Job Growth Rebounds Less Than Expected

Hiring Has Clearly Lost Momentum

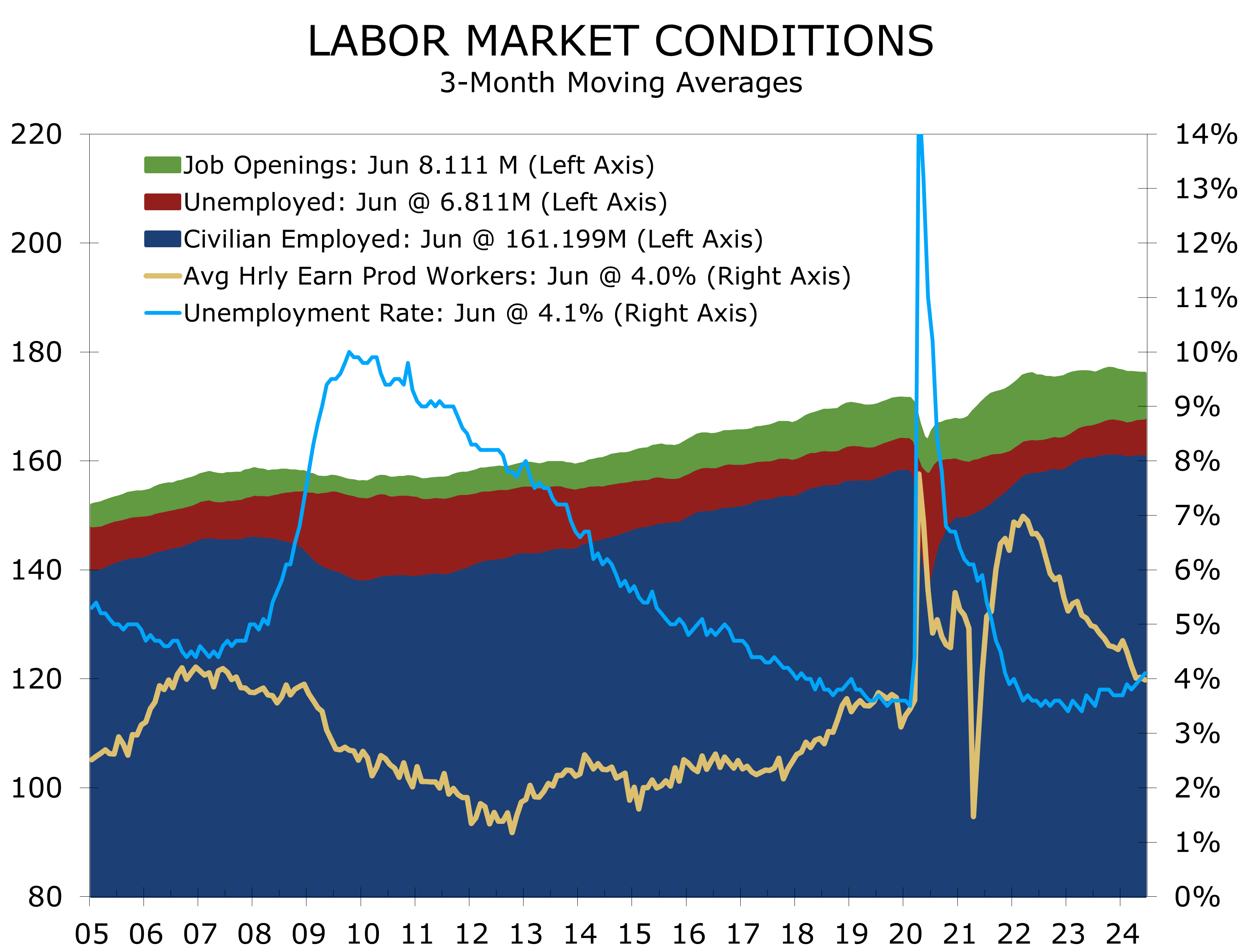

- Employers added 142,000 jobs in August, falling well below the 12-month average of 202,000. Revisions to June and July payrolls lowered job gains by a total of 86,000, emphasizing the ongoing slowdown in economic momentum.

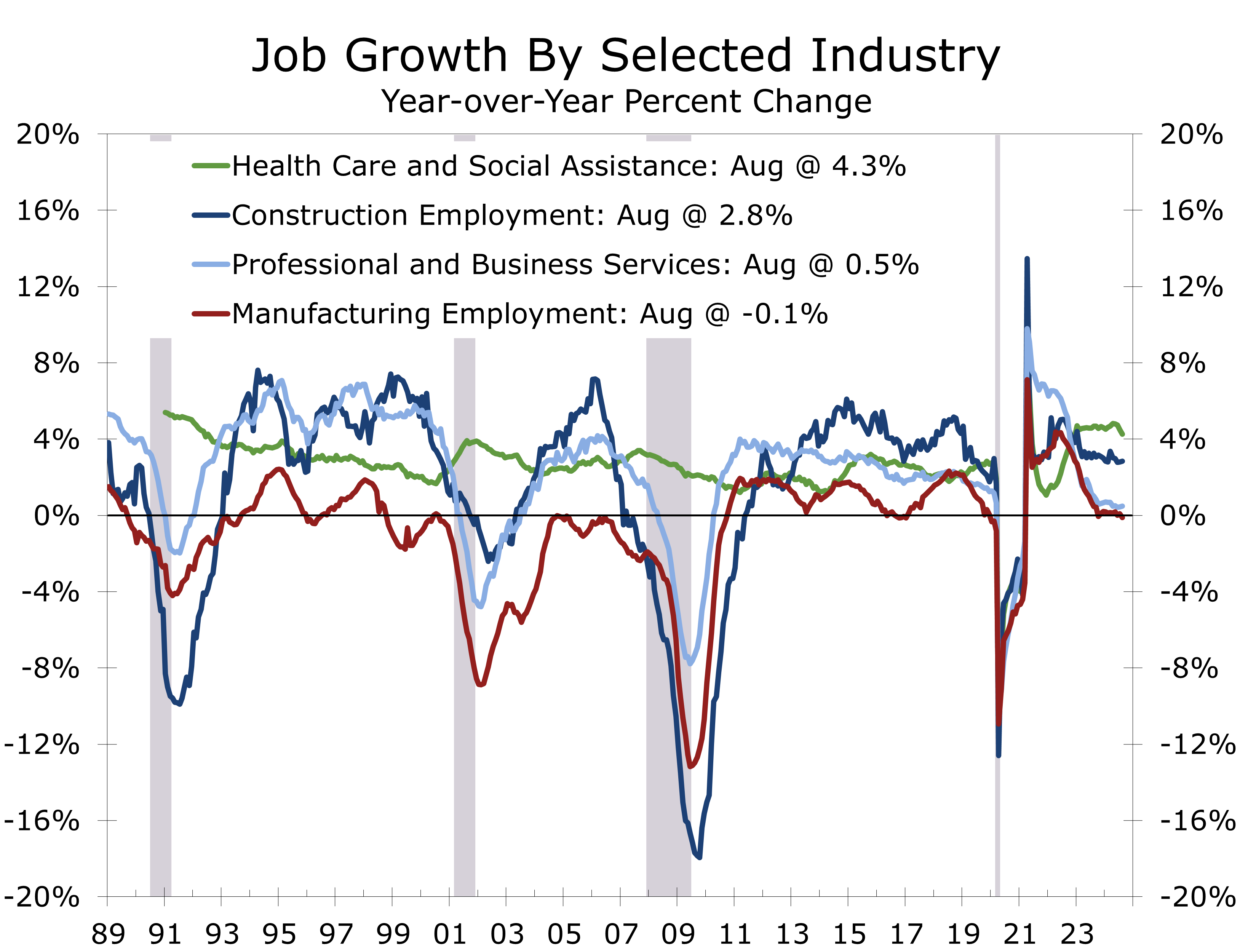

- Leisure and hospitality (+46K), health care and social assistance (+44.1K), construction (+34K) and government (+24K) continue to account for the bulk of net new jobs (80%+ of the total).

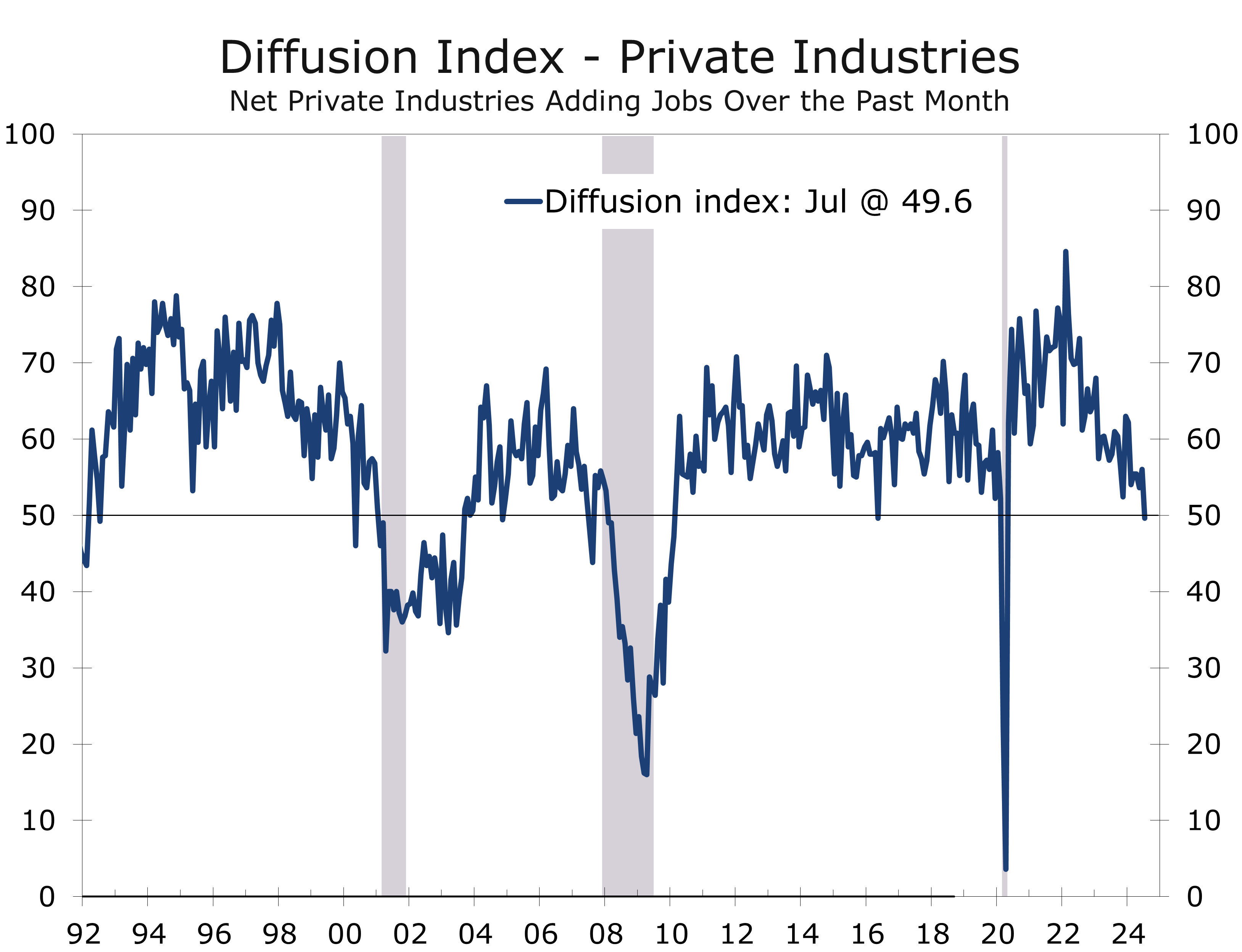

- The diffusion index improved slightly, climbing 5.4 point to 53.2. July is the only reading below 50 since the Pandemic.

