business travel is also picking up—particularly in major business hubs like NYC, LA, Miami, Houston, Charlotte, and Atlanta—reviving hospitality, events, and urban mobility.

Surging immigration has added fuel to the rebound, especially in traditional gateway cities. The influx of foreign-born residents helped stabilize the labor force, replenish school enrollment, and reenergize urban corridors. Meanwhile, office-adjacent sectors—retail, restaurants, dry cleaners, barbershops—are finally climbing out of the post-pandemic doldrums, adding jobs and pulling job seekers back into the city.

The migration wave into the Sun Belt echoes the late 1970s and early ’80s, when inflation and lifestyle preferences pulled households away from the Northeast and Midwest. The twist today? Back then, California was the haven for many fleeing the Rust Belt and Northeast. Now, it is the launching point for outbound migration. Moreover, parts of the Midwest are enjoying a rebound, as they are now relatively more affordable than major markets elsewhere.

Inflation is a major drive of migration trends, similar as it was in the late 1970s.

Texas metros—Dallas, Fort Worth, Austin, Houston—along with Carolinas’ standouts like Charlotte and Raleigh, and relatively affordable Florida major cities like Jacksonville, Lakeland and the outer reaches of Tampa are absorbing tens of thousands of new residents annually. These areas also now dominate lists of the best places to live, start a business, and raise a family.

Cities outside larger cities are also getting larger, reflecting an affordability migration within metro areas. Deltona, located between Daytona Beach and Orlando; and Sunrise and Plantation, both located South of Fort Lauderdale, all surpassed the 100,000 mark, underscoring the breadth of migration trends across metro tiers. Atlanta’s growth continues to stretch further up I-85, driving growth in Jackson County, which is also benefitting from growth spilling over from neighboring Gainesville and Athens. Texas continues to punch above its weight, with five counties among the top 10 for new housing units added.

