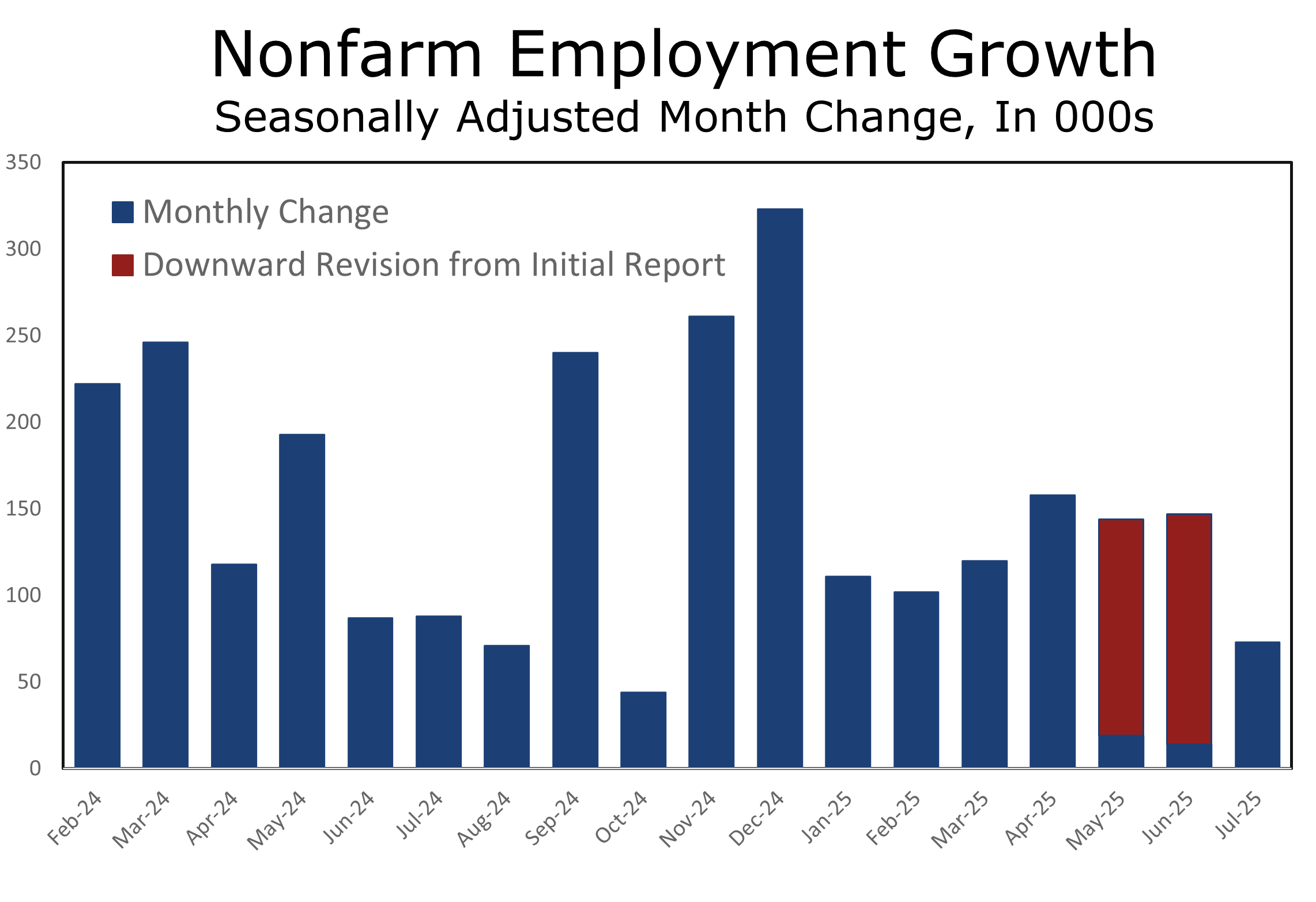

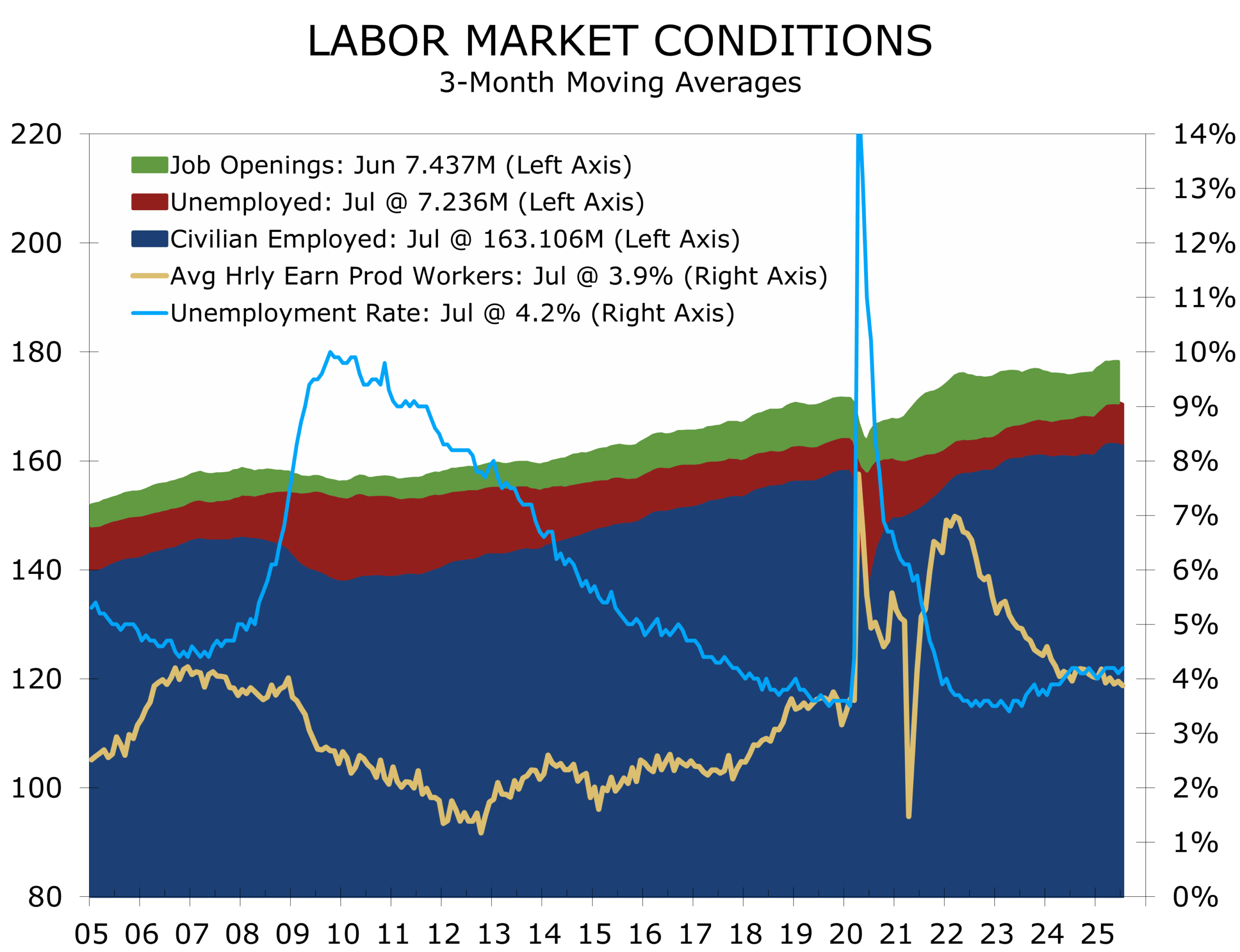

Weaker Payroll Growth is Finally Apparent

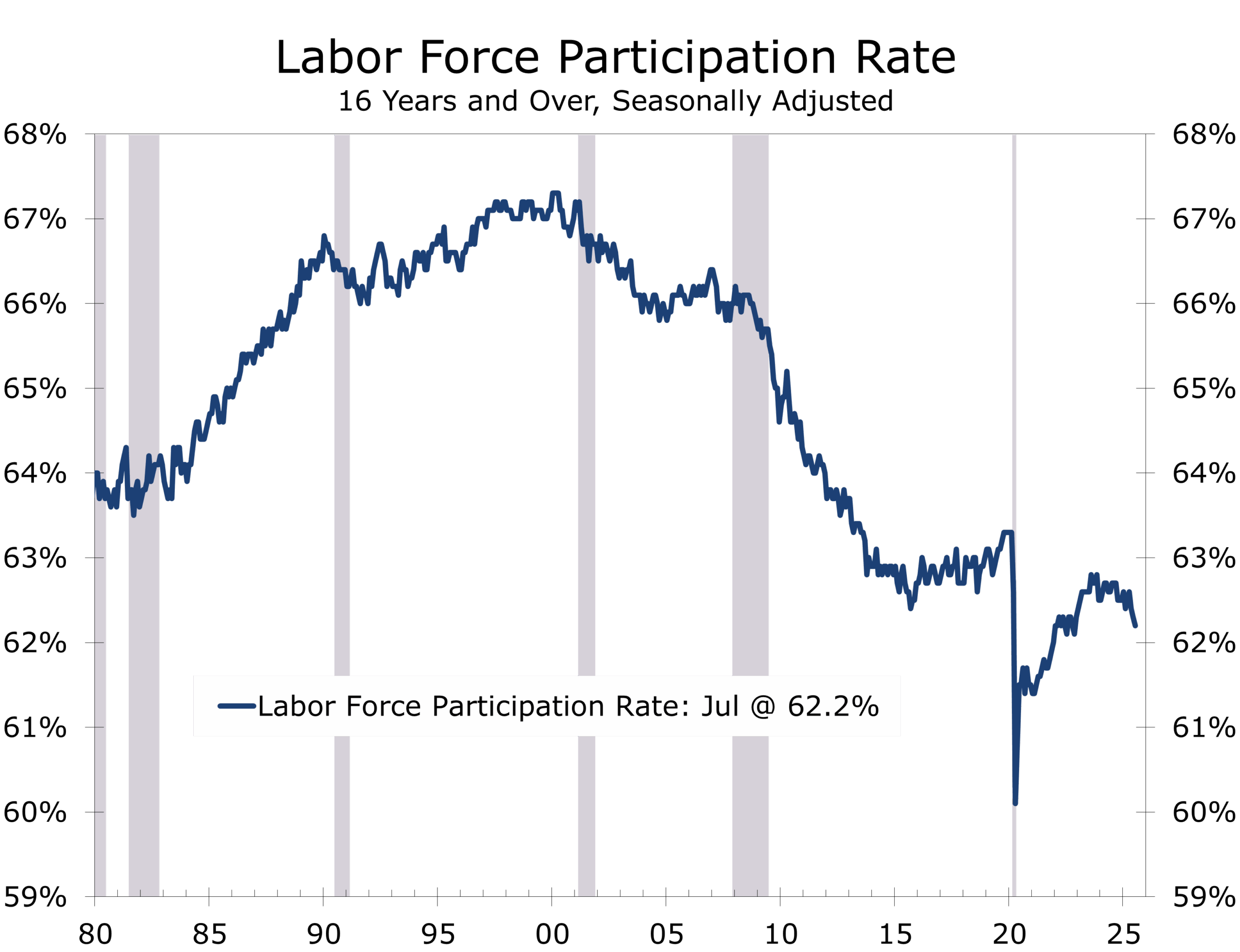

Unemployment is Also Deceivingly Low

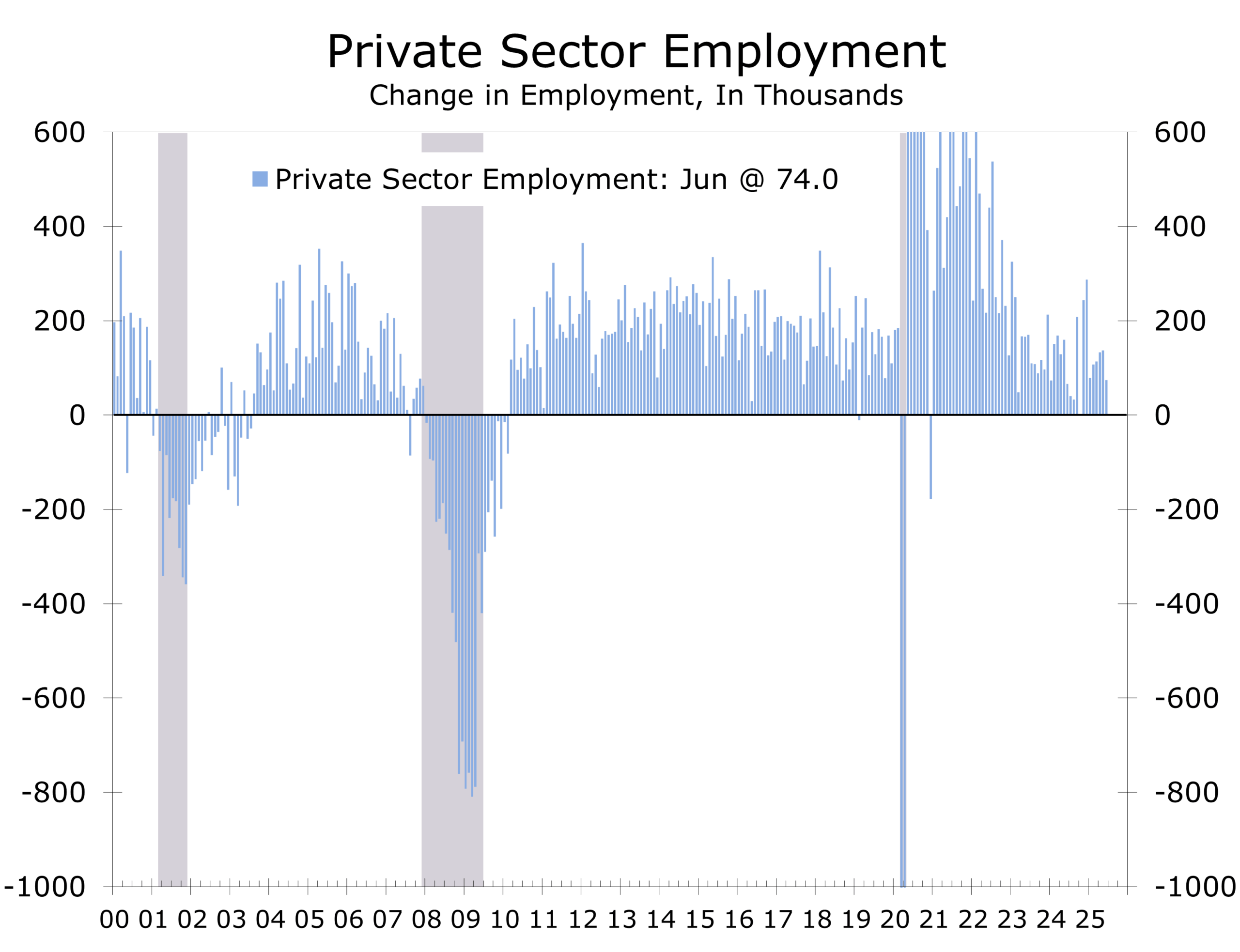

- Nonfarm payrolls rose just 73,000 in July, with steep downward revisions of 258,000 to May and June. The three-month average now stands at just 35,000.

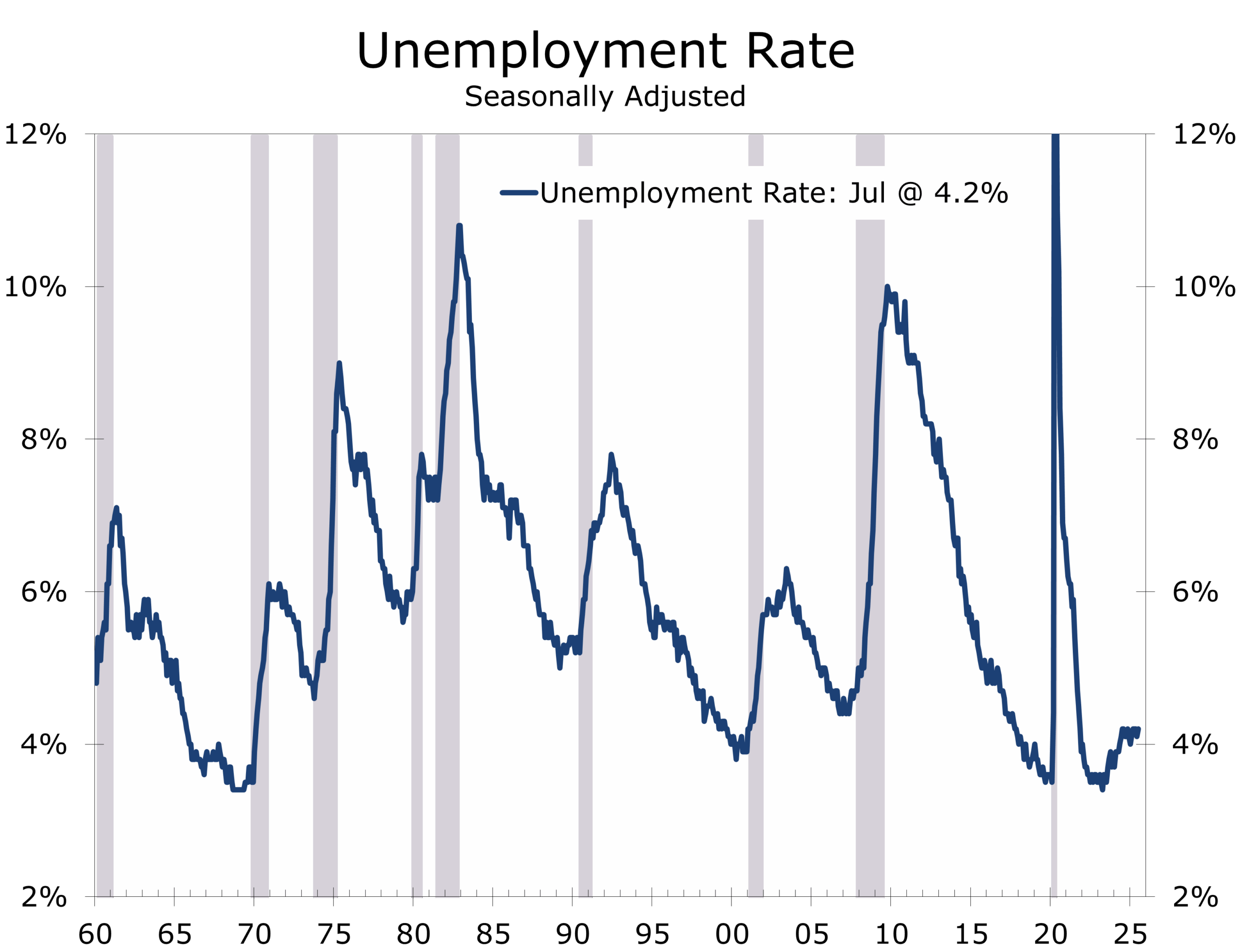

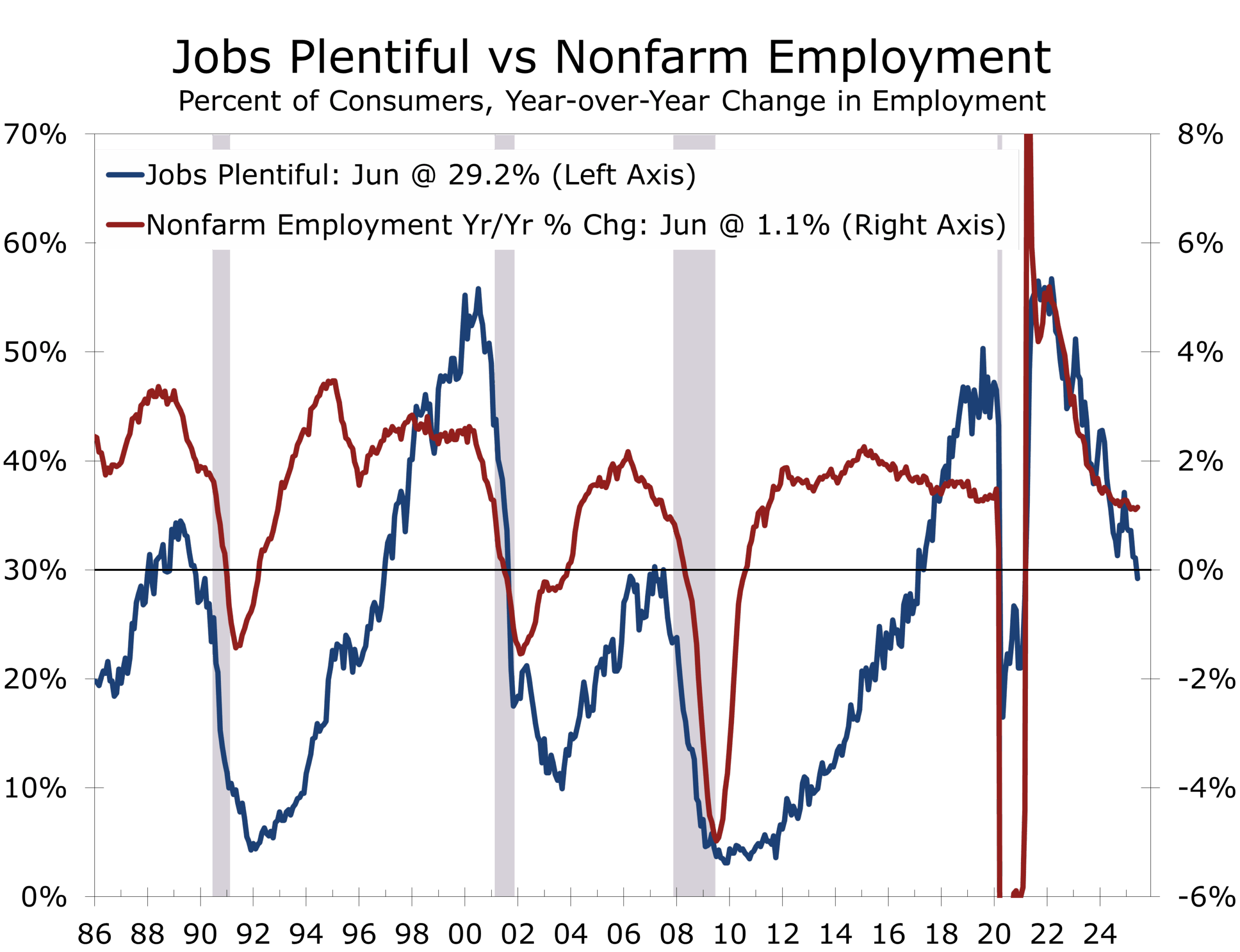

- The unemployment rate rose to 4.2%, but labor force participation fell to 62.2%, the lowest since the pandemic recovery.

- Long-term unemployment rose by 179K to 1.8 million, the highest since early 2022, and accounts for nearly 25% of unemployment

- Payroll gains were narrowly concentrated in health care (+55K) and social assistance (+18K). Most other sectors flat or declining.

- Federal government payrolls fell another 12K in July and are down 84K year-to-date.