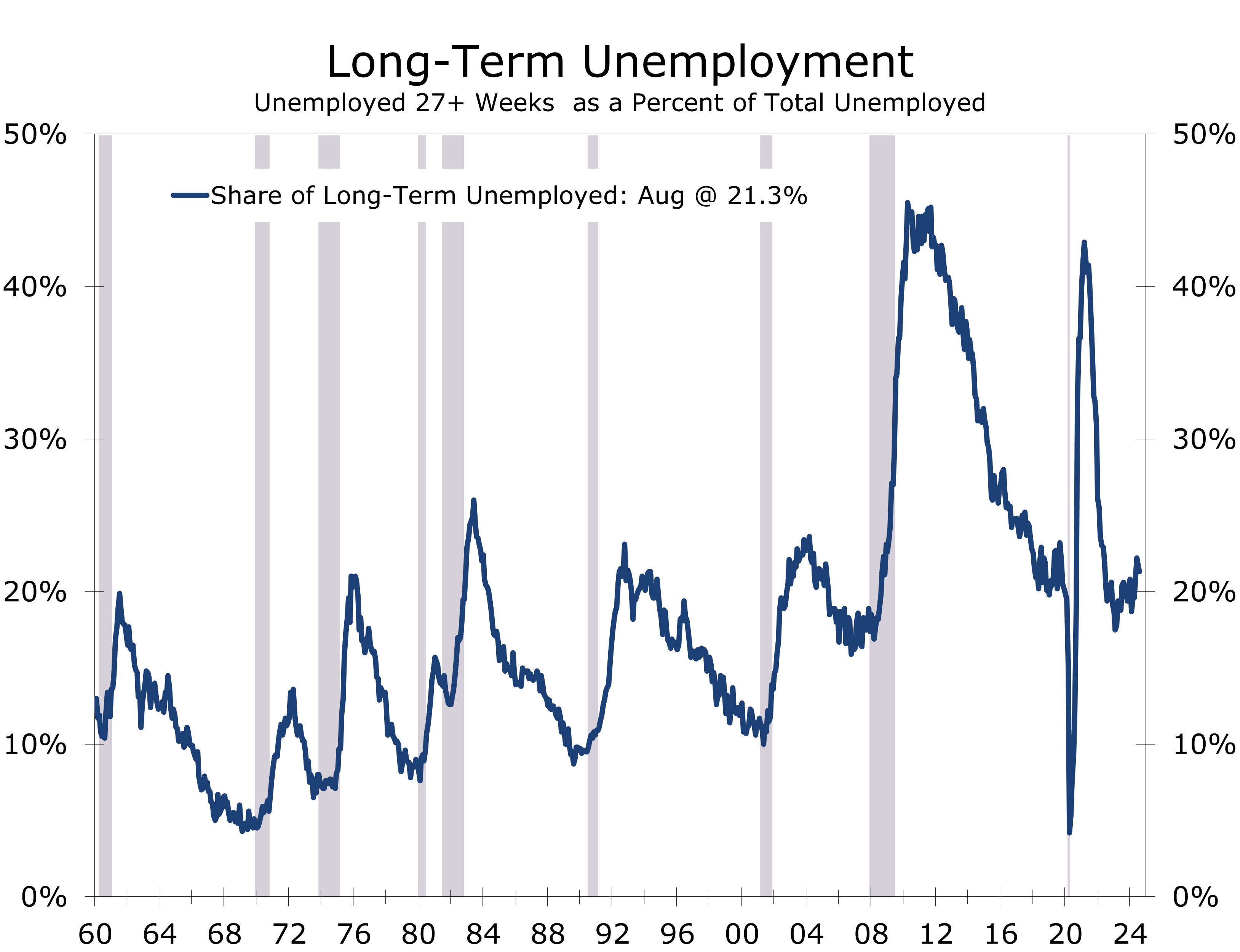

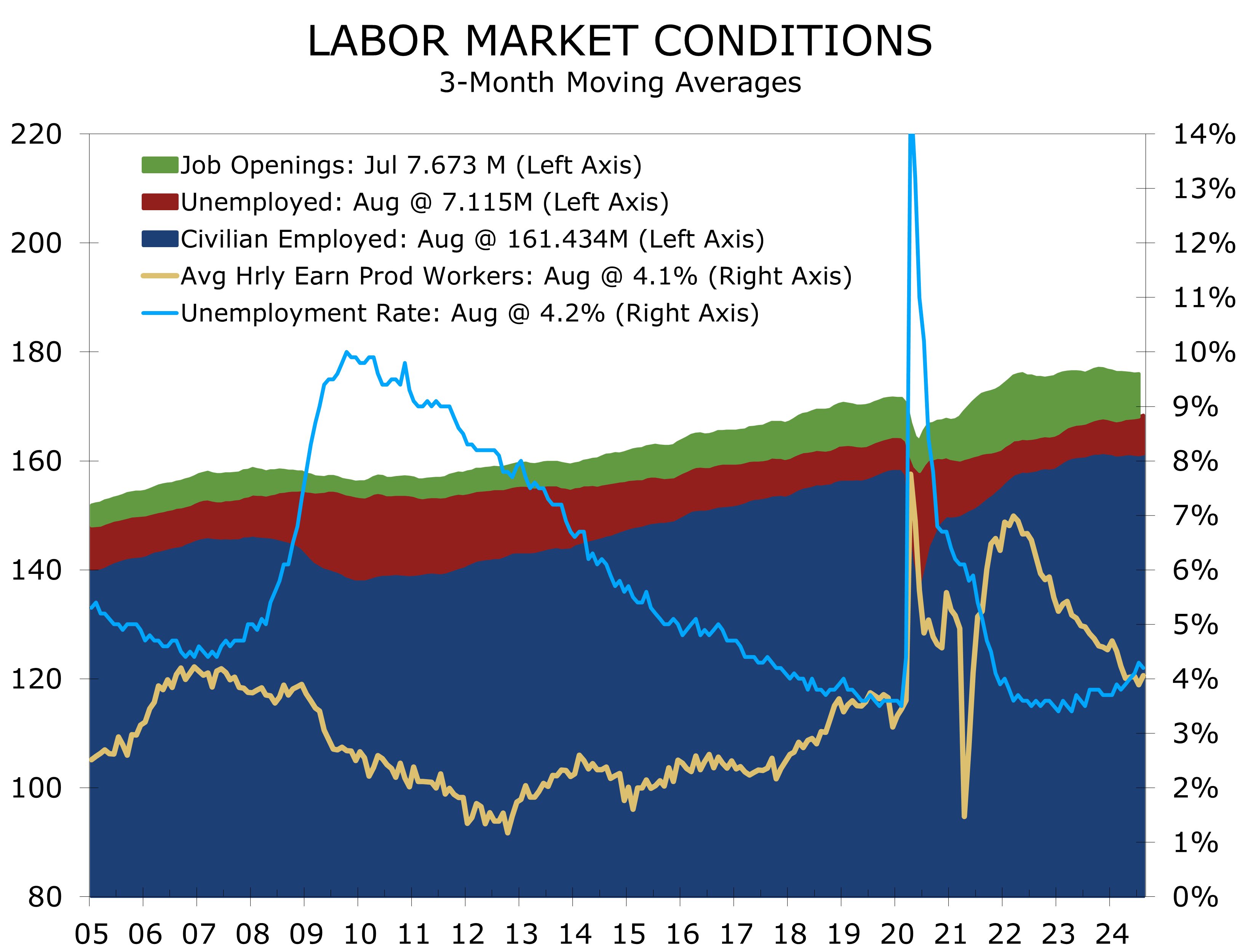

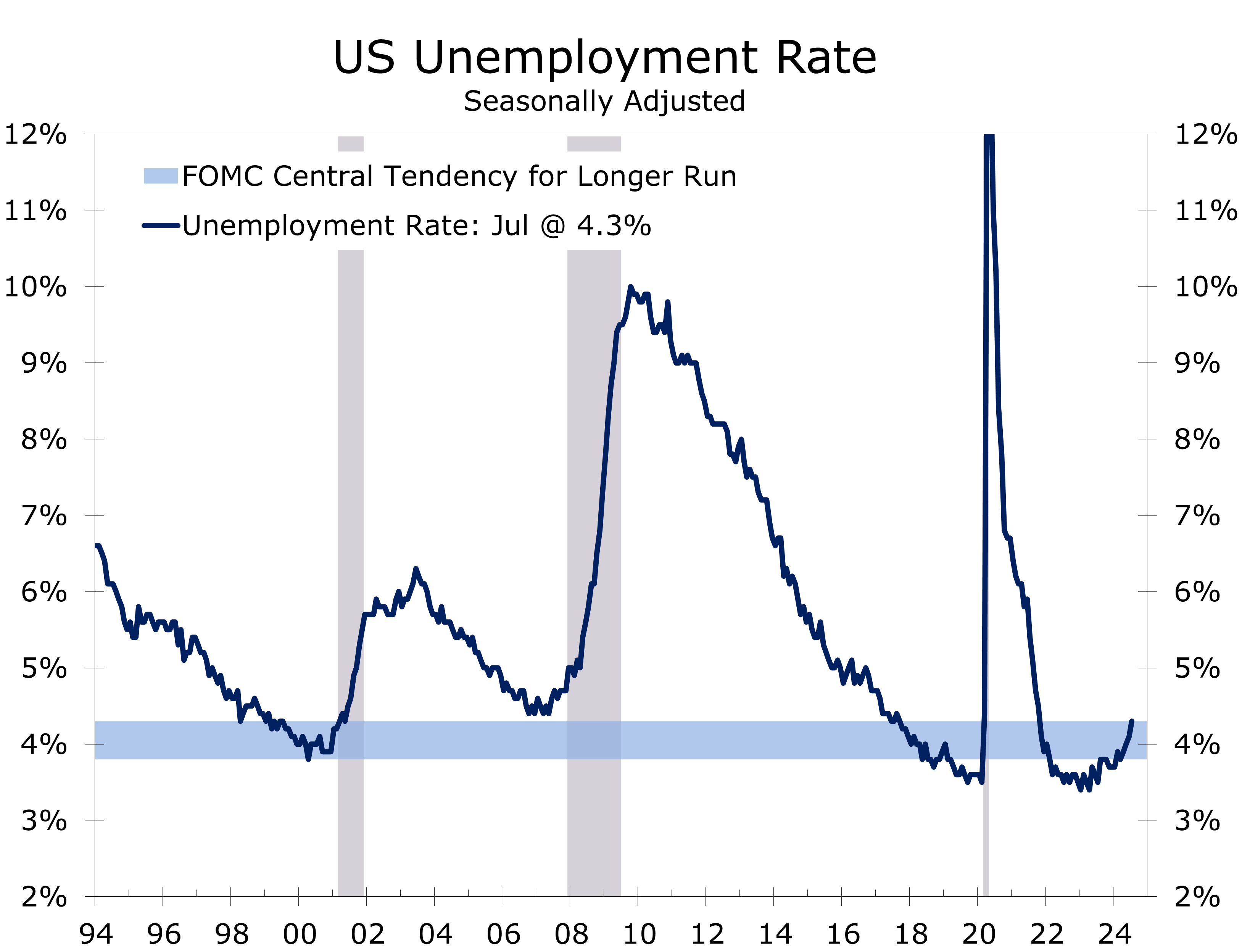

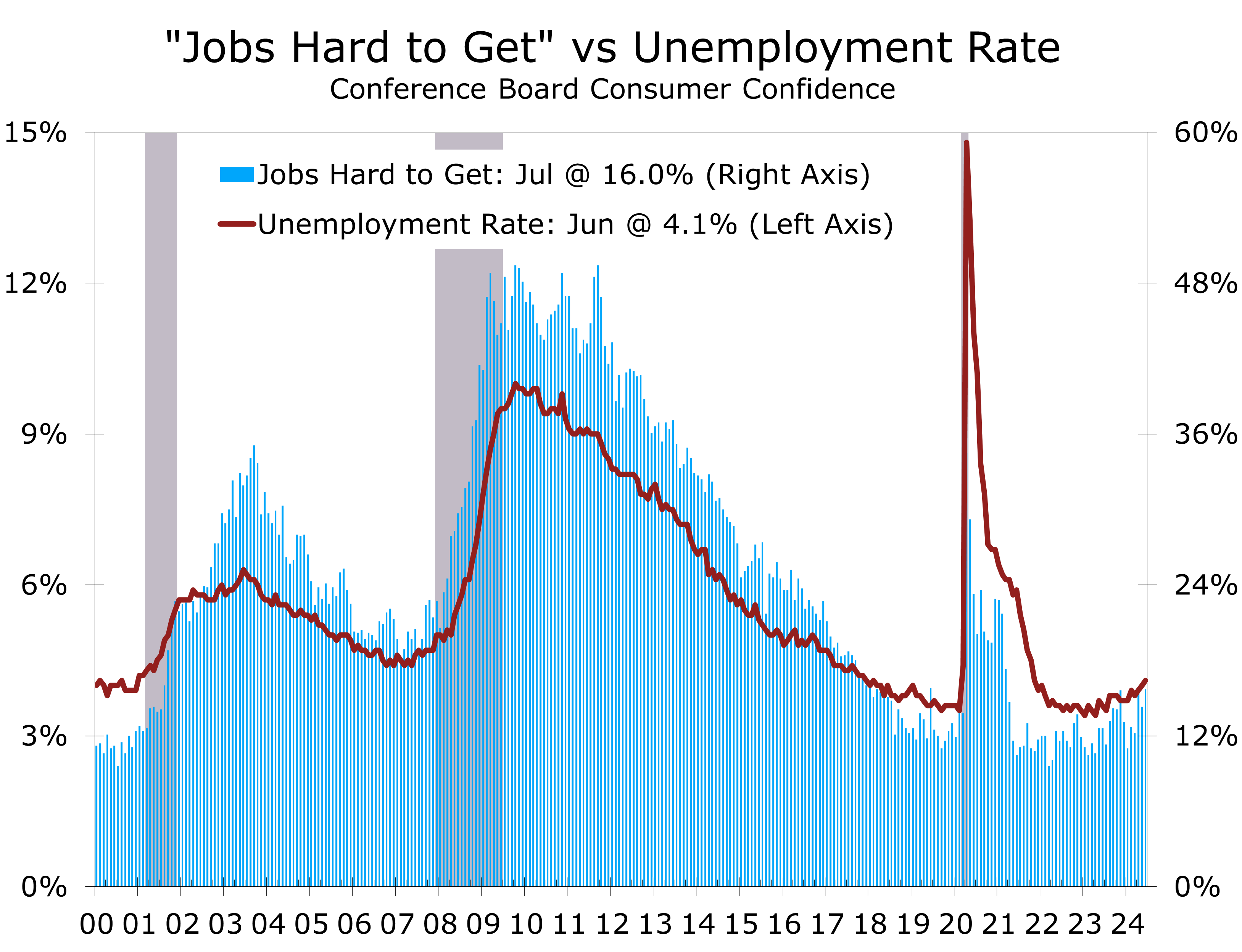

- The unemployment rate edged 0.1 percentage point lower to 4.2%. Long-term unemployment held steady at 1.5 million, making up 21.3% of total unemployment.

- The August employment report met expectations, but the composition of job gains and significant downward revisions to previous data suggest the report is weaker than it appears. Job growth continues to rely heavily on a few industries, many of which offer lower wages. Notably, hiring in professional services remains particularly weak.

Total nonfarm payroll employment increased by 142,000 in August, representing continued deceleration in job creation. This past month’s gain follows the smallest monthly gain since the Pandemic and is well below the prior 12-month average of 197,000 new jobs. Job growth was driven primarily by leisure and hospitality (+46,000), construction (+34,000), health care (+31,000), and government (+24,000). However, the broader slowdown in hiring was evident, as manufacturing lost 24,000 jobs, mainly due to a 25,000 drop at durable goods producers.

The narrowing breadth of job growth is likely pulling long-term unemployment higher.

Revisions to previous months were surprisingly large and negative, subtracting a combined 86,000 jobs from the June and July figures. The diffusion index, which measures the breadth of job gains across industries, rebounded 5.4 point August to 53.2 but the prior month’s reading was revised lower, to 47.6, marking the only month where more industries cut jobs than added them. Such declines are rare outside recessions.

The unemployment rate edged 0.1 percentage point lower to 4.2%. Despite the improvement, the jobless rate remains nearly half a percentage point higher than its year ago level. Long-term unemployment (those out of work for 27 weeks or more) remained flat at 1.5 million, representing 21.3% of all unemployed.

The number of long-term unemployed has risen over the past year, climbing from a cycle low of 1.05 million in March of last year to 1.53 million today. The increase partly reflects slower job growth in professional services. From this perspective the employment picture looks a little softer than a soft landing, particularly for college graduates. Hiring has also slowed in financial services and other occupations requiring a college degree.

Job growth is weakening in professional services but remains strong in many trades.

While professional employment has weakened, job growth remains strong in many trades. Construction added 34,000 jobs in August, surpassing the 12-month average of 19,000. Heavy and civil engineering contributed 14,000 jobs, as did nonresidential specialty trade contractors, reflecting the buildout driven by various fiscal initiatives. By contrast, residential construction job growth appears to be slowing, as the apartment boom winds down.

Health care employment increased by 31,000, well below the 12-month average of 60,000. Gains were led by ambulatory health care services (+24,000) and hospitals (+10,000), while social assistance added 13,000 jobs, with 18,000 coming from individual and family services.

Manufacturing employment edged lower, reflecting a net loss of 24,000 jobs, mostly in durable goods. Transportation equipment accounted for about half that loss, but cuts were broad based. Durable goods payrolls have shown little change throughout the year and remain a drag on broader job growth.

Other major industries, including mining, retail trade, transportation, information, and financial services, showed little change in employment. Average hourly earnings for private workers rose by 0.4% to $35.21 in August, translating to a 3.8% year-over-year increase. Production workers wages are up 4.1% year-to-year.

With job growth slowing, a quarter-point cut in the federal funds rate looks certain this month.

The weaker job growth, stagnating manufacturing sector, and higher unemployment rate make a quarter-point cut at the September FOMC meeting highly likely, with the possibility of a more aggressive move. Revisions to June and July data—showing a combined 86,000 fewer jobs—suggest labor market momentum may be waning faster than expected. Additionally, the narrowing breadth of job gains suggest the economy may be decelerating slightly beyond a “soft landing.”

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

September 6, 2024

Mark Vitner, Chief Economist

Piedmont Crescent Capital

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

Miami Resumes Their Rivalry Against Florida

Miami vs Florida in the Swamp

- Florida will host Miami in the Swamp this Saturday afternoon, rekindling a rivalry that has become more intermittent due to conference expansion.

- The University of Miami, located in Coral Gables, has been one of college football's most successful programs in the modern era, though they have struggled to regain their former dominance in recent years.

- The University of Florida, located in North Central Florida, in a region that still reflects 'Old Florida,' is a key economic driver for the state and hosts a top-tier healthcare program.

- The game will be broadcast on ABC at 3:30 pm as part of a triple-header kicking off the network’s SEC coverage.

- Miami enters the game as a 2.5-point favorite with a deeper and more talented roster on paper. However, the Swamp is a notoriously tough venue, and Florida is more formidable than they may appear. An upset could set the stage for a strong start to Florida's season before the schedule intensifies in the second half.

Week Zero kicked off the 2024 college football season with a major surprise as unranked Georgia Tech defeated then-10th ranked Florida State University in Dublin, a game we previewed last week. This weekend marks the traditional start of the college football season, with over 130 games scheduled from Thursday through Monday night.

Key matchups this week include #14 Clemson vs. #1 Georgia at Mercedes-Benz Stadium in Atlanta, #7 Notre Dame at #20 Texas A&M, #23 USC vs. #13 LSU in Las Vegas, and #19 Miami at Florida.

The Clemson-Georgia game is the weekend’s marquee matchup. A Clemson victory over Georgia, combined with FSU’s loss to Georgia Tech, could help the ACC move past its recent struggles. Georgia, despite some concerns at running back, boasts a deep and talented team that is the consensus #1 pick of nearly every ranking service. This game will kick off ABC’s SEC coverage at noon.

Our weekly football report highlights the return of the intrastate rivalry between the University of Miami and the University of Florida. The game is set for 3:30 p.m. at Ben Hill Griffin Stadium in Gainesville, likely under hot and steamy conditions. This rivalry, part of the Florida Cup that also includes Florida State, was a fixture each year until 1988.

Despite conference expansion limiting non-conference games, the teams have met frequently, most recently in Orlando in 2019, where Florida won 20-16. This year marks the start of a home-and-home series, with Miami leading the rivalry 29-27. Both teams, under relatively new coaches, are aiming to rebound from disappointing seasons with strong recruiting classes.

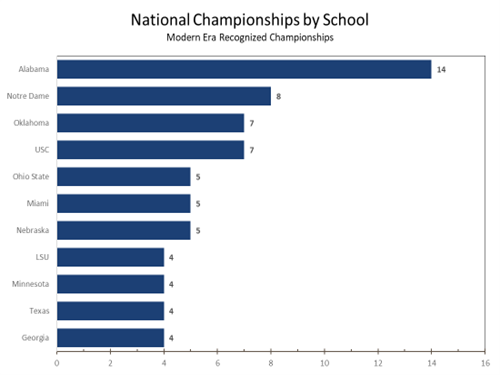

The University of Miami and the University of Florida are two of the most successful college football programs since the AP poll began, benefiting from Florida’s rich talent pool. Miami, which began football in 1926, has won five national championships (1983, 1987, 1989, 1991, 2001), tying Ohio State and USC for the fourth-highest total, behind Alabama, Notre Dame, and Oklahoma.

Florida, a founding SEC member in 1933, won its first conference title in 1991 and secured four consecutive SEC titles from 1993 to 1996, along with three national championships (1995, 2005, 2010). This matchup, featuring a triple-header as part of ABC’s SEC coverage debut, highlights the eight national titles between the two programs and promises a compelling start to the season.

The rivalry has produced numerous classic games, with 27 of the 56 matchups decided by a touchdown or less. The last meeting was in 2019, with Florida winning 20-16. Two of the greatest games were in 1983 and 1984. In 1983, Miami, a 3.5-point underdog, lost 28-3 to Florida but went on to win their first national championship that season after a historic comeback

against what had previously been thought to be an unbeatable University of Nebraska in the Orange Bowl.

The following year, in a game marking ESPN’s first primetime college football broadcast, Miami defeated Florida 32-20 after a dramatic last-minute drive led by Bernie Kosar. A last second pick-6 padded the score. Florida, ranked #17 at the time, went on to finish #3, their best-ever ranking, but had their SEC title (their first ever) vacated due to NCAA sanctions. This year promises another intense showdown as both teams aim to return to their former prominence.

Miami appears to be slightly ahead on that front and is widely expected to compete with Florida State, Clemson and NC State for the ACC Tittle. The Florida Gators have had a disappointing past few seasons and are a younger and less experienced team, expected to finish near the middle of the pack in the expanded SEC. The Gators have one of college football’s toughest schedules, particularly in the second half of the season. Florida will play the state’s two other major programs, hosting Central Florida on October 5th and ending the regular season against Florida State in Tallahassee.

University of Miami and South Florida

The University of Miami is located seven miles south of downtown Miami in Coral Gables. Established in 1925 during South Florida’s land boom, UMiami has significantly contributed to the region’s development, weathering challenges like hurricanes, the Great Depression, and World War II. Post-war, enrollment surged, mirroring South Florida’s development and the university has evolved both academically and culturally with the greater Miami area.

Today, UMiami is recognized as a top private university, offering a wide range of undergraduate, graduate, and professional programs. It has strong research initiatives, particularly in areas like medicine, marine science, and engineering. The University is Coral Gables’s largest employer and Miami-Dade’s second largest and helps further diversify the region’s economy, especially in tech and e-commerce.

