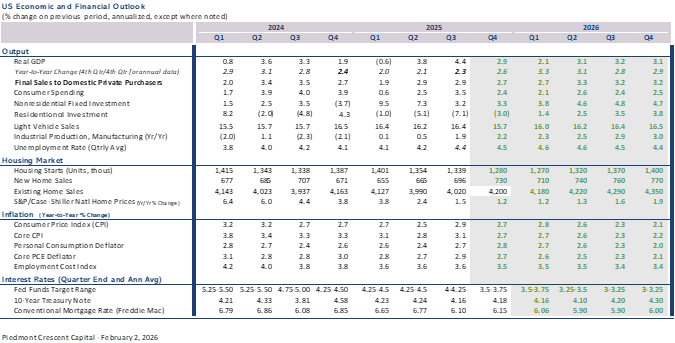

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Signals, Sentiment, and the First Green Shoots

Highlights of the Week

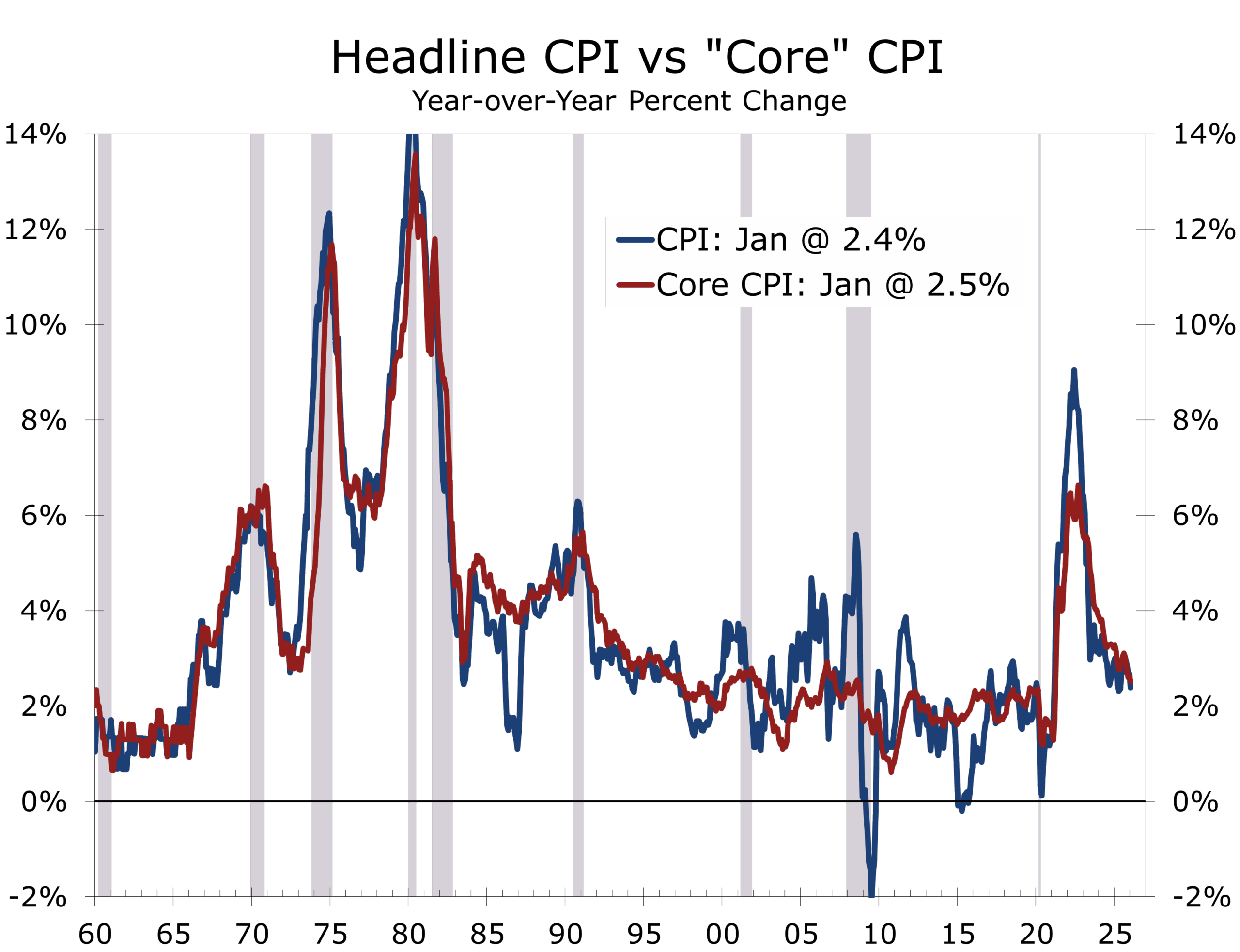

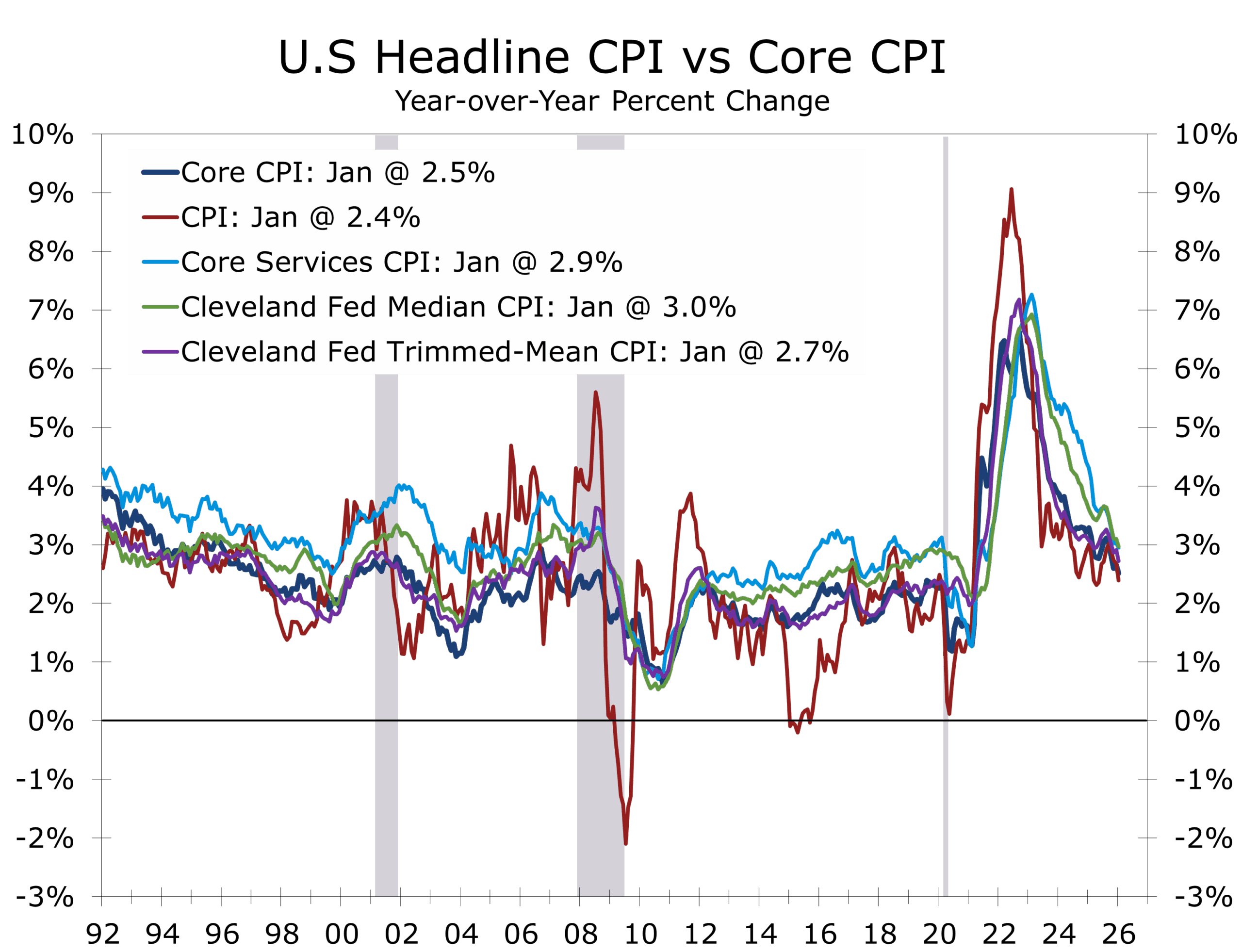

- January CPI cooled to 2.4% headline and 2.5% core year-over-year, broadly in line, with leading components pointing to further moderation into the second half of 2026.

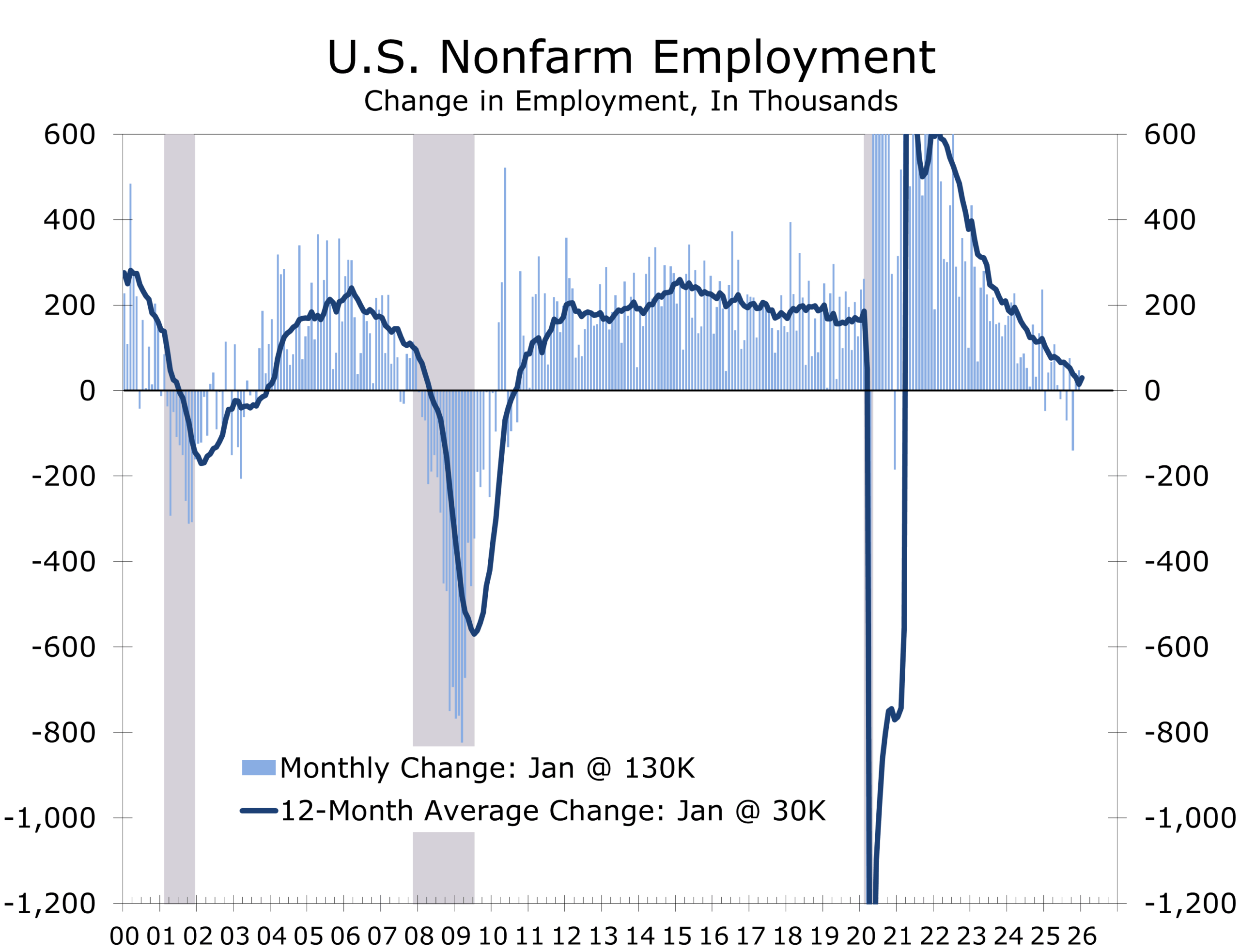

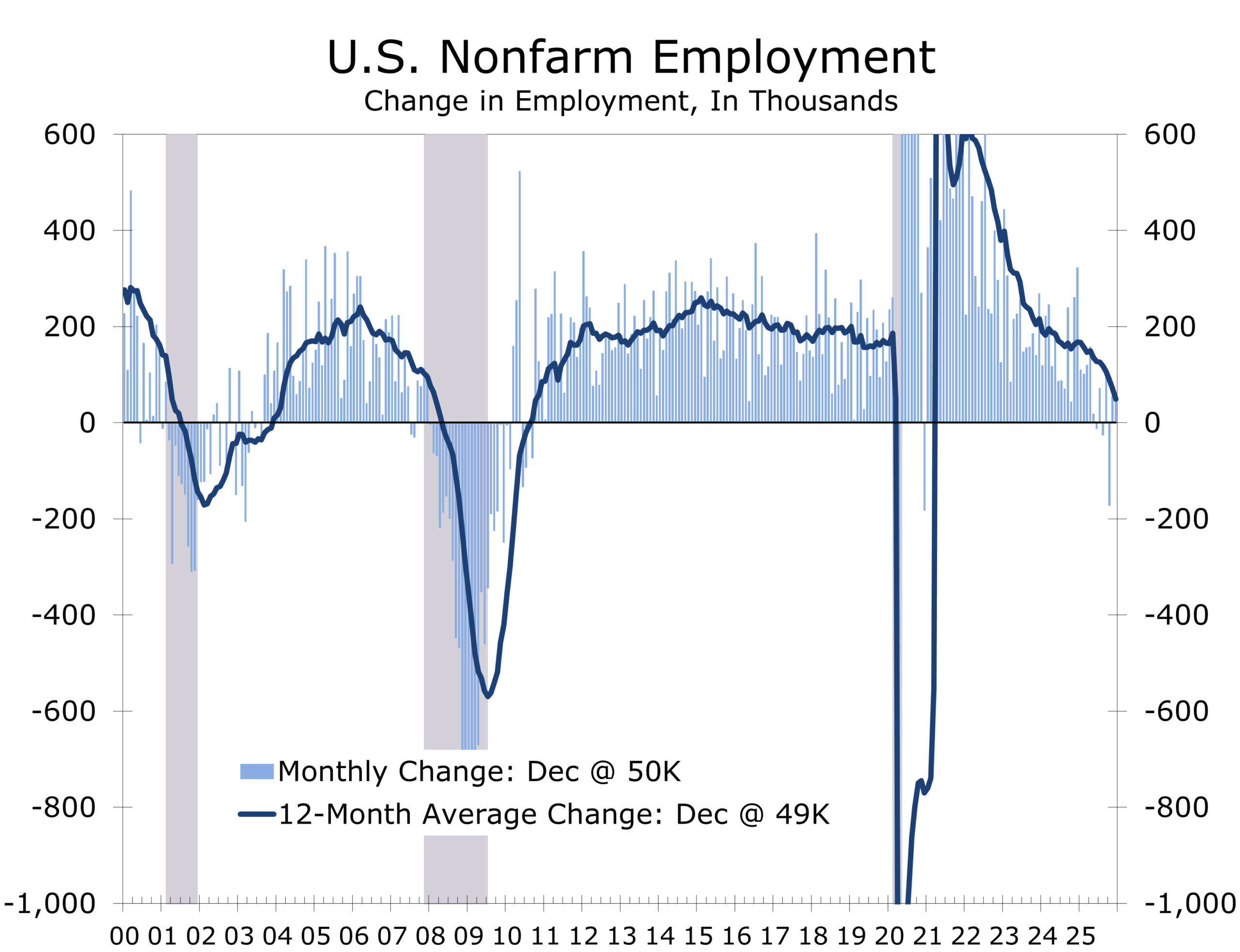

- Payrolls rose 130,000 in January, nearly double what we believe the underlying pace is. Private payrolls rose an even larger 172,000.

- Retail sales and housing softened but largely reflect weather distortions and payback from earlier strength rather than structural retrenchment.

- Markets are recalibrating from “limitless AI” to selective productivity gains, while Fed cut odds remain volatile but not urgent.

- Geopolitics is now a structural input into capital allocation, not merely a tail risk.

Stabilization, Green Shoots and a Lower Bar

The past week delivered textbook Goldilocks data (firmer employment, moderating inflation, and no visible credit stress), yet equities sagged and Treasury yields fell to multi-month lows. The divergence owes more to positioning and narrative fatigue than to macro deterioration.

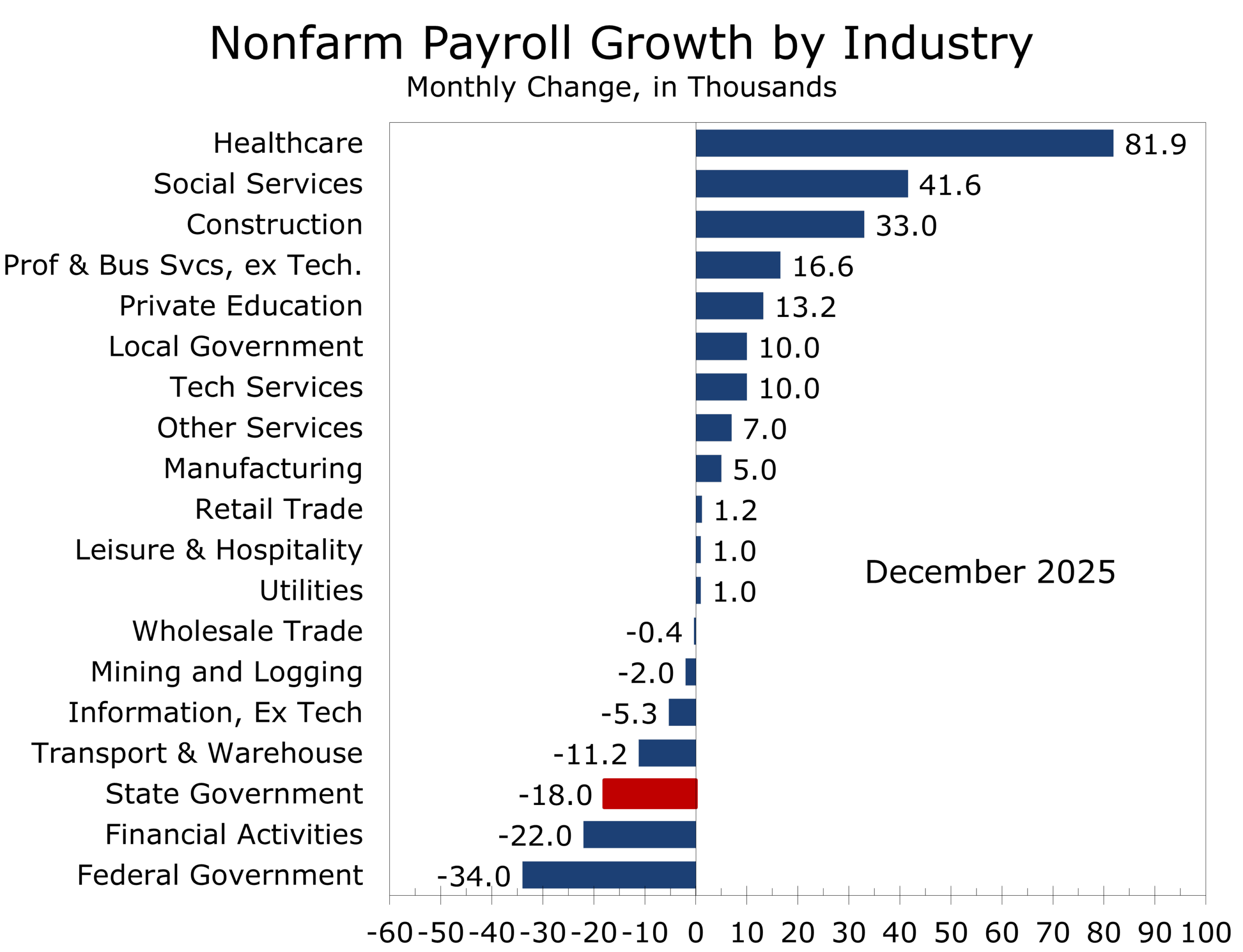

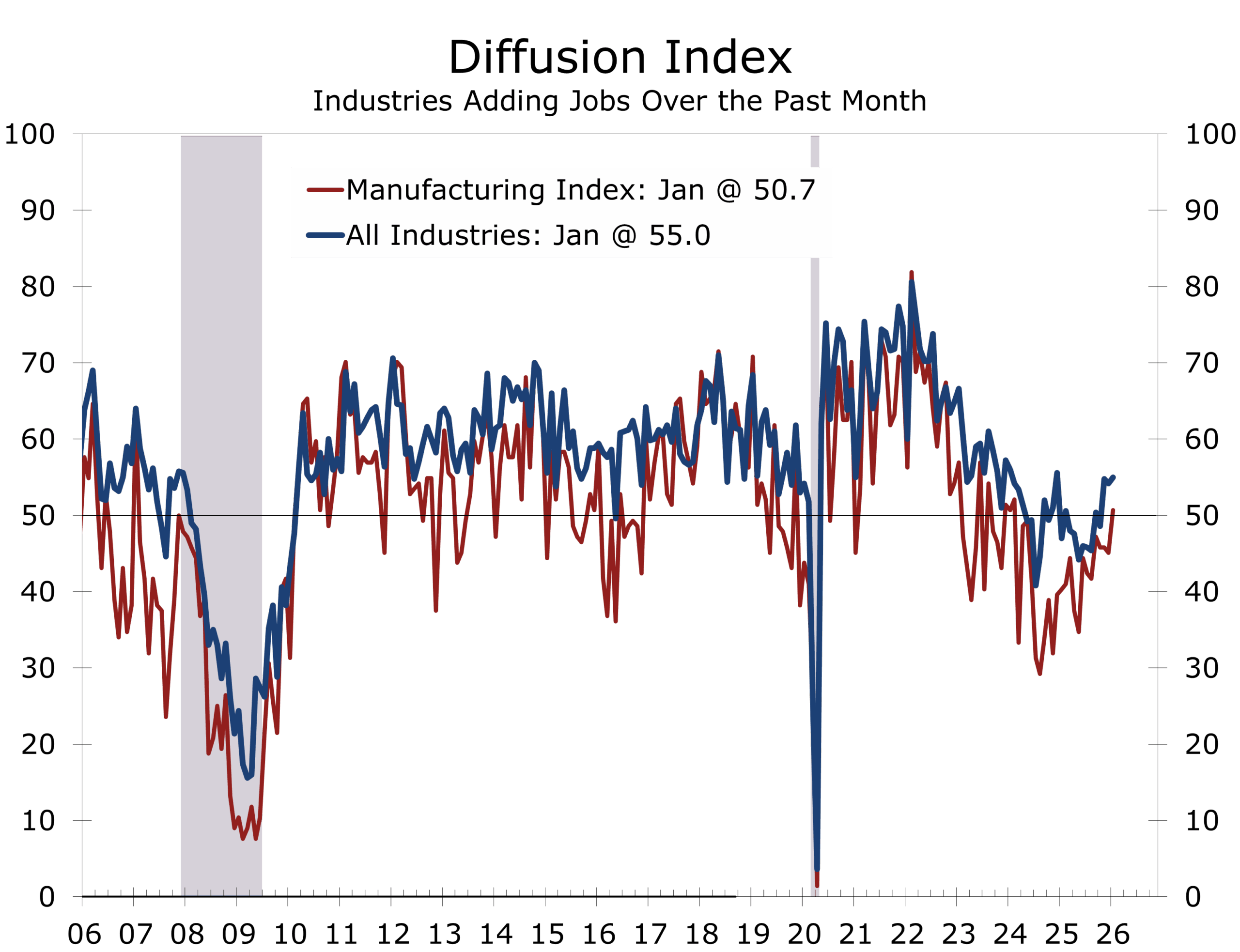

Read in isolation, the employment report signals stabilization, not slowdown. January’s stronger-than-expected gains and annual revisions suggest the labor market is stabilizing earlier than anticipated. While job growth remained heavily concentrated in healthcare and social services, the overall diffusion index has stayed above 50 for three consecutive months, and the manufacturing diffusion index returned above 50, consistent with the recent upside in the ISM manufacturing survey.

