A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Welcome Back to the Seventies — Markets, Metals, and the Illusion of Peace

Highlights of the Week

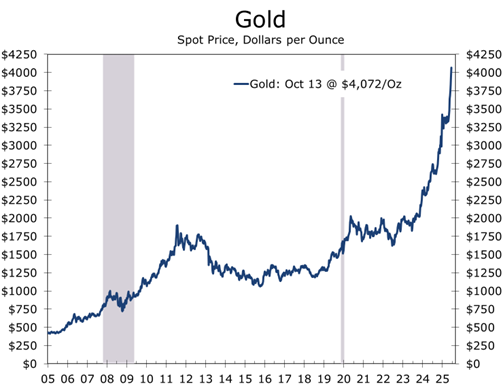

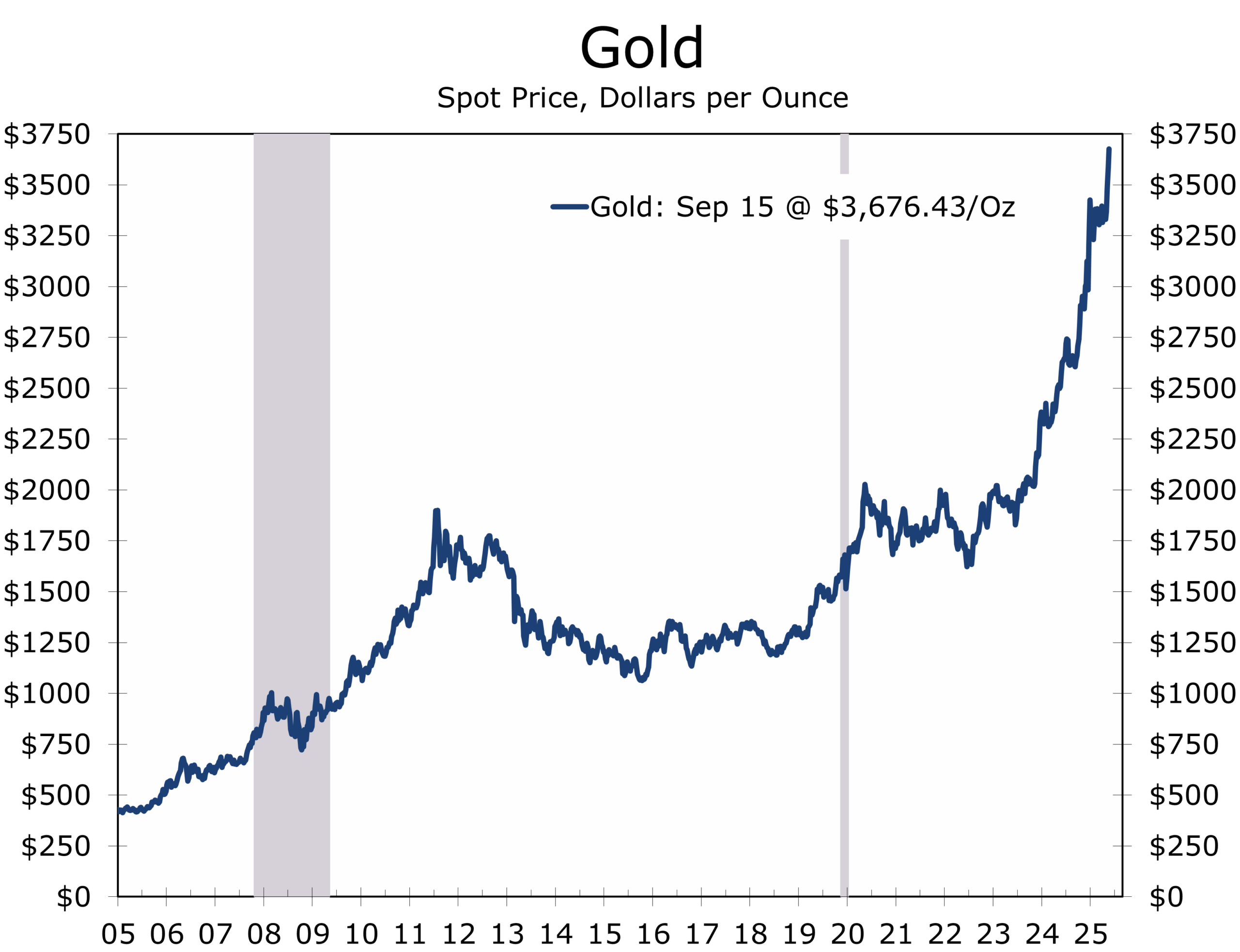

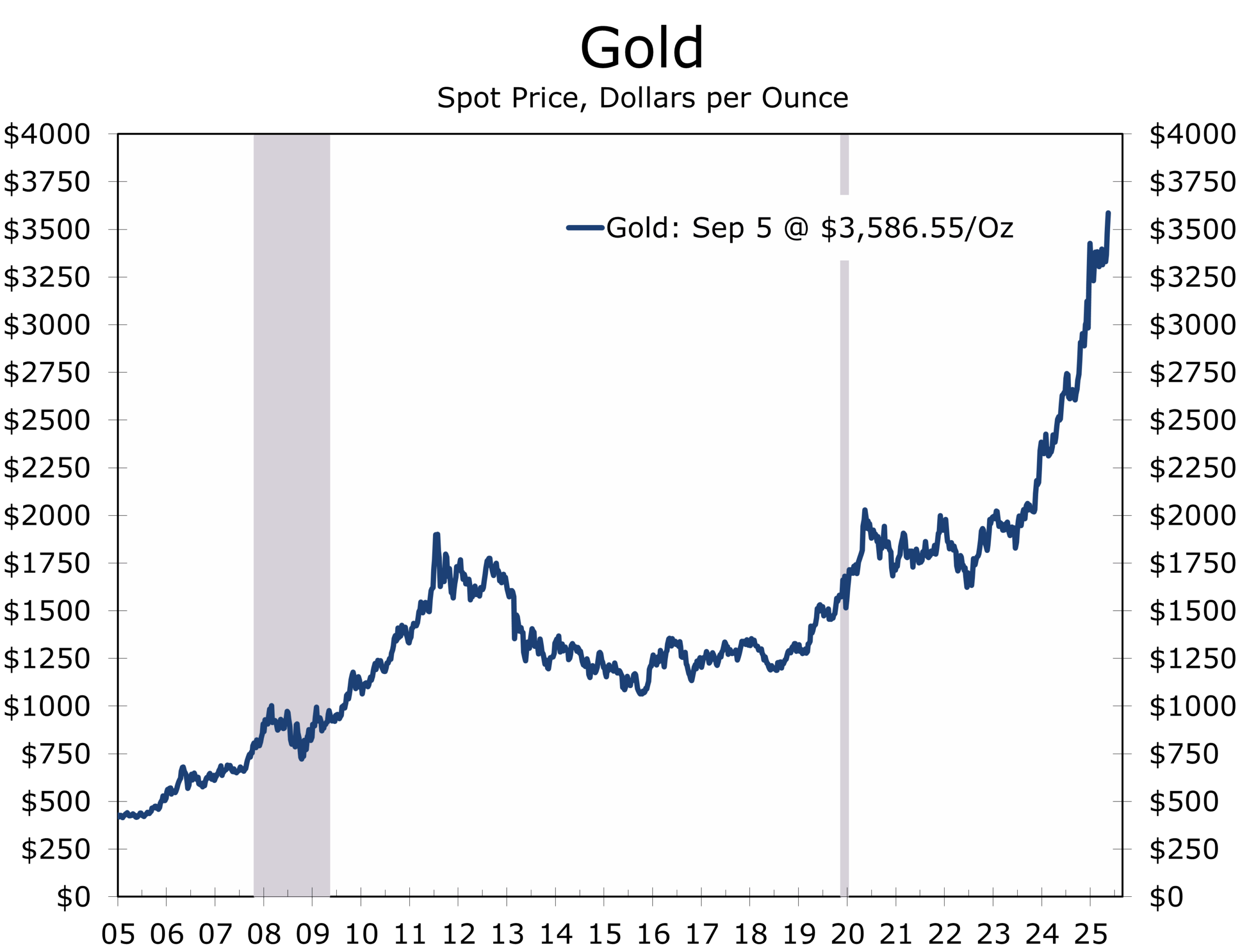

- Gold’s rally evokes a 1970s déjà vu — a mix of inflation anxiety, policy division, and global unease.

- Markets closed the week defensively as trade tensions resurfaced and data visibility dimmed under the government shutdown.

- The Nobel Peace Prize went to Venezuela’s María Corina Machado, sparking celebration abroad and political theater at home.

- A ceasefire took effect in Gaza, expected to return all living hostages and the remains of those who died in captivity — but peace remains elusive.

- Tariff and currency volatility reemerged as global risk drivers, with China’s export curbs and Washington’s 100% tariff threat triggering safe-haven flows into gold and Treasuries.

- Bond yields compressed and equity volatility climbed, as investors priced in slower growth, policy uncertainty, and a potential October rate cut.

- Investors appear to be buying insurance against uncertainties: both known and unknown. The Gaza ceasefire is a good first step at bringing some certainty back into play.

Headwinds and Handlebars: Some Vacation Reflections – Somewhere along Italy’s Adriatic coast this past week, I found myself pedaling into a headwind strong enough to feel personal. The road hugged the sea, sunlight glinting off an endless stretch of whitecaps as we made our way back from Santa Maria di Leuca — the southernmost point of the Salento Peninsula, or more simply, the heel of Italy’s boot. Even on the downhill stretches, the wind was so fierce you had to keep pedaling just to make headway. It struck me that markets are doing much the same.

Confidence has become the currency of this cycle — and gold is its barometer.

The resistance traditional assets face — inflation anxiety, political distrust, and weakening confidence in global institutions — are headwinds for growth but tailwinds for gold, crypto, and other safe havens. Progress now depends on the sectors still pedaling hardest — AI, data centers, and infrastructure — whose steady effort keeps the economy moving even when gravity should be taking over.

A few days later, our ride wound inland through Puglia’s ancient olive groves, where gnarled trees — some planted before the discovery of the New World, and capitalism itself — still yield oil as golden as the coins now coveted by investors. Those trees have endured conquests, plagues, and wars, their deep roots and slow reward standing in quiet defiance of today’s jittery markets — driven by the next big thing but weighed down by the next big worry.

Each turn of the pedals brought a reminder of equilibrium: effort met by resistance, progress tempered by patience. Investors are doing much the same — stretching for yield, recycling old assumptions to reconcile a new set of risks, and trying to shape something smooth from systems that refuse to remain still.

.

It is always hard to find time for a long vacation, particularly one that requires careful planning. When we departed, the timing seemed perfect. The weather forecast was ideal, and the U.S. government shutdown meant most data releases would be suspended for the bulk of our trip. The world’s attention was focused on the proposed and now agreed upon ceasefire in the Israel–Gaza conflict. Yet even from afar, it was clear that markets were wrestling with the same question I faced on that windy coastal road — how to keep balance when the terrain keeps changing.

The Week in Markets: A 1970s Show Reboot

Gold stole the show last week, climbing to record highs as investors dusted off a script last performed in the 1970s — when inflation, geopolitics, and trust all seemed to unravel at once. Back then, Americans waited in gas lines by day and watched prices spiral by night as the global financial order wobbled in real time. After Nixon severed the last link to the Gold Standard, gold and silver became the decade’s twin obsessions — safe havens for some, speculative addictions for others.

.

Today’s version stars an overworked Fed, underinformed markets (thanks to the prolonged shutdown), and a global audience binge-watching for clues — wondering whether this time, the ending is different. But the cast of commodities has changed: where oil once defined the economic anxieties of the 1970s, rare earths and high-end semiconductors now occupy center stage, as China’s expanded export controls threaten to weaponize supply chains and extend the trade war far beyond tariffs.

Gold’s latest rally has little to do with inflation — and everything to do with confidence, or the lack thereof. Confidence has become the currency of this cycle. It anchors expectations when data go dark and defines market psychology when the instruments go blank.

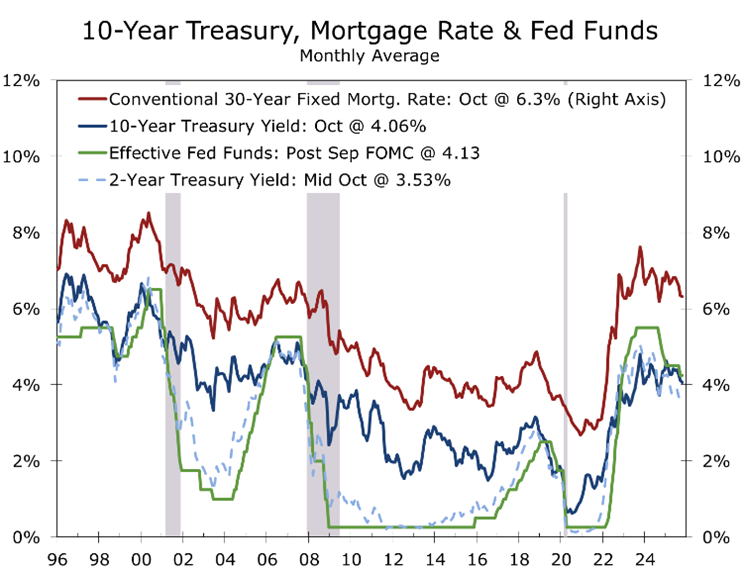

Bond yields retreated, particularly in the 2-to-10-year range, as traders extended bets on an October rate cut, now priced around 65%. Treasuries caught a late-week flight-to-safety bid after President Trump threatened a “massive increase” in China tariffs is response to Beijing’s unusually harsh new restrictions on rare earth exports— a reminder that in today’s economy, minerals and microchips have replaced oil as the leverage points of global power.

Israel Under Pressure—and Shifting Global Currents

With no official jobs or inflation data released, markets flew on instruments guided by private signals. Reports from ADP and Challenger released earlier this month show the labor market continuing to lose momentum. High-frequency data suggest this trend continued into mid-October, perhaps amplified slightly by federal payroll cuts. State filings and shutdown-related disruptions point to jobless claims near 235,000 — consistent with a labor market that is cooling gradually, not collapsing.

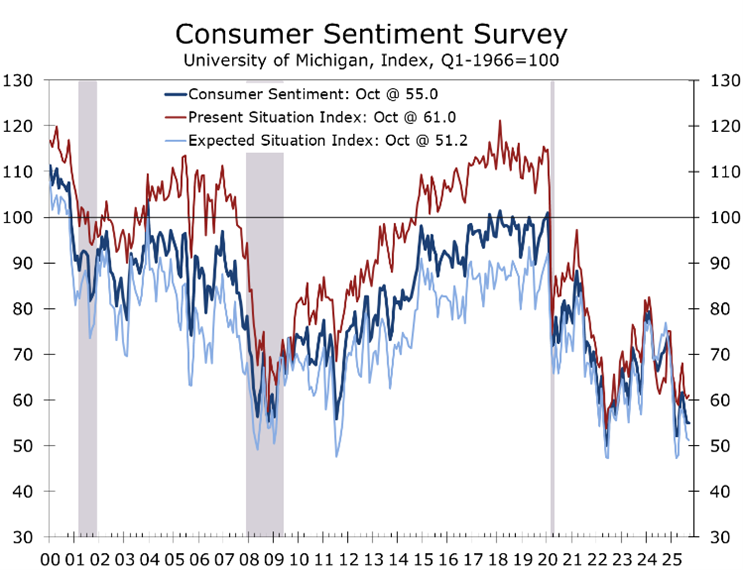

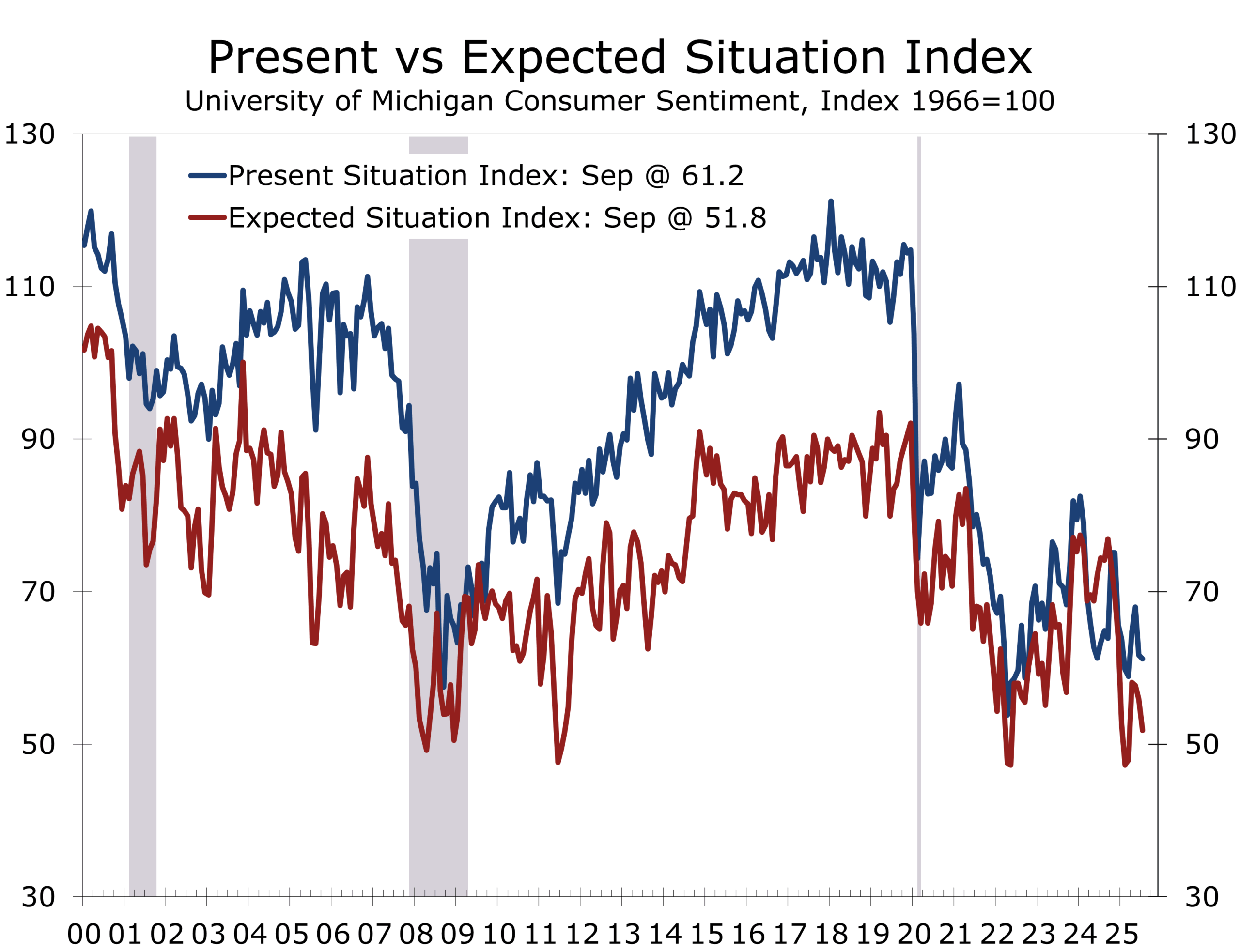

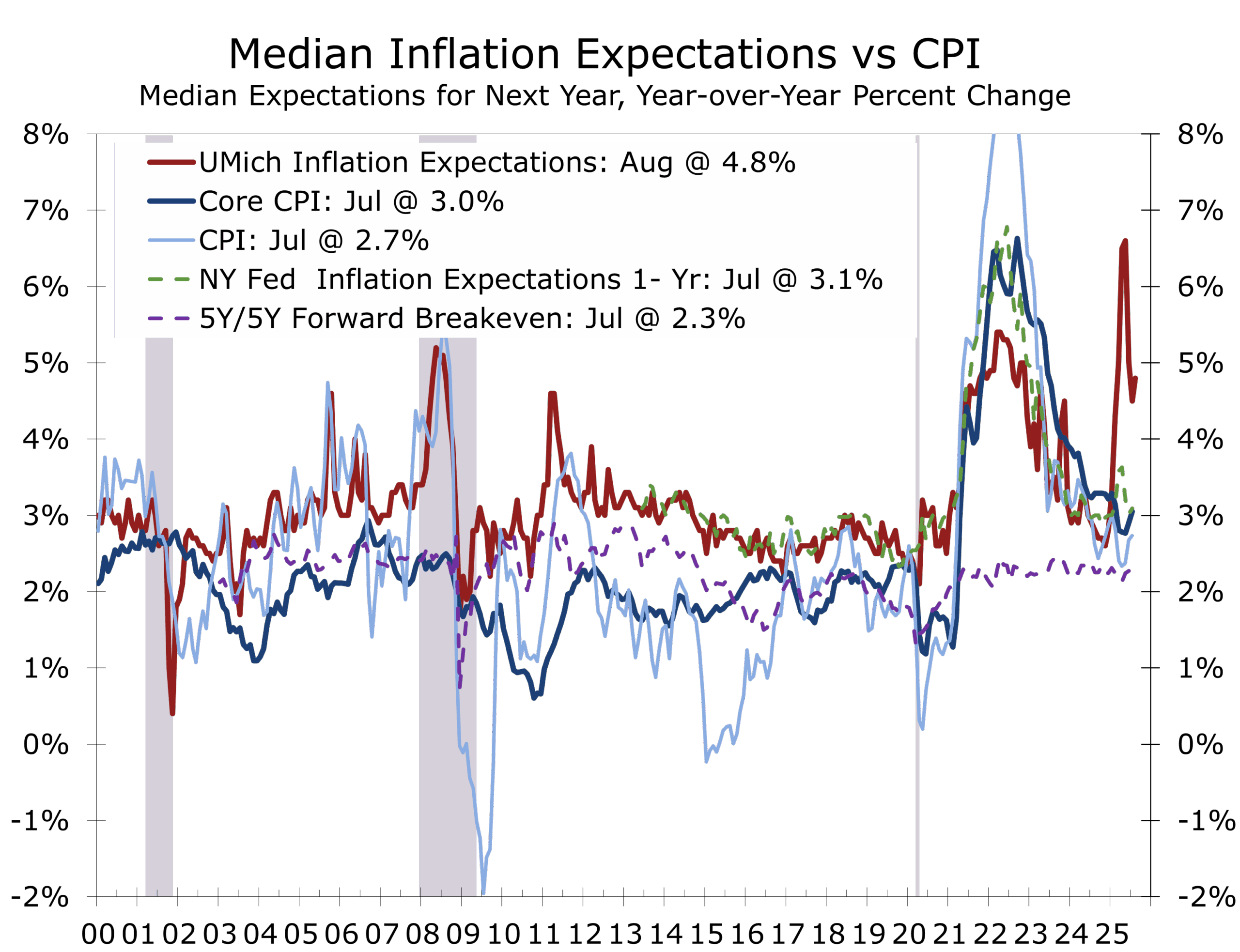

The early read on October consumer sentiment was steady on the surface but softening beneath. The University of Michigan index was virtually unchanged at 55.0 (down from 55.1), but consumers rated now as the worst time to buy durable goods since 2022. Year-ahead inflation expectations slipped modestly to 4.6%, while long-run expectations held at 3.7% — still above the Fed’s comfort zone.

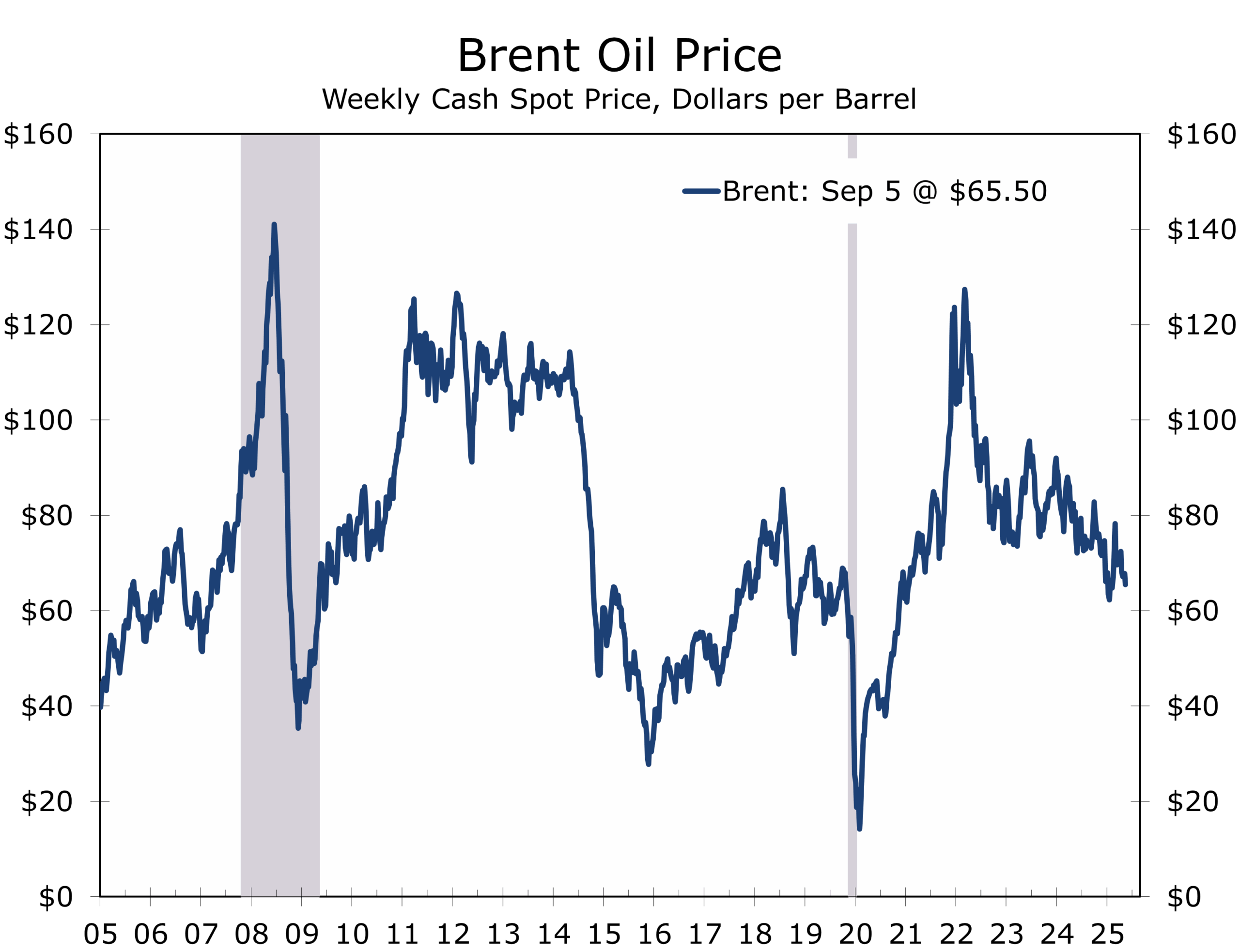

Stocks ended the week lower as tariff headlines erased midweek gains. The S&P 500 fell 1.3%; the Nasdaq 1.8%, led by megacap pullbacks. The 10-year Treasury yield dipped below 4.1%; oil prices fell roughly 3.5%; and Bitcoin hovered near $112,000 — a speculative mirror to the VIX.

