Amid Unevenly Clearing Fog: Nervous Markets, Missing Data, and the New Age of Deficits

- The fog is finally lifting, but visibility remains uneven. The return of federal data should re-anchor expectations, and early releases appear likely to confirm what private indicators already signaled: a cooling yet still resilient economy.

- Markets remain choppy, with narrow leadership, rising volatility, and investors on edge. Headlines like The Economist’s “How the markets could topple the global economy” resonate sharply with investors who still carry memories of the GFC.

- Inflation continues to ease beneath the surface, with goods prices softening and core services showing further deceleration. Private trackers suggest official CPI will confirm a continued—if uneven—disinflation. The relaxation of several tariffs may support further goods disinflation.

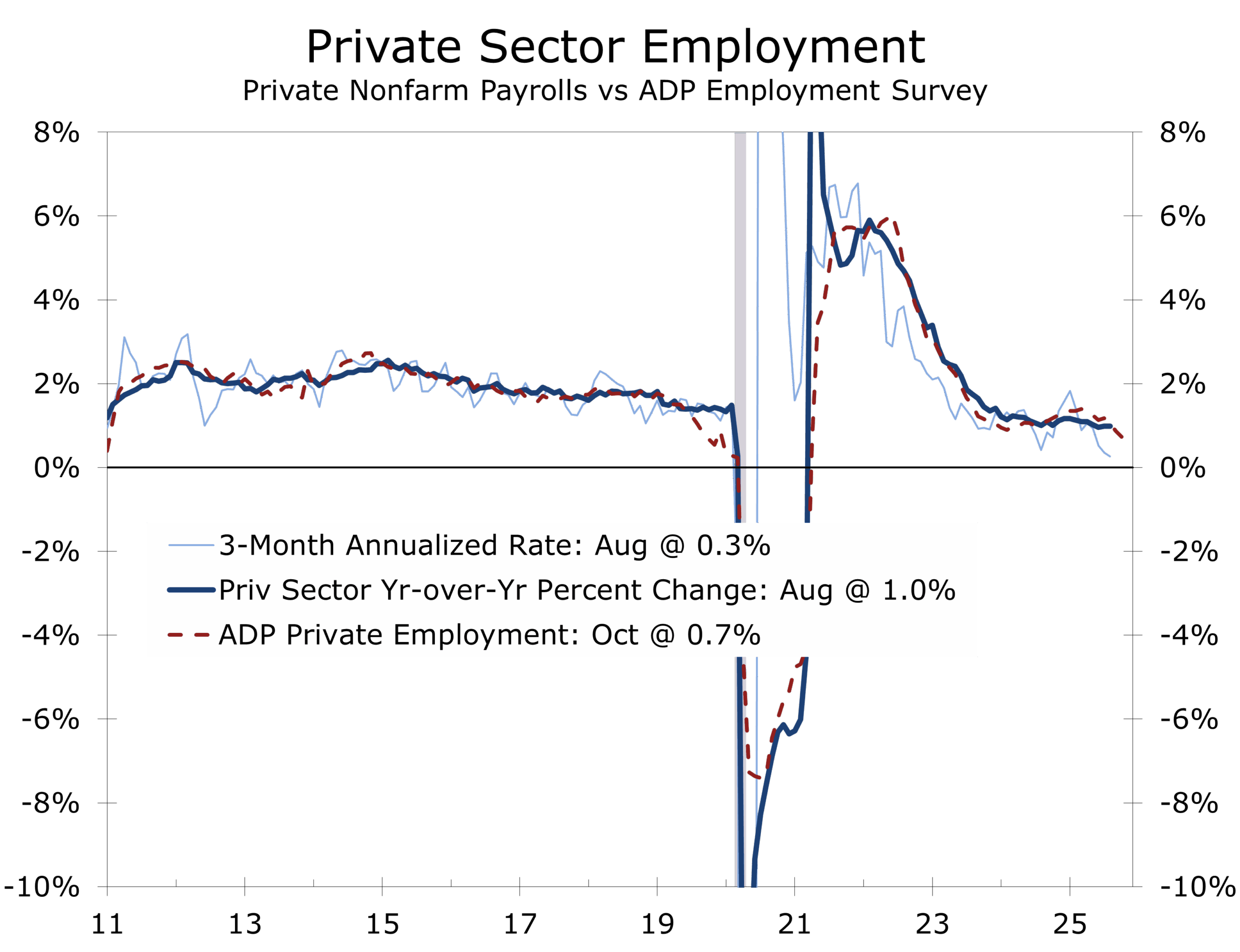

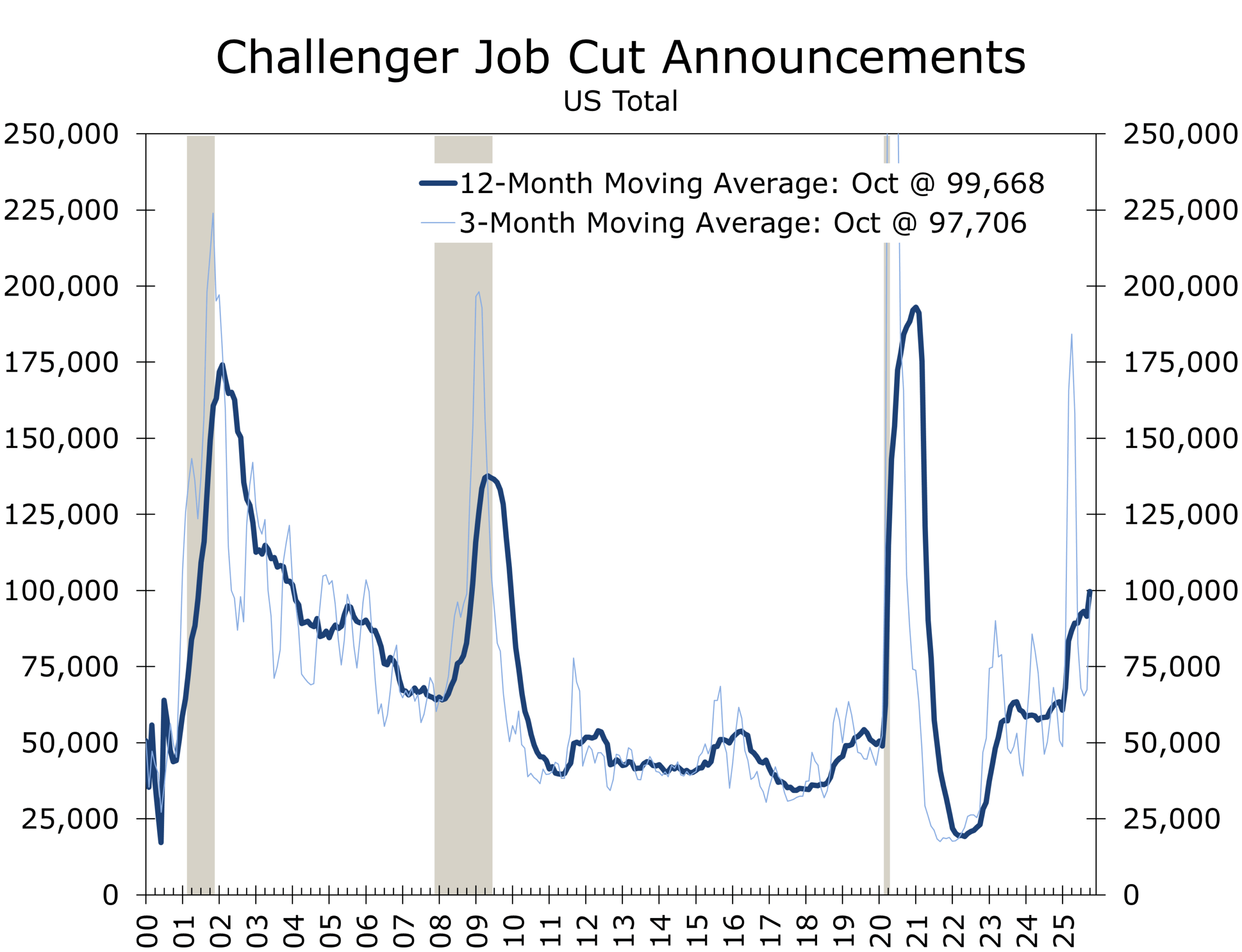

- The labor market is bending, not breaking, as hiring slows and layoff announcements rise, but weekly initial claims remain low. The gig economy and surging Baby Boomer retirements continue to cushion the adjustment.

