Highlights of the Week

- Markets are drifting into a summer calm, but risks are accumulating beneath the surface.

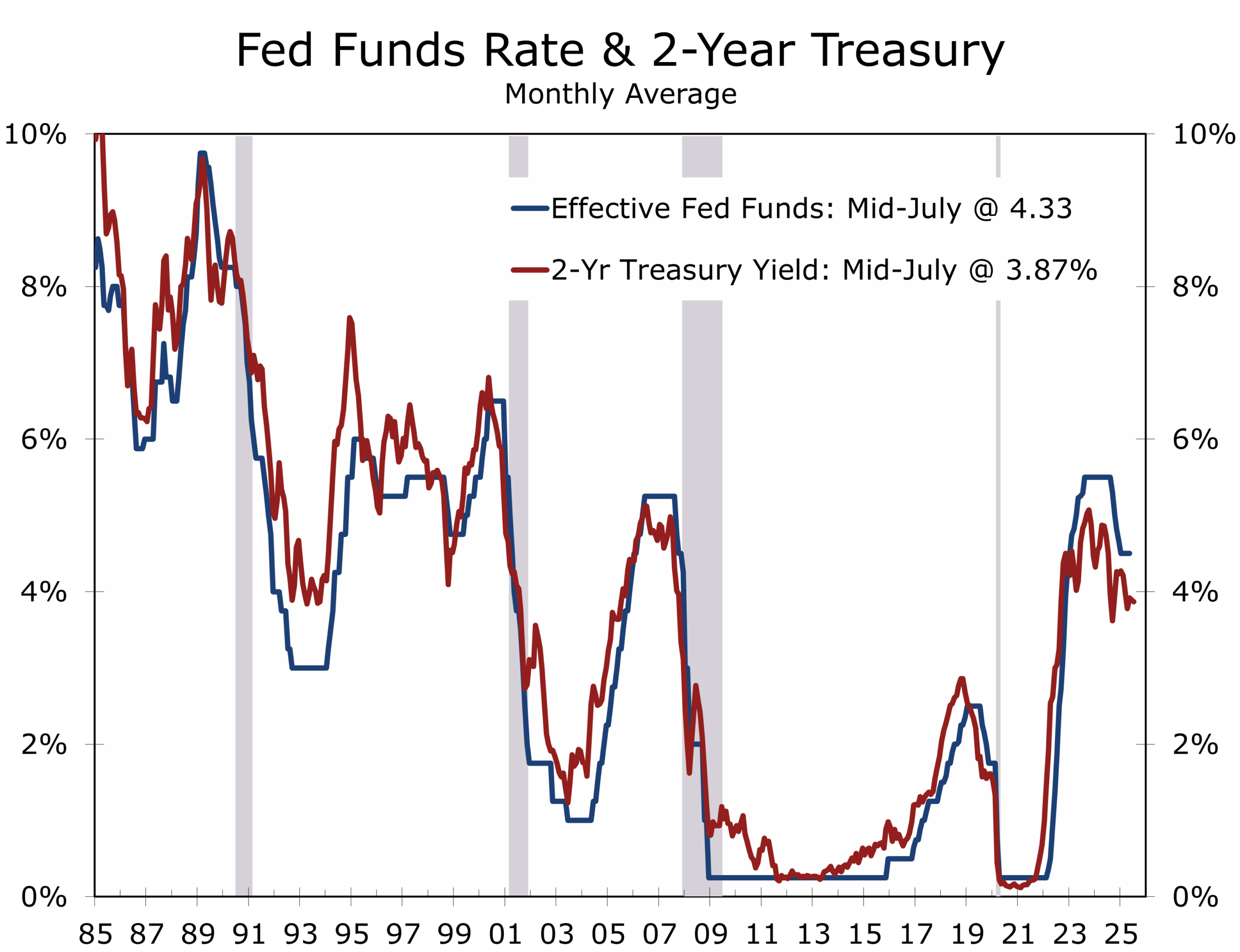

- Fed officials are increasingly aligned behind a September rate cut, with Waller leading the charge.

- Inflation is decelerating across core services, particularly ex-housing, but real wages remain under pressure.

- Tariff pass-through remains limited—for now—but may accelerate as new trade frameworks lock in higher rates.