- Household survey data showed a loss of 260,000 jobs, while the employment-population ratio slipped to 59.6%.

- Average hourly earnings rose 0.3% in July and are up 3.9% y/y. The workweek edged up to 34.3 hours, within its recent range.

- Tighter immigration enforcement and accelerating retirements have likely constrained labor supply, suppressing the unemployment rate. Adjusted for these trends, the jobless rate would likely currently be between 4.5% and 5%.

A Weak Report with Deceptively Stable Optics

The July employment report reveals a labor market losing altitude at an accelerating pace. Nonfarm payrolls rose a modest 73,000, but downward revisions to May and June erased 258,000 previously reported jobs. Over the past three months, job growth has averaged just 35,000—well below replacement level and consistent with recessionary conditions. When adjusted for likely overstatement in the establishment survey, the underlying trend may be close to flat.

Job gains were once again narrowly concentrated in health care (+55,000) and social assistance (+18,000). Construction, manufacturing, retail, professional services, and information were flat or negative. Federal employment fell by another 12,000 and is down 84,000 year-to-date. Private hiring breadth remained weak, with the total private diffusion index rising only slightly to 51.2 and the manufacturing index slipping to 43.8.

Job growth has become dangerously narrow, and unemployment appears understated.

Labor Force Shrinks, Long-Term Unemployment Rises

The unemployment rate rose slightly to 4.2%, but that low rate masks significant deterioration beneath the surface. Labor force participation slipped to 62.2%—the lowest since the pandemic recovery—while the employment-population ratio fell to 59.6%. These declines reflect both cyclical weaknesses, especially among younger workers, and structural pressures from tighter immigration and an aging workforce.

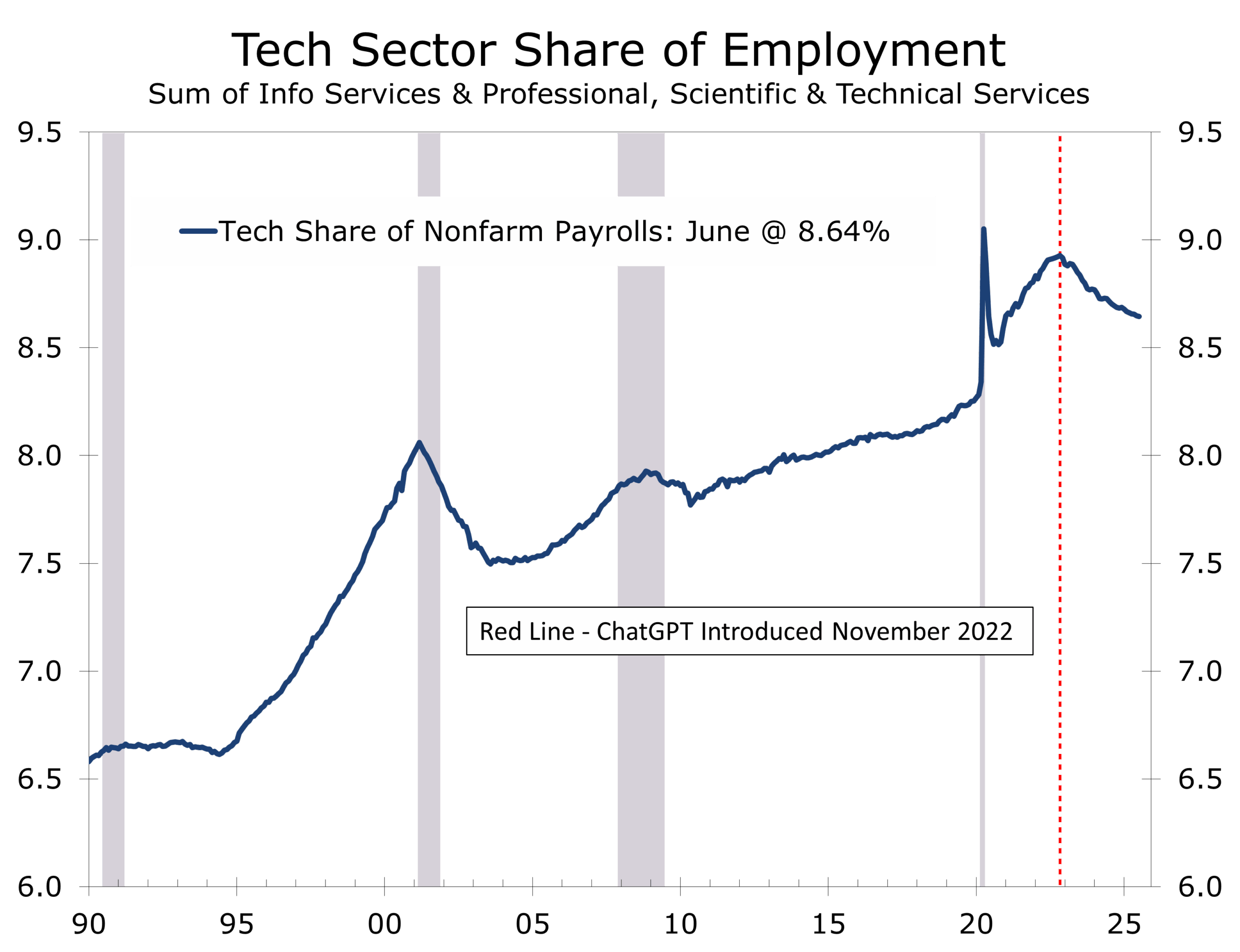

The household survey showed a net loss of 260,000 jobs in July. Long-term unemployment rose by 179,000 to 1.8 million—the highest since early 2022—and now accounts for nearly a quarter of the total unemployed, a troubling indicator historically tied to weakening labor demand and emerging AI-related displacement. Tech’s share of employment has declined since the launch of ChatGPT in November 2022. A narrow subset of tech-related roles we track within information and professional and technical services has now fallen for seven consecutive months, losing 12,300 jobs in July and 33,200 over the past three months.

AI disruption is quietly reshaping white-collar employment—and likely just getting started.

The True Unemployment Rate Is Likely Higher

The official 4.2% jobless rate is not fully reflecting labor market weakness. Structural constraints—particularly tighter immigration enforcement and accelerating Baby Boomer retirements—have limited labor force growth and artificially suppressed the headline unemployment rate. Economists estimate that absent these distortions, the true unemployment rate would be 4.5% or more.

As a result, job gains of just 35,000 a month were enough to stabilize the unemployment rate, whereas in prior years such a low print would have pushed it sharply higher. The decline in labor force participation confirms that the drop in joblessness is increasingly being driven by exits from the labor force, not hiring.

Tariffs and Uncertainty Continue to Weigh on Hiring

The drag from policy uncertainty is growing. President Trump’s latest tariffs—imposed just ahead of a August 1 deadline—have added a 35% duty on Canadian imports and expanded duties on dozens of trading partners. Businesses are reacting with hiring freezes and greater selectivity. Temporary help, retail, and tech services remain weak. The previously reported stability in the factory sector also looks suspect, with revised data showing a bit more weakness.

The Fed has the evidence to cut—waiting may turn the slowdown into a downturn.

A September Cut Might be Too Late

Downward revisions, rising long-term unemployment, flat household employment, and a declining participation rate all point to a labor market steadily losing steam. We estimate payrolls are overstated by about 50,000 jobs per month, suggesting employment may have actually declined in both May and June—back-to-back drops are rarely seen outside of recessions. The Fed now has sufficient data to justify a rate cut by September; the real question is whether waiting that long will prove too late. There was a time when the Fed would act decisively after a clearly weak jobs report. This may be one of those moments.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

August 1, 2025

Mark Vitner, Chief Economist

(704) 458-4000

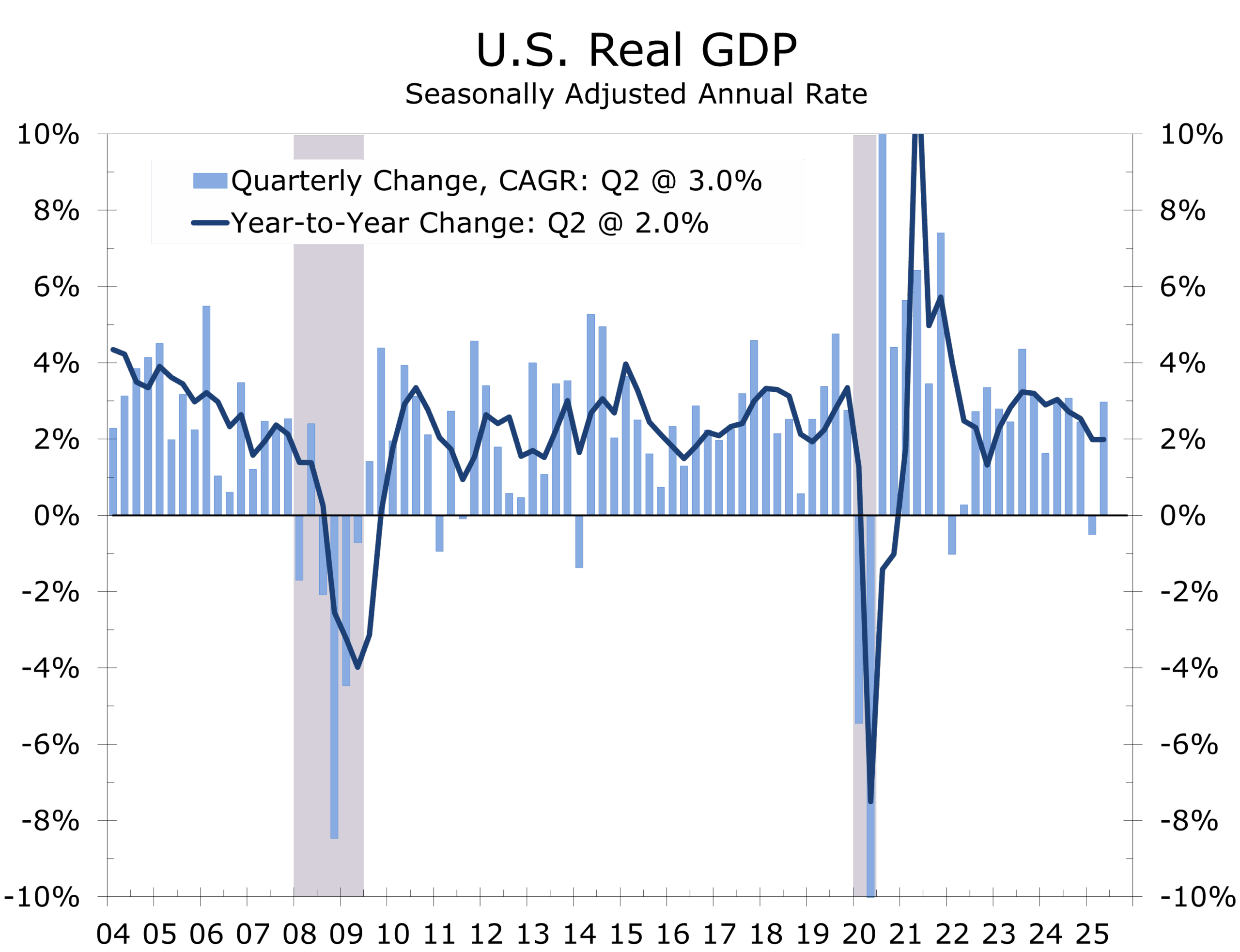

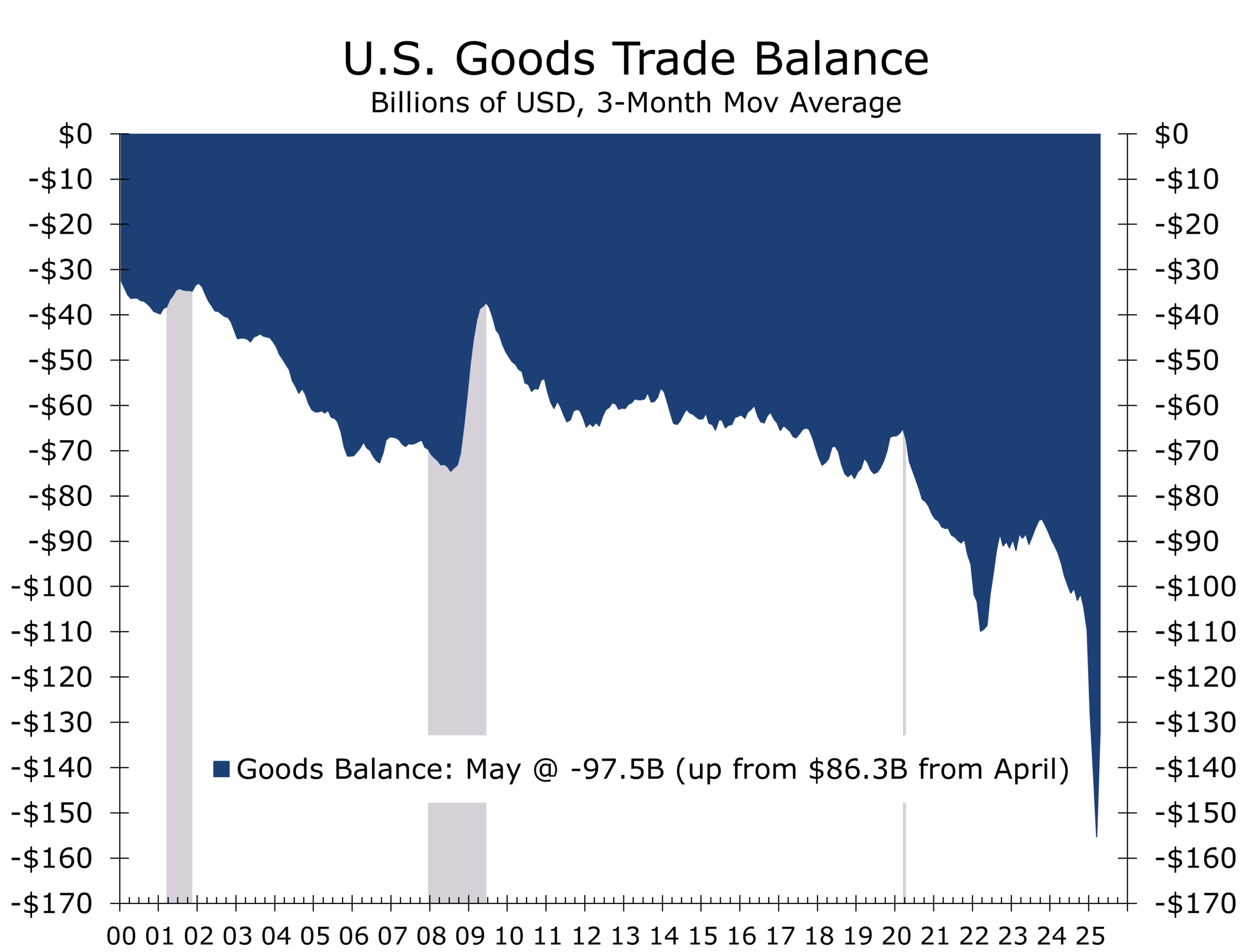

Output Rises Modestly Through Tariff Distortions

Domestic Demand Growth Slows to 1.2% in Q2, Averages 1.55% in First Half

- Real GDP rose at a 3.0% annual rate in Q2, reversing Q1’s 0.5% contraction

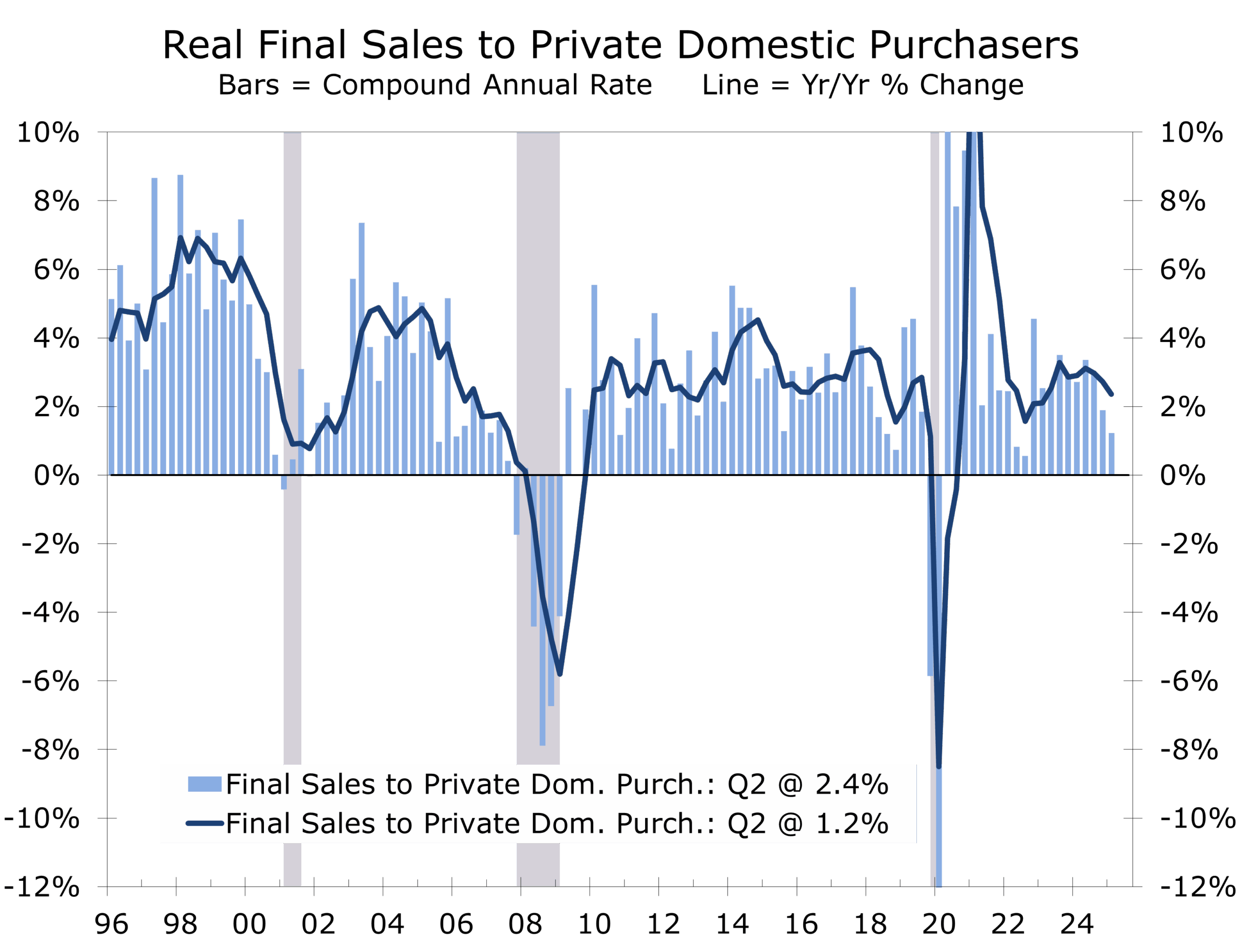

- Final sales to private domestic purchasers—a key gauge of core domestic demand—rose just 1.2%, the slowest pace since Q4 2022

- Trade dynamics reversed: net exports added 5.0 ppt to growth after subtracting 4.6 ppt in Q1

- Consumer spending edged up at a 1.4% annual rate, with goods purchases rising 2.2% and services outlays climbing 1.1%

- Business fixed investment rose at a 1.9% pace, with solid gains in equipment and intellectual property

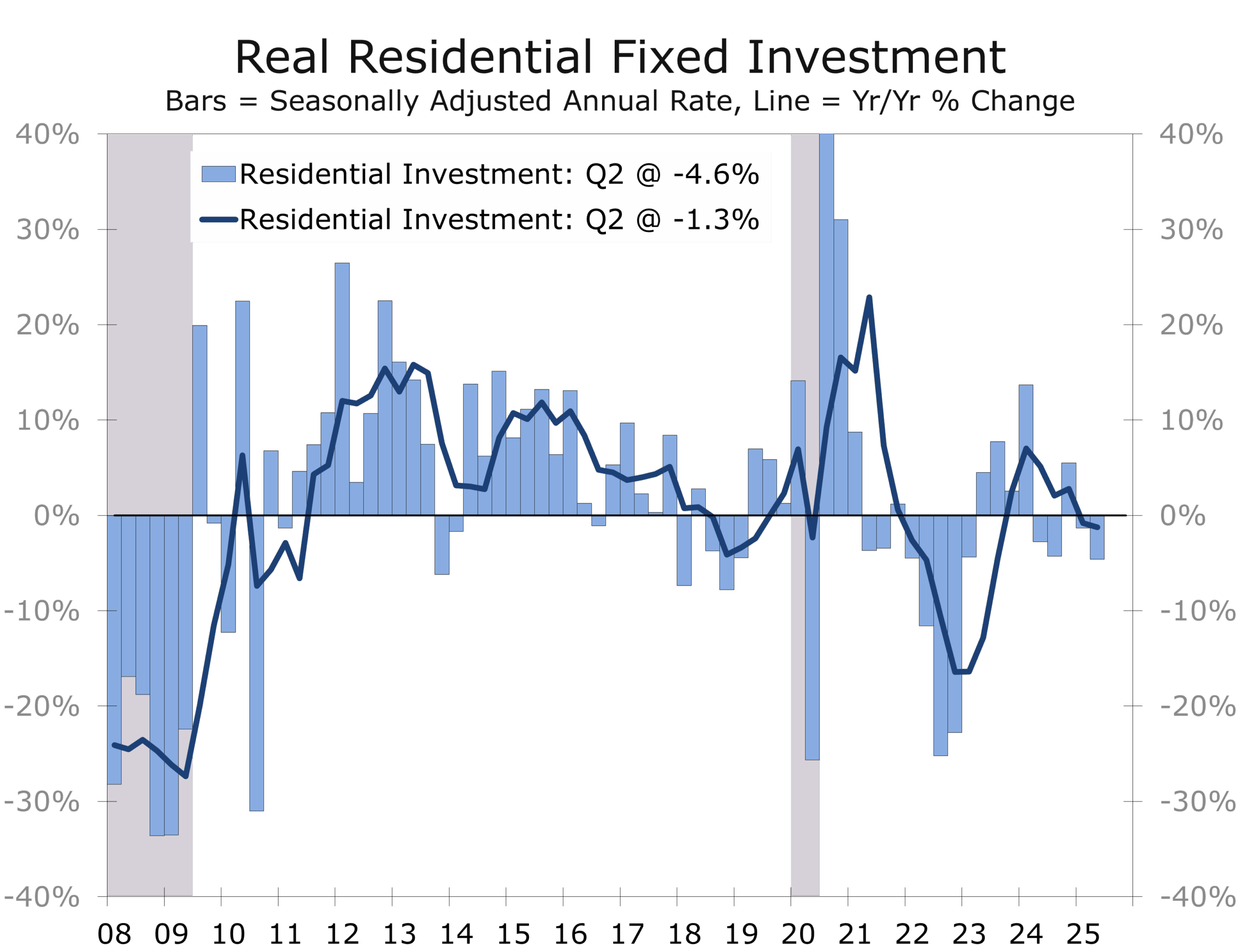

- Residential investment declined 4.6%, reflecting weaker home sales and a dwindling pipeline of new construction

