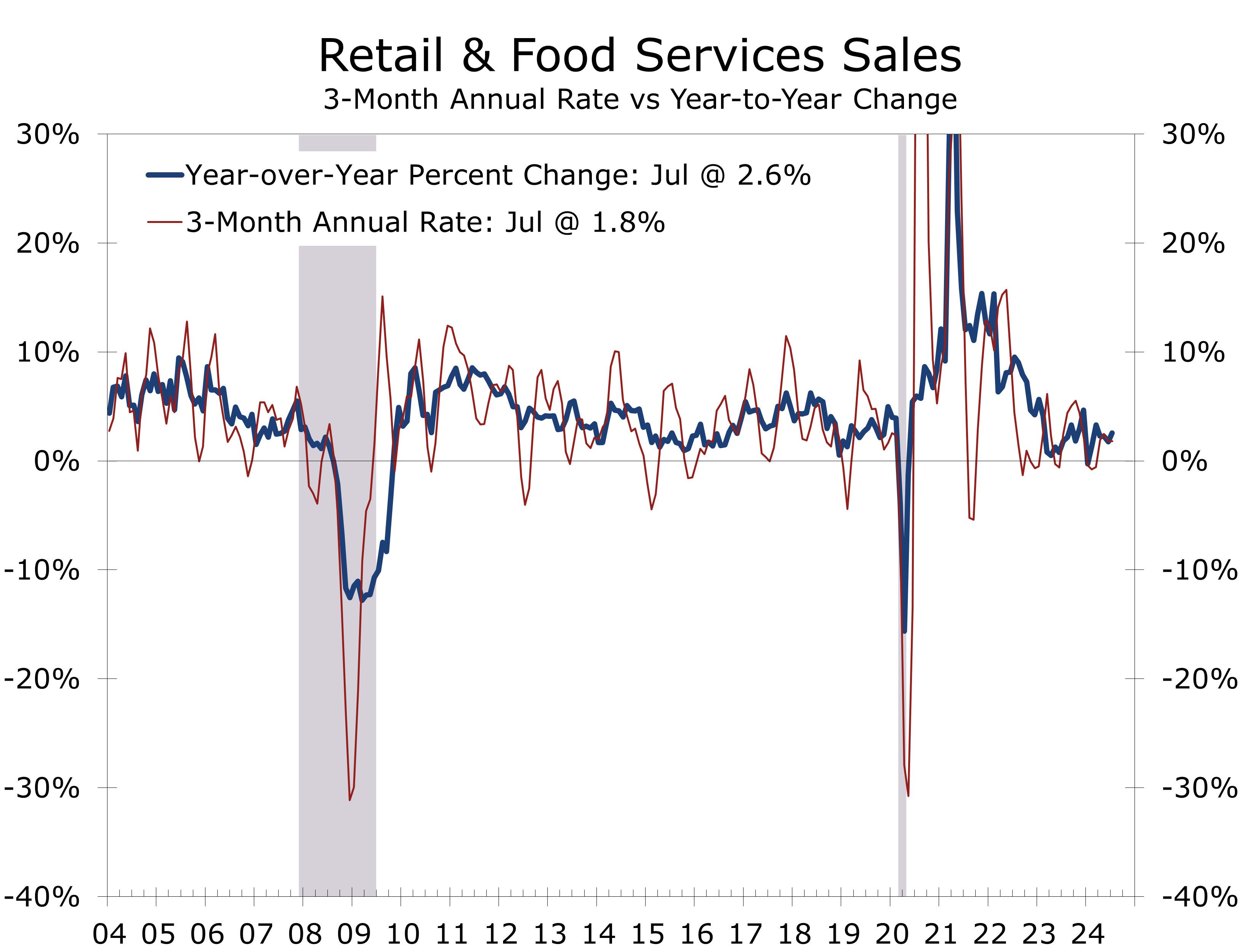

Headline Rise Overstates Consumer Strength

- Retail sales rose 1.0% is July, far exceeding the consensus of 0.3%.

