The Red River Rivalry: The ‘Newest’ SEC Tradition

Texas and Oklahoma Meet in Dallas

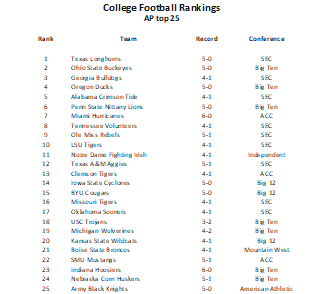

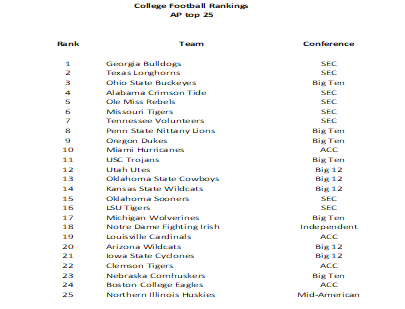

- The college football season is now nearly at the halfway mark and Week 7 brings a number of key clashes, headed by #2nd ranked Ohio State traveling to #3 Oregon.

- Our report focuses on one of college football’s most storied rivalries between the top ranked Texas Longhorns and 18th ranked Oklahoma Sooners.

- Both teams rank among the nation’s winningest programs and have competed for years in the Southwest Conference, Big-12 and now, for the first time, in the SEC.

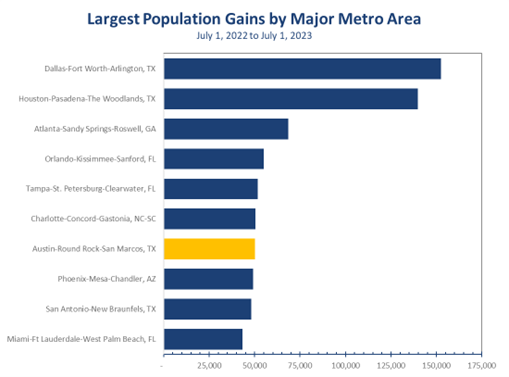

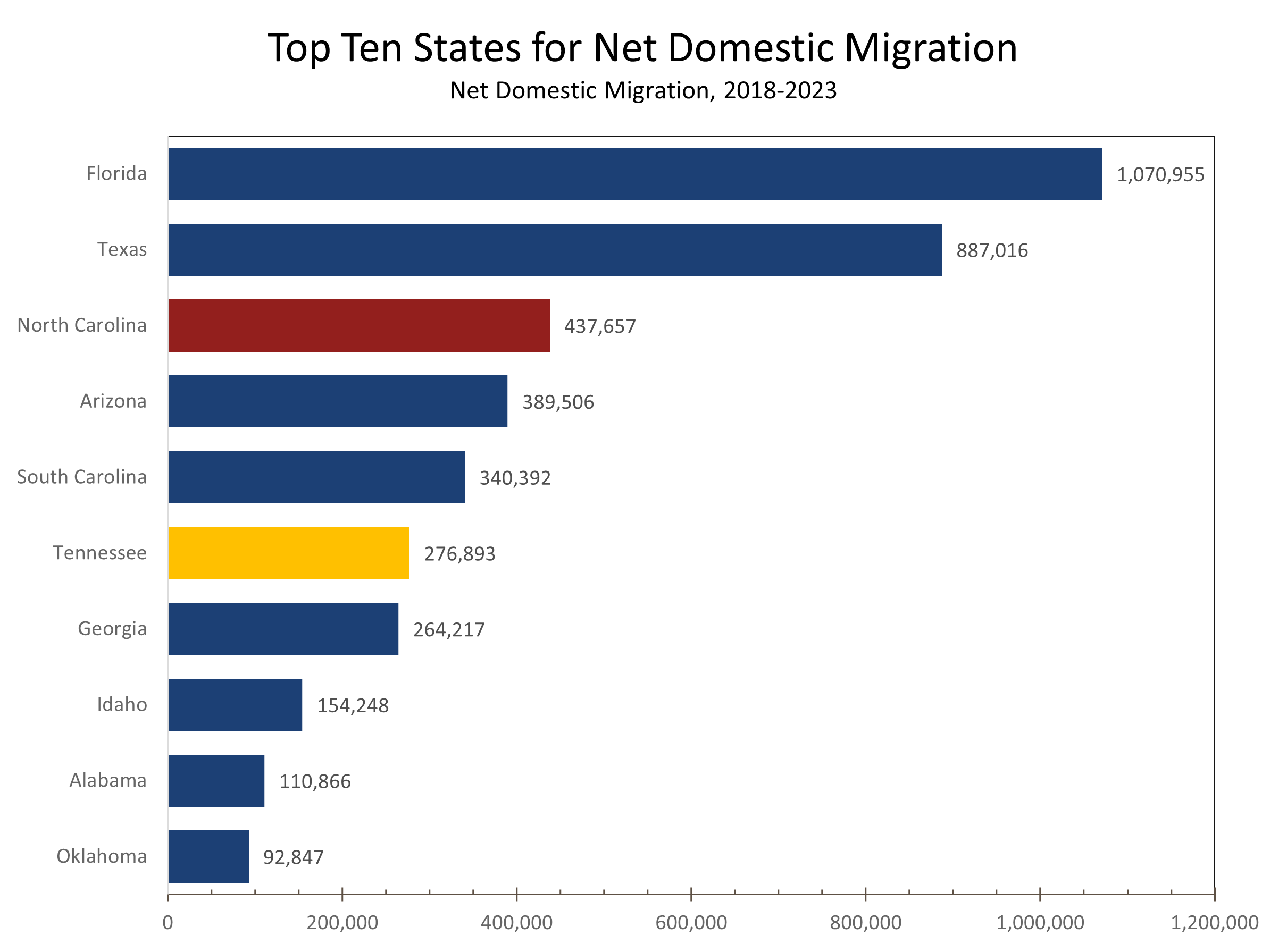

- Texas has been the fastest growing state since the pandemic. Most of the growth is in the Triangle between Dallas-Fort Worth, Houston and Austin and San Antonio.

- Austin has been one of the nation’s fastest growing major metro areas for the past decade and has capitalized on the outflow of tech firms from California.

- Texas is a 15.5-point favorite and comes into the game 5-0 and ranked #1.

- #18 Oklahoma (4-1) has been rebuilding since Lincoln Riley rode off to California.

The first week of October highlighted how conference realignment, Name, Image, and Likeness (NIL), and the transfer portal have forever transformed college football. There are now several competitive teams and fewer doormats. A prime example of this shift was Vanderbilt’s stunning 40-28 victory over Alabama. While the Crimson Tide may have underestimated Vanderbilt, the Commodores dominated the game from the outset, excelling at the line of scrimmage and controlling time of possession. Alabama appeared ill-prepared and undisciplined throughout the contest.

Arkansas also made headlines, scoring a late go-ahead touchdown for a 19-14 victory over then 4th-ranked Tennessee. Other top teams that faltered last week include Michigan, losing 27-17 on the road to Washington, and 11th-ranked Southern California, which fell to Minnesota 24-17, with the Golden Gophers scoring 14 unanswered points in the fourth quarter. Ninth-ranked Missouri was also overwhelmed by 25th-ranked Texas A&M, losing 41-10, propelling the Aggies up 13 spots to 12th in this week’s poll.

As we enter Week 7, we are right in the middle of the season, a crucial time to identify the real contenders. This weekend features a number of key matchups, with the headliner being a showdown between No. 2 Ohio State and No. 3 Oregon in Eugene. This marks the Ducks’ first major test since joining the Big Ten, as they host a perennial powerhouse expected to contend for the National Championship.

Other significant matchups this week include 5th-ranked Penn State traveling to face a Southern California team that is backed up against the wall, and 9th-ranked Ole Miss taking on 13th-ranked LSU.

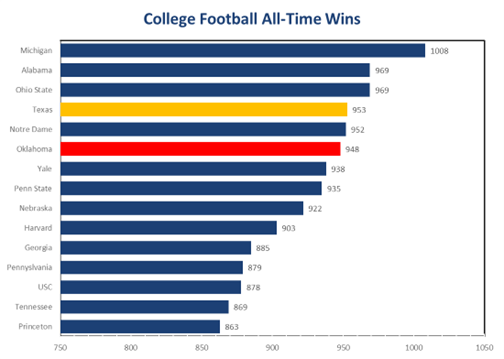

Our report will focus on the Red River Rivalry, featuring top-ranked Texas squaring off against 16th-ranked Oklahoma for the first time as SEC rivals. Both schools rank among the winningest programs of all time.

The Red River Rivalry

The Red River Rivalry is one of college football’s most storied and intense matchups. Held annually at the Cotton Bowl in Dallas, during the Texas State Fair, the game highlights both competition and cultural significance. The rivalry began in 1900, with Texas leading the all-time series 63-51-5. However, Oklahoma has dominated since World War II and has a 17-8 edge since 2000.

Both teams boast rich football traditions, including 7 modern-era National Championships, 4 for Texas and 3 for Oklahoma and 7 Heisman Trophy winners, all at Oklahoma. The neutral site in Dallas fosters an electric atmosphere with fans from both sides. Notable games include Oklahoma’s 55-48 comeback in 2021 and Texas’ 34-30 victory in 2023. This year, Texas (5-0) is ranked #1, while Oklahoma (4-1) comes in at #18.

The University of Texas

The University of Texas at Austin was founded in 1883 after the Texas Constitution of 1876 called for the establishment of a public university. The school opened with one building and 221 students, quickly growing in stature and laying the foundation for what would become a leading higher education institution.

In the early 20th century, UT expanded its academic programs, adding law, engineering, and medicine. By the 1930s, the university’s enrollment surged, surpassing 6,000 students. A landmark moment came in 1937 with the discovery of oil on university-owned land, creating the Permanent University Fund (PUF), which provided significant financial resources for growth and development.

After World War II, the university expanded dramatically. The GI Bill brought veterans to campus, swelling enrollment. The 1950s and 1960s saw the integration of African American students, with Heman Sweatt becoming the first Black student admitted to UT’s law school after the landmark Supreme Court ruling in Sweatt v. Painter (1950). UT’s reputation grew in research, particularly in fields like engineering and business, earning it national recognition.

In the 21st century, UT Austin has continued to grow in size and influence. In fall 2024, the university reached a record-breaking enrollment of 53,864 students, reflecting its continued appeal as a leading institution in higher education. UT became a member of the prestigious Association of American Universities (AAU), cementing its status as a top research institution. The university has also made significant strides in diversifying its student body and expanding its global impact.

UT Austin boasts a distinguished alumni network, including Michael Dell, founder of Dell Technologies; Rex Tillerson, former U.S. Secretary of State and ExxonMobil CEO; Matthew McConaughey, Academy Award-winning actor; Lady Bird Johnson, former First Lady of the U.S.; Neil deGrasse Tyson, renowned astrophysicist; and Walter Cronkite, legendary broadcast journalist.

Today, UT consistently ranks among the top public universities in the U.S., with particularly strong programs in engineering, business, law, and computer science. In 2024, UT Austin ranked 10th among U.S. public universities, with the McCombs School of Business and Cockrell School of Engineering being particularly well-regarded.

The university’s athletic program, particularly the Longhorns football team, is deeply embedded in the state’s identity. The Texas Longhorns began playing football in 1893 and has since become one of the most successful programs in college football history. The Longhorns have won four national championships (most recently in 2005 under coach Mack Brown) and 32 conference titles. Known for their iconic burnt orange uniforms and passionate fan base, the Longhorns have produced numerous All-Americans and NFL stars. The Long Horns have helped establish the UT brand and that success has extended to other areas of the University, including leading edge research, impact on public policy in Texas and around the world, and a passionate alumni base.

Austin

The Austin metropolitan area continues to experience rapid growth and has established itself as one of the most dynamic economies in the United States. Often referred to as “Silicon Hills,” due to its location in the Texas Hill Country, Austin has become a major technology hub, with global companies such as Dell, Apple, Tesla, Google, Meta, and Oracle expanding their operations in the region. Significant investments, including the Tesla Gigafactory and Samsung’s new semiconductor plant, have further solidified the city’s reputation as a tech powerhouse. In addition to technology, education and research play a vital role in Austin’s economy, with the University of Texas helping drive innovation in engineering, computer science, and business. This academic influence helps fuel Austin’s high-tech industry and contributes to a highly educated workforce.

While Austin is primarily known for its tech sector, the region’s economy is continuously broadening. Companies such as Whole Foods, YETI, and Dimensional Fund Advisors are based in Austin. The opening of the Dell Medical School in 2015 catalyzed the development of Austin’s growing biotech and pharmaceutical sectors, further diversifying the local economy. As a result, Austin has evolved into a hub for health care and life sciences.

Known as the “Live Music Capital of the World,” the city attracts global visitors through events like South by Southwest (SXSW) and Austin City Limits, which generate substantial revenue for the hospitality industry. Meanwhile, the surrounding cities of Pflugerville, Georgetown, and Cedar Park have also experienced rapid growth as rising housing costs and increased congestion in Austin push people outward. Suburbs like San Marcos, home to Texas State University, also now among the fastest-growing cities in the nation.

With a metropolitan population of approximately 2.4 million and the city of Austin’s population nearing 1 million, the region boasts a highly educated workforce, with nearly 50% of residents holding at least a bachelor’s degree. The local labor market remains robust, driven by the tech, healthcare, and professional services sectors. However, as Austin continues to expand, it faces challenges such as rising housing costs and increased traffic congestion. Housing affordability is a significant issue, with home prices and rents steadily climbing due to demand outpacing supply. Infrastructure upgrades, including improvements to Austin-Bergstrom International Airport and public transportation, are crucial to managing the region’s growing population and economic activity.