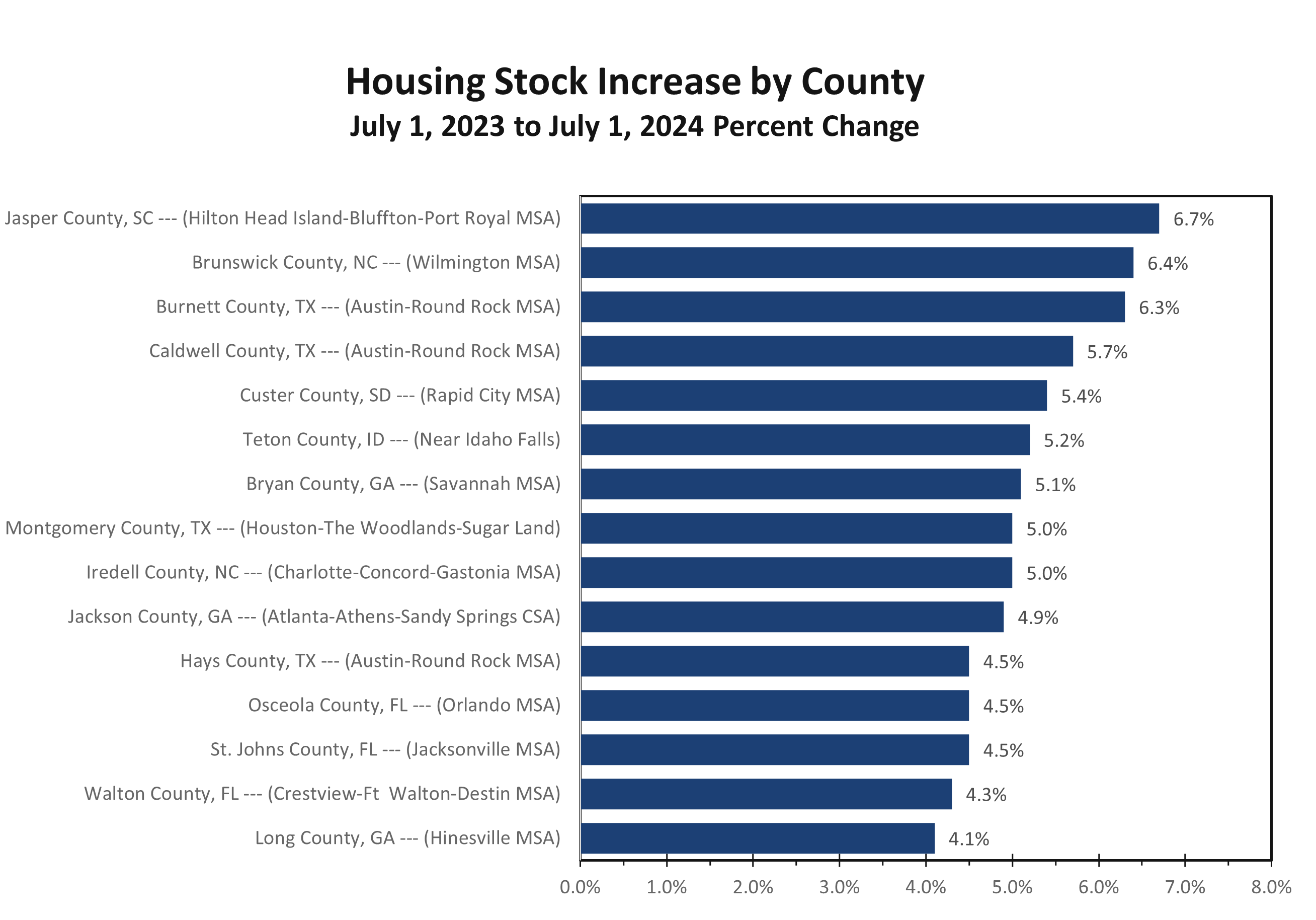

Overall, the U.S. added 1.4 million housing units between 2023 and 2024, a 1.0% increase. Idaho (+2.2%), Utah (+2.0%), and North Carolina (+1.9%) led the way. Jasper County, SC, located between Hilton Head Island, SC and Savannah, GA; topped the list of fastest-growing counties by housing stock (+8.4%). Still, supply remains behind the curve in the most in-demand metros, supporting continued rent growth and development. LA County, Maricopa County (AZ), home to Phoenix, and Harris County (TX), home to Houston, drove the largest numeric additions, but builders in these counties are still not fully catching up with underlying demand.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

May 16, 2025

Mark Vitner, Chief Economist

(704) 458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics

Relief Rally as Trade Tensions Ease

- U.S.–China Tariff Pause: A 90-day rollback sharply reduces U.S. tariffs from 145% to 30%, and China’s from 125% to 10%.

- Initial Market Response: Global equities surged, the dollar strengthened, oil prices rose, and gold fell as investors pivoted to risk assets.

- May FOMC Meeting: The Fed held rates steady at 4.25%–4.50%, citing inflation uncertainty and labor market risks. Core PCE came in at 2.6% Year-over-Year.

- Geopolitical Risks: India-Pakistan conflict erupted over Kashmir, triggering one of the largest aerial engagements since WWII before a U.S.-brokered ceasefire.

- Data Watch: CPI, PPI, retail sales, Fed speeches, and consumer sentiment reports all due this week, with Tuesday’s CPI being the key report.

- Market participants will closely scrutinize this week’s CPI report and inflation expectations in the preliminary Univ of Michigan Consumer Sentiment survey for any sign inflation expectations are becoming unanchored.

The U.S. and China have agreed to a significant de-escalation in their trade war by implementing a 90-day pause on heightened tariffs. This agreement, emerging from this past weekend’s Geneva talks, sharply reduces tariffs from extreme levels—with the U.S. cutting tariffs on Chinese goods from 145% to 30%, and China reducing U.S. tariffs from 125% to 10%.

President Trump proclaimed the agreement a total reset—though it likely reflects more of a shift in mindset than a change in principle. The news spurred a surge in global stock markets, sent the dollar broadly higher, boosted oil prices, and reversed some of the recent spike in gold prices as investors shifted to riskier assets. While the immediate market reaction is positive, the agreement marks only a temporary rollback and does not address long-standing trade issues. Still, the two sides appear committed to working toward a more comprehensive deal. Following the latest developments, we slightly lowered our recession probability for this year from 45% to 40%.

