Financial Markets Adjust to the Fed’s Hawkish Cut

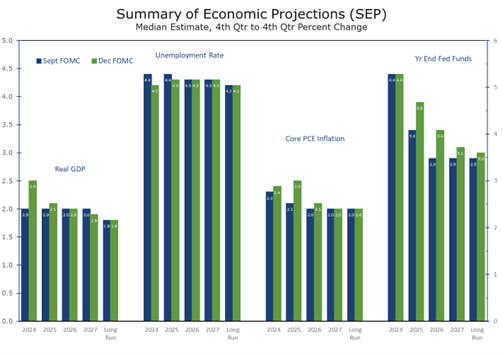

A Hawkish Quarter Point Cut in December

- The Dow Jones Industrial Average sold off 1,123 points following the Fed’s interest rate decision and Powell’s press conference.

- The FOMC lowered its target range for the federal funds rate by 25 basis points (bps) to 4.25%-4.50%, marking the third consecutive cut since September.

- There were few changes in the Fed’s policy statement, but it now emphasizes the “extent and timing” of additional adjustments, signaling a potential pause and higher endpoint for future rate cuts.

- The December Summary of Economic Projections (SEP) now calls for stronger GDP growth, higher inflation, and a higher federal funds rate in 2025 and 2026.

- The financial markets were clearly put off by the Fed’s policy statement and Powell’s press conference. The stock market sold off sharply, and the yield on the 10-year Treasury surged to 4.52%. The rise in long-term yields reflects reduced expectations for Fed rate cuts and higher expectations for growth and inflation, all of which argue for higher long-term rates.

The Fed’s Federal Open Market Committee (FOMC) cut its federal funds rate target by 25 bps to 4.25%-4.50%, bringing the cumulative reduction to 100 bps since September. While the Fed’s decision was widely expected, changes to the language in the policy statement and Summary of Economic Projects revealed a more hawkish shift to monetary policy than had been expected.

Chair Powell characterized the decision as a “closer call” and described the meeting as more contentious than previous ones. Cleveland Fed President Beth Hammack dissented, opposing further rate cuts. Additionally, the “dot plot” indicates that other Federal Reserve Bank presidents might have dissented if they were voting members this year.

The Fed’s policy statement suggests the Fed will slow the pace of rate cuts, with periodic pauses.

Despite the contentious nature of the meeting, the Policy Statement saw minimal changes. The most notable was the addition of the phrase “the extent and timing” when referencing the process for analyzing future rate cuts, signaling the possibility of a pause at the January meeting and fewer cuts ahead.

The Summary of Economic Projections (SEP) reflects expectations for stronger near-term growth, higher inflation, and a slower trajectory for future rate cuts. Additionally, the estimate for the long-run neutral federal funds rate has been slightly increased.

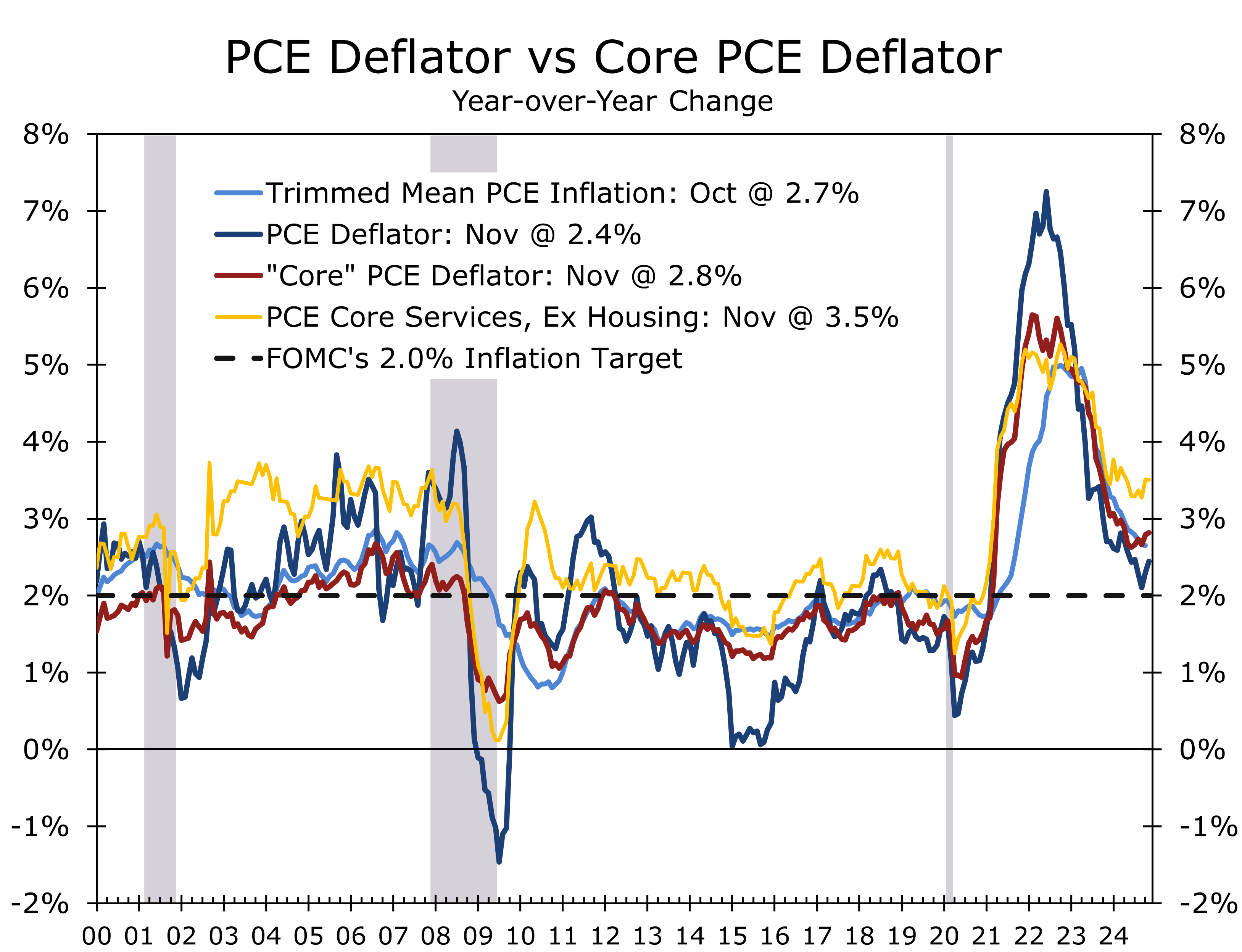

The latest data largely validate the Fed’s actions and Chair Powell’s remarks. Q3 real GDP growth was revised up to 3.1%, and the core PCE deflator, the Fed’s preferred price measure, continues to decelerate. Both the overall and core PCE deflators rose just 0.1% in November. Year-to-year, the overall PCE deflator increased 2.4%, while the core PCE deflator rose 2.8%. Excluding housing, the core PCE deflator is up 3.5%.

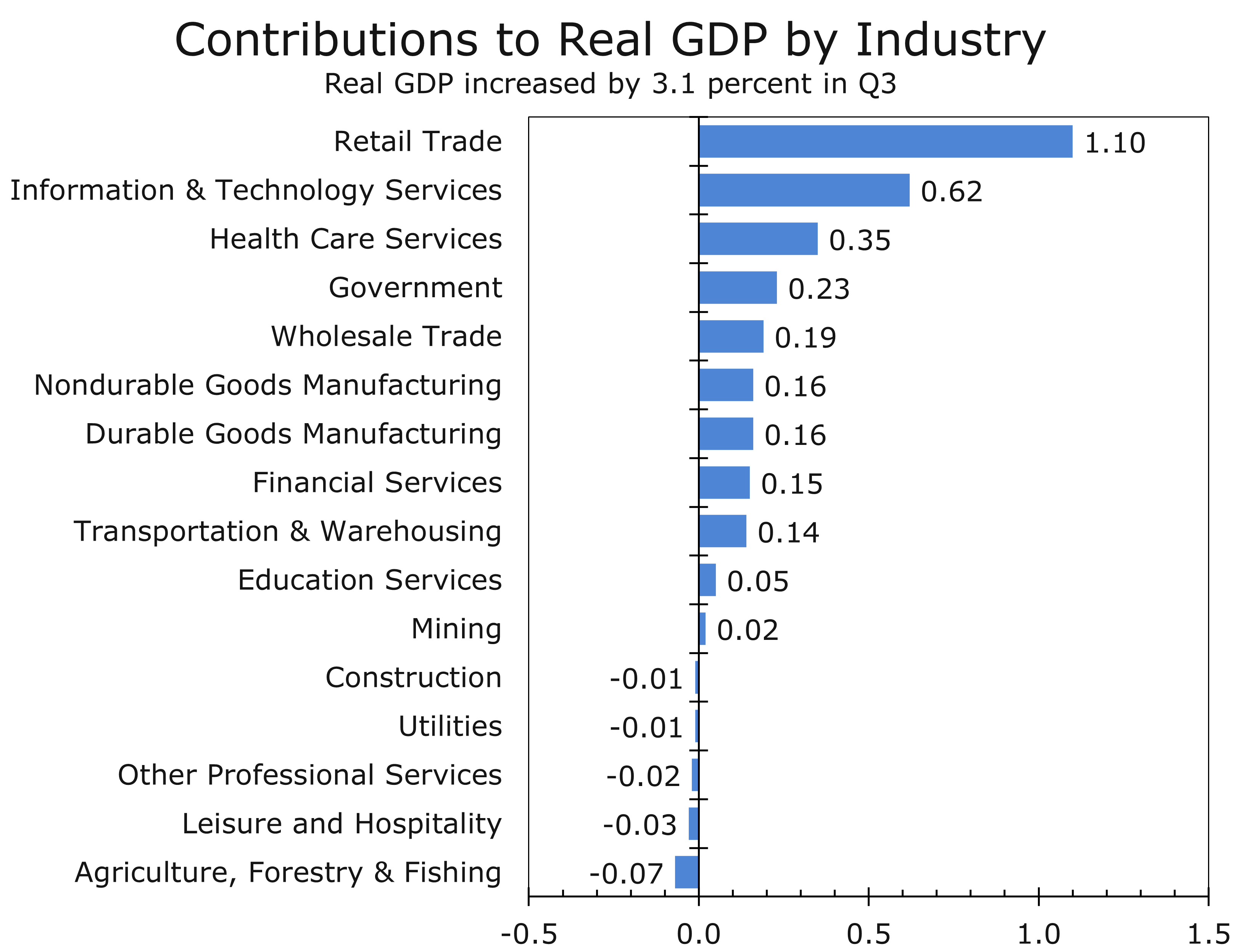

The benefits of economic growth are unevenly distributed across industries and sectors.

The strong GDP numbers present a paradox for the Fed. Real GDP has been growing at nearly a 3% pace for the past two years, and the unemployment rate remains near full employment. Why, then, would the Fed need to cut interest rates? The answer lies in the lagged effects of monetary policy. Changes to interest rates today influence the economy 12 to 18 months down the road, when growth is expected to slow, and unemployment is anticipated to rise modestly.

The economic data reveal another paradox: the benefits of economic growth are unevenly distributed. This disparity is evident in GDP by industry, where just 4 categories accounted for nearly three-quarters of Q3 growth. Similarly, the stock market reflects this concentration, with the “Magnificent 7” and their peers generating the bulk of this past year’s surge.

Monetary policy is a blunt instrument, and the Federal Reserve has limited ability to target rate cuts to specific sectors. Construction is a notable weak spot, with overall home sales near the lows of the financial crisis and rising inventories of unsold new homes. Commercial construction also remains under pressure. Lower interest rates would benefit both sectors.

Powell acknowledged that while inflation is declining, prices remain high—particularly for necessities such as food, transportation, and housing. He emphasized that the Fed works for those most affected by these costs, which is why it has adopted a more cautious approach to achieving its 2% inflation target.

Powell stressed that while inflation is slowing, prices for key necessities remain high.

The extended timeline for reaching 2% inflation still leaves room for rate cuts. We expect two quarter-point cuts in the first half of 2025, though the timing remains uncertain. While the Fed may prefer to pause, it may act to avoid provoking President Trump, who takes office just before the January FOMC meeting. Annual revisions to nonfarm payrolls, released a week later, are also expected to reveal weaker prior job growth.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 20, 2024

