Our Weekly Commentary on Money, Credit, Exchange Rates and Geopolitics

A View from the Piedmont

Strong Jobs, a Fraying Truce, a Boxed-In Fed

Highlights of the Week

- Jobs: May payrolls rose 172,000 versus 88,000 expected, with prior months revised up 93,000. Unemployment held at 4.3%, and U6 slipped to 8.1%.

- Beneath the surface: Hiring broadened: the employment diffusion index improved again, including in manufacturing. Yet the long-term unemployment share rose to 27.5%, a cycle high.

- Manufacturing: ISM rose to 54.0, a four-year high. With factory breadth turning up, the cyclical impulse is improving; prices paid near 82 keep the cost squeeze in view.

- Markets: A chip-led rout hit Friday: the Nasdaq fell 4.2%, its worst day since April 2025, as strong jobs lifted yields (10-year 4.54%) and the market began pricing a hike.

- Geopolitics: Iran fired missiles at Israel on Sunday night, the first such strike in two months; President Trump urged Netanyahu not to retaliate to keep the Iran talks alive.

- Fed: Warsh chairs his first FOMC on June 16 to 17; a hold is expected, with a hawkish tone.

- Our view: We push the first cut out; no 2026 cut in our base case, the market has begun to price a hike, and we stay cautious on duration.

Market Snapshot

Three threads ran through the week and into the weekend: a May employment report that came in far stronger, and broader, than the consensus feared; a Middle East truce that frayed through the week and cracked on Sunday night; and a stock and bond market that repriced hard for a Fed that is not cutting. The jobs data did the most work. Payrolls rose 172,000 against expectations near 88,000, the prior two months were revised up 93,000, and the breadth of hiring improved, with the employment diffusion index rising again, including in manufacturing. The capital-cycle thesis we have carried all year remains intact, and the cyclical signal is, if anything, firmer. What the report does not fix is the bottom. The share of the long-term unemployed rose to a cycle high, and the workers losing jobs are not the ones the new hiring is reaching.

The geopolitical track deteriorated. The tentative memorandum we described last week stalled, U.S. and Iranian forces exchanged fire near the strait, and on Sunday night Iran fired a volley of missiles at northern Israel, its first such strike in two months, after an Israeli operation against Hezbollah in Beirut. No one was hurt, and the more telling development was Washington’s response. President Trump moved to restrain Israel, pressing Netanyahu not to retaliate so as not to derail the Iran talks. The truce is back on the brink, but the United States is actively holding Israel back to protect it.

Markets had already turned before the weekend. After a run of records, Friday brought a violent, chip-led selloff. The Nasdaq fell 4.2%, its worst day since the tariff turmoil of early 2025, as the strong jobs report spiked Treasury yields, the market cut its rate-cut bets, and high-multiple technology took the brunt. Investors sold stocks, bonds, gold, and bitcoin together. The weekend escalation sets up a risk-off open. What follows walks through the May employment report and the improving breadth beneath it, what the high share of long-term unemployed tells us, what to expect from Chairman Warsh’s first FOMC on June 16 and 17, the renewed escalation with Iran, and the Friday selloff and the repricing behind it. We close with the CFO corner, the scenario framework, and our forecast revisions.

The May Jobs Report: A Blowout, and a Broadening

The May employment report was the week’s main event, and it was a blowout. Nonfarm payrolls rose 172,000, roughly double the 88,000 the consensus had penciled in, and the prior two months were revised up by a combined 93,000, lifting March to 214,000 and April to 179,000. The three-month average is now 188,000, well ahead of the six- and twelve-month trends of 92,000 and 42,000, and the firmest stretch in over two years. The unemployment rate held at 4.3%, but the detail ran hotter than the round number: the unrounded rate ticked down, and the broader U6 underemployment rate fell to 8.1% from 8.2% even with participation steady. With payrolls now running well above the most recent estimates of the employment breakeven rate, which has dropped sharply as labor-force growth has slowed, the report points to labor-market slack dissipating rather than building.

