A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics -- Signals, Strains, and Shifting Sands

Highlights of the Week

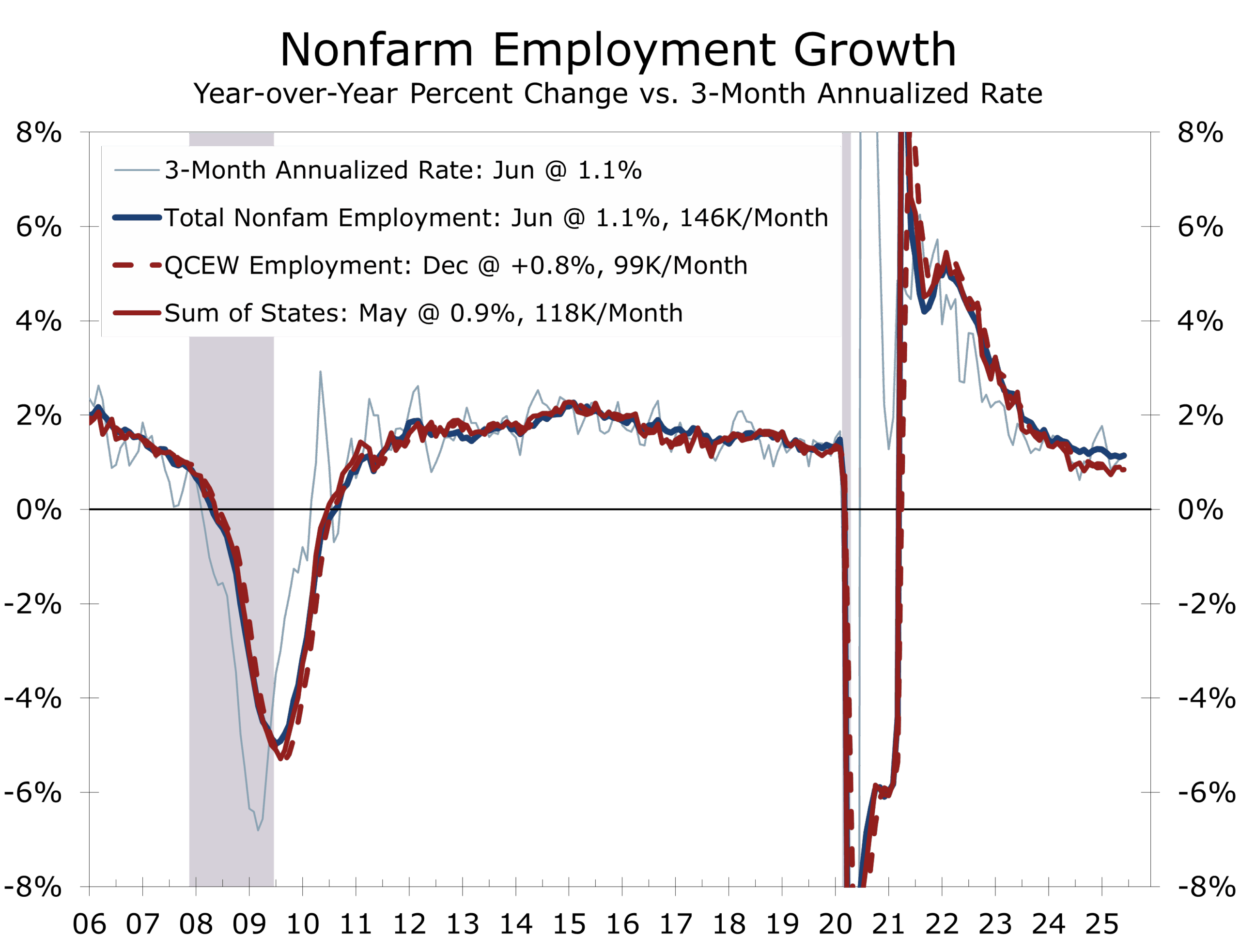

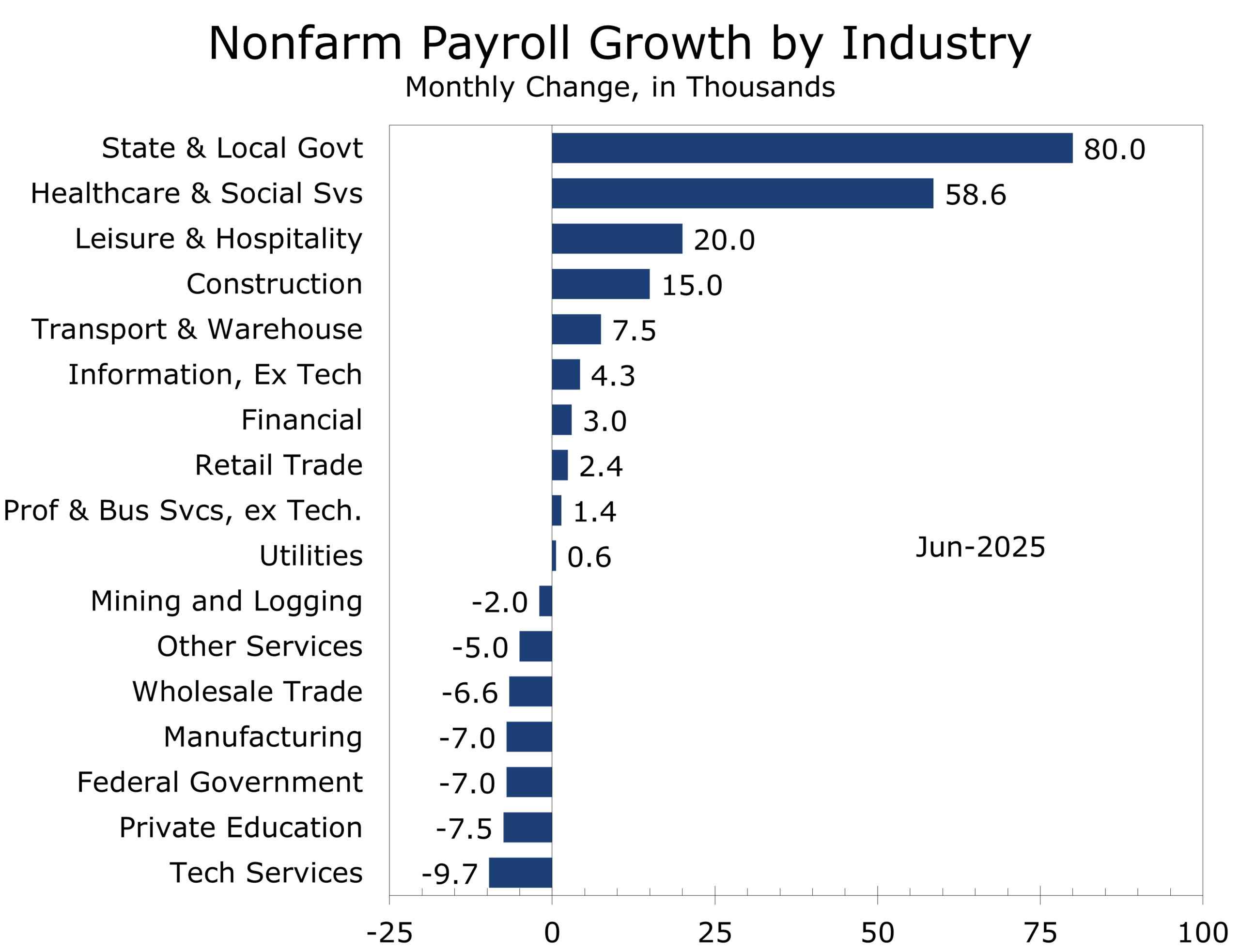

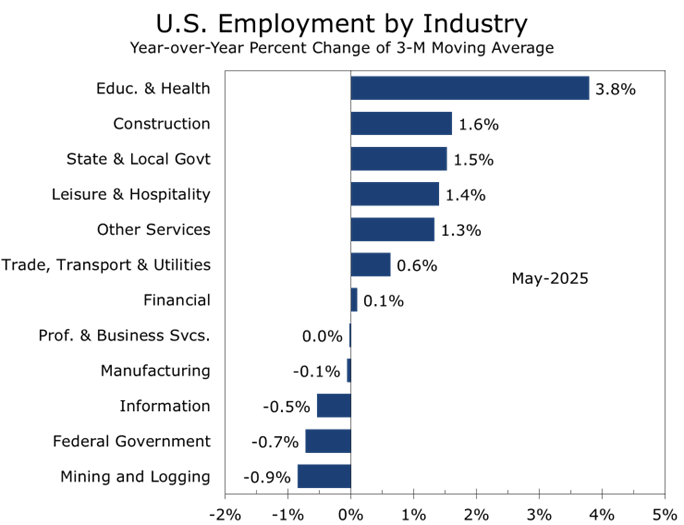

- June's employment report showed modest headline growth, but hiring remains narrowly based and the most recent QCEW data points to a weakening labor market.

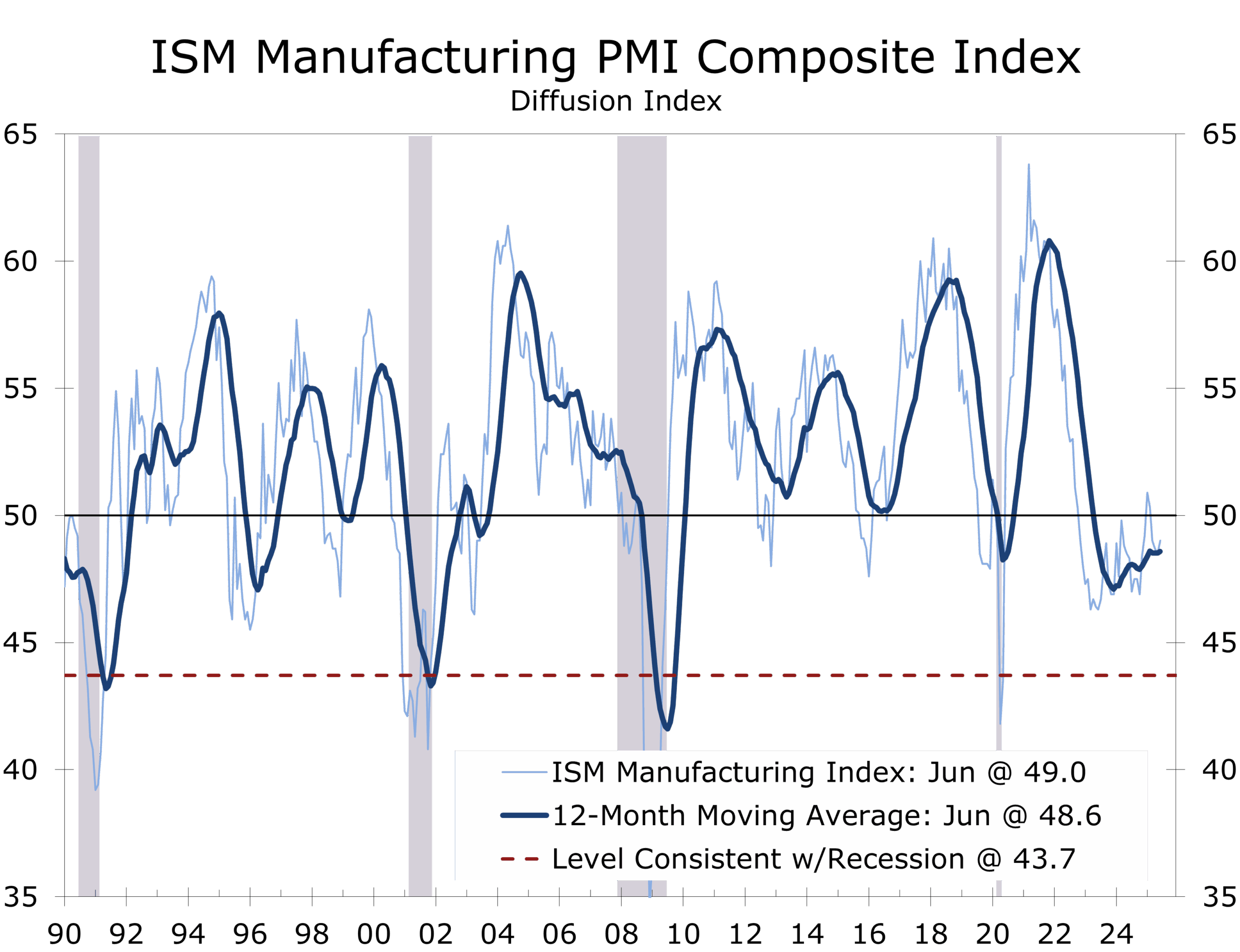

- ISM data confirmed the economy continues to grow modestly, with inflation pressures slightly easing.

- Construction spending continues to decline, with private residential and nonresidential investment both under pressure.

- The U.S. secured a tariff deal with Vietnam and moved closer to triggering tariff hikes on nations outside U.S. trade pacts.

- President Trump signed the "Big Beautiful Bill" into law, extending the 2017 tax cuts and prolonging massive budget deficits, fanning fears over fiscal dominance.

- Zohran Mamdani's New York Democratic victory signals growing economic angst.

- The Texas Hill Country floods exposed breakdowns in local emergency preparedness, not federal weather forecasting programs.

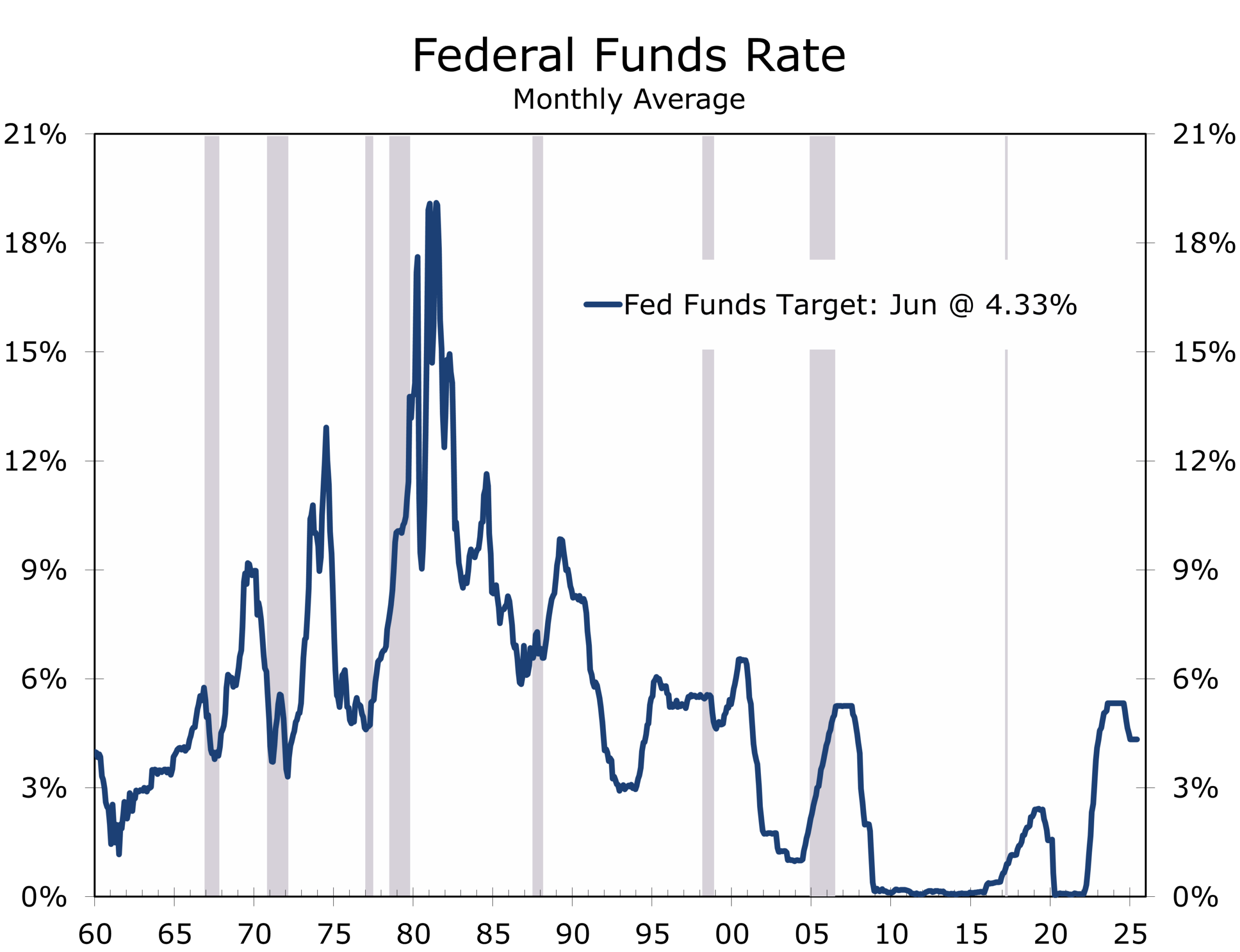

- Uncertainty and volatility have pulled back considerably since the April 2nd Liberation Day announcements. While trade deals have been slow to materialize, the economy has likely passed the peak tariff impact. The Fed is also closer to cutting interest rates and the decision at the July FOMC meeting will likely be a closer call than currently thought.