Mark Vitner, Chief Economist

704-458-4000

Job Growth: Neither Booming nor Busting

Payrolls Are Not as Fragile as Previously Feared

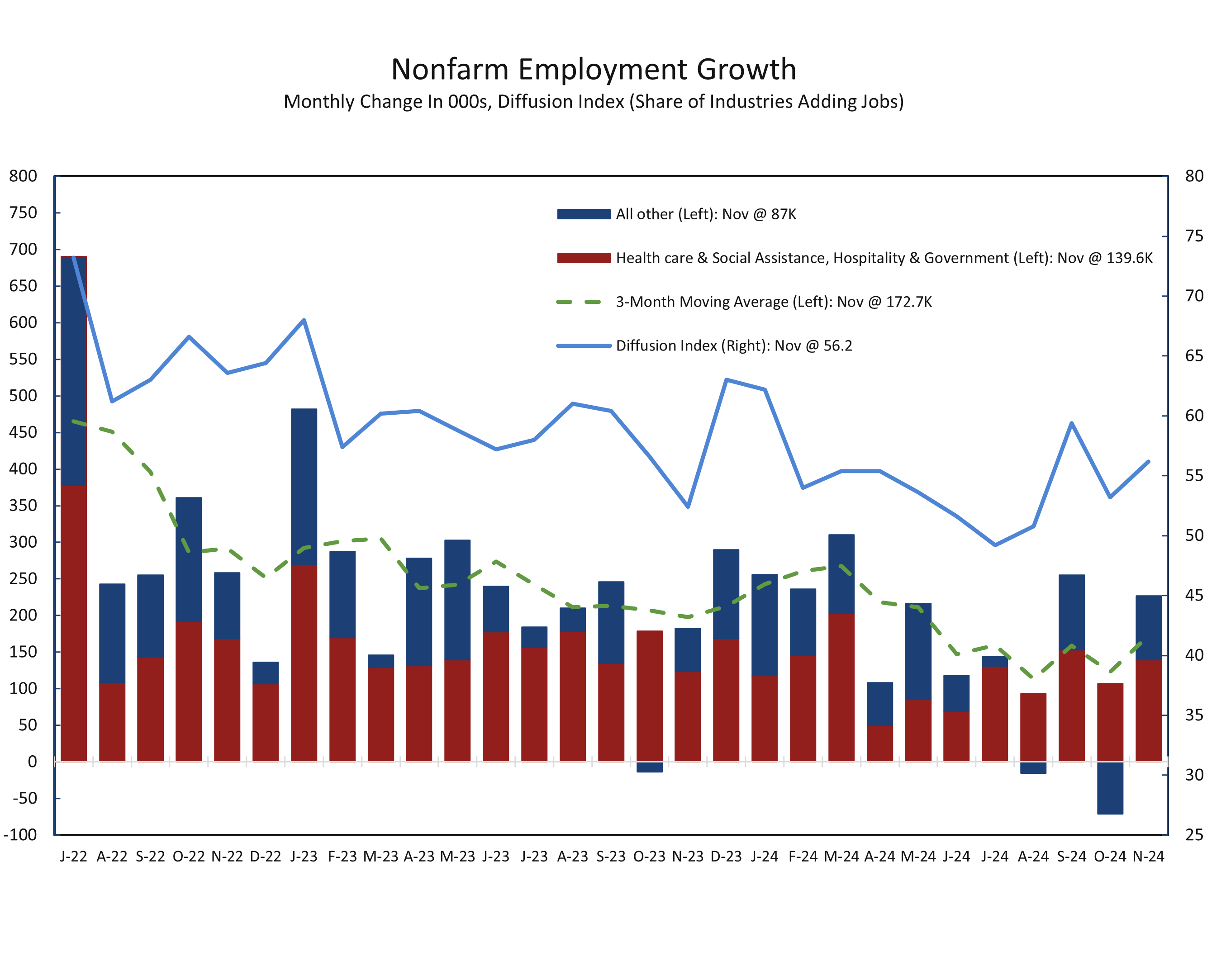

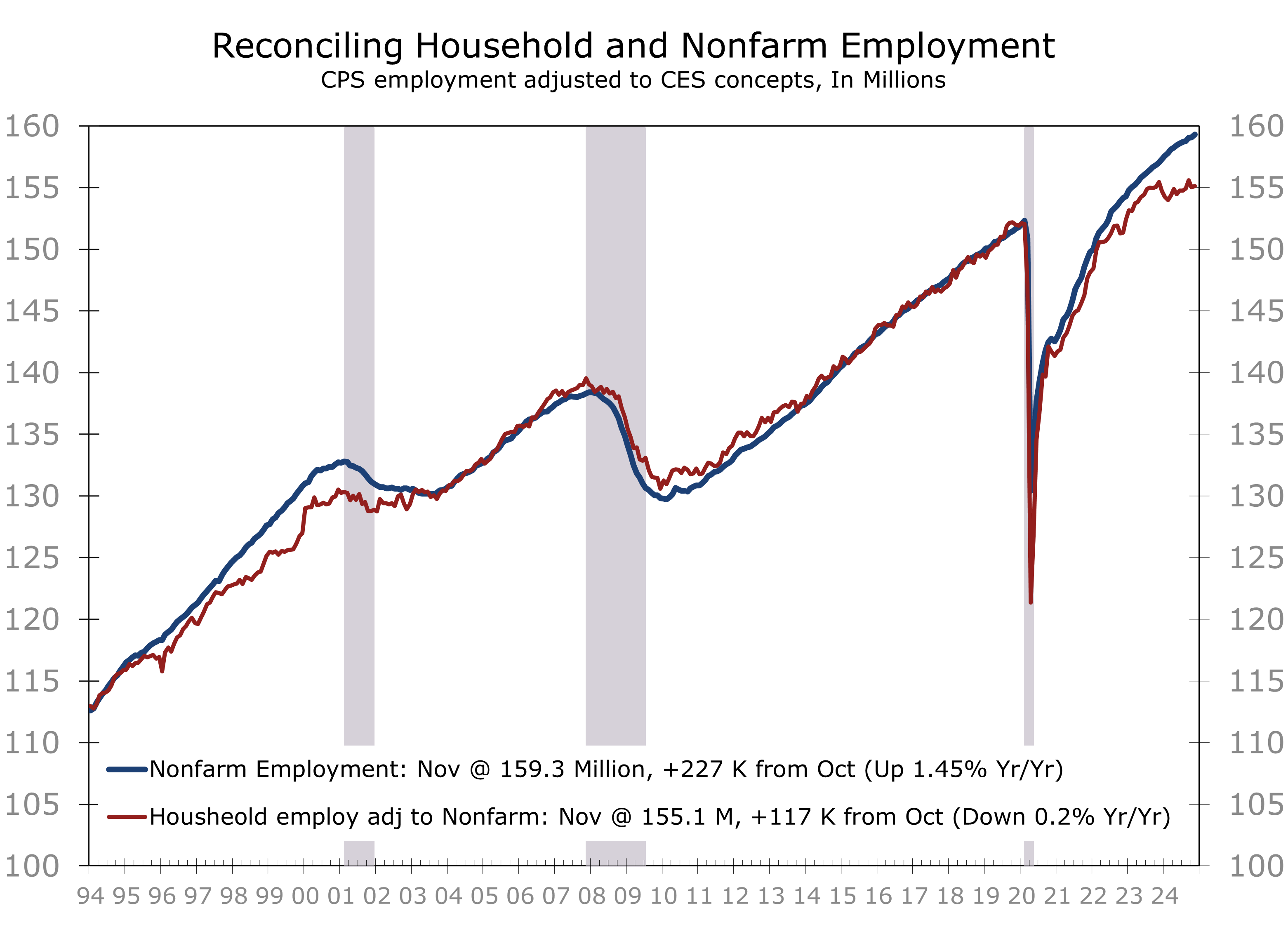

- Nonfarm payrolls increased by 227,000 in November, reflecting broad-based hiring across industries.

- While hiring improved broadly health care, social assistance, leisure and hospitality, and government sectors led job creation.

- Restaurants and bars, impacted by Hurricane Helene in October, showed signs of recovery. Hiring in hard hit areas, such as fall-tourism mecca Asheville, with take longer to get back on track.

- Retail hiring was subdued due to the later-than-usual Thanksgiving, with more holiday hiring expected to appear in December.

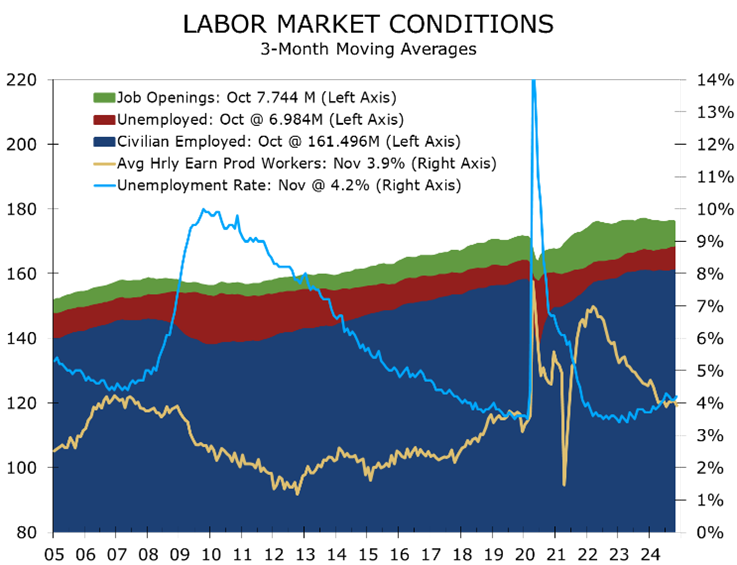

- The unemployment rate edged higher to 4.2%, up from 3.7% a year earlier. The jobless rate in Asheville surged to 7.3%, up from 2.9% one year earlier.

- The labor market remains surprising resilient. Employers added 237,000 jobs November, and job growth was revised higher for the prior two months. While health care and social services, leisure and hospitality, and government accounted for the bulk of net new hires, hiring rose more broadly. The unemployment rate did edge higher to 4.2%.

November’s employment looks strong on the surface but also reveals some underlying challenges. Nonfarm payrolls rose by 227,000 and more complete data shows that job growth in the prior two months was notably stronger. Specifically, October’s payroll growth were revised up by 24,000 to 36,000 jobs, and September’s was boosted by 32,000 to 255,000 jobs. These revisions show the economy is not nearly fragile as earlier feared. The three-month average job growth is now at 173,000, up from the previous 123,000 jobs per month reported last month.

The return of striking workers and recovery from October’s hurricanes bolstered hiring.

Service-producing industries led job creation in November, adding 160,000 jobs. Health care and education, leisure and hospitality, and professional and business services accounted for 158,000 of those new jobs. Government payrolls increased by 33,000, while private payrolls jumped by 194,000, reversing a slight decline of 2,000 in October. The diffusion index, which measures the share of private industries adding jobs, rose 3 points to 56.2, the highest since January.

Although job gains were more broadly distributed, the bulk of growth continues to come from health care and social services, leisure and hospitality, and government, which together accounted for 80% of the jobs added over the past three months.

Manufacturing employment rose 22,000 in November, boosted by the return of 38,000 striking workers. This recovery is likely to be reflected in the upcoming industrial production data. However, the rebound does not signify the end of challenges for the factory sector. Goods producers have faced a prolonged slump over the past year, driven by a shift in consumer spending from goods to services and experiences.

Construction payroll growth looks set to slow as the pipeline of projects begins to dwindle.

Construction firms added 10,000 jobs following a modest increase of 2,000 in October. The bulk of this growth came from nonresidential specialty contractors, which added 7,000 jobs. However, both commercial and residential building activity has slowed recently. Much of the recent job growth has been driven by specialty contractors completing projects initiated a year or more ago. With the pipeline of ongoing projects shrinking, payroll growth in this sector is likely to decelerate in the coming months.

Leisure and hospitality also saw a significant rebound, adding 53,000 jobs following a minimal 2,000-job increase in October. The sector was heavily impacted by hurricanes Helene and Milton, which temporarily disrupted employment at restaurants and bars. Hiring has not fully recovered, especially in Asheville, where the unemployment rate surged to 7.3% in October.

The unemployment rate increased slightly, rising from 4.145% to 4.246%. This uptick reflects a combination of factors, including a 193,000 decline in the labor force and a 355,000 drop in household employment.

The unemployment rate edged higher and household employment data remain weak.

A key concern is the rise in permanent job losses, which reached a three-year high in November. This trend has been accompanied by a lengthening duration of unemployment, with the median number of weeks increasing from 10 in October to 10.5 in November—the longest since December 2021. Although layoffs remain limited, those who lose their jobs appear to face greater challenges in finding new employment.

Wage growth remained modest in November, with average hourly earnings rising 0.4%. Year-over-year, wages increased by 4%, consistent with the Fed’s 2% inflation target when incorporating recent productivity gains. We anticipate the Fed will reduce the federal funds rate by a quarter point in December and signal that only a limited number of additional cuts—likely just two, spread across the first half of 2025—remain in the pipeline.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 6, 2024

Mark Vitner, Chief Economist

704-458-4000

Manufacturing Remains Soft

Modestly Better but Still Soft

- The ISM Manufacturing Index rose by 1.9 points to 48.4% but remained below the key 50 breakeven level, signaling contraction, for the 8th consecutive month.

- Manufacturing has been a persistent soft spot in what on appears to otherwise be a strong economy. The Manufacturing PMI® has been in contraction for 24 of the past 25 months.

- The overall PMI® has remained near its recent level for the past two years, consistent with a soft landing. The PMI® would need to fall below 42.5 to consistent with a recession.

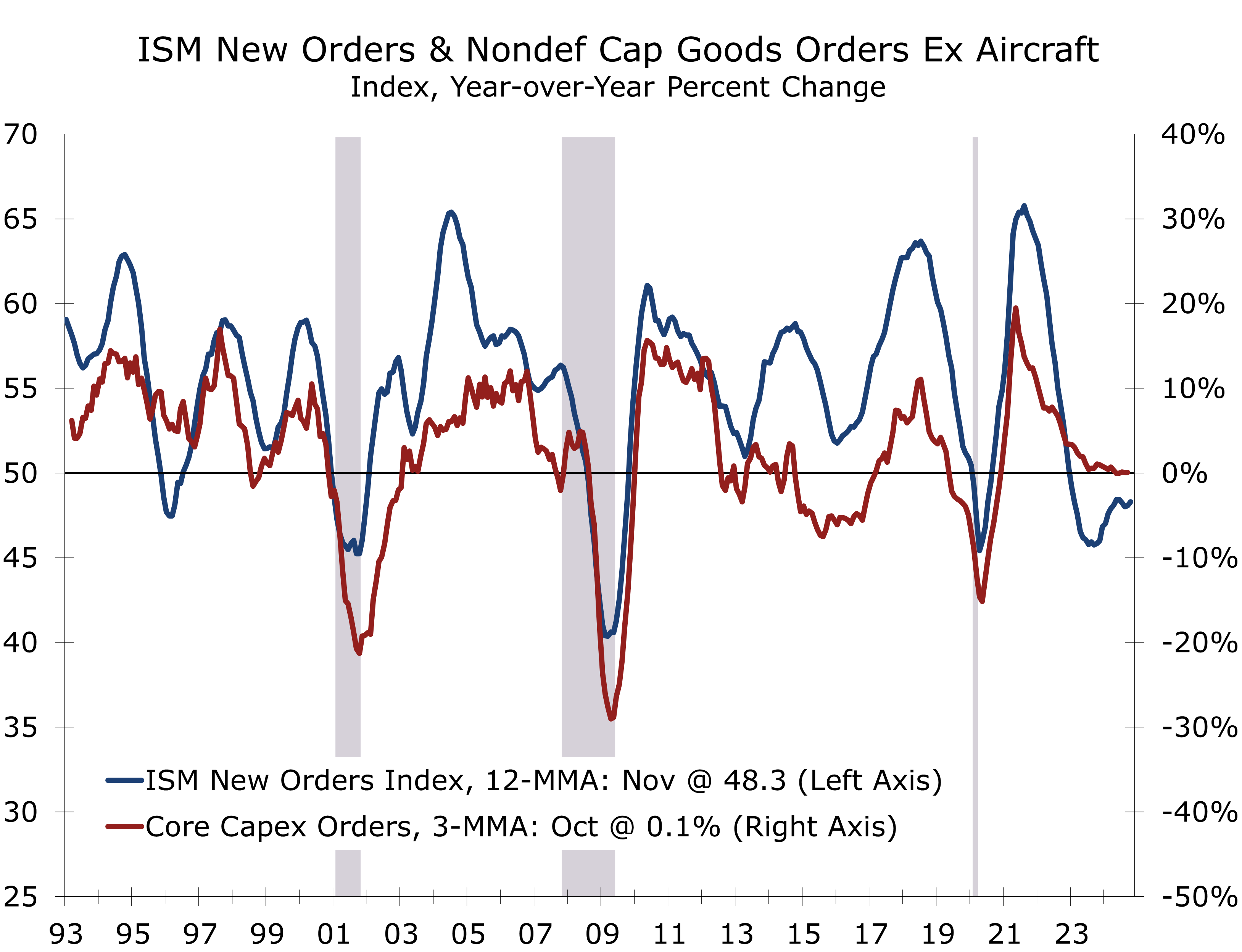

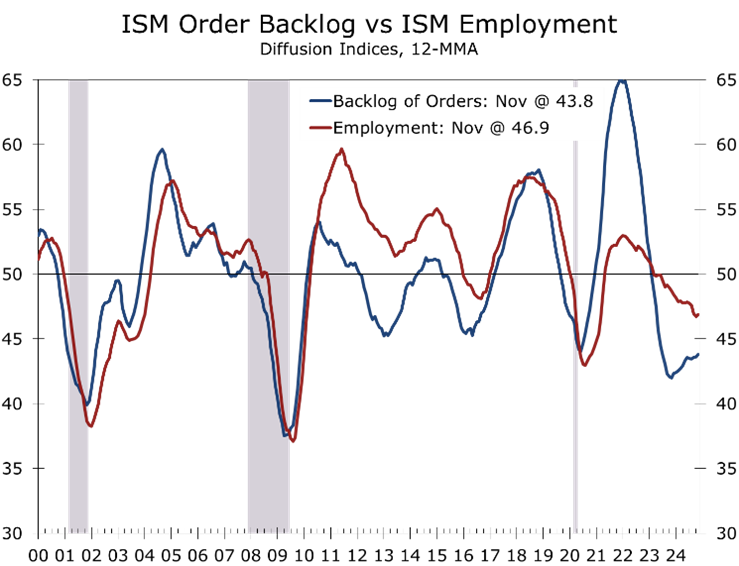

- The underlying details remain consistent with a soft landing, with new orders rising 3.3 points to 50.4, production climbing 0.6 to 46.8, and employment increasing 3.7 to 48.1.

- Supply chains also continue to normalize, with the suppliers’ delivery index declining 3.3 to 48.7, and the average lead time for production materials falling 2 days to 79 days.

- Persistent weakness in the factory sector has been a key reason for the Federal Reserve's eagerness to cut interest rates, despite an otherwise healthy economy. While manufacturing represents a smaller share of overall output, it continues to drive much of the cyclical swing in GDP growth, signaling slower growth in coming quarters.

The ISM Manufacturing PMI® rose 1.9 percentage points to 48.4 in November, which topped expectations but remains well into contraction territory. The increase brought the index to its highest level since June, signaling some near-term stability.

The underlying details in the report were modestly positive. The New Orders component rose by 3.3 points to 50.4, while the Production and Employment indices also edged higher, increasing by 0.6 points and 3.7 points, respectively. However, both indices remain in contraction, with Production at 46.8 and Employment at 48.1, respectively.

Despite averaging 3.0% GDP growth over the past two years, manufacturing remains soft.

The ISM index and its subcomponents provide insight into the breadth of the manufacturing sector’s strength or weakness. The Pandemic distorted the index to a certain degree in that widespread shortages drove the supplier delivery index sharply higher and exaggerated the extent of improvement when the economy reopened. Part of the recent weakness may be a payback for this earlier strength. The PMI® has averaged 47.6 over the past 2 years, a level that would be consistent with just 1.5 percent real GDP growth, half of what BEA has reported for this period.

While several key components showed improvement, overall activity is expected to remain soft. Uncertainty has likely risen in the aftermath of the presidential election, with ongoing questions about taxes, tariffs, and regulations. Additionally, diminishing order backlogs—a typical precursor to hiring slowdowns—signal potential challenges ahead.

Manufacturers of building materials appear headed for a slowdown, particularly those tied to commercial construction. The construction backlog has thinned considerably, with fewer new projects starting and the previously record-high backlog of projects beginning to decline. This trend has notably impacted producers of wood products and fabricated metals.

The slowing pace of construction will likely weigh on factory output in the coming months.

Demand for big-ticket consumer goods, including motor vehicles and furniture, remains soft and is unlikely to recover meaningfully until job and income growth reaccelerate.

There are a few bright spots. Orders for capital equipment in the IT sector remain robust, driven by the ongoing impact of the CHIPS Act. Additionally, orders for industrial machinery have shown improvement. However, just five of the 15 sectors reported net growth during November, indicating that factory output will remain in low gear the next few months.

