The Long and Winding Road Back to Normal

Plotting a Course Back to the New Normal

- Attention remains keenly focused on the Federal Reserve’s plans to begin to reverse the tightening they put in place a couple of years ago after they realized inflation would prove more persistent. The financial markets now look for the Fed to begin cutting the federal funds rate no sooner than June and look for a total of three quarter-point cuts this year – a view the Fed affirmed at its March 20 FOMC meeting.

- The slower consensus view on rate cuts follows a series of stronger monthly employment reports and hotter inflation reports. Job growth is simply too strong, and inflation is too high to allow rate cuts any earlier than June. Most other economic reports paint a softer economic portrait, with retail sales and industrial production remaining weak, consumer confidence remaining guarded, and survey of consumers and businesses continuing to show inflation and wages moderating.

- The Federal Reserve is currently tracking multiple objectives. The principal target is long-term price stability, which means returning core inflation measures back to a 2% pace. The second is maintaining full employment, which means keeping the unemployment rate around 4% and maintaining high levels of labor force participation. A third objective is to avoid surprises and policy missteps, particularly ones that would lead to financial volatility. The Fed’s final objective is to accomplish all of this without becoming a political issue in this year’s election.

- While the Fed’s objectives are straightforward their timetable remains fluid and is ongoing. The recent obsession with the latest employment and inflation numbers misses this point, as the Fed is looking more at where the economy is headed rather than where it has been or currently is. Monetary policy works with a long and variable lag, so the Fed’s moves must be taken before employment slows too much and well before inflation has returned to target.

- We have made some slight adjustments to our forecast and see economic growth moderating this spring and summer. The Fed is expected to cut the federal funds rate by a quarter percentage point in June and follow that with cuts in September and December. We expect additional cuts in 2024 but do not believe the Fed is in any hurry to bring the federal funds rate back to neutral.

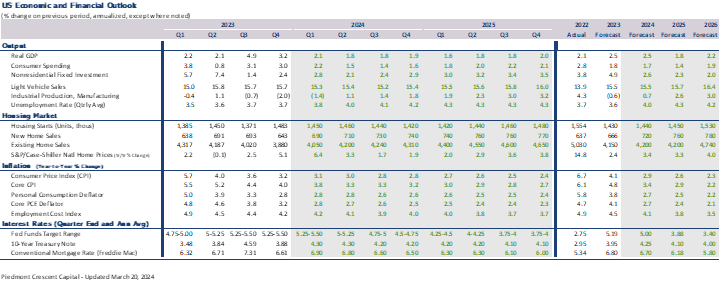

The March Federal Open Market Committee (FOMC) meeting marked a seminal event for many forecasters and market participants. While the Fed was widely expected to leave the federal funds rate unchanged, attention was keenly focused on any adjustments made to the forecast for economic growth, inflation, and interest rates. Back-to-back strong employment reports raised expectations for growth this year, while the first two rounds of inflation reports showed inflation would likely prove sticky this year and take long to return to the Fed’s 2% long range target. Most other economic data have been mixed, with retail sales beginning the year on a weak note and industrial production and most survey data suggesting economic growth is slowing.

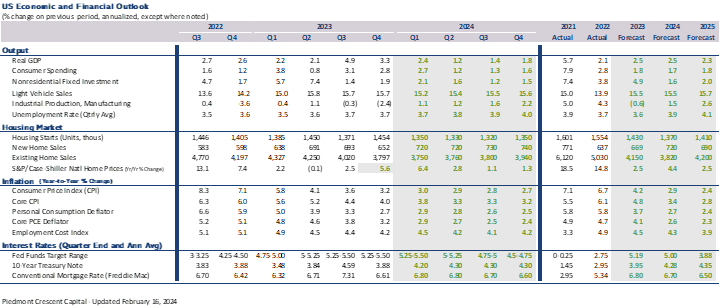

For its part the Fed raised its estimate for economic and now expects real GDP to rise 2.4% from the end of 2023 to the end of 2024, versus 1.4% previously, and to rise 2% in both 2025 and 2026. The unemployment rate is expected to remain close to 4%, while inflation, as measured by the core PCE deflator, is expected to gradually decelerate to 2.6% this year and 2.4% in 2025, before finally returning to the Fed’s long-run target of 2% in 2026. The Fed continues to expect three quarter-point rate cuts in 2024, following by three more in both 2025 and 2026, bringing the federal funds rate down a cumulative 225 basis points to 3.125% by the end of 2026.

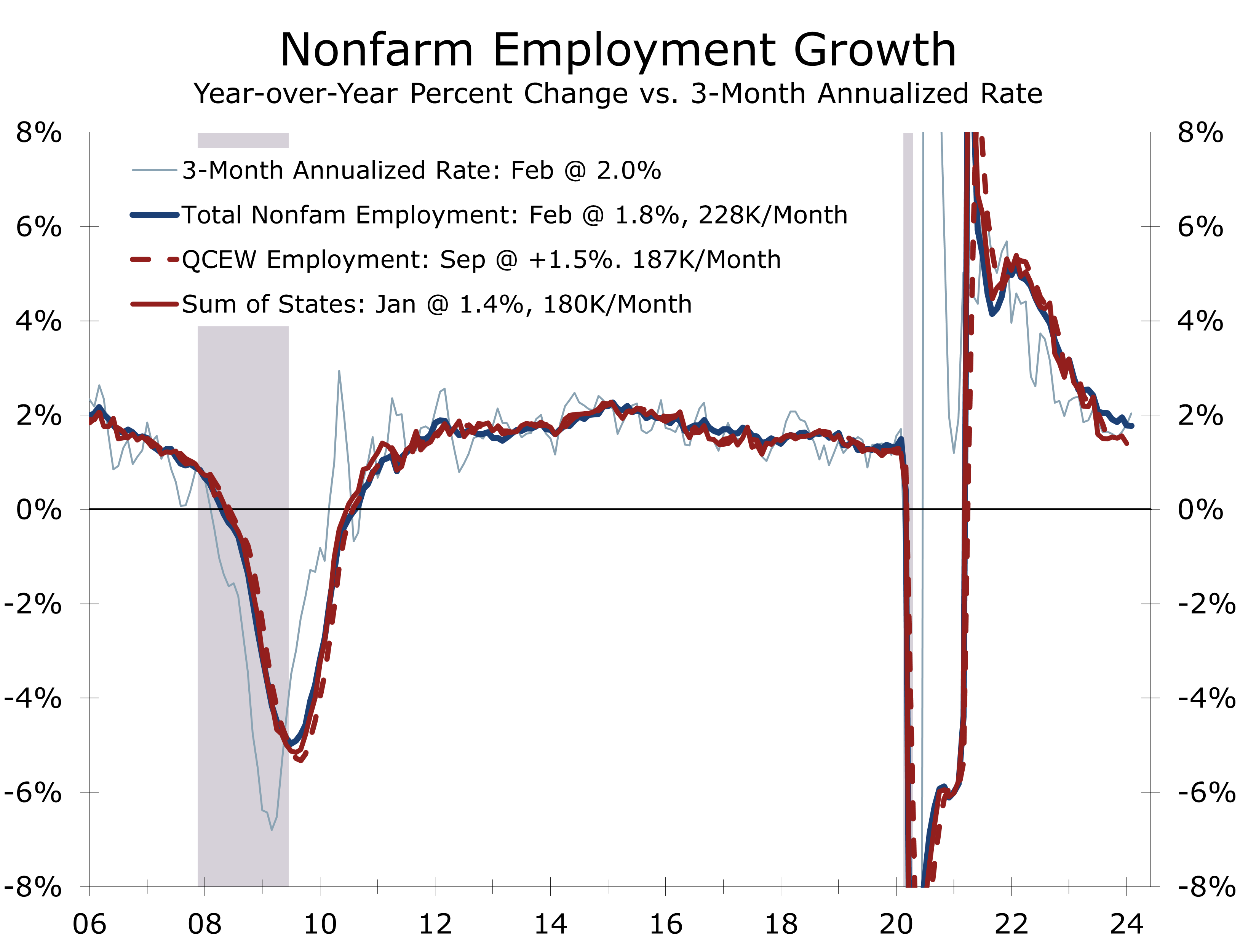

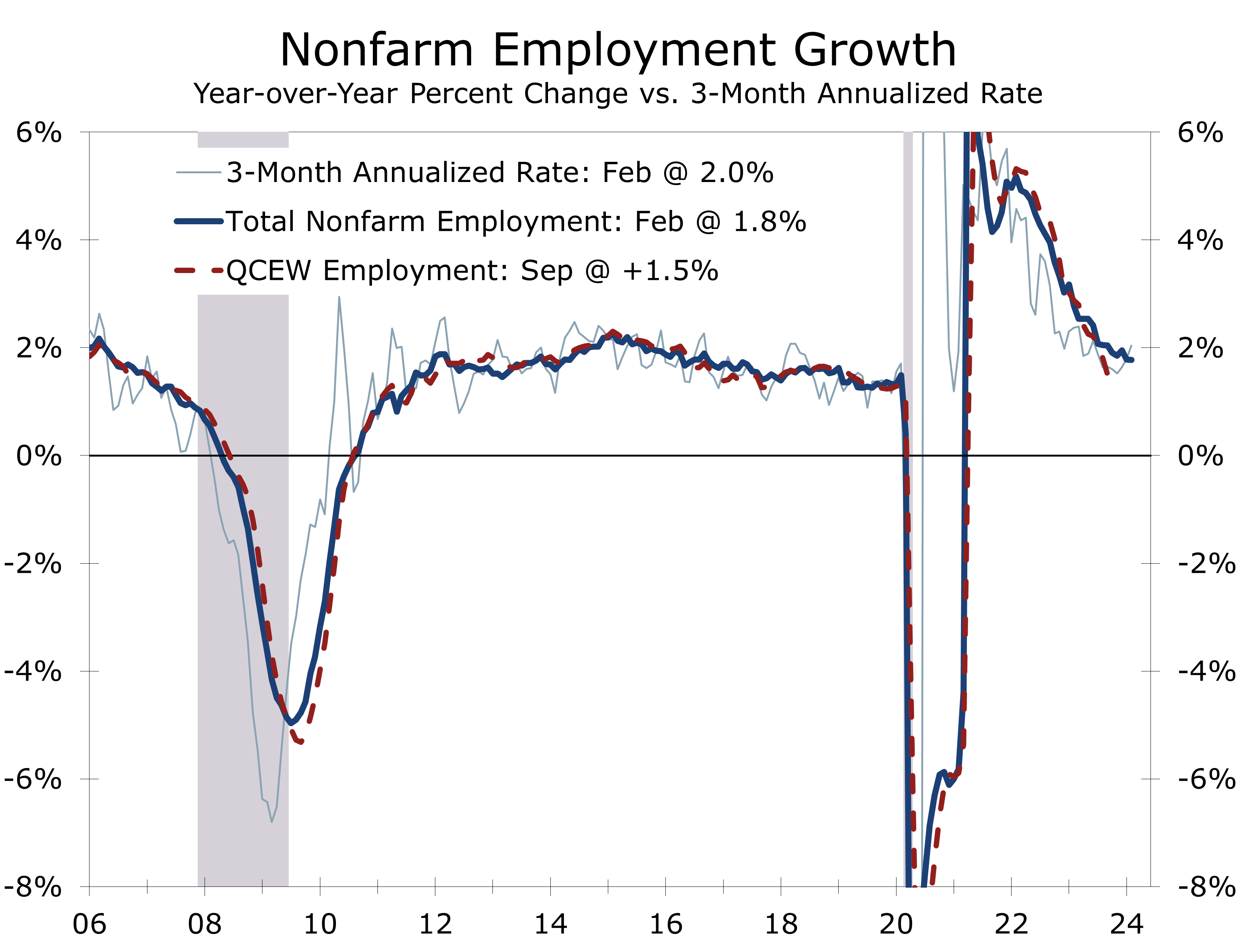

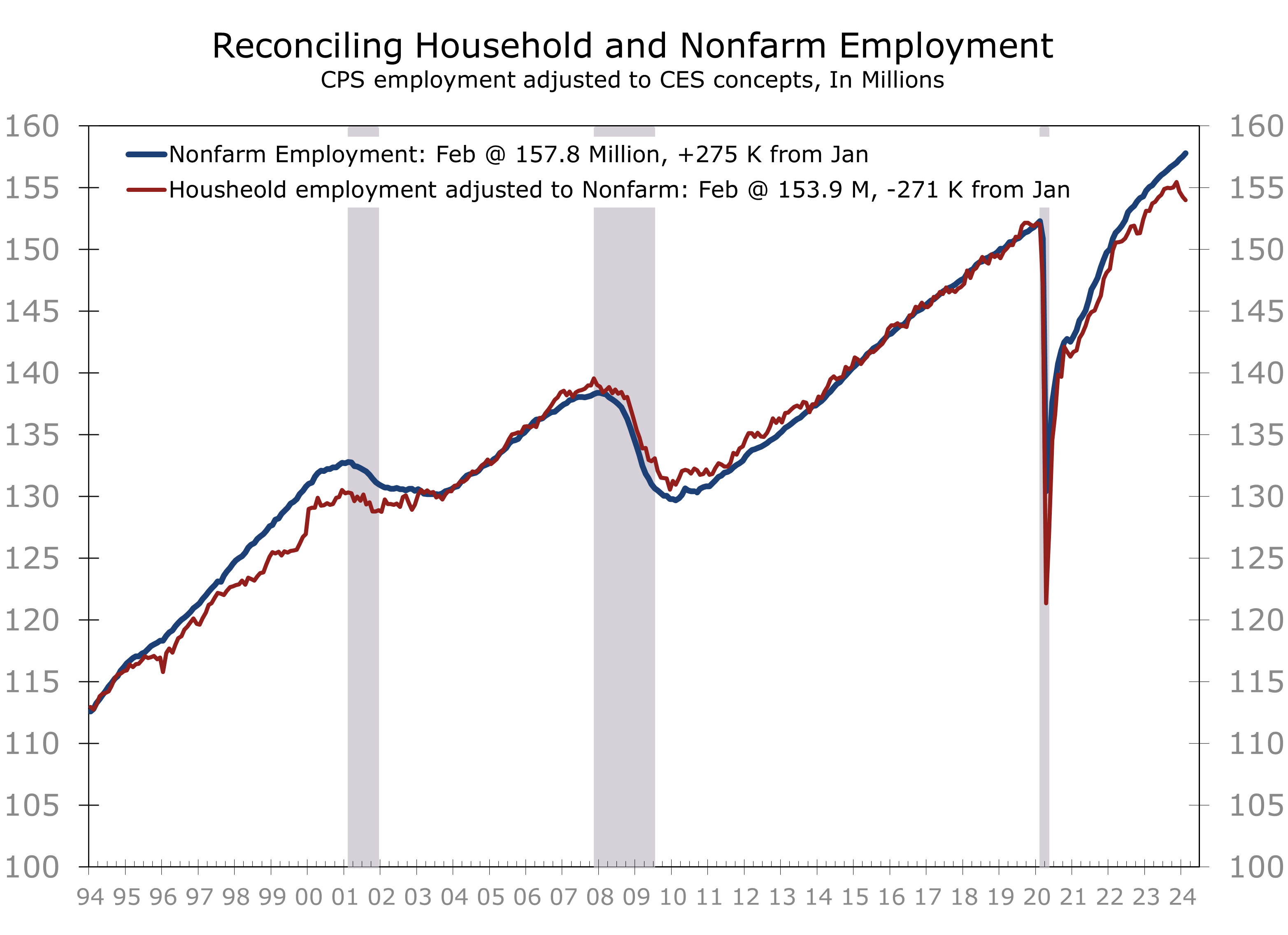

To paraphrase Yogi Berra, it’s tough to make predictions, especially about the future – even if you are the Federal Reserve. The Fed’s stronger economic forecast is consistent with the stronger employment data reported for the past three months. Private and public employers have added an average of 265,000 jobs a month for the past three months and an average of 229,000 per month over the past year. Our research suggest the currently reported employment data overstate nonfarm employment by approximately 800,000 jobs, however, and peg monthly job growth over the past year at just 175,000 jobs per month. We expect to see a moderation in reported job growth this spring, aligning more closely with the recently released Quarterly Census of Employment and Wages, as well as the revised state and local employment data.

Slower job growth would make the Fed’s job easier, particularly if the inflation data continue to come in hotter than expected over the next few months. The one change in the Fed’s policy statement following the March FOMC meeting was to acknowledge the strong job growth reported over the past three months, noting that “job gains had remained strong”. This is a slight upgrade from prior meetings. While the Fed sees job growth remaining strong, they also see the labor market moving back into balance, with job openings and the quit rate both declining, which is a precursor to a further moderation in wage gains.

If job growth slows along the lines we expect, the Fed will more easily be able to justify cutting interest rates, even if inflation continues to prove resilient. Seasonal adjustment issues likely understated core inflation during the second half of 2023 and the payback for that is now boosting it. The Fed left themselves a little more room on this front by slightly lifting their expectation for core PCE inflation to 2.6% this year from 2.4%.

The Fed’s stronger economic outlook and more cautious view on inflation not only match up well with recent economic reports but also provide them with a great deal of flexibility, which they very well may need. The Fed operates with multiple objectives, primarily centered on achieving long-term price stability with a 2% inflation target, while simultaneously striving to maintain full employment, defined by a roughly 4% unemployment rate. The primary tool used to accomplish the Fed’s goals is raising or lowering the federal funds rate, which they strive to do in a way that avoids policy missteps, prevents financial volatility, and remains apolitical, particularly during election cycles.

The Fed’s strategy and tactics change over time, reflecting both short-term cyclical and long-run structural influences. The Fed aggressively slashed interest rates at the onset of the pandemic, reduced interest rates to zero and substantially expanded its balance sheet to bolster liquidity to the broader economy and financial markets and to also accommodate the surge in federal spending. This extraordinarily accommodative stance persisted until early 2022, when mounting inflation pressures emerged due to the economy’s reopening amid widespread supply chain disruptions and bottlenecks.

