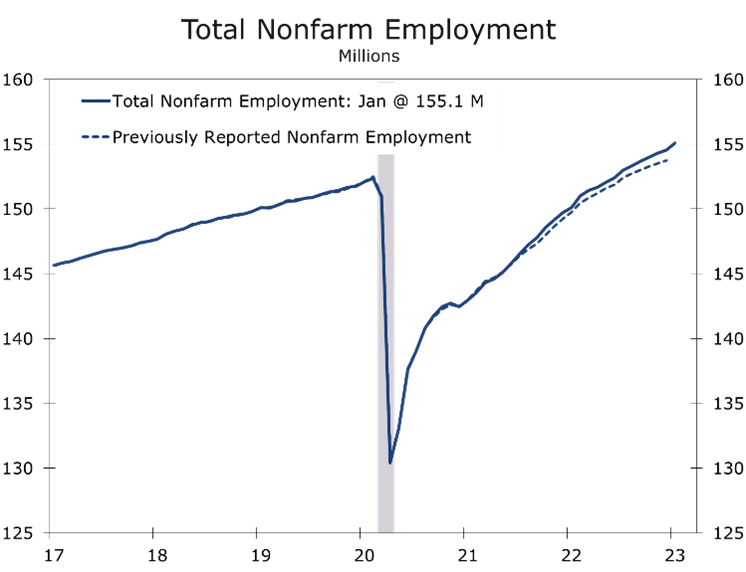

The Job Market Remains Remarkably Resilient

Q1 Will Likely Be the Strongest Quarter for Jobs

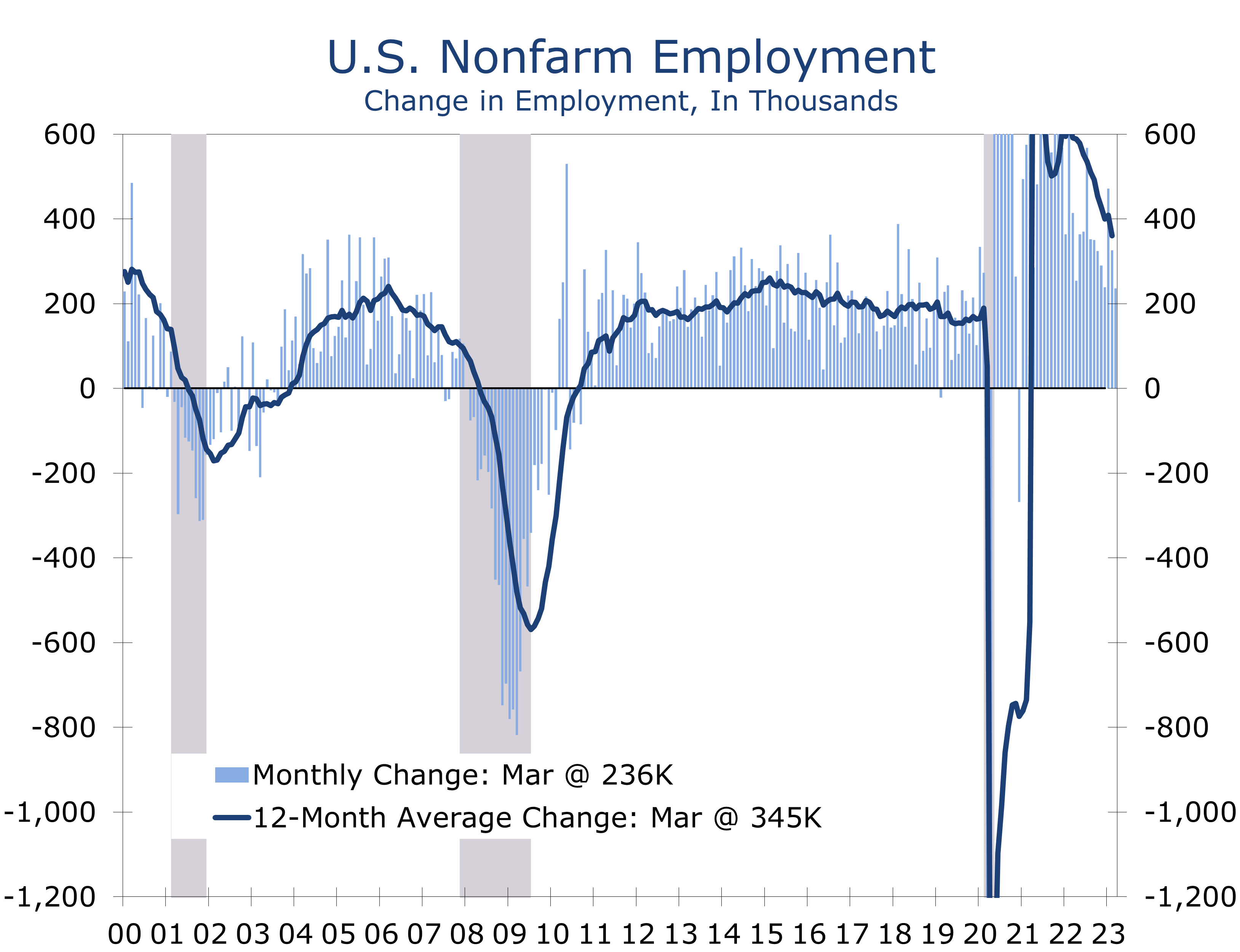

- Nonfarm employment rose by 236,000 in March. Revisions to the prior two months’ data subtracted a net 17,000 jobs.

- Private sector payrolls added a net 189,000 jobs in March, following gains of 266,000 in February and 353,000 in January.

- Job gains continue to be concentrated in industries that have generally struggled to add back workers. Leisure and hospitality added 72,000 jobs in March and health care and social assistance added 50,800 jobs.

- The most cyclically sensitive industries – construction (-9K) and manufacturing (-1k) lost jobs in March. In addition, temporary staffing firms cut 10,700 jobs.

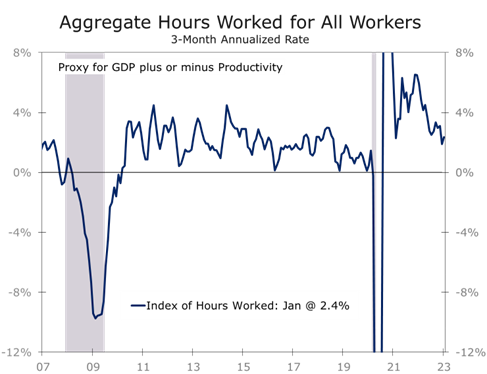

- Aggregate hours worked edged 0.1 higher and rose at a 2.5% pace in Q1 – roughly equivalent with 3.5% real GDP growth.

- The civilian labor force participation rate rose 0.1 to a post-pandemic high 62.6.

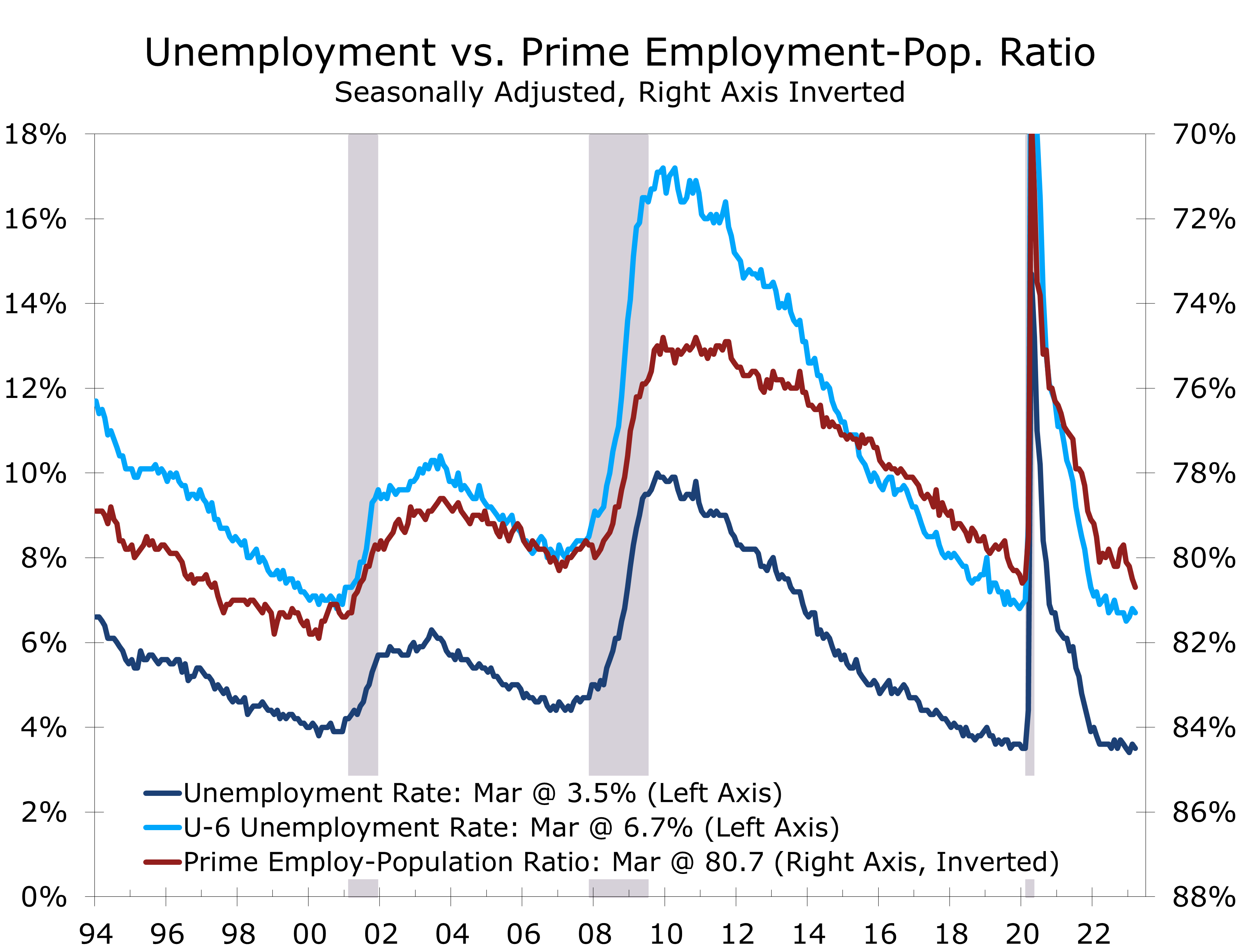

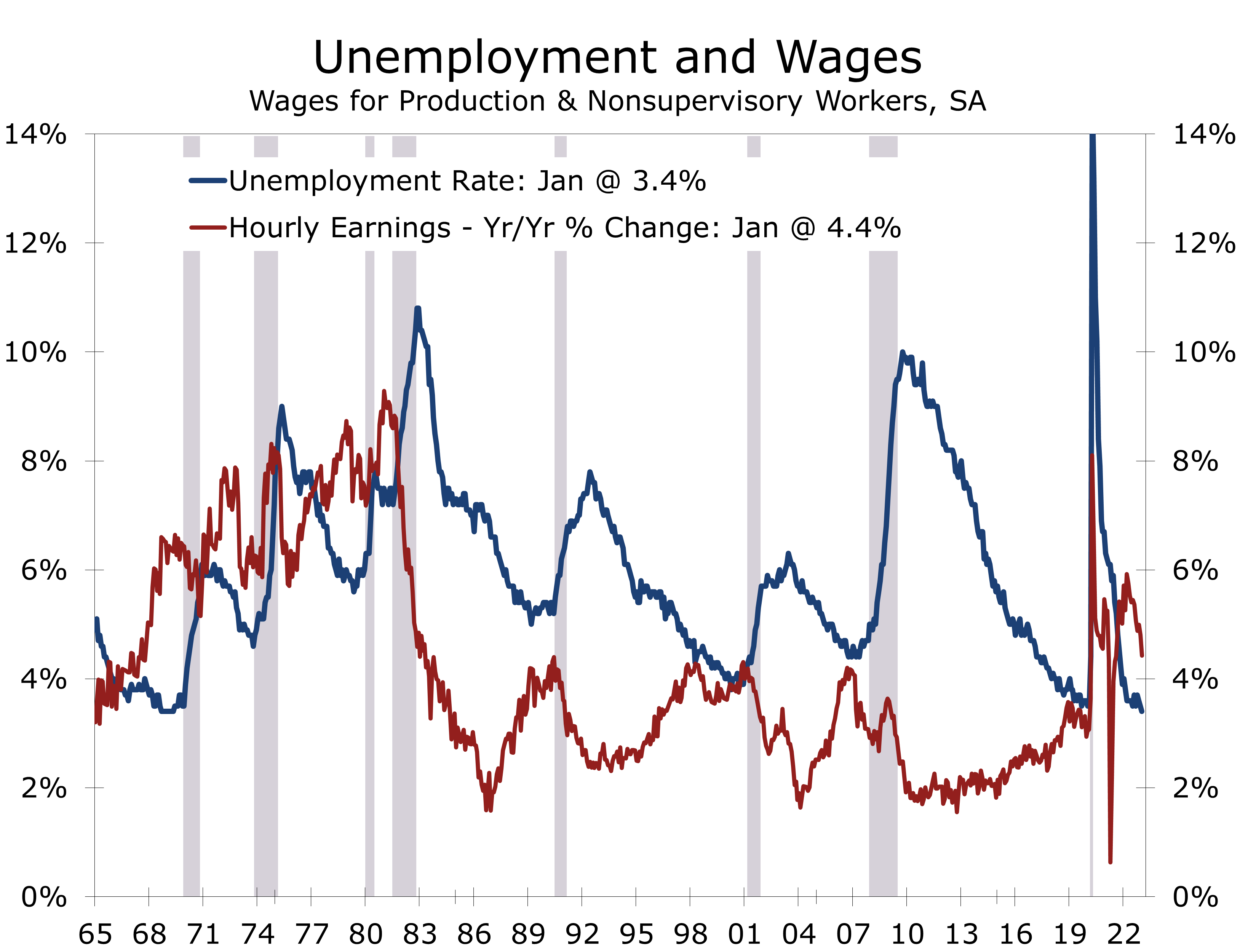

- The unemployment rate fell 0.1 point to 3.5%, while average hourly earnings rose 0.3% and are now up 4.2% year-to-year.

Employers added a net 236,000 jobs in March and average hourly earnings rose 0.3%. Data for the prior two months were revised slightly lower, subtracting 32,000 jobs from January’s previously reported gain but also adding 15,000 jobs to the February data.

The first quarter will likely be the high-water mark for job growth this year. Employers added a total of 1.034 million jobs during the quarter. A disproportionate share of those gains came from parts of the economy that have struggled to rehire, most notably the leisure and hospitality sector, certain parts of health care and social assistance, and government. These three areas accounted for two-thirds of overall job gains.

Even with recent outsized gains, restaurants and bars still largely remain understaffed. Payrolls in the leisure and hospitality sector remain 2.2% below their pre-pandemic levels, or 368,000 fewer jobs. Employment at nursing and residential care facilities also remains well below its pre-pandemic level, as do payrolls at private child care centers. Government payrolls are 1.4% below their pre-pandemic level, or 314,000 jobs.

Despite the recent outsized job gains, a few cracks are now emerging in the labor market.

We look for job growth to decelerate this spring, partly as a payback for an earlier than usual rise in payrolls due to unseasonably mild weather in much of the U.S.