Manufacturing employment figures have been impacted by strikes in recent months and may see some near-term improvement. However, today’s ISM report indicates that any gains are likely to be short-lived. Manufacturers continue to grapple with elevated operating costs and heightened uncertainty, compounded by a consumer shift toward spending on services and experiences.

The manufacturing sector still provides the cyclical impulse to the broader economy.

The Prices Paid Index fell 4.5 points to 50.3 but has remained above 50 for the past two months, indicating that more manufacturers are reporting higher input costs. Aluminum, copper, and natural gas saw slight price increases, while prices for steel, plastic resins, and crude oil declined.

The Fed closely monitors manufacturing data and has historically relied heavily on the ISM surveys. The latest figures provide some reassurance that the economy continues to lose momentum, despite a resurgent stock market and strong GDP figures. We remain skeptical that economic growth will reaccelerate without better results from the ISM report.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Moving to a New Economic Epoch

Looking Ahead to 2025

- We have had a couple of weeks to adjust to the impact of the 2024 presidential election. As we expected, Trump won with a resounding electoral college majority and the republicans won control of the Senate and narrowly retained control of the House. We expect swift action with policies regarding border security, regulatory relief, extending the Trump tax cuts, land use, trade negotiations, and tariffs. The financial markets have priced in more persistent large budget deficits and modestly higher inflation, which is partly reflected in our own forecast.

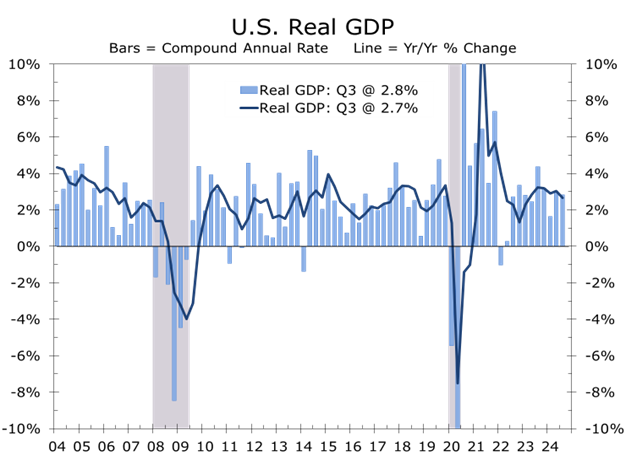

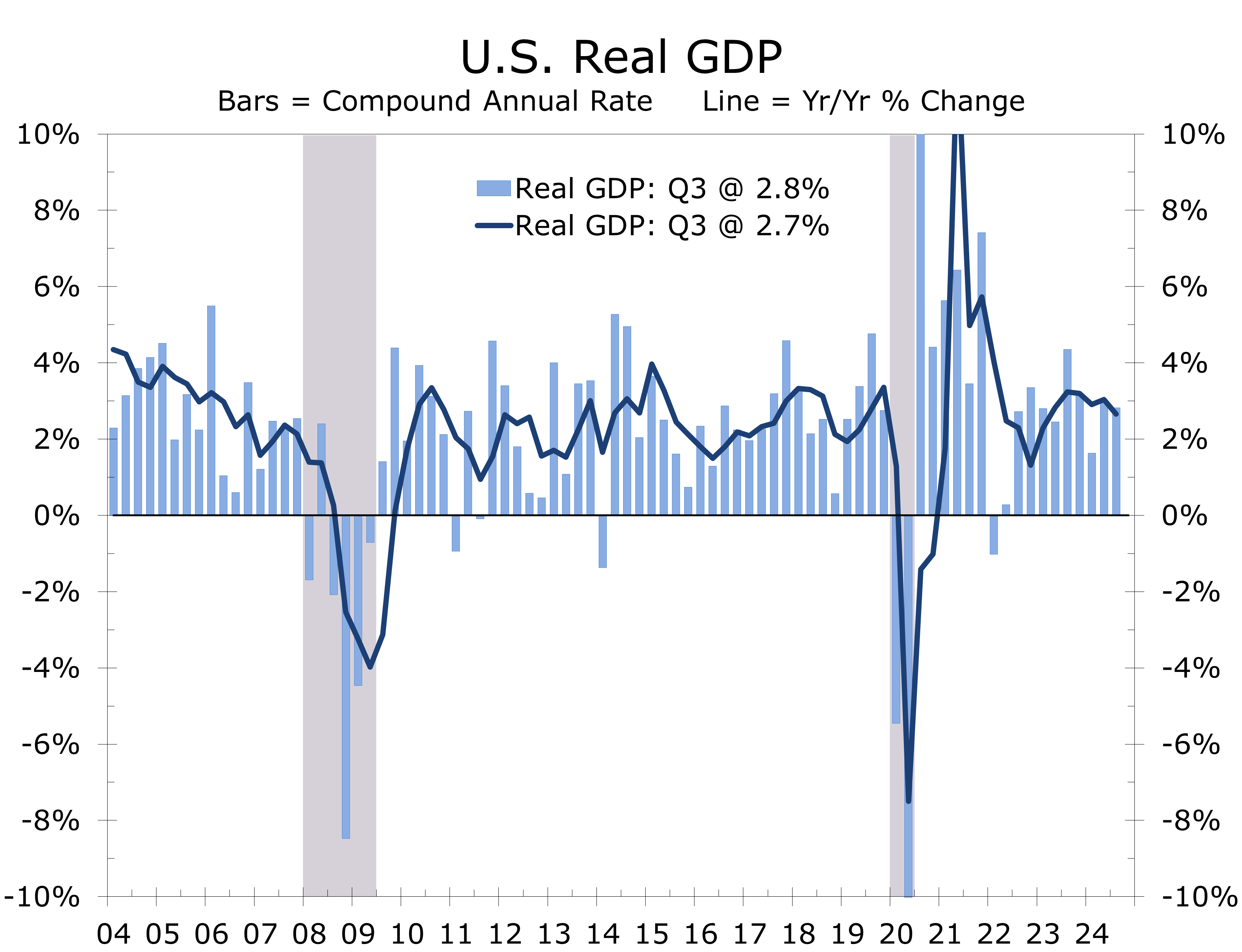

- The economy remains remarkably resilient, with revised real GDP growing at an annualized rate of 2.8% in the third quarter and 2.7% year-over-year. The economy has maintained a growth rate of approximately 3.0% in 7 of the past 8 quarters, marking a remarkable run. Despite this stronger headline growth, consumer sentiment has been uneasy throughout much of this period, casting doubt on the veracity of the GDP data.

- This divergence between robust GDP growth and uneasy consumers highlights the waning but notable impact of fiscal stimulus on capital spending, offset by frustration over high prices for essentials. Both business investment and consumer spending are expected to moderate in the coming quarters, as uncertainty surrounding the new administration delays capital spending. Fourth-quarter growth is projected at 2.3%, with solid consumer spending through the holidays.

- Inflation has eased this past year, providing some relief to household budgets. Further progress may prove challenging, however, as wages and core service prices are easing much more slowly. While concerns about tariffs, trade wars, and stricter immigration policies are fueling inflation fears, we believe these concerns are overstated and expect only a modest impact on inflation.

- The outcome of the U.S. presidential election will refocus attention on global hotspots, particularly Ukraine and the Middle East. The Trump Administration is likely to pursue a Ukraine peace deal with stronger guarantees than currently anticipated, while Iran may seek an exit from the conflict it initiated. The key question in both scenarios is whether any agreement is worthwhile if it merely postpones the conflict, giving Russia and Iran time to regain leverage.

The 2024 Presidential Election outcome will drive significant policy shifts in the coming year. The incoming Trump Administration aims to quickly appoint cabinet members focused on streamlining government, reducing regulation, expanding federal land use for energy and other resources, cutting taxes, reforming trade and immigration, and implementing tariffs. On foreign policy, Trump has pledged to quickly end Russia’s war in Ukraine and Iran’s conflict with Israel, as well as redouble efforts to expand the Abraham Accords. While new administrations often enter with ambitious plans, the first 100 days are critical and typically set the tone. Narrow congressional majorities mean the speed of cabinet confirmations will heavily influence the Administration’s success.

Trump’s initial cabinet choices, including Matt Gaetz for Attorney General, Robert F. Kennedy Jr. for Health and Human Services Secretary, and Pete Hegseth for Defense Secretary, have sparked controversy among mainstream political insiders. However, these selections are highly popular with Trump’s base and appear intended to maintain their support during the administration’s early months. While it remains uncertain whether the Senate will confirm all these controversial picks, Trump’s cabinet is expected to align closely with his populist agenda. Notably, he has yet to announce a Treasury Secretary, though the shortlist includes several credible candidates, and he has been relatively quiet about the Federal Reserve.

On foreign affairs, we do not expect Trump to end Russia’s war with Ukraine immediately upon taking office. Both Russia and Ukraine are likely to escalate their efforts before January 20 to strengthen their bargaining positions. For Russia, this likely involves attempting to push Ukrainian forces out of occupied areas near Kursk, bolstered by additional manpower from North Korean troops, and intensifying missile strikes on Kyiv. For Ukraine, the strategy will focus on holding these territories and inflicting significant casualties on Russian forces and military infrastructure. These actions would bolster Ukraine’s negotiating position should Putin accept Trump’s mediation offer. The Ukraine War has vastly exceeded Russia’s expectations in terms of lives lost, costs incurred, and its overall duration.

In the Middle East, Israel is expected to continue operations against Hamas, Hezbollah, and Iran. While there are signs that Iran may ask Hezbollah to pull back along the lines proposed by Israel, Hamas and the Houthis remain far apart with Israel on terms of a possible cease fire. The Biden administration may push for a settlement before Trump takes office, but Israel is likely to remain cautious, preferring guarantees Trump could more credibly provide for enforcing and maintaining a ceasefire.

Domestically, Trump is likely to prioritize swift implementation of his agenda during his first two years, as GOP control of the House may be difficult to maintain in the mid-term elections, and the next presidential race looms shortly thereafter. Reducing regulation, which was more impactful than tax reform during Trump’s first term, is an area where quick action is likely. We also expect the Trump tax cuts to be extended and anticipate Trump using tariff threats to secure stronger trade deals. While tariffs are unlikely to significantly impact inflation, an escalating trade war may lead to renewed supply shortages..

The incoming Trump Administration inherits an economy that, on the surface, appears firm but is significantly softer in the middle. The forces propelling economic growth have been narrowing, with health care and government accounting for a disproportionate share of job growth. Overall GDP growth has been bolstered by unprecedent fiscal stimulus, which has bolstered business fixed investment in EV-related and Chip-related ventures and boosted state and local government outlays. Growth in other areas of the economy has cooled and the pipeline of incentive-driven projects is winding down.

How much of the current slowdown is reflected in the data remains uncertain. Key indicators, such as employment figures, have been distorted by several significant exogenous events, including Hurricanes Helene and Milton, strikes at Boeing and East Coast ports, and the usual pullback in capital spending and hiring that precedes presidential elections. The Bureau of Labor Statistics (BLS) has already disclosed that nonfarm payrolls will see a substantial downward revision when the annual updates are released with the January payroll data. Preliminary figures indicate employers added 818,000 fewer jobs from March 2023 to March 2024 than initially reported, even before the recent hiring slowdown became apparent.

After adding just 12,000 jobs in October, we anticipate a partial rebound in November as workers return from temporary strikes and disruptions caused by back-to-back October hurricanes. However, recovery from Hurricane Helene is expected to be unusually slow due to extensive flood damage, which typically requires more time to repair, and delays in relief efforts reaching rural areas. These recovery efforts are likely to boost construction payrolls as cleanup crews are mobilized. Conversely, the leisure and hospitality sectors, along with retail trade, may experience a more gradual recovery. Additionally, this year’s late Thanksgiving could shift holiday-related hiring into December, potentially resulting in another weak month for November data.

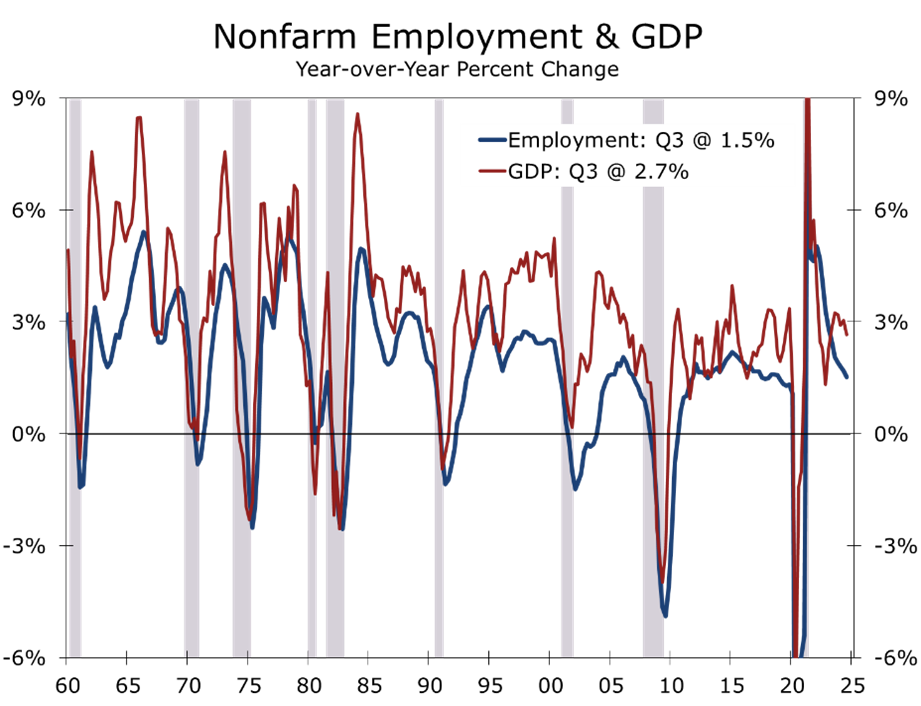

This past year’s slowdown in job growth is not fully reflected in the GDP data. Real GDP grew by 2.7% over the past year, compared to 3.2% in the previous year, while job growth slowed to 1.5% from 2.1% a year earlier. The implication is that productivity growth and the economy’s potential growth rate are somewhat stronger than previously estimated. As a result, inflation should continue to decelerate, albeit at a much slower pace than seen over the past two years.

.

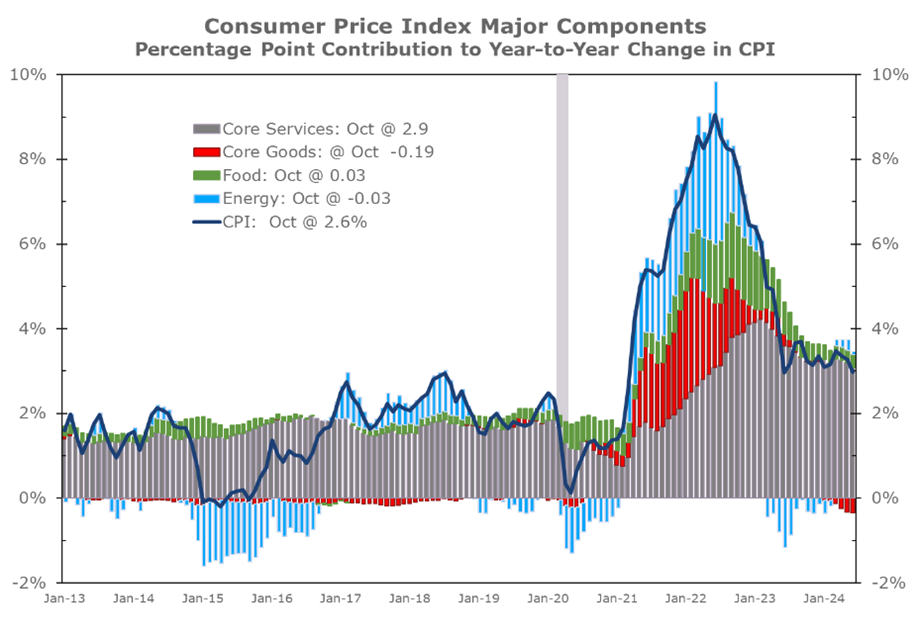

The path back to the Fed’s 2% inflation target appears increasingly challenging, as recent reports highlight persistent price increases in key areas of the economy, particularly in the service sector, where labor costs heavily influence pricing. The easiest phase of disinflation now appears to be behind us, with energy prices declining and food prices largely stabilizing. Core goods prices have also fallen, driven by slower global economic growth—particularly in China—which has led to a surge in exports to the U.S., exerting downward pressure on final core goods prices.