After recognizing the threat from inflation was considerably more extensive than just shortages and bottlenecks the Fed ramped up the pace and magnitude of their rate hikes, including hiking the federal funds rate by 75 basis at four successive meetings back in summer and fall of 2022 before tamping down the pace of rate hikes this past year. At the December FOMC meeting, the Fed said that it had likely finished hiking interest rates for this cycle, which turned attention to the prospect of rate cuts in 2024. At first, market expectations had priced in six rate cuts for this year. Expectations for rate cuts have been scaled back more recently, following back-to-back stronger than expected employment reports and hotter than expected inflation reports.

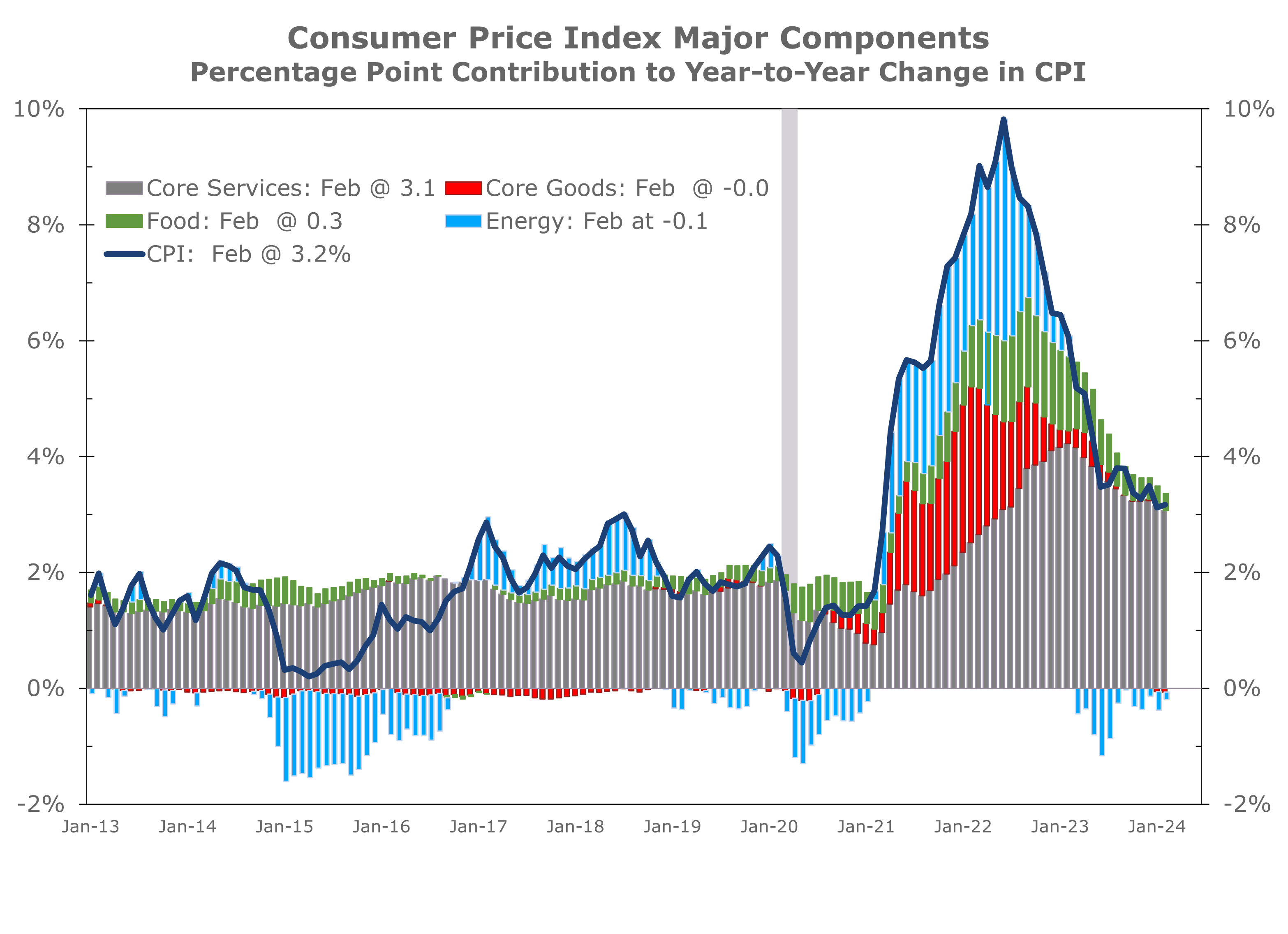

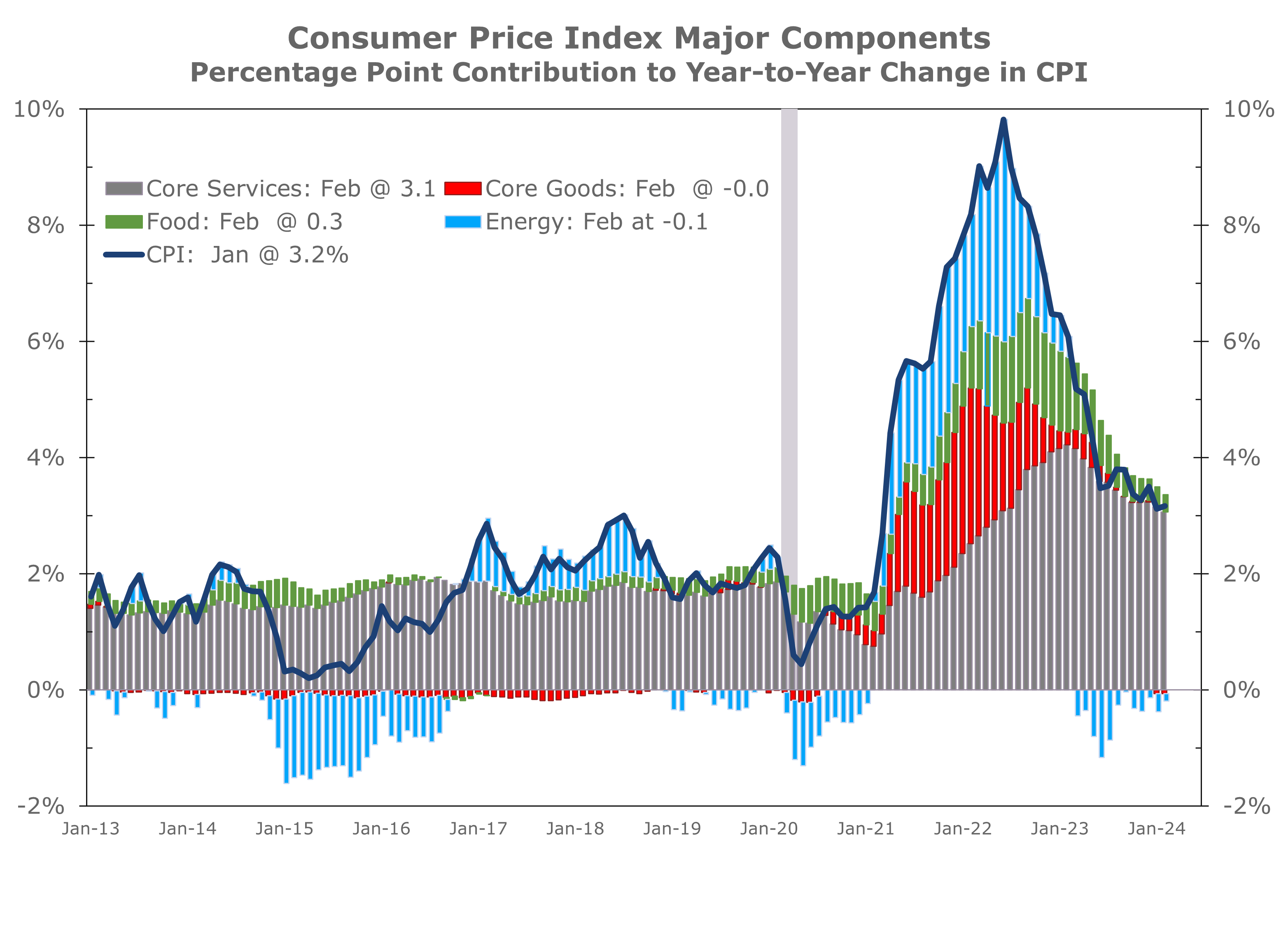

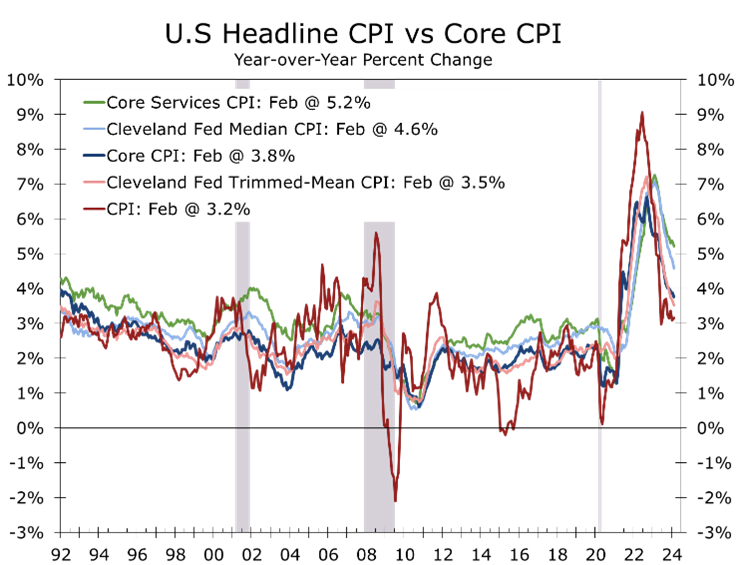

While inflation has remained more persistent than expected, it has slowed considerably since the Fed became more aggressive about hiking interest rates. The year-to-year change in the Consumer Price Index peaked out at 9.1% in June 2022 to just 3.2% in February of this year. Most of that improvement came from falling energy prices. Prices for used cars and SUVs also reversed much of the spike seen during the pandemic and food prices, which had risen sharply in 2021 and 2022, rose less rapidly this past year. Core services prices, which account for the bulk of consumer outlays, have moderated much less and now account for the bulk of overall inflation.

We remain cautious regarding inflation, especially given the pandemic’s impact on price fluctuations. Certain sectors such as used cars, health care services, and apartments experienced significant price swings, which likely distorted seasonal adjustments and led to underestimated inflation, particularly in the latter half of last year despite a general moderation in overall price increases. Looking ahead, we anticipate inflation to remain elevated until the middle of this year, particularly as prices for health care services rebound from their previously understated levels towards the end of last year. Additionally, energy prices are on the rise once again, with crude oil recently surpassing $80 a barrel and national retail gasoline prices recently topping $3.50 per gallon, according to AAA.

Core services prices continue to pose the primary challenge to reducing overall inflation. Excluding energy, services prices increased by 5.2% over the past year, with core services inflation reaching a peak of 7.2% in February 2023 and decelerating less than overall core inflation since then. Housing costs, particularly owner’s equivalent rent and residential rent, have been significant areas of concern, as they have slowed less compared to many widely followed private rent indices. These indices predominantly sample asking rates on professionally managed apartments and single-family rental homes, whereas rents for lease renewals have shown greater resilience. With 450,000 new rental apartments expected to enter the market this year, residential rents will likely moderate further and this moderation should show up more clearly in the government inflation data.

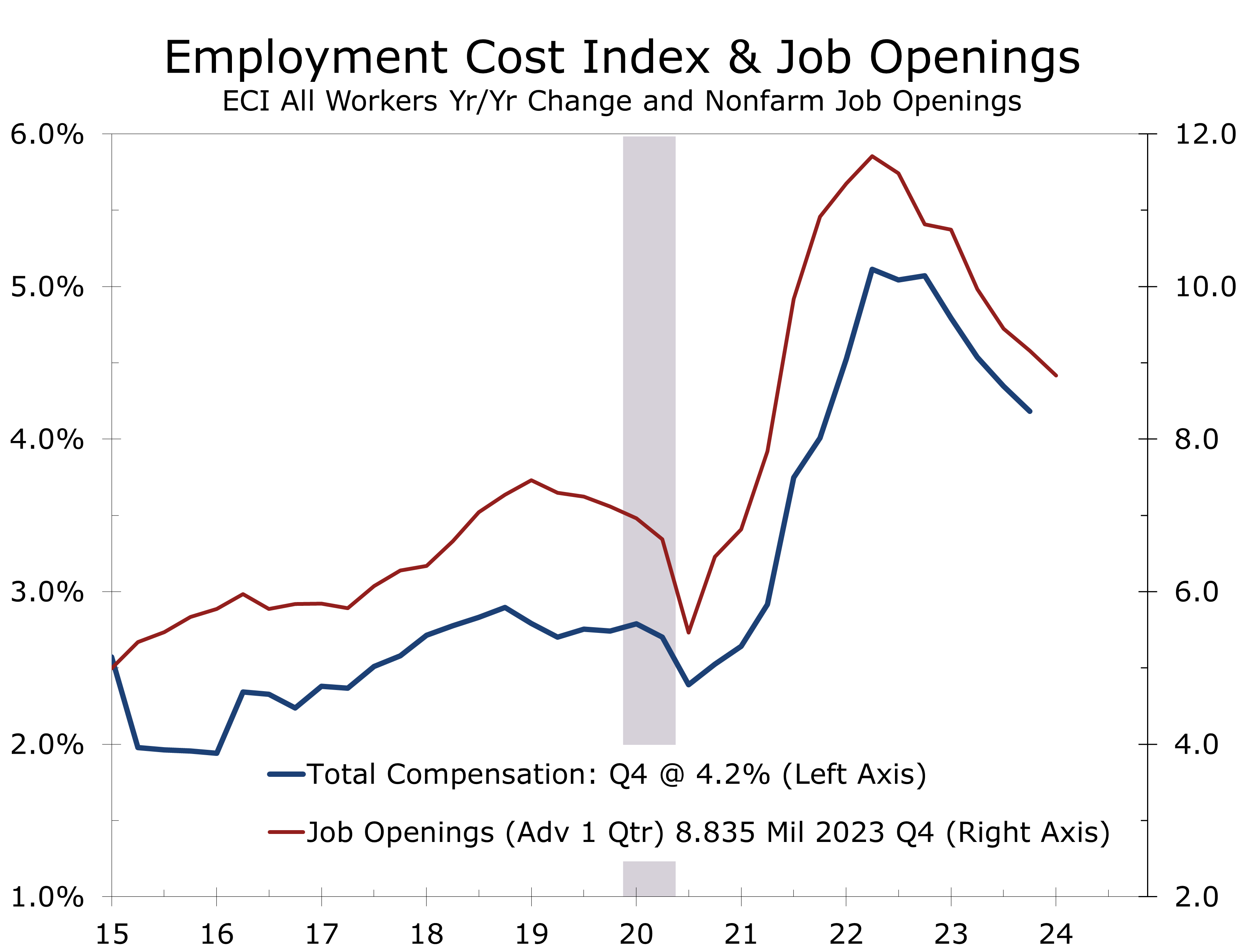

Core services inflation, excluding housing, remains problematic, surging 0.9% in January and rising 0.5% in February. Auto insurance and car repair have been a major part of the problem, but prices are up sharply in almost every industry where labor makes up a large proportion of costs. The focus on core services prices brings attention back to the labor market, where the number of job openings has cooled off considerably over the past 18 months. There is a pretty tight relationship between job openings and the Employment Cost Index (ECI), which is a broader measure of labor costs that includes benefits. We expect job openings to recede further this year, although the rate of deceleration is expected to slow somewhat. Much of the recent strength in job growth has been at state and local governments, health care, and the leisure hospitality sector, which are all striving to bring hiring back in line with their pre-pandemic trend.

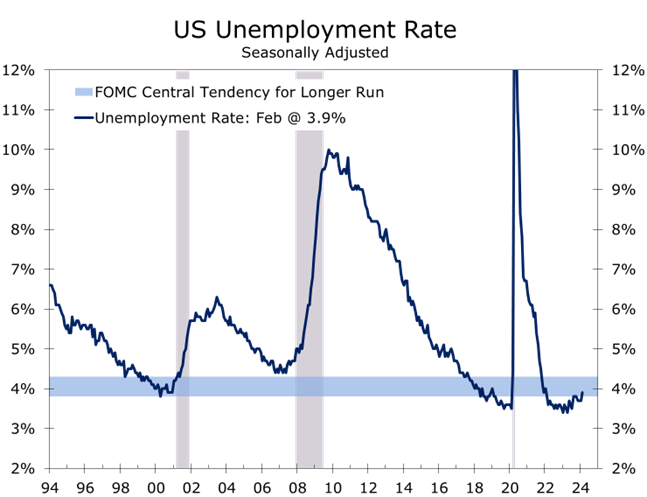

Another sign that the labor is moving back into balance is that the unemployment rate has edged higher in recent months, climbing to 3.9% in February. With the latest rise, the unemployment rate is back within the Fed’s long-run target range of between 3.8% and 4.3%. The rise in the unemployment results from slower household employment and slightly stronger labor force growth. The household employment measure is notoriously volatile around the turn of each year when there is significant movement into and out of the labor force and the Labor Department also makes their annual population adjustment.

How much should be made of the recent uptick in the unemployment rate remains to be seen. An increase in the unemployment rate of half a percentage point or more has typically marked the start of a recession. The jobless rate is now up 0.5 percentage points from its low hit in April of last year and is 0.2 pp above its average for the past year. Why this rule would hold any more sway in the post-pandemic environment than the inverted yield curve or nearly two-year slide in the Leading Economic Index is certainly a key point to consider. A better counterpoint, however, is weekly unemployment claims remain at 50-year lows and there are still more job openings than there are unemployed. Consumer surveys also show relatively little concern about job security.

We suspect the rise in the unemployment rate reflects a host of factors. Part of the increase is purely cyclical. Manufacturing has endured a slowdown this past year, which has seen industrial production decline 0.8% over the past year and manufacturing employment has been essentially flat for the past year. Hiring has also slowed in construction, reflecting a winding down of some commercial projects and some slowing in industrial projects. Much of the strength in hiring has been in government, health care and the leisure and hospitality sector.

Structural factors may also be pushing the unemployment rate higher. There was a surge of immigration in 2023, which likely pushed labor force growth higher and resulted in a slightly higher unemployment rate when hiring slowed during the second half of last year. We look for the unemployment rate to continue to edge higher this year, eventually rising to 4.2%, where we expect it to remain through much of next year. From a longer-term perspective the jobless rate should remain relatively low, as a growing number of Baby Boomers continue to retire and exit the workforce. The last Baby Boomer will turn 65 in 2029.