Labor Market: Cracks Beneath the Surface

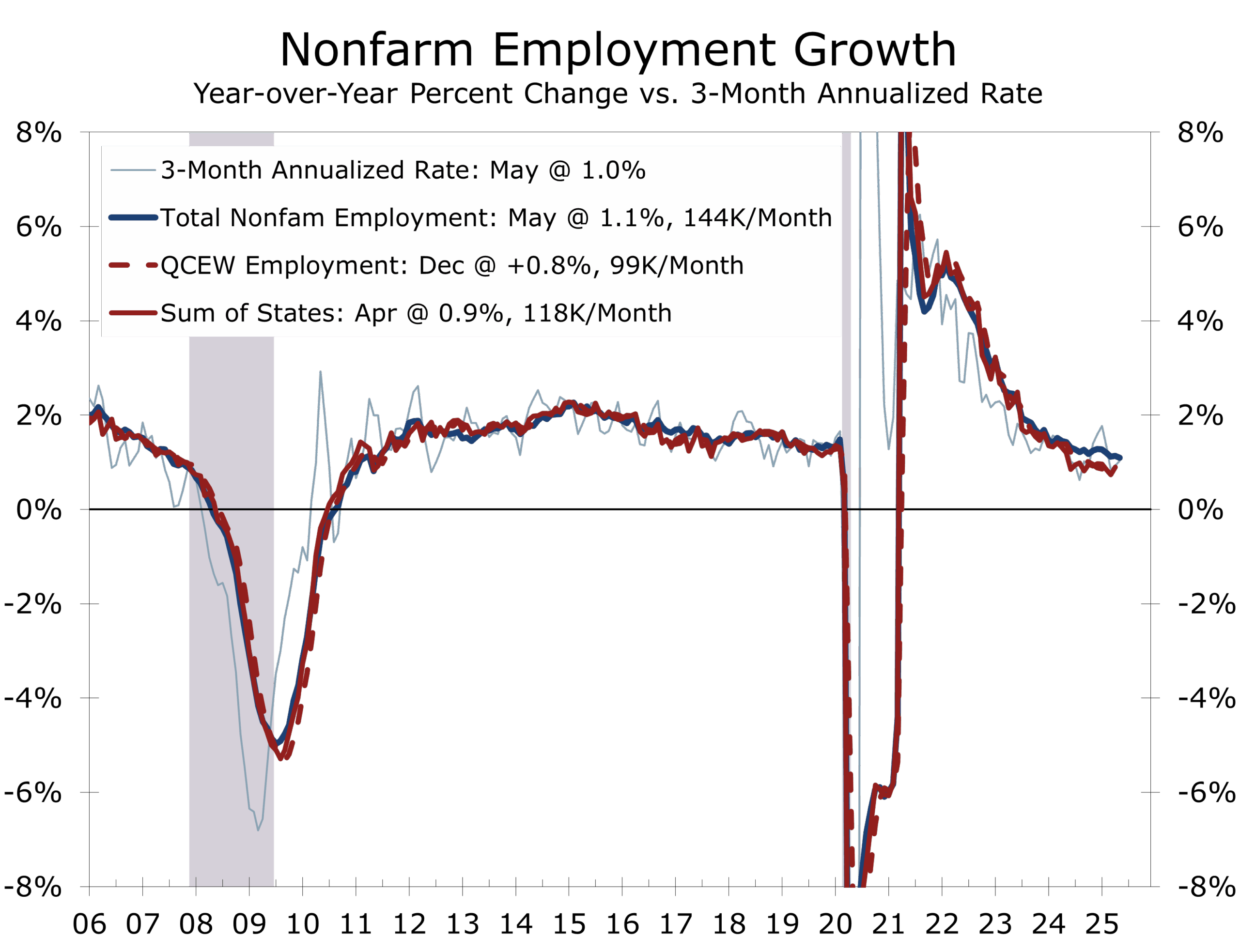

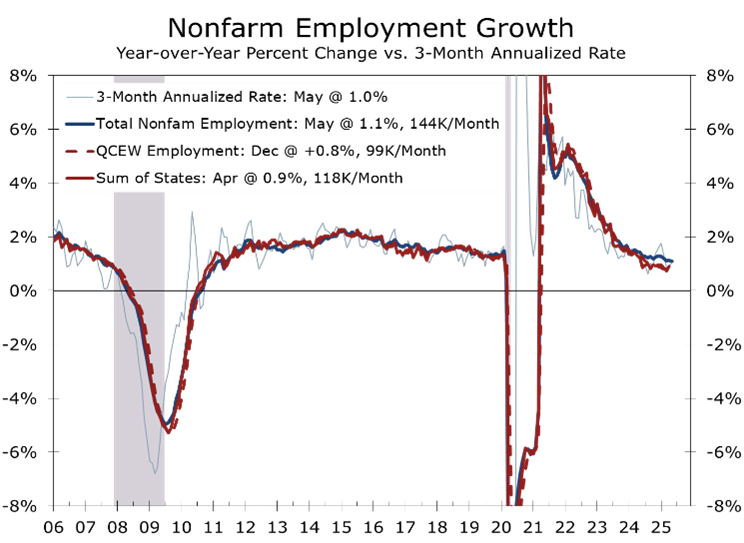

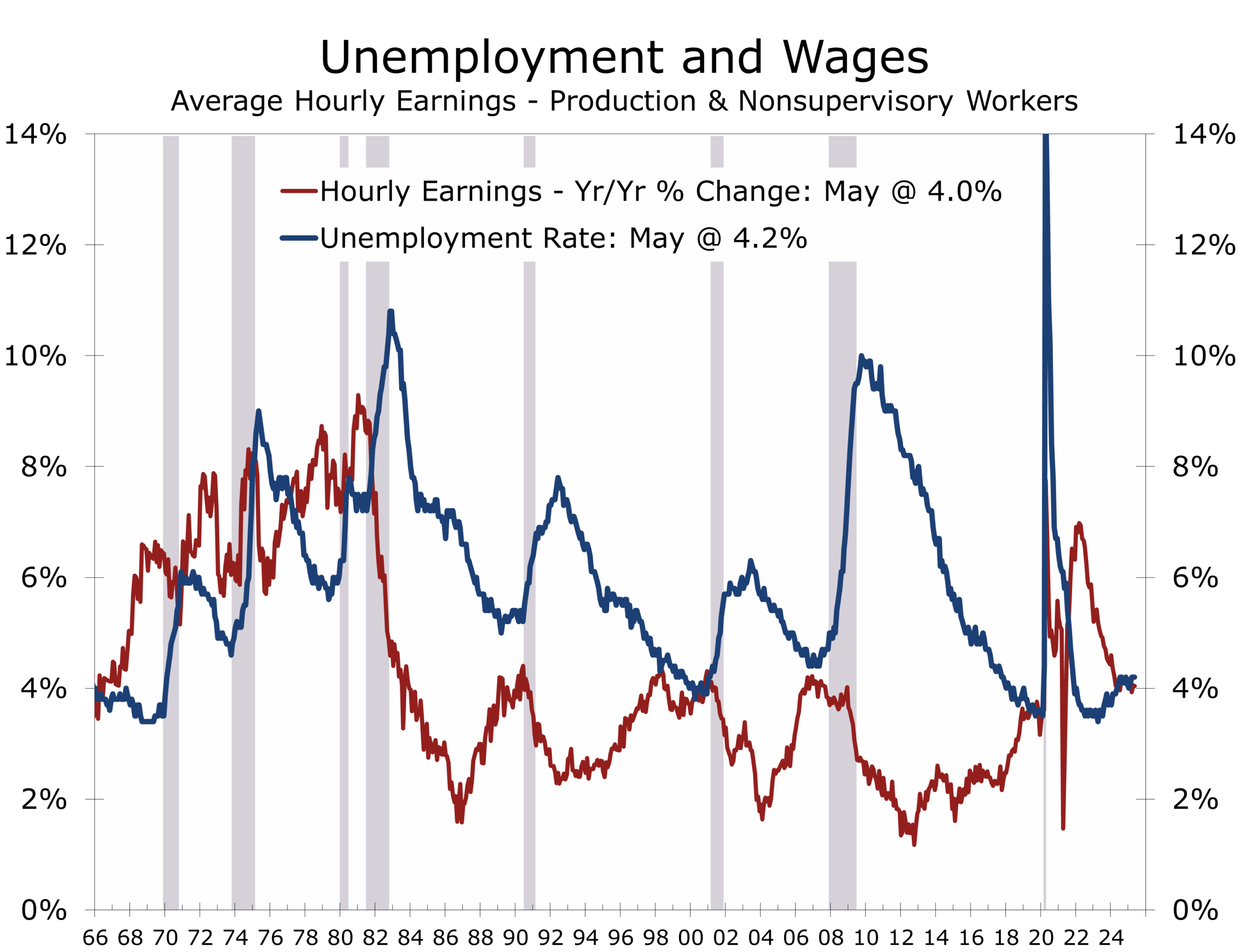

June’s nonfarm payrolls rose by 147,000, with modest upward revisions to April and May. The unemployment rate edged down to 4.1%, but the internals tell a different story. Hiring was concentrated in healthcare, education, and government. Employers have added an average of 150,000 jobs a month for the past three months, with most of that gain coming from healthcare, leisure and hospitality, and state and local government. Separately, the ADP employment measure reported a loss of 33,000 private-sector jobs during June, its first decline in 27 months—driven by a 47,000 drop at firms with fewer than 50 employees.

Even the slower growing nonfarm payroll numbers likely overstate job growth. As we’ve noted repeatedly, the QCEW data, which reflect a count of jobs from unemployment insurance tax rolls, suggest job gains have likely been overstated by around 900,000 jobs. We will get updated data through March 2025 (which is the preliminary source material used for the annual revisions) on September 9, three weeks ahead of the September FOMC Meeting. Another variable to watch is federal employment, which fell again in June and is down 69,000 since January. More declines are likely as retirements pick up, allowing attrition to further reduces staff levels.

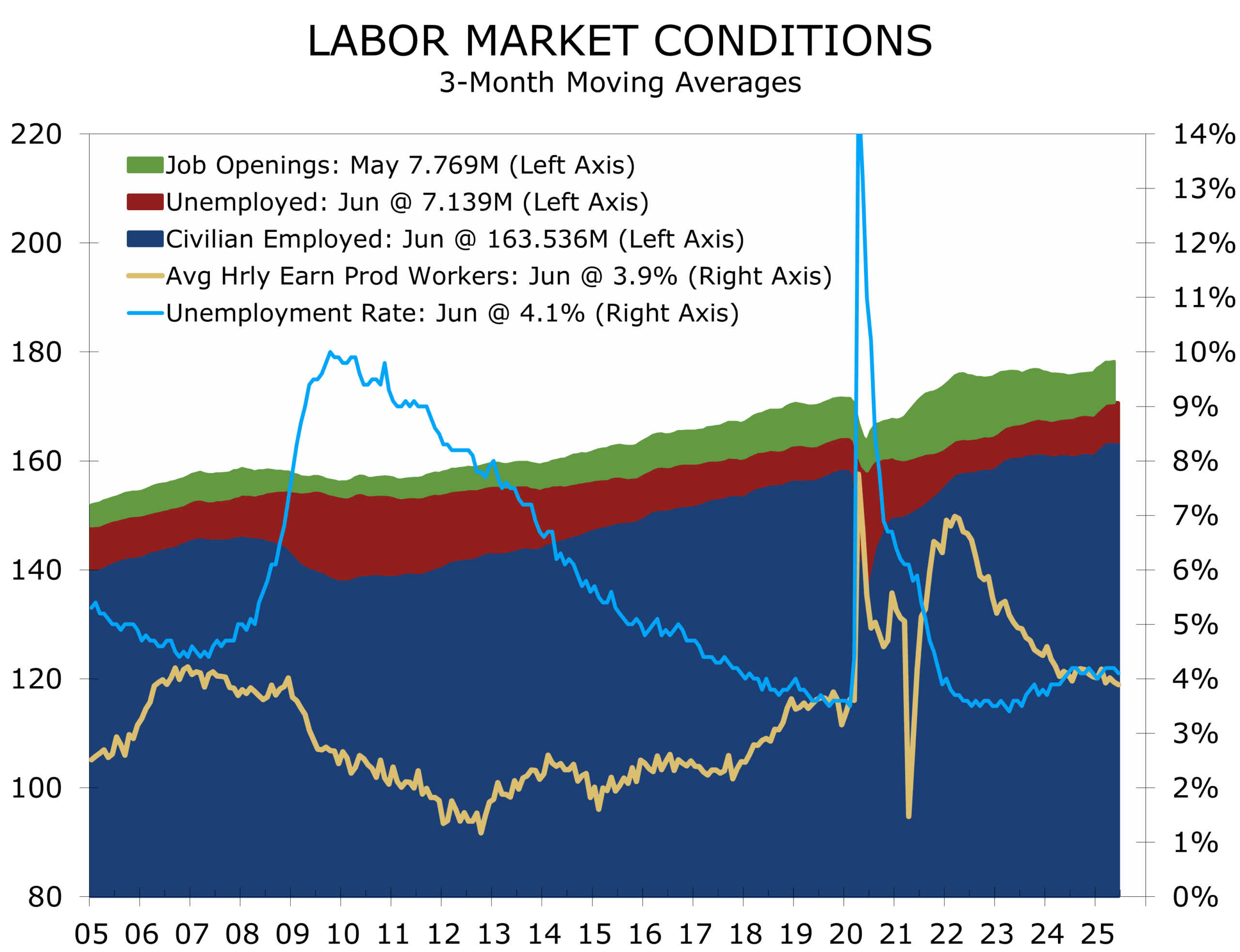

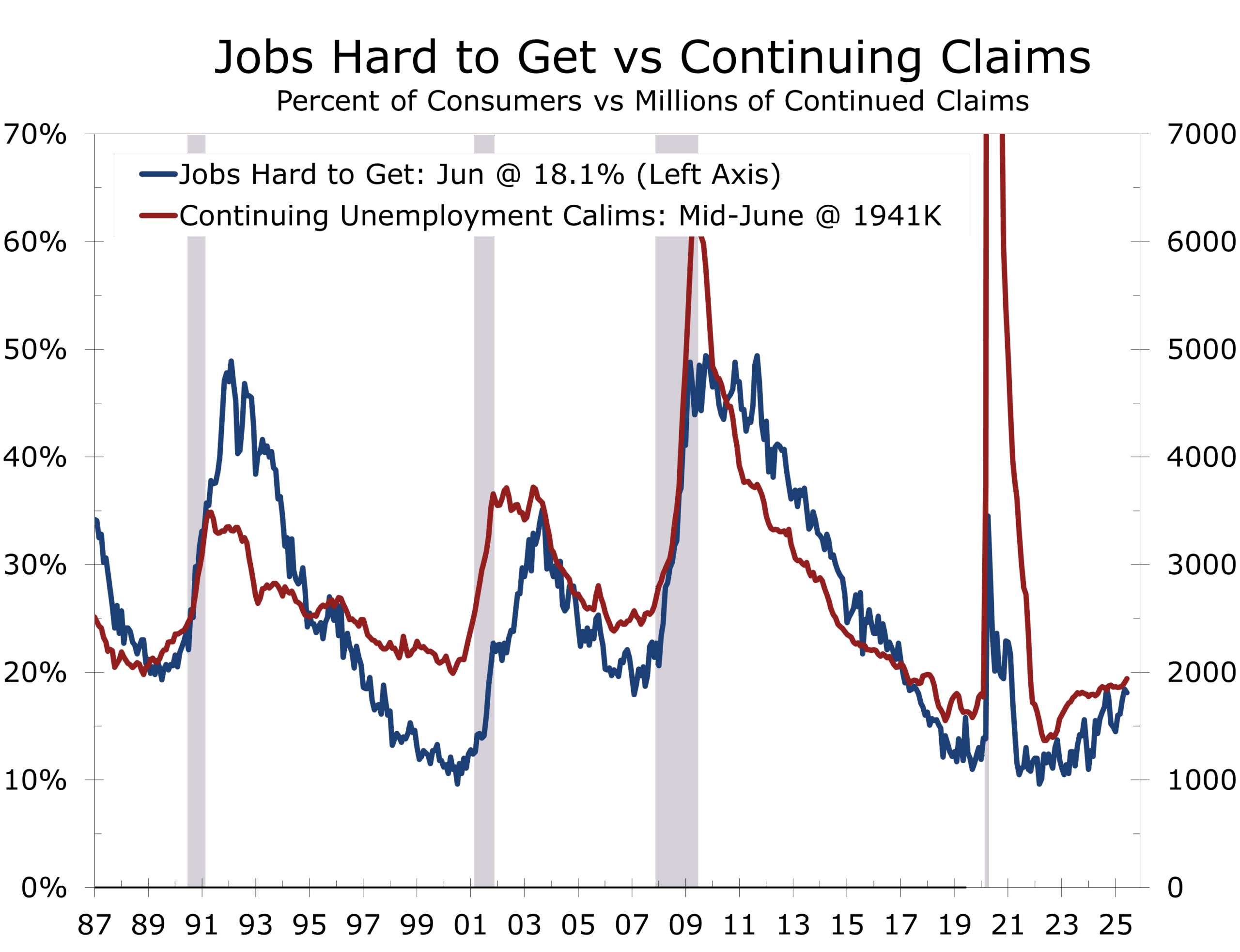

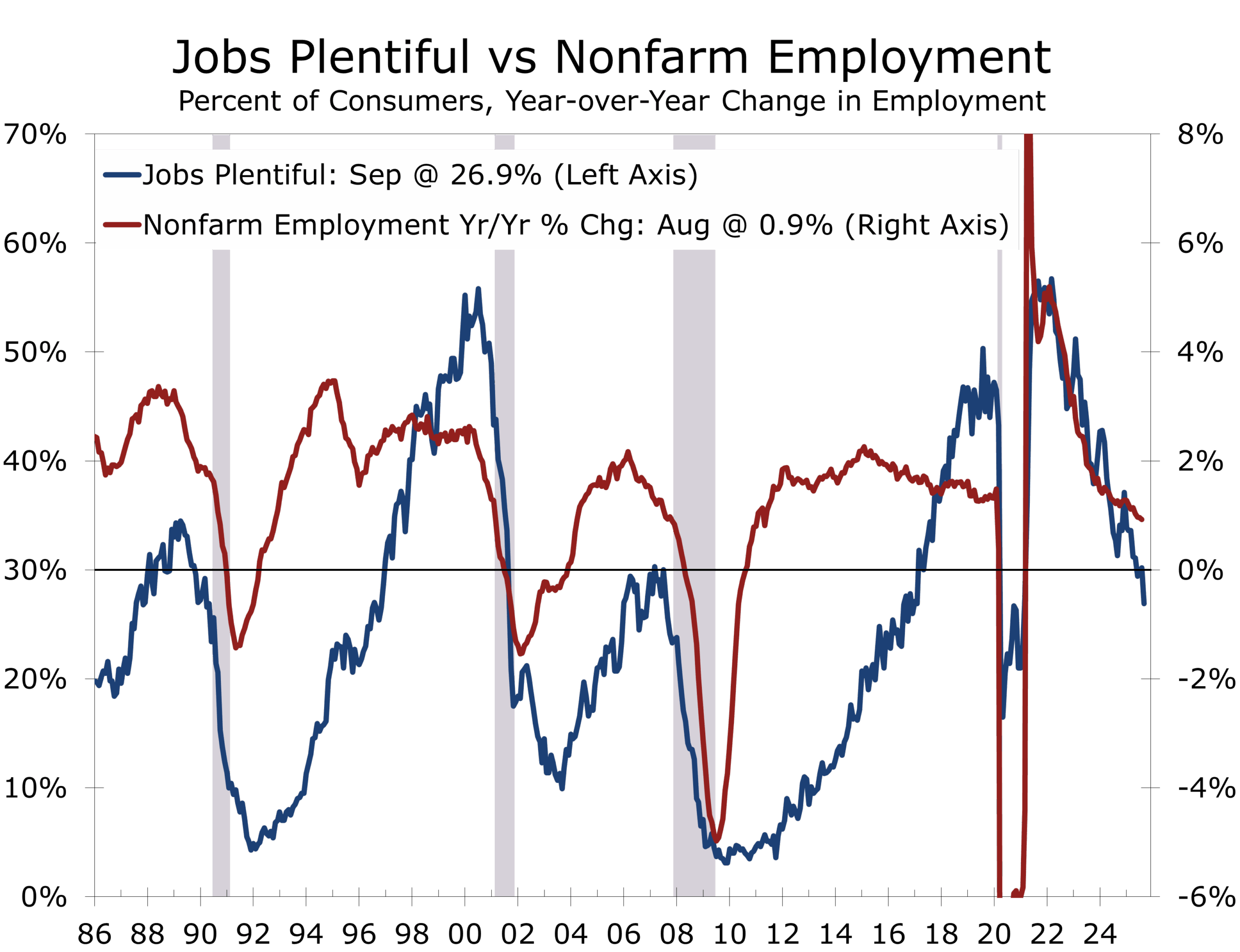

The May JOLTS report showed job openings rising to 7.77 million, but 80% of the gain came from accommodation and food services—likely a seasonal blip or possibly a response to tightening immigration enforcement. Hiring dipped, layoffs remain low and the quits rate remains subdued. With the unemployment rate at 4.1%, it’s hard to argue the labor market is unbalanced—but momentum is clearly fading, as seen in the narrowing breadth of job gains, rising level of continuing claims and dwindling share of consumers stating that jobs are plentiful.

Slowing immigration is weighing on labor force growth and restraining the unemployment rate.