One month does not make a trend. Should cyclical segments continue to rebound, we would revise our underlying job-growth estimate higher, from approximately 65,000 per month currently to approximately 75,000 in the first half of the year and potentially 90,000 in the second half. Manufacturing payrolls recorded their first gain in 14 months in January. Sustaining that improvement will require modest labor-supply relief, likely from some easing of immigration enforcement (as we expect) and higher participation among younger workers.

The labor market no longer needs 150,000 jobs a month to hold the unemployment rate stable. It needs between 50,000 and 75,000, and January easily cleared that bar.

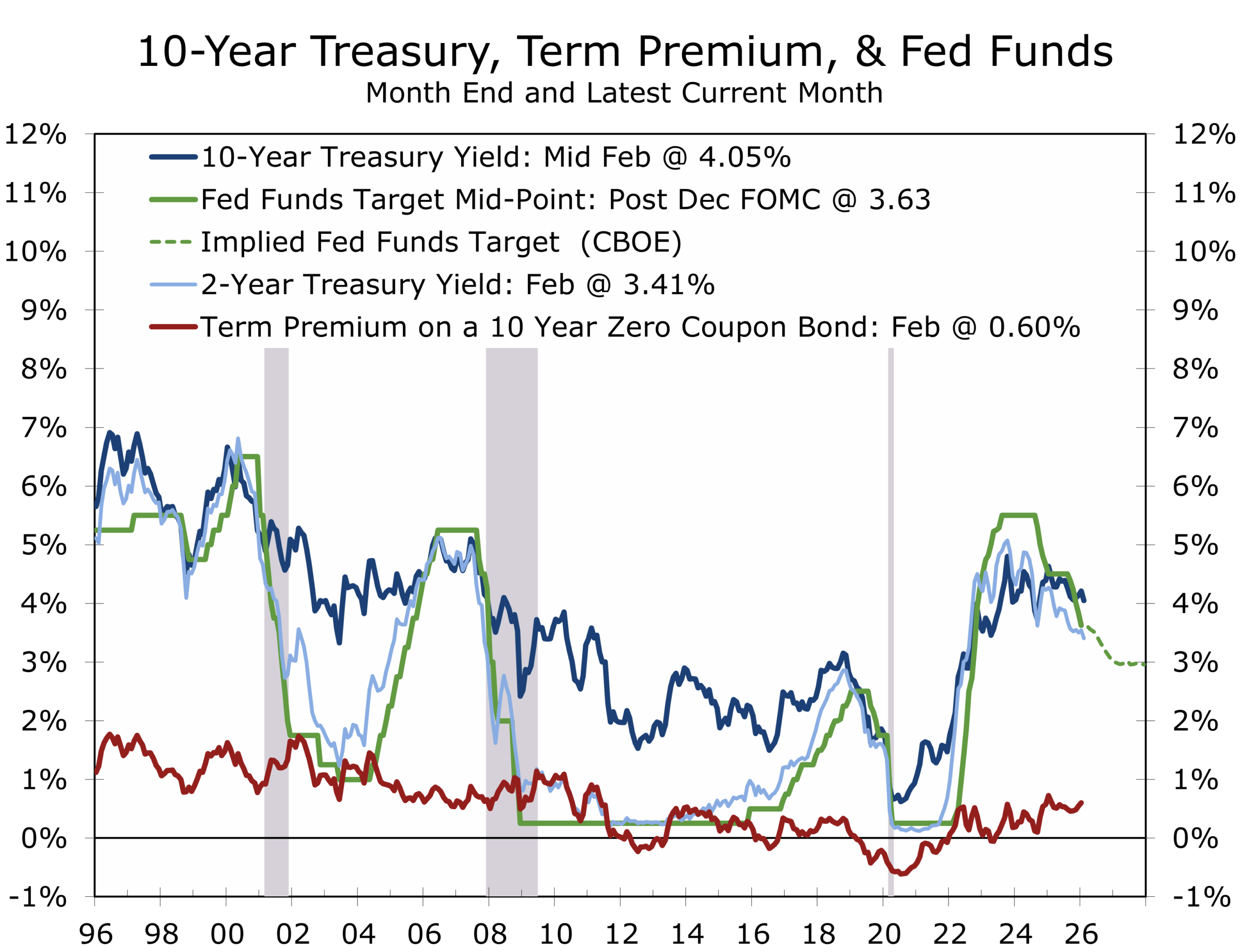

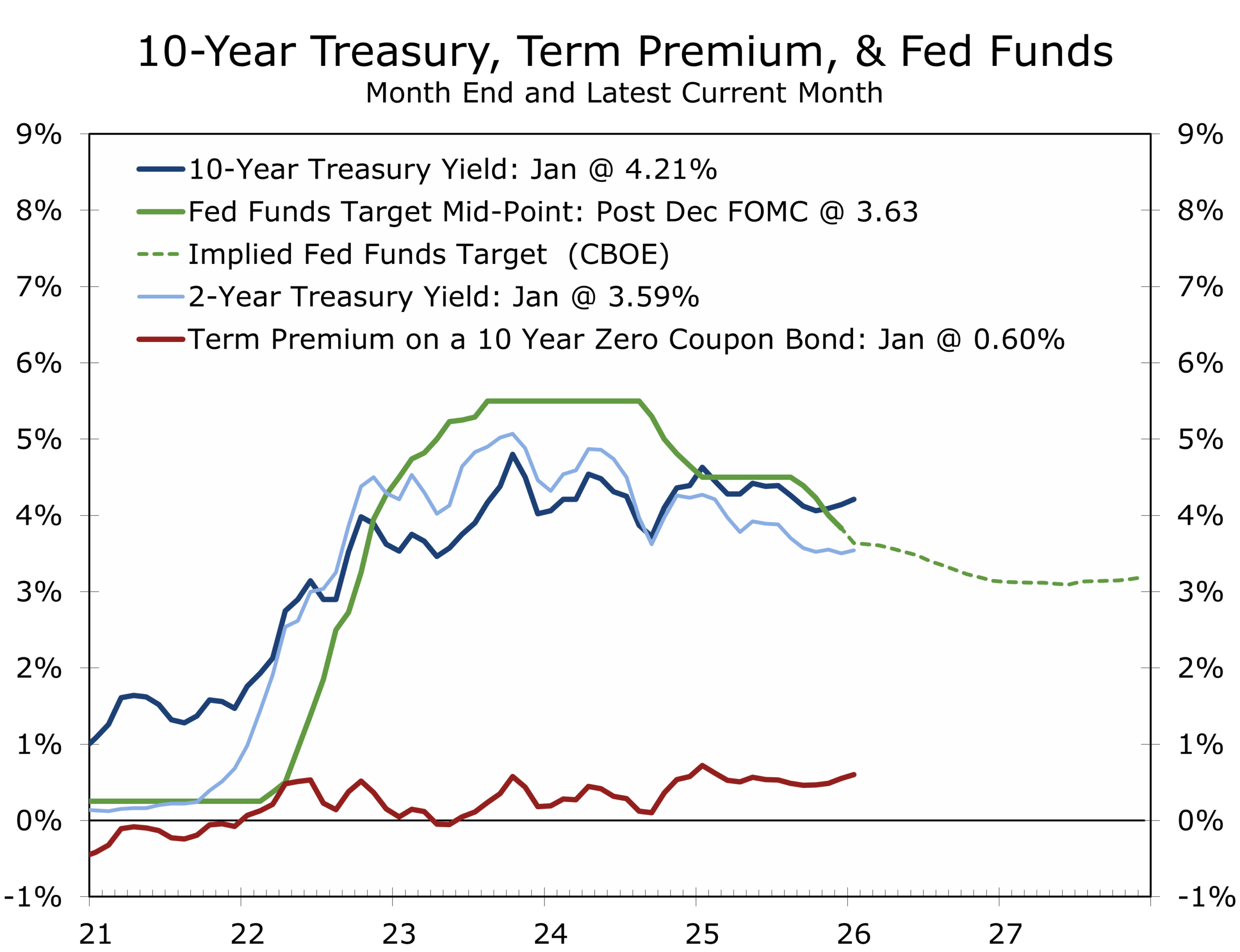

The bottom line is that the breakeven pace of job growth has declined from a year ago. That lowers the threshold for maintaining a steady unemployment rate, but it also means the Fed may have less room to cut rates aggressively. We still expect easing later this year, but likely not to the extent or duration currently priced by markets.

A Cyclical Rebound vs AI-Related Compression

January’s 130,000 payroll gain, powered by a 172,000 rise in private-sector jobs, cleared a far lower bar than in prior cycles. With working-age population growth curtailed by demographics and reduced immigration, January’s job growth pulled the unemployment rate dipped to 4.3%, as new and re-entrants were absorbed. Other early cyclical green shoots were also evident: manufacturing added 5,000 jobs, temporary help services stabilized, average hours worked rose, and the unemployment rate.

Yet breadth remains strikingly narrow. Healthcare and social assistance drove approximately 95% of total gains (approximately 124,000 jobs), with most other sectors flat or negative. Ongoing heavy capital investment in AI infrastructure, advanced manufacturing, reshoring, and grid modernization continues to drive output while adding relatively few workers. AI adoption is directly displacing some labor demand without widespread layoffs, further compressing the sustainable pace of hiring.

The labor market is stabilizing, not broadly reaccelerating. Modest cyclical improvement is emerging atop a structural, productivity-driven foundation, but limited breadth and persistent AI-related restraint point to only modest upside. Downside risks to labor demand have eased while the potential for a cyclical rebound has increased.

Disinflation Broadens

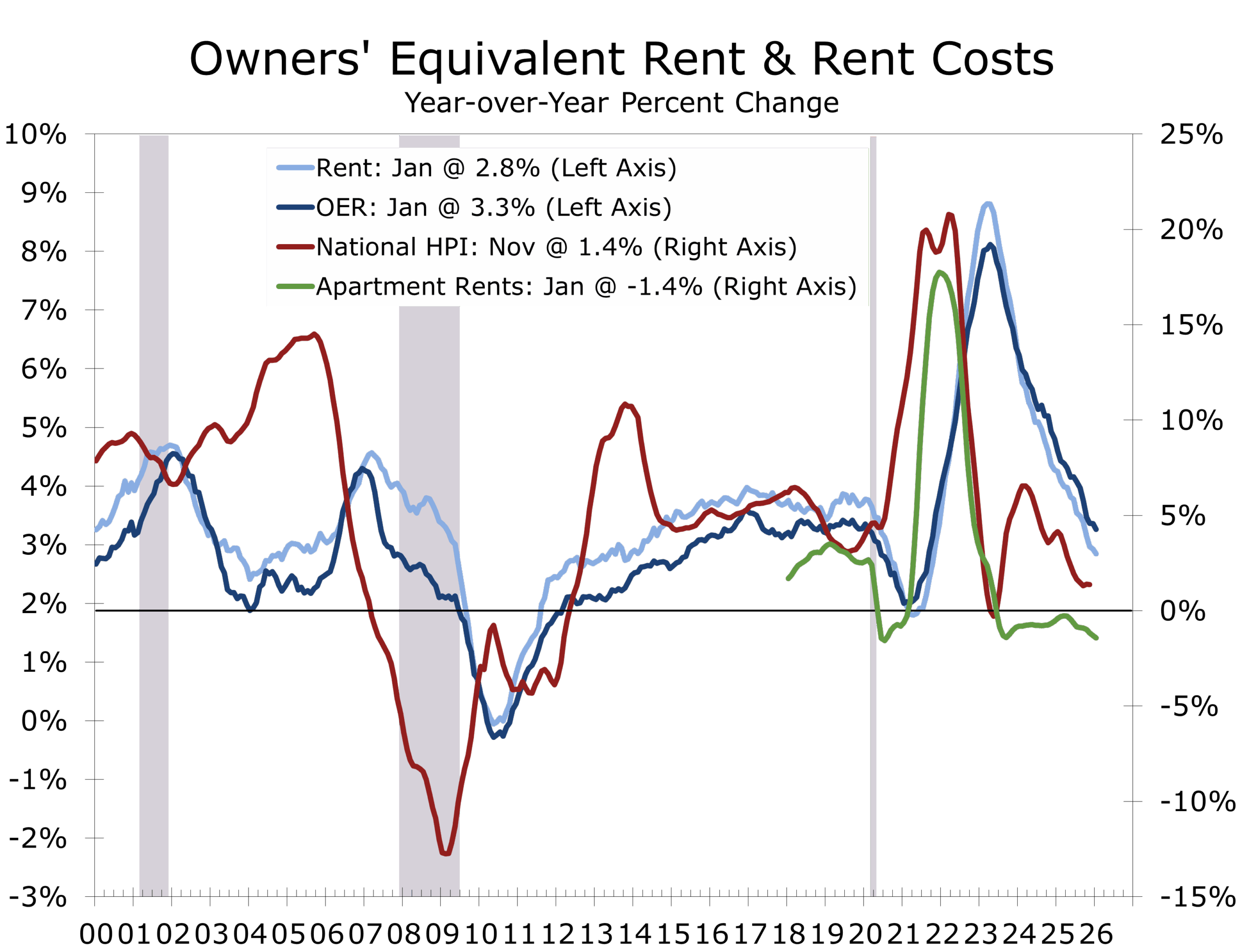

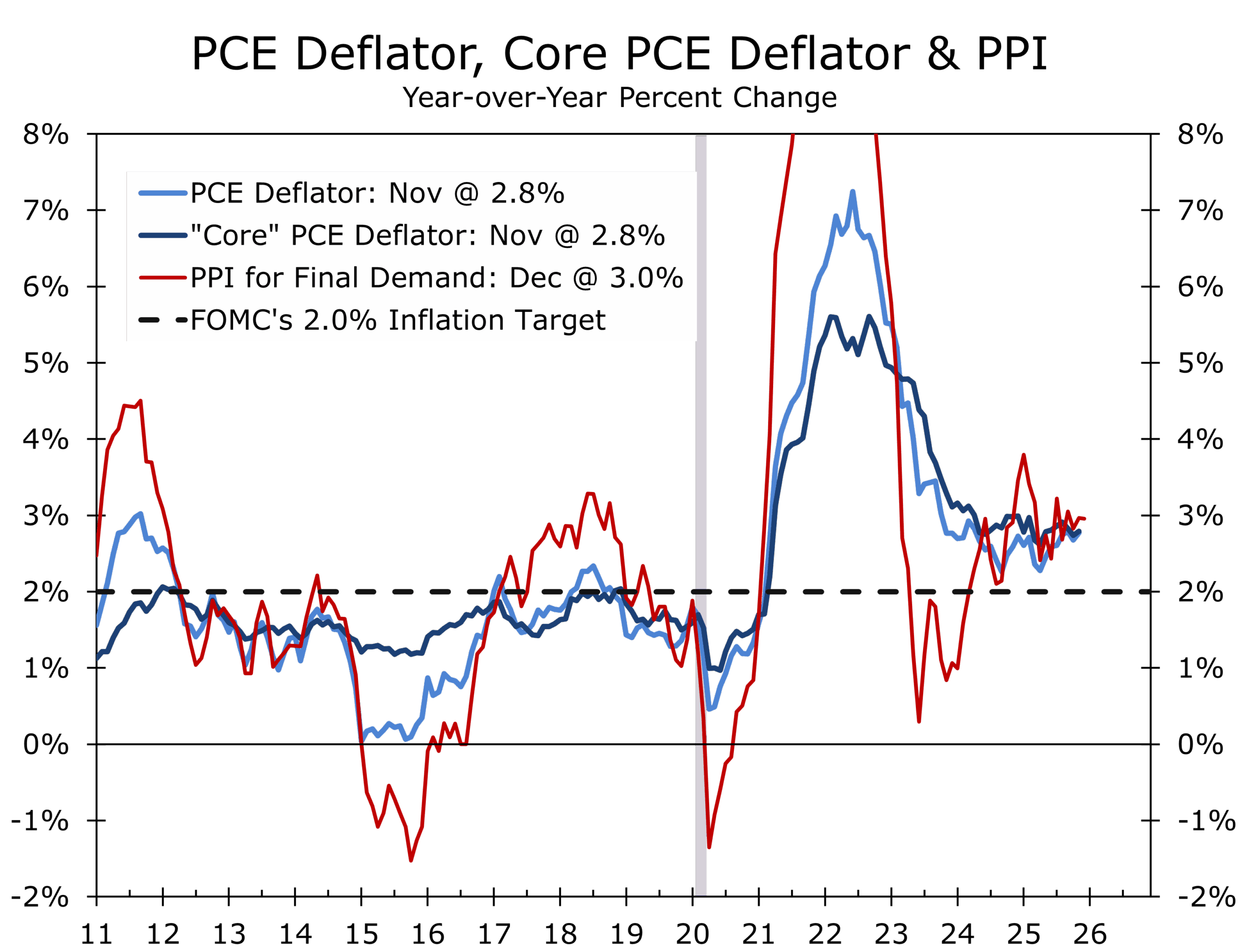

January’s CPI report reinforces the disinflation trend. Headline inflation eased to 2.4 percent year over year and core inflation held at 2.5 percent. Energy prices declined during the month, helping suppress the headline figure, while shelter rose just 0.2 percent and continues to trend lower on a year-over-year basis.