This U.S.-China trade deal signals a willingness by China to work to address U.S. grievances.

At its May 6–7 meeting, the Federal Reserve maintained their federal funds rate target at 4.25% to 4.50%, continuing the pause initiated in January after 100 basis points of cuts between September and December 2024. The Fed’s policy statement reflected increased caution, citing persistent inflation pressures and growing risks to the labor market.

Chair Jerome Powell emphasized a data-dependent approach, noting the need for more time to wait and see if the recent soft economic data indicates a meaningful slowdown or is merely noise amid rapidly changing tariff pronouncements. Our read is that it is a little bit of both. Growth is slowing, but the noise around the Liberation Day tariff announcements greatly amplified growing economic anxieties among businesses and consumers. The latest inflation data shows core PCE up 2.6% year over year in March, still above target but trending downward. However, tariffs and related disruptions to trade are expected to lift the core PCE to at least 3% this year.

Trade talks overshadowed a major conflict between India and Pakistan.

While the markets were fixated on the trade talks, India launched air strikes against Pakistan on May 7 in retaliation for a terrorist attack in Pahalgam, Kashmir, that killed 28 civilians. The conflict intensified into one of the largest aerial engagements since World War II, involving over 100 fighter jets and missile exchanges.

A U.S.-brokered ceasefire was reached on May 10, but the situation remains fragile. The conflict underscores the risk posed by Pakistan’s harboring of terrorist groups and their occasional use of those groups to further geopolitical aims—comparable to Iran’s use of proxies like Hamas, Hezbollah and the Houthis. For markets, the de-escalation reduces immediate risk. The U.S. role in mediating the crisis also bolstered confidence in U.S. leadership, strengthening the dollar and pulling gold prices lower.

The temporary ceasefire in the U.S.–China trade conflict has delivered short-term relief to financial markets and granted the Federal Reserve additional breathing room. With no immediate need to adjust policy, the Fed can now take a “wait and see” approach as it assesses incoming economic data and evolving trade dynamics. That patience will be tested this week with a heavy slate of reports and Fed commentary.

Tuesday’s Consumer Price Index (CPI) report is expected to show a 0.3% increase for both headline and core measures. While inflationary pressures remain broad-based, a cooling in shelter inflation could help offset rising costs in auto and home insurance, as well as tariff-sensitive products. Used car prices are likely to fall this month, although recent increases in the Manheim Index suggest upward pressure may reemerge this spring or early summer. Year-over-year, core CPI is expected to hold at 2.8%, but this figure may creep higher in the months ahead.

Markets will also turn their attention to Wednesday’s remarks from Fed Governors Waller, Jefferson, and Daly—three voices with differing policy leanings. Their comments will be closely watched for signs of shifting tone or new forward guidance in light of the recent trade developments. Each brings a unique lens on how inflation, employment, and external shocks like tariffs should influence the Fed’s reaction function.

Thursday delivers a data deluge, headlined by the Producer Price Index (PPI), retail sales, initial jobless claims, and regional manufacturing surveys from the New York and Philadelphia Feds. The regional Fed surveys cover the period from late April through early May and might provide a better assessment of conditions, which worsened at the start of April, following the Liberation Day tariff announcements.

Chair Powell is also scheduled to speak. While Powell has not signaled any immediate changes to policy, he has warned that tariffs may eventually force the Fed into a difficult trade-off: prioritizing inflation fighting or job market support. His remarks will be parsed for any signs that this balance is beginning to shift.

Retail sales should be read in context. The late timing of Easter likely inflated March figures and could suppress April’s readings. The two months data should be averaged together to get a clearer view of the consumer’s trajectory. These figures are seasonally and calendar-adjusted, but distortions from holiday timing remain a persistent challenge.

Friday brings reports on housing starts, import prices, and consumer sentiment. Housing may show modest improvement from the disappointing March data. Inflation expectations will remain a key focus in the Consumer Sentiment data. If consumers believe prices will rise and adjust their behavior, expectations might become self-fulfilling. On the whole, sentiment is expected to bounce after a recent run of declines.