- Geopolitical risks are rising. Ukraine’s conflict is escalating, Israel faces a widening northern front, and Japan’s snap election raised uncertainty but did not get in the way of a U.S. blockbuster trade deal.

- Liquidity strains in the Treasury market could force coordinated Fed–Treasury action before year-end.

- Margins are narrowing for households, businesses and policymakers. The Fed is nearing its first rate cut as disinflation continues, albeit with some bumps, and labor market slack further diminishes. We feel the data support a July rate but expect the Fed to pivot more slowly and cut in September. The Treasury faces mounting pressure to stabilize long-term yields.

Disinflation Holds, but Tariffs Cast a Longer Shadow

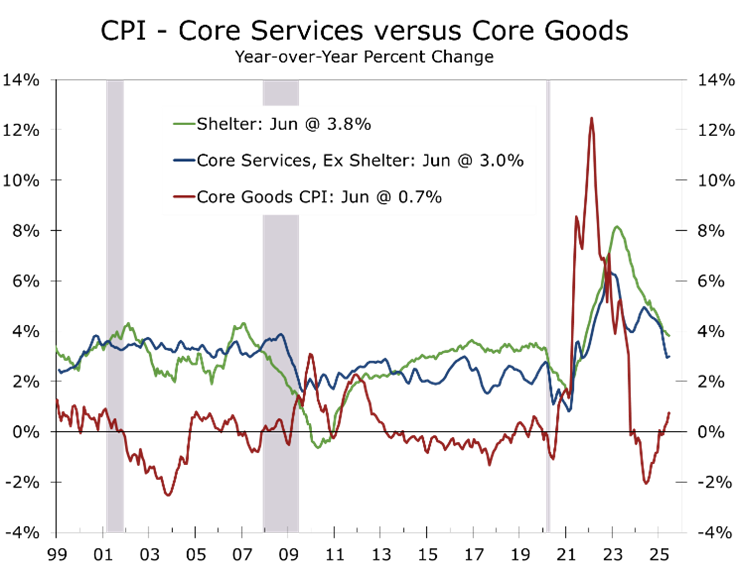

June’s inflation data reaffirmed that disinflation remains intact, though not without friction. Core CPI rose 0.23% month-over-month, slightly below expectations, while the year-over-year pace edged up to 2.9%. Headline CPI increased 0.29%, driven by energy and food. Softer categories like lodging (-2.9%), used cars (-0.7%), and new vehicles (-0.3%) helped contain the core, while goods likely impacted by early-stage tariffs—furnishings, apparel, toys, and sporting goods—saw price gains between 1.0% and 1.8%.

Inflation Slows Below the Surface as Trade Pressures Begin to Break Through.

More notably, core services excluding housing—a key focus area for the Fed—rose just 0.27% in June and is up less than 3% year-to-year, which is the slowest pace since it started climbing in the fall of 2021. Medical care, recreation, and transportation services all moderated, signaling that some of the stickiest components of inflation may be easing.

PPI and import price data supported this mixed view. Final demand PPI rose more than expected, with core goods prices up 0.4%. Import prices excluding petroleum were flat, even though consumer goods rose 0.4%, likely tied to tariffs. The BLS also flagged outsized increases in capital equipment and industrial supplies—both categories heavily exposed to tariffs.

Tariff-related cost pressures are surfacing across multiple channels. The latest Beige Book cited “moderate to pronounced” input cost increases in every district. While many firms are still absorbing these costs, most expect to raise prices in the second half of the year. Tighter immigration enforcement is also contributing to labor constraints in skilled services, raising the potential for wage pressure.

Tariffs pass-through is being restrained by slower income growth.

Even so, the broader inflation trend remains favorable. Shelter costs are easing gradually. Core goods, which is where tariffs will most clearly be evident, are firming less than feared, and energy prices, while volatile, remain below year-ago levels. The Fed can take comfort in the direction of travel—but the terrain is uncertain. If pass-through accelerates or wage gains broaden, the glidepath to 2% may grow bumpier.