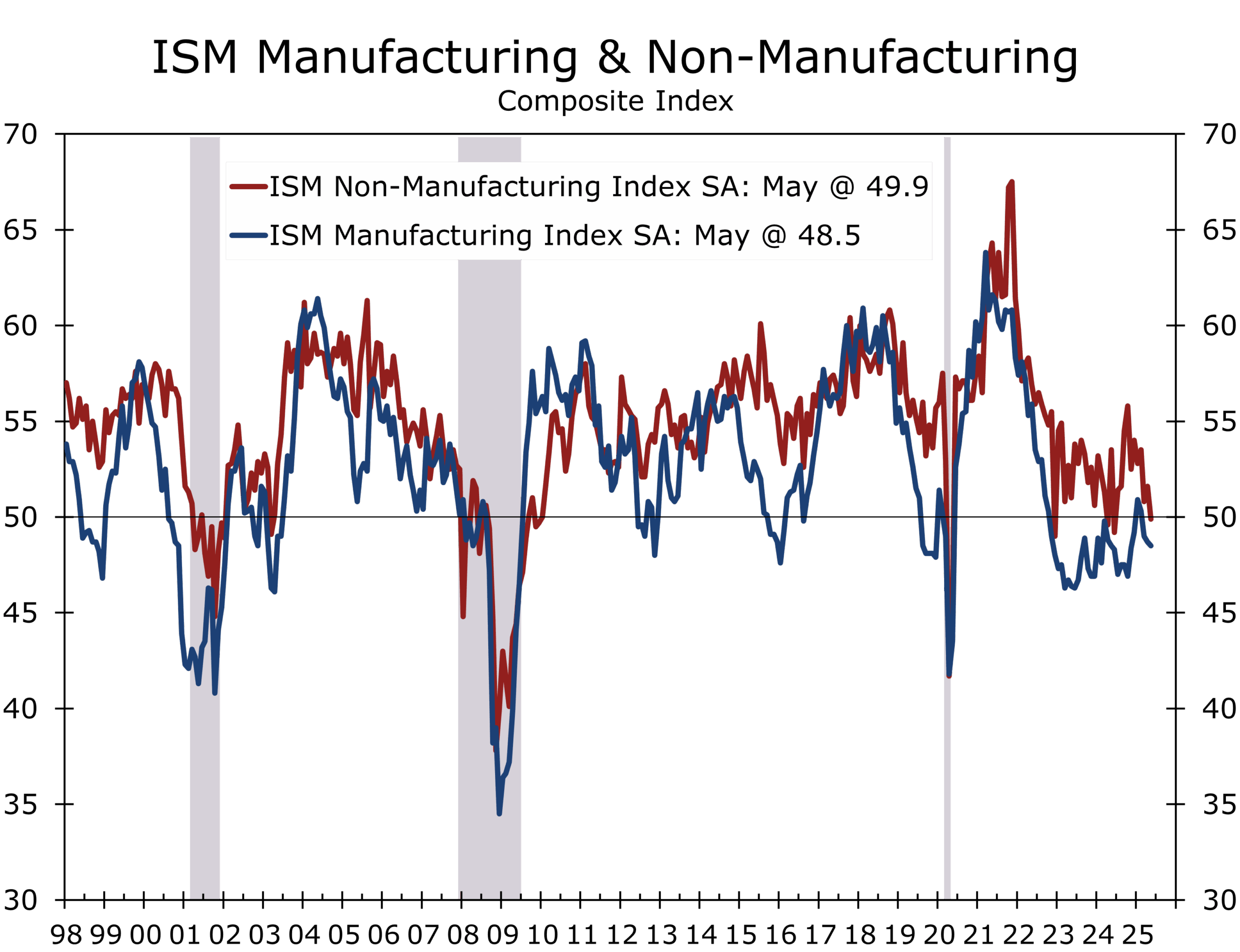

ISM: Stabilization Without Strength

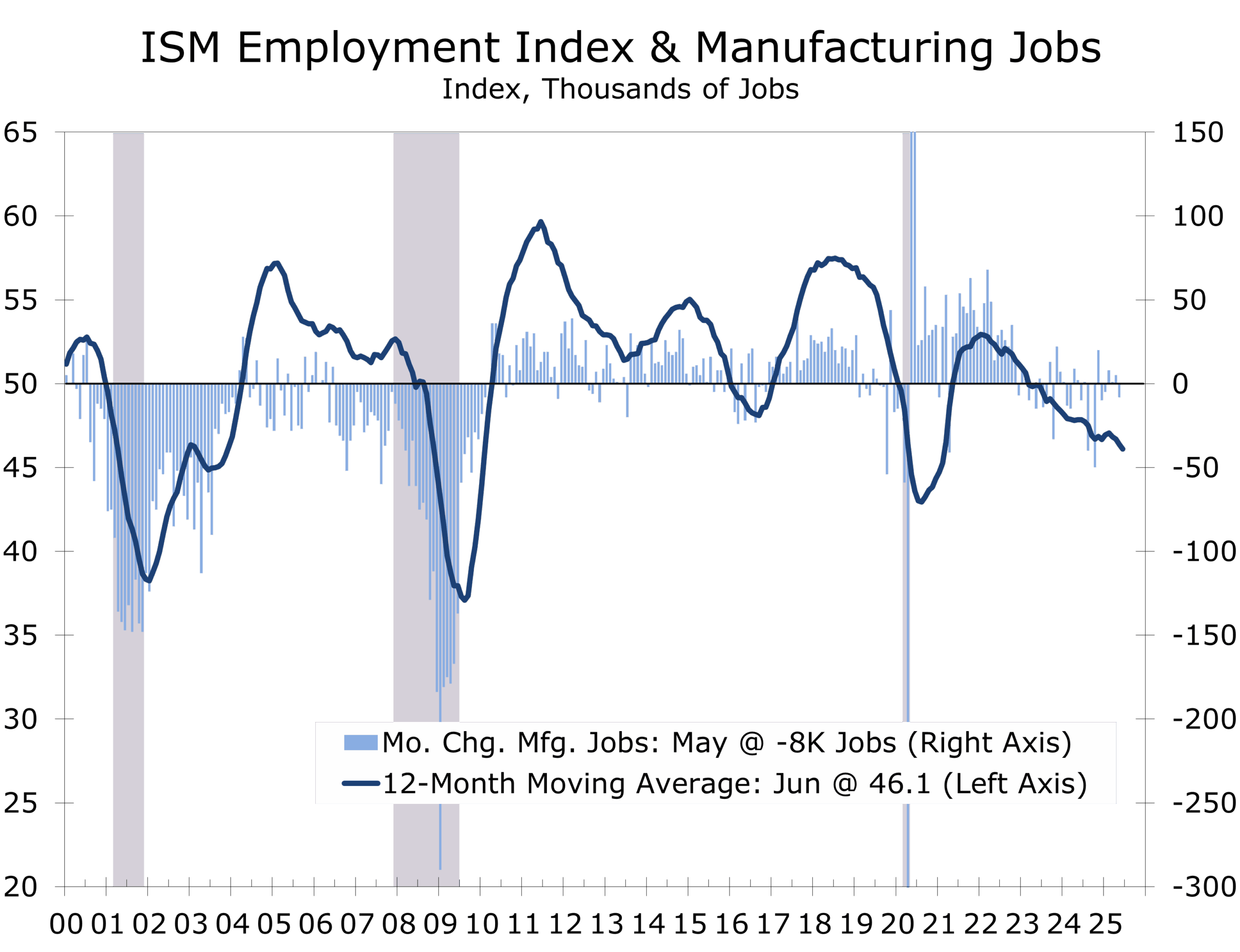

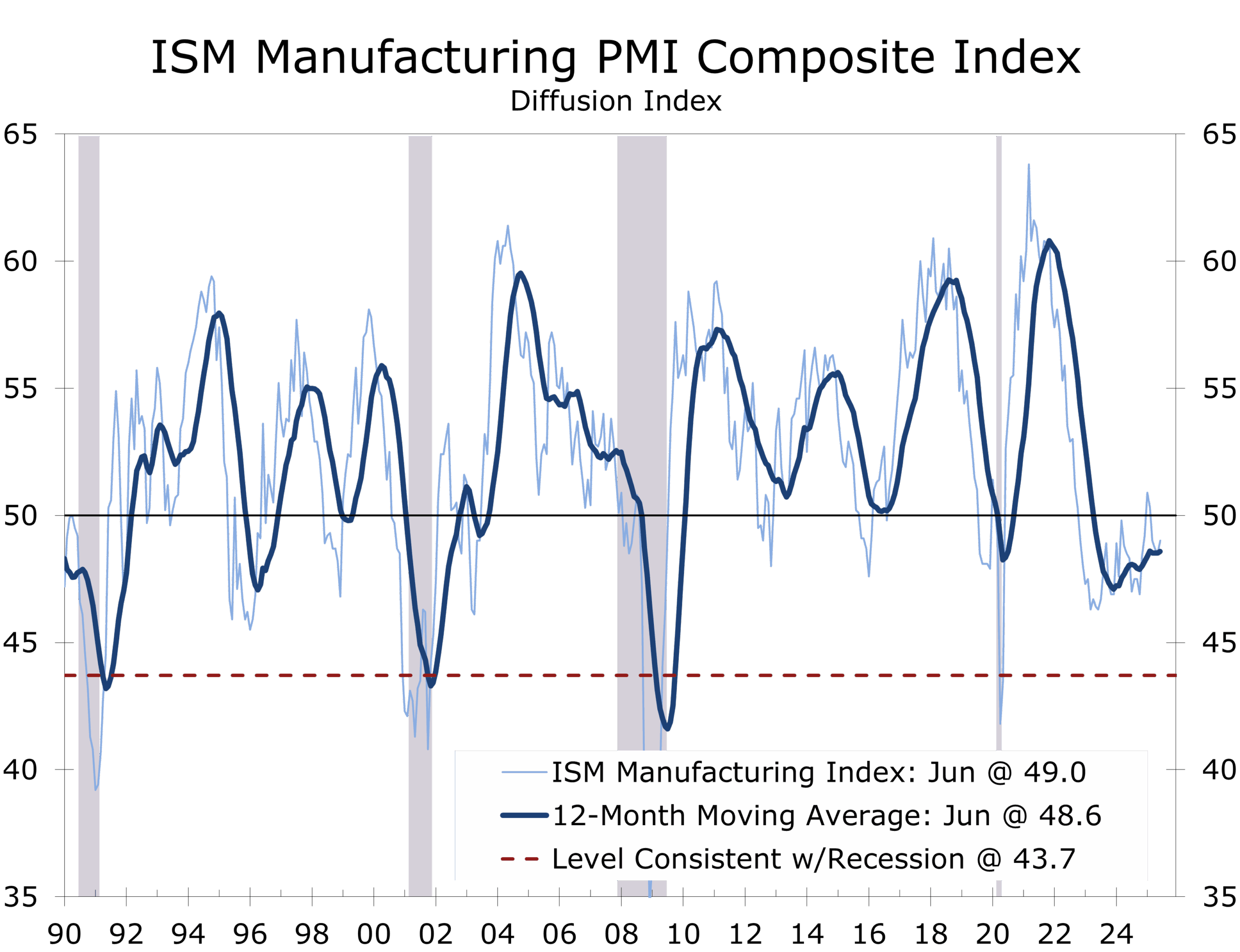

The ISM Services index edged back into expansion at 50.8, while ISM Manufacturing remained just barely in contraction at 49.0. New orders softened to 46.4, while employment fell further to 45.0, with manufacturers trimming staff to cut costs amid margin compression from rising input costs, tepid final demand and tariff-related uncertainty. Production ticked up, but new order backlogs fell, and hiring remains on hold.

The ISM indices are consistent with slower economic growth but not a recession. The Manufacturing Index would need to dip below 43.7 to be consistent with a downturn. Still, the soft recent readings are another sign the economy is losing momentum.

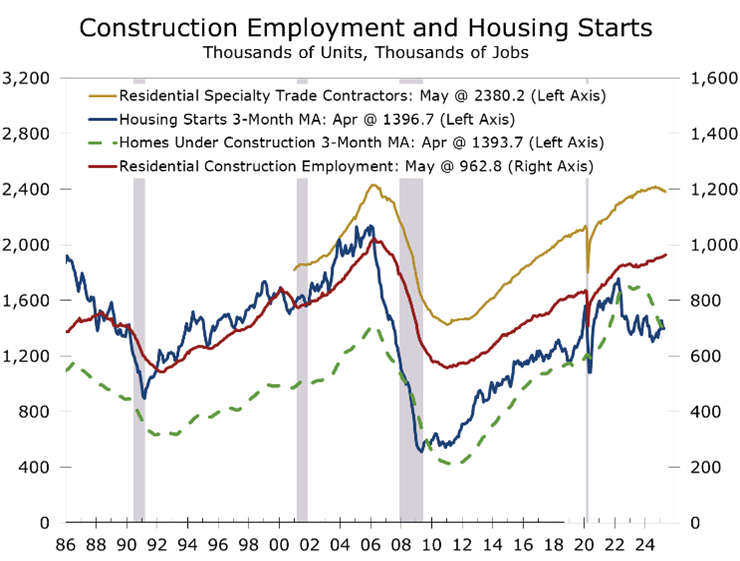

Housing and Nonresidential Construction Weaken

Construction spending declined for the ninth straight month in May. Residential investment is now tracking an 7% annualized decline for Q2, driven by weakness in single-family construction and hesitancy among potential homebuyers. Nonresidential structures are also faltering, with business investment in structures on track to decline at a 5.5% pace in Q2. Data center construction is a bright spot, but factory and power structure investment is retreating, particularly for plants requiring foreign-produced machinery. The tax bill’s levy on China-linked solar and wind projects may further depress green infrastructure spending.

Trade and Tariffs: Trump’s Revenue Engine

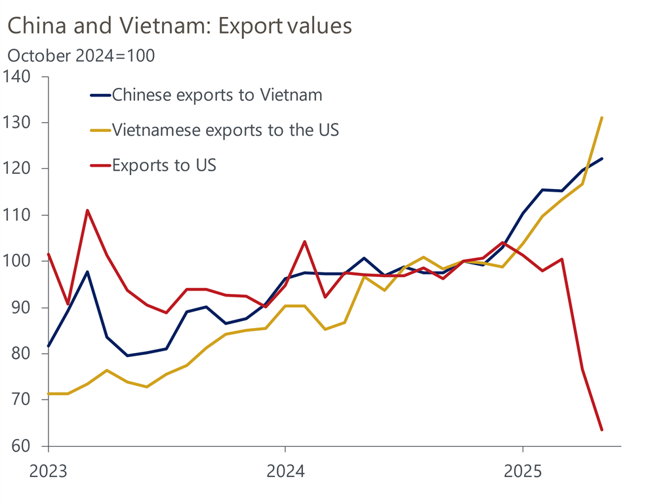

President Trump announced a tariff agreement with Vietnam, reducing U.S. duties from 46% to 20% in exchange for duty-free access for American exports. Goods transshipped through Vietnam—primarily from China—will face a 40% tariff. This follows earlier bilateral deals with China and the U.K.

Vietnam maintains the third largest trade deficit with the U.S. and has become an important destination for manufacturing operations moving out of China due to trade or costs concerns, particularly for shoes, furniture and consumer electronics The 40% tariff goods routed through Vietnam is likely a signal of where Chinese tariffs are ultimately headed, particularly for transshipped products, regardless of which country they are routed through.

Fiscal Dominance and the Dollar

President Trump signed the expanded “One Big Beautiful Bill” into law, potentially increasing annual deficits to $3.3 trillion annually by 2035. The package relies on optimistic scoring and a Treasury pivot to short-term debt issuance. We feel the CBO is underestimating the positive impacts from the budget bill but still see extremely large deficits for as far as the eye can see. Trump is openly pressuring the Fed to lower rates to contain borrowing costs—a potential shift toward fiscal dominance.

Trump continues to pressure Powell to cut rates to spur growth and lower financing cost.

“Fiscal dominance” refers to a regime in which the central bank subordinates monetary policy to fiscal needs, effectively monetizing debt to keep government borrowing costs manageable. It’s not just about buying bonds—it is about the Fed losing the ability to fight inflation independently, cornered by the size of the deficit and rising interest payments.

We are not there yet, but the risks are no longer merely theoretical. The newly signed spending bill adds to an already unsustainable fiscal trajectory, and markets are questioning how long the Fed can keep monetary and fiscal policy in separate lanes. The weakness in the dollar, strength in gold and crypto are all warning signs about the unsustainability of fiscal policy.

Still, today’s Fed is far more independent than in the past—and far less likely to monetize debt outright. The greater risk may be the opposite: that the Fed will delay rate cuts simply to avoid the appearance of political capitulation. That would be a policy error. Inflation is clearly easing, PCE is near 2%, inflation expectations remain anchored or are becoming more so, and the real economy is slowing. Employment growth is narrowing, housing is stagnant, and business investment is losing steam.

In that context, the Fed should cut rates by 75 basis points, starting at the July FOMC meeting. September is more likely—but every delay increases the risk of overtightening into a slowdown already unfolding both above and beneath the surface.

The 1970s taught us what happens when monetary policy caves to political pressure. But that era also reminds us how quickly confidence-driven mistakes can become structural ones—especially when the Fed hesitates at the wrong moment.

Despite surging deficits, bond yields have been volatile, and the dollar has dropped nearly 11% year-to-date. Treasury auctions this week will once again test market demand amid growing concerns about foreign participation.

Mamdani and the Message from New York

Zohran Mamdani’s Democratic primary win in New York highlights rising discontent with establishment economic policy. Mamdani’s socialist platform has drawn comparisons to 1970s India, while his foreign policy stances have drawn criticism for anti-Israel and antisemitic rhetoric. Still, his rise reflects a deeper concern: the economy no longer works for many Americans. The share of national income going to wages has been declining for decades, a trend exacerbated by the rise of China and the erosion of U.S. manufacturing employment.

Both the far right and far left are gaining traction by focusing on pocketbook issues long ignored by the political center—even if many of their proposed solutions are economically incoherent or politically untenable. The underlying sentiment, however, is not to be dismissed: frustration with inequality, affordability, and economic insecurity is driving a new wave of political realignment. The two major political parties should focus on finding practical and meaningful solutions.

Israel: Escalation Avoided, Fragile Progress Continues

President Trump’s Monday meeting with Israeli Prime Minister Benjamin Netanyahu comes as the region shifts from confrontation to cautious diplomacy. A 60-day pause in Gaza fighting is underway, and indirect ceasefire talks between Israel and Hamas have resumed. Iran, weakened by Israel’s systematic destruction of its proxy network and then highly effective U.S. and Israeli airstrikes against its air defenses and nuclear infrastructure, has signaled openness to restarting nuclear negotiations, and the White House has opened quiet channels with Syria’s new government.

Trump hopes to leverage these developments into a broader diplomatic breakthrough—including an expanded Abraham Accords framework. Beyond Saudi Arabia, the administration is exploring the possibility of drawing in Syria and even Lebanon. While politically complex, such moves represent the most ambitious extension of the accords to date.

Meanwhile, an unprecedented initiative in Hebron could test a bottom-up model of Israeli-Palestinian diplomacy. Sheikh Wadee’ al-Jaabari and four other leading tribal figures have signed a letter recognizing Israel as a Jewish state and proposing the formation of an independent Emirate of Hebron. Their plan calls for joining the Abraham Accords, establishing a joint economic zone, and replacing the Oslo-era Palestinian Authority with clan-based leadership grounded in local legitimacy.

The initiative pledges “zero tolerance” for terrorism and outlines a phased labor partnership with Israel. It has been quietly supported by Economy Minister Nir Barkat and has drawn attention from both U.S. and Saudi officials. With the backing of clan leaders representing over 500,000 Hebron-area residents, the proposal could serve as a test case for a decentralized, pragmatic approach to governance. While the sheikhs’ plan represents a sharp departure from the stagnant Oslo framework, its success will depend on both political will and regional coordination.

A broader Middle East peace deal would have substantial carry through to other parts of the globe and would be a positive for global financial markets and U.S. leadership. Russia and China have used the Middle East conflict to tie the U.S. up and weaken support throughout developing countries. Without this wedge, more progress will be possible elsewhere.

Volatility Retreats, But Uncertainty Lingers

Despite economic crosscurrents, global business and financial markets do not appear overly anxious. Business sentiment surveys show muted concern, and the market-implied probability of severe outcomes (like a U.S. recession or a 20% drop in equities) has declined. Implied volatility in currency markets has also fallen, providing some stability following a long slide in the value of the dollar. Treasury yields have also fallen back off their recent highs, despite heightened concerns about persistent large budget deficits. Expectations for Fed rate cuts have also increased, with the markets currently pricing in between 3 and 4 quarter point cuts by the middle of next year, with kickoff coming in September.

Looking Ahead: Week of July 8–12

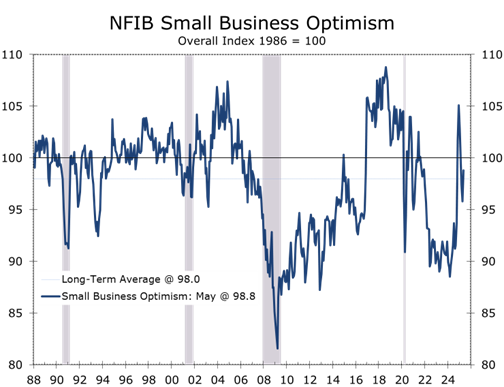

- NFIB Small Business Optimism (Tuesday, July 8): We are looking for a modest rise in the NFIB index, as easing geopolitical pressures and recent financial market stability boost expectations.