Stronger immigration is one of the reasons the Federal Reserve raised their forecast for economic growth this year. The Congressional Budget Office estimates immigration, including undocumented individuals, surged to 3.3 million in 2023, which is well above its pre-pandemic pace and roughly 2.3 million ahead of the CBO’s projection for 2023 made back in 2019. While political factors will likely slow immigration this year, we still expect a net gain of at least 2.3 million residents, which will bolster labor growth and potential GDP.

Domestic factors will also bolster economic growth, with household formation and live births both expected to increase this year. The increase in household formations continues to be driven by younger households, which is one reason apartment demand has remained so strong. Apartment vacancy rates are expected to increase this year, however, as just over 450,000 apartments are expected to be completed, primarily in the South and Mountain West. Millennials are also increasingly forming families and having children, which is driving demand for starter homes.

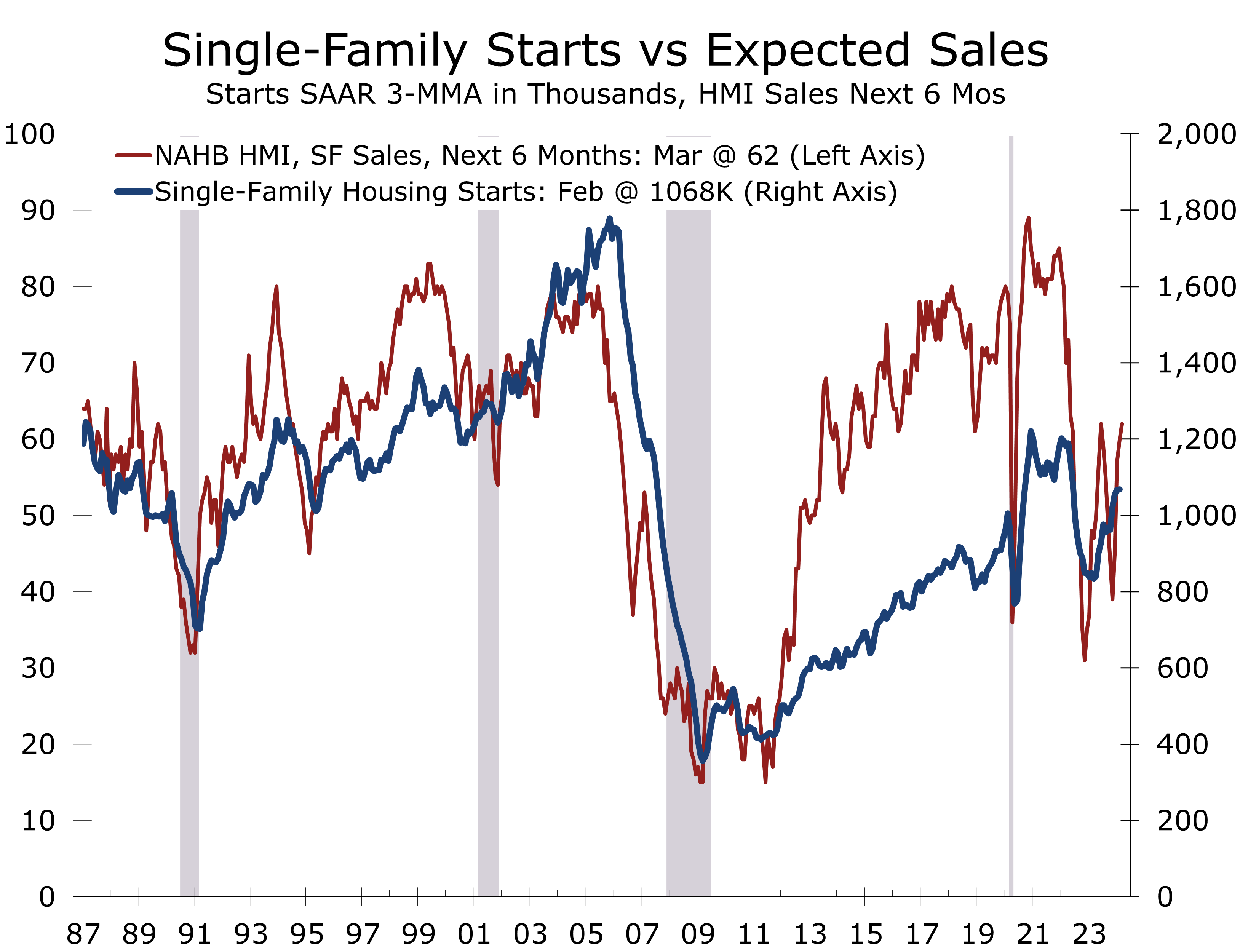

Home building is expected to be a significant driver of economic growth this year. Mortgage rates are projected to decline, with the rate for a 30-year conventional mortgage expect to fall to 6.50% by the end of the year. Home builders are extensively utilizing mortgage rate buydowns, resulting in a steady rise in buyer traffic. The NAHB/Wells Fargo National Housing Market Index (HMI) climbed 3 points in March to 51, marking its fourth consecutive increase and reaching its highest level since July of last year. Builder expectations for sales over the next 6 months also rose by 2 points to 62, matching their highest level in 21 months.

The rise in home builder optimism is apparent in the latest housing starts, which surged by 10.7% to a pace of 1.52 million units in February. Single-family starts rose by 11.6% to a 1.13 million unit pace, are up 35.3% from last February. Multifamily starts, primarily rental apartments, rebounded by 8.3% in February to a 392,000 unit pace, following a 27.9% decline the previous month. Despite this rebound, multifamily starts remain 35% below their year ago pace. The rise in single-family starts is expected to have positive ripple effects, as an increasing number of new home sales are from first-time buyers who will require financing, insurance, and furnishings for their homes. This will boost financial services and the production and sales of furniture, household appliances, home furnishings, and building materials used in home construction.

We have extended our forecast out through 2025 on a quarterly basis and 2026 on an annual basis. Current quarter real GDP growth is estimated at 2.1%, fueled by strong growth in consumer spending and stronger sales of both new and existing homes. Business fixed investment also looks solid, although we are seeing a growing number of Electric Vehicle-related projects postponed. Growth is expected to moderate this spring and summer to just under a 2% annual rate. Our forecast for the year calls for real GDP to rise at a 2.5% annual rate on an annual basis and 1.9% pace on a Q4-to-Q4 basis, slightly below the Fed’s 2.1% projection.

There has been a great deal of discussion following the March FOMC meeting regarding the decision to raise both the growth and core inflation forecast but keep plans for a June rate cut in place. The return to the Fed’s 2% target is more likely to reflect a long and winding road rather than straightway. Chair Powell acknowledged as much in his press conference. We expect to see this debate heat up following what we believe will be disappointing inflation numbers next month. The inflation data should look better later this spring, however, and we feel confident they will cut in June and September and then wait until after the presidential election to cut a third time. Inflation is not expected to return to a 2% pace on a sustained basis until 2026.

We see some upside risks to our forecast. The most cyclical parts of the economy appear to be regaining momentum. Early reads on manufacturing activity in March show an improvement in orders, output, and shipments. Construction activity also appears to be ramping up, with single-family starts up 35% from their year ago levels. New home sales are expected to rise 8% this year and existing home sales are expected to rise at least 1% to a 4.2 million unit pace. The risk is to the high side, however, as a growing number of homeowners are putting their homes on the market. The resulting knock-on effects will lift economic growth more broadly.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Mark Vitner, Chief Economist

Piedmont Crescent Capital

April 1, 2024

Weaker Job Growth Across Much of the Country

MSA Jobs Data Show Hiring Losing Momentum

- The latest MSA jobs data reveal a much weaker recovery across much of the country.

- The latest data include benchmark revisions to data prior to April 2023 and show a much slower trajectory since that date.

- The greater New York City area is a notable exception, with only minor revisions evident.

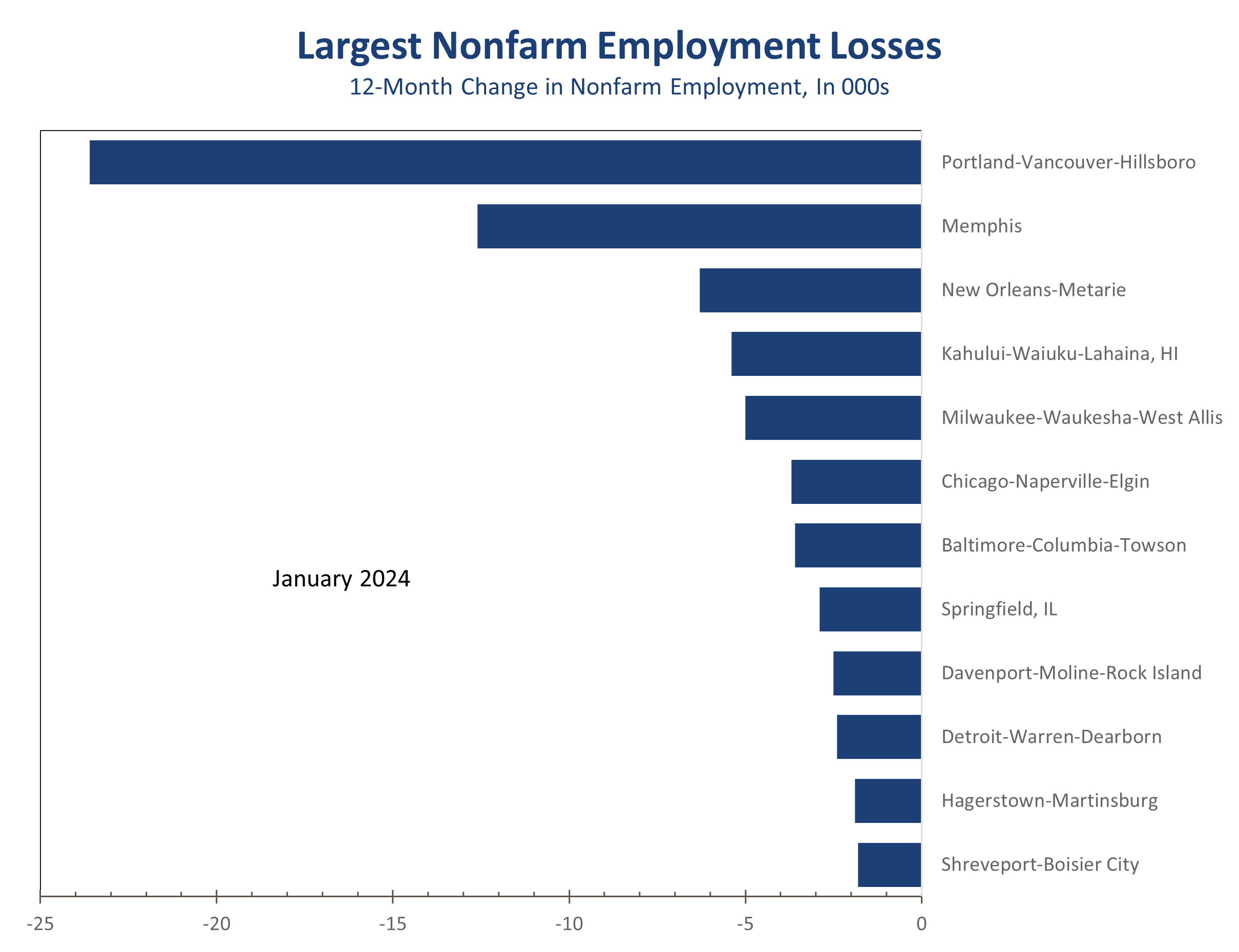

- Job growth is significantly slower in manufacturing-intensive metros. Detroit now shows a slight year-to-year job decline, as do Chicago and Milwaukee, instead of the solid job gains reported in the preliminary data.

- Portland, Oregon is another notable weak spot. Nonfarm payrolls plunged 1.9% over the past year, as employers cut 23,600 jobs.

- Job growth was also notably weaker in the South, with Atlanta, Charlotte, Nashville, and Raleigh adding about half as many jobs as the preliminary data had reported.

- We feel the latest MSA jobs data provide a more accurate assessment of the labor market, which is cooling significantly faster than the monthly national payroll data suggest. The latest QCEW data through September suggest job growth nationally is overstated by at least 800,000 jobs, which means the nation is currently adding just 174,000 jobs per month rather than the now widely assumed 228,000 jobs per month pace.

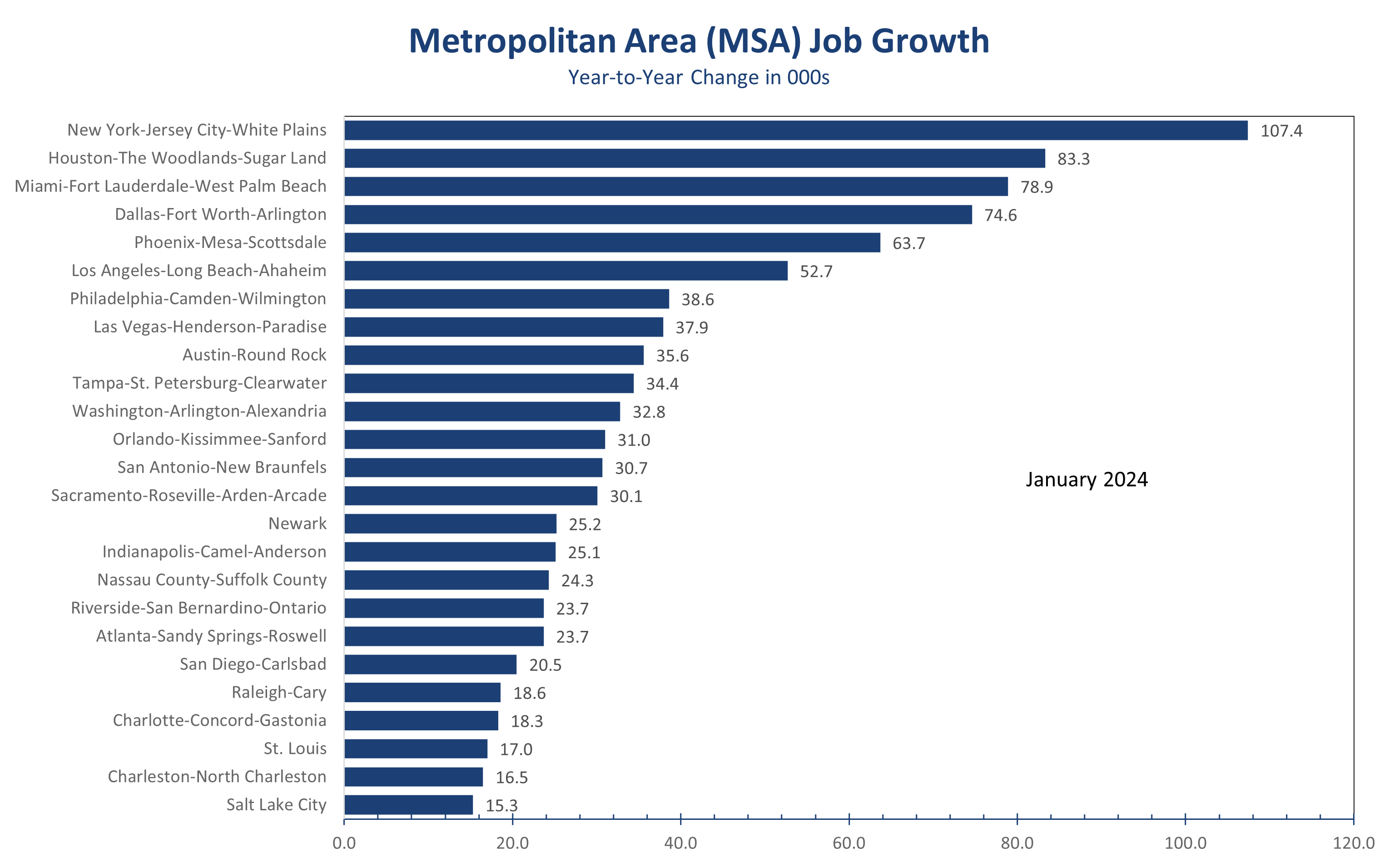

This morning release of the MSA employment data for January 2024 bolster the case that the widely followed monthly national Nonfarm employment data are significantly overstated. The latest state and local employment data include benchmark revisions to data prior to April 2023 and show a much slower trajectory since that date that closely mirror the most recent QCEW data, which are the source data for the annual revisions.

State & Metro Area employment data show job growth slowed significantly across the country.

The Sum of the States data shows nonfarm employment growth slowing to just a 1.4% pace and closely match the QCEW data reported through September. The CES data which are reported the first Friday of the month show job growth averaging a stronger 1.9% pace. The difference is roughly 800,000 jobs and would reduce job growth to an average of 174,000 job per month over the past year, compared to the currently report 228,000 jobs per month.

Differences between national and local economic data are not unusual. What we see peculiar today is the unusual timing of the split and consistency of the divergence between the two series.

From a timing perspective, the national Current Employment Statistics (CES) data, the series published the first Friday of each month, were just revised in January to the March 2023 benchmark. That benchmark was largely based on the Quarterly Census of Employment and Wages (QCEW) data through March of last year. At the time of the revision, data were also available through June and the CES data math up closely with those data, rising 2.41% year-to-year compared to a 2.39% in the QCEW series.

We suspect the national nonfarm payroll growth are now significantly overstated.

Just two weeks after the January employment report, however, QCEW data were released through September, which diverged significantly from the CES figures. While the monthly CES showed 2.1% year-to-year job growth from June to September, QCEW data indicated only 1.5% growth. We noted the unusual divergence from the benchmark revision’s direction in our January and February employment commentaries. National nonfarm job growth through March 2023 were revised lower by 0.2 percentage points but were revised higher for the second half of last year.

The AI-driven stock market rebound hinted the economy might be on the verge of a rebound in hiring, lending some support to the stronger second half jobs numbers. The recent metro area jobs data, however, cast doubt on this theory. San Francisco and Silicon Valley saw sharp downward revisions to job growth, with San Jose/Silicon Valley now showing a 0.1% year-to-year employment decline.