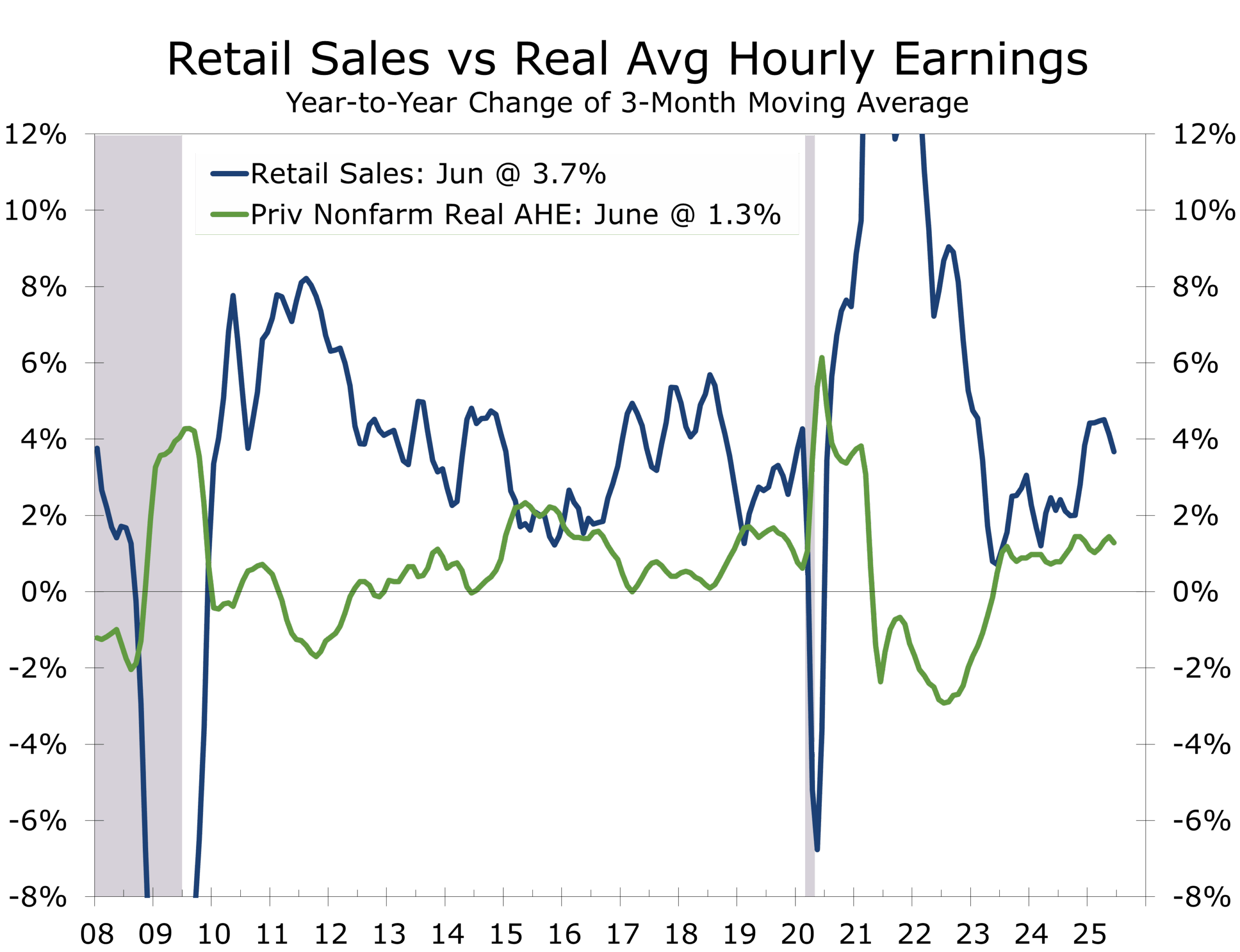

Real average hourly earnings slipped 0.1% in June, marking the second drop in the past three months. Real weekly earnings fell 0.4%, as inflation outpaced nominal pay gains and the average workweek shortened. Year-over-year, real earnings are still up 1.0%, but momentum is weakening. This deceleration is already weighing on discretionary spending and will likely continue to act as a soft brake on household demand in the second half.