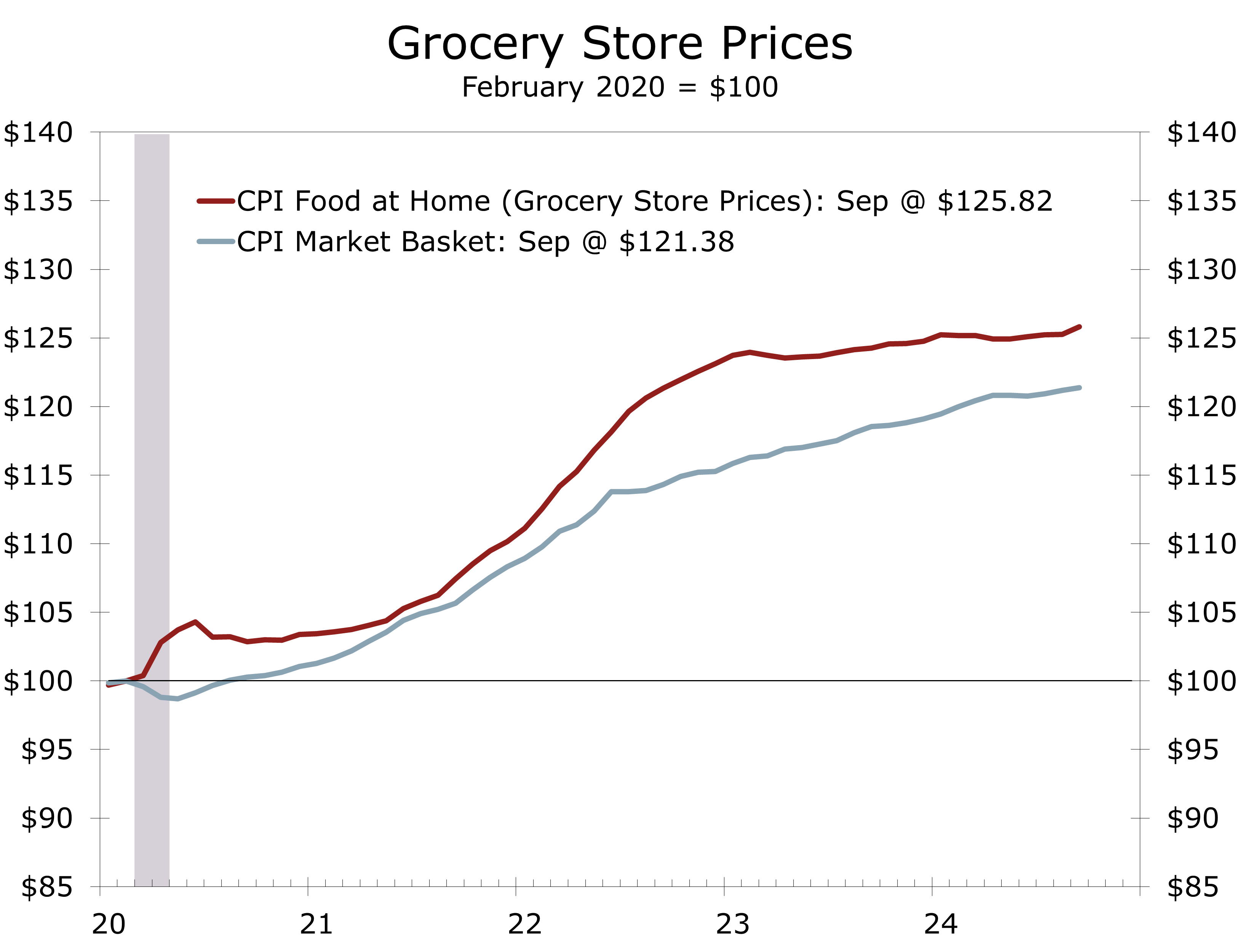

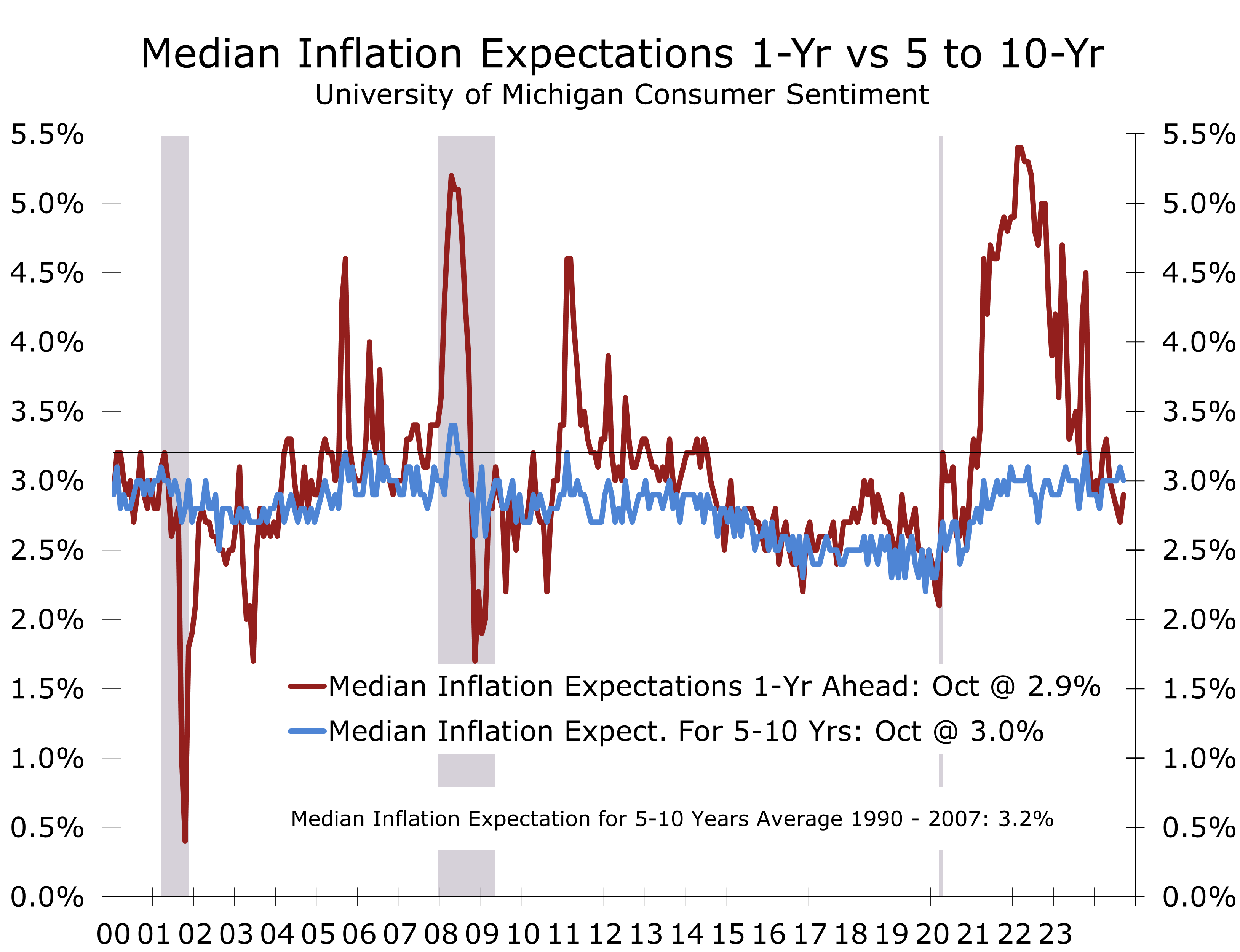

The relief from inflation has been insufficient for many consumers, as voters cited higher grocery bills and housing costs as key factors for choosing Trump over Kamala Harris. Overall, prices are roughly 20% higher than when the Biden-Harris administration took office, with grocery store prices and residential rents both up by 26%. Inflation expectations have risen since the election, driven in part by recent firmer inflation data and concerns over potential tariffs and large-scale deportations

We believe concerns about tariffs are overstated. While Trump has announced plans for significant tariff increases—proposing a 10% across-the-board tariff and a 60% tariff on Chinese imports—we view these proposals as largely a negotiating tactic. We anticipate tariffs, currently averaging around 3%, to rise modestly to approximately 6%, with Chinese goods facing somewhat steeper increases. One key objective is to curtail transshipments of steel, light vehicles, and other goods through free-trade partners. This practice circumvents tariffs by routing shipments of high-value-added products from China though Mexico or Canada or other nations under U.S. free trade agreements, where some light assembly or processing is completed.

The link between tariffs and consumer prices is less direct than commonly assumed. Tariffs are applied to the customs value of imports, but the landed cost—what wholesalers and distributors pay—includes tariffs, transportation, and insurance costs. Landed costs account for only a fraction of final retail prices: roughly one-third for furniture and clothing, and as little as 10% for high-end luxury goods such as jewelry and perfume. To mitigate tariff impacts, importers can ship less-assembled goods and complete assembly in the U.S., a long-standing practice for products like light trucks and furniture.

We estimate tariffs will ultimately add about 0.3 percentage points to the Consumer Price Index (CPI), modestly extending the path back to the Fed’s 2% inflation target. The primary risk lies in the potential for a broader trade war, which could lead to shortages of key inputs in the U.S. and dampen global economic growth.

.

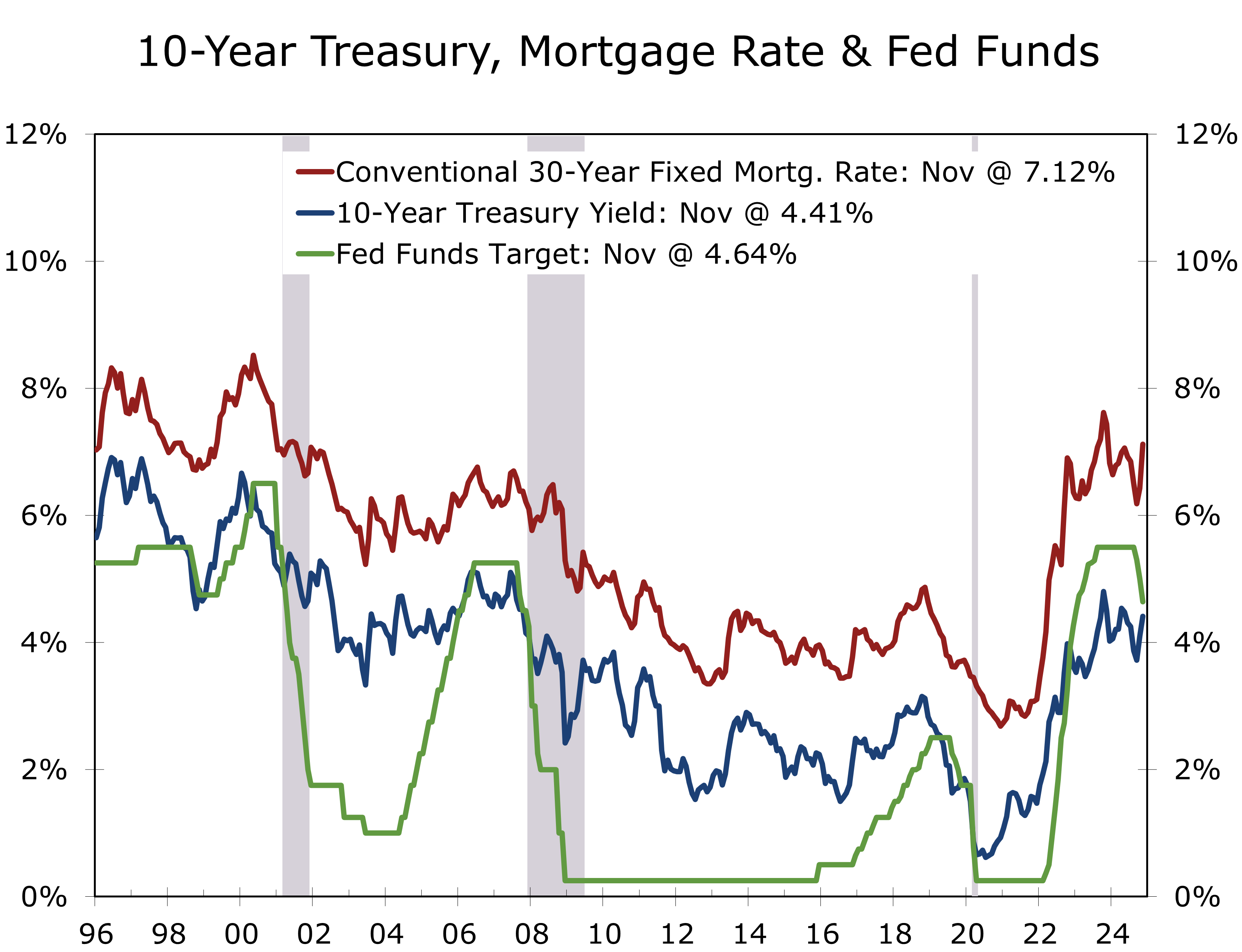

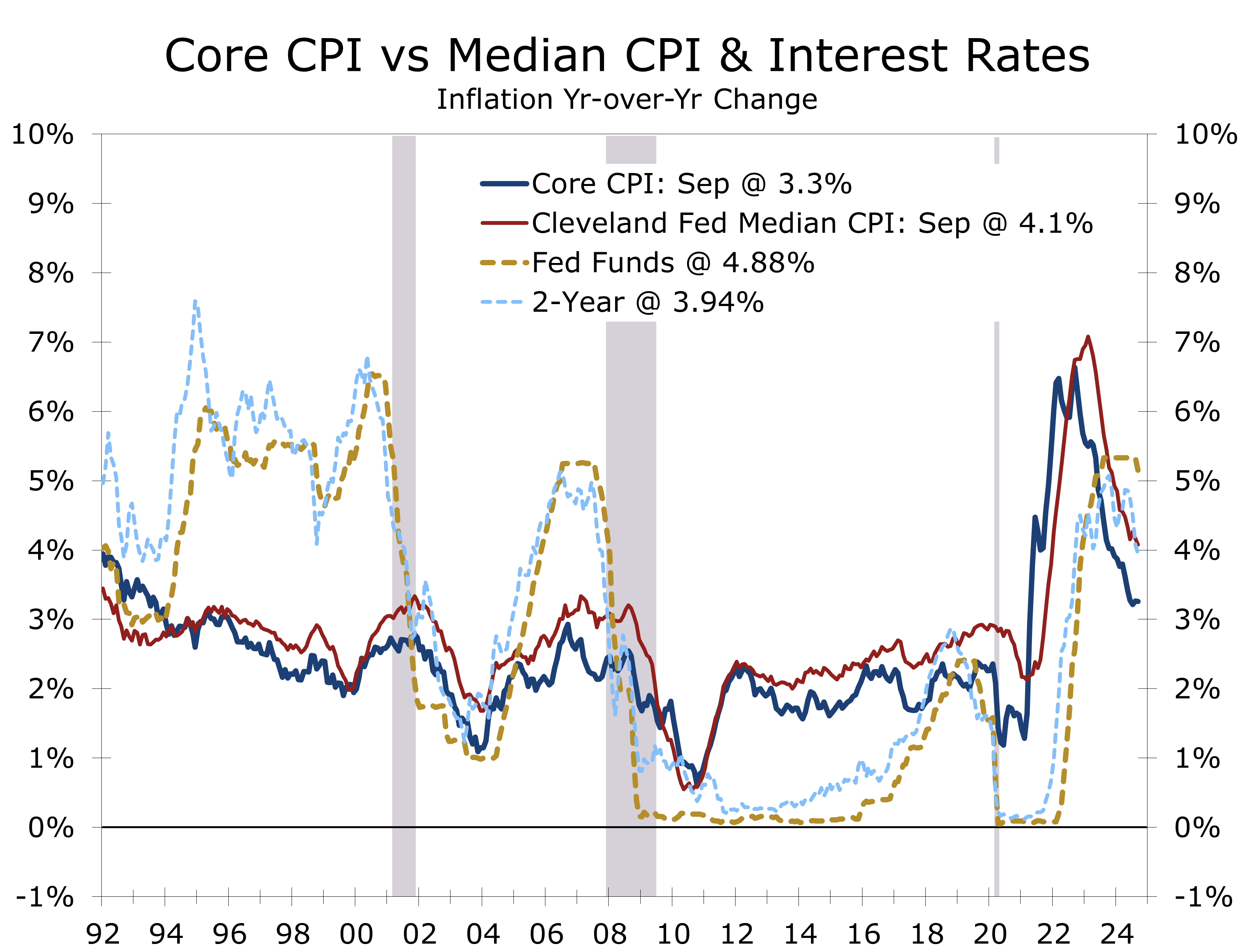

Bond yields have risen sharply in the weeks leading up to and following the presidential election, driven by a few disappointing inflation reports, a less optimistic inflation outlook in general, expectations for fewer Federal Reserve rate cuts, and growing concerns about persistent large federal budget deficits. We now anticipate the Fed will cut the federal funds rate by a quarter percentage point just three more times, with reductions at successive FOMC meetings in December and January, followed by a pause in March and another cut in May. The yield on the 10-Year Treasury Note has climbed from 3.80% in late September to around 4.40%, while the 2-Year Note has risen to 4.29%, aligning with this outlook.

