ECONOMIC INDICATOR REPORT · SMALL BUSINESS OPTIMISM, MAY 2026

Frozen and Pricier

Hiring Frozen at Spring-2020 Lows as Selling Prices Reaccelerate: A Cost Squeeze That Keeps the Fed Boxed In

EARLY SIGNAL

- Optimism eased to 95.3, slipping 0.6 point to a third straight month below the 52-year average of 98.0. The headline move is small; the internals are not.

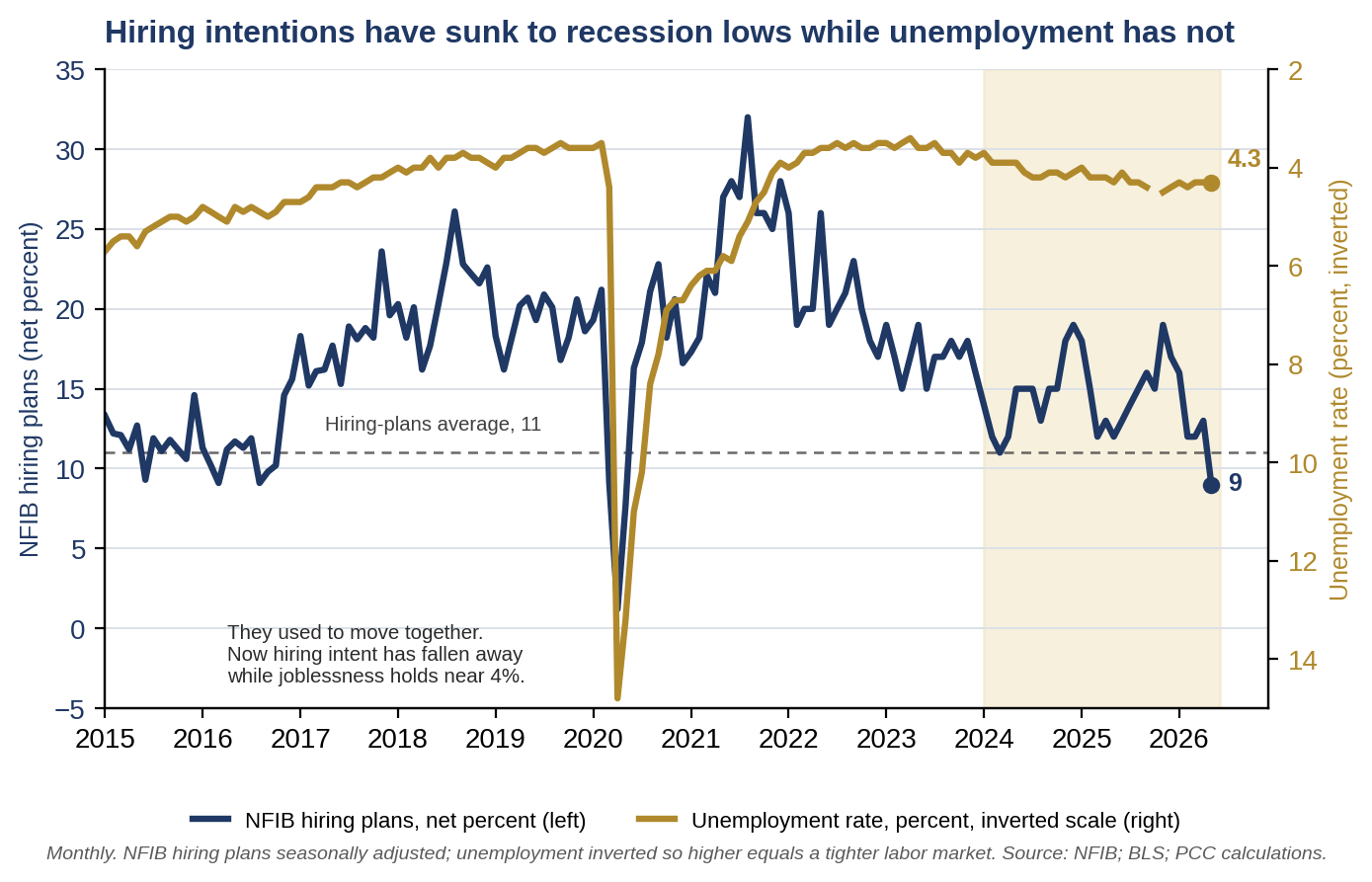

- Hiring plans fell to a net 9% and unfilled openings to 29%, both the lowest since May 2020. These are recession-grade labor readings in an economy that is not in recession and is experiencing solid top-line growth.

- The binding labor constraint has flipped. Labor cost is now the top labor complaint at a record 14% of owners, while labor quality fell to 13%, its lowest since December 2016.