- A 3.6% surge in auto sales, following June’s cyber-attack driven drop, was a major driver of the headline gain.

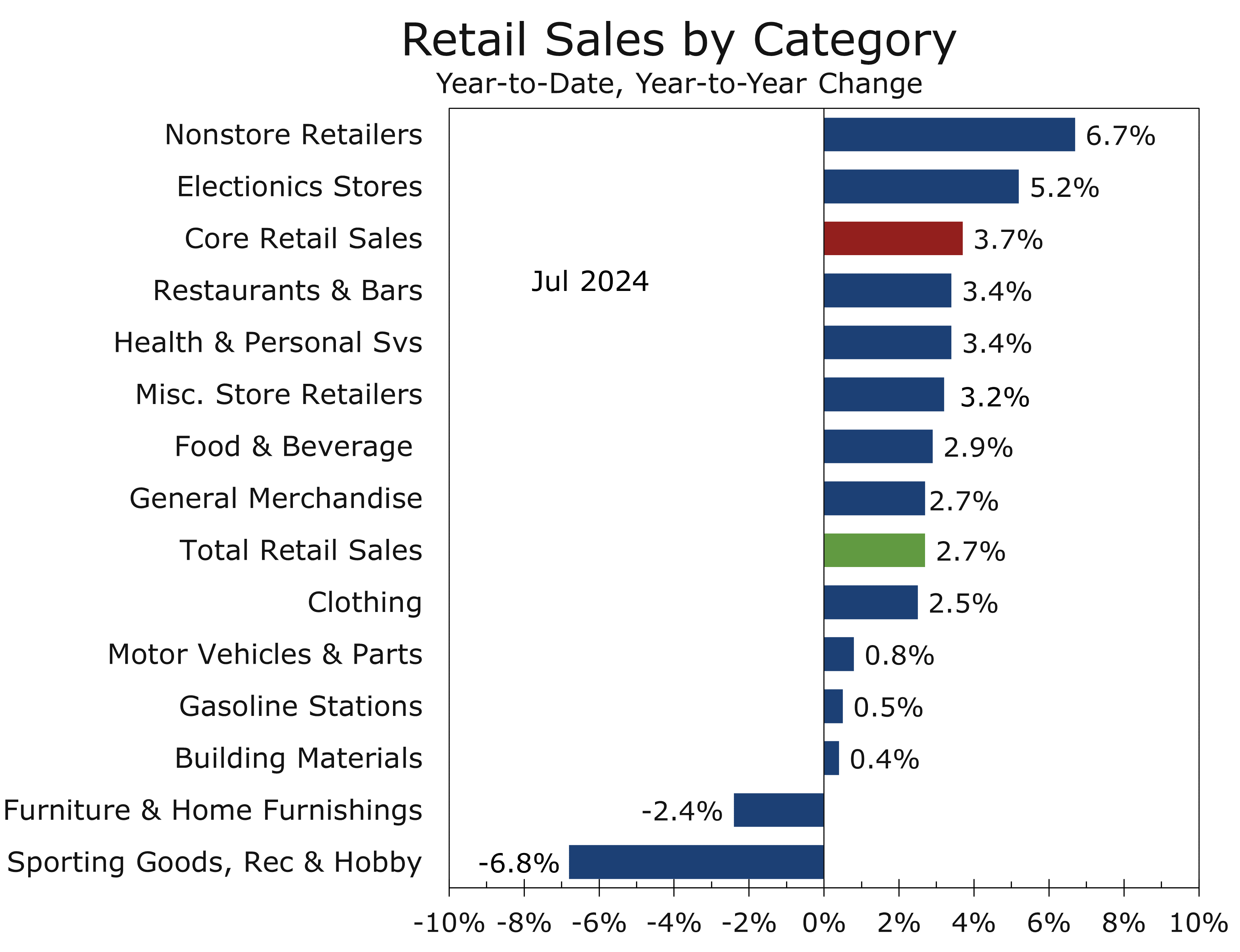

- Excluding autos, retail sales increased by 0.4%, with 11 of the 13 major business categories posting gains in July.