Inflation concerns and worries about larger budget deficits are not the only drivers of rising interest rates. Annual benchmark revisions revealed stronger-than-expected economic growth, particularly in Gross National Income, which saw significant upward adjustments in real after-tax income and corporate profits. Stronger income growth means the economy is more resilient to outside shocks and rising interest rates. Strong growth also reflects stronger productivity growth which supports the argument that potential GDP growth and the neutral federal funds rate are higher than the Fed’s long-term estimates in its Summary of Economic Projections. Productivity growth has averaged 1.9% over the past five years, compared to 1.3% in the five preceding years. Coupled with 0.6% labor force growth, potential real GDP growth now stands at approximately 2.5%.

We estimate the neutral federal funds rate to be between 3.50% and 4%. Consequently, we expect the Fed to pause once the federal funds rate reaches the 3.75%-4% range. Lower short-term rates should steepen the yield curve, boosting banks’ interest rate margins and encouraging more lending. While mortgage rates are tied to the 10-Year Treasury yield, the spread between the two has been unusually wide due to elevated funding costs for lenders. As funding costs decline, we anticipate lenders will adopt more aggressive pricing, gradually narrowing the spread between 30-Year mortgage rates and the 10-Year Treasury yield toward its long-run average of 170 basis points. As a result, mortgage rates could fall from current levels even if the 10-Year Treasury yield rises further. Similarly, lower funding costs should enable banks to price auto loans more competitively, which we feel will become apparent this spring.

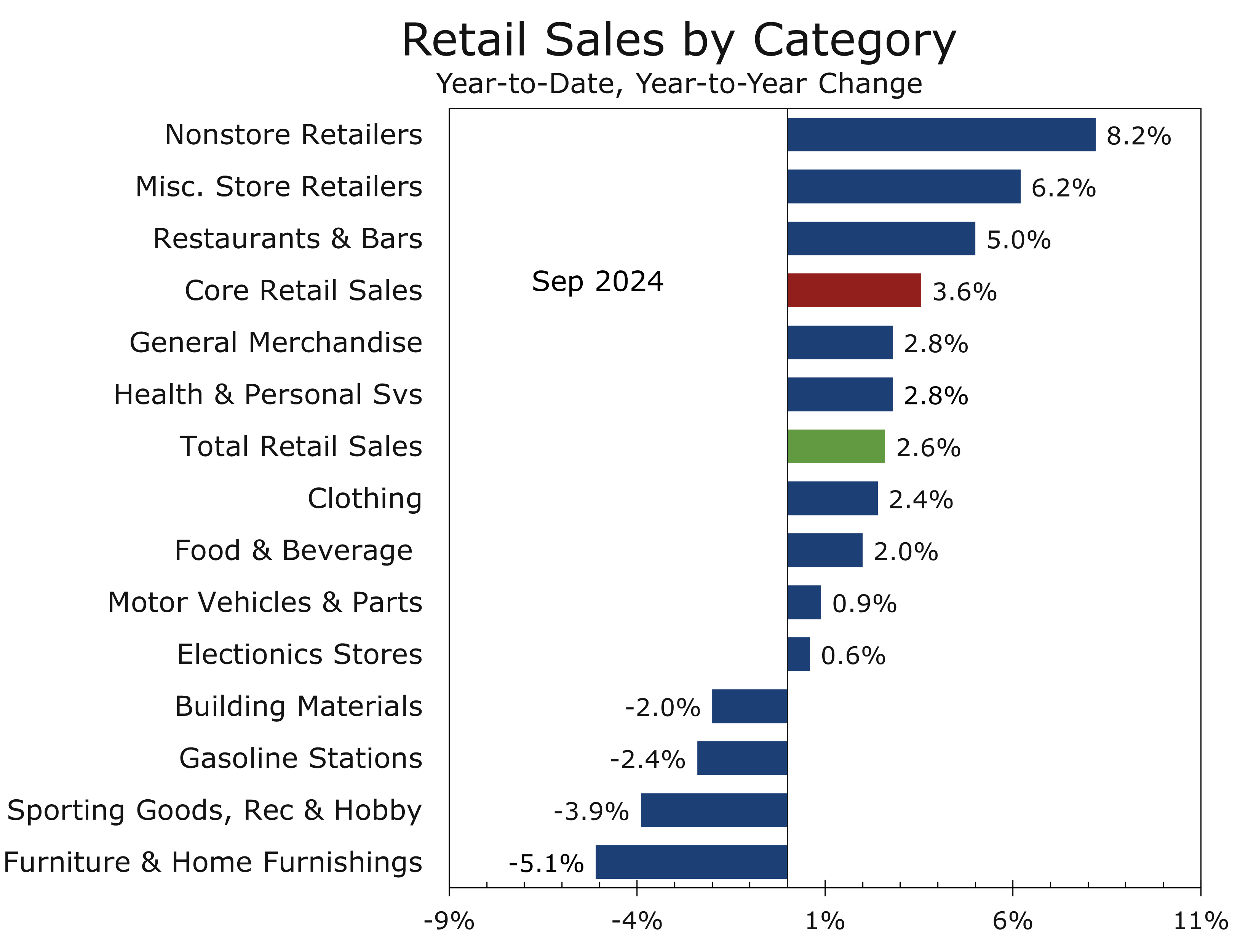

We have raised our Q4 real GDP growth estimate to 2.3%, reflecting stronger core retail sales and continued support from business fixed investment. Holiday retail sales should see solid gains, though the unusually late Thanksgiving may shift more activity into December. We have also increased our growth estimate for the first half of 2025, as businesses are likely to accelerate exports and imports ahead of a potential tariff hike. While inventory building should boost growth early in the year, homebuilding and consumer durable goods purchases are expected to drive growth in the second half.

The policy mix is expected to become more favorable, with an extension of the Trump tax cuts and modest expansions to current law, including partial relief on the cap for state and local tax deductions and tax breaks on tip income. Regulatory relief and land-use reform are poised to provide an immediate supply-side boost, enabling faster growth without increasing inflation. Risks remain from tariffs and potential deportations, though administrative solutions allowing working immigrants to remain could mitigate disruption.

Internationally, the Trump Administration has an opportunity to reset relations strained by Russia’s invasion of Ukraine and Hamas’s attack on Israel. Geopolitical maneuvering is likely as all parties jockey for position ahead of U.S. leadership changes. A preliminary peace outline for Russia and Ukraine has been circulating by will likely require stronger guarantees for Ukraine, such as limited EU and NATO observer status. In the Middle East, while lasting peace remains elusive, a ceasefire returning hostages and advancing the Abraham Accords offers the best path to stability and hope for the region.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice. Any forward-looking statements or forecasts are not guaranteed and are subject to change at any time. Information from external sources have not been verified but are generally considered reliable.

© 2024 CAVU Securities, LLC

November 21, 2024

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

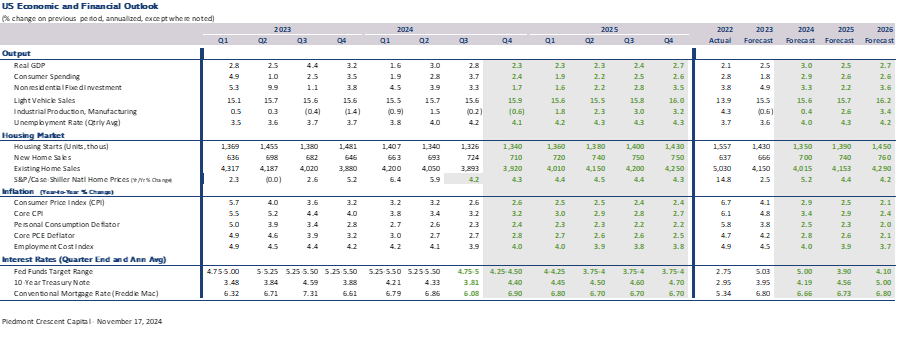

Housing Starts Come Up Short in October

Hurricanes Held Back Starts in the South

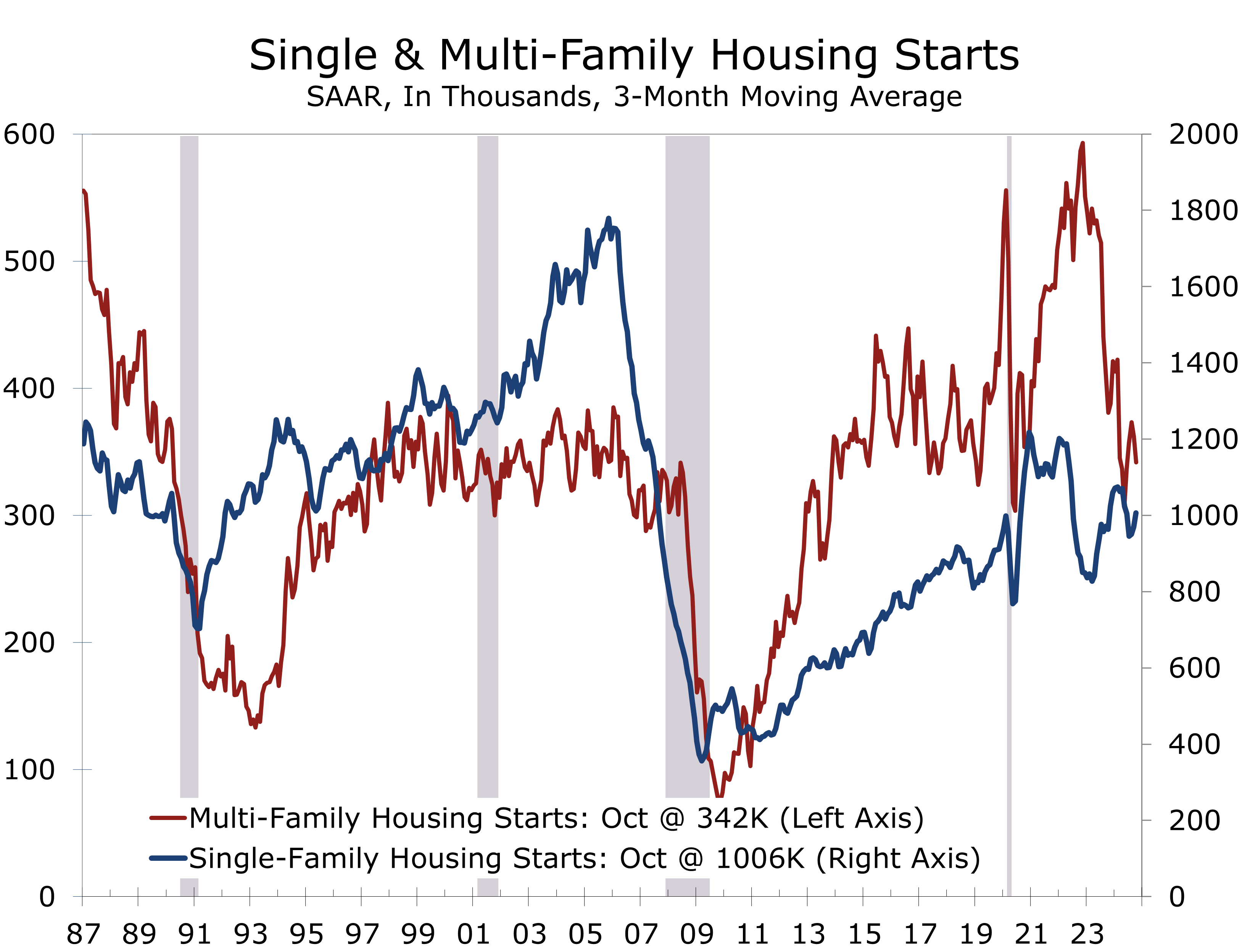

- Housing starts came in slightly short of expectations in October, falling 3.1% to a 1.311-million-unit annual rate.

- Single-family starts fell 6.9% in October, while multi-family starts rose 9.7%.

- Despite falling back below a 1 million unit pace, single-family construction remains resilient at a 970,000-unit annual rate.

- Year-to-date, single-family starts are up 9.3%, fueled by strong pent-up demand and limited resale inventory, while multi-family starts are down 29.3%, pressured by higher vacancies, falling rents, and tighter credit.

- The West (+21.1%) and Midwest (+9.4%) saw strong gains, while the South (-8.8%) and Northeast (-32.9%) faced disruptions from hurricanes and affordability hurdles.

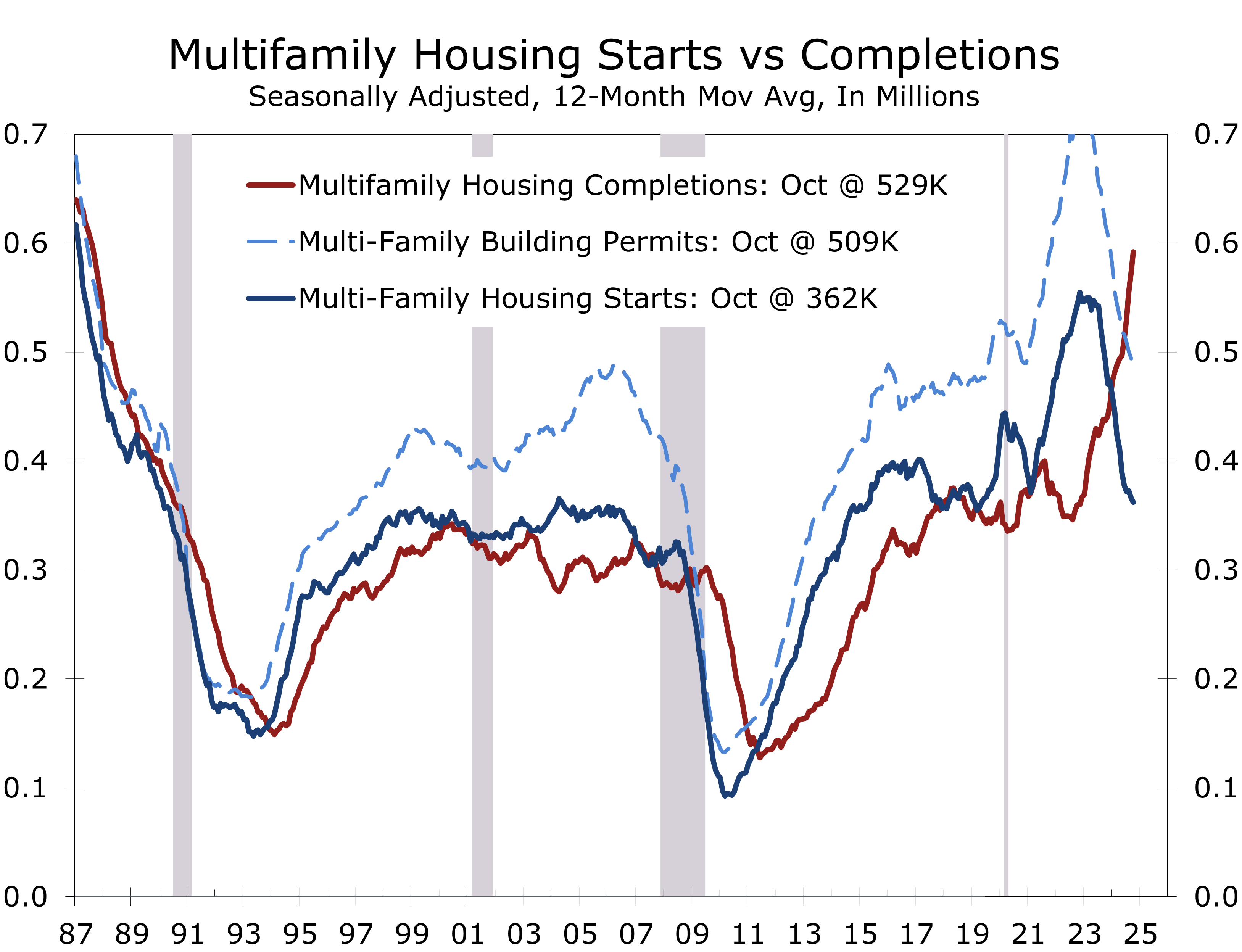

- Overall housing completions rose 16.8% year-over-year, driven by a wave of multi-family completions, addressing the supply overhang from the 2022-2023 boom.

- Housing starts fell short of expectations, as back-to-back hurricanes hindered activity in the South. In contrast, milder-than-usual fall weather in the West and Midwest bolstered starts. Builder confidence has improved, driven by lower short-term rates and continued hopes for lower mortgage rates.