For all the talk of gold bugs, the message was broader: when markets doubt the pilots, they reach for parachutes — and last week, they bought a lot of them.

Macro Backdrop: Flying Blind

The economy remains resilient, even with poor visibility. With the government still shuttered, investors have been forced to navigate by intuition and incomplete signals. The picture that emerges is one of an economy that continues to move forward — but increasingly by feel rather than sight.

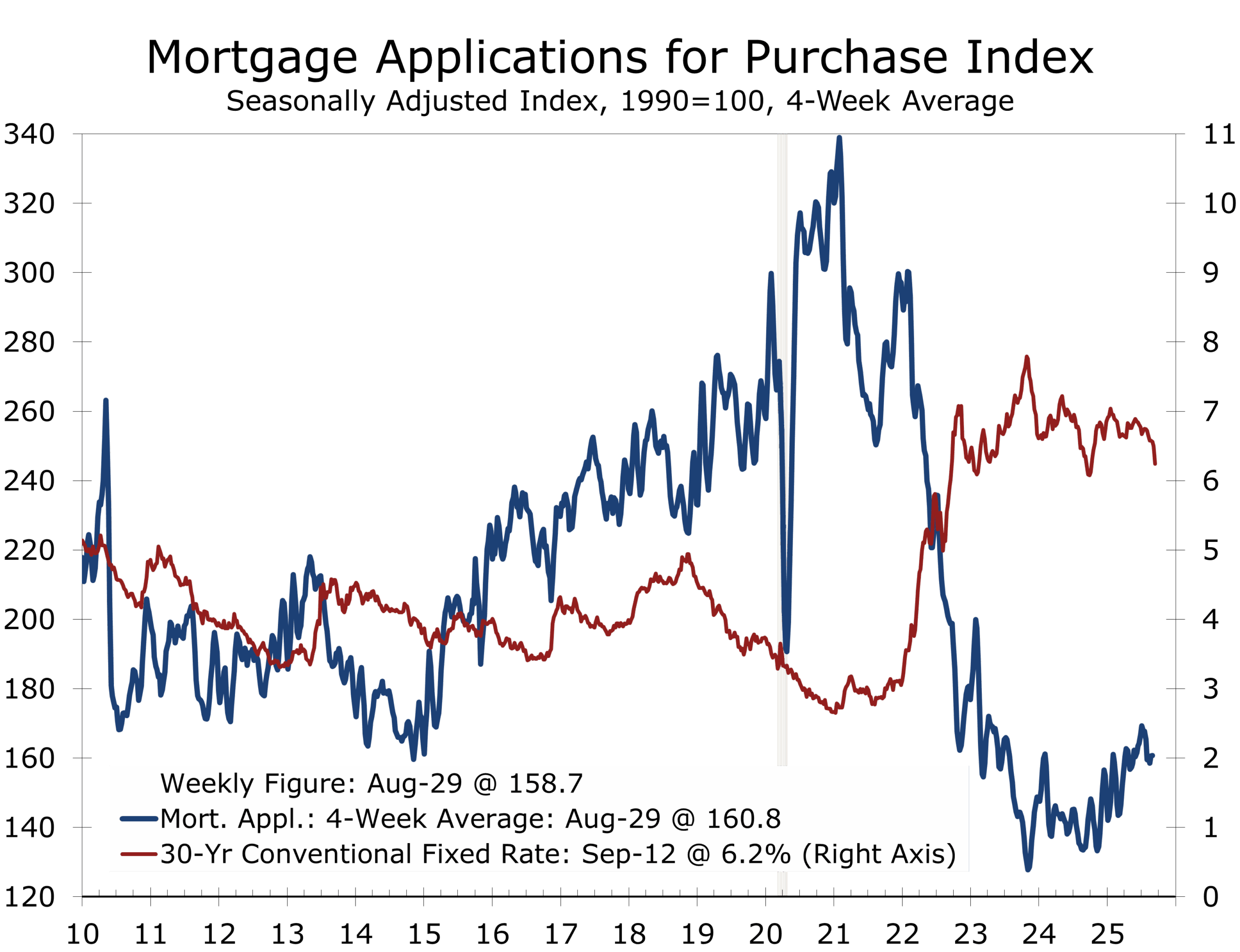

Private consumption indicators are steady, business investment remains strong in AI and related infrastructure, and housing shows tentative signs of stabilizing. Mortgage demand has rebounded as rates ease toward 6%, and builders are discounting prices to clear a growing inventory of unsold new homes. Job creation is clearly ebbing, however, and the Fed’s “dual mandate” is beginning to split along partisan lines. Inflation expectations have nudged modestly higher — not on data, but on psychology.

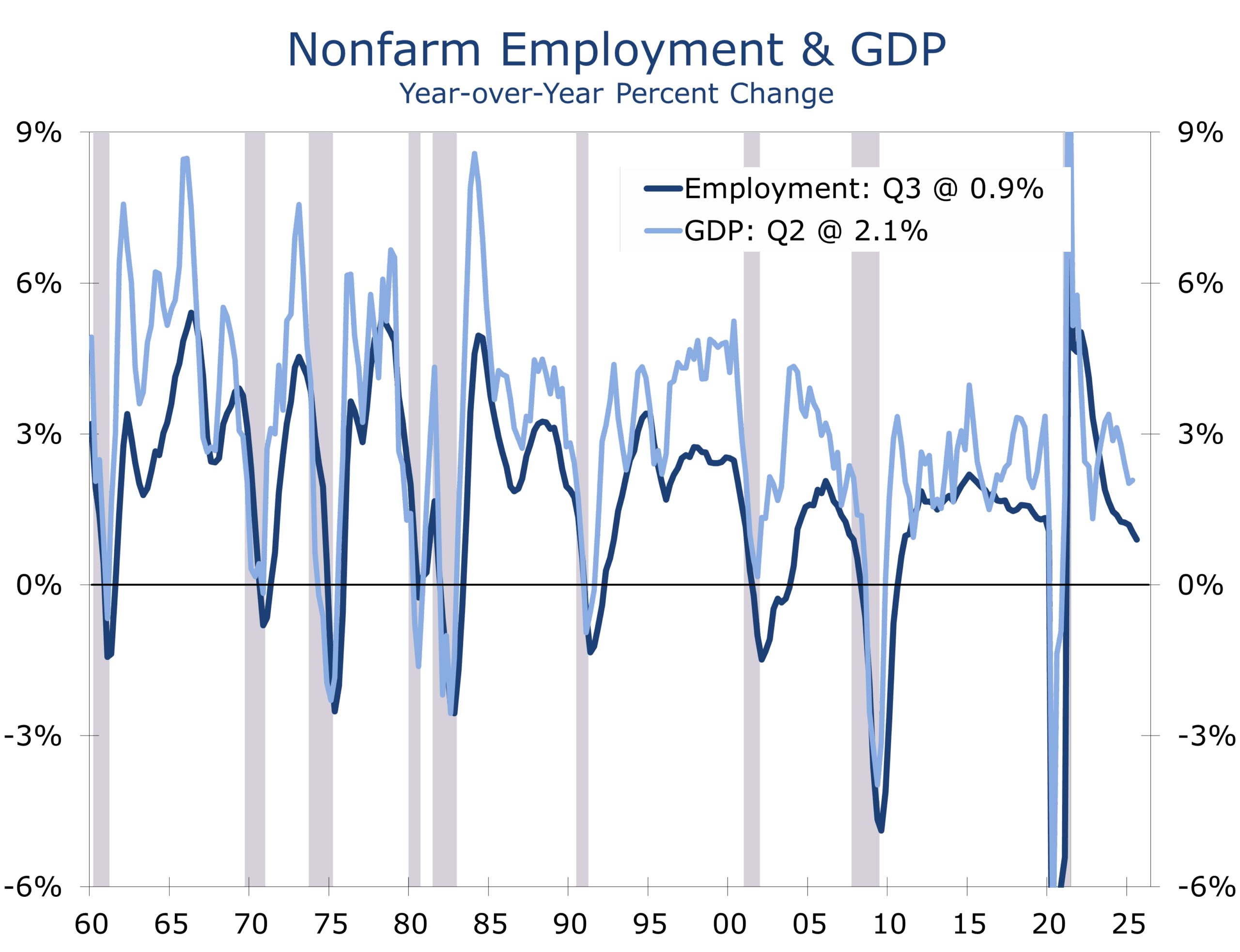

Meanwhile, the shutdown has turned the nation’s data stream into radio static. Economists have become codebreakers, piecing together fragments from Redbook, ADP, and credit-card data to fill the void. Expectations for Q3 GDP growth remain near 3%, but most Q4 forecasts have slipped into the 1.5%–1.8% range (a touch below our own 2.0%) as uncertainty delays spending and hiring decisions. Private indicators — and the federal furloughs that have thinned payrolls — suggest job growth is tepid at best and may already be turning negative. The larger question is how long the expansion can endure with the labor market faltering. History would say not long, but perhaps we are witnessing the rise of a second “new economy.”

.

U.S.–China: Tariffs, Technology, and the New Oil

Trade tensions flared again after Washington threatened to impose 100% tariffs on all Chinese imports — a dramatic escalation aimed at countering Beijing’s newly expanded export controls on rare earth elements and related technologies. Under the new rules, Chinese exporters must obtain government approval if Chinese content accounts for more than 0.1% of a product’s value, with licenses limited to six-month terms and subject to discretionary renewal — signaling that Beijing may selectively target rapidly growing U.S. technology and defense-related firms.

Beijing has already been slow-rolling existing export approvals, effectively tightening supply without a formal ban. These measures mark a shift from tariffs to technological choke points, turning access to critical minerals into a lever of geopolitical power. Washington’s retaliatory tariff threat — coupled with potential export controls on U.S. software and aircraft components — underscores how both sides are now weaponizing their comparative advantages: China’s dominance in critical mineral refining and America’s leadership in innovation and code.

We believe President Trump and President Xi are positioning themselves for negotiations later this year, likely using these threats to shape leverage ahead of potential discussions on the sidelines of the upcoming APEC summit in South Korea. While both sides may delay implementation for several weeks as talks proceed, the episode introduces yet another headwind for a global economy already losing momentum.

It’s a confrontation reminiscent of the 1970s energy shocks. Then, oil linked geopolitics to inflation and power; today, that role belongs to rare earths and semiconductors. Supply chains have become the new battle lines of national security, and markets — once buffered by globalization — now move in rhythm with each strategic announcement from Washington or Beijing.

Europe and Asia: Fragile Mandates, Fading Margins of Error

Political turbulence in France and Japan added fresh layers of uncertainty. In Paris, President Emmanuel Macron reappointed Sébastien Lecornu as prime minister after a destabilizing resignation. The reshuffle underscores Macron’s eroding authority in a divided parliament, where fiscal reform has stalled amid budget battles and social unrest. With borrowing costs rising, France’s paralysis threatens to widen OAT-Bund spreads and rekindle talk of a “two-speed Europe.”

In Tokyo, the collapse of Japan’s ruling coalition after Komeito’s withdrawal left Prime Minister Sanae Takaichi struggling to form a majority. The yen’s slide to multi-decade lows reflects doubts about the BOJ’s willingness to exit ultra-loose policy. Inflation has stabilized near 2%, but wage growth remains weak, and fiscal expansion tied to defense and energy subsidies has blurred the line between monetary and fiscal policy.

In both nations, credibility — not capacity — is the constraint. France faces pressure to enforce fiscal discipline without unrest; Japan, to defend the yen without reigniting deflation. The erosion of confidence in long-ruling parties has become a global motif — one that helps explain why gold and cryptocurrencies continue to climb.

The Nobel Peace Prize: Symbolism in a Cynical Age

The 2025 Nobel Peace Prize was awarded to María Corina Machado, the Venezuelan opposition leader long barred from public office by Nicolás Maduro’s regime. The committee cited her “unwavering advocacy for peaceful democratic transition.”

Machado dedicated the award to “the people of Venezuela — and to those who stood with us,” a clear nod to Donald Trump’s diplomatic pressure on Caracas. The move sparked admiration abroad and outrage at home, turning a humanitarian prize into a political lightning rod.

Nominations for the prize were due on January 31 — just eleven days after President Trump took office — far too early to reflect his later diplomatic achievements, including the breakthrough agreement between Israel and Hamas.

Internationally, the award was celebrated as a moral statement — democracy over détente — but in the United States it reopened partisan wounds. Some critics called it a “snub” to Trump, while others praised the committee’s independence. Like so many peace prizes, this one said more about the state of the world than about peace itself: it celebrated courage but reminded us how rare peace has become.

The Week Ahead

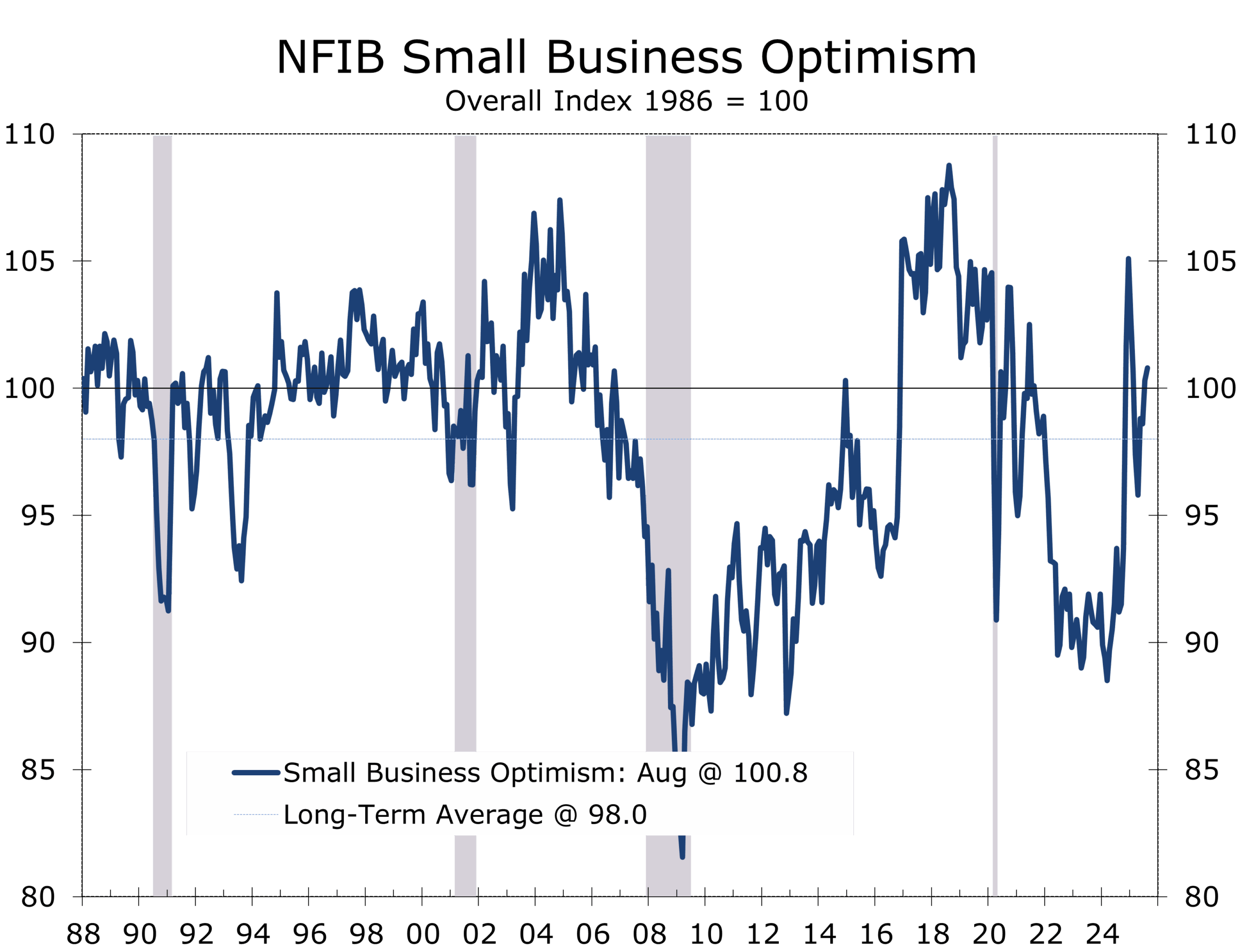

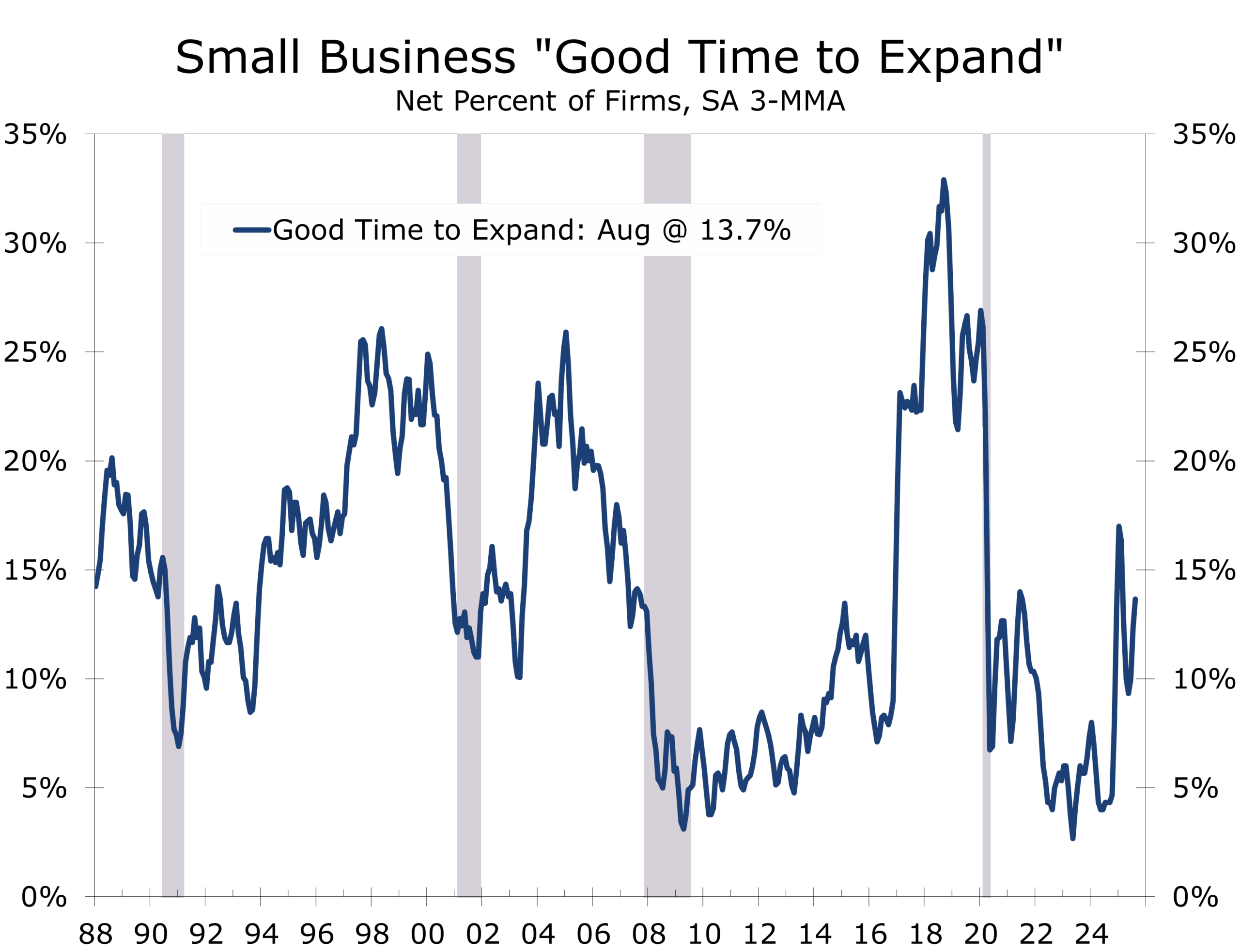

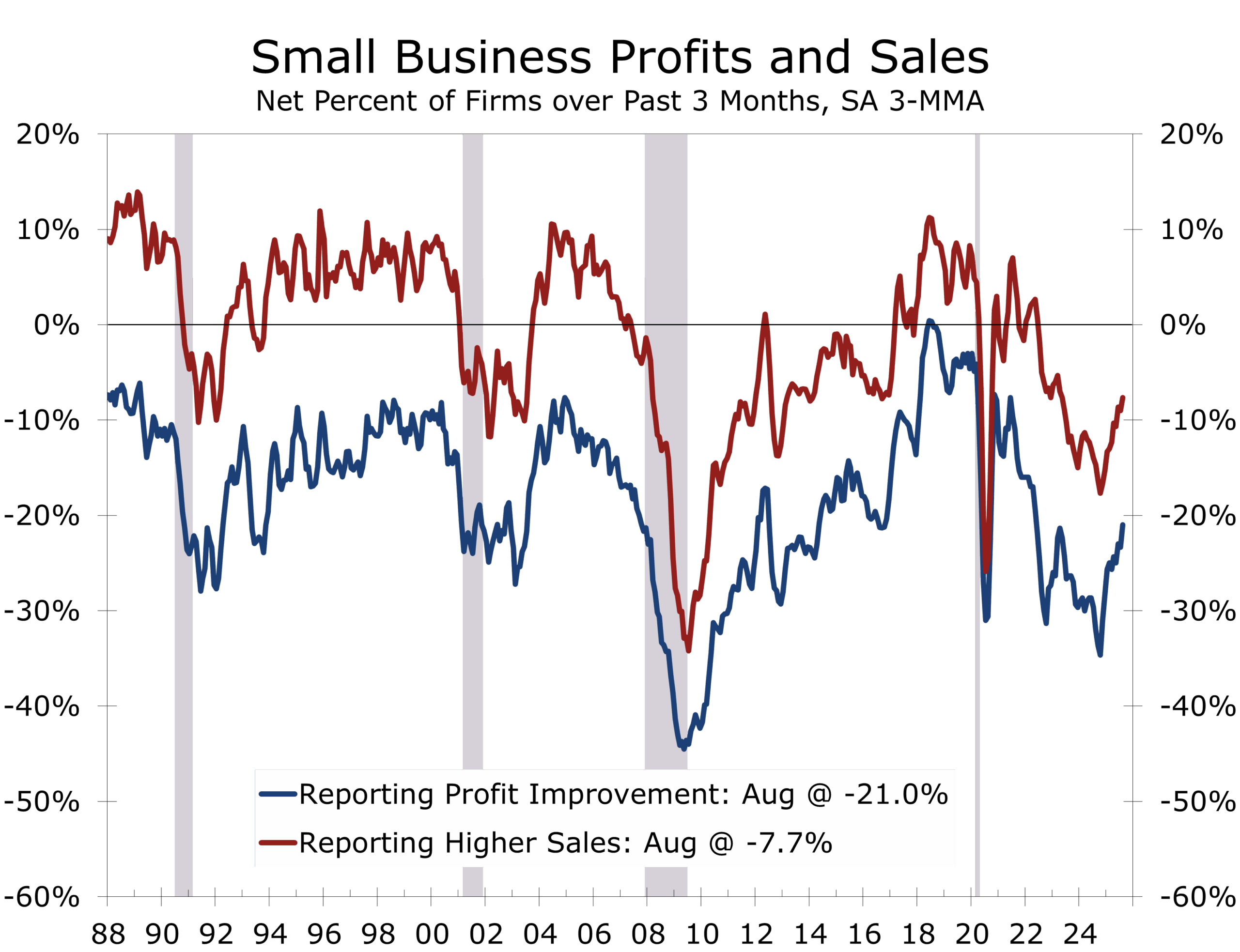

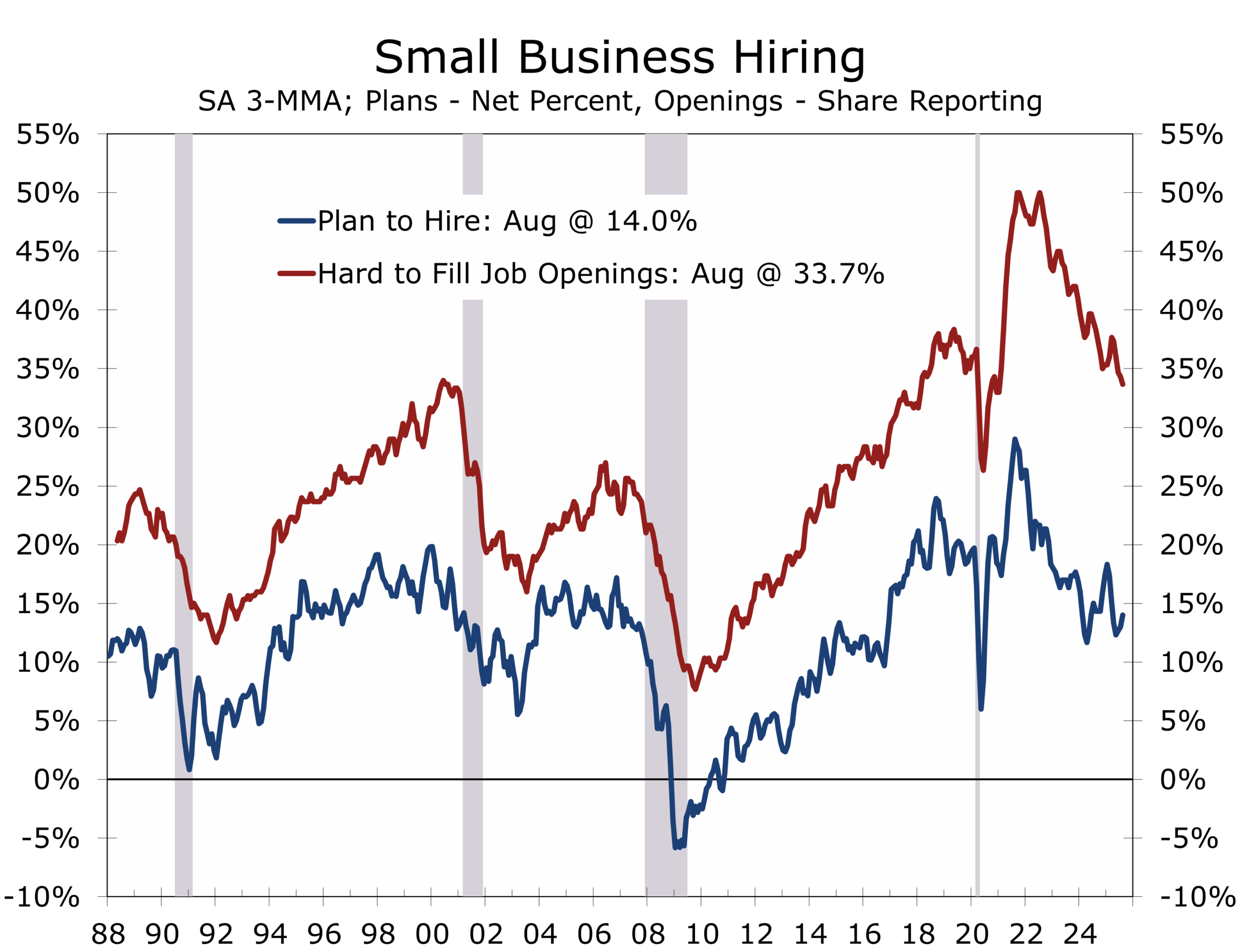

- U.S. Data: The shutdown’s continuation means limited new information, though private trackers for retail sales and jobless claims will be closely watched. The NFIB Small Business Optimism Survey (Tuesday) will be key for clues on supply chain strain and inflation pressures.