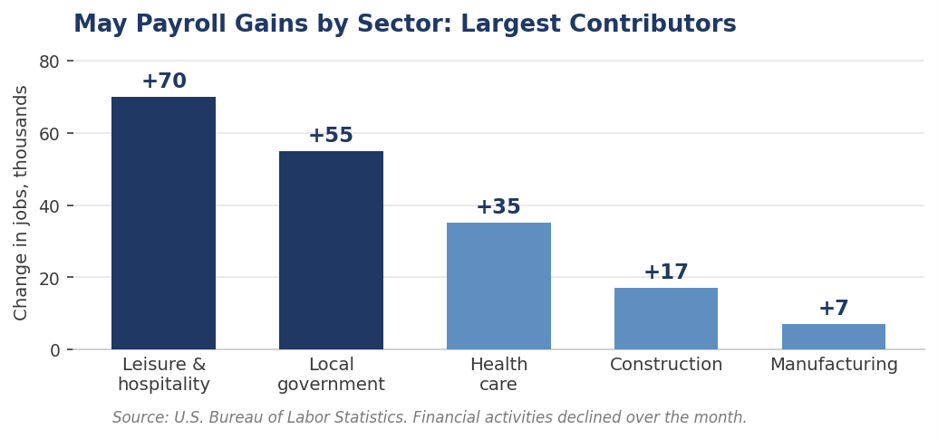

Leisure and hospitality led, but the World Cup is a side story. Leisure and hospitality added 70,000, five times its trailing-year pace, with food services and drinking places contributing 48,000. The easy explanation is the World Cup, which opens June 11, and we think it is the wrong one. The tournament falls after the May survey week, so its hiring will mostly land in June, and we judge it a minor factor in May. Two more prosaic forces did more of the work. Memorial Day fell unusually early this year, only about a week after the survey reference week, which likely pulled seasonal hiring into the May count that would normally show up in June. And more travelers appear to be vacationing closer to home, which lifts hiring at the drive-to destinations that account for a large share of domestic leisure employment. The strength is real; the driver is seasonal timing and a shift in travel patterns more than a one-off sporting event.

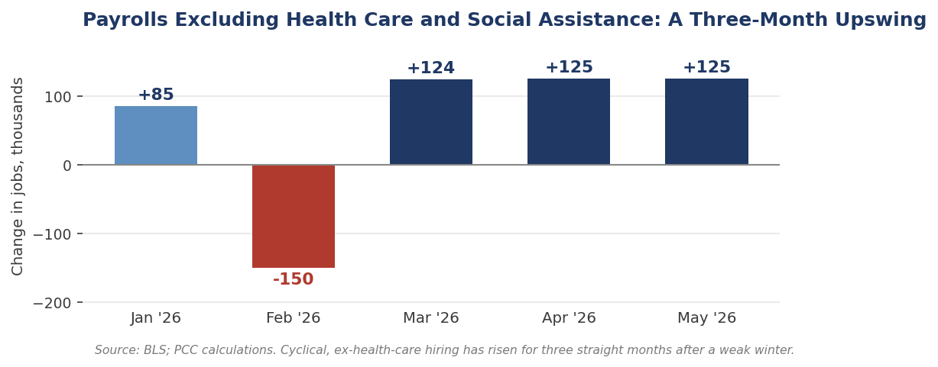

The breadth improved, and it is the cyclical kind. The more important measure than which sector was largest is how widely hiring was spread, and breadth improved. The employment diffusion index, which tracks the share of industries adding to payrolls, rose again in May for total private employment and, notably, within manufacturing. A cleaner way to see it is to strip out the two most acyclical engines that have carried payrolls for the past year. Employment excluding health care and social assistance has now risen for three straight months, after falling through the winter. That is the signature of an upswing in the more economically sensitive parts of the economy, not just the steady, demographically driven hiring in health care and social assistance.