More fundamentally, job growth is slowing in response to higher interest rates and the expectation that credit will tighten further in coming months. More and more businesses are focusing on cutting costs, which has led to a decline in job openings. The process is most apparent in the tech sector but has spread more recently to financial services and increasingly to most other industries.

Hiring in the most cyclically sensitive parts of the economy has clearly slowed. Construction employment, which was buoyed by unseasonably mild weather in January and February, lost 9,000 jobs in March. Manufacturing payrolls lost 1,000 jobs for the second month in a row, with notable losses in chemicals, fabricated metal products and semiconductor manufacturing.

Mining remains a bright spot, with oil exploration in the Permian Basin continuing to drive hiring. Midland and Odessa, Texas posted the fastest job growth over the past year of any metropolitan area, with hiring up 10.1% and 6.6%, respectively.

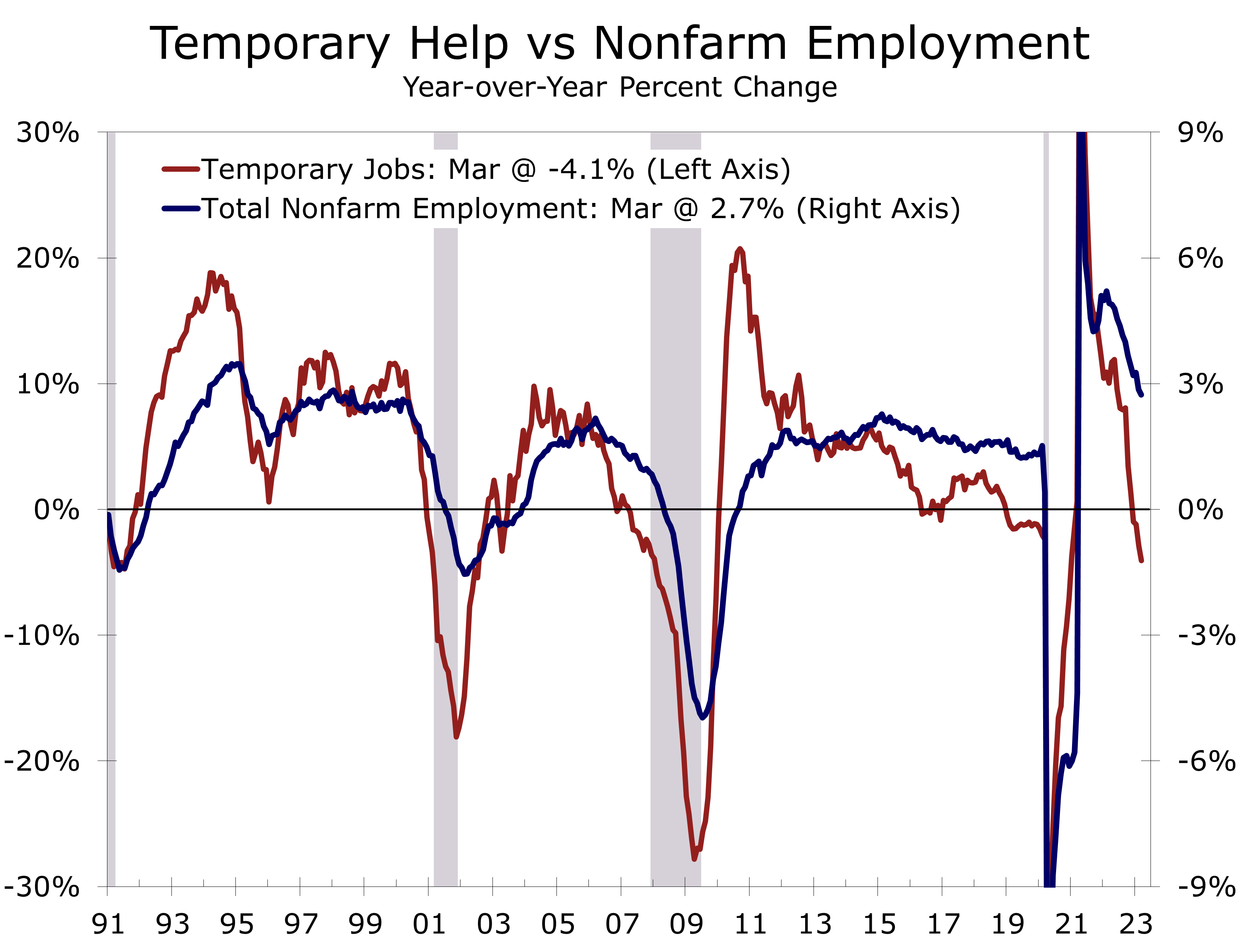

One of the more reliable leading indicators of payroll growth is the trend in hiring at temporary staffing firms, which has fallen 4.1% over the past year and is now at levels that have coincided with recessions in the past. Temporary staffing firms cut a net 10,700 jobs in March and have lost 146,500 jobs over the past year.

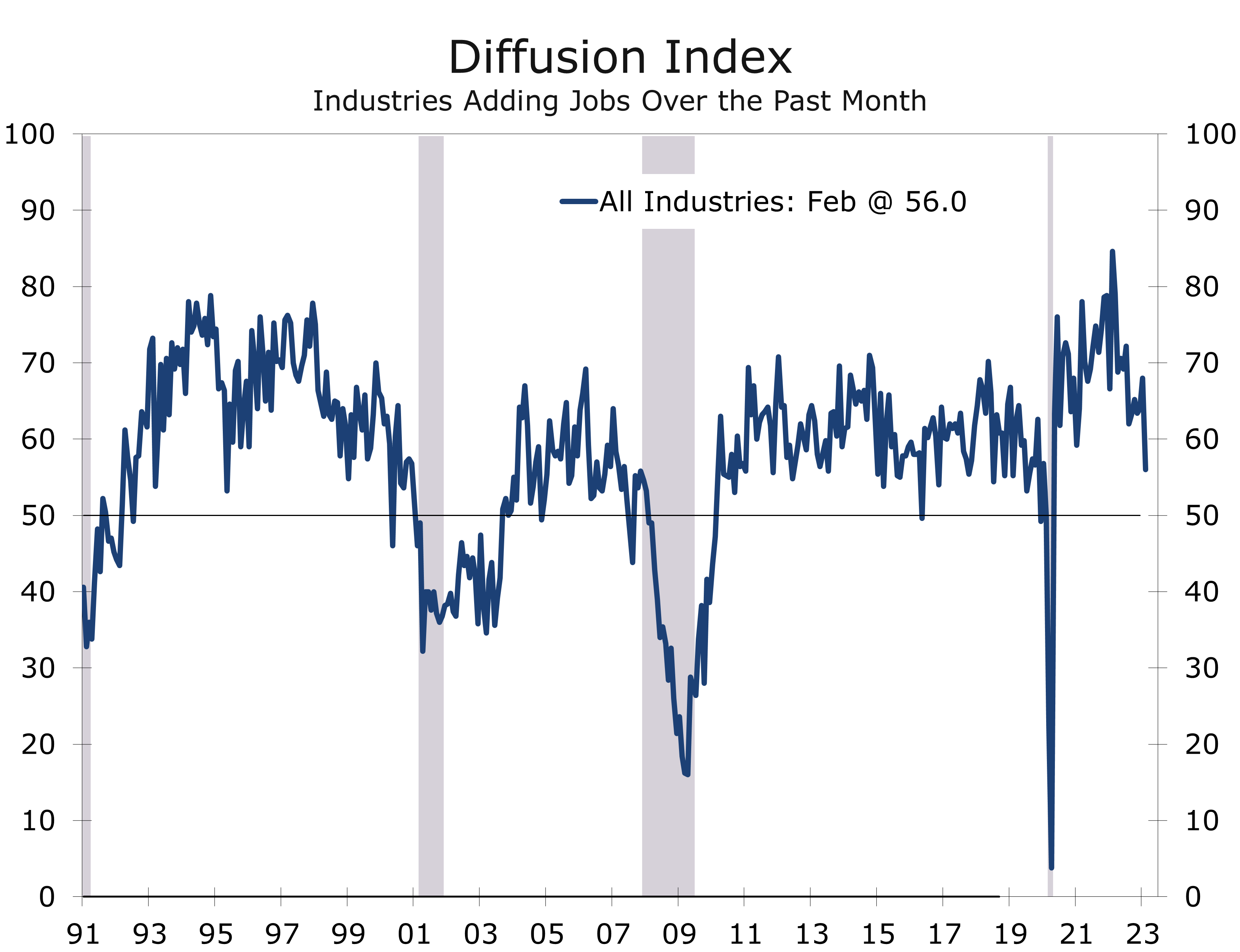

While the swoon in temporary staffing jobs looks ominous, most economic indicators continue to point toward a soft landing, at least in the near term. Job gains are still broad based, with 60.2% of industries adding jobs in March. Hiring is less broadly based than it used to be, however, with March marking the third smallest share since the start of the pandemic.

The unemployment rate fell 0.1 point to 3.5%.

The unemployment rate fell 0.1 point to 3.5% in March, as household employment rose by 577,000, outpacing a 480,000 rise in the civilian labor force. The labor force participation rate and prime employment population rate both rose in March, rising to their highest levels since the pandemic. The prime employment-population ratio rose 0.2 points to 80.7 and is now slightly higher than before the pandemic.

Given the latest employment data, the Fed is inclined to continue leaning toward another quarter-point interest rate hike at the May FOMC meeting. The May meeting will precede the April employment data, so March inflation reports are now front and center. The key report for the Fed, however, will likely be the April ISM report that will be reported on May 1.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Existing Home Sales Surge in February

Lower Rates Bring Buyers Back

- The National Association of Realtors reported that existing home sales surge 14.5% in February, which marks the largest increase since July 2020.

- The surge in existing sales reflects closings on contracts written in December and January when mortgage rates briefly fell back toward 6%.

- February is normally a slow month for home sales, so the seasonal adjustment is one of the largest of the year, which exaggerated the extent of the resurgence in sales.

- Sales were bolstered by the return of buyers that were priced out of the market when mortgage rates surged last fall and milder than usual weather across much of the US.

- Even with the surge in sales, homes are remaining on the market longer and prices are falling.

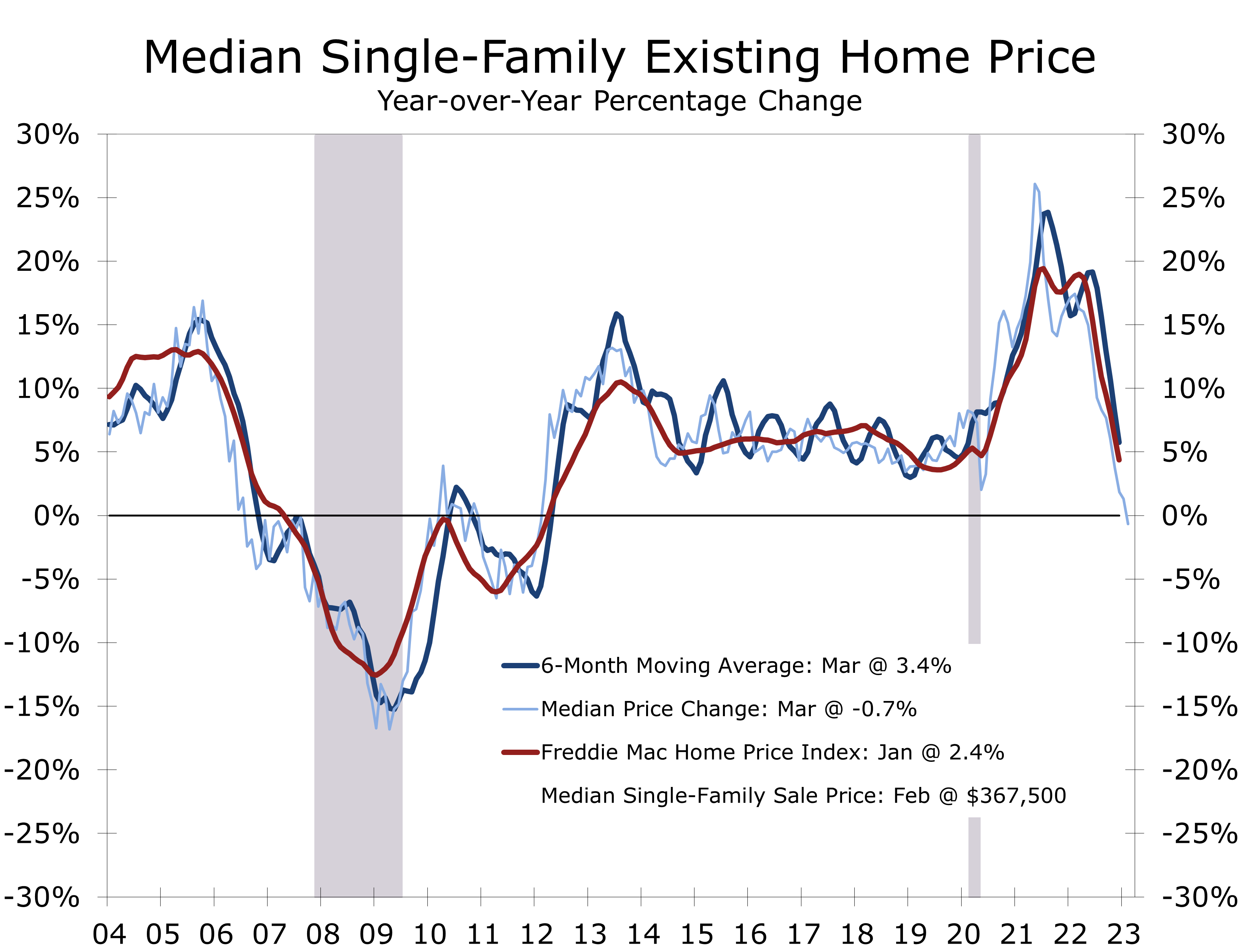

- The median price of an existing home has now fallen 0.2% over the past year, the first year-to-year decline since February 2012.

Sales of existing homes easily blew past expectations in February, with overall sales surging 14.5% to a 4.58 million unit rate. Sales of single-family homes rose an even larger 15.3% to a 4.14-million-unit pace, while sales of condominiums and co-ops rose 7.3% to a 440,000-unit pace.

February’s jump in sales, which was three times the consensus estimate, was fueled by a sharp pull back in mortgage rates in late December and January, when mortgage rates briefly fell back to 6%. Mortgage lenders likely dialed up clients that saw sales fall through as many buyers that had written contracts early last fall found they no longer quailed when mortgage rates surged to 7%. Milder weather also helped, as February is usually one of the slowest months for home buying.

The wide swings in home sales and mortgage rates mean last fall’s weakness was overstated.

The wide swings in home sales and mortgage rates mean last fall’s weakness was likely overstated, just as February’s resurgence now is. Some analysts have even gone as far to say that home sales bottomed last fall and look for sales to steadily increase this year. We doubt it, as mortgage rates have already rebounded, and housing affordability remains historically challenging. After averaging 6.36% in February, mortgage rates rose steadily during the first half of March and are currently around 6.75%.

