February Retail Sales: : Broad-Based Rebound Masks Geopolitical and Tariff Headwinds

Consumer Spending Was Solid Ahead of the Iran War

- Retail sales rose 0.6% MoM in February 2026, a broad-based rebound following January’s upwardly revised –0.1% decline; the gain beat consensus estimates across all major categories.

- Core retail sales rose solidly. Sales excluding autos, gasoline, building materials, and restaurants rose +0.4% — the best reading since August 2025. Along with our estimate of services outlays, this points to a +0.6% nominal and +0.2% real increase in PCE for Februaryf.

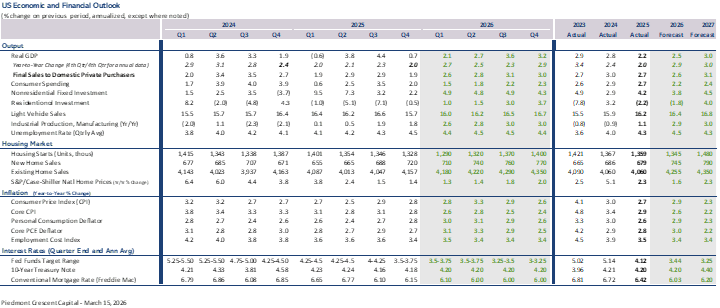

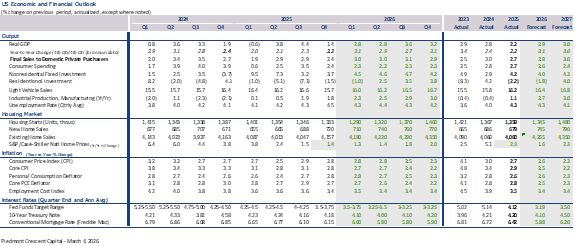

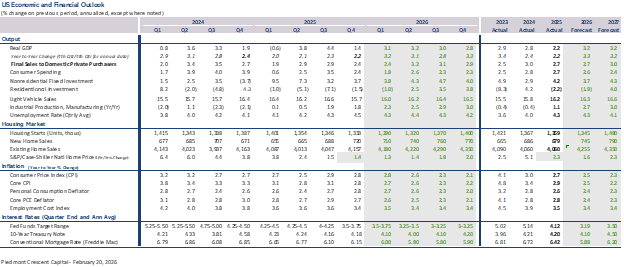

- We have lowered our Q1 real GDP forecast by 0.1 percentage point to a 2.0% annual rate. Real PCE is tracking a 1.5% annualized gain in Q1, consistent with our previously published forecast. We expect growth to strengthen modestly in Q2 and to end the year with solid momentum.

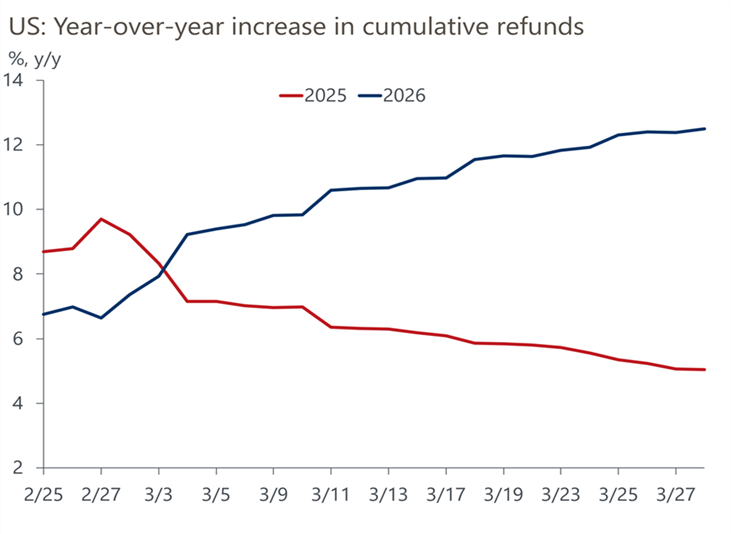

- The U.S./Israel war with Iran will begin weighing on March data, as gasoline prices averaged approximately 75 cents per gallon higher than in February. The near-term buffer comes from income tax refunds, which are running +12.5% YoY — cushioning discretionary spending for another month or two.

- Import prices surged +1.3% in February, the largest monthly jump since March 2022, compressing real purchasing power — most acutely for lower- and middle-income households who face a disproportionate tariff burden.

- Our 2026 outlook remains essentially the same as was published in March. We see real personal consumption expenditures rising at just a 1.6% pace in the first half of 2026, but look for spending to rebound to a 2.1% pace in the second half, aided by larger tax refunds and lower energy prices.

Data Note

Source and Methodology

This report draws on the U.S. Census Bureau’s Advance Monthly Retail Trade Survey (MARTS) released April 1, 2026, covering February 2026 activity. The release was rescheduled from March 16 following a lapse in federal appropriations. All figures are seasonally adjusted and not adjusted for price changes unless stated. Oxford Economics/Haver Analytics commentary (April 1, 2026) provides the analysis of cumulative year-over-year tax refunds, which helped influence the forecast for personal consumption expenditures.

| +0.6%

Total retail & food services, MoM — February 2026 |

+0.4%

Control group (ex-auto, gasoline, building material, food services) — 6-month high |

| +1.5%

Real PCE, Q1 2026 annualized — consistent with prior forecast |

2.0%

Piedmont Crescent Capital Q1 real GDP forecast (annualized rate) |

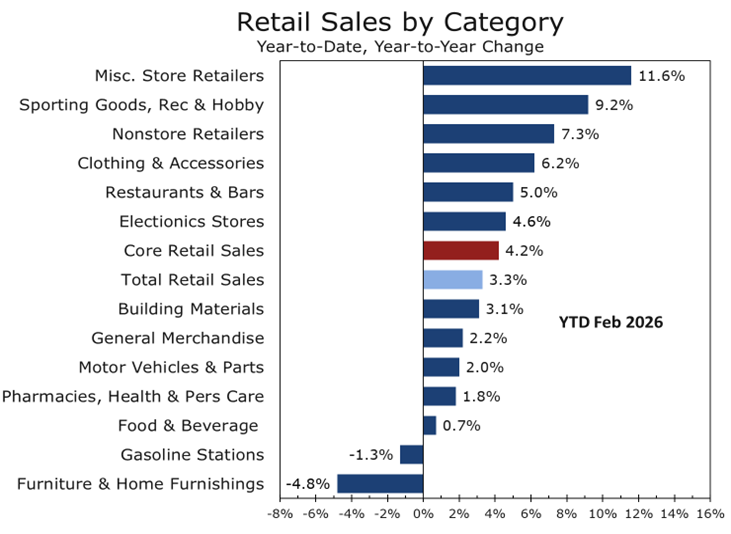

The February Rebound: Sales by Category

February’s +0.6% gain was the broadest monthly advance since mid-2025. The increase was broad-based and includes gains in categories where spending was likely depressed by weather in January — automobiles and restaurants and bars in particular. The only two categories to register outright declines were furniture, which continues to be weighed down by elevated mortgage rates and weak existing-home sales, and grocery stores, where deflation in some food categories is depressing the nominal total. Motor vehicles drove the headline increase, but the control group’s +0.4% print — which strips out autos, gas, building materials, and food services — confirms that the underlying demand signal is broad and genuine.

Full Category Breakdown — February 2026

| Category | MoM Change | YoY Change |

| Total Retail & Food Services | +0.6% | +3.2% |

| Control Group | +0.4% | +3.5% |

| Motor Vehicles & Parts Dealers | +1.5% | +2.8% |

| Food & Beverage Stores | –0.3% | +2.9% |

| General Merchandise Stores | +0.2% | +2.6% |

| Clothing & Accessories | +1.5% | +3.8% |

| Health & Personal Care | +1.7% | +4.5% |

| Nonstore Retailers (e-Commerce) | +0.8% | +10.9% |

| Food Services & Drinking Places | +0.5% | +4.2% |

| Gasoline Stations | +0.9% | –2.1% |

| Furniture & Home Furnishings | –1.0% | –0.4% |

| Electronics & Appliances | +0.3% | +1.8% |

| Building Materials & Garden | +0.8% | +2.3% |

Key Signal

Control Group at 6-Month High: PCE Pointing to +0.2% Real Gain in February

The control group — ex-auto, gasoline, building materials, and food service sales — rose +0.4% in February, its strongest reading since August 2025. Combined with our estimate of services outlays, this points to a +0.6% nominal and +0.2% real increase in PCE for February. For Q1 as a whole, real consumer spending is tracking an annualized rate of approximately 1.5%, consistent with our previously published forecast. This metric feeds directly into the BEA’s GDP consumption estimate and is the single most important data point in the retail report for near-term GDP tracking.

Forces Shaping the Consumer Outlook

The February retail print is constructive at face value. However, three forces are converging to pressure consumer spending through the spring and into summer: the U.S./Israel war with Iran and the attendant energy price shock, continuing tariff passthrough into consumer goods prices, and a bifurcation in real income growth that is concentrating spending gains at the upper end of the income distribution. Recent financial market volatility and disruptions around spring break travel may also sideline some discretionary spending by upper-income households in the near term.

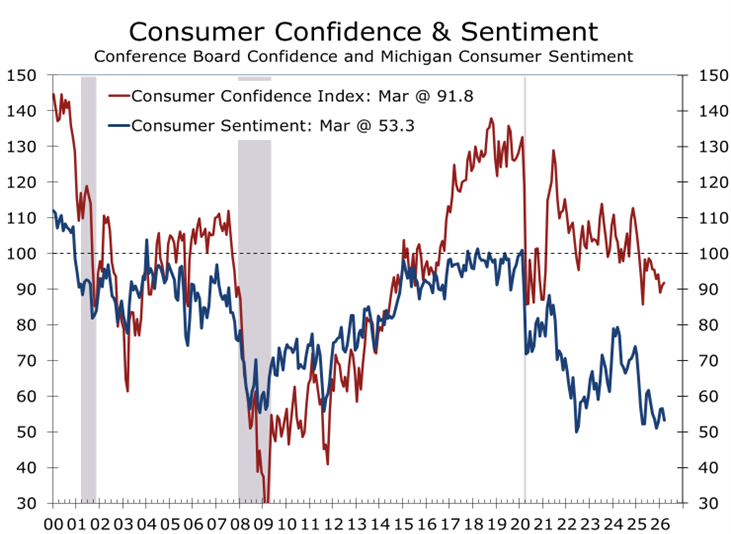

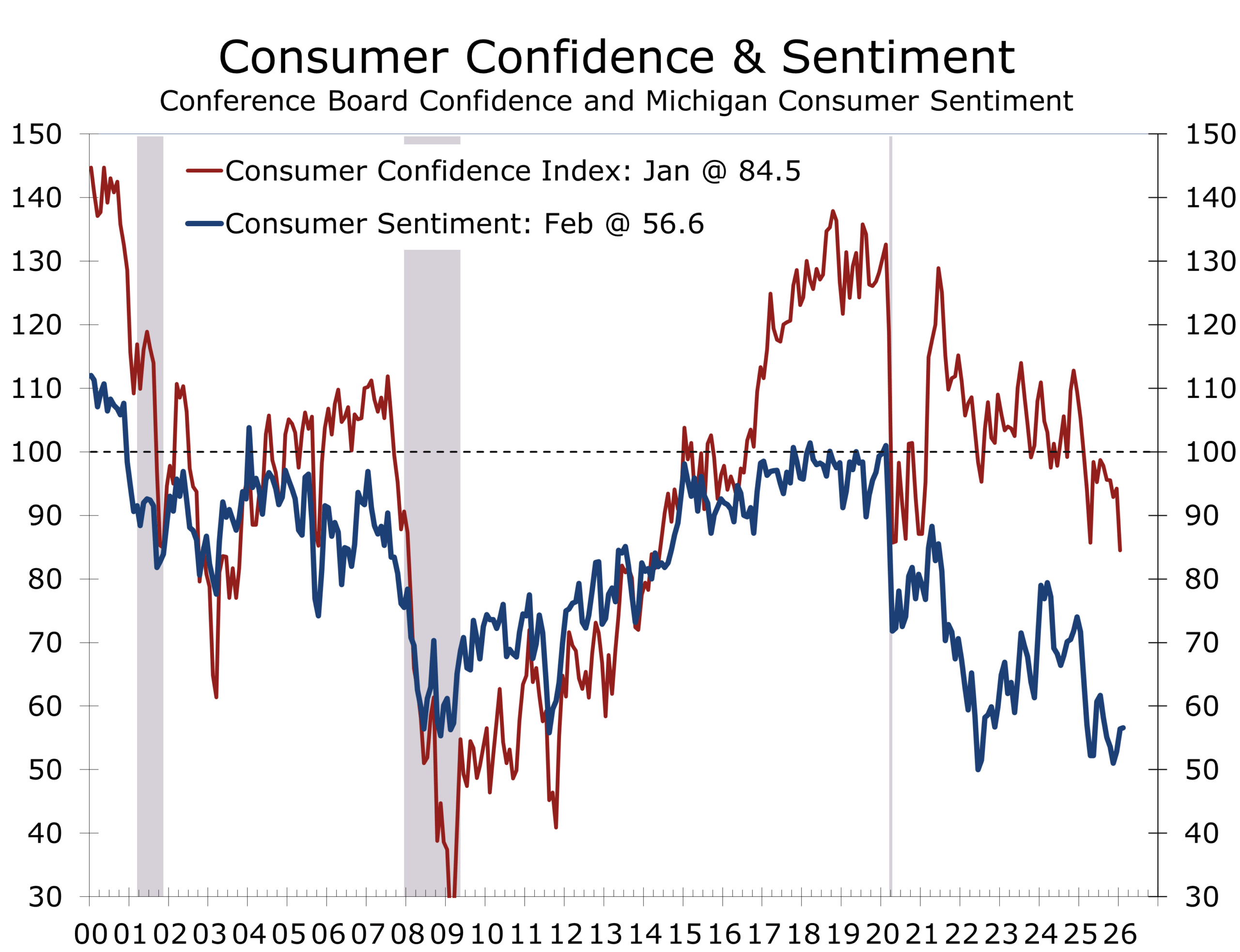

Consumer confidence data presents a mixed picture. The University of Michigan Consumer Sentiment Index has plummeted in recent months, while the Conference Board Consumer Confidence measure has shown more resilience. We suspect that concerns about rising gasoline prices and uncertainty about what the war’s implications for supply chains and inflation will weigh on actual spending this spring, even among households whose balance sheets remain relatively healthy.

The War with Iran: A More Immediate Risk to Consumer Spending

The U.S./Israel war with Iran introduces a risk that is more immediate in its consumer spending impact than tariff pressures. Gas prices averaged approximately 75 cents per gallon higher in March compared to February — a swift, regressive increase in household energy costs. Higher energy prices should become evident in the March retail sales data, with spending on durable goods and discretionary services bearing the brunt of the adjustment. We left our consumption forecast unchanged, however, as we had already assumed a substantial pullback in spending would take hold in March and persist through much of the second quarter.