- Tariff Deadline (Wednesday, July 9): President Trump is expected to send ‘letters’ to countries without finalized deals. Watch for additional announcements on BRICS-aligned penalties.

- FOMC Minutes (Wednesday, July 9): Look for confirmation of the Fed’s cautious tone and insight into members’ views on tariffs and labor slack.

- Jobless Claims (Thursday, July 10): Jobless claims remain exceptionally low going into a seasonally volatile period for claims that could see initial claims move lower. Continued claims, however, continue to trend higher, reflecting a tougher market for job seekers.

- Treasury Auctions: 3-, 10-, and 30-year bond sales may test market tolerance for ballooning debt.

Final Thought: A Delicate Balance

Markets may be rallying, but the fundamentals are drifting. Hiring is slowing, margins are compressed, the Fed remains boxed in, and global trade rebalancing is still underway. Yet geopolitical risks have eased—at least temporarily—and fiscal stimulus is flowing. The second half of 2025 will be a test of execution. The pieces are now coming into place such that a modest, well-timed interest rate cut could set the stage for a resurgence in growth next year. Policymakers must stay disciplined until the inflation threat fully recedes.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 8, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

A Softer Report Behind the Headline Relief

Hiring Remains Soft, As Job Gains Narrow

- Nonfarm payrolls rose by 147,000 in June, narrowly above the revised May figure of 144,000 and in line with the 12-month average of 146,000.

- The unemployment rate ticked down to 4.1%, but underlying slack continues to build, with long-term unemployment and marginal labor force attachment both rising.

- Headline strength masked concentration: state and local government, health care, and social services accounted for nearly all of June’s job gains.

- Federal payrolls declined again, bringing cumulative losses to 69,000 since January.

- Construction added jobs, but only in specialty trade contractors—typically late-cycle hires—suggesting project backlogs are being completed, not expanded.

- Tech-related hiring remained flat, with no net gains in professional and technical services or the information sector—further evidence of AI-driven disruption and cautious budgeting.

- Financial markets were surprised by the stronger-than-expected headline, but the soft internals justify the Fed’s cautious stance and leave the July cut discussion on the table. We still expect the Fed to kickoff the next round of rate cuts in September.

Jobs Report: Nowhere Near as Strong as the Headline

The June employment report delivered a superficially strong headline—nonfarm payrolls rose 147,000, and the unemployment rate edged down to 4.1%—but the underlying data tell a more fragile story. Hiring continues to slow, with gains increasingly dependent on just a few sectors. The three-month average now stands at 143,000, and job gains were narrowly concentrated in public education, health care, and social assistance. These sectors added over 120,000 jobs combined, while most other areas—including retail, manufacturing, transportation, and finance—were effectively flat.

Federal employment fell another 7,000 and is down 69,000 cumulatively since January. While court rulings have temporarily halted some layoffs, voluntary quits, and retirements continue to chip away at headcount. The public sector’s strength lies entirely with state and local governments, particularly in education (65.5K).

Job growth is dependent on just a handful of sectors, as hiring remains largely on hold.

Construction saw a moderate increase, but all gains were in specialty trade contractors—workers typically hired at the tail end of building projects. Combined with softer construction spending and housing starts, this points to waning momentum and fewer new projects entering the pipeline.

Tech-related hiring remains under pressure, with IT services shedding 9,700 jobs in June. The AI-driven transformation, combined with ongoing cost discipline, continues to suppress hiring—particularly in white-collar roles. Unemployment is rising for programmers. Despite the productivity narrative, the headcount story remains defensive, as firms reassess staffing under mounting pressure to demonstrate returns on AI investment.

Despite booming equity values, high tech firms are continuing to reduce head count.

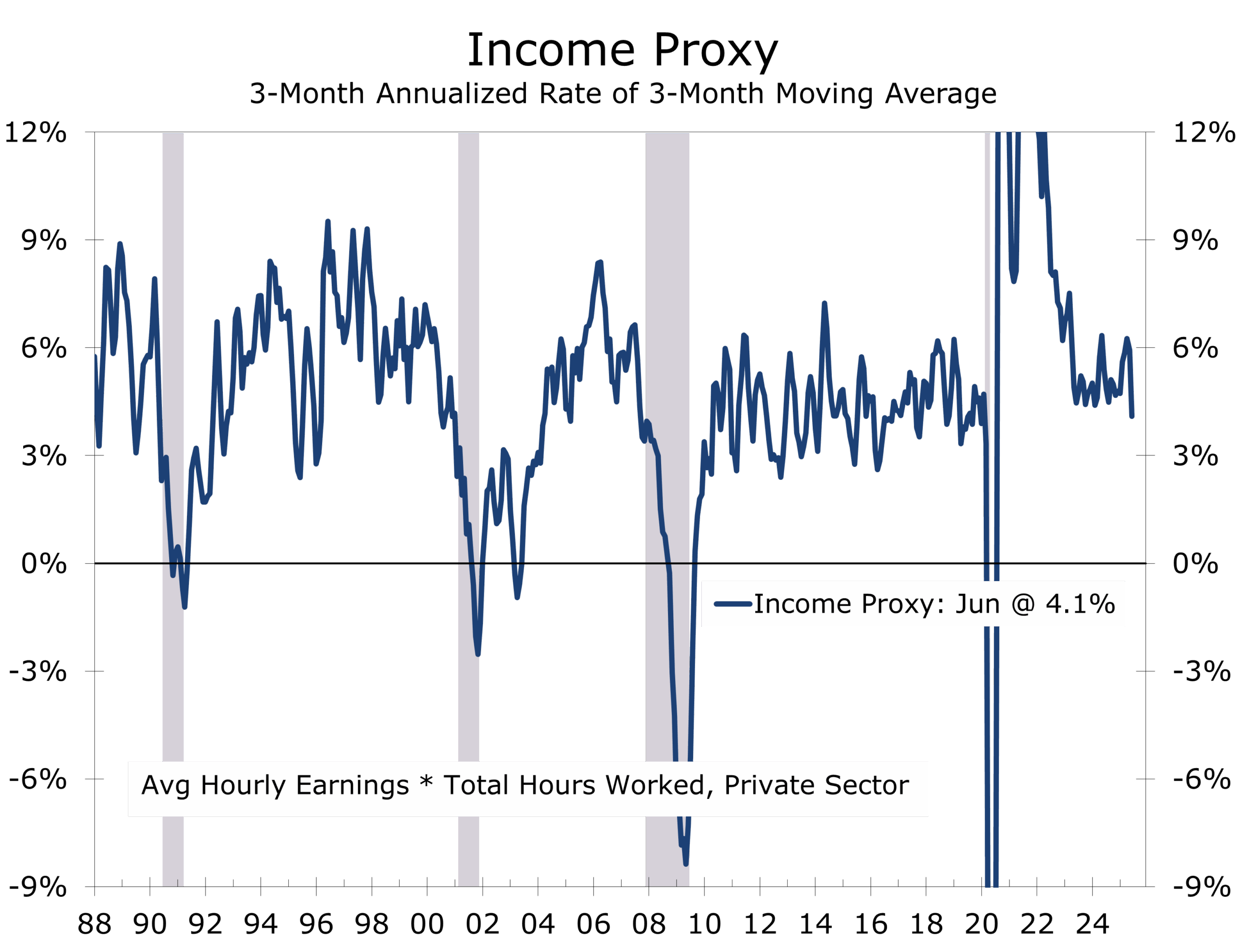

Elsewhere, job growth was notably absent. The diffusion index dropped back below the key 50 break-even level. Wage growth also cooled noticeably. Average hourly earnings rose just 0.2% in June, down from 0.4% in May. On a year-over-year basis, wages rose 3.7%, decelerating from 3.9%. The average workweek slipped to 34.2 hours. Together, this data points to softening labor demand, lower aggregate income gains and cautious consumer spending. Our income proxy has slowed just a 4.1% annual rate.

The underlying data are consistent with the market’s expectation for a weaker report. Businesses are not slashing payrolls; they are just reluctant to add to staff. The Conference Board’s measure of job availability has continued to weaken. While JOLTS job posting rose in May, hiring managers are clearly being more selective.

Markets briefly reacted to the stronger headline print, but internals quickly tempered the response. The Fed is likely to remain on hold in July, albeit with a less hawkish tone. Decelerating wages, flat private hiring, and rising slack strengthen the case for a rate cut later this summer, particularly if tariff risks, final demand, and global tensions continue to ease.

Tariffs—and the reluctance to appear politically influenced—continue to cloud the Fed’s decision.

FOMC Implications – July Rate Cut Talk Still in Play

June’s report reinforces the Fed’s wait-and-see stance. A strong headline justifies holding in July, but soft internals—slower wage growth, narrowing job gains, and rising long-term unemployment—keep a summer cut in play. With inflation subdued but tariffs still fueling inflation expectations, the bar for easing is high but increasingly within reach. The most likely kickoff remains the September FOMC meeting.

The labor market is not yet unraveling, but it is leaning harder on government and care-sector hiring. Private sector hiring largely remains on hold, while state and local governments and government-adjacent sectors continue to add staff. As H2 2025 begins, this narrow foundation limits upside surprises and reinforces a cautious policy bias.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 3, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

704-458-4000

Manufacturing Holds Just Below Expansion in June, With Cost Pressures Rising

Manufacturing Cools but Remains Resilient

- The ISM Manufacturing PMI rose slightly to 49.0 in June, marking its fourth straight month below 50 but showing continued stabilization.

- New orders softened to 46.4, pointing to ongoing weakness in underlying demand.

- Production ticked up to 50.3, just above breakeven, driven by easing supply chain bottlenecks.

- Employment fell to 45.0 as firms remain cautious about hiring and leave positions open to help curb costs.

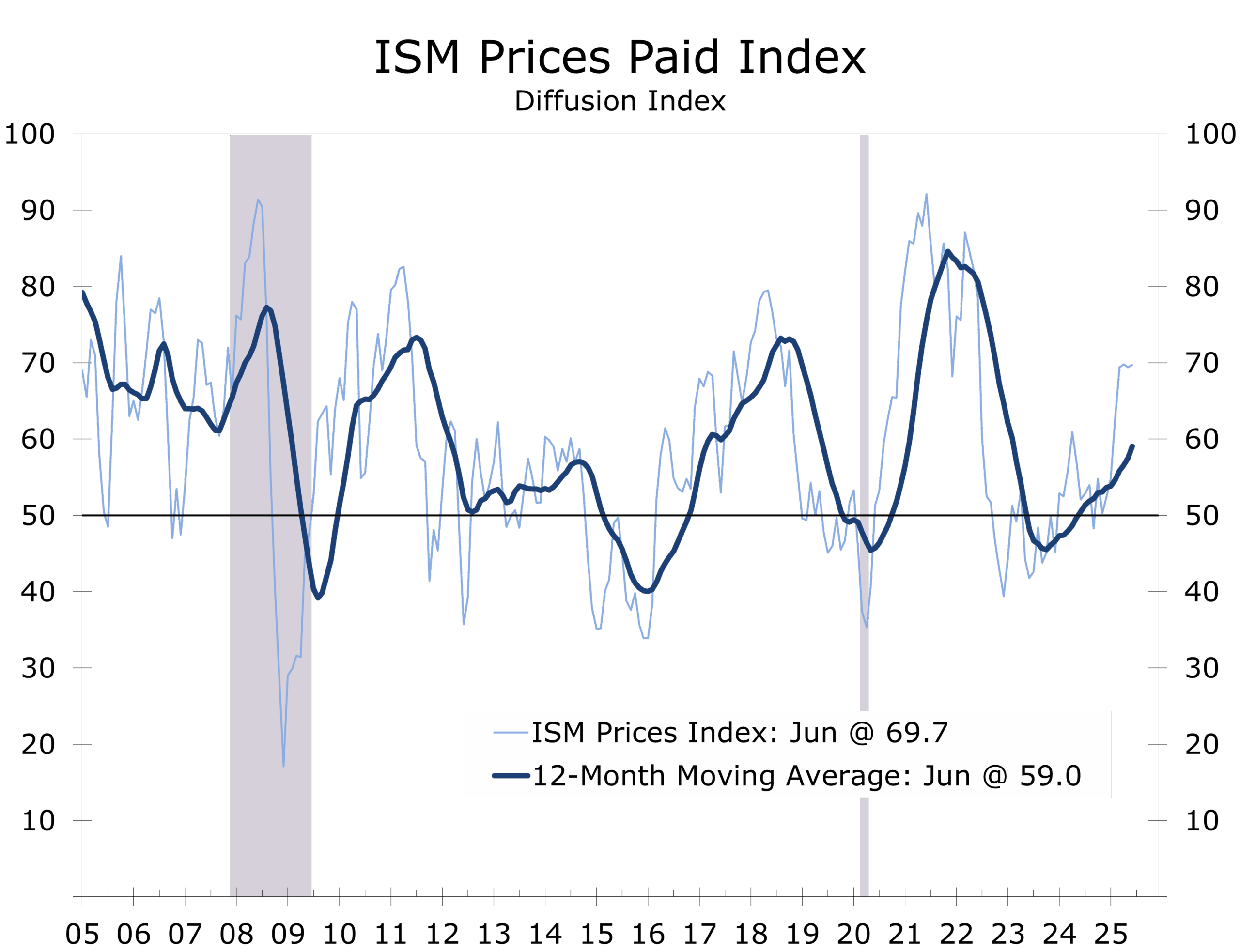

- Prices paid rose to 69.7, reflecting intensifying input cost pressures.

- Alan Greenspan once called the ISM his favorite economic indicator, praising its timeliness and ability to capture cyclical inflection points. The latest reading suggests we are not yet at such a juncture, and the Fed can afford to wait for greater clarity on the evolving tariff landscape and fiscal policy mix. While still soft, the PMI remains closer to expansion territory (50+) than to levels typically associated with recession (43.7 or lower).

Modest Uptick Masks Crosscurrents Beneath the Surface

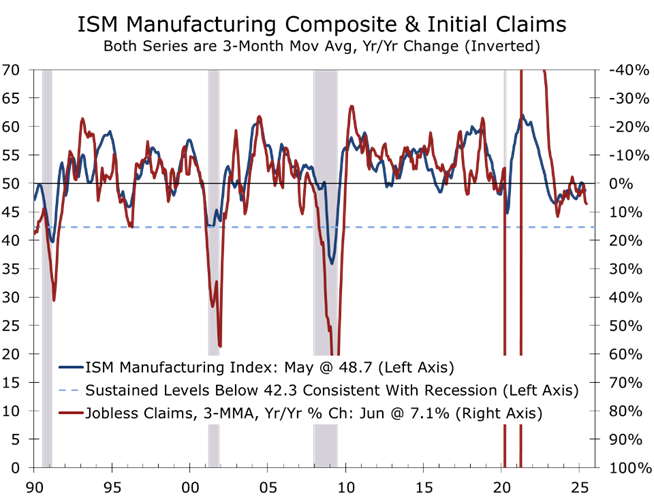

As we expected, the ISM Manufacturing Index remained just below the key 50-breakeven level in June, rising to 49.0 from 48.5 in May. As a diffusion index, the ISM measures the breadth of change rather than magnitude—so while more firms reported weakening conditions than improving, the reading remains well above the 43.7 mark that historically signals a broad-based recession.

Production rose for a second straight month and eked into expansion territory, reflecting slightly better delivery times and inventory normalization. Businesses are holding off major commitments but with lean customer inventories and solid order backlogs, production should hold up reasonably well. The resilience in production, however, was offset by a decline in new orders, which fell 1.2 points to 46.4—marking a renewed pullback in forward demand.

The employment index slipped to 45.0, indicating increased hesitation among firms to bring on new staff. Most survey respondents noted they are controlling costs via hiring freezes and reduced overtime, rather than mass layoffs. That aligns with broader labor market trends: manufacturing job growth is flat, but layoffs remain contained. The latest JOLTS data show 414,000 job openings in manufacturing as of May, which is up slightly from April but down from 576,000 openings a year ago.

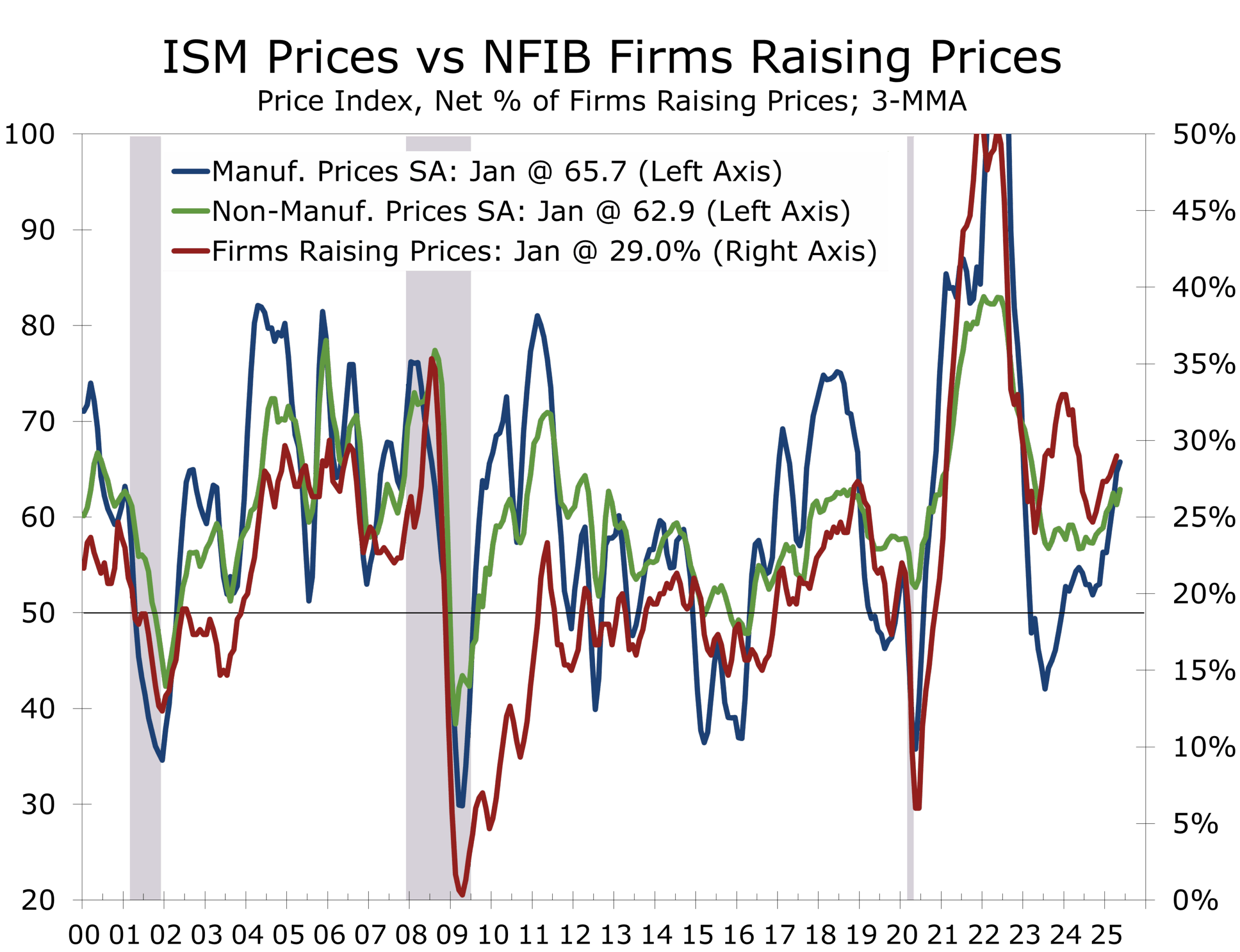

Tariffs Recede, But Price Pressures Reemerge

The headline narrative has shifted from tariffs to margin pressure. With input costs rising and end demand soft, many firms find themselves caught in a vice. Prices Paid rose 0.3 points to 69.7—driven by higher metals, chemicals, and shipping costs—while supplier delivery times increased slightly, complicating production planning. The Prices Index has increased 17.2 percentage points over the past six months, with the past three months readings marking the index’s highest since June 2022

Fading tariff concerns in the financial markets have not brought relief to manufacturers. Survey comments indicate that sourcing frictions and price mismatches persist, especially for intermediate goods. Manufacturers are facing a tougher environment for passing through price increases, with customer resistance growing amid slower final demand. Geopolitical uncertainty has also stifled demand overseas.