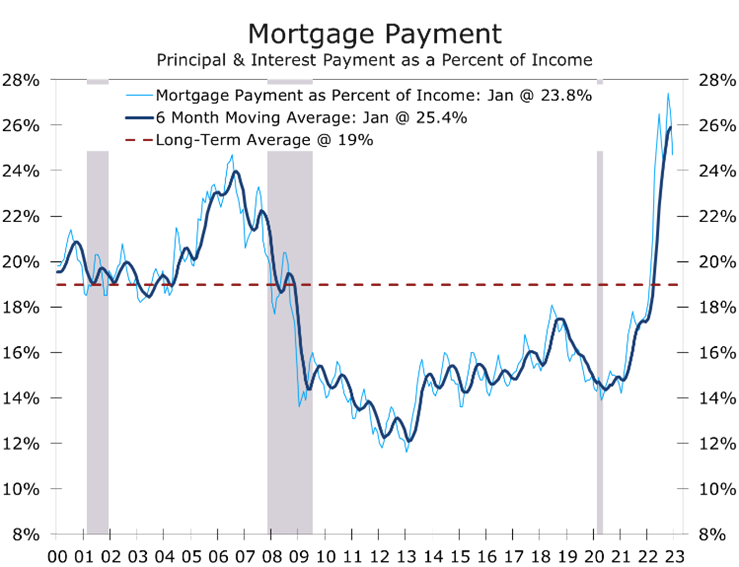

Lower mortgage rates and falling home prices had begun to make some inroads at restoring housing affordability. Qualifying income for a family earning the median income and purchasing the median price home has fallen 11% since October, from $98,064 to $86,736. The drop reflects the pullback in mortgage rates from 6.98% in October to 6.35% in January. The median price of an existing single-family home fell 5.6% over that 4-month period and is now down 13.7% since peaking in June.

Unfortunately, homeownership is still out of reach for far too many households. Monthly principal and interest payments for that median home totaled $1,807 in January, down from $2043 in October. Monthly principal and interest payments still consume an outsized 23.8% of median family income, which is roughly equivalent to what it was at the peak of the housing bubble 15 years ago.

For affordability to return to its long-run average, mortgage rates would need to fall more than a percentage point lower and home prices would have to fall further, while median family income increased. All those things are likely to eventually happen, but they will not happen quickly. Moreover, we are likely to see family income growth slow as job growth weakens. Credit underwriting will also likely tighten.

Home prices edged higher in February, with overall prices climbing 0.5% to $363,000 on a non-seasonally adjusted basis and prices of single-family homes rising 0.6% to $367,500. The gains mark the first increases in 8 months. Overall prices are down 12.3% since June of last year, while single-family prices have fallen 12.7%.

The median price of an existing home has fallen 12.3% since June and is down 0.2% year-to-year.

Home prices are now down 0.2% on a year-to-year basis and such comparisons are likely to deepen over the next 4 months, as comparisons with peak home prices will become more difficult.

February’s surge in existing home sales likely makes the Fed’s decision a little easier. We expect the Fed to hike the federal funds rate by a quarter percentage point at the conclusion of the FOMC meeting tomorrow and expect the target for the terminal funds rate for the cycle to come down from 6% to around 5.5%. The crisis surrounding Silicon Valley Bank and other West Coast Specialty lenders will likely result in some tightening of credit conditions ahead of the release of bank stress-test results in June. This will effectively do some of the Fed’s work for them.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Consumer Prices Rise Close to Expectations

Inflation Continues to Slowly Decelerate

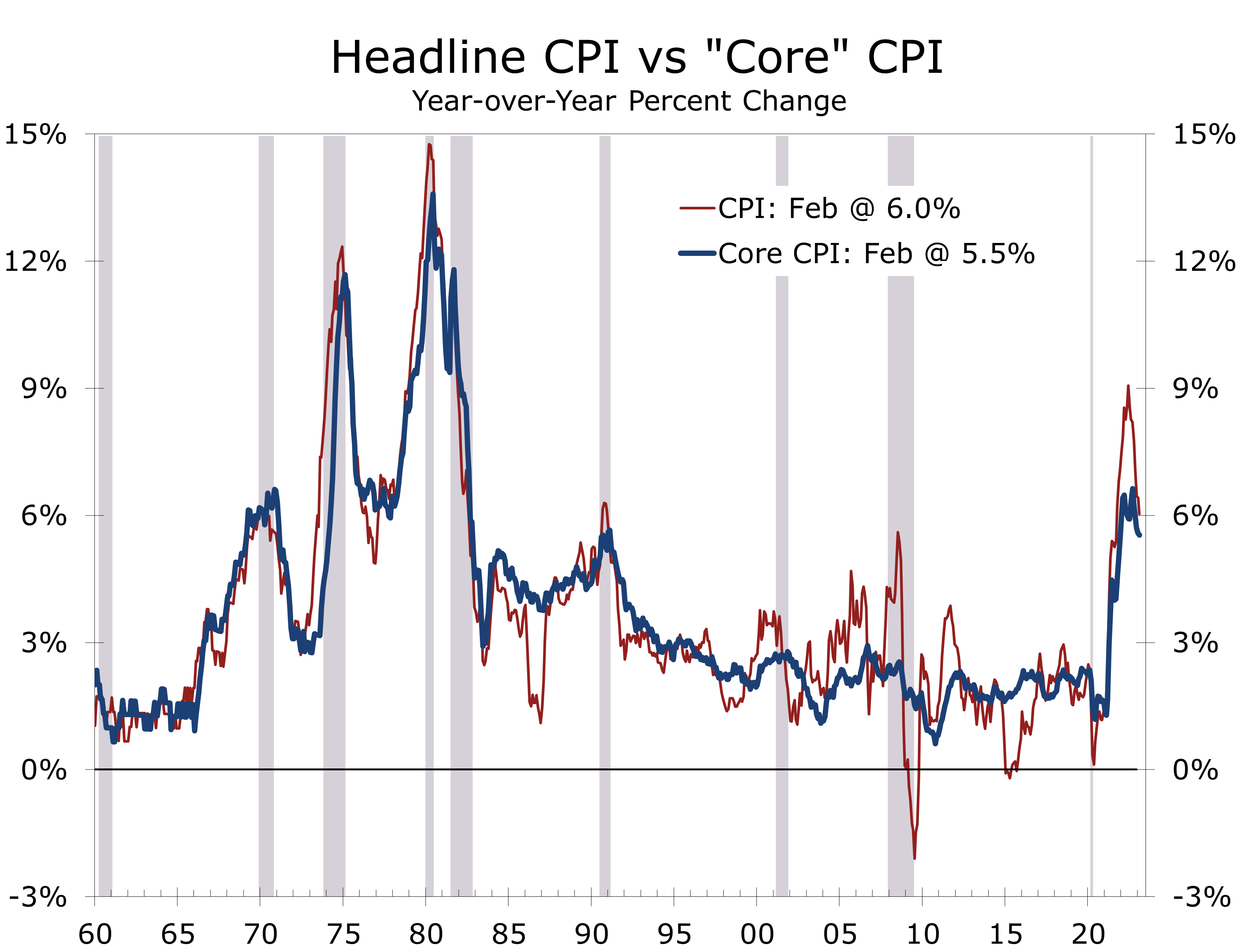

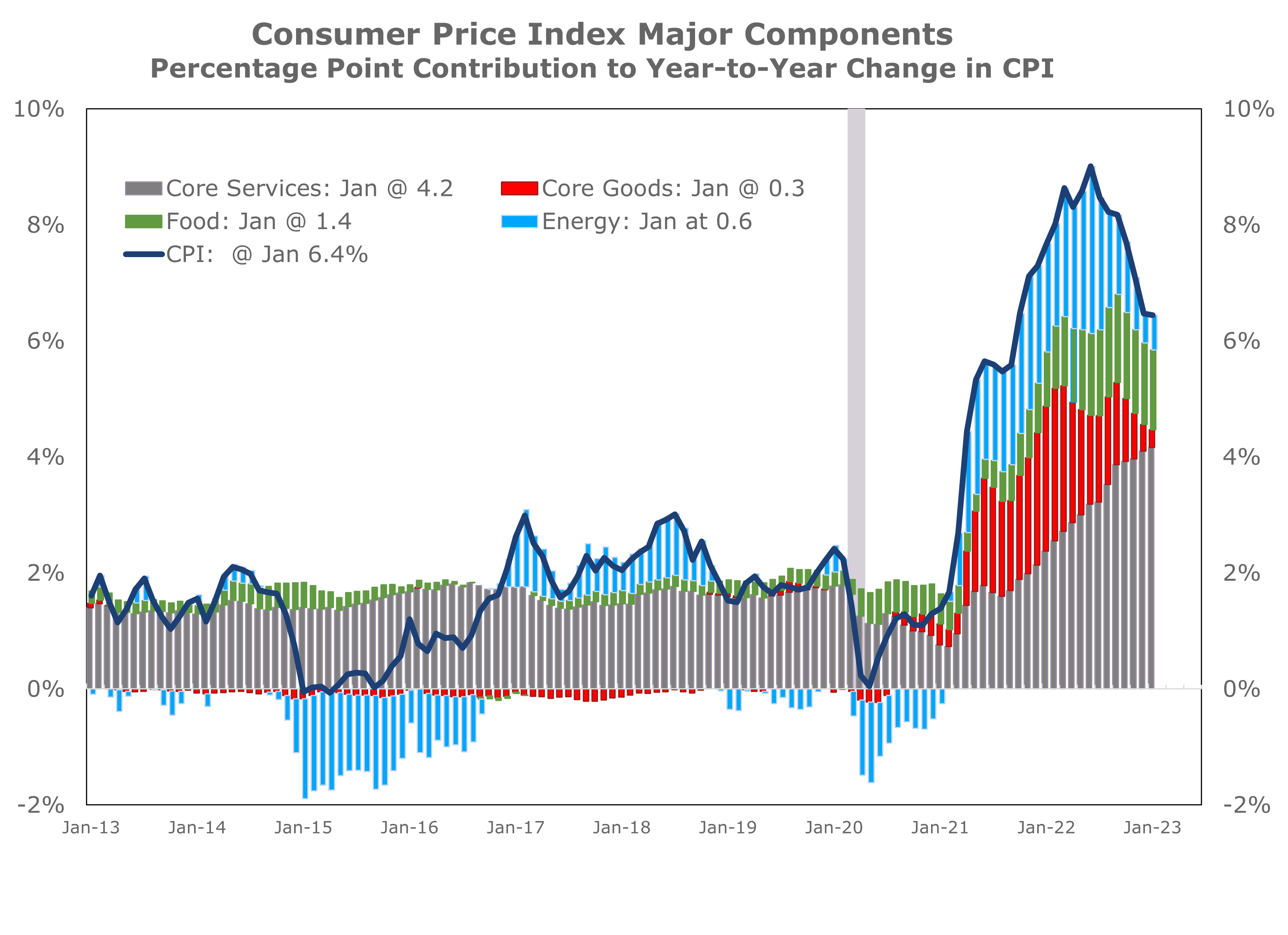

- The Consumer Price Index came in close to expectations, with the headline index rising 0.4% and the core rising 0.5%.

- February’s gains leave the headline index up 6.0% year-to-year, and the core up 5.5%.

- Price increases eased at the grocery store, with food prices rising 0.4% overall and just 0.3% at the grocery store.

- Sharply lower prices for fuel oil and natural gas – both byproducts of milder winter weather – pulled energy prices down 0.6%.

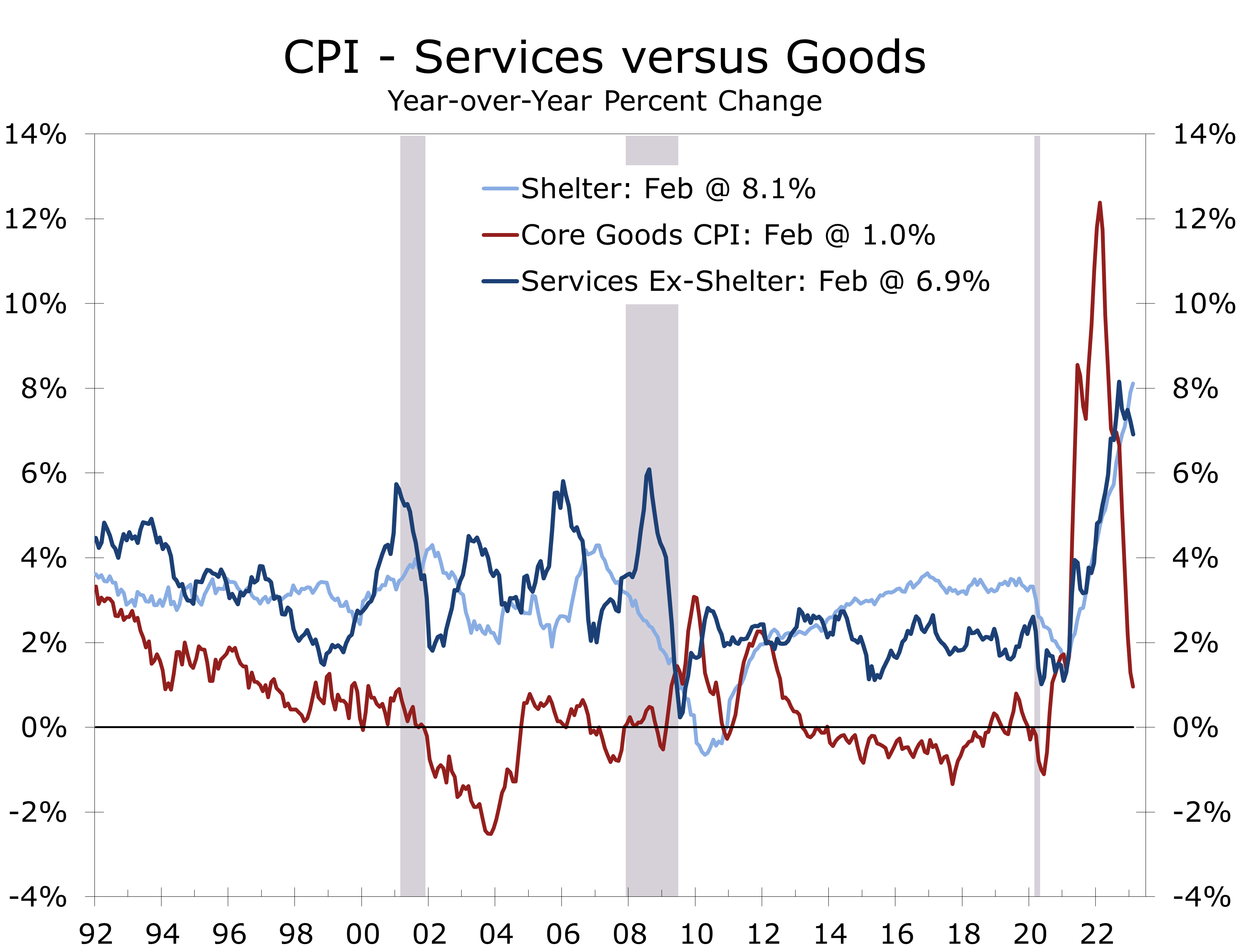

- Used-car prices fell 2.8% but higher prices for airfares and another big rise in shelter cost more than offset that drop, resulting in a slightly larger-than-expected rise in the core CPI.

- Shelter costs were driven higher by an 0.8% increase in residential rents and 0.7% rise in owners’ equivalent rent.

- Medical care costs fell 0.5%, reflecting a 0.5% drop in physician’ services as well as uncharacteristically small increases in hospital services and prescription drugs.

After this past week’s surprise blow up in the banking sector, a ho-hum CPI report was sorely needed. Inflation is now moving in the right direction, although the moderation is still too modest to allow the Fed to end its tightening regimen. We expect another quarter-point hike at next week’s FOMC meeting, provided concerns about the banking system subside.