The near-term impact is cushioned by a powerful, if unusual, buffer: income tax refunds. Refund issuance is running approximately +12.5% YoY through late March, a notable departure from the typical pattern in which the YoY increase peaks early in the filing season and then fades. The One Big Beautiful Budget Act is expected to generate a jump in refund issuance of approximately 20% for the full year. Crucially, the increase is occurring more gradually than usual, meaning a disproportionate share will accrue to upper-income households who tend to file later in the season.

| Risk Factor

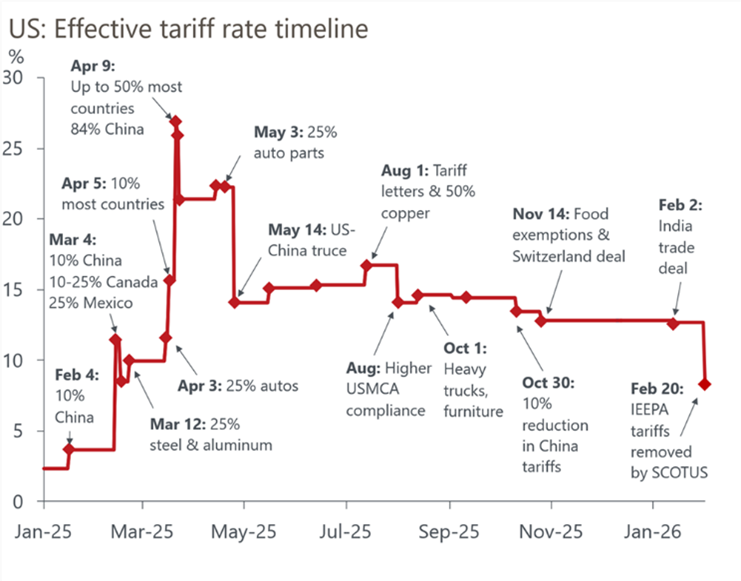

War and Tariffs: Twin Pressures Compressing Real Spending Power Import prices jumped +1.3% in February 2026 — the largest monthly increase since March 2022 — even before the Iranian war’s energy price shock has fully registered. Gasoline prices will likely remain elevated through Memorial Day, weighing on consumer spending through at least mid-Q2. The Yale Budget Lab estimates current tariffs represent a 9.8–13.7 percentage point increase in the effective U.S. tariff rate, the highest since 1941, creating an effective cost burden of $600–$1,300 per household annually. Lower-income cohorts bear approximately three times the proportional tariff burden of top-decile earners, underscoring the regressive nature of the combined energy and trade policy shock. |

The Tax Refund Buffer: Buying Time, Not Immunity

The unusual pattern of tax refund issuance is central to understanding why consumer spending has held up despite sharply deteriorating sentiment and rising energy costs. In a typical year, the YoY increase in cumulative refund issuance peaks early in the filing season — when lower-income households, who tend to file first, receive their refunds — and then gradually fades. In 2026, the opposite is occurring: the YoY increase has been rising through late March, reaching approximately +12.5% compared to the same period in 2025.

This pattern has significant distributional implications. A disproportionate share of the 2026 refund increase will accrue to upper-income households who file later in the season. The One Big Beautiful Budget Act created a structural increase in refund issuance estimated at approximately 20% for the full year. Higher-income filers receiving larger-than-normal refunds is providing support for spending in premium retail and warehouse-club formats even as lower-income cohorts face simultaneous tariff, energy price, and food inflation pressures. This dynamic reinforces the K-shaped character of the current consumer environment: aggregate spending metrics hold up reasonably well, while conditions for a large share of American households are materially more difficult.

The structural shift toward e-commerce continues to shape the distribution of retail gains. Nonstore retailers posted +10.9% YoY growth in the latest reading, maintaining substantial outperformance over brick-and-mortar formats. Q4 2025 e-commerce reached $316.1 billion seasonally adjusted — equivalent to 16.6% of total retail sales, up from 15.8% a year earlier. This channel shift has important implications for commercial real estate, logistics infrastructure, and labor demand across the retail sector.

| Structural Context

E-Commerce and Income Bifurcation Are Reshaping the Retail Landscape Full-year 2025 U.S. e-commerce totaled approximately $1.23 trillion, up +5.4% from 2024. NRF data indicate that the top 10% of earners now account for approximately 50% of all U.S. consumer spending. Clothing (+1.5% MoM) and health and personal care (+1.7% MoM) led the February gains, categories that skew toward higher-income consumers. Meanwhile, furniture (–1.0% MoM) and grocery stores (–0.3% MoM) — categories more broadly consumed across the income distribution — were the only segments to register outright declines. These divergences will likely widen as the energy price shock from the war with Iran takes hold in coming months. |

Conclusion: Consumer Resilience in a Crosscurrent Environment

The February 2026 Advance Retail Sales report underscores the fundamental resilience that has characterized U.S. consumer spending throughout this economic cycle. A broad-based +0.6% headline gain, a six-month high in the control group measure, and an Oxford Economics PCE nowcast pointing to +0.2% real consumer spending growth confirm that the January weakness was weather-driven rather than structural. The consumer entered the spring in solid shape.

Our assessment of Q1 GDP and the near-term outlook remains constructive. Real PCE is tracking a 1.5% annualized rate in Q1 2026, consistent with our previously published forecast, and underpins our Q1 real GDP forecast of 2.0% annualized. We expect growth to strengthen modestly in Q2 as the tax refund buffer continues to support upper-income spending, and we look for the economy to end 2026 with solid momentum as energy prices gradually recede and real incomes recover.

| Never Underestimate the American Consumer

“The American consumer has repeatedly defied expectations of a meaningful slowdown. Despite declining sentiment, rising energy costs, and the cumulative weight of tariff-driven price increases, aggregate spending has remained positive. February’s broad-based rebound reinforces our view that the structural foundation of consumer spending — employment, income growth, and household net worth — remains sufficiently intact to sustain positive growth through 2026.” — Mark P. Vitner, Chief Economist, Piedmont Crescent Capital |

Three considerations shape our near-term outlook. First, the energy price shock from the war with Iran will be visible in the March retail data, and we expect it to restrain discretionary spending through at least Memorial Day. Second, the tax refund buffer — while real and meaningful — is a stock rather than a flow; once deployed, households will face the underlying pressures of elevated goods prices and rising energy costs without this cushion. Third, the coincidence of tariff passthrough and energy inflation creates a compounding price burden that falls most heavily on lower- and middle-income consumers, limiting the breadth of any spending recovery.

| The Economy Keeps Chugging Along, Despite Significant Drags from the War and Tariffs

“We are maintaining our forecast for Q1 real GDP growth of 2.0% annualized, supported by a 1.5% annualized gain in real consumer spending and 4.7% rise in business fixed investment. Looking ahead, we expect growth to strengthen modestly in Q2 as refund-supported spending by upper-income households partially offsets the energy price drag, and to build further into year-end as oil prices gradually recede and real household income growth resumes a more supportive trajectory. The full year is shaping up to be one of moderate but durable expansion.” — Mark P. Vitner, Chief Economist, Piedmont Crescent Capital |

Key data releases to monitor: March retail sales (April 16) will provide the first direct measure of the war’s impact on consumer spending; the Q1 GDP advance estimate (April 30) will confirm whether the February control group strength flowed through to final demand; April CPI will indicate the velocity of energy and goods price passthrough; and the Federal Reserve’s May communications will clarify whether policymakers intend to ‘look through’ the war- and tariff-driven inflation or respond to it.