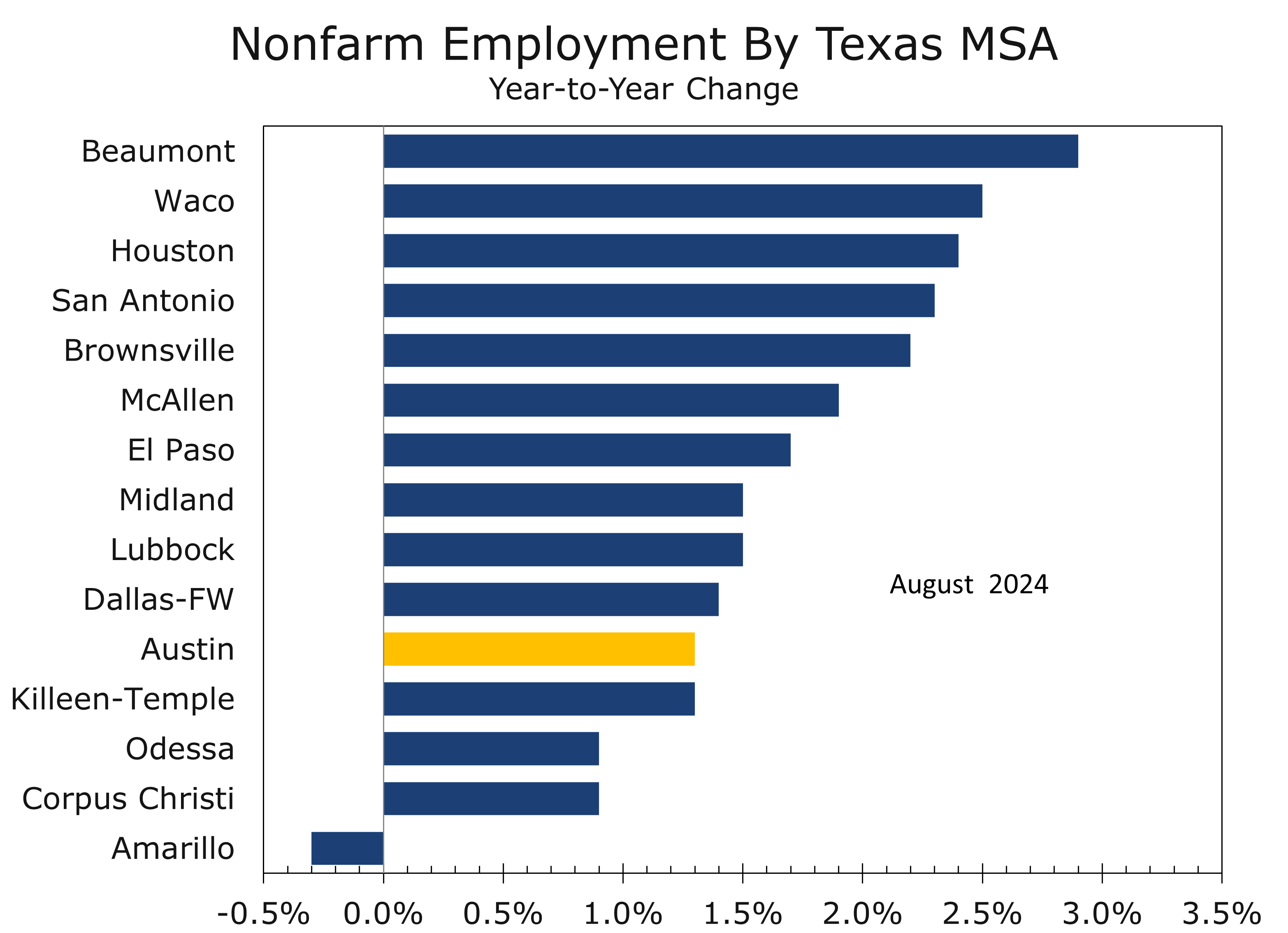

Population and employment growth has moderated in the past year, with nonfarm employment has slowed to just 1.3%. The slower pace has allowed rents and home prices, which had soared, to ease slightly. Austin remains a top destination for young professionals, despite losing its #1 status. Balancing rapid development while preserving the high quality of life that initially attracted residents is a key challenge for city planners, public officials and business leaders alike.

The University of Oklahoma

The University of Oklahoma (OU), founded in 1890 in Norman before Oklahoma became a state, began classes in 1892 with 119 students. Despite a fire that destroyed its main building in 1903, OU quickly rebuilt and expanded, demonstrating early resilience.

In the early 20th century, OU grew in size and academic stature. Under President William Bennett Bizzell in the 1920s and 1930s, the university bolstered its research focus and developed nationally recognized programs. New facilities built during this era helped solidify OU as a key regional academic institution.

After World War II, the GI Bill spurred a surge in enrollment. The university’s development continued under subsequent presidents, notably George Lynn Cross, who expanded graduate education and research. OU’s meteorology program, established in the 1960s, positioned the university at the forefront of severe weather research.

OU’s athletic prominence, particularly in football, began under coach Bud Wilkinson in the 1940s and 1950s, establishing a tradition of athletic excellence that continues today. OU has won three National Championships (1975, 1985, 2000) in the modern era and seven Heisman Trophy winners, the most recent of which are Kyler Murray (2018) and Baker Mayfield (2017).

Notable alumni include former U.S. House Speaker Carl Albert, broadcaster Jim Lehrer, astronaut Fred Haise (Apollo 13), NFL coach Barry Switzer, and actor James Garner.

Academically, OU is known for its strengths in meteorology, energy management, law, and aerospace engineering. Home to the National Weather Center, OU is a leader in meteorological research and is consistently ranked among top public research institutions, particularly for its contributions to STEM and public policy.

Today, with over 30,000 students, the University of Oklahoma is a major educational hub, balancing academic excellence with a storied athletics tradition and a strong alumni network.

Norman

Norman, Oklahoma, located about 20 miles south of Oklahoma City, was founded in 1889 during the Land Run, when settlers staked claims in the newly opened Unassigned Lands. Named after Abner Norman, a surveyor for the federal government, the city quickly grew as part of the early settlement boom in the Oklahoma Territory. Norman became home to the University of Oklahoma in 1890, a decision that significantly shaped the city’s future.

Throughout the 20th century, Norman expanded its economy beyond agriculture, driven largely by the growth of the university and its research programs. The city also played a key role in World War II, hosting the Naval Air Technical Training Center, which contributed to local economic growth and infrastructure development.

Today, Norman is the third-largest city in Oklahoma, with a population of around 130,000. It remains closely tied to the University of Oklahoma, which is a major economic driver and a central cultural institution. Norman has also developed a growing technology sector, while maintaining a reputation as a vibrant college town with a strong sense of community.

Looking Ahead to the Game

The Texas-Oklahoma matchup is always one of the most anticipated games of the year. Oklahoma has dominated the rivalry recently, winning four of the last five meetings, even when coming in as the lower-ranked team. Key to an Oklahoma upset will be special teams, red zone efficiency, and perhaps some well-timed trick plays. Oklahoma’s defense also has to show up big time. Not only must the Sooners contain quarterback Quinn Ewers and avoid big plays, but they must also get some three-and-outs and keep their offense on the field as much as possible.

Vanderbilt’s victory over Alabama provides a possible roadmap for Oklahoma. If you hold onto the ball for 42 minutes, then your opponent will have to execute nearly perfectly in the 18 minutes you allot them. That will be a tall order for Oklahoma but is what they will likely need to do to win.

For Texas, this is another opportunity to solidify their national title credentials ahead of a major test against Georgia next week. The Longhorns have been scoring lots of points and has not lost a step as Arch Manning subbed for injured Quinn Ewers the past few weeks. While focused on the Sooners, Texas knows they can’t afford any weaknesses being exposed in this classic rivalry. They also cannot let Oklahoma hang around, as they have in previous years because the Sooners have a way of coming back.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

A View from the Piedmont – Something Seems Off with Goldilocks

Markets Wrestle with Inconsistencies

- Many were quick to label September’s jobs report as a return to a Goldilocks. We feel this complacency is misplaced.

- While stronger growth helps alleviate fears the labor market had cooled off too much, the composition of job gains remains skewed toward just a handful of industries.

- Hours worked also weakened in September despite the big jump in payrolls.

- Last week’s other economic reports were mixed, with the ISM manufacturing data remaining weak and ISM services data showing surprising strength.

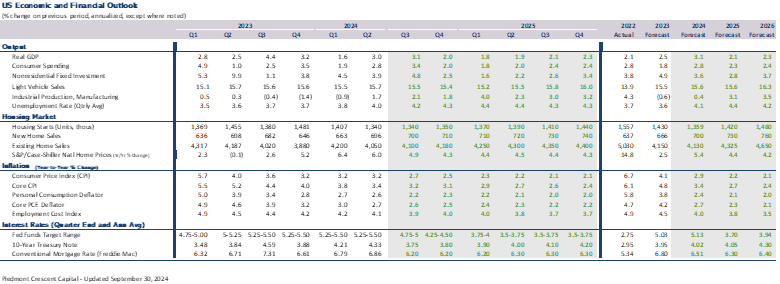

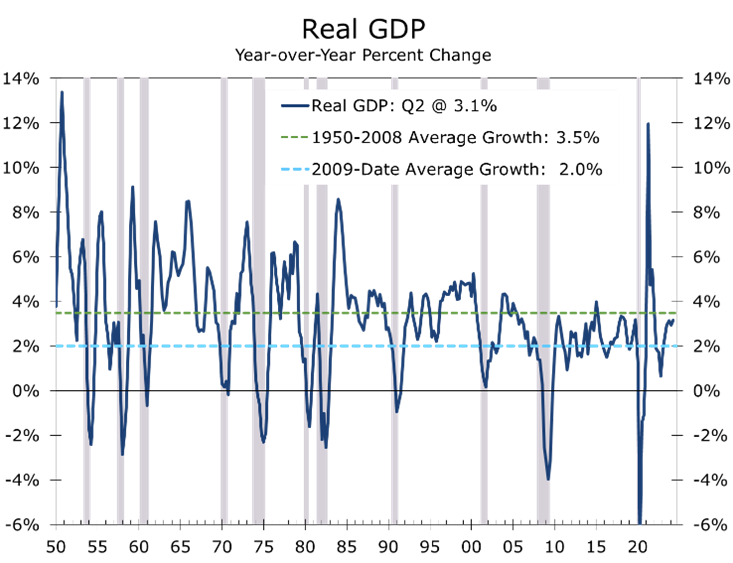

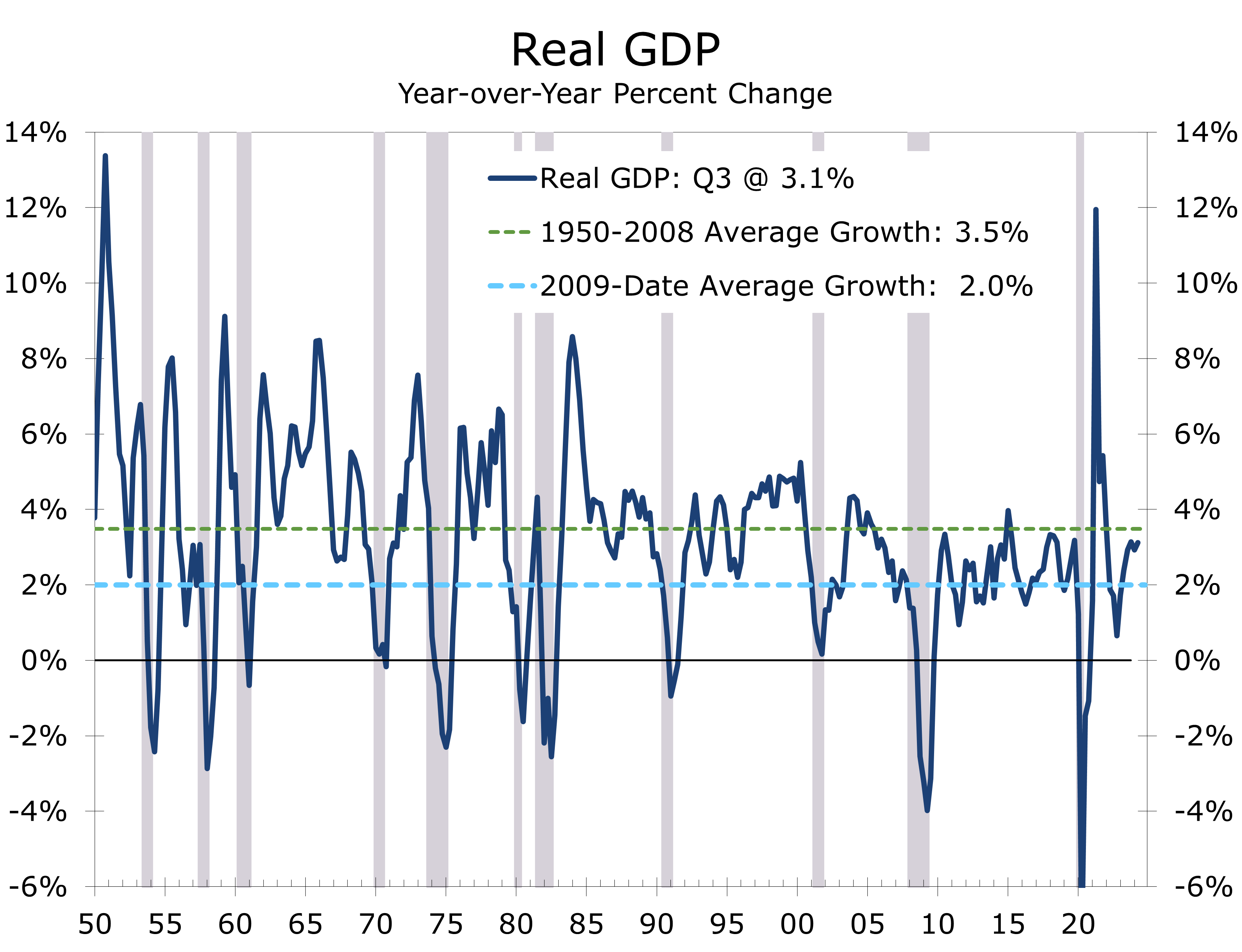

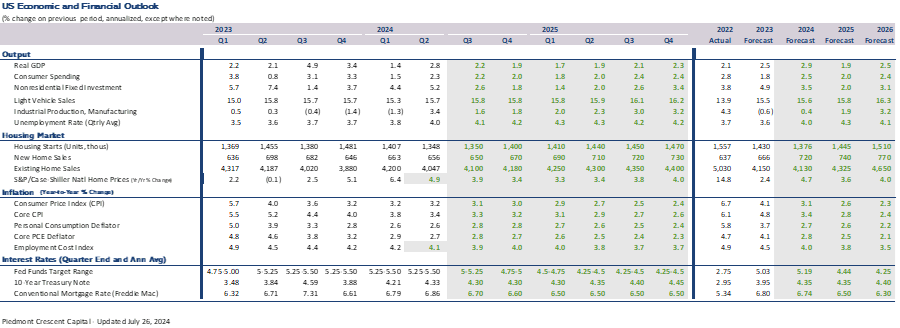

- We see third quarter real GDP rising at a 3.1% annual rate.

- The suspension of the dockworkers’ strike comes at a huge cost. Dockworkers are set to receive a 62.5% over the next five years. That ‘settlement’ is already spurring demands for larger wage gains elsewhere.