- Fed Watch: Markets will parse speeches from Waller and Bowman, as well as Wednesday’s Beige Book, for signals on whether October remains “live” or if a cut is now a virtual certainty.

- Geopolitics: All eyes on the Gaza truce — if it holds, oil could retreat; if it fails, risk spreads widen again.

- Earnings: Banks kick off reporting season — providing stress test results for credit conditions and consumer sentiment.

Closing Thoughts: The Road Ahead

On the final day of the ride, coasting downhill toward Monopoli, the wind finally shifted at my back. The Adriatic shimmered in the evening light, and for the first time in days the climb felt worth it. It was that same afternoon the trade deal with China came off the rails — Beijing tightening exports of critical materials and magnets, Washington retaliating with threats of 100% tariffs. The headwinds that had eased along the coast were rising again in the markets, unseen but unmistakable.

Progress in policy, like cycling through crosswinds, rarely comes with momentum alone. It demands endurance — the ability to keep pace when the path tilts against you and the signals ahead blur. Gold’s gleam this month reflects less fear of inflation than a loss of faith: in policymaking, in coordination, and in the systems meant to anchor both.

Like those ancient olive trees rooted in the rocky soil of Puglia, investors who hold their ground through seasons of strain tend to outlast the storm. The road ahead will twist and rise again — it always does — but those who shift gears with purpose rather than panic will find that even the steepest ascent offers a broader view from the summit.

Concluding Thoughts: The Penalties from Hell

Vacations have a way of inviting reflection — especially when surrounded by inspiring architecture, landscapes, and art. We have switched from biking to touring — and from one coast to another. On our first day in Sorrento, we toured an exhibition of Joan Miró, whose work was as colorful as it was thematic across the decades of his long and illustrious career.

Israel’s long war with Hamas brings to mind Miró’s Les Pénalités de l’Enfer — “The Penalties of Hell” — a phrase that captures both the fury and the necessity of this drawn-out conflict. The title originated in Miró’s early 1970s collaboration with poet Robert Desnos, where chaos, color, and anguish collided on the page. Miró’s vision was an artistic outcry against cruelty and constraint; Israel’s version is tragically literal — a campaign of force aimed at dismantling an organization that glorified death and desecrated innocence. Each, in its own way, represents a struggle to make sense of evil through expression — whether on canvas or in combat.

The parallels with 1973 extend beyond the calendar. Then, the Yom Kippur War triggered the Arab oil embargo and unleashed the inflationary spiral that defined the decade. Today’s conflict unfolds amid a different kind of shock — less about oil, more about trust and technology — dividing the world once again into blocs aligned with the U.S. and Europe on one side, and Russia, China, North Korea, and Iran on the other. Yet this time, the arc may prove more hopeful. The Abraham Accords have opened a path toward normalization between Israel and its Arab neighbors — a peace built not on illusion, but on mutual interest: trade, security, and shared resistance to extremism.

The 1970s ended in disillusionment and disorder. This decade could still close in redefinition and renewal. The “penalties from hell,” both as art and as policy, remind us that order often emerges only after the most violent ruptures. What Miró rendered in abstraction, Israel now lives in reality — a confrontation with darkness that tests whether civilization still has the will to defend itself.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

October 13, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Private Data, Public Impasse

Highlights of the Week

- The economy ended Q3 with modest but stable growth, though momentum has softened as hiring slows and confidence slips.

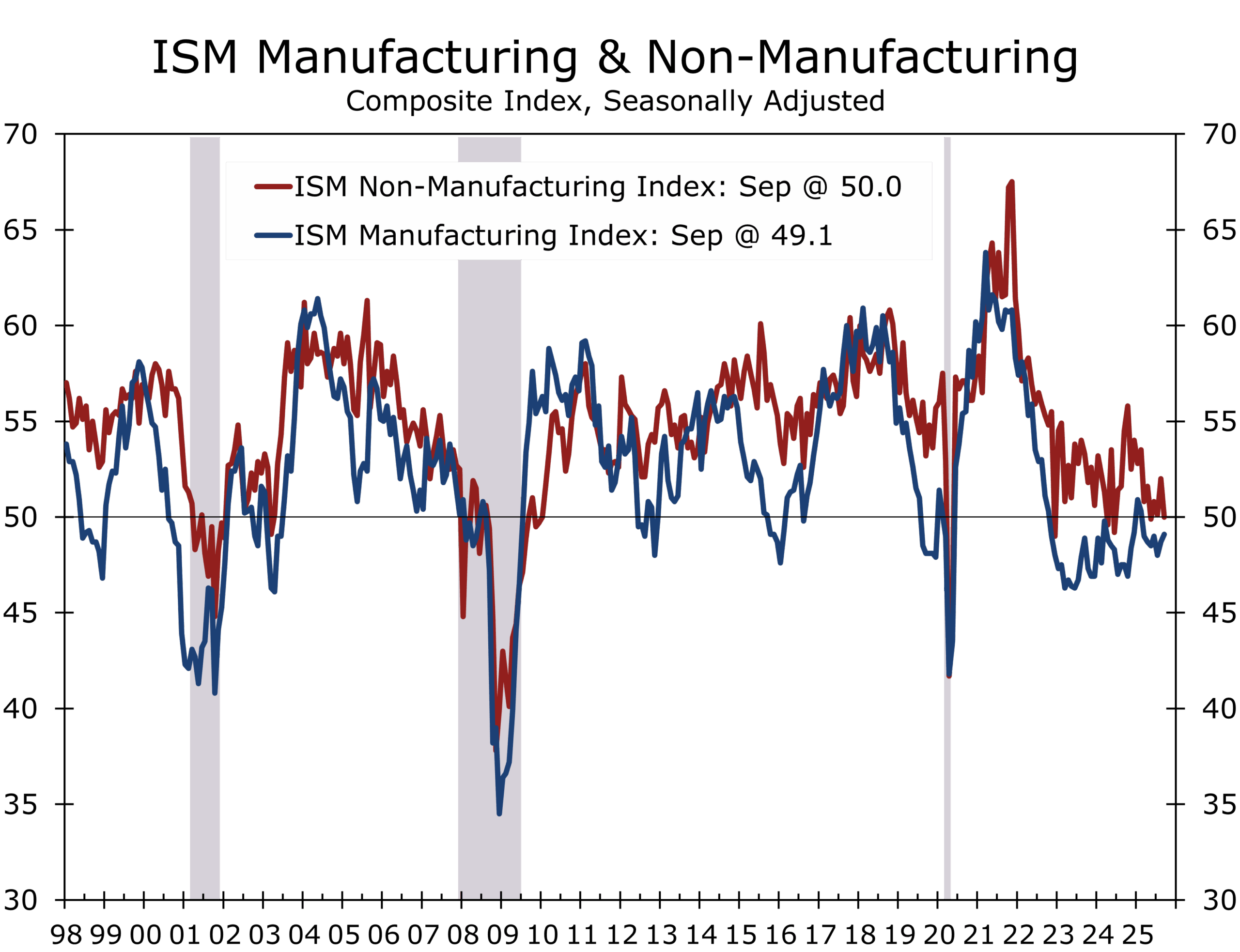

- ISM Manufacturing rose to 49.1 while ISM Nonmanufacturing fell sharply to 50.0 — both employment subindexes contracted, pointing to weaker labor demand.

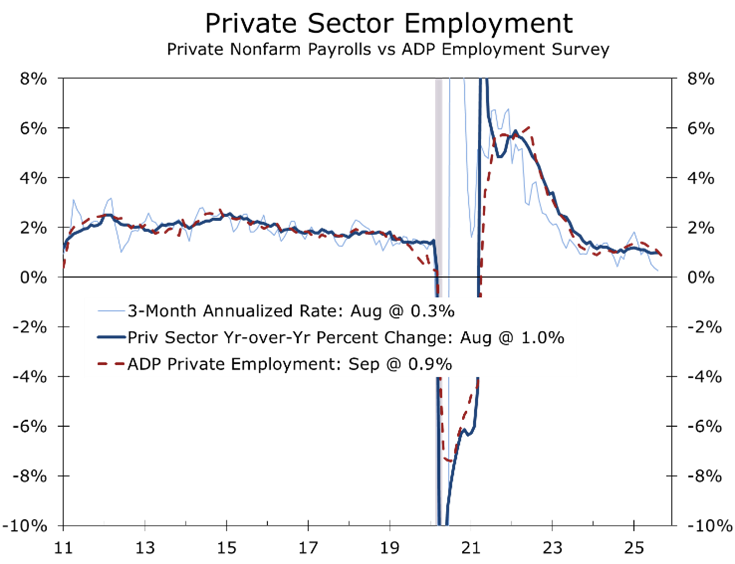

- The ADP report showed a 32,000-job decline, concentrated in small firms, and NFIB data confirm hiring plans remain strong but hard to execute amid skill mismatches.

- Private consumption finished Q3 on a high note as vehicle sales surged 2% before the expiration of EV tax credits; that strength will fade in Q4.

- The government shutdown has suspended key data releases, creating a “data fog” that may push the Fed toward an October rate cut, already priced into markets.

- Treasury yields declined 5–8 basis points as the curve steepened, equities gained, and investors stayed positioned for a soft-landing.

- Housing shows early signs of stabilization as mortgage rates approach 6%, while home price growth continues to cool without collapsing.

- Geopolitical tensions intensified with renewed ceasefire pressure on Israel, Moldova’s pro-EU election, Japan’s new conservative leadership, and protests across Europe supporting Hamas.

Macro Update: Private Data, Public Impasse

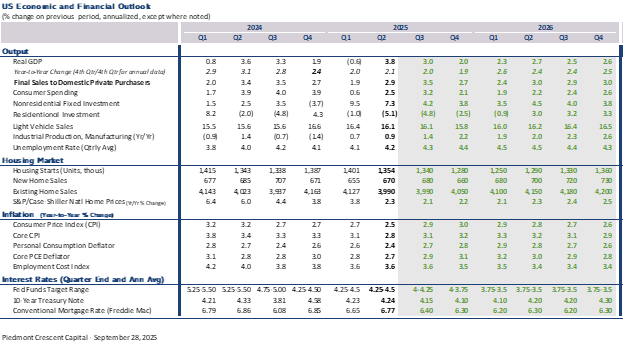

The early weeks of October find the economy balancing steady private-sector momentum against fiscal and geopolitical uncertainty. With the government shutdown delaying key official releases, investors have turned to private surveys, diffusion indexes, and real-time models as proxies. Together, these data suggest the economy remains resilient but is losing a little altitude, with hiring softening and confidence fraying at the margins. Our forecast now pegs Q3 growth at 3 %, reflecting the inertia of consumer spending and business investment even under constrained policy conditions.

Even amid gridlock, the private economy kept its footing, with Q3 growth likely near a 3% pace.

The September ISM manufacturing and services reports suggest the economy ended the third quarter with modest but stable forward motion. The manufacturing PMI edged up to 49.1 from 48.7 in August, alleviating some weakness while remaining in contraction territory but still well above levels typical of recession. New orders softened, inventories continued to shrink, input costs remained elevated, and employment showed tentative signs of stabilization.

On the services side, the ISM nonmanufacturing PMI fell to 50.0 from 52.0, the lowest reading since early 2023, indicating near-stagnation in service-sector output. The employment component weakened further to 47.2, confirming slower hiring momentum even as demand steadied.

With the shutdown suspending the release of BLS employment and initial claims data, markets have leaned heavily on alternative signals. The Challenger report again showed hiring extremely slow and layoffs steady—an extension of the “low hiring, low firing” regime. The Chicago Fed’s real-time model estimates unemployment ticked up to 4.34 % from 4.32 %.

The ADP private payrolls release revealed a 32,000 decline, with significant downward revisions to past months, pointing to a weaker private employment trend. Regional Fed manufacturing surveys signaled mild job cuts across districts, and consumer surveys showed a rising share of respondents describing jobs as hard to get—a signal that labor demand is softening faster than supply. August JOLTS data also revealed continued loosening in cyclical industries, while Indeed job ads fell.

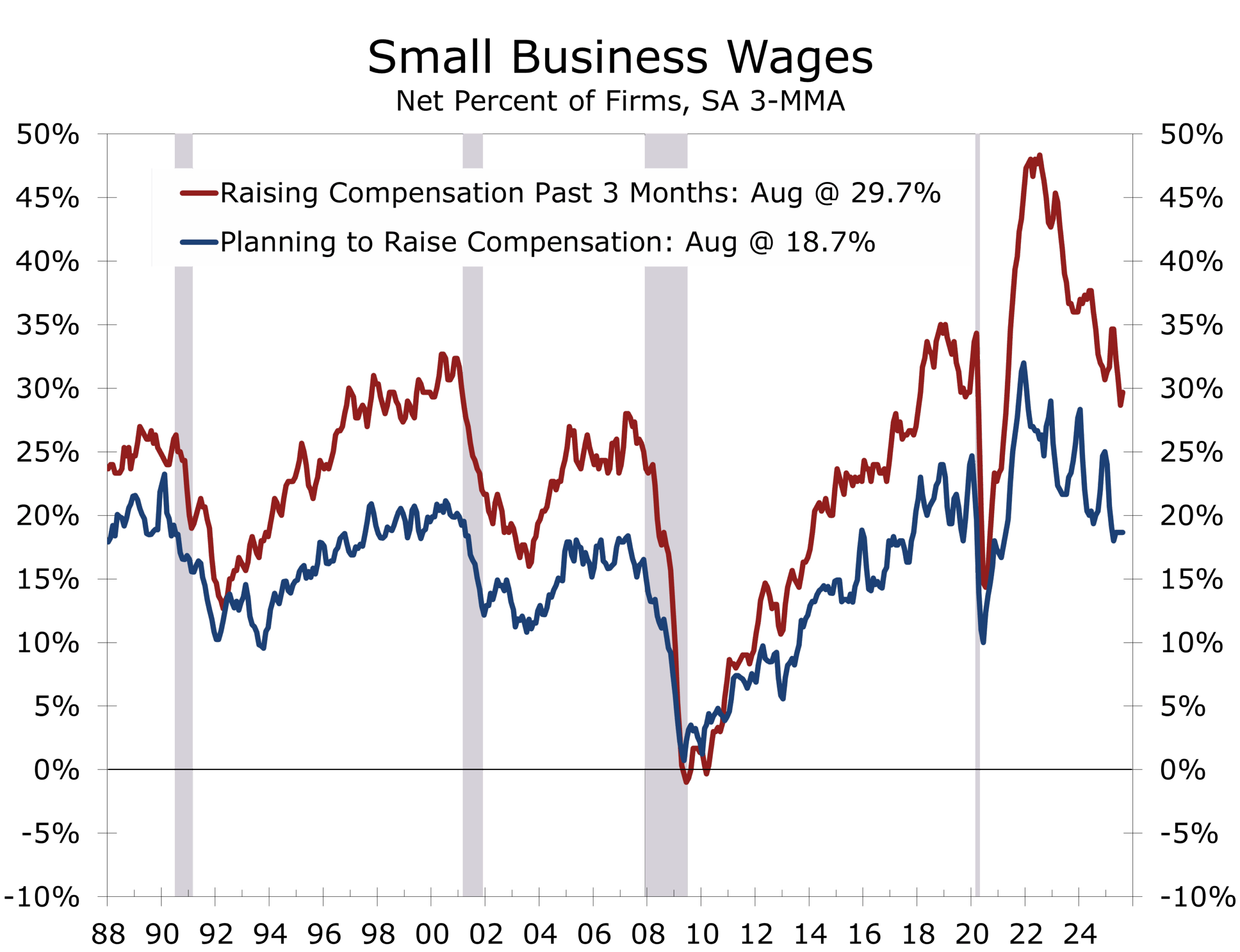

Adding further nuance, the NFIB small-business survey showed that net hiring plans rose to 16%, the highest since January, suggesting firms still intend to expand. Yet that intention exists amid constraints: 32% reported unfilled job openings, and, among those hiring, 50% said they had few or no qualified applicants. Labor quality remains the top constraint, while labor costs as a top operating concern edged up to 11 %. A net 31 % of firms said they raised compensation in September, and 19 % planned pay increases in the next quarter.

Data delays leave markets flying blind; private reports keep an October cut on the radar.

Taken together, these indicators point to a labor market that is cooling rather than collapsing. Market consensus remains that the Fed cut at each of the next three meetings, banking on further softening. Still, the risk asymmetry is clear: sharper-than-expected labor weakness could pressure earnings, while a resurgence in inflation would constrain policy flexibility. Our base case remains a soft landing, but we remain cognizant of both tail risks. We would prefer the Fed alternate meetings for rate cuts, which would extend the cycle. That looks unrealistic today, however.

The Atlanta Fed’s GDPNow model, prior to the shutdown, placed Q3 growth at 3.8%; private data since then have largely upheld that estimate. The rush to lock in EV incentives creates some upside risk to Q3 GDP. While a short-lived shutdown will likely have muted effects on Q4 growth, extended paralysis could erode confidence, disrupt capital spending, and slow government-driven flows—risks that would erode the momentum that private activity has carried thus far. We expect the shutdown to be resolved by mid-October. The House will be back in session on October 13 and military members need to be paid on the 15th.

.

Israel Under Pressure—and Shifting Global Currents

For nearly two years, Israel has fought the multi-front war that began with the October 7 attacks. Prime Minister Benjamin Netanyahu’s government expanded operations from Gaza to the northern frontier with Hezbollah while carrying out precision strikes across the West Bank and Syria. That strategy—focused on threat eradication—now faces increasing constraints: diplomatic pressure for a ceasefire, internal political fractures, and rising risk of regional escalation.

Following Israel’s strike on Hamas leadership in Qatar, the U.S. has quietly shifted toward diplomacy, working with Egypt, Qatar, and other intermediaries to explore phased ceasefire arrangements tied to the release of all hostages and security assurances. Iran continues to press via proxies in Lebanon, Iraq, and Yemen, as well as stoking resistance in Europe through intermediaries (both knowing and unknowing) complicating Israel’s margin for maneuver. U.S. military posture in the region has been adjusted to deter escalation, but domestic fiscal and institutional stress may limit strategic flexibility.

The region is tired or war and we expect the U.S.-brokered peace deal to take hold. The ever-elusive perfect peace deal will not get in the way of a very good settlement.

In Europe, Moldova’s pro-European Party of Action and Solidarity, led by Maia Sandu, secured a clear parliamentary majority, reinforcing a westward orientation and delivering a political setback to Kremlin influence. Moscow has already challenged the result, citing limitations in expatriate polling access, and may deploy disinformation or economic pressure tactics to destabilize the new government. The victory will force the new administration to balance reliance on EU leverage with the latent risks surrounding Transnistria, where Russian military presence endures.

In Asia, Japan’s Liberal Democratic Party elected Sanae Takaichi as leader, making her the country’s first woman to become prime minister. A long-time conservative figure and confidant of the Abe era, she signals a more assertive security posture and renewed emphasis on defense cooperation with the U.S. Economically, she favors fiscal stimulus over monetary tightening, likely delaying any aggressive BOJ normalization. Regionally, her style could revive disputes with China and Korea if nationalistic signals intensify, even as she seeks to consolidate power within the fractious LDP.

Across Europe, sustained protests in support of Hamas and against Israel’s Gaza campaign have mobilized hundreds of thousands in capitals from Rome to London, Berlin to Paris. In Italy, protests extended over several days, with parts of the movement targeting ports and arms shipments. In London, police made nearly 500 arrests during Palestine Action demonstrations. European governments are now confronted with the challenge of reconciling domestic pressure with their diplomatic commitments to Israel. At the same time, the protests energize fringe movements across the political spectrum, raising broader security and stability risks in a continent already grappling with inflation, energy stress, and slow growth.

Taken together, these dynamics underscore the fracturing of the post-war global consensus. Leadership transitions, social unrest, and cross-pressured alliances are accelerating realignments. The global economy may still be holding up, but the buffer zone in which policymakers can absorb shocks is narrowing fast—and missteps will carry greater consequences.

Looking Ahead

In the week ahead, markets will look for high-frequency proxies for labor market, consumer spending, economic activity and capital spending and, assuming the government reopens, the CPI and PPI prints. The consensus still leans toward cuts in October and December, and more likely January as well, but geopolitical volatility and legislative risks in Washington could derail that script. The economy is managing by momentum—for now—but the durability of that run rate is becoming more fragile. The real test in coming months will be whether markets and governance can absorb noise without breaking down.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

October 6, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

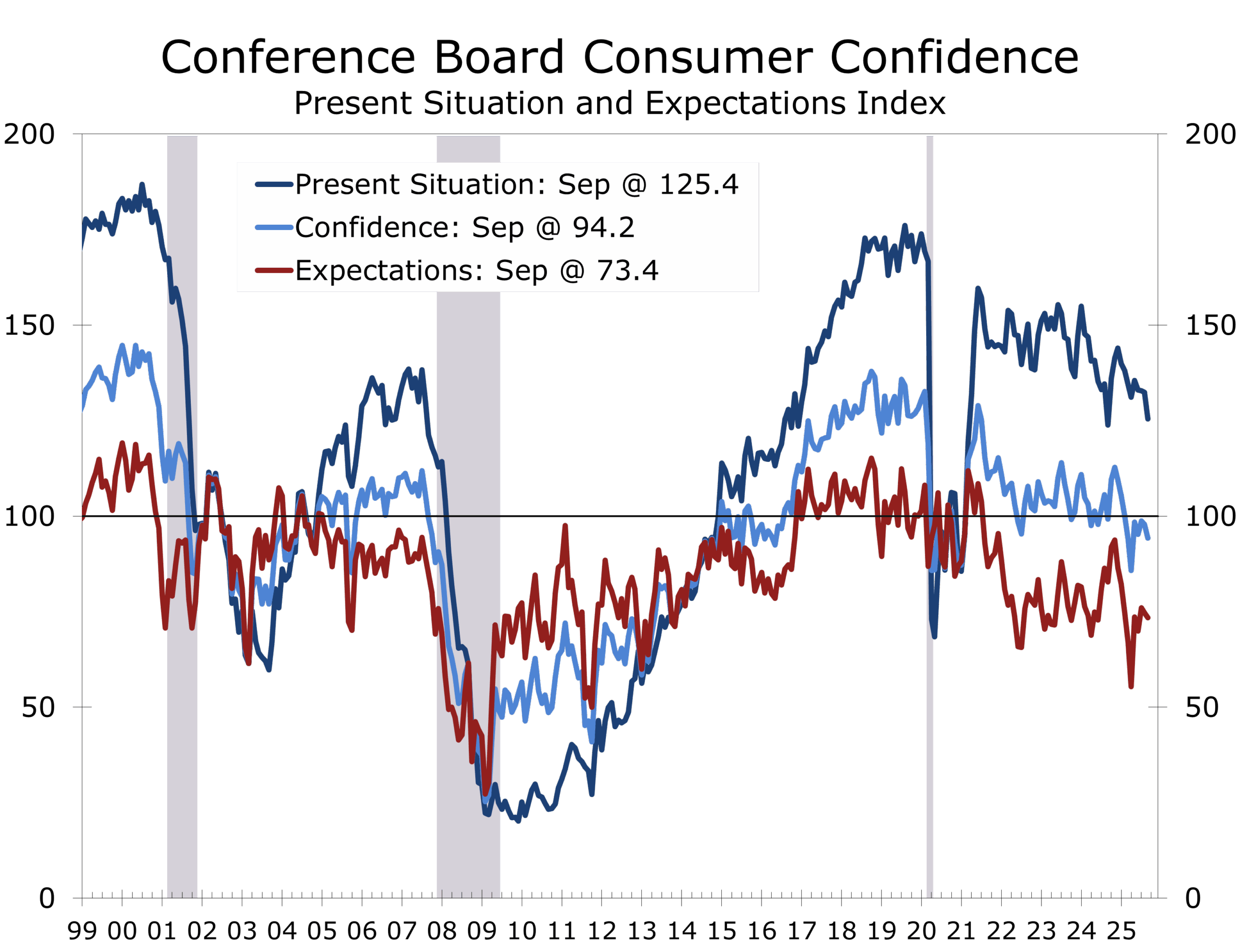

Consumer Confidence Declines More Than Expected

Confidence Continues to Slide as Job Security Concerns Increase

-

- The Conference Board’s Consumer Confidence Index® slipped 3.6 points in September to 94.2, modestly weaker than expected but still near recent averages.