Inflation is clearly decelerating on a year-to-year basis. The headline CPI peaked at 9.1% last June and has now slowed to just 6.0%. Most of that deceleration has come from a sharp reversal in energy prices due to the draw down of the Strategic Petroleum Reserve and milder than usual winter weather in much of the U.S. and Europe. Falling prices for used cars and light trucks and some moderation in food prices has also helped pull down the headline and core numbers.

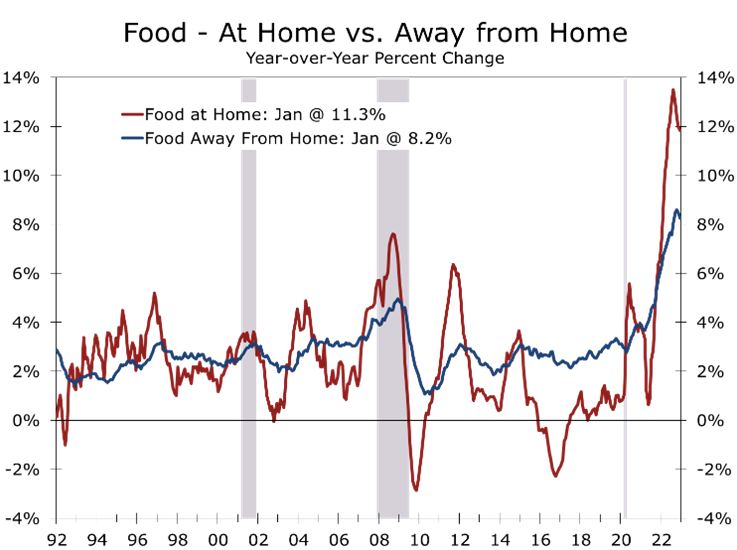

Food prices are finally moderating, thanks to lower fuels costs and fewer bottlenecks.

Prices for groceries rose just 0.3% in February, marking their smallest gain since March 2021. The moderation reflects some easing of supply bottlenecks and lower prices for diesel fuel. Prices for meats, poultry, fish and eggs fell 0.1% in February, marking their first monthly drop since December 2021. Egg prices fell 6.7% in February, following huge increases in prior months. Even with the declines in these highly visible areas, grocery store prices remain 10.2% higher than they were a year ago.

Energy prices fell 0.6% in February, following a 2% rise the prior month. The price of natural gas declined 8%, marking the largest 1-month drop since October 2006. The price of fuel oil fell 7.9% in February. Demand for both fell sharply this past month, as much of the country enjoyed unseasonably mild weather. Gasoline prices rose 1% in February, following a 2.4% rise the prior month.

Prices excluding food and energy rose 0.45% in February and remain up 5.5% year to year. Prices for core goods were unchanged in February and are now up just 1% year-to-year. Much of the deceleration in core goods prices is due to falling prices for used cars and trucks, which fell 2.8% in February and are down 13.6% over the prices year.

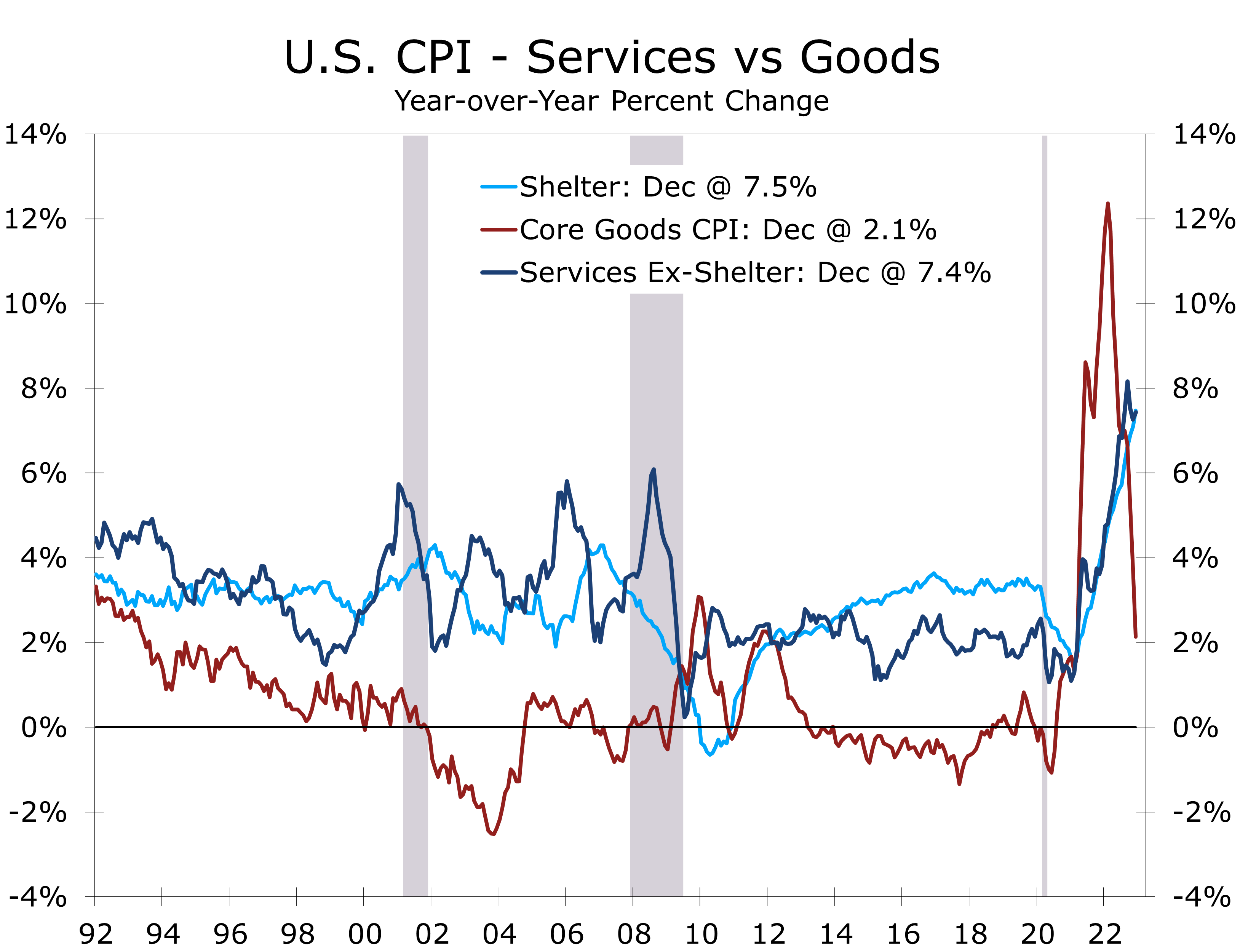

Shelter costs continue to increase, reflecting past increases in market rents.

Prices for services excluding energy rose 0.6% in February, with high shelter costs accounting for much of the gain. Shelter costs rose 0.8% in February and are up 8.1% year to year. Rent of primary residence and owners’ equivalent rent account for the bulk of shelter costs. Both measures are calculated by the BLS using a complex formula that appropriately captures the costs of housing for renters and homeowners but tends to lag changes in market rents.

The lags of shelter costs and their outsized weight in the CPI have prompted questions about whether inflation has already decelerated enough for the Fed to stop tightening. We do not believe so. Wages are still rising faster than productivity and price measures where wages are the primary driver of selling prices have been slower to moderate. Prices for services excluding energy and shelter, a category repeatedly mentioned by Fed Chair Jerome Powell, have risen 6.0% over the past year, which is down only modestly from their peak of 6.7% hit last September.

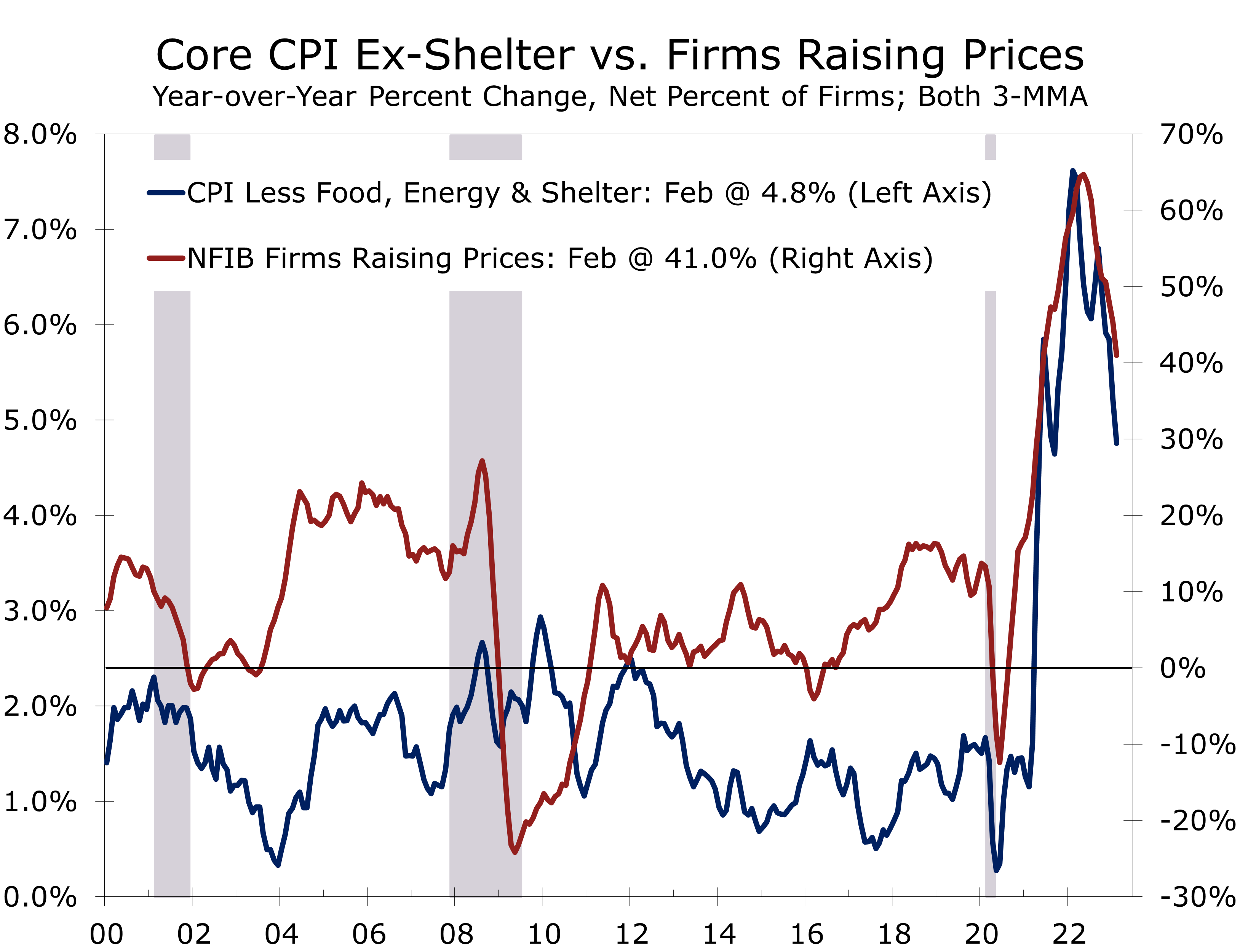

The share of firms raising prices has fallen sharply, hinting inflation will decelerate further.

One of our favorite inflation measures is the share of small businesses raising prices over the past three months. This measure surged to a record high when the economy reopened following the pandemic and is a big reason why we never bought into the “transitory” inflation story. The more recent data is encouraging, with the share raising prices over the past three months falling 4 points in February to 38, which is the lowest level April 2021. A similar measure of firms boosting compensation remains notably higher, however, and has fallen more slowly.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Small Business Optimism Edges Higher in February

Small Businesses Remain Concerned About the Outlook

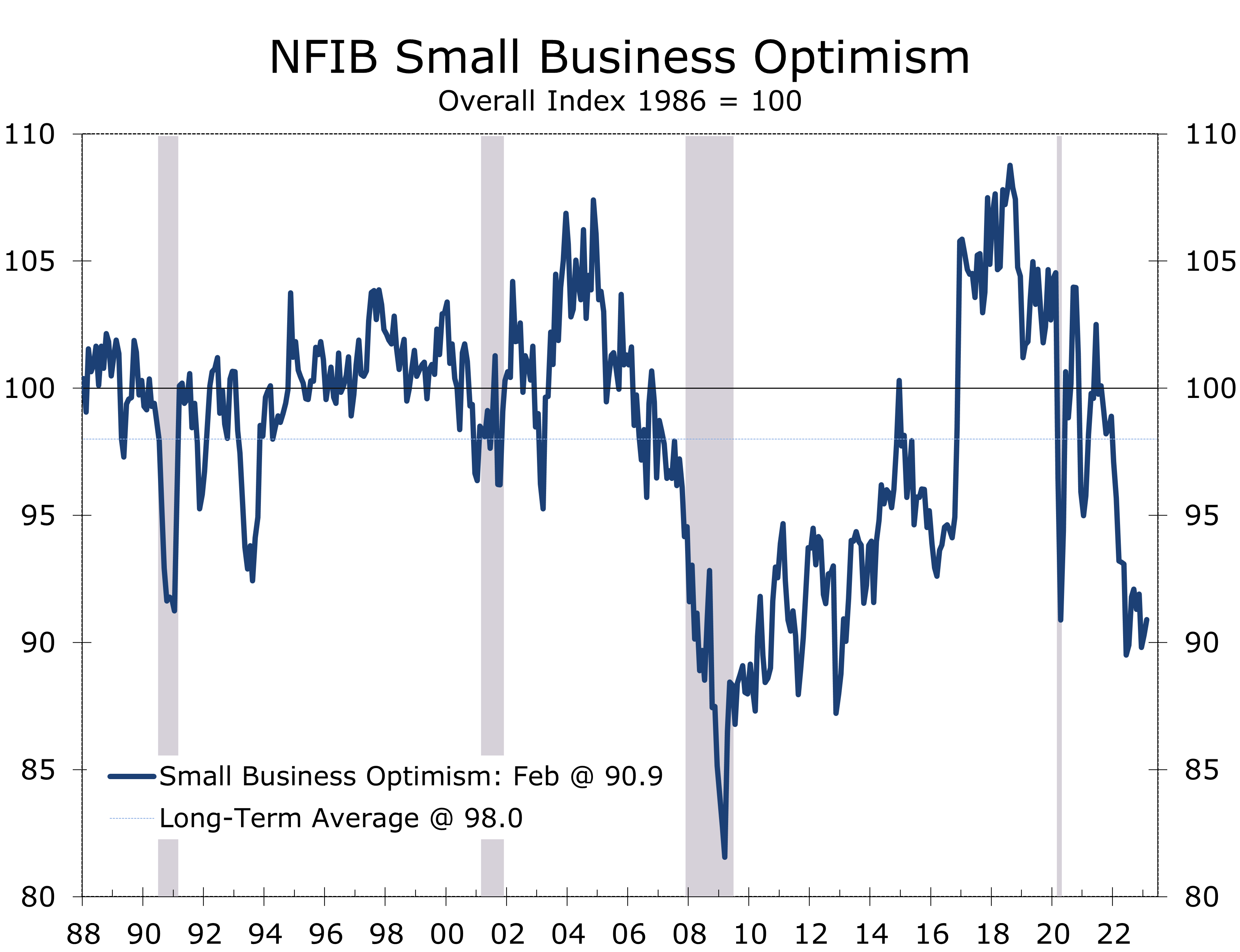

- The National Federation of Independent Business (NFIB) Small Business Optimism Survey rose 0.6 points to 90.9 in February.