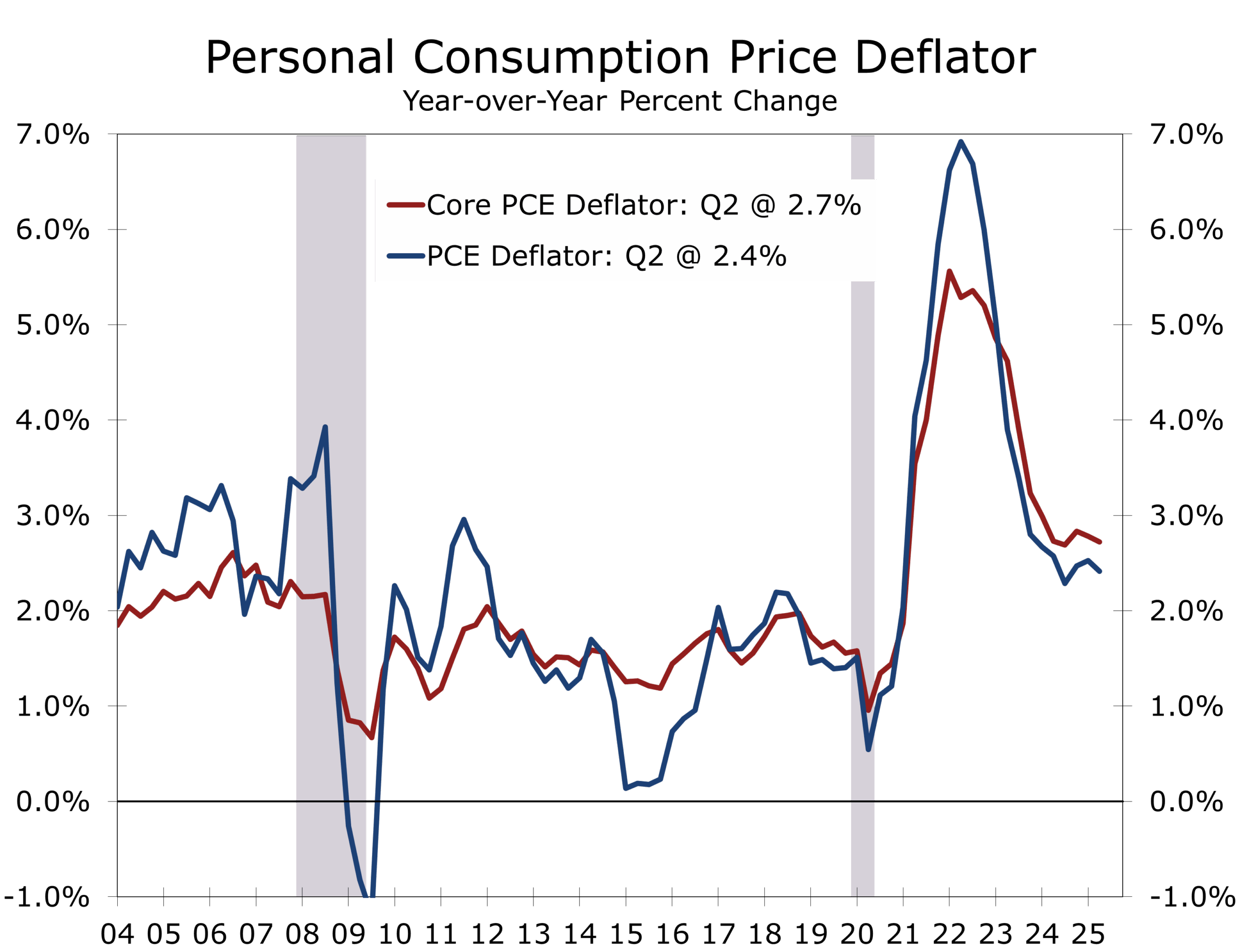

- The GDP price index rose 2.0%; Core PCE inflation increased at a 2.5% pace, while the overall PCE deflator rose just 2.1%. On a year-over-year basis, inflation is running at 2.4%, and Core PCE at 2.7%. Though above the Fed’s 2% target, the central bank retains room to ease restrictive policy

GDP Growth Rebounds on Trade Reversal, But Underlying Demand Cools

Real GDP expanded at a 3.0% annualized pace in Q2 2025, exceeding the consensus forecast of 2.4% and sharply reversing Q1’s 0.5% decline. The better-than-expected print followed reports of a much smaller May goods trade deficit, which lifted net exports.

The underlying economy, however, delivered far more modest gains—closer to 1.5%. Much of the bounce reflects reversing trade distortions that have clouded GDP readings for two quarters running.

In Q1, businesses accelerated imports to beat sweeping new tariffs, causing net exports to subtract 4.8 ppt from GDP growth. That flipped sharply in Q2 as imports normalized, driving net exports to add 5.0 ppt to growth.

Tariff Reversal Drives 5.0 ppt Boost to GDP. Core Domestic Demand at Two-Year Low.

A simple average of the two quarters shows roughly 1.25% growth. Final sales to private domestic purchasers climbed 1.2% in Q2, down from 1.9% in Q1 and marking the weakest core GDP reading since Q4 2022—highlighting how trade volatility is obscuring underlying demand.

Consumer Spending Cools, Business Investment Softens

Consumption rose only 1.4% in Q2. Goods spending was supported by a 2.2% gain (nondurables +3.7%, durables +1.3%), while services rose 1.1%—an improvement from Q1’s 0.6%, but still below trend. Rising imports may be crowding out domestic-focused services like travel and dining, which are clearly softening.

Business fixed investment grew a modest 2.3%. Equipment spending rose 4.4%, while intellectual property products posted a strong 6.4% gain. Structures investment remained weak, reflecting challenges in commercial and energy sectors. Declining nondefense capital goods orders hint at possibly slower capex ahead—but we expect investment activity to revive later in 2025 and into 2026 as policy uncertainty subsides.

Housing Slumps to Worst Pace Since 2002. Capex Holds—But Outlook Turns Cautious.

Housing Drag Grows, but Weakness Could Be Short‑Lived

Residential investment fell 4.6%, the steepest drop since Q4 2002. A slowdown in home sales and an inventory build from completed, unsold units lifted vacancy rates and weighed on activity. Homebuilders face higher financing costs and waning demand. The drag is compounded by falling commission income, another component of residential investment. Housing may remain a headwind until mortgage rates ease and excess inventory is absorbed.

Overall government spending was unchanged. Federal outlays declined 3.7%—largely reflecting a pullback in nondefense spending (-11.2%), possibly due to DOGE initiatives. DOGE launched via executive order in January 2025 to modernize federal operations and cut waste. Defense spending rose 2.2%, while state and local outlays grew at a 3.0% pace.

Inflation Softens, Policy Flexibility Expands

Inflation trends eased in Q2. The GDP deflator rose 2.0%, with Core PCE inflation at 2.5%. Year-over-year, headline PCE stands at 2.4%, while Core PCE is 2.7%. Despite remaining above target, the moderation supports the possibility of upcoming rate cuts.

The Fed has room to ease despite inflation running slightly above its 2% target.

Murky Growth Outlook Persists Into H2

While the 3.0% GDP growth is eye-catching, beneath the surface the economy is growing more slowly. Weaknesses in final sales and trade distortions suggest muted momentum ahead. With nearly 60% of imports still uncovered by trade deals and persistent uncertainty over trade policy, growth is expected to average only about 1% in the second half of 2025.

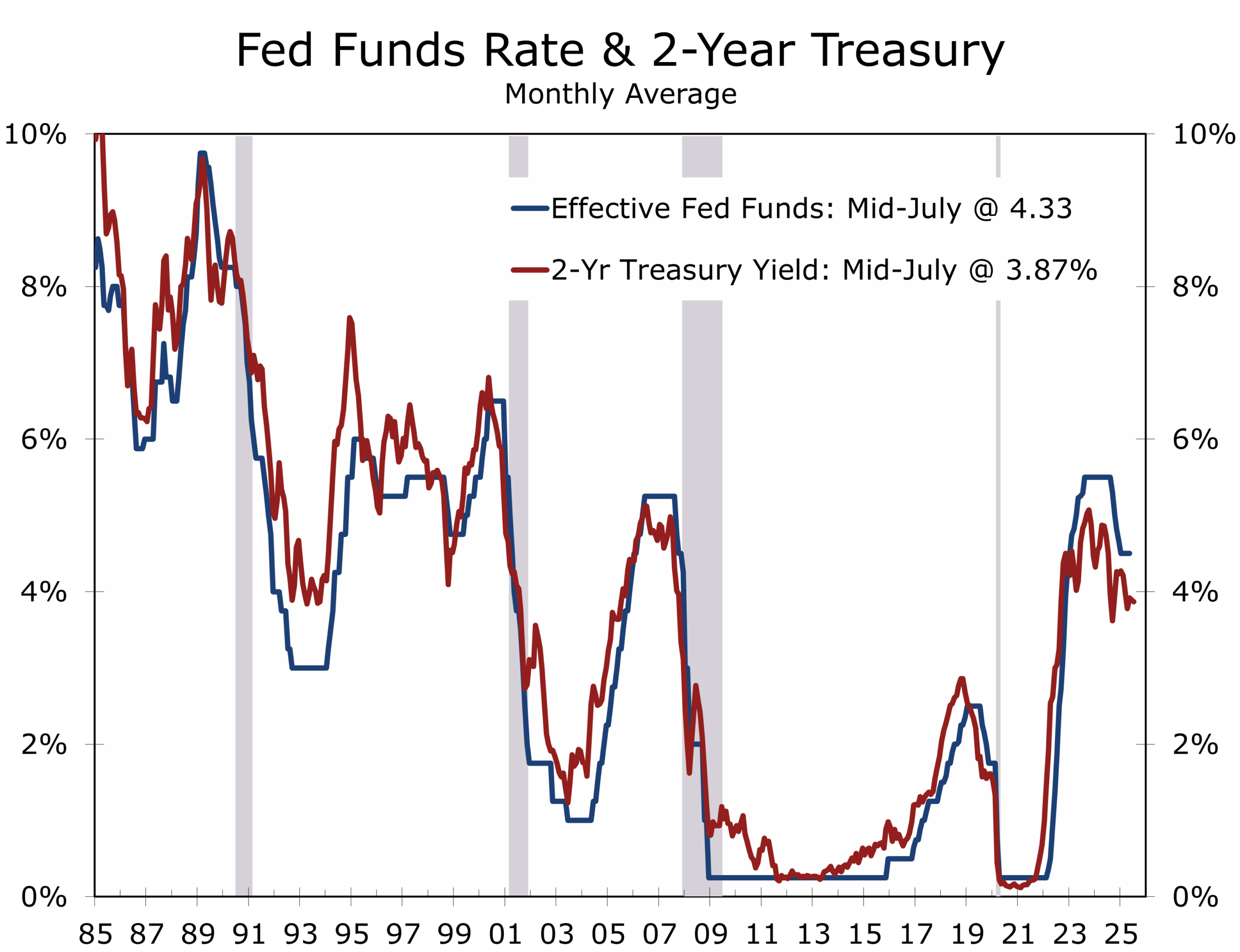

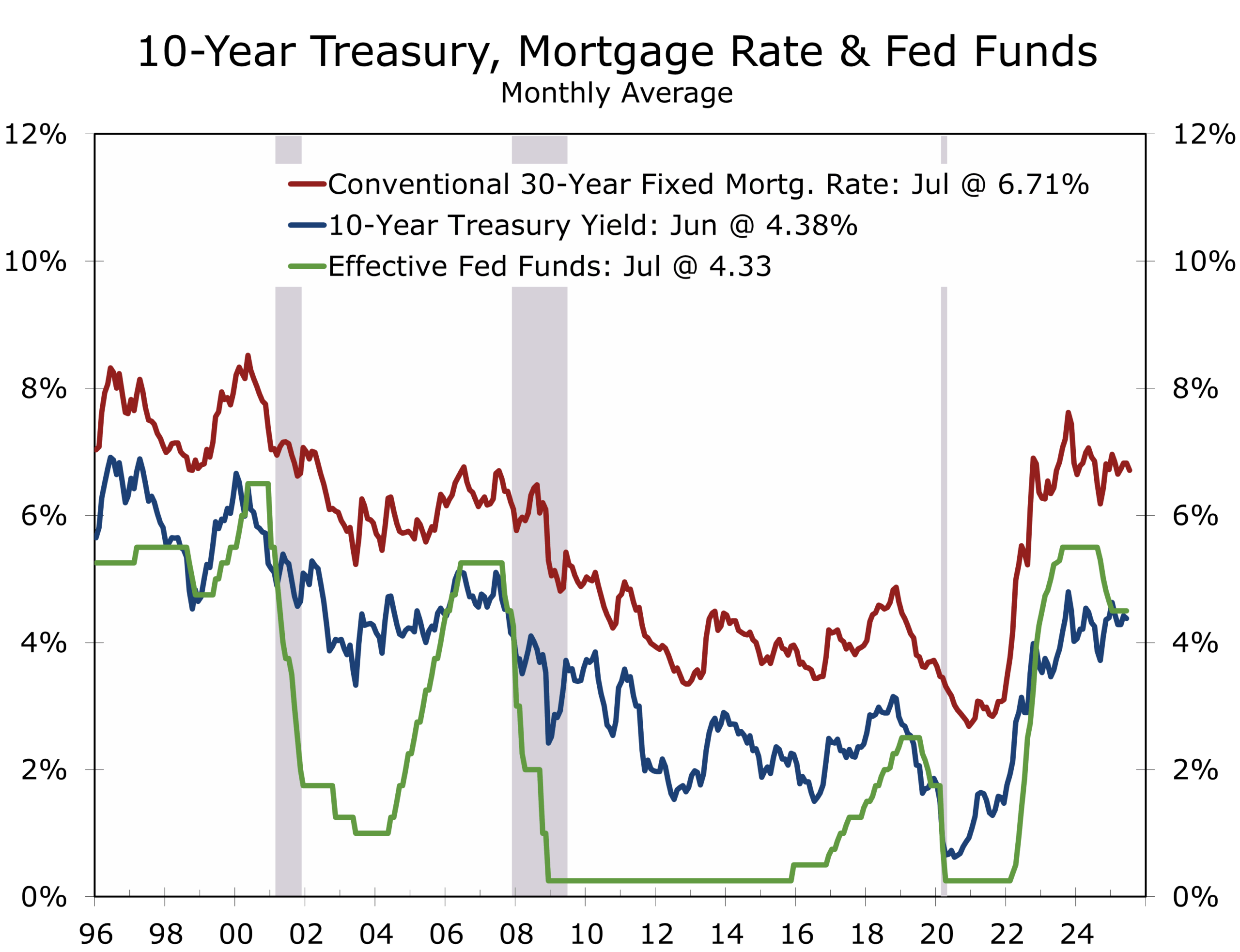

The Fed is expected to maintain its policy rate at 4.25%–4.50% at the July FOMC meeting but may initiate up to three rate cuts by year-end. Clear signaling will be needed to reassure markets that easing is possible with inflation above target, which be made easier give softening labor conditions. While a recession is not forecast, near-term risks are elevated compared to 2026. Clarity on trade policy and lower rates may help shift the landscape later in the year as business investment and housing gradually improve.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 30, 2025

Mark Vitner, Chief Economist

(704) 458-4000

Expectations Improve, Yet Downside Risks Remain

Confidence Firms as Labor Slack Deepens

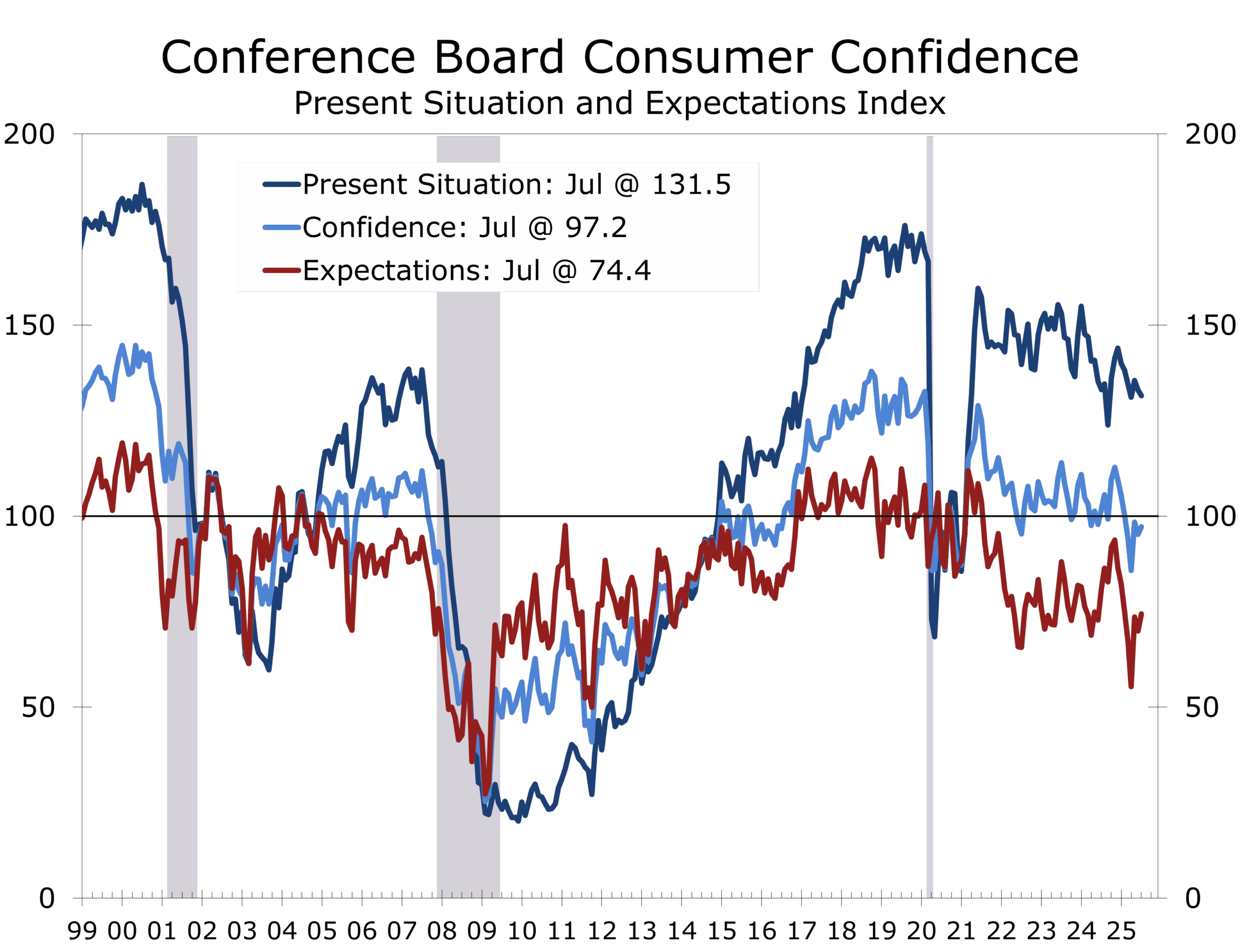

- The Conference Board’s Consumer Confidence Index® rose 2.0 points to 97.2 in July.

- Consumers’ view of present economic conditions slipped 1.5 points to 131.5, while the Expectations Index rose 4.5 points to 74.4.

- The Expectations Index remained below the key 80 threshold for the sixth straight month—a traditional recession warning signal.

- The July 20 survey cutoff allowed consumers time to digest the “Big Beautiful Bill,” which modestly lifted sentiment among Republican respondents.

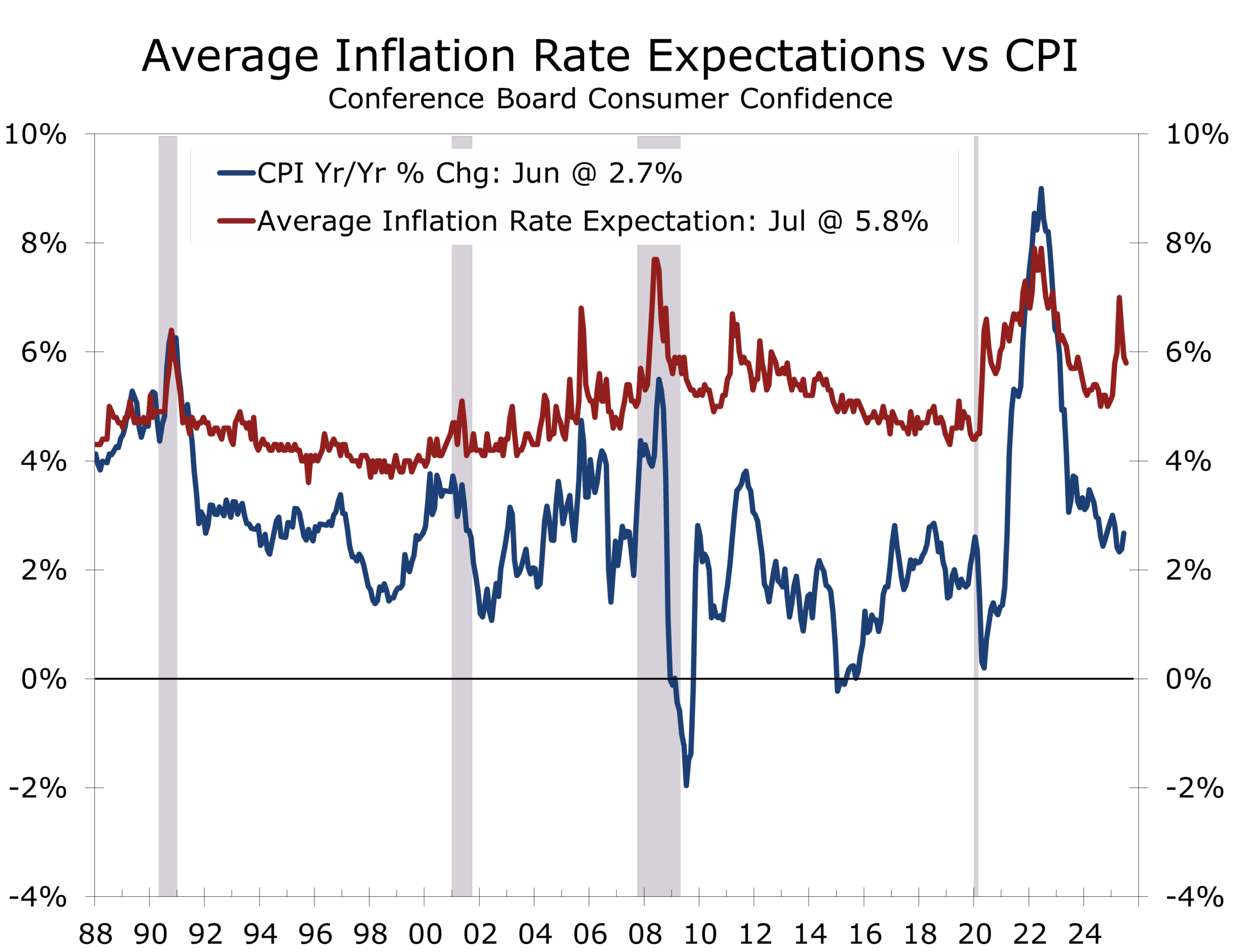

- Tariffs remain top of mind, continuing to stoke inflation fears—even as 12-month expectations eased slightly to 5.8%.