- The Present Situation Index fell 7.0 points to 125.4, its largest drop in a year, while the Expectations Index eased 1.3 points to 73.4, remaining well below the recession-warning threshold of 80 for an eighth straight month.

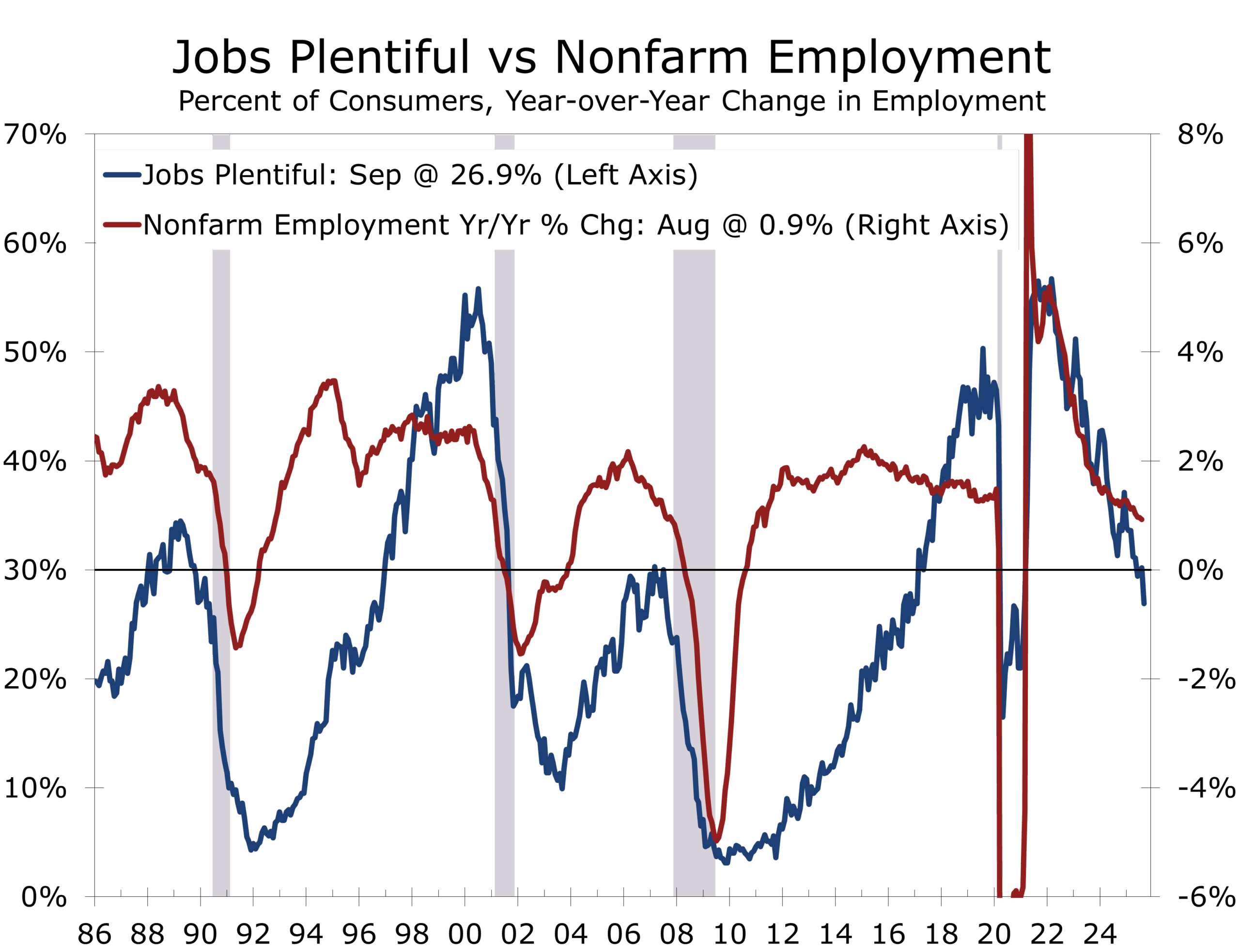

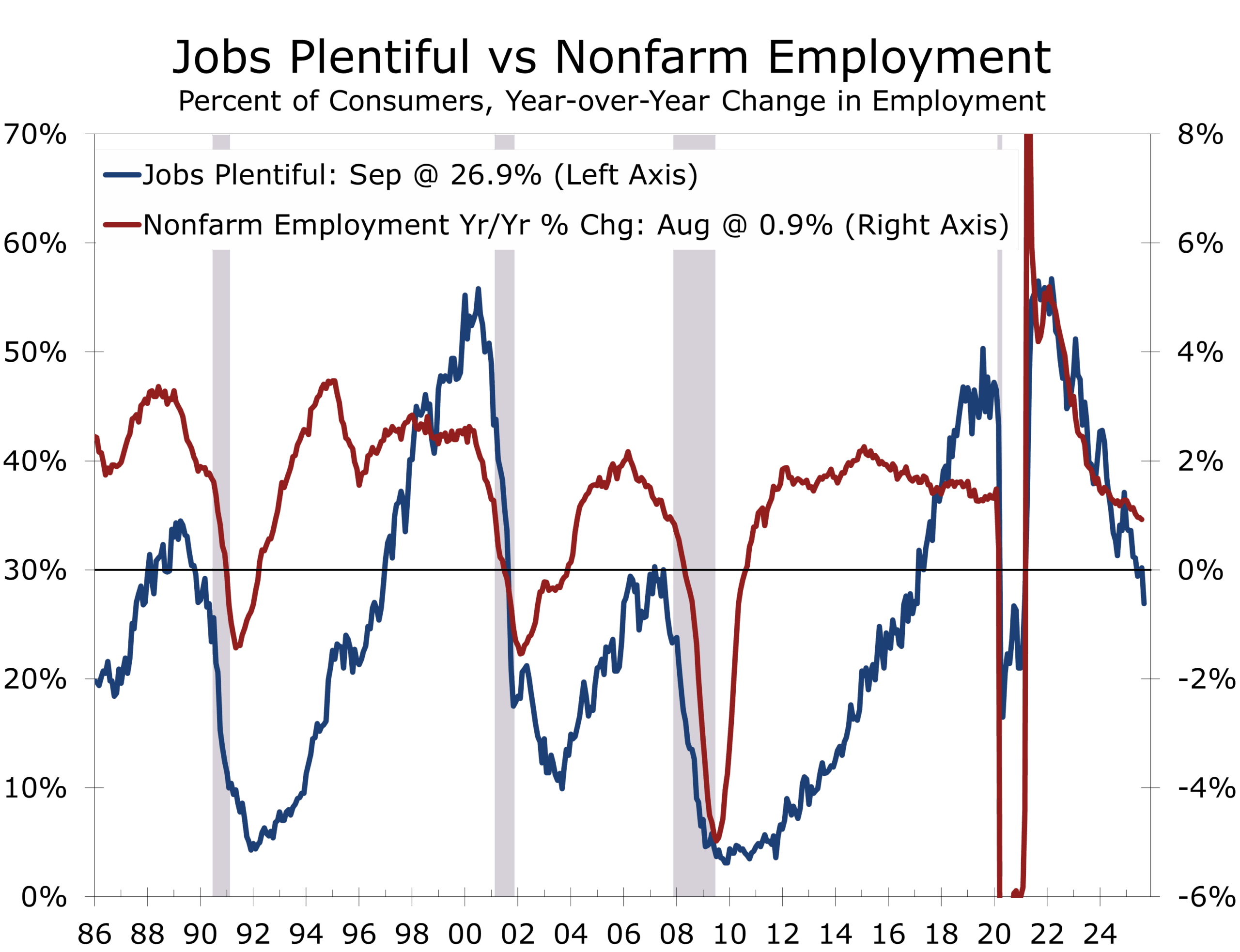

- The labor differential narrowed to 7.8—its lowest level since February 2021—signaling weaker job availability.

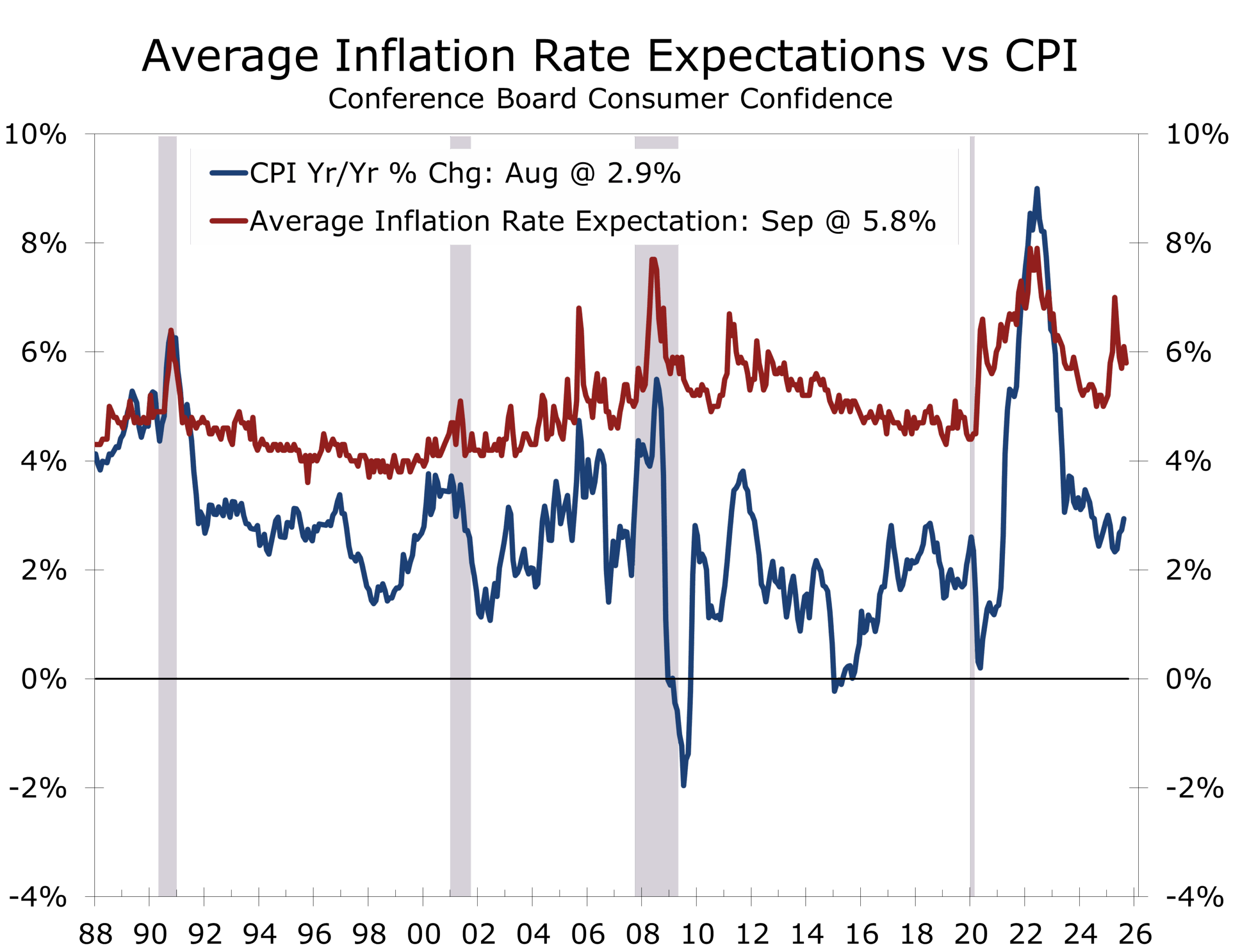

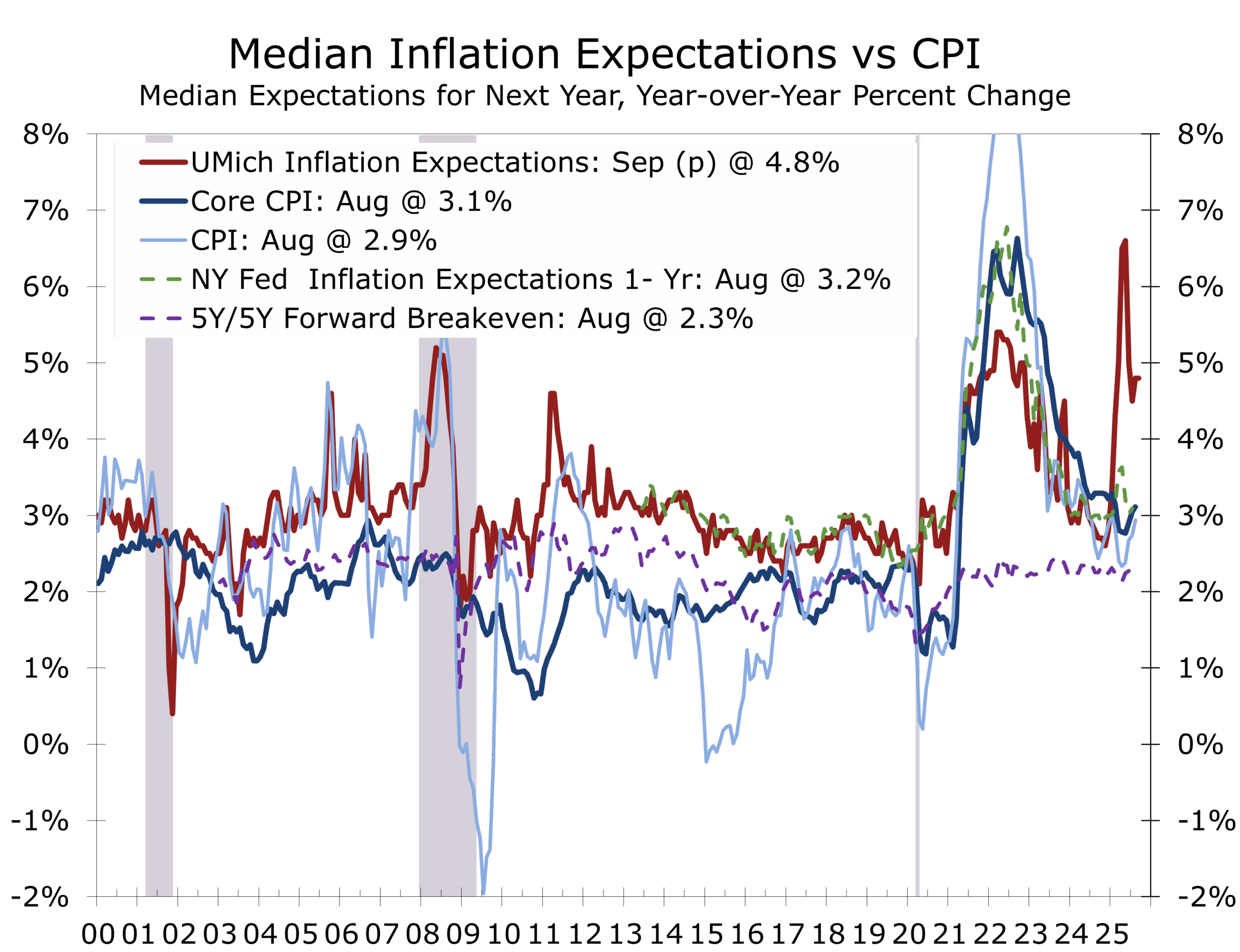

- Inflation expectations edged down to 5.8%, but consumer write-ins showed renewed concern about prices. Mentions of tariffs declined, though they remain associated with price pressures.

- Spending intentions were mixed: home buying plans hit a four-month high, but car buying and travel-intentions weakened.

Upper-Income Resilience vs Middle-Income Angst

Consumer confidence fell slightly more than expected and the underlying details suggest the expansion remains more fragile than recently upgraded GDP forecasts suggest. The steep decline in the Present Situation Index reflected growing unease about business conditions and job availability. The share of consumers saying jobs are “plentiful” fell to 26.9%, down from 30.2% in August, while 19.1% said jobs are “hard to get.” This pushed the labor market differential down to 7.8, its lowest reading since February 2021.

Traditionally, the labor differential leads the unemployment rate, which has been rising as the differential has fallen. The relationship between the two, however, may be shifting. With fewer foreign workers entering the workforce, slower labor force

two, however, may be shifting. With fewer foreign workers entering the workforce, slower labor force growth could temper the rise in unemployment even as consumers report weaker job availability. The deterioration in the differential still stands as a clear warning that labor market conditions are weaker than the headline employment numbers suggest. The latest JOLTS report reinforced this picture of a “low hiring, low firing” economy—job openings remain plentiful relative to history, but hiring rates have slipped, making it harder for job seekers to gain traction.

Upper-income spending holds on asset gains, while middle-income caution grows.

Consumer spending stayed resilient this summer, with stronger July and August retail sales lifting Q3 GDP forecasts. But the gains were driven mainly by upper-income households benefiting from rising equity and housing wealth.

Middle-income households, by contrast, are showing greater caution. Job security appears to be waning, and more job seekers are finding it harder to land positions in a softer hiring environment. These households also remain more sensitive to inflation, which explains why inflation references reemerged as the top consumer concern in September’s survey.

Middle-income households pull back as job security wanes and inflation fears linger.

Meanwhile, middle-income households in the region’s manufacturing and logistics sectors are retrenching, constrained by weaker hiring pipelines and persistent price pressures on essentials. This divergence echoes national trends but is magnified in regions like the South, where growth has long depended on the persistent in-migration of job seekers. The risk is that confidence erosion at the middle-income level could begin to sap the broader consumer base that has historically underpinned growth across the Southeast.

Inflation expectations provided a small offset, easing to 5.8% from 6.1% in August. Even so, consumers’ write-in comments suggest they are not convinced inflation pressures are truly receding. Tariff mentions declined but remain elevated, a reminder that trade policies continue to shape consumer psychology even as pass-through effects have been surprisingly modest.

Spending intentions remain uneven. Home buying plans climbed to a four-month high as lower mortgage rates lured some buyers back, but auto purchases slipped under the weight of high financing costs. Travel plans weakened further, with international trips leading the decline. The link between sentiment and spending has loosened. Spending is outperforming income growth, however, indicating that wealth is helping sustain spending as job growth slows and worries about employment security increase.

Spending outpaces income growth, sustained by wealth effects as job worries mount.

The September Consumer Confidence report captures a consumer mood that has softened at the margin but is still far from collapsing. Confidence declined slightly more than expected, but the sharper deterioration in the present situation underscores risks around jobs and spending intentions. Inflation anxieties remain sticky, and middle-income households appear more cautious even as upper-income spending supports headline growth. For the Fed, this mix—sliding confidence, a weakening labor backdrop, and persistent price concerns—supports a cautious, gradual approach to rate cuts.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

September 30, 2025

Mark Vitner, Chief Economist

(704) 458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Gridlock vs Goldilocks

Highlights of the Week

- GDP Revised Up: Q2 GDP rose at a 3.8% pace, with private final domestic demand up at a 2.9% pace, led by stronger consumer spending and business fixed investment.

- Industry Drivers: GDP by Industry highlights strength in intellectual property, equipment, and financial services; housing remains a drag.

- Consumer Resilience: August PCE data show real spending up 0.4% m/m, tracking Q3 growth at 2.6–2.8%. Gains are increasingly concentrated among higher-income households.

- Labor Stabilizing: Jobless claims trending lower; payrolls (if released) might open the door for the Fed to skip October and waits until December to cut rates-which would extend the easing cycle.

- Housing Bifurcated: New-home sales surged but likely overstated strength; completed-home inventories remain elevated, while existing supply is shrinking on delistings as home prices ebb.

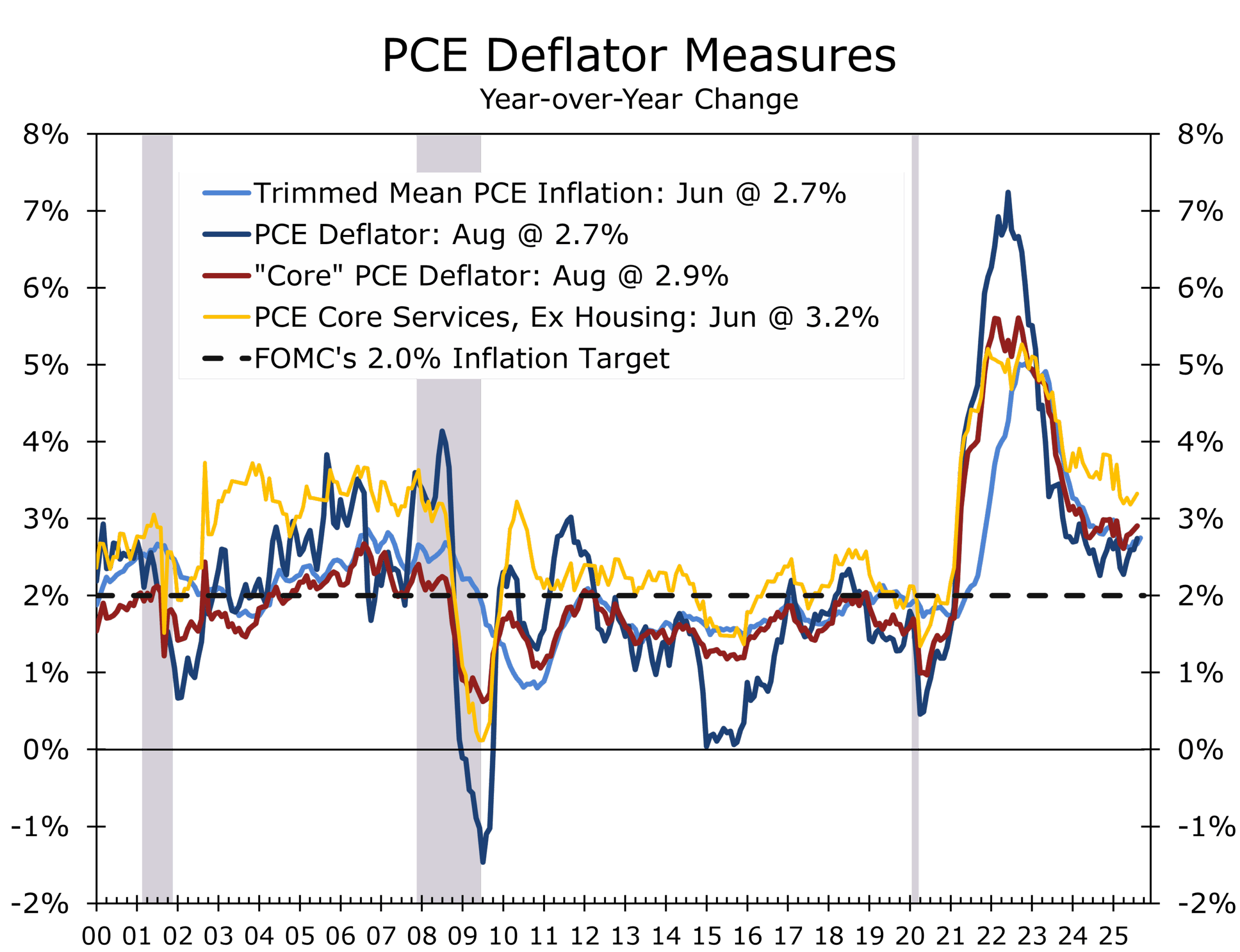

- Inflation Sticky but Moderating: Core PCE rose 0.23% in August, 2.9% y/y. Tariffs are keeping goods prices firmer than services prices.

- Markets and Credit: Treasury yields drifting higher; Investment-Grade spread curves flattening at the back end due to supply-demand dynamics, not credit stress.

- Energy Security: Aging grids and rising AI/defense power needs place metals-intensive investment at the center of national security.

- Washington Risk: High probability of a short shutdown as fiscal year ends Sept 30; even without one, delayed disbursements represent stealth tightening.