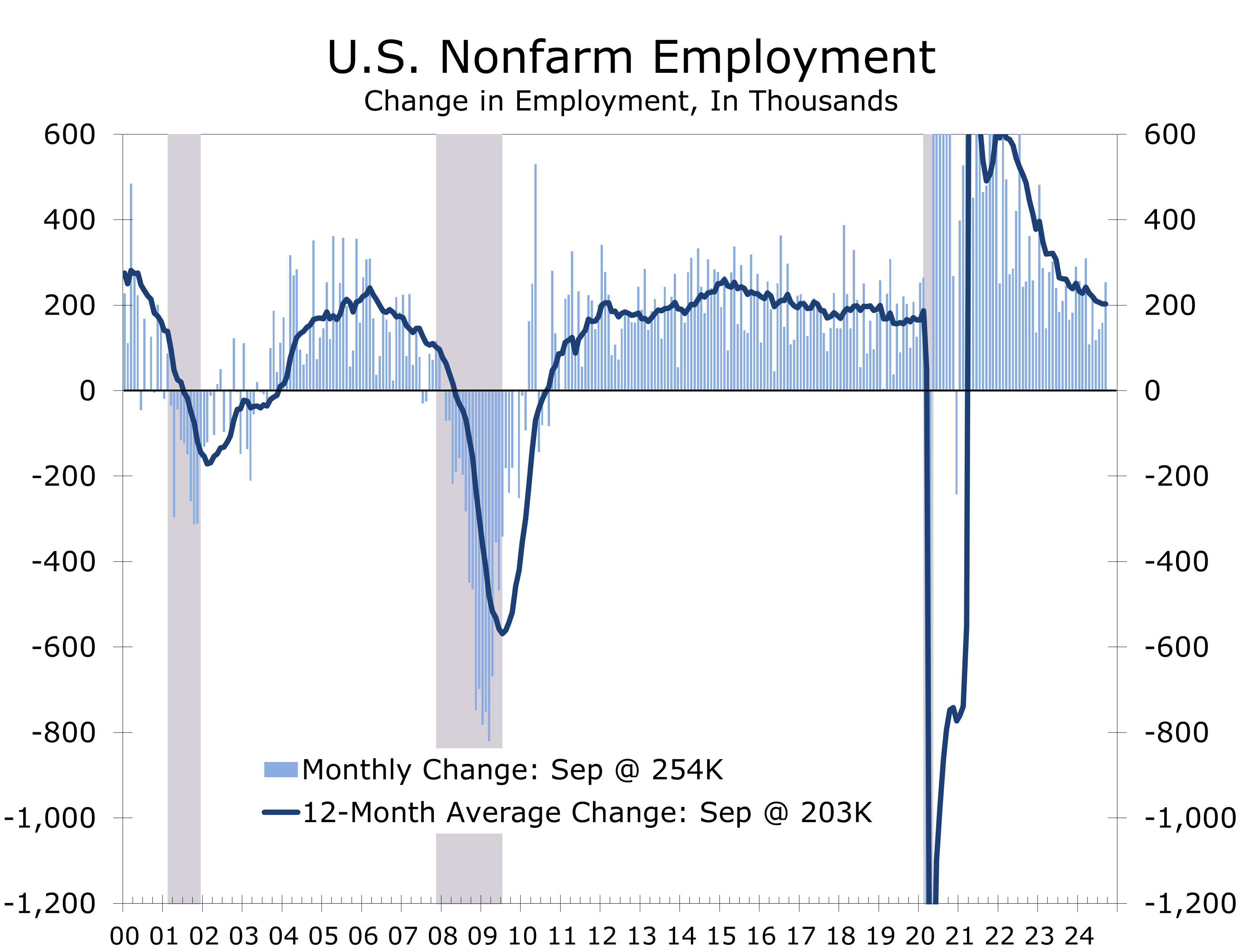

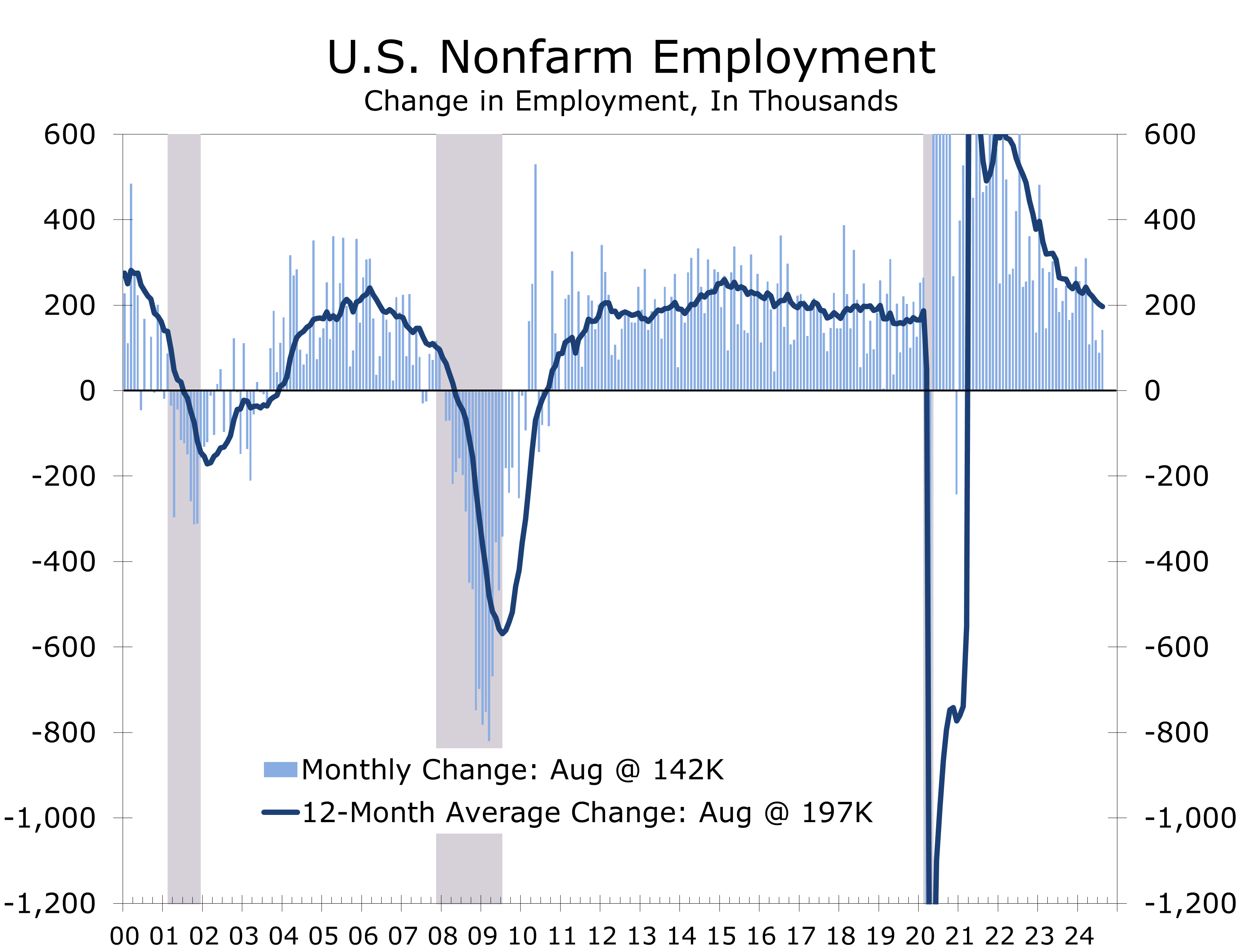

The markets were relieved to learn that the labor market was not nearly as weak as the July and August employment data had indicated. Employers added 254,000 jobs in September, and job growth for July and August was revised modestly higher. Suddenly, the economy does not look as vulnerable as it did when the Fed opted to kick off its easing cycle with a half-percentage-point cut in the federal funds rate.

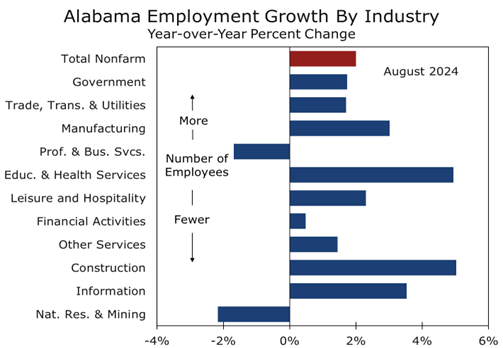

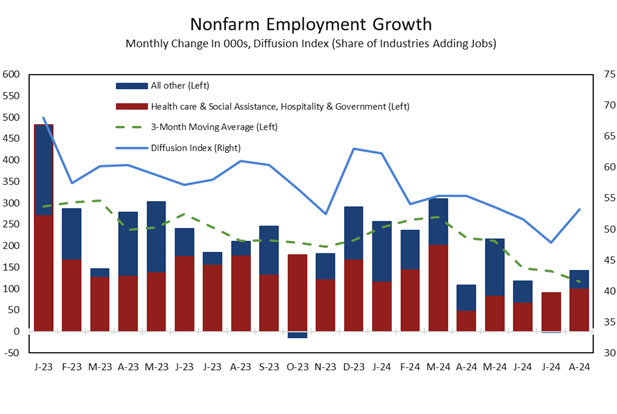

The September jobs data are encouraging. Not only did job growth ramp up, but gains were more widespread, with the diffusion index rising to 57.6, the highest since January. While more industries added workers, the bulk of job gains continued to come from just four sectors: leisure & hospitality, health care, government, and construction.

The Household Survey was also quite strong, with employment rising by 430,000, significantly outpacing the 150,000-person increase in the labor force. As a result, the unemployment rate fell from 4.22% to 4.05%. Wages remain under pressure, with average hourly earnings rising by 0.4% to $35.36, marking a 4% year-over-year increase—higher than the Fed’s target amid ongoing strike activity.

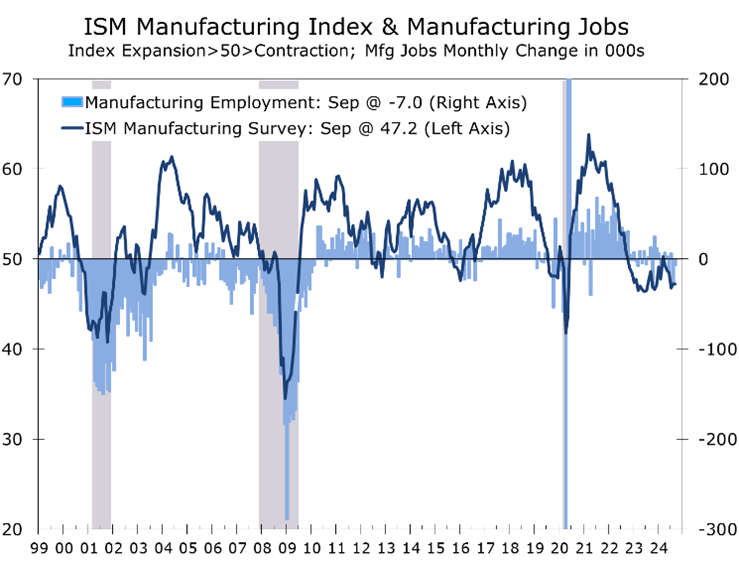

While overall employment conditions improved, manufacturing continues to struggle, with payrolls declining over the past two months and 40,000 jobs lost this year. The Boeing strike, which began in September, will impact October’s data. Weak demand for goods reflects the impact of higher interest rates. The ISM manufacturing index was unchanged at 47.2 in September and has remained below the 50 break-even level for 22 of the last 23 months, signaling ongoing contraction. While the employment index fell, production and new orders rose slightly, though all remained below 50. Manufacturing job losses align with the ISM index on a historical basis.

On a more positive note, the ISM services survey, which includes construction, rose 3.4 points to 54.9. The composition was mixed, the business activity (+6.6 points to 59.9) and new orders (+6.4 points to 59.4) components both increased strongly, driving the overall index higher. The employment component declined by 2.1 points to 48.1, signaling some softness in labor markets for the service sector, which is evident. The prices paid index moved higher, up 2.1 points to 59.4, indicating some inflationary pressures.

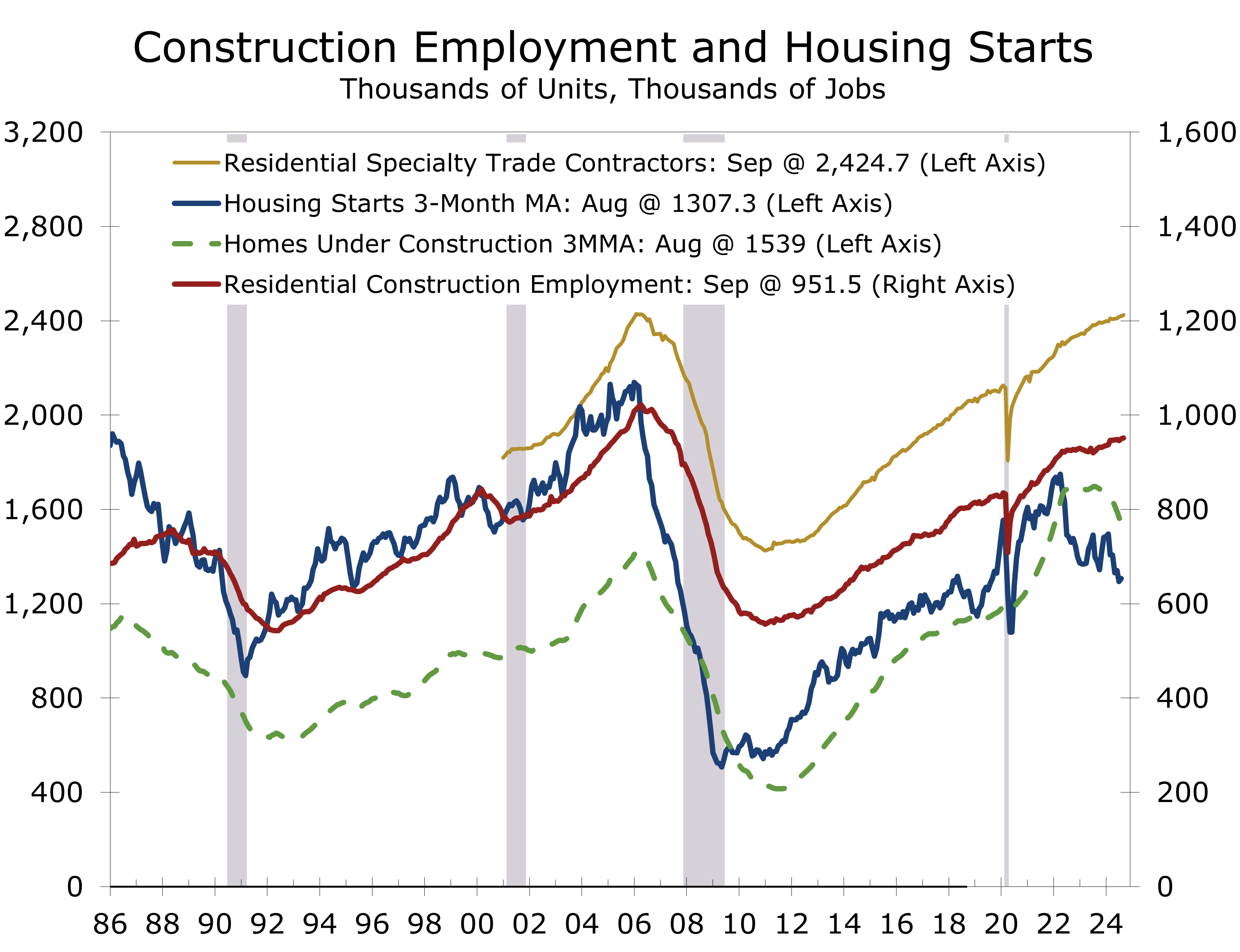

Construction has been a source of strength recently, benefitting from both residential and nonresidential construction. While housing starts have weakened of late, particularly new apartment projects, there is still a great deal of work in the pipeline. Nonresidential continues to benefit from major fiscal initiatives including construction of EV assembly and parts plants, microchip plants and infrastructure improvements. Here too, new projects are slowing but there remains a considerable pipeline of projects underway.

One reason construction employment has held up so well is that there has been an abundance of open positions and hiring has slowed in other industries. Immigration has also helped, with a large number of recent immigrants receiving temporary work permits. This has been particularly helpful in many of the trades, including framing, painting and landscaping.