Miami Economy

Miami, founded in 1896 and named after the Miami River, which itself was named after the Mayaimi Native American tribe, was initially a small settlement, known as Fort Dallas and was an important outpost during the second Seminole War. The city’s growth accelerated with Henry Flagler’s railroad investment along Florida’s East Coast and the development of Miami Beach in 1913. Despite setbacks during the Great Depression and numerous natural disasters, Miami’s post-World War II boom saw it become a key business hub.

The 1959 Cuban Revolution and subsequent Caribbean migrations accelerated Miami’s growth, establishing it as a hub for Latin American culture and commerce. In recent decades, Miami has experienced significant “Manhattanization,” with a rise in high-rise developments and an influx of financial firms, earning it the nickname “Wall Street of the South.” With over 440,000 residents in just 36 square miles, Miami is the fourth-densest major city in the U.S. Business-friendly policies and its role as the financial and technology capital of Latin America have cemented Miami’s status as a key financial hub.

The term “Miami” can be ambiguous, as it often refers to much of South Florida. Miami-Dade County, which includes the City of Miami, comprises 19 cities, six towns, and nine villages, ten of which have “Miami” in their names. Other notable Miami-Dade cities include Hialeah, Homestead, Coral Gables, and Doral. The Miami Metropolitan Statistical Area (MSA) encompasses Miami, Fort Lauderdale, and West Palm Beach.

The broader Combined Statistical Area, often referred to as South Florida, has over 7 million residents and includes Stuart, Port St. Lucie, Vero Beach, the Florida Keys, and Okeechobee County. The Gulf Coast from Naples to Tampa is known as Southwest Florida. Miami has a history of booms and busts, with the latest boom beginning when Florida reopened from the pandemic earlier than other states, triggering a wave of relocations and expansions.

The economy in South Florida has slowed along with national trends. While the region experienced a resurgence in tourism and a rapid recovery in international trade post-pandemic, job growth has moderated recently, with nonfarm payrolls increasing by just 2.6% over the past year. The unemployment rate has risen by 0.8 percentage points to 3.4%.

Construction remains a bright spot, with numerous tower cranes dotting the landscape and construction firms expanding payrolls by 8.7% over the past year. Tourism continues to thrive, with record cruise traffic through the Port of Miami.

The University of Florida & Gainesville

The University of Florida (UF) was established in 1906 following the Buckman Act, which consolidated various agricultural and theological schools across Florida. Initially focused on agriculture, UF’s growth was significantly boosted by the GI Bill and the admission of female students. Today, UF is a leading public university known for academic excellence, a top-tier medical school, and a successful athletics program.

Located in Gainesville, approximately two hours north of Orlando and 90 minutes southwest of Jacksonville, UF is situated in the heart of “Old Florida.” The surrounding areas were historically agrarian, producing Sea Island cotton before the boll weevil infestation of 1916-18 devastated the industry. The region’s citrus industry had also been affected by the Great Freeze two decades earlier. Today, local agriculture focuses on vegetables and cattle.

Gainesville’s economic shift began in 1905 with the consolidation of four institutions into what is now UF. The university has since become the cornerstone of Gainesville’s economy, particularly after World War II. The establishment of the J. Hillis Miller Health Science Center in 1956, followed by Shands Hospital and the UF Medical School in 1958, further transformed the region.

The University of Florida’s healthcare complex is a major economic driver, with its six health-focused colleges contributing roughly half of UF’s record $1.25 billion in research funding for Fiscal 2023. The UF College of Medicine led with $378 million, while the Herbert Wertheim UF Scripps Institute added $97.6 million. UF’s research spending has surged nearly 80% since 2012, driven by federal and state funding.

The UF Health Cancer Center recently achieved National Cancer Institute (NCI) designation, becoming the only public university in Florida with this status. This recognition reflects the center’s excellence in research, leadership, and outreach. Since receiving the designation, the center has increased cancer research funding by 43%, recruited new researchers, and expanded programs, including collaborations with the Scripps Institute. It has also improved infrastructure for clinical trials and boosted participation among underrepresented groups. Significant investments in data science and early detection, along with enhanced training opportunities for future researchers, have further strengthened the center’s impact.

The healthcare sector’s growth has advanced Gainesville’s development beyond its traditional college town status. Major private employers in the area include AavantiBio, AxoGen, RTI Surgical, Exactech, and Invivo Diagnostics. This thriving sector has established an ecosystem that attracts and retains other industries, reinforcing Gainesville’s economic foundation.

Job growth in Gainesville is modest, with government, healthcare, and leisure sectors comprising most of the employment base. Recent data show employment up 2.4% over the past year and the unemployment rate rising slightly to 3.6%. The region’s population grows modestly compared to Florida, with the three-county metro area housing 350,000 residents and the broader Combined Statistical Area, including Lake City and Columbia County, reaching just over 425,000.

Miami Hurricanes vs. Florida Gators

Miami enters the rivalry with a stronger roster, enhanced by Mario Cristobal’s successful recruiting and transfer efforts. Washington State transfer Cam Ward and former Oregon State running back Damien Martinez could make Miami’s offense one of the ACC’s strongest. On defense, Miami benefits from coordinator Lance Guidry and new additions like Tyler Baron, Simeon Barrow, and Jaylin Alderman.

Miami’s secondary has some gaps, which Florida quarterback Graham Mertz might exploit. Florida’s ground game, led by Montrell Johnson, could challenge Miami’s untested defensive front. Despite struggling in 2023, Florida’s new leadership and key transfers offer hope for improvement.

Miami, despite a 7-6 record last season, was statistically superior to Florida, which finished 5-7. Both teams have added significant talent from the transfer portal, with Miami bringing in 15 players and Florida 16, including key contributors.

Early-season results can be unpredictable, as shown by Florida State’s loss to Georgia Tech. While Miami appears stronger on paper, Florida’s home-field advantage in the Swamp and the extreme heat and humidity could level the playing field, making this a closely contested game. The outcome will influence perceptions of both programs and impact the critical third seasons for head coaches Billy Napier and Mario Cristobal.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

HBCU Football Kicks Off 2024 Season in Prime Time

Florida A&M vs. Norfolk State in Atlanta

- The 2024 HBCU football season kicks off with Florida A&M University taking on Norfolk State University, as part of the Cricket MEAC/SWAC Challenge Kickoff.

- The game is scheduled for August 24 at Center Parc Stadium in Atlanta and will be broadcast nationally on ABC.

- FAMU, is located in Tallahassee, and is the defending HBCU National Champion, finishing the 2023 season 12-1.

- Florida A&M is the nation’s second largest HCBU and provides undergraduate and graduate degrees across a broad assortment of majors.

- Norfolk State, located in Norfolk, Virginia, is the nation’s 16th largest HCBU and plays a key role in supporting the Hampton Roads regional economy.

- Norfolk State finished 3-8 last year and is in a rebuilding mode.

- The Cricket MEAC/SWAC Challenge is an annual HBCU football kickoff event played in Atlanta that highlights the growing role HBCUs have in today’s economy. The event also serves as a key gathering for alumni, friends and supporters.

The 2024 Historically Black College and University (HBCU) football season kicks off with the Florida A&M University (FAMU) Rattlers taking on the Norfolk State University (NSU) Spartans. Scheduled for August 24 at Center Parc Stadium in Atlanta, this matchup is part of the Cricket MEAC/SWAC Challenge Kickoff and will be broadcast nationally on ABC at 7:30 pm. This report is part of a new series exploring the historical and cultural significance of the participating HBCUs. We review the broader impact of HBCUs and HBCU football, as well as Atlanta’s role as a cultural and economic hub for the Black community. We also provide an update on each area’s economy.

Florida A&M is the reigning HCBU National Champion, having defeated Howard 30-26 in the Celebration Bowl at Atlanta’s Mercedes-Benz Stadium last December. The HCBU Championship pits the conference champions of the Southwestern Athletic Conference and Mid-Eastern Athletic Conference.

Florida A&M returns a number of starters from last year’s team and features some 36 seniors and graduate students. Norfolk State, which went 3-8 last year, will face a momentous challenge. Their team is younger and less experienced. Interconference games are often surprising, however, early in the season and NSU is expected to be amped up to play before a national audience in prime time.

Florida A&M University (FAMU)

Founded on October 3, 1887, Florida A&M University (FAMU) is a prominent public, historically Black university and land-grant institution within the State University System of Florida. Accredited by the Southern Association of Colleges and Schools, FAMU’s main campus is situated on the highest hill in Tallahassee, covering 422 acres with 156 buildings. Besides the main campus, FAMU operates several satellite locations, including the College of Law in Orlando and pharmacy program sites in Miami, Jacksonville, and Tampa.

Located where Florida’s Big Bend meets the Florida Panhandle, Tallahassee, which is also the state capital, serves as a quintessential college town. With a population of nearly 400,000, it is home to Florida State University, Florida A&M University, and Tallahassee State College. As the seat of Florida’s government, Tallahassee hosts the State Capitol, the state Supreme Court, the Governor’s Mansion, and numerous state agencies. It also stands as a regional center for scientific research with the National High Magnetic Field Laboratory.

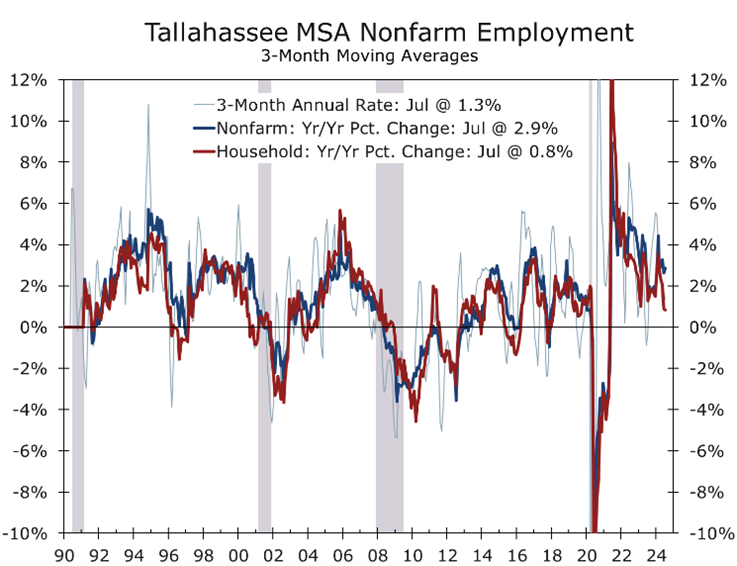

Over the past few years, Tallahassee has seen solid economic gains. Nonfarm employment rose by 3.0% this past year, driven by government, transportation, warehousing, and education and healthcare.

FAMU offers a broad array of academic programs, including 54 bachelor’s degrees, 29 master’s degrees, and 11 doctoral programs across 12 schools and colleges. Key undergraduate programs include architecture, journalism, computer information sciences, and psychology, while its graduate programs are well-regarded, especially pharmaceutical sciences, public health, physical therapy, and engineering. The university has notable alumni in various fields, including politics, entertainment, and law.

The Rattlers football team, competing in the Football Championship Subdivision (FCS) of the NCAA, has a rich history. Since joining the Southwestern Athletic Conference (SWAC) in 2021, FAMU has built on its legacy, with 16 Black College Football National Championships, 29 Southern Intercollegiate Athletic Conference (SIAC) titles, eight MEAC titles, and one SWAC title. Notably, they won the inaugural NCAA Division I-AA National Title (now FCS) in 1978, the only HBCU to do so. With an impressive record of 594-340-22 and 38 conference championships, FAMU’s football program remains a powerhouse in HBCU sports.

Norfolk State University (NSU)

Norfolk State University was founded on September 18, 1935, as part of Virginia Union University. Initially directed by Samuel Fischer Scott, the institution was renamed Norfolk Polytechnic College in 1942 and became part of Virginia State College (now Virginia State University) shortly thereafter. By 1950, the college had grown to 50 faculty members and 1,018 students and adopted the “Spartan” name for its athletic teams in 1952.

The college’s permanent site on Corprew Avenue was established in 1955 with the completion of Brown Hall. Norfolk State granted its first bachelor’s degrees in 1956. In 1969, the college became Norfolk State College and received accreditation from the Southern Association of Colleges and Schools. By 1975, it began offering master’s degrees in communications and social work. Dr. Harrison Benjamin Wilson Jr. succeeded Dr. Lyman Beecher Brooks in 1975.

In 1979, the institution was renamed Norfolk State University by the Virginia General Assembly. It celebrated its 50th anniversary in 1985 with an enrollment of 7,200, which grew to a peak of 9,112 by 1995. Today, Norfolk State University enrolls approximately 5,300 students and is the 16th largest HBCU.

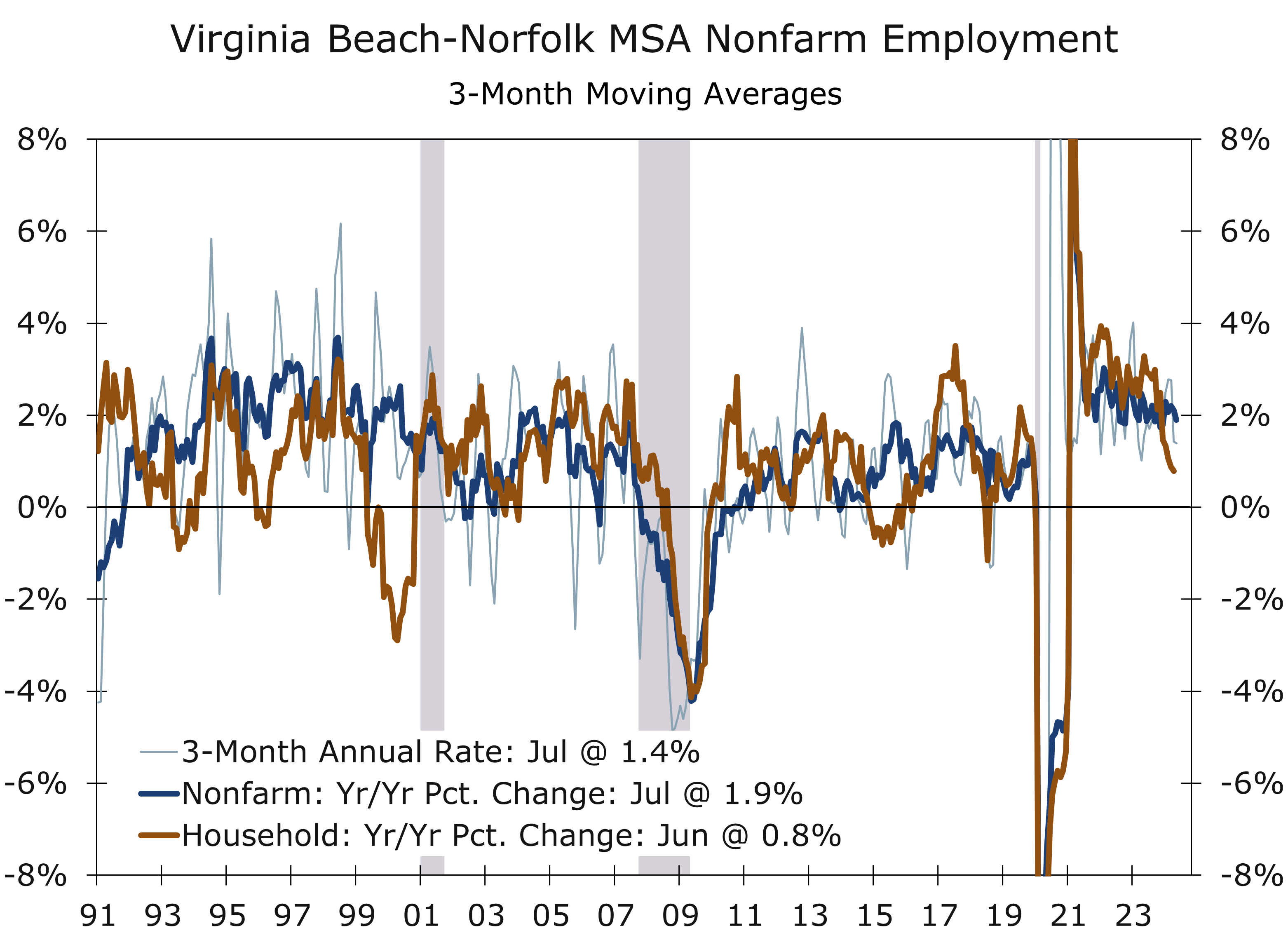

The Norfolk and Hampton Roads region, which includes Norfolk, Virginia Beach, Williamsburg, and Newport News, has a population of just under 1.8 million residents. The Norfolk Naval Station, the world’s largest naval base, is a central economic pillar, supporting around 62,000 active-duty personnel, 75 ships, and 132 aircraft. The defense sector, including military personnel and defense contracting, contributes more than a third of the metro area’s Gross Domestic Product and has largely driven economic growth since the pandemic.

The Port of Hampton Roads, benefiting from a deep harbor and strategic location, ranks as the third-largest port in the U.S. by cargo volume and leads globally in coal exports. The Virginia Port Authority oversees facilities like Norfolk International Terminals (NIT), which has the world’s largest container cranes. Shipbuilding and repair operations is also important, including Huntington Ingalls and BAE Systems.

Wholesale trade and distribution, professional services, health, retail trade and tourism are also key drivers for the region. The steady stream of young, skilled military retirees is also a major draw for industry, as is the large number of Navy spouses.

Hampton Roads has struggled to attract new corporate headquarters to the region. One recurring risk to the region is deployment risks, with ships being deployed more frequently and staying out longer, depriving the region of military personnel and their families.

Overall economic growth remains relatively solid. Nonfarm employment has risen 1.9% over the past year. The unemployment rate remains historically low at just 2.0%. Growth has moderated this past year, however, reflecting an outright decline in government payrolls and slower growth in leisure and hospitality. Hiring remains strong in education and health care and in professional services.