Growth & the Consumer

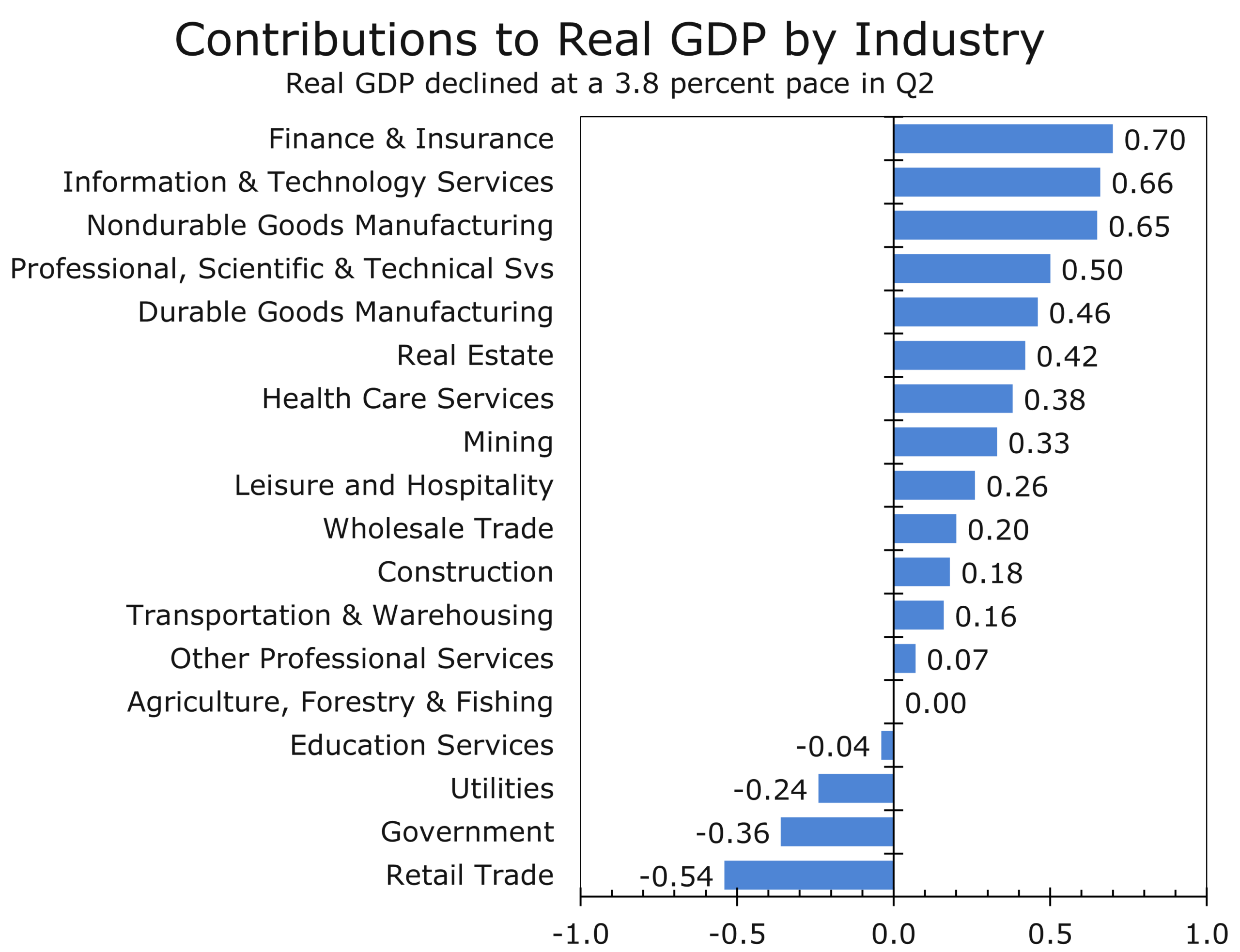

The GDP revisions were a reminder not to bet against the U.S. consumer. Real GDP growth was revised up to 3.8% in Q2, with private final domestic demand advancing 2.9%. Stronger consumption (+2.5%) and a 7.3% rise (annualized) in nonresidential fixed investment were the main drivers.

Consumer spending was led by light vehicle sales and increased outlays for health care, financial services, and travel and entertainment. Business fixed investment was supported by spending on tech equipment, commercial aircraft, and research and development. Structures investment declined, reflecting the wind-down of stimulus-driven outlays for EV and green energy projects. Some projects were halted or canceled during the quarter, but many are now coming back on track.

The GDP by Industry data highlight how growth is distributed across the economy. Intellectual property products and equipment investment led the way, while transportation, finance, and other services provided steady contributions. Housing investment, however, remained a drag, contracting at a 5.1% pace and subtracting from overall Q2 growth. The chart underscores the uneven but resilient character of U.S. growth: productivity-rich sectors are expanding even as rate-sensitive housing lags.

That strength appears to be carrying into Q3. August PCE showed real spending up 0.4% m/m, with revisions boosting earlier months. Our tracking estimate now points to 3.2% growth in Q3 real personal consumption. The composition is skewed toward higher-income households, supported by asset income and wealth effects, while middle- and lower-income consumers remain constrained by moderating wage growth and stubbornly high prices for groceries, rent, transportation, and insurance.

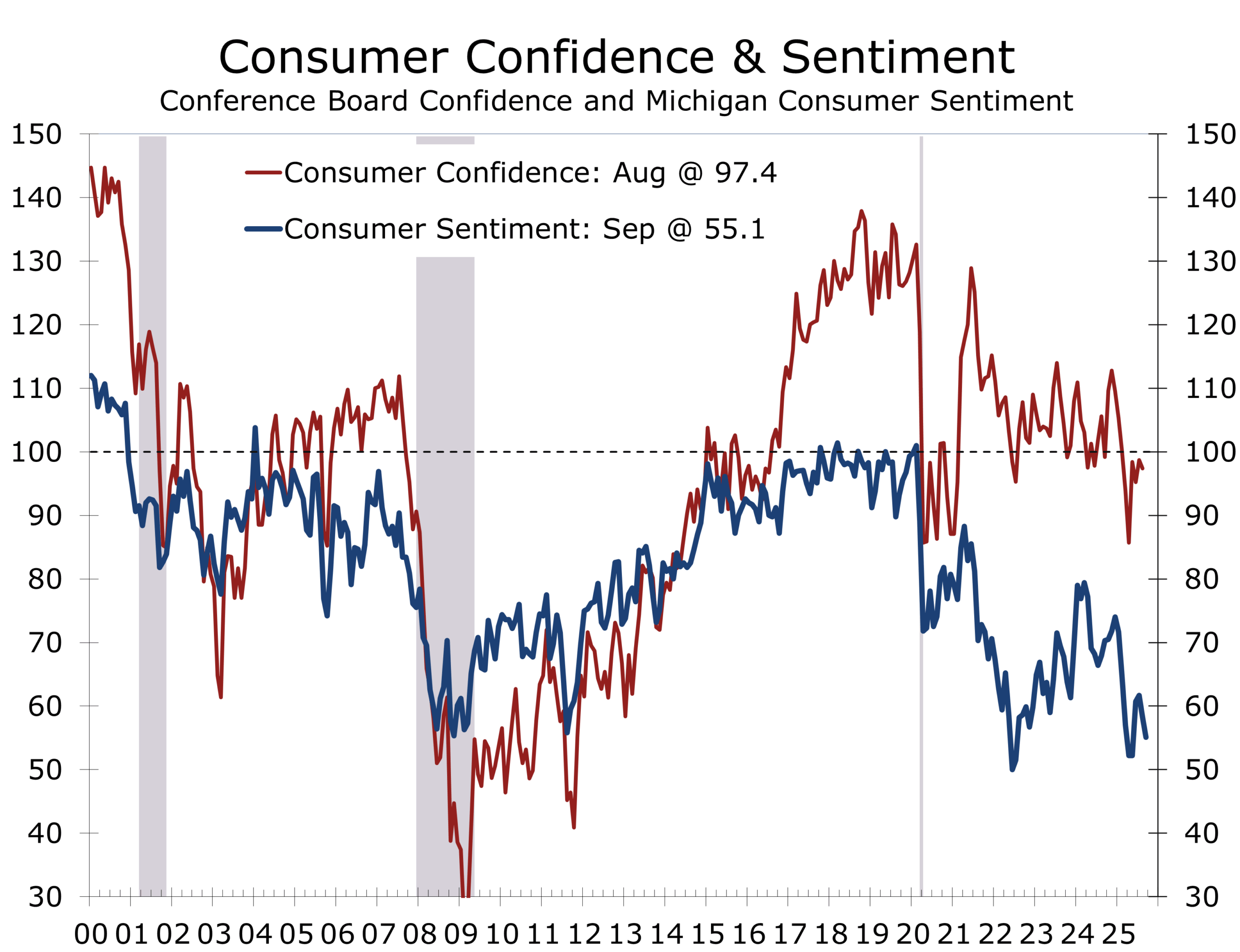

In contrast to the strong spending numbers, Consumer Sentiment slipped in September, with the final University of Michigan index falling to 55.1. Consumer Sentiment remain at levels that are more typical of a deep recession than one growing at around a 3% annual rate. Buying conditions for durables hit a one-year low, underscoring the divergence between higher income and middle and lower income households. Consumers also appear more apt to spend than they say they will.

Shutdown Raises Stakes for September Payrolls

The labor market continues to soften at the margin but is also showing signs of stabilizing. Initial jobless claims fell to 218,000 in the week ended Sept 20, with the four-week average edging lower. Continuing claims also declined modestly, suggesting layoffs remain limited and rehiring continues.

Nonfarm payrolls now serve as both economic signal and political casualty, complicating Fed decision-making.

This week’s September payrolls report, if a government shutdown does not prevent its release, will be pivotal. Markets are looking for a modest rebound from August’s soft print and a steady 4.3% unemployment rate. Nonfarm payrolls fell in June and employers have added an average of just 41,000 jobs a month since April. A shutdown would delay the release and leave the Fed with less clarity heading into the October FOMC meeting — strengthening the case to skip October and wait until December to resume easing. The ADP data will take on more relevance than usual if the government shuts down Wednesday morning..

.

Housing – Locked In and Locked Out

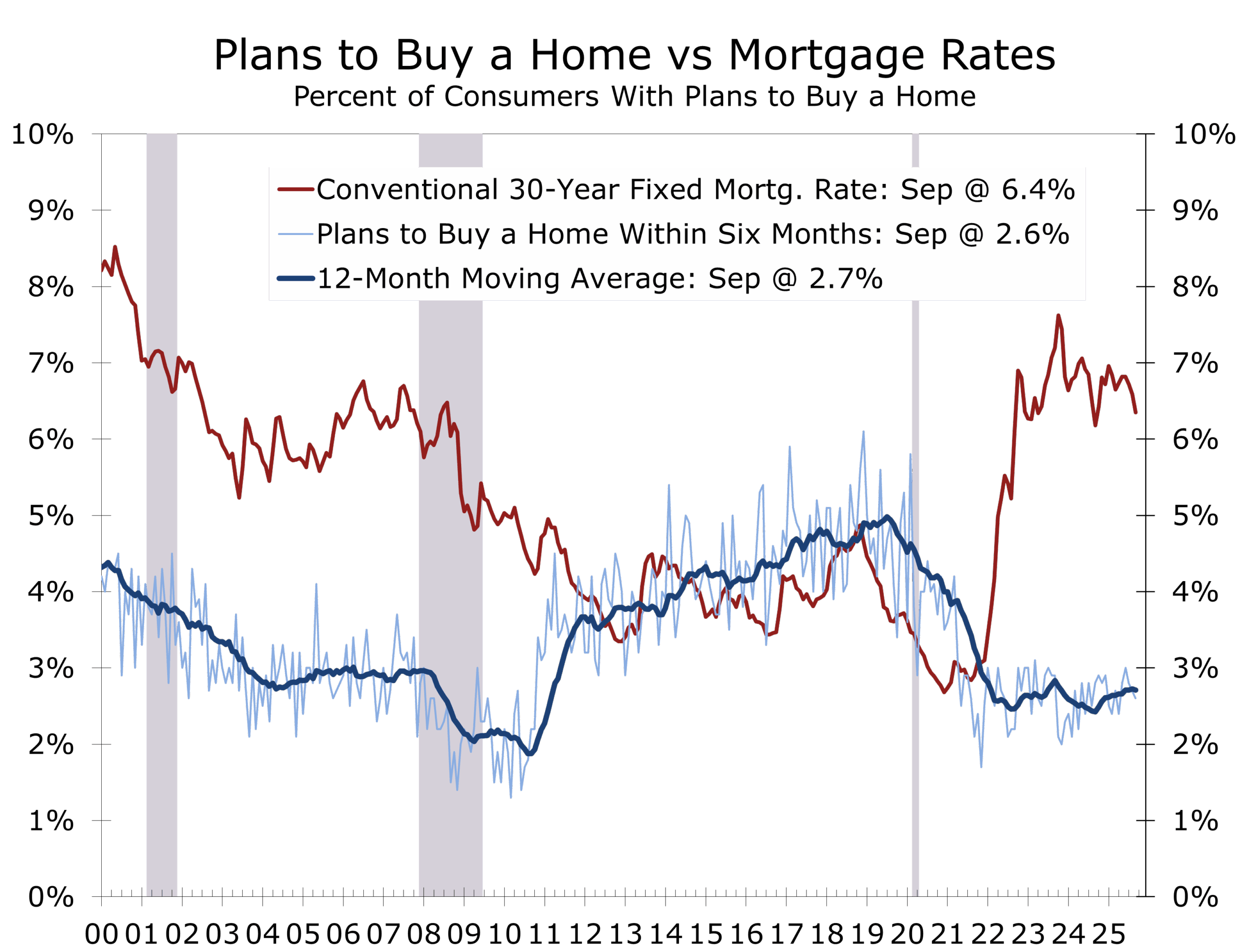

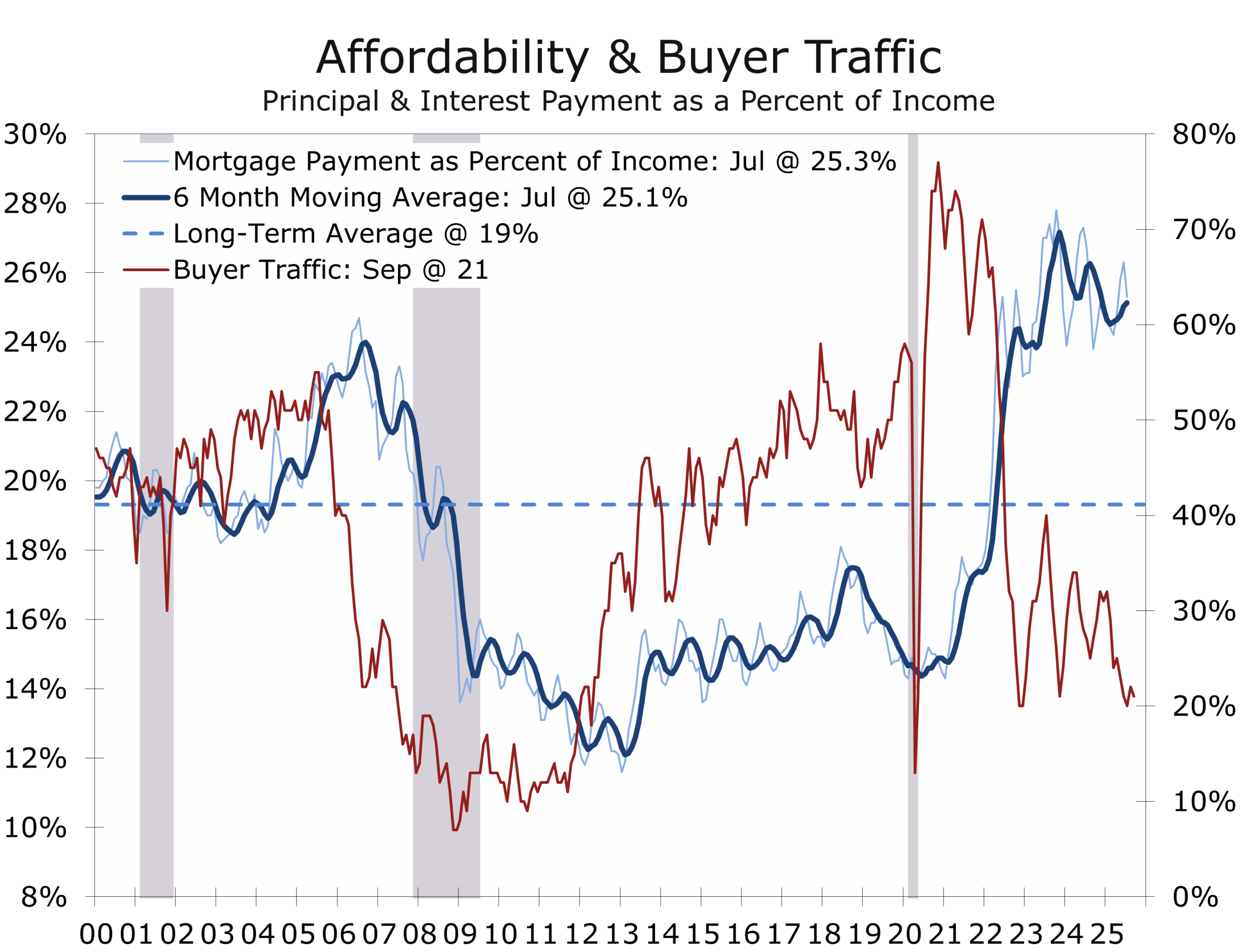

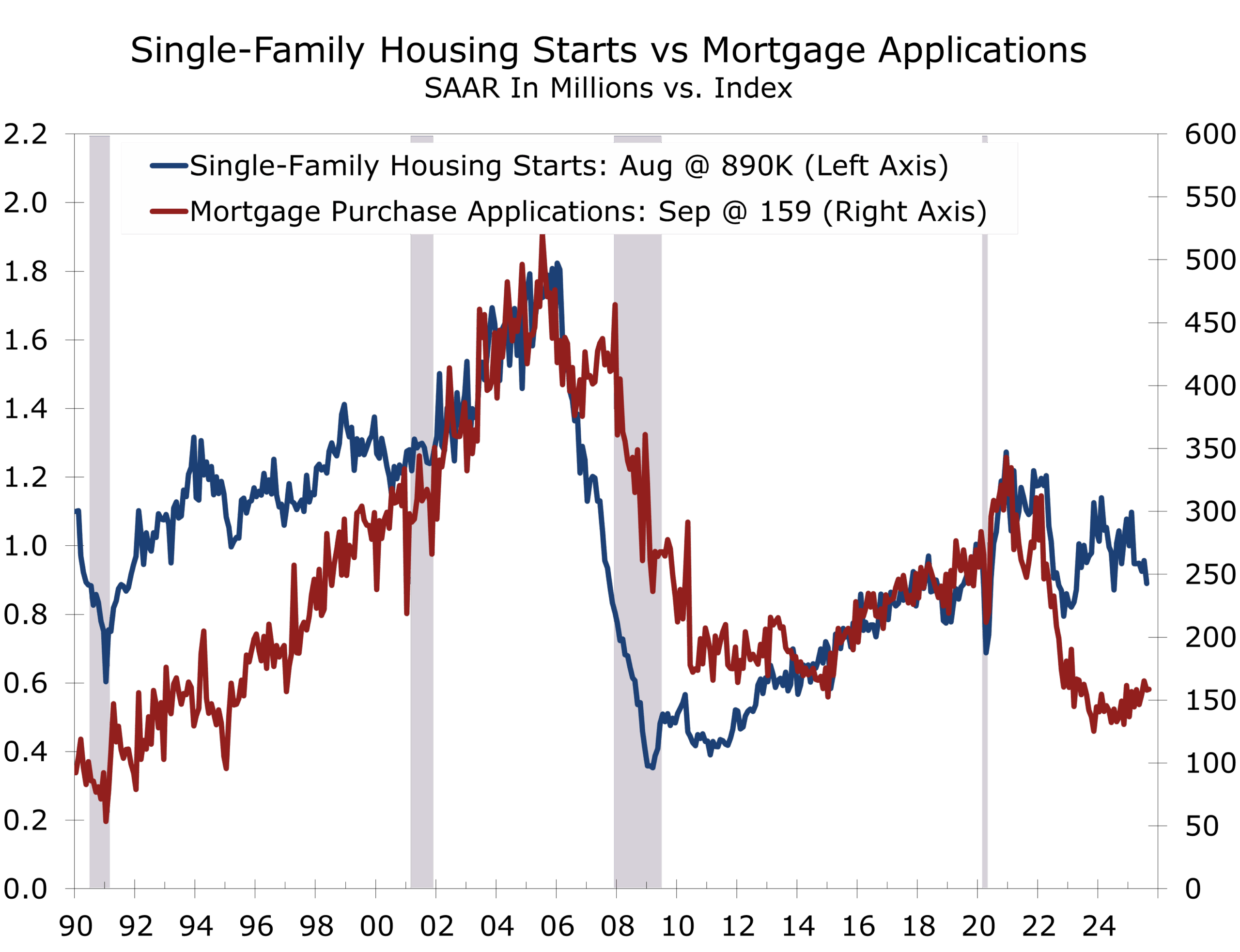

The housing data remain confounding. New-home sales surged to an annualized pace of 800,000 units in August, the strongest since early 2022. But the series is notoriously volatile and prone to revision, and the spike likely overstates the sector’s true momentum. Builders have been offering increasingly aggressive discounts and incentives to clear inventories, and the stock of completed new homes remains the highest since 2009. At August’s pace, the months’ supply of new homes fell to 7.4 from 9.0 in July, but the overhang of finished units should continue to weigh on single-family starts in the months ahead.

With affordability near 40-year lows, many potential home buyers remain on the sidelines.

Existing-home sales were little changed at an annual rate of 4.0 million units in August, slightly better than expected. Inventories slipped modestly on the month but were still up nearly 12% from a year earlier. A growing number of homeowners are delisting properties after failing to receive acceptable offers, suggesting supply could tighten into year-end. That could provide some support to prices, which edged lower in August but remain about 2% higher than a year earlier. The National Association of Realtors estimates the average homeowner has gained nearly $141,000 in equity over the past five years, but much of that wealth remains locked in place by the “golden handcuffs” of ultra-low mortgage rates.

Sticky Inflation, Uneven Spending

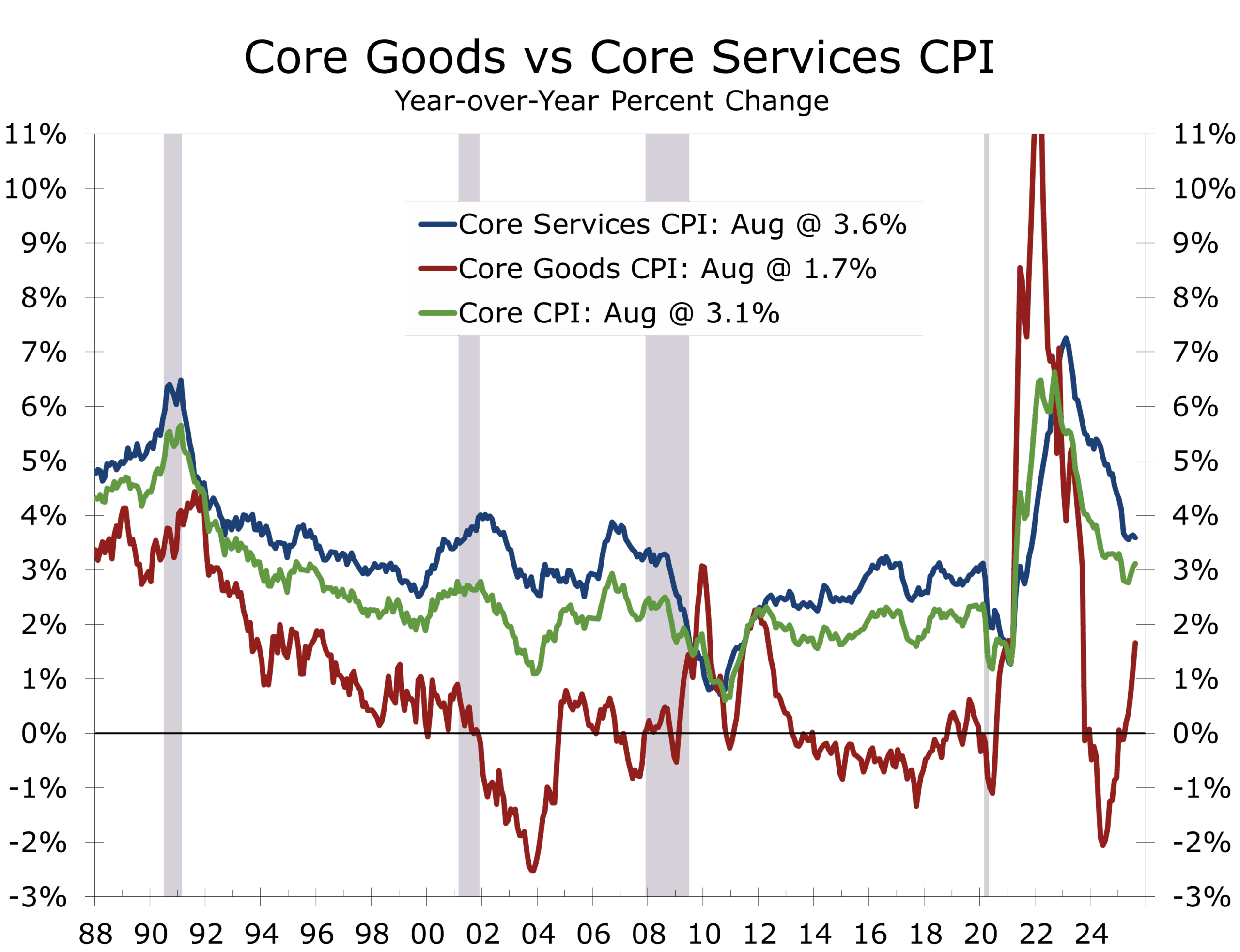

Inflation remains sticky but is gradually easing. Core PCE rose 0.2% in August, leaving the year-over-year rate at 2.9%, while headline PCE held at 2.7%. The distinction between headline and core remains critical: energy prices have been subdued, but tariffs are keeping core goods inflation firmer than it otherwise would be. Excluding tariffs, underlying inflation would likely be closer to 2.5%.

The real story lies in services. Core services inflation has steadied near 3.6%, with shelter costs gradually decelerating but still elevated. Excluding housing, services prices are running closer to 3.0%, underscoring persistent stickiness in categories such as insurance, healthcare, and transportation. This is why the Fed continues to emphasize services ex-housing as the clearest gauge of whether inflation is truly on track toward target.