- Labor market concerns are intensifying, particularly among younger workers facing a tightening job market.

- We forecast just 90,000 net new jobs were created in July and expect the unemployment rate to tick up to 4.2%.

The Conference Board’s Consumer Confidence Index® rose 2.0 points in July to 97.2, marking a third straight monthly gain but remaining below the critical 100 level historically associated with strong economic expansion. The Present Situation Index declined 1.5 points to 131.5, while the Expectations Index climbed 4.5 points to 74.4—still under the 80 recession-warning threshold for the sixth consecutive month.

The survey’s cutoff date of July 20 allowed consumers ample time to digest the passage of the budget reconciliation package informally dubbed the “Big Beautiful Bill.” The legislation appeared to bolster sentiment among Republican respondents, while leaving Democrats relatively unmoved. Still, the bill did not rank high among consumer concerns, and few viewed it as a decisive factor shaping their economic outlook.

Tariffs, however, remain top of mind. Consumers continue to associate tariffs with higher prices, reinforcing concerns about persistent inflation. That said, the absence of a renewed inflation surge—despite the hectic pace of trade negotiations and announcements—has begun to shift perceptions. Inflation expectations edged down to 5.8% in July, a modest improvement from the 7% peak in April.

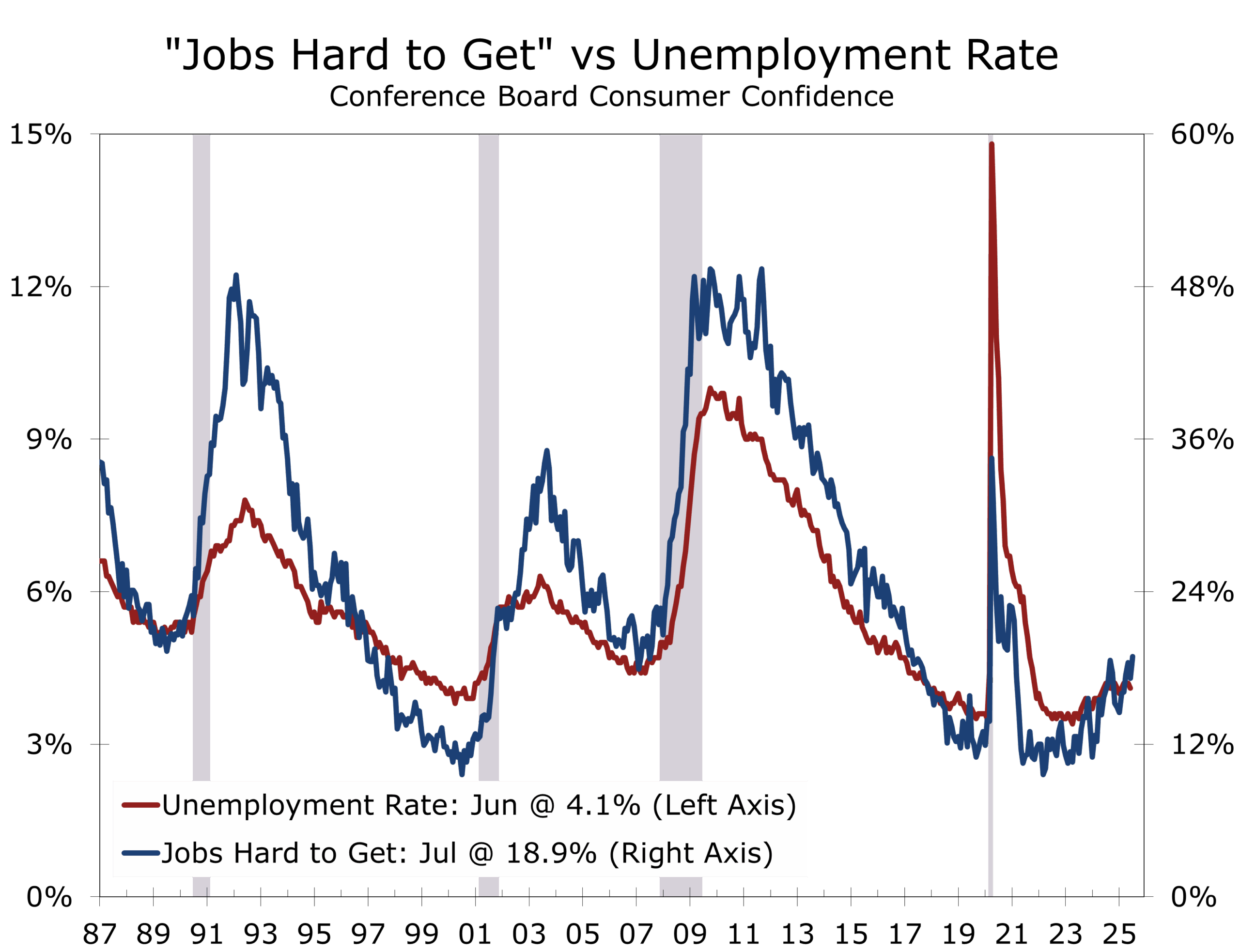

The labor market outlook continues to deteriorate. Although 30.2% of consumers still say jobs are “plentiful,” a growing 18.9% say jobs are “hard to get”—the highest reading since March 2021. The labor market differential has narrowed to just 11.3, suggesting growing concern about job availability. Notably, younger workers appear to be bearing the brunt of this shift, as firms scale back entry-level hiring. These trends support our call for just 90,000 net new jobs in July and rise in the unemployment rate to 4.2%.

While overall sentiment improved modestly, consumers earning under $15,000 reported no gains in confidence—underscoring how the hiring slowdown, inflation, rising borrowing costs are disproportionately burdening the most vulnerable households. Write-in responses revealed that tariffs remain closely tied to inflation fears, while concerns about rising credit card interest rates grew more prominent in July.

Confidence is eroding most among younger households worried about jobs and expenses.

Equity market sentiment offered a partial offset but likely to upper income households. The share of consumers expecting stock prices to rise climbed to 47.9% in July, rebounding from a 16-month low in April. This optimism, however, has not translated into stronger spending plans. Purchasing intentions for big-ticket items like appliances and vehicles remain mixed, and domestic vacation plans continued to decline—even as international travel interest ticked higher.

Spending intentions are beginning to fray. Plans to purchase cars and homes slipped modestly, though longer-term trends remain flat. Consumers’ appetite for discretionary services weakened for a second consecutive month. Dining out, travel, and lodging—previous mainstays of post-pandemic spending—saw the steepest pullbacks. Vacation intentions declined overall, with more consumers looking abroad while domestic travel plans fell.

Despite the modest headline gain in confidence, the narrowing of the gap between current and expected conditions continues to reflect a softening baseline. The number of respondents expecting a recession over the next 12 months ticked lower but remains elevated compared to pre-2024 levels.

The slight rise in confidence reflects growing unease—not growing optimism.

Consumers appear to be cautiously recalibrating their expectations following what now looks like irrational fears about tariffs. Few are confident enough to spend freely. The prevailing mood is one of restraint, shaped by uncertainty over jobs, prices, and interest rates.

Consumer confidence edged up in July, but recession risks remain embedded in the data. Tariff-driven price fears linger, even as inflation expectations ease. The labor market is cooling more visibly, with younger workers feeling the pinch first. While Republican-leaning respondents saw a confidence boost following the “Big Beautiful Bill,” broad-based concerns over inflation, jobs, and political uncertainty remain. The Fed is likely to take these mixed signals seriously as it prepares for a potential pivot in September, with three or four quarter-point cuts by spring 2026.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 29, 2025

Mark Vitner, Chief Economist

(704) 458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Tariff Diplomacy and the Global Fairway

Highlights of the Week

- The U.S.-EU trade deal narrowly avoided escalation, codifying 15% tariffs on most EU exports. The move buys time—but not a final settlement—in a broader trade realignment aimed squarely at China.

- Strategic cooperation is being reframed as large-scale foreign investment in U.S. infrastructure, energy, and defense supply chains—much of it backed by federal loan guarantees.

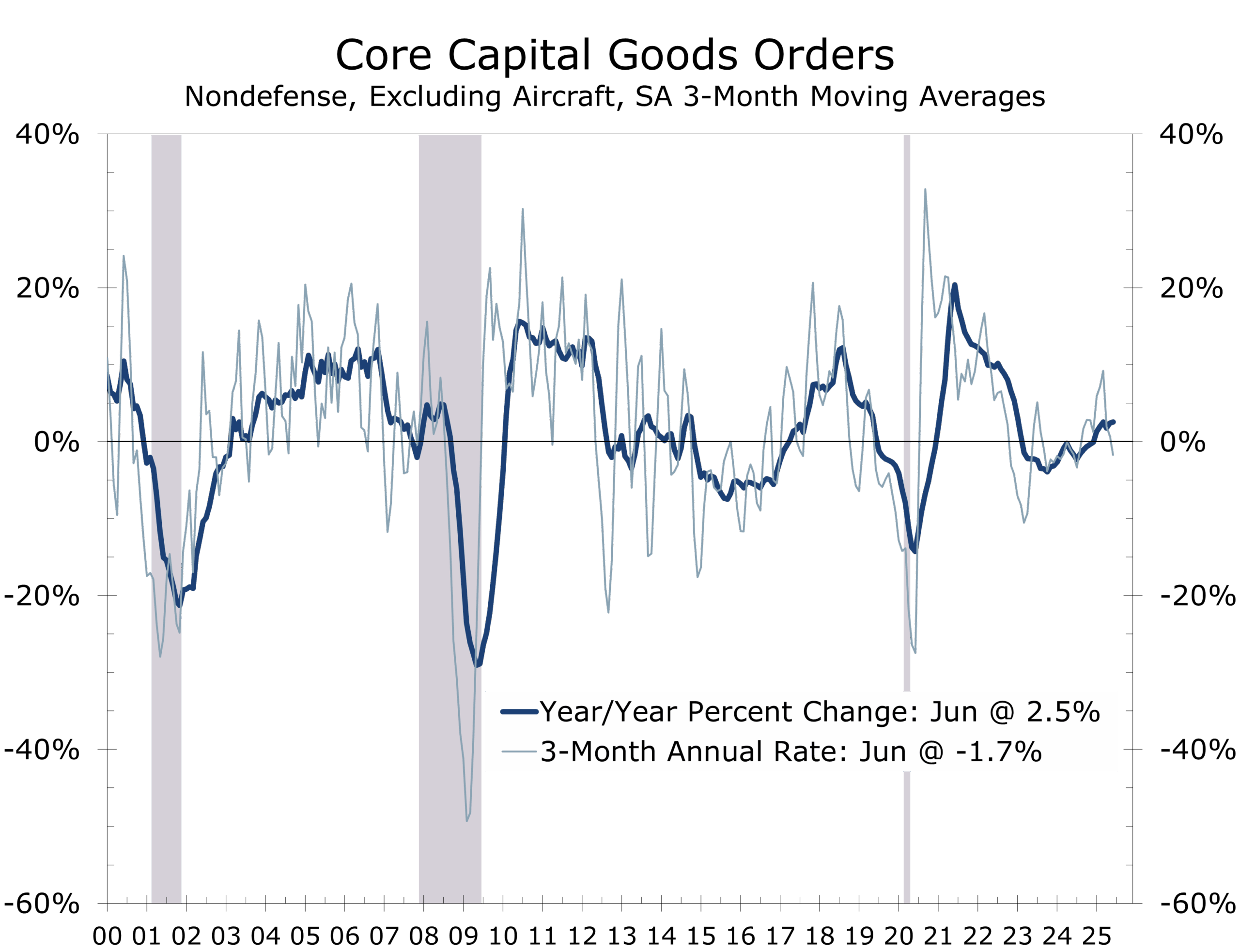

- Durable goods orders slipped less than expected, but core capital goods fell for the third straight month, pointing to softening investment amid tariff uncertainty.

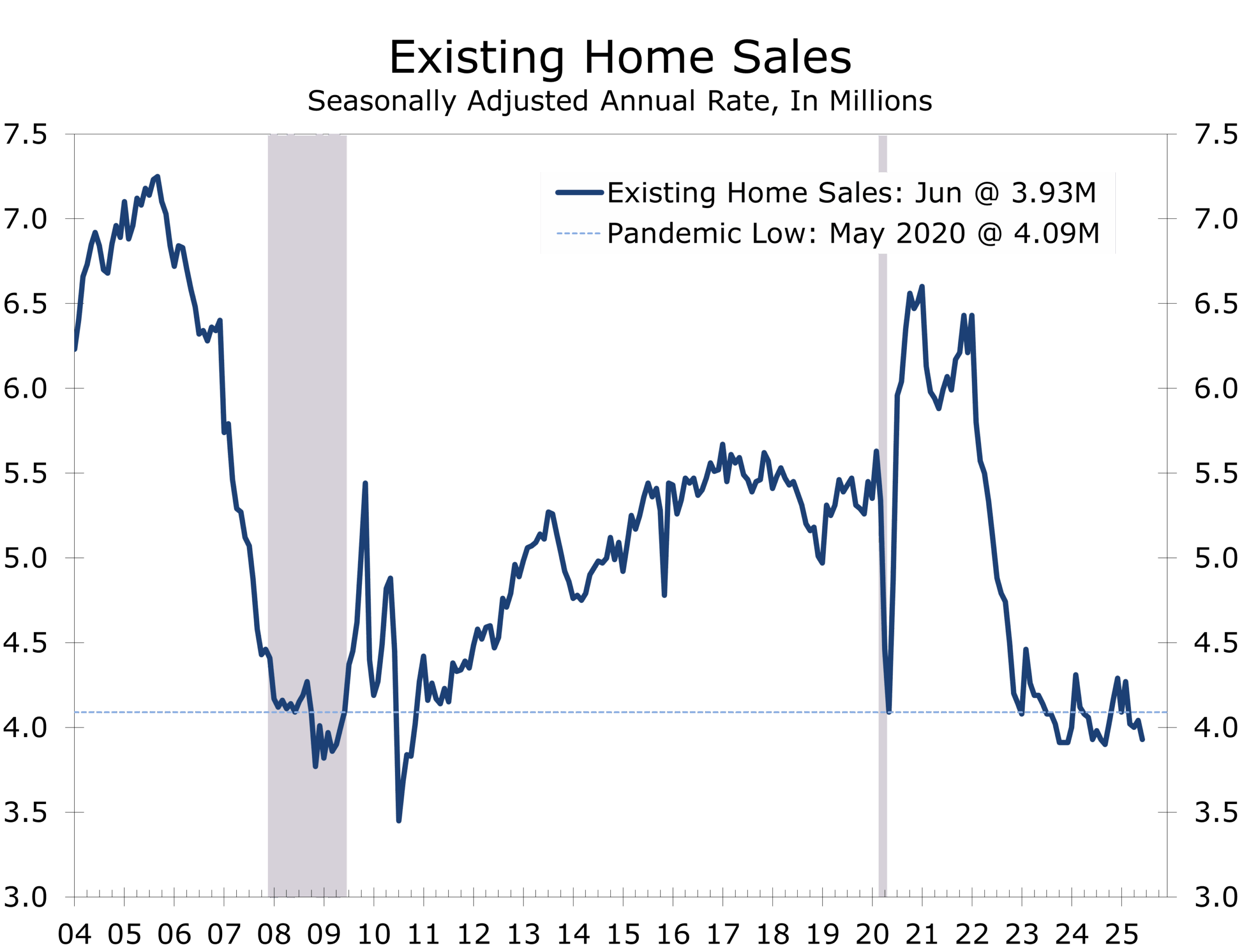

- New and existing home sales both disappointed in June, and housing inventories are building—especially at the higher end—constraining momentum for construction and consumption. The weakened state of housing is a macroeconomic concern.

- Labor market data remain mixed: initial claims edged down, but continuing claims are trending higher, suggesting fewer re-hires and weaker hiring momentum.

- Escalating conflicts Israel-Gaza and at the Thai-Cambodian border briefly rattled markets, though cease-fires and trade-linked diplomacy have helped reduce near-term geopolitical risk.

- Markets now expect the Fed to tee up a September rate cut. This week’s data onslaught—including payrolls, inflation, ISM, and the FOMC decision—will help determine the timing and magnitude of the next move.

Driving Toward China

President Trump was not merely playing through at his Scottish golf resort last week—he was laying down the contours of a new trade regime. The U.S.-EU deal announced Sunday sidesteps a tariff spike just before the August 1 deadline, setting a 15% baseline tariff on most EU exports, including autos. That is a gentler swing than the 25% some had feared, but it still embeds lasting friction into the U.S.-Europe trade relationship.

Trump is not just negotiating trade—he is improving the lie ahead of the next big shot.

The bigger game remains China. As we noted in The CAVU Compass, Trump’s approach to trade diplomacy is less about bilateral wins and more about setting the global lie ahead of a final showdown. By locking in terms with allies—Japan, Vietnam, Indonesia, and now the EU—Trump is creating a global framework designed to isolate Beijing and force its hand on critical minerals, semiconductors, and intellectual property enforcement. China is currently engaged in talks ahead of the August 1 deadline and is widely expected to strike a deal.

The structure of Trump’s trade deals is evolving into a new form of strategic cooperation—not simply tariff relief, but access to U.S. markets in exchange for meaningful investment in American infrastructure and industrial capacity. The message is clear: allies may keep their trading lanes open if they help America re-industrialize. Countries are buying into the strategy as the most effective way to manage China’s rise. There is broad recognition that the United States must remain a credible counterweight to a more assertive China.

That help increasingly takes the form of large capital commitments—many of them supported by U.S. loan guarantees—to fund energy infrastructure, logistics, and defense supply chains. A prime example is the push to unlock vast reserves of natural gas in northern Alaska. Multiple bilateral discussions with Japan and South Korea have centered on financing export terminals, pipelines, and processing hubs to bring Alaskan LNG to Asia. Similar arrangements are in discussion for critical mineral processing, semiconductor packaging, and submarine cable networks. Energy is also a key pillar of the EU deal and is intended to reduce dependence on Russian natural gas.

This is industrial policy at global scale. The new model is part trade deal, part energy alliance, and part security compact. It redefines globalization as conditional access—with terms enforced not just by tariffs, but by capital flows and strategic alignment. Tariffs are likely to settle in at a 15% base rate on all imports to the United States, lower rates on U.S. exports, and higher rates on strategic sectors such as steel, aluminum, semiconductors, and electric vehicles. Investment pledges—largely structured as loans or loan guarantees—allow the administration to claim that most of the long-term financial benefit remains in the United States. Interest payments are not profits.

Both the Japan and EU deals were par fours—difficult, but straightforward plays from the fairway. The China deal, however, is shaping up to be a long par five—narrow, uphill, and fraught with hazards. The outcome will define not just the trade balance, but the structure of the global economy for decades to come.

Trade and the Treasury Market: Sand Traps Ahead

Markets greeted the EU trade deal with cautious optimism. Treasury yields initially moved higher overnight as risk sentiment improved, but the rally quickly faded. The long end of the curve remains vulnerable to supply concerns and lingering inflation risks, with the 10-year note briefly testing support near 4.5%. While the deal provided a modest lift to the dollar, the broader trend remains downward as the Fed edges closer to a dovish pivot and the terms of trade continue to deteriorate.

The U.S. remains the cleanest scorecard in the clubhouse—and likely to remain so.

Tariff revenues are climbing, but so are investor concerns about policy unpredictability and inflation passthrough. The flurry of recent trade agreements has reduced—but not eliminated—uncertainty. The dollar’s recent weakening reflects this shift, as global investors begin to question how long the U.S. can remain the cleanest scorecard in the clubhouse.

We remain confident that the dollar will hold its status as the world’s reserve currency for the foreseeable future. While increased foreign direct investment may require producers abroad to export more to the U.S. to finance those flows, the investment itself—and the economic growth it spurs—will ultimately boost returns on dollar-denominated assets. We expect near-term softness but anticipate dollar strength to return within 18 to 24 months.