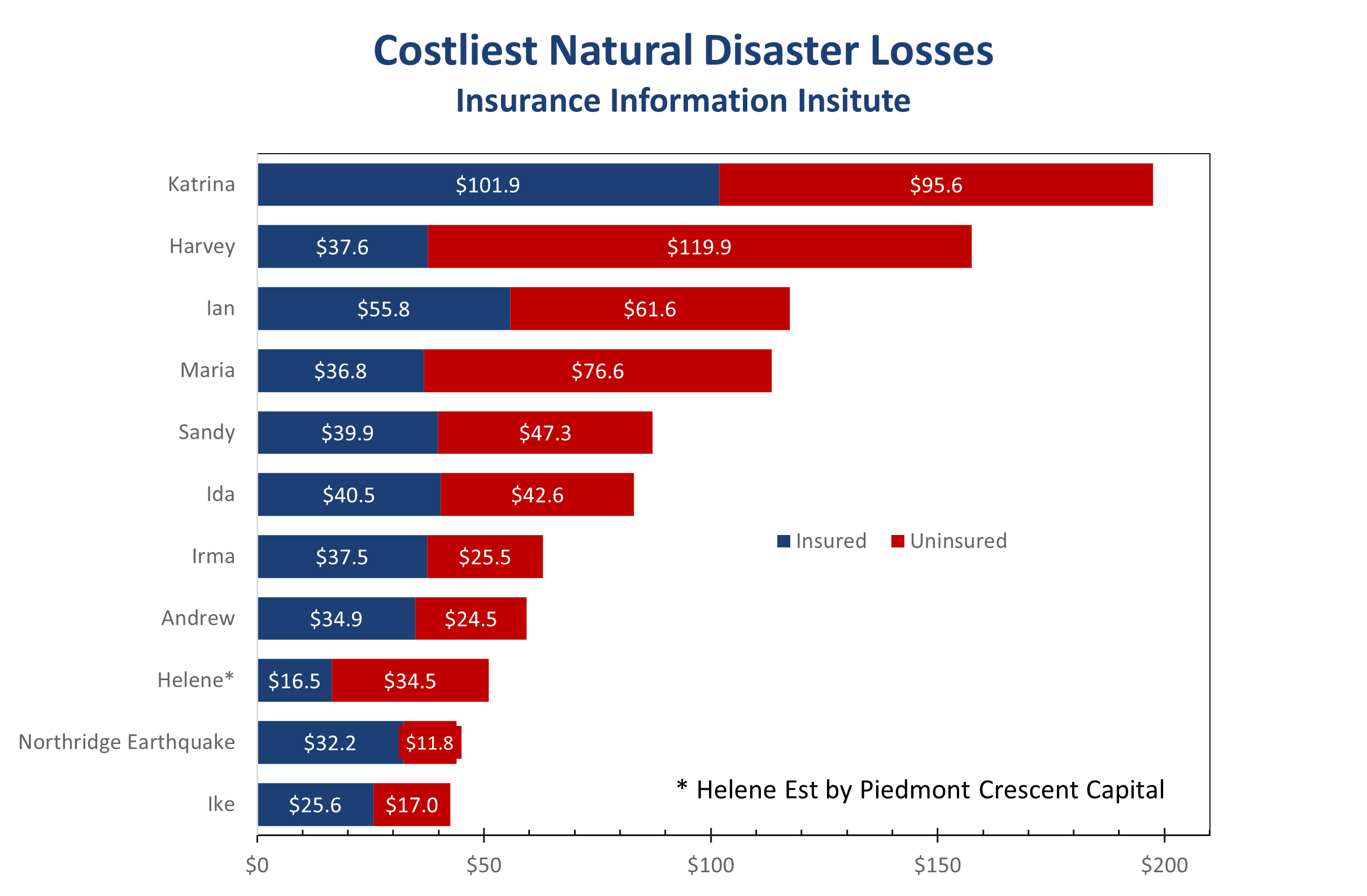

The latest estimates put losses from Hurricane Helene at 230 fatalities and approximately $41 billion in property damage, much of it from uninsured flood damage. The storm impacted Florida’s Big Bend, swept across Georgia from the southwest to the northeast, and hit the western Carolinas, eastern Tennessee, and southwest Virginia.

The greater Asheville area, up to the Tennessee border, was hardest hit by flooding and is expected to face prolonged economic disruption. October is the peak of the tourist season, as visitors flock to see the changing leaves. We estimate that Helene-related closures could reduce October nonfarm payrolls by around 50,000 jobs, primarily in leisure and hospitality, as well as professional services. Construction may see a modest uptick due to cleanup efforts.

Flood damage is difficult to assess, and early estimates are likely conservative. We estimate insured losses at approximately $16.5 billion, mostly from wind, with uninsured losses more than doubling that, reaching $34.5 billion. Recovery from the storm is expected to be slow, particularly in areas hardest hit by flooding.

In the longer term, we expect migration out of the affected areas, as rebuilding efforts will require stricter standards, potentially pricing out many residents. As housing becomes even less affordable, many residents are likely to resettle in major metro areas in the region, particularly Charlotte, Greenville, and Winston-Salem.

October also marks the one-year anniversary of the war between Hamas, Iranian proxies, and Israel. The surprise attack on October 7 caught Israel off guard and marked one of the largest intelligence and operational failures in its history. Not only was Israel dealing with the largest loss of Jewish life since the Holocaust, but ordinary Israelis were concerned about the survival of the Jewish state.

Israel has come a long way over the past year. Its victory over Hamas has defied expectations from virtually all Western governments, particularly the U.S. The recent pivot to targeting Hezbollah has been nothing short of spectacular, resulting in the elimination of much of Hezbollah’s leadership and enabling Israel to make significant gains against its rank-and-file forces while resulting in minimal civilian and Israeli casualties.

Will Israel choose to send a message to the snake or opt to cut off the head of the snake?

Today, it is Iran’s leadership that is concerned about its survival, actively sending messages to other nations to rein Israel in. The question now is how and when Israel will respond to the 180-missile barrage Iran launched at Israel on October 1. There is widespread speculation that Israel will target Iran’s oil production and distribution facilities or possibly their nuclear sites. Israel’s leadership remains tight-lipped.

The critical question for Israel is whether to send a message, as it did in April, and potentially scare off the snake, or to go straight for the head. If they choose the former and fail, Iran will likely push more aggressively to develop nuclear weapons. If they choose the latter, they must succeed, as failure could undo much of what Israel has accomplished so far.

We expect Israel to continue pushing hard into Lebanon and Gaza as the U.S. moves closer to the presidential election. We would be surprised if Israel tipped its hand before acting, given the remarkable success of their surprise beeper and walkie-talkie attacks against Hezbollah, as well as their more direct efforts to eliminate the leaders of Hezbollah and Hamas.

Our final thought this week circles back to where we began. There seems to be growing complacency around the belief that the Federal Reserve has successfully engineered a soft landing, with diminished risks of inflation and a slowdown in job growth or the broader economy. We do not share this view.

Moreover, we are concerned about the inconsistency in both the Fed’s and consensus forecasts, which call for another 150 basis points of cuts in the federal funds rate, while predicting strong economic growth and low unemployment. If growth is that strong, the Fed wouldn’t need to cut rates.

While third-quarter growth is likely to come in around 3%, we expect fourth-quarter growth to slow to less than 2%, as businesses and consumers pull back ahead of the presidential election and the hurricanes cut spending. Additionally, we believe the risk of inflation remaining above the Fed’s target is higher than what the market has priced in. The suspension of the dockworkers’ strike, while a relief, comes at a cost—labor unions are now emboldened, making a resolution to the Boeing strike more difficult.

Our forecast calls for economic growth to slow to just under a 2% pace over the next three quarters. This slowdown should allow the Fed to continue cutting the funds rate down to 3.50%. However, with unemployment remaining low, we expect the yield curve to steepen, making it harder for lower short-term rates to effectively boost economic growth.

The election looks too close to call, but the Harris campaign seems to be steadily losing momentum. A divided government remains the best result from the market’s perspective and still appears to be the most likely outcome. A sweep by either party raises the risk of even larger federal deficits.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

College Football Kicks Off October With A Wave of Surprises

October Surprises – Let the Chaos Begin

- October began with 4 major upsets among top 11 teams, including Vanderbilt’s shocking 40-28 victory of #1-ranked Alabama.

- Miami, Texas A&M, Indiana along with Army and Navy are some of this season’s early surprises.

- Our focus this week is on the Mississippi-South Carolina game, which turned out to be a much more lopsided affair.

- Ole Miss began the season with high hopes but stumbled at home against a very good Kentucky team.

- South Carolina beat Kentucky earlier this year but has struggled since essentially giving away what would have been a signature victory against LSU.

- South Carolina’s economy continues to transition toward higher value-added manufacturing and R&D.

- Mississippi’s economy has also made great strides at attracting high-wage industry.

October kicked off with one of the wildest weekends in recent memory. Week 6 saw unranked teams upset four of the top 11 teams in the AP Poll, a phenomenon not seen since November 2016.

Vanderbilt’s victory over Alabama earned top billing. The Commodores controlled the game from the start, dominating time of possession and limiting Alabama’s explosive offense, ultimately winning 40-28. This upset comes just weeks after former Alabama coach Nick Saban remarked that Vanderbilt was one of the safest places to play on the road, often filled with Alabama fans. The win marked Vanderbilt’s first-ever triumph over a top-ranked team, leading to a rush onto the field and the tearing down of the goalposts, which were later paraded down Broadway in Nashville.

Week 6 thrusts the college football hierarchy into chaos, with 4 of the AP top 11 teams losing.

The chaos continued beyond Nashville as Arkansas, which has been in a constant state of rebuilding, contained 4th-ranked Tennessee’s high-powered offense and scored a late go-ahead touchdown for a 19-14 victory. Tenth-ranked Michigan lost 27-17 on the road to Washington, while 11th-ranked Southern California fell to Minnesota 24-17, with the Golden Gophers scoring 14 unanswered fourth quarter points. Ninth-ranked Missouri was also throttled by 25th-ranked Texas A&M 41-10, propelling the Aggies up 13 spots to 12th in this week’s poll.

East Coast fans who stayed up late on Saturday witnessed one of the greatest comebacks of the season, as Miami overcame a 25-point deficit at California to secure a last-minute victory. Despite the heroics, it was not a good week for ranked teams playing on the road.

Texas A&M is one of the early surprises of the college football season through Week 6. The Aggies are now 5-1 and tied with Texas for the lead in the SEC. Other early surprises include 6th-ranked Miami and 19th-ranked Indiana, both 6-0. Both Army and Navy are undefeated, marking the first time both have done simultaneously this long since 1945.

Our weekly football report looks at key games throughout the South, which is home to the Piedmont. This past week’s focus was on the Ole Miss-South Carolina game, which turned out to be much more one-sided than expected. South Carolina had shown promise earlier in the season, with a road victory at Kentucky and a narrow home loss to LSU. Ole Miss had been ranked in the top 10 all season before losing to Kentucky at home in Week 5.

Ole Miss dominated South Carolina on Saturday, cruising to a 27-3 victory. The Rebels excelled on both sides of the ball, with a stifling defense that recorded six sacks and ten tackles for loss while holding the Gamecocks to just 4.1 yards per play. Offensively, they capitalized on numerous South Carolina mistakes, including several untimely penalties—eight for 90 yards—and a few questionable coaching decisions that would have appeared brilliant had they worked.

History of the University of South Carolina

The University of South Carolina (USC) was established in 1801 as South Carolina College by the state’s General Assembly, with the goal of bridging the cultural divide between the Lowcountry and Backcountry regions. Located in Columbia, near the state capital, the college quickly gained a reputation as one of the premier institutions in the South. However, the Civil War disrupted its operations, with many students joining the Confederate Army. The campus was eventually repurposed as a hospital for Confederate troops. After the war, the college was re-established as the University of South Carolina in 1865. During Reconstruction, USC became the first Southern state university to admit Black students, though this period of integration ended with the withdrawal of federal troops in 1877.

In 1880, USC reopened as an all-white agricultural college, reflecting the political climate of the time. Significant progress came in 1895 when women were first admitted, and by the early 20th century, USC began expanding beyond its agricultural roots. The institution regained full university status in 1906 and earned accreditation in 1917. The Great Depression brought financial hardship, but World War II revitalized the university. Military training programs and the influx of students through the G.I. Bill dramatically increased enrollment, prompting the university to expand its physical infrastructure and academic offerings.

The 1960s were a transformative era for USC, marked by the Civil Rights Movement and desegregation. After years of resistance, the university was forced to integrate in 1963 following a legal battle. Henrie Monteith, Robert Anderson, and James Solomon became the first Black students to enroll at USC since Reconstruction, ending segregation at the last Southern flagship university to do so. The Baby Boomer generation fueled massive growth, with student enrollment rising from 5,500 in 1960 to over 26,000 by 1980. In 1981, women outnumbered men in the student body for the first time, reflecting broader social changes.

Today, USC is renowned for several academic programs, particularly in International Business, which ranks among the top in the world, and Nursing, considered one of the best in the country. The university also excels in law, public health, and engineering. Its research capabilities have grown significantly, especially in areas like health sciences, nanotechnology, and cybersecurity. USC’s partnerships with South Carolina’s aerospace and manufacturing industries have bolstered the College of Engineering and Computing, making it a key player in the state’s economic development.

USC’s athletics, particularly its football team, have also brought national attention to the university. The Gamecocks have competed in the Southeastern Conference since 1992, and Williams-Brice Stadium is one of the hottest, toughest, and loudest venues in the league.

Prominent alumni include musician Darius Rucker, baseball player Mookie Wilson, U.S. Senator Lindsey Graham, and Fox News television host Ainsley Earhardt. Today, USC continues to expand, boasting a student population exceeding 34,000 and offering more than 300 academic programs, blending a rich historical legacy with forward-looking initiatives in research, innovation, and diversity.

South Carolina Gamecocks

The University of South Carolina fielded its first football team on December 24, 1892, against Furman, though the team was not officially sanctioned by the university at the time. They were initially nicknamed the “College Boys” and wore garnet and black. The program formally adopted the “Gamecocks” nickname in 1900, inspired by the school’s fighting spirit and competitive nature.

The University of South Carolina fielded its first football team on December 24, 1892, against Furman, though the team was not officially sanctioned by the university. Initially nicknamed the “College Boys,” they wore garnet and black. The program formally adopted the “Gamecocks” nickname in 1900, inspired by the school’s fighting spirit and competitive nature.

The term “Gamecock” reflects a rich local heritage, with historical roots in the Carolinas where cockfighting was popular in pre-revolutionary times. Gamecocks were prized for their fighting spirit. The university officially adopted the nickname in 1901, in honor of Francis Marion, a military officer in the American Revolutionary War, known for his guerrilla warfare tactics against the British. Marion was often called the “Carolina Gamecock,” and his legacy of resilience and bravery became a symbol for the university’s athletes. Today, the Gamecocks represent not only the university’s sports teams but also the pride and tenacity of the South Carolina community.

The Gamecocks won their first game in 1895 and hired their first head coach, W. H. “Dixie” Whaley, the following year. They faced their arch-rival Clemson for the first time in 1896, winning 12–6. Under coach Bob Williams in 1903, the team achieved its first 8-win season (8–2) before the rivalry with Clemson was paused until 1909 due to a notable incident/riot.

From 1953 to 1970, the Gamecocks were part of the Atlantic Coast Conference (ACC), achieving a No. 14 ranking in the 1958 final AP poll and winning the 1969 ACC Championship. Between 1971 and 1991, they operated as a major independent, producing Heisman Trophy winner George Rogers in 1980 and finishing in the final AP top 25 in 1984 and 1987, ranked No. 11 and No. 15, respectively. Since joining the SEC in 1992, the Gamecocks won the SEC East Division in 2010 and secured seven final top-25 rankings, including three top-10 finishes and one top-5 finish.

The program has produced a National Coach of the Year (Joe Morrison, 1984), three SEC Coaches of the Year (Lou Holtz in 2000, Steve Spurrier in 2005 and 2010), and one ACC Coach of the Year (Paul Dietzel, 1969). Additionally, they have had two overall No. 1 NFL Draft picks (George Rogers in 1981 and Jadeveon Clowney in 2014) and five members in the College Football Hall of Fame, including players George Rogers and Sterling Sharpe, and coaches Holtz and Spurrier, along with former Athletic Director Mike McGee.

South Carolina has struggled in recent years. Last season, the Gamecocks finished 5-7, a disappointing result following an 8-5 season the previous year, which ended with a top-20 ranking.

Economic development in Columbia remains robust, highlighted by a $2 billion investment from Scout Motors, a subsidiary of Volkswagen. This new manufacturing plant will produce electric trucks and SUVs, positioning Columbia as a key player in the emerging “Battery Belt.”

Mississippi’s Economy

Mississippi’s economy has evolved from its historic reliance on agriculture—particularly cotton and textiles—into a more diversified mix of manufacturing, energy production, and services. Technological advancements, industrialization, and policy changes have propelled Mississippi’s shift, enabling it to capitalize on the expanding automotive, aerospace, and defense sectors in the South.