Historical Context of HBCUs

Historically Black Colleges and Universities (HBCUs) were established primarily to educate African Americans before the Civil Rights Act of 1964. Today, 101 HBCUs serve over 228,000 students and award more than 20% of all bachelor’s degrees to African Americans. Alabama, North Carolina, Texas, Georgia, South Carolina, Louisiana, Mississippi, Tennessee, and Virginia are the states with the most HBCUs.

The Second Morrill Act of 1890 required land-grant universities to integrate or establish new institutions for African American students, leading to the creation of many HBCUs. Early HBCU football began with Johnson C. Smith University’s 1892 win over Livingstone College, setting a precedent for significant HBCU football rivalries. Johnson C. Smith and Livingstone still compete annually in the Commemorative Classic.

Post-segregation, HBCUs faced financial challenges and competition as African American students gained access to more institutions. Currently, only about 8% of Black college students attend HBCUs, and many face funding challenges compared to their flagship counterparts. Despite this, HBCUs remain competitive in NCAA FCS and continue to be vital in producing graduates and professionals.

The title of ‘HBCU national champion’ has evolved over time, with the Celebration Bowl established in 2015 as a de facto championship game for the MEAC and SWAC. Although Tennessee State, with 16 HBCU titles, plays in the Ohio Valley Conference, the tradition of crowning an HBCU national champion persists.

HBCUs have been crucial in advancing African American education and professional development. They were the primary option for Black higher education for nearly a century and continue to play a significant role in producing graduate degree holders and contributing to the professional landscape.

HBCU football games, including classic matchups and homecomings, are major cultural events that engage alumni, students, and the business community. These games often feature historic rivalries and celebrate Black heritage.

Atlanta’s Role as a Black Mecca

Atlanta’s hosting of the MEAC/SWAC Challenge underscores its status as a cultural and economic epicenter for the Black community. Known as the “Mecca of Black Culture,” Atlanta earned this moniker through years of civil rights activism and leadership, community solidarity in the workforce, and the powerful influence of Black churches. Today, the city is marked by intense economic activity, serving as a hub not only for culture but also for business and industry.

A recent Harvard study revealed that Atlanta has one of the deepest income divides in the nation and lags behind other cities in economic mobility for residents that have grown up there. It is a bitter irony for a city that has seen so much accomplished in the African American community.

On average, 2.7% of U.S. businesses are Black-owned, but in Atlanta, that number nearly triples to 8.8%. This is largely due to multiple factors, including the robust network of colleges and universities in the area, such as Spelman College, Morehouse College, Clark Atlanta University, Georgia Tech and Georgia State University. These institutions produce graduates who are not only staying in the area but also receiving more federal support than ever to start their own businesses. Small Business Administration loans have more than doubled for Black-owned businesses in recent year, helping fuel this growth.

Atlanta has long been home to some of the most prominent Black-owned names in entertainment, such as Tyler Perry Studios and the thriving blues and hip-hop scenes in neighborhoods like the East Village. Black industry in the city has expanded significantly in recent years. With innovation centers like Georgia Tech and influx of large technology firms, Atlanta has become the fastest-growing location for young Black professionals in the tech sector.

Atlanta’s diverse economic activities, including its thriving entertainment industries and innovation hubs, along with its growing population of young Black professionals, highlight the city’s vital role in celebrating and advancing Black cultural and economic interests.

A Few Final Notes on the Game

While this year’s Cricket MEAC/SWAC Challenge Kickoff matches up one the powerhouses in HBCU with a program that is rebuilding from a disappointing year, we expect to see a relatively close game. Kickoff classics serve as a huge motivator, particularly for underdog teams. As noted earlier, the game itself is just part of the celebration of the return of college football and perseverance of Historically Black Colleges and Universities.

One last minute wrinkle is that Norfolk State recently announced that former University of South Carolina walk-on quarterback, Jalen Daniels, will start this Saturday, as All-MEAC QB Otto Kuhns serves an NCAA suspension. The team has apparently prepared for this contingency, with Daniels, a talented transfer from Garden City Community College, quickly adapting to the NSU system. Kuhns will rejoin the QB competition after his four-game suspension.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

August 22, 2024

Mark P. Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

Chief Economist (704) 458-4000

Ethan Jacobs

Economic Analyst Intern

Benjamin Jacobs

Economic Analyst Intern

College Football Returns: Florida State vs Georgia Tech

A Key Early Season ACC Matchup

- Florida State and Georgia Tech will kick off the 2024 College Football season on Saturday, August 24th, in Ireland.

- ESPN will make its first trip outside the U.S. to provide pre-game coverage at its usual time. Kickoff is scheduled for noon ET.

- Our football reports combine elements of economics, school and team history, and an outlook for a key game each week.

- This week’s matchup features major college teams from the state capitals of Florida and Georgia, the two largest states in the Southeast. Texas, located in the Southwest, joins the SEC this year.

- We review how Atlanta and Tallahassee became their respective state capitals.

- Both schools are key economic drivers for their regions, a role they have enthusiastically embraced in recent years.

- Florida State is an 11.5-point favorite going into the game. The Seminoles went undefeated in the regular season last year and won the ACC Championship. Georgia Tech returns a high-powered offense from last year’s team, which finished strong.

The college football season will kick off Saturday internationally this year in Dublin, Ireland. The Georgia Tech Yellow Jackets will face the Florida State Seminoles at Aviva Stadium on Saturday, August 24th in the Aer Lingus College Football Classic. This marks the sixth time since 2012 that this venue has been used for an American college football game, reflecting Ireland’s ongoing efforts to attract American tourists. Many of the previous matchups featured Catholic institutions like Notre Dame and Boston College, an intentional choice to appeal to Irish American and Catholic visitors. This will be Georgia Tech’s second trip to Dublin in the last decade, following their 2016 game against Boston College. For Florida State, this will be their first overseas matchup.

This game will also be the first time ESPN’s award-winning pre-game show, College Gameday, is held outside the United States. Historically, college football games in Ireland have drawn affluent tourists who not only attend the game but also plan extended vacations around the event. With Aviva Stadium’s capacity of over 50,000, the game is expected to bring a significant influx of visitors to Dublin. Event officials estimate that past matchups have contributed approximately €100 million in tourism revenue to the region. However, this will be the first game in Ireland without a traditionally Catholic school, which could pose a challenge for attendance.

On the field, the game promises to be competitive. Florida State narrowly missed the College Football Playoff last year despite an undefeated season and winning the ACC Championship. The Seminoles, who lost 10 players to the NFL Draft, have been aggressive in the transfer portal and continue to recruit well. Meanwhile, Georgia Tech, which has been in a rebuilding phase, finished last season strong. The Yellow Jackets challenged arch-rival Georgia as well as any team did all season in their regular-season finale and went on to win the Gasparilla Bowl, finishing 7-6.

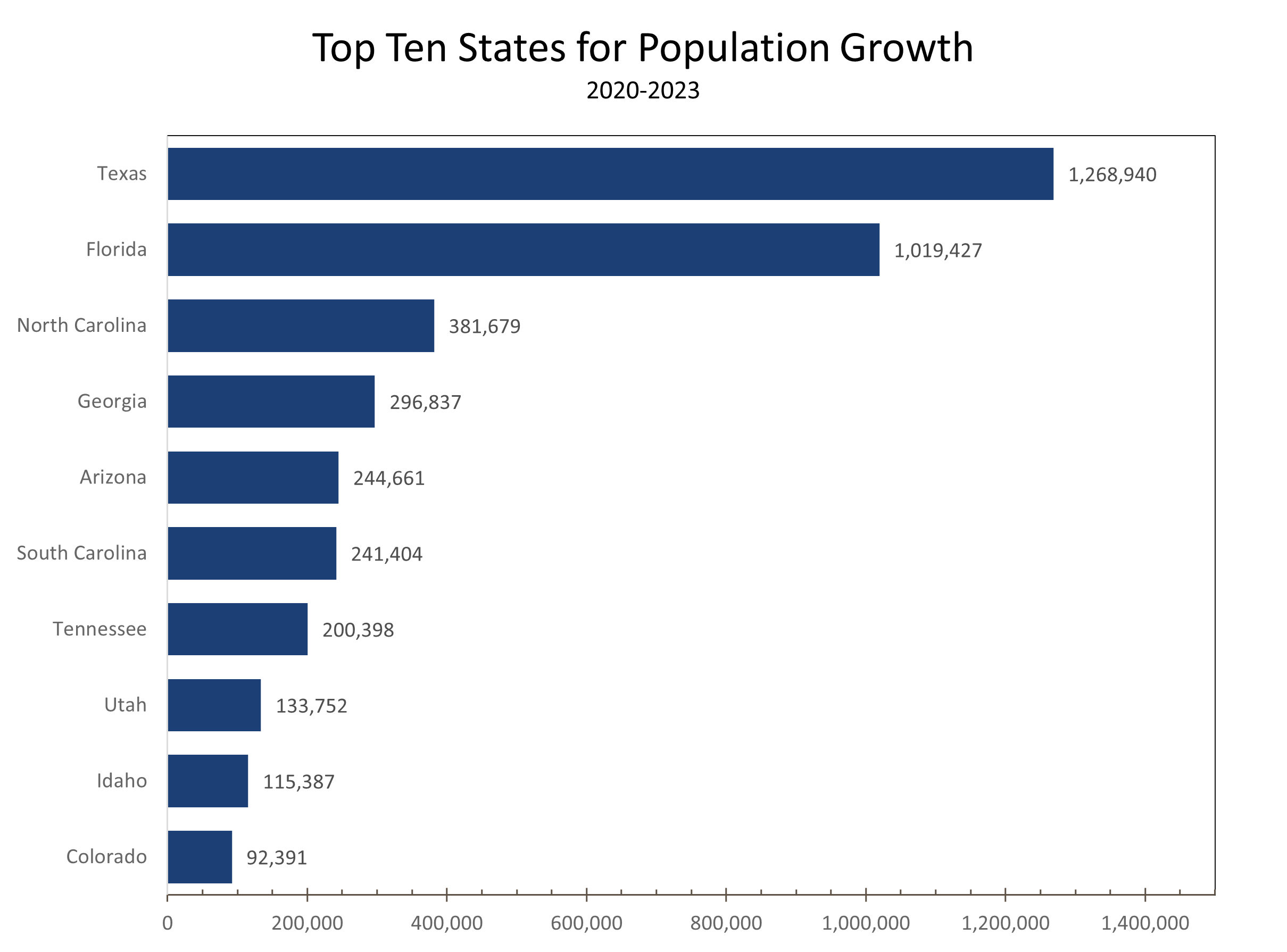

The matchup also features schools from the state capitals of the Southeast’s two largest states. The South has accounted for the majority of the nation’s population growth since the pandemic, with Florida and Georgia being two of the biggest beneficiaries. Despite this common trend, the two capitals could not be more different.

The Atlanta metropolitan area, often referred to as the capital of the Southeast, boasts a population of over 6.3 million residents and serves as a major hub for business and tourism. In contrast, Tallahassee is situated in North Central Florida, near the junction of Florida’s sparsely populated Big Bend region and the Panhandle, far from the state’s main population centers. The Tallahassee metropolitan area’s population is growing steadily and is currently home just under 415,000 residents.

Georgia Tech is situated in Atlanta’s Midtown, about 2 miles north of downtown. Atlanta became Georgia’s capital in 1868, replacing Milledgeville. Savannah, which originally served as the colonial entry point and a defensive position against Spanish forces, was Georgia’s original capital. After Savannah fell to the British during the Revolutionary War, the capital moved to Augusta. Post-war, both Savannah and Augusta served as seats of governance until Augusta became the official capital in 1786.

The expansion of agriculture and the search for flatter land prompted legislators to move the capital further inland to Milledgeville, requiring a new treaty with the Creek tribe. Milledgeville remained the capital for 60 years, a city modeled after Savannah and Washington, D.C., and carved out of the wilderness. The region thrived during the cotton boom and largely survived Sherman’s March to the Sea, preserving much of its architecturally significant structures and squares.

After the Civil War, the capital was relocated to Atlanta, which, despite being burned by Sherman, remained a vital railroad hub. The name “Atlanta,” derived from the Atlantic Railroad, was chosen as a compromise to avoid the more feminine name, Martha. After two decades and multiple rounds of voting, Atlanta was officially designated as the state capital. This move symbolized a push to industrialize the South during Reconstruction, aiming to compete with the North’s growing production capabilities.

This same drive led to the founding of the Georgia Institute of Technology in 1885 to advance technological development in the predominantly agrarian region. Today Georgia Tech occupies 450 acres in Midtown Atlanta, educates 16,000 students and employs over 4,900 staff members. Sixty percent of its students are from Georgia, contributing to the school’s $4 billion impact on the state and $3 billion impact on Atlanta.

Initially located on the eastern side of the downtown connector where I-75 and I-85 merge through the heart of downtown Atlanta, Tech expanded in the late 1990s by purchasing eight acres to develop “Tech Square” as part of its business outreach program.

By 2021, Tech Square had become the Southeast’s densest hub of startups, corporate innovators, and research centers, hosting 100 startups, 25 corporate innovation centers, 10 research labs, and seven venture funds. Georgia Tech’s emphasis on community partnerships in Midtown has spurred a wave of innovative projects from North Avenue to Brookwood Station. Additionally, new developments from the Woodruff Arts Center, a Savannah College of Art and Design campus, and numerous businesses have led to 50 new buildings valued at $13 billion. With an average of 60 new residents moving to Midtown each week, it has become one of the region’s fastest-growing submarkets.

Florida State University is located in Tallahassee—a location many newcomers and outsiders likely find unusual for a state capital. Tallahassee is Florida’s 14th largest metropolitan area and sits about 460 miles away from South Florida, where over a quarter of the state’s population resides. This choice dates back to a time when Florida was divided into two separate territories, and most of the population concentrated in the northern part of the state. The western territory’s capital was Pensacola, while the eastern territory’s capital was St. Augustine, both coastal cities central to their respective regions.

In 1819, the western territory seceded from Spain and was claimed by the United States, which took over Pensacola and other port cities during a military campaign, including raids against the Creek and Seminole tribes (the namesake of Florida State University). When the eastern territory was ceded to the U.S., Florida became one unified territory, and Tallahassee was chosen as the capital.

While economic and demographic power has since shifted southward, the northern part of the state still retains considerable clout. The region is home to the state’s two largest universities, the University of Florida and Florida State, as well as the largest Historically Black College and University, Florida A&M. Even the University of South Florida, located in Tampa, is still 246 miles northwest of ‘South Florida.’

In 1851, the Florida State Legislature called for the creation of two educational institutions on opposite sides of the Suwannee River. By 1854, the City of Tallahassee established the Florida Institute, a boys’ school run as a seminary. In 1858, the Florida Institute absorbed the Tallahassee Female Academy and became a coeducational institution.

After serving as a military academy during and after the Civil War, the school grew into a recognized collegiate institution. By 1901, it was officially known as Florida State College, then Florida Female College in 1905 and Florida State College for Women in 1909, with male students relocated to Gainesville. In 1947, the growing demand for education following the G.I. Bill led to its designation as Florida State University.

The university has continued to expand, graduating its first PhD candidate in 1952, adding research facilities for Molecular Biophysics and Space Biosciences in the 1960s, establishing the National High Magnetic Field Laboratory (MagLab) in 1990, and adding the College of Medicine in 2001. FSU has grown from its original few acres to 1,550 acres, comprising over 500 buildings. The university has focused on investing in programs that can be commercialized, attracting researchers, research funding, and new industries to Florida. Currently, Florida State is home to over 44,000 students and 14,700 employees.

Bobby Dodd Stadium and Atlanta

Georgia Tech plays its football games at Bobby Dodd Stadium in the shadows of Midtown Atlanta. Originally opened in 1913 as Grant Field, the stadium was renamed in 1988 to honor legendary coach Bobby Dodd. The stadium has undergone several expansions and renovations. Its capacity, which peaked at about 58,000 in the 1980s, is now around 55,000. Known for its classic bowl-shaped design, historic charm, and skyline backdrop, Bobby Dodd Stadium features modern synthetic turf and is the oldest FBS college football stadium, with college football continuously played at the site since 1905. Most recently the stadium was renamed “Bobby Dodd Stadium at Hyundai Field” following a sponsorship by Hyundai, which has a large and growing Georgia presence.

One of the more memorable games at the stadium occurred in 2015 when Georgia Tech upset the 9th-ranked Florida State. With Florida State leading 16–13 and driving late for a potential game-clinching score, a pass was deflected off Georgia Tech cornerback Lawrence Austin’s shoe and intercepted by Georgia Tech’s Jamal Golden. Harrison Butker subsequently tied the game with a 25-yard field goal.

Florida State had a chance to win the game in the final seconds but Roberto Aguayo, who had been perfect for the fourth quarter, saw his 56-yard field goal attempt blocked by Patrick Gamble. Lance Austin returned the blocked kick 78 yards for a touchdown as time expired. This thrilling finish was the high point of a disappointing season and came to be known as the Miracle on Techwood Drive. The Yellow Jackets, who began the year ranked in the top 20 and rise to #14 before losing 5 straight games, finished the year 3-9.

Atlanta’s selection as Georgia’s state capital was driven by its role as the South’s primary railroad hub. This foresight was validated as Atlanta’s transportation significance grew with the expansion of the federal highway system, the creation of the nation’s largest airline hub, and the intersection of major fiber optic networks in the metro area. These developments have cemented Atlanta’s status as the Southeast’s economic capital, home to 16 Fortune 500 companies and a leader in trade, transportation, digital payments, sports, and entertainment.