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

April 1, 2026

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

April 1, 2026

Mark Vitner, Chief Economist

(704) 458-4000

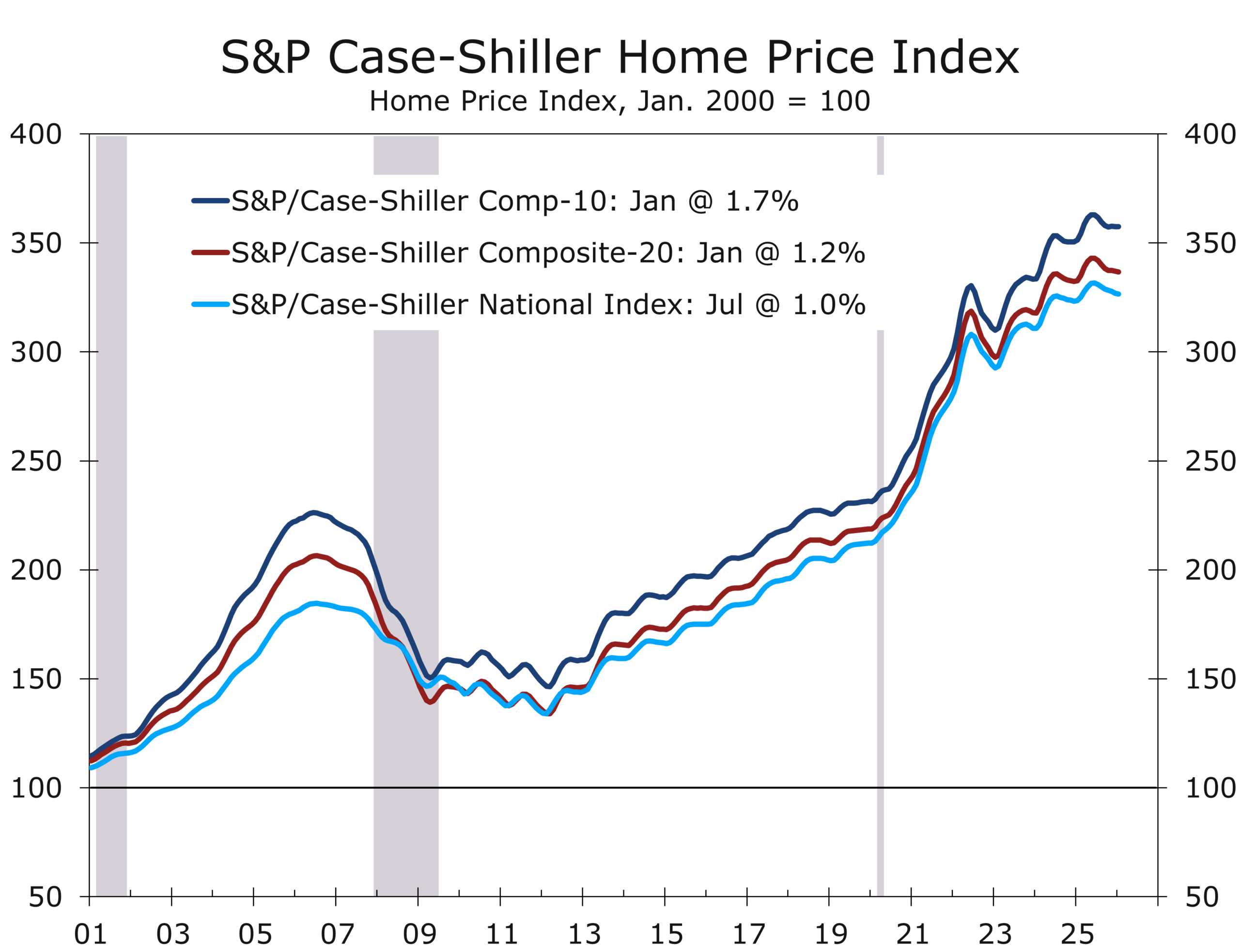

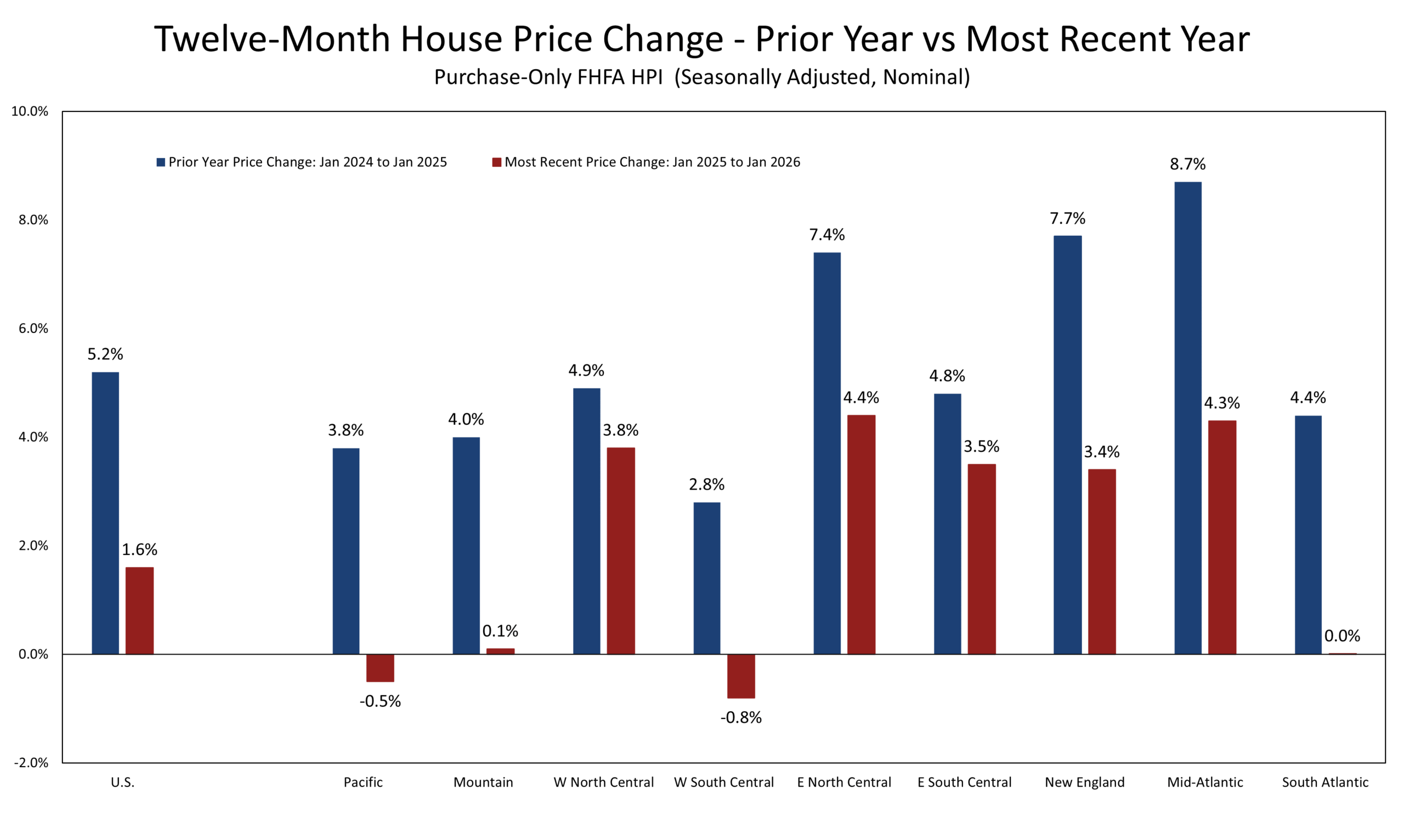

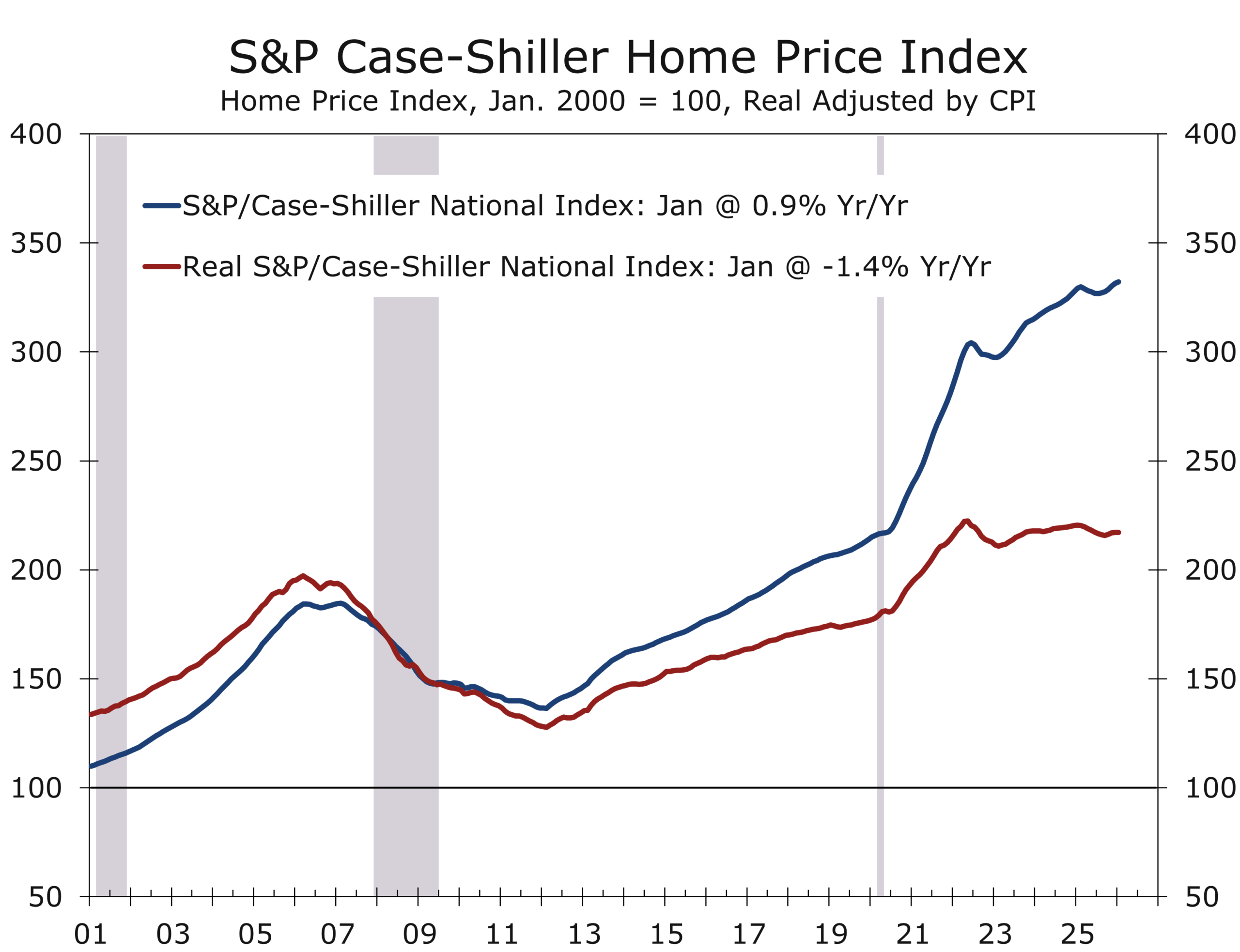

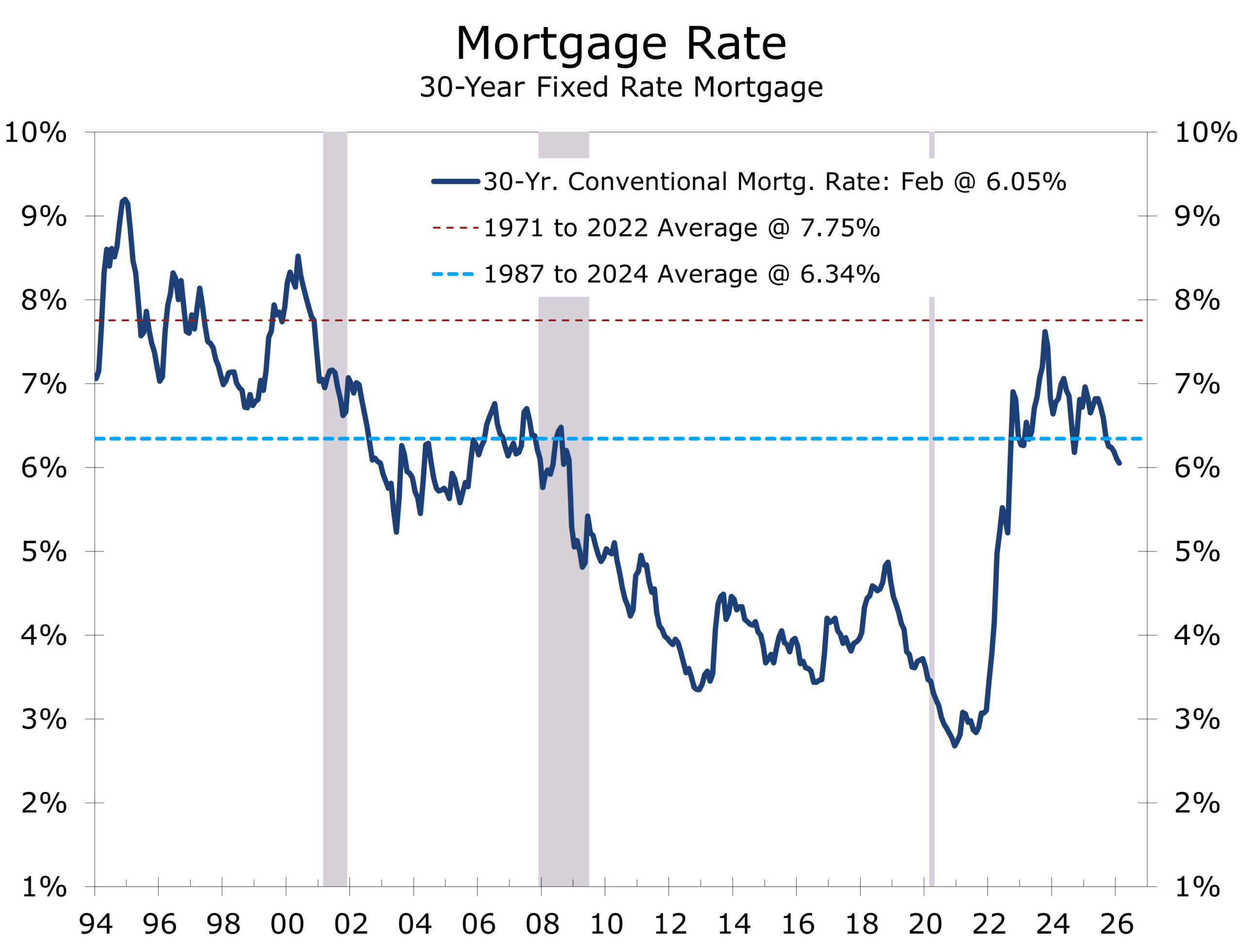

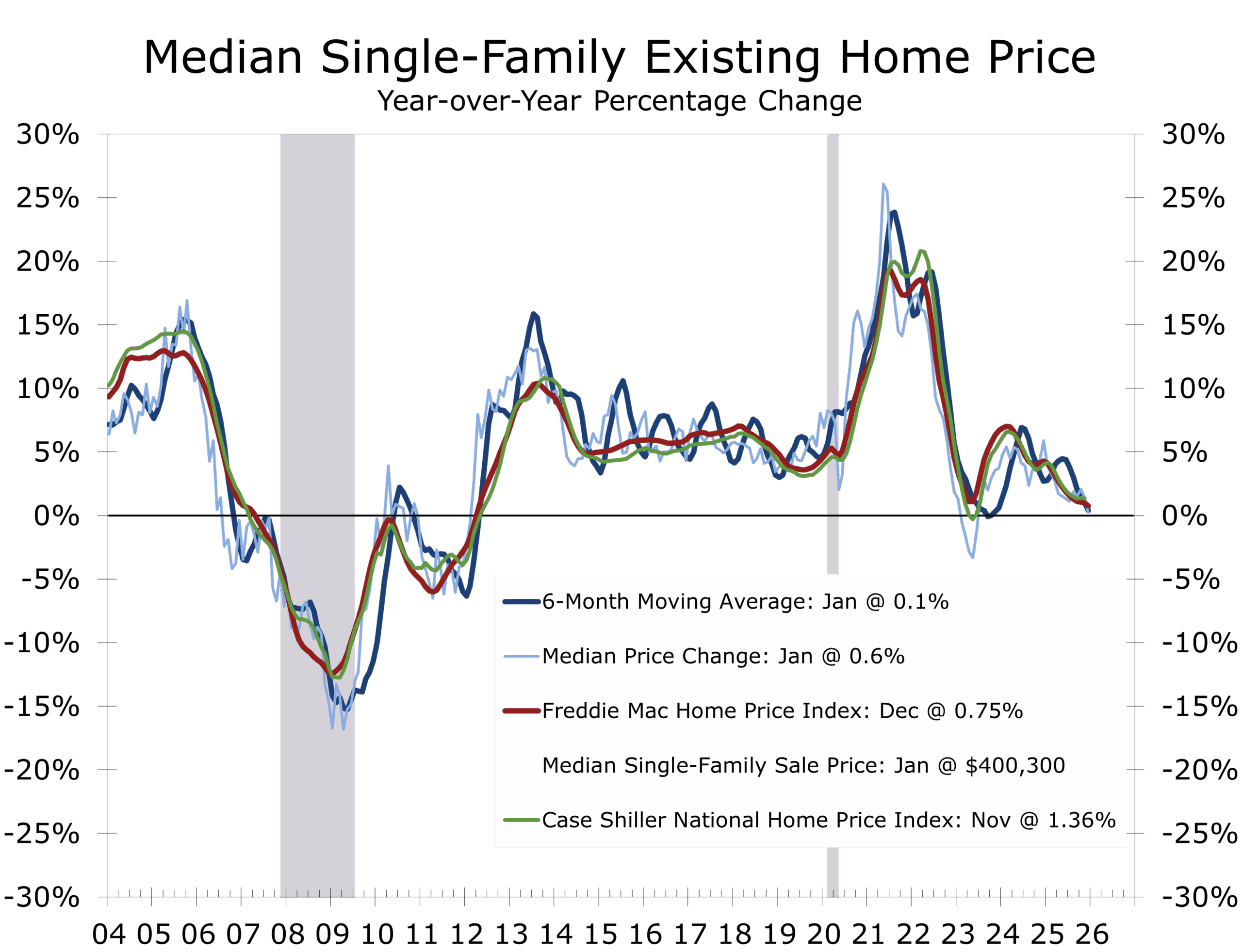

Home Prices: Losing Momentum, but Still Rising, and Splitting Along Regional Lines

Key Takeaways

-

- Home price appreciation continued to decelerate in early 2026, with both S&P CoreLogic Case-Shiller Home Price Index and FHFA House Price Index showing low-year-to-year single-digit gains.

- Monthly momentum is soft. Prices are drifting higher on a seasonally adjusted basis but slipping slightly on an unadjusted basis.

- Regional divergence has widened. The Midwest and Northeast are now leading, while several Sun Belt markets are flat to declining. Florida is a notable soft spot.

- Real home prices are falling modestly as inflation runs ahead of nominal appreciation.

- The housing market remains constrained by affordability. Higher mortgage rates are offsetting any benefit from slower price growth.

Price Growth Is Positive, But Fading

January’s data reinforces a theme that has been building for several quarters: the housing market has cooled but the overall supply of homes for sale remains tight, which is supporting home prices.

The S&P CoreLogic Case-Shiller Home Price Index rose 0.9% year over year in January, down from 1.1% in December. The 10-city and 20-city composites slowed to 1.7% and 1.2%, respectively. The FHFA House Price Index showed a similar pattern, rising 1.6% year over year, with a modest 0.1% monthly gain.

The signal is clear. Home prices are still rising, but only marginally. The market has shifted from strong price appreciation to something closer to stall speed as demand remains constrained by affordability constraints and a weaker job market

Nominal home price appreciation has slowed enough that inflation is now outpacing home prices.

On a monthly basis, the Case-Shiller national index declined slightly on a non-seasonally adjusted basis and rose just 0.2% after seasonal adjustment. FHFA reported a similarly modest 0.1% increase.

This is not the profile of a market under stress. It is the profile of a market constrained to the point that it is stalling. Buyers are sensitive to monthly payments, not just prices, and the recent back up in mortgage rates has likely caused many would-be buyers to pause.

The result is a low-velocity market. Transactions are limited, inventories are gradually rising off historically low levels, and prices are drifting rather than moving decisively in either direction.

Regional Divergence Is Now the Defining Feature

Variations in regional price performance offer confirming evidence on the most recent Census data, which should population growth remaining strong Texas, the Mountain West and the Southeast, with the exception of Florida. The Midwest is showing more resilience, as housing is relatively more affordable compared to other regions. New York’s prices reflect the full return to the office amid a scarcity of homes available for sale.

In the Case-Shiller 20-city index, New York, Chicago, and Cleveland posted the strongest gains, while Tampa remained firmly negative year-over-year. Prices were flat or down in several formerly high-flying Sun Belt markets, including Phoenix, Dallas, and Seattle.

Leadership has shifted from Sun Belt hot spots to the Midwest, Northeast, and more affordable parts of the South.

FHFA’s regional data tell the same story. The East North Central division posted the strongest annual gains, while West South Central, which includes Texas, was negative. The East South Central, which includes Tennessee and Alabama, shows more resilience, however.

The pandemic-era leaders are no longer carrying the market. Instead, price growth has rotated toward regions where affordability remains less strained, and valuations did not overshoot as dramatically.

Real Prices Are Quietly Declining

With the CPI running above the pace of home price appreciation, inflation-adjusted values have edged lower over the past year. This marks a notable shift from the prior two years, when housing was a primary driver of household wealth gains.

Real home prices are declining modestly, even as nominal prices remain positive.

This adjustment is doing some of the work that outright nominal declines would otherwise accomplish. It is easing valuation pressures, albeit slowly and unevenly.

Despite the moderation in price growth, affordability has not meaningfully improved. Mortgage rates remain elevated, and in recent weeks have moved higher alongside Treasury yields. That keeps monthly payments high and limits the pool of qualified buyers.

This dynamic explains why slower price growth has not translated into stronger activity. The constraint is not price levels alone, but the cost of financing those prices. The market is caught between two forces: limited supply from rate-locked homeowners and constrained demand from payment-sensitive buyers.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

March 31, 2026

Mark Vitner, Chief Economist

(704) 458-4000

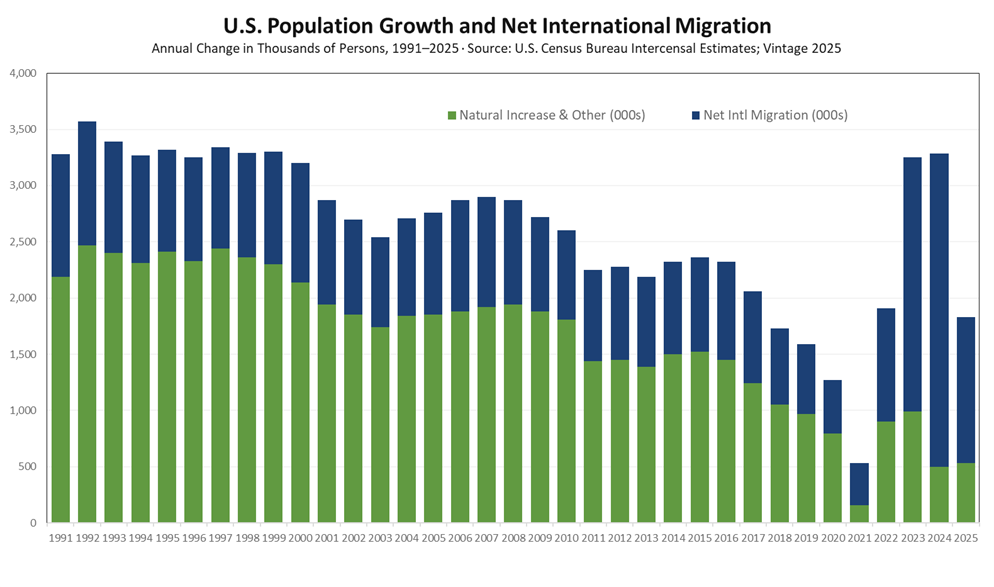

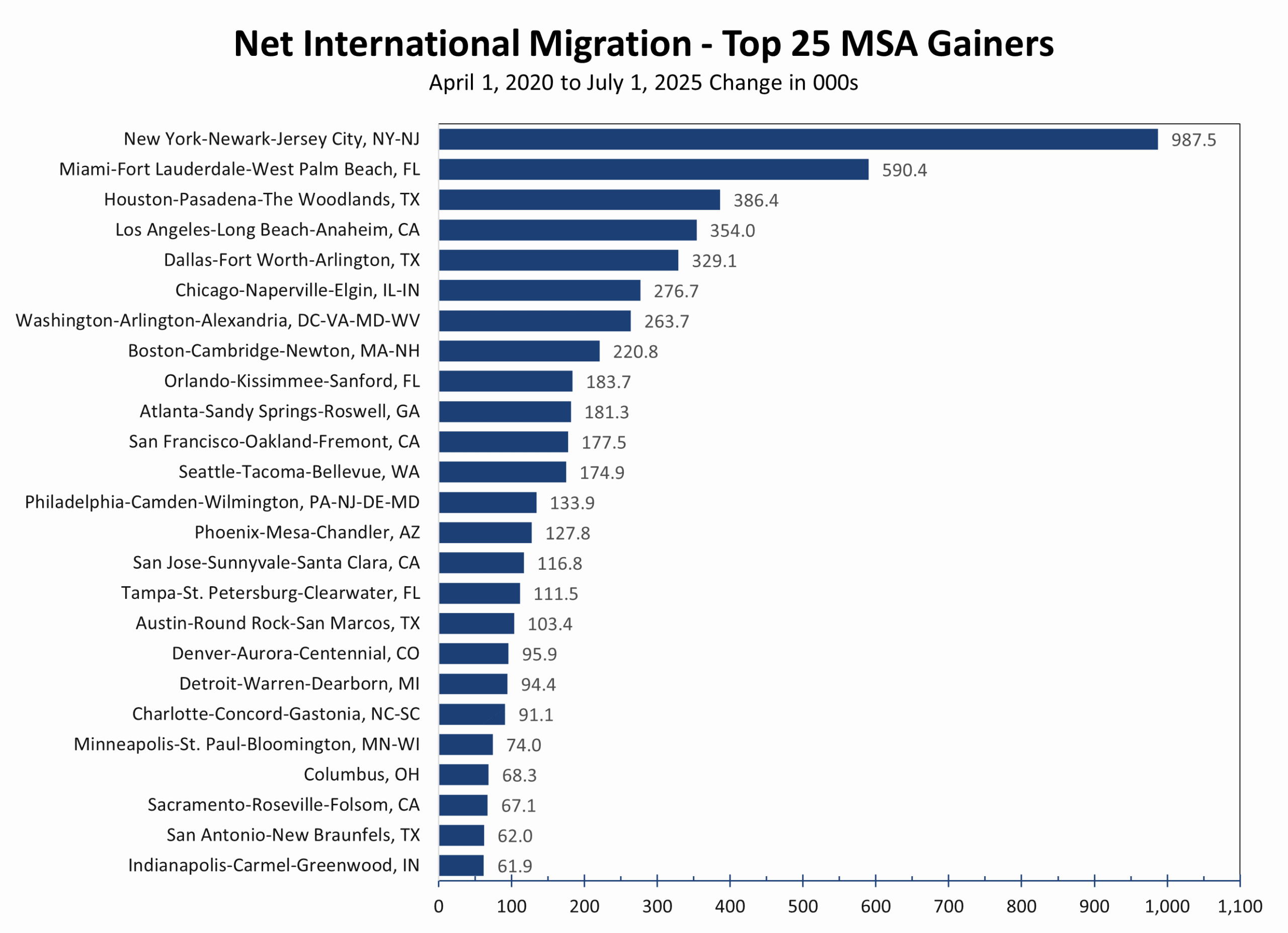

A Breaking Population Wave: MSA Population Growth in 2024–25: Overall Deceleration, the Immigration Inflection, and a Historic Redistribution of Wealth

Key Takeaways

- Metro Growth Rate: Fell from 1.1% (2023–24) to 0.6% (2024–25) — the sharpest single-year deceleration of the post-pandemic period, with metros adding only 1.7M residents vs. ~3.2M the prior year.