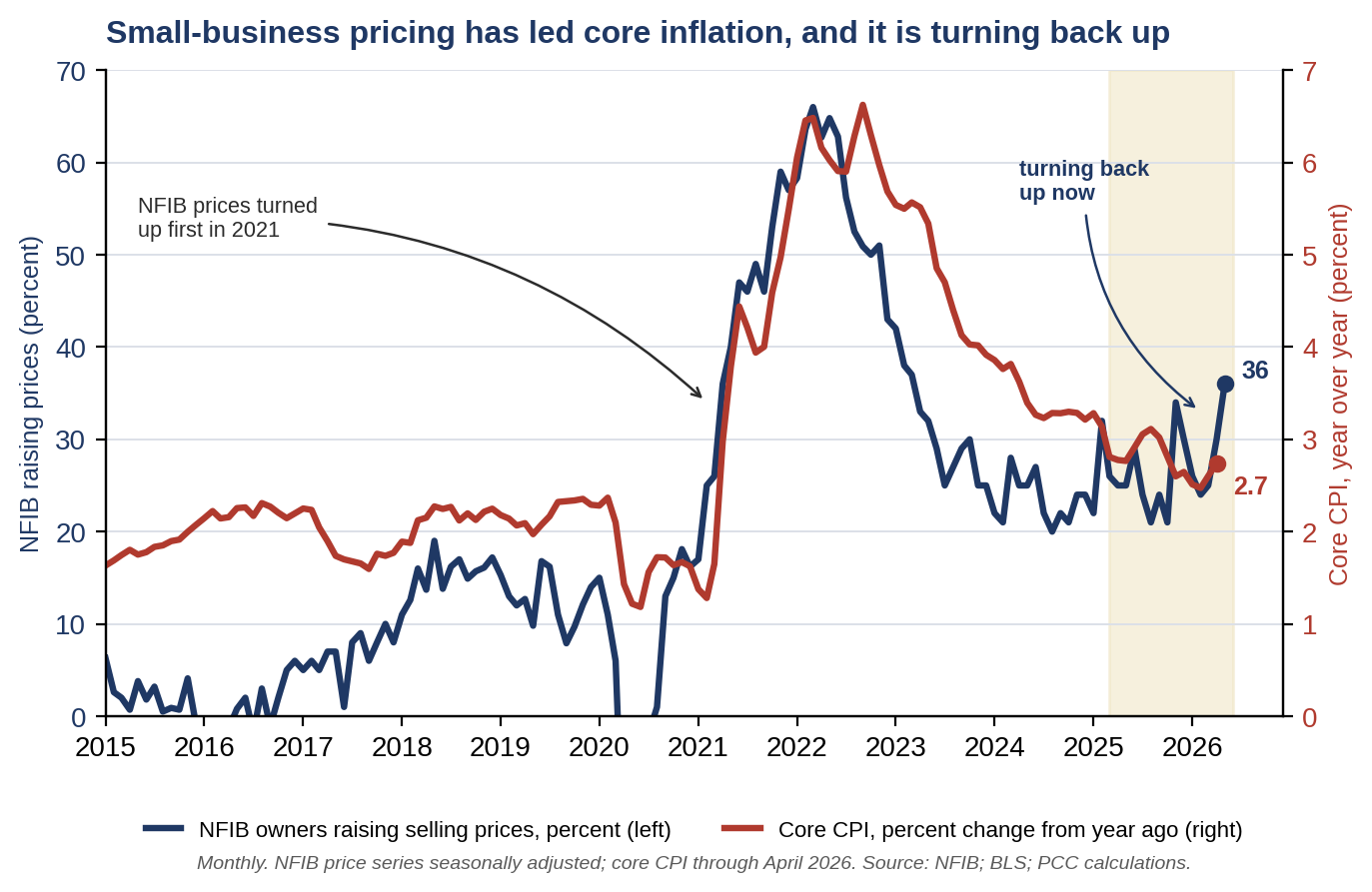

- Selling-price increases jumped to a net 36%, the most since March 2023, with price plans at a net 34%, the most since July 2022. The NFIB price reading has led core inflation through this cycle and is turning back up.