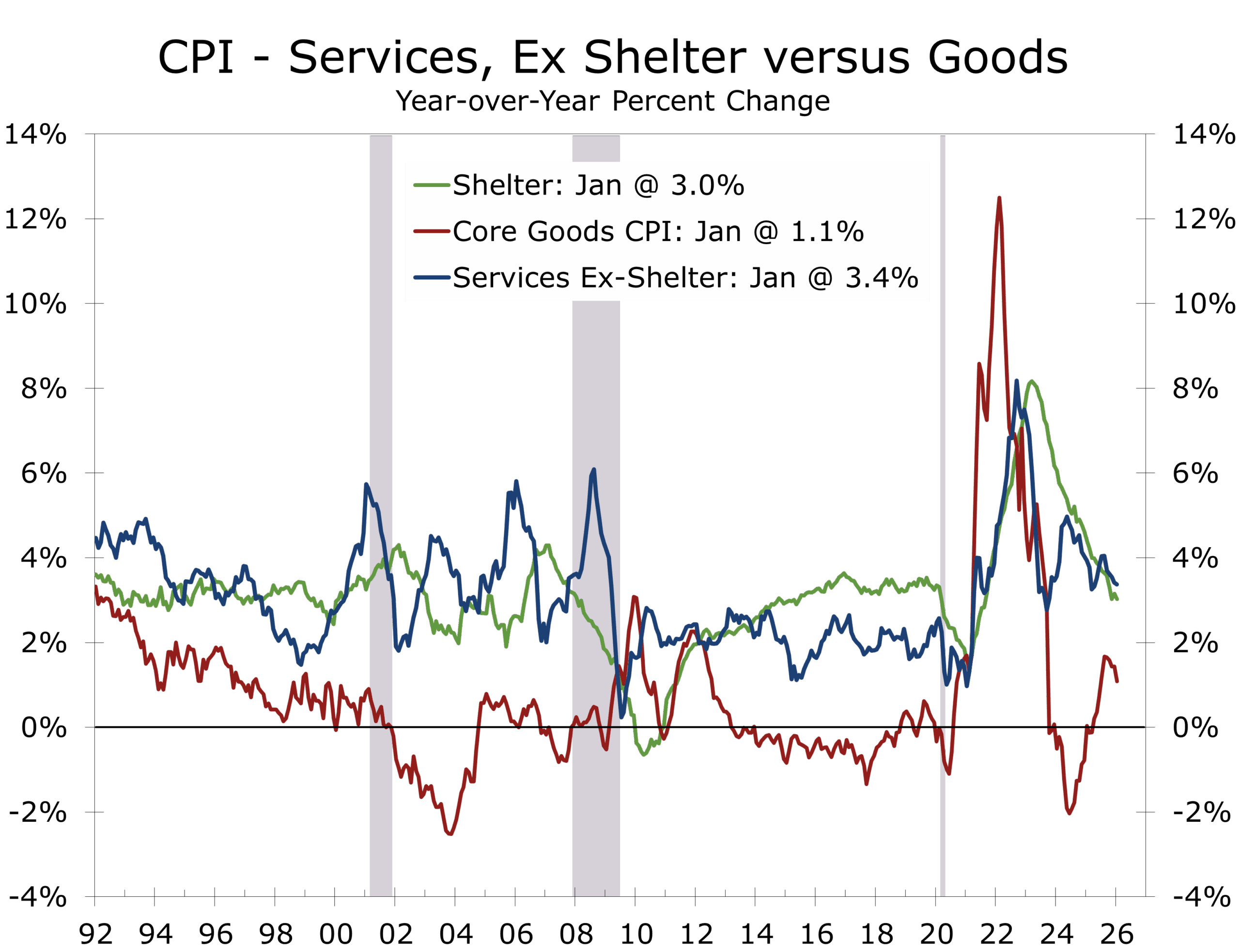

Core goods inflation remains contained, with most tariff pass-through effects now behind us. Services inflation is still firmer than the Fed would prefer, but the breadth of pressure is narrowing. Inflation is no longer broad based. It is concentrated and gradually converging toward target.

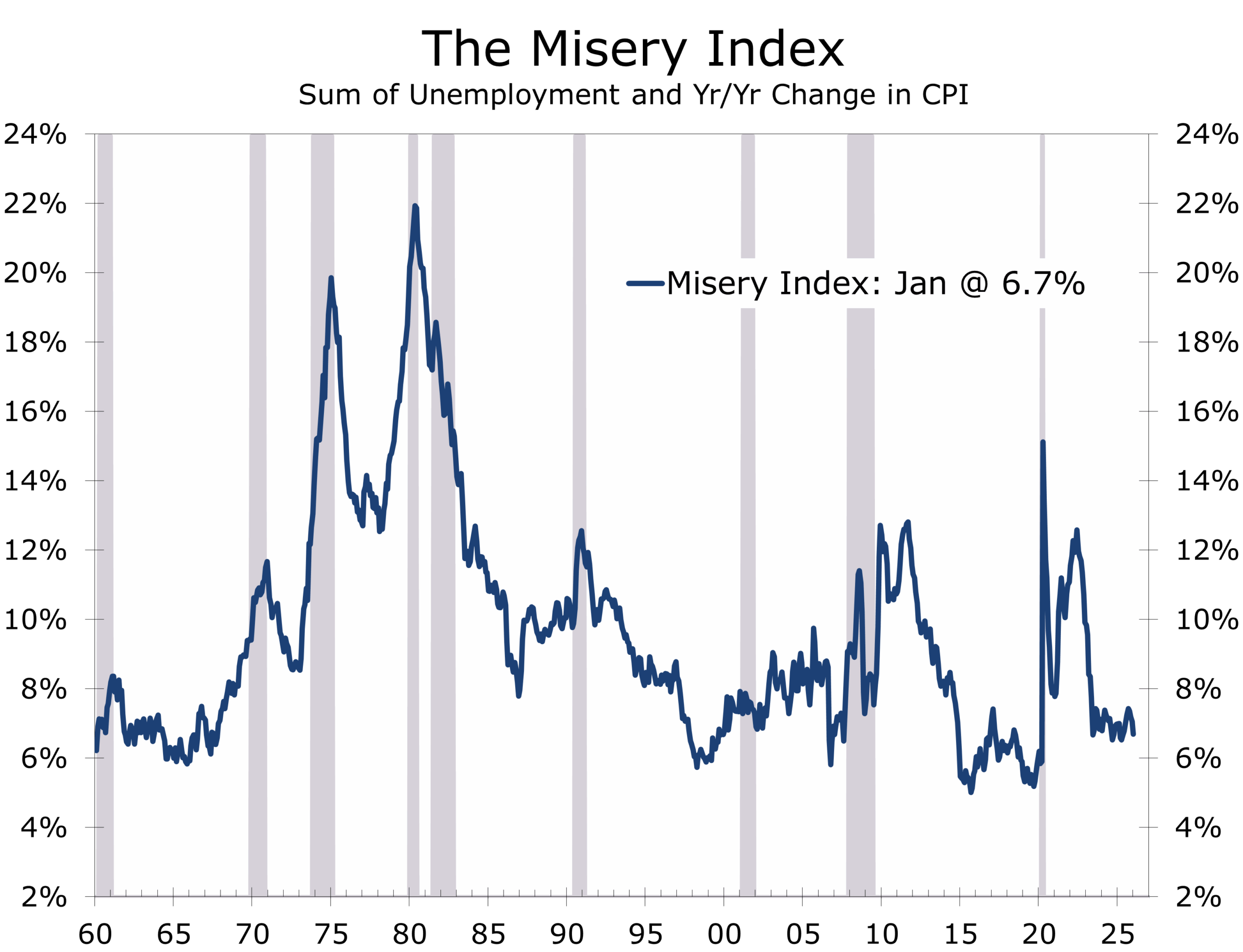

The Misery Index, defined as the unemployment rate plus inflation, has now fallen below where it stood when President Trump took office. Lower inflation and a stable labor market have materially reduced overall economic strain.

This gives the Federal Reserve flexibility, but not urgency. Rate cuts before mid-year would likely require clearer evidence of further disinflation. For now, policy remains positioned to hold steady throughout the first half of the year, with easing possible later if trends continue.

If sustained, the improved economic backdrop could begin to reshape expectations heading into the midterm elections. Sentiment tends to lag the data, but better fundamentals eventually matter.

Consumer and Housing: Weather, Not Weakness

Consumer spending softened at the start of the year, but the weakness appears more short-term oriented. Overall retail sales were flat in December and core retail sales fell 0.1%. Even after the cooldown, holiday retail sales turned in a solid performance, rising 3.7%. December’s drop reflects payback effects from earlier strength and harsh winter weather weighing on activity. Final demand remains supported by steady employment and easing inflation, limiting downside.

This looks like weather distortion and seasonal payback, not a demand pullback.

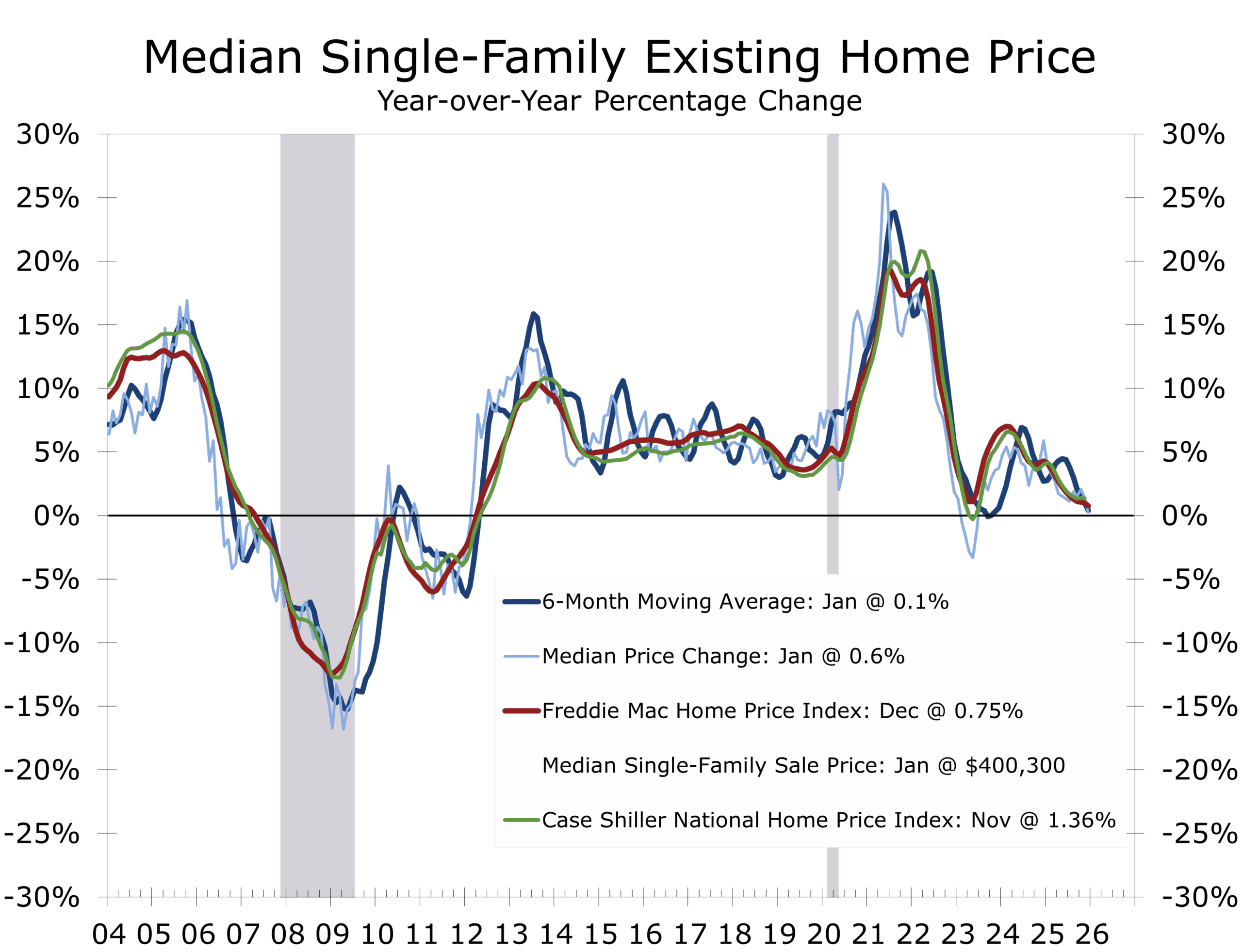

Housing activity also started 2026 on a weak note. Existing home sales fell 8.4 percent in January to a 3.91 million annual pace, well below expectations, with prior months revised lower. Harsh winter weather likely contributed to the decline, and tight inventories compounded the slowdown. For-sale supply slipped again in January and remains constrained, though inventory typically improves heading into spring.

Median home prices fell 2 percent and are up just 0.9 percent over the past year. As mortgage rates ease and labor markets stabilize, sales should gradually climb back. We are looking for a solid spring selling season and look for housing to add to economic growth in the second half of 2026.

Markets: Narrative Reset

Strong jobs plus softer inflation would normally lift equities and steepen yield curves. Instead, stocks weakened and Treasury yields declined. Recent volatility reflects a shift in market narrative more than deteriorating fundamentals. Despite encouraging jobs and inflation prints, investors are cautious about AI’s disruptive potential, with headline tech and broader indexes struggling to trend higher amid sector rotation and valuation pressures.

Markets are shifting from “limitless AI” to “measured productivity,” and the transition is inherently volatile.

Narrative fatigue has replaced 2025’s “limitless AI” optimism with a more selective “measured productivity” stance, as market participants debate which industries will benefit or be disrupted. At the same time, tighter labor supply driven by slower immigration and aging demographics is lowering the breakeven pace of job growth, complicating the narrative about job destruction.

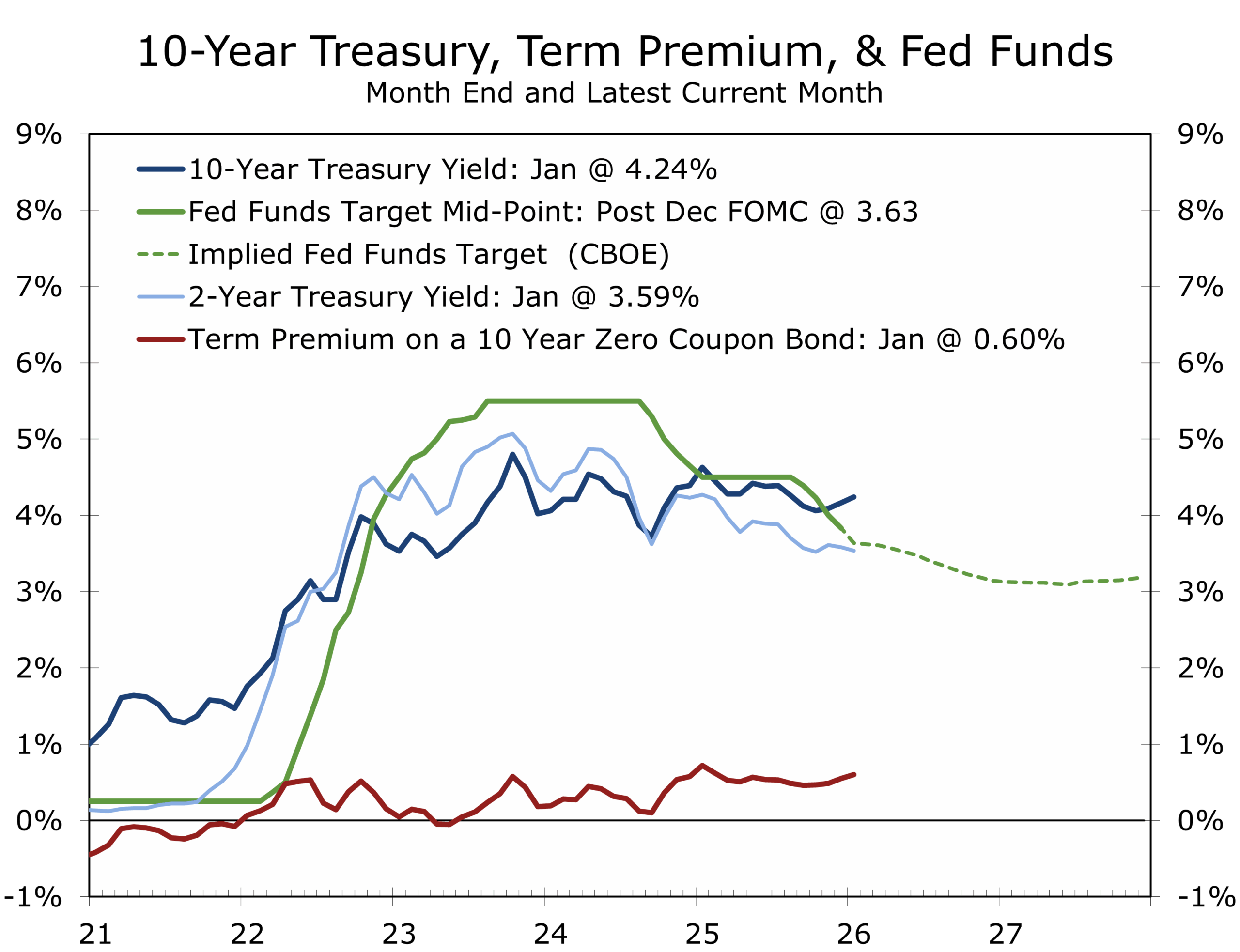

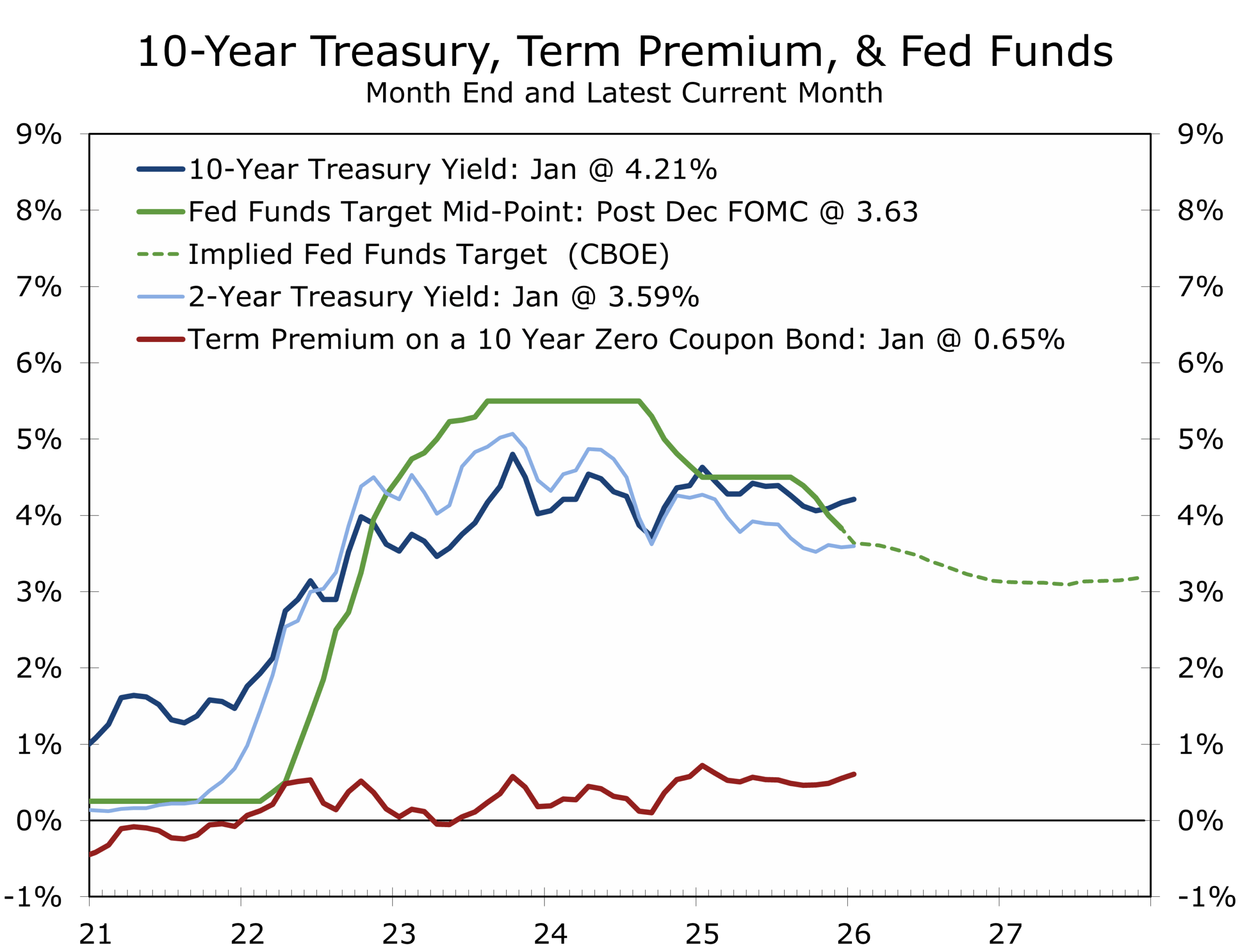

Funding Windows in a Range-Bound Rate Environment

With the Fed likely on hold in the first half and easing only probable in the second half, funding costs remain range-bound but elevated. Upside labor surprises could push front-end yields higher and flatten the curve again, while downside surprises could pull rates lower and create opportunities to lock in low rates. We expect to see some payback for January’s outsized gain. The true underlying pace of job growth will likely be reflected in the average for the first three months of the year.

If disinflation continues and labor stabilizes near breakeven, the Fed gains room to normalize policy without crisis. But if job openings continue to fall and AI adoption accelerates hiring restraint, the downside risks to growth could climb quickly. In that event, credit spreads would likely widen.

Locking in duration opportunistically remains prudent. Hedge labor and commodity inputs where possible. Monitor openings and hiring rates more than payroll headlines, as lower turnover is a major factor restraining hiring.

Source: National Association of Realtors, Freddie Mac and S&P Cotality

The Piedmont Perspective – A Conflict of Visions: Munich 2026 and the Limits of Design

The Munich Security Conference made clear that geopolitics is no longer episodic volatility or a distant tail risk. It has become a structural input into markets.

In his classic work A Conflict of Visions, economist and philosopher Thomas Sowell contrasted two fundamental worldviews: the “unconstrained” vision, which holds that institutions, markets, and goodwill can gradually reshape incentives and diminish the role of hard power, and the “constrained” vision, which emphasizes enduring limits and trade-offs. Europe’s post-Cold War approach largely reflected the unconstrained vision. Russia’s invasion of Ukraine shattered that assumption, exposing not a lack of resolve but a profound shortfall in capacity: energy dependence, depleted munitions stockpiles, and atrophied defense-industrial bases built on decades of underinvestment.

Energy policy had quietly become security policy. Ambitious climate goals accelerated the retirement of coal and nuclear capacity before alternatives were secured, leaving Russian natural gas as the primary bridge fuel. When the bridge was cut, trade-offs could no longer be deferred: higher costs, weakened competitiveness, and constrained strategic options arrived all at once.

.