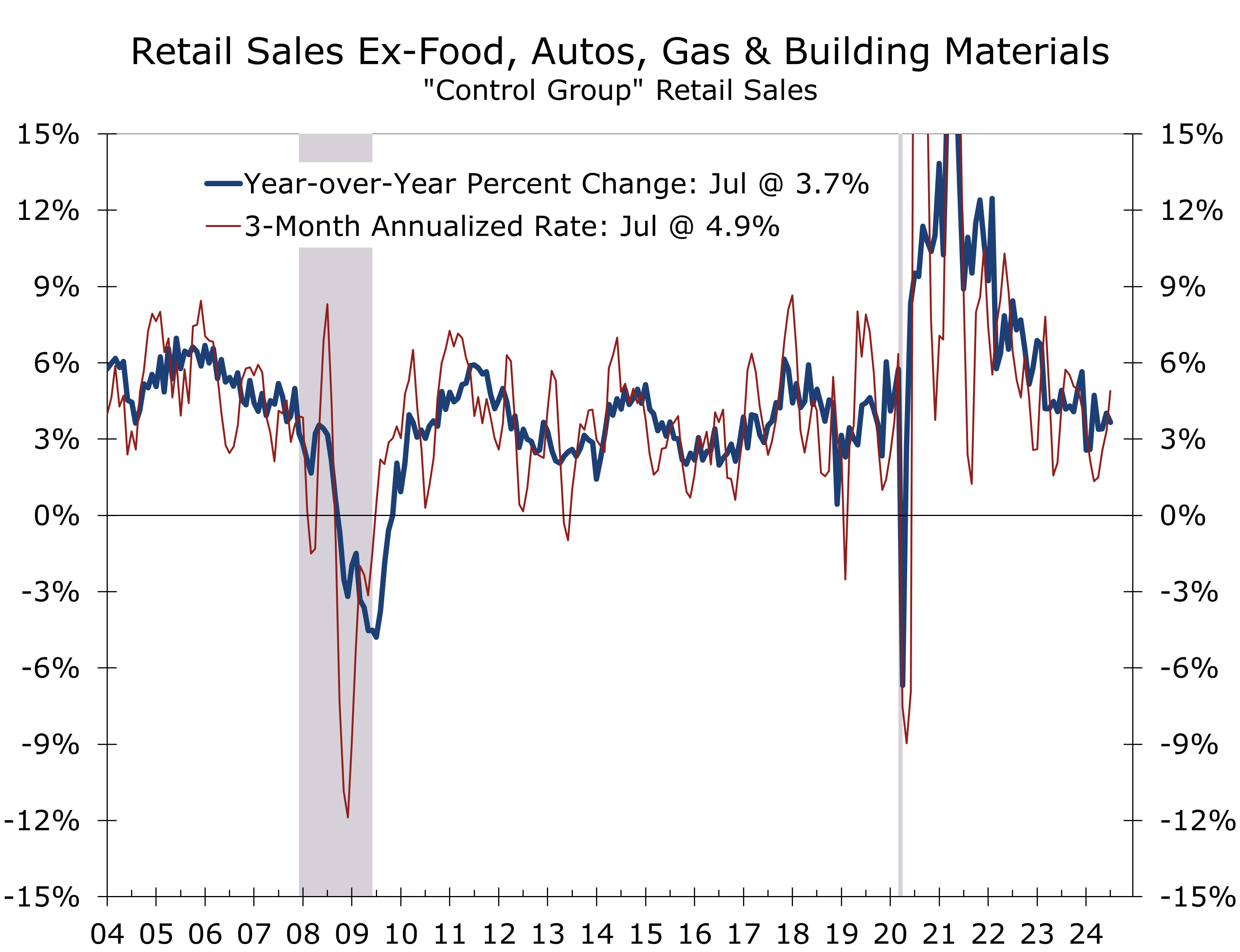

- Core retail sales, which exclude autos, gasoline, building materials and food; rose 0.3% and are up 3.7% year-to-year.