- Business owners remain concerned about the economic outlook and continue to be challenged by higher input cost rising wages.

- The share of business owners expecting the economy to improve over the next six months fell 2 points to -47%.

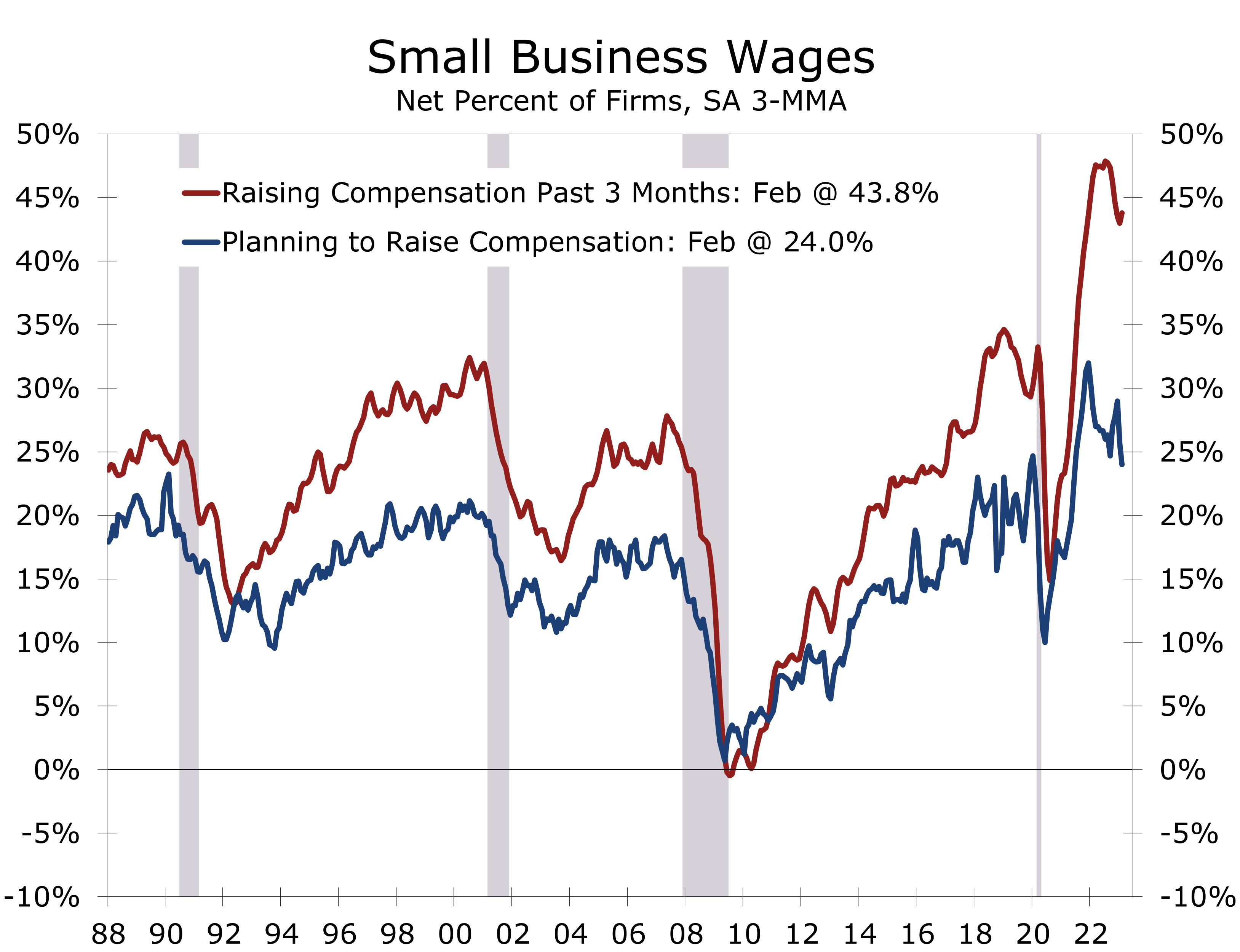

- The spread between the number of firms boosting compensation and those planning to boost compensation remains extremely wide, reflecting efforts to maintain margins.

- The share of firms raising prices fell 4 points to 38 - the lowest share since April 2021.

- Thirty percent of firms report they are borrowing regularly, the highest share since January 2000.

- With profit margins coming under pressure and credit set to tighten, we expect small businesses to curb hiring, reduce inventories and cut capital spending in coming months.

This morning’s update on Small Business Optimism is not likely to steal the headlines from the SVB banking crisis or the latest CPI data. The report shows another modest increase, with the headline index rising 0.6 points to 90.9. Small Business Optimism been below its long-term average for 14 consecutive months and remains at levels typically seen in a recession.

While 5 of the index’s 10 components increased, most rose from severely depressed levels. The share of businesses expecting sales to improve rose 5 points to -9%, indicating more firms still expect sales to fall than expect them to increase. Earnings trends also improved, rising 3 points to -23%, while the net share with job openings and share expecting credit conditions to improve both rose 2 points.

On the plus side, the net share of firms raising prices over the past 3 months fell 4 points to 38%, which is the lowest reading for this closely watched series since April 2021. Moreover, the share of firms planning to raise prices in the next 3 months fell 4 points to 25%.

The NFIB Index has consistently provided one of the earliest warnings of economic distress.

Small Businesses operate on the economy’s front lines and the pressures business owners face often precede those at larger firms. This is one reason why the NFIB index has consistently provided one of the earliest warnings of impending economic distress.

One of the more troubling aspects of the NFIB survey has been the historically large share of business owners expecting general business conditions to worsen. The net share has been in negative territory since December 2020 and steadily weakened as higher inflation drove interest rates higher. The index hit an all-time low of -61% in June 2022 and has averaged -48.7% over the past year.

Heightened concerns about the economy are likely impacting decisions on hiring, inventory levels and capital spending. The net share of small business owners planning to increase staff fell 2 points in February to 17% – the lowest since January 2021.

While hiring plans have fallen, small businesses still have plenty of job openings and a large share report difficultly remaining fully staffed. The share of small businesses with job openings rose 2 points to 47% in February. Of those firms hiring or trying to hire in February, 90% reported few or no qualified applicants for the positions they were trying to fill.

The net share of businesses reporting inventories increased fell 7 points in February to -1%. Moreover, the next share of business owners stating inventories were too low fell 3 points to -4%, meaning more firms feel inventories are too high than feel they are too low. Not surprisingly, a net -7% of business owners plan to increase inventories in coming months.

Businesses have also become more cautious about capital spending. The share of firms planning to increase capital outlays was unchanged at 21% in February. While that is still well into positive territory, it marks the smallest share of small businesses planning to increase capex since March 2021.

One of the key drivers for capital outlays are efforts to boost efficiency. Small businesses are price takers for labor and compensation costs have been sharply outpacing planned increases for quite some time. The gap between the share of firms raising compensation over the past 3 months and those planning to raise compensation has averaged a record 20 percentage points for the past year.

Small businesses are price takers for labor.

The persistent pressure on wages will make it difficult to bring inflation down to the Fed’s 2% target. Wages make up a large share of core services prices, a key metric the Fed has identified in determining how much higher they need to push up short-term interest rates. We still feel the Fed will follow through with a 25 basis point hike at next week’s FOMC meeting, provided fears about the banking system continue to subside.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Employment Rises Solidly in February

Employment Rises Solidly in February

- Job Growth Remained Strong in February

- Employers added 311,000 net new jobs in February, which was above market expectations but in line with the average gain for the past six months.

- Job gains continue to be led by a resurgence in hiring at restaurants, bars, hotels, and entertainment venues – where payrolls still remain 2.4% below pre-pandemic levels.

- Hiring also continues to bounce back in other sectors that have been slow to recover, including health care, childcare, personal services, and local government.

- The most cyclical parts of the economy show a bit more weakness. Manufacturers cut 4,000 jobs, while trucking and warehousing lost 21,500 jobs. Construction payrolls, however, added 24,000 jobs.

- The unemployment rose 0.2 percentage points to 3.6%, while average hourly earnings rose just 0.2%.

February’s larger than expected 311,000-job rise in nonfarm payrolls did not settle the question whether the Fed will raise rates by a quarter or a half of a point at their March 22 FOMC meeting. While the headline came in hot, the gain was below the average for the past 6 months and the underlying details show clear signs of deceleration. Moreover, the unemployment rate rose 0.2 percentage points to 3.6% and average hourly earnings rose a smaller than expected 0.2%.

The employment data were eclipsed by the abrupt collapse of Silicon Valley Bank and worries about the potential fallout. Concern about secondary impacts has triggered a flight-to-quality, which has pulled share prices lower at banks, tech firms and the stock market more broadly. Bond yields have also tumbled, despite ongoing inflation concerns.

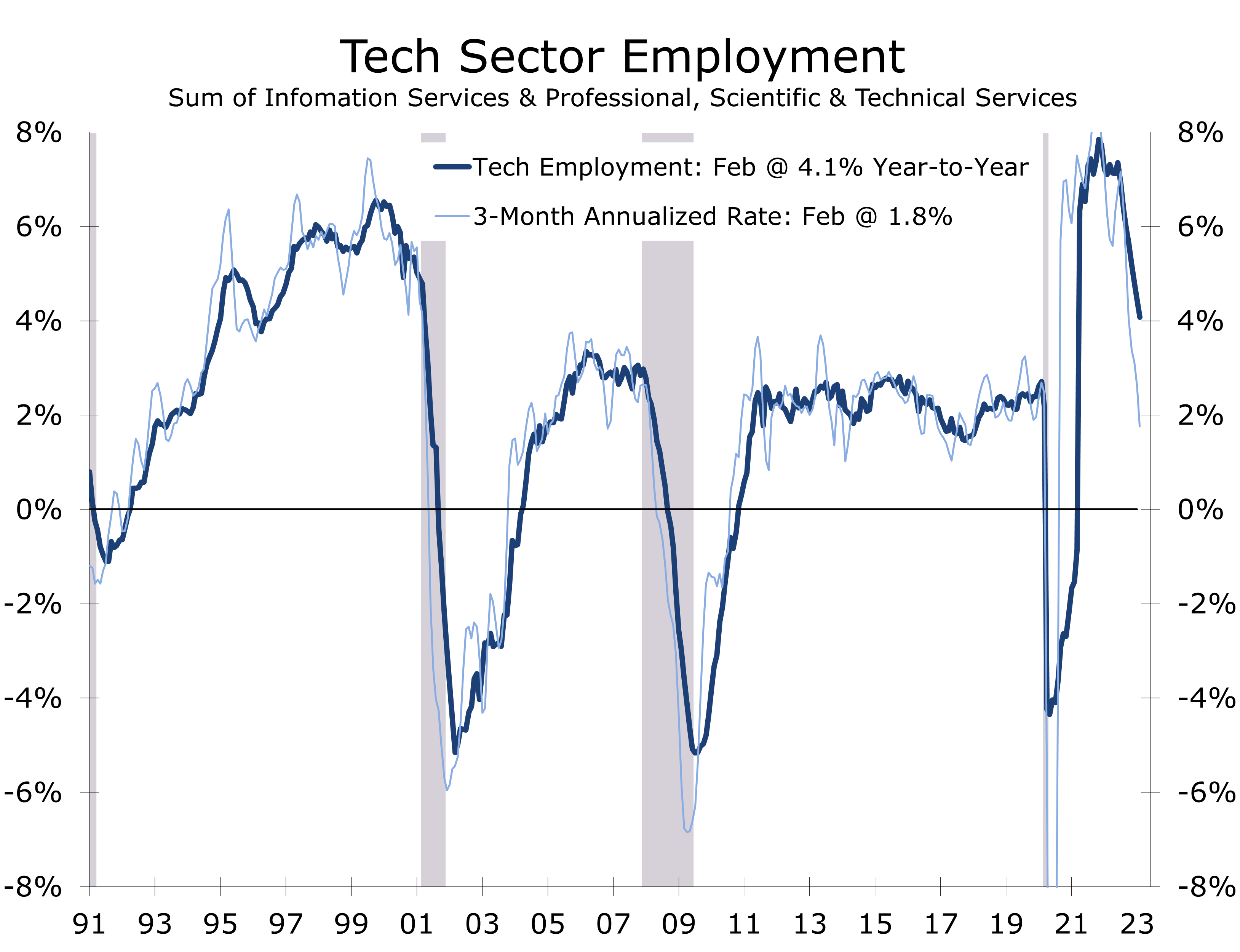

The collapse of Silicon Valley Bank and heightened uncertainty at some West Coast specialty lenders is tied to the ongoing correction in the tech sector. Private equity values have tumbled as exits for startups have become more difficult due to the sell-off in tech shares and heightened scrutiny nearly every merger and acquisition faces today. The only recourse for young firms is to cut costs and those cutbacks are now readily apparent in the jobs data.

Private equity values have tumbled as exits for startups have become more difficult.

The information sector lost 25,000 jobs in February and has cut 54,000 jobs over the past 3 months. Hiring in professional, scientific, and technical services is also decelerating. The most tech-centered subcomponent – computer systems design and technical consulting – lost 2,400 jobs in February. These two sectors provide a timely but imprecise measure of tech payrolls.

Job growth remains exceptionally strong on an overall basis, although a deceleration is also now readily apparent. Employers added 311,000 jobs in February, which was 86,000 more than market consensus. Hiring continues to be driven by the recovery of jobs in the leisure and hospitality sector, which added back 105,000 jobs in February. Health care and social assistance (62,800), retail trade (50,100) and professional and business services (45,000) all posted strong gains during the month. Construction payrolls also rose by 24,000 jobs, hinting that mild weather may have also bolstered the headline increase.

In addition to the earlier noted 25,000-job loss in the information sector, job losses were also reported in trucking and warehousing (-21,500) and manufacturing (-4,000). The weakness in the goods sector likely reflects the pullback in consumer goods purchases. Within manufacturing, plastics and rubber products (-4,700), furniture (-2,800), and textile and apparel (-3,100) all posted notable job losses.

Overall job growth for the prior two months was also revised slightly lower. Payrolls now show a gain of 504,000 jobs in January and 239,000 in December, a combined 34,000 fewer jobs than earlier reported. The breadth of overall job gains was also the weakest since the lockdowns at the start of the pandemic, with the diffusion index falling 12 points in February to 56.

The weakness in the goods sector likely reflects a renewed emphasis by retailers and manufacturers to clear inventories ahead of what is widely expected to be a softer second half of 2023. Trucking and warehousing firms have cut 42,000 jobs since October.

Construction was a notable bright spot in February, with builders adding 24,000 jobs. That gain may have been bolstered by unseasonably mild weather. Nearly half the gain was in residential specialty trade contractors. Home builders are working feverishly to reduce their work-in-process inventory, which remains near a multi-decade high. Heavy and civil engineering construction added 7,700 jobs, benefitting from rising spending for road and bridge projects.