For investors, this is not abstract philosophy. Rising defense budgets are reshaping industrial policy across Europe. Energy diversification and reshoring are rewiring supply chains. Sustained fiscal commitments to security are influencing real yields, currency dynamics, and capital allocation.

Geopolitics has moved from tail risk to a key balance-sheet variable.

Durable strategy demands both aspiration and constraint. Markets ultimately reward capacity and production, not intentions or rhetoric.

Parting Thoughts

The macro backdrop remains constructive. Inflation is easing. Labor is stabilizing near a lower breakeven threshold. Housing appears to be bottoming. Business investment remains firm.

The risks sit in two places: labor demand erosion from AI or declining job openings, and market volatility driven by shifting narratives rather than fundamentals.

The signal remains steady. The sentiment is shifting. And the first green shoots of stabilization are visible—but still tentative and fragile.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 16, 2026

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

The Piedmont Perspective – A Conflict of Visions: Munich, Ukraine, and the Limits of Design

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 16, 2026

Mark Vitner, Chief Economist

Piedmont Crescent Capital

Consumer Price Index – January 2026: Energy Suppresses Headline, Shelter Eases Further

While Structural Forces Boost Growth, Cyclical Weakness Is Helping Curb Underlying Inflation

-

- Headline CPI rose 0.2% in January, slowing the year-over-year rate to 2.4%, the lowest since early 2021.

- Core CPI increased 0.3%, leaving core inflation at 2.5% y/y.

- Energy prices fell 1.5%, with gasoline down 3.2%, suppressing headline inflation.

- Shelter rose 0.2%, as falling rents and easing home prices continue to restrain housing costs.

- Core goods inflation remains subdued, reflecting fading tariff pass-through and soft used vehicle prices.

- Services inflation firmed modestly, led by airline fares and medical care.

- Policy signal: Disinflation remains intact, giving the Fed room to cut rates further to support rate-sensitive sectors despite strong headline GDP.

Inflation Continues to Cool — Gradually, Not Dramatically

January’s CPI report confirms that the disinflation process is advancing, though not in a straight line.

Headline inflation eased to 2.4% year over year, down from 2.7% in December. The monthly increase of 0.2% reflects a continued moderation in broad price pressures, even as select service categories posted firm gains.

The story is increasingly one of composition rather than direction. Inflation is no longer broad-based. It is concentrated, uneven, and influenced by a handful of sectors.

Energy is suppressing headline inflation, while the fading impact of tariffs is helping pull the underlying trend lower. Housing costs, once the dominant source of acceleration, are now reinforcing the deceleration.

Inflation is cooling, both on an overall and core basis— and its footprint is narrowing.

Headline vs. Core: Energy Provides Visible Relief

Energy prices fell 1.5% in January, led by a 3.2% decline in gasoline. On a 12-month basis, gasoline prices are down 7.5%, pulling the overall energy index slightly negative year over year.

Energy once again acts as a suppressor of headline inflation rather than a driver. Absent a renewed commodity shock, energy’s contribution should remain neutral to mildly disinflationary in coming months.

Meanwhile, core CPI rose 0.3% in January, leaving the annual core rate at 2.5%. While slightly firmer month-to-month, the broader trajectory remains consistent with gradual convergence toward the Fed’s 2% objective.

Core Inflation: Goods Soft, Services Sticky

The composition of core inflation continues to improve.

Used vehicle prices fell 1.8% in January and are now down 2.0% year over year. Household furnishings declined modestly. Core goods inflation stands at just 1.1% year over year — a far cry from the broad-based goods pressures seen in 2022

Tariff-driven goods inflation has largely run its course. Services are the final battleground.

Retailers have largely worked through higher-cost inventory, and tariff-driven price resets have moderated. Supply chains have normalized, and competitive dynamics are reasserting themselves.

Services remain the primary source of pressure. Airline fares jumped 6.5%, while medical care services rose 0.3%. Recreation and personal care also posted firm gains. Part of this reflects continued strong demand for higher-end services and experiences. We see pricing power ebbing here as well, though at a slower pace than in goods.

Inflation is no longer systemic; it is sector specific.

Shelter: Lower Housing Costs Reinforce the Trend

Shelter rose 0.2% in January, with both rent and owners’ equivalent rent increasing modestly. Year-over-year shelter inflation now stands at 3.0%, down sharply from its peak.

This moderation reflects real market dynamics. Multifamily supply remains elevated across much of the country, particularly in the South and Sun Belt. Vacancy rates have increased. Concessions have become widespread. Lease renewals are resetting lower.

Lower rents and softer home prices are reinforcing disinflation into 2026.

At the same time, home price appreciation has slowed materially as mortgage rates stabilized near 6–6.5%. In several markets, prices have flattened or edged lower. That easing in home price momentum is feeding into OER with a lag.

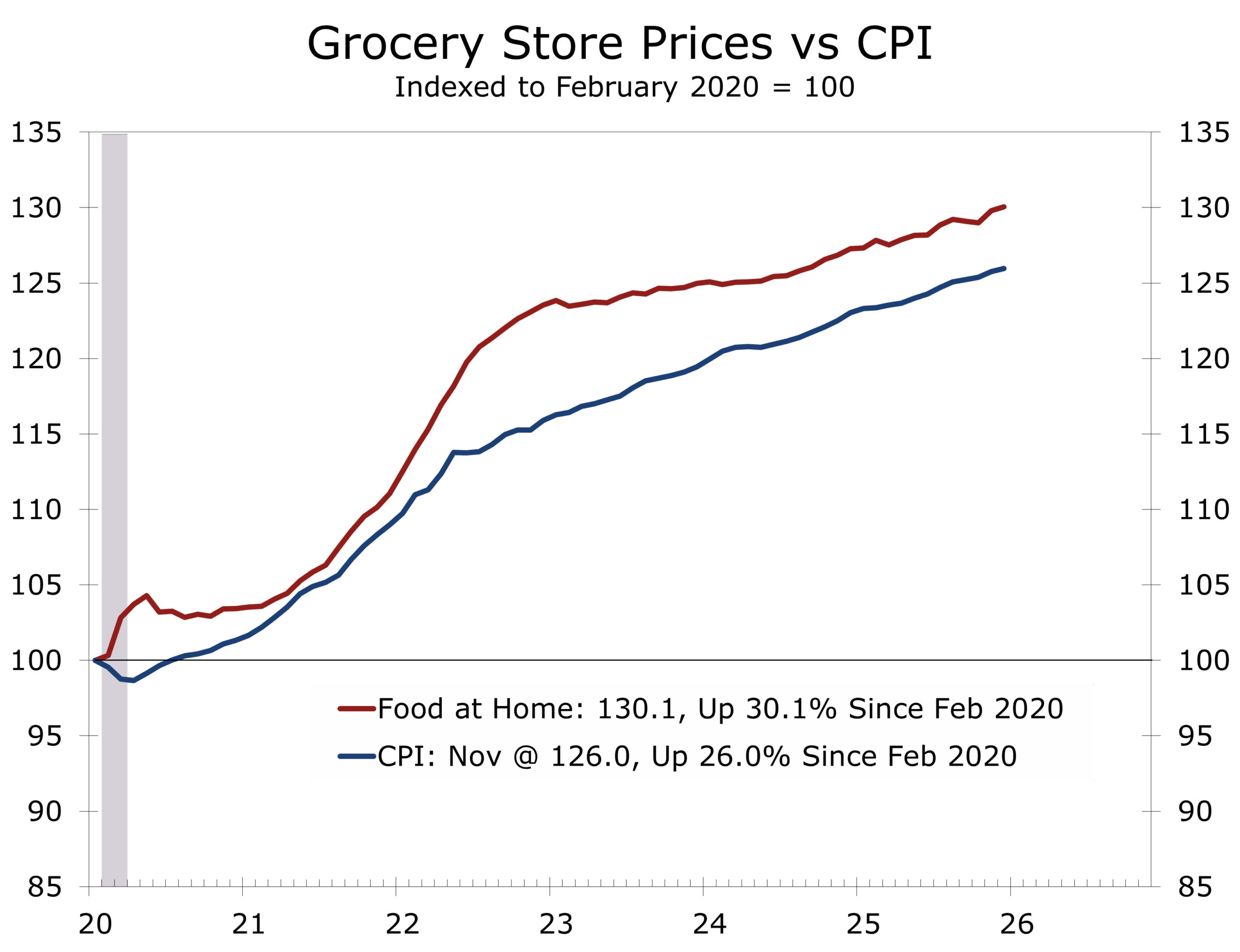

Food Inflation: The Political Economy of Cumulative Prices

Food prices rose 0.2% in January. On a year-over-year basis, food inflation stands at 2.9%, with food away from home still elevated at 4.0%.

The monthly change, however, understates what consumers feel.

At the grocery store, it is the cumulative price level that matters. Food-at-home prices remain just over 30% higher than they were on the eve of the pandemic. Most of that increase occurred during the post-pandemic inflation surge under President Biden, but consumers benchmark against memory, not momentum.

Cumulative grocery inflation, not monthly changes, shapes consumer psychology.

If grocery prices do not moderate further this year, political pressure will intensify — regardless of when the initial increase occurred.

Structural Boom, Cyclical Softness

Real GDP is expected to run strong this year. But the drivers are structural.

The expansion is being powered by:

- AI infrastructure buildout

- Large pharmaceutical investment tied to GLP-1 therapies

- Reshoring of strategic manufacturing

- Revitalization in civilian aerospace

- Defense rearmament

These are capital-intensive, long-duration investment cycles that are ultimately disinflationary.

The cyclical side of the economy tells a different story. Consumer spending on durables remains soft. Housing activity is constrained by affordability. Capital expenditures outside AI, pharma, aerospace, and defense remain cautious.

The weakness in consumer durables and housing is one of the key factors pulling inflation lower. The weakness in cyclical parts of the economy provides the Fed some room to cut interest rates further but not until headline price measures move closer to their long-range target.

Policy Implications: Disinflation Creates Room

With headline inflation at 2.4%, core at 2.5%, shelter easing, and tariff pressures fading, the inflation constraint on monetary policy has eased materially.

Lower inflation is supportive of additional rate cuts, even with strong headline GDP growth. Structural strength does not eliminate cyclical weakness.

Monetary policy operates with a lag. Lower rates would primarily support housing, consumer durables, and cyclically oriented capital investment — the sectors still feeling the effects of earlier restrictive policy.

At this stage, rate cuts are best understood as insurance rather than stimulus. They would move the federal funds rate back toward neutral, or modestly below it.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 13, 2026

Mark Vitner, Chief Economist

(704) 458-4000

January Employment Report: Green Shoots in a Capital-Intensive Cycle

Early Signals of a Spring Rebound

-

- January payrolls surprised to the upside, rising 130,000 — roughly two and a half times consensus expectations.

- Private-sector payrolls jumped 172,000, signaling firmer underlying momentum.

- The unemployment rate edged down 0.1 percentage point to 4.3%, with declines among reentrants and new entrants.

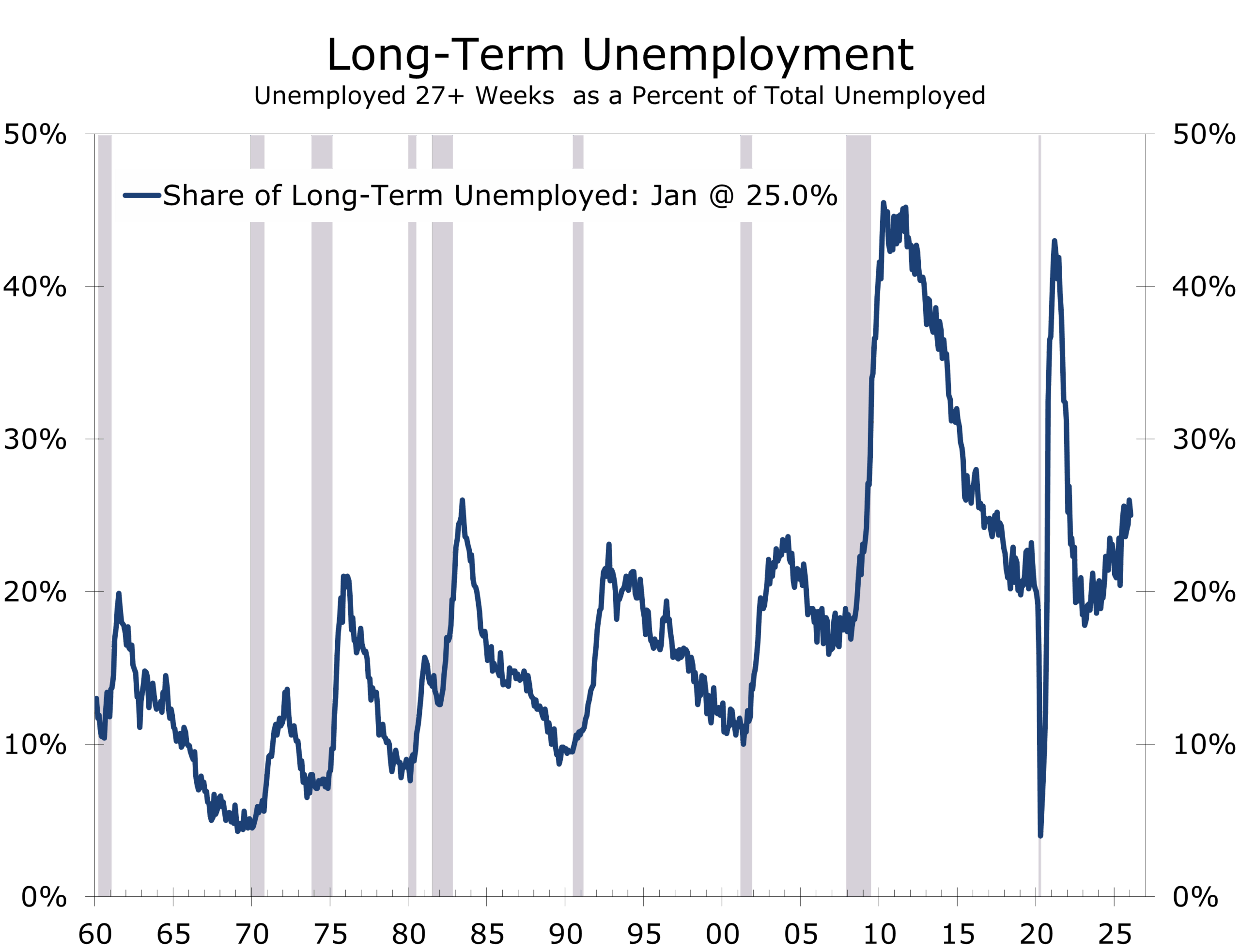

- We see several early signs of a cyclical rebound including a modest drop in the number of long-term unemployed.

- Manufacturing employment rose by 5,000, ending a multi-month stretch of softness.

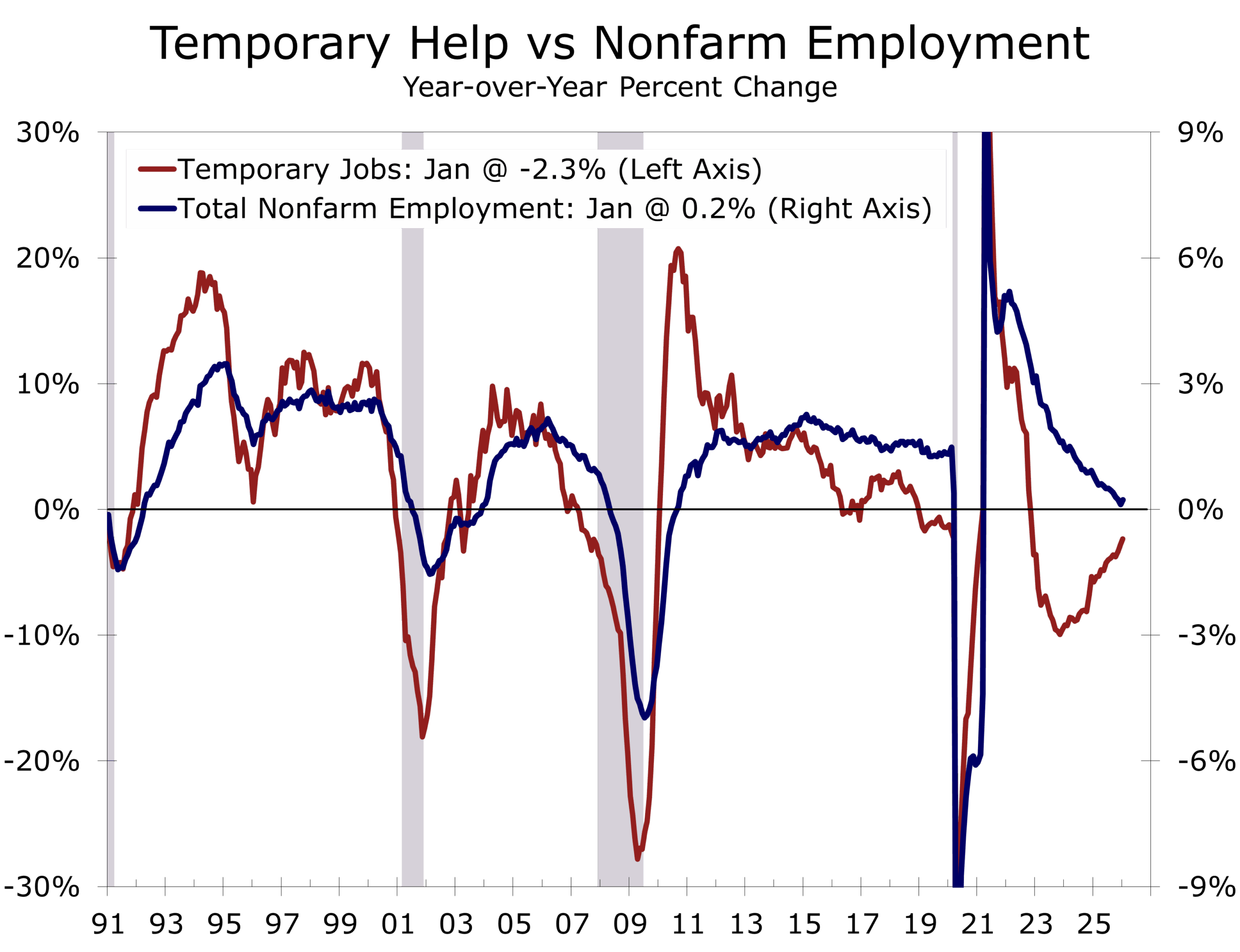

- Temporary staffing employment and average weekly hours improved, both consistent with a cyclical bounce.

- Hiring remains concentrated but may be beginning to broaden.

- We see emerging Green Shoots supplementing what has been a structural, capital-intensive expansion this past year. We expect to see more compelling evidence of this later this year.

January Payrolls: A Firmer Start Than Anticipated

January payroll growth handily exceeded expectations, with employers adding 130,000 net new jobs — roughly twice consensus expectations and materially stronger than our 50,000-job increase forecast.

More notably, private-sector payrolls rose 172,000. The divergence from the headline reflects declines in government employment and underscores firmer hiring within the private economy.

Gains remain concentrated in health care, social assistance, and construction — sectors that have carried much of the employment load over the past year. Demographic trends, infrastructure spending, and reshoring-related activity continue to support hiring in these areas.

Manufacturing employment rose by 5,000 in January, ending a multi-month stretch of weakness. While modest, the increase is notable given the sector’s earlier softness and aligns with improving manufacturing survey data.

Temporary staffing, the sector that predicted the slowdown, is now hinting at stabilization.

Temporary help employment has improved over the past several months. This sector weakened well ahead of the broader slowdown in nonfarm payrolls and often serves as a leading indicator. Its recent firming suggests that hiring may begin to perk up as we move into the spring and summer.

Breadth is not yet robust. But directionally, several indicators are turning less negative.

Subtle but Constructive Improvement

The unemployment rate edged down 0.1 percentage point to 4.3% in January.

The number of unemployed declined modestly, with the reduction occurring primarily among reentrants and new entrants into the labor force. That detail matters. It suggests that job seekers are being absorbed rather than discouraged.

January household data are inherently volatile due to seasonal adjustments and annual updates. Still, the direction of change aligns with other cyclical indicators.

Long-term unemployment declined slightly as well, reinforcing the notion that labor market slack is not building in a meaningful way.

Stability is giving way to incremental improvement.

Taken together with better-than-expected ISM Manufacturing report, these data point toward early cyclical improvement in 2026 — supplementing the structural capital-intensive growth that has defined the past several quarters. We expect these Green Shoots to become more prominent this spring and summer, producing a more durable and more highly visible expansion.