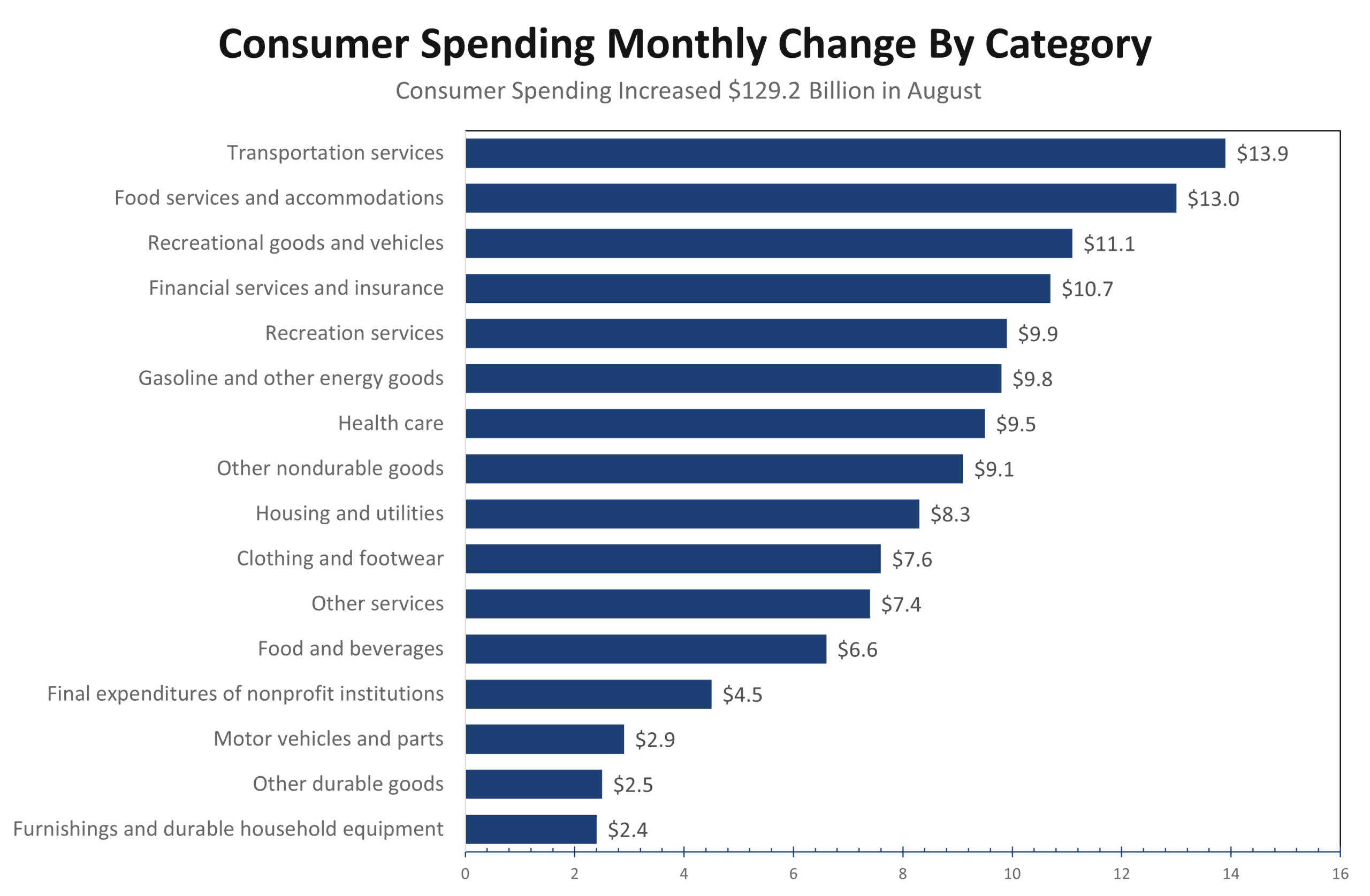

On the spending side, momentum remains solid. Real personal consumption expenditures rose 0.4% in August, with prior months revised higher. The revisions also lifted estimates of household income, reinforcing the view that consumer resilience is increasingly “top heavy.” Affluent households, buoyed by equity and real estate wealth, continue to spend freely on discretionary categories such as travel, dining, and financial services. By contrast, middle- and lower-income households remain stretched by persistent inflation in everyday necessities like groceries, rents, and insurance.

Consumer resilience is increasingly top heavy, with affluent households driving growth.

This mix supports a cautious Fed. Inflation is cooling, but not fast enough to justify a faster rate-cut path, especially with spending still resilient. Measured inflation may tick somewhat higher in the near term before drifting lower and converging toward the Fed’s 2% target in 2026.

Markets Constructive, Long End Costly

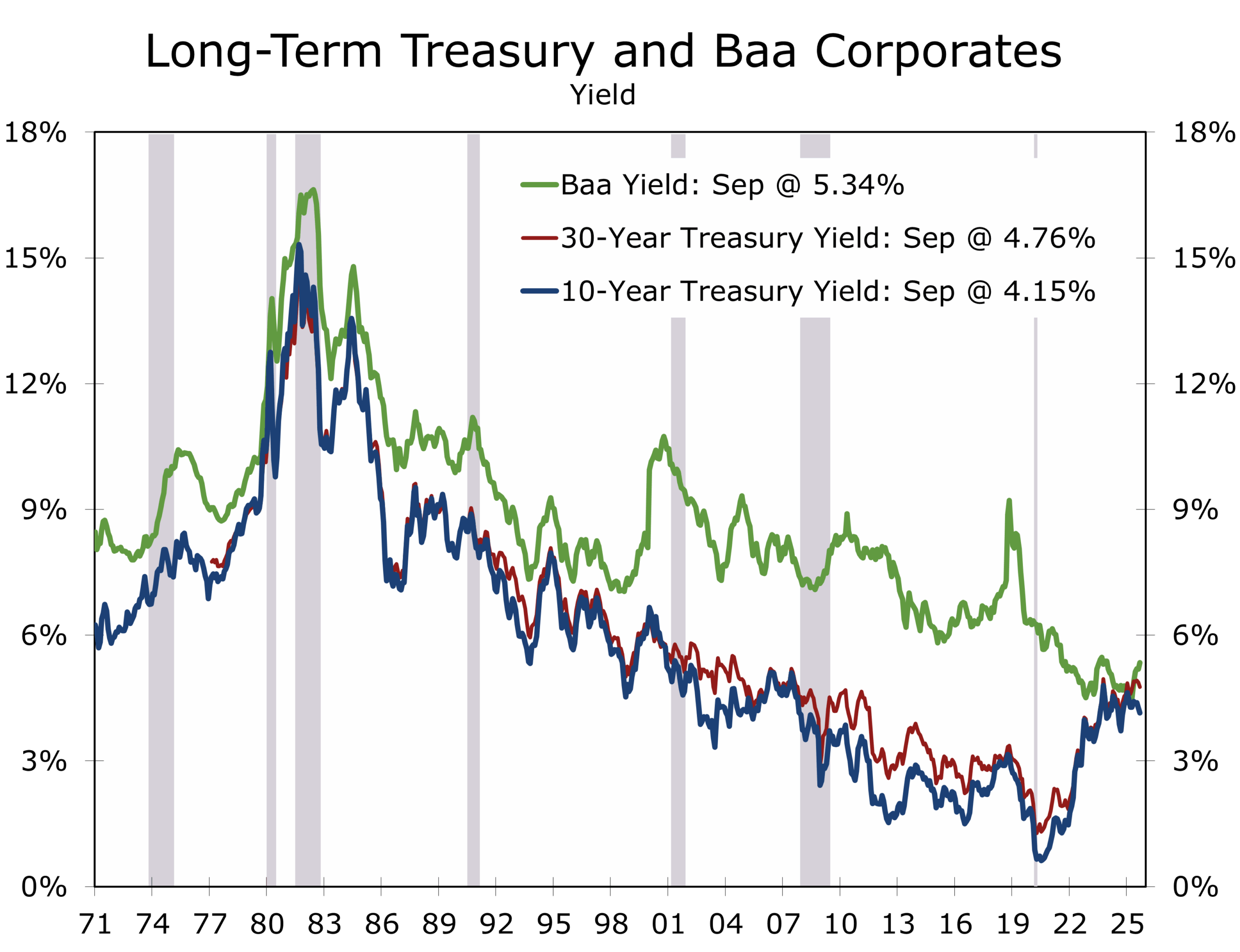

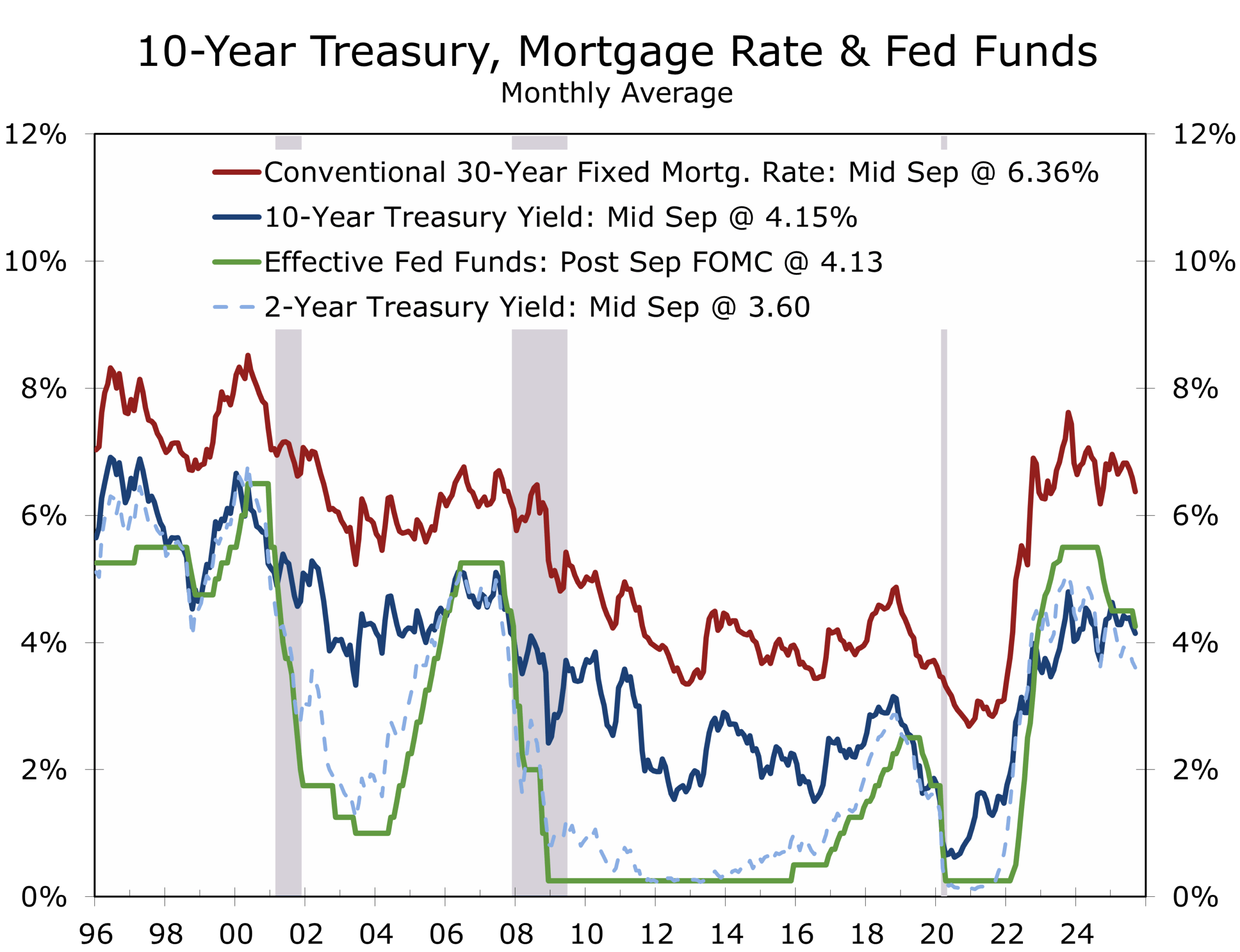

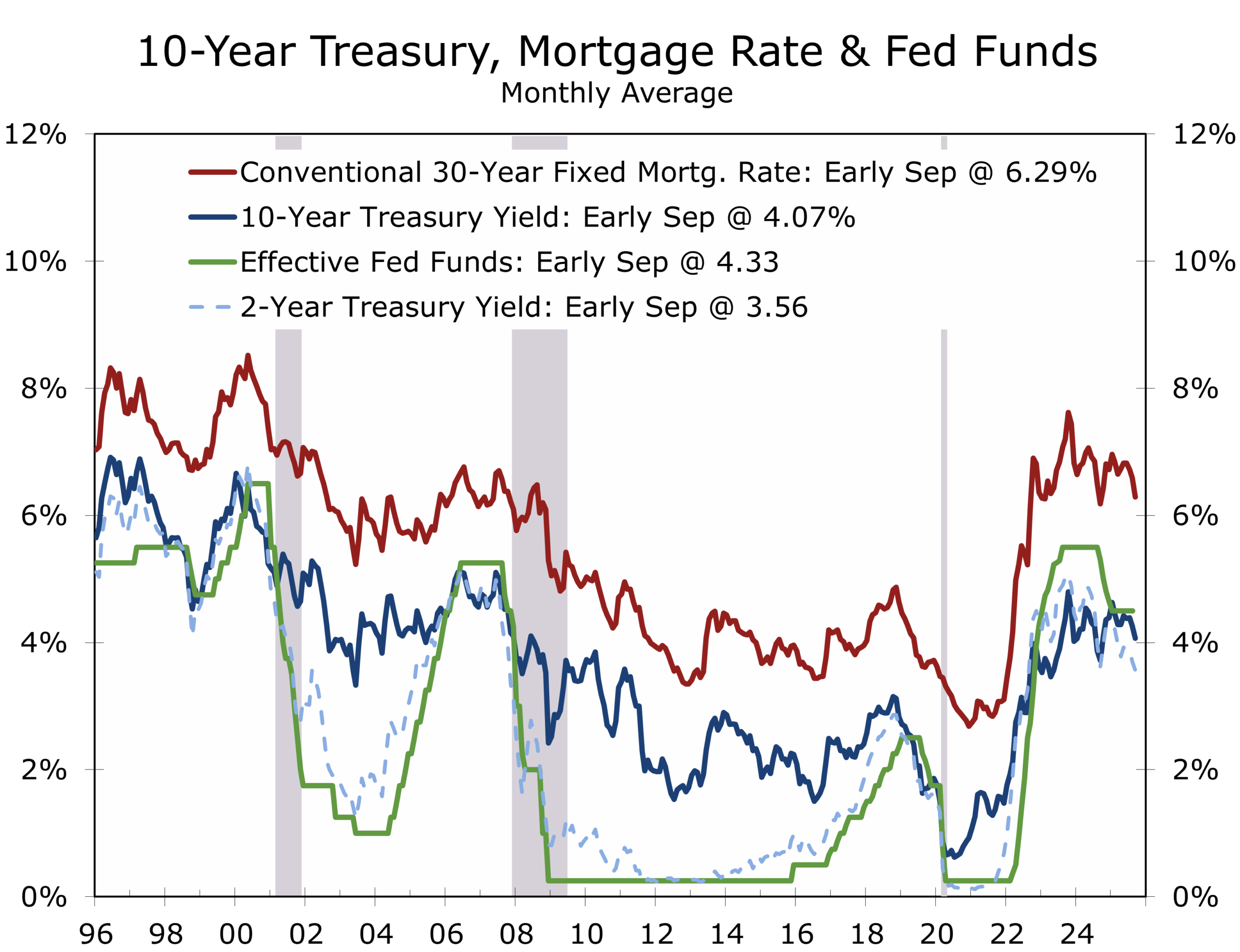

Treasury yields drifted higher last week, with the 2–7 year sector up 8–10 bps as markets unwound near-term easing bets. Repo rates showed the usual quarter-end firmness, and effective fed funds inched higher — evidence of underlying money-market tightness as quarter-end approaches. Longer maturities were steadier, leaving the curve slightly flatter and reinforcing the sense that near-term policy repricing is doing most of the work.

Credit markets remain constructive. Investment-grade spreads are holding near cycle tights, supported by healthy corporate balance sheets and steady demand. Curve dynamics are unusual, however. The back end of corporate spread curves has flattened, even modestly inverted in some cases, reflecting technical factors such as pension and insurer demand and limited issuance. Importantly, this does not signal rising default risk. For CFOs, the message is that all-in long-end funding costs remain elevated — not because spreads are widening, but because Treasury yields at the back end are still high. That leaves liability-driven investors active, but keeps opportunistic issuance focused in shorter maturities.

Geopolitics & Policy: Escalation Ladders, Energy Arithmetic, and the Dollar’s Two Tracks

Russia-NATO tensions are climbing the escalation ladder. Analysts mark up the probability of military incidents spilling into sanctions enforcement and energy logistics, with a 40% chance of broader Ukraine escalation into Q4. Expect tighter sanctions enforcement on Russian energy flows and a tactical bias toward oil strength before gold reasserts its role as a safe haven over 12 months.

On China, stimulus paired with a 15th Five-Year Plan growth target around 5% per annum would put a floor under activity, but U.S. and EU measures are likely if Moscow presses its advantage. Expect Washington to tighten sanctions on Russia first, while dangling tariff relief for allies to manage coalition politics.

Stikes on Russian energy infrastructure and tighter sanctions likely to lift oil and distillates.

The Middle East remains combustible but less likely to erupt into a region-wide war. Israel is still seaking a knockout punch against Hamas, which has European leaders scrambling for cover, recognizing a nonexistent Palestinian state. U.S. strategic exports and Gulf supply increases help lean against crude spikes, but distillates and logistics premia are more likely to feel the strain.

FX markets reflect the duality of dollar “dominance” versus persistent depreciation pressures. Liquidity and settlement flows anchor the dollar, but diversification by reserve managers continues. Expect USD strength on shocks but drift otherwise.

Finally, Washington gridlock is front and center. The probability of at least a short shutdown this week is high. Even absent a lapse, disbursement delays amount to stealth tightening for contractors, healthcare providers, and universities. A shutdown would also delay the monthly payroll report, reducing Fed visibility ahead of the October meeting.

Underreported Risks

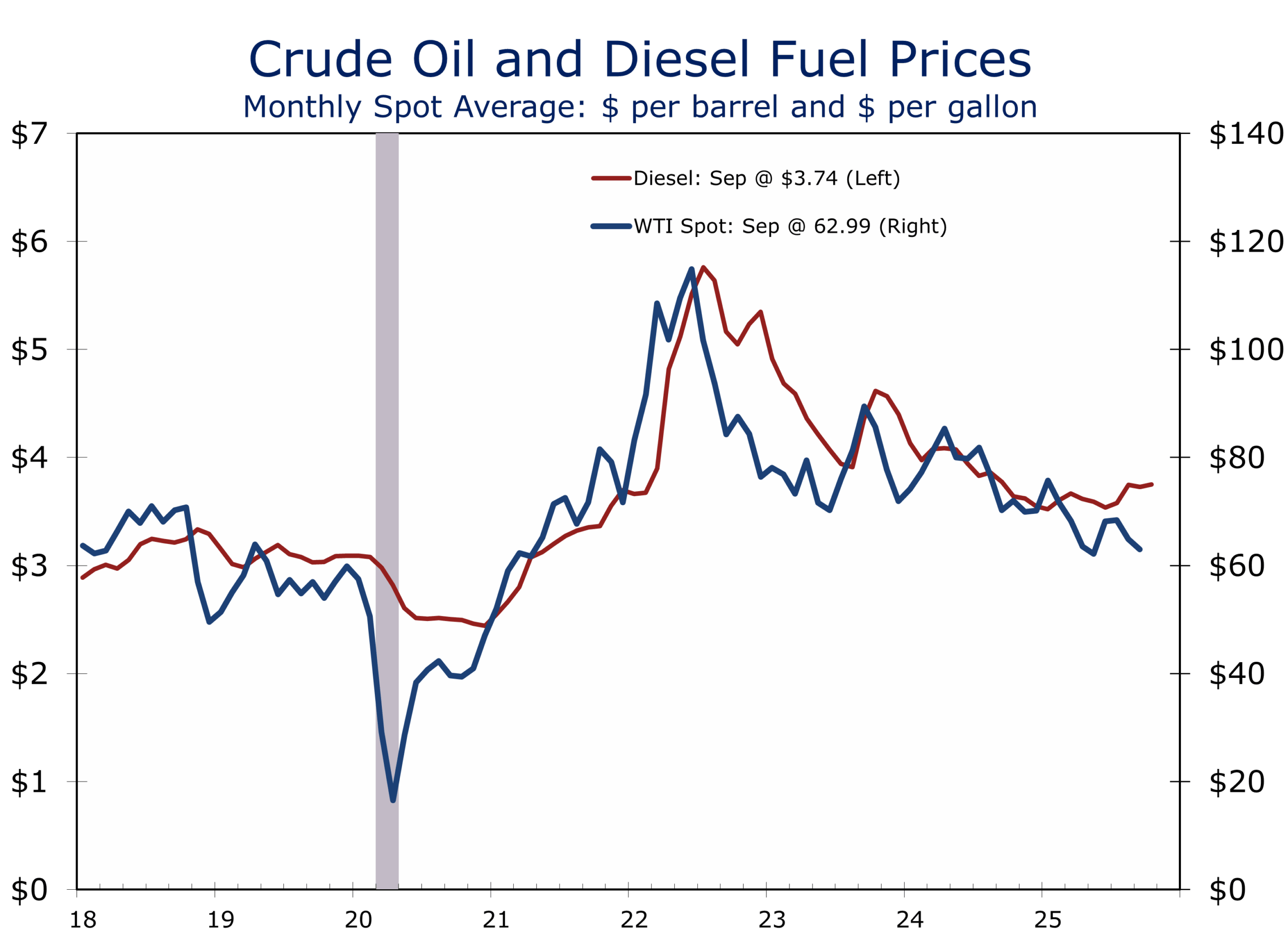

While markets focused on Washington’s budget standoff, a significant escalation unfolded at sea. Houthi forces stepped up attacks on Israel, hitting a hotel in Eilat, and on commercial shipping in the Red Sea, resuming a campaign that had eased earlier in the summer. Insurance premia are rising again, rerouting costs are mounting, and the risk of further disruptions to global supply chains is material. Unlike headline crude, the more immediate impact is likely to show up in diesel and freight markets, where margins are already tightening.

Beyond the Middle East, GPS jamming incidents in the Baltic and stepped-up Ukrainian strikes on Russian refineries are adding to global logistics pressure. Together, these developments highlight a vulnerability that often escapes market attention: the security of supply chains and transport corridors. For corporates, the lesson is to stress-test exposure not just to headline oil shocks but to refined product shortages, shipping insurance costs, and transit disruptions that can ripple quickly into working capital and inventory management.

The Week Ahead

- Monday: White House meeting with congressional leaders on funding; Pending Home Sales, Dallas Fed manufacturing survey.

- Tuesday: Consumer confidence, S&P Case-Shiller Home Prices, and JOLTS .

- Wednesday: ADP employment, ISM manufacturing, construction spending and light vehicle sales.

- Thursday: Jobless claims, Challenger layoffs, factory orders.

- Friday: September payrolls (subject to shutdown), ISM services.

Shutdown brinkmanship is the wild card. A short lapse would delay payrolls and complicate the Fed’s decision-making. Meanwhile, energy and shipping risks keep distillates and logistics costs in focus more than headline crude.

Resilience vs Risk

The contrast between Washington’s gridlock and the private economy’s Goldilocks resilience is striking. GDP revisions and PCE data show private demand powering ahead, while Congress edges toward dysfunction. For the Fed, this mix argues for patience: cut gradually, but avoid overcommitting. For businesses, the lesson is clear — the private economy is adapting and expanding, but execution risk from Washington remains a wild card.

The economy does not simply grow — it constantly evolves. Today, it is evolving in two directions: private-sector strength and public-sector paralysis. Which side dominates in the quarters ahead will determine whether Goldilocks prevails or gridlock takes its toll. We believe Goldilocks will prevail and are encouraged that Congress has passed all its appropriation bills ahead of the fiscal year-end — something not seen in decades.

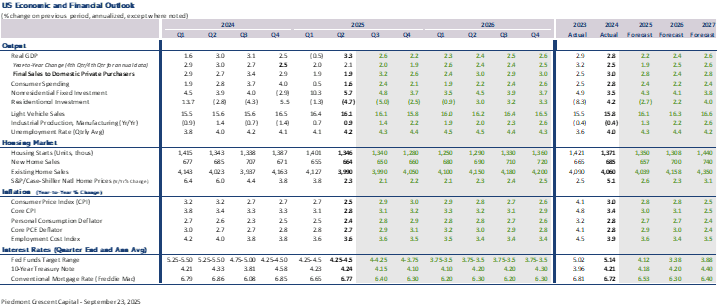

We have updated our forecast to incorporate the latest GDP data and annual revisions. Real GDP is now expected to rise at a 3% annual rate in Q3, followed by a 2% pace in Q4, when trade and inventories are likely to again subtract from headline growth. Our baseline assumes quarter-point reductions in the federal funds rate at each of the next three FOMC meetings, though we are sympathetic to the case for cuts at alternating meetings. A slower cadence would extend the easing cycle and better align with the timeline needed to foster a more sustainable recovery in home sales and new construction — allowing home prices, interest rates, and incomes to gradually move back into buyers’ favor.

We have updated our forecast to incorporate the latest GDP data and annual revisions. Real GDP is now expected to rise at a 3% annual rate in Q3, followed by a 2% pace in Q4, when trade and inventories are likely to again subtract from headline growth. Our baseline assumes quarter-point reductions in the federal funds rate at each of the next three FOMC meetings, though we are sympathetic to the case for cuts at alternating meetings. A slower cadence would extend the easing cycle and better align with the timeline needed to foster a more sustainable recovery in home sales and new construction — allowing home prices, interest rates, and incomes to gradually move back into buyers’ favor.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

September 29, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

Sticking with Our Touch and Go Scenario

Sticking with Our Touch and Go Scenario: A Stronger but Uneven Expansion

- Growth Surprises to the Upside: The U.S. economy is tracking 2.6% Q3 GDP growth, well above midyear expectations, confirming a rebound after a slowdown following the rollout of tariffs.

- Survey Signals Lower Recession Odds: CNBC’s September Fed Survey places the probability of recession over the next 12 months at 40%, up from 31% before the July 31 FOMC meeting but broadly in line with the prior four meetings. We put recession odds closer to 30%, reflecting recent soft employment data but resilient consumer spending.

- Consumers Driving Q3: Retail sales in July and August were stronger than expected, but spending is being driven predominantly by higher-income households while lower-income segments show rising financial stress.

- AI and Aerospace Lead Investment: Massive AI infrastructure buildouts and a surge in aerospace and defense spending are offsetting weakness in other sectors and driving productivity gains.

- Housing Remains Weak: Housing starts fell in August, and inventories of new homes are at their highest since 2009, delaying a sector recovery until mid-2026.

- Inflation Progress, but Tariffs Complicate: Core CPI rose 0.3% in August as tariffs pushed up goods prices, while services inflation remains well-behaved and expectations stay anchored.