Trade and Inventory Signals Remain Mixed

Export orders rose 6.2 points to 46.3, benefitting from recent reprieves on tariffs with major trading companies. Companies are still awaiting greater clarity on trade deals, which we expect to see in the second half of this year. Imports edged down, partly due to deliberate efforts to trim inventory risk. Customer inventories rose 2.2 points by remain in relatively good shape at 46.7, suggesting some room for future restocking if demand firms and tariff uncertainty gives way more rapidly. Backlogs continue to decline, falling 2.8 points to 44.3, reflecting a softening production pipeline, which will keep managers cautious.

Outlook & Policy Implications

The June report confirms that manufacturing remains in a cautious holding pattern. Businesses are navigating a complex mix of excruciating slowly fading tariff threats, resurfacing cost pressures, and lackluster demand. That triple squeeze is forcing firms to cut costs, delay hiring, and tighten capex plans.

For policymakers, the ISM data signal ongoing fragility rather than crisis. Factory activity is soft, but not recessionary. The Fed is likely to interpret this as another argument for patience—watching how pricing power and demand evolve in the second half of the year before cutting rates. We still expect the next cut to come in September and now expect successive quarter point cuts at the three meetings afterward.

Former Fed Chair Alan Greenspan once said the ISM “tells you where the turning points are,” and right now, the signal is: we are not there yet. The squeeze manufacturers are dealing with is painful but is also the reason why higher import prices have not spilled more forcefully over into consumer prices. We expect to see a little more spillover this summer but look for slower economic growth to limit inflation and for lower interest rates, trade deals and tax incentives for capital spending to drive growth in the spring and summer of next year.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 1, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

704-458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Hawks, Doves, Dealmakers and Skeptics

Highlights of the Week

- The U.S. economy shows signs of slowing beneath the surface: consumer spending, housing, and employment have softened, while a spike in aircraft orders drove a jump in durable goods orders.

- Consumer Sentiment rebounded on easing tariff fears and market gains, while Consumer Confidence slipped amid diminished hiring.

- Core PCE inflation is tracking below 3%, strengthening expectations for a rate cut.

- The U.S. and Israel dealt a strategic blow to Iran’s nuclear infrastructure in a coordinated air campaign, significantly degrading Iran’s enrichment capabilities and command structure.

- Trump’s influence is growing across foreign policy, trade, and fiscal negotiations, as G7 nations recalibrate and momentum builds to end the Gaza War and expand the Abraham Accords.

- The NATO summit marked a dramatic political win for Donald Trump, securing European pledges to raise defense spending to 5% of GDP.

- The financial markets are taking note of the improved economic and geopolitical trend, sending share prices to new highs.

Beneath the Resilience, a Slowing Core

Economic data for the week offered a mixed view: on the surface, business investment and durable goods orders showed surprising strength, but underlying demand is softer than earlier thought and many key measures are flashing warning signals.

Real consumer spending was flat in May, with a downward revision to April. The details were more concerning: services spending fell outright, and goods spending gains came from volatile durables, not essentials. Real disposable income is running below 2% year-over-year, even as the savings rate edges higher — a sign tariffs and broader geopolitical, fiscal and labor market risks weighed on consumer behavior this past spring.

After pulling big-ticket purchases forward ahead of tariffs, consumer spending has moderated.

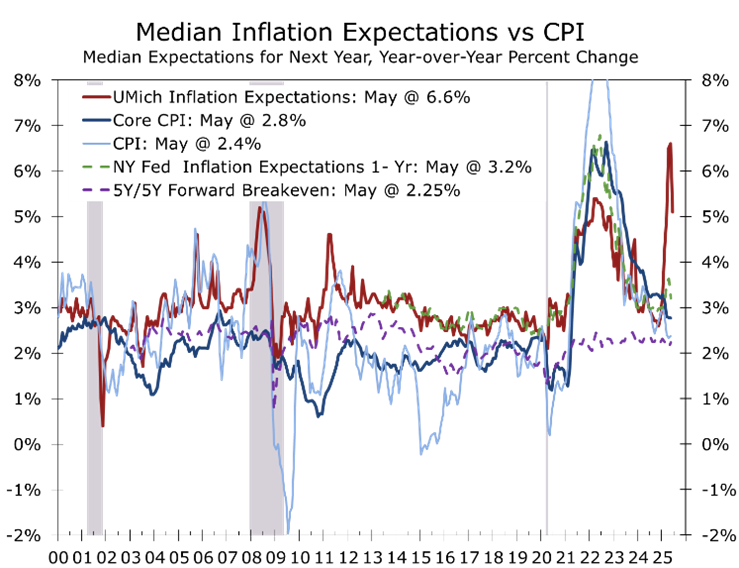

Consumer sentiment rebounded in June, following six consecutive months of declines. The index was revised higher to 60.7, up 8.5 points or 16% from May, as easing tariff pressures, falling energy prices and rebounding share prices bolstered household finances. Notably, high-income households reported the largest improvement in buying conditions for durable goods. Moreover, the absence of a tariff-induced price surge is improving consumer psyche. Year-ahead inflation expectations fell to 5.0% — still elevated but down significantly from May’s 6.6%.

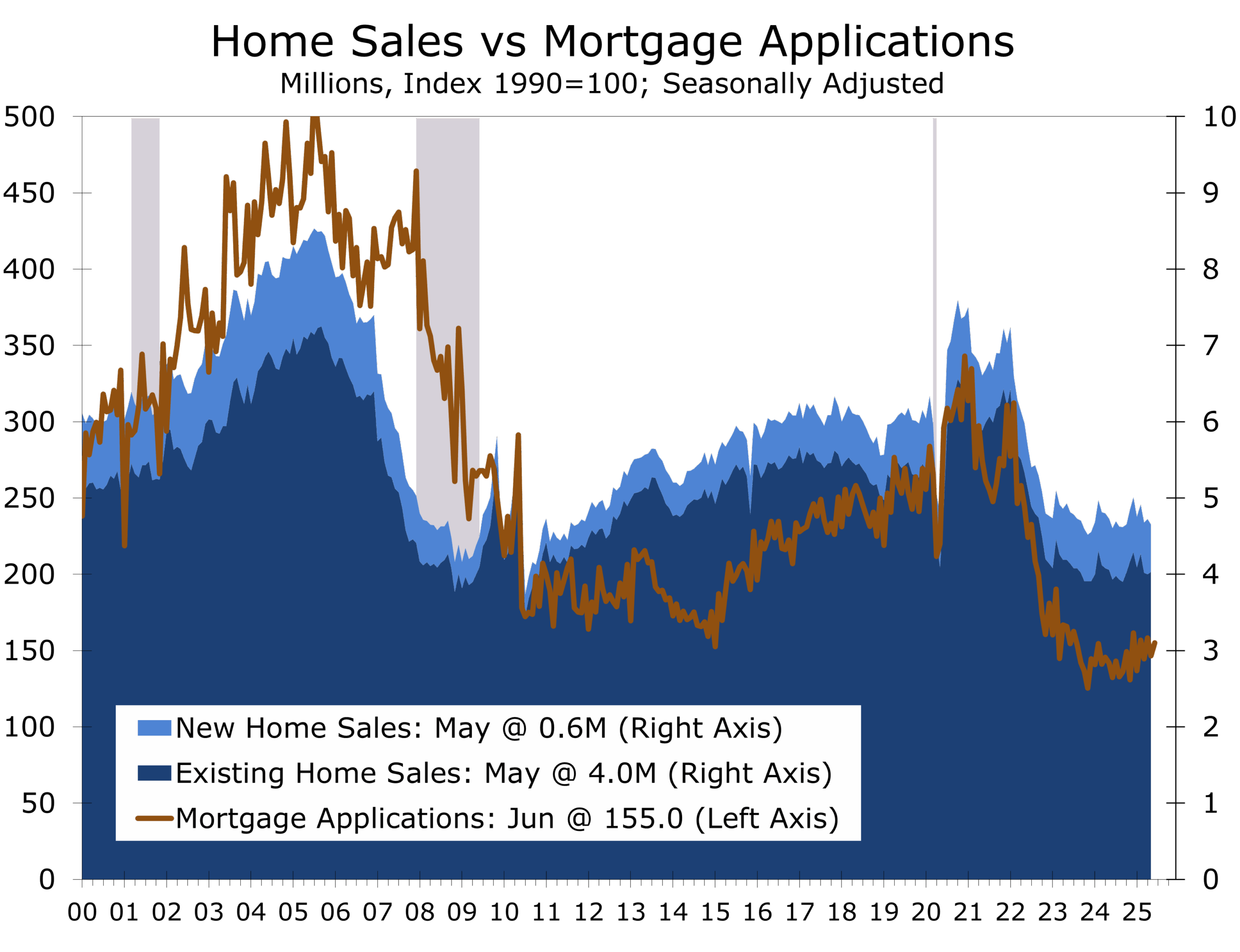

Pending home sales rebounded in May but only partially offset April’s decline. Mortgage rates hovered near 7%, and affordability challenges continue to weigh on demand, especially in the resale market. New home sales also fell, dropping 13.7% to a 623,000-unit pace — the slowest since October 2024 — despite generous builder incentives.

The slowdown in home buying is rebalancing the housing market, with sellers now outnumbering buyers in many areas. Existing home inventory has risen to a 4.4-month supply, while new home inventory has climbed to 9.8 months at May’s pace. This added supply is pressuring prices: the median existing home price is up just 1.7% year-over-year, and new home prices, though higher in May, are down 1.9% on a three-month average.

A surge in commercial aircraft orders sent factory orders soaring in May.

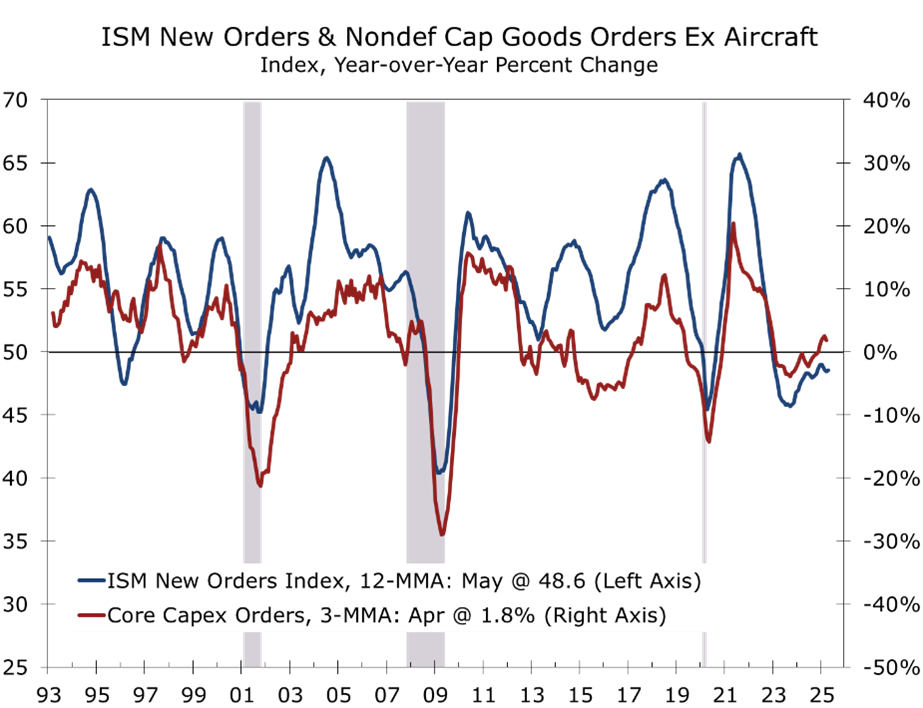

Durable goods orders surged 16.4% in May, the largest increase in over a decade, driven almost entirely by a 230% spike in commercial aircraft following a major Boeing deal with Qatar. Excluding transportation, orders rose a more modest 0.5%, with broad-based gains led by computers, electrical equipment, and fabricated metals. Core capital goods shipments — the key input for GDP business investment — also rose 0.5%, raising expectations for Q2 growth.

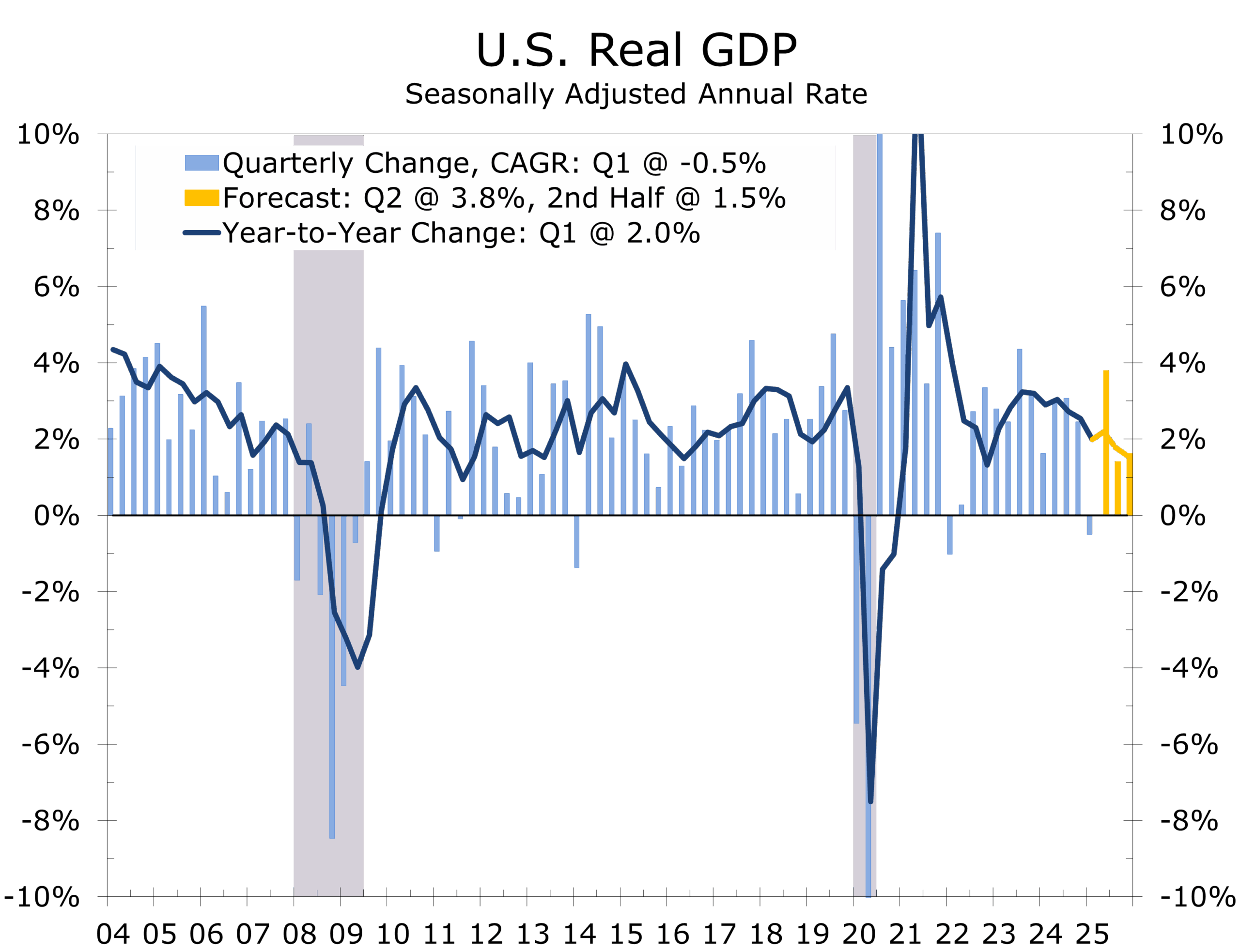

Revised GDP data revealed that Q1 growth was even weaker than previously reported. Headline growth was downgraded to a -0.5% annualized pace, as downward revisions to consumer spending and inventories outweighed a modest upside in net exports. More importantly, real final sales to domestic purchasers — a key gauge of underlying demand — rose just 1.9%, the slowest pace in over two years. Nonetheless, our internal tracking model still estimates Q2 GDP growth at 3.8%, supported by resilient consumer spending and business investment in capital equipment.

Awaiting Clarity on the Labor Market and Inflation

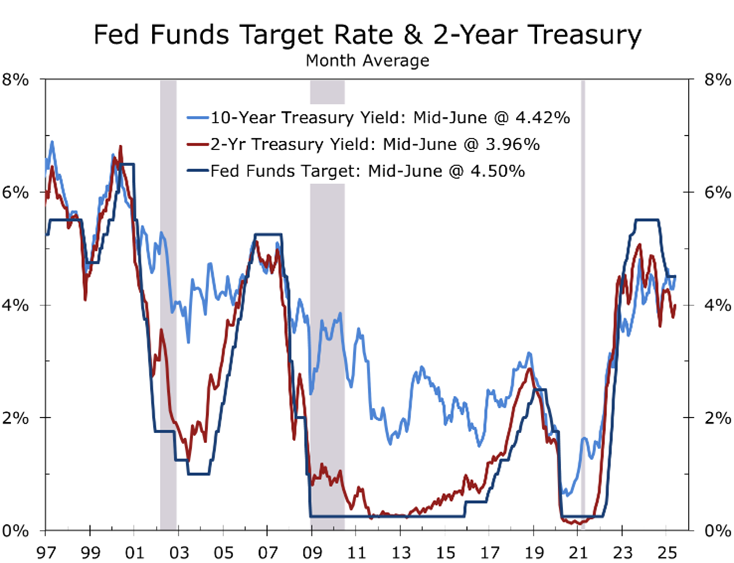

Powell reiterated in his congressional testimony that the Fed is “well positioned to wait.” The June SEP projections imply two cuts in 2025, but the dot plot reflects a wider divergence in view. September remains the most likely time for the next Fed move.

The labor market continues to lose momentum. While initial jobless claims declined modestly in the latest week, continuing claims — a better gauge of trend softness — rose again, hitting the highest level since November 2021. The rise in continuing claims suggest job seekers are having a harder time landing a new job and matches the climb in the share of consumers stating that jobs are hard to get in the Conference Board’s Consumer Confidence survey.