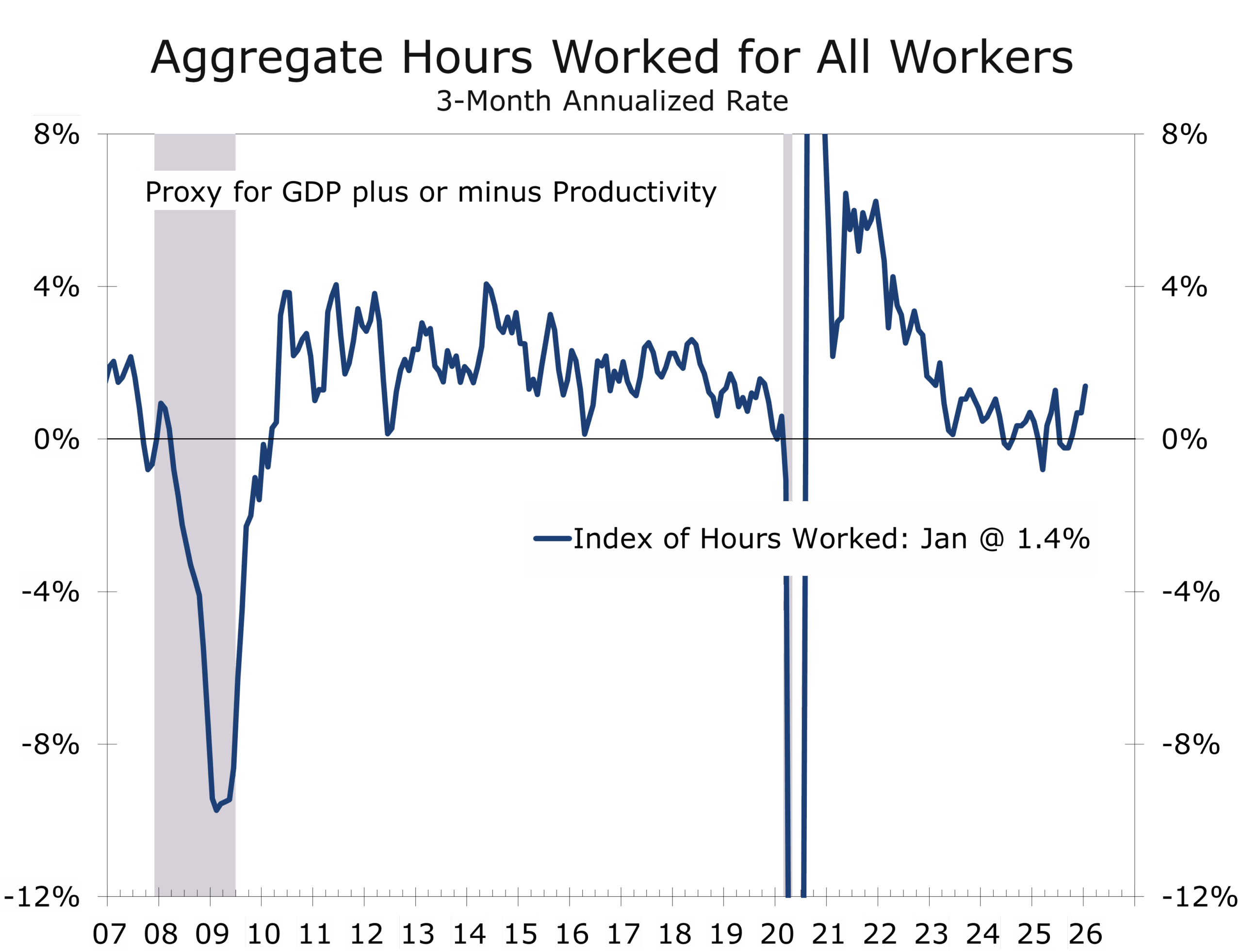

Hours Worked: An Early Signal

Average weekly hours improved in January, and aggregate hours worked rose as well.

Employers typically increase hours before expanding payrolls. When demand begins to firm, firms stretch existing labor first. The improvement in hours reinforces the view that labor demand may be stabilizing beneath the surface.

If sustained, rising aggregate hours support income growth and help stabilize consumption without requiring rapid payroll acceleration.

Hours tend to turn before headcount.

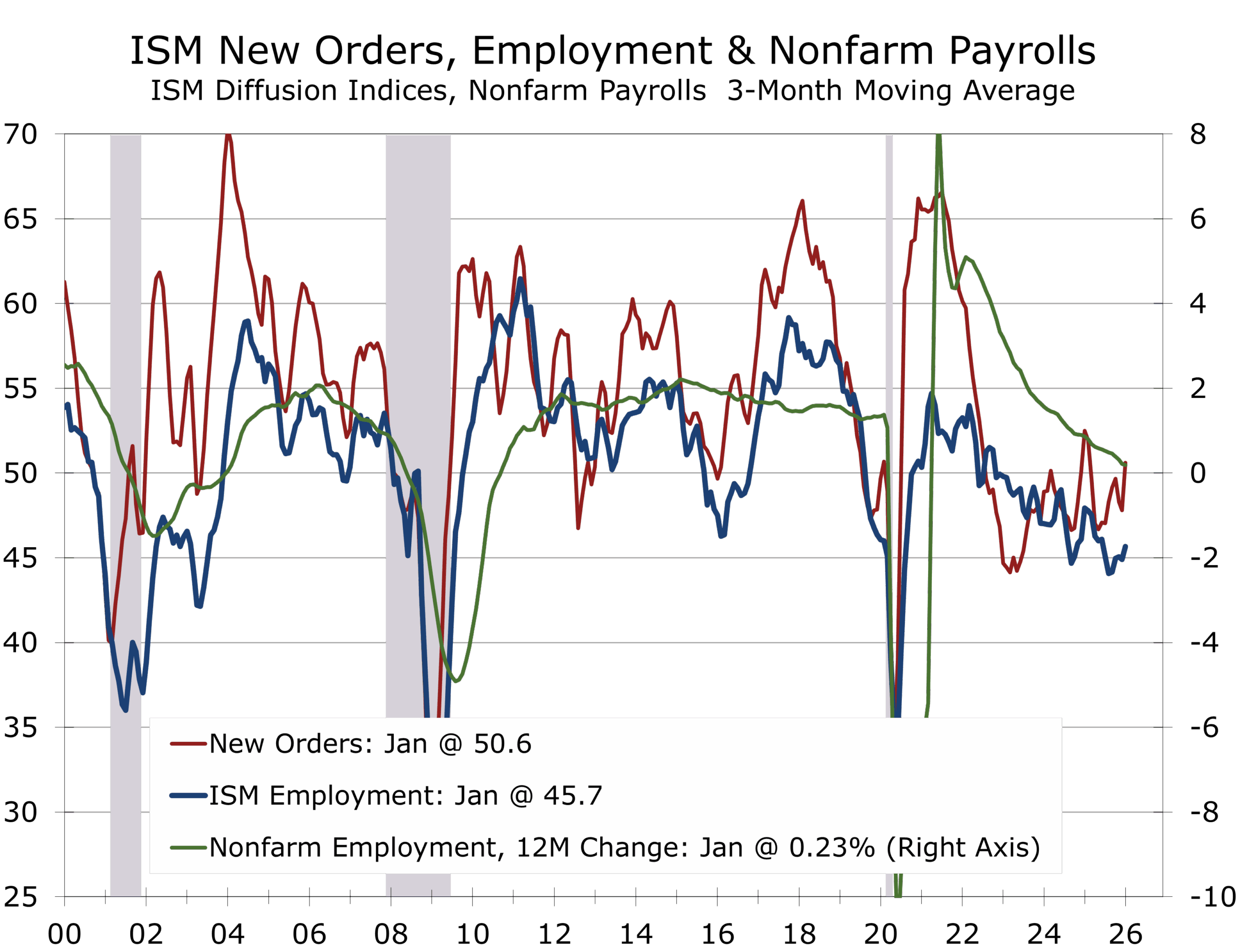

Recent ISM readings surprised to the upside, particularly in the new orders and employment components.

Historically, payroll growth follows sustained improvement in ISM components with a lag of one to three months. The emerging pattern is consistent with that sequence:

- Surveys stabilize

- Hours improve

- Temporary staffing firms

- Payroll growth firms

January’s report suggests that sequence may now be underway.

Structural Protein Meets Cyclical Lift

The broader economy continues to benefit from structural, capital-intensive investment in AI infrastructure, advanced manufacturing, reshoring, grid modernization, and defense-related activity. That investment wave has been productivity enhancing but labor light. January’s data suggests cyclical forces may now begin to supplement that structural base.

Stabilization gives the Fed room to normalize policy and re-energize the expansion.Bottom of Form

Even with the recent eye-popping GDP growth, we are not describing a boom. We are observing Green Shoots emerging within a labor market that cooled but never contracted meaningfully.

Wages and Inflation Context

Average hourly earnings rose 0.4 percent in January, bringing year-over-year wage growth to 3.7 percent. While the monthly increase was firm, the broader trend remains consistent with gradual disinflation and well below peak inflation-era levels.

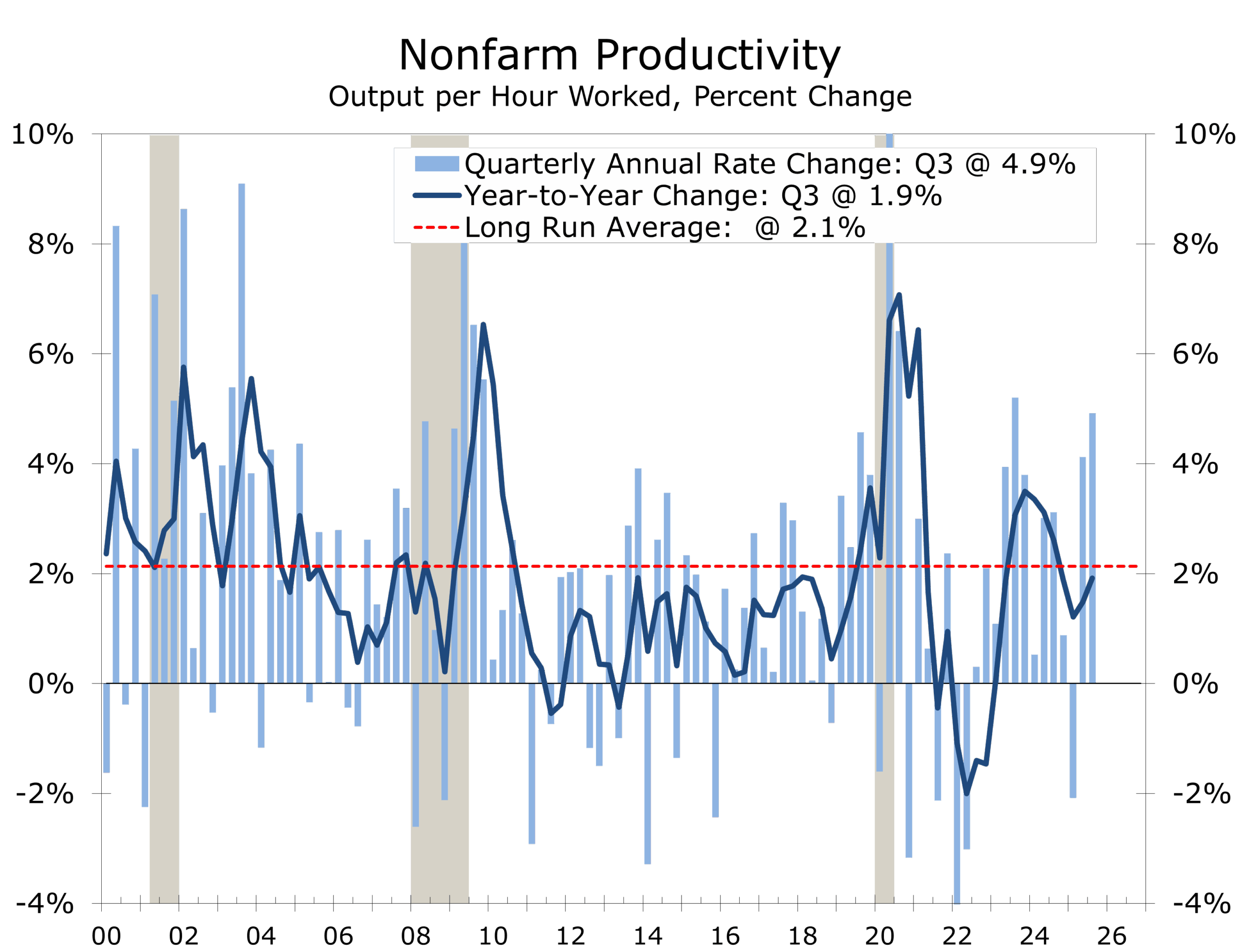

The improvement in hours worked amplifies aggregate income growth without signaling renewed wage acceleration. The combination of firmer hours, stable unemployment at 4.3 percent, and wage growth holding in the upper 3 percent range supports real income gains while keeping inflation pressures contained. When combined with recent productivity trends, aggregate hours worked imply Q1 real GDP is on pace to grow at 3% pace.

For policymakers, this is a constructive mix. Wage growth is no longer the primary source of inflation concern, and income gains are increasingly supported by productivity and improved labor utilization rather than accelerating compensation.

January’s report reduces the urgency for immediate policy easing but does not eliminate the case for further normalization later this year. Modestly firmer hiring, improving hours, contained wage growth, and declining long-term unemployment point to a labor market that is stabilizing rather than overheating.

That distinction matters.

If cyclical indicators continue to firm while wage pressures remain contained, the Federal Reserve gains flexibility to deliver two or even three additional rate cuts over the course of the year. Such moves would not signal weakness. They would reflect confidence that inflation is on a sustainable path lower and that real rates no longer need to remain deeply restrictive.

The current configuration of steady job growth, improving labor utilization, and moderating wage pressures is precisely the environment in which policymakers can ease gradually without reigniting inflation.

Protein built the floor. Cyclical lift may now be adding incremental momentum.

If rate cuts unfold as we expect, the result should be a classic cyclical recovery in interest-rate-sensitive sectors this spring and summer. Lower borrowing costs would likely improve housing affordability and unlock pent-up demand, support light vehicle sales that remain below long-term replacement needs, reinforce spending on household durables and home improvement, and encourage a modest reacceleration in residential construction activity.

The labor market is not signaling boom conditions. It is signaling that downside risks have diminished and that cyclical momentum may begin to complement the structural, capital-intensive expansion already in place. If hiring breadth expands — the 1-month diffusion index rose back above 50 in January — and hours continue to improve, markets may reassess second-half growth expectations. Longer-term yields could stabilize, and credit conditions may ease further as recession concerns fade.

For now, the message is balance. Not overheating. Not contraction. And balance is precisely what sets up a classic cyclical recovery.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 11, 2026

Mark Vitner, Chief Economist

(704) 458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Momentum Without Mastery

Highlights of the Week

- Markets opened the week unsettled by reports that President Trump plans to nominate Kevin Warsh as the next Fed Chair, reviving concerns over balance-sheet discipline and Federal Reserve credibility.

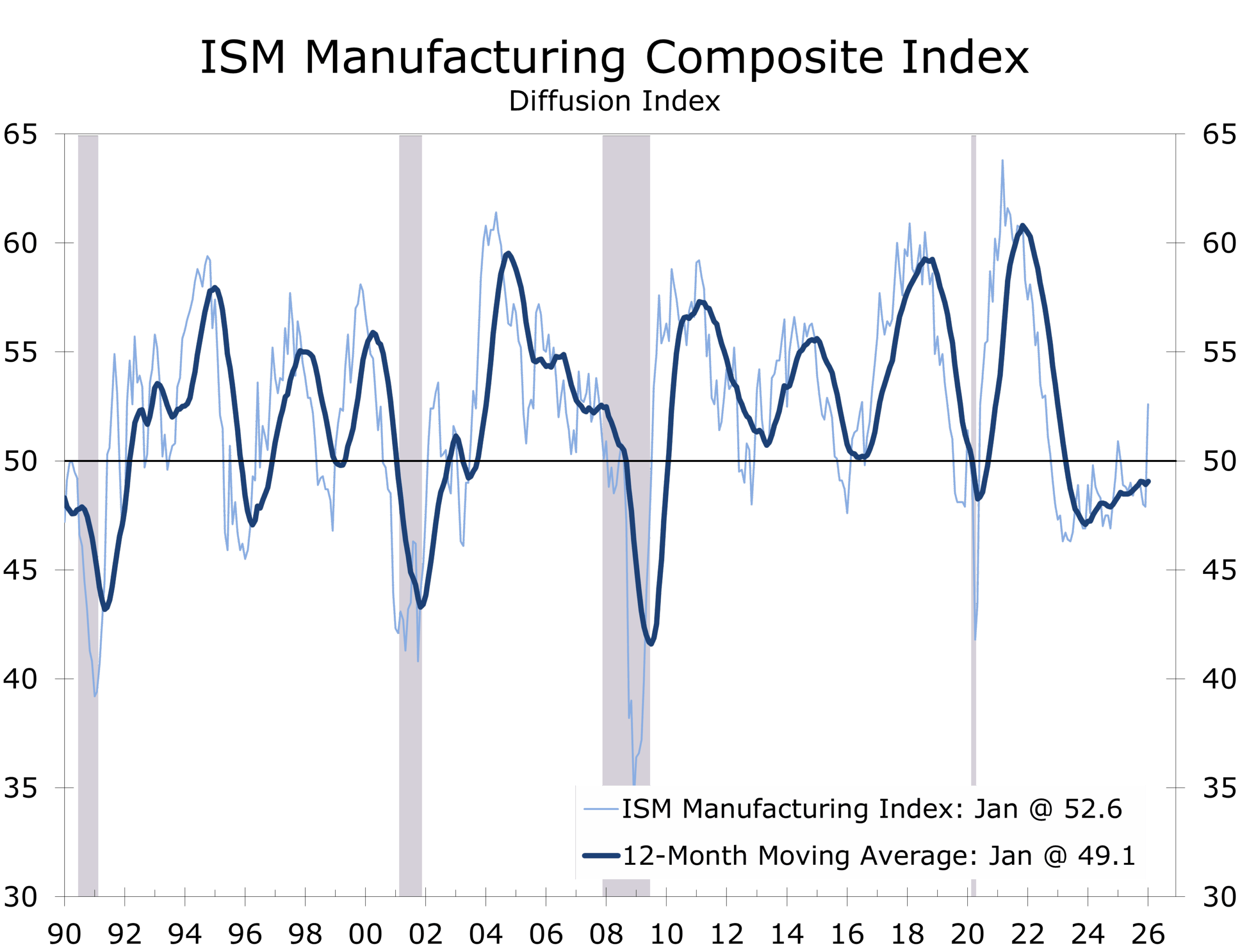

- The ISM Manufacturing Index delivered its strongest reading in three years, possibly signaling tentative improvement after a prolonged industrial slump.

- Labor market data point to cooling through slower hiring and low turnover, not a surge in layoffs.

- Consumer inflation expectations continued to ease across multiple surveys.

- Despite early volatility, the Dow Jones Industrial Average reached an all-time high, underscoring late-cycle resilience and selective risk appetite.

Markets Test the Reins

The week began on uneasy footing after reports that President Trump is considering appointing Kevin Warsh as the next Chair of the Federal Reserve. Markets were quick to dust off old priors. Warsh’s reputation as a balance-sheet hawk revived deeper concerns about whether the Fed is prepared to reassert credibility after more than a decade of extraordinary accommodation. For years, balance-sheet expansion acted as a persistent tailwind for asset prices, compressing credit spreads and suppressing volatility. Even without an imminent policy shift, the prospect of renewed discipline was enough to put investors on notice.

What makes this moment especially difficult to read is that productivity signals are emerging again before confidence, much as they did in the early 1990s. Markets are being asked to price gains that appear real but remain uneven, capital-intensive, and difficult to measure in real time.

Early market weakness was led by technology. Investors continued to reassess the cost, capital intensity, and evolving profit model of the AI buildout. The debate has shifted. AI’s transformative potential is no longer in question; the uncertainty lies in returns, timing, and who ultimately captures the surplus. Software stocks have been particularly vulnerable as investors weigh whether AI enhances pricing power or compresses it through commoditization.

Against that unsettled backdrop, last week’s economic data proved more constructive than early market sentiment implied.

The best ISM Manufacturing reading in three years may signal a turn in the factor sector.

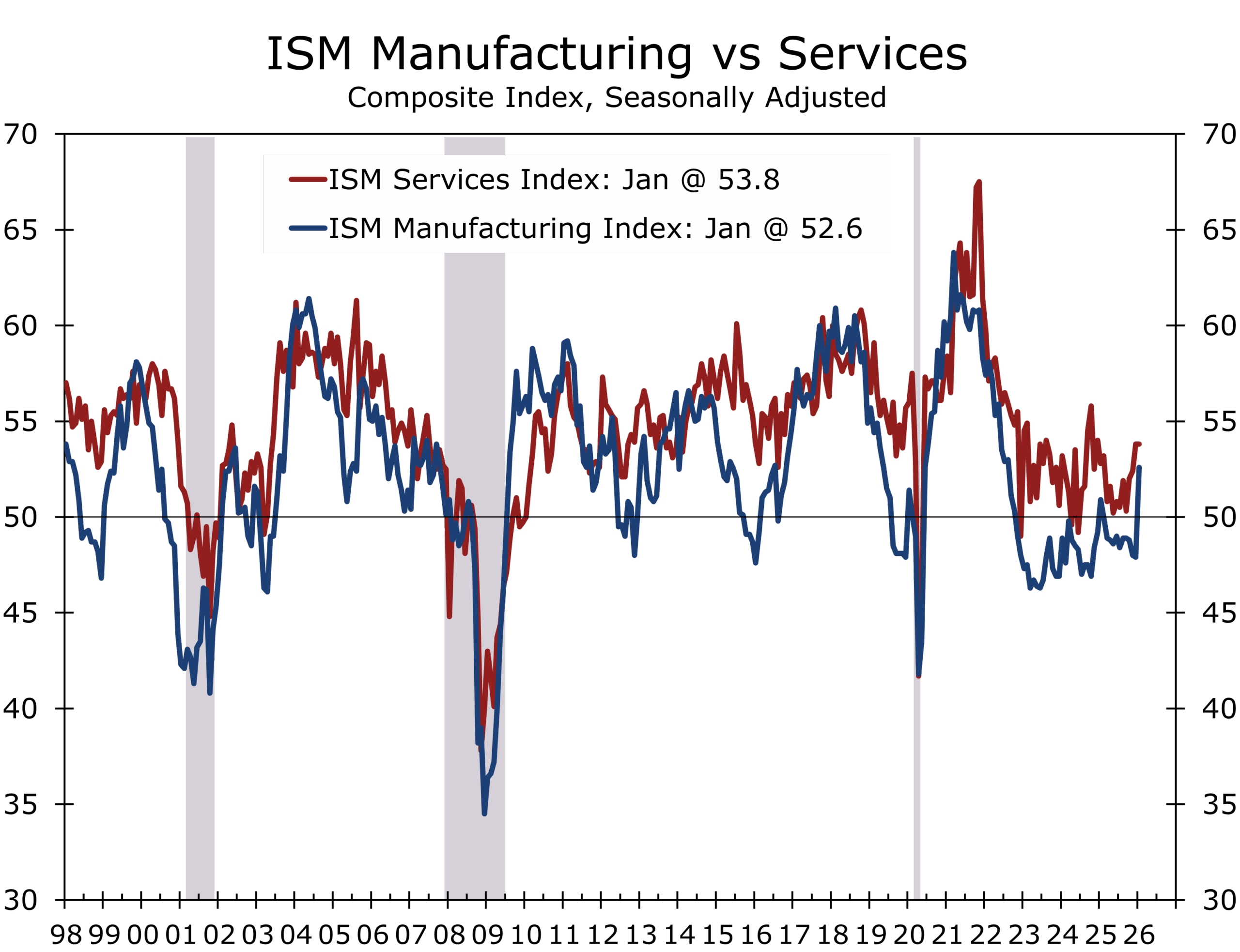

The ISM Manufacturing Index surprised decisively to the upside, jumping 4.7 points to 52.6, its best reading in roughly three years. While activity is now back above the key 50 threshold separating expansion from contraction, the internal composition was notably stronger. New orders and production improved, supplier delivery times lengthened modestly, prices paid remained contained, and inventories stayed lean.