Many manufacturing-intensive metro areas, including Detroit, Chicago, and Milwaukee along with several smaller Midwest metros like Elkhart-Goshen, Kokomo, and Columbus, Indiana, experienced substantial job declines, aligning with soft ISM manufacturing data.

On the plus side, New York City, the Texas major metros, and Florida’s largest MSAs all remain bright spots. New York City added 160,100 jobs, while Houston added 83,300, and 78,900 jobs were added in South Florida.

Job growth was revised lower in many fast-growing metro areas, particularly in the Southeast, with hiring now up roughly half as much as initially reported in Atlanta, Nashville, Charlotte, Raleigh, and Jacksonville.

The weaker state and local jobs data suggests a soft landing remains in play, albeit with slightly higher-than-expected inflation. We anticipate a further slowing in job growth in coming months, with payroll growth decelerating to around 130,000 jobs per month by mid-year. This should pave the way for a rate cut at the late June FOMC meeting.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Mark Vitner, Chief Economist

Piedmont Crescent Capital

(704) 458-4000

Inflation is Still Running Hot

Inflation Once Again Tops Expectations

- Both the overall CPI and the core CPI rose 0.4% in February and are now up 3.2% and 3.8% year-to-year, respectively.

- We have continuously warned inflation would remain stubbornly high during the first half of 2024, reflecting continued pressures from labor-intensive sectors as well as some seasonal adjustment issues.

- Prices held steady at grocery stores and rose only slightly at restaurants. Unfortunately, both remain sharply higher than prior to pandemic, leaving budgets stretched.

- Energy prices rose 2.3% in February, with gasoline prices jumping 3.8% and prices for natural gas (+2.3%), fuel oil (+1.1%) and electricity (+0.3%) all climbing.

- Excluding food and energy products, the core CPI rose 0.4%, driven by another outsized rise in shelter costs. Prices for airline fares (+3.6%) and car insurance (+0.9%) also rose sharply.

- Inflation continues to come in hotter than expected. The breadth of price increases is narrowing, however, with much of this past month’s gains coming from higher housing and energy costs. We continue to expect the Federal Reserve to begin cutting interest rates in June, followed by additional quarter-point cuts in September and December.

Inflation once again exceeded expectations in February, with the CPI rising 0.4% and prices excluding food and energy also rising 0.4%. Despite the disappointing report, price increases were slightly less widespread than in January and show signs of moderating. However, the pace of moderation is slower than what financial markets had anticipated, leading many forecasters to push the Fed’s first rate cut out to June, a position we have held for some time.

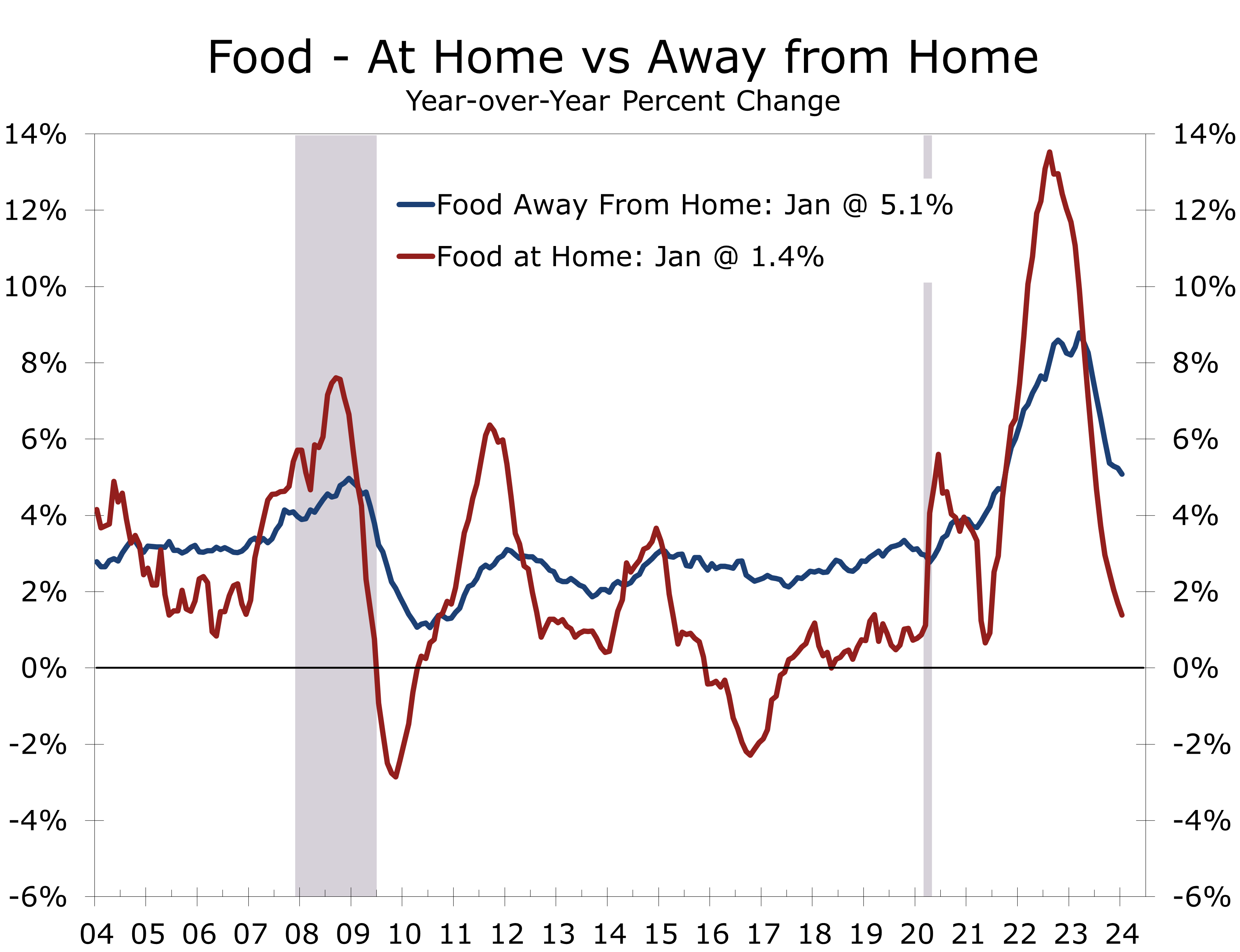

One clear bright spot in the February data is that food prices are rising less rapidly. Prices remained unchanged at grocery store, following a 0.4% increase in January. Prices at restaurants rose just 0.1%, compared to a 0.5% increase in January.

Despite the moderation in food costs, consumers have not seen much relief. Grocery store prices are currently 25% higher than they were in February 2020 – the month before the pandemic hit.

Although prices eased last month, groceries and restaurant costs remain burdensome.

Prices at restaurants have risen by a similar magnitude since February 2020, surging 25.5%. Labor costs have increased sharply at both, rising by 24.9% at grocery stores over the past four years and 28.5% at restaurants. With wages sticky, a moderation in price increases is about as good as it is likely to get.

Persistently high food prices are one reason consumers feel discouraged about the economy. Families are spending 11% of their after-tax income on food, the highest proportion since 1991 according to recent USDA figures. With more income devoted to food, consumers have had to spend less on other items, had to dip into savings, or gone further into debt.

Election year politics is mischaracterizing the causes and remedies for high food costs.

President Biden has taken note of higher food prices and repeatedly cited “Shrinkflation” as one of the causes of higher inflation. Shrinkflation involves reducing the size or quantity of a product while keeping the price steady. The inference is that greedy companies or store owners are behind the higher prices. However, this explanation for inflation is fundamentally flawed and has been used over time, mostly by politicians, to shamelessly shift blame for higher prices, often toward middleman minorities.

Persistent inflation is always a monetary phenomenon. The money supply increased dramatically following the onset of the pandemic, as the Federal Reserve accommodated the massive increase in federal spending by increasing its purchases of federal debt. The growth in the money supply nearly perfectly matches the 25% cumulative increase in food prices.

Energy prices rose by 2.3% in February after two consecutive months of declines, with gasoline prices jumping by 3.8%. Energy prices have been the main contributor to lowering inflation over the past year. Even a slight reversal could significantly slow the improvement in the headline CPI.

Excluding food and energy, the core CPI increased by 0.4% and rose by 3.8% year-on-year. Most goods experienced moderate price changes, although apparel and used car prices rebounded last month. Core goods prices fell 0.3% over the past year.

Core services present the greatest inflation challenge, with prices climbing 0.5% in February and 5.2% over the past year. Housing, particularly residential rent, drove much of the increase, with rents for single-family homes and lease renewals seeing significant rises. In contrast, rents for new leases are slightly declining.

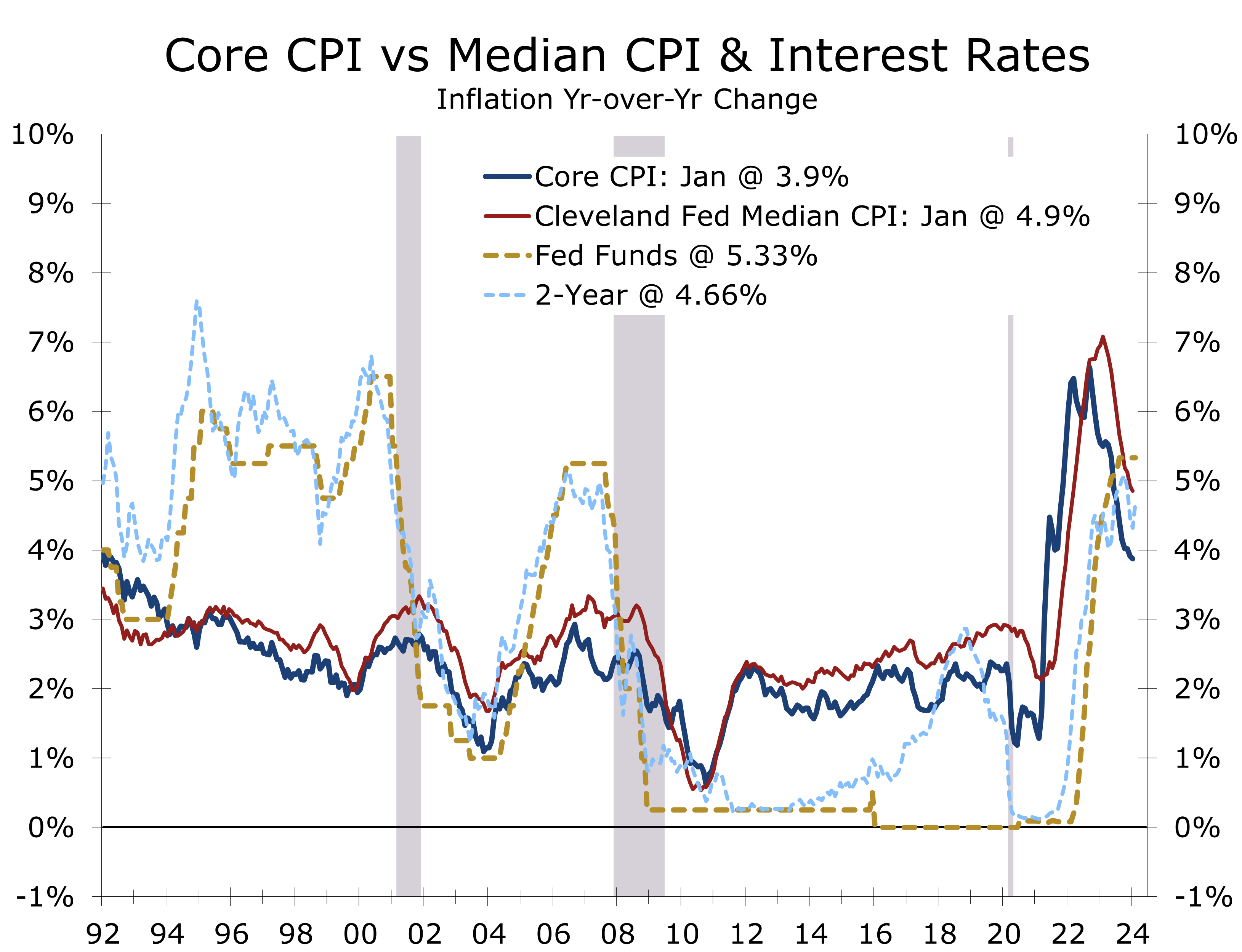

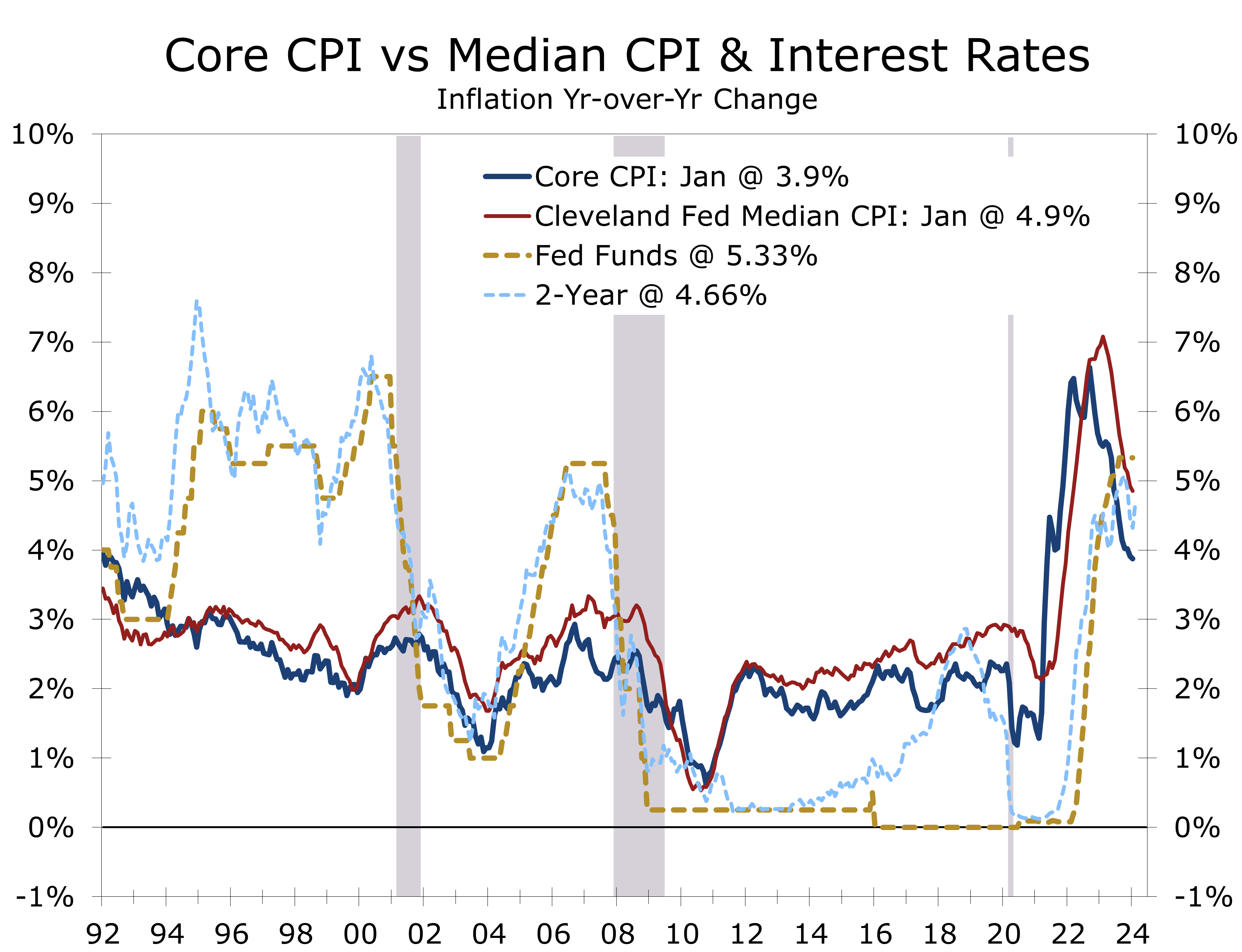

We expect inflation to slowly moderate this spring and summer, allowing the Fed to begin cutting the federal funds rate in late June. We continue to closely monitor the median and trimmed mean inflation figures published by the Federal Reserve Bank of Cleveland, which continue to show a slower and longer journey back to the Fed’s 2% inflation target.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

704-458-4000

Another Confounding Employment Report

Softening is Evident Beneath the Headlines

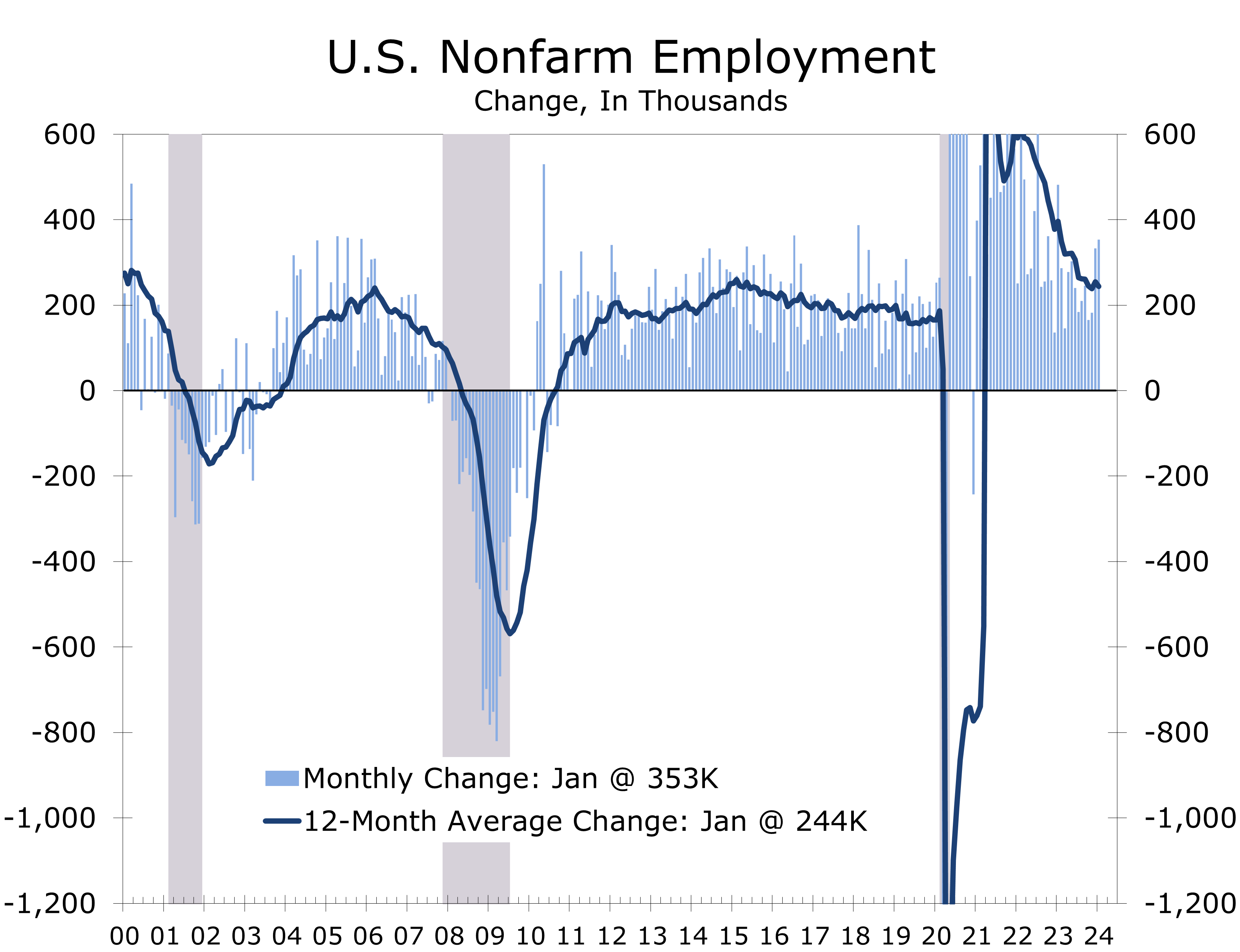

- Nonfarm employment once again topped consensus expectations, with employers adding a net 275,000 jobs in February.