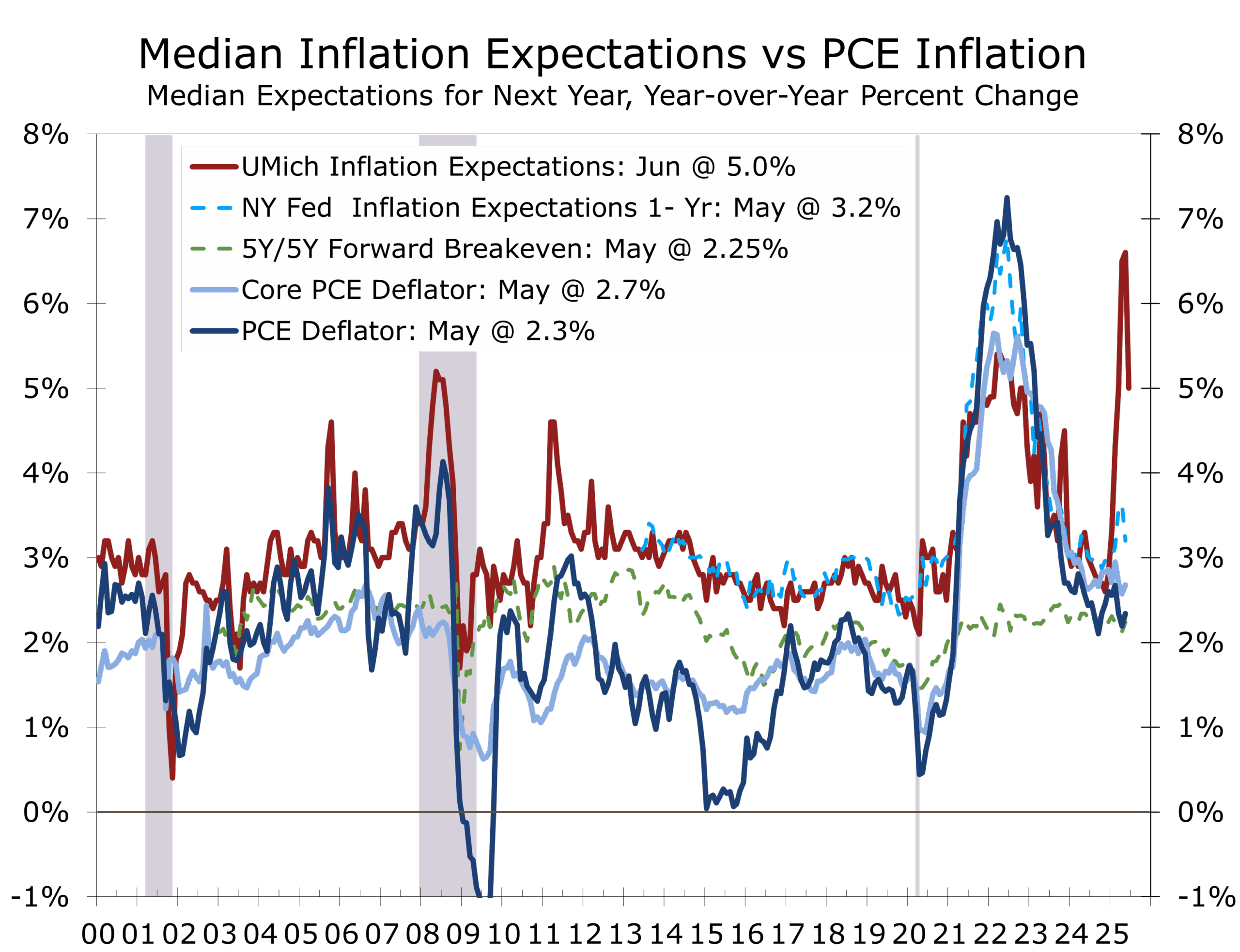

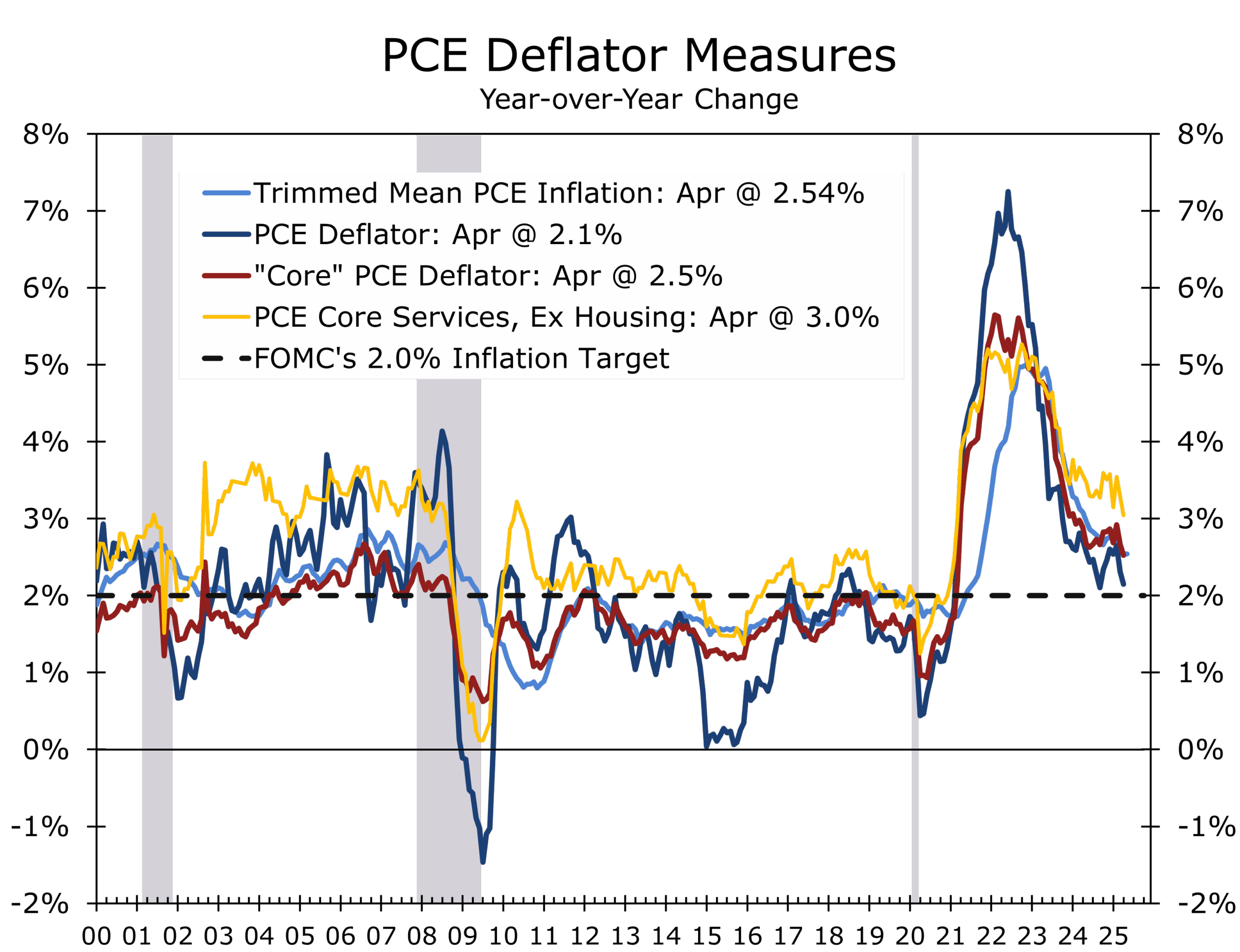

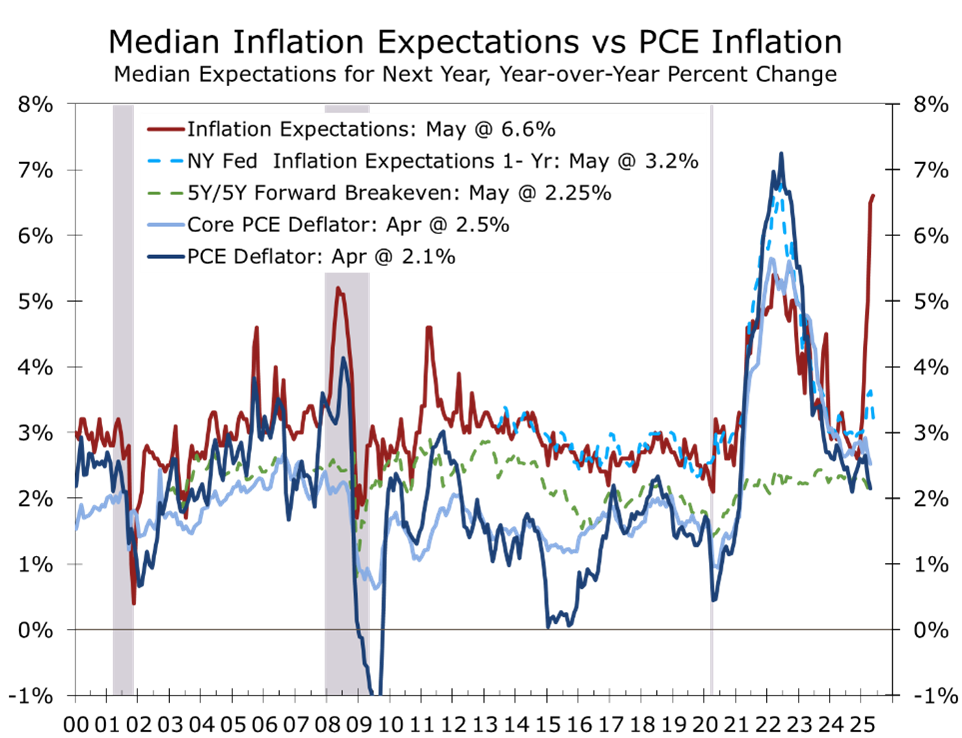

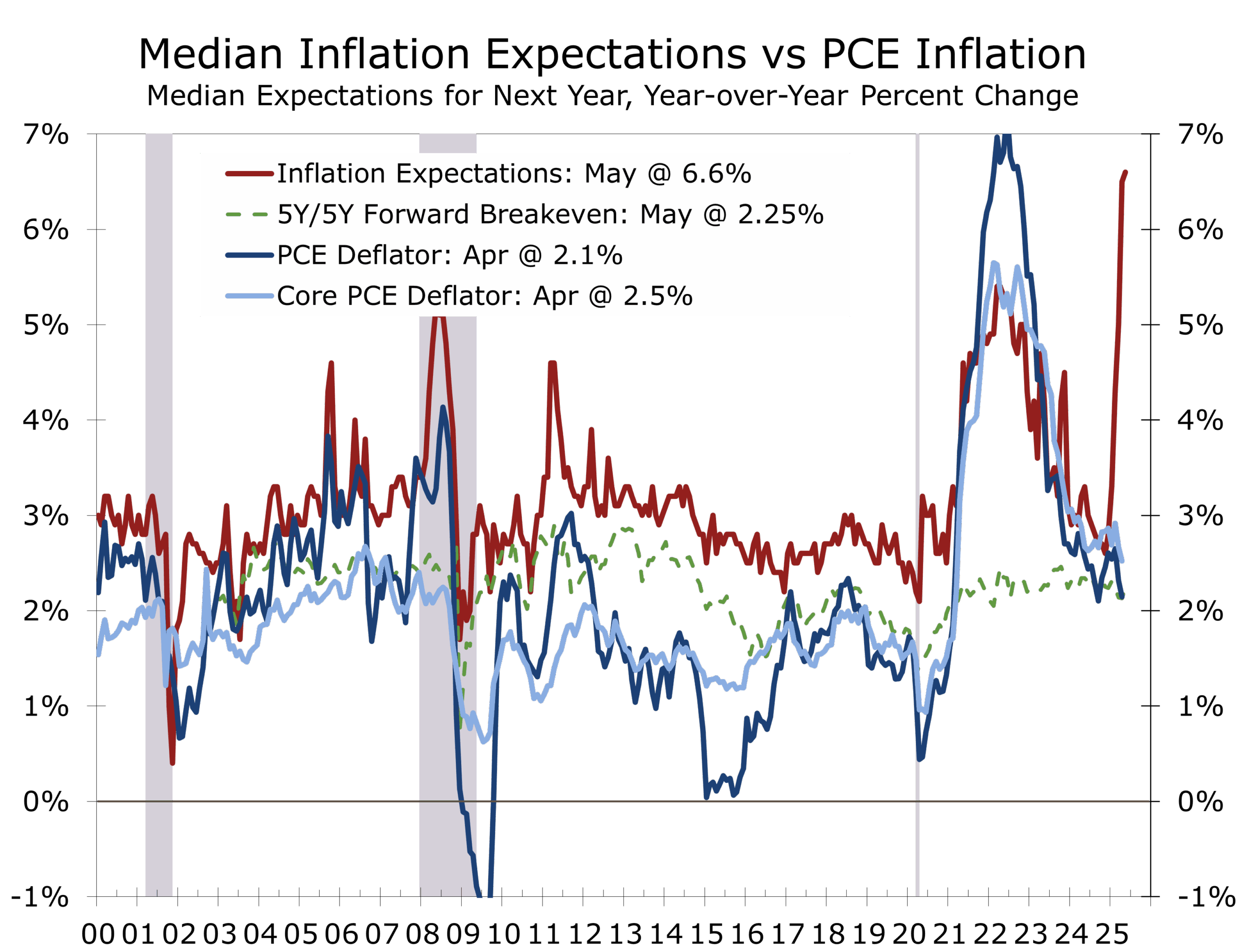

Inflation continues to cooperate. May’s PCE deflator and core PCE deflator came in close to expectations. While inflation remains above the Fed’s 2% target, the trend is moving in the right direction, particularly for problematic areas like core services’ prices.

Precision Strikes, Summits, and Shifting Alignments

The past two weeks marked one of the most consequential periods in global security since the Cold War. Israel launched a coordinated campaign against Iran’s nuclear infrastructure — including the Fordow and Esfahan enrichment sites — in response to what it determined was an “imminent” threat. The United States played a decisive supporting role, deploying B-2 bombers and submarine-launched cruise missiles to finish the job and neutralize deeply hardened targets. The IAEA has confirmed that Fordow’s centrifuges are “no longer operational.”

While Israeli forces led the majority of the strikes, U.S. capabilities were instrumental in penetrating Iran’s fortified facilities. The use of overwhelming force has significantly delayed — and possibly neutralized — Iran’s near-term nuclear breakout potential. Still, uncertainty lingers over whether Tehran managed to relocate any enriched uranium or advanced centrifuges in advance of the strikes. Recent intelligence casts doubt on those claims, and Israel’s targeting of military leadership, nuclear scientists and Iran’s classified nuclear archive will make any restart more costly, complex, and time-consuming.

Back in Washington, public debate focused more on language than results. The strikes’ effectiveness became a political flashpoint, as critics questioned terminology (such as the meaning of obliterated) rather than impact. In reality, Operation Midnight Hammer was a tactical and geopolitical success — the product of operational discipline, deliberate deception, and precision targeting. In an age of leaks, the mission’s secrecy underscored the professionalism of those involved and restored confidence in the Pentagon’s ability to deliver under pressure.

The political implications are equally significant. The operation’s success shifted the landscape, which is likely the driving pushback from outlets historically critical of the administration. While some coverage attempted to reframe the strikes through a partisan lens, the result was unambiguous: the White House delivered on its 60-day ultimatum, and the Pentagon executed with precision and resolve, dispelling lingering doubts about American credibility that had persisted since the failed Afghanistan withdrawal.

A ceasefire between Israel and Iran was announced shortly after the operation concluded. Though early hours saw sporadic retaliatory fire, President Trump moved quickly to deescalate. In a widely reported moment before boarding Marine One en route to the NATO summit, Trump dropped the “F-bomb” in pointed and targeted way before the press. Trump’s use of profanity is rare and deliberate—something he notes in Trump: The Art of the Deal, strategic disruption can be an effective negotiating tool. In this case, the expletive underscored the urgency of de-escalation, sent a clear message to both allies and adversaries, and ultimately helped lock in the ceasefire.

At the NATO summit in The Hague, Trump translated that momentum into broader geopolitical capital. All but one alliance member — Spain — committed to raising defense spending to 5% of GDP over the next decade. It marked a break from post–Cold War norms and reasserted NATO’s relevance in a more volatile multipolar world. Trump’s blend of hard-power diplomacy and political theater resonated, resetting the alliance’s deterrence posture in real time. Trump’s reception at the summit was, by far, the best that he has seen as president.

Meanwhile, the Abraham Accords are regaining momentum. U.S. and Israeli officials have signaled that Saudi Arabia and Syria may be open to joining as part of a broader regional stabilization framework. Proposals are under discussion for temporary Arab League oversight of Gaza and the release of remaining hostages. Trump and Netanyahu are reportedly aligned on a phased ceasefire and long-term political settlement. In a region long defined by deadlock, this moment represents rare forward movement — and the window for action may not remain open for long.

On the trade front, the U.S. and China reached a limited trade agreement late last week, ironing out the details of the Geneva agreement reached to earlier in the month. In addition to a partial rollback of tariffs and renewed Chinese commitments to purchase U.S. agricultural and energy exports, the agreement includes critical provisions on rare-earth minerals. China agreed to resume and expedite rare-earth exports to the U.S., addressing a key bottleneck in supply chains essential for electric vehicles, defense systems, and semiconductors. The deal removes a major overhang for U.S.-based EV and battery manufacturing projects, many of which had stalled due to input shortages and uncertainty around equipment sourcing. While the agreement remains narrow in scope, it serves as a strategic reset—intended to stabilize trade flows, support industrial investment, and ease bilateral tensions ahead of broader negotiations later this summer.

Political Capital Meets Legislative Headwinds

Despite recent geopolitical victories, including the Iran ceasefire and NATO defense pledges, progress on President Trump’s reconciliation package has run into some additional resistance from budget hawks in the Senate. While the administration originally targeted passage before the July 4 holiday, the president has since acknowledged that the timeline is flexible and that negotiations may extend into mid-July.

The most significant development came last week when the Senate parliamentarian ruled that several Medicaid-related provisions — projected to generate roughly $600 billion in savings — violated reconciliation rules. Proposals to cap provider taxes and tighten eligibility standards were deemed noncompliant with the Byrd Rule, which prohibits policy provisions lacking a direct budgetary impact. The ruling forced Senate Republicans to revise the bill’s fiscal framework, removing key offsets and increasing pressure to pare back the legislation’s scope.

While party leaders remain optimistic about passage, the final package is now expected to focus on more politically viable components, including extending the lower tax rates from the 2017 tax bill, some modest tax reforms, energy permitting, and trade enforcement measures. Broader entitlement reforms are likely to be deferred to future legislation.

Headed into the Second Half of the Year

The first half of 2025 has been marked by rapid and consequential shifts on both economic and geopolitical fronts. One theme has emerged with unmistakable clarity: the reassertion of U.S. leadership. From brokering an end to the India–Pakistan conflict to coordinating precision strikes on Iran’s nuclear infrastructure and halting the 12-Day War, the White House has reestablished its strategic presence. A reinvigorated NATO defense posture and renewed momentum behind the Abraham Accords have further reshaped the global security landscape.

Meanwhile, the U.S. economy has navigated a complicated mix of disinflation, softening consumer demand, and intensifying policy debates over trade, tariffs, and fiscal strategy. From the battlefield to the bond market, the first half of the year was defined by disruption, recalibration, and strategic signaling. After early volatility, markets appear to be adjusting to a faster, more forceful pace of change.

As the second half begins, attention will likely turn from disruption to execution. The challenge now lies in translating bold strategic moves into durable outcomes—whether through stabilizing trade relations with China, securing passage of a restructured fiscal package, or reinforcing fragile geopolitical agreements. Institutional resilience, rather than headline momentum, will define this next phase. Financial markets will look for policy follow-through in an environment of cooling growth and rising policy complexity. We continue to expect two rate cuts from the Federal Reserve, with the first likely in September. The path forward may be less volatile, but will demand discipline, coordination, and an ability to manage through this new rapid tempo without making a policy misstep.

Looking Ahead: Week of July 3, 2025

- Chicago Business Barometer (June) – Monday, June 30:

A quiet start to the week, with the Chicago PMI as the sole release. While regional, the index offers an early read on manufacturing sentiment heading from a manufacturing intensive area in a holiday-shortened but consequential week. - ISM Manufacturing Index (June), JOLTS (May), Construction Spending (May) – Tuesday, July 1:

Manufacturing continues to hold its ground amid tariff disruptions. Lean inventories and strong backlogs should keep the ISM index in the high 40s—above the 43.7 level typically associated with recession.

JOLTS job openings will be closely watched. Rising continuing claims and a decline in the share of consumers saying jobs are plentiful suggest growing friction for job seekers.

Construction spending likely declined in May, as residential and commercial activity softened. Data centers remain a key area of strength, but tariffs on Chinese equipment are delaying major manufacturing projects.