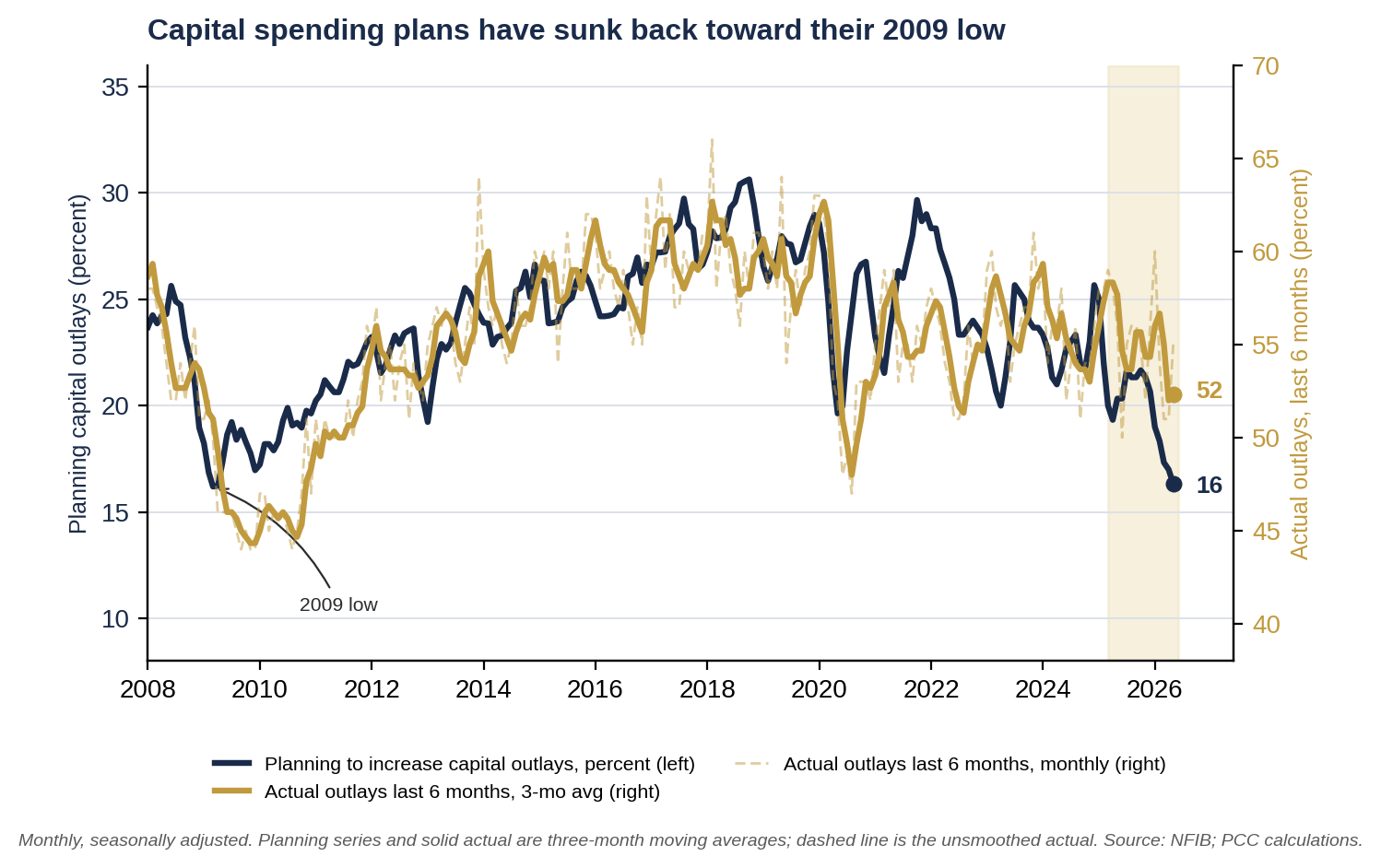

- Capital spending plans slipped to 16%, the weakest since March 2009, while the Uncertainty Index rose to 91, far above its norm near 68.

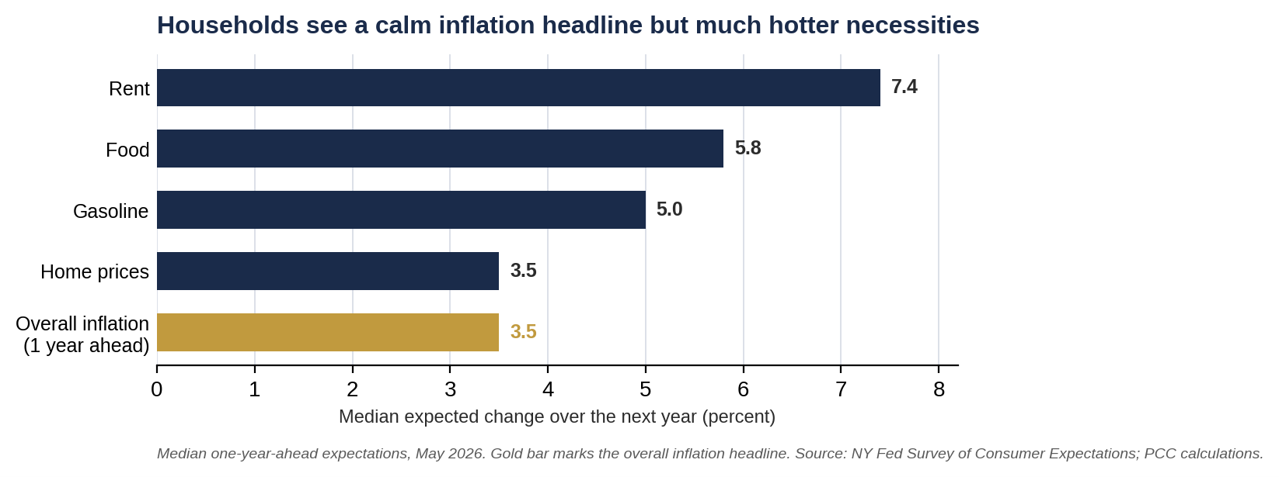

- Households are sending the same signal. The May New York Fed consumer survey shows three- and five-year inflation expectations stuck near 3%, the job-finding rate down to 43.7%, and the share feeling much worse off than a year ago at a three-year high.

A QUIET HEADLINE OVER A WIDENING SPLIT

Much like headline GDP growth and overall employment growth, the Small Business Optimism Index is doing a good job of hiding the action beneath it. May’s 0.6-point decline to 95.3 looks like a quiet month, and at the index level it was. Three of the ten components rose, six fell, and one held flat, leaving the composite roughly where it has sat all spring. We would caution against reading the calm headline as a calm survey.