In short, while the tariff pause provides the Fed with a little more time to assess how much of the weakening in the soft data reflects actual changes in behavior. Our read is that consumers are still spending freely, and we see recession risk subsiding. Global leaders and the financial markets are also becoming more comfortable with the Trump Administration, which may temper some of the recent market volatility.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

May 12, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics

Relief Rally as Trade Tensions Ease

- U.S.–China Tariff Pause: A 90-day rollback sharply reduces U.S. tariffs from 145% to 30%, and China’s from 125% to 10%.

- Initial Market Response: Global equities surged, the dollar strengthened, oil prices rose, and gold fell as investors pivoted to risk assets.

- May FOMC Meeting: The Fed held rates steady at 4.25%–4.50%, citing inflation uncertainty and labor market risks. Core PCE came in at 2.6% Year-over-Year.

- Geopolitical Risks: India-Pakistan conflict erupted over Kashmir, triggering one of the largest aerial engagements since WWII before a U.S.-brokered ceasefire.

- Data Watch: CPI, PPI, retail sales, Fed speeches, and consumer sentiment reports all due this week, with Tuesday’s CPI being the key report.

- Market participants will closely scrutinize this week’s CPI report and inflation expectations in the preliminary Univ of Michigan Consumer Sentiment survey for any sign inflation expectations are becoming unanchored.

The U.S. and China have agreed to a significant de-escalation in their trade war by implementing a 90-day pause on heightened tariffs. This agreement, emerging from this past weekend’s Geneva talks, sharply reduces tariffs from extreme levels—with the U.S. cutting tariffs on Chinese goods from 145% to 30%, and China reducing U.S. tariffs from 125% to 10%.

President Trump proclaimed the agreement a total reset—though it likely reflects more of a shift in mindset than a change in principle. The news spurred a surge in global stock markets, sent the dollar broadly higher, boosted oil prices, and reversed some of the recent spike in gold prices as investors shifted to riskier assets. While the immediate market reaction is positive, the agreement marks only a temporary rollback and does not address long-standing trade issues. Still, the two sides appear committed to working toward a more comprehensive deal. Following the latest developments, we slightly lowered our recession probability for this year from 45% to 40%.

This U.S.-China trade deal signals a willingness by China to work to address U.S. grievances.

At its May 6–7 meeting, the Federal Reserve maintained their federal funds rate target at 4.25% to 4.50%, continuing the pause initiated in January after 100 basis points of cuts between September and December 2024. The Fed’s policy statement reflected increased caution, citing persistent inflation pressures and growing risks to the labor market.

Chair Jerome Powell emphasized a data-dependent approach, noting the need for more time to wait and see if the recent soft economic data indicates a meaningful slowdown or is merely noise amid rapidly changing tariff pronouncements. The latest inflation data shows core PCE up 2.6% year over year in March, still above target but trending downward. However, tariffs and related disruptions to trade are expected to lift the core PCE to at least 3% this year.

Trade talks overshadowed a major conflict between India and Pakistan.

While the markets were fixated on the trade talks, India launched air strikes against Pakistan on May 7 in retaliation for a terrorist attack in Pahalgam, Kashmir, that killed 28 civilians. The conflict intensified into one of the largest aerial engagements since World War II, involving over 100 fighter jets and missile exchanges.

A U.S.-brokered ceasefire was reached on May 10, but the situation remains fragile. The conflict underscores the risk posed by Pakistan’s harboring of terrorist groups and their occasional use of those groups to further geopolitical aims—comparable to Iran’s use of proxies like Hamas, Hezbollah and the Houthis. For markets, the de-escalation reduces immediate risk. The U.S. role in mediating the crisis also bolstered confidence in U.S. leadership, strengthening the dollar and pulling gold prices lower.

.

The temporary ceasefire in the U.S.–China trade conflict has delivered short-term relief to financial markets and granted the Federal Reserve additional breathing room. With no immediate need to adjust policy, the Fed can now take a “wait and see” approach as it assesses incoming economic data and evolving trade dynamics. That patience will be tested this week with a heavy slate of reports and Fed commentary.