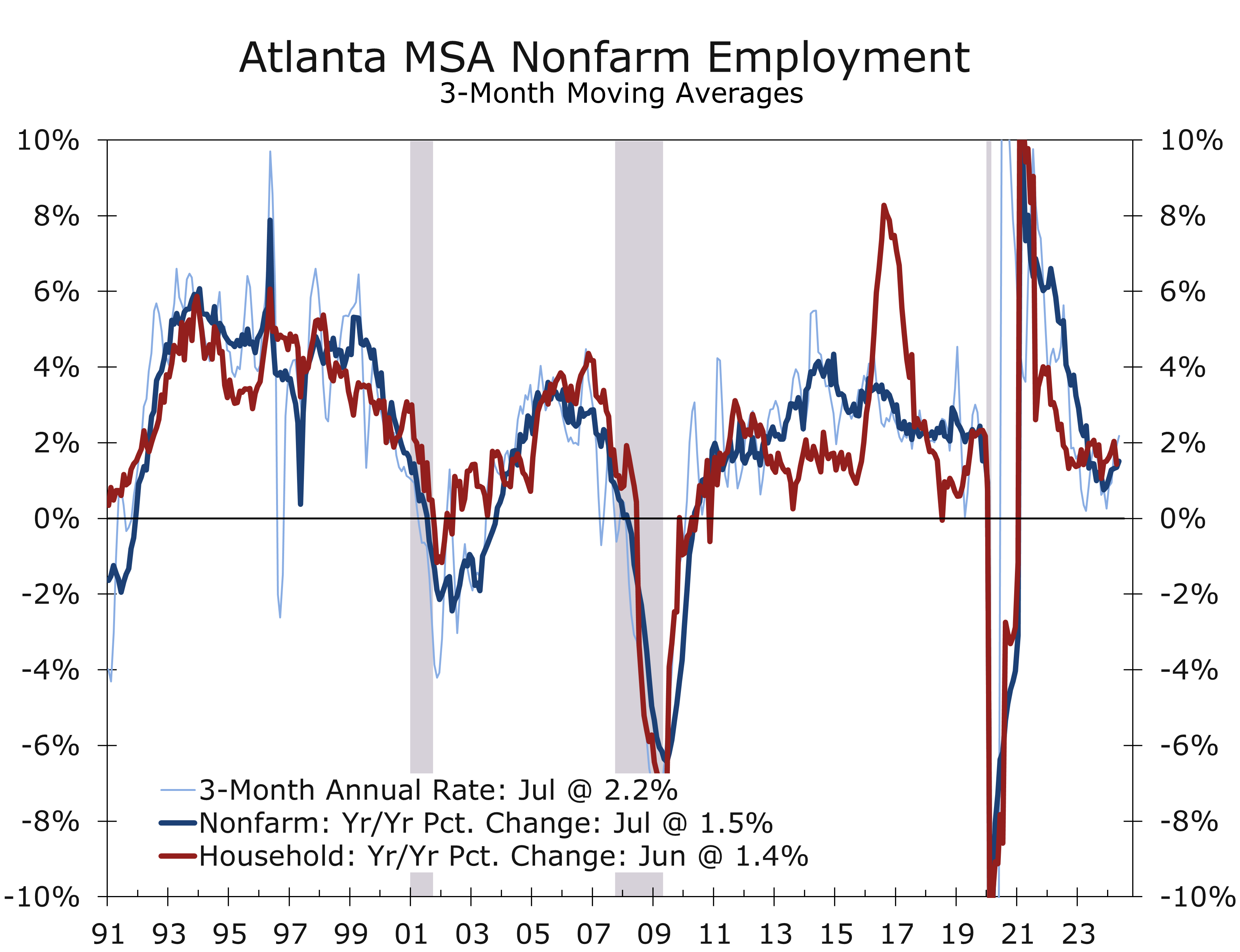

Atlanta’s economy has recently endured an unusually sluggish patch. Overall job growth has slowed as the entertainment industry has struggled in the aftermath of the writers’ and actors’ strikes, as well as financial challenges by many long-time industry leaders. Transportation and warehousing have also come under pressure, as the economy has worked through a goods recession after pent-up demand from the pandemic was sated after the economy reopened.

Nonfarm employment has risen just 1.5% over the past year, which slightly trails the state, and the unemployment rate has edged up to 3.9%. Atlanta has regained momentum more recently, as the headwinds impacting the goods sector and entertainment industry have abated somewhat. Atlanta remains a top choice for corporate expansions and relocations and is in the midst of a data center building boom. Several new studio complexes have also recently opened, presaging a rebound in film production.

FSU’s Relationship with the Seminole Tribe

Florida State University is situated on land historically inhabited by the Seminole Tribe and maintains a unique partnership with the tribe. Despite growing criticism regarding the use of Native American symbols in sports, Florida State remains committed to honoring the Seminole tradition. In 2005, when the NCAA reviewed its guidelines on the use of Native American nicknames, the Seminole tribal council unanimously approved FSU’s use of the Seminole name.

The Tribe is actively involved in decisions related to the use of the Seminole symbol. For example, the regalia worn by Osceola, the student who rides to midfield to plant the flaming spear, was designed with the tribe’s approval. The Tribe also provided input on the redesigned uniforms for the 2014 season.

Importantly, Florida State does not have a traditional mascot but rather uses a “symbol” to show respect and honor to the tribe. FSU continues to honor the Seminole Tribe with traditions like the War Chant and the Tomahawk Chop.

A Surprisingly Competitive Rivalry

Florida State holds an all-time record of 556-260-16, while Georgia Tech’s modern-era record stands at 750-519-40. In their head-to-head series, Florida State leads 15-11-1, with the Seminoles winning the most recent matchup in 2022, though Tech claimed victory in the two prior meetings.

Georgia Tech is one of college football’s most storied programs, with much of its success rooted in the early decades of the sport. The football program, which dates back to 1892, has accumulated an all-time record of 756-540-43. Tech claims four National Titles, the first of which was won in 1917 under the legendary coach John Heisman. Additional titles followed in 1928, 1952, and 1990, with unclaimed titles in 1916, 1951, and 1956.

Georgia Tech was a founding member of the Southeastern Conference (SEC) but left in 1963 due to frustrations with over-signing—the practice of recruiting more than the 25 allotted scholarship players, which often led to player cuts and transfers. This practice put Tech at a disadvantage and cast a poor light on Alabama. The Yellow Jackets, particularly head coach Bobby Dodd, accused Alabama of holding summer tryouts among these players to prepare for the season. After a rule proposing a ban on these tryout camps was voted down, Tech decided to leave the SEC. They played independently for almost three decades, navigating a tough schedule when there were still many independent programs.

Georgia Tech joined the ACC in 1992, enjoying remarkable success in their first decade in the conference. However, in recent years, they have faced challenges from cross-divisional rival Clemson and other conference powerhouses. Last year, the Yellow Jackets finished with a conference record of 5-3.

Florida State had a flawless 9-0 conference record last year and is ranked 10th in both the AP and Coaches pre-season polls. FSU has been a football juggernaut since the 1980s, never finishing a season ranked below fourth nationally between 1987 and 2000. The program also went forty years without a losing season, from 1977 to 2017. Although the Seminoles have not dominated since the introduction of the College Football Playoff, they remain one of college football’s most respected programs.

Florida State Football History

Florida State University’s athletic program began in 1902, when Florida State College, its former name, fielded a varsity football team called “The Eleven.” The team wore gold uniforms with a large purple “F” and had minimal protection, featuring lightly padded pants, leather helmets with ear guards, and metal nose guards. W.W. Hughes, a Latin professor and head of men’s sports, was the first coach. The team won their inaugural game against the Bainbridge Giants of Georgia, 5–0, and later split games with Florida Agricultural College.

In 1903, the team’s popularity grew, and “The Eleven” scheduled six games, including matches against Georgia Tech and Florida Agricultural College. They concluded the season competing for the Florida Times-Union Championship Cup. Jack Forsythe, who would later become the first head coach of the Florida Gators, took over as coach in 1904 and led the team to an unofficial state championship by defeating Stetson. However, the team disbanded after the 1904 season due to the Buckman Act of 1905, which reorganized Florida’s colleges by gender and race, renaming Florida State College to Florida Female College and later Florida State College for Women.

After World War II, the influx of veterans led to the renaming of Florida State College for Women to Florida State University, allowing men to enroll. Football resumed in 1947, with the Seminoles briefly competing in the Dixie Conference (1948-1950) before becoming an independent program from 1951 to 1991. The early years saw mixed success under coaches Ed Williamson, Don Veller, and Tom Nugent. Veller led the team to its first unbeaten season in 1950, while Nugent secured the Seminoles’ first win over an SEC opponent in 1958.

Head coach Bill Peterson, who arrived in 1960, began FSU’s rise to national prominence. Under Peterson, the Seminoles beat the Florida Gators for the first time in 1964 and earned their first major bowl bid. Peterson also gave Bobby Bowden his first major college coaching opportunity and led the Seminoles to their first top ten and number one ranking, according to the Dunkel College Football Index, in 1964.

Bobby Bowden, head coach from 1976, transformed FSU into a national powerhouse. The Seminoles played in five national championship games between 1993 and 2000, winning two. They set an NCAA record with 14 consecutive Top 5 finishes from 1987 to 2000. Bowden retired in 2009 with 377 career wins, though FSU later vacated 12 wins due to an academic scandal.

Jimbo Fisher succeeded Bowden in 2010 and led the Seminoles to a national championship in 2013. After a period of decline, Fisher resigned in 2017. Willie Taggart, hired as head coach, was fired after a disappointing 2019 season. Mike Norvell took over in 2019, leading the team to an undefeated regular season and a conference championship in 2023, though FSU was controversially excluded from the College Football Playoff.

Doak Campbell Stadium & Tallahassee

Doak Campbell Stadium, located on Florida State University’s campus in Tallahassee, opened in 1950 with a capacity of 15,000 and has since expanded to over 79,000 seats, reflecting FSU’s rise in college football under coach Bobby Bowden. Named after FSU’s first president, the stadium has seen multiple expansions and renovations, including the addition of the University Center in 2003 and modern amenities in the 2010s. The field was renamed “Bobby Bowden Field” in 2004. Major renovations are currently underway, which will reduce seating capacity by about 24,000 this season. Florida State’s will play its home opener against Boston College on Labor Day weekend.

Tallahassee’s economy is driven primarily by government and education, with the State of Florida and local governments, Florida State University, Tallahassee Community College, and Florida A&M University as top employers. Other key sectors include healthcare, with hospitals like Tallahassee Memorial Healthcare, and retail and wholesale trade. Professional services, especially in law, lobbying, and consulting, is another major employer. The city also serves as a regional trade and distribution hub, with growing tech and innovation sectors.

Over the past few years, Tallahassee has seen solid economic gains. Nonfarm employment rose by 3.0% this past year, driven by state and local government, transportation, warehousing, and education and healthcare. Despite its remote location, Tallahassee’s trade area, extending from South Georgia to the Gulf Coast, is expanding. The metro area is widely recognized as a top place to do business. Population growth averaged 0.5% over the past three years. Job growth is expected to moderate to 2.5% in the coming year, reflecting slower overall U.S. economic growth.

Florida State is Favored by 11.5 Points

Florida State enters Saturday’s game as an 11.5-point favorite. The Seminoles are likely still smarting from last year’s College Football Playoff snub and the 63-3 thrashing by Georgia in the Orange Bowl. On paper, they appear to be the superior team, bolstered by a wealth of talent, including several high-profile transfers like former Clemson QB DJ Uiagalelei. After starting 28 games for Clemson, Uiagalelei transferred to Oregon State, where he completed 57% of his passes and threw for 21 touchdowns. Florida State also brought in key defensive transfers to replace NFL-bound players, including standout defensive end Jared Verse.

Georgia Tech, returning eight starters on offense, led the ACC in rushing last season with 204 yards per game. Jamal Haynes spearheaded the attack with 1,059 yards on 174 carries, becoming Tech’s first 1,000-yard rusher since 2017. The offense is powered by dual-threat QB Haynes King, who passed for 2,842 yards and rushed for 737 more, completing 61.6% of his passes with 27 touchdowns and 16 interceptions. However, the defense, returning seven starters, remains a concern, particularly against the run, where they allowed over five yards per carry last season.

Florida State is somewhat of an unknown this year, starting the season ranked 10th largely due to their legacy of success and recent influx of transfers. A key question is how quickly the Seminoles can sync up. FSU will likely focus on establishing the run to keep Tech’s offense off the field.

Georgia Tech is also an unknown quantity, particularly with new defensive coordinator Tyler Santucci, who worked wonders at Duke last season. Tech will need to score early to prevent FSU from controlling the game with their ground attack. If Tech can get an early stop or turnover and capitalize with points, they might have a shot at the upset. However, if Florida State establishes their running game, Tech could struggle to keep pace with the deeper, more physical Seminoles.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

August 21, 2024

Mark P. Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

Chief Economist (704) 458-4000

Ethan Jacobs

Economic Analyst Intern

Economic Analyst Intern

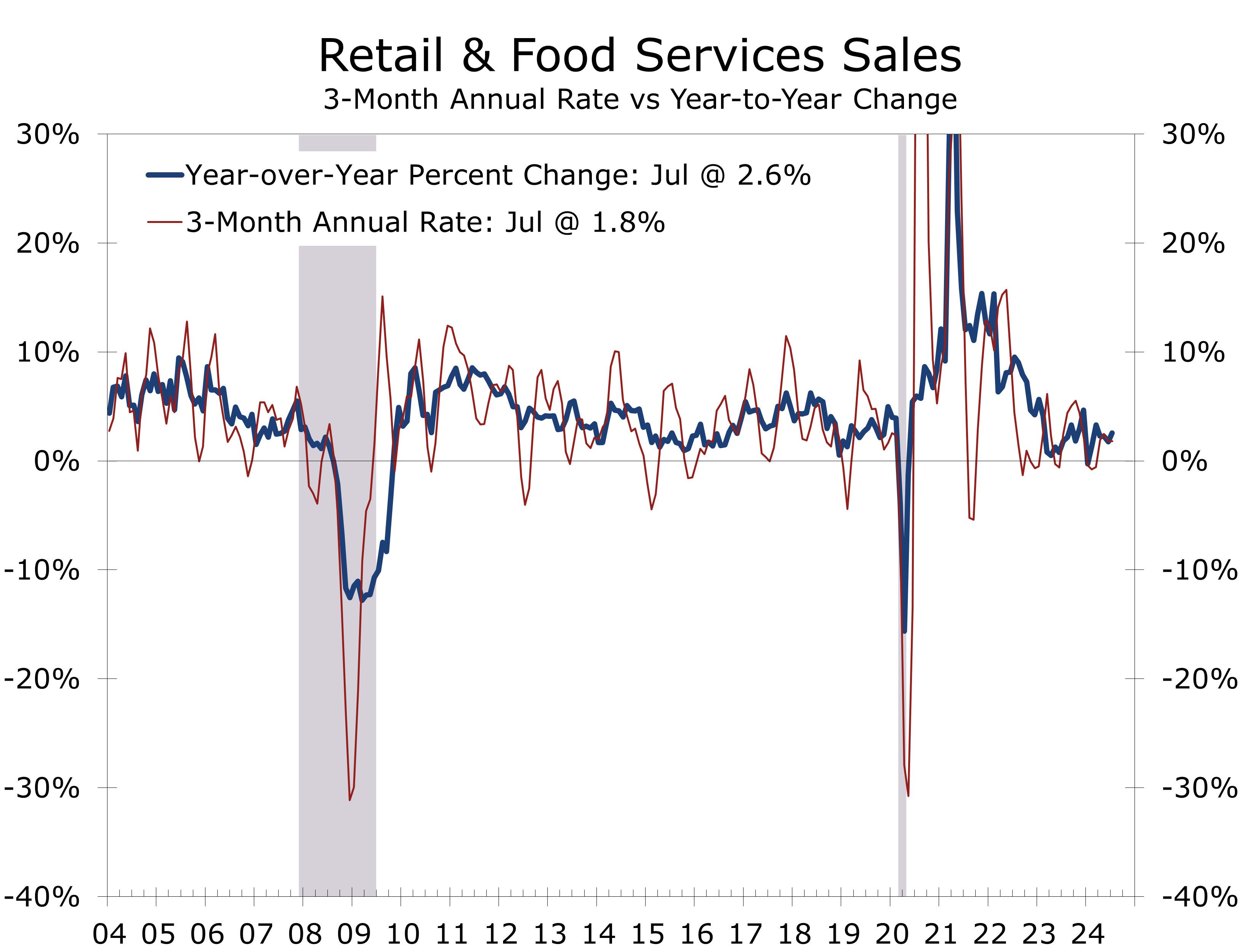

Retail Sales Soar Past Expectations in July

Headline Rise Overstates Consumer Strength

- Retail sales rose 1.0% is July, far exceeding the consensus of 0.3%.

- A 3.6% surge in auto sales, following June's cyber-attack driven drop, was a major driver of the headline gain.

- Excluding autos, retail sales increased by 0.4%, with 11 of the 13 major business categories posting gains in July.