After a prolonged slump, manufacturing appears to be stabilizing, particularly in capital-intensive, defense-linked, and reshoring-oriented segments. A sustained improvement, however, will likely require greater stability on the tariff and trade front.

The ISM Services report was steadier, consistent with a services sector that is slowing but not rolling over. Business activity held firm, while new orders and employment softened. Pricing pressures moderated further. Together, the ISM surveys point to an economy rotating away from post-pandemic excess toward a more sustainable growth profile

Labor market indicators reinforced that theme. ADP private payroll growth came in below expectations, reflecting a gradual downshift in hiring momentum. Job gains remain concentrated in healthcare and population-driven services, while professional and business services continue to lag. Firms are adjusting primarily through hiring restraint rather than layoffs.

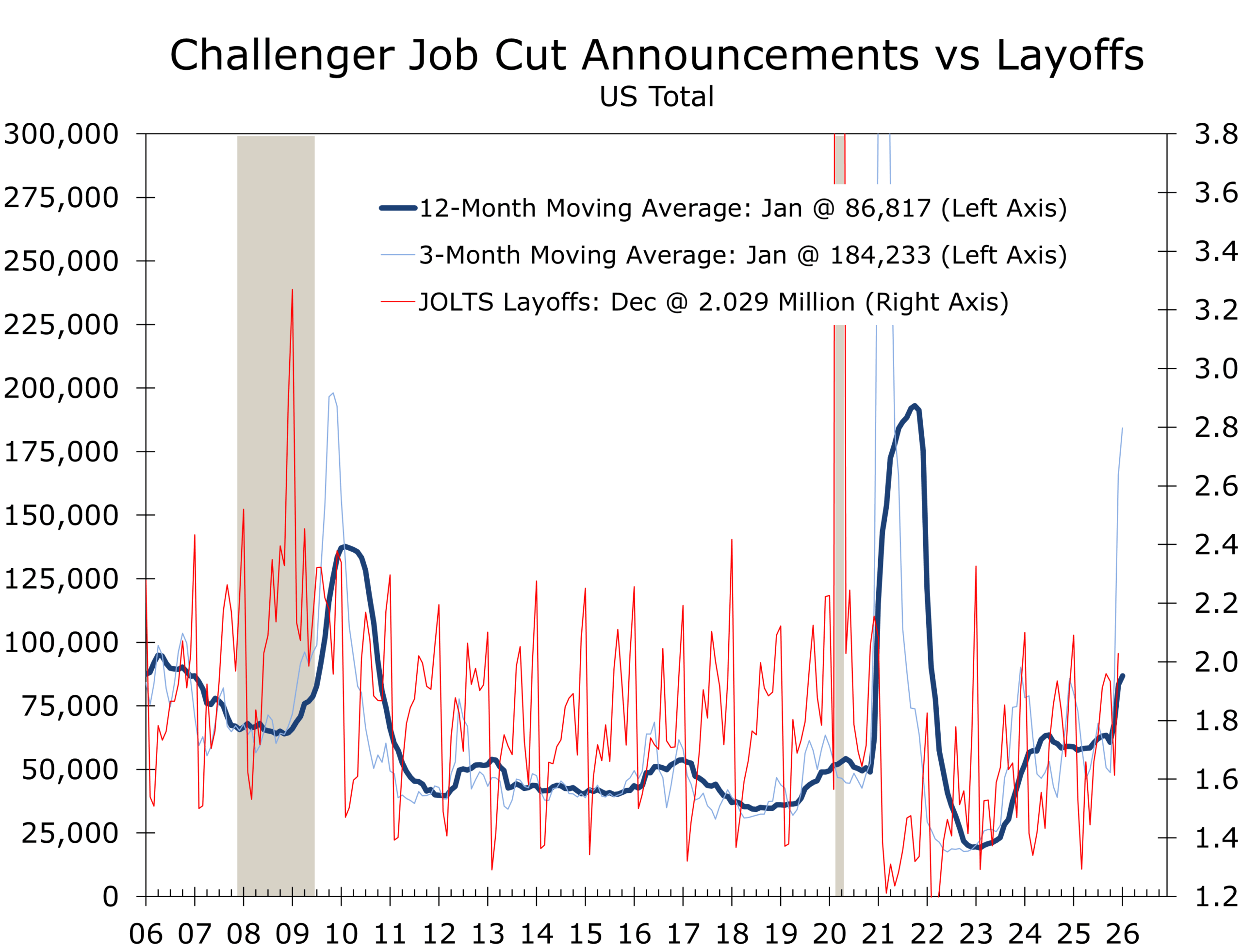

Challenger layoff announcements increased, driven largely by technology and other white-collar sectors. Importantly, these announcements reflect restructuring and productivity initiatives rather than broad financial distress. Layoff levels remain low by historical standards and are not corroborated by required government filings on mass layoffs (WARN notices) or by the Job Openings and Labor Turnover Survey (JOLTS), which shows a far more muted rise in separations.

The start of the year also tends to generate a flurry of restructuring announcements during earnings season, which likely pushed January’s totals higher. Weekly jobless claims rose to their highest level since early December but remain well below recessionary thresholds. Initial claims are drifting higher, continuing claims remain elevated, and labor-market turnover is subdued. Employers across sectors report that voluntary turnover remains exceptionally low. This low-hire, low-fire dynamic helps explain why unemployment pressures can build gradually even as layoffs remain contained.

The labor market continues to cool via less hiring, not more layoffs.

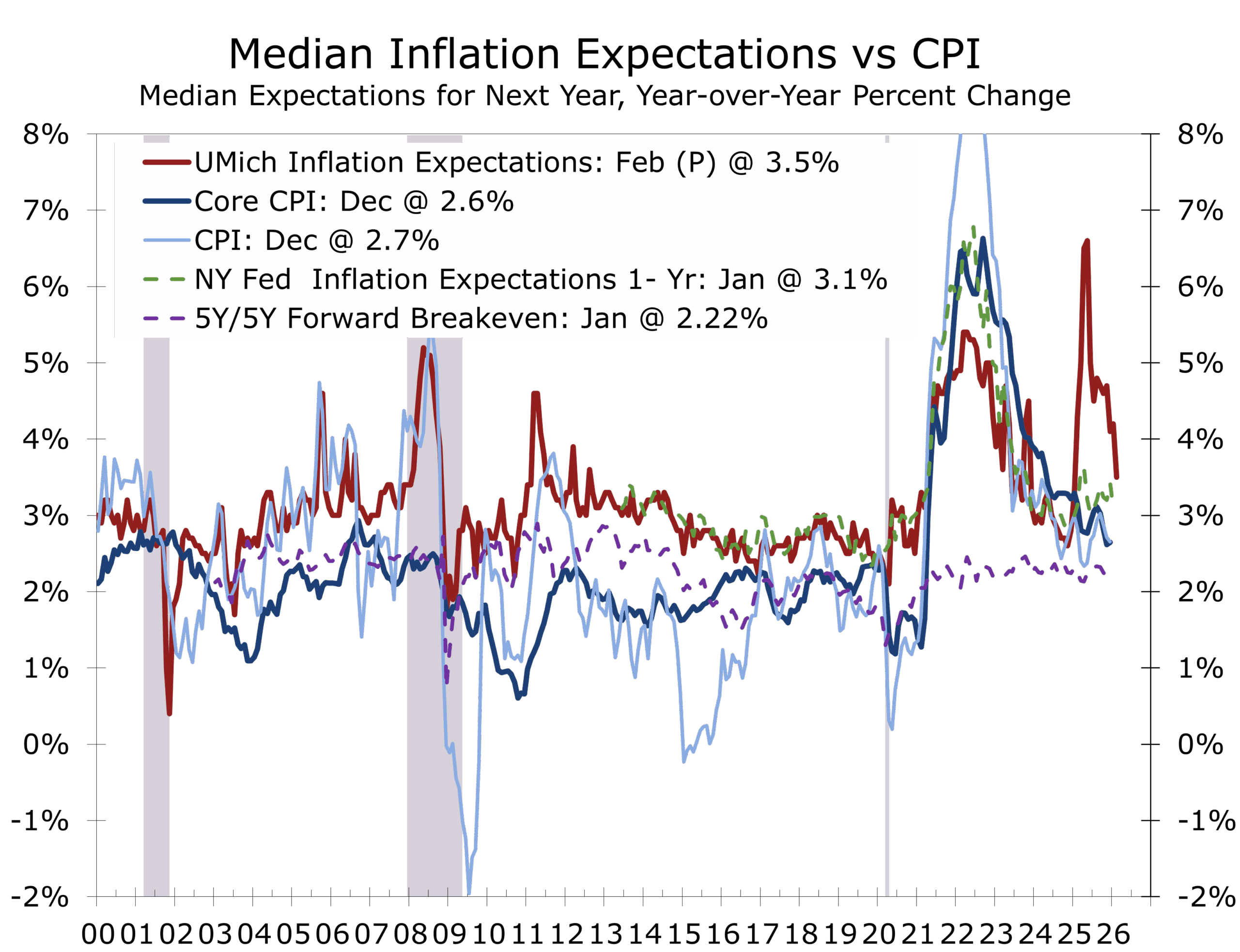

On the consumer side, sentiment data were cautiously encouraging. The University of Michigan survey posted its first significant improvement in headline confidence in several months alongside a sharp drop in one-year inflation expectations. Longer-term expectations edged slightly higher but remain anchored. Consumers continue to report pressure on household finances, but fear of accelerating inflation is fading and will likely slide further in coming months.

That message was reinforced by the New York Fed Survey of Consumer Expectations, which showed further easing in short-term inflation expectations and stable longer-run views. Concerns about credit availability persist, but inflation fears continue to fade.

By week’s end, markets reconciled these crosscurrents. Despite early volatility and lingering unease, the Dow Jones Industrial Average reached an all-time high, reflecting the resilience of large-cap, cash-generative firms. Leadership narrowed, rotation replaced retreat, and durability once again commanded a premium.

Funding, Liquidity, and Capital Allocation

Liquidity risk has re-entered the conversation in a meaningful way. Even speculation about renewed Federal Reserve balance-sheet discipline has reminded markets that monetary accommodation is no longer a background condition. Balance-sheet flexibility, diversified access to funding, and disciplined capital allocation are becoming more important as markets grow less forgiving of leverage that depends on benign liquidity conditions

The era of liquidity as a background condition is fading, requiring greater scrutiny of leverage and capital deployment.

Capital discipline is back in focus. Investors are increasingly scrutinizing returns on invested capital, particularly in AI-related spending where upfront costs are large and payoff horizons uncertain. Firms that can sequence investment and demonstrate measurable productivity gains are being rewarded over those pursuing scale for its own sake.

Labor market softening remains orderly but real. Hiring has slowed, turnover is lower than usual, and adjustment is occurring primarily through restraint rather than layoffs. This argues for cautious workforce planning that preserves critical talent while avoiding commitments based on a broad-based resurgence in demand that has yet to materialize.

Inflation risk continues to diminish. Pricing power is becoming harder to sustain outside essential services and regulated industries, shifting margin management toward cost control, productivity, and procurement discipline. A growing number of food companies are rolling back prices, reflecting consumer pushback as well as subtle shifts in tastes and preferences toward healthier lifestyles.

Finally, selective resilience is creating opportunity. Firms with strong cash flow and modest leverage retain strategic optionality in a more cautious macro environment. That optionality is once again a competitive advantage.

Geopolitical Developments

Geopolitical risk remains elevated but, for now, largely contained from a market perspective. In the Middle East, tensions involving Iran and Israel continue to generate episodic volatility, particularly in energy markets. Pricing behavior suggests investors are assigning a modest risk premium rather than anticipating imminent disruption. The risk, however, is that markets may be extrapolating from recent experience, expecting any confrontation with Iran to resemble limited U.S. involvement in the 12-Day War or the relatively contained Venezuelan operation. That assumption may prove complacent. A direct conflict involving Iran would likely be viewed by its leadership as existential, raising the odds of escalation and materially greater disruption to energy flows and regional stability.

Markets are pricing geopolitical risk as a premium rather than a shock, a posture that leaves little margin for escalation.

The conflict in Ukraine grinds on, reinforcing Europe’s longer-term recalibration toward higher defense spending, energy security, and industrial resilience. Both sides increasingly appear to be waiting for a more favorable negotiating position, with Ukraine’s leverage arguably improving over time. While the war remains economically consequential, its marginal impact on global markets has diminished as it has become embedded in baseline expectations.

In Asia, recent Japanese election outcomes provided a measure of political clarity while renewing longer-term questions around fiscal sustainability and policy coordination. Markets have treated the results as incremental rather than transformative. Developments in the Japanese government bond market nevertheless remain a useful leading indicator for global duration markets, including the United States.

Taken together, these geopolitical crosscurrents matter less for near-term growth than for financial conditions. They add friction to global supply chains, volatility to commodity markets, and a persistent upward bias to global term premia, an underappreciated constraint in an already liquidity-sensitive environment.

Looking Ahead

The coming week features a dense economic calendar that will test the market’s emerging narrative of cooling growth, easing inflation pressures, and a patient Federal Reserve.

Key releases include retail sales, the January employment report, and the January CPI report. Retail sales will offer an important read on whether easing inflation expectations are translating into firmer real spending or whether consumers remain cautious amid slower job growth and tighter credit conditions.

The employment report will be closely watched for confirmation of slower payroll growth, revisions tied to the annual benchmark update, and signals from wages and the unemployment rate. We are expecting substantial downward revisions to the previous data but the recent ADP data hint that the recent payroll data could show more resiliency.

The CPI remains the key element to the policy outlook, particularly as seasonal factors and tariff-related distortions complicate the near-term inflation picture. January oftentimes surprises to the upside as firms rush to implement price hikes at the start of the year.

In addition, the week features a heavy slate of Federal Reserve speakers, including Governors Waller and Miran, Vice Chair Bowman, and several regional Fed presidents. Markets will be listening for clarity on how officials are balancing slowing labor momentum against inflation that clearly appears to be decelerating but remains above target, and whether balance-sheet policy is beginning to re-enter the discussion more explicitly.

Taken together, this week’s data and commentary should help determine whether last week’s resilience hardens into confidence, or whether volatility remains the dominant feature of a Year of the Horse still finding its stride.

The Piedmont Perspective – Breaking in the Horse

The Year of the Horse is rarely about comfort. It is about motion, force, and the test of control. Historically, such periods expose imbalances rather than resolve them. Both 1978 and 1990 were years of disruption, marked by inflation, recession, geopolitical shock, and policy uncertainty. The payoff, when it came, arrived later.

That history resonates today. Productivity gains are real, but uneven. As in the early 1990s, they are showing up first in capital-intensive sectors and operational processes rather than in headline data or confidence measures. Markets are struggling to price gains that are still being discovered.

The risk is not that this expansion lacks power. It risks outrunning understanding. When liquidity expands faster than productive capacity, markets move quickly and often misprice risk. When credibility weakens, momentum does not slow. It veers. Record index levels can coexist with uncertainty when prices run ahead of comprehension.

This expansion is not broken. But it has not yet been fully broken in. The task for policymakers is to reassert credibility without choking off productivity gains that are quietly reshaping the economy. The task for investors and executives is to listen carefully for those signals, while avoiding the noise that surrounds them.

In the Year of the Horse, credibility is the saddle, liquidity is the rein, and productivity determines whether the ride ultimately rewards patience or punishes excess.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 9, 2026

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Confidence, Credibility, and a Job-Light Expansion

Highlights of the Week

- The economy continues to expand above trend, but confidence is deteriorating, leaving markets increasingly sensitive to governance and policy credibility.

- Growth is being driven by capital spending and productivity rather than labor or consumer leverage, producing a job-light expansion.

- Inflation is cooling toward trend, but uneven upstream pressures and energy volatility are keeping term premia elevated.

- Kevin Warsh’s nomination refocuses markets on credibility and balance-sheet policy rather than the near-term rate path.

- Corporate behavior has shifted toward paying for certainty as policy, geopolitical, and duration risks crowd the outlook.

The Data Beneath the Noise

This past week reinforced a theme that has been building quietly but persistently. The U.S. economy continues to expand at a healthy pace, yet confidence is eroding. Markets are increasingly pricing governance risk, policy credibility, and term-premium dynamics rather than cyclical deterioration.

From a cyclical standpoint the economy is looking a little stronger, as data continues to surprise to the upside. Business investment remains a clear bright spot, particularly in equipment tied to artificial intelligence, automation, energy infrastructure, and advanced manufacturing. Core capital goods orders rose again in November, reinforcing that firms are still deploying capital even as surveys signal caution.

Most of the other data released in this past week’s holiday shortened calendar reinforced a tension that has been building for months: the economy continues to expand, even as markets behave as though the margin for error has narrowed.

Manufacturing Momentum Breaks Through the Noise

Today’s ISM manufacturing report delivered a decisive upside surprise and reinforced the resilience of the production side of the economy. The headline index rose to 52.6 in January, returning to expansionary territory for the first time in a year. The improvement was broad-based. New orders surged, production accelerated, and the employment component firmed, though it remains consistent with a job-light expansion rather than a hiring boom.

Manufacturing has re-entered expansion. Hiring has not. That gap defines this phase of the cycle.

The stronger ISM report provides confirmation of a capital-driven growth model in which firms expand output through investment, automation, and productivity rather than payrolls. Supplier delivery times lengthened modestly, pointing to firmer demand and emerging capacity constraints. Price pressures edged higher but remain well below prior-cycle peaks. Tariff uncertainty featured prominently in survey commentary, underscoring how policy signaling, rather than demand continues to shape sentiment.

Productivity as the Critical Offset

Productivity growth remains the central stabilizer. Third-quarter productivity held at a strong pace, with gains broad-based rather than confined to technology. That breadth matters. It raises the economy’s effective speed limit and allows growth to run faster without reigniting inflation, even as hiring remains subdued.

The result is a defining feature of this cycle: a job-light expansion. Firms are producing more with fewer incremental workers. Layoffs remain low, hiring remains historically soft, and labor leverage continues to erode. The firewall against recession remains intact, but it is thinner than in past cycles.

The Consumer Split Widens

The sharpest divergence last week came from the consumer. Confidence fell sharply at the start of the year, reaching its lowest level in more than a decade, driven by concerns about prices, tariffs, and job availability. Yet spending continues to hold up.

Consumer spending is holding up. Confidence is not, as worries about the labor market mount.

The explanation lies in a bifurcated consumer. Higher-income, asset-rich households continue to drive discretionary spending, supported by equity gains and accumulated wealth. Lower- and middle-income households remain constrained by the level of prices, not the rate of inflation. Lower inflation helps, but it does not reset affordability.

Piedmont Perspective: Identifying Productivity Gains

Kevin Warsh will step into the Fed chair with a mandate to restore credibility. Markets have translated that mandate into balance-sheet discipline and firmer control over term premia. His immediate challenge, however, will be to recognize productivity gains before they appear in the official data.

Today’s capital-driven expansion is likely to see productivity move past its long-run average.

In the 1990s, productivity surfaced first in margins and capital spending, not statistics. The same pattern is emerging today. Output remains firm even as employment growth slows. Credibility is not preserved by rigidity. It is preserved by recognizing change as it occurs and before it is reported.

A longer standalone version of this Piedmont Perspective is available on our website.

Markets Are Paying for Certainty

Across asset classes, behavior is shifting. Corporate treasurers are locking in funding. Investors are paying for insurance. Energy-intensive firms are prioritizing reliability over price.

Energy markets delivered a parallel signal. Winter weather disruptions stressed grids and pushed wholesale power prices sharply higher in some regions. Energy risk now includes availability and resilience, not just price

Warsh: Credibility First

President Trump’s nomination of Kevin Warsh as the next Federal Reserve Chair resolved one uncertainty while sharpening the market’s focus on credibility and balance-sheet policy. Warsh’s hawkish reputation is well earned but narrowly targeted.