- ADP Employment Report (June) – Wednesday, July 2:

ADP payrolls have shown more weakness than the official jobs report, though they may better align with revised BLS data over time. We expect another soft print, though some upward revision to the prior month wouldn’t be surprising. - Employment Situation Report (June), ISM Services (June), U.S. Trade Balance (May), Initial Jobless Claims – Thursday, July 3:

Nonfarm job growth has averaged 135,000 over the past three months, driven by healthcare, hospitality, and local government. We estimate true underlying job growth is closer to 100,000 and are forecasting a 115,000 gain in June. Seasonal noise tied to the school calendar and summer hiring may lead to downside volatility.

ISM Services is expected to rebound modestly, pushing the index back above the key 50 break-even threshold.

Trade data and jobless claims will round out a dense morning of macro releases.

- Geopolitical Watch:

The Big Beautiful Bill could pass the Senate early this week, though reconciliation with the House remains. Final passage is likely by mid-July, with key changes expected on healthcare offsets and fiscal scope.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

June 28, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

October 28-29 FOMC Meeting Recap: The Fed Cuts Again — Balancing Diligence and Destination

Find a Way to Balance Rising Risks at Both Ends of the Mandate

- Decision: The Federal Reserve cut the target range for the federal funds rate by 25 bps to 3.75–4.00%, marking a second consecutive reduction as policymakers sought to buffer a cooling labor market and maintain financial stability.

• Liquidity Management: The Fed announced it will halt balance sheet runoff on December 1 and begin reinvesting proceeds from maturing MBS into Treasury bills, effectively restarting limited Treasury purchases to preserve market liquidity.

• Tone: The statement acknowledged that “downside risks to employment rose in recent months,” while inflation “remains somewhat elevated.”

• Context: The decision was complicated by the federal government shutdown, which limited access to official data and forced reliance on private-sector indicators.

• Dissents: Governor Stephen Miran favored a 50 bp cut; Kansas City Fed President Jeffrey Schmid preferred no change. The split underscores the uncertainty about how much economic activity and job growth have slowed and how much more tariffs will add to headline inflation.

• PCC View: We expect quarter-point cuts in both December and January, with the funds rate bottoming at 3.125% in Q1. The Fed may opt to skip a meeting, however, which would extend the duration of the easing cycle but not the depth. While headline inflation remains "elevated, the core PCE deflator should end 2026 near 2.5%, down from around 3% this year.

Policy Decision and Statement

The Federal Reserve lowered the federal funds rate by 25 basis points to 3.75–4.00%, citing a “shift in the balance of risks” toward weaker employment. The statement described economic activity as expanding at a “moderate pace,” but noted that job gains have slowed and the unemployment rate has edged higher.

Inflation was said to have “moved up since earlier in the year and remains somewhat elevated,” language suggesting concern about price stickiness but confidence that inflation pressures will subside over time. The Committee acknowledged elevated uncertainty and reaffirmed it would “carefully assess incoming data” ahead of any further adjustments.

The Fed needs to find a way to balance rising risks at both ends of its mandate.

The policy statement also confirmed that the Fed will conclude its balance sheet runoff on December 1, marking the end of quantitative tightening and a shift to full reinvestment of maturing securities, primarily into short-dated Treasuries. This reflects concern about tightening liquidity conditions and the Fed’s longstanding commitment to maintaining “ample reserves.”

The operational shift is a technical but meaningful adjustment. By reinvesting MBS proceeds into Treasury bills, the Fed will maintain the size of its balance sheet while subtly improving liquidity in the front end of the curve..

Recent strains in money markets—compounded by the government shutdown’s disruption of Treasury issuance—prompted the move. Powell and key officials have been explicit that this is not a return to quantitative easing, but rather a precautionary step to stabilize short-term funding markets and prevent another repo-style disruption.

This balance-sheet decision complements the rate cut: one addresses the cost of money; the other ensures the availability of money.

FOMC members will likely have a wider range of forecasts for growth, inflation and rates.

The 10–2 vote revealed the most ideologically divided Committee since the pandemic era.

- Governor Stephen Miran, who again dissented in favor of a 50 bp cut, is effectively playing the role once held by the Vice Chair—serving as the public voice of the Administration and advocating a faster easing pace to support employment.

- Kansas City Fed President Jeffrey Schmid, who voted against any rate cut, reflects the Kansas City Fed’s long-standing hawkish tradition, shaped by its historic focus on price stability and commodity-related inflation risks.

This dual dissent—from opposite ends of the policy spectrum—highlights the Fed’s internal balancing act: navigating slowing job growth without reigniting inflation or appearing politically influenced.

The government shutdown has limited official data, forcing policymakers to rely on alternative sources such as ADP, Homebase, and private job postings, which collectively suggest the labor market is weakening faster than the headline numbers imply.

At the same time, business investment remains firm, supported by AI infrastructure, defense technology, and reshoring of critical manufacturing. These conflicting signals—resilient capital spending versus softening labor demand—make this one of the most complex policy environments of Powell’s tenure.

Inflation from recent tariffs has been milder than anticipated. The Fed now sees price pressures easing back toward target over the next 18 months, assuming no renewed supply disruptions.

Powell’s Press Conference: Themes to Watch

Powell struck a measured, data-dependent tone at his press conference, reinforcing the Fed’s pivot from a rules-based framework to one guided by “discretion, diligence, and destination.”

Key themes:

- Labor risk management: “We cannot declare victory on inflation, but we must acknowledge the emerging risks to employment.”

- Liquidity assurance: Reinvesting MBS into T-bills is about function, not stimulus.

- Data limitations: Powell Stress the difficulty of policymaking amid a statistical blackout. “What do you do when you are driving in a fog? You slow down.”

- December outlook: “Policy is not on a preset course” Powell emphasized this point repeatedly and is keeping his options open while implying that another 25 bp cut remains on the table.

- Neutral Rate and the next move: We are now back in the range of where most FOMC participants believe the neutral funds rate is. “There is a growing course that maybe we should wait a cycle.”

- Equity Markets: “We do look at any particular asset, we look at the overall financial system and ask whether it can withstand a shock.”

- The AI Boom: It is different from the 1980s. The companies driving the boom are earning money. These are investment not just ideas.

Piedmont Crescent Capital’s baseline scenario now assumes:

- We still see two additional 25 bp cuts — most likely in December January — bringing the funds rate to a cycle low of 3.125% in Q1 2026. The markets are pricing in less than that, with the 2-Year Treasury rising to 3.59%—essentially pricing in one more cut by the middle of next year.

- Core PCE inflation ending 2025 at around 2.5%, down from 3% this year, as supply normalization and tighter credit cool demand.

- The Fed may opt to skip a meeting and wait for more hard data on inflation and employment. That would essentially extend the duration of the easing cycle without making it any deeper.

- We see the long-run neutral rate around 3% but it is likely edging higher as the buildout of AI infrastructure boosts productivity and long-run potential growth.

We see the Fed nearing the end of its easing cycle, shifting from active accommodation to sustained vigilance. Cutting rates while headline inflation remains “elevated” demands precise messaging. Lower short-term rates and a stable balance sheet should gradually support credit-sensitive sectors in early 2026, fostering a modest pickup in activity without reigniting inflation. If markets perceive the Fed as easing too aggressively, however, long-term yields could rise and offset much of the intended benefit.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

October 29, 2025

Mark Vitner, Chief Economist

704-458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Flashpoints, Upgrades and a Fragile Calm

Highlights of the Week

- CPI and PPI came in lower than expected, reinforcing recent disinflation trends ahead of a tariff-driven bump.

- Upstream pricing shows limited tariff pass-through, though businesses are reporting otherwise and tariff revenue has surged.

- Small business optimism rebounded slightly but investment and hiring plans remain subdued amid policy uncertainty.

- Consumer sentiment rebounded in early June and inflation expectations fell.

- The labor market continues to show signs of softening, with jobless claims firming and continuing claims elevated.

- The U.S. and China tentatively reached a tentative deal to reduce tariffs and allow exports of critical materials; Israel struck Iran’s nuclear facilities—killing key military figures and drawing drone and missile retaliation.

- G-7 leaders to meet in Canada next week; geopolitical risk and energy security expected to dominate the agenda.

- Inflation trends and the volatile policy/geopolitical environment support the Fed’s pause. The labor market is cooling, however, and the balance of risks is shifting as inflation undershoots expectations. The Israel–Iran conflict has recalibrated global risks, with global growth likely to decelerate further.

Inflation: Unexpectedly Cooling

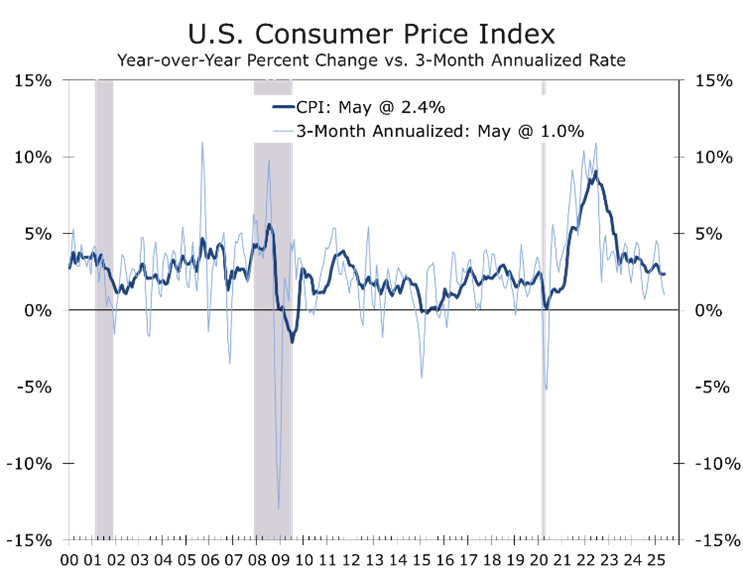

May’s CPI and PPI prints once again surprised on the soft side—headline and core CPI rose +0.1% m/m; and the headline PPI matched that pace, with core goods prices declining. Businesses are apparently absorbing tariffs or deferring their impact by relying on previously source goods, especially in new motor vehicles and apparel. The core CPI has risen at just a 1.7% annualized pace over three months, while falling energy prices and smaller price hikes at the grocery store have held the overall CPI to just a 1% pace. This has allowed real wages to eke out modest gains, supporting consumer spending.

Tariffs are not proving to be as terrifying, as inflation continues to run below expectations.

Inflation fears appear overblown. While tariffs will eventually raise prices on select imports, they also reduce consumers’ discretionary spending power—limiting broader inflationary spillover. With roughly two-thirds of household spending concentrated in domestic services, any tariff-driven rise in goods prices is likely to be offset by disinflation in categories such as travel, dining, and recreation. The net effect is a dampened pass-through to overall inflation, opening the door for a rate cut.

Nearly every measure of inflation is moderating faster than expected, including measures of core services, which were problematic a year ago.

Consumer sentiment improved in early June, with the preliminary University of Michigan index rising to 60.5 from 52.2. The rebound, which broke a five-month downtrend, appears tied to the recent easing of U.S.–China tariff tensions, lower gasoline prices, easing grocery prices, and a resilient labor market.

All five of the survey’s components increased, with current conditions rising 4.8 points and expectations climbing 10.5. Encouragingly, the sentiment recovery was broad-based—cutting across income, geography, and political affiliation. The improvement in expectations is notable, as they are most closely tied to actual spending and had been severely depressed.

Consumer sentiment improved broadly in early June, while inflation expectations declined.

Year-ahead inflation expectations fell 1.5 percentage points to 5.1%, and long-run expectations edged lower to 4.1%, signaling some tentative improvement in inflation psychology. The retreat in expectations was overdue and came alongside equity market gains and another round of surprisingly benign inflation reports. The lack of a resurgence in inflation tied to tariffs reduces the risk that consumers will pull back spending preemptively. The data also preceded Israel’s attack on Iran’s nuclear facilities and defense infrastructure.

Business Sentiment: Cautious Stabilization

NFIB small business optimism rose to 98.8 in May—its first increase in six months—as sales expectations improved. Owners remain frustrated by the lack of progress on tax and regulatory relief and are struggling to absorb tariff-related cost increases. Capital spending plans are muted, with policy uncertainty delaying investment. Survey results align with ISM and factory orders data showing flat demand and persistently weak exports.

Labor Market: Cooling, Not Cracking

Initial jobless claims held at 248,000 for the week ending June 7, while the four-week average rose to 240,250—its highest since August 2023. Continued claims climbed to 1.956 million, the most since late 2021. While some of the increase may reflect seasonal transitions, the broader trend points to a softening labor market.

Federal employee claims remain below February highs, but signs of structural slack are emerging. The long-term unemployed share is rising, and surveys signal slower hiring amid tariff uncertainty. Layoffs remain low, yet job postings are down and reemployment is taking longer—pointing to growing friction. Still, conditions remain stable enough for the Fed to prioritize inflation control, though risks now tilt toward further labor market weakening.

Trade Outlook: Pause, Not Peace

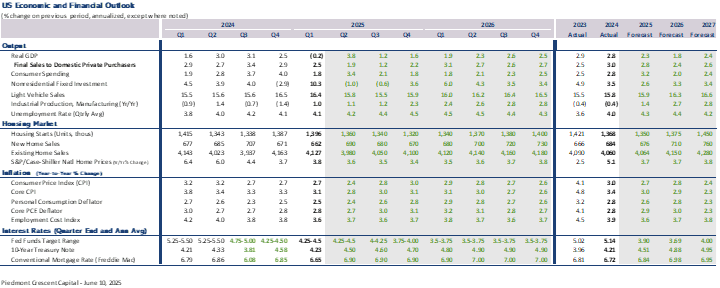

The U.S.–China trade deal capped U.S. tariffs at 55%, China’s at 10%, and introduced a temporary rare-earth export agreement. The deal is tentative and allows companies to apply for a six-month license to purchase rare earths and magnets. While this removes some downside risk—a final settlement remains far off. GDP forecasts for 2025 have increased slightly. Our latest forecast, released Tuesday, calls for 3.8% growth in Q2, following by 1.4% growth in the second half of the year. For the year as a whole, we see real GDP rising 1.7% on a Q4/Q4 basis.

Recent Treasury auction data show mixed demand: the June 10-year note auction cleared at 4.45%, with soft indirect demand, pointing to market caution amid elevated supply. Meanwhile, the May Monthly Treasury Statement showed a $316 billion deficit—better than last year’s $347 billion—but fiscal year-to-date deficit widened 13.5% versus FY2024 thanks to a torrent of spending late last year and in early 2025. Rising entitlement costs, defense spending, and elevated interest payments remain structural headwinds.

Tariff revenue, now expected to contribute $2.5 trillion over the decade, provides some cushion and comes close to covering the CBO-project revenue loss from the GOP-led One Big Beautiful Bill’s tax cuts and spending hikes.

Geopolitical Risk: Rising Lion and Global Fallout

Israel launched a major military campaign—Operation Rising Lion—striking upwards of 100 Iranian nuclear and military sites, including Natanz and Isfahan. The strikes killed IRGC Commander Hossein Salami and senior commanders Mohammad Bagheri and Amir Ali Hajizadeh. Iran responded by launching 100 drones, which were largely intercepted by Israeli defenses.

New intelligence suggests the Israeli campaign included covert drone strikes, launched within Iran, on ballistic missile launchers and a decapitation operation targeting senior military leadership. Confirmed airstrikes included high-value targets such as the Natanz Enrichment Complex, Kermanshah underground missile storage, and key sites in Tehran and Esfahan. Much of Iran’s military leadership was eliminated in highly targeted strikes. Iran’s immediate response was muted—analysts believe Israel’s disruption of missile infrastructure and the deaths of key military leadership delayed a coordinated counterstrike. Iran has since launched missile barrages, most of which have been intercepted.

Iranian Supreme Leader Khamenei vowed retaliation but offered no specifics. Meanwhile, Tehran has suspended nuclear negotiations and may escalate its regional posture through proxies like the Houthis and Hezbollah. Israel apparently has free reign over Iranian skies and is openly refueling fighter bombers in clear daylight. Nuclear facilities are likely to be hit repeatedly in order to destroy the hardened bunkers they reside in. Israel has said the operation could last for up to two weeks and the objective is to eliminate the nuclear program—not set it back.

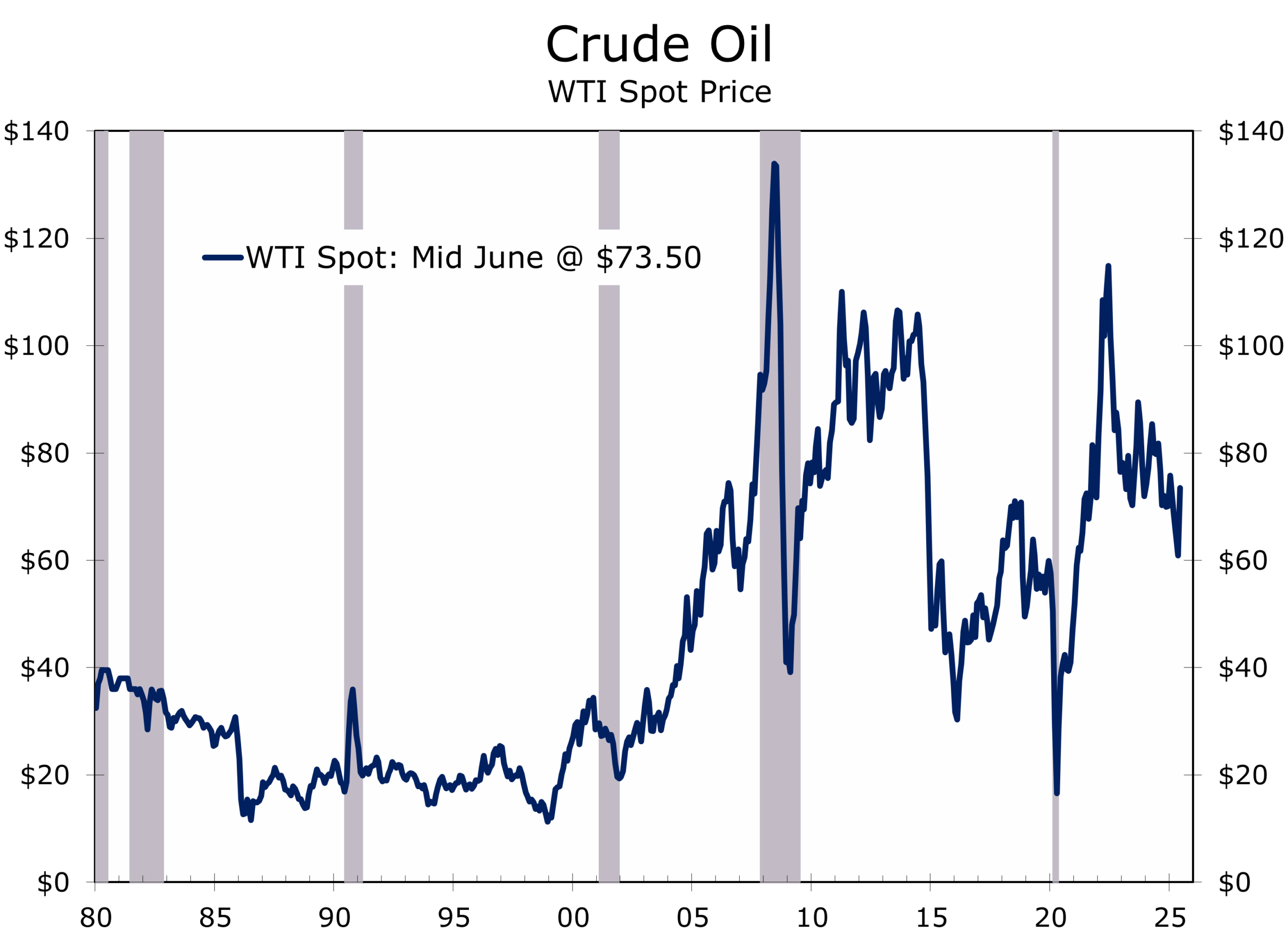

A frustrated and defeated Iran may lash out at its population, which was openly feeding information to Israel via the internet before Iranian authorities worked to shut down internet access. Iran might also strike neighboring oil facilities. Oil markets reacted with a 7–8% spike, and safe-haven demand surged for Treasuries and the dollar. Oil prices are still lower than they were a few months ago.