Manufacturing is the cyclical tell. The factory sector punches above its payroll weight because it supplies the cyclical impulse to the rest of the economy; goods production turns first, and services follow. The signals there are turning up. Construction added 17,000 and manufacturing 7,000 in May, modest in level but a clear improvement after a prolonged soft patch, and manufacturing overtime rose to its highest since early 2023, the kind of leading signal that shows up before firms commit to new headcount. Read alongside the ISM factory index at 54.0, a four-year high with new orders expanding for a fifth straight month, the improving manufacturing diffusion points to strengthening conditions ahead, even if it is showing up so far as only marginally stronger job growth. The one caveat is price: the ISM prices-paid index sits near 82, its second-highest reading since 2022, so the factory recovery is arriving with a cost, and that cost is the inflation story in miniature.

The high share of long-term unemployed is the harder signal underneath. For all the improvement in breadth and the dip in broader underemployment, one series is moving the wrong way. The share of the unemployed out of work for 27 weeks or longer rose to 27.5%, the highest of this cycle, and the count is up 524,000 over the year. This is what a low-hire, low-fire labor market looks like from the inside. The aggregate is tightening, slack is dissipating and U6 fell, but that is because fewer people are being let go, not because the jobless are being rehired quickly, and the broadening in hiring is reaching new entrants and job-switchers rather than those already stranded, hinting at a skills mismatch. The longer someone is out, the harder the return becomes, as skills atrophy and employers screen on recent experience, which is how a cyclical problem hardens into a structural one and the natural rate of unemployment drifts up. It also feeds the consumer-credit stress we flagged last week, because the long-term unemployed exhaust savings and lean on revolving credit. So the labor market is strengthening at the margin and scarring at the core at the same time, and the long-term-unemployment share is the single series we would watch to know which force is winning.

Wages cooled, but the policy risk did not. Average hourly earnings rose 0.3% on the month and 3.4% from a year earlier, down from 3.6% in April, so the wage line is contained for now. The problem is the combination. A labor market that is tightening, with slack dissipating and the breakeven rate this low, sitting on top of the broad inflation pressures still in the pipeline, is exactly the mix that can force a central bank to consider hikes rather than cuts. That is why the blowout report reinforces our caution on duration. The asymmetry in long yields is increasingly to the upside, and we would not be extending duration into it.

Piedmont Perspective: Two Americas, One Labor Market

Last week we wrote about the K-shape in the consumer-credit data: record S&P 500 margins on one side, the highest credit-card delinquency since 2011 on the other. This week the same split showed up inside the jobs report, but with a twist. The top line is not just strong, it is broadening: more industries are hiring, the cyclical impulse from manufacturing is improving, and the asset-owning, capital-deploying economy is doing well. The break is no longer about whether the labor market is broad enough. It is about who the breadth reaches. The new hiring is going to entrants and job-changers, while the workers already stranded, the long-term unemployed, are not being pulled back in. The labor market is the hinge between the two Americas, and for now its low-hire, low-fire setting keeps the average looking steady while the stranded cohort grows.

That is the more durable version of the K-shape. A broadening expansion that leaves a hardening core of long-term jobless behind is exactly the configuration that lets headline growth and household distress coexist for quarters at a time. The capital cycle will eventually feed through into wages and into demand for harder-to-place workers, as it has in past investment booms, but that transmission takes time, and the bottom half of the distribution has to hold on through elevated living costs until it does.

The risk we are watching is not the breadth of hiring, which is improving, but whether the long-term unemployed get reabsorbed before their detachment becomes structural. A labor market can broaden at the margin and scar at the core at the same time. The long-term-unemployment share is the single series we would watch to know which force is winning, and right now it is still drifting the wrong way.

The Warsh Fed: A Hawkish Debut in Prospect

Chairman Warsh, sworn in May 22 and elected by the Committee the same day, chairs his first FOMC meeting on June 16 and 17. Last week brought the opening round of commentary from the new Board under his lead; this week’s data did most of the work in shaping what that first meeting is likely to deliver. The setup is not friendly to easing. Payrolls reaccelerated, the better inflation gauges have not yet reached target, and energy is pushing the headline higher. Markets now price roughly a two-thirds probability of a hold, and we agree.