- Top Numeric Gainers: Houston, Dallas-Fort Worth, Atlanta, Phoenix, Charlotte — all in the South/Sun Belt corridor. Texas alone claimed four of the top nine metros by numeric gain..

- Top % Growth: Ocala, Myrtle Beach, Spartanburg, Lakeland, Punta Gorda, Huntsville — smaller markets riding domestic inflows as primary Sun Belt hubs fill in and costs rise..

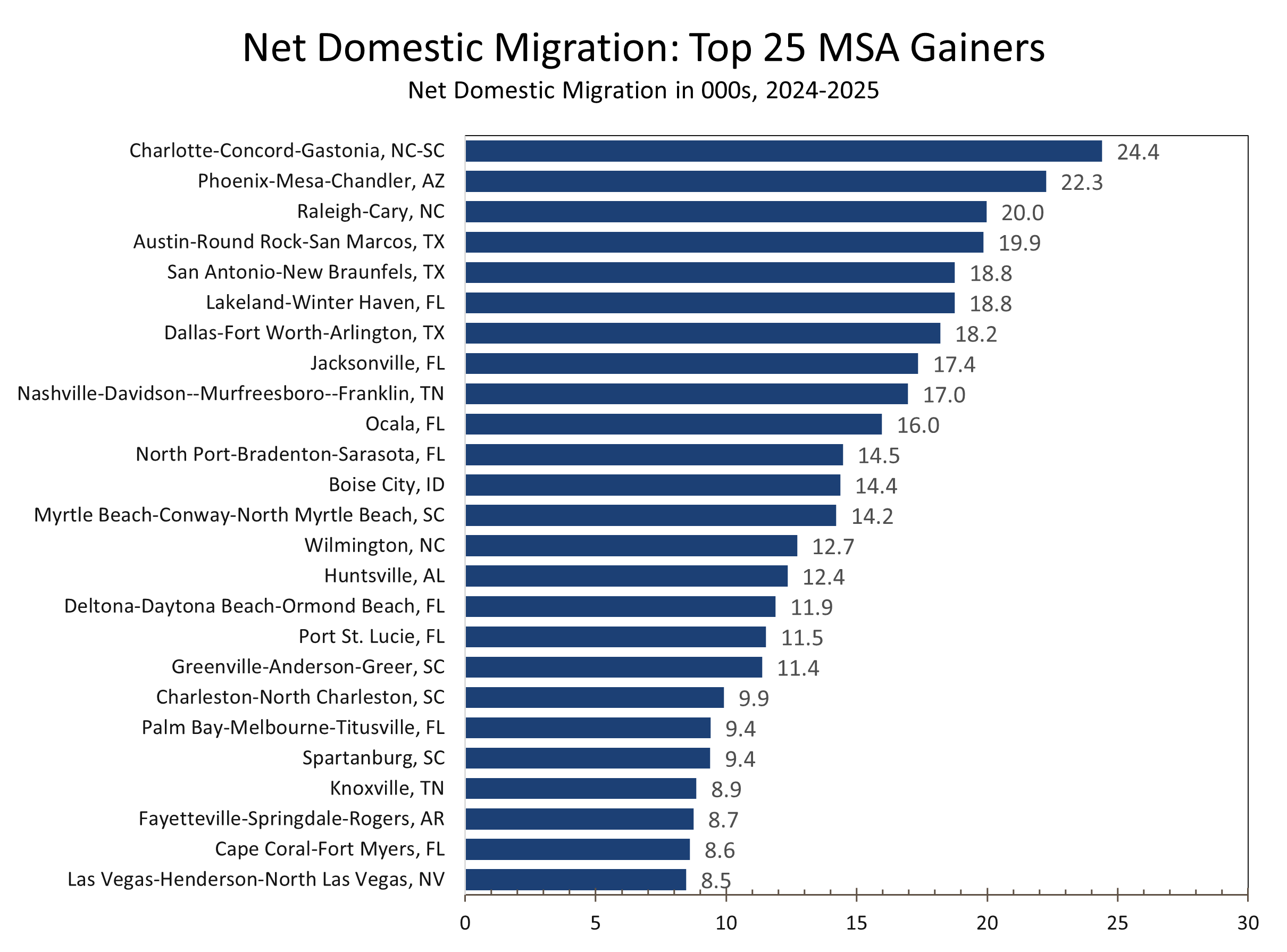

- Domestic Migration: Charlotte led all 387 MSAs in net domestic in-migration; Phoenix, Raleigh, Austin, San Antonio follow. NC ranked 3rd nationally in IRS net migration (79,317 individuals on 40,999 returns).

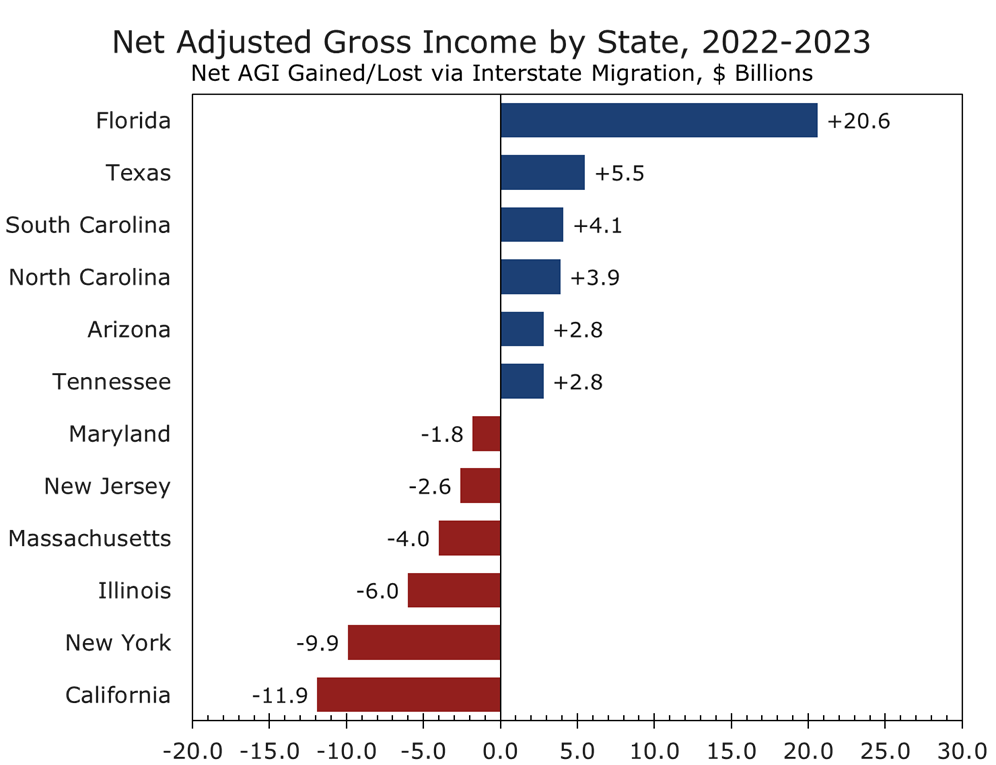

- Wealth Redistribution: IRS data confirm this is not just a headcount story: NC gained $3.9B and SC gained $4.1B in net AGI in 2022–23. The Carolinas combined captured $8.0B — trailing only Florida and Texas. NY lost $9.9B. CA lost $11.9B..

- Gateway Metros: Los Angeles, Miami-Dade, and the NYC metro are losing population or stagnating as immigration recedes. New York fell from 1st to 13th in numeric gains in a single year..

- Border MSAs: Laredo (3.2%→0.2%), Yuma (3.3%→1.4%), El Centro (1.2%→-0.7%) — sharpest growth-rate collapses; these border markets lead the national immigration trend by 6–12 months.

- Piedmont Corridor: Charlotte, Raleigh-Durham, and the resurging Piedmont Triad form one of the most durable growth corridors in the Southeast, confirmed by both Census headcount and IRS income-flow data.

- Key Risk: Nine of ten U.S. counties recorded lower net international migration in 2024–25. The trend is accelerating under the current enforcement policy and will take 12–24 months to fully manifest.

Data Note: This report draws on two complementary datasets released in March 2026: (1) U.S. Census Bureau Vintage 2025 population estimates, which measure headcount migration through July 2025; and (2) IRS Statistics of Income (SOI) Migration Data for Filing Year 2022–2023, which captures AGI flows, household counts, and migrant age profiles. Together they provide both the current population trajectory and the income quality of the migration.

The Wave Has Broken

Population growth is among the most consequential first-order economic variables in any analytical framework. It shapes labor supply, household formation, and long-run consumer demand. The latest Census Bureau data (the Vintage 2025 estimates released in March 2026) make three things clear: the post-pandemic surge in metropolitan area growth is over, the deceleration is broad-based, and the geography of American expansion is narrowing. The IRS’s newly released migration data for 2022–23 reveal a crucial second dimension: the people who are moving are not a random cross-section of the population. They are disproportionately working-age and above-median income — and where they go, economic capacity follows.

Metro areas as a whole grew 0.6% between July 2024 and July 2025, exactly half the 1.1% rate recorded in the prior year. In absolute terms, U.S. metros added roughly 1.7 million residents, down from nearly 3.2 million the year before. That comparison captures the scale of the deceleration. Growth did not just slow; it was cut in half.

| 0.6%

Metro area population growth rate, 2024–25 — half the prior year’s 1.1% pace |

1.7M

Net new metro residents added in 2024–25, down from 3.2M the prior year |

The proximate cause is well-documented: net international migration (NIM) collapsed. Nine out of ten U.S. counties recorded lower NIM in 2024–25 than in 2023–24; the remaining tenth saw essentially no increase. The Biden administration began tightening border security in the second half of 2024, and enforcement tightened considerably further under President Trump. Border metros felt it first and most acutely, but the effect has radiated outward to nearly every major immigration hub in the country.

What makes this cycle particularly instructive is the contrast with 2023–24. That year, post-pandemic normalization of global mobility produced an unusually large immigration surge — approximately 2.7 million net international migrants flowing into metro areas alone. That surge temporarily reversed population losses in several major gateway metros that had been bleeding residents for years. New York, Los Angeles, Chicago, San Francisco, Washington, Miami: all posted gains. For many, that story read like a comeback. It was not. The reprieve was a temporary bridge, and that bridge has now been removed.

What lies beneath that bridge is the structural reality many large gateway cities had been deferring: persistent domestic outmigration that immigration was masking but not curing.

Three Forces, One Direction

Population change in any MSA is the arithmetic sum of three components: net international migration, net domestic migration, and natural increase (births minus deaths). Understanding 2024–25 requires understanding what each is doing — and why the balance has shifted so decisively.

International Migration: The Dominant Variable, Now Contracting

NIM has been the swing factor in U.S. metro growth since the pandemic ended. Its rise from 2022 to 2024 inflated national growth rates and masked divergences between metros that were organically healthy and those merely benefiting from their geography as immigrant entry points.

The contraction now underway is structural, not cyclical. Tighter border enforcement has reduced new arrivals. Elevated deportation activity and the chilling effect on would-be migrants compound this. The Census Bureau’s own demographers flagged border metros as the clearest leading indicator: Laredo’s growth rate fell from 3.2% to 0.2% in a single year. Yuma dropped from 3.3% to 1.4%. El Centro went negative at -0.7%. These are not rounding errors — they are collapses.

| Border Metro Collapse: A Leading Indicator

The three sharpest single-year growth-rate declines among all U.S. MSAs are in border communities: Laredo (−3.0 ppts), Yuma (−1.9 ppts), and El Centro (−1.9 ppts, now shrinking). These markets lead the national trend by 6–12 months. What is happening at the border today will be visible in gateway metro data by mid-2026. |

Gateway metros saw the same dynamic play out at larger scale. Miami-Dade — the second-largest county gainer in the entire country in 2023–24 — lost more than 10,000 residents in 2024–25. Many residents are simply moving to other parts of South Florida, however, particularly Broward and Palm Beach counties. Los Angeles County continued its decade-long decline. New York City, which had briefly re-entered growth mode on immigration inflows, resumed contraction. The data reflect only the early phase of tighter enforcement; the full effect will take 12 to 24 months to fully manifest.

One facet of immigration often overlooked — and that is essential for correctly reading the domestic migration data in the next section — is that a person is counted as an immigrant when they first relocate to the country. When they subsequently move from their initial landing spot (typically one of the nation’s largest gateway cities) they appear in the data as a domestic out-migrant from that area. This secondary dispersal is one reason most large gateway metros have recorded persistent domestic outflows even during periods of strong overall immigration. It also means the domestic outmigration figures for cities like New York and Los Angeles understate the degree to which those metros’ populations have become dependent on continuous fresh immigration just to hold their footing.

Domestic Migration: Where the Real Votes Are Cast — and the Money Follows

Net domestic migration is one of the most revealing signals in demographic data. It reflects active, discretionary decisions by households, people choosing to leave one place and move to another. It responds to wages, housing costs, tax burdens, labor market conditions, and quality of life. And as the newly released IRS data make clear, what is migrating is not just population — it is purchasing power, tax base, and entrepreneurial capital.