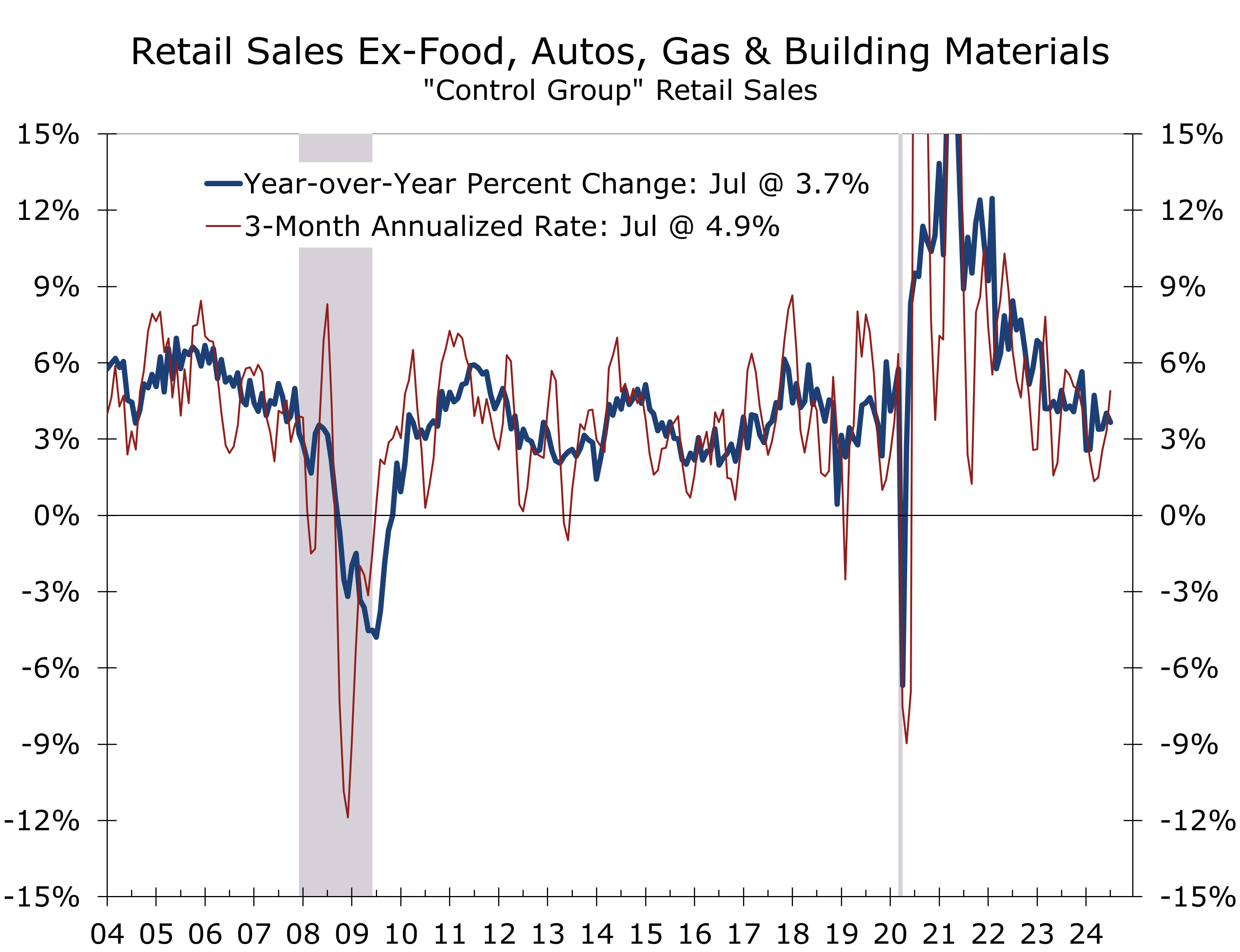

- Core retail sales, which exclude autos, gasoline, building materials and food; rose 0.3% and are up 3.7% year-to-year.

- The rise in core retail sales gives spending a strong start for Q3, though we remain cautious due to slowing services outlays.

- The July retail sales report coincided with Walmart's strong earnings and followed another benign inflation report, all of which are interconnected. Moderating gains in grocery prices are freeing up some discretionary dollars and consumers appear to be gravitating to items where prices have eased somewhat. This favors discount stores but provides less relief to department stores.

Retail sales easily beat expectations in July, rising a robust 1.0% from the prior month. The headline gain was primarily driven by a 3.6% rebound in auto sales following a cyberattack-related disruption in June. Excluding autos, retail sales still posted a healthy 0.4% gain, as spending rose solidly across most major business categories. Moreover, spending rose in 11 of the 13 major business categories tracked in the retail sales report.

While the underlying details were not as strong as the headline figures, the data supports a solid outlook for consumer spending in Q3. Coming on the same day as Walmart’s better-than-expected earnings, the financial markets took the surprisingly strong July retail sales report as a sign that consumers are shrugging off slowing job and income growth and leaning more into their stronger balance sheet. Mortgage refinancing applications did pop up this past week, with the MBA noting refi applications jumped 35% in early August.

We remain somewhat more cautious and look for real personal consumption expenditures to rise at a 2.5% annual rate for the quarter. This is likely a bit lower than the current consensus. July is one of the lightest months of the year for retail sales, so it does not take much out of the ordinary to move the seasonally adjusted data. Walmart also appears to be better positioned to benefit from recent shifts in consumer behavior, as any money saved on groceries can bolster spending elsewhere on the same shopping trip.

Consumer spending remains resilient, though we’re adopting a more cautious stance on the third-quarter outlook. Control group sales, which are crucial for calculating Personal Consumption Expenditures (PCE) and real GDP, rose by 0.3% in July, following a strong 0.9% increase in June. Over the past three months, control group retail sales have grown at an impressive 4.9% annualized rate, indicating solid momentum.

The recent strength in core retail sales gets the third quarter off to a strong start.

This strength suggests that the third quarter is off to a strong start. Even if control group sales remain flat in August and September, sales would still rise at a 4% pace for the quarter. We anticipate further gains, however, as back-to-school sales in August and September boost spending at department stores and clothing retailers, two categories that saw declines in July, down 0.2% and 0.1%, respectively. Spending on services is likely to rise less rapidly in Q3, reflecting some moderation in outlays for travel and experiences.

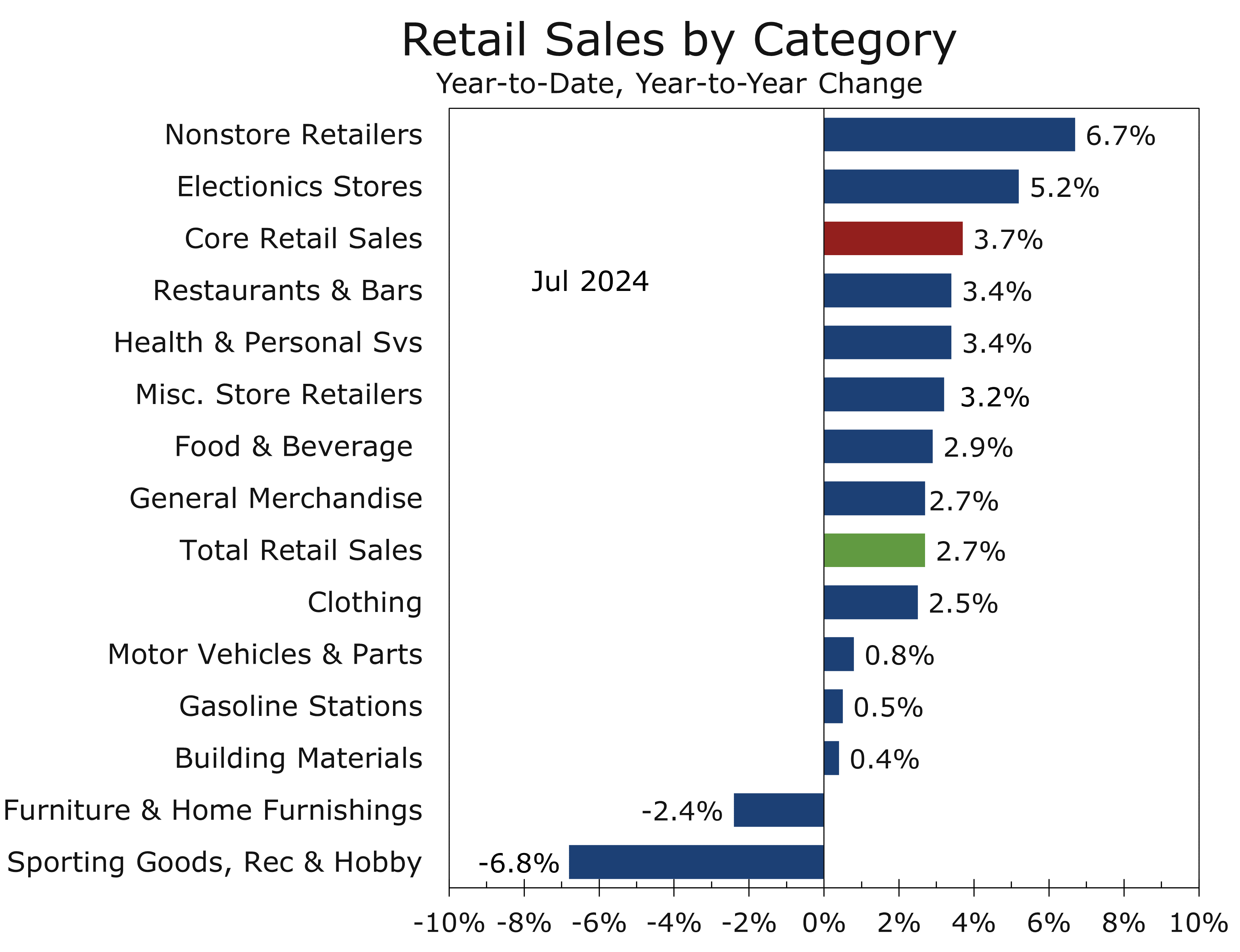

Non-store retailer sales, which includes e-commerce, rose a surprisingly soft 0.2% increase in July. This subdued performance occurred despite Amazon Prime Day, which appears to have had less impact this year compared to a 2.2% rise in non-store retail sales last July. Non-store sales remain up solidly year-over-year.

One of the more encouraging aspects of July’s retail sales report is that sales rose broadly, with 11 of the 13 business categories posting gains in July and on a year-to-year basis. This broad-based increase suggests the strength in retail sales will prove more durable and less susceptible to downward revision.

Gains in retail sales were broad based, which suggest the strength will prove more durable.

In addition to the 6.7% year-to-year rise in non-store sales, sales rose 5.2% at electronics stores and climbed 3.4% at restaurants and bars. Price for the latter two categories have behaved dramatically differently, with prices for televisions and household appliances declining 5.4% and 3%, respectively, suggesting exceptionally strong gains over the past year on an inflation-adjusted basis; while prices for food consumed away from home rose 4.1%, implying a real decline in spending after accounting for inflation.

July’s stronger-than-expected retail sales helps alleviate concerns the economy is on the verge of a recession. The data also diminishes the likelihood of a more aggressive 50 basis point rate cut at the upcoming September FOMC meeting.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

August 15, 2024

Mark Vitner, Chief Economist

Piedmont Crescent Capital

mark.vitner@piedmontcrescentcapital.com

704-458-4000

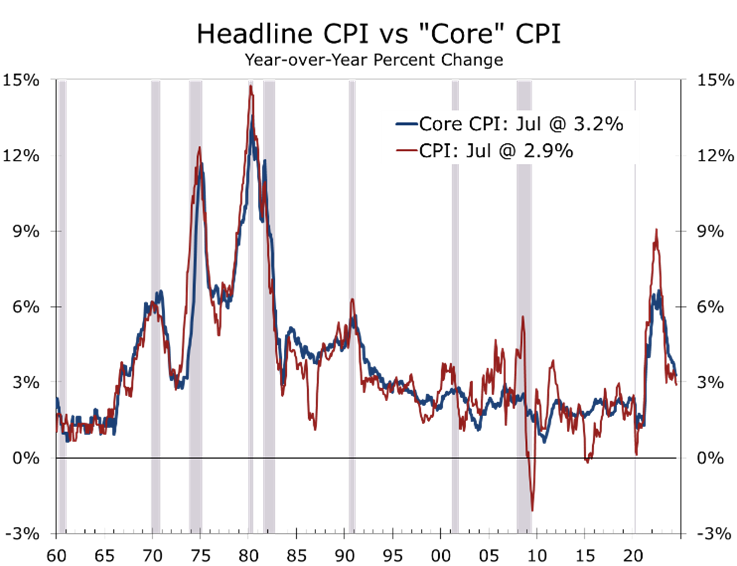

CPI Inflation Bounces Back to its Recent Trend

Inflation Rises Close to Expectations in July

- The headline CPI rose 0.2% in July, following a 0.1% drop the prior month.

- Shelter costs rose 0.4%, driving nearly 90% of July’s overall CPI increase.

- Residential rent rose 0.5% in July and is up a 24.5% from its pre-pandemic level.

- Energy prices were flat, with gasoline prices also unchanged for the month.

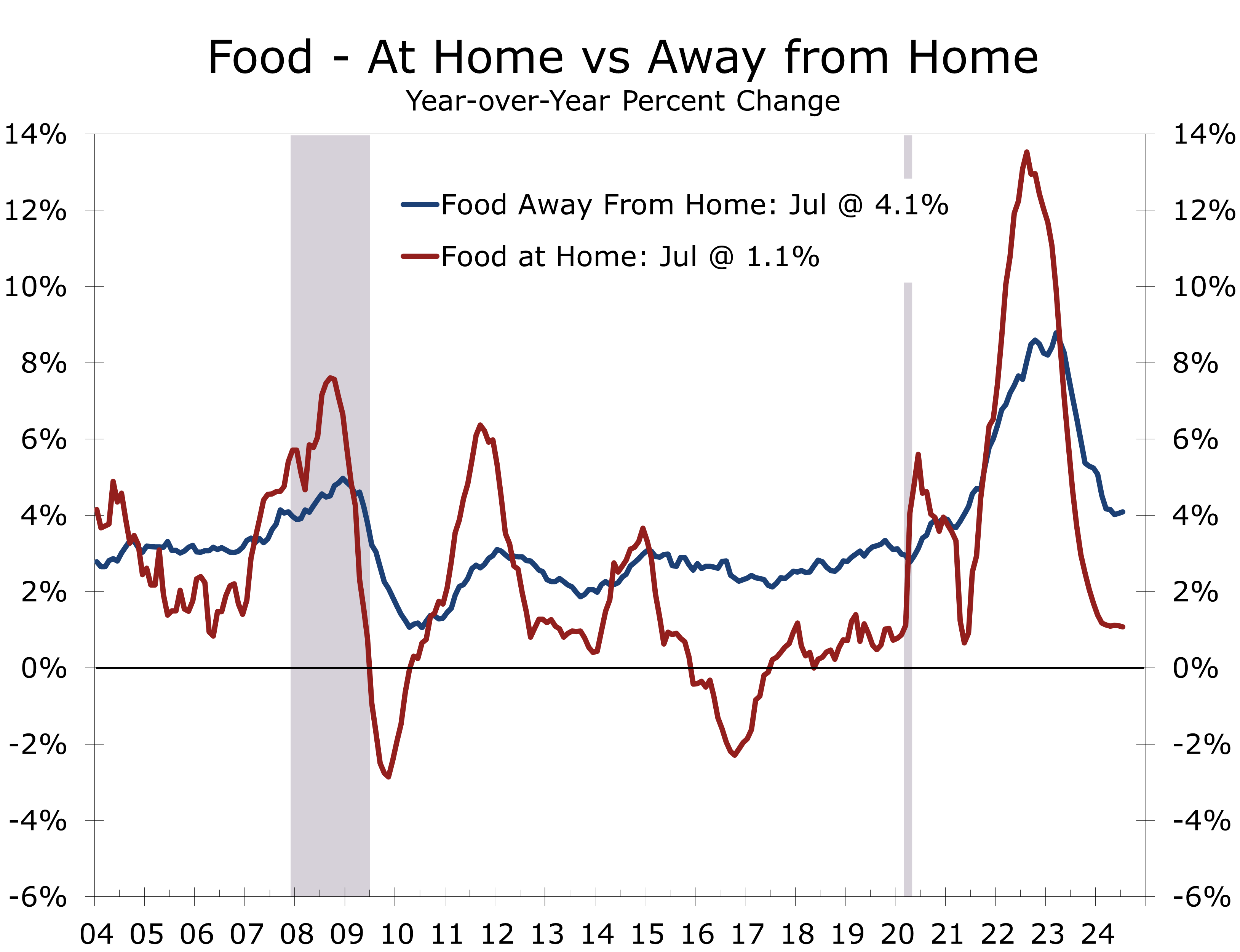

- Food prices rose 0.2%, the same as in June. Prices rose 0.1% at grocery stores, while prices for food away from home rose 0.4%.

- On a year-to-year basis, the headline CPI fell to 2.9%, the smallest increase since March 2021, while the core rose 3.2%.

- Within the core CPI, transportation costs rose sharply, driven by higher insurances cost. Medical care costs declined slightly.

- Inflation is moderating as anticipated, supporting a potential rate cut in September. Markets remain divided on whether the Fed will begin its easing process with a quarter- or half-point cut, with the Jackson Hole conference offering some possible insights. The key determinant, however, will likely be whether the August jobs data refute or reinforce the message from the surprisingly weak July jobs data.