- While hiring rose in most industries, gains were concentrated in health care, leisure and hospitality and government.

- Weather also boosted job growth, lifting construction payrolls, and also contributed to a big rebound in weekly hours.

- Job growth was revised lower by a combined 167,000 jobs for the prior two months.

- The unemployment rate also jumped 0.2 pp to 3.9%, as household employment fell by 184K and the labor force grew by 150K, lifting unemployment by 334K.

- Newly released data indicate third-quarter payrolls were also significantly overstated.

- The monthly employment data remain confounding, with initial reports continuing to come in well ahead of market expectations but downward revisions to prior data allaying fears of the economy overheating. We believe hiring is slowing more than the headlines suggest and look for payroll growth to meaningfully decelerate this spring.

Nonfarm employment blew past consensus expectations, with employers adding 275,000 jobs in February. Upside surprises to monthly payroll growth are becoming the norm. The markets appear to be discounting the strong headline gains; however, data have repeatedly been revised lower.

This was the case in the February report, which saw payroll growth revised lower for January and December by a combined 167,000 jobs. Even after the downward revisions, payroll growth for the past three months still averaged a whopping 265,000 jobs per month. Nonfarm employment has risen at a 2% annual rate over the past three months, slightly ahead of the 1.8% pace maintained over the past year.

We suspect job growth is currently significantly overstated and look for hiring to decelerate.

Job growth around yearend is notoriously volatile and may be even more so today, given the wide swings in economic activity during and after the pandemic lockdowns. These wider swings likely distorted seasonal adjustments.

We suspect payrolls are now overstated, as recently released QCEW data reveal only a 1.5% year-to-year increase in Q3 2023, approximately 800,000 jobs fewer than the currently reported 2.4% growth. The smaller job gain will show up in next year’s annual revisions.

We do not believe there is anything nefarious in today’s overstated jobs figures. For starters, the response rate to the monthly employer survey is well below its pre-pandemic norm, resulting in larger revisions to prior month’s data. Seasonal adjustment is also likely being exaggerated by the larger swings in payrolls that occurred around the pandemic. Additionally, employers are holding onto seasonal hires amidst a persistently tight labor market.

Hiring was broad based, as improved weather lifted hiring in a number of industries.

Job growth was broad-based in February, as hiring rebounded in several industries previously hindered by unusually harsh winter weather in January. Construction payrolls rose by 23,000 in February, driven by significant gains in heavy construction. Hiring also saw a resurgence in transportation, warehousing, retail, and restaurant sectors. Overall, we estimate that the improvement in weather contributed to around 50,000 of February’s net job gains.

Although hiring rebounded in many industries, job growth remained highly concentrated, with health care (+66.7K) and social assistance (+24K) accounting for nearly one-third of February’s gain. Government (+52K) and leisure and hospitality (+58K) also experienced robust job gains. However, manufacturers cut 4,000 jobs.

We expect nonfarm payroll growth to decelerate to 160,000 jobs per month this spring. The unemployment rate is also expected to edge higher to just over 4%. This should allow the Fed to cut the federal funds rate by a quarter point in June, followed by similar cuts in September and December.

February’s household employment data was surprisingly weak. The number of employed individuals fell by 184,000, while the labor force increased by 150,000, resulting in 334,000 more unemployed. As a result, the unemployment rate rose to 3.9%.

A rebound in weekly hours helped reverse last month’s spike in average hourly earnings.

Household employment, which has historically been good at detecting turning points, is meaningfully weaker than the payroll data when viewed on a consistent basis. Adjusted household employment has now fallen for three consecutive months and is down a collective 1.474 million jobs since November.

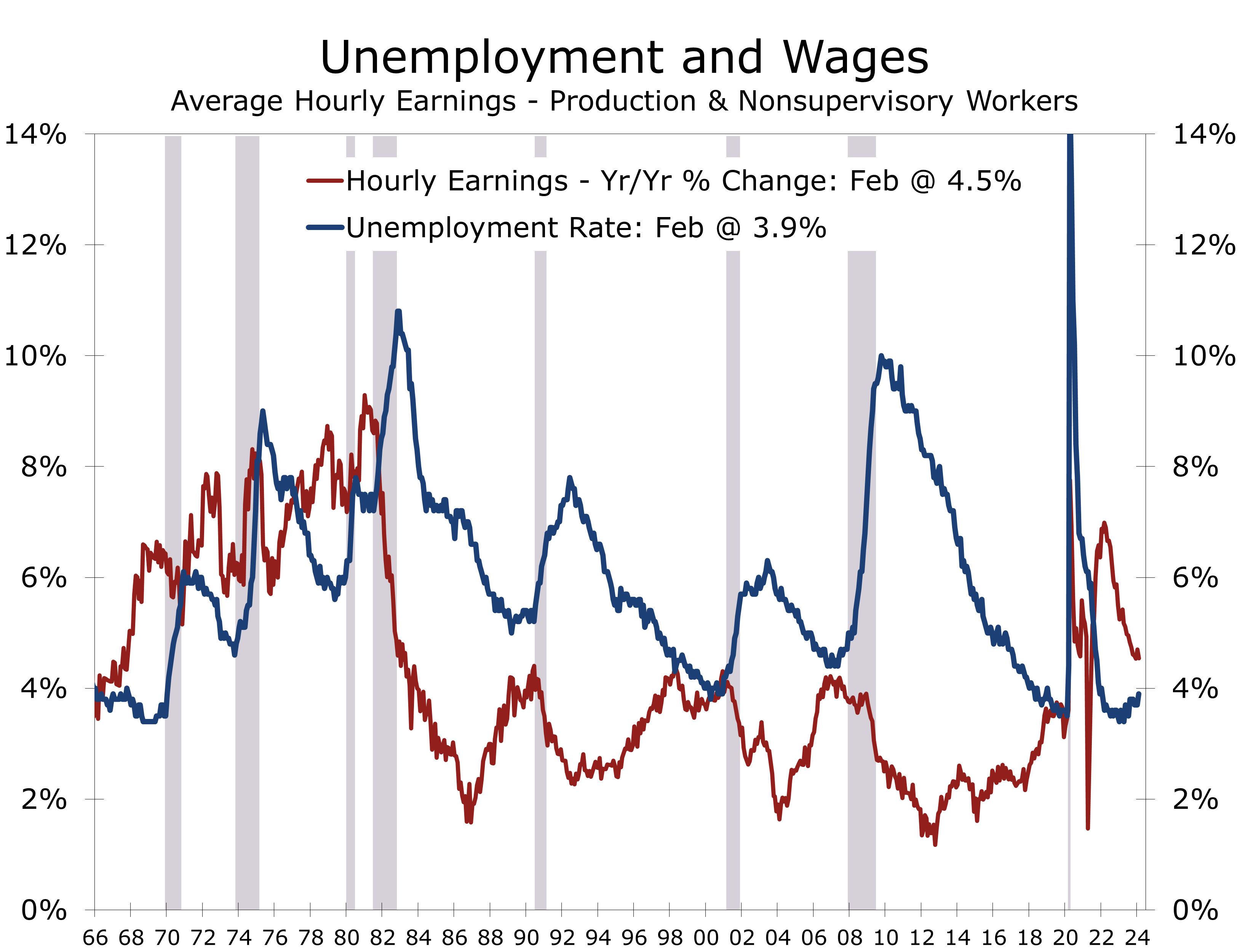

Rising unemployment should help contain inflation. Average hourly earnings grew by just 0.1% in February and are now up 4.3% over the past year.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

In Rate Cuts We Trust

Soft Landing Hopes Are Closely Tied to Rate Cuts

-

- January’s astonishing 356,000-job rise in nonfarm employment and upward revisions to prior months’ data suggest the economy began the year with surprisingly strong momentum. Consensus forecasts for first quarter GDP growth have been ramped up and remain above 2%, even following disappointing reports on retail sales and industrial production. Our own forecast calls for real GDP to rise at a 2.4% in Q1 and 2.5% for all of 2024 (annual basis).

- A larger than expected rise in the January’s Consumer Price Index was the most disruptive data point this past month. The slightly larger than expected increase in both the headline and core price measures indicates inflation will not likely moderate as fast as the markets had expected. Broader prices measures, such as the Cleveland Fed’s Median CPI, show that inflation remains sticky in many labor-intensive parts of the economy. The PPI data also came in on the high side.

- Higher and stickier inflation throws a wrench into the mechanics of forecasts calling for aggressive cuts in the federal funds rate this year. If inflation remains higher, real rates will rise less and likely limit the Fed to 3 or, at most, 4 quarter-point cuts this year, beginning in May or June. That trajectory is in line with the recent 2-Treasury yield, which consistently provides a good approximation of the federal funds rate one year out.

- While the U.S. economy is proving resilient, global economic growth is surprisingly weak. Concerted efforts by manufacturers to diversify their production base and supply chains continues to weigh on China’s economy. Japan and the U.K. have both fallen into recession. The US, India and Mexico are notable upside surprises and offset part of this weakness.

- Weaker global growth should help curb inflation, giving the Fed room to cut rates. Geopolitical risks are boosting shipping costs, however, adding to global uncertainty. While the U.S. economy has repeatedly proved resilient, the business cycle appears both old and delicate in some respects, while vibrant and dynamic in others. Notably, the stock market's strength, driven by the AI revolution, mirrors the mid-1990s technology boom, producing a then record-long expansion.

Early data for the first quarter show the economy had strong momentum headed into the new year. Most notably, employers added 356,000 net new jobs in January and job gains for preceding months were revised higher. The gains were a bit of a surprise, as the annual benchmark revisions released with January’s data lowered the level of employment for the March 2023 benchmark month by 266,000 jobs. Hiring bounced back in the second half of the year, however, and ended the year slightly higher than previously reported under the 2022 benchmark. With the revisions, average monthly job growth for 2023 was revised up to 255,000 from 225,000 previously.

The upward revisions to the second half of the year’s jobs data are extremely unusual. Typically, revisions to subsequent months’ job growth follow the direction of the benchmark revisions, which were about 0.2% lower. While data for most months were revised slightly lower, data for December was revised up sharply, more than making up for the slight downward revisions. While unusual, the stronger job gains are consistent with stronger GDP growth during the second half of the year, which averaged a whopping 4.1% pace. The breadth of employment growth also improved toward the end of the year and in January.

How much weight should be assigned to January’s stronger employment data remains unclear. Nonfarm employment growth has averaged a 289,000-job pace over the past three months, much of which was due to a surge in job growth in December (333,000) and January (353,000). By comparison, employment growth in the prior year averaged just 244,000 jobs per month.

Employment is unusually volatile around yearend, with holiday hiring at retailers, restaurants, and delivery services spiking in November and December and typically plummeting in January. Seasonal adjustment smoothed these swings but the pandemic and changes in consumer behavior afterward have distorted this process. Just how large these seasonal factors are cannot be exaggerated. On a non-seasonally adjusted basis, employers cut 2,635,000 jobs in January. Since that was fewer job losses than usual, the seasonally adjusted data reported a 353,000-job gain.

Average weekly hours declined in January, falling 0.2 to 34.1 hours, the lowest since the Pandemic. The drop was impacted by harsh weather during the survey week. After leaping to 4.2% following the ISM manufacturing and construction spending reports, the closely watched Atlanta Fed GDPNow forecast for first quarter GDP growth settled in at 3.5% in the aftermath of the strong employment figures. This measure has since retreated to 2.5% as more economic data have been released, close to our own forecast of 2.4% growth.

Stronger employment growth also implies the stellar productivity data reported for the fourth quarter might be revised lower from their preliminary 3.2% pace reported. The preliminary data also show productivity for the nonfarm business sector rose 1.2% for the year, which should be impacted slightly less. With 1.2% productivity growth and 4.5% wage growth, the Consumer Price Index will have a tough time breaking significantly below the most recent 3.1% year-to-year increase. Indeed, prices have been sticky for about anything where labor makes up a large proportion of costs.

Wages appear to have risen sharply in January, when higher minimum wages took effect in 22 states. Grocery prices rose 0.4% in January but have risen a modest 1.4% this past year. Prices have surged by 21.1% over the past three years, however, four times the pace of the preceding three years! The increase over the past three years is equivalent to the cumulative rise in grocery store prices from 2008 to 2021.

President Biden addressed rising grocery prices in a TikTok message before the Super Bowl, blaming ‘greedy’ corporations for what he called Greedflation and Shrinkflation. Shrinkflation involves reducing package sizes while maintaining the same price. Lael Brainard from the White House National Economic Council echoed these concerns, emphasizing wider profit margins at grocery stores. We see the inflation problem as more genuine. Average hourly earnings for grocery store workers skyrocketed 18.3% over the past three years and consumers have pushed back at efficiency measures, such as self-checkout. The problem with inflation is one of too much money chasing too few goods. While product shortages have diminished, wages are sticky and grocery stores, which historically operate on paper thin profit margins, have little capacity to cut prices.

Restaurants are another area where higher wages are being passed along to customers. Restaurants have been short staffed since the economy emerged from the Pandemic, which has sent average hourly earnings soaring 31.7% over the past three years. Not surprisingly, prices are up substantially, making restaurant dining more of a luxury for about everyone. Sales at restaurants and bars were one of the bright spots in an otherwise dreary January retail sales report. Sales at restaurants rose 0.7% in January and are up 6.3% over the past year. After accounting for inflation, however, sales rose just 0.2% in January and are up just 1.2% over the past year.

We remain cautious about inflation. Pandemic-driven price swings, particularly for used cars, health care services, and apartments, skewed seasonal adjustments and understated inflation as prices stabilized in 2023. We expect inflation to remain firm through the middle of this year, as prices for health care services rebound during the second half of last year.

The Cleveland Fed’s Median CPI provides a more consistent assessment. Despite higher readings, this measure still suggests moderating prices, enabling the Fed to initiate a quarter-point cut in the federal funds rate by the end of June, followed by successive cuts in September and December. Our forecast is well below the market consensus, as shown by the CME’s fed funds futures but the aligns with the recent trend in the 2-Year Treasury Note, which has reliably provided an indication of where the federal funds rate will be one year ahead. Fed funds futures are continuing to look for five or six quarter-point cuts over the next year.

Let there be no doubt, the Fed is walking a fine line. Monetary policy is tight today, as can be seen by higher real interest rates. The effective federal funds rate is currently 5.33%, which is 213 basis points (bp) above the latest change in overall CPI and 143 bp over the core CPI. A neutral fed policy, with the economy at full employment, would peg the real federal funds rate at between 50 bp and 100 bp over the core CPI. The Fed would like to be able to lower interest rates, which might extend the business cycle and help avoid the problems in the commercial real estate sector from metastasizing into a systemic threat. The Fed does not want to ease too early or by too much, which would put its hard-won gains at bringing down inflation at risk.

We see the overall CPI easing to 2.7% by the end of 2024 and look for the core CPI to decelerate to 3.2%. That should provide the Fed with enough room to cut the funds rate three or four times by year-end. While our forecast still has three rate cuts in it, recent data show the global economy slowing more abruptly. China is now a source of global disinflation in goods, reflecting efforts to stem the exodus of firms looking to diversify their supply chains. Growth has also weakened in Japan and the UK – both of which are in recession. Weaker global growth may cause inflation to ease faster and might allow the Fed to ease a little sooner.

The Fed also must guard against further fueling asset bubbles. The stock market has rallied strongly ever since the December FOMC meeting when the Fed made it clear that they had finished raising interest rates. While the markets suffered a brief setback following January’s disappointing CPI report, the market quickly bounced back and handled the disappointing Producer Price Index data much better. Initial public offerings and mergers and acquisitions have also increased, as have share buyback announcements and even the venture capital market. All of which are good things in moderation but can lead to a massive hangover if they rise out proportion with the underlying fundamentals.

Lower interest rates would surely benefit the housing sector. Many current homeowners secured ultra-low interest rates during the prolonged period of near-zero short-term rates during and immediate after the pandemic. Presently, around 78.7% of first-lien mortgages have rates of 5% or less, with 59.4% below 4% and 22.6% below 3%. With current mortgage rates hovering around 6.80%, homeowners are understandably hesitant to sell their homes, fearing significant increases in their housing cost even if they are downsizing. Consequently, there is a shortage of existing homes for sale, which has driven up prices and led to near-record lows in housing affordability.