In the 19th century, Mississippi was a leading cotton producer, thanks to the cotton gin and fertile land. This prosperity, built on enslaved labor, was shattered by the Civil War, leading to economic struggles during Reconstruction. Cotton remained dominant, but price fluctuations, the boll weevil infestation, and the Great Depression hurt the agricultural sector. Mechanization further reduced the need for manual labor, exacerbating rural poverty.

To counter these challenges, Mississippi pursued new industries in the early 20th century, with textile mills becoming a key economic driver. New Deal programs modernized infrastructure, and World War II spurred industrial growth, particularly in military production. Post-war, the state diversified further, gaining manufacturing strength in automotive parts, chemicals, and energy, supported by infrastructure improvements like the Interstate Highway System.

By the late 20th century, manufacturing had grown significantly, with companies like Nissan and Ingalls Shipbuilding becoming major employers. The Gulf Coast became a hub for shipbuilding and energy. In the 1990s, riverboat casinos transformed cities like Biloxi and Gulfport into tourism and gambling centers.

In the 21st century, Mississippi continues to expand its advanced manufacturing sector, particularly in automotive, shipbuilding, aerospace, and alternative energy. While these industries have driven job growth, challenges persist in education, poverty, and healthcare. Despite these obstacles, the state is working to attract foreign investment, improve workforce training, and leverage its central location in the growing Southern economy.

Agriculture, particularly soybeans, catfish farming, and poultry, remains important. However, the state’s economy now includes a mix of traditional industries like furniture manufacturing and newer sectors like tourism, casinos, and aerospace.

The University of Mississippi (Ole Miss)

Founded in 1844 in Oxford, the University of Mississippi (Ole Miss) is the state’s first public institution of higher education. Unlike many universities of its time, which focused on agriculture and technical skills, Ole Miss adopted a broad curriculum, establishing early programs in engineering and law. During the Civil War, the entire student body enlisted in the Confederate Army as the “University Greys,” suffering significant casualties. The campus became a wartime hospital and burial ground. After the war, former Confederate General A.P. Stewart served as the first chancellor.

Despite its Confederate ties, Ole Miss has been a leader in progressivism. The university admitted women in 1882 and became the first in the Southeast to hire a female faculty member in 1885. The G.I. Bill and state investment, including the establishment of a medical school in Jackson in 1950, helped the university grow in the 20th century.

The university’s most pivotal moment came in 1962 when James Meredith became the first African American to enroll, sparking violent protests that required federal intervention. This marked a turning point for Ole Miss in its efforts toward inclusivity, which continue today with the removal of Confederate symbols.

Today, Ole Miss is a comprehensive institution with an R1 research designation and over 200 programs. Its medical center and research initiatives contribute significantly to Mississippi’s economy. The university also has a storied athletic history, with its football program driving school spirit and national recognition.

Prominent alumni include Nobel Prize-winning author William Faulkner, U.S. Senators Roger Wicker and Trent Lott, and football icon Archie Manning. These alumni reflect the university’s wide-reaching influence in literature, politics, and sports. Ole Miss continues to evolve while maintaining its position as a flagship educational institution in Mississippi.

Oxford, Mississippi

Oxford has evolved from the agrarian town in Northern Mississippi its was founded as in 1837 into a lively cultural hub. The establishment of the University of Mississippi in 1844 anchored its economic development. Despite the disruption and destruction caused by the Civil War, including the burning of Oxford in 1864, the university served as a stabilizing force in the town’s post-war recovery.

In the 20th century, Oxford diversified beyond agriculture. The G.I. Bill after World War II increased enrollment at Ole Miss, sparking growth in housing, retail, and hospitality. The integration of Ole Miss in 1962 brought national attention and federal investment, further solidifying Oxford’s economic base.

By the late 20th century, Oxford had become a cultural destination, largely due to its association with Nobel laureate William Faulkner. The university continued to drive growth in sectors like real estate, retail, healthcare, and research. Today, Oxford offers a blend of Southern charm, academic influence, and cultural richness, making it an attractive place for both residents and visitors.

The town’s downtown area, known as The Square, is the heart of the community, offering a mix of boutiques, restaurants, and cafes. The historic courthouse stands as a focal point. The dining scene is diverse, with a blend of Southern and contemporary cuisine. Famous establishments like City Grocery and Ajax Diner add to Oxford’s culinary reputation.

The Grove, a 10-acre area on the Ole Miss campus, is renowned as one of the most iconic tailgating spots in college football. Game-day tailgating at Ole Miss is a cultural event, with fans setting up elaborate tents featuring fine dining, chandeliers, and the school’s red and blue colors. Southern dishes like fried chicken, deviled eggs, and barbecue are popular, adding to the festive atmosphere. The Grove’s tailgating experience is widely recognized as one of the best in the country.

Oxford, located in central Lafayette County about 75 miles south of Memphis, Tennessee, has a population of around 28,000. Its Micropolitan area, including Lafayette County, is home to just under 60,000 people. The city’s hilly terrain and grid-patterned streets reflect its unique geographical position compared to the nearby Mississippi Delta.

Ole Miss Football

The University of Mississippi, known as Ole Miss, has a rich football history that began in 1893. Nicknamed the Rebels, the program quickly established itself in the Southern Intercollegiate Athletic Association before becoming a founding member of the Southeastern Conference (SEC) in 1933, where it remains today.

Initially facing challenges, Ole Miss gained traction in the 1930s, culminating in its first SEC championship in 1947. Under coach John Vaught, who took over that same year, the Rebels became a national powerhouse, winning three national championships (1959, 1960, and 1962) and six SEC titles. Vaught’s tenure fostered significant rivalries, especially with Alabama and LSU, and cultivated a strong, loyal fan base.

Mississippi’s population and economy were on par with its Southern neighbors in the 1930s, 40s, and 50s but steadily lost ground in subsequent decades. According to the Census, Mississippi’s 1960 population was slightly below its 1950 population, as residents relocated to more vibrant economies in the South and Midwest. That outflow made it more difficult for Mississippi to compete for top-notch talent.

Following Vaught’s retirement in 1973, Ole Miss struggled to maintain its success. However, under coaches like Billy Brewer and Tommy Tuberville in the 1990s, the Rebels experienced a resurgence, highlighted by a 13-0 victory over Air Force in the 1992 Liberty Bowl.

The 2000s were marked by further volatility. In 2008, Coach Houston Nutt led Ole Miss to a key victory over Florida and a Cotton Bowl win over Texas Tech. Nutt took the Rebels to another Cotton Bowl victory the following year but then struggled and was replaced by Hugh Freeze in 2012. Freeze led the Rebels to four straight bowl games, including their first New Year’s Six, the 2015 Sugar Bowl, where they defeated Oklahoma State 16-13 and finished 12th in the AP Poll.

After enduring NCAA sanctions that vacated much of Hugh Freeze’s success, head coach Lane Kiffin helped reinvigorate the program in the 2020s. In 2023, the Rebels achieved their first-ever 11-win season, capped off by winning the Chick-fil-A Peach Bowl. Ole Miss aggressively pursued players in the transfer portal and was a popular outsider pick to challenge Georgia, Alabama, and Texas for the SEC title. After rising to fifth in the nation, hopes dimmed following a 20-17 loss to Kentucky in the SEC opener in Week 5.

Despite the disappointing loss, Ole Miss remains in contention for the SEC title. The Rebels rebounded with a solid road victory over South Carolina and were one of the few ranked teams to perform well on the road last week. Alabama’s loss and Georgia’s earlier defeat mean the conference championship is still up for grabs. Texas and Texas A&M are the only remaining unbeatens in the SEC, and they will face off against one another the Saturday after Thanksgiving.

Ole Miss travels to 13th-ranked LSU this weekend and then has a bye before hosting 18th-ranked Oklahoma later this month. After that, they face road games at Arkansas and Georgia. Their path to the SEC Championship is challenging but not significantly more difficult than that of any other contender.

South Carolina’s road will not get easier. This week, they travel to Alabama, likely facing a determined and angry Crimson Tide team. That said, Vanderbilt showed that it is possible to run the ball against Alabama and limit their quick-strike offense.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

October 7, 2024

Mark P. Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

Ethan Jacobs

Economic Analyst Intern

Benjamin Jacobs

Economic Analyst Intern

Not Too Hot, Not Too Cold, But Not Quite Right

Goldilocks Still Wants a Big Raise

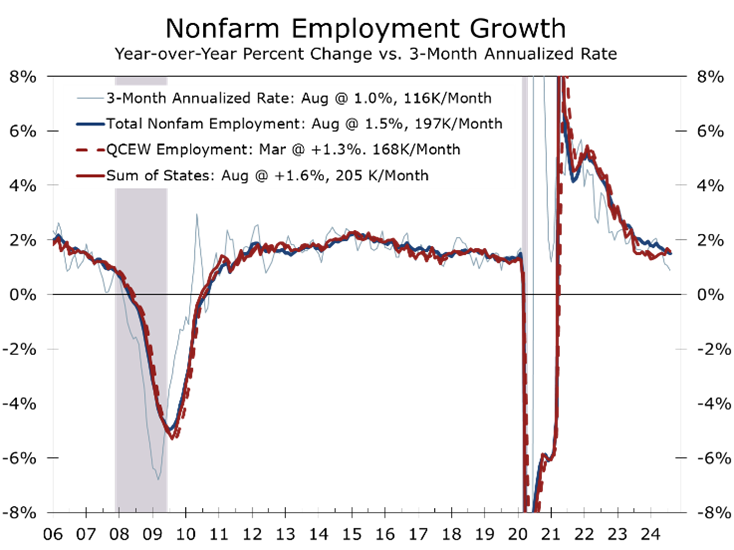

- Employers added 254,000 jobs in September, significantly exceeding the consensus estimate of 150,000.

- Revisions to the prior two months’ data added a combined 72,000 jobs, easing concerns that the labor market had cooled too much.

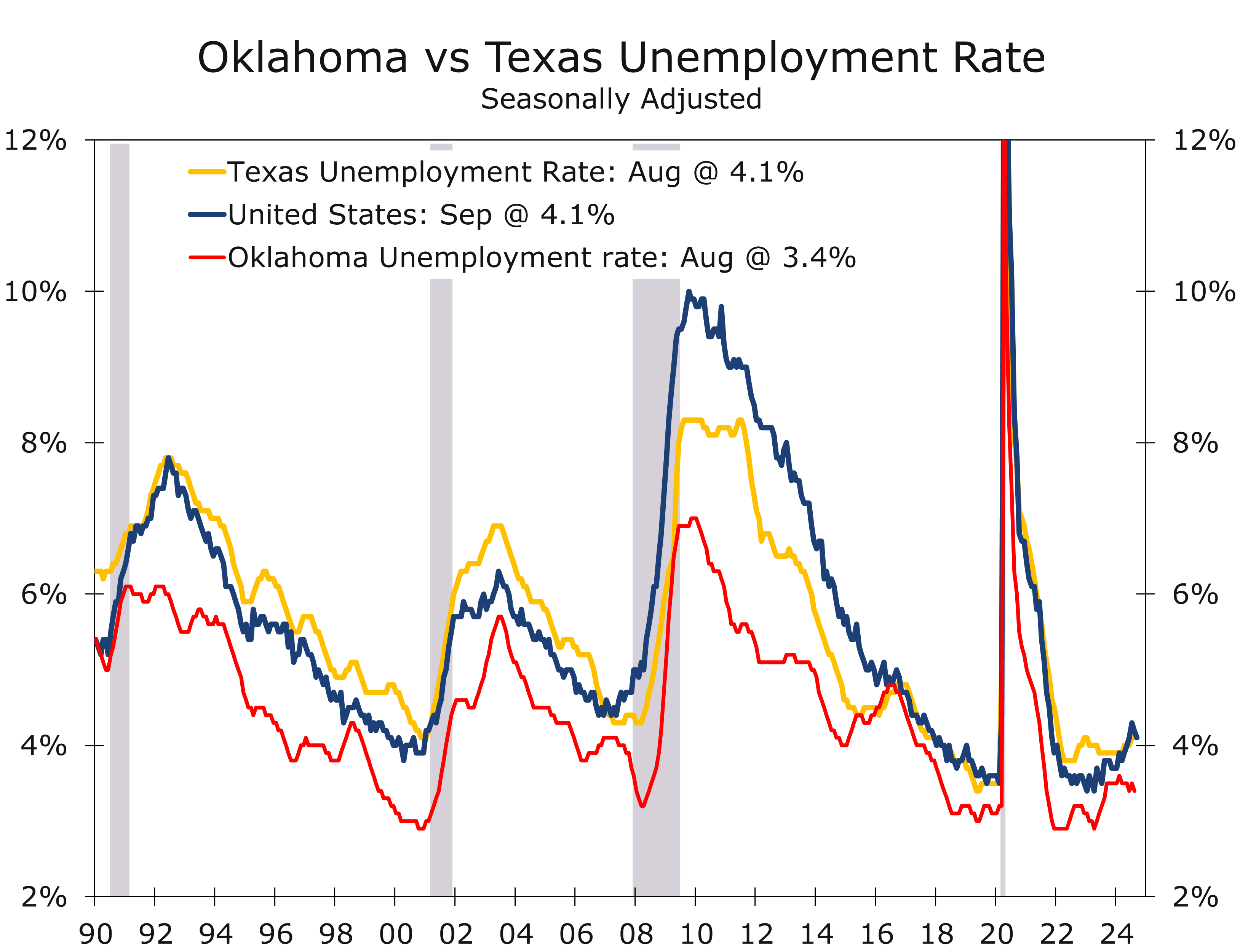

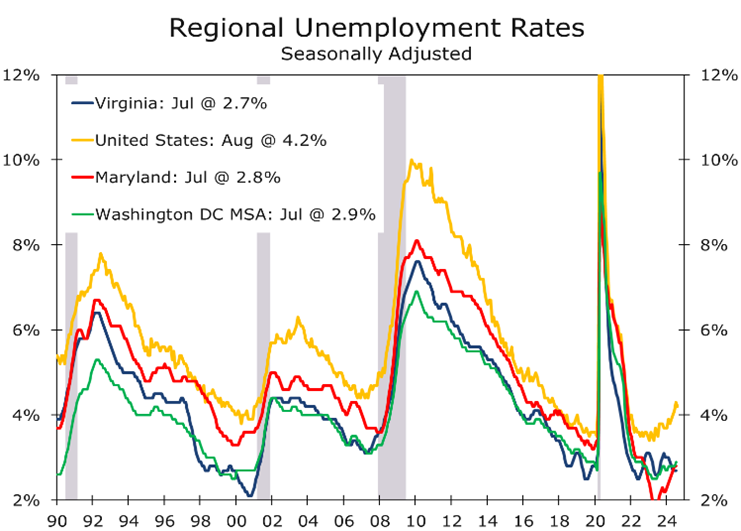

- The unemployment rate fell 0.1 percentage point to 4.1%, as the number of employed persons rose by 430,000 and far outstripped the 150,000-person rise in the labor force.