The interesting development is the divergence inside the report. Labor demand is sliding toward levels typically associated with downturns, while pricing power is turning back up. That combination is not what a single optimism number can convey, and it is the small-business confirmation of the two-speed economy we have been describing for months. NFIB’s own commentary makes the same point in plainer terms, contrasting an investment-led upper tier of the economy with a lower tier that is absorbing higher costs.

A LABOR MARKET THAT READS LIKE A RECESSION

Hiring plans fell four points to a net 9%, and the share of owners with openings they cannot fill dropped five points to 29%. Both are the lowest readings since May 2020, and hiring plans now sit below their long-run average of a net 11%. Taken at face value, these are recession-type numbers.

They are not, however, recession numbers, and the contrast with the unemployment rate is the proof. Hiring intentions have collapsed to levels we normally see only in downturns, yet the jobless rate currently sits at just 4.3%. The two have pulled apart. This is the low-hire, low-fire market we have flagged repeatedly: firms are not cutting staff, they are declining to add, and churn has frozen rather than reversed. Workers are also less apt to leave their current jobs. A frozen labor market is a genuine loss of momentum, but it is a different animal from one that is shedding workers, and it argues for patience rather than alarm.

FROM FINDING WORKERS TO AFFORDING THEM

The most telling rotation in the survey is in what owners identify as their single most important problem. Labor cost rose five points to 14%, the highest reading in the survey’s history. Labor quality fell five points to 13%, its lowest since December 2016. For the better part of three years, the binding labor constraint was scarcity, the inability to find qualified workers. That constraint has eased. What remains is the embedded cost of the workers already on the payroll.

Compensation behavior confirms it. A net 31% of owners raised pay over the past three months, up a point, and a net 18% plan further increases, unchanged from April. Wage growth at the small-business level is decelerating only slowly, and it is doing so from an elevated base. For the inflation outlook, that stickiness matters more than any single openings figure, because it speaks to the cost structure owners are now operating in and trying to pass through.

PRICING POWER IS RISING, NOT FALLING

And pass it through they are. The net share of owners raising average selling prices climbed six points to 36%, the highest since March 2023, with planned increases up seven points to a net 34%, the highest since July 2022. That matters well beyond the survey, because the NFIB selling-price reading has been a dependable leading indicator of realized inflation.

The relationship holds across the cycle. Small-business pricing surged months ahead of the 2021 to 2022 core CPI spike, then led the disinflation that followed. It is now turning back up, with the May reading jumping to 36 while core CPI sits near 2.8%. We read the renewed climb in selling prices as the confirming signature of cost-push, not demand-pull. Firms are lifting prices to defend margins against rising input costs, not because customers are clamoring for more goods and services. NFIB ties the impulse to energy, with gasoline reflecting both a tighter global oil supply and a war risk premium, layered on top of the wage pressure already in the system. Supply-chain friction is feeding it too, with 70% of owners now reporting some disruption, up six points. Reports of inflation as a top problem rose for a third straight month to 18%, the highest since December 2024.

INVESTMENT INTENTIONS AND THE COST OF CAUTION

The cautious posture extends to the balance sheet. Plans to make capital outlays eased to 16%, the weakest reading since March 2009, and the Uncertainty Index rose three points to 91, far above its long-run norm near 68. Only 7% of owners called it a good time to expand, the lowest since October 2024, and expected business conditions fell for a fifth consecutive month. Borrowing costs are no help: a net 6% reported paying a higher rate on their most recent loan, up four points, even as the average short-term rate edged down to 7.8%. When uncertainty is this high and pricing is this defensive, deferring investment is the rational choice, and that is what owners are doing.