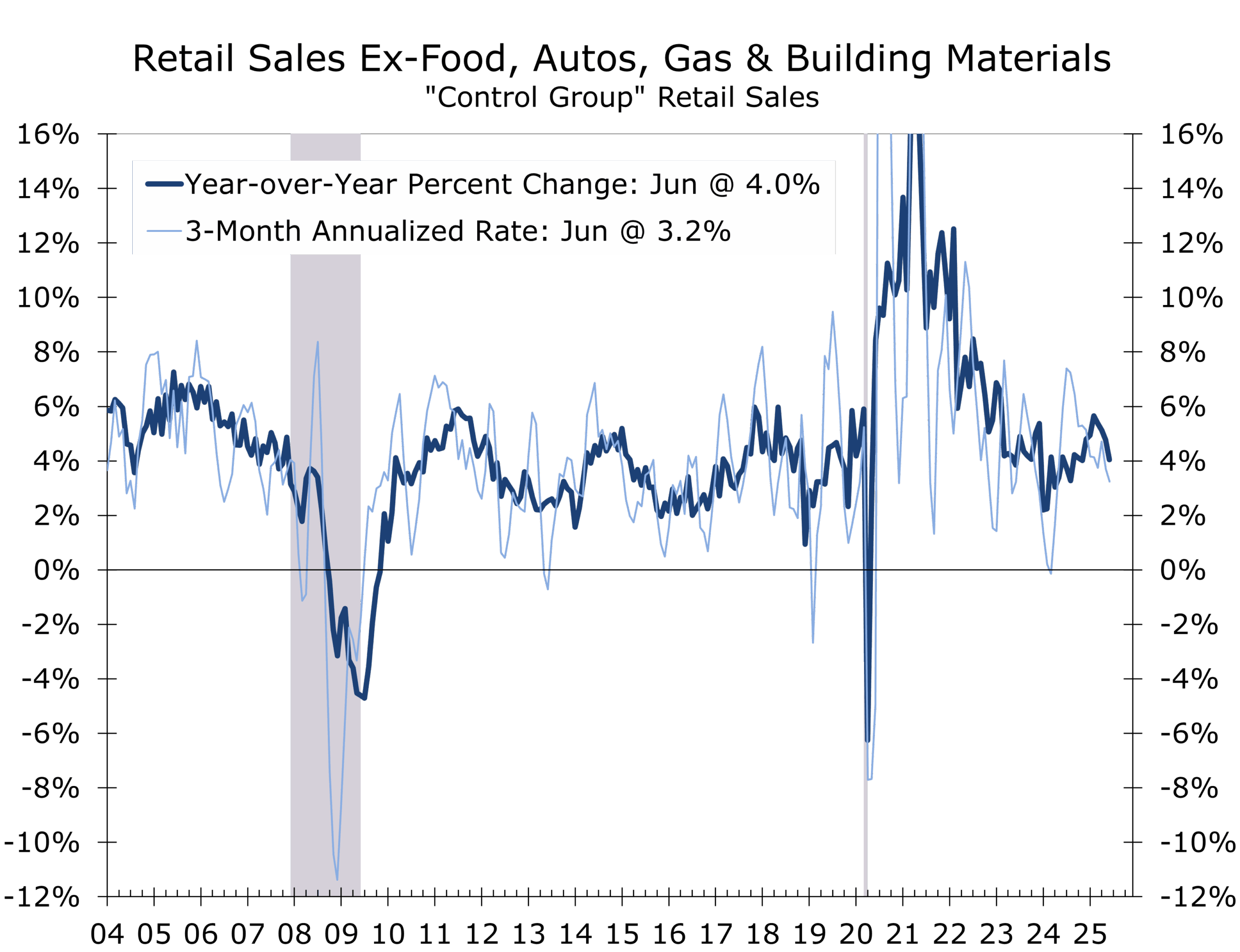

Retail sales in June rose a stronger-than-expected 0.6%, with control group sales up 0.5%. However, downward revisions to April and May dragged the three-month annualized trend in control group sales, which are used to estimate the goods portion of personal consumption expenditures, to a 3.2% pace. The squeeze is especially visible among middle-income households grappling with elevated housing, insurance, and utility costs.

Nominal gains were broad-based, but real volumes told a more nuanced story. Rising goods prices, likely held real goods spending to just a 0.5% pace. Sales declined at electronics and furniture stores—two of the most tariff-sensitive categories—suggesting price hikes are masking even greater real volume weakness. Bars and restaurants rebounded modestly, but discretionary spending on travel and hospitality remains under pressure.