- Messaging Matters: The Fed has to get its messaging right and may be able to accomplish more by doing less. Long-term yields are more likely to remain contained if the Fed avoids appearing politically driven while keeping expectations measured. Post-FOMC speakers largely share this view.

- Geopolitical Flashpoints Rising: Conflicts in Gaza and Ukraine, European recognition of Palestine, and sharper U.S. pressure on allies highlight rising risks to global stability.

Outlook: Growth Holding, Recession Risks Persist

The U.S. economy continues to outperform expectations, defying the cautious outlooks that dominated the summer. The Atlanta Fed’s GDPNow model currently tracks 3.9% for Q3—a sharp improvement from earlier forecasts near 2% and well above private estimates that initially carried a “1-handle.” Our own forecast is more measured, with Q3 at 2.6% and Q4 at 2.2%. For 2025, we project 1.9% growth, fourth quarter-to-fourth quarter, rising to 2.5% in 2026 as interest rates ease and fiscal tailwinds take hold.

The CNBC Fed Survey is more cautious, pegging Q3 at 1.9% and Q4 at 1.4%, with full-year growth of 1.5% in 2025 (Q4/Q4) and 2.0% in 2026. Many of those forecasts were submitted before the stronger mid-September retail sales report for August, which lifted near-term consumption estimates. The divergence between official trackers, survey consensus, and our own forecast highlights just how fluid this expansion remains.

Underlying data confirm the uneven nature of growth. Consumer spending and business investment are carrying the economy, but the breadth of hiring is narrowing, and housing remains stuck in neutral. That mix has allowed GDP to look healthy even as cracks appear below the surface. Strong productivity gains linked to AI and aerospace are buying time, but they are not yet broad enough to ensure a durable cycle on their own.

We have said repeatedly that if the economy could avoid slipping into recession through the summer and early fall, it would likely be fine. That outlook remains intact. The near-term risk of a downturn has diminished as growth has accelerated, but the recovery is still fragile. The economy has momentum, but it remains vulnerable to policy mistakes, external shocks, and the risk that tariff-related price pressures linger longer than expected.

This dynamic fits our “Touch and Go” framework outlined in earlier reports. The economy slowed sharply earlier this year, briefly touched down, and is now climbing again. The question is whether it can gain enough lift to reach cruising altitude or whether turbulence forces another pass. The uneven distribution of strength across sectors makes this one of the most complex expansions in recent memory.

Recession risks are diminished but not extinguished. Policy should focus on broadening the recovery—through labor-market participation, housing affordability, and infrastructure channels—rather than assuming resilience in a few sectors will carry the cycle indefinitely.

Consumers: Resilience Amid Uneven Labor Markets

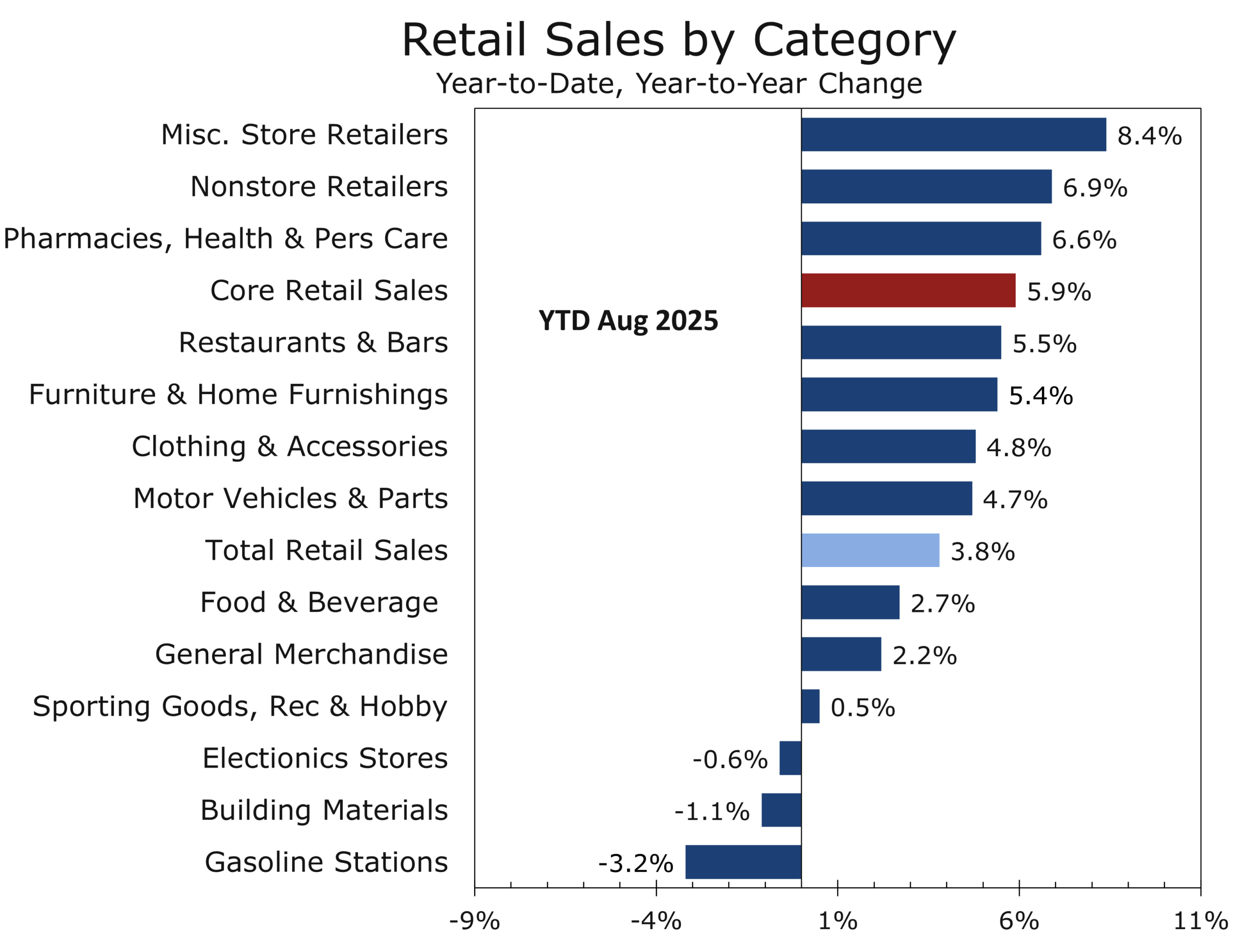

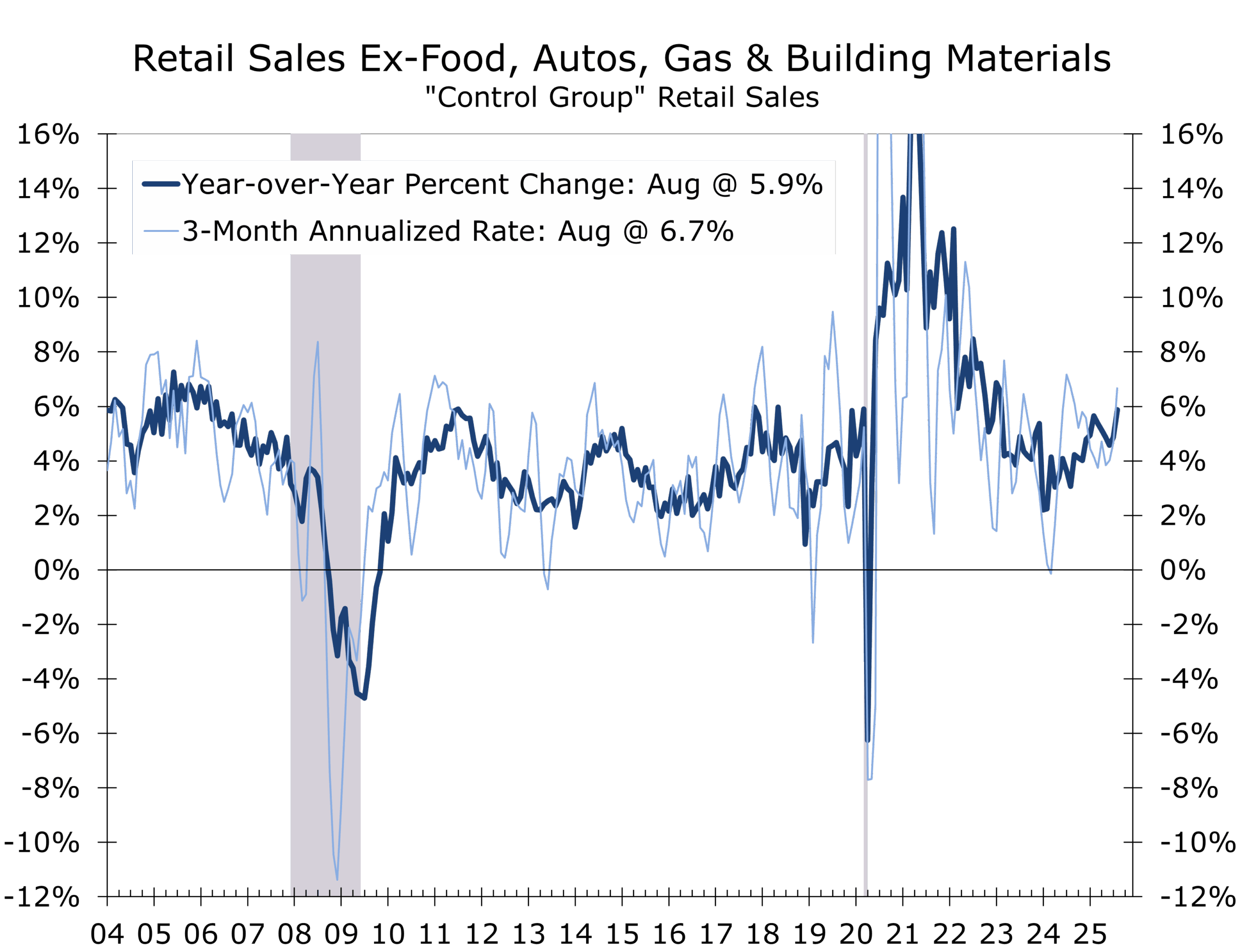

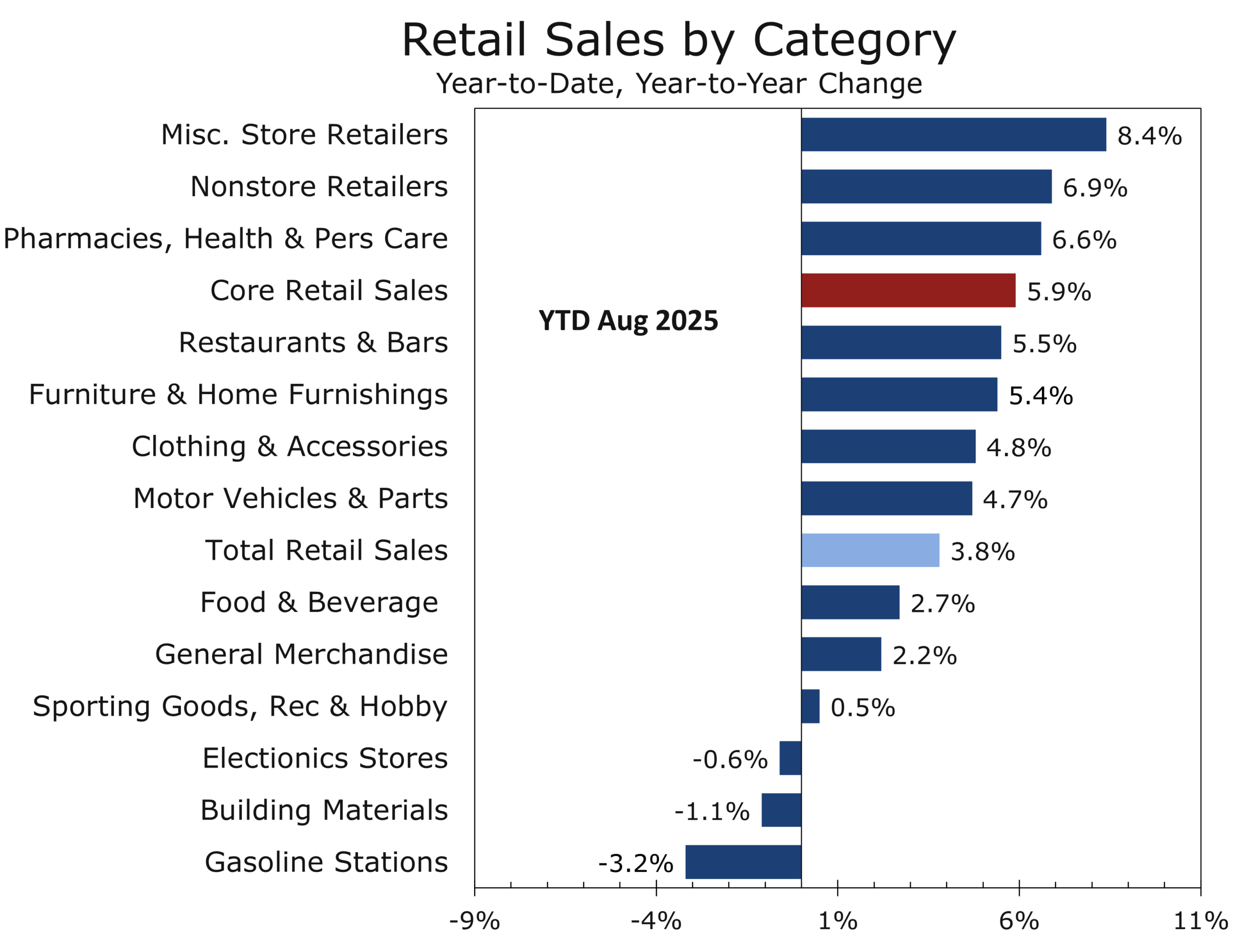

Consumer spending remains the backbone of the rebound. August retail sales rose 0.6%, while July was revised up to 0.5%, following June’s 0.9% jump. Gains were broad-based: non-store retailers +2.0%, clothing +1.0% (a strong back-to-school season), and food services +0.7%. We estimate real core retail sales rose 0.5% in August and are running at a 5.5% three-month annualized pace, placing Q3 consumption growth well north of 2% annualized and providing upside risk to GDP.

The resilience is clearly bifurcated. Higher-income households—roughly one-fifth of the population but responsible for more than two-fifths of spending—continue to fuel discretionary categories such as dining, travel, recreation, and e-commerce. Their balance sheets remain healthy, supported by wealth gains from equities and home values. In contrast, middle- and lower-income households are increasingly pressured by higher borrowing costs, tariff-driven price increases, and a softening labor market. Rising auto and credit-card delinquencies are early warning signs that stress is mounting.

The labor market’s narrowing breadth amplifies the divide. The employment diffusion index has slipped below 50, showing that job gains are concentrated in just a handful of sectors—health care, aerospace, and leisure/hospitality—while hiring in many other industries has stalled. Real disposable income growth is slowing as wage gains moderate and pandemic-era savings are nearly depleted. Sentiment surveys capture the fragility, with households citing tariffs, borrowing costs, and job security as top concerns.

While consumer spending will keep Q3 GDP afloat, the expansion is becoming increasingly top-heavy. Deferred purchases and pent-up demand are still providing a lift, but without broader labor-market gains and relief for financially stretched households, aggregate demand risks losing momentum heading into 2026—underscoring why the Fed has placed greater emphasis on supporting the labor market.

Business Investment: AI and Aerospace Take the Lead

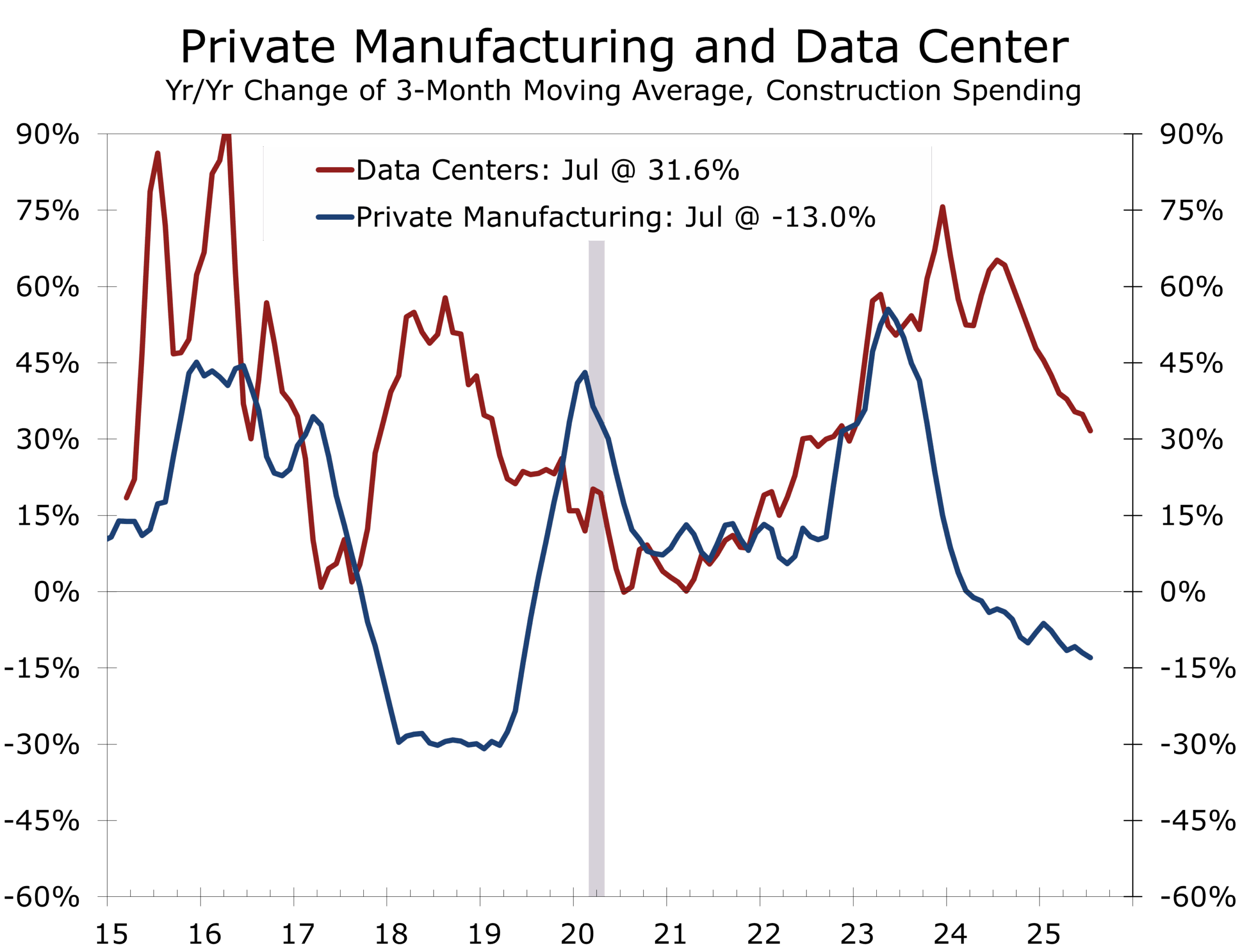

The defining story of this cycle is the rise of artificial intelligence infrastructure and aerospace/defense as the dominant engines of business investment. Data-center construction is expanding at a record pace, with spending up more than 30% y/y and accelerating. Corporate outlays on high-tech equipment—servers, GPUs, and networking systems—are surging, with some subcategories growing more than 40% y/y. AI-related spending could exceed $350 billion in 2025, directly adding around 0.5 percentage point to GDP growth and potentially closer to a full point in 2026 as adoption broadens. More importantly, these investments are reviving productivity, the foundation for long-run growth.

The impact is not confined to Silicon Valley. Mega-projects are reshaping regional economies from Northern Virginia’s data-center corridor to new builds in Texas, Arizona, and across the Southeast, driving demand for skilled labor, energy infrastructure, and industrial construction. These localized booms are creating new growth corridors and reinforcing America’s competitive edge in emerging technologies.

Aerospace has re-emerged as the second growth pillar. Commercial aviation is supported by record backlogs at Boeing and Airbus, while defense budgets are lifting demand for advanced fighter jets, drones, and space-based systems. Aerospace exports are cushioning the drag from weaker auto sales and softer consumer-goods manufacturing, keeping industrial output on firmer footing.

Together, AI and aerospace have kept nonresidential investment positive even as office construction, energy exploration, and other manufacturing activity weaken, following a tax-incentive and stimulus driven surge. These sectors are acting as stabilizers, preventing the economy from losing altitude and giving policymakers a wider margin of safety.

Investment strength is effectively raising the economy’s speed limit—but execution will matter. Permitting, power generation, and transmission capacity will need to expand alongside workforce pipelines to translate record capex into durable productivity gains. Without this support, investment could lose momentum as bottlenecks mount.

Housing: A Sector Stuck on the Ground

Housing remains the weakest sector of the economy, weighed down by both structural and cyclical headwinds. After a brief rebound in July, August housing starts fell 8.5% and permits dropped 3.7%, leaving them more than 11% below year-ago levels. Inventories of new homes have risen to a 9.3-month supply, the highest since 2009, prompting builders to slow starts and focus on clearing speculative units already on the market. Discounts and incentives are increasingly being used to move this excess stock, particularly in the South and West where building had been most aggressive.

The two biggest impediments to a healthier housing recovery are clear. First, a lack of affordable product continues to lock out entry-level buyers. Elevated home prices, combined with higher insurance costs and property taxes, leave few options for households trying to buy at the lower end of the market. Second, slowing job growth has reduced relocations, traditionally a major driver of home sales and construction in fast-growing regions. The cooling labor market has blunted one of housing’s most reliable sources of demand.

Meanwhile, the inventory of existing homes remains historically tight, as many owners are reluctant to sell and give up sub-4% mortgages. This limits buyer choice in the resale market and keeps pricing pressure elevated even as demand has softened.

Taken together, these dynamics leave housing unlikely to contribute meaningfully to GDP growth before mid-2026. At best, the sector may move from drag to neutral in 2025 as builders finish working through their backlog of spec homes and inventories gradually normalize. Mortgage applications have picked up as conventional mortgage rates briefly fell back to 6%, which should lift new home sales this fall. Inventories will have to fall back to historic norms before construction ramps up again, which is unlikely until spring or summer 2026.

Inflation: Tariffs Complicate the Descent

The disinflation trend has slowed but has not reversed. Headline CPI rose 0.4% in August (2.9% y/y), while core CPI increased 0.3% (3.1% y/y). Goods inflation, which had been easing for much of the past year, has re-firmed as tariff-related costs work their way through supply chains. By contrast, services inflation has leveled off near 3.6%, still above the Fed’s target but no longer accelerating. Market-based expectations remain stable, with the five-year/five-year forward inflation swap at 2.4%, broadly consistent with the Fed’s long-run objective.

Tariffs remain the wild card. Participants in the CNBC pre-FOMC Survey generally expect tariffs to generate “somewhat more” price pressure but not a broad-based spiral. This aligns with the Fed’s stance of looking through tariff-driven goods inflation while focusing on underlying trends in rents, wages, and services. Powell and other policymakers have made clear they will not react to every tariff-induced bump but will monitor whether these pressures risk becoming embedded.

The greatest risk is persistence. If tariffs remain in place long enough to alter corporate price-setting behavior—or if firms use them as cover to widen margins—the final leg of disinflation becomes harder to achieve. Already, some categories of durable goods, such as washer machines, are showing firmer prices despite slowing demand. On the other hand, wage growth has cooled, labor demand is narrowing, and shelter inflation is steadily grinding lower as new supply filters into the market. These forces suggest that underlying inflation is still on a gradual downward path.

The Fed has some room to continue easing cautiously, but credibility depends on expectations staying anchored. If households or businesses begin to doubt the Fed’s ability to contain inflation, long-term yields could rise even as policy rates fall. Trade policy will be just as important as monetary policy in the months ahead: avoiding new supply frictions in goods, energy, or labor markets is essential to sustaining disinflation without sacrificing growth.

Monetary Policy: Powell’s Risk-Management Pivot

The Fed cut 25 bps in September to 4.00%–4.25%, calling it a “risk-management” step to cushion labor-market risks without reigniting inflation. Chair Powell emphasized that slower hiring reflects narrowing job growth across the economy, not weakness in a single sector. With consumption increasingly dependent on higher-income households, stabilizing employment is now as critical as sustaining disinflation.

Markets expect two more cuts by year-end, with our baseline including a third in January before a pause as growth steadies into spring 2026. The Committee may stretch the cycle—cutting in December, March, and June—but the direction is clear.

Divisions within the FOMC remain. Governor Stephen Miran dissented for a 50 bps cut and reaffirmed his 2025 dot of 2.75%–3.0%, underscoring the doves’ call for faster action. St. Louis Fed President Alberto Musalem supported the September cut but warned against pre-committing, arguing that inflation expectations—not just labor data—should drive decisions. He signaled that two more cuts this year could be excessive without a sharper slowdown. Atlanta Fed President Raphael Bostic reinforced the cautious view, stressing that the Fed must not “overshoot on the downside” and reignite price pressures, calling instead for patience and balance while guarding against political influence.

Much of the easing path is already priced, leaving limited scope for further repricing absent clearer labor-market deterioration. The dollar has remained firm despite political noise, reflecting the U.S.’s relative growth and yield advantage even as policy begins to ease.

The Fed has to get its messaging right and may be able to accomplish more by doing less. Long-term yields are more likely to remain near their current low levels if markets believe policymakers are not bending to political winds at a time when headline inflation is rising. By setting expectations deliberately low—through the dot plot and measured communication—the Fed reduces the risk of disappointment if inflation runs hot or the pace of cuts undershoots market hopes.

A divided FOMC raises communication risk. Consistency and data-dependence will be essential to avoid either re-inflation or a confidence shock that could derail an expansion that remains narrow but resilient.

Geopolitics

Israel’s campaign in Gaza has entered a decisive phase, with ground operations pressing into Gaza City in an effort to deliver a knockout blow to Hamas. The battlefield is shaping the diplomatic terrain: several European governments have recognized a Palestinian state—without borders or functioning institutions—reflecting humanitarian concerns and domestic political calculus. Critics in Jerusalem and Washington view this as rewarding violence while Hamas remains intact.