Tuesday’s Consumer Price Index (CPI) report is expected to show a 0.3% increase for both headline and core measures. While inflationary pressures remain broad-based, a cooling in shelter inflation could help offset rising costs in auto and home insurance, as well as tariff-sensitive products. Used car prices are likely to fall this month, although recent increases in the Manheim Index suggest upward pressure may reemerge this spring or early summer. Year-over-year, core CPI is expected to hold at 2.8%, but this figure may creep higher in the months ahead.

Markets will also turn their attention to Wednesday’s remarks from Fed Governors Waller, Jefferson, and Daly—three voices with differing policy leanings. Their comments will be closely watched for signs of shifting tone or new forward guidance in light of the recent trade developments. Each brings a unique lens on how inflation, employment, and external shocks like tariffs should influence the Fed’s reaction function.

Thursday delivers a data deluge, headlined by the Producer Price Index (PPI), retail sales, initial jobless claims, and regional manufacturing surveys from the New York and Philadelphia Feds. The regional Fed surveys cover the period from late April through early May and might provide a better assessment of conditions, which worsened at the start of April, following the Liberation Day tariff announcements.

Chair Powell is also scheduled to speak. While Powell has not signaled any immediate changes to policy, he has warned that tariffs may eventually force the Fed into a difficult trade-off: prioritizing inflation fighting or job market support. His remarks will be parsed for any signs that this balance is beginning to shift.

Retail sales should be read in context. The late timing of Easter likely inflated March figures and could suppress April’s readings. The two months data should be averaged together to get a clearer view of the consumer’s trajectory. These figures are seasonally and calendar-adjusted, but distortions from holiday timing remain a persistent challenge.

Friday brings reports on housing starts, import prices, and consumer sentiment. Housing may show modest improvement from the disappointing March data. Inflation expectations will remain a key focus in the Consumer Sentiment data. If consumers believe prices will rise and adjust their behavior, expectations might become self-fulfilling. On the whole, sentiment is expected to bounce after a recent run of declines.

In short, while the tariff pause provides the Fed with a little more time to assess how much of the weakening in the soft data reflects actual changes in behavior. Our read is that consumers are still spending freely, and we see recession risk subsiding. Global leaders and the financial markets are also becoming more comfortable with the Trump Administration, which may temper some of the recent market volatility.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

May 12, 2025

Mark Vitner, Chief Economist

Piedmont Crescent Capital

(704) 458-4000

mark.vitner@piedmontcrescentcapital.com

The Real Realignment: Why Switzerland, the Red Sea, and Markets Are Suddenly Linked

Are Quiet Talks a Sign of Real Progress?

- U.S. and Chinese officials convened in Geneva for intensive trade negotiations, marking the first in-person dialogue since the imposition of steep tariffs by both nations.

- The U.S. has implemented tariffs up to 145% on Chinese goods, with China retaliating at 125%, significantly impacting bilateral trade valued at $600 billion annually.

- Despite high tariffs, both nations recognize mutual dependencies, particularly in technology and manufacturing sectors.

- The U.S. is leveraging recent successful military actions in the Red Sea to underscore its role in securing global trade routes, indirectly pressuring China to engage constructively in trade discussions.

- Potential easing of trade tensions could benefit sectors like semiconductors, shipping, and multinational corporations with significant China exposure.

- The Geneva talks suggest a shift from confrontation to cautious cooperation, aiming to stabilize global economic relations.

Geneva Talks: A Potential Turning Point

U.S. Treasury Secretary Scott Bessent and Chinese Vice Premier He Lifeng engaged in over eight hours of trade discussions in Geneva on Saturday and are negotiating again on September 11. President Trump described the meeting as a “total reset,” indicating a possible thaw in relations. While no concrete agreements were announced, the commitment to continue negotiations signals a mutual interest in de-escalating tensions.

The current tariff regime has led to a near standstill in U.S.–China trade. The Trump administration has hinted at reducing tariffs to 80% contingent upon China’s commitments to fair trade practices and curbing fentanyl trafficking. Even at 80%, the tariff remains formidable, but President Trump’s negotiation tactics often involve pushing boundaries well beyond previous norms to secure more favorable outcomes.

Trump’s negotiating strategy often involves pushing boundaries well beyond prior norms.