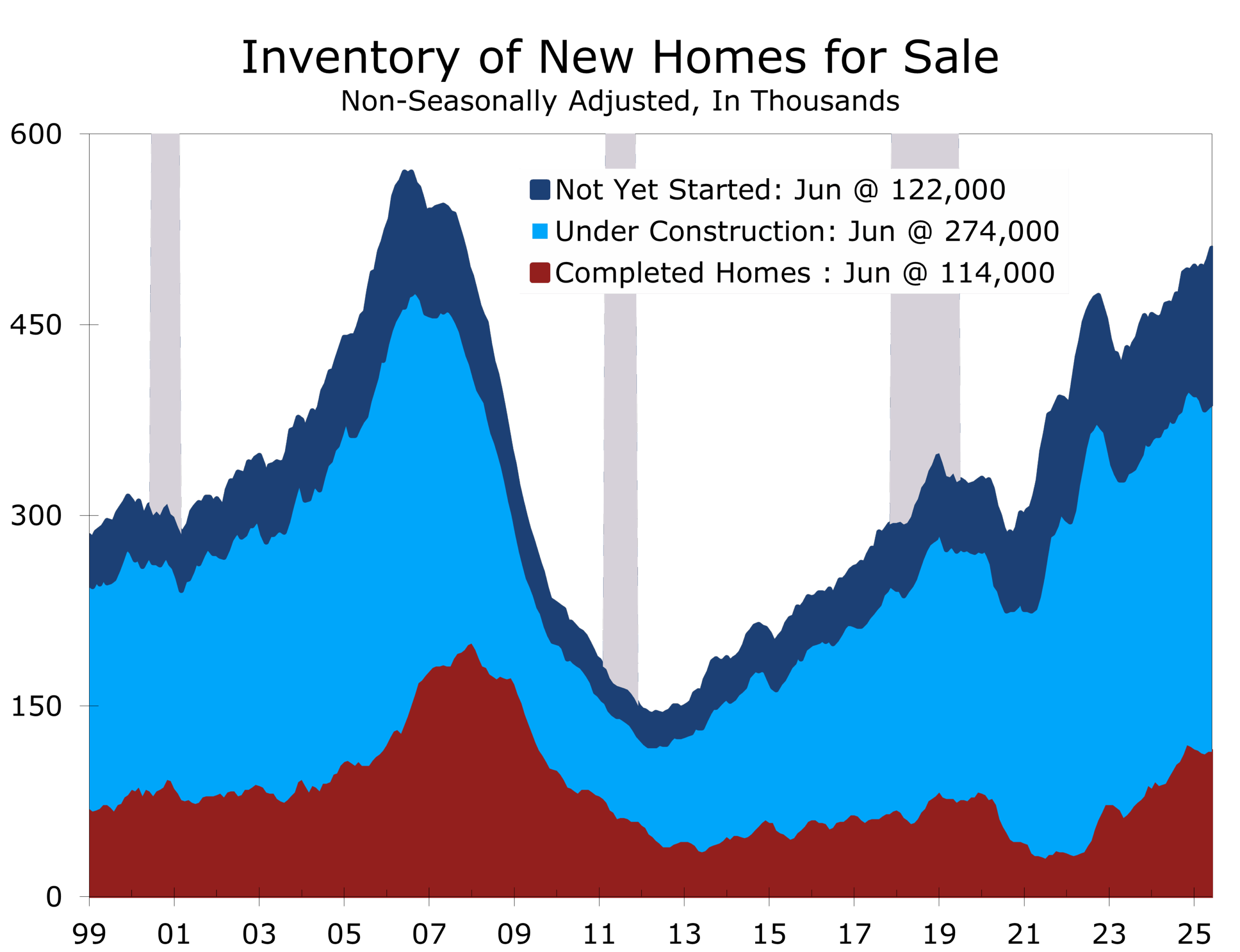

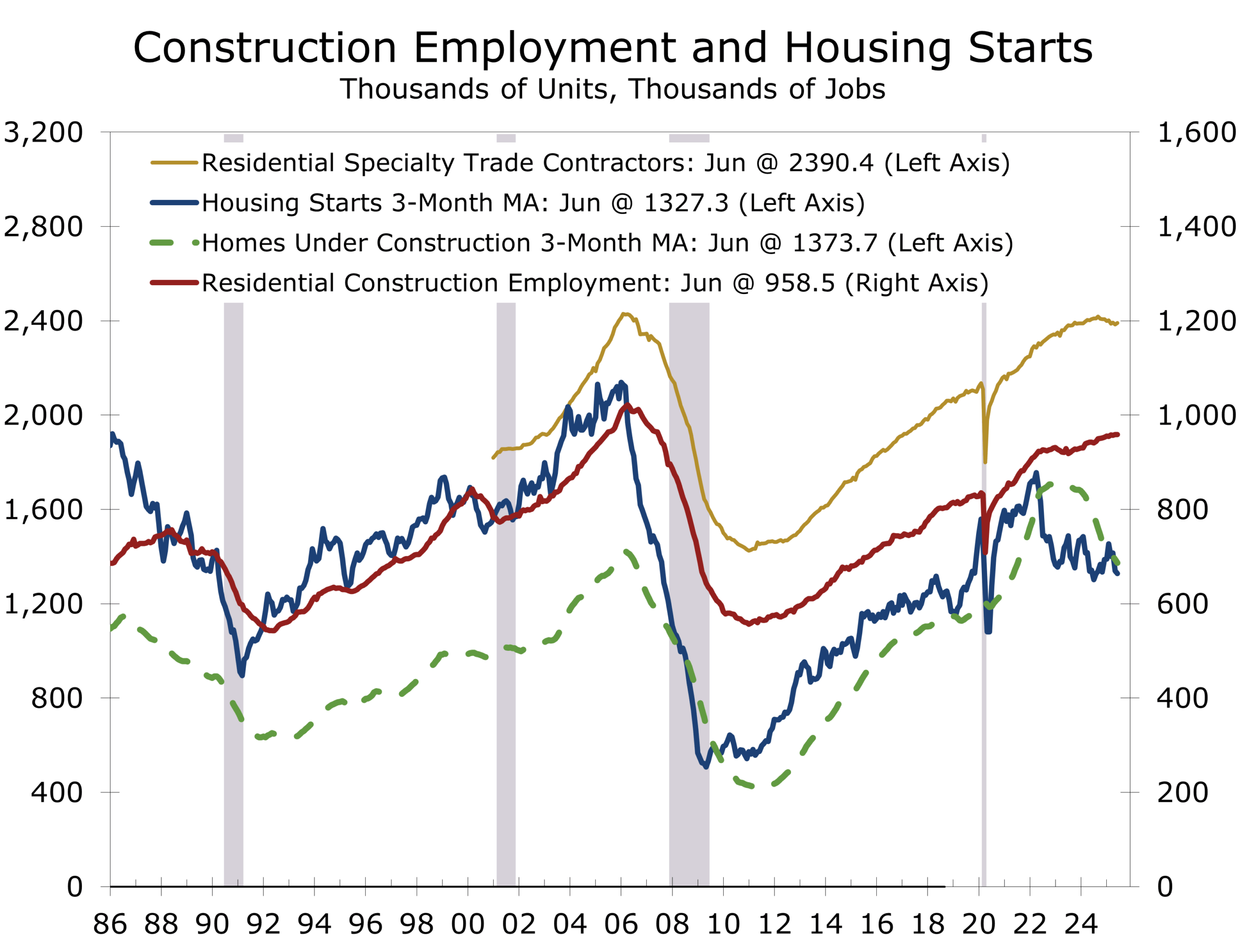

Housing Loses Momentum

June’s existing home sales fell 2.7% to a 3.93 million annual pace, nearing post-GFC lows. The median existing home price climbed to a record $435,300, but that higher median price reflects a lack of inventory at the low end, not resurgent demand. Supply remains more than adequate at the upper end of the market. New home sales edged up just 0.6% to a 627,000 pace and are down 6.6% from a year ago. Builders are leaning on incentives and price cuts to sustain sales, but inventories of completed new homes continue to climb—now at their highest level since 2009. A substantial backlog of homes under construction also persists.

Single-family permits have declined for four straight months, underscoring increased caution among builders. Higher-end inventory is accumulating, while first-time buyers remain constrained by affordability challenges and high mortgage rates. We expect sidelined buyers to return as rates move closer to 6%, but a sustained recovery is unlikely until the labor market stabilizes. New hiring and job switching have both slowed sharply over the past year, reducing mobility for both renters and homeowners.

Business Investment: Chipping Away

Durable goods orders fell 9.3% in June, which was less than expected and only partially reversed the prior month’s 16.5% spike driven by a surge in commercial aircraft orders. Capital goods orders excluding aircraft and defense fell a larger-than-expected 0.7%, marking the third consecutive monthly decline and pulling the measure back into negative territory for the quarter. Business equipment shipments also slipped, suggesting that Q2 business investment will be soft following a strong Q1.

Policy uncertainty is clearly weighing on capital spending. Trade deals—especially provisions requiring reshoring to receive tariff relief—may eventually support investment, but in the short term they are raising costs and clouding visibility. Until the fairway clears, expect firms to play it safe and lay up.

Labor: No Longer Pin-Seeking

Initial jobless claims fell to 215,000—better than expected—but continued claims edged higher to 1.96 million. The divergence suggests a labor market in transition: layoffs remain low, but hiring is slowing. Quits are down, long-term unemployment is ticking up, and recent federal layoffs—enabled by a Supreme Court ruling that curbed agency protections—are beginning to register in the data. AI adoption may also be dampening hiring in the near term, even as it boosts productivity over time. In June, private employers added just 74,000 jobs, and a separate report from ADP showed private sector headcount declining by 33,000.

The recent softness in labor market data is unlikely to trigger a panic rate cut, but it does strengthen the dovish case. Wage growth has moderated, and if the July jobs report shows sub-trend gains or an uptick in the unemployment rate, momentum could shift more decisively toward easing. The unemployment rate, however, may remain artificially low in the near term due to tighter immigration enforcement and an accelerating wave of Baby Boomer retirements.

We are looking for a soft July payroll print this Friday, with nonfarm payrolls rising by just 95,000 jobs. The unemployment rate should edge higher to 4.2%.

Geopolitics: Pressure Points, Limited Market Reaction

Two geopolitical flashpoints dominated headlines last week but left financial markets largely unmoved.

In the Middle East, renewed rocket fire from Hamas prompted fresh Israeli airstrikes in Gaza, escalating a conflict already marked by deep humanitarian strain. Civilian casualties are rising, and critical infrastructure in Gaza remains decimated. U.S. and regional mediators—including Egypt and Qatar—are pushing to restart talks, though the prospects for a durable cease-fire remain slim. Washington has urged Israeli restraint, citing risks to regional energy flows and the fragile stability underpinning the Abraham Accords.

Hamas continues to pursue a strategy aimed at maximizing civilian casualties and leveraging global media to generate sympathy abroad. The group’s stated objective—the eradication of Israel—stands in stark contrast to the portrayal in many widely circulated images, including two this weekend that were factually misleading. One featured a child with cerebral palsy, falsely presented as a typical Gaza victim; the other showed a child receiving long-term medical care in Italy for unrelated reasons.

Israel has consistently found itself on the defensive in the global PR war, with critical coverage emerging before it even responds to attacks. That dynamic has prompted Israel to take more assertive steps to deliver aid, including parachuting in humanitarian supplies—provided by other governments—via IDF aircraft. There is no viable resolution to the conflict that allows Hamas to remain in power, and the longer Hamas holds control, the more the people of Gaza are likely to suffer. That view is not unique to Israel; it is shared by several Arab governments in the region.

In Southeast Asia, Thailand and Cambodia agreed to an unconditional cease-fire after five days of deadly clashes along their contested border. The conflict, rooted in a century-old dispute over ancient temple sites, displaced more than 300,000 civilians and claimed at least 35 lives—mostly noncombatants. A breakthrough came after President Trump made a cease-fire a precondition for further trade talks, threatening a 36% reciprocal tariff on Thai and Cambodian exports. The deal was brokered in Kuala Lumpur by Malaysian Prime Minister Anwar Ibrahim, with quiet support from both U.S. and Chinese officials.

Despite the use of drones, naval assets, and heavy weaponry, markets barely reacted. Risk assets held steady, oil prices remained stable, and Treasury yields stayed within recent ranges.

The muted response reflects a familiar pattern: unless geopolitical shocks directly threaten global supply chains or major energy corridors, markets are inclined to look through them. Still, the growing use of trade tools to influence regional conflict outcomes is a trend worth watching—particularly as tariff diplomacy increasingly doubles as security policy.

The Turn: Tight Lies and Tighter Margins

This week will tell us a lot—about where the economy stands, where it’s headed, and how much room the Fed has to maneuver.

Wednesday’s FOMC meeting will anchor the week, with Powell expected to strike a more cautious tone. Thursday brings the June PCE inflation report and the Employment Cost Index. Friday delivers the July payrolls report, ISM manufacturing data, and consumer sentiment.

Markets are also watching trade. August 1 marks the formal implementation date for the new tariff regime. Last-minute exemptions are still possible, but the direction is set: more trade friction, more policy uncertainty, and greater reliance on industrial strategy over free trade.

On the earnings front, over 150 S&P 500 firms will report—including Apple, Amazon, Microsoft, and Meta. Corporate commentary on hiring, pricing, and investment will provide critical insight into how companies are adjusting to higher costs and slower demand.

The Fed may be nearing a rate cut, but this is no easy putt. The economic recovery remains intact—but vulnerable. Tariff policy is distorting inflation signals, business investment is fading, and the labor market is losing altitude. With each deal struck, the stakes grow higher for the U.S.-China endgame—and the global fairway narrows.

This Week’s Scorecard: Key Data on the Tee

Tuesday, July 29 – Opening Shots

- Advance Goods Trade Balance (June)

Expect a widening deficit as exports slow and pre-tariff imports remain elevated. - Wholesale Inventories (June, preliminary)

Inventories likely dipped slightly, playing it safe from the rough. A larger drop would cause forecasters to scale back Q2 GDP estimates. - FHFA House Price Index (May)

Continued declines expected as sellers adjust to tighter conditions. - S&P Case-Shiller Home Price Index (May)

Price softness is deepening, particularly in Florida and Texas, with more markets joining the slide. - JOLTS (June)

Openings likely declined again; many remain posted but unfilled. The quits rate is the one to watch. - Consumer Confidence (July)

A modest rebound is expected, helped by easing tariff concerns and steadier market conditions—though labor market nerves could hold sentiment back.

Wednesday, July 30 – The Mid-Round Turn

- ADP Employment Change (July)

Following last month’s miss-hit, expect a partial recovery—about +55,000—plus possible revisions. - Q2 Advance GDP

Forecasted at +2.6%, powered by net exports and moderate consumption. Atlanta Fed GDPNow is tracking at 2.4%. - Pending Home Sales (June)

A slight gain is likely, supported by lower mortgage rates and a small lift in purchase applications. - 2:00 PM – FOMC Statement

- 2:30 PM – Chair Powell Press Conference

Thursday, July 31 – Staying in the Fairway

- Employment Cost Index (Q2)

Expected to rise 0.8%, with annual wage growth easing to 3.5%. A slight fade from earlier strength. - Personal Income & Spending (June)

Income +0.3%, spending +0.2%. Core and headline PCE expected at +0.3%, though a softer read is possible on core.

Friday, August 1 – A Crucial Approach

- Nonfarm Payrolls (July)

Job growth is expected to slow to +90,000, with the unemployment rate ticking up to 4.2%. Hiring restraint and seasonality are in play. - ISM Manufacturing Index (July)

Still under par at just below 50. Defense and tech are driving modest strength, while construction and consumer sectors struggle. - Construction Spending (June)

Residential and commercial weakness continues, though infrastructure may provide a lift from the sand trap. - University of Michigan Consumer Sentiment (July, final)

Sentiment should edge higher with steadier inflation expectations and market gains—but survey polarization remains a hazard.

Final Putt: A Narrow Fairway Ahead

As the Fed eyes the back nine, the course ahead grows more complex. This is not merely the halfway point—it is the start of a tougher stretch where precision matters, hazards multiply, and the margin for error narrows. How we navigate this stretch won’t just determine the score this round—it will shape the course we play going forward.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

June 28, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

Locked-In and Priced-Out: The Stalemate in Existing Home Sales

Housing Hits a Wall—But the Foundation Holds

- Existing home sales fell 2.7% in June to a 3.93 million unit annualized pace—below expectations.

- Single-family home sales fell 3.0% to 3.57 million; median price rose 2.0% y/y to $441,500.

- Condo and co-op sales were flat at 360,000; median price rose 0.8% y/y to $374,500.

- Median price for all existing homes hit a record $435,300 (+2.0% y/y), 24th consecutive annual gain.

- Inventory declined 0.6% m/m but is up 15.9% y/y—rising but still skewed to higher-end single-family units or condominiums.

- The market remains gridlocked by affordability, high mortgage rates, and persistent undersupply of affordable homes.

- Housing’s multiplier effect remains powerful—policy support may be necessary to reignite activity. Further inaction risks deepening housing’s drag on labor mobility, GDP, and inflation rebalancing.

Existing home sales fell 2.7% in June to a 3.93 million unit annualized pace, disappointing consensus and underscoring the persistent paralysis in housing. Sales were flat versus a year ago, but structural cracks are widening. High borrowing costs, anemic affordable supply, and declining participation continue to weigh on turnover.

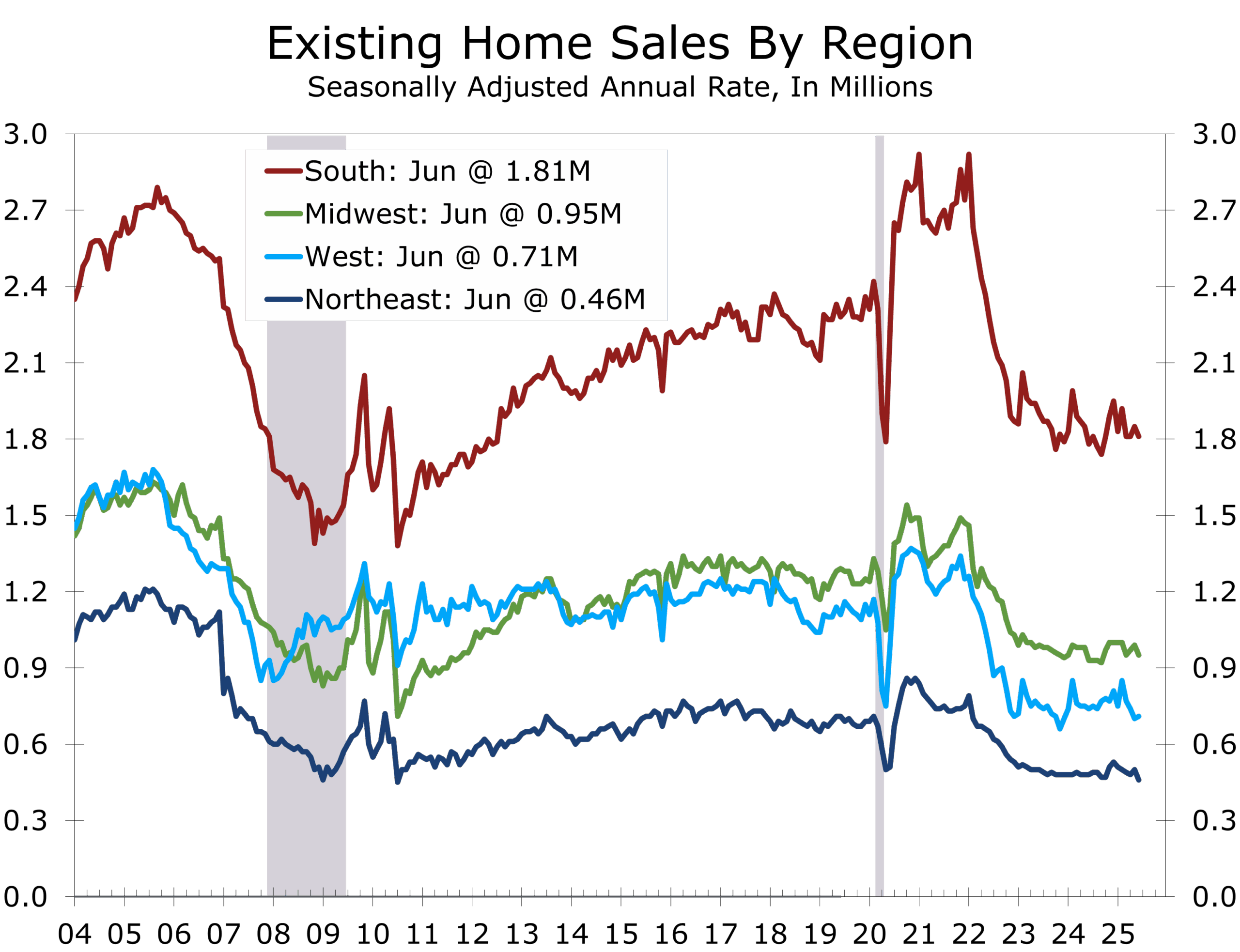

Single-family sales fell 3.0% to a 3.57 million rate, though modestly higher (+0.6%) from last June. The median price for single-family homes rose 2.0% y/y to $441,500. Condominium and co-op sales held steady at 360,000 units, down 5.3% year-over-year. Condo prices edged up 0.8% to $374,500. The divergence reflects the same pattern seen across the broader market—tight inventory at the low end, modest activity at the high end.

Record prices mask a market paralyzed by high rates and locked-in equity.

Across all housing types, the median price rose to a record $435,300, up 2.0% year-to-year. That marks the 24th straight annual gain, driven less by demand strength and more by supply distortions and a skewed sales mix. With higher-end properties accounting for a growing share, prices are rising even as unit volume remains muted. The small rise in sales in the West, which has the highest median home prices in the nation, also pulled prices higher. Home sales fell in the Midwest and South, where the median price is lower.

NAR estimates the average homeowner has gained $140,900 in equity over the past five years, but that wealth is locked in place by the “golden handcuff” of 3% mortgages.

Inventory slipped 0.6% in June to 1.53 million units, though levels remain 15.9% above a year ago. At 4.7 months of supply, the market is at its most balanced since 2016—but the relief is concentrated in higher-end and newly built homes. Entry-level supply remains structurally scarce.

Regionally, only the West posted a gain (+1.4%). Sales dropped sharply in the Northeast (-8.0%) and declined in the Midwest (-4.0%) and South (-2.2%). The South—home to nearly half of all sales—is seeing price growth stall, while the West continues to cool off its pandemic peak.

Participation remains narrow. First-time buyers held steady at 30%. Investors and second-home buyers fell to 14%, the lowest share since 2022. Cash buyers accounted for 29%—underscoring the outsized role of equity-rich households and institutional buyers in affordable submarkets in high-growth metro areas.

While housing directly accounts for less than 4% of GDP, its multiplier is far greater. Each sale fuels demand for everything from appliances and furniture to lending, legal, and moving services. That flywheel has slowed. Retail activity tied to housing—especially in furnishings and home improvement—remains weak. Labor mobility is constrained, weighing on productivity and wage growth.

Policy Implications

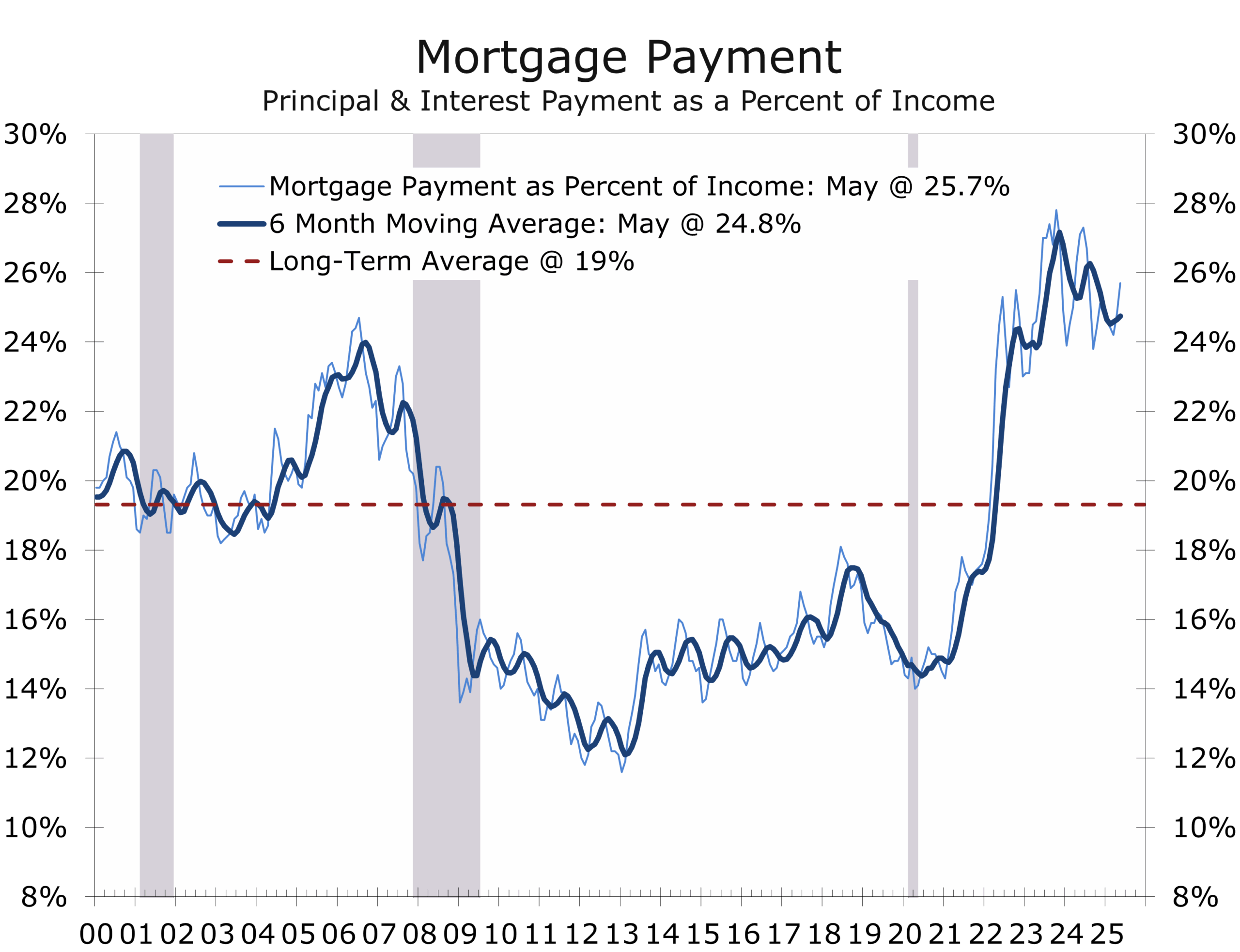

June’s weak sales underscore housing’s role as a growing policy bottleneck. For a median-income household putting 10% down on a median-priced home, principal and interest now consume over 25% of income—well above historical norms. With turnover frozen, lower rates are not translating into broader economic momentum. A drop toward 6% could spur some demand, but structural constraints run deeper.