What to expect. We look for a hold, a hawkish tone, and the removal of any residual easing bias from the statement language. Warsh has been explicit in leaning on the trimmed-mean measures as the cleaner read on underlying pressure, and on that gauge the Dallas series at 2.3% argues the trend is contained and pointed lower. But a Chair in his first meeting, with payrolls running near 190,000 on a three-month basis and oil elevated, has every reason to wait. The risk to our hold call is not a cut; it is a more hawkish framing of the inflation risks than the market is positioned for. That hawkish inflation framing might be coupled with some skepticism on the recent run of stronger payroll numbers, preserving optionality.

The revision to our path. This is the week we move our own forecast. We had carried a September cut as the base case. After the May report, and with the energy-driven price impulse still live, we no longer treat a 2026 cut as the base case. We now look for a prolonged hold, with the first move pushed toward year-end at the earliest and conditional on energy disinflation and shelter moderation, and with a small but no longer trivial probability of a hike if price pressures broaden. The market has run further than we have, swinging on Friday toward pricing a hike by year-end as the more likely outcome. We think that overstates the case, but the direction is right. We would rather be early in flagging the shift than caught describing a September cut the data has already taken off the table. We have removed any cuts from our forecast and still see a cut in December as possible.

Geopolitics: The Truce Cracks, and Washington Steps In

The week’s de-escalation did not hold. The tentative U.S.–Iran memorandum we described last week, a 60-day ceasefire extension, a toll-free reopening of the Strait of Hormuz, and a restart of nuclear talks, stalled within days. Tehran suspended the indirect channel, tying any resumption to an Israeli withdrawal from Lebanon and a halt to operations there and in Gaza, and U.S. and Iranian forces exchanged fire near the strait. A mid-week Israel–Lebanon ceasefire briefly looked like a way back. It did not survive the weekend.

Iran struck Israel directly. On Sunday night Iran fired a volley of roughly ten ballistic missiles at northern Israel, its first direct strike in two months, in response to an Israeli operation against a Hezbollah stronghold in Beirut. Israeli air defenses engaged the barrage and no casualties were reported, but the attack pushed the region back toward the brink of the wider war that the spring ceasefire had paused. Israel’s military signaled it was ready to retaliate but was asked by President Trump to hold off. Iran’s move was likely aimed at their domestic audience and was intentionally light and well-telegraphed so that Israel would intercept it.

The more important move came from Washington. President Trump intervened to keep the situation from spiraling, pressing Prime Minister Netanyahu not to strike back and making clear that the United States, not Israel, would set the terms of any agreement with Tehran. He acknowledged the missile attack does not help the negotiations but said it had not changed his intent to reach a deal. The signal for markets is twofold. Near-term escalation risk is real and two-sided, but the United States is now openly restraining its closest ally to protect the diplomatic track and, with it, the path to a Hormuz reopening. That is a meaningful cap on the tail, even as the headline risk rises.

Oil. Brent eased toward $93 by Friday’s close, down from the mid-May high near $119, on softer Chinese demand and a record-long string of U.S. product draws. That was before the weekend strike, which should reassert a risk premium at the Monday open. The two-sided setup is unchanged in character but sharper in degree: a contained outcome with Washington holding Israel back points Brent toward the mid-$80s by year-end, while a retaliation spiral that puts Hormuz in play puts the May highs, and a fresh leg of headline inflation, back on the table.

Markets & Financial Conditions

The bond market repriced first. The 10-year Treasury backed up to about 4.54% after the jobs report, its highest since late May, and the 2-year jumped to 4.16%, its highest since early 2025, as traders pushed cut expectations out and began to price the opposite. The front end led, flattening the 2s10s curve toward 38 basis points from above 60 a week earlier, and the dollar firmed. By Friday the market had swung to pricing a rate hike by year-end as more likely than not, a striking reversal from the September cut it had assumed only days before. We think that is an overshoot. Our base case remains a prolonged hold with no cut in 2026; the hike risk is real but not yet the central path. If inflation cools, as we expect, then real rates will rise and implement any tightening that is needed. Term premium, not the policy rate, continues to do the heavier lifting at the long end, where heavy issuance and a growth backdrop the market increasingly accepts keep a floor under yields. We stay cautious on duration into that mix.