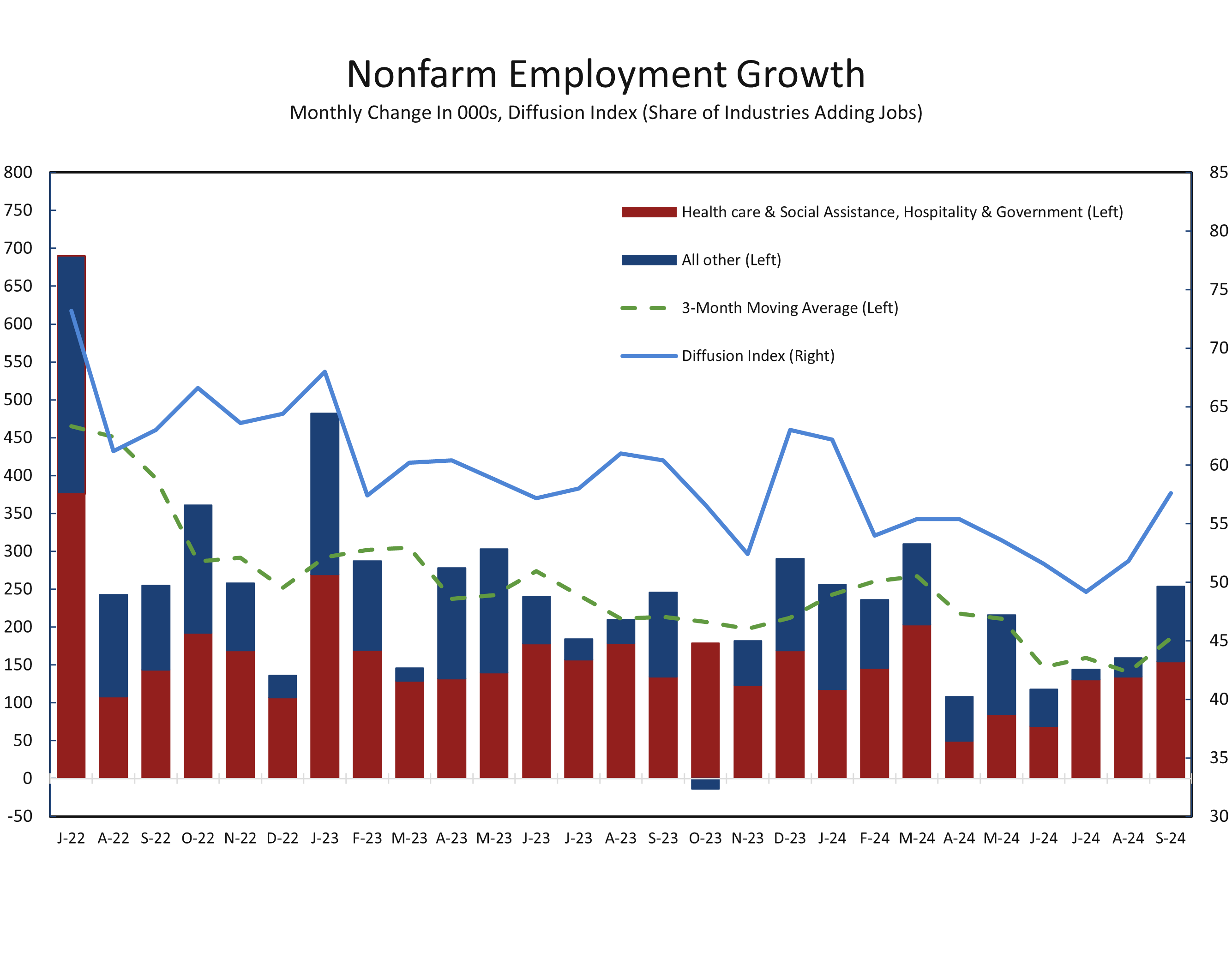

- Leisure and hospitality (+78K), health care and social assistance (+72K), government (+31K) and construction (+25K) continue to account for the bulk (80%+) of net new jobs.

- Job gains are more widespread, however, with the diffusion index rising to 57.6, up 8.4 points from its July low.

- Many pundits labeled September's job report as a return to a Goldilocks economy—not too hot, not too cold. While some data supports this view, something is off. Labor unrest persists. The tentative port deal includes a 62.5% pay raise over five years and limits on productivity-enhancing investments. This hardly seems consistent with a cooling labor market.

The September employment report exceeded expectations, with employers adding 254,000 net new jobs—the most in six months. Revisions to July and August added another 72,000 jobs, suggesting the labor market was not as weak as the Fed feared at the September FOMC meeting. Job gains were also slightly more broad-based, and the strength in payrolls was confirmed by a 430,000-job gain in the household survey. The drop in the unemployment rate is actually larger than it appears. The unemployment rate fell by 0.17 percentage points to 4.1%. The August unemployment rate was rounded down to 4.2% and September’s rate is now being rounded up to 4.1%.

Job growth exceeded expectations, easing fears but dashing hopes for aggressive rate cuts.

The improved labor market assessment follows unexpectedly large upward revisions to the National Income and Product Accounts (NIPA) last week, which showed that growth, income, savings, and corporate profits are all in better shape than previously thought. This more robust economic backdrop was acknowledged by Fed Chair Jerome Powell earlier this week, signaling a cautious approach to further rate cuts. Powell noted that any further weakening of the labor market would be unwelcome. Those concerns now seem overblown, which may prompt some forecasters to lower expectations for rate cuts in 2025.

While job gains were broad-based, leisure and hospitality, healthcare, government, and construction made up the bulk of the increases. The diffusion index for private nonfarm payrolls, which tracks the percentage of industries adding staff, rose to 57.6% in September, up from 49.2% in July and marking the highest level since January. Job growth has slowed significantly across several sectors, including wholesale trade, retailing, transportation and warehousing, information, financial activities, professional and business services, and other services.

While more industries added jobs in September, job growth remained highly concentrated.

Manufacturing remains a weak spot, with payrolls declining over the past two months and down more than 40,000 this year. The Boeing strike, which began in September, may impact October’s data. More fundamentally, demand for goods has softened since the Fed began raising rates and will take time to recover. We expect lower interest rates to boost home buying and durable goods purchases by next spring.

Hours-worked are another weak spot. Average weekly hours declined slightly to 34.2. Total hours worked fell by 0.1% in September and rose at just a 0.2% annual rate in the third quarter. Changes in hours worked are closely watched because they often precede changes in employment.

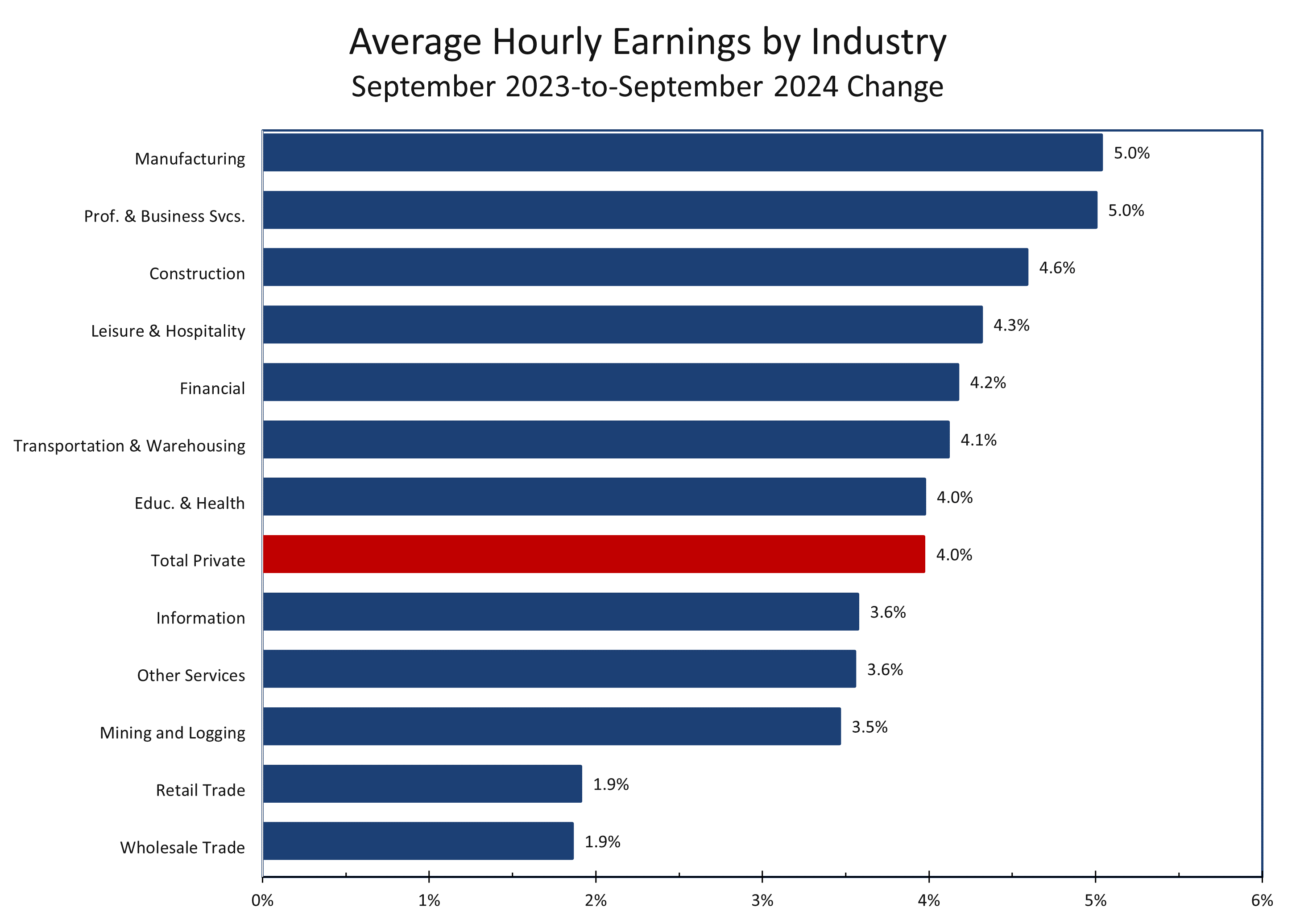

Average hourly earnings for private nonfarm employees rose by 13 cents (0.4%) to $35.36 in September, reflecting a 4.0% increase over the past year. Wages for private-sector production and nonsupervisory workers increased by 8 cents (0.3%) to $30.33. Despite recent productivity gains, these wage increases exceed the Fed’s preferences, particularly amid heightened strike activity and significant wage settlements. Even with improved productivity, annual wage gains of 4% or more are inconsistent with a sustained return to 2% inflation.

Overall, September’s employment report wasn’t as strong as the headlines suggest. While job growth rebounded, much of it came from just four sectors—restaurants, retail, healthcare, and government—all still working to restore staffing to pre-pandemic levels, with many of the jobs added being in lower-paying occupations.

Combined with stronger income and profits data, the economy appears less vulnerable than previously feared. The Fed is expected to proceed with a more measured pace of rate cuts, likely opting for 25 basis-point reductions in both November and December. We have also removed one of the rate cuts we had penciled in for 2025.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

October 4, 2024

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704)-458-4000

A View from the Piedmont: Looking Forward to an Eventful Year-End

Another Pivotal Week for the Economy

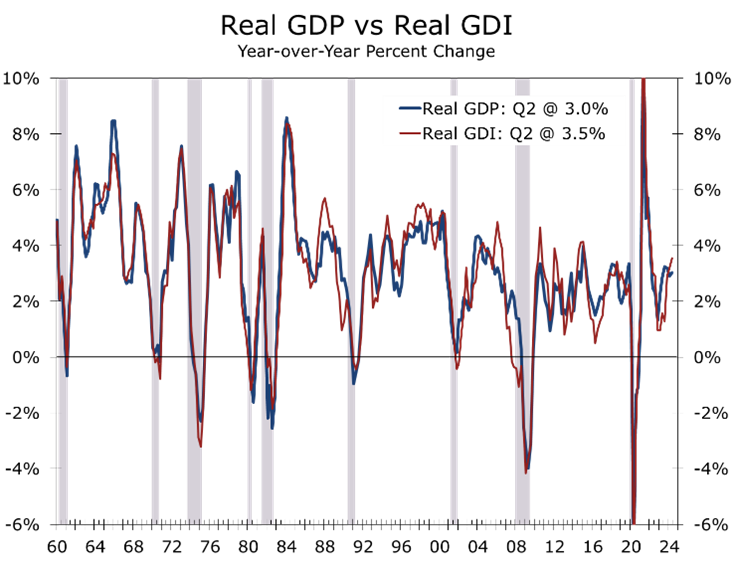

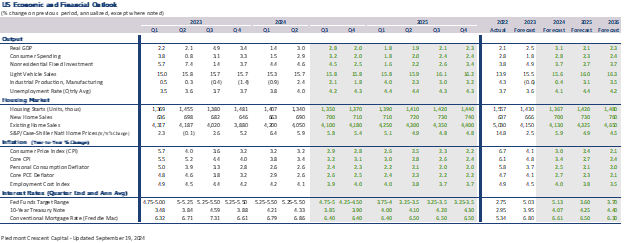

- Revisions to Q2 real GDP left growth unchanged at 3.0%. The composition is slightly weaker, with downward revisions in consumption and capital expenditures offset by higher government spending and increased business inventories.

- 2023H1 growth was stronger, while growth in the second half was revised lower.

- Gross Domestic Income (GDI) growth was revised up sharply, narrowing the statistical discrepancy with GDP.

- The saving rate for Q2 and earlier was revised higher, suggesting consumers have a little more spending capacity.

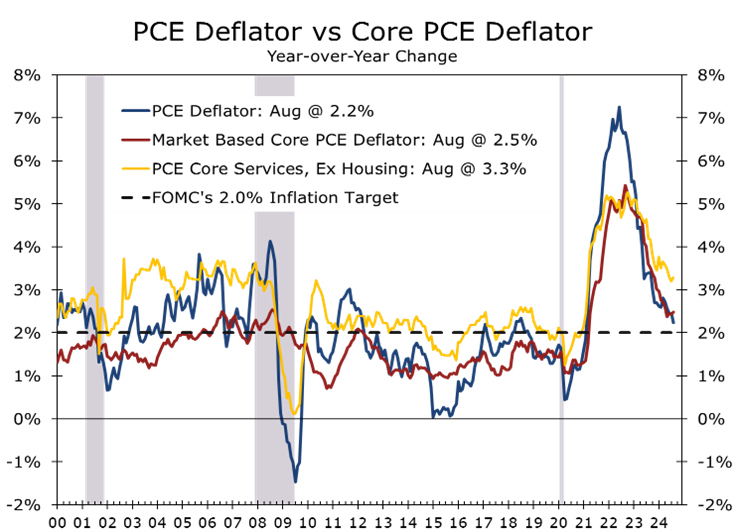

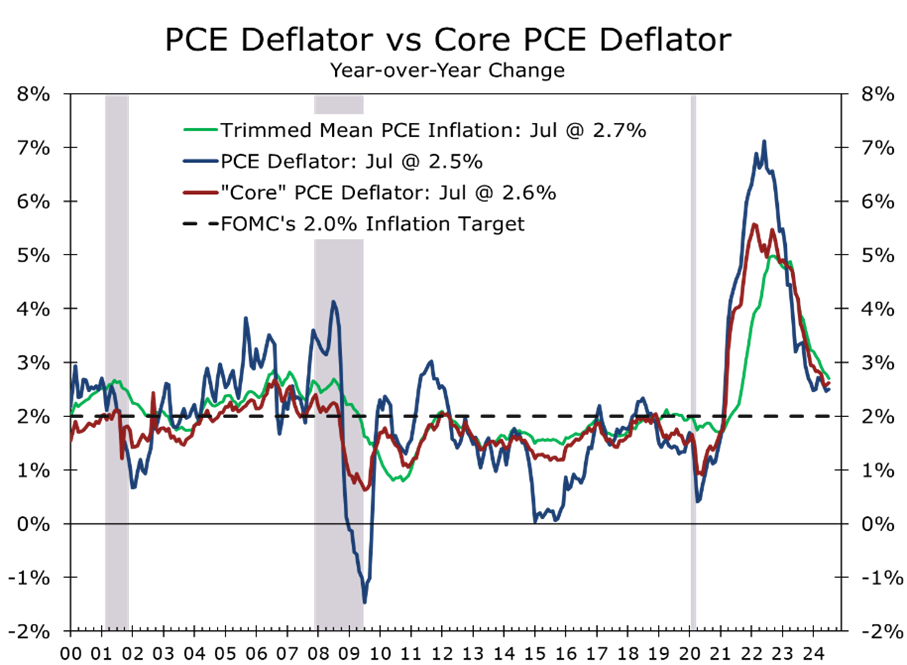

- Core PCE inflation rose 0.1% in August, with the year-over-year rise moderating to 2.7%.