The Census Bureau counts tell part of the story: the country’s fifty most populous counties collectively lost 637,634 residents to domestic outmigration in 2024–25. But the IRS data for 2022–23 tell us what those people earned. California lost $11.9 billion in net adjusted gross income (AGI) to outmigration — the largest income loss of any state. New York lost $9.9 billion. Illinois shed $6.0 billion. Massachusetts lost $4.0 billion. New Jersey, $2.6 billion. These are not budget rounding errors; they are structural fiscal wounds that compound annually.

| -$11.9B

California net AGI lost to outmigration, 2022–23 |

-$9.9B

New York net AGI lost to outmigration, 2022–23 |

| -$6.0B

Illinois net AGI lost to outmigration, 2022–23 |

-$4.0B

Massachusetts net AGI lost to outmigration, 2022–23 |

On the receiving end of these flows, the picture is equally clear. Florida gained $20.6 billion in net AGI — the largest income gain of any state. Texas gained $5.5 billion. North Carolina gained $3.9 billion, and neighboring South Carolina added $4.1 billion. Tennessee captured $2.8 billion. Arizona gained $2.8 billion. The directional pattern is consistent, persistent, and policy-linked: states with lower tax burdens, more competitive regulatory environments, and a more cooperative relationship between business, government, and labor are capturing income, investment capital, and the entrepreneurial activity that accompanies high-earning households.

| +$20.6B

Florida net AGI gained from in-migration, 2022–23 |

+$5.5B

Texas net AGI gained from in-migration, 2022–23 |

| +$4.1B

South Carolina net AGI gained, 2022–23 |

+$3.9B

North Carolina net AGI gained, 2022–23 |

Massachusetts offers a particularly instructive case study in policy-driven migration. In 2022, the state enacted a 4% tax surcharge on income exceeding $1 million, raising its top marginal rate to 9%. In the subsequent filing year, taxpayers earning more than $200,000 accounted for 70% of the state’s net outflows — roughly double their share in 2019. New Hampshire, the state’s zero-income-tax neighbor, captured nearly $900 million of that income directly from former Massachusetts filers. Washington state offers a comparable cautionary tale: after enacting a 7% capital gains tax in 2021, the state shifted from being one of the country’s largest income gainers to recording a net outflow of approximately $500 million in 2022–23.

| The High-Earner Flight Premium

Among taxpayers with $200,000 or more in AGI, the most attractive destination states in 2021–22 were Florida, Texas, North Carolina, South Carolina, and Arizona. The least attractive: California, New York, Illinois, Massachusetts, and New Jersey. Florida alone gained 29,771 affluent filers in a single year — adding $28.7 billion to its AGI base. California lost 24,670 of them, removing $16.1 billion. The migration of high earners is not incidental to the reallocation; it is the dominant driver of it. |

Charlotte led all 387 metro areas in net domestic in-migration in the Census data. The IRS data provide the income context behind that ranking. North Carolina ranked third nationally in net IRS migration with 79,317 individuals on 40,999 returns in 2022–23, trailing only Florida and Texas. Critically, 55.4% of those arriving in North Carolina were between the ages of 26 and 44 — prime working-age, household-formation years. These are not retirees or students; they are earners, spenders, and taxpayers arriving in concentrated form. This age and income profile makes North Carolina an unusually attractive destination for employers seeking skilled labor in a tight market, and for builders and retailers tracking where household formation demand will concentrate over the next decade.

Natural Increase: Stabilizing, Not Driving

Natural increase (the excess of births over deaths) contributed roughly 614,000 to metro population in 2024–25. That figure has improved from the pandemic low, when mortality spiked and fertility was suppressed. But approximately 65% of U.S. counties still experience natural decrease — more deaths than births — reflecting the ongoing aging of the baby boom cohort. Natural increase can pad the growth calculation; it is not the engine.

| Natural Increase: A Floor, Not an Engine

65% of U.S. counties record more deaths than births annually — a figure that has held steady for three consecutive years. Natural increase contributes roughly 614,000 metro residents per year nationally, cushioning the deceleration but unable to offset the loss of 2+ million in annual NIM. The math improves with younger in-migrant populations, which is precisely why the IRS age data matters: domestic migration destinations are receiving disproportionately young, working-age arrivals who will improve natural increase over time. |

Where Growth Is Actually Occurring – Absolute Leaders: Scale Compounds

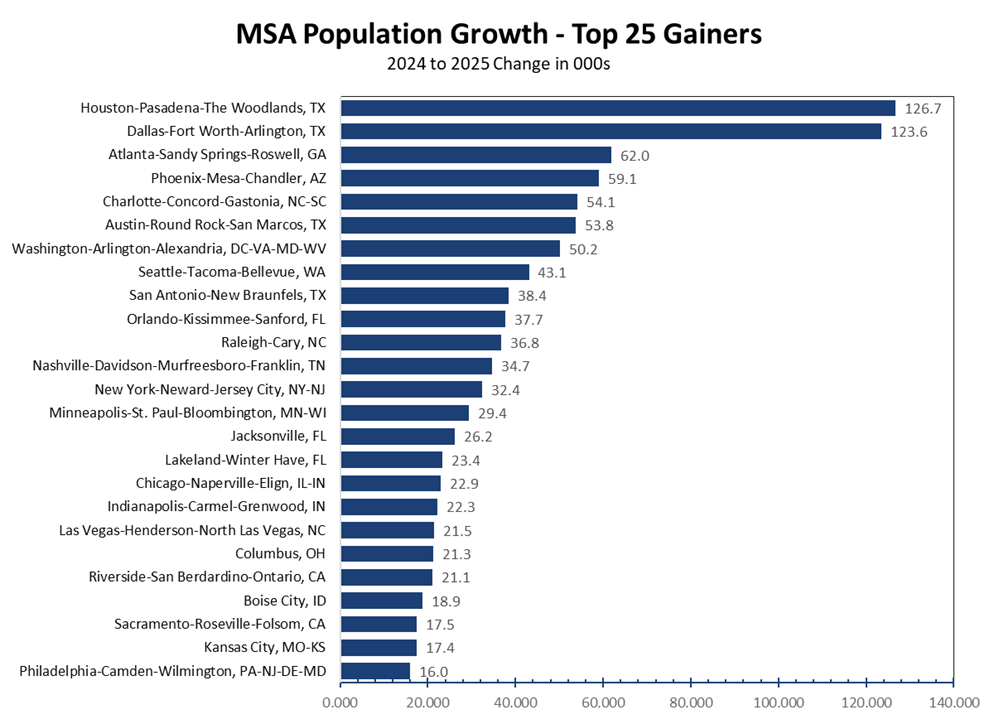

In terms of raw numeric growth, the top MSAs reinforce a now-familiar hierarchy. Houston led all metro areas in 2024–25, followed by Dallas-Fort Worth, Atlanta, Phoenix, and Charlotte. Together, these five markets account for a disproportionate share of net new metro population, and Texas alone had four of the top nine fastest-growing metros by population.

Houston deserves particular mention. It is one of the few large metros where international migration remains robust even as the national trend weakens: a reflection of its longstanding role as a major immigrant destination tied to energy, medicine, and international trade. That combination of strong domestic inflows and continued immigration makes Houston’s growth profile more resilient than most peers at its scale.

Dallas-Fort Worth continues its trajectory as one of the great economic absorbers of the American economy, drawing corporate relocations, logistics investment, and a steady stream of working-age migrants from the coasts. Dallas has been the biggest winner from the out-migration of businesses from California, with more choosing to locate in the greater Dallas area than any other metro in the U.S.

The suburbs around Dallas are booming. Princeton, Texas, grew its population by nearly one-third in a single year. Forney, Texas (21 miles from downtown Dallas) has more than 25,000 future residential lots in the pipeline. The IRS data reinforce why: Texas gained $5.5 billion in net AGI in 2022–23, and among high-income filers nationally it ranked as the second-most-attractive destination in the country.

Percentage Leaders: Where Momentum Is Building

Percentage growth leaders tend to be smaller markets where a modest population base amplifies migration impact. Ocala, Florida and Myrtle Beach-Conway, South Carolina led all metros in growth rate — both driven overwhelmingly by domestic in-migration. Spartanburg, Lakeland, Punta Gorda, and Huntsville round out the fastest-growing tier. Retirees account for much of the growth in Ocala, Myrtle Beach, Lakeland, and Punta Gorda; in Spartanburg and Huntsville, however, industrial development is the primary driver: a distinction with meaningfully different long-run economic implications.

All these markets share several traits: proximity to larger metros, housing availability, lower costs of living, and in some cases proximity to military or industrial employment anchors. They represent the overflow valve from the larger Sun Belt hubs as prices rise and supply tightens in primary markets. The IRS data confirm that secondary Sun Belt markets are not just receiving people — they are receiving migrants with the same income profile as those heading to larger neighbors, but at a lower cost basis. The investor implication is less the growth rate itself and more what it signals about the diffusion of demand across regional secondary markets.

A note on Florida: hurricanes Helene and Milton complicated the state’s demographic picture in 2024–25. Pinellas County lost nearly 12,000 residents — the second-largest numeric decline in the country — as storm displacement compounded an already difficult demographic structure (deaths exceed births in Pinellas by the widest margin of any U.S. county). The Miami metro posted a 0.1% population decline. Twenty of Florida’s twenty-two metros still grew, but the hurricane effect is a reminder that the state’s story is more layered than it appears. Rising insurance costs are causing some potential migrants to re-evaluate Florida alternatives in neighboring states, most directly South Carolina and Georgia. Notably, Florida’s $20.6 billion net AGI gain in the IRS data predates these storms — the state’s income attraction fundamentals remain intact, but the geographic distribution of that attraction is shifting.

| Florida: Two Stories in One State

Hurricane displacement subtracted an estimated 15,000–20,000 residents from Southwest Florida in 2024–25 — a disruption that is partly temporary, but whose insurance cost aftermath is structural. Investors should disaggregate storm-affected coastal counties (Pinellas, Charlotte, Sarasota, Lee) from inland and Northeast Florida, which continued growing normally. Miami-Dade’s decline is immigration-driven, not weather-related: a distinction with materially different long-term implications. |

The Piedmont Corridor: Charlotte, Raleigh, and a Rising Third Node

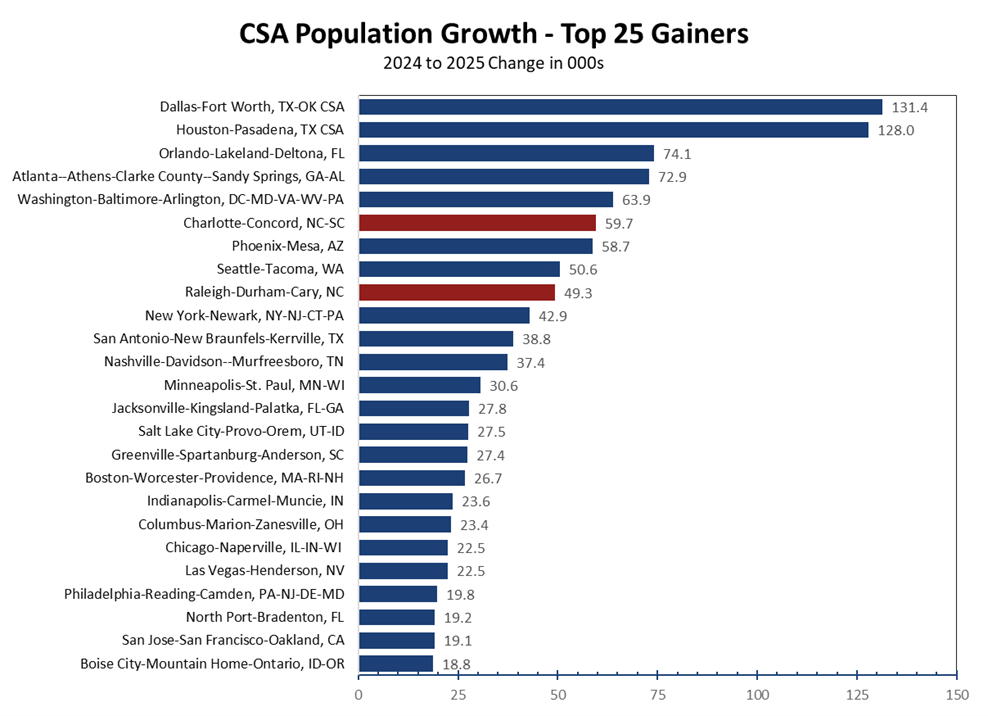

No region better illustrates the intersection of scale and momentum than the Piedmont Crescent — the arc connecting Charlotte and Raleigh-Durham across central North Carolina. Both metros are performing at the top of national rankings on multiple dimensions simultaneously, and a third node is emerging between them. Critically, this outperformance is confirmed by two independent data sources: the Census Bureau’s population counts and the IRS’s income-flow data point in exactly the same direction.

Charlotte: The Migration Leader — in Headcount and Income

Charlotte’s leadership in net domestic migration is not a surprise to anyone who has watched the region’s corporate development pipeline, but the breadth of inflows is worth emphasizing. Households are arriving from the Northeast, neighboring states, the Midwest, and the West Coast. The IRS data confirm that North Carolina’s in-migrants skew young and working-age: 55.4% of individuals moving to NC in 2022–23 were between 26 and 44 years old, compared to just under 50% for Florida and South Carolina. This age profile matters for long-run demand — it implies accelerating household formation, rising school enrollment, and a tax base that will compound for decades.

| Charlotte: The Convergence of Headcount and Income

Census data: #1 MSA nationally in net domestic migration, 2024–25. Lancaster County, SC: 2.7% growth rate — fastest of all 11 MSA counties. IRS data: NC ranked #3 nationally in net AGI gained ($3.9B); SC gained $4.1B — Carolinas combined $8.0B, trailing only FL and TX. Age profile: 55.4% of NC in-migrants aged 26–44 — highest working-age share among top destination states. Employment: Charlotte nonfarm payrolls +2.7% YoY through Nov 2025, adding ~37,800 net new jobs — outpacing Atlanta, Dallas-Fort Worth, and Miami. |

North Carolina as a whole ranked third nationally in IRS net migration with 79,317 individuals on 40,999 returns — and $3.9 billion in net AGI gained. Charlotte accounts for a disproportionate share of that figure. The region’s income attraction is not incidental; it is a function of its employment base. Charlotte remains the second-largest U.S. banking center, with Bank of America, Truist Financial, and several major domestic and foreign-bank regional operations anchoring a financial ecosystem that is expanding, not contracting.

Recent corporate commitments reinforce this trajectory. Capital Group’s planned East Coast hub will create approximately 600 jobs. Scout Motors selected Charlotte for its new corporate headquarters, expected to generate roughly 1,200 positions. These additions build on a formidable established base: Charlotte is home to seven Fortune 500 companies (Bank of America, Lowe’s, Honeywell, Nucor, Duke Energy, Truist, and Sonic Automotive) and nineteen Fortune 1000 companies in total, including Ingersoll-Rand, Coca-Cola Consolidated, and Sealed Air, spanning financial services, energy, industrial manufacturing, specialty chemicals, and logistics. Few cities of Charlotte’s size can match the depth or diversification of that corporate roster. The Charlotte Douglas International Airport, which consistently ranks as one of the nation’s busiest by passenger traffic, is a major draw, as is the availability of skilled workers that continue to relocate to the area.

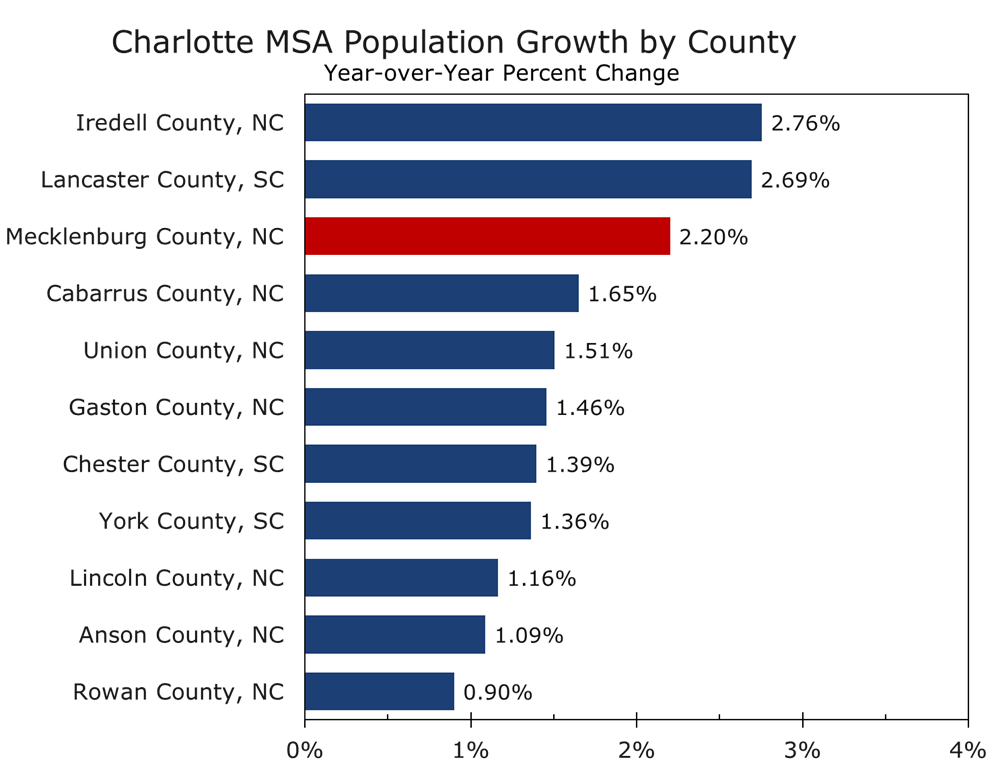

Charlotte also possesses a structural geographic advantage that peers lack. The final leg of Charlotte’s beltway, I-485, did not open until 2015, effectively unlocking vast tracts of land for development just as the national migration toward the Sun Belt accelerated. Unlike most metros that grow primarily in one direction, Charlotte expands in all four — and uniquely among major U.S. metros, it straddles a state line. The Charlotte-Concord-Gastonia MSA spans eleven counties across both North Carolina and South Carolina, and in 2024–25 it was the South Carolina counties that posted the fastest percentage gains within the metro.