The dearth of existing homes has been a godsend for home builders. Many potential home buyers that would have purchased an existing home are now looking to purchase a new home and home builders have ramped up their offerings of entry-level homes. Home builders are also offering financing incentives to reduce the sting of higher mortgage rates. The result is a two-tiered housing market. New home sales and single-family housing starts are holding up well, while existing home sales, which is a much larger market, continue to struggle.

Mortgage rates had pulled back prior to January’s surprising CPI report but have now surged back toward 7%. That earlier pullback in mortgage rates had boosted home buying but buyer traffic has slowed more recently. We expect mortgage rates to decline gradually this year and to end the year around 6.40%. Unfortunately, mortgage rates will have to drop well below 6% before a substantial number of existing homeowners will feel comfortable enough to part with their current low-rate mortgage and put their current home on the market.

Lower interest rates would be even more beneficial in helping resolve the brewing troubles in commercial real estate. Real estate values are closely tied to interest rates, as the stream of rents earned from owning income producing properties is more valuable when interest rates are lower. Property values skyrocketed during the pandemic period and its immediate aftermath, when short-term interest rates were near zero and real estate investors who were overcommitted to gateway markets rushed into secondary markets in the Sun Belt. Apartments and industrial properties saw the largest increase. Prices for retail and office properties rose less.

Property price appreciation surged in late 2021 and early 2022, but then slowed sharply as the Fed raised interest rates more aggressively than anticipated. Office building prices, especially older ones in downtown areas, were significantly impacted. Concerns have arisen about a potential repeat of the Global Financial Crisis, but Fed and Administration officials, including Treasury Secretary Janet Yellen, do not foresee a systemic crisis threatening the banking system.

The problems in commercial real estate are both simple and complex. From a simple standpoint, commercial real estate values have come under pressure because interest rates have risen abruptly, while rents have risen less rapidly or fallen. Moreover, insurance and operating costs have risen substantially. Changes in consumer behavior in the aftermath of the pandemic introduce a more complex component into the outlook. One of the most obvious changes has been the slow return to the workplace, particularly in downtown areas, which has led many large employers to consolidate office space and sent values for some office buildings plummeting.

Not all office buildings are struggling, however, and office buildings are just one asset class within commercial real estate. Newer office buildings are performing relatively well, as employers are striving to entice workers back to the office. Many suburban properties are also faring better, as workers are more inclined to return to offices in the suburbs that are closer to home and do not charge for parking.

Commercial real estate looks far less menacing outside of the office market. There are a record number of apartments currently under construction, which will cause vacancy rates to rise later this year. But all these apartments will not be completed at once and there is an undersupply of housing in general. Nevertheless, property prices will fall this year and some investors may have trouble rolling over their maturing debt. Lower interest rates would make this easier.

Elsewhere, the industrial market and retail market are likely to see few problems. To be certain, property prices are correcting but demand remains strong. The industrial market is benefiting from reshoring and continued growth in online retailing. Both have much further to run. The retail market is also doing better. The sector has seen little construction this past decade and is seeing strong demand for open-air retail space. Flexible work schedules mean workers have more time to shop, travel and entertain, which is good for brick-and-mortar retail.

We have once again boosted our near-term forecast and see real GDP rising at a 2.4% annual rate during the first quarter. When taken together with the stronger growth in the second half of last year, real GDP is likely to grow 2.5% this year on an annual average basis, even though not one single quarter will see growth that high. On a fourth quarter-to-fourth-quarter basis, we look for real GDP to rise 1.7% in 2004.

Inflation is expected to continue to moderate, although labor-intensive services will continue to see larger price gains. Shipping delays due to the attacks in the Red Sea and low water levels in the Panama Canal have also boosted container rates, which presents some near-term risk. We look for a more meaningful deceleration in inflation in the second half of this year, which should allow the Fed to gradually reduce the federal funds rate.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice. Any forward-looking statements or forecasts are not guaranteed and are subject to change at any time. Information from external sources have not been verified but are generally considered reliable.

© 2024 CAVU Securities, LLC

February 20, 2024

mark.vitner@piedmontcrescentcapital.com

Chief Economist (704) 458-4000

Haley Tries to Make a Stand in South Carolina

Are the Primaries Over Before They Get Started?

- South Carolina's upcoming primary, traditionally pivotal, is expected to be a mere formality this year, given the dominance of Trump and Biden in previous contests.

- The Democrats already held their primary in South Carolina, which was their first official primary. Biden easily won with 96% of the vote. Voter turnout was extremely light.

- Nikki Haley is the sole remaining Republican challenger to Donald Trump and trails the former president badly despite being a popular former governor and successful UN Ambassador for President Trump.

- Despite facing a likely defeat in her home state, Haley remains determined to continue her campaign through Super Tuesday, eyeing delegate-rich states to gather support and potentially challenge Trump at the convention.

While we are still at the start of the primary season, with just three states having cast their votes so far, the outcomes of both the Democrat and Republican races appear to have already been decided. On the Democrat side, President Joe Biden has faced only token opposition, while a bevy of Republican challengers to former President Donald Trump has been narrowed down to one: former South Carolina Governor and UN Ambassador Nikki Haley.

The Iowa Caucuses, the inaugural event of the primary season, mirrored pre-caucus polling, extinguishing the hopes of anti-Trump Republicans. Formerly perceived as a formidable contender, Florida Governor Ron DeSantis bowed out of the race following a lackluster performance and threw his support behind the former president. The Democrats skipped Iowa altogether.

Anticipation surrounded the New Hampshire primary, where a potential showdown between Trump and former Governor Nikki Haley was projected. Trump emerged as the unequivocal victor, however, further cementing his frontrunner status. With Haley remaining as the only major Republican challenger, Trump maintains a commanding lead in polling. On the Democrat side, Biden cruised to an easy victory.

The upcoming South Carolina primary, traditionally a pivotal event, is now poised to serve as a mere formality. In 2020, the South Carolina primary proved crucial for Joe Biden, who beat back an unexpectedly strong challenge from Bernie Sanders following a key endorsement from Congressman Jim Clyburn. South Carolina was the turning point of Biden’s campaign.

The Democratic primary was held earlier this year, partially to build off the momentum Biden gained from the 2020 South Carolina primary. Biden faced only token opposition and won the Palmetto State, garnering 96.2% of the vote. However, voter turnout was extremely light, with just 4% of registered Democrats casting their votes, down from 16% in 2020.

The Republican primary will be held on Saturday, February 24th. Despite running against a popular and charismatic former governor, Donald Trump has maintained a substantial lead in every major poll, averaging over thirty points most recently. Trump has also garnered multiple endorsements, including Governor McMaster and Senators Tim Scott and Lindsey Graham.

Despite being a popular and well-liked former governor, Nikki Haley has few endorsements.

Haley’s list of allies in her home state is comparatively thin. Her most significant endorsement comes from Congressman Ralph Norman, who represents the Rock Hill area.

Nikki Haley was viewed as a top contender for the Republican nomination for years before her campaign’s launch. She involved herself directly in the 2016 primary by endorsing Senator Marco Rubio of Florida. Haley’s work as UN Ambassador in the Trump administration kept her in the national spotlight.

Her tenure at the UN is viewed as extraordinarily successful. Haley was a staunch advocate for Israel and pushed back forcefully against critics of both the United States and Israel. Her unwavering support for Israel became especially relevant after the October 7th attack and subsequent war in Gaza. She is one of a handful of Trump appointees who left the Administration in good standing.

Haley’s tenure as governor, which extended from January 2011 to January 2017, is also widely viewed as successful. South Carolina consistently outperformed the nation as the economy recovered from the Great Recession and welcomed waves of new businesses.

Despite being a popular and well-liked former governor, Nikki Haley has few endorsements.

South Carolina particularly excelled in attracting international investment, boasting the highest foreign direct investment per capita in the nation. Notable projects secured during Haley’s leadership include new plants for companies like Volvo, Mercedes Benz, Continental Tire, and Torey Materials. Additionally, Haley helped secure a major expansion of Boeing’s operations in North Charleston and subsequently joined their board of directors. These successes earned South Carolina the nickname “Beast of the Southeast,” a label proudly touted by Haley during her campaign.

Haley governed South Carolina as a pro-business conservative. She cut taxes and regulations, courted new industry, and expanded investments made by her predecessors. Additionally, she took on organized labor and defeated a unionization attempt at Boeing. She did this at a time when the US economy was slowly emerging from the Great Recession and faced competitive challenges from neighboring states.

While some critics suggest Haley gets too much credit for South Carolina’s success, the record shows she played an active role in the state’s economic growth and attracting industrial investment in particular. Moreover, Haley, who hails from Bamberg, South Carolina, a small city in the state’s Lowcountry region, did a remarkable job in ensuring the investment boom reached every corner of the state.

Haley also adeptly managed delicate social crises. Following the 2015 mass shooting at Charleston’s Emanuel Church and the shooting of Walter Scott, an unarmed African American man pulled over for a traffic stop, Haley drew national attention when she orchestrated the removal of the Confederate flag from the state capitol. The debate over the Confederate flag had been a long-running divisive issue and became increasingly more difficult to defend as South Carolina’s population grew and new industry relocated to the state. Haley stopped short of condemning the flag altogether, stating that for many, the flag symbolizes heritage rather than hate.

Haley’s skill in handling race-related issues as a southern governor was commendable, but her recent omission of slavery as the root cause of the Civil War in New Hampshire drew criticism and tarnished her otherwise well-thought-of reputation on the subject.

Haley’s center-right stance on cultural issues, including her refusal to support a North Carolina-style bathroom bill and her opposition to national abortion legislation, has drawn criticism from some likely Republican primary voters. Despite this, many see these positions as key to her electability in the general election.

If Haley overperforms expectations on Saturday, she would owe it to South Carolina’s status as an open primary state. Independents and Democrats who did not cast ballots in the earlier Democratic primary will have the option to vote in the Republican contest. These voters would presumably break for Haley over Trump. The Haley campaign banked on such crossover votes in New Hampshire, however, and still fell considerably short. South Carolina is significantly more conservative than New Hampshire, so Haley will need more than just moderates to make it close.

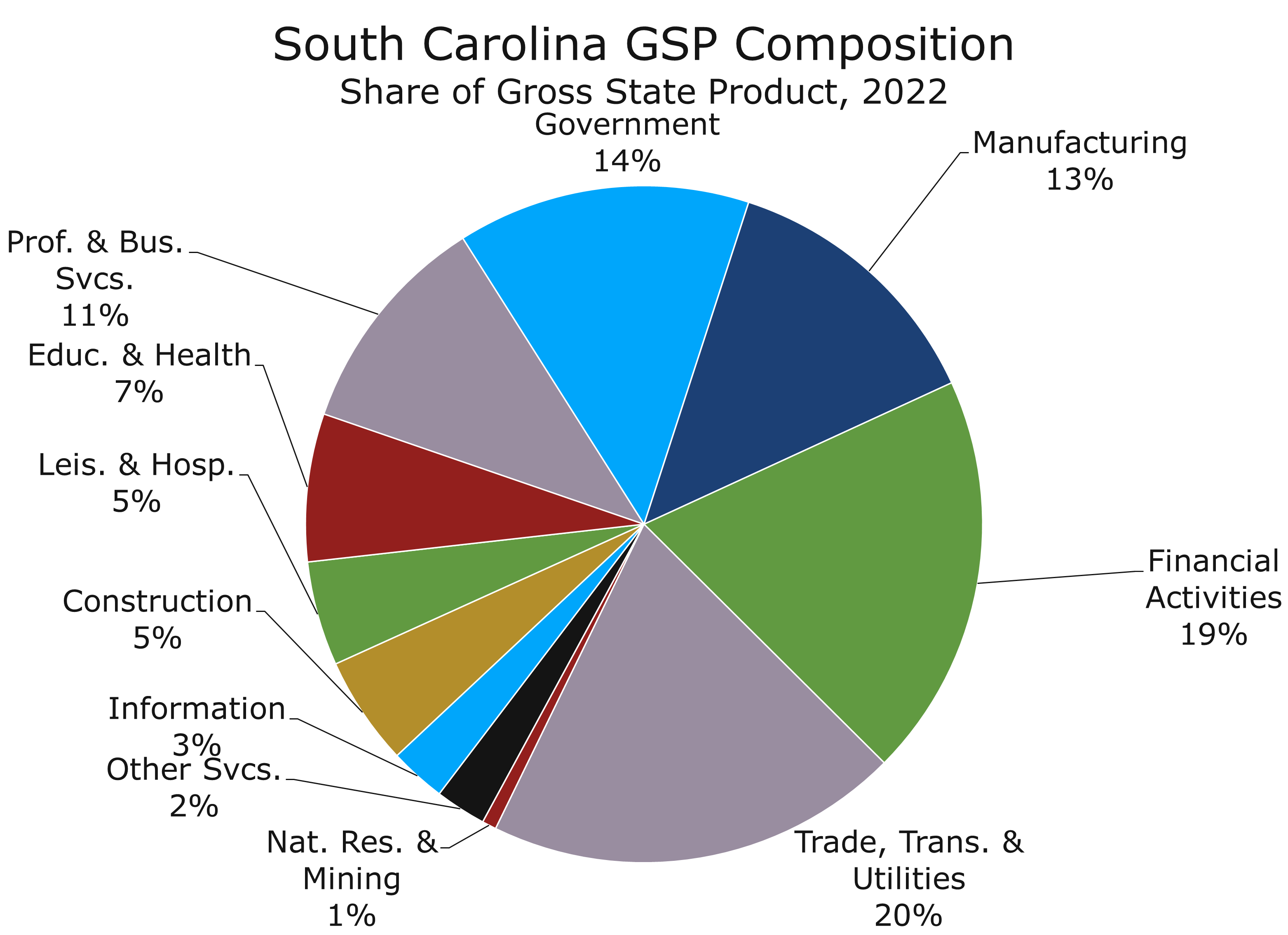

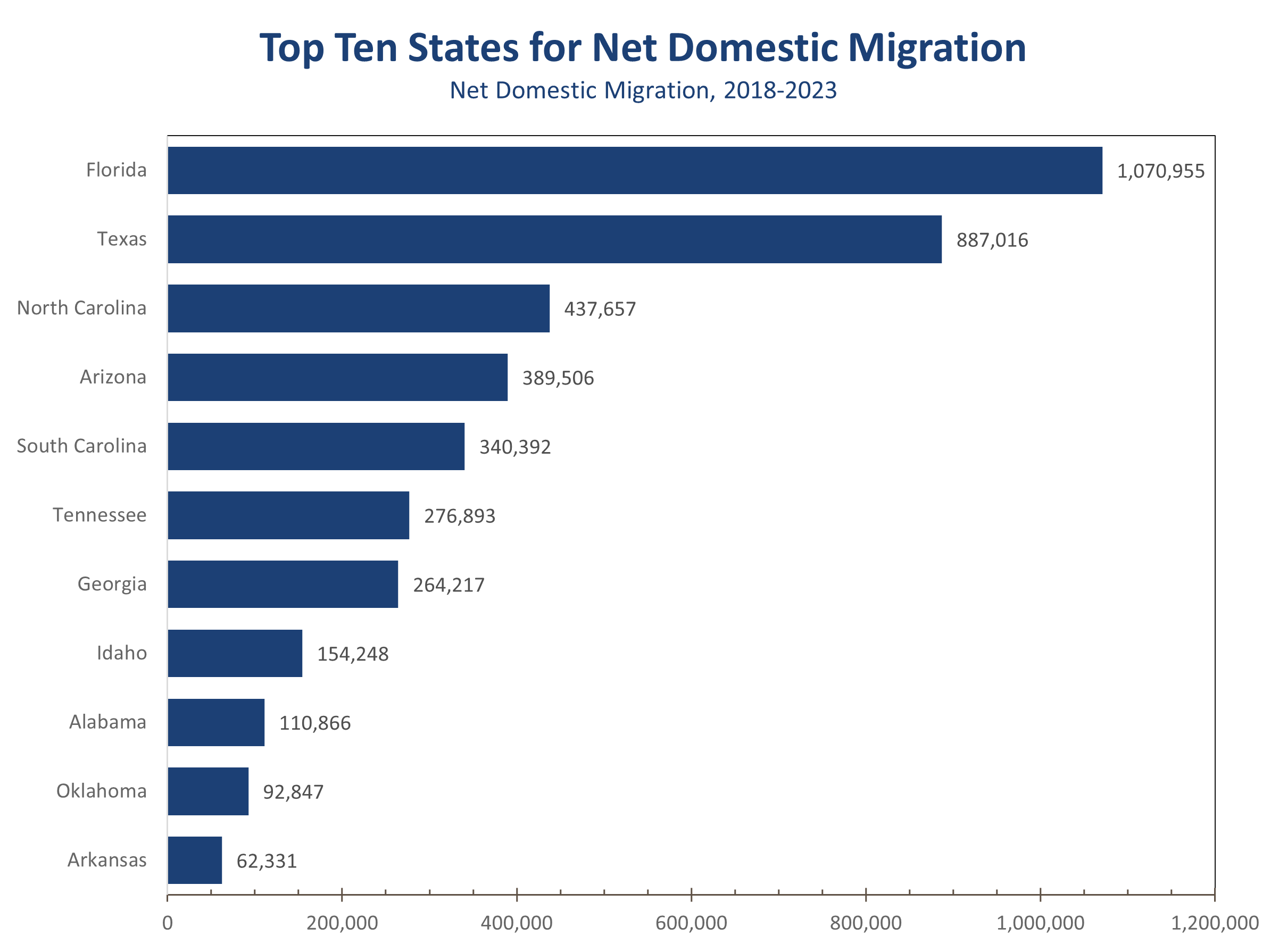

New voters might also help. South Carolina has enjoyed strong domestic in-migration in the past few years and led the nation in domestic in-migration in percentage terms this past year. In absolute numbers, 340,392 more people have moved to South Carolina over the past 5 years than moved away, with many relocating from the Northeast.

Despite facing a likely defeat in her home state, Haley vows to continue her campaign through Super Tuesday, focusing on delegate-rich states like California and Massachusetts. While victory in any state on March 5th seems improbable, her aim is to gather enough delegates to present a viable option at the convention, especially if Trump’s campaign encounters setbacks away from the campaign trail.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 22, 2024

mark.vitner@piedmontcrescentcapital.com

Chief Economist (704) 458-4000

saul.vitner@piedmontcrescentcapital.com

Policy Analyst (704) 458-8570

The CPI Comes in Higher Than Expected

Inflation Rises Slightly Faster in January

- The Consumer Price Index rose 0.3% in January, a touch above the consensus estimate of 0.2%.