- Economic data looks surprisingly benign, while inflation is moderating slightly more than expected. This gives the Fed room to lower rates further, but likely at a slower and more cautious pace. Geopolitical risks remain high, with Israel intensifying its response to Hezbollah’s attacks.

This past week featured a full calendar of economic releases, led by the third revision of second-quarter GDP growth. Overall growth remained unchanged from the previous estimate, with real GDP rising at a 3.0% annual rate in Q2. However, the composition of growth was slightly softer, with downward revisions to consumer spending, business investment, housing, and net exports. These declines were offset by upward revisions to government spending and business inventories. Real GDP growth for the first quarter was revised slightly higher, bringing the growth rate for the first half of the year to 2.4%, up from the previously reported 2.2%.

Although the second quarter now feels distant, this report included revisions dating back to 2019, revealing several surprises. The revisions show the economy is slightly stronger. Real Gross Domestic Income (GDI) growth for Q2 was revised up by 2.1 percentage points to 3.4%, narrowing the previously wide gap between GDP and GDI. GDI growth was also revised higher over the past few years, reflecting stronger corporate profits and net interest payments. These changes resulted in a 1.3 percentage point upward revision for 2023, with smaller adjustments for 2022 and 2021, moving the year-over-year GDI from 1.1 points below GDP to half a point above it.

With more income growth, the personal saving rate for Q2 was revised up by 1.9 percentage points to 5.2%. This improvement was driven by stronger employee compensation in late 2023 and early 2024, helping to explain the resilience of consumer spending this year despite slower job growth.

While earlier income data were revised higher, the most recent figures came in soft. Personal income rose just 0.2% in August, slightly below expectations, as solid gains in employee compensation (+0.5%), rental income (+0.7%), and transfers (+0.1%) were offset by declines in proprietors’ income (-0.2%) and interest and dividends (-0.5%). Consumer spending edged up 0.2%, driven primarily by a 0.2% increase in services spending, while real goods spending remained flat.

Wages and salaries are growing steadily, which should support holiday season spending.

The saving rate edged down to 4.8% from an upwardly revised 4.9% in July, reflecting recent national accounts revisions. A month ago, consumers appeared strapped, with the saving rate reported at just 2.9%.

Inflation continues to moderate gradually. The core PCE price index rose 0.1% in August, bringing the year-over-year change to 2.7%. Core services, excluding housing, increased 0.16% in August and are up 3.3% year-over-year. The market-based core PCE deflator rose 0.15% and is up 2.5% year-over-year. All measures seem to be on a path toward the Fed’s 2% target.

Despite a slight slowdown in August personal consumption, we have raised our Q3 GDP forecast to an annual rate of 3.1%. Advanced indicators point to a narrowing goods trade deficit and solid growth in core durable goods orders.

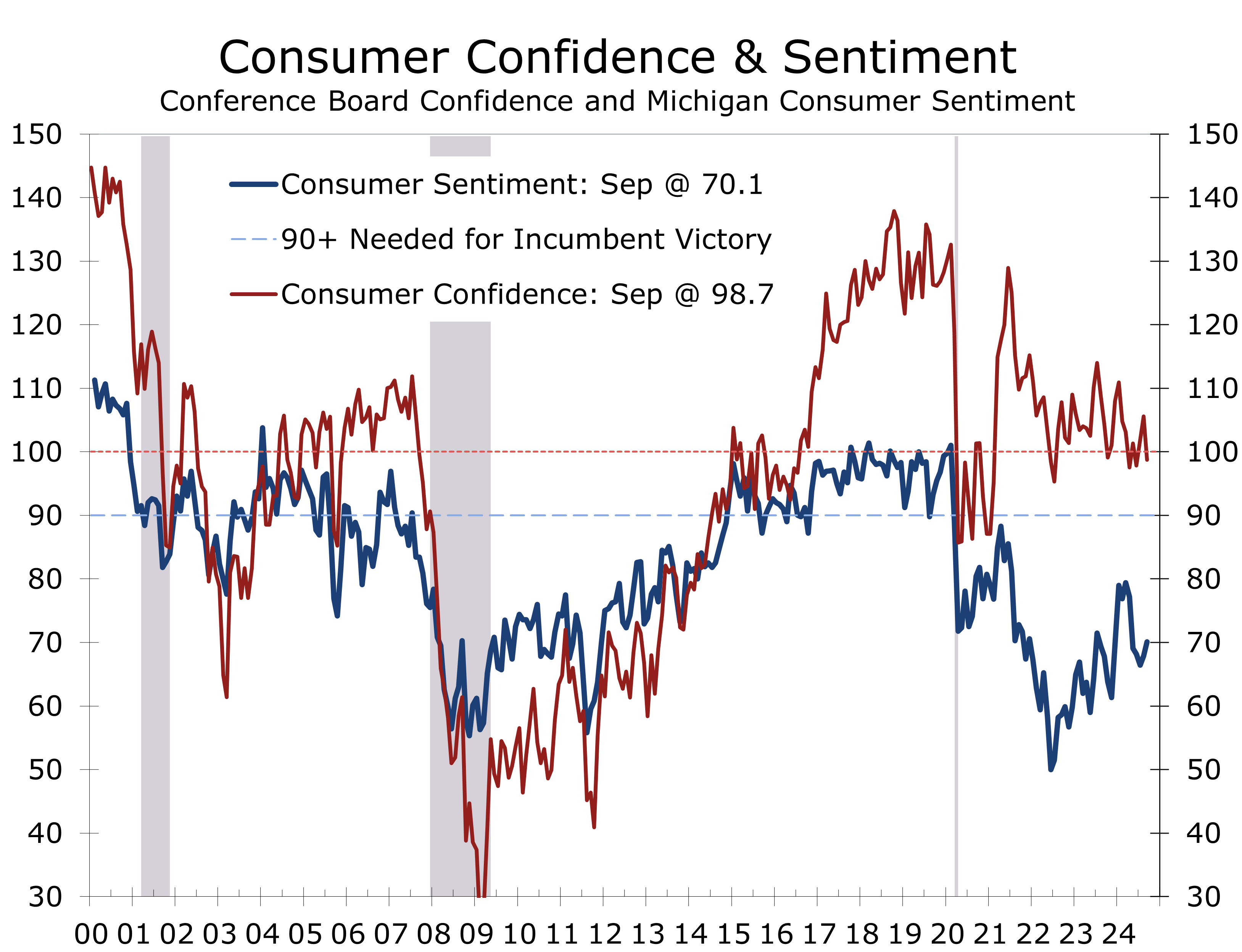

Despite upward revisions to GDP and earlier income growth, consumers remain uneasy about the economy. The Conference Board’s consumer confidence index fell by 6.9 points to 98.7 in September, below expectations. This drop was slightly offset by an upward revision to August’s data, which raised that month’s reading to 105.6. Both components of the index declined in September, with the expectations index down 4.6 points to 81.7, and the present situation index falling more sharply by 10.3 points to 124.3.

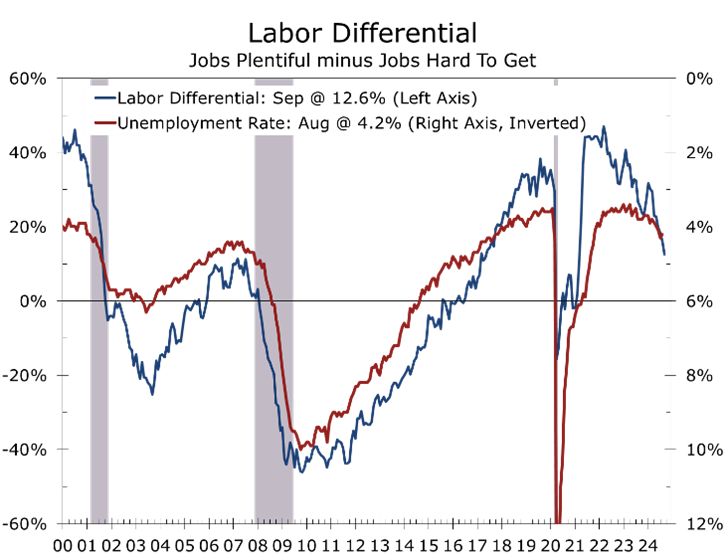

The labor market differential—the gap between respondents reporting jobs as plentiful and those saying jobs are hard to get—also weakened, falling 3.3 points to 12.6. This marks a significant drop from earlier in the year, sitting about 18 points lower than in Q1 2024 and well below the 2019 average of 33.2. The labor market appears to be correcting remarkably close to what monetary theory suggests, with job growth beginning to slow one year after the Fed started raising the federal funds rate, and the bulk of the impact from higher rates weighing on job growth 18 months after the first hike.

Consumer perceptions of the likelihood of a U.S. recession in the next 12 months rose 0.5 percentage points to 66.5%. The survey was completed by September 17, just before the Fed initiated its easing cycle with a larger-than-expected rate cut.

The half-point rate cut might help boost future sentiment. Despite declining confidence and labor market concerns, the outlook for consumer spending remains strong, supported by low jobless claims and healthy household finances. However, a clear divide persists between income groups: upper-income households benefit from a strong stock market, while middle- and lower-income households face rising costs for housing, groceries, and transportation.

The University of Michigan’s Consumer Sentiment Index showed slight improvement, rising 1.4 points to 67.8 in August, the first increase since March. Current economic conditions fell 1.8 points to 60.9, while the consumer expectations component rose 3.3 points to 72.1, likely influenced by the Fed’s larger-than-expected September rate cut, which came too late to affect the Conference Board’s data. From a political perspective, Consumer Sentiment remains well below the level typically needed for the incumbent party candidate to return to the White House.

Inflation expectations in the Michigan survey remained steady, with a 2.9% projected rise in prices over the next year, and long-term expectations for the next 5-10 years holding at 3.0%. This is still slightly elevated compared to historical norms and reflects the higher cumulative price increases, which continue to weigh on overall sentiment.

The other major story this past week was Hurricane Helene, which made landfall in Florida’s Big Bend region before rapidly moving north, dumping heavy rainfall across Georgia and North Carolina’s mountains. Early reports indicate over 100 lives lost, with monetary damages expected to exceed $150 billion. A significant portion of the damage is due to flooding, with many losses likely uninsured, which will slow the rebuilding process and dampen local economic activity in the coming months.

The geopolitical landscape remains volatile but shows signs of progress. Israel has swiftly neutralized threats on its northern border, utilizing superior intelligence and technology against what appeared to be a larger, more formidable force. Israel understands that decisive victories are essential to maintaining credibility in the Middle East. The swift dismantling of Hezbollah’s leadership sends a strong message to both Iran’s government and its opposition. Israel is expected to continue its efforts for a decisive victory over Hezbollah and the Houthis, particularly ahead of the U.S. elections. This could pave the way for broader peace agreements with Saudi Arabia and other Arab nations.

This coming week will feature several key reports, with ISM and employment data shaping market expectations for the Fed’s next move. We anticipate payrolls to increase by 150,000 in September, with a slight upward revision to the August figures. The Fed is likely targeting quarter-point rate cuts at both the November and December FOMC meetings. Powell noted that revisions to Gross Domestic Income and a higher saving rate have reduced some downside risks to the economy. We’ve raised our Q3 GDP forecast to 3.1%, though we still expect growth to slow toward its long-term potential. We’ve also adjusted our forecast for total rate cuts in this easing cycle to 175 basis points, 50 of which have already occurred.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

September 30, 2024

Mark Vitner, Chief Economist

Piedmont Crescent Capital

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

Georgia Travels to Tuscaloosa to Take on the Crimson Tide

The Biggest Game of the 2024 Season, So Far

- College football get real this week, with the 2nd-ranked Georgia Bulldogs traveling to Tuscaloosa to take on the 4th-ranked Alabama Crimson Tide. Both teams enter the game a ‘perfect’ 3-0.

- Georgia began the season strong, with a convincing 34-3 victory over currently 17th-ranked Clemson but struggled in its most recent game, winning 13-12 at Kentucky.

- Alabama has had a slower start, struggling to put points on the board early against relatively weak opponents in the first two weeks of the season before ultimately winning convincingly. The Tide looked much better in their most recent game, defeating Wisconsin 42-10.

- The Georgia economy has been on a roll recently, with huge investment in electric vehicle plants, battery plants, and green energy helping drive construction and manufacturing.

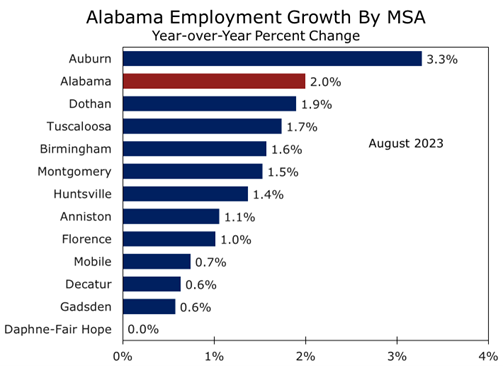

- The automotive sector has also been a key contributor to Alabama success. The state is also enjoying strong in-migration, particularly in Huntsville, Birmingham and along the Gulf Coast.

Unforeseen complications with travel, combined with an unusually busy schedule, forced us to call an audible last week and take Week 4 off from our nearly weekly football series. We had planned to cover the JMU-UNC matchup, which turned out to be one of the more notable blowouts of the week.

The most consequential game of Week 4 saw Tennessee visiting Oklahoma for the Volunteers’ first significant SEC test. Winning on the road is always difficult in the SEC, but the Volunteers passed the test convincingly, winning 25-15. Questions remains, however, whether Oklahoma is simply a middling SEC team. The Sooners had not previously been tested.

Week 5 brings a crucial top five matchup as #2-ranked Georgia visits #4-ranked Alabama.

Among several exciting Week 5 matchups, Georgia travels to Tuscaloosa to face Alabama. Both teams had byes last week, so they should be well-rested and healthy. Alabama has dominated Georgia in recent years and has benefitted from a significant edge in favorable calls and no-calls during legendary coach Nick Saban’s tenure. he Crimson Tide is now under the leadership of Kalen DeBoer, who guided Washington to the College Football Playoff last year. Georgia, which was ranked preseason number one, slipped to number two following their narrow 13-12 win over Kentucky in Week 3.

We have two reports this week. The first is a preview of the #2-ranked Georgia vs. #3 Alabama game, set for Saturday evening on ABC. This game should set the tone for the SEC race this year. Georgia faces one of the toughest regular season schedules ever devised, with road games against #4 Alabama, #1 Texas, and #5 Mississippi, before returning home to face #6 Tennessee. Alabama’s road ahead is slightly less daunting, as they host #2 Georgia, then go on the road to face #5 Tennessee, #16 LSU, and #15 Oklahoma, before returning home to host #7 Missouri.

The matchup between the nation’s second and fourth-ranked teams is expected to draw the largest television audience for a college football game so far this season. ESPN College Football GameDay will be in Tuscaloosa for the event. The game will be televised on ABC, with kickoff at 7:30 PM. Georgia and Alabama games have consistently ranked among the most-watched in the regular season, and their SEC Championship and playoff matchups rank among the most-viewed. On a historical note, the Georgia-Alabama matchup was the first college football game ever televised by ABC, and this year’s game will likely be the biggest one they have broadcast since winning the SEC contract from CBS.