Lancaster County, SC — anchored by the rapidly growing unincorporated community of Indian Land and a constellation of active adult and retirement communities — grew 2.7% in 2024–25, adding nearly 3,000 residents and recording the second fastest growth rate of any of the MSA’s eleven counties. York County, SC, home to Rock Hill and Fort Mill, has added approximately 25,000 residents since the 2020 Census. The pattern is consistent with what is seen across the Sun Belt: as core counties fill in and prices rise, growth cascades outward into adjacent counties with more land, lower costs, and direct access to the core employment base. Charlotte’s bi-state geography gives it an unusually wide spillover zone — and South Carolina’s competitive tax environment accelerates it.

The IRS data confirm this dynamic at the state level: South Carolina gained $4.1 billion in net AGI from in-migration in 2022–23, actually exceeding North Carolina’s $3.9 billion gain despite having a smaller population base. The Carolinas together captured $8.0 billion in net income from domestic migration in a single filing year — a combined figure that places this bi-state corridor among the most powerful wealth-attraction zones in the country, trailing only Florida and Texas. Markets that can build can sustain growth. The Charlotte metro, sprawling across two growth-oriented states, is building on both sides of the border.

Raleigh-Durham: The Innovation Anchor

A note on Census geography is warranted before discussing this region’s population dynamics. The Census Bureau defines the Raleigh-Durham area as two separate Metropolitan Statistical Areas: the Raleigh-Cary MSA (Wake and Johnston counties) and the Durham-Chapel Hill MSA (Durham, Orange, and Chatham counties). These are treated as distinct geographies in population tallies, which creates an analytical gap that can mislead: the two metros are highly economically integrated and are far better understood together. Research Triangle Park (the 7,000-acre research campus that is the region’s dominant employment hub) sits mostly in Durham County but extends into Wake County, physically straddling both MSAs. No serious economic analysis of the region treats the MSA boundary as a meaningful divide.

The more analytically useful geography is the Raleigh-Durham-Cary Combined Statistical Area (CSA) — a Census-defined framework that groups two or more adjacent MSAs with demonstrated economic and social linkages, as measured by commuting flows and employment ties. Where an MSA captures a single core urban area and its immediate labor shed, a CSA captures how multiple cores function as a single integrated regional economy. The Raleigh-Durham-Cary CSA encompasses Wake, Johnston, Durham, Orange, and Chatham counties, stretching roughly 60 miles from the northern edge of the Research Triangle to the southeastern suburbs of Johnston County, a crescent of rapidly growing communities connected by I-40, U.S. 1, and the regional rail corridor. The region is known colloquially as the Triangle, a name that references its three anchor universities: Duke University in Durham, the University of North Carolina at Chapel Hill, and North Carolina State University in Raleigh.

On a combined basis, the Raleigh-Durham-Cary CSA totaled approximately 2.48 million residents as of the most recent estimates — making it the 30th largest CSA in the country and the fifth largest in the Southeast behind Atlanta (7.43M), South Florida (7.26M), Central Florida (4.74M), and Charlotte (3.53M). Looking at the component MSAs: the Raleigh-Cary MSA reached nearly 1.60 million people by mid-2025, having grown 12.9% since the 2020 Census — roughly four times the national average over that span and one of the strongest five-year growth rates of any large metro in the country. The Durham-Chapel Hill MSA reached just over 625,000, growing 6.2% over the same period. The combined five-year addition of roughly 220,000 residents places the Triangle among the most consequential growth stories in modern American demography.

On net migration, both components of the CSA performed strongly relative to national peers. Raleigh-Cary added over 39,000 residents in 2023–24, growing at 2.6% — among the highest rates of any metro with more than one million residents. Both Raleigh and Durham ranked in the top 25 fastest-growing places nationally for 2023–24 in U.S. News analysis using Census net migration data. Durham-Chapel Hill’s educational attainment profile has also sharpened dramatically as migration has accelerated: the share of adults with a bachelor’s degree or higher rose eight percentage points to 53.4% between the 2015–2019 and 2020–2024 ACS estimates, the highest rate of improvement among major North Carolina metros. This is a signal of the quality, not just the quantity, of the in-migration flow.

The economic character of the Triangle is distinct from Charlotte’s financial and industrial identity and distinct from the Triad’s manufacturing transformation. It is an innovation economy in the strictest sense — one where proximity to Duke, UNC, and NC State generates a continuous pipeline of research commercialization, startup formation, and specialized talent that compounds over time. Life sciences anchor the employment base: GlaxoSmithKline, Biogen, Pfizer, and Novo Nordisk all maintain significant Research Triangle Park operations, and the region has become one of the top five U.S. destinations for biopharma capital deployment. Recent major commitments in semiconductor-adjacent manufacturing deepen a clustering dynamic that is self-reinforcing: talent and capital attract further talent and capital.

Supply has kept pace with demand across the Piedmont Corridor in a way that most high-growth markets cannot claim. North Carolina ranked third nationally in housing unit growth in 2023–24 at 1.9%, trailing only Idaho and Utah. Charlotte and Raleigh are both expanding in multiple directions from their urban cores. The primary risks to the broader Piedmont region’s outlook are federal funding exposure, particularly for the Triangle’s research institutions, and the broader deceleration in immigration that reduces the overall labor pool available to employers. Both are real. Neither, in our view, alters the region’s structural position.

The Piedmont Triad: An Ascending Third Node

Lying between Charlotte and Raleigh-Durham, the Piedmont Triad — the Greensboro–Winston-Salem–High Point–Burlington Combined Statistical Area — is a region whose manufacturing legacy in textiles, furniture, and tobacco is being rapidly displaced by a new industrial identity centered on aerospace and advanced manufacturing. The Triad’s higher education sector is a meaningful contributor to this evolution: Wake Forest University, ranked 51st nationally by U.S. News, anchors a research and medical ecosystem in Winston-Salem that includes the Wake Forest School of Medicine (ranked 48th in research programs) and the Wake Forest Institute for Regenerative Medicine, an international leader in tissue engineering and bioprinting. High Point University and Elon University have both expanded substantially in enrollment and programmatic breadth over the past decade, adding to a talent pipeline that also draws from UNC Greensboro and North Carolina A&T State University, the nation’s largest HBCU. In total, more than 30 post-secondary institutions serve the Triad region, enrolling over 60,000 students.

The investment pipeline at Piedmont Triad International Airport (PTI) is among the most consequential in the American Southeast. Boom Supersonic completed its $500 million Overture Superfactory at PTI in June 2024, establishing the world’s first dedicated supersonic commercial aircraft manufacturing facility. Honda Aircraft Company remains headquartered at the airport, producing its HondaJet line. In June 2025, aerospace startup JetZero announced a $4.7 billion investment for a commercial all-wing aircraft production facility at PTI — the largest economic development commitment in North Carolina history by job count, with a pledge of more than 14,000 positions. Marshall Aerospace USA has also committed to the campus. In total, PTI-area companies have pledged more than 20,000 jobs and $5.3 billion in capital investment, with potential for further clustering as the campus fills.

| Piedmont Triad Aerospace Cluster: Scale of Commitment

$5.3B in capital pledged at PTI · 20,000+ jobs committed · JetZero $4.7B = largest NC economic development commitment by job count ever · Toyota EV battery plant (Liberty, NC): ~$14B investment, initial production underway 2025 · Siemens Energy: $421M expansion in Winston-Salem (gas turbine parts) and Charlotte (power transformers) · Nucor Steel Lexington: $350M plant in Davidson County, 180 jobs averaging ~$100K · Siemens Mobility: $220M rail manufacturing hub in Lexington, 500 jobs · approximately 200 aerospace companies now operating across the Triad |

Complementing the aerospace cluster, Toyota Battery Manufacturing North Carolina, located in Liberty just east of the Triad, is ramping its nearly $14 billion electric-vehicle battery plant, with initial production underway in 2025 and a commitment of more than 5,100 jobs at full build-out. The broader regional capital commitment now spans aerospace, rail, advanced steel, energy infrastructure, and EV batteries: a diversification that insulates the Triad from any single sector’s cycle.

The Triad’s competitive advantages — lower housing costs than Charlotte or Raleigh, proximity to both markets, a deep technical education ecosystem, and a deep manufacturing culture — position it as a credible long-term beneficiary of the regional capital wave. It is no longer riding the coattails of its larger neighbors; it is building its own industrial identity. Population growth has lagged its larger neighbors but is accelerating. Burlington, the Triad’s fastest-growing node, expanded at a 1.5% rate in 2024–25, led by domestic in-migration, and the broader CSA posted its strongest five-year growth since the early 2010s. As with the Triangle, the best way to view the Piedmont Triad’s economy is by looking at the Combined Statistical Area, which includes Greensboro-High Point-Winston-Salem-Burlington. The 10-county region boasts a 2025 population of 1.78 million and has added 81,281 residents since the 2020 Census.

The Gateway Metro Problem

The large coastal gateway metros (New York, Los Angeles, San Francisco, Chicago, Miami, Washington) occupy a structurally different position. For most of the 2010s, they were losing population through domestic outmigration. The post-pandemic immigration surge interrupted that trend and produced what looked like a recovery.

That recovery was real but temporary. As immigration decelerates, the underlying domestic outmigration dynamic is reasserting itself. Los Angeles has been losing residents every year for a decade; no immigration volume was ever going to fix the structural cost and governance problems driving those outflows. New York briefly led the country in numeric gains in 2023–24, adding over 213,000 residents — then fell to thirteenth place the following year as immigration dried up.

The IRS income data reframes this problem in fiscal terms. New York lost $9.9 billion in net AGI to outmigration in 2022–23. California lost $11.9 billion. Illinois shed $6.0 billion. These are not merely population trends; they are annual revenue-base erosions with compounding consequences. Each year’s outflow reduces the income tax base, raises per-capita fixed costs, and creates pressure for higher rates — which accelerate the next year’s outflow. The gateway metro fiscal problem is self-reinforcing in a way that headcount data alone do not fully capture.

| The Gateway Fiscal Feedback Loop

Stagnant or declining population creates a compounding fiscal problem: fewer taxpayers, maintained pension obligations, slower property tax base growth, and pressure to raise rates — which accelerates further outmigration. New York, Chicago, and Los Angeles are at varying stages of this cycle. The IRS data put the scale in plain terms: New York and California together lost over $21 billion in annual AGI to outmigration in a single filing year. That is not a gap that retaining a few corporate headquarters can close. |

The gateway metros most exposed are those with the weakest domestic migration trends and the highest immigration dependency. Los Angeles and Miami-Dade fit that profile squarely. New York is a close third. San Francisco has shown some domestic migration resilience in the most recent period, possibly reflecting the growth spurt tied to AI. Housing constraints remain severe in the Bay Area, however, and the region’s recovery is not yet durable.

What Comes Next

The data we are analyzing reflect, at most, the first several months of the current immigration enforcement regime. Deportation volumes, legal immigration processing slowdowns, and a broader chilling effect on migration intent will take 12 to 24 months to fully manifest in population estimates. The direction of travel is not ambiguous — NIM will continue to weaken in 2025–26. The question is how steep and for how long.

The IRS data add an important forward dimension to the Census deceleration story. The wealth redistribution captured in the 2022–23 IRS data did not begin with the pandemic and will not end with the immigration pullback. It reflects a durable structural shift in where high-income households choose to live — driven by tax differentials, regulatory environments, housing affordability, and quality of life. The immigration reversal reduces total migration volume, but it does not alter the direction of the income flows captured by the IRS. If anything, it concentrates the domestic migration premium into fewer, stronger destination markets.

For investors, corporate site selectors, and municipal strategists, the most powerful analytical frame combines both datasets: use the Census Bureau numbers to assess current momentum, and the IRS income flows to assess the quality and durability of that momentum. Markets with strong domestic in-migration and high average AGI per arriving return are the most defensible positions. Charlotte, Raleigh, the broader Carolinas corridor, Dallas-Fort Worth, and Houston score well on both dimensions. The Piedmont Triad is ascending into that tier.

The wave of post-pandemic population growth has broken. What remains is a more selective, more structurally revealing distribution of American economic momentum — and with the IRS data now in hand, a clearer picture of where that momentum is carrying not just people, but wealth. The markets capturing both are not doing so by accident. They built it through business environment, infrastructure investment, and housing policy. The markets losing ground are discovering that deferring those choices has consequences that immigration can postpone but not eliminate — and that the IRS confirms, year after year, in the returns.

The geography of U.S. growth has not changed. The rules governing who participates in it have — and the IRS data now tell us how much it costs to be on the wrong side of that divide.

Important Disclosures & Data Notes: This publication has been prepared for informational purposes only and is not intended as a recommendation, offer, or solicitation to purchase or sell any security or other financial instrument, nor does it constitute investment advice.

This report draws on two primary data sources: (1) U.S. Census Bureau Vintage 2025 population estimates (released March 2026), covering July 2024 to July 2025; and (2) IRS Statistics of Income (SOI) Migration Data for Filing Year 2022–2023 (released March 2026), reflecting tax year 2022 income reported on 2023 returns. IRS data cover approximately 70–80% of the U.S. population (tax filers only) and are subject to an 18–24 month lag relative to current Census estimates. Beginning with the 2022–2023 release, SOI enhanced its matching methodology, resulting in approximately 5% more returns than prior vintages. Adjusted Gross Income (AGI) figures represent net flows (inflows minus outflows) and are stated in nominal dollars.

Statements regarding future conditions reflect the views of our analysts and are subject to uncertainty and change. Past demographic trends are not indicative of future outcomes. Recipients should conduct their own independent analysis and due diligence before making any investment decisions.