Housing starts declined 3.1% in October to a 1.31-million-unit seasonally adjusted annual rate (SAAR), a slightly slower than expected pace. Starts are down 4.0% year-to-year, with a notable split between the relatively resilient single-family starts and the ongoing challenges in the multi-family segment. The shortfall in starts also reflects the impacts from back-to-back hurricanes, which cut starts in the South, which is by far the largest region for new home building.

Single-family housing starts fell 6.9% in October to a 970,000-unit pace. Despite this decline, single-family activity remains robust on a year-to-date (YTD) basis, rising 9.3% compared to the prior year. Strong pent-up demand for new homes, coupled with historically low levels of resale inventory, continues to provide a potent tailwind for single-family construction, even amid affordability concerns and higher mortgage rates.

October’s rise in multi-family starts suggests the apartment market is finding its footing.

Multi-family starts rose 9.7% to a 326,000-unit pace but remained down a sharp 29.3% YTD. While tighter credit, rising vacancies, and slower rent growth weigh on development, stronger-than-expected apartment demand has allowed more projects to move forward. The October increase suggests near-term stabilization, though the sector remains in correction.

Building permits, which are less impacted by weather distortions, edged 0.6% lower to a 1.416-million-unit SAAR in October. This modest decline reflects a 3.0% drop in multi-family permits, counterbalanced by a 0.5% rise in single-family permits, reflecting some tentative stability in single-family construction activity.

The apartment boom continues to wind down, with the backlog of projects gradually declining.

Housing completions paint a more dynamic picture. Overall completions fell 4.4% in October, possibly reflecting some impact from Hurricanes Helene and Milton. Completions have surged 16.8% over the past year, however, driven by a wave of apartment completions. That onslaught of supply has pushed vacancy rates higher and weakened asking rents. Fortunately, the sector’s backlog is finally clearing, which is allowing a handful of projects in faster growing market to move forward.

Regionally, housing starts rose in the West (+21.1%) and Midwest (+9.4%) due to strong single-family demand and a rebound in multi-family activity. The Northeast (-32.9%) and South (-8.8%) saw declines. The South, which generates 55% of U.S. housing starts, was hit by hurricanes and waning affordability migration as rising home prices diminished the appeal of relocating from higher-cost parts of the country.

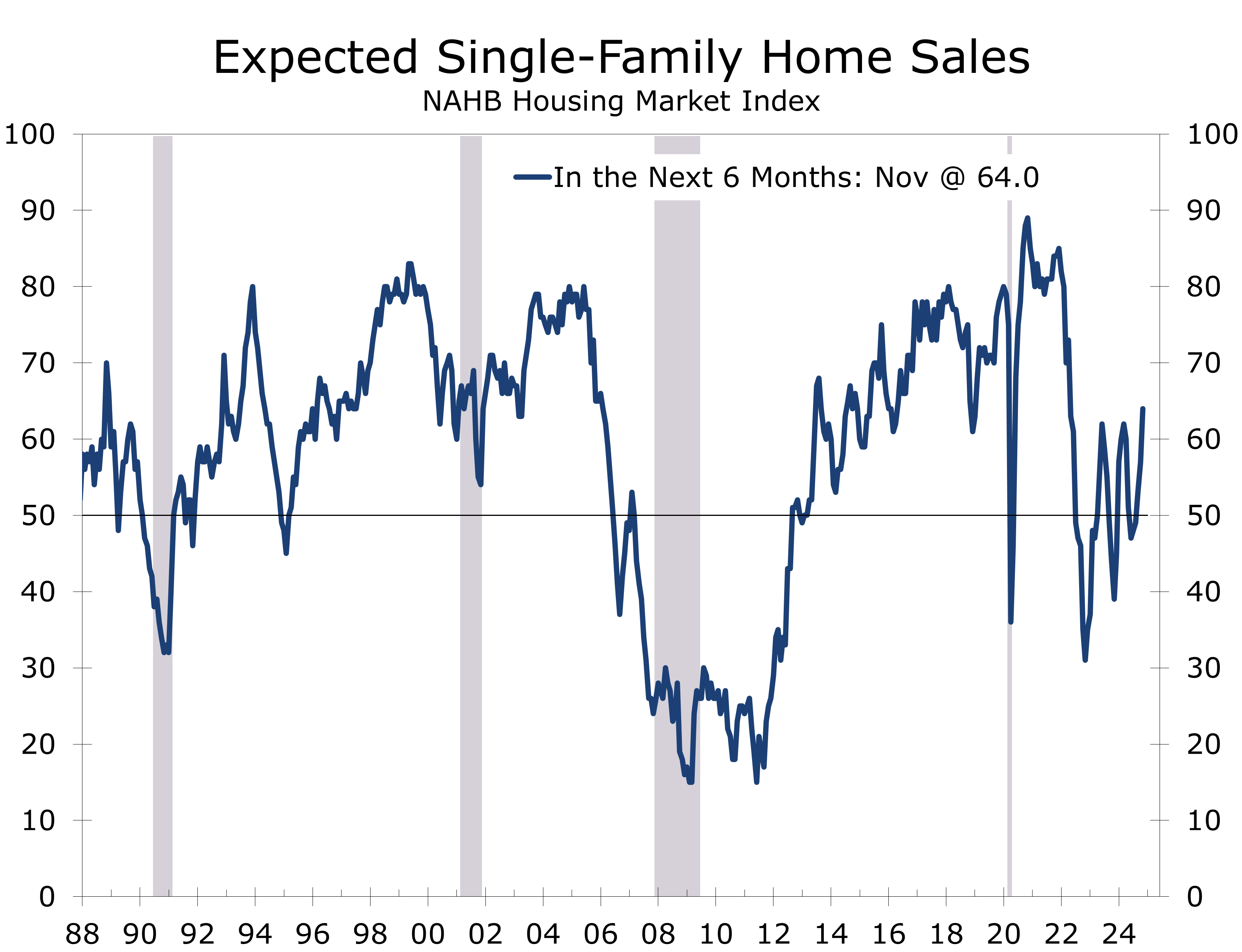

Builder sentiment improved for the third consecutive month in November, with the NAHB/Wells Fargo Housing Market Index (HMI) rising 3 points to 46. Optimism was likely driven by the Republican sweep of the presidency, House, and Senate, which is expected to ease regulations and open more land for development. Expectations for sales over the next six months surged, likely at least partly because of this.

Despite rising confidence, builders face persistent challenges, including labor shortages, a shortage of buildable lots, and high building material costs. Moreover, mortgage rates surpassing 7% have further strained affordability. In November, 31% of builders reduced home prices, with average price cuts easing slightly to 5%, while the share of builders offering sales incentives dipped from 62% to 60%.

All three HMI sub-indices improved in November: current sales conditions rose 2 points to 49, sales expectations jumped 7 points to 64, and buyer traffic increased 3 points to 32. Regionally, the Northeast gained 4 points to 55, the Midwest rose 3 points to 44, the South edged up to 42, and the West held steady at 41. Single-family construction is expected to strengthen this spring as mortgage rates dip below 7%.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 19, 2024

Mark Vitner, Chief Economist

Piedmont Crescent Capital

(704) 458-4000

Inflation Fatigue Fails to Dampen Q3 GDP Growth

Another Solid Quarter for Economic Growth

- Real GDP grew at a 2.8% annual rate in Q3, a slight deceleration from the 3.0% pace in the prior quarter. The underlying details were strong, while inflation came in slightly lower than market expectations.

- Real final sales to private domestic purchasers, which we call core GDP, grew at a 3.2% pace and has averaged a 3.1% pace for the past 7 quarters (or yearend 2022).

- Growth continues to be driven by a remarkably resilient consumer. Real personal consumption expenditures rose at a 3.7% pace in Q3 and have averaged a 2.9% pace since yearend 2022.

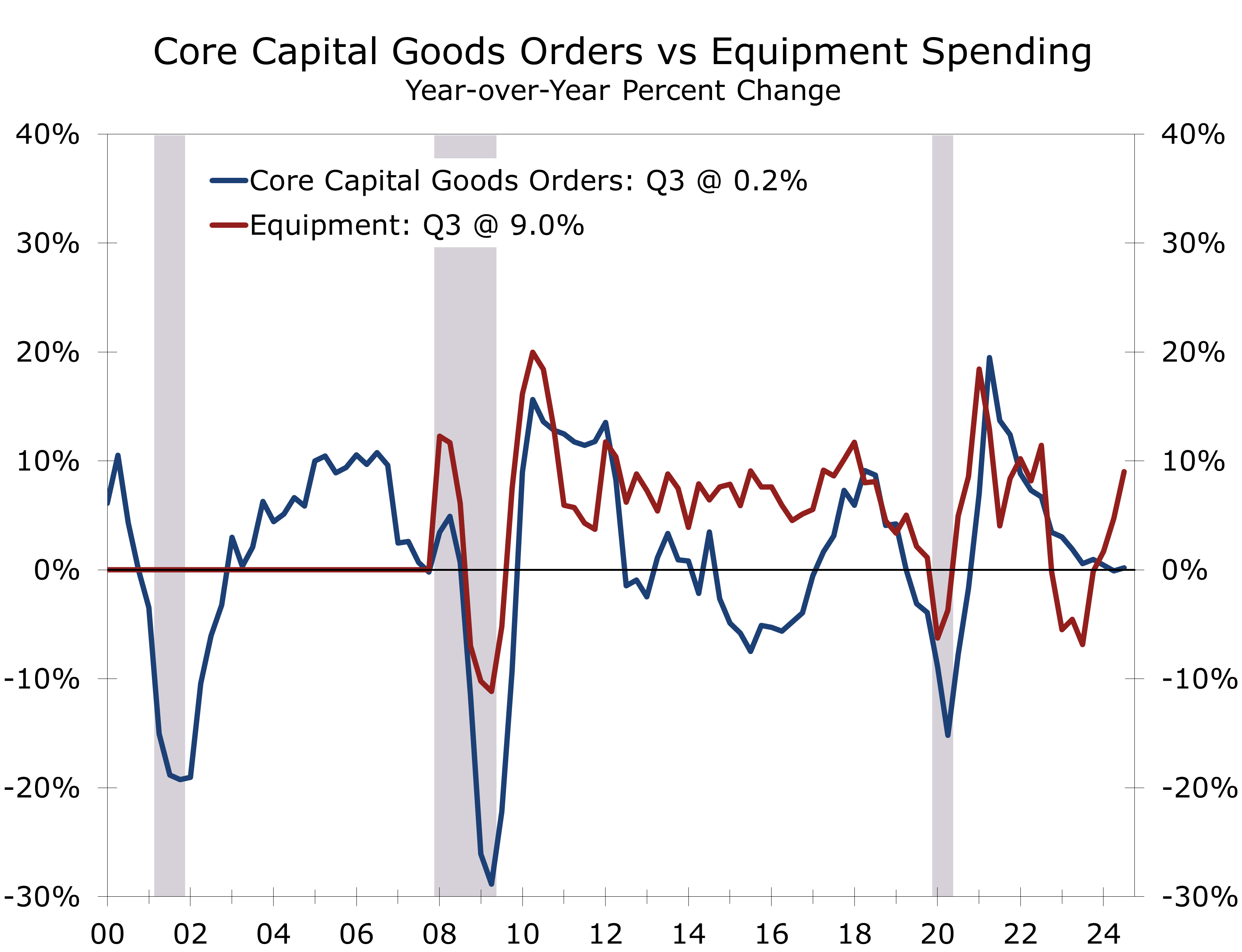

- Fixed investment grew at a solid 3.3% pace, driven by another surge in equipment spending. Structures investment declined, while intellectual property outlays posted another uncharacteristically modest gain. Residential investment fell at a 5.1% pace.

- The GDP data remain confoundingly positive. Since 2022, private final demand for goods and services has averaged over 3%, despite stagnant home and light vehicle sales. Growth is largely driven by a shift toward services and experiences.

The U.S. economy expanded at a solid 2.8% annualized rate in Q3, with real final sales to domestic purchasers hitting their highest mark since early 2023. This pace is hard to square with this past summer’s softer jobs number and calls for aggressive interest rates and reflects resilient consumer spending and business fixed investment.

Consumer spending remains the key underpin to the economy’s recent momentum, with spending supported by easing inflation and a resilient labor market. Moderating inflation, particularly for gasoline, is bolstering consumer purchasing power.

Consumer spending rose at a 3.7% pace in Q3. Goods purchases rose at an astounding 6.0% pace, the strongest pace since the first quarter of 2023. Spending for durable goods climbed at an 8.1% pace, while spending for nondurables rose at a 4.9% pace.

Falling gasoline prices helped drive real consumer spending higher this past summer.

The rise in goods purchases aligns with expectations, as core retail sales surged by 6.4% in Q3, pushing earlier GDP estimates higher. Key drivers included other nondurable goods, notably GLP-1 prescription drugs, and motor vehicles and parts, including maintenance and repairs. Services spending was led by strong gains in healthcare and continued growth in dining, hotels, and other experiential sectors, including sporting events, concerts and other live performances.

Business fixed investment rose at a solid 3.3% pace, driven by an 11.1% surge in equipment investment. This increase likely reflects a catch-up to the earlier spike in factory construction. Additionally, the East Coast port strike likely prompted firms to accelerate deliveries, which could result in a payback in Q4. The recent trend in orders supports this notion.

A surge in capital equipment spending continues to drive business fixed investment.

Outlays for structures fell at a 4.0% annual rate, reflecting a dwindling pipeline of incentive-driven projects. Hyundai’s massive EV assembly plant outside Savannah recently began production, and Taiwan Semiconductor’s plant in Arizona has also been completed. Additionally, oil and gas exploration expenditures, which contribute to structures investment, have also slowed.

Spending on intellectual property, which encompasses software and film production, remains weak, with investment growing at only a 0.6% annual rate, following a 0.7% increase in the previous quarter. This minimal growth coincides with a slowdown in hiring in key tech hubs like Silicon Valley, Austin, and the Research Triangle. Additionally, a slump in the entertainment industry is impacting hiring in major film centers in Southern California and Atlanta.

Government spending grew at a robust 5.0% pace in Q3, led by federal defense outlays, which surged at a 14.9% pace. State and local government spending rose at a healthy 2.3% pace, reflecting strong revenue growth and residual stimulus dollars.

While economic growth was stronger than expected, inflation was slightly lighter. The GDP deflator rose at just a 1.8% annual rate, while the PCE deflator climbed at a rate of 1.5%, largely due to a decline in gasoline prices. Excluding food and energy prices, the core PCE deflator—the Fed’s preferred inflation gauge—rose at a 2.2% pace and is up just 2.3% over the past year.

Despite the recent improvement, consumers are still suffering from inflation fatigue. Overall prices are about 20% higher than they were before the pandemic, with grocery prices up 25% and rent rising by 30%. Wages have not kept pace with inflation, and the proportion of the population able to afford a new or existing home, as well as a new car or SUV, remains near an all-time low. This situation reflects consumers’ frustration with the economy and is why the Fed will likely tread carefully in reducing short-term rates. It also explains the restlessness among voters heading into the election.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

October 30, 2024

Mark P. Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

Undefeated Johnson C. Smith Tries to Keep Rolling Against Winston-Salem State

A Historic Rebuild at Johnson C. Smith

- The drama continues in college football, with big games every week reshaping the rankings and the playoff picture.

- Week 8 saw #5 Georgia defeat #1 Texas in Austin. Alabama also took its second loss, losing 24-17 to Tennessee.

- Some of this season's biggest surprises face challenges this week, with Washington visiting undefeated Indiana, Notre Dame heading to undefeated Navy, and LSU taking on Texas A&M in a showdown between the last two teams still unbeaten in SEC play this year.

- Our featured matchup focuses on another surprise team this year, Johnson C. Smith, which is off to their best start since 1969. The Golden Bulls travel to Winston-Salem State, where they have not won since 2010.

- Johnson C. Smith is located just outside downtown Charlotte in Biddleville, which is Charlotte’s oldest surviving predominantly African American neighborhood.

- Winston-Salem State is located just east of downtown Winston Salem near the historic Happy Hill neighborhood.

College football has quite a few Cinderella stories going late into the season year. Most Cinderella’s slip up way before week 9 into the season and see pumpkins arrive way before Halloween. This week will serve a dose of reality one way are another.

Two of the feel-good stories in a year everyone is question conference realignment and NIL deals are Army and Navy. Both schools remain undefeated, something that has not occurred since the 1940s. Navy will get its first real test this week, when Notre Dame travels to Annapolis to take on the Midshipmen. A similar feel-good story is brewing in the Midwest, with Indiana off to a 6-0 start and atop the Big Ten conference. Usually by now, Hoosiers are giving thanks that they are basketball school. The Hoosiers will host Washington Saturday night and are also enjoying a rare football season visit from ESPN GameDay.