Warsh is hawkish on the balance sheet and inflation, but less so when it comes to growth.

Warsh has consistently drawn a line between interest-rate policy and balance-sheet expansion. His framework allows rates to support real activity as inflation cools while restraining balance-sheet tools that distort capital allocation and weaken institutional credibility.

Inflation continues to decelerate towards trend, but upstream pressures remain uneven, particularly in services and energy-linked categories. Credibility, not complacency, now sets the price of capital.

For treasury teams, this matters. Long Treasuries remain liquid and credit-safe, but they are no longer immune to flow-driven volatility.

Expectations for an aggressive balance-sheet unwind should be tempered. Structural support for an ample-reserves framework remains strong, even as balance-sheet discipline tightens at the margin.

A Crowded Geopolitical Map, With Iran Back in Focus

Geopolitics continue to act as a volatility amplifier rather than a growth shock. Iran stands out as the most immediate source of asymmetric risk, with heightened rhetoric around proxy activity, shipping security, and sanctions enforcement.

The transmission channel is familiar. Energy markets react first, followed by shipping and defense costs, with inflation expectations moving at the margin.

Relations with Canada have also grown more contentious, adding friction to trade, energy flows, and cross-border investment. These are not growth threats, but they add uncertainty in a market already sensitive to policy signaling.

Parting Thoughts

This was not a week about cycles. It was a week about confidence. The data describe an economy that is expanding and cooling gradually, not one on the brink of recession. Markets, however, are pricing governance risk, credibility, and global term-premium dynamics with increasing urgency.

The most important signal did not come from a data release. It came from behavior.

Quiet Data, Missing Payrolls, Loud Signals

The coming week is light on top-tier economic releases but heavy on signaling risk. ISM services, jobless claims, and consumer credit should confirm ongoing expansion rather than alter the outlook.

Notably, the Bureau of Labor Statistics has announced that the January employment report will not be released this week due to the government shutdown. The January data are believed to be complete and will contain revisions dating back to early 2024 and will provide a better read on the current pace of job growth The absence of payrolls data increases the market’s reliance on surveys, high-frequency indicators, and Fed communication.

In an environment where confidence is fragile and positioning is cautious, missing data tends to amplify noise rather than dampen it. For corporate treasurers and CFOs, the message remains clear: this is a market that rewards preparedness, not precise timing.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 2, 2026

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

President Trump Appoints Kevin Warsh: A Balanced Hawk in a Capital-Driven Economy

Kevin Warsh as Fed Chair: Key Takeaways

-

- Credible nomination: Kevin Warsh is a serious, market-literate choice with a clear framework focused on restoring Federal Reserve credibility.

- Targeted hawkishness: Warsh is hawkish on balance-sheet expansion and QE, not reflexively hawkish on growth or rate cuts.

- Misread by markets: The initial market reaction priced Warsh as a broad tightening signal, pushing long yields higher and pressuring risk assets, but that interpretation overlooks his distinction between rate policy and asset reflation.

- Inflation context matters: Inflation has eased toward its long-run trend, but today’s PPI release underscores uneven upstream pressures, reinforcing the need for vigilance.

- Capital-driven economy: The expansion is increasingly powered by capital deepening and productivity rather than consumption leverage, reducing overheating risk.

- Warsh fits this phase of the cycle, inflation vigilant, credibility focused, and increasingly optimistic about capital-led growth. The central risk is not excessive tightening but rather underestimating how much credibility itself has become policy.

Headline Inflation: A Firm Finish to the Year

President Trump’s nomination of Kevin Warsh as Federal Reserve Chair is a strong and credible choice. From a short list of qualified candidates, this outcome appeared increasingly likely. Warsh’s hawkish reputation is well earned, rooted in his focus on inflation credibility and long-standing criticism of the Federal Reserve’s oversized balance sheet. At a time when institutional credibility itself has become a market variable, that focus matters.

Importantly, Warsh’s hawkishness is targeted rather than ideological. He has consistently drawn a line between interest rate policy, which can support real economic activity as inflation cools, and balance-sheet expansion, which he believes blurred the Fed’s mission, distorted capital allocation, and weakened public confidence. That distinction was largely missed in the initial market reaction, which treated the nomination as a signal of across-the-board tightening.

Warsh is hawkish when it comes to the Fed balance sheet but pragmatic about growth.

Today’s Producer Price Index release reinforces why inflation vigilance remains essential. While the broader disinflation trend continues, upstream price pressures remain uneven, particularly in services and categories tied to energy, logistics, and geopolitics. In that context, Warsh’s emphasis on discipline and credibility is less a brake on growth than a necessary guardrail.

The Market’s Initial Read

The immediate market response reflected a shallow interpretation of Warsh as a pure hawk. Long-term Treasury yields moved higher, equities sold off with rate-sensitive sectors leading the decline, and precious metals retraced sharply as the dollar firmed. Crypto assets traded heavy, as liquidity assumptions were reset.

The markets heard “hawk.’ Warsh’s record points to credibility first and flexibility second.

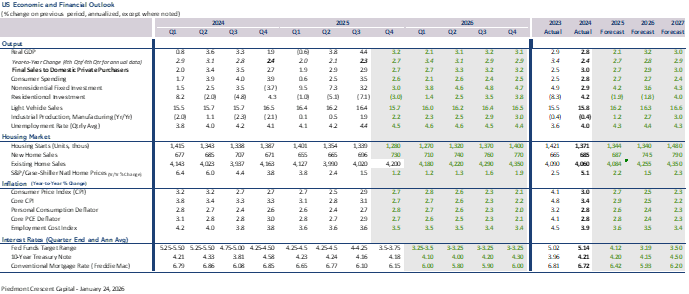

The economy continues to confound late-cycle pessimism. Growth is shifting away from consumption-led sugar highs toward capital-intensive, productivity-driven endeavors. Capital spending is adding meaningfully to growth. Our baseline outlook assumes productivity growth near 2.7 percent, with headline inflation approaching 2 percent by year-end even as real GDP growth runs at around a 3 percent pace.

Several forces support that view. Capital deepening is expanding supply capacity faster than demand, which is disinflationary and margin supportive. Inventory rebuilding and a gradual thaw in housing activity are stabilizing demand without recreating excess. Fiscal policy remains supportive, with the first-quarter FY2026 deficit near $600 billion, cushioning private-sector softness. Labor markets remain in a low-hire, low-fire regime, with jobless claims near cycle lows and participation stabilizing.

The PPI data highlights the tension in this environment. Consumer-level inflation is cooling, but pockets of upstream pressure remain. That combination argues for a Fed chair who is neither complacent nor reactive.

Warsh’s Stance: Hawkish Roots, Productive Optimism

Warsh’s path to the Fed runs through Wall Street, public service, and his tenure as a Fed Governor from 2006 to 2011. Like Chair Powell, he is not a PhD economist, but he brings deep market awareness and institutional memory. His hawkish instincts were evident during the post-crisis period, particularly in his skepticism toward inflation risks and large-scale asset purchases.

More recently, his thinking has evolved without abandoning discipline. Warsh has acknowledged that rates should be lower in a world where artificial intelligence and capital deepening raise productive capacity. At the same time, he has remained firm in his view that an expansive balance sheet and repeated QE undermine the Fed’s credibility and misallocate capital. He has also criticized regulatory burdens on smaller banks, aligning with a more pragmatic supervisory approach.

This is where the caricature breaks down. Warsh is not hostile to easing in principle. In a capital-driven economy, he recognizes that growth can remain strong without running hot. That view fits squarely with our protein-over-sugar thesis.

The Balance Sheet Reality

Warsh’s critique of the Fed’s balance sheet is well documented. The Fed still holds roughly 14 percent of outstanding Treasuries and about 25 percent of agency mortgage-backed securities, amounting to more than 20 percent of GDP. Structural constraints make rapid shrinkage unlikely. The more realistic outcome is a shift in emphasis, away from balance-sheet tools and toward clearer separation between monetary policy and asset-price management.

Warsh’s hawkishness targets QE and reflects openness to a productivity-led expansion.

Confirmation should be achievable but not automatic. Political friction around Fed leadership and independence remains a live issue, and even the perception of interference feeds directly into term premia, currency markets, and real-asset hedging. For markets and corporate decision-makers alike, Fed optics now matter almost as much as the policy path.

That backdrop includes the unresolved legal dispute involving Federal Reserve Governor Lisa Cook, whom the Administration sought to remove in August 2025 over mortgage-fraud allegations, which Cook denies. Courts blocked the removal under the Federal Reserve Act’s “for cause” standard, and the case is now before the Supreme Court, raising broader questions about presidential authority and central bank independence.

We expect the Administration to shift toward a more neutral posture during Warsh’s confirmation. The emphasis is likely to move toward governance and institutional stability rather than confrontation, providing him a clear runway into hearings and tenure while also building constructive momentum ahead of the State of the Union.

Implications for Market Participants

Policy continuity at the FOMC limits abrupt change, but Warsh may be more willing to cut rates ahead of the dots if inflation continues to cool. Bond markets remain vulnerable to credibility and fiscal risk, particularly at the long end. Equity valuations depend more on profit execution than multiple expansion. Energy markets continue to emphasize reliability over direction, with recent natural gas volatility reinforcing that lesson. Precious metals remain hedges against policy and governance risk rather than inflation plays.

Kevin Warsh is well suited to this phase of the cycle. He is inflation vigilant, credibility focused, and increasingly confident that a capital-driven economy can grow without overheating. The divergence between real GDP growth and employment is likely to persist, keeping pressure on the Fed to ease. The central risk is not reflexive tightening, but markets underestimating how much credibility itself has become policy.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 30, 2026

Mark Vitner, Chief Economist

(704) 458-4000

Reduced Immigration Slows U.S. Population Growth: Migration Within the U.S. has also Shifted

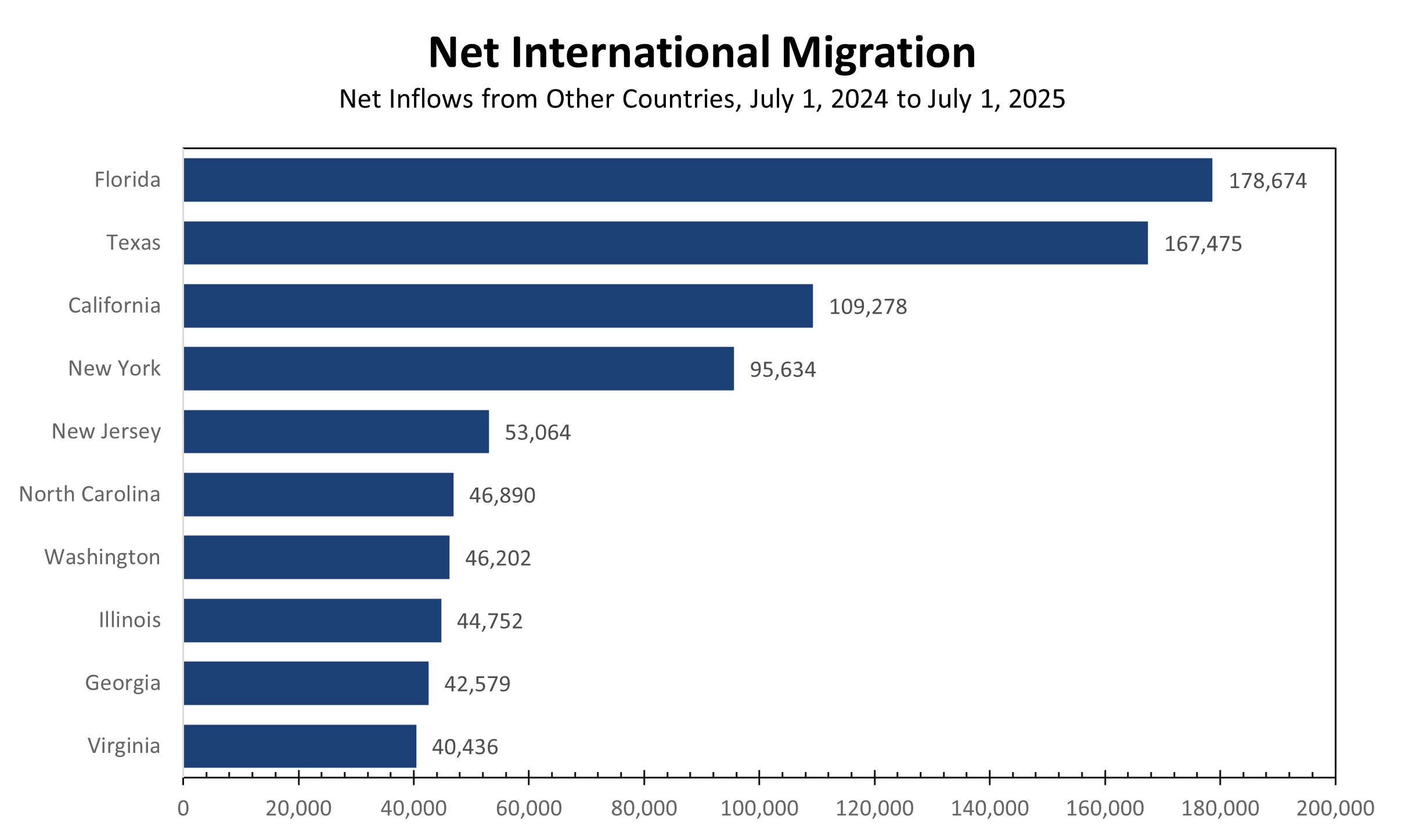

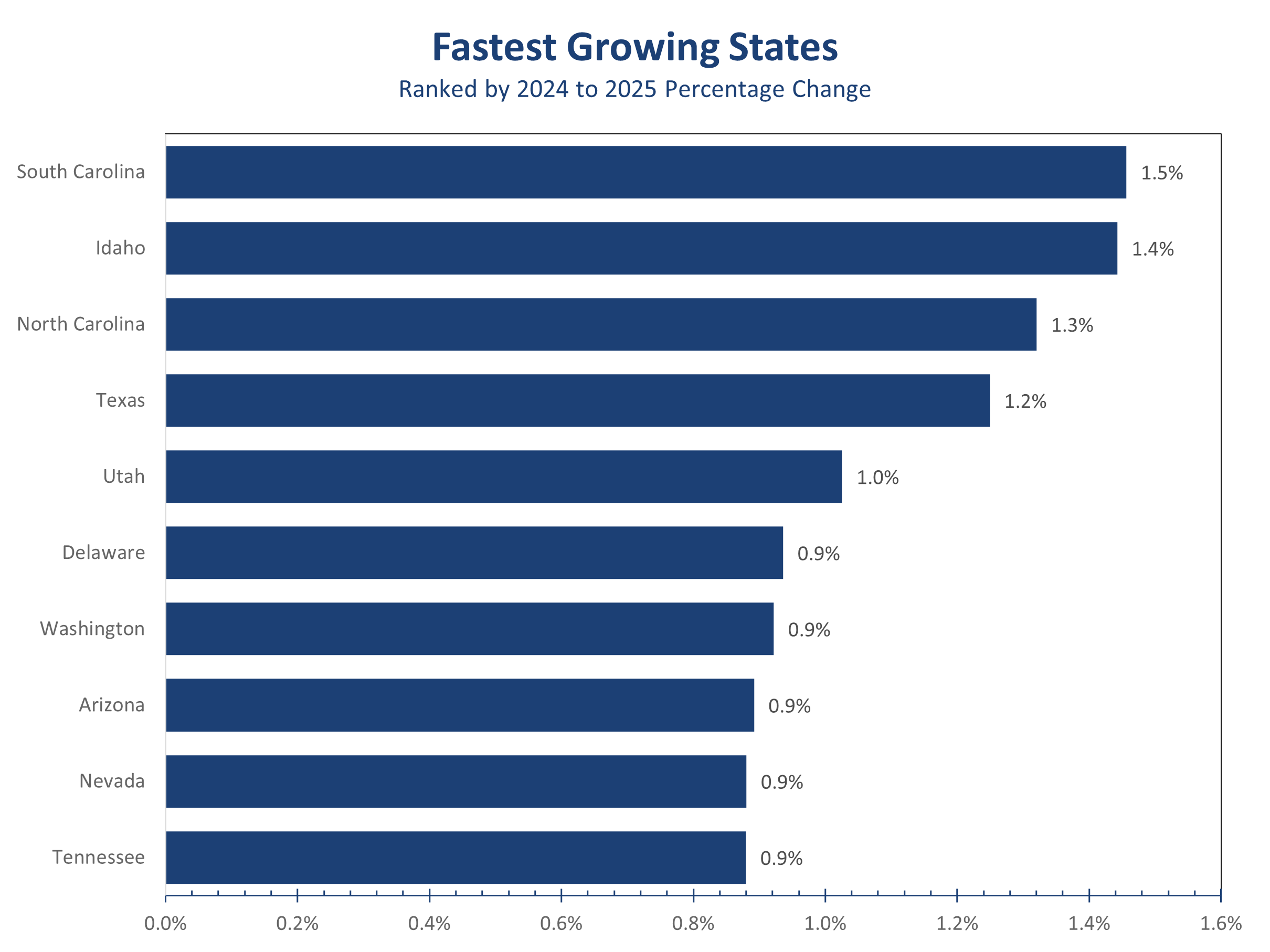

The Center of Gravity is Shifting South

- U.S. population growth slowed to 0.5% (+1.8 million), the weakest pace since the early pandemic, driven by a sharp decline in net international migration.

- Domestic migration provides the clearest signal: Americans continue to vote with their feet, overwhelmingly favoring the South.

- North Carolina led the nation in net domestic migration, edging out Texas and surpassing long-time leader Florida.

- Florida and Georgia remain net domestic gainers, but inflows slowed sharply as affordability, insurance costs, and congestion concerns increased.

- South Carolina was the fastest-growing state in the nation and ranked third in net domestic migration, with broad-based gains across metros and regions.

- Tennessee and Alabama posted rising domestic inflows, signaling a widening second tier of Southern growth markets.

- The July 2024–July 2025 estimates already reflect slower immigration ahead of the election and in the early months of the Trump Administration; a more pronounced immigration slowdown is likely from mid-2025 to mid-2026, further elevating the importance of domestic migration.

Americans Continue to Vote with Their Feet

The Vintage 2025 Census population estimates mark a clear inflection point in the U.S. growth story. National population growth slowed to 1.8 million people, or 0.5%, between July 1, 2024 and July 1, 2025, down sharply from the 3.2-million-gain recorded the year before. The primary driver was not a collapse in births or a surge in deaths, but a historic decline in net international migration, which fell by more than half and coincides with tighter immigration enforcement.

That shift elevates the importance of domestic migration, the cleanest measure of revealed preference. Unlike immigration flows, which are heavily influenced by federal policy, domestic migration reflects millions of individual decisions about where households believe opportunity, affordability, and quality of life are best aligned.

Americans continue to relocate to the South in search of jobs, affordability, and quality of life.

Despite a year marked by slowing population growth nationally, domestic migration flows reinforced a familiar but increasingly consequential pattern. Households continued to gravitate toward Southern states where job creation has been stronger, housing costs remain comparatively more attainable, regulatory environments tend to be lighter, and climates are generally warmer.

The South Still Wins — but the Map Is Being Redrawn

The South remains the nation’s top destination for domestic movers, but the internal hierarchy is shifting.

North Carolina emerged as the leading state for net domestic migration, surpassing both Texas and long-time leader Florida. This strength is not concentrated in a single metro. Growth remains broad-based across Charlotte, the Research Triangle, the Triad, the Coast, Asheville, and the Mountain counties, reflecting an unusual combination of scale, economic diversity, and livability. Even a year disrupted by Hurricane Helene failed to materially slow in-migration.

Charlotte warrants special attention. As a metro straddling the North Carolina–South Carolina border, its growth increasingly spills across state lines. Fort Mill, Rock Hill, and Lancaster County rank among the fastest-growing communities in South Carolina, benefiting from proximity to Charlotte’s job base paired with lower taxes and more attainable housing.

The South Is still winning, just not in the same places that is used to.

South Carolina was the fastest-growing state in the nation and ranked third in net domestic migration. Beyond the Charlotte spillover, growth remains strong in Charleston, Greenville, and Myrtle Beach, each powered by distinct mixes of logistics, advanced manufacturing, tourism, retiree inflows, and defense-adjacent investment. The state’s performance reflects not a single boomtown, but a statewide alignment of cost structure, governance, and demographics.

Florida and Georgia: Still Growing, But Cooling

Florida remains a population growth heavyweight, but its domestic migration advantage has narrowed sharply. Net domestic inflows fell dramatically from the peaks of 2022 and 2023, pushing Florida out of the top tier of domestic migration rankings. Rising homeowners’ insurance costs, higher density, and eroding affordability are increasingly shaping household decisions. Florida continues to grow but is now doing so more through international migration than domestic inflows, a notable shift. One unique aspect of Florida’s international migration, however, is that movement between the Sunshine State and Puerto Rico is counted as internatiional migration, even though this is a U.S. territory.

Florida and Georgia remain key gateways, but domestic movers are increasingly looking for more affordable and less congested opportunities elsewhere.

Georgia followed a similar trajectory, though less pronounced. Net domestic migration remained positive but slowed meaningfully from prior highs. Atlanta’s economic fundamentals remain strong, but the state is no longer absorbing domestic movers at the pace seen earlier in the decade as competition from the Carolinas intensifies.

One important cautionary anecdote is that South Florida and Atlanta are both major gateways for immigration, which bolsters their international net migration numbers. After arriving and initially settling, many new arrivals eventually move to neighboring states, when they show up as domestic out-migrants, depressing net domestic migration for those states.