The unemployment rate rose 0.2 percentage points to 3.6% in February, as a 177,000 increase in household employment was more than offset by a 419,000 rise in the civilian labor force. Average hourly earnings came in slightly below expectations, rising just 0.24%, and is now up 4.6% year-to-year. The smaller than expected increase reflects the larger share of job gains occurring in lower paying industries. Average hourly earnings for production and non-supervisory workers rose 0.46% in February and are up a larger 5.3% year-to-year.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Housing Starts Decline Modestly in January

Housing Starts Decline Modestly in January

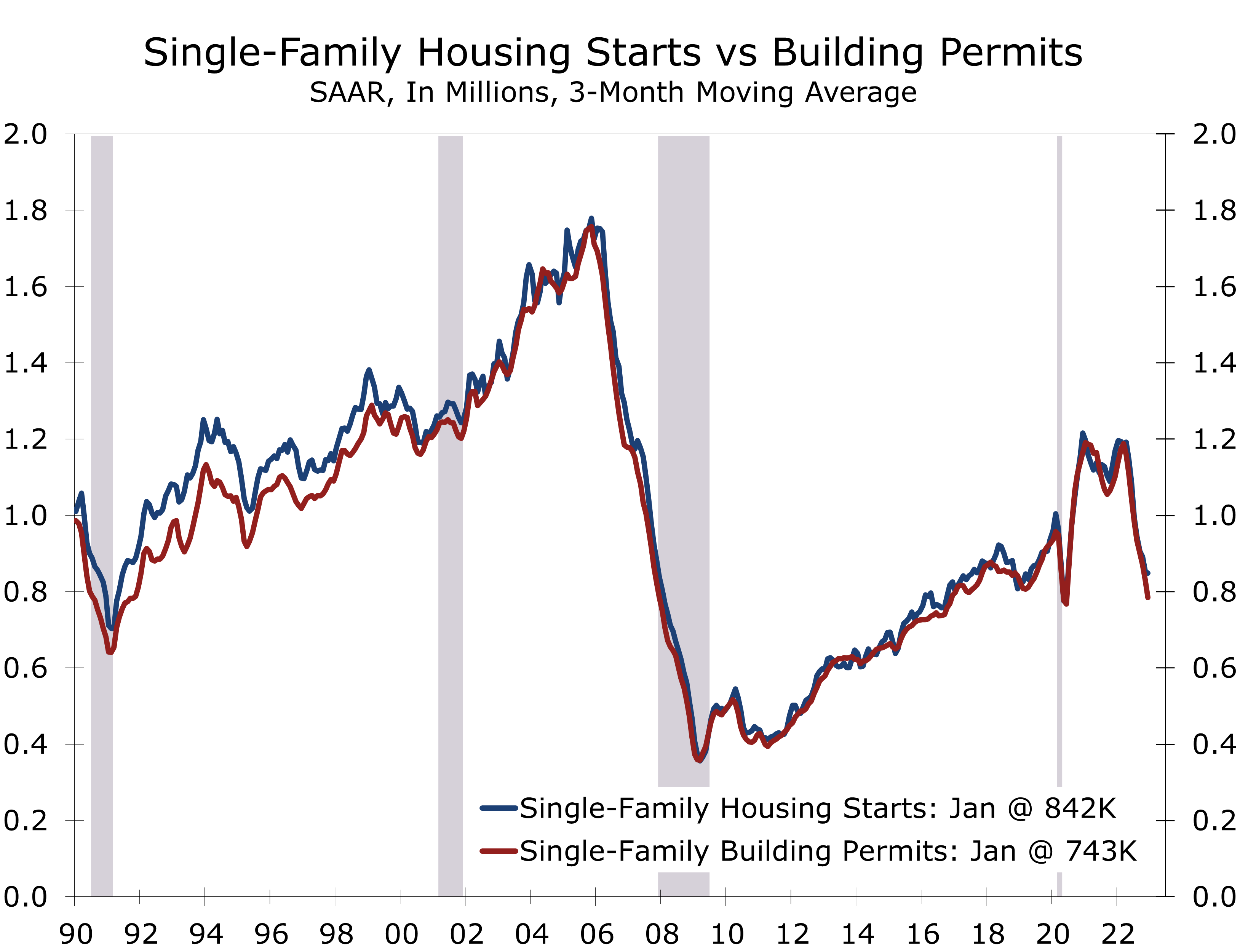

- Housing starts fell 4.5% to a 1.309-million unit pace. Single-family starts fell 4.5% to an 841,000 unit pace, while multi-family starts fell 4.9% to a 468,000-unit pace.

- The monthly housing starts data are extremely volatile during the winter months, when swings in weather conditions can lead to wide month swings.

- Weather appears to have influenced the data, with starts plunging 42.2% in the Northeast and 25.9% in the Midwest but rising 7.3% in the South and 5.5% out West.

- Permits are less impacted by the weather and were little changed in January.

- Last year’s slide in housing starts may be subsiding. The NAHB Home Builders’ Survey improved for a second month in February, reflecting a rise in present sales.

- Home builders continue to work down their backlog of work in process, with many making a concerted effort to get lean.

January’s 4.5% decline in housing starts broke a nascent string of improving reports for the housing sector. Home builders have reported a rise in buyer traffic in recent months and pending home sales and mortgage demand had shown some promise. Our sense is the pullback in mortgage rates brought some buyers back to the market that had canceled deals or put off home purchases when mortgage rate were closer to 7%. Those buyers came back in when rates fell back closer to 6%. Many builders also offered incentives to buy down mortgage rates.

While we would like to join the rising chorus of analysts expressing optimism about the housing market, we remain more cautious. Affordability remains extremely challenging and we have only seen a modest rebound in buyer traffic. Home builders have a huge backlog of single-family homes under construction and are actively working to reduce their inventory of completed homes and work-in-process.

Starts and permits still appear to be trending lower, as builders work to reduce inventory.

Housing starts are extremely volatile during the winter, particularly single-family starts, which rose 8.9% in December. Most of that rise was in the Northeast, where starts nearly doubled. Starts plummeted back to their prior trend in the Northeast in January but jumped to their highest level since June in the South, where weather was unusually mild. Permits are less influenced by the weather and do not show these wide swings. Starts and permits are both trending lower on a three-month moving average basis.

Multi-family starts fell 4.9% in January, while permits rose 2.5%. Both starts and permits are trending lower on a three-month moving average, however, as apartment developers appear to have their hands full with projects currently underway.

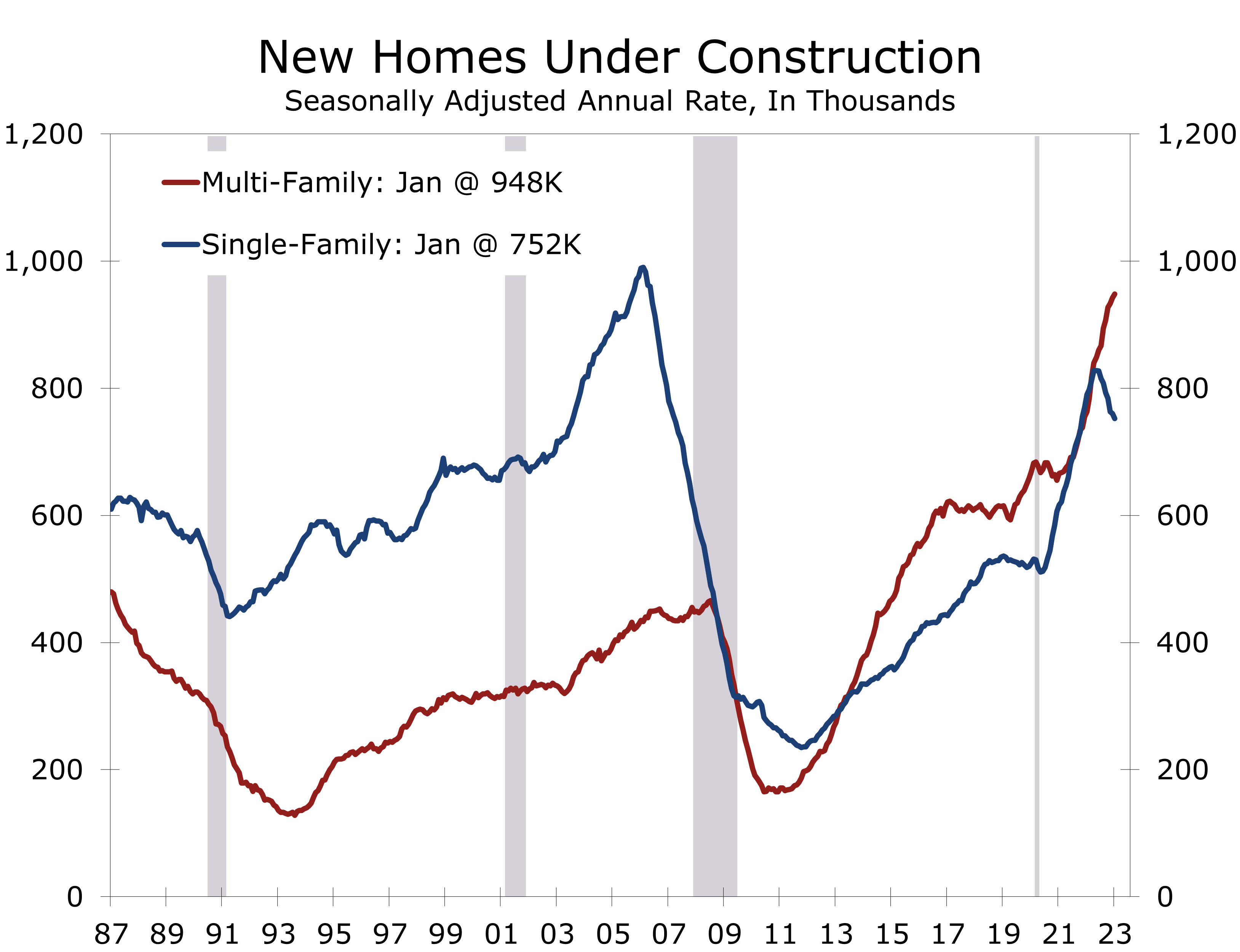

Shortage of materials and workers and the preponderance of mid-rise and high-rise apartment projects has stretched out the timeline for completing apartment developments. The number of multi-family units under construction, the overwhelming majority of which are apartments rose by 6,000 in January to a 948,000-unit pace, which is the highest since 1974. The number of authorized multi-family permits that have not been started also continues to trend higher.

Rents have been falling the past few months and lenders have tightened underwriting.

Demand for apartments has weakened in recent months, largely reflecting affordability issues. Rents have been declining the past few months and lenders have tightened underwriting standards for new developments. All signs point to fewer new multi-family projects entering the pipeline until the backlog of developments begins to clear and participants have a better sense of how demand is holding up. We are looking for around a 15% pullback in multi-family starts this year, and about a 20% drop in permits.

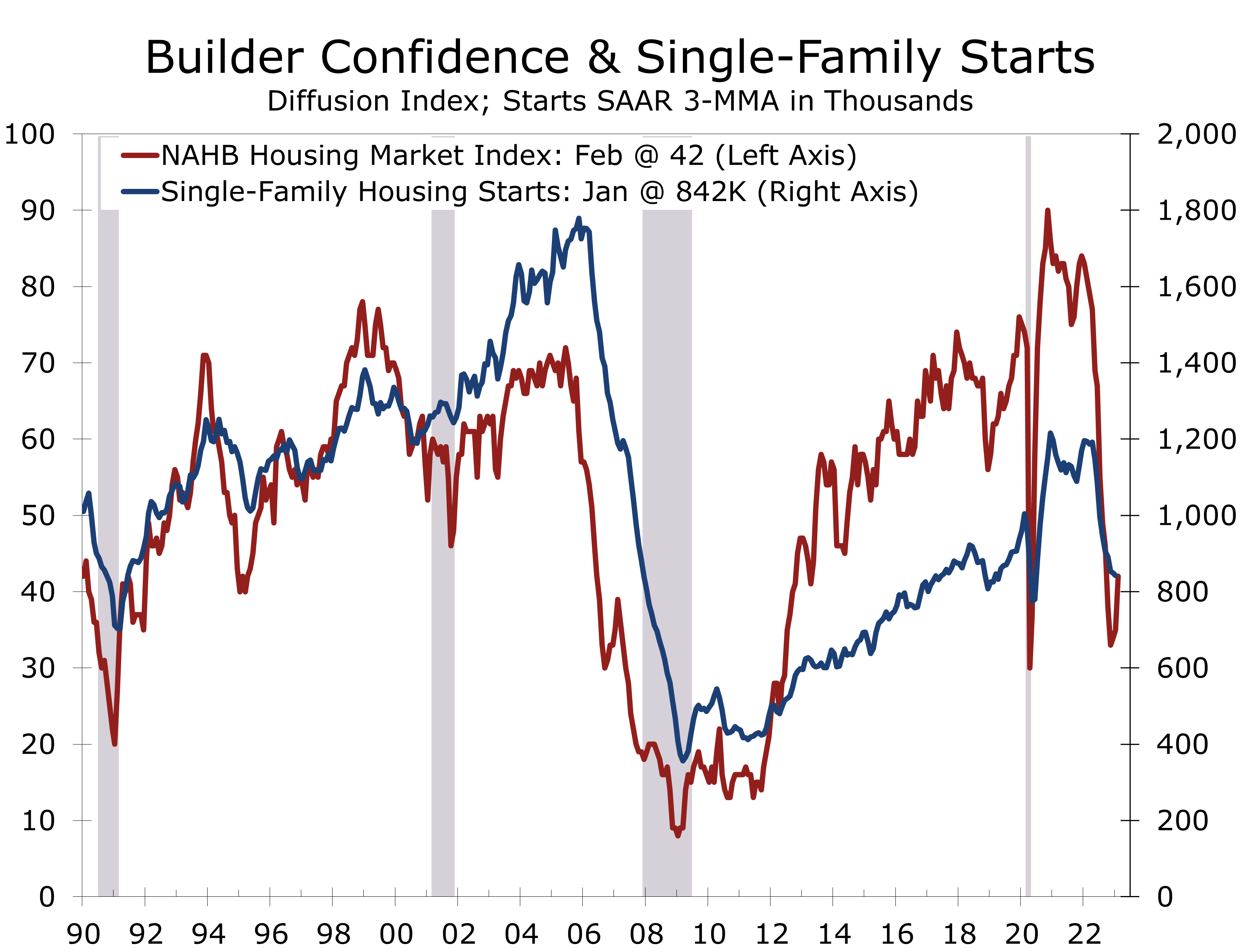

Back-to-back improvements in the NAHB/Wells Fargo Housing Market Index (HMI) boosted optimism ahead of January housing starts. The HMI jumped 7 points in February to 42, after rising 4 points in January. Any reading below 50 means more builders see conditions deteriorating than see them improving.

We suspect new home sales rose in January, confirming the improvement in builder sentiment.

The present sales index rose 6 points to 46, after rising 4 points in January. Expected sales over the next six months rose 9 points to 48, while prospective buyer traffic rose 6 points to 29. We suspect new home sales rose in January, reflecting lower mortgage rates and various incentives by builders to bring buyers back to the table. Builders have mostly been buying down mortgage rates, to reduce the sting from rising rates.

We feel it would be a mistake to interpret the bounce in builder confidence as a sign the housing market is stabilizing. Housing starts are almost certainly headed lower, as interest rates remain higher for longer. Builders will concentrate on clearing their construction backlog and will discount prices to point. Other than lumber, however, raw material prices are still rising.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Inflation Perks Back Up in January

Inflation Perks Back Up in January

- The Consumer Price Index rose largely in line with market expectations. The headline index rose 0.5% and the core rose 0.4%.