March 30, 2026

Mark Vitner, Chief Economist

(704) 458-4000

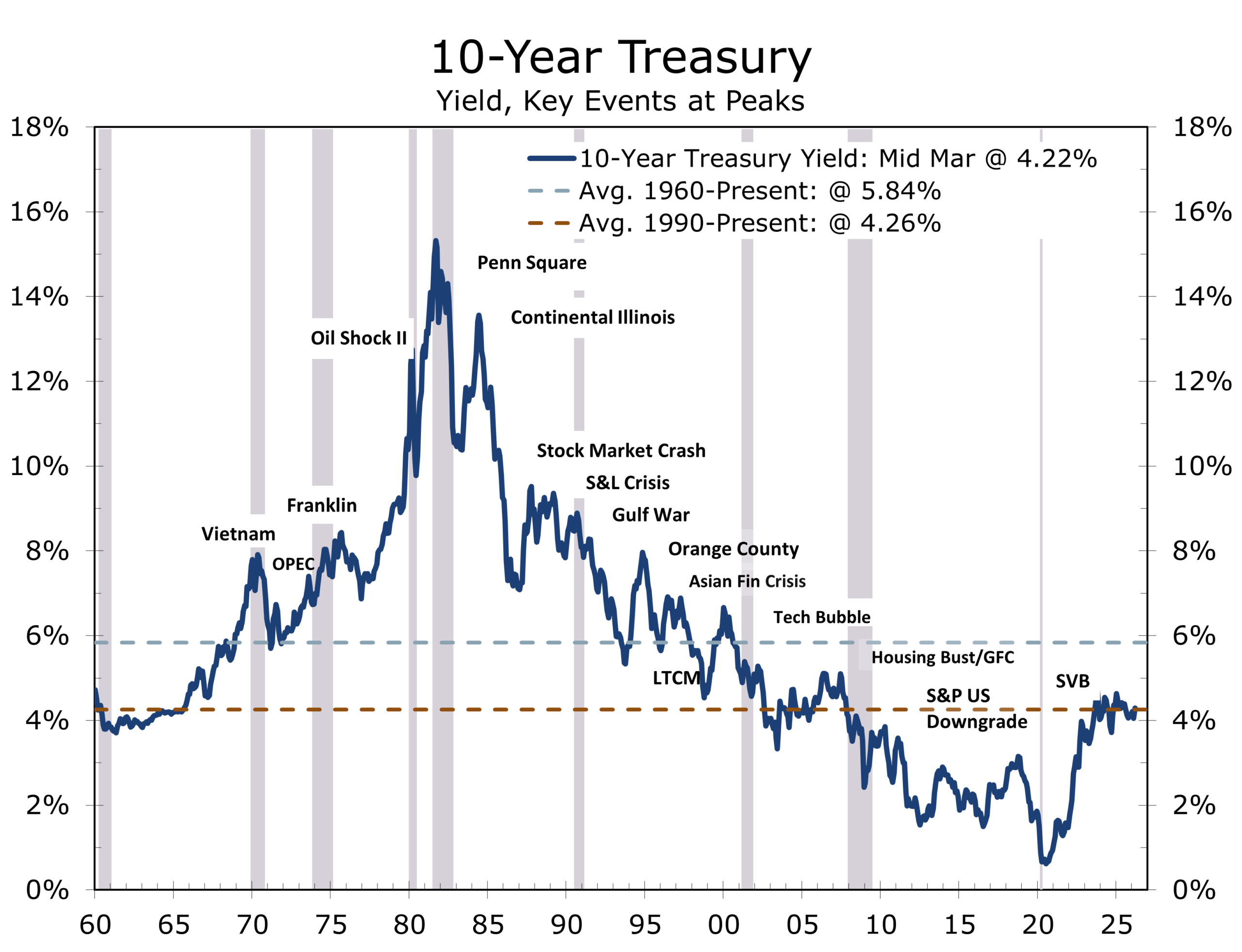

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Risky Shoals and a Shrinking Policy Cushion

Highlights of the Week

- The expansion remains intact but is navigating a materially narrower channel as the Iran shock evolves from event to constraint.

- Markets have repriced toward policy-constraining inflation, not a classic growth scare.

- The Fed is on hold and the bar to easing this year has risen meaningfully.

- The labor market remains stable on the surface but fragile underneath.

- The energy shock is broadening into a multi-channel supply disruption beyond oil, encompassing chemicals, fertilizer and key industrial materials.

- The apparent pause in the escalation of the Iran conflict appears credible, though fragile, with recent developments suggesting at least a temporary halt to planned strikes and tentative movement toward negotiations. This pause may open the door to a Venezuela-style outcome, where sustained pressure redirects an ongoing conflict toward a negotiated equilibrium, even as U.S. forces and assets continue to build in the region.

Unknown Unknowns in Narrower Water

The past week marked a decisive turn in the cycle. What began as a central-bank-dominated narrative has been overtaken by energy, geopolitics, and the reintroduction of constraints. The Federal Reserve may still set the policy rate, but it is no longer setting the tone. That role now belongs to geopolitics, where oil flows and shipping lanes are only part of the equation, and where markets are increasingly forced to price the harder-to-quantify variables, namely President Trump’s often opaque strategic calculus and the uncertain present and future leadership of Iran.

Three weeks into the Iran shock, markets have stopped reacting and started repricing. The distinction matters. Initial reactions tend to overshoot and reverse, particularly on Fridays and Mondays. Repricing embeds. Oil, the dollar, equity markets, and Treasury yields are no longer moving independently. They are moving as a system, and that system is signaling something unambiguous: the path forward for policy has narrowed.

“There are known knowns…there are known unknowns…but there are also unknown unknowns—the ones we don’t know we don’t know.” — Donald Rumsfield

This is increasingly a market defined by what Donald Rumsfeld once called the “unknown unknowns,” where the greatest risks are not the ones investors can model, but the ones they cannot yet fully see.

This is not a classic risk-off environment. It is something more nuanced and more challenging. Markets are not primarily pricing a collapse in growth. They are pricing a constraint on policy. Oil has risen enough to lift near-term inflation expectations, but not enough to immediately crush demand. Yields have moved higher, not lower. The dollar has firmed. Even gold has struggled to behave like a traditional haven, reflecting higher real rates rather than panic. Taken together, this is the signature of a stagflation scare in its early, more subtle phase. The first casualty is not growth, but flexibility, meaning the ability of policymakers to ease, of markets to rally on weaker data, and of households and businesses to absorb higher costs without cutting back somewhere.

The Federal Reserve finds itself in a familiar but unenviable position. It held rates steady at its March meeting and emphasized uncertainty tied to developments in the Middle East. The tone was more cautious than dovish or hawkish. Policymakers explicitly acknowledged the risk that higher oil prices could feed into inflation expectations, even as the labor market shows signs of softening beneath the surface. The result is a policy stance that is neither tightening nor easing but rather waiting for more information. In this instance, “Wait and see” is less of a placeholder and more of a strategy for now. The futures market does not see another cut until the middle of 2027.

History offers a useful frame for understanding the moment, and it is not a comfortable one. The current posture sits somewhere between Chamberlain’s “peace for our time” and Kennedy’s pledge to pay any price and bear any burden in defense of strategic interests. An early capitulation, or TACO moment, would carry series long-term negative implications for the security of the Middle East, Asia and U.S. homeland. The decision to pay any price and bear any burden comes down to U.S. taxpayers picking up the tab for stakes and burdens than impact much of the world and energy-dependent Europe in particular.

This puts the situation somewhere in the middle defined by caution but shadowed by the risk of escalation. Policymakers are attempting to avoid overreaction while recognizing that underreaction carries its own costs. There is also, still at the far edge of the distribution, the possibility of something closer to a Venezuela-style outcome, where the current conflict is redirected, under sustained external pressure, toward a negotiated equilibrium rather than further escalation. That framework aligns with President Trump’s stated objective of bringing Iran’s enriched uranium under control and establishing joint oversight of the Strait of Hormuz, a solution that would seek to convert military leverage into a new geopolitical arrangement.

For now, the energy shock is doing what energy shocks typically do. It is acting like a tax on the global economy. Higher gasoline and diesel prices are already eroding purchasing power, particularly for lower-income households, while also raising costs across transportation, logistics, and production. Airlines, railroads and trucking firms are already making hard choices to control cost. The more important development, however, is that the shock is broadening. This is no longer just about oil and diesel fuel. Fertilizer, liquefied natural gas, industrial gases, and shipping costs are all being drawn into disturbance. When supply shocks move beyond a single commodity and into the wider production network, they tend to persist longer and prove more difficult to unwind, particularly if fears of shortages and higher prices become embedded in decision-making.

The labor market, at least on the surface, continues to hold. Initial jobless claims remain low, and layoffs are contained. Yet the underlying dynamics are less reassuring. Hiring has slowed materially, and much of the apparent stability reflects a lack of firing and reduced voluntary turnover rather than resilient demand. This “no-hire, fewer-quits, no-fire” equilibrium is consistent with a productivity-driven expansion, where firms are producing more with fewer workers, supported by capital investment and technological gains. With turnover down by roughly one-third from its prior norm, businesses not only need to hire fewer workers but also spend less on training and onboarding, while benefiting from a more experienced workforce. This is an equilibrium that can shift quickly, however, if demand weakens further.

Housing offers a similar story. Earlier in the year, lower mortgage rates provided a modest lift, raising hopes that the sector might stabilize. That window now appears to be closing. Rising Treasury yields have pushed mortgage rates higher again, affordability remains stretched, and inventories are beginning to build. Housing does not need to lead the expansion, but it does need to find a floor. For now, higher rates are delaying that process. As a result, residential investment is likely to remain a modest drag on growth in the near term rather than the source of support seen in prior cycles.

Globally, the constraint is more pronounced. Europe remains particularly exposed due to its reliance on imported energy and a more fragile industrial base. Central banks are responding accordingly. The ECB has shifted in a more hawkish direction, the Bank of England is warning of renewed inflation pressures, and even in Japan the tone is beginning to change. The common thread is clear: higher energy prices are limiting the ability of central banks to support growth.

This tension between sustaining growth and preventing a supply shock from evolving into broader inflation is now the defining feature of the cycle. The broader framework we have outlined in recent months still holds. This remains a capital-led expansion, driven by infrastructure, reshoring, and artificial intelligence. Productivity gains are real and continue to support output, but they are unevenly distributed. Capital spending can remain firm, supported by long lead times and strategic investment decisions, even as consumer spending becomes more volatile. The result is a two-speed economy, where strength at the top coexists with increasing strain at the household level.

Looking Ahead

Looking ahead, the usual calendar of economic data matters, but it is no longer the primary driver. Productivity, consumer sentiment, and inflation expectations will provide important signals, but markets are taking their cues from a different set of variables. Oil prices, the dollar, long-term yields, equity market breadth, and inflation expectations measures now form the core dashboard. These are the indicators that will determine whether the current shock stabilizes, intensifies, or begins to fade.

The range of outcomes is relatively clear. A de-escalation in the Middle East would allow oil prices to stabilize, financial conditions to ease, and the Federal Reserve to regain some flexibility. A prolonged disruption would keep inflation elevated and growth below trend, forcing policymakers to remain cautious for longer. A further escalation, particularly one that damages energy infrastructure or meaningfully impairs shipping through the Strait of Hormuz for an extended period, would force difficult trade-offs for businesses and policymakers and further narrow the margin for error.

For all the disruption stemming from the Iran crisis, the expansion is still underway. The underlying structure remains intact. Jobless claims are low, capital investment is firm, and productivity gains continue to support output. But the environment has changed. The system is more sensitive, and the buffer provided by stable energy prices, easing inflation, and improving financial conditions has diminished.

The global economy is still moving forward. It is simply doing so in shallower water, with less room to maneuver, more complex trade-offs, and a policy cushion that is thinning by the week.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

March 23, 2026

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

A 21st-Century Energy Shock

A 21st-Century Energy Shock: A Stress Test for the West

- The joint U.S.–Israeli strikes against Iran and the expanding conflict involving Hezbollah in Lebanon have introduced a new geopolitical shock to the global economy. The principal transmission channels are higher energy prices, tighter financial conditions, weaker consumer confidence, larger budget deficits, and greater uncertainty around capital investment.

- The confrontation stems from a long-running regional conflict that intensified following the October 7 attacks on Israel. Iran’s support for militant proxy networks across the Middle East and its direct role in planning and training the October 7 attacks made a direct confrontation inevitable, particularly after Israel systematically dismantled Iran’s key proxies: Hamas and Hezbollah.

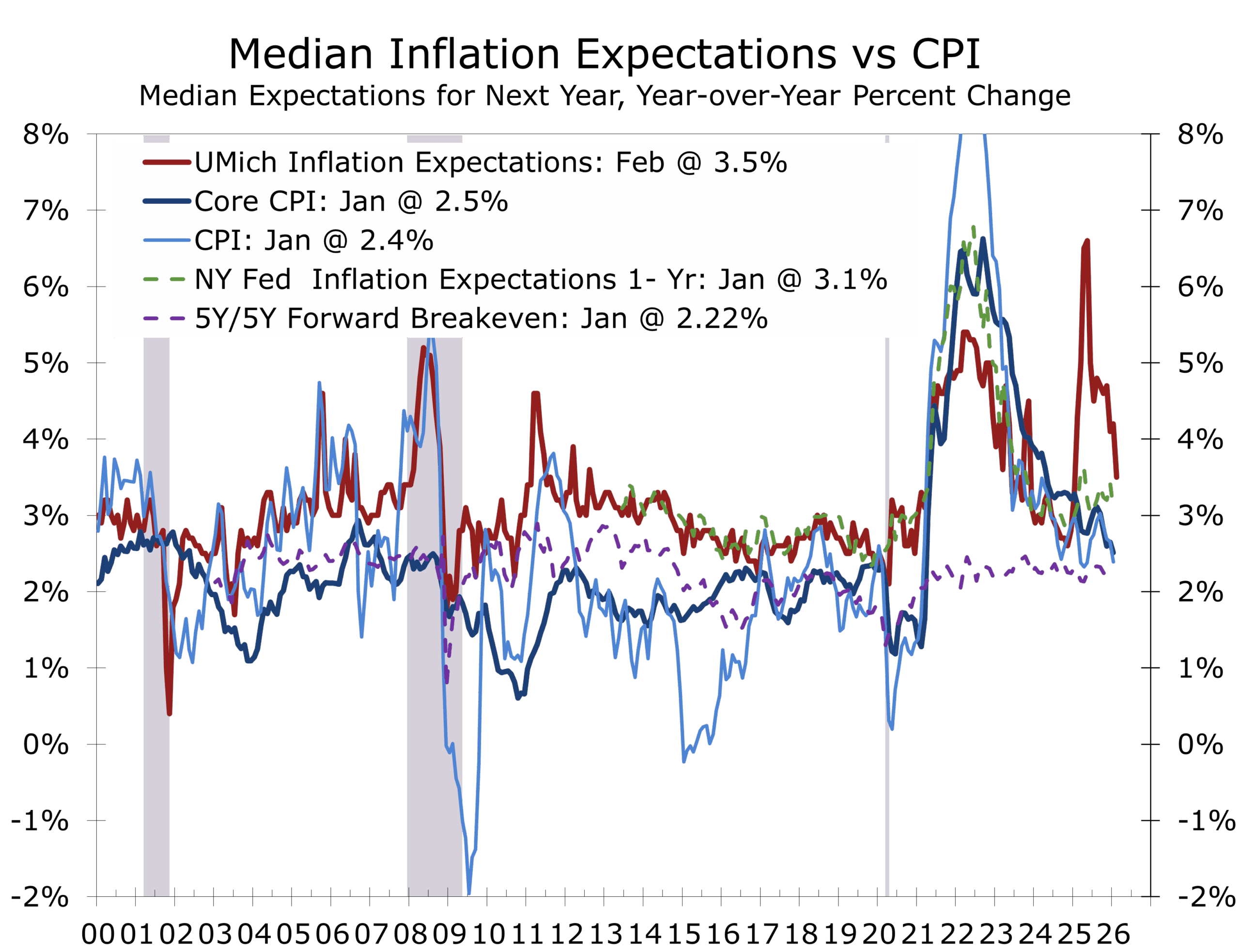

- The shock remains largely concentrated in energy markets. Higher oil prices will likely lift headline inflation during the first half of the year while slowing economic growth modestly.

- Headline PCE inflation could run roughly 5 percentage point higher than previously expected, while core PCE may rise about 0.2 to 0.3 percentage points more than earlier thought. The increase is meaningful but not transformative, particularly since most of the adjustment occurs early in the year.

- Economic growth is likely to slow modestly, reflecting softer consumer spending on durable goods and some delays in capital investment.

- Structural changes in the global economy should limit the risk of a sustained inflation spiral. The U.S. economy is far less energy-intensive than in the 1970s and domestic energy production is far higher. Moreover, today’s modern monetary policy framework emphasizes maintaining inflation credibility.

- One secondary risk lies in credit markets. Elevated energy prices and tighter financial conditions amplify the ripples with private credit and modestly restrain capital investment.

- Our baseline outlook remains one of continued expansion, though with slower growth, fewer near-term rate cuts, and greater financial market volatility. Real GDP is expected to rise 2.9% in 2026, while the headline PCE deflator rises 2.6% and the core PCE deflator rises 2.5% (all Q4/Q4 basis).

The Geopolitical Shockwave

The joint U.S.–Israeli military campaign against Iran and the widening conflict involving Hezbollah in Lebanon have introduced a new layer of uncertainty into the global economic outlook. The macroeconomic consequences are being transmitted primarily through higher energy prices, tighter financial conditions, declining consumer confidence, increased budget deficits and Treasury issuance, and greater uncertainty surrounding business investment decisions.