Conference expansion and Name, Image and Likeness (NIL) has found a way to kick up the competitive level of the SEC. Vanderbilt has been of this season’s biggest surprises, defeating Alabama and Kentucky, while getting off to a 5-2 start. The task gets even tougher for the Commodores as they host the Texas Longhorns, which hope to get back on track following last week’s loss to Georgia.

The leadership in the SEC race is also on the line this week, with LSU traveling to Texas A&M, with both teams 6-1 and undefeated in conference play.

Brick by Brick: Johnson C Smith Has Built a Contender

One of the best stories in HBCU football is taking shape just outside downtown Charlotte, where the Johnson C. Smith Golden Bulls have begun the year 7-0 and are now the only undefeated Historically Black College and University football team. This week will bring a major test for the Golden Bulls as they take on the Winston-Salem State Rams at Bowman Gray Stadium this Saturday afternoon. The Rams have dominated the series in recent years, and Johnson C. Smith has not won in Winston-Salem since 2010.

Coach Maurice Flowers has been on a mission to reset the culture at Johnson C. Smith. His first season was challenging, with the Golden Bulls finishing at 2-7. Flowers knew that changing the culture would be difficult and would require changes both on and off the field. He is a strong believer that wins correlate with Grade Point Averages and has pushed his team to boost their average above a 3.0.

Johnson C. Smith has a great opportunity to flourish. Charlotte is hungry for a winning football program, with the Panthers still in the early stages of what looks like a multi-year rebuilding effort. Johnson C. Smith also has a powerful legacy. The predecessor institution, Biddle Memorial Institute, played the first-ever game between two Black colleges, defeating Livingstone College from nearby Salisbury, 5-0, back in 1892.

Coach Flowers is working to add a new chapter to this history, pushing the Golden Bulls toward dominance not only in HBCU circles but across Division II football. The Golden Bulls moved up a spot this past week following an unexpectedly hard-fought 21-14 victory over Shaw, played in front of one of the largest audiences to ever watch a game at the Irwin Belk Complex on the Johnson C. Smith campus.

Last week’s game was homecoming. This week will mark a greater challenge and a greater opportunity. A win against Winston-Salem State would set up a coming-out party, as the Golden Bulls would move further up the rankings and be in the driver’s seat for the CIAA Championship.

Johnson C. Smith University

Johnson C. Smith University (JCSU) is a Historically Black College and University (HBCU) located in Charlotte, North Carolina, with significant contributions to the region’s academic, athletic, and economic landscape. Founded in 1867, JCSU is located in the heart of Biddleville, Charlotte’s oldest African American neighborhood. The university’s rich history reflects its role as an educational leader, a catalyst for economic development, and a cultural institution with a deep impact on Charlotte and beyond.

JCSU was originally founded as the Biddle Memorial Institute in 1867, just two years after the Civil War. Established by the Presbyterian Church to educate newly emancipated African Americans, it received financial support from Mary D. Biddle, widow of Union Army Major Henry Biddle, who contributed $1,400 in his memory. Initially a theological institution, JCSU focused on training African American men as ministers and teachers, which was crucial to rebuilding African American communities during Reconstruction. The university quickly expanded its curriculum to include liberal arts and sciences, offering one of the first four-year degree programs for African Americans in the South.

In 1923, the school was renamed Johnson C. Smith University after businessman Johnson C. Smith, whose widow, Jane Berry Smith, made a significant financial contribution. Her donation helped construct new buildings and supported the university’s growing academic programs. This period of expansion saw JCSU producing graduates who played prominent roles in education, politics, and business throughout the South. Despite the challenges of segregation, JCSU remained a respected institution committed to academic excellence and social progress.

During the Civil Rights Movement, JCSU was instrumental in Charlotte’s African American community. Students and faculty actively participated in efforts to end segregation, particularly in local schools and businesses. In the post-Civil Rights era, JCSU expanded its campus and programs to meet the changing needs of students and the broader community. Today, JCSU is known for its strengths in STEM, business, and the arts, continuing to promote higher education for African Americans and underserved communities. The university remains a cornerstone of the Biddleville neighborhood and a leading HBCU.

The JCSU football program, established in the 1890s, quickly became a source of pride for the university. The Golden Bulls earned a reputation as a strong contender among HBCUs. Despite racial discrimination and limited resources, the team persevered and helped elevate African American collegiate football. JCSU was one of the founding members of the Central Intercollegiate Athletic Association (CIAA) in 1912, a conference dedicated to HBCU athletics.

The 1950s and 1960s were a golden era for JCSU football, led by coaches like Eddie McGirt, who became head coach in 1958. Under McGirt’s leadership, the Golden Bulls won numerous conference championships, including the CIAA title in 1969. McGirt was later inducted into the CIAA Hall of Fame for his contributions. During this time, football helped boost the university’s visibility and fostered unity and pride in Charlotte’s African American community. Homecoming games became major cultural and social events.

JCSU football faced challenges in the 1980s and 1990s, including financial struggles and inconsistent performance. However, a resurgence in the 2000s brought renewed focus on recruiting and facility improvements. In recent years, the Golden Bulls have remained competitive in the CIAA, regularly reaching the playoffs. The football program continues to be a key part of student life, providing opportunities for leadership development, academic success, and representing the university.

Historic Biddleville

As the largest institution in Biddleville, JCSU has played a crucial role in the neighborhood’s economic and social development. Biddleville, one of Charlotte’s oldest African American communities, has historically faced challenges such as underinvestment, economic isolation, and gentrification. Johnson C. Smith University has served as a stabilizing force, acting as both an educational anchor and a source of economic opportunity.

Over the years, JCSU has made significant investments in its campus, with new academic buildings, residence halls, and athletic facilities contributing to the revitalization of Biddleville. These developments have spurred economic activity in the surrounding area, attracting businesses and residents to the neighborhood. One of the most prominent examples of JCSU’s impact is Mosaic Village, a mixed-use development project that includes student housing, retail space, and community amenities. Opened in 2012, Mosaic Village stands as a cornerstone of the university’s efforts to improve the neighborhood and promote economic growth in the West End.

Beyond its direct influence on Biddleville, JCSU has played a key role in Charlotte’s broader economic development. The university’s focus on workforce development, entrepreneurship, and community engagement has helped establish Charlotte as a center of opportunity for African Americans and underserved populations. JCSU has long been a leader in producing graduates in business, science, technology, engineering, and math (STEM) fields, all of which are critical to the local and regional economy. As Charlotte has grown into a major financial and business hub, JCSU graduates have filled key roles in banking, healthcare, technology, and education.

The university’s Center for Innovation and Entrepreneurship (CIE) supports students and community members in launching businesses and fostering economic growth. By offering resources such as mentorship, business planning, and networking opportunities, the CIE has cultivated a culture of entrepreneurship in Charlotte, particularly among minority-owned businesses.

JCSU’s leadership in civic and cultural engagement has also contributed to Charlotte’s economic and social development. The university has been at the forefront of promoting diversity, inclusion, and social justice in the city, providing a platform for addressing systemic inequality and advocating for economic mobility in underserved communities.

Through community service projects, partnerships with local organizations, and research on pressing social issues, JCSU has worked to uplift Charlotte’s most vulnerable populations. The university’s outreach programs in education, healthcare, and economic empowerment address the root causes of poverty and inequality, contributing to the city’s long-term prosperity.

Charlotte

Charlotte’s early settlement in the mid-18th century, primarily by European immigrants, laid the groundwork for its agrarian-based economy, with cotton and tobacco as key crops. This agricultural prosperity was instrumental in driving future economic growth. The introduction of the North Carolina Railroad in the 1850s transformed Charlotte into a transportation and trade hub, spurring population growth and industrialization. Manufacturing, particularly in textiles and furniture, along with banking, began to shape the city’s economy in the post-Civil War era.

Today, Charlotte has established itself as a leading economic hub in the South, fueled by a diverse economy, strong population growth, strategic transportation connections, and a business-friendly climate that attracts new businesses and residents.

Charlotte rapidly grew to become a major financial center in the 1980s and 1990s, with NCNB and First Union/Wachovia racing to become two of the largest banks. Charlotte hosts headquarters for Bank of America (the successor to NCNB/NationsBank) and Truist Financial (BB&T and SunTrust), as well as the largest employee base for Wells Fargo (the successor to First Union/Wachovia). It is also the principal location for Ally Financial’s operations. This financial sector is crucial to Charlotte’s economy, providing thousands of jobs across investment banking, specialty finance, insurance, and financial technology (FinTech).

In addition to finance, Charlotte benefits from robust healthcare, energy, technology, and logistics sectors. Healthcare is bolstered by key players like Atrium Health and Novant Health, which contribute significantly to the economy and serve the region’s expanding population. Atrium’s partnership with Wake Forest University has brought a medical school and a tech campus to Charlotte, enhancing the city’s healthcare and educational footprint.

Charlotte’s energy sector also plays a critical role, with Duke Energy headquartered in the city and advancing renewable energy and sustainability initiatives. The technology sector is growing rapidly, supported by local university talent and Charlotte’s emerging reputation as a FinTech center. Companies like LendingTree and AvidXchange have grown from startups to industry leaders, and Eli Lilly’s recent $1 billion investment in a manufacturing facility for GLP-1 drugs underscores the city’s role in life sciences innovation.

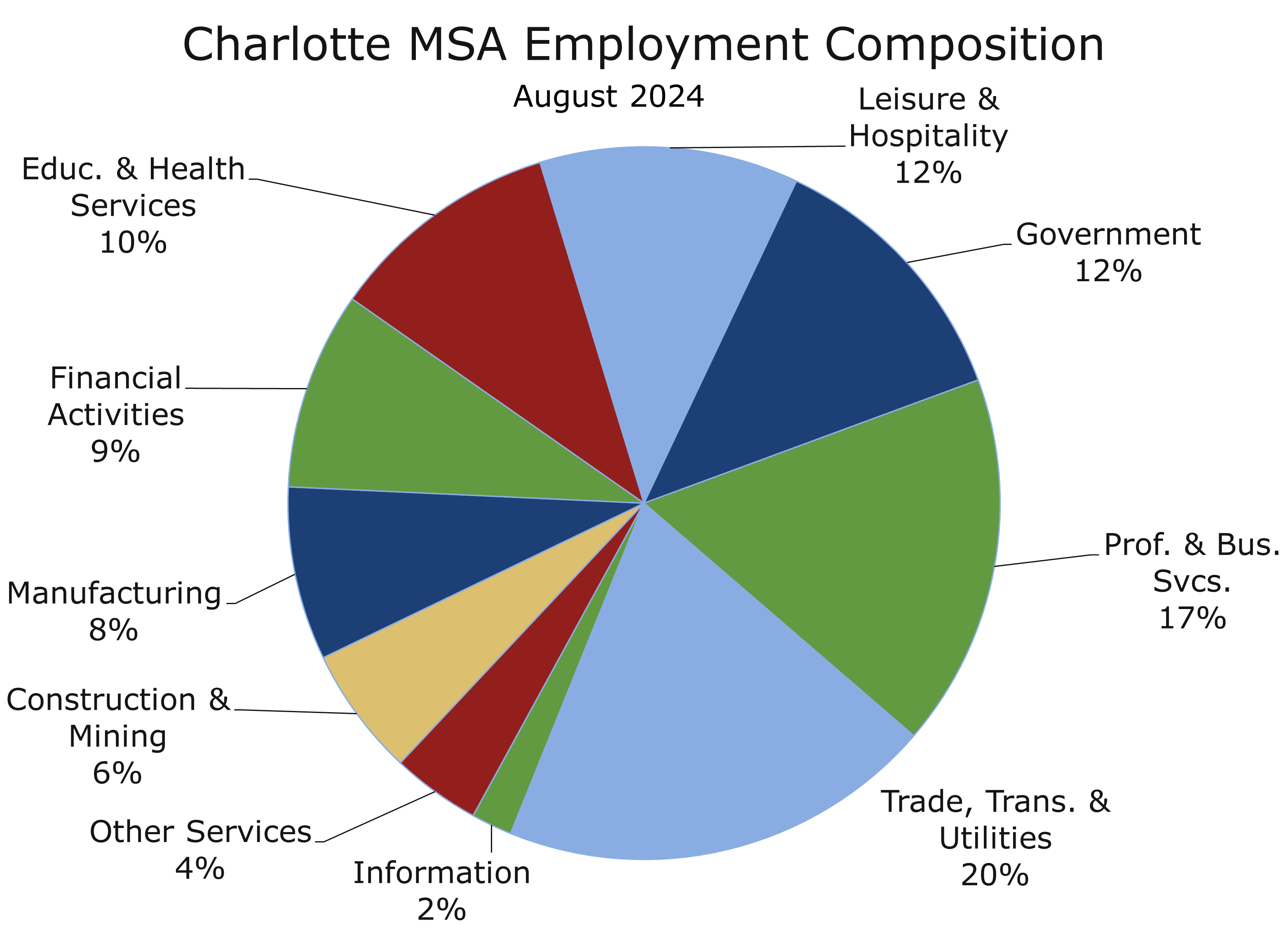

Advanced manufacturing and logistics in Charlotte are bolstered by the city’s strategic position and extensive infrastructure. Charlotte Douglas International Airport, the second-largest hub for American Airlines, ranks as the ninth-busiest U.S. airport, offering over 700 nonstop flights to 190 destinations, including key international markets. The airport’s connectivity has been pivotal in attracting corporate and regional headquarters to the city. Charlotte hosts seven Fortune 500 headquarters (Lowe’s, Honeywell, Nucor, Duke Energy, Bank of America, Truist, and Sonic Automotive) and numerous regional and international headquarters. Additionally, Charlotte’s location at the intersection of I-85 and I-77 supports its role as a regional distribution center for the Northeast and Midwest.

While vacancy rates have risen, the metro area’s commercial real estate market remains resilient, particularly in Uptown, South End, SouthPark, and Ballantyne, as corporate relocations and population growth fuel demand for residential and office spaces. Recent arrivals include Honeywell, which moved its headquarters to downtown Charlotte, and Lowe’s, which opened a technology center in a 20-story tower in South End. The return to the office has gained momentum in recent months, which is bolstering business at restaurants and retailers.

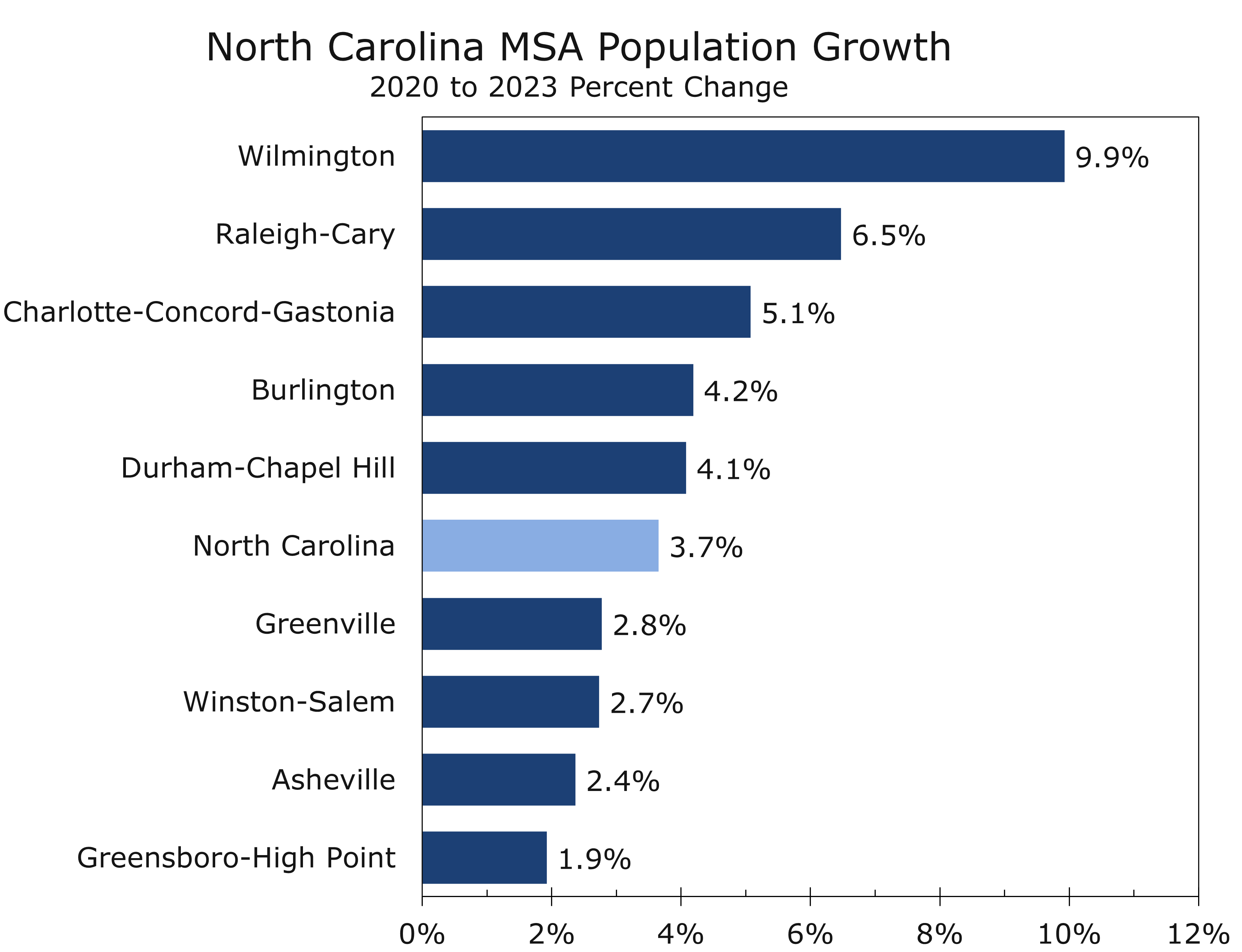

Charlotte’s population surged by over 50,000 in 2023, and projections indicate an increase of another 55,000 residents in 2024, bringing the metro area’s population to 2.86 million. This growth underscores Charlotte’s increasing appeal as both an economic and lifestyle destination. The city has been ranked as one of the top locations for “baby chasers,” grandparents moving closer to where their grandchildren live.