- The slide in inflation, so apparent during the second half of last year, is now moderating.

- The BLS updated the weights assigned to various components of the CPI to reflect the most recent survey of consumer spending patterns and updated their seasonal factors.

- Revisions to the seasonal factors slightly reduced inflation in the first half of last year and slightly raised it during the second half.

- Prices for food and energy items picked up in January, with food costs climbing 0.5% and energy prices rising 2%.

- Prices for labor-intensive services rose notably, including hotels (1.5%), nursing homes (1.4%), car repair (1.3%) and food away from home (0.6%).

- The January inflation data is supportive of recent Fed statements that “ongoing increases” in the federal funds rate target would be appropriate.

The monthly Consumer Price Index report continues to rival the employment report as the key piece of information released each month. The latest report came in close to expectations, which had been prepared for firmer price hikes by last week’s release of revised seasonal factors and component weights for the index. Those revisions had taken the shine off the lighter inflation numbers initially reported late last year. Most notably, December’s previously reported 0.1% drop in the headline CPI is now a 0.1% increase.

The adjustments to the seasonal factors and component weights will make the inflation data more relevant with current economic behavior. The shelter categories have been slightly increased, while weights for used cars and some other core goods – which saw prices fall last year – have been slightly reduced.

Shelter costs, which account for 43% of the core CPI, remain problematic. Rent and owners’ equivalent rent each rose 0.7% in January, even though market measures of asking rent for new tenants have eased considerably. The CPI measure of rents includes rents for new tenants and renewals of existing residents, the bulk of which are seeing significant increases due to earlier spikes in asking or market rents. Prices for hotel and motel rooms rose 1.5% in January, following a 1.2% rise the prior month and is up 8.5% year-to-year.

Residential rent and owners’ equivalent rent each rose 0.7% in January.

The bulk of the deceleration in inflation last year came from falling energy prices and lower prices for used cars. Further progress on each will be difficult this year.

Energy prices fell sharply during the second half of 2022, benefitting from the record drawdown of reserves from the Strategic Petroleum Reserve and warmer than usual winter weather in Europe and the Northeast U.S. With heightened geopolitical pressures around the world, the now severely depleted Strategic Petroleum Reserve will need to be refilled, which will effectively put a floor under oil prices.

Used car prices will also provide less help in containing inflation. While used car prices fell 1.9% January, the Manheim used car price index edged higher, signally the bulk of price declines are behind us. Moreover, new car inventories remain exceptionally low, which should continue to divert demand to used cars. Higher vehicle prices are also fueling steep price gains for auto insurance, with the cost of vehicle insurance rising 1.4% in January and climbing 14.7% over the past year.

Higher vehicle prices are fueling steep price increases for auto insurance.

Food prices most likely head the list of consumers’ frustration today. Prices for food at home, which is mostly groceries, have spiked 11.3% over the past year. Eggs are the greatest source of pain, with prices surging 8.5% in January and 70.1% over the past year. Prices for many other food items, including meats (0.0%), pork (0.0%), poultry (-0.1%) and fish (-0.1%) all moderated in January, continuing recent trends.

The most problematic area for inflation remains core services, which include shelter as well as several labor-intensive categories. There has been considerable blowback at the BLS for how shelter costs are measured, with the BLS measuring rents paid for rental housing and the implied rent paid by homeowners. We feel the BLS’s measure is correct, with the 34% weight in the CPI closely corresponding with the share of income households devote to rent or its equivalent.

While the CPI rent measure lags several market measures, it does a good job of capturing actual changes in housing costs. Renters are facing steep increases as leases renew. Moreover, with more than a third of expenses tied to rent, higher residential rents feed back into wage demands.

With more than a third of expenses tied to rent, higher rents feed back into wage demands.

January’s CPI data, combined with the earlier reported stronger jobs data, have cleared the way for the Fed to move forward with hiking interest rates. Market expectations for the federal funds rate are now in line with the Fed’s, calling for at least two more quarter-point rate hikes this year and anticipating no cuts in interest rates until 2024 or later.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Small Business Optimism Rises Modestly in January

Small Businesses See Modest Improvement

- Small Business Confidence began the year on a slightly more optimistic note.

- The National Federation of Independent Business (NFIB) Small Business Optimism Survey rose 0.5 points to 90.3 in January.

- January’s rise primarily reflects a decline in pessimism rather than any sudden recognition of more positive trends.

- The share of business owners expecting the economy to improve rose 6 points to -45%.

- Many of the largest gains were tied to hiring and compensation, both of which remain strong and reflect the exceptionally tight labor market.

- The share of firms raising prices fell 1 point to 42% in January.

- The share of firms making capital expenditures over the past 6 months rose 4 points to 59%. Business owners, however, remain cautious about capital spending and inventories in the coming year.

January’s 0.5 percentage point rise in the NFIB Small Business Optimism Index primarily reflects a slight drop in pessimism among small business owners rather than rising optimism. The proportion of firms expecting the economy to improve in coming months rose 6 points but remains exceptionally low at -45%. Most of the other components posting large gains were tied to hiring and compensation, which is clearly a double-edged sword right now. Hiring plans rose 2 points to 19% but a whopping 45% of firms had job openings they have not been able to fill.

Less pessimism is still better than the alternative and there were some notable positives within the report. The share of firms reporting they made capital outlays during the past 6 months rose 4 points to 59%. Earnings trends also improved, rising 4 points to a less negative 26%. The net share of firms raising prices also fell 1 point to 42%.

The net share of firms raising prices over the past three months fell 1 point to 42%.

Price hikes were most prevalent in construction, retailing, wholesale trade and transportation. The share of firms hiking prices remains well above levels historically consistent with the Fed’s 2% inflation goal. Plans to raise prices rose 5 points in January to 29%.

Labor market conditions remain much closer to the peak levels than where they would be if the economy was truly on the precipice of recession. The NFIB noted that 57% of small business owners reported they were hiring or trying to hire in January, which was up 2 points from December. Of those businesses hiring or trying to hire, 97% reported they had few or no qualified applicants for their open positions.

Fifty-seven percent of small business owners were hiring or trying to hire in January.

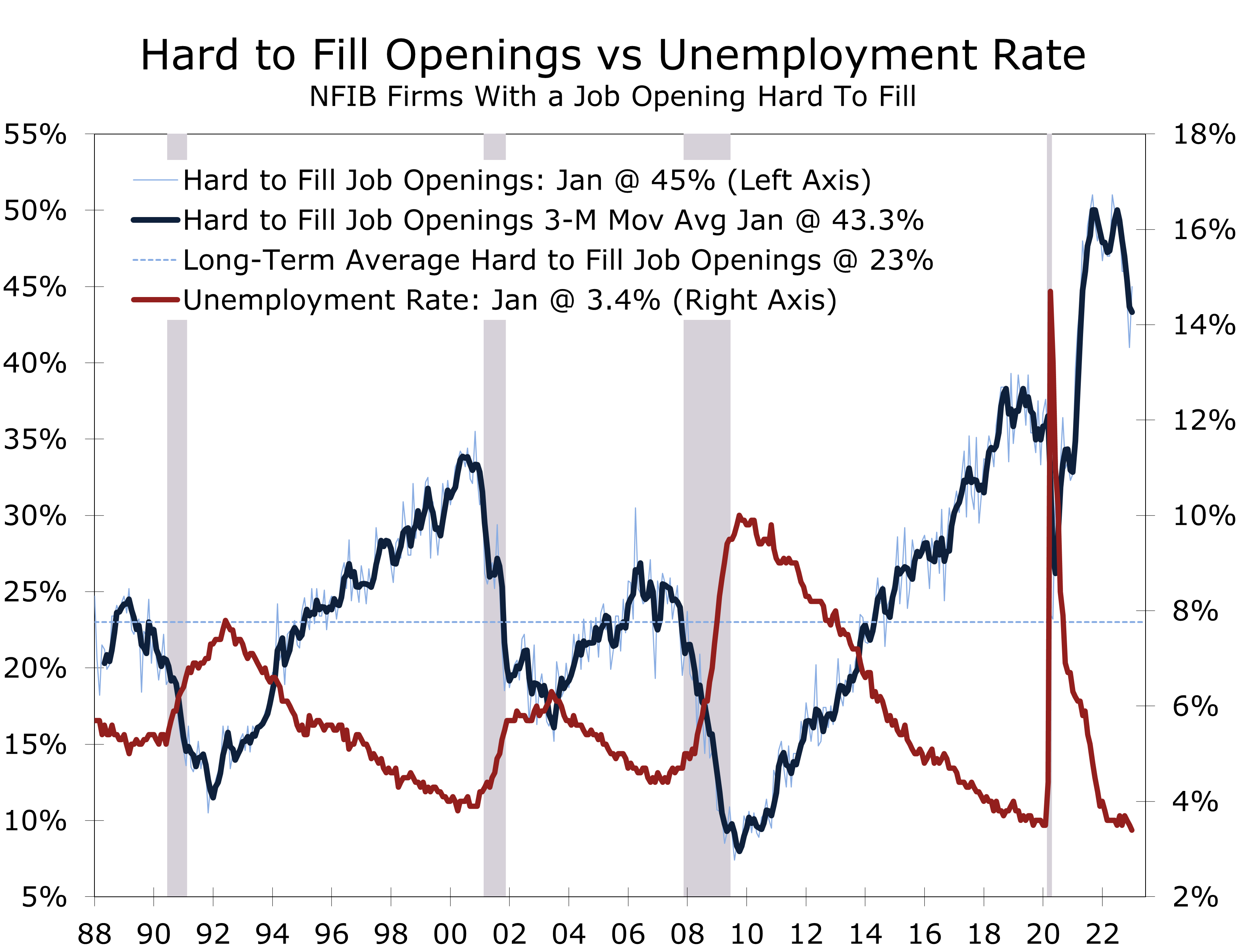

After showing some incipient signs of loosening, the labor market tightened further in January, a month that saw the unemployment rate fall to 3.4%. The NFIB noted that 45% of small business owners reported they had job openings they could not fill in January, which is up 4 points from December and just 6 points below its all-time peak of 51% hit in May 2022. The long-run average for job openings, dating back 49 years, is 23%, a level last seen in early 2014.

While lower unemployment rates are often celebrated as a sign of economic success, there appear to be structural impediments in the labor market today that make it tougher for businesses to hire even when the economy is growing only modestly. Ongoing shortages of workers are forcing business owners to boost compensation, hire less qualified workers, reduce operating hours, or offer fewer products and services.

Concerns about the quality of labor have risen to historic heights, with 24% of small business owners rating labor quality as their top concern. Another 10% of business owners rate labor costs as their top problem, which is up 2 points from December.

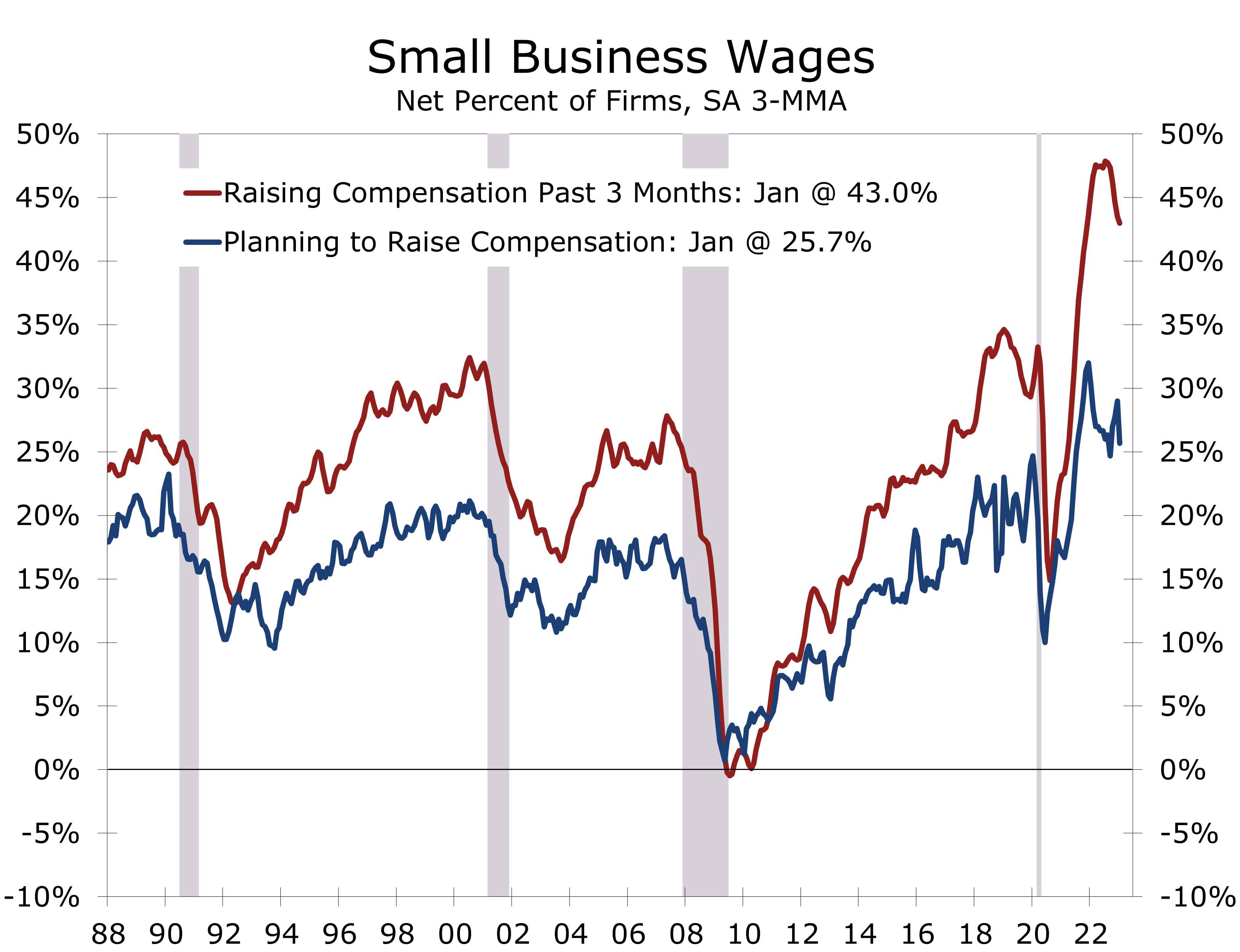

With labor markets so tight, businesses are having to pay more to attract and retain workers. A net 46% of business owners raised compensation during the past 3 months, which is up 2 points from the December and just 4 points below the record high hit in January of last year. The share of firms planning to raise compensation fell 5 points in January to 22%.

Significantly more businesses are boosting compensation than are planning to.

The share of businesses boosting compensation is more than twice the share planning to raise compensation. The gap is historically wide and provides insight into the persistence of stiff price hikes in labor-intensive parts of the economy as well as the ongoing pressure on operating margins.

Businesses are passing along their higher costs. Inflation in the most labor intensive parts of the economy rose 0.6% in January and is up 7.2% year-to-year. Today’s NFIB report shows the labor market remains too tight to support a sustained deceleration in wages and prices. The persistence of wage and price pressures raises the likelihood the Fed will raise rates a little higher this year and hold them there longer.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Stronger Employment Growth Shows the Economy Is Not Landing Anytime Soon

Employment Surges in January

- Nonfarm employment surged by 517,000 jobs in January, which was more than double consensus estimates.

- While hiring was led by another big jump in hiring at restaurants and bars, job gains were extremely broad based.