Years of underbuilding, restrictive zoning, and limited entry-level supply continue to suppress market access. Fiscal tools like down payment assistance, first-time buyer credits, and portable subsidies can help on the margin. But real relief depends on zoning reform, faster permitting, and incentives for infill—none of which are quick fixes or politically easy.

Housing’s stagnation is no longer just a sectoral issue; it is a macro headwind. It is curbing labor mobility, dampening inflation adjustment, and weakening the impact of monetary easing. The shelter component of CPI remains sticky in part because turnover is too low.

Housing is not collapsing—but it is not healing either. Without improved affordability and stronger policy support, it will continue to drag on growth and limit the effectiveness of Fed rate cuts.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 23, 2025

Mark Vitner, Chief Economist

(704) 458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics – Calm Markets, Fraying Margins, Shifting Risks

Highlights of the Week

- Markets are drifting into a summer calm, but risks are accumulating beneath the surface.

- Fed officials are increasingly aligned behind a September rate cut, with Waller leading the charge.

- Inflation is decelerating across core services, particularly ex-housing, but real wages remain under pressure.

- Tariff pass-through remains limited—for now—but may accelerate as new trade frameworks lock in higher rates.

- Geopolitical risks are rising. Ukraine’s conflict is escalating, Israel faces a widening northern front, and Japan’s snap election raised uncertainty but did not get in the way of a U.S. blockbuster trade deal.

- Liquidity strains in the Treasury market could force coordinated Fed–Treasury action before year-end.

- Margins are narrowing for households, businesses and policymakers. The Fed is nearing its first rate cut as disinflation continues, albeit with some bumps, and labor market slack further diminishes. We feel the data support a July rate but expect the Fed to pivot more slowly and cut in September. The Treasury faces mounting pressure to stabilize long-term yields.

Disinflation Holds, but Tariffs Cast a Longer Shadow

June’s inflation data reaffirmed that disinflation remains intact, though not without friction. Core CPI rose 0.23% month-over-month, slightly below expectations, while the year-over-year pace edged up to 2.9%. Headline CPI increased 0.29%, driven by energy and food. Softer categories like lodging (-2.9%), used cars (-0.7%), and new vehicles (-0.3%) helped contain the core, while goods likely impacted by early-stage tariffs—furnishings, apparel, toys, and sporting goods—saw price gains between 1.0% and 1.8%.

Inflation Slows Below the Surface as Trade Pressures Begin to Break Through.

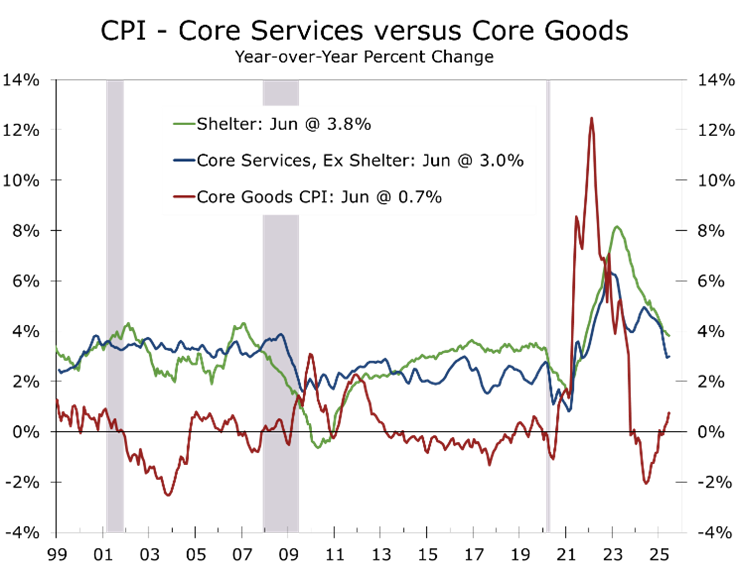

More notably, core services excluding housing—a key focus area for the Fed—rose just 0.27% in June and is up less than 3% year-to-year, which is the slowest pace since it started climbing in the fall of 2021. Medical care, recreation, and transportation services all moderated, signaling that some of the stickiest components of inflation may be easing.

PPI and import price data supported this mixed view. Final demand PPI rose more than expected, with core goods prices up 0.4%. Import prices excluding petroleum were flat, even though consumer goods rose 0.4%, likely tied to tariffs. The BLS also flagged outsized increases in capital equipment and industrial supplies—both categories heavily exposed to tariffs.

Tariff-related cost pressures are surfacing across multiple channels. The latest Beige Book cited “moderate to pronounced” input cost increases in every district. While many firms are still absorbing these costs, most expect to raise prices in the second half of the year. Tighter immigration enforcement is also contributing to labor constraints in skilled services, raising the potential for wage pressure.

Tariffs pass-through is being restrained by slower income growth.

Even so, the broader inflation trend remains favorable. Shelter costs are easing gradually. Core goods, which is where tariffs will most clearly be evident, are firming less than feared, and energy prices, while volatile, remain below year-ago levels. The Fed can take comfort in the direction of travel—but the terrain is uncertain. If pass-through accelerates or wage gains broaden, the glidepath to 2% may grow bumpier.

Real average hourly earnings slipped 0.1% in June, marking the second drop in the past three months. Real weekly earnings fell 0.4%, as inflation outpaced nominal pay gains and the average workweek shortened. Year-over-year, real earnings are still up 1.0%, but momentum is weakening. This deceleration is already weighing on discretionary spending and will likely continue to act as a soft brake on household demand in the second half.

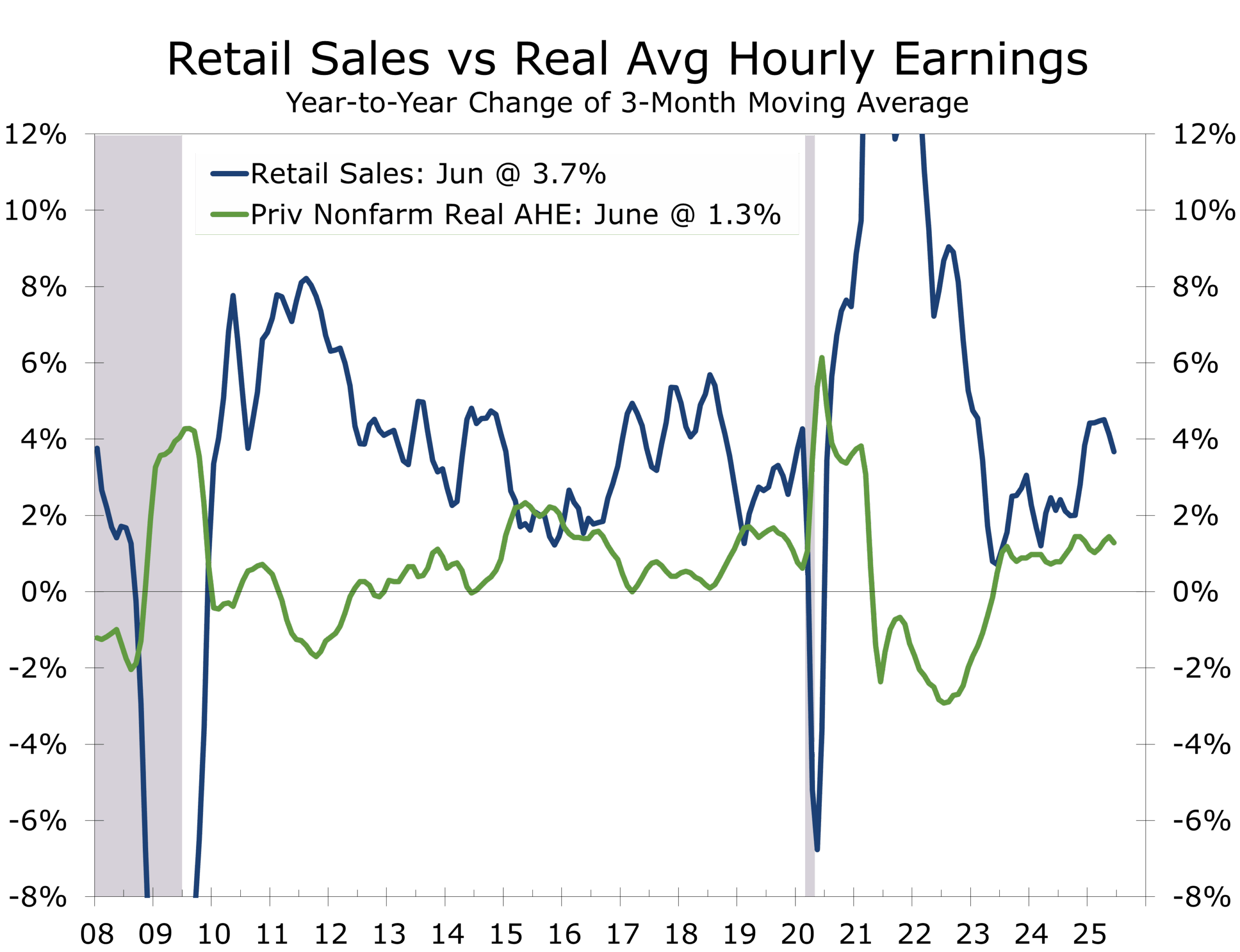

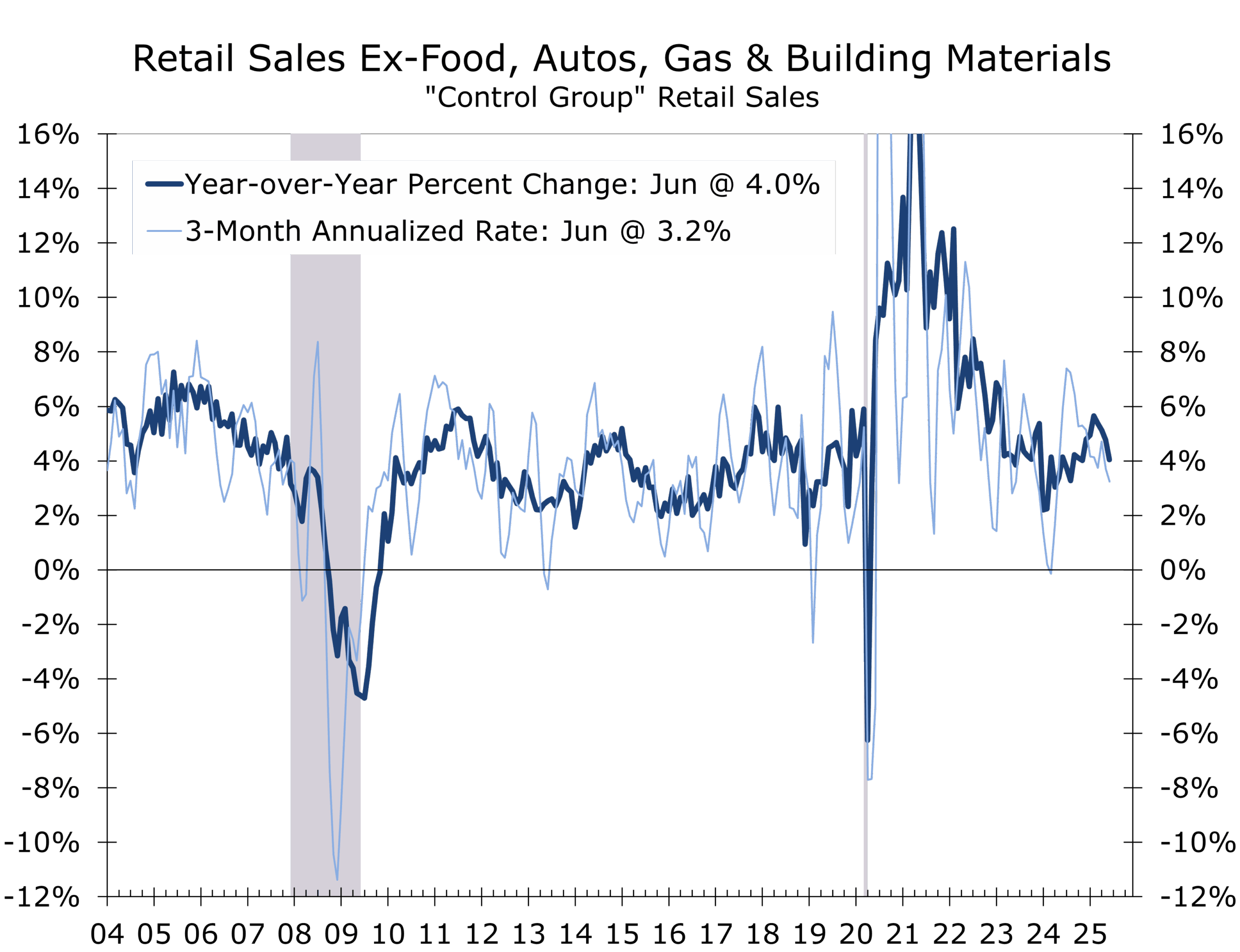

Retail sales in June rose a stronger-than-expected 0.6%, with control group sales up 0.5%. However, downward revisions to April and May dragged the three-month annualized trend in control group sales, which are used to estimate the goods portion of personal consumption expenditures, to a 3.2% pace. The squeeze is especially visible among middle-income households grappling with elevated housing, insurance, and utility costs.

Nominal gains were broad-based, but real volumes told a more nuanced story. Rising goods prices, likely held real goods spending to just a 0.5% pace. Sales declined at electronics and furniture stores—two of the most tariff-sensitive categories—suggesting price hikes are masking even greater real volume weakness. Bars and restaurants rebounded modestly, but discretionary spending on travel and hospitality remains under pressure.

The July University of Michigan consumer sentiment index ticked up to 61.8, marking the second consecutive monthly gain. Year-ahead inflation expectations fell to 4.4%, with long-term expectations easing to 3.6%—the lowest since February. Yet sentiment among low-income households deteriorated, reflecting the early impact of tariffs and the absence of wealth effects from equity gains. The bifurcation in consumer resilience is likely to deepen as fiscal policy changes and higher import costs take hold.

The global trade environment continues to grow more fragmented. Tighter enforcement of transshipment rules and conditional tariff arrangements with Vietnam and Indonesia are raising compliance costs and introducing new frictions into global supply chains. U.S. exporters face weak global demand, limited pricing power, and elevated shipping costs.

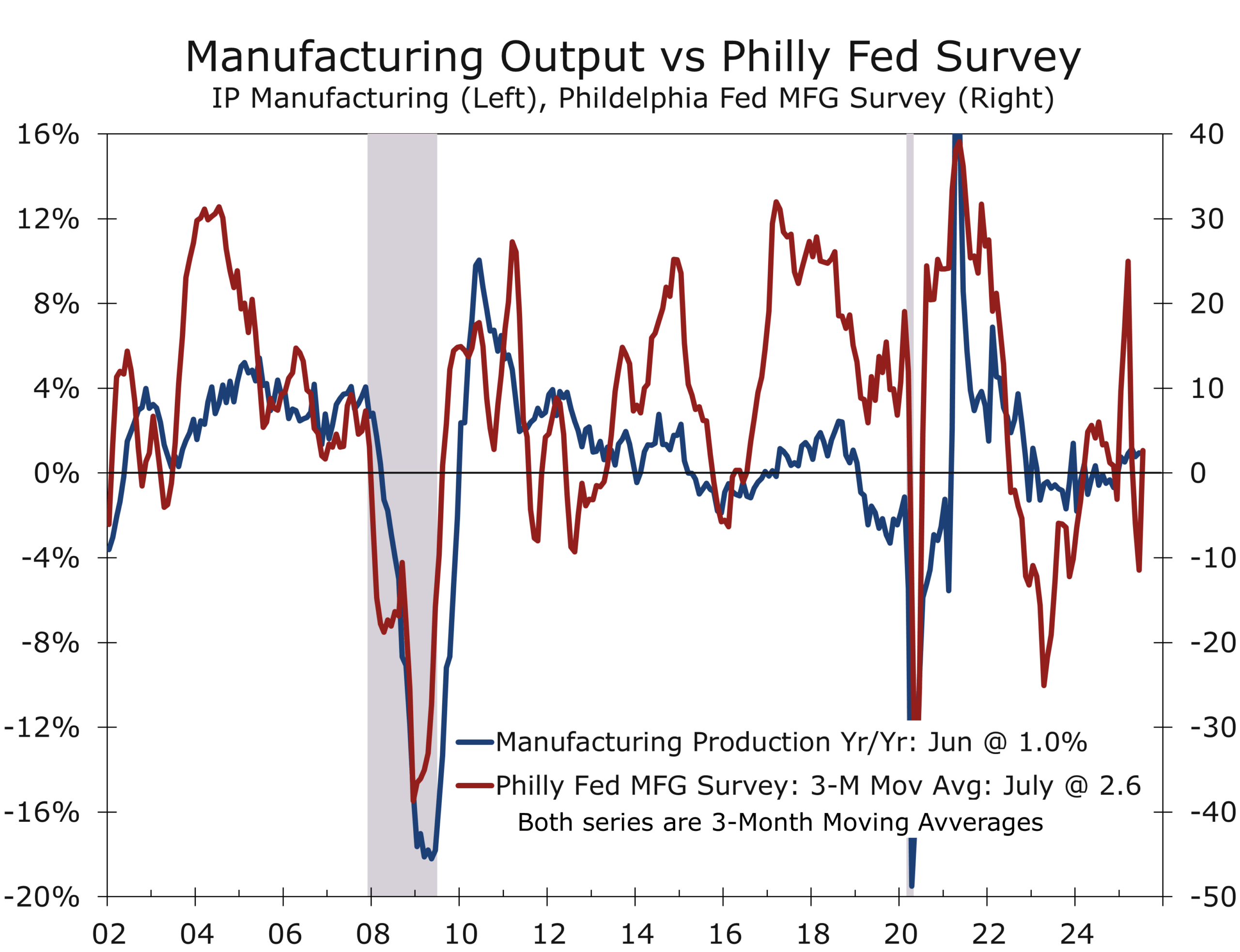

Despite these headwinds, several industrial sectors are showing resilience. U.S. industrial production rose 0.3% in June, underpinned by strength in utilities and primary metals. Manufacturing output edged 0.1% higher, surprising to the upside amid expectations for a decline. While motor vehicle production pulled back following a surge earlier in the year, output in high-tech equipment, aerospace, and primary metals continued to climb. The Philadelphia Fed’s July Manufacturing Survey added to the positive tone, with the general activity index rebounding to +15.9—its highest level since February—and indicators for new orders and shipments also rising sharply.

Steelmakers are boosting output, buoyed by strengthening demand and a supportive tariff environment. Aerospace is benefiting from improved manufacturing systems, as well as ramped-up defense spending and stronger international demand. High-tech manufacturing continues to lead in productivity and investment, with strength concentrated in electronics, automation, and digital infrastructure.

Just as we were set to publish, the Trump Administration announced a trade deal with Japan. Under the agreement, the U.S. will reduce reciprocal tariffs on Japanese goods from 25% to 15%—and from 27.5% to 15% for autos—while Japan has committed to investing roughly $550 billion in U.S. industries, including manufacturing, agriculture, and industrial automation. The deal is expected to stabilize margins in the auto sector and support capex recovery for Japanese OEMs and U.S. suppliers of MedTech.

Trump continues to pressure Powell to cut rates to spur growth and lower financing cost.

Trade negotiations are moving at a breakneck pace, with outcomes often uncertain until the final hour. Additional agreements with major trading partners are likely in the run-up to the August 1 tariff deadline. We expect the new trade regime—featuring a lower base tariff and steeper rates on transshipped goods and critical industry imports—to be largely in place by early fall. Not all countries will be on board by then, however, setting the stage for selective enforcement and ongoing friction.

Corporate Earnings: Cost Discipline and Caution

Second-quarter earnings continue to deliver a familiar narrative: modest revenue gains, flat-to-lower margins, and an intense focus on cost control. Companies like Procter & Gamble, Honeywell, and 3M have cited tariff-related input cost pressures in consumer goods, chemicals, and industrial electronics. The majority are holding price to protect volume and share, opting against broad-based hikes that might test already brittle consumer demand.

Hiring plans remain muted. Amazon is paring back corporate headcount and consolidating fulfillment operations. Intel continues to streamline its cost base, and J.B. Hunt joined other freight and logistics firms in slowing hiring as freight volumes plateau. Across sectors, capital expenditures remain steady but are increasingly tilted toward automation, AI-driven productivity tools, and deferred maintenance—rather than expansion.

Forward guidance has turned cautious. Analysts have trimmed third- and fourth-quarter S&P 500 EPS forecasts by 1.2% and 1.5%, respectively, amid rising macro uncertainty, slower nominal growth, and tightening financial conditions. Companies are increasingly relying on discipline—not demand—to protect profitability.

The message from management is consistent: margin compression is real, and flexibility is narrowing. Tariffs remain a manageable headwind at current levels, but a second wave of enforcement or broader global retaliation could elevate cost pressures and weigh more heavily on earnings into year-end.

A Dovish but Disciplined Turn

Fed Governor Christopher Waller became the first senior official to publicly endorse a July rate cut, citing disinflation in core services, below-potential GDP growth, and labor market softening. Speaking at NYU, Waller dismissed tariff-driven inflation as a one-time price level shift and argued that the policy rate is now too restrictive. He emphasized that the risk of cutting too late outweighs the risk of cutting too soon.

Governor Adriana Kugler echoed this concern, warning of asymmetric risks in delaying. Still, most FOMC participants—including Daly, Williams, and Bostic—favor waiting for more clarity on inflation and tariffs.

Markets are now pricing in 75bps of easing by year-end. A July cut is possible, but the meeting will likely be used to lay out the economic basis for a September cut. As noted in our CAVU Compass, payroll growth is near stall speed, and the Fed is monitoring lagging indicators like wage gains and quits more closely. Margins for error are shrinking.