The July University of Michigan consumer sentiment index ticked up to 61.8, marking the second consecutive monthly gain. Year-ahead inflation expectations fell to 4.4%, with long-term expectations easing to 3.6%—the lowest since February. Yet sentiment among low-income households deteriorated, reflecting the early impact of tariffs and the absence of wealth effects from equity gains. The bifurcation in consumer resilience is likely to deepen as fiscal policy changes and higher import costs take hold.

The global trade environment continues to grow more fragmented. Tighter enforcement of transshipment rules and conditional tariff arrangements with Vietnam and Indonesia are raising compliance costs and introducing new frictions into global supply chains. U.S. exporters face weak global demand, limited pricing power, and elevated shipping costs.

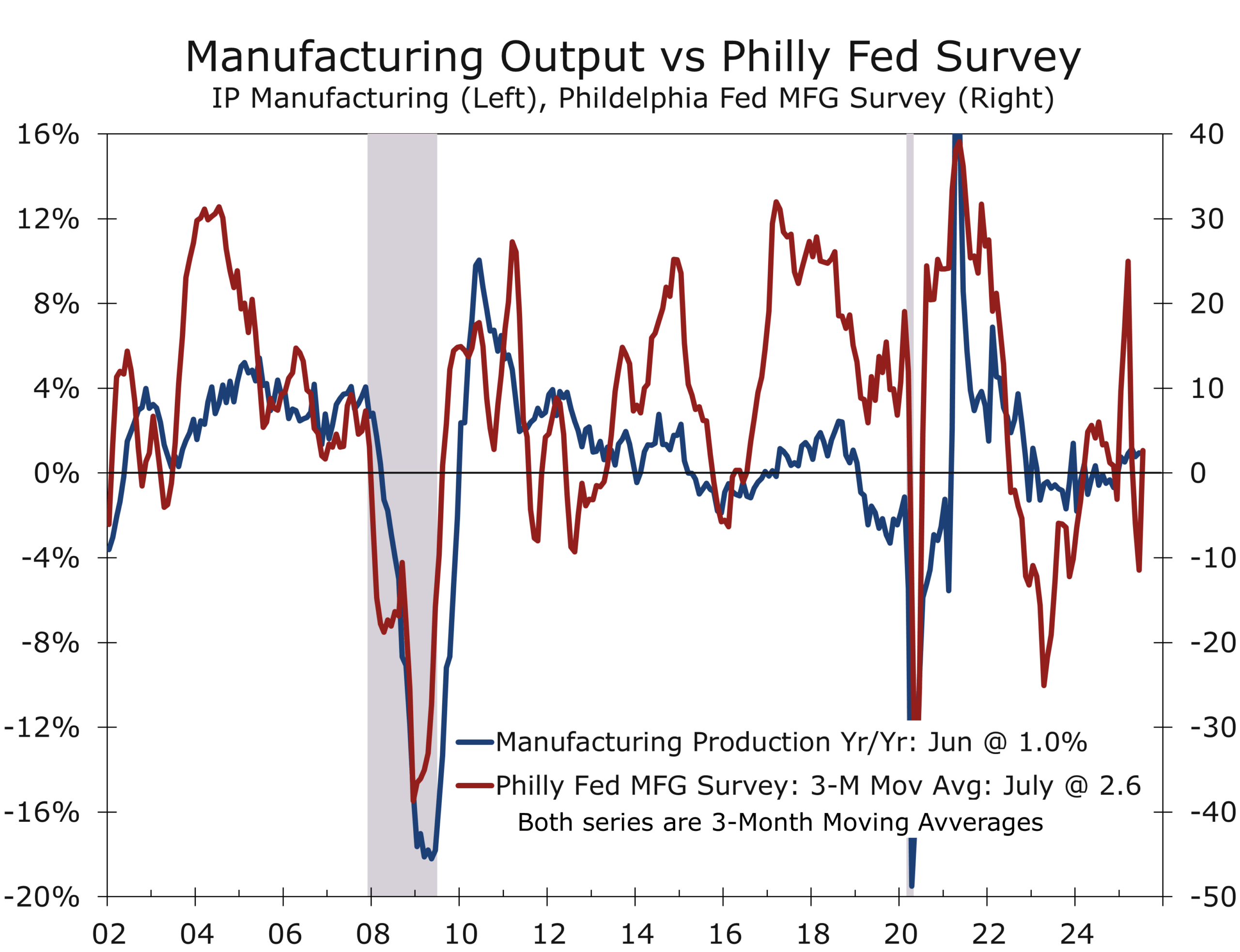

Despite these headwinds, several industrial sectors are showing resilience. U.S. industrial production rose 0.3% in June, underpinned by strength in utilities and primary metals. Manufacturing output edged 0.1% higher, surprising to the upside amid expectations for a decline. While motor vehicle production pulled back following a surge earlier in the year, output in high-tech equipment, aerospace, and primary metals continued to climb. The Philadelphia Fed’s July Manufacturing Survey added to the positive tone, with the general activity index rebounding to +15.9—its highest level since February—and indicators for new orders and shipments also rising sharply.

Steelmakers are boosting output, buoyed by strengthening demand and a supportive tariff environment. Aerospace is benefiting from improved manufacturing systems, as well as ramped-up defense spending and stronger international demand. High-tech manufacturing continues to lead in productivity and investment, with strength concentrated in electronics, automation, and digital infrastructure.

Just as we were set to publish, the Trump Administration announced a trade deal with Japan. Under the agreement, the U.S. will reduce reciprocal tariffs on Japanese goods from 25% to 15%—and from 27.5% to 15% for autos—while Japan has committed to investing roughly $550 billion in U.S. industries, including manufacturing, agriculture, and industrial automation. The deal is expected to stabilize margins in the auto sector and support capex recovery for Japanese OEMs and U.S. suppliers of MedTech.

Trump continues to pressure Powell to cut rates to spur growth and lower financing cost.