The Second Ring Is Expanding

Beyond the traditional Sun Belt leaders, Tennessee and Alabama recorded rising domestic migration, signaling a broadening of growth across the South as affordability-driven migration expands. These states are increasingly attractive to households priced out of higher-cost metros but still seeking warmer climates, lower taxes, lighter regulatory environments, and job markets anchored by manufacturing, logistics, and energy.

Tennessee’s advantage lies in its depth: growth across multiple metros, not reliance on one.

Tennessee illustrates this shift particularly well. Nashville remains the state’s primary growth engine, benefiting from its expanding healthcare, technology, and a bevy of corporate relocations. But growth is no longer confined to Middle Tennessee. Chattanooga, Knoxville, and much of Eastern Tennessee have been growing rapidly, supported by advanced manufacturing, logistics access, and quality-of-life appeal. Memphis, long a laggard in domestic migration, has gained momentum more recently, aided by logistics investment, manufacturing reshoring, and renewed interest tied to its cost structure and central location.

Within Alabama, two standouts underscore the same pattern. Gulf Shores has seen population surge as the area gains recognition as a lower-cost alternative to the Florida Panhandle. Huntsville, in northern Alabama, remains one of the fastest-growing metros in the country, benefiting from continued inflows tied to technology, advanced manufacturing, and aerospace. NASA’s Artemis “return to the Moon” program and the relocation of U.S. Space Command headquarters are likely to bring renewed attention and investment to the region. Birmingham, Mobile and Montgomery have all gained momentum this past year.

This widening footprint is also lifting Arkansas, supported by major investment in its steel industry, and Mississippi, which has quietly emerged as a force in aerospace, space systems, and shipbuilding. Growth across these markets reinforces a broader trend: the South’s advantage is no longer concentrated in a handful of headline metros.

This widening aperture matters. It suggests the South’s growth advantage is becoming more distributed and more resilient, reducing reliance on any single state or metro.

The Competitive Map Is Clearer Than Ever

Population growth has slowed, but the competitive map is clearer than ever. Americans continue to vote with their feet, and those votes still favor the South. Within that shift, North Carolina has emerged as the domestic migration leader, South Carolina is accelerating fastest, and Florida’s long-standing dominance has cooled. The coming year is likely to reinforce these patterns rather than reverse them, as immigration slows further and domestic migration becomes the decisive margin.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 28, 2026

Mark Vitner, Chief Economist

(704) 458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Out of Greenland, Into Term Premium

Highlights of the Week

- Policy risk, not economic data, set the market tone, even as growth, spending, and labor indicators remained constructive.

- Gold and silver crossed psychological thresholds as hedges against policy and institutional uncertainty, with positioning amplifying the move in silver.

- Japan delivered the most consequential signal in global rates markets, as a selloff in super-long JGBs helped reprice term premia worldwide.

- Corporate behavior is shifting toward certainty, with more firms choosing to lock in funding rather than wait for calmer markets.

- The week ahead is light on data but heavy on policy signaling, increasing the risk that headlines overpower fundamentals.

- Greenland marks a shift from strategic ambiguity to permanent U.S. access, achieved through alignment rather than acquisition.

Policy Shock as the Primary Catalyst

This was a week in which geopolitics, rather than macroeconomic data, set the market’s tone. The Greenland episode—tariff threats deployed as leverage and then partially walked back—was notable less for its substance than for its speed. Markets reacted to each development the way they once reacted to payrolls or inflation surprises.

Risk assets sold off, Treasury yields rose, and the dollar softened before partial relief emerged as tensions eased. The pattern itself has become familiar. What stood out was how quickly correlations shifted. At several points, equities and long-duration bonds declined together, a reminder that policy shocks can overwhelm the traditional diversification playbook.

For CFOs and treasurers, the implication is straightforward. Policy posture has become a first-order macro variable. When it changes abruptly, markets adjust through the term premium rather than through growth expectations.

The Data Beneath the Noise

Lost in the headline churn was a reasonably constructive set of economic releases from the holiday-shortened week. The data reinforced a tension that has been building for months: the economy continues to expand, even as markets behave as though the margin for error has narrowed.

When geopolitics outpace the economic data, term premia tend to adjust.

Growth and GDP

Revised GDP figures confirmed that the economy entered year-end with solid momentum. Prior-quarter growth was revised higher, and forward-looking indicators continue to point to above-trend activity. The Atlanta Fed’s GDPNow estimate for Q4 remains elevated, at +5.4%, suggesting growth has not meaningfully rolled over, which is perplexing given the weaker nonfarm payroll data.

Personal Income, Spending, and PCE Deflators

Personal income growth was modest but steady, while consumer spending posted another firm monthly gain. Households continue to spend, though without much enthusiasm. PCE inflation came in broadly as expected, with headline and core measures still above target but no longer accelerating. From a policy perspective, the data argue for patience rather than urgency.

Labor Markets

Initial unemployment claims edged higher but remain near historically low levels. The labor market continues to exhibit a low-hire, low-fire pattern: hiring has slowed, but layoffs remain contained.

That combination presents a familiar puzzle. Payroll growth has softened in a way that would typically be associated with a slowdown, yet layoffs show no sign of accelerating. Historically, that mix is inconsistent with recession.

The economy is not flashing red. Markets are reacting to governance risk, not growth risk.

Consumer Sentiment

The University of Michigan sentiment index improved modestly, but from depressed levels. Consumers are less pessimistic than late last year, though far from confident. The message aligns with the spending data. Households are coping, but also sulking about continued high, albeit no longer rapidly rising, prices for key necessities.

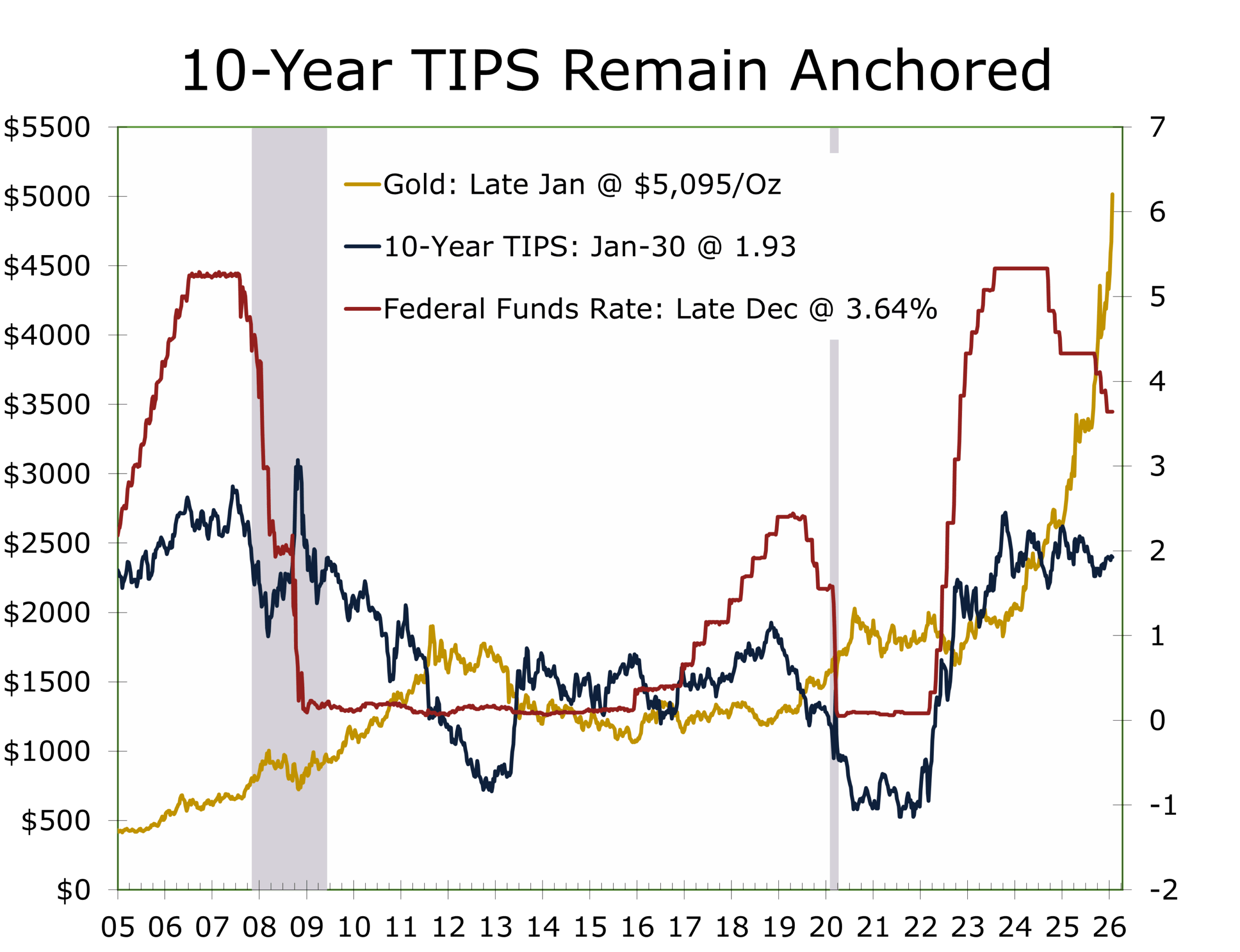

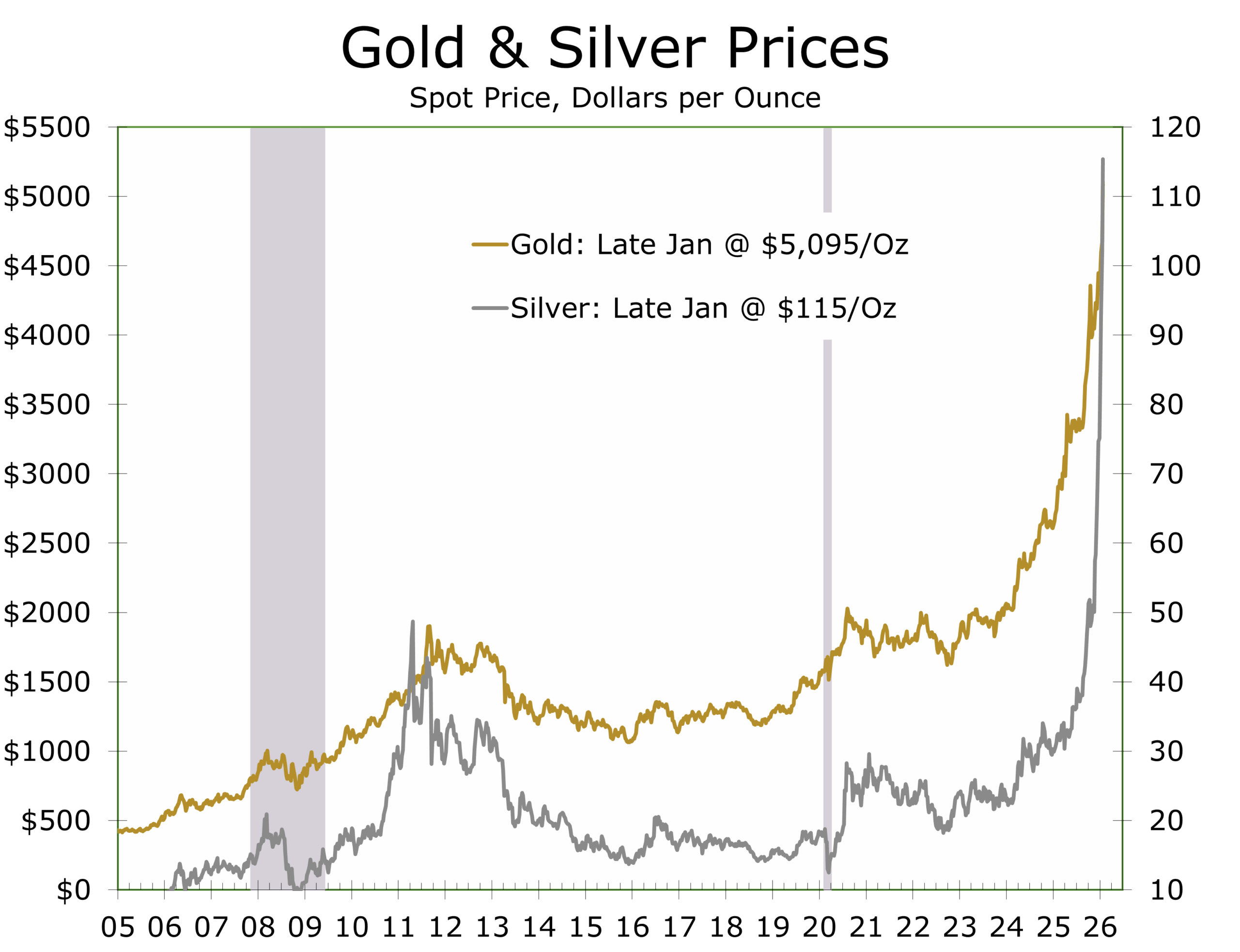

Gold, Silver, and the Price of Uncertainty

Precious metals delivered the clearest emotional signal of the week. Gold surged to within striking distance of $5,000 per ounce, while silver moved decisively through $100. These were not incremental moves. They were threshold events.

Gold behaves like insurance. Silver behaves like insurance—with leverage and air pockets.

The character of the rally matters. Gold’s advance increasingly resembles a hedge against policy uncertainty and institutional credibility, reinforced by central-bank accumulation and private-sector demand for assets without counterparty risk. This looks less like an inflation trade and more like a confidence trade.

Silver told a slightly different story. Alongside the macro narrative, its smaller and more volatile market structure amplified momentum. Crowded positioning and forced short covering likely accelerated the move once key technical levels gave way. That does not negate the signal, but it does make silver a higher-beta expression of the same underlying concern.

Japan and the Return of Global Term Premium

This past week’s most underappreciated development came from Tokyo. Japanese government bonds, long the anchor of global duration markets, experienced a sharp selloff. Yields on 30- and 40-year JGBs rose to levels that would have seemed implausible just a few years ago.

The implications were immediate. As Japan’s super-long yields moved higher, global investors were forced to reassess what long-dated “risk-free” assets should yield elsewhere. U.S. Treasuries felt the pressure, particularly at the long end, with the curve steepening even as risk sentiment deteriorated.

This was not a warning about U.S. credit quality. It was a reminder that the global supply of patient, price-insensitive buyers of long-dated sovereign debt is not infinite. When Japan’s anchor slips, term premia become more mobile everywhere.

Japan did not cause U.S. yields to rise. It did, however, raise the global hurdle for duration.

For treasury teams, this matters. Long Treasuries remain liquid and credit-safe, but they are no longer immune to flow-driven volatility.

Certainty Is the New Optionality

Against this backdrop, corporate behavior is changing. Firms are increasingly refinancing earlier and locking in rates rather than waiting for a cleaner window. This is not panic. It is a rational response to a market in which policy headlines can move the curve more than a quarter’s worth of economic data.

In a volatile policy regime, the cheapest debt is not always the best debt.

Notably, this shift is occurring even as the economic backdrop remains constructive. GDP growth is solid, layoffs are limited, and real-time growth estimates remain elevated. The move toward certainty reflects volatility management, not recession anxiety.

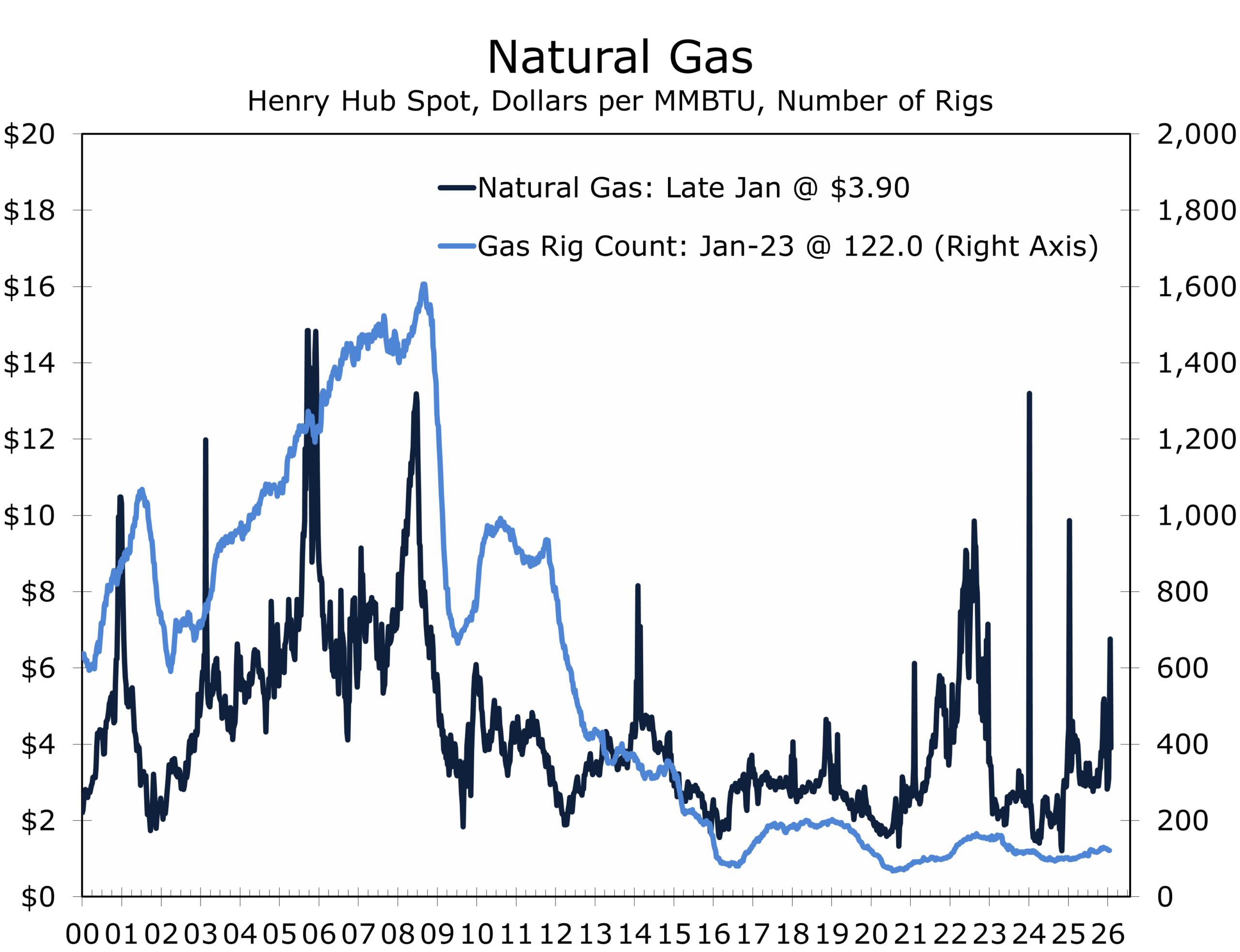

Energy and the Cost of Reliability

Energy markets offered a parallel reminder that volatility is no longer theoretical. Natural gas prices surged as extreme winter weather drove a sharp increase in heating demand, disrupted production, and stressed regional power grids, pushing wholesale electricity prices to extraordinary levels in parts of the country. The speed of the move, rather than its magnitude, caught many participants off guard. While the spot price has jumped to nearly $7 MMBtu the March futures are well under $4 MMBtu.

For energy-intensive firms, the issue was less about price than about continuity. Energy risk now includes availability and operational resilience, not just cost. That reality increasingly pulls treasury, operations, procurement, and capital planning into the same risk-management conversation.

Energy risk is shifting from price volatility to reliability risk.

What Comes Next for Natural Gas

Looking ahead, the balance of evidence suggests that the recent spike in natural gas prices is likely to prove acute rather than prolonged. As temperatures normalize, production recovers, and storage draws moderate, spot prices should retrace some of their gains. However, the episode reinforces a more structural shift: U.S. gas markets are now tightly linked to global conditions through LNG exports, leaving prices more exposed to weather shocks, infrastructure constraints, and geopolitical spillovers than in prior cycles.

For corporate buyers, this new environment argues less for betting on price reversals and more for planning around volatility as a recurring feature rather than a tail risk. The world is full of surprises, and the weather is just the latest one to assert itself.

The Week Ahead: Data Quiet, Policy Not so Much

The coming week is light on market-moving data but heavy on policy signaling.

When the data are quiet, that makes room for policy noise to get louder.

The January FOMC meeting is expected to result in no change in policy rates; the focus will be on language, particularly whether the Committee acknowledges that policy uncertainty and geopolitical risk are tightening financial conditions at the margin. Durable goods orders and jobless claims should confirm ongoing expansion rather than alter the outlook. With fundamentals broadly stable, markets remain vulnerable to headline-driven volatility. On the policy front, the fatal shooting of a Minneapolis resident by federal immigration agents has intensified partisan opposition to the Department of Homeland Security funding bill, with Senate Democrats vowing to oppose the measure absent substantive reforms—raising the prospect of a partial government shutdown as early as the end of this week and injecting a new political risk premium into markets.

With fundamentals broadly stable, markets remain vulnerable to headline-driven volatility. As the Greenland episode demonstrated, policy signaling now moves prices faster than most scheduled releases.

What This Past Week Taught Us

This was a week about confidence rather than cycles. The data continues to describe an economy that is expanding and cooling gradually, not one on the brink of recession. Markets, however, are pricing governance risk, policy uncertainty, and global term-premium dynamics with increasing urgency.

Gold and silver reflected that shift first. Japan’s bond market translated it into rates. Corporate treasurers are responding by paying for certainty. In that sense, the most important signal of the week did not come from a data release. It came from behavior.