Equities did not hold up. After a run of records earlier in the week, Friday brought a violent, chip-led selloff. The Nasdaq fell 4.18% for its worst day since the tariff turmoil of early 2025, the S&P 500 lost 2.64% and snapped a nine-week winning streak, and the Dow gave back nearly 700 points a day after closing at a record. Semiconductors were the epicenter, with the largest names down high-single to mid-double digits, the unwind of a crowded, concentrated trade that a soft Broadcom outlook had already started midweek. The proximate trigger was rates: a stronger labor market means the economy needs less monetary support, which lifts the discount rate and presses hardest on high-multiple technology whose profits sit furthest in the future. Notably, the usual pattern broke. Yields and oil had been moving together on the war; on Friday yields rose on the jobs data even as oil fell, a sign the driver has shifted from energy-driven inflation to a growth-and-rates repricing. Investors sold stocks, bonds, gold, and bitcoin together, the signature of a rates shock rather than a growth scare. The AI trade is bruised, not broken, and its concentration is now the market’s main vulnerability into a hot CPI and the weekend’s escalation.

Credit has stayed comparatively calm, with investment grade tight and high yield only modestly wider on the consumer story we flagged last week. For all the equity drama, financial conditions have merely come off an extreme; nothing here forces the Fed’s hand, and the spring’s easy conditions are part of why the Committee can afford to wait.

CFO & Treasurer Corner: What This Means for Corporate Finance

Funding and liquidity. The back-up in yields reopens the question of timing. With the 10-year near 4.54% and the front end repricing, the case for opportunistic fixed-rate issuance is stronger, not weaker, because the near-term cut that might have lowered funding costs has been pushed out. Floating-rate borrowers should stress coverage on a 10-year holding at or above 4.50% and a policy rate unchanged through at least the third quarter.

Energy and input costs. Brent near $93 is off its peak but still elevated, and the ISM prices data says the cost pressure is broad on the factory floor. Firms exposed to freight, logistics, or petrochemical inputs should keep 2026 cost stress tests in place and should not assume relief from a deal that is not signed.

Labor and wages. The planning signal is the split inside the report. Hiring is broadening and the cyclical impulse from manufacturing is improving, which supports demand-side plans, but the long-term-unemployed share is rising, so a broad reabsorption of displaced workers is not yet underway. Firms relying on slack to refill roles cheaply should not assume it; firms exposed to lower- and middle-income demand should keep modeling the stress on that cohort. Wage pressure is easing at the margin, which helps the cost line.

Equities and the cost of capital. Friday’s repricing is a reminder that the discount rate, not just earnings, drives high-multiple valuations, and that the index is concentrated in a handful of chip and AI names. Treasurers planning equity-linked issuance or buybacks should assume more two-way volatility and a higher cost of equity than the spring’s calm implied. The fixed-rate funding case is, if anything, stronger now that the near-term cut has been pushed out.

Capital allocation. The capital-cycle thesis holds. Commitments tied to AI, power, grid, and reshoring remain on plan, and the market continues to reward credible productivity narratives over undisciplined spending. The bar for capex without a clear margin path keeps rising.

Planning assumption. Our base case is a prolonged Fed hold with no cut in 2026, a fragile truce that holds because Washington is actively restraining Israel, Brent drifting toward the mid-$80s by year-end once the strait normalizes, and full-year GDP near 2.5% led by capital spending. Boards should now model a no-cut-in-2026 case as the central path rather than the risk case, keep a war-escalation case live for the third quarter given the weekend’s strikes, and treat the equity-concentration risk as a financial-conditions variable in its own right.