Red Lines, Flashpoints, and Political Crosswinds

Geopolitical tensions are intensifying across multiple fronts. In Ukraine, Russian strikes have escalated in Kyiv and Kharkiv, with mounting civilian casualties. President Trump reaffirmed U.S. support but warned that secondary tariffs may be imposed on countries maintaining commercial ties with Russia—putting India, Brazil, and Turkey on notice. The threat introduces the potential for major strains in global trade and investment flows.

In the Middle East, Israel has opened a second northern front following a wave of cross-border attacks by Iranian-backed militias on Druze civilians. Airstrikes on Syrian army positions killed over 300, even as Houthi attacks persist in the south. The fighting put normalization talks with Saudi Arabia on hold. We still expect to see Saudi Arabia, Lebanon, and perhaps Syria, reach an agreement with Israel, as they seize on the opportunity presented by a weakened Iran.

Markets appear complacent. Secondary sanctions could redraw global energy and commodity trade routes, adding volatility and inflation risk. Increased support for Ukraine comes at a time of intense budget pressures in the U.S., resulting in some crafty arrangements with NATO allies. Surprises from the Middle East always hold potential to disrupt the markets in a number of ways.

Meanwhile, Japan’s snap election delivered a fractured outcome. Prime Minister Kishida’s ruling coalition held power but lost its supermajority, weakening the mandate for deeper reform. But the result did not derail progress on trade negotiations. The U.S. and Japan announced a sweeping trade agreement this week, with President Trump confirming a reciprocal 15% tariff rate and Japan pledging $550 billion in U.S. investment—including joint ventures in LNG and critical industries. Automotive tariffs, a key sticking point, were reduced from 25% to 15%, offering major relief to Japan’s export-driven economy. Markets welcomed the deal. The Nikkei closed 3.5% higher.

Looking Ahead: The Glidepath Narrows

The Conference Board’s Leading Economic Index fell 0.2% in June—marking its 17th decline in the past 18 months—and is down 2.8% over the past six months. While the index continues to signal recession risk, weakness remains concentrated in softer survey-based components. Hard data—payrolls, industrial production, and real retail sales—point to a decelerating but still expanding economy.

This week’s housing focused calendar could shape expectations ahead of the Fed’s July 31 decision:

- Wednesday, July 23 (today):

- Existing Home Sales (June) declined to 3.93 million SAAR, slightly below expectations. Rising inventories of completed new homes are providing competition for existing homes, as builder incentives attract buyers.

- Thursday, July 24:

- S&P Global Flash PMIs (July) June’s PMI data showed global growth supported by a pickup in manufacturing—its fastest pace since February—even as services activity cooled. Input cost pressures stabilized.

- New Home Sales (June) – expected to rebound modestly, supported by builder incentives and rising inventories of completed homes.

- Friday, July 25:

- Durable Goods Orders (June) – headline orders are expected to rise 0.7%. Core capital goods orders, a proxy for business fixed investment, will be closely watched.

- Monday, July 28:

- University of Michigan Consumer Sentiment (final, July) – expected to confirm the preliminary reading of 61.8 and year-ahead inflation expectations, which eased to 4.4%. Long-term expectations fell to 3.6%, the lowest since February.

- Thursday, August 1:

- Q2 Advance GDP Estimate – expected to show 2.6% annualized growth, supported by a smaller trade deficit, modest gains in consumption, and more support from business inventories than previously expected.

Markets continue to price in 75bps of cuts by year-end. The Fed is expected to hold steady next week, but the data is trending in favor of a September cut. Financial conditions are easing, but the margin for error is narrowing as labor market softness becomes more visible and trade risks reemerge.

The Glidepath Narrows

The Fed is approaching closer to cutting rates. The data supports a cut. Treasury yields are under pressure, and market liquidity is thinning. Margins are narrowing—not just for corporations, but for policymakers. The glidepath remains intact, but the descent is rougher than expected. Expect volatility to pick up in August, with rising odds of coordinated action between the Fed and Treasury

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

June 23, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000

Proceeding Along a Fragile Glidepath

A Narrow Path to a Soft Landing

- While inflation has firmed slightly, tariff passthrough has been less than feared. Meanwhile, higher interest rates are exacting a heavier toll on the real economy—dragging down homebuilding, commercial construction, and big-ticket consumer spending. The labor market is also softening beneath the surface. Despite a low unemployment rate and subdued weekly claims, stress is mounting. Tighter immigration enforcement and accelerating Baby Boomer retirements may be masking deeper labor market slack.

- Trade policy volatility remains elevated, with proposed baseline tariff hikes, sector-specific duties, and the threat of secondary sanctions on Russia impacting a wide range of countries. New trade deals continue to trickle in, with Indonesia the latest to strike an agreement. President Trump has reaffirmed the August 1 deadline for reciprocal tariffs, though he also hinted at flexibility for nations actively negotiating. The endgame appears to mirror the Vietnam and Indonesia deals: a 20% base tariff, and a higher 40% rate on Chinese goods transshipped through those countries.

- Home sales and new construction have slowed to a crawl as affordability concerns and higher interest rates push buyers to the sidelines. Construction employment has held up for now, supported by a large backlog of projects. But inventories are rising, pressuring prices. Existing home prices are rising more slowly—and declining outright in a growing number of markets.

- Fiscal dominance concerns are rising as growing debt burdens collide with monetary policy decisions, renewing questions about Fed independence. Some degree of coordination between the Treasury and the Fed now appears inevitable. We do not expect President Trump to fire Chair Powell—it would likely prove counterproductive to his own economic objectives.

- Geopolitical risk is rising again, with the Russia–Ukraine conflict escalating and the Middle East remaining a persistent flashpoint. Both theaters carry the potential to disrupt global trade, energy markets, and investor confidence.

- After wide swings in Q1 and Q2—driven by tariff front-running, inventory volatility, and erratic consumer spending—we expect the economy to stabilize in the second half of the year. Disinflationary trends remain intact, and the labor market is cooling beneath the surface. Barring a major geopolitical or financial shock, we anticipate the Federal Reserve will begin a gradual easing cycle, with 25-basis-point cuts at the September, October, and December FOMC meetings. Fed officials are increasingly signaling readiness to pivot as inflation expectations anchor and downside risks to growth accumulate. The rate path beyond December remains data-dependent, but we expect the Fed to maintain a dovish bias heading into 2026.

Trade & Tariffs: Delay, Double Down, Distort

The next wave of tariffs has been delayed until August 1, but the structure is largely set. A 10% global baseline anchors U.S. trade policy, layered with 20% to 60% sector-specific duties on Chinese goods—targeting critical minerals, semiconductors, EV components, and medical supplies. The regime will cover nearly $2 trillion in annual imports.

Washington is leaning hard into tariff-first diplomacy—using trade barriers to accelerate reshoring, pressure adversaries, and rewire global supply chains. Inflation impacts remain modest. We estimate only 20% of tariff costs have been passed to consumers, with the rest absorbed via margin compression, efficiency gains, and supplier concessions. Durable goods have seen more pricing pressure; commoditized goods less so.

That cushion is unlikely to hold. As tariffs become a permanent feature of trade policy, passthrough will rise. Transshipping restrictions are tightening, targeting Chinese goods routed through third countries like Vietnam and Indonesia, where blended tariff rates now approach 40%. Compliance is no longer optional.

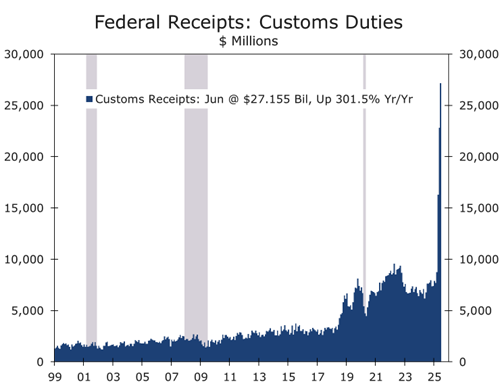

Tariff revenues are surging, providing Treasury with a growing source of funding. Collections have reached their highest level since the original China tariffs in 2018 and are poised to rise further as enforcement expands. While tariffs won’t erase the deficit, they will meaningfully offset shortfalls from the recently enacted budget deal—which notably excluded tariff revenues from its projections.

The Indonesia deal exemplifies this new model: a 19% base tariff with partial relief tied to mineral quotas and investment thresholds. The earlier Vietnam agreement, with its 17% floor and more lenient terms, now looks like an outlier. The message is clear: tariff relief must be earned, not assumed.

While some foreign policy experts remain puzzled by Trump’s trade strategy, we view it as the next evolution of globalization—an explicit response to China’s rise as an economic competitor and geopolitical threat.

Meanwhile, secondary sanctions on countries continuing trade with Russia—including India, Brazil, and parts of Europe—remain under active consideration, threatening to upend global sourcing and raise compliance costs.

Bottom line: Tariff volatility is no longer background noise—it is policy. The delayed inflation impact will not last. Slower trade, higher costs, and deeper fragmentation are reshaping business strategy and narrowing the Fed’s margin for maneuver.

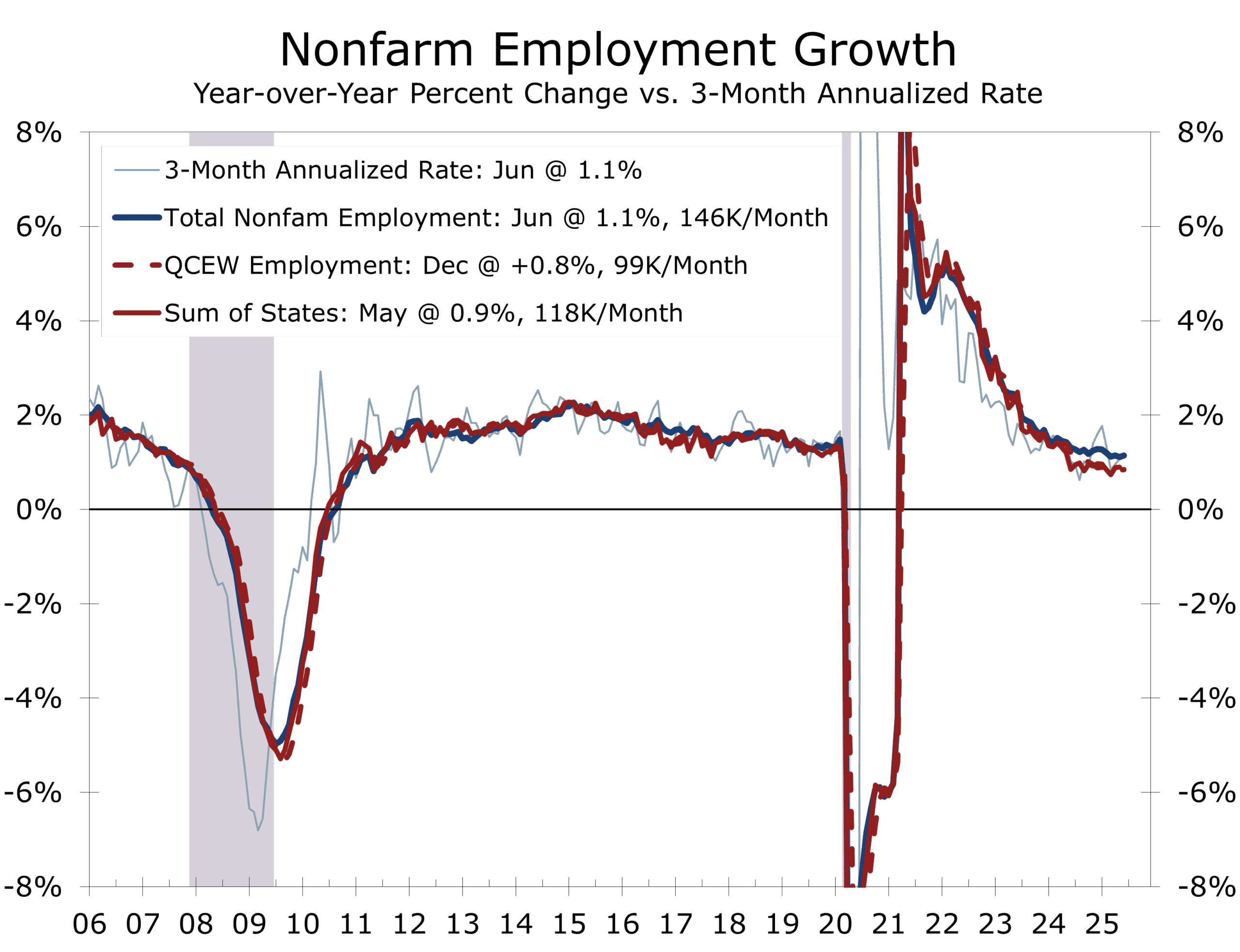

Labor Market: A Shaky Foundation

The U.S. labor market remains caught in a slow-motion deceleration. Employers added just 150,000 jobs a month over the past 3 months, down from 168,000 a month in 2024 and 220,000 jobs a month in 2023. Not only has hiring slowed but it is also much more narrowly based. Health care, leisure and hospitality, and state and local government have accounted for the bulk of job gains this past year, and there is growing evidence that these gains have been overstated.

We have long warned that the monthly nonfarm payroll series is overstating job growth, and recent data continue to support that assessment. The Quarterly Census of Employment and Wages (QCEW)—which underpins the BLS’s annual benchmark revisions—and state employment data, which integrate those figures more quickly, both suggest that job gains have been overstated by as much as one-third. These more comprehensive datasets, drawn from actual UI tax filings, point to a labor market that is far weaker beneath the surface than the monthly headlines imply.

The latest ADP private payrolls report, which posted its first decline in several months, offers additional confirmation. While official payroll data show private-sector job gains of 1.8 million over the past year, nearly half of that—878,000 jobs—comes from education and health care. Yet ADP data show that the same sectors accounted for just 13% of its measured payroll gains. This glaring discrepancy underscores how concentrated—and potentially overstated—hiring has become.

The divergence between headline strength and underlying softness is also evident in the unemployment claims data. Initial claims remain relatively low, but continuing claims have climbed to post-pandemic highs, indicating that displaced workers are struggling to find new jobs. The labor market is transitioning from one defined by robust churn to one marked by stagnation—less hiring, less firing, and fewer opportunities for job seekers.

We believe the labor market is on the verge of a more pronounced downshift and that the FOMC would do well to heed the warnings recently made by Kevin Warsh and Fed Governor Waller. Key sectors that fueled the post-COVID recovery—warehousing, e-commerce, and residential construction—are now paring headcount. The lagged effects of tighter monetary policy and front-loaded hiring are beginning to show in other areas, including construction and consumer spending on big-ticket items. The pull-forward in demand from tariff-related inventory building and a massive construction backlog have masked much of the weakness. But those tailwinds are fading, and with them, the scaffolding supporting labor demand.

Labor force participation has plateaued, while demographic trends—particularly the retirement of baby boomers—and more stringent immigration enforcement are muting labor supply. These shifts help suppress the unemployment rate, giving a false sense of resilience even as underlying slack builds across the economy.

Housing Outlook: The Inventory Illusion Meets the Vanishing Dream

The U.S. housing market is increasingly defined by contradiction. Existing home supply remains tight, as owners cling to ultra-low mortgage rates secured during the pandemic. Meanwhile, inventories of unsold new homes are rising, especially in high-growth markets like Texas, Florida, and the Carolinas—where 7%+ mortgage rates are eroding demand.

The divergence between new and existing homes is distorting market signals. Builder incentives are widespread: 62% offered concessions in July, and 38% cut prices—the highest share since tracking began in 2022. Absorption remains weak. Builder sentiment edged up following passage of the One Big Beautiful Bill Act, which aims to ease regulatory hurdles and support affordable housing. But the NAHB/Wells Fargo Index remains deeply negative at 33—its 15th straight month below neutral.

As backlogs clear and permits decline, housing starts—particularly single-family—are expected to fall in H2 2025. Labor demand is already softening, especially in markets tied to new construction. The shift may ease shelter inflation in CPI and PCE data but won’t resolve the broader affordability crisis. Most new supply still targets mid-tier and upscale buyers, leaving few options for first-time homeowners.

That dream is slipping further out of reach. First-time homebuyers fell to just over 1.1 million in 2024, the lowest since NAR began tracking in 1989. The average age of a first-time buyer is now 38, up from the late 20s in the 1980s—delaying wealth accumulation, retirement, and financial security.

Affordability metrics tell the story. The median price of a single-family home hit $427,800 in May, up from $357,100 in 2021. Buyers now need to earn $126,700 annually, up from $79,300 just three years ago. Mortgage rates remain double their 2020 lows, while real incomes lag. Even stable prices can’t offset these financing costs.

Renting has become the default. John Burns Research reports that entry-level homes now cost double the price of renting, a gap last seen in 2006. That spread is freezing mobility and inventory alike.

Homeownership remains a core aspiration, but for millions—especially younger Americans—it’s becoming a distant hope. Without a shift in policy, financing, and land use, the housing ladder may remain out of reach—and the fallout could extend well beyond the housing market.

Geopolitical Risk: Ukraine Escalates, Syria Ignites

Geopolitical tensions are intensifying on two fronts—Eastern Europe and the Middle East—adding complexity to an already fragile global backdrop. A more aggressive Russian offensive and an unexpected Israel–Syria flare-up threatens to derail ceasefires, rewire trade alignments, and disrupt capital flows.

Russia has ramped up its summer offensive with deeper drone and missile strikes on Kyiv and Kharkiv. The Kremlin is betting on fading Western support. In response, President Trump reaffirmed U.S. backing for Ukrainian sovereignty while threatening secondary tariffs on nations trading with Russia. This would mark a major policy shift and could force countries like India, Brazil, and Turkey to rethink ties with Moscow.

Markets have yet to fully price in the threat. Strategic decoupling is accelerating, with “friend-shoring” replacing global integration as the dominant model.

While Gaza ceasefire talks grind on, Israel’s northern border with Syria has erupted. After attacks on Syria’s Druze minority, hundreds of Israeli Druze crossed into Syria to defend family members. Israel responded with precision strikes on Syrian Army positions, killing at least 350 and reactivating a once-dormant front.

The intervention—officially humanitarian but strategically aimed at Iranian militias—complicates Israeli politics and undermines prospects for a Syria-Israel agreement. Netanyahu’s coalition has lost its majority, with early elections in 2026 increasingly likely.

Meanwhile, Houthi missile strikes from Yemen continue to target southern Israel, widening the conflict and highlighting Iran’s proxy reach.

Markets are underpricing escalation risk. In Ukraine, secondary sanctions could redraw trade lanes and rekindle energy price volatility. In the Middle East, a hot Syria front likely puts the brakes any chance of normalization with Israel under the Abraham Accords. For the U.S., this means deeper reengagement in global security and more pressure on fiscal policy. For the Fed, geopolitical risk raises inflation tail.

Investors should brace for volatility. These simultaneous flashpoints are not isolated—they are pressure points in a rapidly shifting global order.

Between the Fed and a Fiscal Place

Fiscal dominance—where high government debt constrains central bank policy, effectively forcing interest rates lower to manage borrowing costs—is no longer theoretical. It’s shaping monetary and fiscal decisions in real time. Elevated long-term yields are pressuring both Treasury and the Fed to act—balancing funding needs against credibility and independence.

At Treasury, yield curve control is quietly returning in softer form. While formal caps remain unlikely, issuance is tilting toward shorter maturities, buybacks are expanding, and long-end debt is being selectively absorbed during market stress. The goal: shape the curve without triggering alarm. With net issuance climbing and foreign demand retreating, crowding out is no longer a risk—it’s a present reality.

The Fed’s bind is subtler but increasingly urgent. Governor Christopher Waller became the first senior Fed official to back a July rate cut, citing disinflation in core services and mounting labor market slack. He argued that acting now would support a soft landing without undermining credibility—framing the move as data-driven, not political. Governor Adriana Kugler echoed similar concerns, warning that delay could create asymmetric risks—overcorrecting on inflation while ignoring real economic strain.

Former Governor Kevin Warsh, a possible successor to Chair Powell, added institutional context with a call for a new Fed–Treasury accord modeled on the 1951 Agreement. His aim: shrink the Fed’s $6.7 trillion balance sheet and restore monetary autonomy through coordination with the Treasury. Warsh floated a hybrid strategy—pairing rate cuts with accelerated asset runoff—to balance near-term easing with long-term fiscal discipline. His proposal highlights how rising debt and political volatility are narrowing the Fed’s policy space.

Politics are muddying the waters. Trump’s handwritten accusation that Powell is “costing the USA a fortune” has put monetary policy on the campaign trail. Yet delay risks deepening the downturn, while action risks appearing compromised. The Fed is walking a narrowing tightrope, with stakes rising weekly.

Liquidity risks are resurfacing too. Standing repo facilities and broader collateral eligibility are back on the table as buffers against tariff shocks or geopolitical jolts to Treasury markets. Coordinated, clearly signaled action may be the only way to steady yields and preserve room to maneuver as risks converge.

Soft Landing, Touch and Go, or Another Go-Around?

The outlook has steadied. After two rocky quarters, Q3 is starting with firmer footing—retail sales have normalized, manufacturing has stabilized, and ISM indexes are no longer slipping. But fragilities remain. Consumer credit is tightening, delinquencies are inching higher, and business investment is weak.

A soft landing is still within reach, but the approach vector is narrow. The Fed must pivot preemptively while avoiding the perception of political capitulation. Treasury must finance larger deficits without destabilizing the long end of the curve. And Trump’s tariff-first diplomacy must avoid choking off supply chains or igniting retaliatory measures.

We anticipate three 25-basis-point rate cuts—September, October, and December—with a possible fourth in Q1 2026. Powell is unlikely to be replaced in the near term; doing so would expose Trump to blame if the economy stumbles. Still, Powell must communicate any cuts as economically warranted—not politically motivated.

A more volatile glidepath is forming. Each new shock—tariffs, sanctions, oil disruptions, or a credit crunch—narrows the Fed’s window and complicates execution. A misstep could stall growth or reignite inflation.