Despite this growth, the Charlotte region has faced challenges related to economic inequality and housing affordability, both of which have been exacerbated by the city’s rapid expansion. Efforts to address these challenges have focused on improving economic mobility, which is notably low in Charlotte compared to other U.S. cities. Community-driven initiatives, such as investments in education, workforce development, and affordable housing, have been central to bridging the wealth gap.

Economic mobility in Charlotte is being addressed through programs that aim to create pathways out of poverty, particularly for historically underserved communities. Organizations like the Leading on Opportunity Task Force emphasize the importance of education, early childhood development, and skill-building to enhance economic mobility. Workforce development initiatives, including collaborations between local businesses and educational institutions, are also crucial in providing residents with the training and support needed to access higher-paying jobs. Additionally, sustainable urban planning and affordable housing projects are part of a broader strategy to ensure that Charlotte’s growth benefits all its residents, fostering long-term economic inclusion and equity.

These efforts are yielding results. The most recent study by Chetty’s Opportunity Insights shows that Charlotte has moved up from 50th out of 50 MSAs in 2014 to 38th, demonstrating one of the greatest improvements. The 2014 report galvanized civic leaders, and government, businesses, and community organizations have collaborated to increase opportunities for disadvantaged residents.

Winston-Salem State University

Winston-Salem State University (WSSU) was founded as the Slater Industrial Academy in 1892 by the North Carolina Baptist State Convention. The school was established to provide vocational and academic training for African Americans in the region, addressing the educational needs of newly freed individuals after the Civil War. The academy’s mission was to equip students with practical skills and academic knowledge to thrive in a post-emancipation society.

In 1925, the institution was renamed Winston-Salem Teachers College and began focusing on teacher education. This shift reflected the growing demand for qualified educators in the African American community, particularly as schools across the South began to integrate. The college became known for its strong programs in education, liberal arts, and sciences.

In 1969, Winston-Salem Teachers College achieved university status and was renamed Winston-Salem State University. This transition marked a significant milestone in the institution’s history, allowing it to expand its academic programs and offer a wider range of degrees, including baccalaureate and graduate programs. WSSU became a member of the University of North Carolina System in 1971, further enhancing its status and resources.

Over the following decades, WSSU continued to evolve, increasing its enrollment and diversifying its academic offerings. Today, WSSU provides undergraduate and graduate programs in various fields, including health sciences, business, education, and the arts.

In recent years, WSSU has focused on enhancing its academic programs, infrastructure, and community engagement. The university has invested in new facilities, such as the Winston-Salem State University Student Center, which serves as a hub for student life and activities. WSSU has also strengthened its partnerships with local businesses and organizations, promoting workforce development and community service.

As a Historically Black College and University (HBCU), WSSU has played an essential role in advocating for social justice, equity, and access to quality education for African Americans and other underserved communities. The university continues to uphold its mission of producing graduates who are well-equipped to contribute to society.

The WSSU football program has a rich history dating back to the early 1900s. The first organized football team was formed in 1905, competing against other HBCUs and local teams. The program developed steadily over the years, with the university’s focus on athletics contributing to its growth.

In its early years, the team faced numerous challenges, including limited resources and racial discrimination. However, the program’s resilience and commitment to success allowed it to flourish, establishing a strong following within the university and the local community.

The 1950s and 1960s marked a golden era for WSSU football. Under the leadership of notable coaches, the team experienced significant success in the Central Intercollegiate Athletic Association (CIAA), consistently competing for conference championships. WSSU players earned recognition for their athletic prowess, and several alumni went on to play professionally in the National Football League (NFL).

The football program served as a source of pride for the university, fostering a sense of community and unity among students, alumni, and fans. Homecoming games became major events, drawing large crowds and reinforcing the university’s cultural significance in Winston-Salem.

The WSSU football program faced challenges in the 1980s and 1990s, including fluctuating enrollment and financial constraints. However, the university’s commitment to athletics remained strong, leading to a renewed focus on recruitment and program development in the 2000s.

In recent years, the Golden Rams have seen a resurgence, with improved performance in the CIAA and increased community support. The football program continues to be an integral part of student life at WSSU, providing student-athletes with opportunities for personal and professional growth.

Winston-Salem State University (WSSU)

Winston-Salem State University (WSSU) has significantly contributed to the economic growth of Winston-Salem and the surrounding area through its focus on education and workforce development. The university prepares students for careers in high-demand fields such as healthcare, education, business, and technology, with graduates filling critical roles across various industries and supporting the region’s economic stability.

WSSU has established partnerships with local businesses and organizations, facilitating internship and employment opportunities for students. The university’s emphasis on experiential learning enables students to gain practical skills and connect with potential employers, enhancing their career prospects and contributing to the local economy.

WSSU’s commitment to community engagement extends beyond the classroom. The university actively participates in initiatives addressing social and economic challenges in Winston-Salem, including programs focused on healthcare access, educational equity, and economic empowerment.

With a strong emphasis on health sciences, WSSU partners with local health organizations to promote public health initiatives. The university’s nursing and allied health programs train healthcare professionals who provide essential services to the community. Research conducted by faculty and students also contributes to advancements in public health and healthcare access, further enhancing the region’s economic development.

WSSU plays a vital role in preserving and promoting the cultural heritage of African Americans in Winston-Salem. Its commitment to social justice, equity, and community service fosters a sense of pride among residents and contributes to a vibrant local culture.

The university hosts various events, including cultural festivals, art exhibitions, and educational conferences, which attract visitors to Winston-Salem and stimulate the local economy. These events not only celebrate African American contributions but also promote community cohesion and economic activity.

Winston-Salem

Winston-Salem, North Carolina, was formed through the merger of two towns: Winston, founded in 1849, and Salem, established earlier in 1766 as a Moravian settlement. The Moravians, a European religious group, sought to create a community centered around values of education and agriculture. Salem developed into a significant hub for Moravian culture, with its well-preserved architecture reflecting deep historical roots.

Winston grew as a trade and transportation center due to its strategic location along major roads. Named after K.D. Winston, a local landowner instrumental in its founding, the town expanded as industries such as tobacco, textiles, and furniture manufacturing began to thrive. By the late 19th century, Winston-Salem experienced substantial industrial growth, particularly in tobacco production. The establishment of the R.J. Reynolds Tobacco Company in 1875 marked a turning point, positioning the city as a tobacco industry leader and spurring population growth.

The official merger of Winston and Salem in 1913 created a unified municipality, fostering coordinated development and planning. The city continued to grow, establishing key educational institutions, including Winston-Salem State University in 1892 and Wake Forest University, which relocated to Winston-Salem in 1956.

Throughout the 20th century, Winston-Salem diversified its economic base beyond tobacco, moving into textiles, banking, and healthcare, becoming North Carolina’s economic center through the 1970s. Major companies, such as Krispy Kreme Doughnuts, were founded here, enhancing its reputation as an entrepreneurial hub. However, globalization and declining tobacco consumption impacted the region’s economy, straining textile and furniture manufacturers. The city has also faced challenges retaining corporate headquarters, with Truist and Krispy Kreme relocating to Charlotte.

In the late 20th century, Winston-Salem evolved into a cultural and educational center. Establishments like the Winston-Salem Arts Council and the North Carolina Black Repertory Company enriched its arts scene, while healthcare expanded through institutions like Wake Forest Baptist Medical Center and Novant Health. This diversification sustained the economy while honoring its historical roots.

In the 21st century, Winston-Salem has focused on technology and entrepreneurship, launching initiatives to attract tech companies and support startups. Downtown revitalization has transformed the area into a vibrant hub filled with restaurants, shops, and cultural attractions. Winston-Salem continues to balance its historical legacy with innovation, remaining a key player in North Carolina’s economy with a diverse economy, rich cultural heritage, and a strong commitment to community development.

Previewing the Game

Johnson C. Smith remains the only undefeated team in HBCU football, with hopes of clinching their first CIAA championship appearance since 1972. Currently, they hold a 4-0 conference record, tied with Virginia Union for the best in the CIAA. Johnson C. Smith defeated Virginia Union earlier this year but must still get past Winston-Salem State to secure a spot in the CIAA Championship. A victory would solidify their position and give them some breathing room heading into their final two games (Fayetteville State and Livingstone).

The key for Johnson C. Smith is to maintain their strong defensive play. The Golden Bulls boast the top defense in the CIAA, allowing just 11.7 points per game, with standout linebackers Benari Black and Jack Smith playing pivotal roles; Black leads the conference in tackles.

On offense, Darius Ocean leads the CIAA in passing, averaging 243.3 yards per game with 14 touchdowns. His primary target, Brevin Caldwell, has over 800 receiving yards. How these two match up against WSSU’s solid defense will be crucial.

Winston-Salem State enters the game with a 5-2 record, with losses to North Carolina A&T and Virginia Union. WSSU has a potent offense, scoring over 30 points in each of their past two games. However, their defense has been inconsistent; Virginia Union racked up 31 points in their victory, while North Carolina A&T scored 27 points. No other opponent has managed to score more than two touchdowns against the Rams this season.

We expect a close game and give the edge to Johnson C. Smith. The Golden Bulls seem to have a sense of destiny, and it would not be surprising to see them finish the season undefeated. That said, WSSU has historically dominated this series, winning 13 of the past 14 meetings. Johnson C. Smith won last year, and we expect them to repeat this year.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Tulane Visits Rice: A Clash Between Two ‘Southern Ivies’

Its Crunch Time for College Football

- Conference realignment continues to produce marquee matchups each week.

- Week 7 saw #2 Oregon edge out Ohio State 32-31, and #3 Penn State battle back to defeat Southern Cal 33-30 in overtime.

- This week brings another slate of key games, with #5 Georgia traveling to Austin to take on the #1-ranked Texas Longhorns.

- Our featured matchup features Rice traveling to New Orleans to face the Tulane Green Wave. Both programs have a rich history but have faced challenges returning to the upper ranks of college football.

- Houston, the energy capital of the world, has maintained one of the nation’s strongest economies over the past 25 years.

- New Orleans has struggled since Hurricane Katrina but is seeing improved momentum as it focuses on the Eds and Meds sectors to grow its economy.

- Tulane (4-2) is a three-touchdown favorite against Rice (2-4) and is undefeated in the AAC. The Green Wave’s two losses were to Kansas State and Oklahoma. Rice is coming off a 29-27 victory over UT-San Antonio.

Mid-October may very well bring an end to many schools’ playoff hopes as the season reaches a critical juncture. The SEC is home to two crucial matchups this week, with 5th-ranked Georgia making its first visit to Austin in 66 years to take on the top-ranked Texas Longhorns. Texas has looked like a number one team for much of this year, albeit against relatively light competition. Coming into the game, Texas is a 5-point favorite, marking the first time the Dawgs have been underdogs since 2021, ending a streak of 49 games. This matchup not only holds playoff implications but also serves as a litmus test for both programs, as Georgia aims to prove its mettle against a top-tier opponent.

The other significant game in the SEC features 7th-ranked Alabama traveling to Knoxville to take on the 11th-ranked Tennessee Volunteers. Alabama is still reeling from its last trip to Tennessee, where it lost to Vanderbilt in Nashville two weeks ago. The Crimson Tide enters this matchup as a 3-point favorite, but the stakes are high; the loser of this game may very well be eliminated from at-large consideration for the 12-team playoff. This game is crucial not only for postseason aspirations but also for maintaining pride within the storied programs.

Another game to keep an eye on this week is 12th-ranked Notre Dame traveling to Atlanta to face a much-improved Georgia Tech (3-2) team. The Fighting Irish will look to solidify their position in the playoff race against a Yellow Jackets squad that is gaining momentum. Meanwhile, the Big Ten features several intriguing second-tier matchups, including Nebraska traveling to undefeated and 16th-ranked Indiana, and 2nd-ranked Oregon visiting Purdue on Friday night. These games could significantly impact the rankings and playoff landscape as teams vie for position and respect in their respective conferences.

Southern ‘Ivy League’

Our matchup focuses on two of the Southern Ivies – Rice and Tulane. The two programs have a storied past and have had some success in recent years. As always, we look at the history of the two programs and the local economies – Houston and New Orleans.

The Wall Street Journal recently highlighted the growing trend of high school seniors from the North choosing to attend colleges in the South since the COVID-19 pandemic. This trend is most apparent at state schools such as Clemson, Georgia Tech, Alabama, and South Carolina. Several factors drive this shift, including lower tuition, warmer weather, less political polarization, and the vibrant social and sports culture often showcased on social media.

Enrollment of Northerners at Southern public universities has surged dramatically over the past two decades, with some schools seeing increases of over 600%. The pandemic accelerated this trend as Southern schools maintained fewer restrictions, attracting students disillusioned with lockdowns in the Northeast. This shift has significant long-term implications for Southern economies, as many graduates tend to stay in the region for work. However, the growing enrollment also presents challenges for infrastructure and campus capacity.

There is a group of schools in the South that has long been favored by Northerners and is informally known as the “Southern Ivy League.” While there is no formal list, these institutions are recognized for their rigorous academics, strong alumni networks, and influential roles in the region’s educational landscape. While mostly private, the list also includes a few public institutions. Some of the universities often associated with the “Southern Ivy League” include:

Duke University (Durham, North Carolina)

Vanderbilt University (Nashville, Tennessee)

Rice (Houston, Texas)

Emory University (Atlanta, Georgia)

University of Virginia (Charlottesville, Virginia)

Davidson College (Davidson, North Carolina)

Wake Forest University (Winston-Salem, North Carolina)

University of North Carolina at Chapel Hill (Chapel Hill, North Carolina)

Washington & Lee University (Lexington, Virginia)

William & Mary (Williamsburg, Virgina)

Tulane (New Orleans, Louisiana)

Southern Methodist University (Dallas, Texas)

Furman University (Greenville, South Carolina)

Sewanee: The University of the South (Sewanee, Tennessee)

Rhodes College (Memphis, Tennessee)

The term “Southern Ivy League” is a colloquial expression that acknowledges the high caliber of these institutions compared to Ivy League schools in the Northeast. This label reflects the growing recognition of Southern universities as leaders in higher education, emphasizing their commitment to academic excellence, innovative research, and vibrant campus life. These institutions boast competitive admissions and attract top students from around the world.

Tulane University

Tulane was founded in 1834 as the Medical College of Louisiana by seven New Orleans doctors. At the time, it was only the second medical school in the South, created to train doctors to combat outbreaks of smallpox, cholera, and yellow fever in the growing New Orleans region. The school expanded in 1847 when the Louisiana state legislature established the University of Louisiana, combining the medical school with a new law department. An academic school was added in 1851, transforming it into a more traditional university. Early financial struggles were exacerbated by limited funding from the state legislature and donors. Dr. Francis Lister Hawks, the first university president, was hired largely for his ability to support himself financially, as the school could not provide a salary.

Before the university could overcome its financial troubles, the Civil War broke out. With no hope of securing government funds and over three-quarters of the student body leaving to join the war effort, the school closed in 1862. Though it reopened in 1865, the financial challenges persisted due to the South’s agricultural depression and limited public funding. The university was saved by a $1 million endowment from New Orleans merchant Paul Tulane, which inspired further donations, including millions from Josephine Louise Newcomb.

Paul Tulane’s legacy, however, is marred by racism and discrimination. His endowment stipulated that the university only admit white students, and he successfully lobbied for a Louisiana law to codify this condition. In 1884, to avoid integration, the University of Louisiana was privatized and renamed Tulane University of Louisiana.