Recent U.S. military actions targeting Houthi positions in the Red Sea region are not merely regional security measures but also strategic signals. By ensuring the security of vital maritime routes like the Strait of Hormuz and Bab el-Mandeb, the U.S. reinforces its role as a global trade guarantor. China, with its ties to Tehran and reliance on these shipping lanes, is indirectly prompted to support de-escalation efforts to maintain trade stability. In short, the U.S. is setting the chessboard—offering diplomacy on neutral ground, backed by hard power where it counts.

The ongoing U.S.–China trade negotiations are under close scrutiny by industries dependent on cross-border commerce. Key sectors such as semiconductors, shipping, and multinational corporations with significant exposure to China are particularly sensitive to developments in these talks.

Structured cooperation between the two nations, even if occasionally strained, can mitigate tail risks associated with global supply chains. Notably, any advancements in technological collaboration or trade stabilization are likely to precede formal announcements. One area to monitor is the potential easing of restrictions on rare earth elements, which are critical to various high-tech industries

Reducing trade tension is an important first step toward broader trade reforms.

The trade war’s impact extends beyond international relations, significantly affecting the U.S. economy. Small businesses, in particular, are struggling under the weight of increased tariffs, leading to layoffs and reduced operations. The manufacturing sector faces supply chain disruptions, while consumers encounter higher prices for goods. A resolution in the trade talks could alleviate these pressures, potentially stabilizing markets and fostering economic growth.

Budget Deal Prospects

President Trump’s ability to reach a budget deal is intertwined with the outcomes of these trade negotiations. A successful agreement with China could bolster economic confidence, providing the administration with leverage in budget discussions. Conversely, prolonged trade tensions may exacerbate fiscal challenges, complicating efforts to achieve a balanced budget.

Global Geopolitical Tensions

The Geneva talks occur against a backdrop of escalating global geopolitical tensions:

- India-Pakistan: A fragile ceasefire appears to be holding after recent hostilities over Kashmir, with the U.S. offering to increase trade with both nations to encourage stability.

- Iran: U.S. military actions targeting Houthi positions in the Red Sea region serve as strategic signals to Iran and its allies, emphasizing the U.S.’s role in securing vital maritime routes.

- South China Sea: China’s assertive activities in the region continue to raise concerns, with the U.S. reaffirming its commitment to freedom of navigation and regional security.

The Geneva trade talks represent a critical opportunity to reset U.S.–China relations and address broader economic and geopolitical challenges. While significant obstacles remain, continued dialogue and a commitment to cooperation could pave the way for a more stable and prosperous global economy. Stakeholders across sectors should closely monitor these developments, as their outcomes will shape the economic and political landscape in the months ahead. Closer to home, the U.S. economy has moved back from the edge of recession in recent days and successful trade talks will reinforce that shift.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

May 11, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

May FOMC Meeting Highlights: The Fed Flags Stagflation Risks Amid Tariff Uncertainty

Uncertainty Keeps Fed in Wait-and-See Mode

- The Fed held its federal funds rate target steady at 4.25%-4.5%, maintaining the pause that began in January following 100 bps of cuts from September to December 2024.

- The Fed notes that economic growth remains solid despite volatility in net exports, which pulled down first quarter real GDP growth.

- The policy statement also noted that uncertainty about the economic outlook had increased further since the last meeting.

- The Fed also noted that the risks of higher unemployment and higher inflation had have risen, which has amplified talk of stagflation.

- Powell noted that it is too early to know how tariff policy will ultimately settle out and what that would mean for inflation and labor market conditions. With both in a relatively good place, now is not a bad time to wait and see where trade policy evolves.

- We continue to believe the Fed is underestimating labor market risks and anticipate weaker job numbers in the coming months, which may prompt the Fed to begin to cut rates as early as July.

The Federal Reserve left its federal funds rate target unchanged at 4.25% to 4.50% at its May 6–7 meeting, extending a pause that began in January following 100 basis points of cuts between September and December 2024. The decision was widely anticipated, but the accompanying policy statement reflected a more cautious tone, with the Fed highlighting increased uncertainty about – rather than around previously – the economic outlook, persistent inflation pressures, and growing risks to the labor market. The slight switch implies an acknowledgement that the risk of recession have increased.