European leaders are balancing humanitarian aims against the risk of unrest among immigrant and diaspora communities. The recognition strains transatlantic ties but reflects domestic pressures across Europe. The Abraham Accords remain the most promising path to durable normalization and economic integration; symbolic recognitions risk hardening divisions.

In parallel, Ukraine’s refinery strikes have disrupted more than 1 mb/d of Russian capacity, exposing vulnerabilities in Russia’s domestic supply. Moscow’s attritional strategy persists, but sanctions and revenue pressures are eroding fiscal buffers. The prospect for larger disruptions is increasing, which is boosting oil and natural gas prices.

At the UN General Assembly, President Trump’s remarks were sharper than in past years. He criticized European recognitions of Palestine, pressed allies to end purchases of Russian energy, praised Ukraine’s resilience, and warned Moscow of stronger economic measures should aggression persist. He also signaled that NATO must be ready to respond to violations of allied airspace. The message was clear: Washington will lean harder on Europe to align policy, with tariffs and sanctions on the table. He further suggested he is prepared to increase support for Ukraine to retake all territory lost to Russia, “if not more.”

Democrats Can Shut Down the Government, But Not Yet. We see roughly a one-third probability of a partial federal government shutdown before November, with odds rising toward year-end. The sticking point is the $350 billion, 10-year extension of enhanced ACA subsidies. A short shutdown would have little macro impact—a temporary dip in GDP followed by a rebound when furloughed workers return—but a month-plus disruption could rattle markets at elevated valuations. Furloughs would also coincide with a wave of federal retirements this fall, risking some ugly employment prints. Past episodes suggest shutdowns can catalyze volatility in both equity and bond markets, especially amid heightened geopolitical uncertainty.

Rising geopolitical flashpoints and domestic brinkmanship elevate uncertainty for businesses and markets. Policymakers will need to balance security, humanitarian, and fiscal priorities while avoiding moves that worsen supply frictions or financial-condition volatility.

The Outlook: Narrow Strength, Rising Altitude

The third quarter has exceeded expectations, so far, underscoring the economy’s surprising resilience. If momentum carries into early Q4, near-term recession risks should ease further. By 2026, lower rates, modest fiscal support, and AI-driven productivity gains should help broaden the expansion.

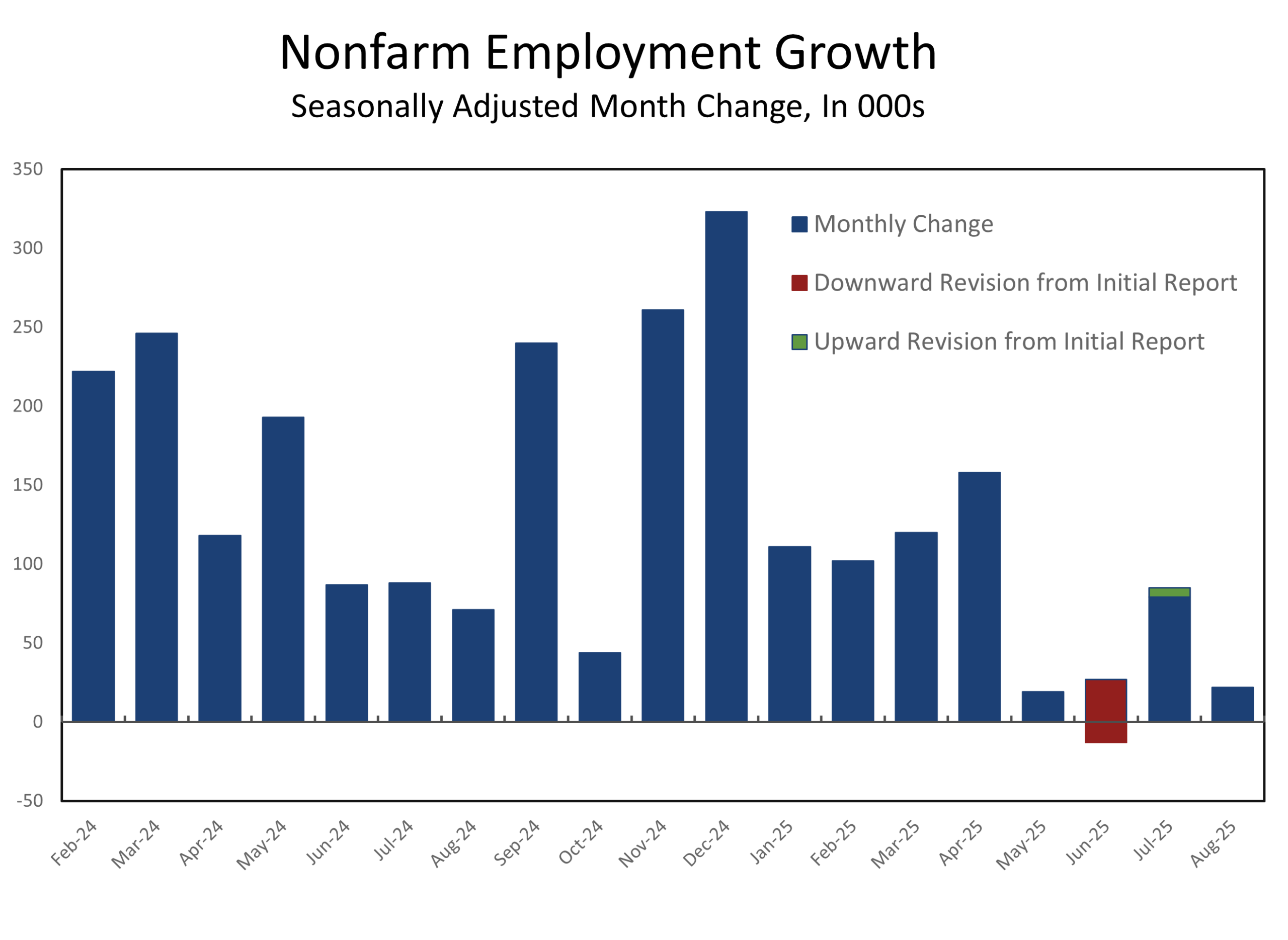

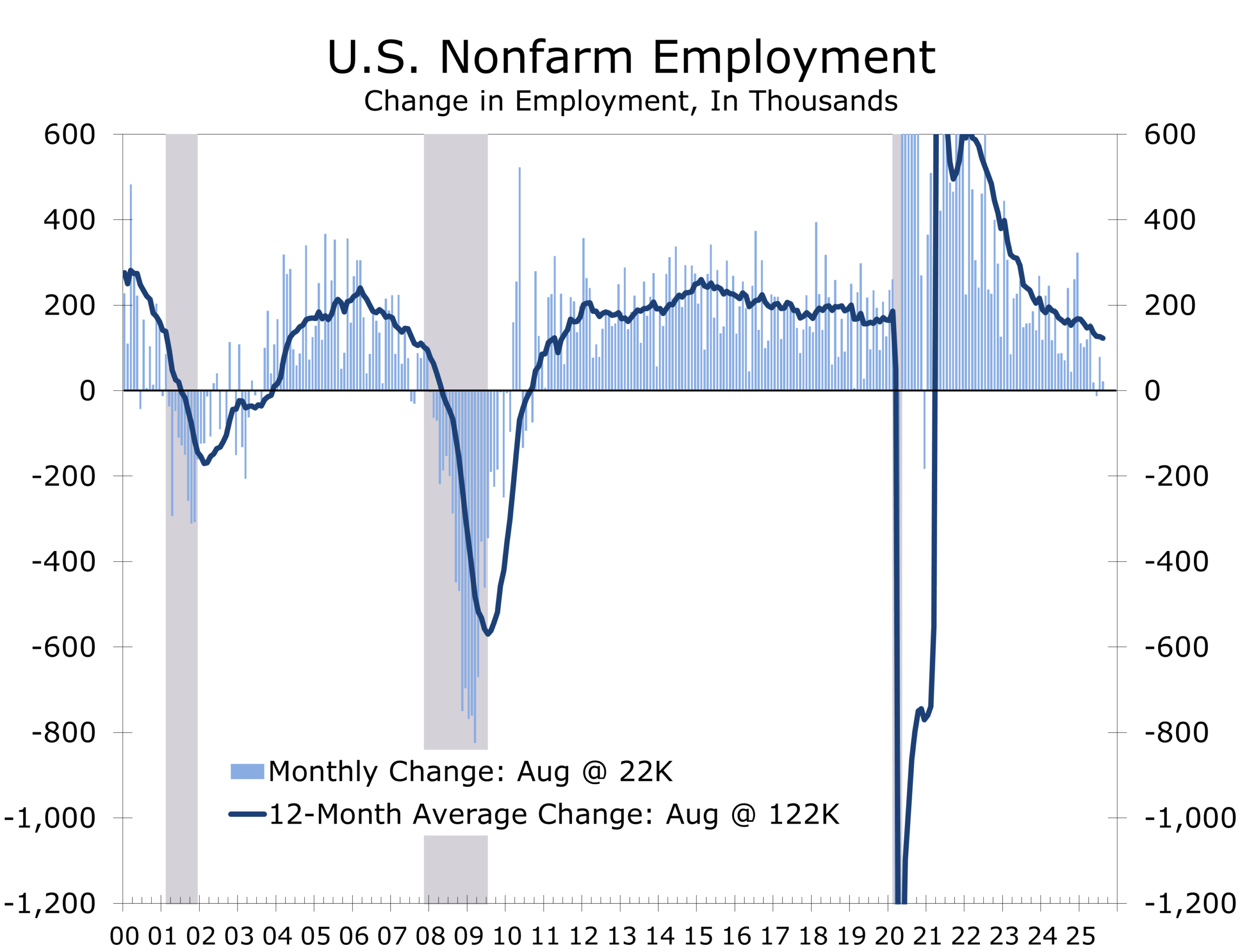

For now, growth remains uneven. Consumers—especially at the upper end—along with AI infrastructure and aerospace are providing lift, while housing, manufacturing, and many services remain soft. The labor market remains fragile, with just 22,000 jobs added in August, and gains narrowly based. This mix leaves the economy more shock-sensitive than the headline numbers suggest but also preserves upside as policy support builds. Business confidence has stabilized from earlier lows, but investment outside AI and aerospace remains hesitant, reflecting uncertainty about tariffs, regulation, and global demand. Global developments will also matter: a stronger dollar and tighter financial conditions abroad could restrain exports even as domestic drivers improve.

Resilience has bought time, but durability requires breadth. Policy should focus on bottlenecks in labor, energy transmission, and housing supply to shift the economy from “Touch and Go” to a sustained climb.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

September 25, 2025

Mark Vitner, Chief Economist

704-458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Signals in the Data, Shadows on the Global Stage

Highlights of the Week

- Economic Data Recap: Industrial production rose on autos and defense while import prices climbed on dollar weakness and firmer global goods prices; sentiment weakened. These signals point to slowing growth with lingering inflation risk.

- Retail Sales: Three straight months of gains put Q3 consumption growth on track north of 2%, providing upside risk to our Q3 GDP forecast. Stronger spending may complicate the Fed’s easing path.

- Markets: Yields eased, the dollar firmed, equities pressed higher. Markets are betting on further Fed easing.

- Fed Policy: The Fed cut rates 25bps last week and signaled more easing ahead. Our view: the Fed can accomplish more by doing less—cutting less than markets expect while anchoring confidence.

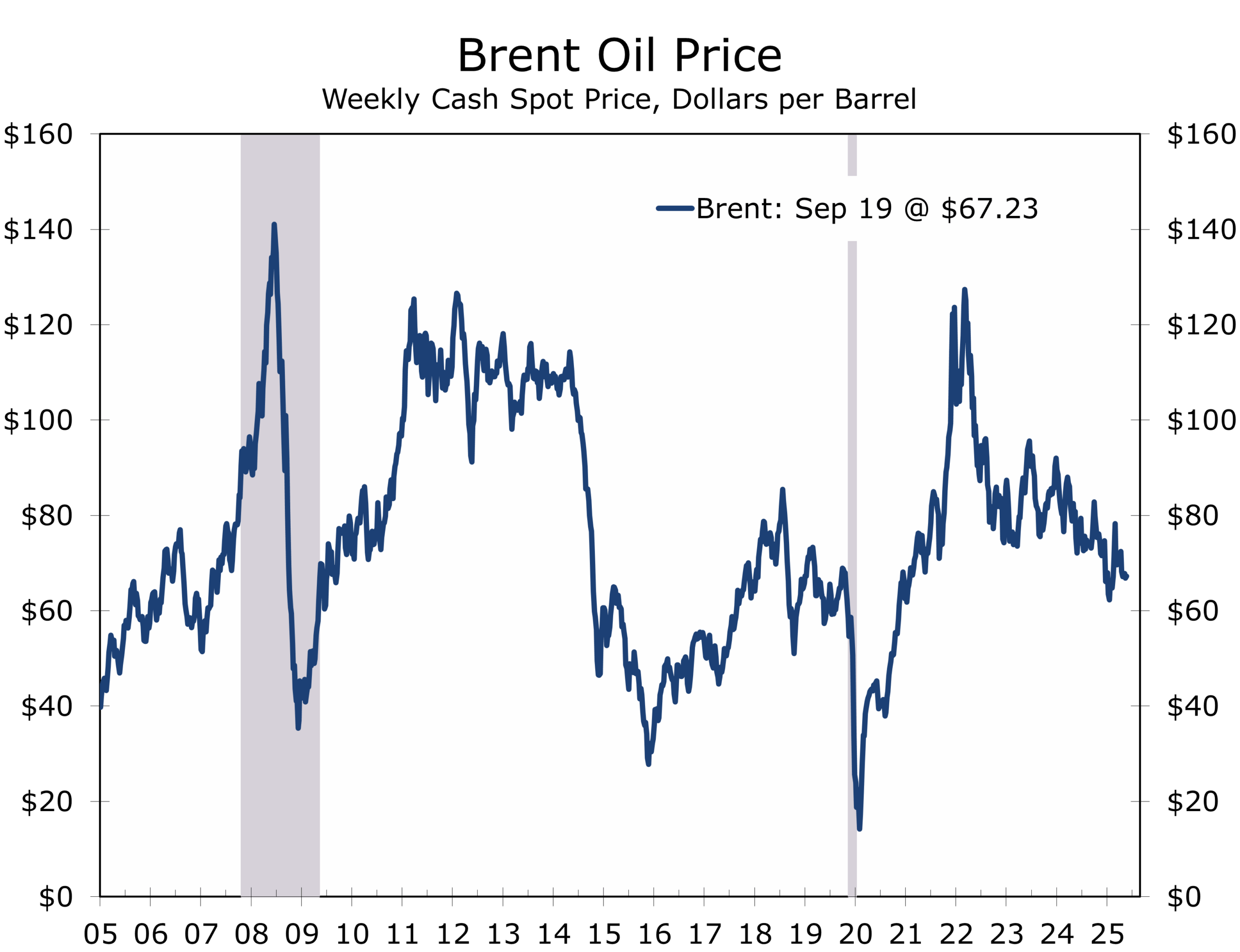

- Energy & Commodities: Brent crude remains capped near $66; gold and precious metals are firming on safe-haven demand and a softer dollar. FX markets show waning U.S. growth premium as investors rotate toward higher-yielding EM currencies.

- UN General Assembly: Fractures on Gaza, Ukraine, and climate finance highlight weak multilateral consensus. The pullback in U.S. leadership has left a void, making solutions to pressing global problems harder to achieve.

- Israel–Qatar Strike: The strike continues to resonate throughout the Middle East, expanding the conflict’s footprint, complicating Gulf unity, and raising energy security risks.

- This Week: New Home Sales on Wednesday, Q2 GDP (third estimate) Thursday; Personal Income & Outlays and the PCE deflators Friday, along with final September Consumer Sentiment.

- Trump’s Tuesday UN General Assembly Address: Will be closely watched for signals of tariff escalation and NATO burden-sharing. Trump’s rhetoric comes amid a leadership vacuum, and markets are weighing whether the U.S. is reasserting leverage or stepping further away from consensus-building

Economic & Market Recap

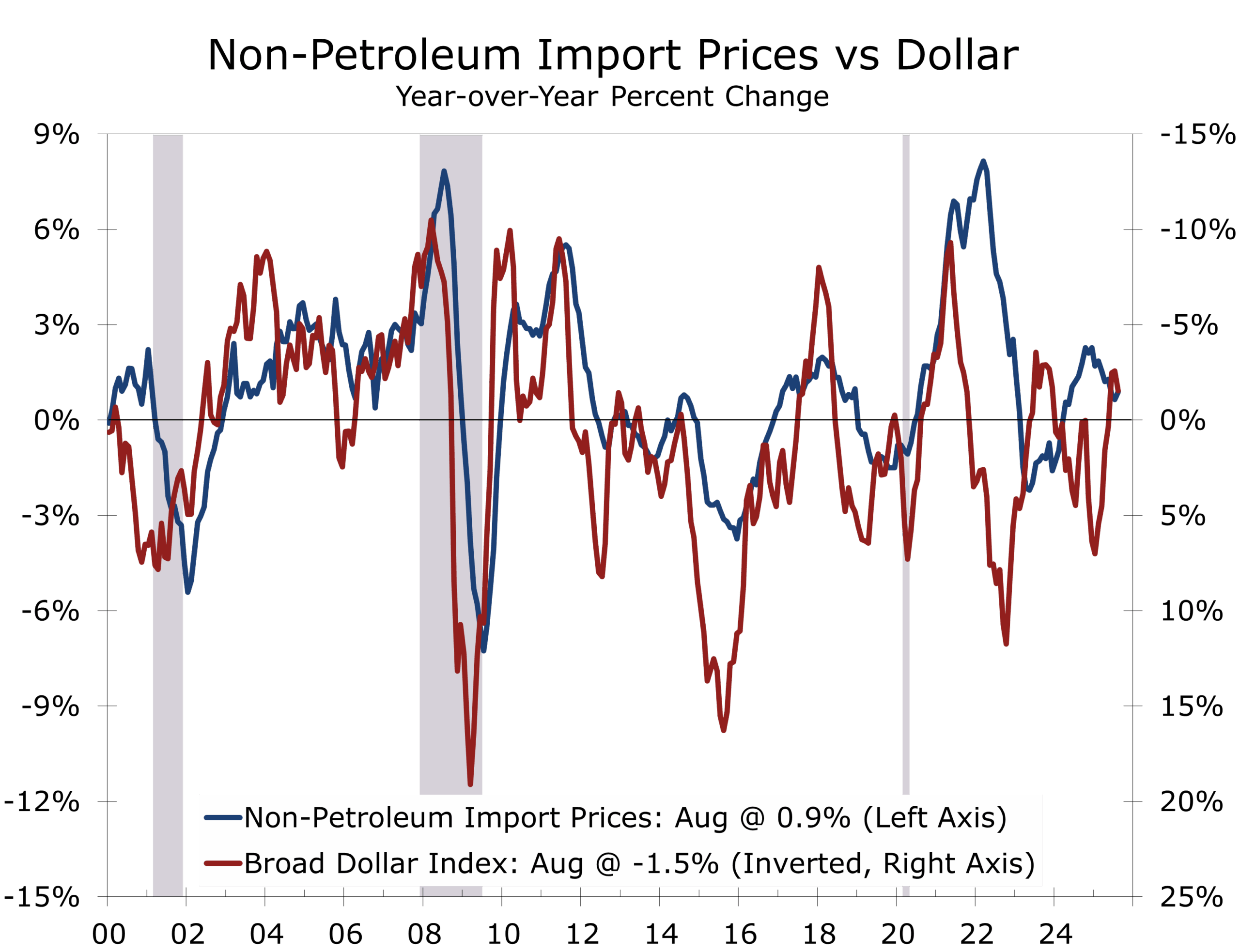

The past week’s data underscored the combination of resilient production and stubborn cost pressures. Industrial production jumped, thanks largely to auto output, underscoring that U.S. manufacturing is not collapsing under high rates. Import prices edged higher, reflecting dollar weakness and firmer global goods prices. While tariffs remain an important policy risk, they do not directly feed into the import price index, which measures values before duties are applied. The upward move nonetheless signals that a softer dollar could complicate the disinflation narrative. Consumer sentiment slipped in early September—households see risks in the job market and are less confident about income growth.

The Fed is being asked to ease policy in an environment that is not fully benign. Growth is slowing, but exchange-rate effects and global price pressures are limiting the pace of disinflation. That explains why Treasury yields fell, the dollar strengthened, and equities still found room to rally—markets are betting that the Fed has room to cut, but the path will likely not be as smooth as implied by the Summary of Economic Projections median points.

Retail Sales: A Stronger Consumer Pulse

August retail sales surprised to the upside, with headline sales rising 0.6% and core control sales up 0.7%, both well above expectations. July was revised higher to a 0.5% gain, following June’s outsized 0.9% increase—underscoring that momentum has carried through the summer. Gains were broad-based: motor vehicles and gasoline each rose 0.5%, while non-store retailers led with a 2% jump. Clothing sales advanced 1%, signaling a strong back-to-school season and offering a positive precursor to holiday spending. Real core retail sales likely climbed 0.5% in August and are running at a robust 5.5% pace on a three-month annualized basis.

The recent string of buoyant retail sales reports provide upside risk to Q3 GDP forecasts.

This resilience has important implications for the broader economy. Consumption had been a soft spot earlier this year, weighed down by weaker discretionary categories and fading sentiment. Three straight months of gains, however, suggest spending has rebounded more quickly than expected from the midyear slowdown. Consumers may also be making up for purchases deferred in the spring, when the economy appeared more fragile.

The stronger retail sales data also provide upside risk to Q3 GDP. While part of the recent strength reflects higher goods prices as tariffs and import costs filter through, real spending is still advancing. The rebound in discretionary categories such as dining and recreation highlights that higher-income households—who account for the bulk of spending—remain in solid shape, even as lower-income households face pressure from a softening labor market and higher living costs.

For the Fed, the message is nuanced. The resilience of consumer spending will bolster confidence that growth is holding up even as labor market conditions cool, reinforcing the case for a gradual approach to easing to support the labor market. At the same time, stronger demand complicates the disinflation narrative, particularly if robust consumption sustains pricing power in services. Markets may need to temper expectations for the pace of rate cuts if activity data continue to surprise to the upside.

This is another reason why the Fed may accomplish more by doing less—signaling support while avoiding the risk of fueling demand that is already proving resilient.

Accomplishing More by Doing Less

The Fed cut the funds rate by 25 basis points last week, lowering the range to 4.00–4.25%. Chair Powell described the move as a “risk management cut,” stressing that downside risks to the labor market had risen and that the Fed did not want conditions to weaken further. The statement added dovish language that echoed September 2024, when the Fed delivered the first in a series of three cuts. Markets took this as a signal that additional easing is likely, with October and December both in play.

Yet the so-called “dots” tell a more complicated story. While the median projection implied three cuts this year, the distribution was scattered, particularly for 2026 and beyond. This wide dispersion highlights the lack of consensus inside the Committee and underscores the danger of markets pricing in too aggressive a path.

Dots are scattered—the financial markets risk overestimating the path of cuts.

Our view is that the Fed may be able to accomplish more by doing less. Signaling a long series of cuts risks pushing long-term yields higher rather than lower, particularly if investors perceive the Fed is leaning into political winds at a time when headline inflation is rising. A steadier approach—cutting less than the market expects, while reaffirming the Fed’s dual mandate—would anchor confidence in both bond and currency markets.

Looking further out, lower interest rates should allow conditions to firm later this year and into early 2026, bolstering home sales and sales of light vehicles and other big-ticket items. This improvement should broaden as uncertainty surrounding trade and immigration policy subsides, supporting a more durable recovery. Futures positioning already reflects heightened conflict between speculators and hedgers, which suggests volatility will remain high. But if the Fed avoids over-committing, it can preserve credibility while still fostering a recovery that builds momentum into 2026. Moreover, postponements of projects in the aftermath of Liberation Day are increasingly coming back on track, producing a tail wind capex in 2026.

Energy, Commodities, and Exchange Rates

Brent crude remains capped near $67, weighed down by OPEC+ supply adjustments and weak demand. The muted risk premium suggests markets are not yet pricing in broader contagion from Middle East conflict, though Israel’s strike in Qatar could quickly elevate LNG risks given Doha’s pivotal role in global exports.

The dollar has eased following the Fed’s “risk management” cut, as narrowing rate differentials encourage flows into higher-yielding emerging market currencies. The euro has traded with surprising resilience, occasionally acting as a quasi-safe haven, while the yen remains under pressure from Japan’s leadership transition but should stabilize once political uncertainty clears.

The broader backdrop is the U.S.–China trade standoff. Tariffs remain disruptive, but sanctions are now a realistic risk, threatening to fracture global supply chains within a year. Asia’s advanced economies are most exposed, but U.S. reliance on Taiwanese semiconductors highlights domestic vulnerability. This underscores the importance of industrial policy, such as the government’s Intel stake, to mitigate supply chain risk while ensuring taxpayers capture part of the upside. A deal on the U.S. operations of Tik Tok also appears to be close.

UN General Assembly

The UN General Assembly showed how fractured global governance has become. Calls for a Gaza ceasefire, pleas for reconstruction, Ukraine funding, and climate finance all vied for attention—but little consensus emerged. The pullback in U.S. leadership has created a void, leaving a vacuum where solutions to the world’s most pressing problems once had an anchor. Without Washington pushing for compromise, competing blocs are left to pursue narrower interests, and the space for consensus has narrowed considerably.

The pullback in U.S. leadership has left a void that President Trump may address in his speech.

Markets rely on institutions like the UN General Assembly to reduce uncertainty. When consensus breaks down, geopolitical risk premia rise. Investors should expect policy to be set more by ad hoc alliances and bilateral deals than by broad-based agreements, with volatility in trade, sanctions, and aid flows likely to persist.

Israel–Qatar Strike Fallout

Israel’s targeted strike on Hamas leadership in Qatar is not just a tactical event—it expands the geographic footprint of the conflict. Qatar has served as a key intermediary in ceasefire talks and hosts vital U.S. military bases. Whether the strike eliminated senior Hamas figures remains uncertain, but it has already opened the door to greater international criticism of Israel.