- The rise in core retail sales gives spending a strong start for Q3, though we remain cautious due to slowing services outlays.

- The July retail sales report coincided with Walmart’s strong earnings and followed another benign inflation report, all of which are interconnected. Moderating gains in grocery prices are freeing up some discretionary dollars and consumers appear to be gravitating to items where prices have eased somewhat. This favors discount stores but provides less relief to department stores.

Retail sales easily beat expectations in July, rising a robust 1.0% from the prior month. The headline gain was primarily driven by a 3.6% rebound in auto sales following a cyberattack-related disruption in June. Excluding autos, retail sales still posted a healthy 0.4% gain, as spending rose solidly across most major business categories. Moreover, spending rose in 11 of the 13 major business categories tracked in the retail sales report.

While the underlying details were not as strong as the headline figures, the data supports a solid outlook for consumer spending in Q3. Coming on the same day as Walmart’s better-than-expected earnings, the financial markets took the surprisingly strong July retail sales report as a sign that consumers are shrugging off slowing job and income growth and leaning more into their stronger balance sheet. Mortgage refinancing applications did pop up this past week, with the MBA noting refi applications jumped 35% in early August.

We remain somewhat more cautious and look for real personal consumption expenditures to rise at a 2.5% annual rate for the quarter. This is likely a bit lower than the current consensus. July is one of the lightest months of the year for retail sales, so it does not take much out of the ordinary to move the seasonally adjusted data. Walmart also appears to be better positioned to benefit from recent shifts in consumer behavior, as any money saved on groceries can bolster spending elsewhere on the same shopping trip.

Consumer spending remains resilient, though we’re adopting a more cautious stance on the third-quarter outlook. Control group sales, which are crucial for calculating Personal Consumption Expenditures (PCE) and real GDP, rose by 0.3% in July, following a strong 0.9% increase in June. Over the past three months, control group retail sales have grown at an impressive 4.9% annualized rate, indicating solid momentum.

The recent strength in core retail sales gets the third quarter off to a strong start.

This strength suggests that the third quarter is off to a strong start. Even if control group sales remain flat in August and September, sales would still rise at a 4% pace for the quarter. We anticipate further gains, however, as back-to-school sales in August and September boost spending at department stores and clothing retailers, two categories that saw declines in July, down 0.2% and 0.1%, respectively. Spending on services is likely to rise less rapidly in Q3, reflecting some moderation in outlays for travel and experiences.

Non-store retailer sales, which includes e-commerce, rose a surprisingly soft 0.2% increase in July. This subdued performance occurred despite Amazon Prime Day, which appears to have had less impact this year compared to a 2.2% rise in non-store retail sales last July. Non-store sales remain up solidly year-over-year.

One of the more encouraging aspects of July’s retail sales report is that sales rose broadly, with 11 of the 13 business categories posting gains in July and on a year-to-year basis. This broad-based increase suggests the strength in retail sales will prove more durable and less susceptible to downward revision.

Gains in retail sales were broad based, which suggest the strength will prove more durable.

In addition to the 6.7% year-to-year rise in non-store sales, sales rose 5.2% at electronics stores and climbed 3.4% at restaurants and bars. Price for the latter two categories have behaved dramatically differently, with prices for televisions and household appliances declining 5.4% and 3%, respectively, suggesting exceptionally strong gains over the past year on an inflation-adjusted basis; while prices for food consumed away from home rose 4.1%, implying a real decline in spending after accounting for inflation.

July’s stronger-than-expected retail sales helps alleviate concerns the economy is on the verge of a recession. The data also diminishes the likelihood of a more aggressive 50 basis point rate cut at the upcoming September FOMC meeting.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

August 15, 2024

Mark Vitner, Chief Economist

Piedmont Crescent Capital

mark.vitner@piedmontcrescentcapital.com

704-458-4000