Chair Jerome Powell reiterated the Fed’s data-dependent stance, emphasizing that more time is needed to assess whether recent soft data foreshadow a meaningful slowdown or simply reflect noise. Powell also underscored the lack of clarity on tariff policy, noting it is too early to determine where trade measures will ultimately land—and how they will impact inflation and employment

Fed Chair Jerome Powell feels that monetary policy is in a pretty good place to wait and see.

The FOMC noted the economy continues to expand at a solid pace, supported by resilient consumer demand and a labor market that remains historically tight. Private final domestic demand grew at a 3% annualized rate in Q1. However, volatility in net exports pulled first-quarter GDP growth down at a 0.3% pace.

The most recent inflation data show prices pressures have moderated, with core PCE up 2.6% year-over-year in March—still above target but moving in the right direction. The impact of tariffs, however, will take time to work its way into the data. The rise in consumer expectations for inflation could become self-fulfilling if consumers rush to purchase goods ahead of tariffs or shortages. Used car prices have already risen sharply.

Surging inflation expectations may feed into actual inflation, becoming self-fulfilling.

More time is needed to fully assess risks. While hiring remains solid overall, surveys suggest momentum is weakening. Job openings have declined, and anecdotal reports indicate job seekers are having a harder time finding work. The share of consumers expecting hiring to slow has also jumped. Powell acknowledged that labor market conditions remain healthy but emphasized the need to monitor for further softening.

The May meeting did not include updated projections, but the March Summary of Economic Projections downgraded 2025 GDP growth to 1.7% and raised core inflation expectations to 2.8%, reviving concerns about stagflation. The May statement noted that risks of both higher inflation and rising unemployment have increased, suggesting that internal growth forecasts have likely been revised down further

Powell emphasized that holding rates steady gives the Fed time to assess the inflation and employment effects of shifting trade policy. The Fed also continues its balance sheet runoff, reinforcing its broader commitment to normalization.

Powell signaled no urgency to move policy in either direction, citing a balanced economic backdrop. However, he acknowledged that tariff-driven inflation could be persistent and hard to isolate. While some measures of inflation expectations have ticked up, market-based gauges remain stable. The 5-year, 5-year forward inflation expectation rate—derived from inflation-indexed Treasuries—continues to reflect well-anchored long-term inflation expectations.

We expect quarter points cuts in both July and September, based on a weaker labor market than the headline data suggests. We estimate true job growth is closer to 100K per month—about one-third slower than reported—just enough to keep unemployment flat. We expect the jobless rate to rise another 50 basis points by year-end, as hiring slows and employers grow more cautious. The economy is approaching the edge of recession, with a roughly 45% probability and the Fed will move more aggressively if conditions worsen.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

May 7, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics

Stagflation Fears Persist Despite Resilient Data

- U.S. labor market continued to show resilience in April, with employers adding 177,000 jobs. Soft undercurrents and downward revisions, however, continue to reinforce downside risks

- Q1 GDP fell at a -0.3% annualized pace, but distortions from frontloaded imports and inventories cloud the picture

- Eurozone inflation was firmer than expected but not enough to derail the ECB’s dovish path

- Oil remains under pressure as demand forecasts soften further, and the Saudis boost production while the rest of OPEC+ remains on the sidelines

- Romania swings right, Australia stays center-left in weekend elections and Canada moves slightly further to the left

Last week’s economic developments offered a clear reminder that the apparent resilience in the headlines likely masks fragility beneath the surface. April’s jobs report eased fears of an imminent downturn, with nonfarm payrolls rising by 177,000 and the unemployment rate holding at 4.2%. Downward revisions to prior months reduced the three-month average payroll gain to just 155,000, suggesting the labor market’s forward momentum is weakening.

Wage growth remains solid but is moderating, with average hourly earnings edging up 0.17% in April and up 3.8% year-over-year. The Employment Cost Index slowed to 3.6% in Q1, a trend consistent with the Fed’s inflation goal but one that suggests higher prices may more sharply erode real incomes and abruptly curb spending later this year.