The risk is not today’s oil spike, but tomorrow’s supply disruption

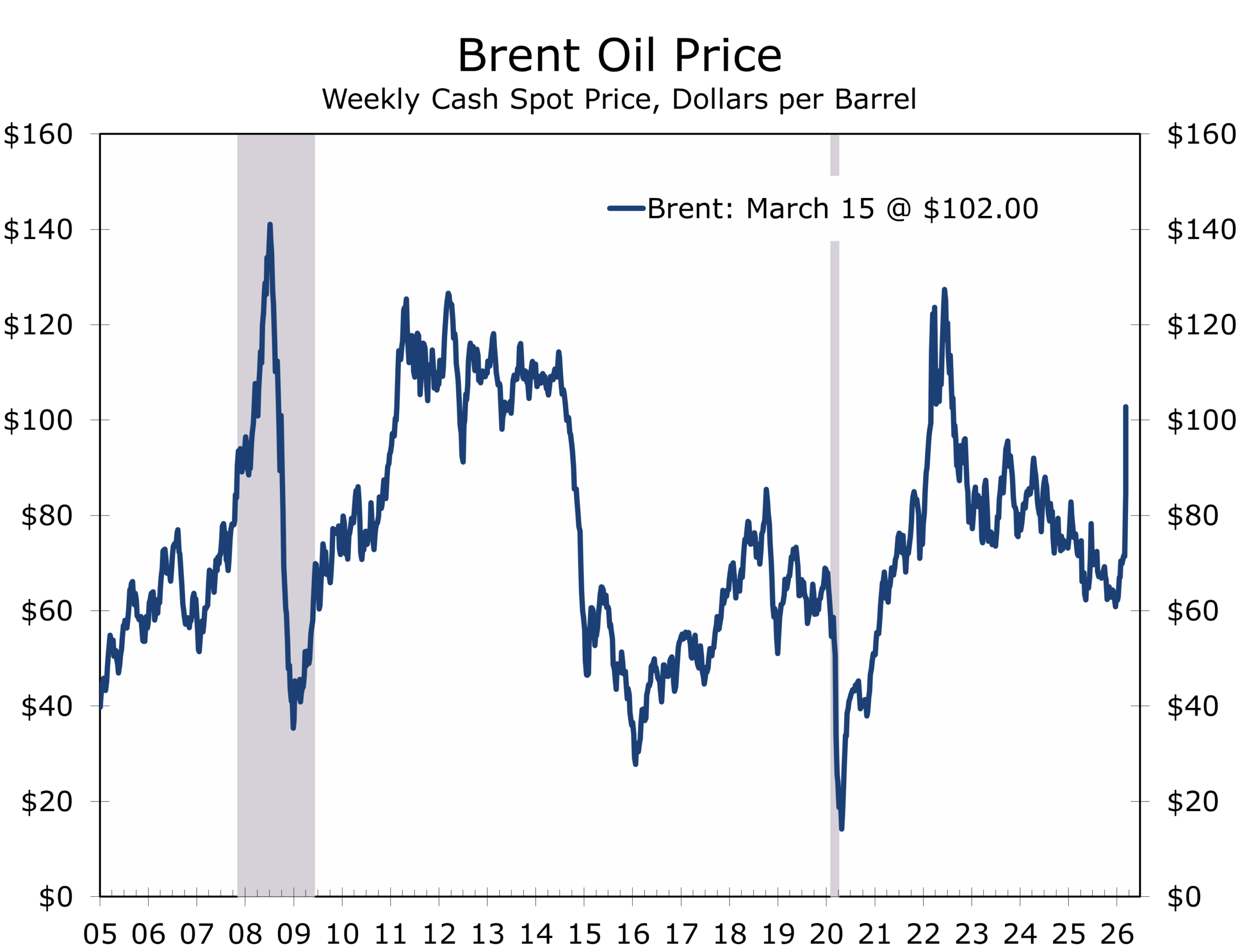

The key question is not whether the shock will affect the global economy but whether it remains contained within energy markets. Financial markets have spent the past few weeks debating whether the conflict could evolve into a broader disruption to global supply chains and financial conditions. Those concerns appear overstated for now. Energy markets entered the crisis oversupplied, a factor that has kept oil prices from surging beyond roughly $120 per barrel.

The conflict itself has deep roots. Iran has spent decades cultivating proxy forces throughout the region, including Hezbollah in Lebanon and Hamas in Gaza. Regular readers of our publications will note that we have long warned that a direct conflict between the U.S. and Iran was a virtual certainty. The October 7 attacks crossed many lines, dramatically escalating tensions and accelerating a trajectory toward direct confrontation that had been building for years. While Israel is the primary target today, a similar attack in the U.S. is a key Iranian objective.

The regional dimension of the conflict is already evident. Hezbollah has launched rockets into northern Israel from Lebanon, while Israeli forces have conducted retaliatory strikes against Hezbollah positions across southern Lebanon and areas surrounding Beirut. The conflict now effectively spans multiple fronts across the region.

The economic implications extend far beyond the battlefield. The Middle East remains central to global energy markets and international shipping routes. Roughly one-fifth of global oil flows pass through the Strait of Hormuz, making it one of the most strategically significant energy chokepoints in the world. A durable resolution to the conflict will ultimately require removing this threat permanently.

For now, spillovers beyond energy markets remain limited. Oil prices have risen sharply, but the broader global supply chain disruptions seen during the pandemic have not reappeared and are unlikely to do so. Shipping costs outside tanker markets remain relatively stable, and industrial supply chains remain largely intact.

Energy shocks tend to lift headline inflation quickly but fade over time. The expected increase in inflation this year appears meaningful but temporary, concentrated primarily in the first half of the year.

Even so, higher energy prices will push inflation somewhat higher and slow growth modestly. Headline PCE inflation may run roughly half a percentage point higher than previously expected, while core inflation may rise about 0.2–0.3 percentage points faster than previously expected. Most of the adjustment is likely to occur during the first half of the year.

The U.S. economy entered this episode with more underlying momentum than recent headline data suggest. Real incomes continue to rise, the labor market remains stable, and layoffs remain historically low. The January data might overstate the economy’s resilience, however. Personal income has a tendency to rise solidly in January and give back most of those gains in following months. The seasonal quirk is likely a legacy of the Pandemic. Hence, recent after-tax income growth and saving rate may currently overstate the resilience of consumer spending.

Momentum remains intact, but seasonal noise and demographics are distorting the data

February’s payroll numbers nearly reversed all of January’s downwardly revised gain. Hiring was impacted by the return of winter weather, strikes in the healthcare sector, and some larger than expected reversals in sectors boosted by the holiday season, such as couriers and delivery workers. The data are also being weighed down by federal retirements. We believe the ADP private sector payroll data, which rose by 63,000 in February and an average of 27,000 jobs per month over the past year and are less impacted by strikes and some season distortions, currently provide a better read on the state of the labor market.

While hiring has slowed, Demographic forces are reshaping the labor market. Slower population growth and reduced immigration have reduced the supply of labor, lowering the pace of payroll gains required to maintain a stable unemployment rate. In this environment, slower job growth does not necessarily signal economic weakness. A low unemployment rate, however, does not necessarily signal a strong labor market.

The bottom line for consumers and the broader economy is that higher energy prices reduce real purchasing power (income effect) and complicate the task facing central banks. Monetary policymakers must balance the inflation impulse from energy prices against the risk that tighter financial conditions slow economic activity. We feel the Fed is still likely to ease, with its primarily motivation being to return monetary policy to neutral. Right now, the next Fed rate cut looks like it will be in September, but an earlier cut is possible if the job growth begins to lose significant momentum.

Transmission Channels

Energy shocks affect the economy through several key mechanisms. In economics the key terms are the income effect and substitution effect.

The most immediate transmission channel is oil prices. Energy markets responded quickly to the escalation of hostilities, reflecting both supply risks and concerns about shipping through the Strait of Hormuz. Even with ample current supplies, markets are forward-looking, effectively pricing the next marginal barrel of oil or shipment of natural gas.

Energy shocks historically weaken durable goods demand first, as households postpone large purchases such as vehicles, furniture and appliances.

Higher gasoline and utility cost’s function much like a tax on economic activity. They reduce household purchasing power and shift spending away from discretionary categories (Income effect).

Durable goods spending is particularly sensitive to these shifts. Purchases of vehicles, appliances, and other large-ticket items often weaken when energy prices rise (Substitution effect).

A second transmission channel is consumer confidence. Energy prices are highly visible and often shape household perceptions of the broader economy.

A third channel involves business investment. Firms frequently delay or stage large capital expenditures during periods of geopolitical uncertainty.

Finally, financial conditions can tighten as investors reassess risk and Treasury issuance increases to finance to war, pushing borrowing costs higher across credit markets.

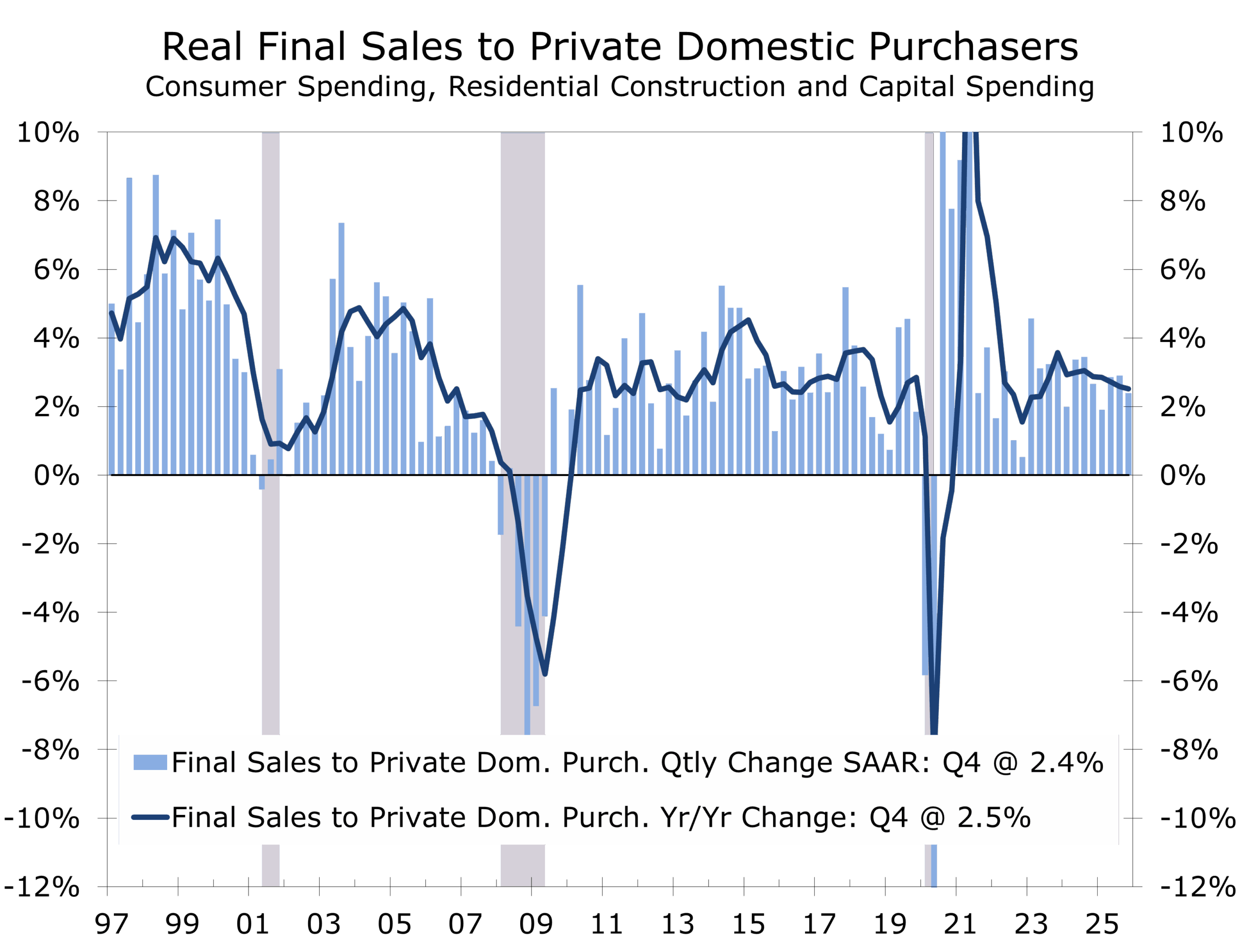

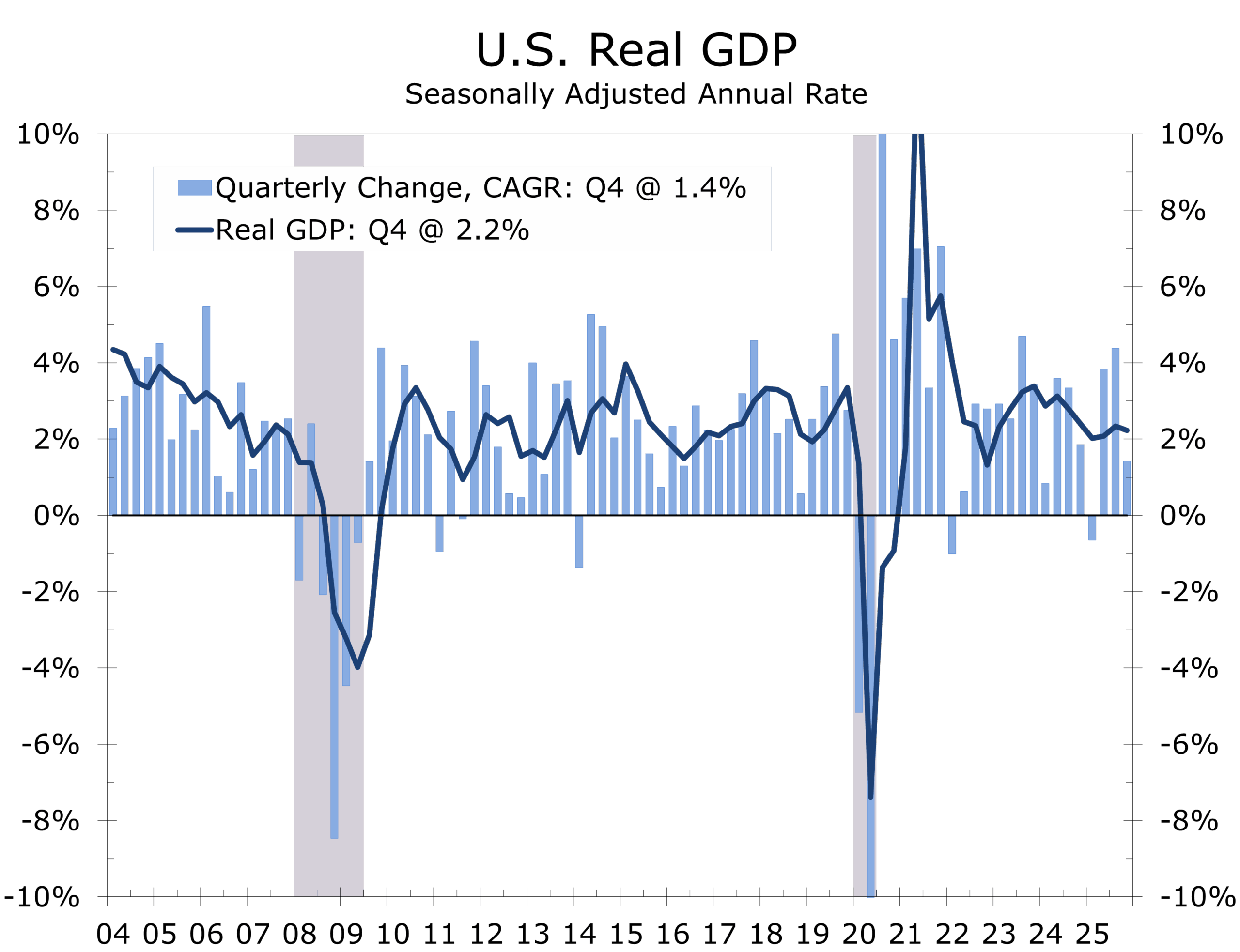

Private domestic final sales rose at a 1.9% annual rate in Q4 and are up 2.5% year-to-year, only modestly below the pace in the third quarter. Consumer spending slowed but remained positive. Business fixed investment increased at a solid clip, led by intellectual property and equipment. Residential investment continued to contract, underscoring that housing remains a lagging sector in this cycle. The composition of growth matters more than the disappointing 1.4% headline Q4 real GDP growth print.

Capital deepening is the primary growth engine, resulting in a capital-led, job-light expansion