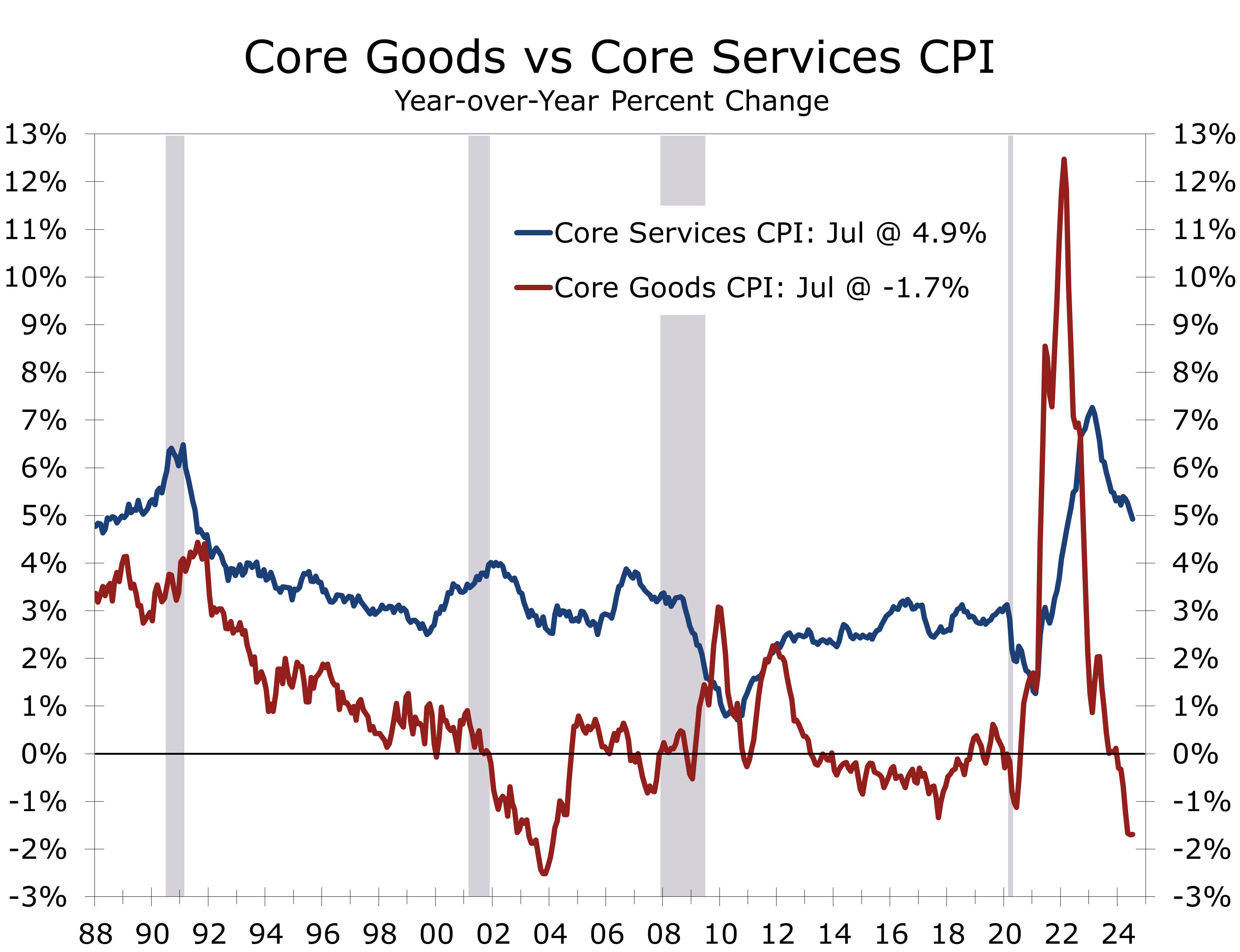

The Consumer Price Index (CPI) rose by 0.2% in July, following a rare 0.1% decline in June. This modest increase met market expectations, offering some relief after recent inflation data volatility. Over the past year, headline CPI climbed 2.9%, marking the smallest annual increase since March 2021. The core CPI, excluding food and energy, also saw a 0.2% uptick, pushing its annual rise to 3.2%.

The underlying details of the report show the continuation of a number of important trends. Core goods prices fell 0.3% in July and are now down 1.9% year-to-year. Used car prices tumbled 2.3% in July, following a 1.5% drop the prior month and are now 10.9% lower than they were a year ago.

Inflation continues to moderate in line with expectations, setting the stage of lower rates.

Core services, including shelter, motor vehicle insurance, and medical care, rose 0.3% in July. Service prices continue to be driven higher by rising costs for shelter and transportation services, which both rose 0.4% in July. Prices for medical care services eased 0.3%, driven by a 1.1% decline in hospital services. Despite this, the overall medical care sector remain up 3.2% year-to-year and remains a significant contributor to overall inflation.

Shelter costs remain the biggest hurdle to bringing down inflation. Shelter costs remained stubbornly high in July, with the shelter index rising by 0.4%. This category accounted for nearly 90% of the overall CPI increase. The acceleration in shelter costs was broad-based, impacting tenant rents, owners’ equivalent rent, and lodging away from home. Residential rent, in particular, continues to prove uncomfortably persistent, rising 0.5% in July and climbing a cumulative 24.5% from its pre-pandemic level. High housing costs have likely kept renters in apartments longer, putting upward pressure on renewal rents.

Core services prices are proving resilient, largely due to persistent pressure on shelter costs.

Over the past year, core services are up 4.9%, with transportation services cost surging 8.8% and shelter climbing 5.1%. The persistent rise in core services prices, which are driven by both an overall shortage of housing, higher labor costs, and, in the case of insurance, some catch up from COVID-related price hikes, is a key variable the Federal Reserve continues to monitor closely. The unusual aspects of the post pandemic era have likely meant that the lags between changes in monetary policy and their impact on economic growth and inflation have changed, which is a subject certain to be discussed at the upcoming Jackson Hole monetary policy conference.

The energy index remained flat in July, following two consecutive months of decline. Gasoline prices were unchanged, while electricity and fuel oil posted modest gains. However, seasonal factors put downward pressure on the overall energy index in July. Looking ahead, these factors will reverse in August, potentially boosting the CPI and adding an element of uncertainty to what will be the final inflation reading before the September FOMC meeting.

Food prices rose by 0.2% in July, maintaining the pace seen in June. Grocery store prices rose 0.1% but the underlying data were mixed, with meats, poultry, fish, and eggs increasing, while cereals, bakery products, and dairy saw slight declines. The consistent rise in food prices underscores ongoing inflationary pressures within this category. Prices at restaurants rose 0.2% in July and are up 4.1% over the past year.

The Fed is likely satisfied with the latest CPI print. Our analysis of the CPI and PPI components hints at a downside surprise for the PCE deflator later this month, with the core PCE deflator rising only 0.1% after rounding down. Despite this, we maintain our forecast for just two quarter-point cuts this year, followed by 2 more in 2025.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

August 14, 2024

Mark Vitner, Chief Economist

Piedmont Crescent Capital

704-458-4000

mark.vitner@piedmontcrescentcapital.com

Higher Interest Rates Bring About a Soft Landing in Georgia

How Much Softer Will Georgia’s Economy Get?

- Higher interest rates weighed on the economy’s most cyclical sectors during the first half of 2024.

- Hiring has slowed overall, with the bulk of growth now coming from less cyclical sectors, such as health care, social services, leisure, hospitality, and government.

- The weakness in the goods sector has weighed on Georgia’s manufacturing and logistics sectors. The state’s large motion picture industry is also working through a lull following the writers’ and actors’ strikes.

- Large numbers of people and new industry continue to move to the state, helping sustain strong momentum in residential, commercial, and industrial development.

- The Fed is poised to cut interest rates, which should lift home sales and housing-related industries. Georgia also continues to invest for its future, with extensive investments in infrastructure and higher education.

- The recent lull in Georgia's economy should continue into the second half of this year. The buildout of EV plants, data centers and key infrastructure is providing a huge lift to construction. Hiring should strengthen by early 2025, as lower interest rates spur home buying and lift housing-related industries.

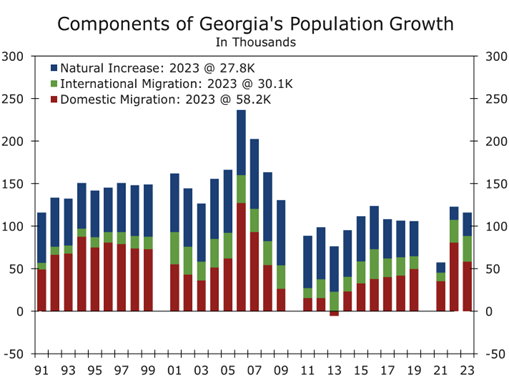

Higher interest rates cooled off Georgia’s economy during the first half of 2024, proving once again how monetary policy works with a lag. The Federal Reserve began to raise interest rates in March 2022 and the full impact of those rate hikes became evident this spring.

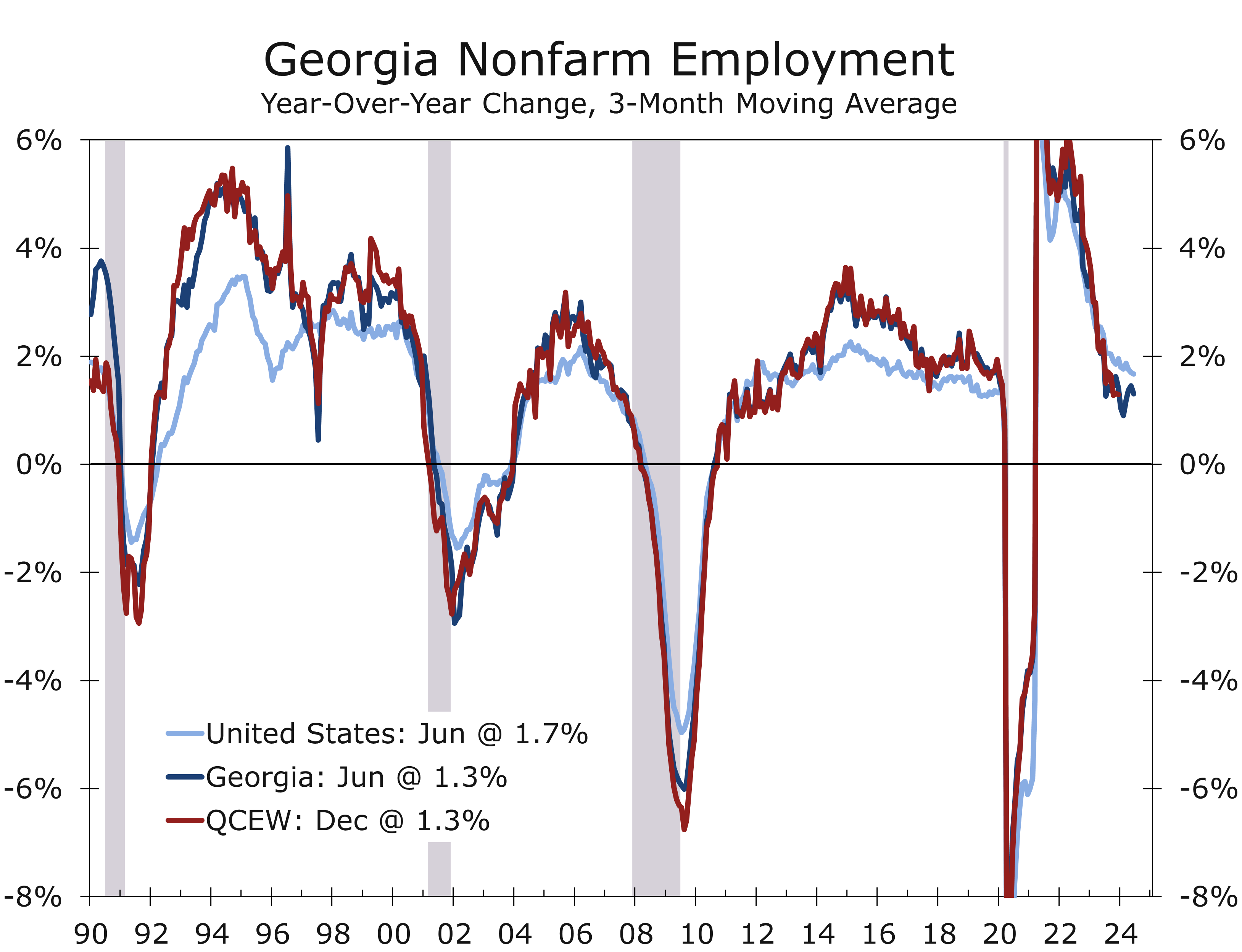

Nationally, real GDP growth slowed from a torrid 4.2% pace in the second half of 2023 to just a 2.1% pace in the first half of 2024. Job growth slowed from 250,000 net new jobs a month in 2023 to just 170,000 per month during the second quarter, while the nation’s unemployment has risen 0.6 percentage points since the start of the year to 4.3%.

After rebounding from the pandemic, Georgia’s economy has cooled along with the nation.

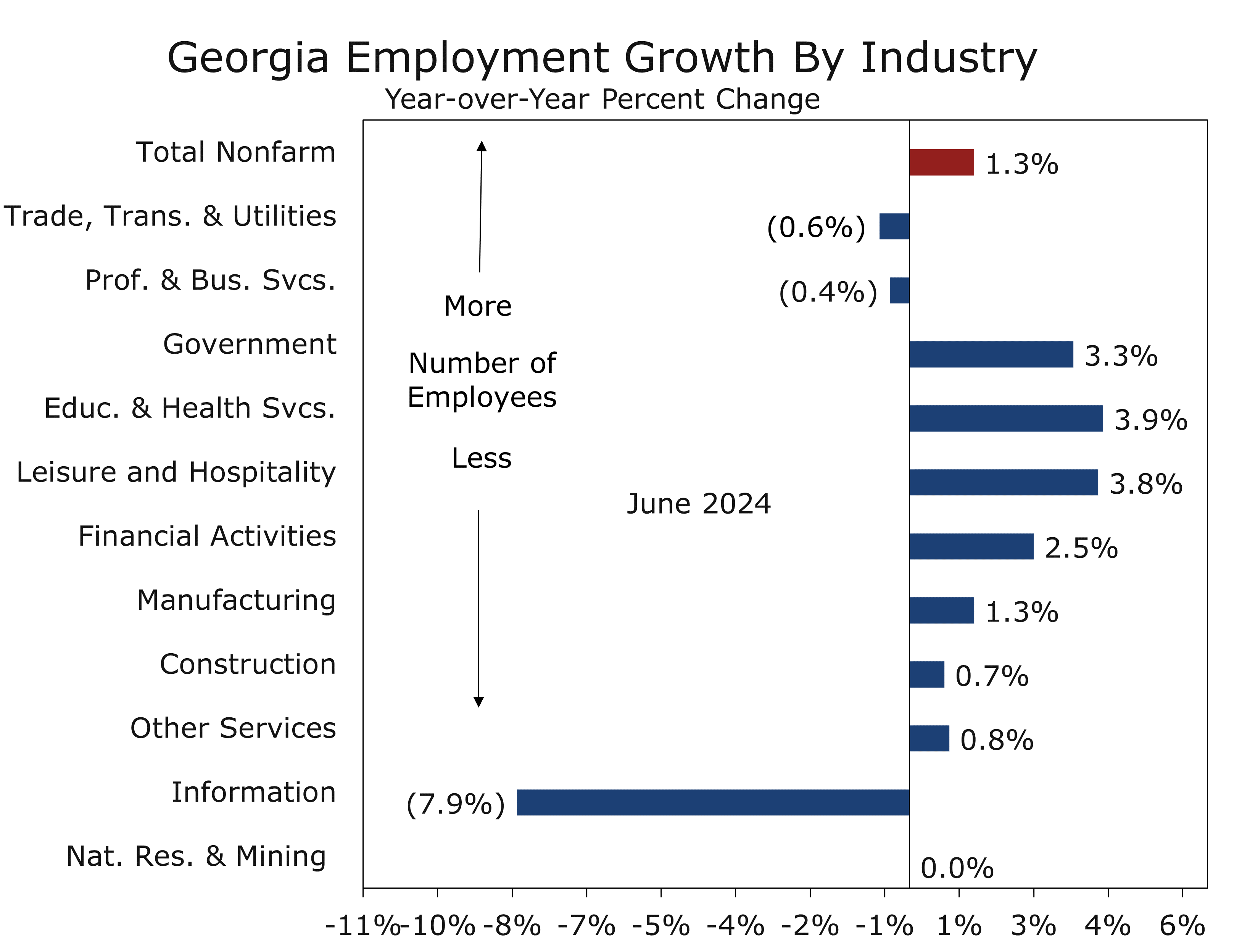

Georgia’s economy cooled off during the first half of 2024. Job growth slowed to just 1.3% on a year-over-year basis from 2.9% a year ago. Job growth is roughly in line with other states but slightly trails the nation. The state’s unemployment rate rose slightly to 3.2%.

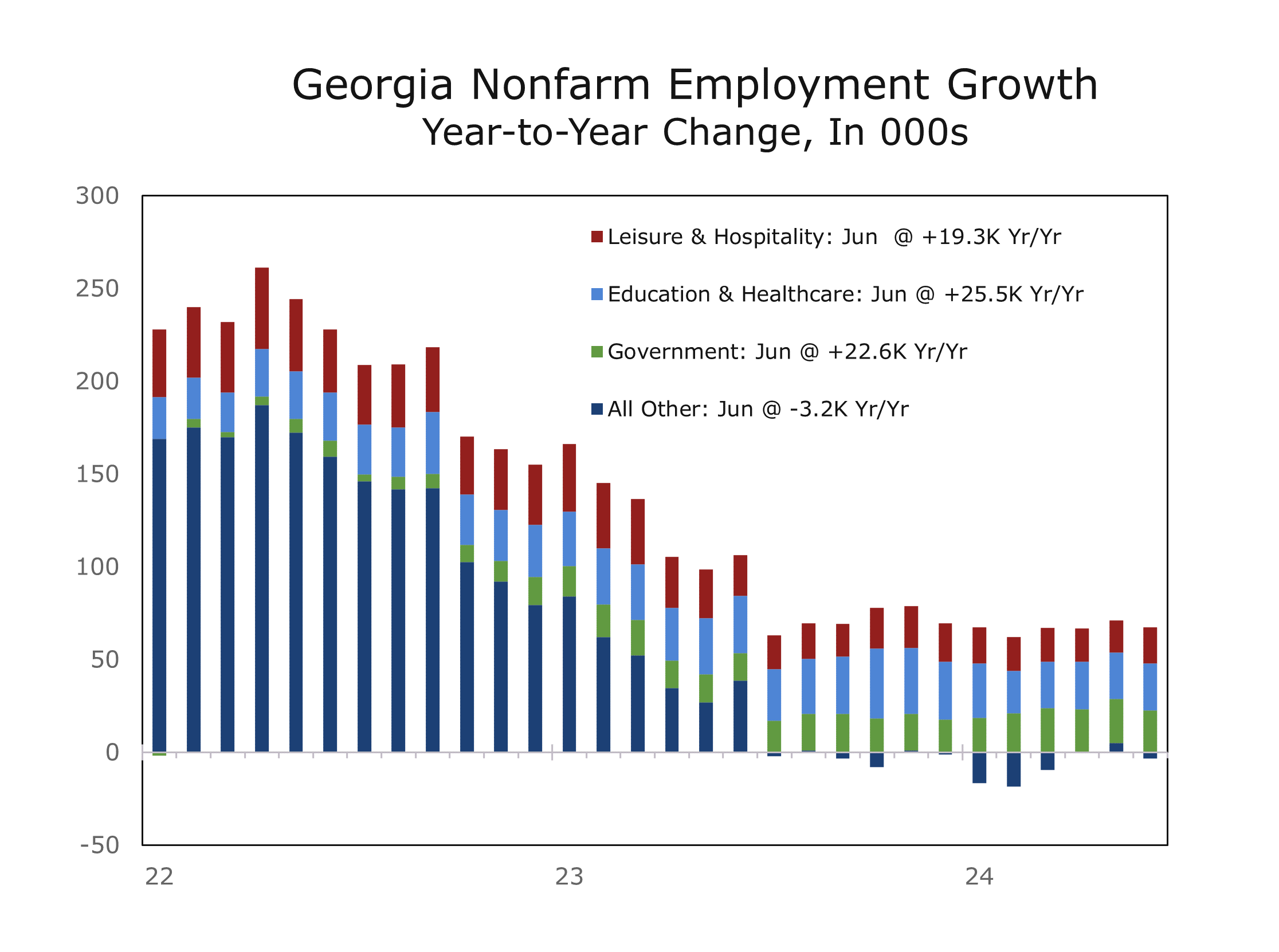

Businesses created 41,600 net new jobs this past year, driven by hiring at hotels, restaurants, and healthcare providers. The public sector also grew, with federal, state, and local governments adding 22,600 jobs. Georgia’s manufacturing and logistics sectors have slowed, however, as consumer spending shifted towards services. The long-running slump in existing home sales and weakening residential construction are also weighing on Georgia’s large floor coverings, home improvement and building products sectors.