- The most cyclical parts of the economy -construction, manufacturing and trucking and warehousing – added a combined 66,900 jobs.

- Seasonal factors bolstered the overall job growth. More cautious holiday season hiring at retailers and delivery firms resulting in fewer than usual layoffs and a big seasonally adjusted gain in January.

- The unemployment fell 0.1 percentage point to 3.4%, while average hourly earning rose 0.3% and are now up 4.4% year-to-year.

- Aggregate hours worked rose a whopping 1.5% in January, which pushes any thoughts about a recession at least a few months out.

There is quite a bit to unpack from this morning’s surprisingly strong employment report. The bottom line is job growth remains exceptionally strong. The January data include annual revisions to nonfarm employment, which incorporate more precise data on hiring. The benchmark revisions, combined with more complete reporting for the prior two months, show there were 813,000 more jobs on nonfarm payrolls in December than first reported. The benchmark revision was three times as large as normal.

Population estimates in the Household Survey were also adjusted to updated population estimates from the Census Bureau. The new data show a 1.1 million increase in the civilian population, and large related increases in the civilian labor force and the household employment measure. There was no net effect on the unemployment rate, which fell to 3.4%. The adjustment boosted the civilian labor force and employment-population ratio by 0.1% each. Both would have been unchanged without the new controls and will likely be reversed in February.

We believe it is still too early to assess the impact of the recent surge in tech layoffs.

The stronger nonfarm employment data appear to contradict the rising number of layoff announcements, most of which are in the tech sector. Weekly first-time unemployment claims have continued to trend lower. We believe it is still too early to assess the impact of layoffs. While employment fell slightly in some tech categories, many displaced workers will not fall off employer payrolls until March. This means these losses will show up in the March and April employment reports, which will be released in April and May.

The upward revision to nonfarm employment also appears to contradict the findings of a recent Federal Reserve Bank of Philadelphia report, which pointed out job growth for the second quarter of last year appeared to be overstated by around 1 million jobs. That survey highlighted to the gap between the Quarterly Census of Employment and Wages (QCEW), which are the source data for the annual benchmark revisions, and the reported CES data. The Benchmark revision, the bulk of which stretches back to March 2021, would not include the second quarter 2022 QCEW data. So, today’s large upward revisions do not refute the Fed study.

The 2022 nonfarm data will be revised once again next February, and we will get some idea of the scope of those revisions when the QCEW data for the third quarter of 2022 will be released on February 22. Our sense is we will a see sizable downward revision next February. There are a whole host of government and private sector data that show economic activity moderating considerably since March 2022, which is when the Fed began to hike interest rates.

Even if we do see a downward revision to the 2022 employment data next year, the labor market clearly looks much stronger today. Any notion of an imminent recession has been pushed further out. Hiring rose across nearly every major industry in January, with even the most cyclical industry segments – construction, manufacturing and transportation and warehousing – adding a combined 66,900 jobs.

The factory workweek rose by 0.4 hours to 40.5 hours, and overtime hours rose 0.1 hour to 3.1 hours. The rise in hours suggests manufacturers are still looking to add workers. This is somewhat surprising given January’s weaker ISM-Manufacturing report and a whole host of weaker regional manufacturing surveys but is consistent with the rise in job openings. Total hours worked in manufacturing – a reliable predictor of industrial production – rose 0.9% in January.

One reason economists closely scrutinize the monthly jobs data is they provide clues about data for the rest of the month. In addition to a rise in industrial production, consumer spending should also rebound, following back-to-back declines. We come to that conclusion by combining the 1.2-point surge in aggregate hours worked and 0.3% rise in average hourly earnings.

The smaller rise in average hourly earnings likely reflects more hiring in lower paid occupations and some moderation in hiring for higher paid jobs. With the unemployment rate now at its lowest level since May 1969, we can expect the Fed to continue raising interest rates for at least the next couple of meetings.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

The Federal Reserve Hikes Interest Rates Amidst Reports of Moderating Economic Growth

A Busy Day for Economic News

- The Fed raised its federal funds rate target a quarter percentage point to between 4.50% and 4.75%. The Fed also indicated ongoing increases will be appropriate.

- Consumer spending rose at a solid 2% pace, with the strongest gains coming in services.

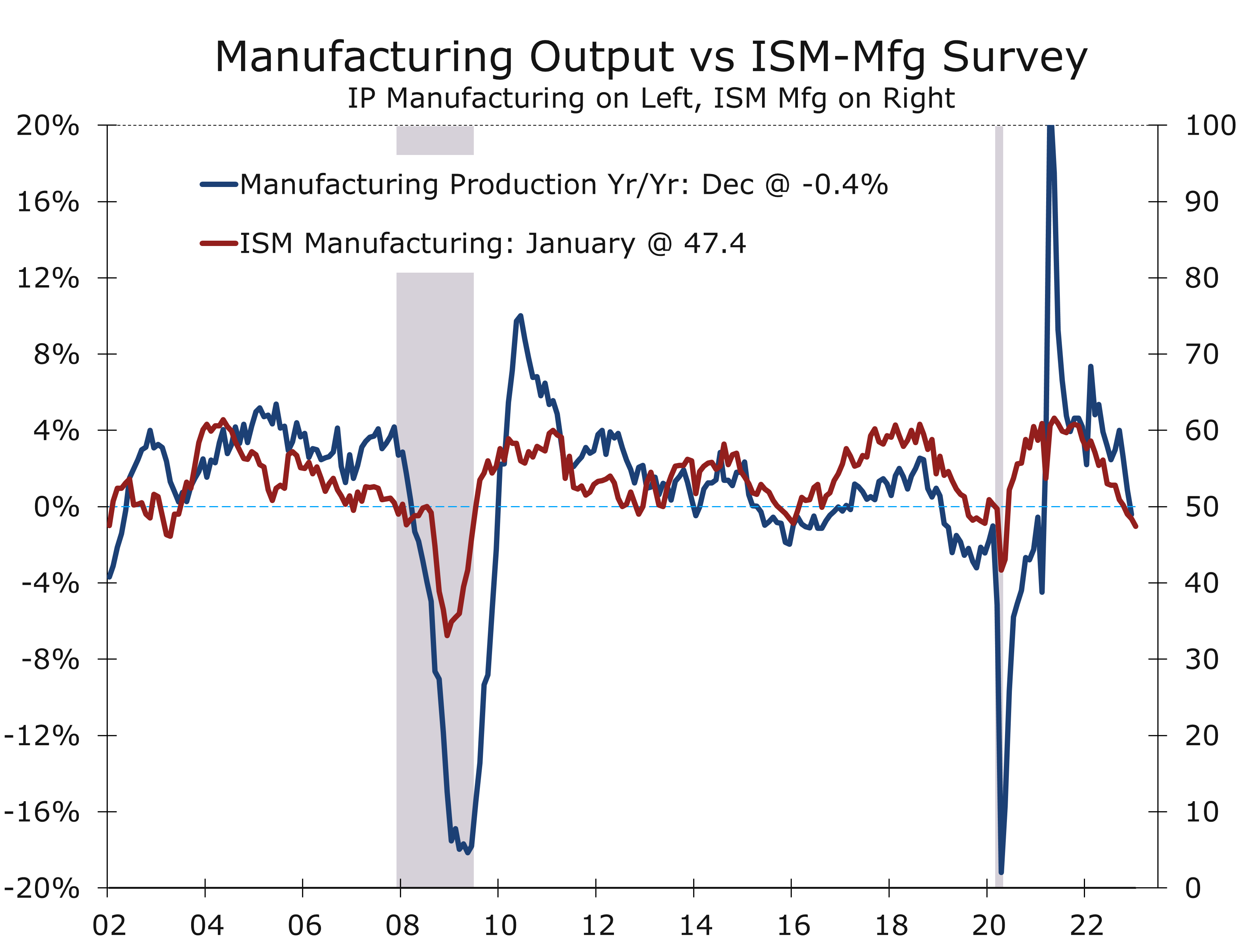

- The ISM Manufacturing Index fell 1 point to 47.4 in January, marking the fifth consecutive monthly drop.

- Overall construction spending fell 0.4% in December. Spending for private single- family homes fell a particularly sharp 2.3%.

- The ADP employment report showed hiring slowed in January, with private sector businesses adding 106,000 jobs, following a 253,000-job gain in December.

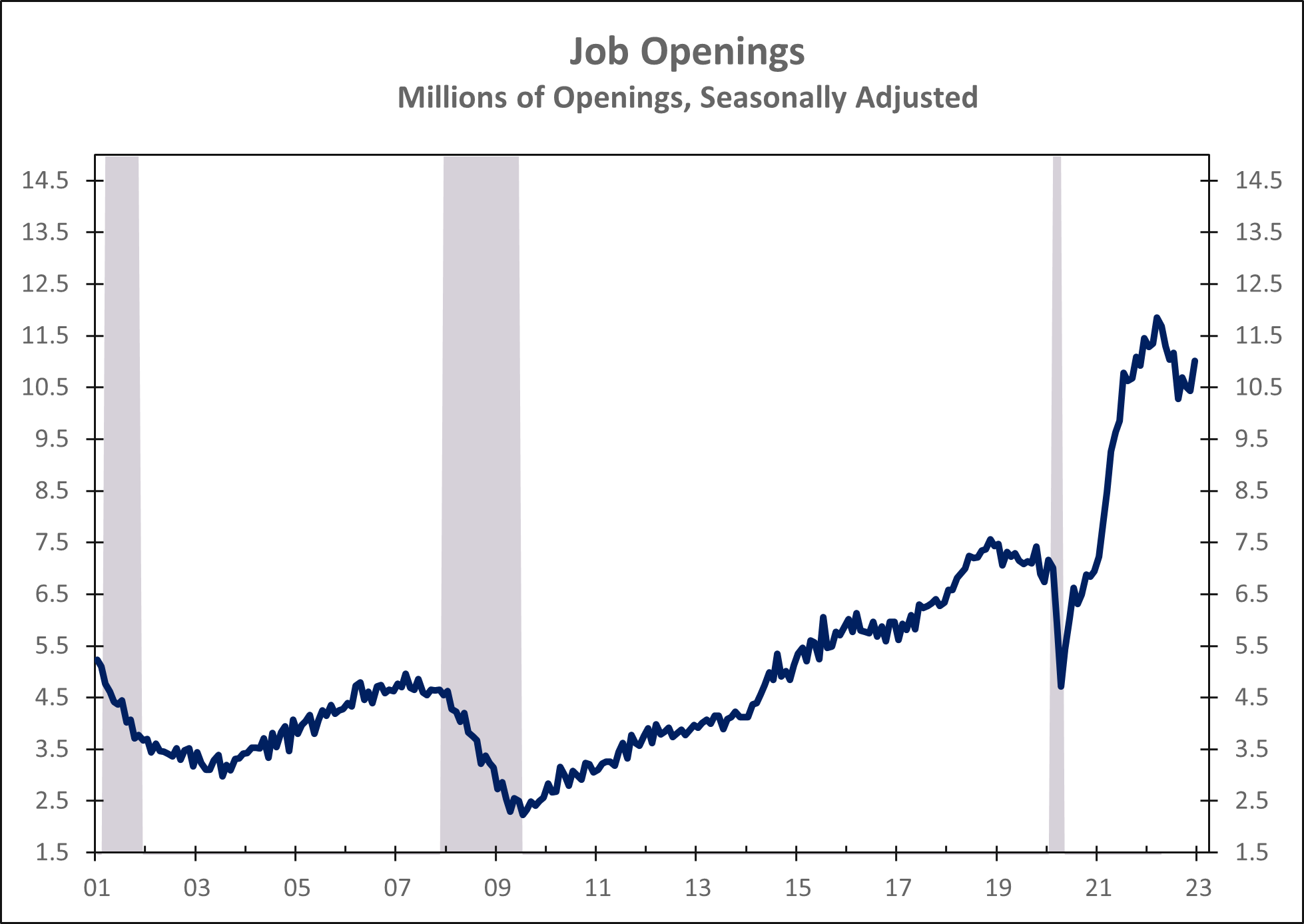

- Job Openings increased by a larger than expected 572,000 in December to 11 million. The bulk of the increase was in the leisure and hospitality sector. Openings fell in the IT sector and in manufacturing.

The Federal Reserve raised interest rates precisely in line with market expectations. The range for the federal funds rate target was increased by a quarter point to between 4.50% to 4.75%. The FOMC also noted they anticipate “ongoing increases in the target range will be appropriate.” Our read is the Fed is looking past the easing in supply chain inflation pressures and now sees tight labor markets and rising wages as the greatest risk to inflation.

The Fed’s assessment of economic conditions in the meeting’s Policy Statement was surprisingly upbeat, noting “recent indicators point to modest growth in spending and production.” The most recent data, however, show back-to-back declines in real consumer spending and three consecutive declines in industrial production. This morning’s ISM manufacturing survey shows even more convincing weakness, with the index declining for five consecutive months and hinting industrial production fell once again in January.

Employment conditions remain too strong for the Fed to end their policy tightening.

Employment conditions appear to be closer to the Fed’s assessment, which noted “job gains have been robust in recent months, and the unemployment rate has remained low.” The latest data are clearly supportive of that view, with weekly first-time jobless claims, the unemployment rate at 50-year lows and job openings rising by a surprisingly 572,000 to just over 11 million in December. Even this morning’s weaker ISM survey showed employment conditions in the factory sector remaining in positive territory, possibly suggesting manufacturers are hoarding working amidst and exceptionally tight labor market.

The Fed now sees the greatest risks to inflation coming from wages rising significantly faster than productivity growth due to the incredibly tight labor market. Chair Powell noted the disinflation process was now well underway, with consumers backing off goods purchases, which has helped ease supply shortages. Housing costs are also beginning to moderate. Powell described this as completing about half the job in bringing inflation back down. The key issue now is price pressures in more labor intensive parts of the service sector, with one of the key variables to watch being consumer prices for services, excluding shelter.

Powell’s tone in the press conference was considerably more balanced. While the inclusion of “ongoing increases” in the Fed’s statement remains consistent with the dot plot released in December, showing two more quarter point federal funds rate hikes, Powell did not put down the financial market’s notion the Fed only has one more rate hike. He reconciled the difference as to financial market participants perhaps being more optimistic about inflation coming down than members of the FOMC currently are.

Powell also appears to have shrugged off the recent easing in financial market conditions. Stock prices rose solidly in January, while bond yields declined. With consumer spending and industrial output declining, the Fed may now see an easing in financial conditions as something that would make a soft landing more likely. By contrast, Powell’s terse press speech at the Jackson Hole conference was widely seen as a warning to the financial markets to not get ahead of themselves and price in lower inflation and a Fed pivot. Today, the Fed is likely relieved mortgage rates have backed off their recent highs, which should help stem to slide in home sales and single-family home building.

The Fed now sees easing financial conditions as something that will help achieve a soft landing.

Powell mentioned the FOMC reviewed the latest Job Openings and Labor Turnover Survey (JOLTS) reported this morning. The data showed a surprising 572,000 increase in job openings in December. Most of these openings were in the leisure and hospitality sector, which includes hotels, restaurants, and entertainment venues – all of which have struggled to rehire staff following the pandemic. Job openings in the IT sector and manufacturing both declined in December.

While the Fed would like to raise rates a couple more times and bring the federal funds rate above 5%, the window for them to do so may not remain open that long. We doubt the Fed will continue to raise interest rates once nonfarm employment begins to decline, which we believe may occur before the May meeting.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.