Trade negotiations are moving at a breakneck pace, with outcomes often uncertain until the final hour. Additional agreements with major trading partners are likely in the run-up to the August 1 tariff deadline. We expect the new trade regime—featuring a lower base tariff and steeper rates on transshipped goods and critical industry imports—to be largely in place by early fall. Not all countries will be on board by then, however, setting the stage for selective enforcement and ongoing friction.

Corporate Earnings: Cost Discipline and Caution

Second-quarter earnings continue to deliver a familiar narrative: modest revenue gains, flat-to-lower margins, and an intense focus on cost control. Companies like Procter & Gamble, Honeywell, and 3M have cited tariff-related input cost pressures in consumer goods, chemicals, and industrial electronics. The majority are holding price to protect volume and share, opting against broad-based hikes that might test already brittle consumer demand.

Hiring plans remain muted. Amazon is paring back corporate headcount and consolidating fulfillment operations. Intel continues to streamline its cost base, and J.B. Hunt joined other freight and logistics firms in slowing hiring as freight volumes plateau. Across sectors, capital expenditures remain steady but are increasingly tilted toward automation, AI-driven productivity tools, and deferred maintenance—rather than expansion.

Forward guidance has turned cautious. Analysts have trimmed third- and fourth-quarter S&P 500 EPS forecasts by 1.2% and 1.5%, respectively, amid rising macro uncertainty, slower nominal growth, and tightening financial conditions. Companies are increasingly relying on discipline—not demand—to protect profitability.

The message from management is consistent: margin compression is real, and flexibility is narrowing. Tariffs remain a manageable headwind at current levels, but a second wave of enforcement or broader global retaliation could elevate cost pressures and weigh more heavily on earnings into year-end.

A Dovish but Disciplined Turn

Fed Governor Christopher Waller became the first senior official to publicly endorse a July rate cut, citing disinflation in core services, below-potential GDP growth, and labor market softening. Speaking at NYU, Waller dismissed tariff-driven inflation as a one-time price level shift and argued that the policy rate is now too restrictive. He emphasized that the risk of cutting too late outweighs the risk of cutting too soon.

Governor Adriana Kugler echoed this concern, warning of asymmetric risks in delaying. Still, most FOMC participants—including Daly, Williams, and Bostic—favor waiting for more clarity on inflation and tariffs.