Homebuilders, manufacturers, and financial markets are bracing for a “touch and go” landing—where easing helps, but momentum fades. Until policy coordination improves and global tensions ease, investors should keep seat belts fastened and stay near the exit row.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 18, 2025

Mark Vitner, Chief Economist

704-458-4000

Price Increases Contained By Softer Growth

Consumers Get Another Pass on Tariffs

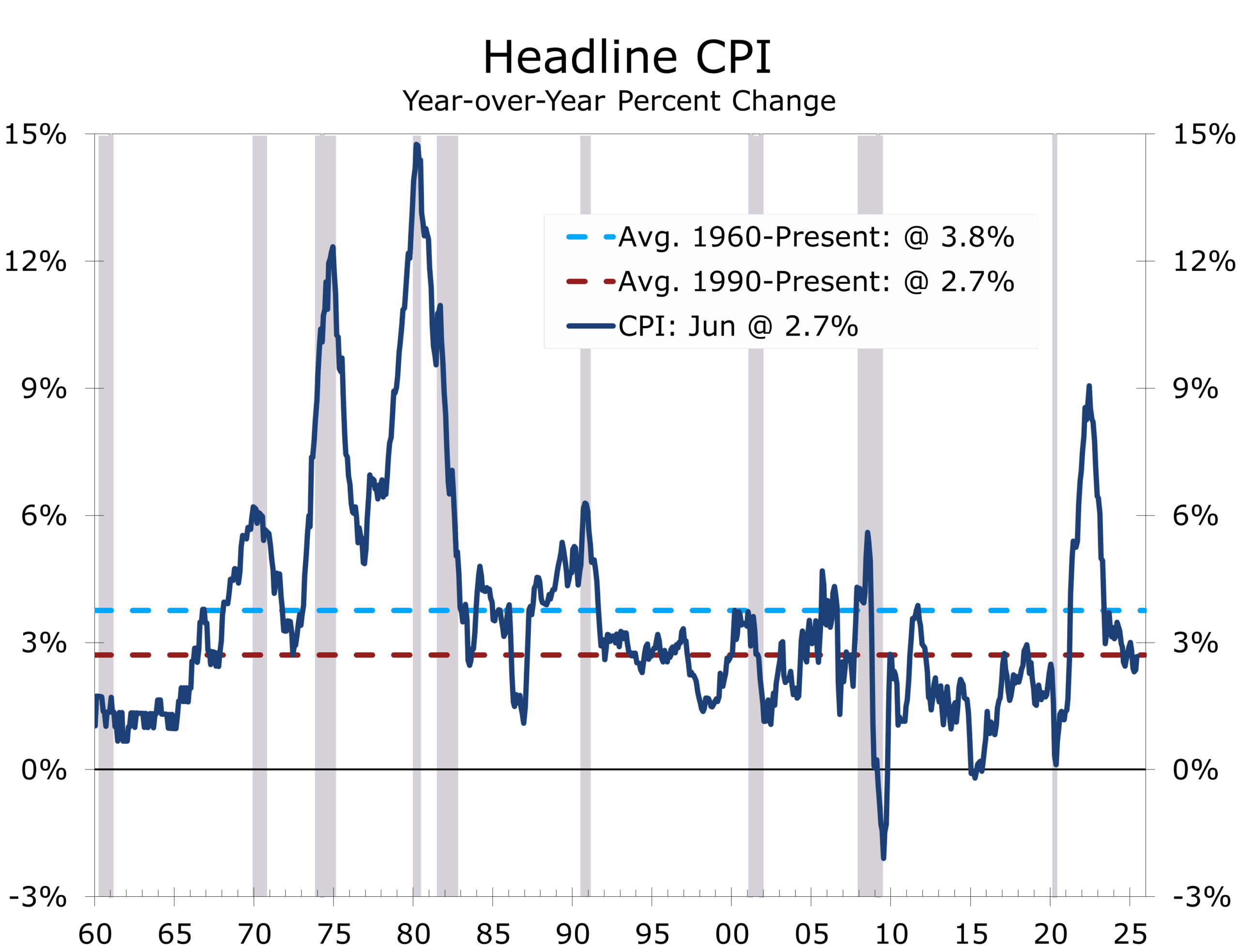

- Headline CPI rose 0.3% in June, up from 0.1% in May. Core CPI advanced 0.2%, consistent with consensus expectations.

- Year-over-year headline inflation ticked up to 2.7%, while core CPI edged up to 2.9%.

- Energy prices bounced 0.9% in June; food prices also rose 0.3%.

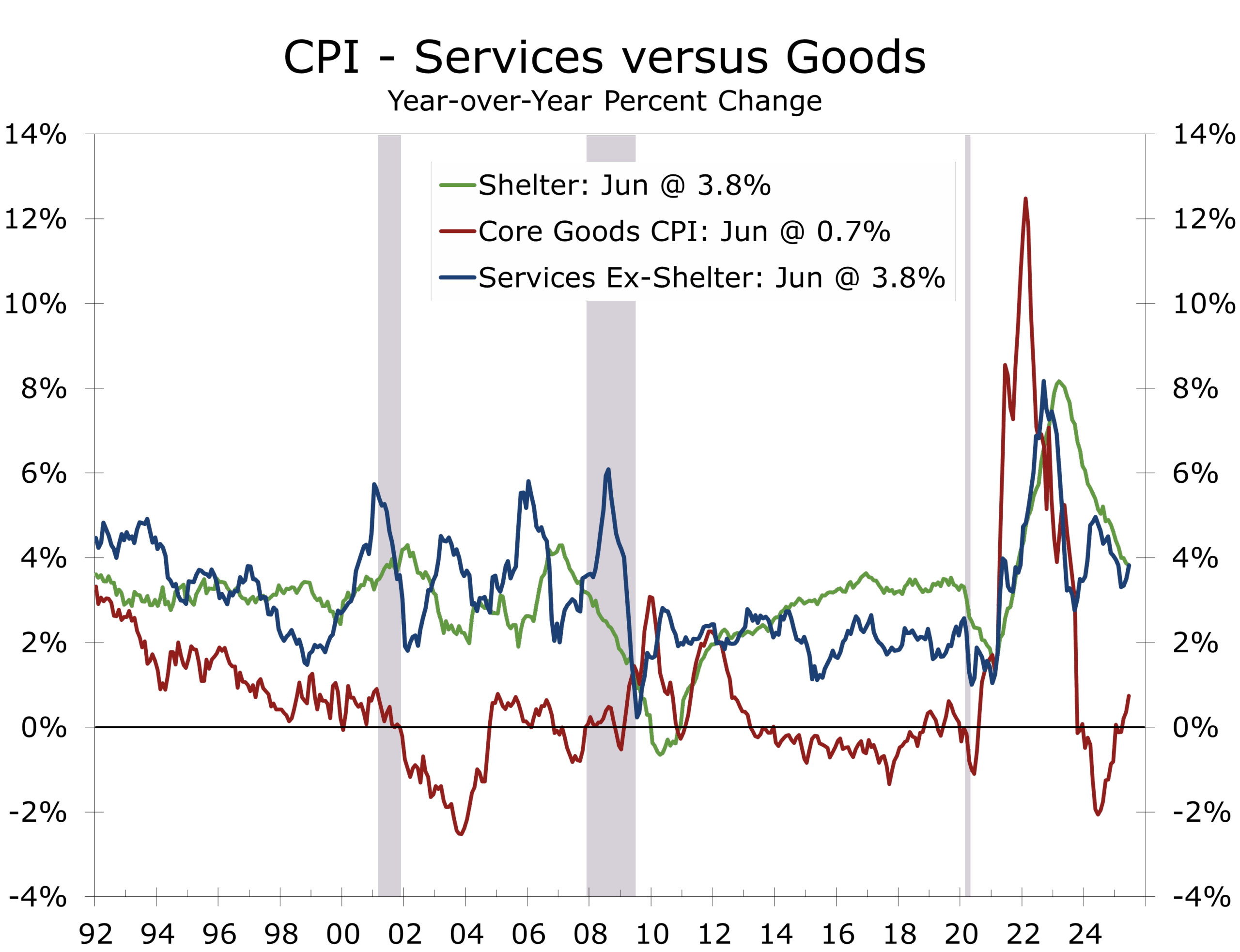

- Shelter inflation eased, with OER up 0.3% and rent up 0.2%, reflecting ongoing housing softness.

- Core goods disinflation persisted: used vehicle prices fell 0.7%, new vehicles -0.3%. Apparel rose just 0.4% and home furnishings rose 1.0%, with appliance prices up 1.9%.

- Real average hourly earnings declined 0.1% in June, while real weekly earnings fell 0.4%, as inflation outpaced wage gains and the average workweek shortened.

- The June CPI report keeps the door open for a September Fed rate cut. Prices rose largely in line with expectation and there is no evidence of broad passthrough of tariffs. Pressures are evident in a few areas, most notably washing machines, toys, coffee, men’s shirts and women’s dresses. There are also some offsets, however, as consumers are cutting back on big-ticket purchases and leisure and travel.

Inflation Eases Where It Matters Most

The Consumer Price Index came in firmer than May’s reading, but still well within the Federal Reserve’s comfort zone. Headline CPI rose 0.3%, driven largely by higher energy and food costs. Core CPI rose 0.2%, keeping the three-month annualized pace at a modest 1.9%.

Year-over-year, headline CPI rose to 2.7% and core to 2.9%. With base effects fading, inflationary momentum remains subdued—especially in categories that previously drove price spikes. Most encouragingly, core services outside of housing have shown sustained improvement over several months.

Base effects pushed up year-over-year inflation, but the underlying trend is still decelerating.

Energy prices posted a broad rebound in June, rising 0.9% following May’s 1.0% decline. Gasoline prices rose 1.0%, natural gas increased 0.5%, and electricity prices jumped 1.0%. However, base effects continue to hold the year-over-year energy index down 0.8%, with gasoline still down 8.3% over the past 12 months. Energy inflation may reemerge this summer if global oil supplies tighten further—but so far, the inflation pass-through has been modest.

While 2.7% inflation remains above the Fed’s 2% target, it aligns with the 35-year historical average. The underlying trend continues to decelerate, driven by easing wage pressures and softer demand for discretionary services.

Food prices rose 0.3% in June, matching May’s gain. Grocery store prices climbed 0.3%, while food away from home rose 0.4%. Within grocery categories, nonalcoholic beverages jumped 1.4%, led by a 2.2% increase in coffee. Fruits and vegetables also posted solid gains (+0.9%), though egg prices plummeted 7.4%, offering some relief. Dining costs continue to outpace grocery inflation, with full-service meals up 0.5% and limited-service up 0.2%.

The housing slowdown is easing pressure on household budgets and services inflation.

Shelter costs, which carry outsized weight in the CPI, are finally showing clearer signs of slowing. Owners’ equivalent rent rose 0.3% and primary rent increased 0.2%—both down slightly from earlier this year. Lodging away from home declined 2.9%, contributing to the broad deceleration. A continued influx of multifamily supply and slowing lease renewals suggest further cooling ahead, although BLS methodology lags real-time rental data by several quarters.

Despite persistent tariff headlines, core goods prices continued to decline. Used vehicles fell 0.7%, new vehicles 0.3%. Apparel, which is a small component of the CPI, rose 0.4%, hinting at early tariff effects, but gains remain modest. Retailers appear to be absorbing higher costs through supplier diversification, margin compression, and delayed restocking.

Tariff effects are beginning to surface in home furnishings, which rose 1.0% in June and are up 1.7% year-over-year. Major appliances led the increase, climbing 1.9% in June and 2.4% over the year, driven by washing machines, which jumped 1.8% on the month and 7.7% year-over-year. Toys and sporting goods also rose 1.8%, likely reflecting early-stage tariff pass-through.

Real average hourly earnings declined 0.1% in June, while real weekly earnings fell 0.4%, as inflation outpaced wage gains and the average workweek shortened. Despite a 1.0% year-over-year increase, the monthly setback highlights the pressure households face from high housing, insurance, and food costs. Weaker real income growth will weigh on spending, particularly for big-ticket items.

The June CPI report gives the Fed room to ease. Core inflation remains subdued, and although year-over-year rates edged higher, they’re broadly consistent with a gradual path back to 2%. Markets now assign a 70–80% chance of a September rate cut, as the Fed grows more concerned about overtightening into a slowing labor market that’s softening even more quickly beneath the surface.

Still, tariff risks are building. While consumer prices have not yet reflected the full impact, producer prices are firming, and a weaker dollar is pushing import costs higher. A quicker pass-through could reignite inflation, but likely unevenly across sectors given softer demand.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 15, 2025

Mark Vitner, Chief Economist

(704) 458-4000

A View from the Piedmont: Our Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics -- Too Late, Too Soon, or Just in Time

Highlights of the Week

- The Fed continues to hold steady, but mounting political pressure—most notably from Trump’s critique of Powell as “too late”—is raising the stakes.

- FOMC minutes reveal a growing internal divide: while most members remain focused on tariff-driven inflation risks, a vocal minority warn that delaying cuts could jeopardize the recovery.

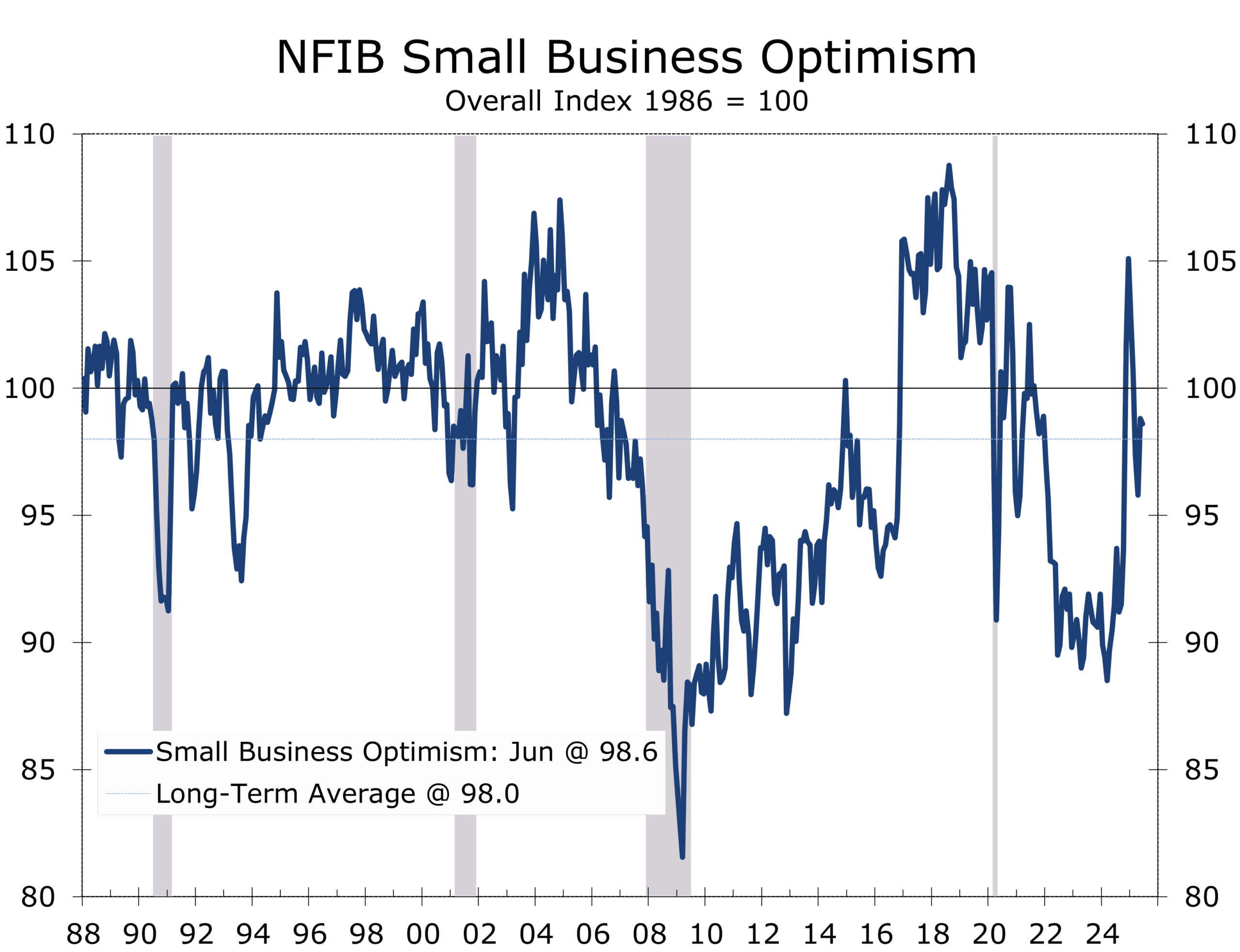

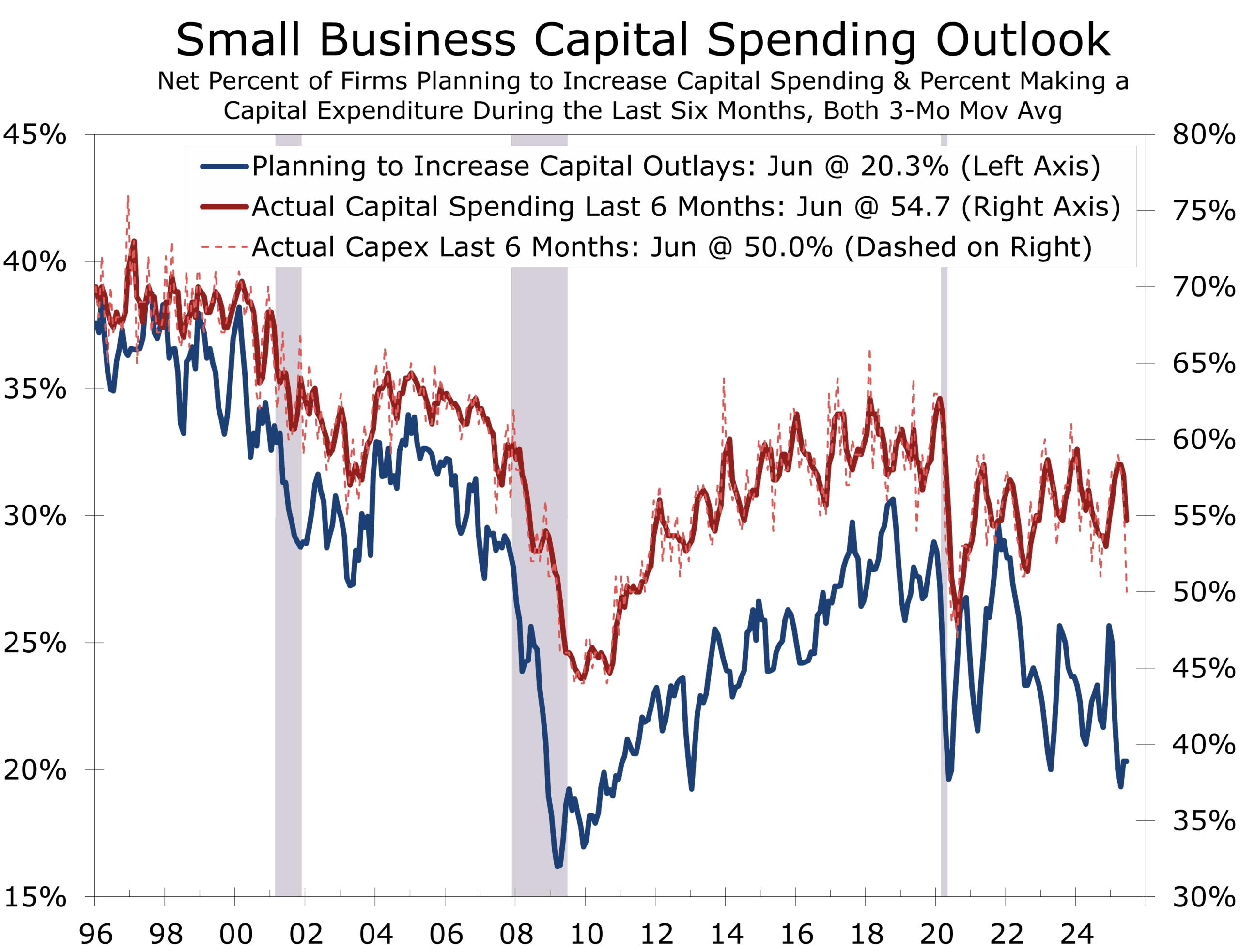

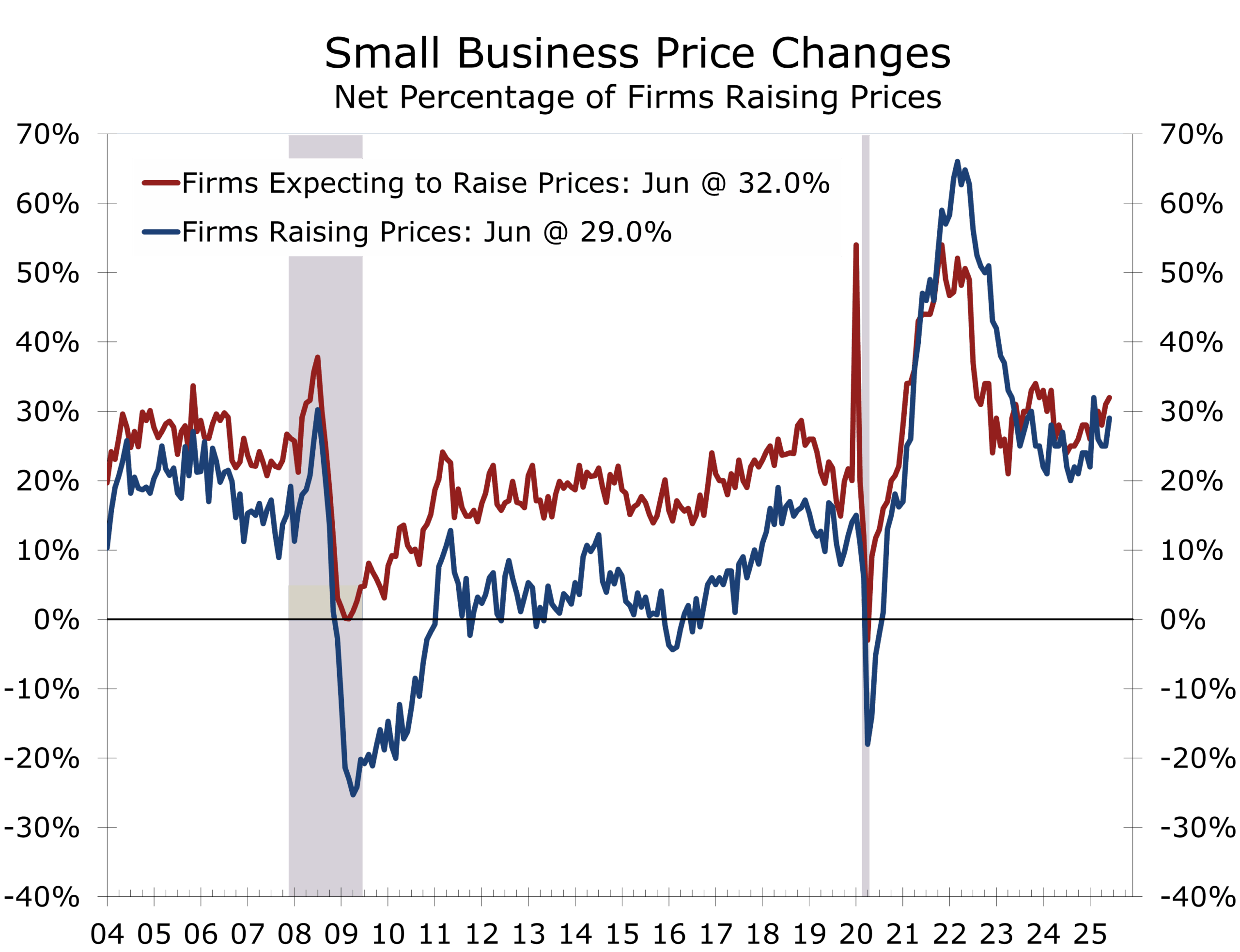

- NFIB Small Business Optimism edged lower in June, reflecting excess inventories, weak demand, and a growing reluctance to purchase new equipment or hire staff.

- Continuing claims climbed to a post-COVID high, signaling an increasingly stagnant labor market, with little hiring or firing.