G-7 leaders, set to meet in Kananaskis, Alberta, Canada from June 15 to 17, 2025, are expected to confront a crowded agenda. Discussions will likely span artificial intelligence, global economic imbalances, defense partnerships, and regional stability—including the Israel–Iran conflict and support for Ukraine. The setting—a return to the Canadian Rockies where the 2002 summit was held—underscores the gravity of the moment. Hosted by Canadian Prime Minister Mark Carney, this 51st summit will also welcome key invitees including Ukraine’s President Zelenskyy, along with leaders from Australia, South Korea, India, Brazil, and Saudi Arabia. Coordination—or lack thereof—will shape market risk sentiment as the G-7 grapples with an increasingly fractured global order.

Recalibrating Risks

Inflation trends and the volatile policy environment support the Fed’s pause. The labor market is cooling, however, and the balance of risks is shifting as inflation repeatedly undershoots expectations and jobless claims edge higher. Tariff and tax uncertainty continue to weigh on investment and hiring.

The Israel–Iran conflict has recalibrated global risks. Treasuries, the dollar and gold are drawing safe-haven demand. The G-7 and FOMC meetings will serve as key diplomatic and economic inflection points to incorporate shifting geopolitical and economic risks. Israel has stated that it is planning a 14-Day operation to eliminate the Iranian nuclear program. Merely setting the program back would be a failure and increased global risks.

Markets will be watching for any shift in diplomatic posture toward Israel and Iran, as well as how the Fed recalibrates the inflationary risks from tariffs and higher energy prices against the disinflationary pressures of slowing growth.

Looking Ahead: Week of June 17, 2025

- FOMC Meeting (June 17–18): Expect the Fed to hold rates steady, but all eyes are on forward guidance and risk assessments. Market focus will be on Powell’s tone amid mixed macro data, slower inflation and elevated geopolitical risks.

- Retail Sales (May): Tuesday’s Retail Sales report will help further shape expectations for Q2 growth. Look for a rebound in discretionary purchases, which jumped in March ahead of tariffs and fell back in April.

- Housing Starts and Permits (May): Homebuilders face demand headwinds from rising insurance premiums and lingering affordability challenges. New home inventories have been rising, and builders have been cutting prices to spur sales. We expect another soft reading for both single- and multifamily starts.

- G-7 Summit (June 15–17, Kananaskis): Leaders from the G-7 and invited nations will tackle AI governance, support for Ukraine, Middle East volatility, global trade, and defense collaboration. Specific attention will be paid to China’s economic coercion, USMCA renewal prospects, and the economic governance gap between the G-7 and BRICS.

- Geopolitical Watch: Iran’s response to Israeli strikes—and whether proxies such as the Houthis or Hezbollah can coordinate retaliatory attacks—remains a key geopolitical risk. Any G-7 coordination on sanctions or diplomatic overtures could meaningfully shift global risks but not until Israel destroys much or all of Iran’s nuclear infrastructure.

- Treasury Refunding Outlook: Watch for potential updates on long-duration issuance plans and bond market reactions to persistent deficit concerns.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

June 13, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

Recalibrating Risk in a Shifting Landscape

Off the Cliff, But Not Out of the Woods

- Job growth is slowing, revisions are trending lower, and key labor metrics are weakening beneath the surface. The latest QCEW employment data imply the monthly jobs numbers are overstated by at least 500,000 jobs and the narrowing breadth of job gains and drop in labor force participation suggest the labor market is losing momentum.

- Tariff uncertainty continues to weigh on trade, manufacturing, and business confidence. Recent reprieves and postponements of tariff deadlines has bolstered confidence that a worst case outcome is less likely.

- Consumer spending is shifting; services are holding up, but goods outlays are softening after a brief surge ahead of tariffs. Income growth remains solid, although not quite as strong as recent headlines imply. Social Security catch-up payment have bolstered personal income growth. Wage and salary growth remains solid, however, and should support consumer spending.

- Actual inflation remains well-contained, but perceptions of rising prices are intensifying. The CPI and PCE deflators continue to come in below expectations and year-to-year gains are close to the Fed’s target. Producer Prices appear more vulnerable to higher tariffs, but tighter margins will limit pass throughs. With consumers spending more for imported goods, they will have less to spending on other goods and services, restraining price gains for these items.

- The Fed remains in 'wait-and-see' mode; a September cut seems plausible, but the Fed may wait longer for events to more fully play out. A surprise budget deal, with greater budget savings, would set the table for more aggressive easing.

- Geopolitical flashpoints—including Ukraine’s deep strikes and the unproductive nuclear talks with Iran—are raising tail risks. Domestically, President Trump’s deportation initiative has gained momentum in the courts but run into oppositions in the streets.

- Renewed U.S.-China trade talks in London offer hope but underscore persistent global uncertainty. A tentative deal looks promising and paves the way for a more substantial deal later this year. Trade deals have so far proved elusive, and the Trump Administration would like to implement the bulk of them before the run up to the midterm elections.

- Q2 GDP forecasts have been revised higher following a sharp drop in the trade deficit. We are currently looking for real GDP to rise at a 3.6% pace in Q2 and slow to a 1.5% pace in the second half of this year before rebounding in 2026. Full-year expectations remain cautious but could strengthen if consumer inflation fears prove overstated or fail to materially impact spending behavior.

Quiet Contraction, Rising Risk

The U.S. economy continues to grind forward, but the gears are clearly slipping. The May employment report underscored a labor market that’s softening beneath the surface. Payrolls rose a modest 139,000, but the three-month average slipped to just 135,000. Downward revisions subtracted 95,000 jobs from prior months, and updated QCEW data suggest 2024 job growth may have been overstated by more than 500,000 jobs. The unemployment rate held at 4.2% but conceals a 0.2-point drop in labor force participation and a 0.3-point decline in the employment-population ratio. Slack is building quietly—and confidence is ebbing.

Job gains are increasingly narrow, centered in healthcare and hospitality. Retail, government, and staffing firms are all shedding jobs. Federal payrolls alone have dropped by 59,000 so far this year. Manufacturing has lost momentum, with the ISM showing sub-50 readings across new orders, employment, and production. Tariffs are complicating cost structures and raising policy risk, making it harder for firms to plan, invest, or pass along higher costs.

Consumer spending, which was front-loaded ahead of tariff hikes in Q1, is now normalizing. Personal consumption expenditures rose just 0.2% in April, entirely on services. Spending on goods declined, led by durables like autos and recreational equipment. Light vehicle sales fell to a 15.2 million unit annual pace in May, down from 15.6 million in March, as affordability constraints and higher insurance costs took their toll. The auto sector is contending with high interest rates, rising delinquency rates, and bloated inventories.

Consumer sentiment remains fragile. The University of Michigan’s final reading for May edged up to 52.2, effectively unchanged from April and still hovering near recessionary lows. The Conference Board’s Consumer Confidence Index rebounded to 98.0 from 85.7 in April but remains well below its historical average. Encouragingly, both surveys pointed to improved perceptions of income growth and durable goods buying conditions—early signs that easing trade tensions may be lifting consumer spirits at the margin.

Factory orders rose 0.7% in April, driven by gains in defense and non-durable goods. But core capital goods orders—a key proxy for private business investment—were flat, reinforcing the narrative of cautious corporate sentiment amid ongoing policy uncertainty.

Bottom Line: the economy is not breaking down, but it is stalling in places. Consumers are more selective. Businesses are conserving cash. Trade frictions, tighter credit, and unpredictable policy signals are weighing on decision-making. With inflation pressures easing and tariffs retreating, conditions are in place for stabilization—but confidence remains brittle, and forward momentum uneven

Tariffs as a Taxing Distortion

The inflationary impact of tariffs remains hotly debated, but the data increasingly support a more nuanced conclusion. Tariffs are a tax and are not broadly inflationary in the monetary sense—they do not expand the money supply—but they do introduce costly distortions. They act as a tax on trade: shifting relative prices, rerouting supply chains, and redirecting household and business spending. This dynamic tends to reduce efficiency, compress margins and suppress real consumption elsewhere in the economy.

April’s PCE report confirmed that overall price pressures remain contained. Headline inflation rose just 0.1%, bringing the year-over-year rate to 2.1%, while core PCE eased to 2.5%. Goods prices fell slightly for the month—down 0.1%, driven by declines in grocery and gasoline prices—while services inflation was muted at 0.1%. Supercore services (excluding housing and energy) were flat. Importantly, the sharp tariff-induced front-loading seen in March reversed in April, with durable goods spending slipping—especially in motor vehicles and recreational equipment. The May CPI and PPI also came in below expectations, with both the headline and core CPI rising just 0.1%.

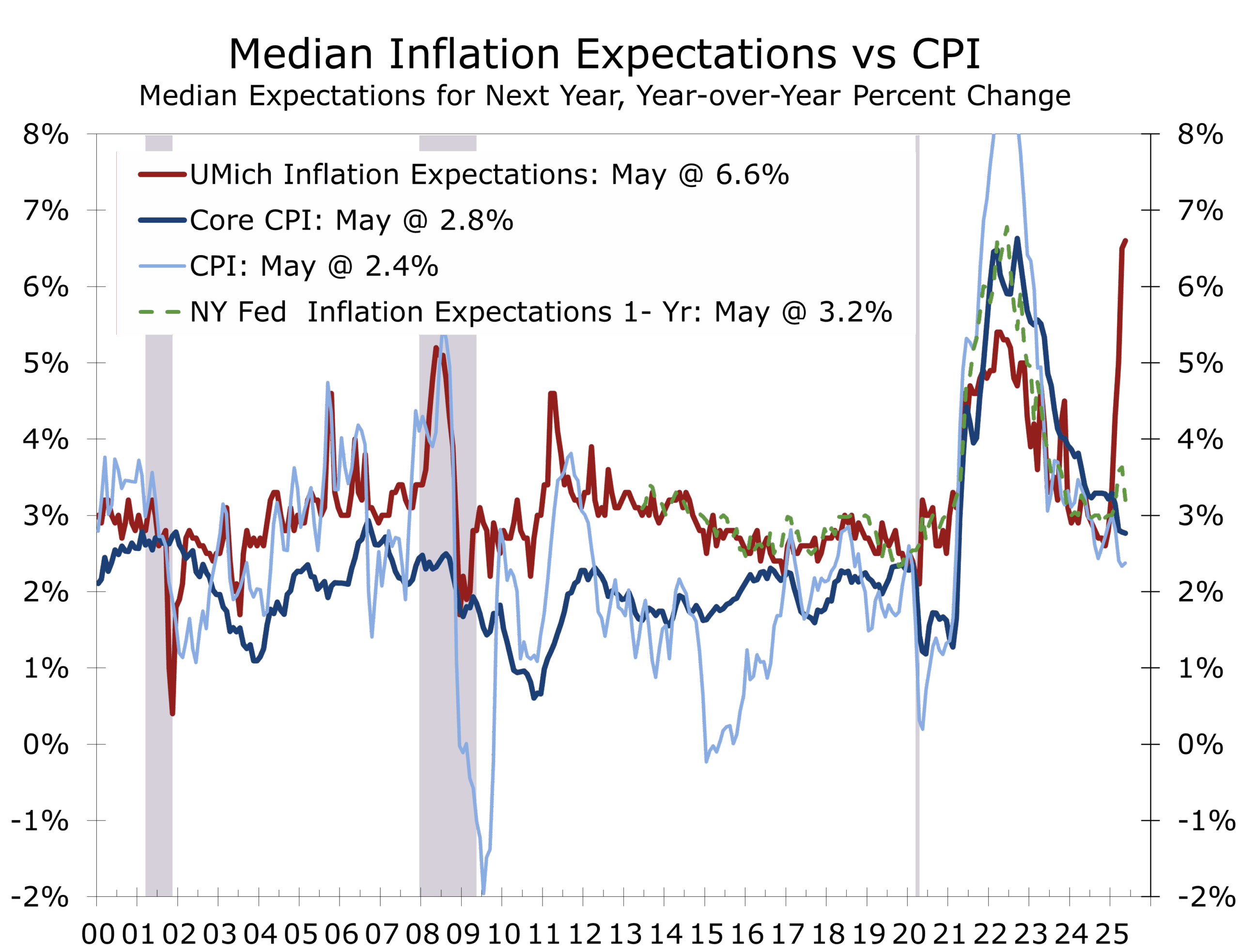

The latest Survey of Consumer Expectations from the Federal Reserve Bank of New York reinforces this picture. Short-, medium-, and long-term inflation expectations all declined in May. One-year-ahead expectations fell 0.4 points to 3.2%, while five-year expectations eased to 2.6%—close to the Fed’s 2% long-run target. Inflation uncertainty also decreased. This suggests that despite persistent rhetoric around rising prices, most households are not yet seeing evidence of sustained, broad-based inflation.

Still, businesses are clearly feeling the pinch. Most are not passing costs along to consumers—at least not directly. Instead, they’re eating the difference. Margins are tightening. Visibility has worsened. Hiring freezes, investment deferrals, and cost-cutting initiatives are becoming commonplace. Many firms now view tariffs as a tax hike they must absorb, especially as price increases risk political backlash. The optics matter: President Trump has repeatedly signaled willingness to “name and shame” companies perceived to be exploiting the inflation narrative.

Treasury Secretary Scott Bessent has defended the tariffs as “surgical and strategic,” aimed at rebalancing supply chains without stoking a consumer price spiral. Nonetheless, research from the Yale Budget Lab warns that tariffs could lift the PCE index by 0.5 percentage points by year-end—an appreciable drag, even if not an inflationary spiral. Meanwhile, former Treasury Secretary Larry Summers has warned of “stagflation-lite”: sectoral bottlenecks and price stickiness amid slowing growth. These scenarios increasingly look like worst-case outcomes.

The inflation conversation is now as much about perception and policy as actual price levels. Tariffs are acting as a brake—not an accelerator—on discretionary spending. The 2022-2023 inflation shock was monetary, as the Fed accommodated the humongous expansion of federal spending. Today’s inflationary pressures are fiscal, regulatory, and geopolitical and will likely prove temporary as long as the Fed does not accommodate them.

The Fed remains appropriately cautious. The path forward hinges not just on prices, but on how tariffs reshape behavior. For now, inflation expectations remain anchored—but sentiment is fragile, and the supply chain chessboard is still in motion.

Manufacturing’s Mixed Signals

The ISM Manufacturing Index (PMI) fell to 48.5 in May, marking the third consecutive month of contraction after two months of expansion earlier in the year. Still, there are tentative signs of stabilization. New orders edged up to 47.6, while customer inventories remained lean at 44.7, suggesting firms are not overstocked and may soon need to restock. Businesses also appear less inclined to cut headcount outright, with the employment index rising slightly to 46.8.

Production remains weak, with the production index holding at 45.4, while trade-sensitive components remain deeply depressed—new export orders dropped to 43.1, among the lowest readings since the early months of the COVID-19 downturn. But the sector isn’t cratering—it’s adjusting.

Order backlogs climbed 3.4 points to 47.1, signaling that unfilled demand is beginning to accumulate. Rising backlogs are typically a precursor to renewed capital spending and hiring. For now, however, businesses are in defensive mode—preserving capital, managing inventories, and delaying expansion until policy clarity improves. The Q1 activity boost from tariff-driven front-loading has run its course.

The persistent trade turmoil has also reignited debate over the importance of U.S. manufacturing. A surprising number of academic papers have questioned whether manufacturing is even necessary in a modern service-based economy.

We find such arguments misguided and surprisingly arrogant. Manufacturing remains indispensable—especially in an era of strategic competition and fragile supply chains. Moreover, manufacturing jobs tend to be among the best-paying opportunities in the geography where new plants are opening (mostly in smaller cities and rural parts of the South, Midwest and Mountain West), particularly for workers without a four-year degree.

Though manufacturing represents just 10.3% of GDP, it typically contributes two-thirds of the swing in GDP during recessions and recoveries. That disproportionate cyclical influence is why the Fed and most forecasters place such weight on ISM Manufacturing data.

Alongside weekly initial unemployment claims, the PMI is considered a key early indicator for the overall economy. The PMI has now been in contraction territory—below 50—in 29 of the past 31 months, dating back to the 2022 slowdown. Still, May’s reading of 48.5 remains well above the critical threshold of 42.3, which historically, over time, aligns with outright recession. For now, the index is consistent with modest GDP growth of about 1.7%—weak, but still positive. That pace is slightly below the economy’s long-run potential, implying a modest rise in the unemployment rate. So far, however, unemployment claims have only risen modestly, reflecting the continued reluctance of businesses to let workers go amidst unusually slow labor force growth.

Global Flashpoints, Fragile Truces

Geopolitical risks continue to hover over the global economy. Kyiv’s audacious Operation Spiderweb—a long-range drone strike campaign against deep-inland Russian airbases—may mark a strategic turning point in the Ukraine war. Dozens of strategic bombers were damaged or destroyed, including nuclear-capable Tu-95s and early warning aircraft, inflicting billions in losses on the Russian Air Force. The precision and depth of the strikes stunned observers and undermined the credibility of Russia’s air defense network, particularly given the domestically-built nature of Ukraine’s drones and the asymmetric return on investment—some missions costing less than an iPhone. The campaign has also amplified doubts about Russia’s second-strike deterrent and exposed the vulnerability of high-value targets across its vast geography.

Even as the battlefield tilts toward stasis, the Kremlin’s ambitions remain expansive. A recently released Ukrainian intelligence assessment claims Russia intends to seize over 55% of Ukrainian territory by the end of 2026, including all of Donbas, Zaporizhzhia, Mykolaiv, and Odesa—denying Ukraine access to the Black Sea. The operational map, shown to U.S. officials, outlines a phased campaign that would require Russia to capture nine unoccupied oblast capitals and sustain a rate of territorial gains far beyond its demonstrated capacity.

Markets, for now, remain largely unshaken. But energy traders and defense analysts are watching closely. Russia’s ongoing efforts to cut off Ukrainian access to ports and conduct information warfare within NATO states suggest that risks are growing, not fading.

Talks between the United States and Iran over a potential nuclear agreement—aimed at limiting or prohibiting uranium enrichment and preventing Iran from developing a nuclear weapon—appear to be faltering. The risk of preemptive action by Israel, and possibly the United States, against Iranian nuclear research and enrichment facilities has increased. Any such strike would likely be highly destabilizing. Unlike Israel’s limited October 26th attacks on Iranian air defense systems and drone production infrastructure, Tehran would likely mount a far more robust response. There are growing concerns that Russia and China may provide Iran with intelligence support. In a sign of escalating tensions, the United States has ordered non-essential personnel to evacuate its embassy in Baghdad, citing fears of retaliatory strikes. Oil prices have responded, with WTI climbing to approximately $67 per barrel, up from $60 earlier in June.

Meanwhile, a new round of high-level U.S.-China trade negotiations is underway in London, where Treasury Secretary Scott Bessent, Commerce Secretary Howard Lutnick, and U.S. Trade Representative Jamieson Greer are meeting with Chinese Vice Premier He Lifeng. The talks follow the fragile Geneva framework established last month, which briefly eased tensions in equity and commodity markets. Implementation, however, has been uneven—particularly on critical exports such as rare earth elements. China’s abrupt suspension of rare earth shipments in April disrupted global supply chains and alarmed manufacturers reliant on Chinese inputs. A tentative agreement has been reached to lower tariffs to 55% on Chinese goods and 10% on U.S. exports to China. In addition, China will allow U.S. firms to purchase rare earths for at least six months.

The presence of Lutnick, who oversees export controls, highlights how central supply chains and dual-use technologies have become to the broader decoupling narrative. While both sides continue to signal optimism, sticking points remain over fentanyl, industrial espionage, Taiwan, and forced technology transfer. The stakes are high. Failure to maintain even a temporary truce risks reigniting a full-scale economic cold war—with cascading consequences for inflation, global investment, and energy security.

Looking Ahead: A Step Back from the Cliff