Our second report attempts to make amends for last week and previews the UNC-Duke matchup. While a basketball contest between these two schools might be more enticing, this football matchup should be high scoring as well. UNC displayed little defense in their lopsided 70-50 loss to James Madison. Duke, meanwhile, has looked impressive so far this year, beating Middle Tennessee State 45-17 last week and edging out Big Ten academic powerhouse Northwestern 26-20 in overtime earlier this season. We will write more about James Madison later this year when they host the Marshall Thundering Herd in late November.

History of the University of Georgia

The University of Georgia (UGA), founded in 1785, holds the distinction of being the oldest public university in the United States. Established by the Georgia legislature in Athens, UGA was initially focused on classical studies and law. It later expanded its curriculum to include agriculture and mechanical sciences, particularly after receiving federal funding in 1872. Over the years, UGA has evolved into a major research institution with 17 different schools and a commitment to public service, boasting over 320,000 living alumni.

Spanning 762 contiguous acres, the UGA campus spreads southeast of its iconic Arch in downtown Athens. In 2011, the university acquired the 58-acre Navy Supply Corps School, enhancing its facilities. The Prince Avenue Campus now houses the Augusta University/UGA Medical Partnership and the College of Public Health, further broadening the university’s academic reach.

In the 19th century, UGA played a pivotal role in shaping higher education in the South. Despite facing significant challenges during the Civil War, including temporary closures, the university rebounded during the Reconstruction era by emphasizing inclusion and access to education. The mid-20th century marked another transformative period for UGA, particularly highlighted by the enrollment of its first African American students, Hamilton Holmes and Charlayne Hunter, in 1961. This event was a significant milestone in the ongoing struggle for equality in education.

Today, UGA is renowned for its strong programs in law, business, education, bioscience, and agriculture, having achieved Research I status due to its robust focus on research and innovation. The Terry College of Business, established in the late 20th century, has become one of the Southeast’s leading business schools. It is currently ranked among the top 15 public business schools in the nation, with 11 programs recognized nationally, including eight in the Top 10. The college emphasizes experiential learning through initiatives such as a student-managed investment fund and a variety of specialized master’s programs. Its state-of-the-art $140 million Business Learning Community, completed in 2019, is a campus unto itself and exemplifies UGA’s commitment to providing a premier educational environment.

The John M. Godfrey Department of Economics also contributes significantly to UGA’s academic offerings, producing rigorous research in public policy, labor economics, and monetary theory.

One of the newest schools is also one of the fastest growing: the UGA College of Engineering, established in 2012, which has grown to 2,400 students.

With a vibrant student body exceeding 42,000, UGA also boasts a rich athletic tradition, particularly in football, while playing a crucial role in the local economy by driving workforce development and public service throughout Georgia. Its enduring legacy continues to shape the educational, cultural, and economic landscape of the state and beyond.

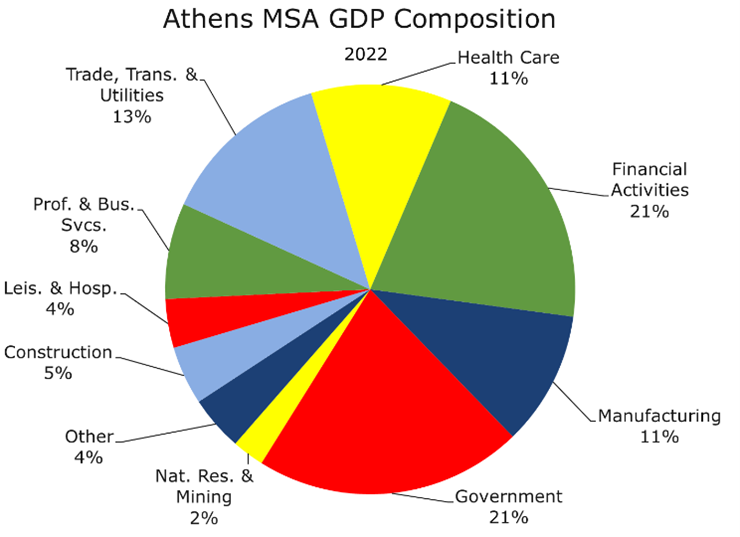

Athens, Georgia

Athens is a quintessential college town located about 70 miles northeast of Atlanta. The four-county Athens-Clarke County MSA has a population of 222,060, while the state’s flagship university has over 42,000 enrolled students. Sanford Stadium seats 93,033. Construction of the stadium, which is built in the valley of a creek near the center of campus, began in 1928, and the first game was played on October 12, 1929, against Yale. The Bulldogs won that game 15-0, and Yale donated their share of the gate receipts to the University to help repay the stadium construction loans. Georgia has long had a close connection with Yale, one of the early powerhouse football programs that helped spread the sport nationwide. Yale’s visit to Athens marked their first game in the South, drawing a record 30,000 fans who paid $3 each—the largest crowd for a football game in the South at the time.

The famous hedges around Dooley Field, named for Coach Vince Dooley, have been a part of the stadium since its opening, except for two key moments. In 1996, the hedges were removed to host soccer matches for the Atlanta Olympics, but new hedges were replanted using 2,100 clippings from the originals. They were also temporarily relocated during the construction of a new locker room and scoreboard on the west end. This year, the hedges planted after the Olympics began being gradually replaced with clippings from the originals once again.

The Athens MSA is part of the much larger Atlanta-Athens-Clarke County-Sandy Springs Combined Statistical Area (CSA), which boasts a 2023 population of 7.2 million and is the economic heart of the Southeast. While part of the broader CSA, Athens is far enough away from Atlanta that it has its own distinctive vibe and is a regional hub in its own right. Its vibrant downtown is full of restaurants, bars, and entertainment establishments, reflecting the growth of its influential music scene that produced leading-edge bands such as the B-52’s, R.E.M., Widespread Panic, Pylon, and the Drive-By Truckers.

The Birthplace of Alternative Rock

The music scene has been a significant cultural force in Athens since the 19th century, evolving through various styles and genres to create a unique sound known as the “Athens Sound.” This scene is notable for its influence on alternative rock and new wave music, producing globally recognized bands and a vibrant local culture.

The music scene in Athens traces back to Native American influences from the Creek and Cherokee tribes. By the time the city was chartered in 1806, it began to grow as a musical hub, particularly during the Civil War when it attracted major touring acts. The Morton Theatre, founded in the early 20th century, quickly became a cornerstone for African American performers and the local music scene, highlighting the city’s rich cultural tapestry.

The 1950s and 1960s music scene was characterized by dance events featuring popular bandleaders. Notable venues included Allen’s Hamburgers and the Canteen, where bands like The Jesters performed. By the late 1960s, the emergence of local bands marked a shift to more original acts. This period saw bands like the Normaltown Flyers and Dixie Grease gain prominence, setting the stage for a more diverse rock scene.

The B-52’s, formed in 1977 after a Valentine’s Day party, brought a campy, new wave aesthetic that would define Athens’ quirky style. Their hits like “Rock Lobster” and “Love Shack” garnered international attention. R.E.M., founded in 1980, quickly became the defining band of the Athens Sound. Their early hit “Radio Free Europe” was a breakthrough hit that eventually led to mainstream success with albums like “Out of Time” and “Automatic for the People.” Their blend of jangle pop and lyrical depth solidified Athens’ reputation as a rock hub. Pylon, formed in 1979, was integral to the local scene, known for their danceable sound and influence on the post-punk movement.

The 40 Watt Club, founded in 1978, became a central location for indie rock performances. Other notable venues include the Georgia Theatre, Caledonia Lounge, and the Foundry Music Venue. The Georgia Theatre has a storied history, having reopened in 2011 after a devastating fire. Events like AthFest and Athens Popfest celebrate local talent and foster a sense of community within the music scene.

The 1990s saw the Athens sound go mainstream, with bands evolving into a more eclectic style that melded numerous genres, most notably the grunge/alternative genre, which took off in Seattle. Some of the top bands of the era include Elf Power, Neutral Milk Hotel, and Of Montreal. While indie rock, punk, and pop music tend to typify the music scene, Athens has also birthed numerous bluegrass and folk artists and played a key part in the emergence of the Americana genre. Bands like the Drive-By Truckers and the Holman Autry Band have incorporated elements of country and rock, enriching the local musical landscape. Recent years have seen the rise of a Latin music scene, along with significant contributions from singer-songwriters and contemporary Christian artists.

Some of the top Athens-based music acts today include the Asymptomatics, Hotel Fiction, Dawes, and Wim Tapley & The Cannons. Athens recently landed a minor league hockey team that will debut this season in the brand-new Akins Ford Arena in downtown Athens. The team, dubbed the Athens Rock Lobsters in homage to the B-52s, is likely the band most responsible for kicking the Athens music scene into higher gear, which really took off with the rapid success of R.E.M.

The Athens economy has shifted from its manufacturing and agriculture roots to an “eds and meds” strategy, typical of many college towns. The largest employers today are the University of Georgia, Piedmont Athens Regional Medical Center, Athens-Clarke County government, and St. Mary’s Health Care System. The University of Georgia is also establishing its own medical school, set to open by 2026, to address the state’s physician shortage, with about a third of Georgia’s doctors nearing retirement.

While the University’s ties are deep, private employment has been growing at an average 2.2% annual pace over the past year. Major private employers include Caterpillar, whose 1,000-employee Bogart plant is the area’s largest manufacturing employer, Pilgrim’s, DialAmerica, and Carrier Transicold. Business-friendly regulations and low costs are assets for small businesses. Athens also saw its first major film studio open this past year, Athena Studios.

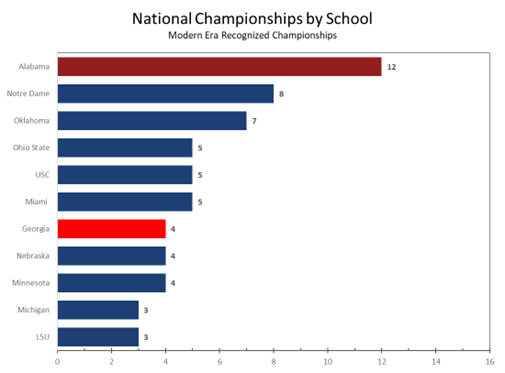

Georgia began playing football in 1892 and can lay undisputed claim to four national titles—1942, 1980, 2021, and 2022. The NCAA officially recognizes Ohio State as the national champion for 1942. The Buckeyes went 9-1 that year, with wins over #4 Michigan and #13 Illinois but a mid-season loss at #6 Wisconsin. Georgia finished that season 11-1 and shut out six of its 12 opponents, including a 34-0 thumping of #2-ranked Georgia Tech. Georgia also defeated #3-ranked Alabama that year. Georgia’s lone loss was to unranked Auburn.

The final AP poll was taken in late November of that year, well before the bowl games, and Georgia finished closely behind Ohio State. Georgia went on to defeat #13 UCLA in the Rose Bowl, and every major poll except the AP recognized them as national champion. Our count of national champions corrects this historic error. The 1942 team featured Heisman Trophy winner Frank Sinkwich, and Charlie Trippi was one of the best Georgia teams of all time. The 1980 team, which won an undisputed national championship, featured future Heisman Trophy winner Herschel Walker. The 2021 and 2022 teams featured Stetson Bennett, the former walk-on who won numerous awards and was the MVP of every college playoff game he played.

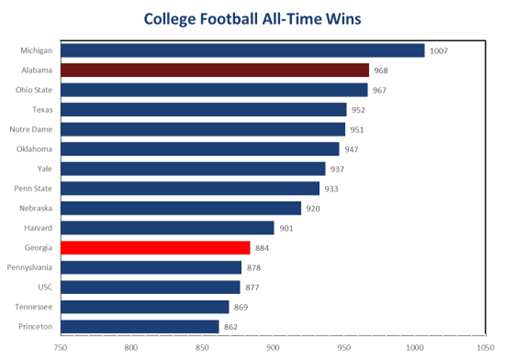

Four other Georgia teams can also lay some claim to being national champions, including the 1920 team headed by first-year coach Herman Stegeman, which went 8-0-1 and was the first Georgia team to go undefeated, outscoring opponents 250-17. The Bulldogs have 844 wins, the 11th most all-time. The team’s beloved live mascot is Uga XI, the eleventh English bulldog of the same lineage to represent the university’s sports teams.

UGA X is the all-time winningest bulldog, with the Dawgs going 91-18 under his watch, including back-to-back national championships. UGA wears a spiked collar and a red jersey and is considered a member of the team. He gets slightly better treatment than the players, however, with an air-conditioned doghouse on the sidelines to cool off during those hot early game days. One of the Bulldogs’ more recent traditions, begun under coach Mark Richt, is the Dawg Walk, when the players march from the buses on Lumpkin Street between two lines of fans into Sanford Stadium.

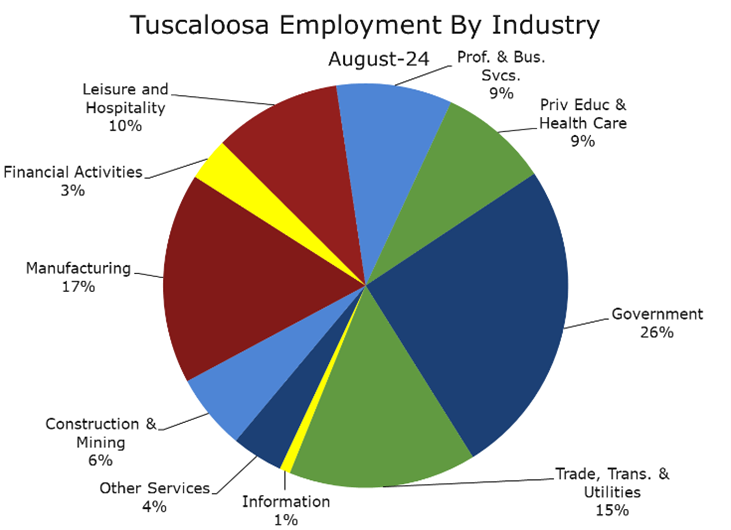

History of the University of Alabama

The University of Alabama (UA), founded in 1831 in Tuscaloosa, is the flagship institution of higher education in Alabama and one of the oldest public universities in the U.S. Initially offering a classical education, it was among the first five schools in the nation to provide engineering classes. The university faced significant challenges during the Civil War, including substantial damage to its campus, but continued to grow during Reconstruction, adding a law school in 1872 and the College of Engineering and School of Education in 1909.

Throughout the 20th century, UA became a focal point in the Civil Rights Movement, desegregating its campus in 1963 with the enrollment of African American students Vivian Malone and James Hood. Today, UA has approximately 38,000 students and is classified as a Very High Research Activity institution by the Carnegie Classification System. It is known for its strong academic programs in law, business, engineering, and the sciences, along with a vibrant athletic tradition, particularly in football, boasting multiple national championships. The University of Alabama continues to play a vital role in workforce development and innovation, upholding its legacy as a leading institution in the South and beyond.

Alabama Football History

The University of Alabama football program, established in 1892, is one of the most storied in college football history. Since the inaugural season, the Crimson Tide have accumulated 968 wins, 18 national championships (xx in the modern era), and a record 73 bowl appearances. Legends of the program include coach Paul ‘Bear’ Bryant, Joe Namath, Bart Starr, Shaun Alexander, and Heisman Trophy winners Mark Ingram and Derrick Henry. In recent years, the program has been a dynasty, winning national titles in 2009, 2011, 2012, 2015, 2017, and 2020.

Under the leadership of legendary coach Paul “Bear” Bryant from 1958 to 1982, Alabama became a dominant force, securing six national championships during his tenure. The tradition of success continued with coaches like Gene Stallings, who led the Crimson Tide to a national title in 1992, and Nick Saban.