Markets are now pricing in 75bps of easing by year-end. A July cut is possible, but the meeting will likely be used to lay out the economic basis for a September cut. As noted in our CAVU Compass, payroll growth is near stall speed, and the Fed is monitoring lagging indicators like wage gains and quits more closely. Margins for error are shrinking.

Red Lines, Flashpoints, and Political Crosswinds

Geopolitical tensions are intensifying across multiple fronts. In Ukraine, Russian strikes have escalated in Kyiv and Kharkiv, with mounting civilian casualties. President Trump reaffirmed U.S. support but warned that secondary tariffs may be imposed on countries maintaining commercial ties with Russia—putting India, Brazil, and Turkey on notice. The threat introduces the potential for major strains in global trade and investment flows.

In the Middle East, Israel has opened a second northern front following a wave of cross-border attacks by Iranian-backed militias on Druze civilians. Airstrikes on Syrian army positions killed over 300, even as Houthi attacks persist in the south. The fighting put normalization talks with Saudi Arabia on hold. We still expect to see Saudi Arabia, Lebanon, and perhaps Syria, reach an agreement with Israel, as they seize on the opportunity presented by a weakened Iran.

Markets appear complacent. Secondary sanctions could redraw global energy and commodity trade routes, adding volatility and inflation risk. Increased support for Ukraine comes at a time of intense budget pressures in the U.S., resulting in some crafty arrangements with NATO allies. Surprises from the Middle East always hold potential to disrupt the markets in a number of ways.

Meanwhile, Japan’s snap election delivered a fractured outcome. Prime Minister Kishida’s ruling coalition held power but lost its supermajority, weakening the mandate for deeper reform. But the result did not derail progress on trade negotiations. The U.S. and Japan announced a sweeping trade agreement this week, with President Trump confirming a reciprocal 15% tariff rate and Japan pledging $550 billion in U.S. investment—including joint ventures in LNG and critical industries. Automotive tariffs, a key sticking point, were reduced from 25% to 15%, offering major relief to Japan’s export-driven economy. Markets welcomed the deal. The Nikkei closed 3.5% higher.

Looking Ahead: The Glidepath Narrows

The Conference Board’s Leading Economic Index fell 0.2% in June—marking its 17th decline in the past 18 months—and is down 2.8% over the past six months. While the index continues to signal recession risk, weakness remains concentrated in softer survey-based components. Hard data—payrolls, industrial production, and real retail sales—point to a decelerating but still expanding economy.

This week’s housing focused calendar could shape expectations ahead of the Fed’s July 31 decision:

- Wednesday, July 23 (today):

- Existing Home Sales (June) declined to 3.93 million SAAR, slightly below expectations. Rising inventories of completed new homes are providing competition for existing homes, as builder incentives attract buyers.

- Thursday, July 24:

- S&P Global Flash PMIs (July) June’s PMI data showed global growth supported by a pickup in manufacturing—its fastest pace since February—even as services activity cooled. Input cost pressures stabilized.

- New Home Sales (June) – expected to rebound modestly, supported by builder incentives and rising inventories of completed homes.

- Friday, July 25:

- Durable Goods Orders (June) – headline orders are expected to rise 0.7%. Core capital goods orders, a proxy for business fixed investment, will be closely watched.

- Monday, July 28:

- University of Michigan Consumer Sentiment (final, July) – expected to confirm the preliminary reading of 61.8 and year-ahead inflation expectations, which eased to 4.4%. Long-term expectations fell to 3.6%, the lowest since February.

- Thursday, August 1:

- Q2 Advance GDP Estimate – expected to show 2.6% annualized growth, supported by a smaller trade deficit, modest gains in consumption, and more support from business inventories than previously expected.

Markets continue to price in 75bps of cuts by year-end. The Fed is expected to hold steady next week, but the data is trending in favor of a September cut. Financial conditions are easing, but the margin for error is narrowing as labor market softness becomes more visible and trade risks reemerge.

The Glidepath Narrows

The Fed is approaching closer to cutting rates. The data supports a cut. Treasury yields are under pressure, and market liquidity is thinning. Margins are narrowing—not just for corporations, but for policymakers. The glidepath remains intact, but the descent is rougher than expected. Expect volatility to pick up in August, with rising odds of coordinated action between the Fed and Treasury

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

June 23, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000