While overall job growth remains robust, most new jobs are being added in occupations where workers must physically be at work and pay relatively low wages. Some of the largest gains have been at restaurants and bars, doctors’ and dentists’ offices, social services agencies and home healthcare providers. Government jobs are also heavily weighted toward jobs that require physical tasks such as sanitation and maintenance workers, and bus drivers.

The split in job growth is striking. Leisure and hospitality, education and healthcare, and government collectively comprise 39% of Georgia’s employment base but have accounted for virtually all the new jobs created over the past year. Other industries have lost a combined 3,200 jobs over this period and this split has been evident for the past year. The same trend has persisted nationally, albeit to a slightly lesser degree.

While statistically, employment in leisure & hospitality, education and healthcare, and government has accounted for all of Georgia’s job growth this past year, the underlying details show most industries still added staff last year. The split in overall job creation results from outsized losses in a handful of Georgia’s largest industry employment supersectors.

Georgia’s job gains and job losses are highly concentrated in a handful of industries.

Trade, Transportation and Utilities is Georgia’s largest employment supersector, including everything jobs at Walmart, Publix, Sysco Foods, Delta Airlines and Georgia Power, as well as myriads of warehouses and distribution centers lining the highways leading into and out of Atlanta and near the Port of Savannah. This supersector accounts for 21% of all jobs in Georgia.

Retail trade accounts for about half the jobs in the supersector and has seen hiring slow significantly this past year, as spending has shifted from goods purchases to experiences such as travel, concerts, sporting events, and services like healthcare. Transportation and warehousing account for just over a quarter of the supersector’s employment base and have seen employment fall by 2.5% this past year, reflecting the global goods recession. Employment at utilities has remained essentially flat.

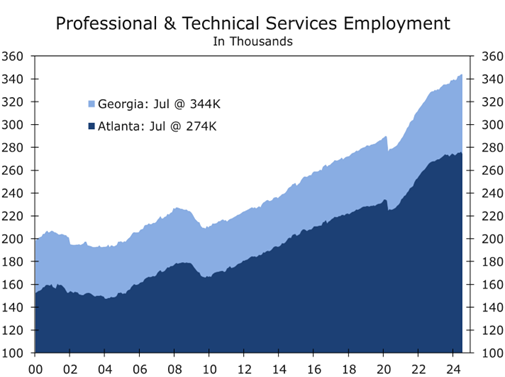

Professional and business services are another large employment supersector that have lost jobs over the past year. This sector includes a broad range of categories, from professional, scientific, and technical services—encompassing everything from lawyers, architects, and accountants to software engineers, researchers, and IT consultants—to the management of corporate enterprises, primarily involving jobs at corporate and regional headquarters. Additionally, it includes administrative, maintenance, and support services, which cover a variety of roles such as office administration, human resources, security services, and cleaning and waste disposal.

Georgia’s large professional services sector has slowed, as employers have tightened their belts.

Among the three major subgroups, employment in professional, scientific, and technical services has fared the best, with employers adding 9,000 jobs over the past year, primarily driven by growth in Atlanta’s tech sector. However, employment at regional headquarters has slowed, with major employers like NCR Voyix, UPS, Intuit, and Home Depot reducing staffing. The most significant shift has been in administrative positions, which lost 14,700 jobs due to decreased demand for temporary workers at warehouses, distribution centers, manufacturers, and corporate offices.

Georgia’s information sector experienced the steepest job loss this past year, with payrolls plunging 7.9% and resulting in 9,500 fewer jobs. Despite being the state’s smallest employment supersector, it carries significant challenges and a high profile.

Though often associated with tech workers, the information sector also includes telephone and cable companies, newspapers, TV and radio broadcasters, and publishing. These industries, particularly in Atlanta, have faced sluggish growth and layoffs due to intense competition from digital streaming.

Conversely, data processing and hosting are continuing to grow. A surge in data center construction, driven by increasing AI demands, underscores Atlanta’s strategic position as one of the nation’s key internet hubs.

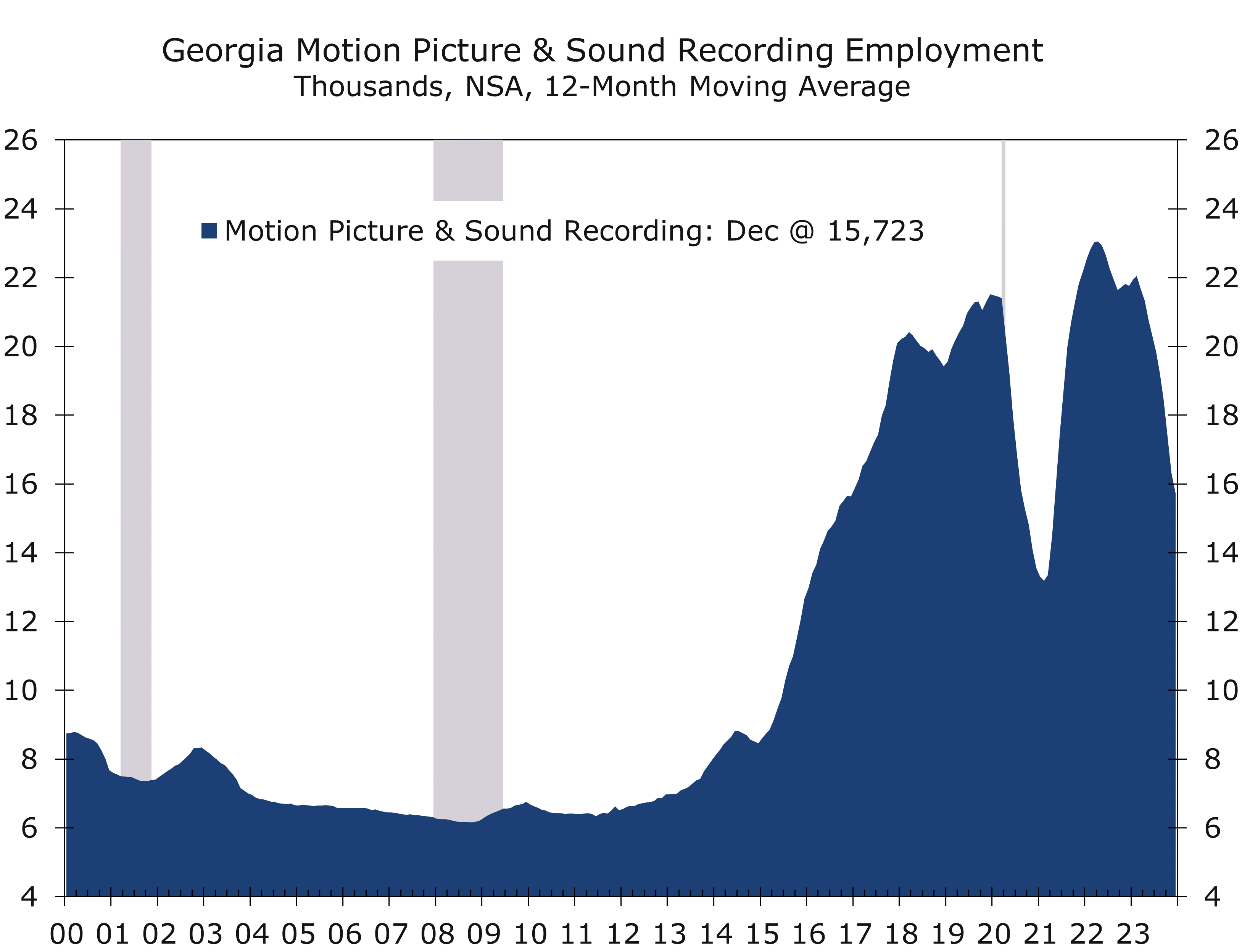

Georgia’s motion picture industry surged post-pandemic but has struggled more recently.

The most significant shift in information services employment has been in the motion picture industry. Georgia’s motion picture sector surged as the economy emerged from the pandemic, with studios reopening much earlier than those in California. However, last year’s actors’ and writers’ strikes caused a slowdown in production, which has been exacerbated by cost-cutting measures at major studios. California has also won back some business.

Georgia’s large manufacturing and logistics sectors are currently experiencing a slowdown. The goods sector has faced significant pressure since consumer spending shifted toward travel and services in 2022. The state’s manufacturing workforce, comprising 435,000 employees, is almost evenly split between durable and nondurable goods producers.

Major manufactured products in Georgia include carpets, engineered flooring, building materials, food processing items, military and corporate aircraft, motor vehicles, and various industrial products. Over the past year, manufacturing employment increased by 1.3%, with notable growth in the automotive and aerospace sectors. However, the production of consumer products and building materials has lagged.

The global goods recession has slowed Georgia’s sizable manufacturing and logistics sectors.

The Atlanta area encompasses 770 million square feet of industrial space, making it the nation’s fourth-largest distribution hub. Savannah and Middle Georgia also serve as key distribution centers. The rapid growth at the Port of Savannah has driven strong demand for industrial space. The logistics sector, which includes transportation, warehousing, and wholesale trade, employs just under 500,000 workers in Georgia, down approximately 1.2% from the previous year.

The modest decline in Georgia’s logistics sector was likely concentrated in the Atlanta area, where most trucking and warehouse workers are based. In addition to layoffs at warehouses and distribution centers, UPS, headquartered in Sandy Springs, also implemented layoffs this past spring. Other notable reductions occurred among logistics firms in Savannah and Middle Georgia.

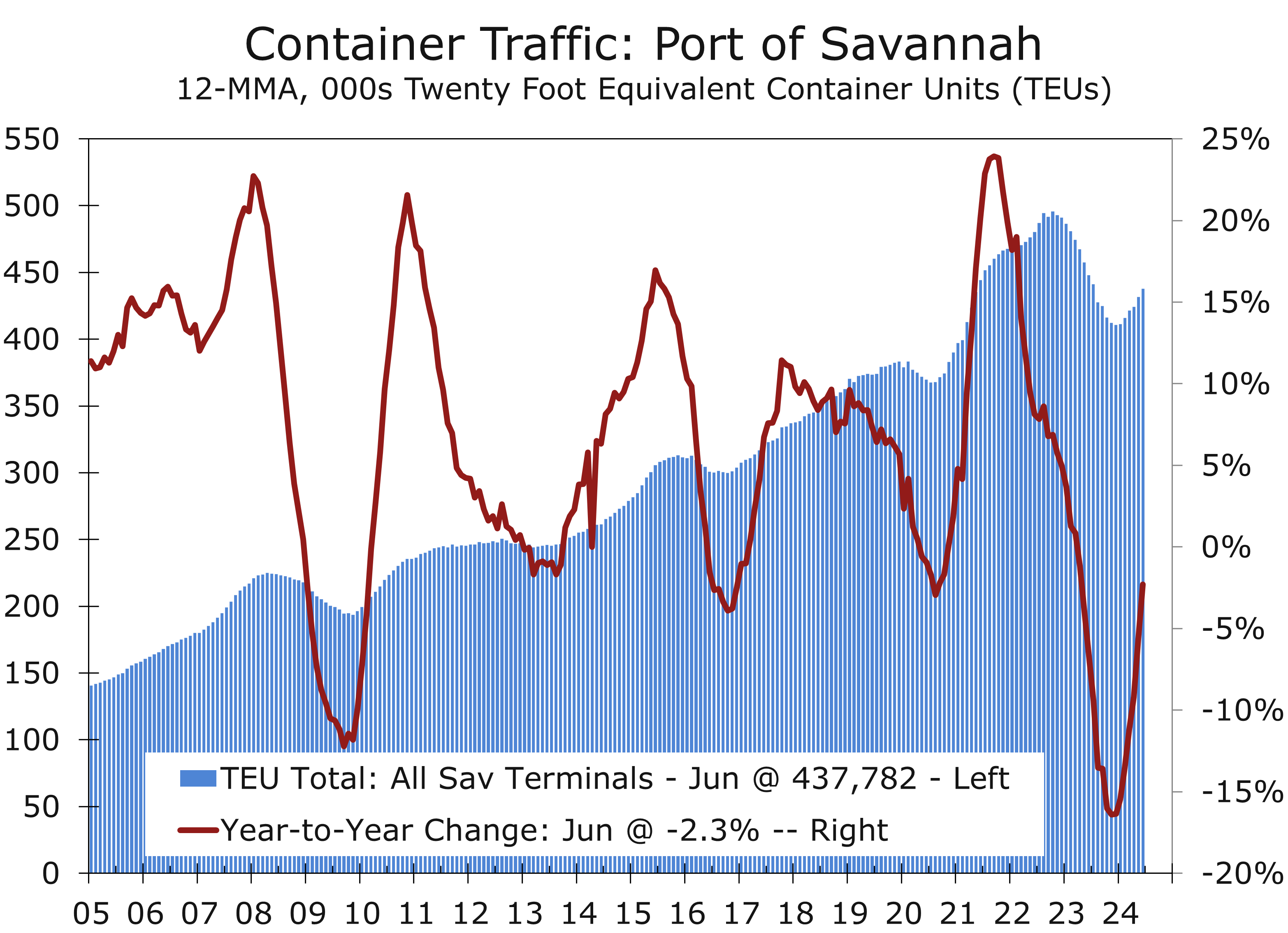

Despite these challenges, the Port of Savannah remains a vital economic engine for Georgia and continues to expand. As the nation’s third-largest container port, it recently completed the new Garden City Terminal West facility. The Port is adding more ship-to-shore cranes and rubber-tired gantry cranes and has extensive rail connections that facilitate quick transfer of containers to trains for shipment across the South and Midwest.

Container traffic saw a modest 2.3% decline for the fiscal year ending June 30, with the Port handling 5.25 million twenty-foot equivalent units. This drop reflects a return of some traffic that had been diverted from the West Coast and a slowdown in shipments amid the global goods recession. Traffic has been improving more recently. Additionally, the Port of Brunswick had a record year in Roll-on/Roll-off cargo, handling 876,000 units of autos and heavy machinery in FY2024, a 21% increase from the previous year.

Atlanta, typically responsible for two-thirds of Georgia’s job growth, has underperformed this year. The metro area has been disproportionately impacted by weaknesses in the logistics sector, significant cuts in information and motion picture jobs, and stagnation in professional and business services. Consequently, Atlanta’s payroll growth slightly lags behind the state’s overall 1.3% gain.

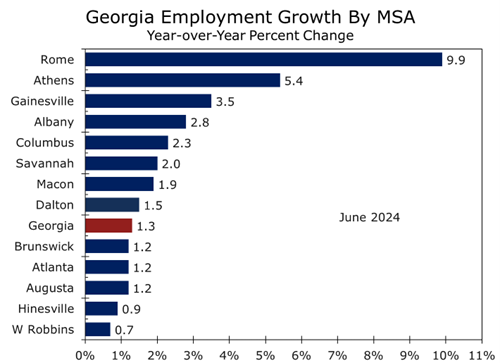

Georgia’s classic metros, Rome and Athens, led the state in job growth this past year.

Strong gains in health care and education drove nonfarm payrolls up by 9.9% in Rome and 5.4% in Athens. Gainesville, just outside the Atlanta metro area, has also prospered due to new industry and population growth, as has Jefferson, located along I-85 between Gainesville and Athens.

Albany, Columbus, and Savannah have shown resilience, supported by strong economic development. In Albany, agriculture, downtown redevelopment, and infrastructure upgrades have all boosted growth. The completion of Plant Vogtle reduced construction jobs in Augusta; without this, payrolls would have risen 1.7% year-over-year. Columbus has attracted several new industrial projects, and Middle Georgia, particularly Macon, remains resilient with payrolls up 1.9%, primarily due to growth in health care and private education.

Despite a recent slowdown in job growth and an uncertain national economic outlook, Georgia’s economy remains well-positioned. The stability of its large manufacturing and construction sectors, the most cyclical parts of the economy, highlights the state’s success in attracting billions in new industrial projects and thousands of new residents each year.