- Prices excluding food and energy items rose 0.4%, also 0.1 percentage point above expectations.

- The slightly larger price gains reflect larger than usual start-of-the-year price hikes in many labor-intensive categories.

- Price increases for several health care services categories posted outsized gains relative to recent months.

- Shelter costs were another problem area, rising 0.6% in January. Owners’ equivalent rent rose 0.6%, while rent of shelter rose 0.4% and lodging costs jumped 2.4%.

- Price increases also picked up at the grocery store, rising 0.4%, while prices at restaurants rose 0.5%. Used care prices continued their retreat, falling 3.4%.

- January’s CPI data are a wake-up call for those that believed the Fed had the all-clear signal to cut rates. Last year’s deceleration in inflation was likely overstated due to pandemic-related price swings. We are now seeing a bit of catch up, which supports our view that the Fed will remain cautious.

Inflation came in slightly higher than expected in January, with the headline CPI rising 0.3% and the closely watched core CPI rising 0.4%. Both were 0.1 percentage point above consensus expectations, which disappointed the financial market. Year-to-year, the CPI is now up 3.1%, while the core is up 3.9%.

Food prices picked back up in January, with prices rising 0.4% at the grocery store and climbing 0.5% at restaurants. Grocery store price increases had largely moderated during the second half of the year, rising at just a 1.8% pace form June to December. Prices for sugar and sweets, fats and oils, other foods each rose 0.6%. Prices for fresh vegetables also increased, rising 0.4%, and prices for eggs jumped 3.4%.

Restaurant prices, influenced more by labor costs, moderated less than grocery prices last year. Minimum wage increases in many areas, effective in January, partly contributed to this past month’s outsized rise.

Labor-intensive services saw significant price increases, partly due to a higher minimum wage.

Energy prices fell 0.9% in January, which is one reason why inflation expectations were so low. Gasoline prices did fall sharply, declining 3.3%, while fuel oil prices fell 4.5%. Electricity prices rose 1.2%, however, and natural gas prices rose 2.0%. Those large price hike likely reflect earlier enacted regulatory approvals that kicked into effect at the start of the year.

Grocery store prices are up a surprisingly modest 1.2% over the past year. The modest increase follows colossal gains in prior years, however. Grocery store prices are up a collective 21.1% over the past three years, which is roughly four times as much as they rose in the prior three years. The increase over the past three years is roughly equivalent to the cumulative rise in grocery store prices from 2008 to 2021.

Shrinkflation? Grocery store prices are up a collective 21.1% over the past three years.

Shelter costs rose 0.6% in January and accounted for over two thirds of the increase in the core CPI. Owners’ equivalent rent, which is the index that attempts to capture the cost of homeownership, rose 0.6% in January and is up 6.2% over the past year. Rent of shelter, which captures the cost of rental apartments and single-family rentals, rose 0.4% and is up 6.1% over the past year.

Shelter costs account for roughly 36.2% of the overall CPI and a whopping 45.4% of the core CPI. The BLS rental measure lags behind market rates, which currently show minimal changes for new leases and about a 2.5% increase for renewals. There is a tidal wave of apartments slated to be completed to be completed this year, which should put additional downward pressure on rents and consumer prices.

Prices for certain pandemic-impacted items, like used cars and trucks, declined by 3.4% in January and fell 3.5% over the past year. In contrast, these prices had surged by 24.2% over the previous two years. Gasoline prices have also fallen sharply, plunging 14.2% this past year.

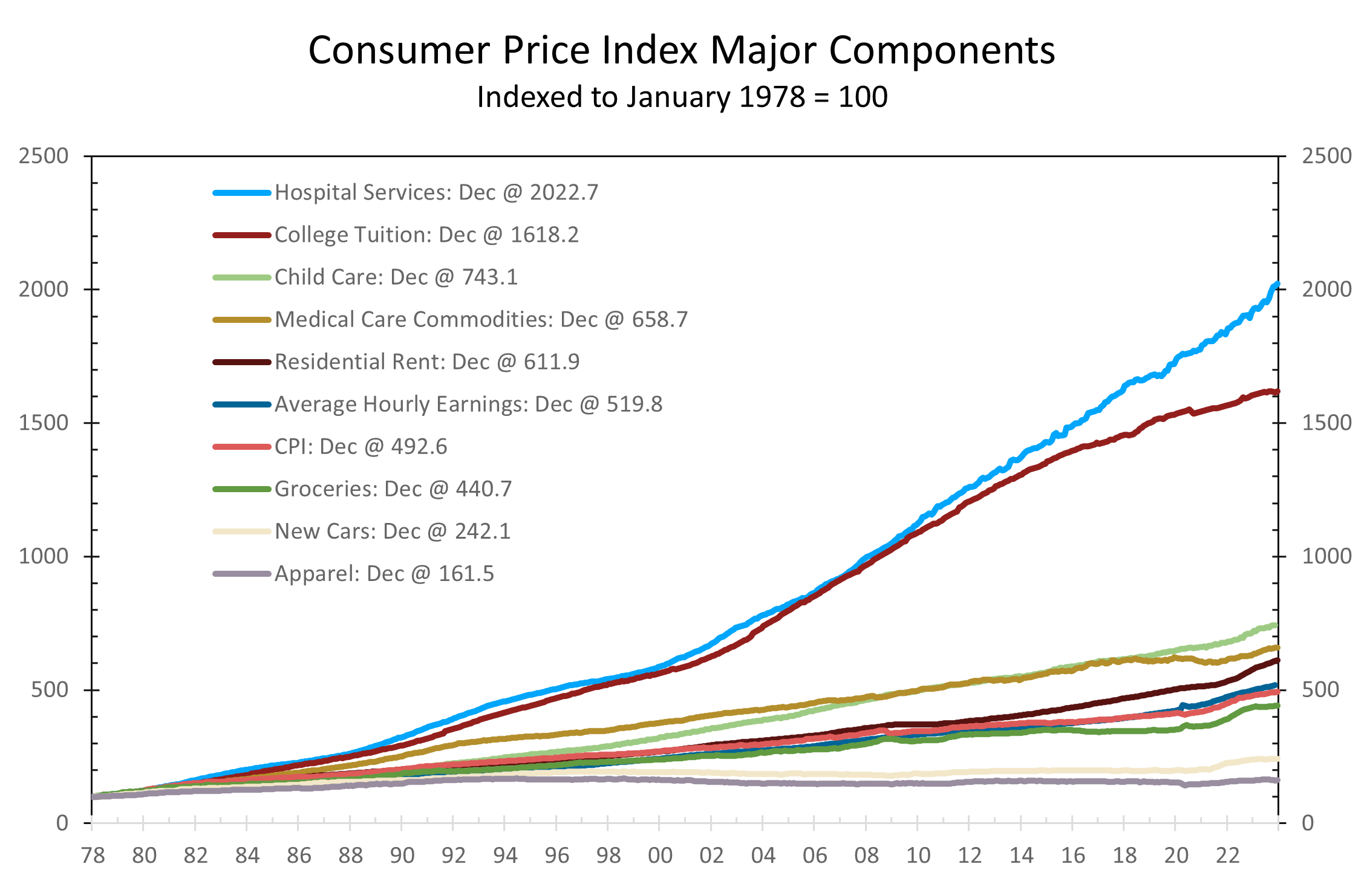

Still other prices remain highly problematic. The cost of motor vehicle insurance has surged 20.6% over the past year. Prices for tickets to sporting events are up 13.5% and prices for hospital services, home health services, nursing homes and day care are all up sharply as well.

Inflation is decelerating more slowly than widely thought, which will push rate cuts further out.

We maintain a cautious view on inflation. Unusually wide pandemic-induced price hikes for key items, such as used cars and apartments, likely distorted seasonal adjustment and understated inflation as prices eased in 2023. The Cleveland Fed’s Median CPI mitigates the impact of these swings. While higher, prices by this measure are still moderating, which should allow the Fed to start cutting the federal funds rate by a quarter point in June, followed by further cuts in September and December — a path is consistent with the 2-Year Treasury, which leads changes in the funds rate.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 13, 2024

mark.vitner@piedmontcrescentcapital.com

Chief Economist (704) 458-4000

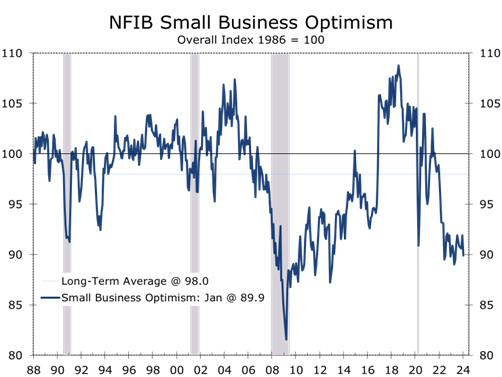

Small Business Owners Remain Cautious

High Operating Costs Squeeze Small Businesses

- The NFIB Small Business Optimism Index declined by 2 points to 89.9 in January, marking the 25th consecutive month it has remained below its 50-year average of 98.

- ix of the 10 components fell in January, while 2 remained unchanged, and 2 rose.

- Sales expectations tumbled 12 points, and now show a net -16% expect sales to increase over the next three months.

- Rising operating costs, including compensation, combined with slowing sales and diminishing pricing power continue to squeeze profit margins.

- Earnings trends also fell 5 points and now show a net -30% believe their earning have improved over the past 3 months.

- While job openings remain historically high and businesses continue to have a hard time filling open positions, fewer firms plan to increase staff over the next 3 months.

- Small businesses continue to get squeezed by higher operating costs, which they are increasingly unable to pass along to their customers. Business owners also remain concerned about higher interest rates and geopolitical uncertainty.

Small business owners remain cautious amidst continuing uncertainties surrounding inflation, interest rates and geopolitics. The NFIB Small Business Optimism Index fell 2 points in January and has now remained below its 50-year average of 98 for 25 consecutive months. Six of the indexes 10 components fell in January, while just 2 increased.

Sales remain lackluster, with a net -11% stating sales had increased over the past 3 months. Expectations for future sales weakened even more, with the proportion of business owners expecting sales to rise over the next 3 months tumbling 12 points to a net -16%, the lowest since May of last year.

With sales under pressure, business owners are paying even closer attention to reducing expenses. Fewer firms are planning to add staff, with the share planning to create new jobs over the next 3 months falling 2 points to 14% and hitting its lowest level since May 2020. Small businesses are also maintaining minimal inventories, even at the risk of losing sales.

Small Businesses are getting squeezed by higher operating costs and are holding off hiring staff.

Given the weakness and sales and persistence of costs pressures, just 8% of small businesses feel now is a good time to expand. When asked why they feel that way, 33% cite weak economic conditions and 10% blame the pollical climate. An additional 7% cite financial conditions and higher interest rates.

The weaker Small Business Optimism report runs somewhat counter to some of the hard data reported for January. Nonfarm employment growth surprised to the upside in January, with employers creating 353,000 net new jobs. Our sense is the NFIB data may be more telling, particularly since January’s weaker NFIB data continue a long running trend. Small business owners are increasingly less likely to add staff, even though job openings remain historically high, and they continue to have a hard time filling many positions.

Weaker hiring plans add some fuel to the notion that January’s job gains were overstated.

Thirty-nine percent of small business owners reported they had a job opening they could not fill, down 1 point from December and the lowest level since January 2021. Open positions are particularly challenging to fill in construction, manufacturing, and non-professional services. Construction job openings declined 11 points in January, but almost half of construction firms have a job opening they cannot fill. Professional services and finance have the fewest openings.

While job openings are inching lower, the proportion of firms struggling to fill them continues to climb, rising 1 point in January to a record 57%. The continuing rise likely stems from the growing number of retirees, particularly in construction and manufacturing.

Weaker sales and higher operating costs continue to squeeze profit margins. Reports of positive profit trends fell 5 points in January to a net -30%, a very weak number. Among owners reporting lower profits, 32 percent attributed it to weaker sales, 15 percent to increased material costs, another 15 percent to seasonal changes, and 11 percent to labor costs.

Weaker sales and higher operating costs continue to squeeze profit margins.

Weaker sales are hindering business owners’ ability to offset higher operating costs. The percentage of firms raising prices in the past 3 months fell 3 points to 22%, the lowest since January 2021, while those raising compensation rose by 3 points to 39% in January. While compensation costs have been sticky, January’s rise was likely bolstered by rising minimum wages in several jurisdictions throughout the country.

January’s weaker NFIB small business confidence report takes some of the shine off January’s spike in nonfarm payrolls and suggests inflation is moderating less than the financial markets have been counting on. We continue to look for three quarter-point cuts in the federal funds rate this year, beginning in June.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 13, 2024

mark.vitner@piedmontcrescentcapital.com

Chief Economist (704) 458-4000

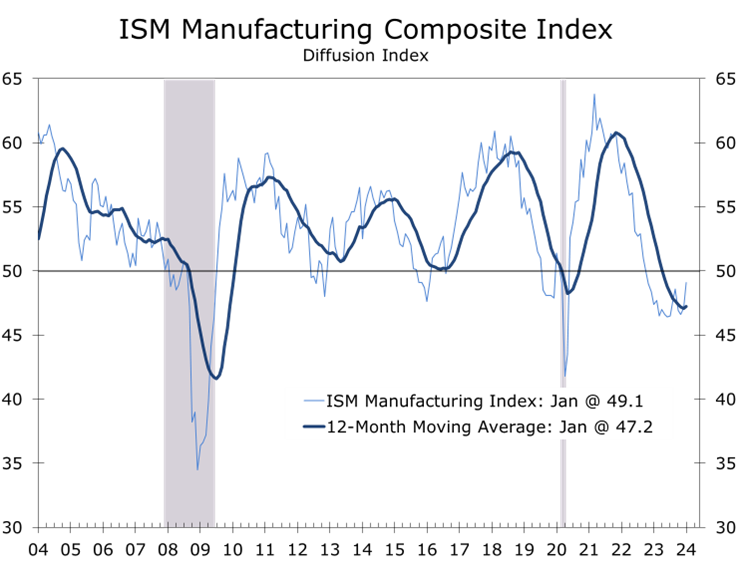

Manufacturing Activity Improves Slightly in January

A Few Green Shoots in the Factory Sector

- The ISM Manufacturing Index rose 2 points to 49.1 in January, exceeding expectations.

- Most regional manufacturing surveys had posted declines in January, including notably sharp declines in surveys by the New York and Dallas Federal Reserve Banks.

- New orders, which are the most leading component of the ISM survey, surged 5.5 points to 52.5.

- Production, which rose 0.5 points to 50.4, also returned above the break-even level.

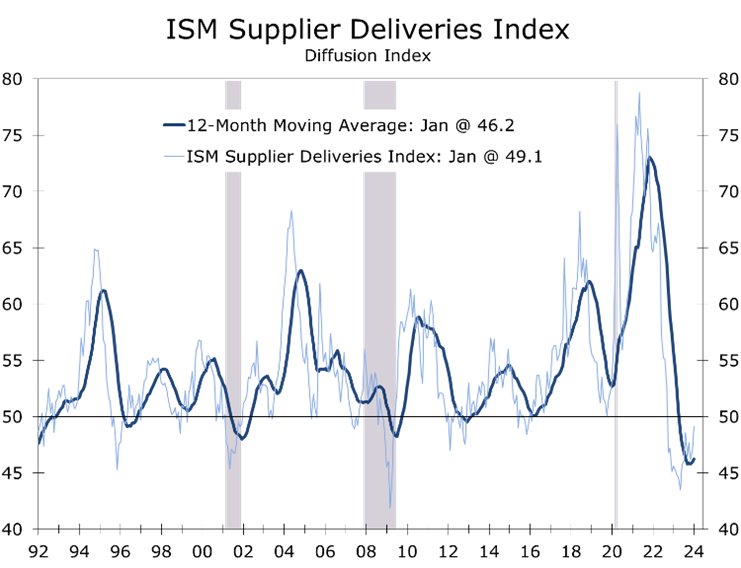

- The supplier deliveries index increased by 2.1 points to 49.1, indicating slower deliveries. While it is likely too soon to see effects from disruptions in the Red Sea, ongoing delays at the Panama Canal may be impacting delivery times.

- The prices-paid index soared 7.7 points to 52.9, likely indicating an end to the easing of raw material prices.

- January’s ISM report exceeded expectations, which had been weighed down by a series of weak regional manufacturing reports. While encouraging, the improvement in the ISM appears to be narrowly based. Manufacturers remain concerned about weak demand for goods and sluggish growth overseas.

The ISM Manufacturing Purchasing Managers’ Index (PMI) exceeded expectations in January, rising 2 points to 49.1, its highest level since October 2022. This follows declines in several regional manufacturing indexes earlier in the month. Despite remaining below the crucial 50-point threshold for the 15th consecutive month, there are signs of improvement, notably a 5.5-point increase in new orders and a 0.5-point rise in production.

The New Orders Index rose to 52.5, marking only the second time it has surpassed 50 in the last 20 months. Three major industrial sectors—Chemical Products, Transportation Equipment, and Fabricated Metals—saw increased orders. This improvement is attributed to strong demand for appetite suppressant medications, recovery from the UAW strike, and growth in industrial construction.

The long slide in manufacturing activity may be ending but a recovery remains uncertain.

The narrow improvement in new orders leaves the timing and extent of recovery uncertain. Only 20.2% of manufacturers noted a rise in new orders, while 23.5% saw a decline. Moreover, exceptionally low customer inventories suggest lower interest rates and less geopolitical uncertainty might quickly lift new orders.

Supplier deliveries rose by 2.1 points to 49.1, reflecting a lengthening in shipping times. Supplier delivery times have been normalizing for some time, even for highly sought after products such as semiconductors. The lead time for production materials increased by 1 day this past month, reaching an average of 83 days. This is still well above 66 days averaged in the year prior to the pandemic but well below the peak of 100 days last reached in July 2022.

Following the wide swings surrounding the pandemic, supply chains are now normalizing.

We believe it is too early to see any impact from delays emanating from attacks on shipping in the Red Sea and the resulting rerouting of traffic. Moreover, the impact from those delays is likely to be greater in Europe than in the U.S.