Looking Ahead

| Day | Release / Event | Why It Matters for CFOs & Markets |

|---|---|---|

| Monday | NY Fed Survey of Consumer Expectations (May); Wholesale Inventories (April) | The expectations survey is the cleanest read on whether the energy spike is unanchoring household inflation views. Watch the one- and three-year series. |

| Tuesday | NFIB Small Business Optimism (May) | Small-business hiring and price plans are the best early read on whether the narrow payroll base is broadening or thinning further. |

| Wednesday | Consumer Price Index (May) | The main event. We expect a gasoline-driven headline with core firmer than comfortable. The print sets the tone for Warsh’s first meeting the following week; watch core services and shelter. |

| Thursday | Producer Price Index (May); Initial Claims | PPI confirms or complicates the CPI read on pipeline pressure. Claims remain the highest-frequency labor signal and sit near historic lows. |

| Friday | Import Prices (May); Univ. of Michigan Sentiment (June, prelim.) | Import prices capture tariff and dollar pass-through. The Michigan inflation expectations are the market’s preferred sentiment gauge into the FOMC. |

The open questions for the week are whether the May CPI confirms that the energy impulse is staying in the headline rather than broadening into core, whether the small-business and claims data corroborate the firmer, broader labor read, and whether the weekend escalation with Iran is contained by Washington’s pressure on Israel or spirals into the strait. A hot CPI on top of the strong jobs print would harden the market’s new bet on a hike and frame an uncomfortable first meeting for the Warsh Fed the following week.

Scenario Framework

| Scenario | Macro & Market Implications | Corporate Finance Action |

|---|---|---|

| Base Case 55% |

Sunday’s missile exchange stays contained because Washington restrains Israel; the indirect channel reopens and Hormuz normalizes by late summer; Brent drifts toward the mid-$80s. Labor stays firm and broadening, though the long-term-unemployed share keeps rising. Warsh Fed holds in June with a hawkish tone; no cut in 2026, first move pushed to 2027 and conditional. The market’s hike bet fades as oil eases. 10-year holds 4.40–4.70%. | Lock fixed-rate funding opportunistically. Stay with productivity-led capex. Model a no-cut-in-2026 base path. Treat equity concentration as a conditions risk. |

| Upside 15% |

De-escalation sticks and the U.S.–Iran MOU is signed; Hormuz reopens cleanly; Brent toward $75. Energy disinflation lets the trend measures resume their drift lower and pulls the long-term unemployed back in. Fed gains room for one cut late in the year. | Step up productivity-led capex. Open the refinancing window. Lean into an energy-sensitive demand recovery. |

| Downside 30% |

Israel retaliates despite U.S. pressure, or a fresh incident closes the strait; Brent back above $115. Headline CPI re-accelerates and the better gauges follow, validating the market’s hike bet. The Warsh Fed is forced to weigh a hike into a falling stock market. Equity concentration unwinds further; consumer-credit and long-term-unemployment stress deepen together. | Stress-test floating-rate exposure and covenant headroom. Build liquidity. Defer non-essential capex. Hedge energy and freight. |

Forecast Update

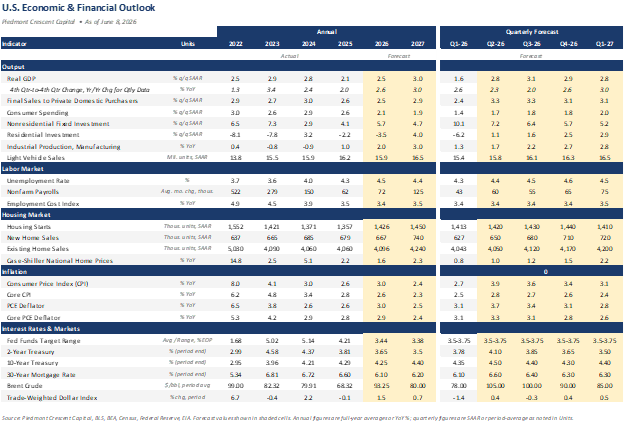

Our full U.S. economic and financial outlook is below, updated for this week’s data and the revised policy path. The headline change is the rate trajectory: with the labor market firmer, slack dissipating, and inflation pressures intact, we no longer carry a 2026 cut in the base case and have nudged up the near-term yield profile. Forecast values are shown in the shaded cells.

This commentary reflects the views of the author as of the date noted and is provided for informational purposes only. It does not constitute investment advice or a recommendation to buy or sell any security. Information has been obtained from sources believed to be reliable, but accuracy and completeness are not guaranteed. Past performance is not indicative of future results. © 2026 Piedmont Crescent Capital.