HOUSEHOLDS ARE SENDING THE SAME SIGNAL

The case does not rest on small-business owners. The New York Fed released its May Survey of Consumer Expectations on June 8, and it paints the household side of the same picture. On inflation, the headline looks benign and the detail does not. Median expectations for the year ahead slipped a tenth to 3.5%, but the three- and five-year horizons held at 3.1% and 3.0%, still well clear of the 2% goal. Underneath the headline, households expect food prices to rise 5.8% over the next year and rent to climb 7.4%, and they marked up expected home-price growth by half a point to 3.5%, the highest reading since July 2022. All are well above our expectations.

On the labor market, the survey echoes the low-hire, low-fire dynamic from the owner side. The mean perceived probability of finding a job after a layoff fell to 43.7%, below its twelve-month average of 46.8% and the lowest since December, even as expectations of a layoff rose. Workers, like owners, sense that hiring has cooled while joblessness has not climbed.

On household finances, the lower tier of the two-speed economy comes into focus. The share of households reporting they are much worse off than a year ago rose more than two points to 13.3%, the highest since July 2022, and net optimism about the year ahead fell to its weakest since October 2022. Expectations for credit availability deteriorated, and the average perceived chance of missing a minimum debt payment in the next three months rose to 12.6%. This is the same squeeze the NFIB commentary describes, now visible in the family budget rather than the income statement.

WHAT IT MEANS FOR THE FED

For the Federal Reserve, the May surveys are an unwelcome combination. The labor data offer the kind of softening that might normally argue for patience tilting toward easing, but the price data refuse to cooperate. Selling-price increases are accelerating, owners and households both expect more inflation, and the NFIB pricing signal that has led realized core inflation through this cycle is turning back up. A frozen labor market that is not actually shedding workers gives the Fed no growth scare to respond to, while re-accelerating prices give it every reason to wait. That is the definition of boxed in. Chair Kevin Warsh, sworn in on May 22, chairs his first meeting on June 16 and 17, with cover to hold but no clean path to cut.

BOTTOM LINE

The May NFIB survey is not a recession signal but remains uncomfortably consistent with a low altitude stagflation. Hiring intentions and job openings have fallen to levels we normally see only in downturns, yet unemployment sits at 4.3% and owners are not cutting staff. At the same time, selling prices are reaccelerating, capital spending plans are the weakest since 2009, and the New York Fed’s consumer survey shows households feeling the same squeeze. This is a small-business sector, and a household sector, caught between a frozen labor market and renewed cost pressure. For the Fed, that mix removes the easy case for easing and keeps the central bank boxed in.

WHAT WE ARE WATCHING

- NFIB price plans and selling prices: Whether the May upturn to a net 36% extends, which would point to renewed pressure in core inflation over the following months.

- The labor-cost complaint: Whether labor cost holds at or above its record 14% share of owners as the single most important problem, a sign that embedded wage pressure is sticky.

- Hiring plans and openings: Whether the spring-2020 lows mark a floor or give way to actual job cuts, which would turn low-hire, low-fire into something worse.

- Capital spending plans: Whether the weakest reading since 2009 stabilizes once uncertainty around the Iran conflict and energy prices recedes.

- The household side: New York Fed inflation expectations, the job-finding rate, and delinquency expectations, for confirmation that the consumer squeeze is or is not deepening.

Mark P. Vitner

Chief Economist, Piedmont Crescent Capital

mark.vitner@piedmontcrescentcapital.com · (704) 458-4000

Sources: NFIB Research Center, Small Business Economic Trends, May 2026; Federal Reserve Bank of New York, Survey of Consumer Expectations, May 2026 (June 8, 2026); U.S. Bureau of Labor Statistics, core CPI and unemployment rate; FRED. Historical series and chart calculations by Piedmont Crescent Capital.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation, offer, or solicitation with respect to the purchase or sale of any security or other financial product, nor does it constitute investment advice. Views are those of the author as of the date of publication and are subject to change.