The Red Sea is not the only trouble spot. Delays in the Panama Canal due to low water levels have been a long running problem that looks likely to persist. Once onshore, however, goods are moving swiftly, with trucking, rail, air, and warehouses all operating with well within historic capacity norms.

With supply chains normalizing, fewer products are in short supply. Long-running shortages of electrical components and electronic components continue. In addition, steel alloy remains in short supply.

The ISM Employment index fell 0.4 points to 47.1, marking the for consecutive month the index has been below 50. Transportation equipment was the only large manufacturing sector where payrolls rose in January. One an overall basis 11% of manufacturers said they added to payrolls, down from 11.7% the prior month. The share of manufacturers reducing payrolls rose 0.4 points to 18.4%.

The moderation in raw materials prices appears to have largely run its course.

The ISM Prices-Paid Index surged 7.7 points to 52.9 in January, ending an 8-month run below 50. Key raw material prices have normalized due to lower energy costs, better supplies, and reduced shipping rates. However, recent energy price increases and higher global shipping rates, triggered by attacks on Red Sea shipping, suggest prices will like firm further.

While January’s ISM data are mixed, they generally support of the Fed’s intention to hold rates steady through late spring or early summer. At 49.1, the ISM index is consistent with 1.9% real GDP growth, which is close to consensus but well below the early projections from the Atlanta Fed’s GDPNow, which are at 4.2%.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Argentina's Warning to the West

Milei Puts the West on Notice

- Argentina's President Javier Milei's speech at the World Economic Forum staunchly defended free-market capitalism and warned against creeping socialism.

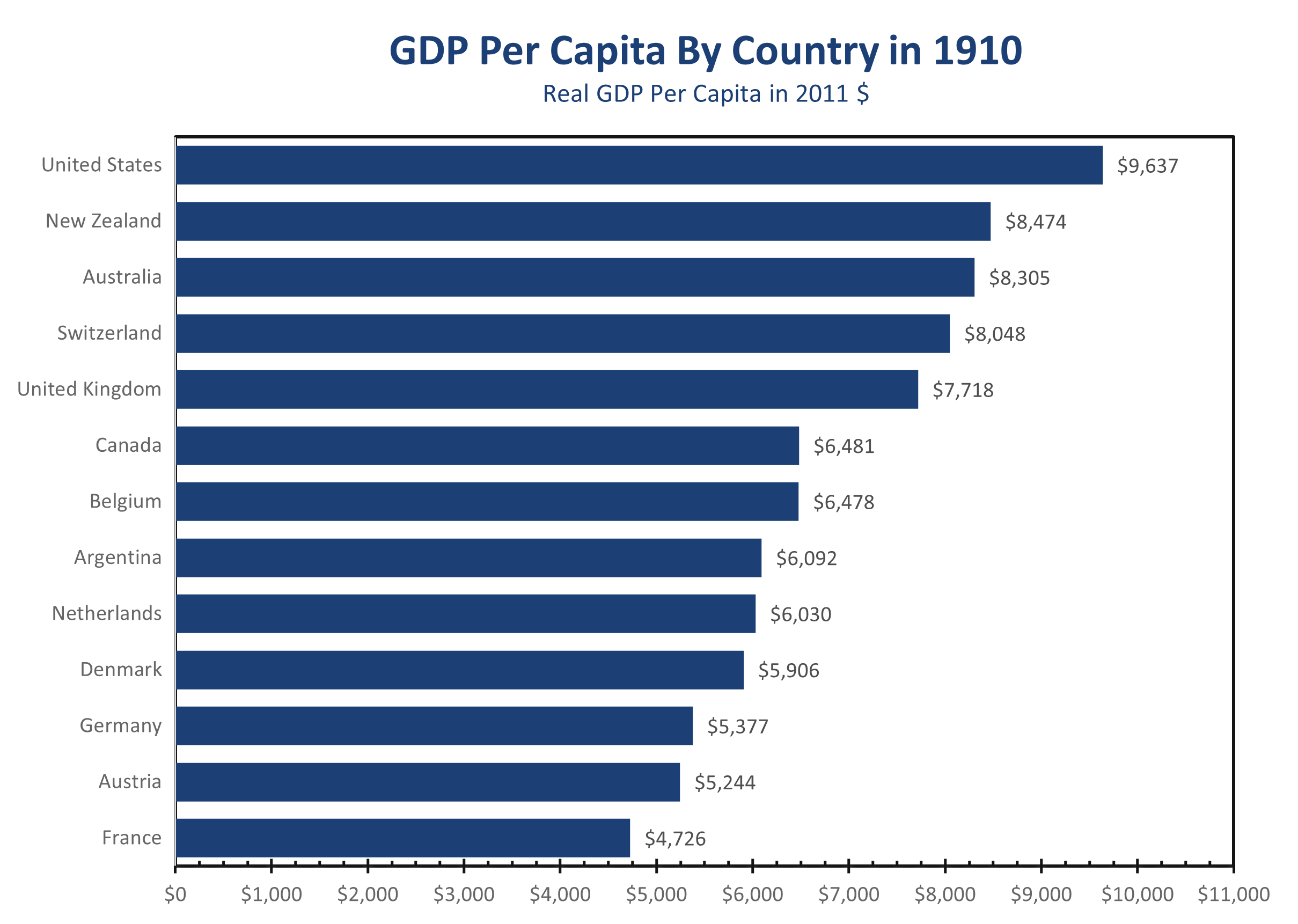

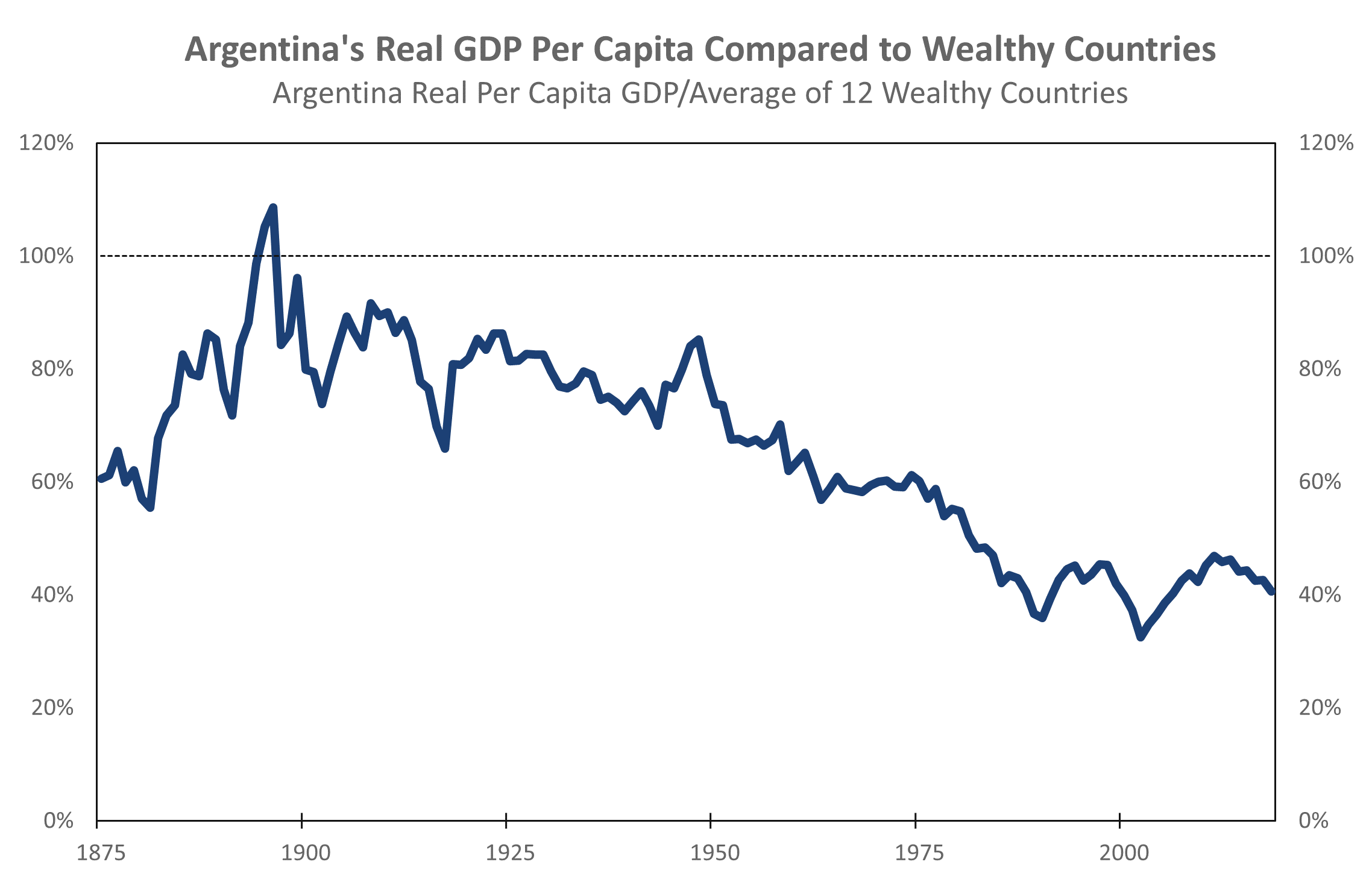

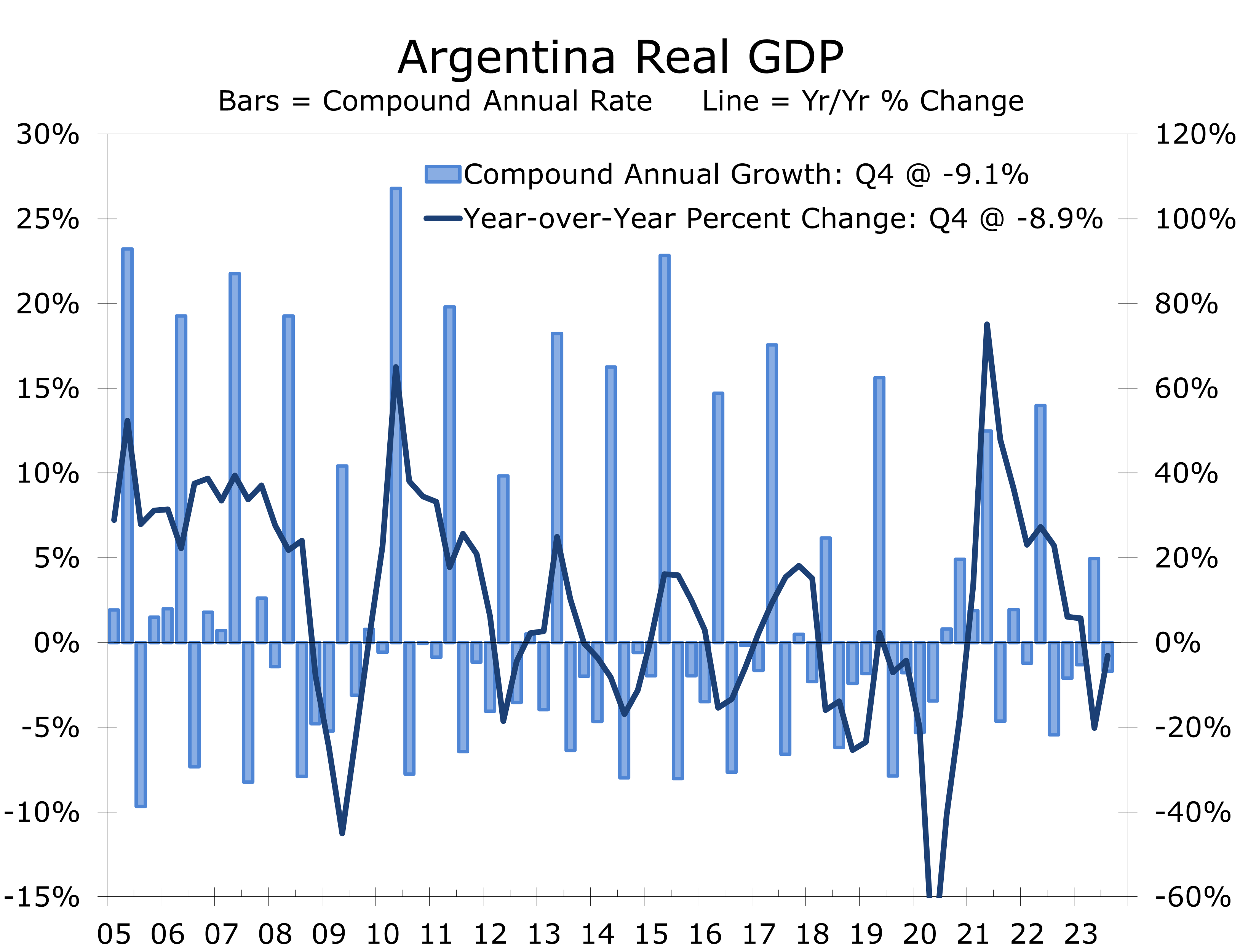

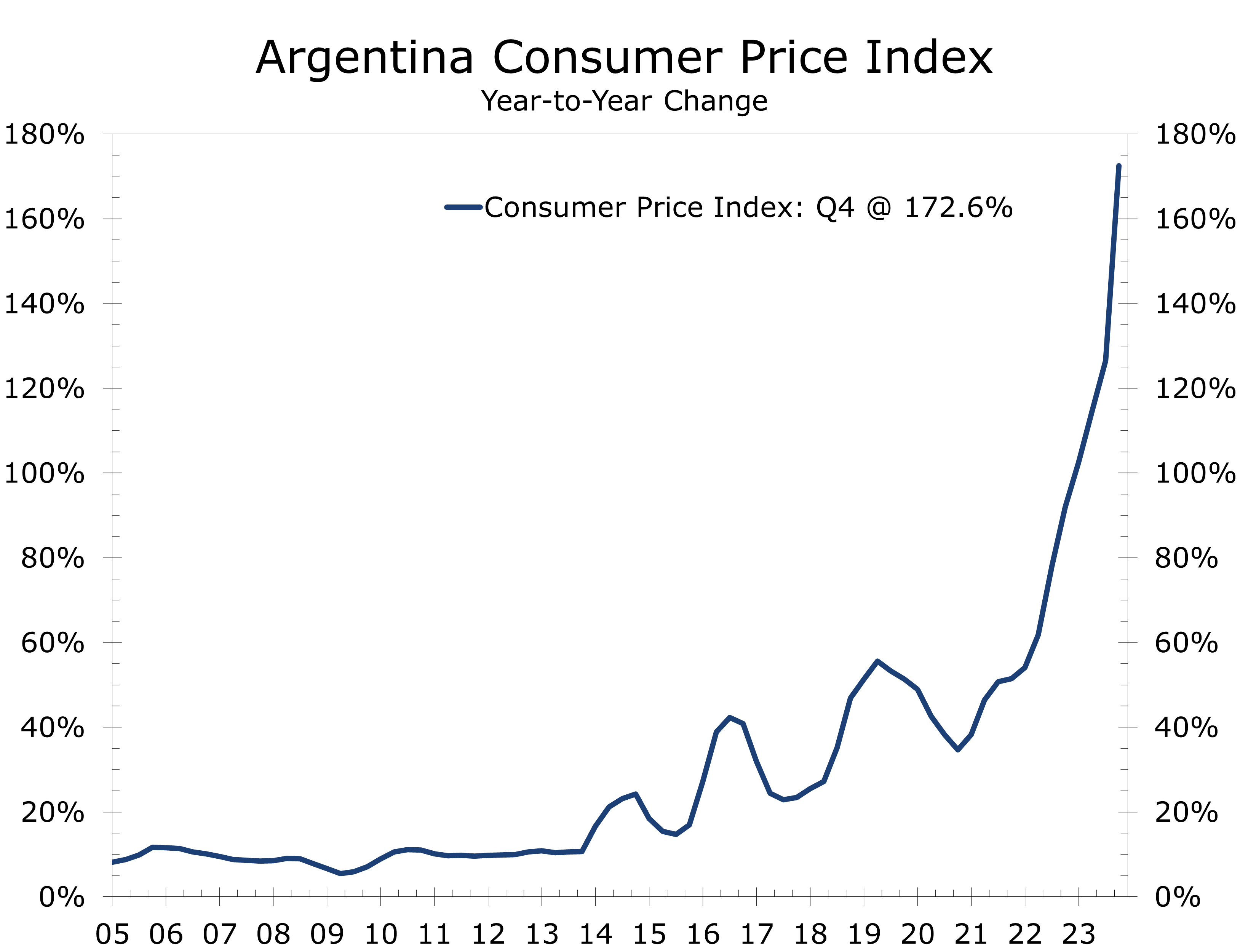

- Argentina has endured a long and arduous slide from one of the world’s wealthiest economies to one of its most troubled.

- Since winning the presidency, Javier Milei, a libertarian economist, has initiated significant reforms, including reducing government ministries, reshaping foreign policy, and issuing Decree 70/2023, which reduces energy and transportation subsidies and does away with rent control.

- The U.S. and the West can learn from Argentina's economic challenges, especially regarding the impact from the persistence of large budget deficits, the pervasive growth of the administrative state, and ever-expanding entitlement commitments.

During this year’s World Economic Forum in Davos, Argentina’s President Javier Milei delivered a notable speech defending free-market capitalism and cautioning against the dangers of creeping socialism. Drawing from Argentina’s decades-long economic challenges, Milei emphasized the detrimental effects of extensive government intervention policies, including income redistribution, price controls, and burdensome regulations, which have led to increasing poverty. He stressed the effectiveness of free-market capitalism in reducing poverty throughout the world and cautioned against moving away from it, foreseeing disastrous consequences.

Researchers often refer to the rise and fall of Argentina as the “Argentine Paradox.” Once one of the wealthiest countries in the world, Argentina experienced a tenuous century of economic decline and political instability. The fall has served as a warning, mostly to Western governments that have run persistent fiscal deficits and have incessantly grown their administrative states. Argentina elected libertarian economist Javier Milei as president, who has vowed to reverse the decline by embracing free market economic principals.

The service sector is the largest in Argentina, contributing to over three-fifths of Argentina’s GDP while manufacturing comprises another fifth. Agriculture is a smaller portion of the Argentine economy, although Argentina is a leading exporter of wheat, soybeans, and beef.