- Consumers are far more worried about affordability than employment, explaining the widening divergence between deeply pessimistic Sentiment readings and the still-resilient Confidence measure.

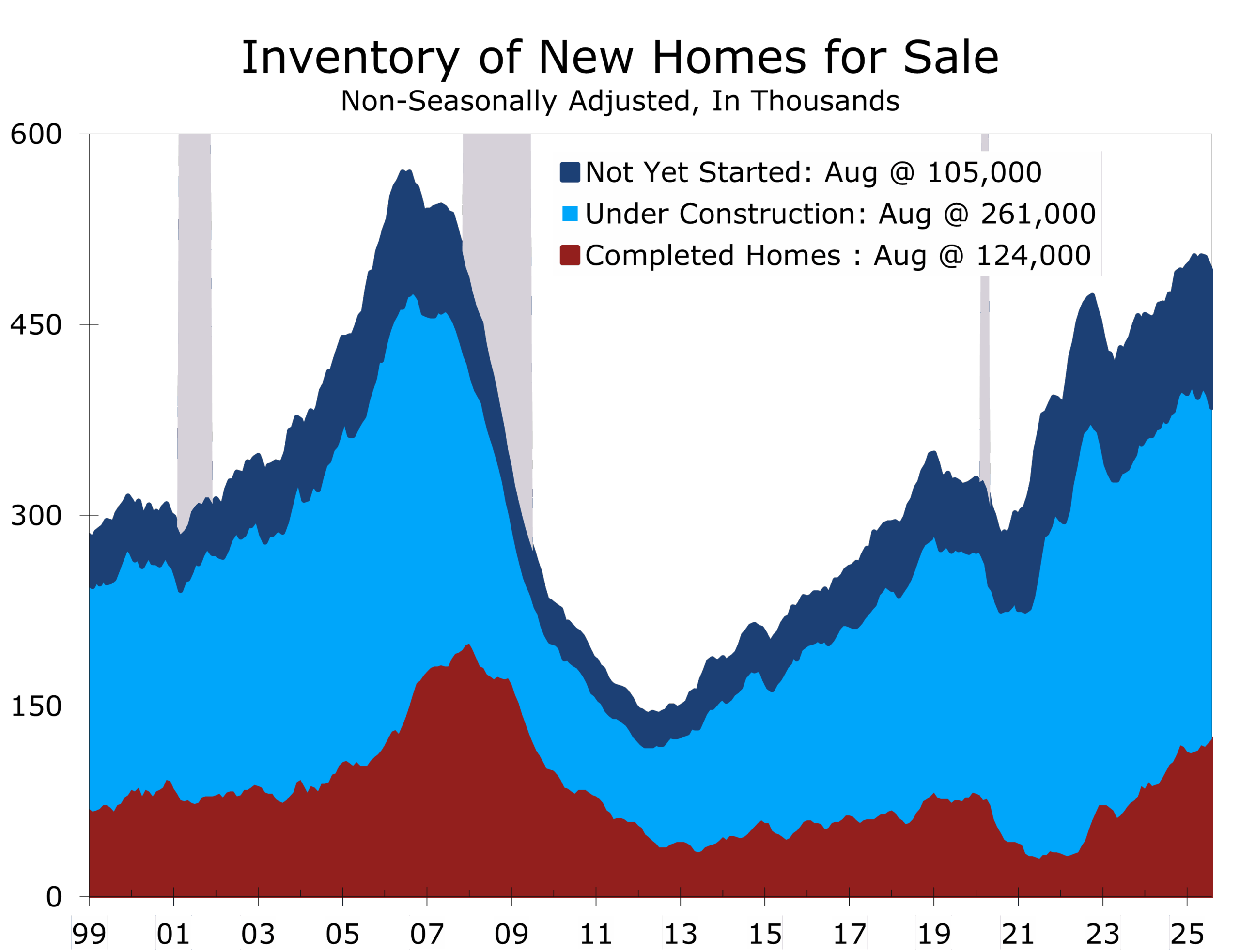

- Housing remains a paradox, with resale supply historically tight while new-home inventories climb. Lock-in dynamics, regional overbuilding, and demographic tailwinds support prices despite intense affordability pressures.

- AI skepticism reflects more dot-com trauma than current fundamentals. Today’s data show strong earnings, clean balance sheets, limited leverage, and capex aligned with real compute demand—conditions inconsistent with a speculative bubble.

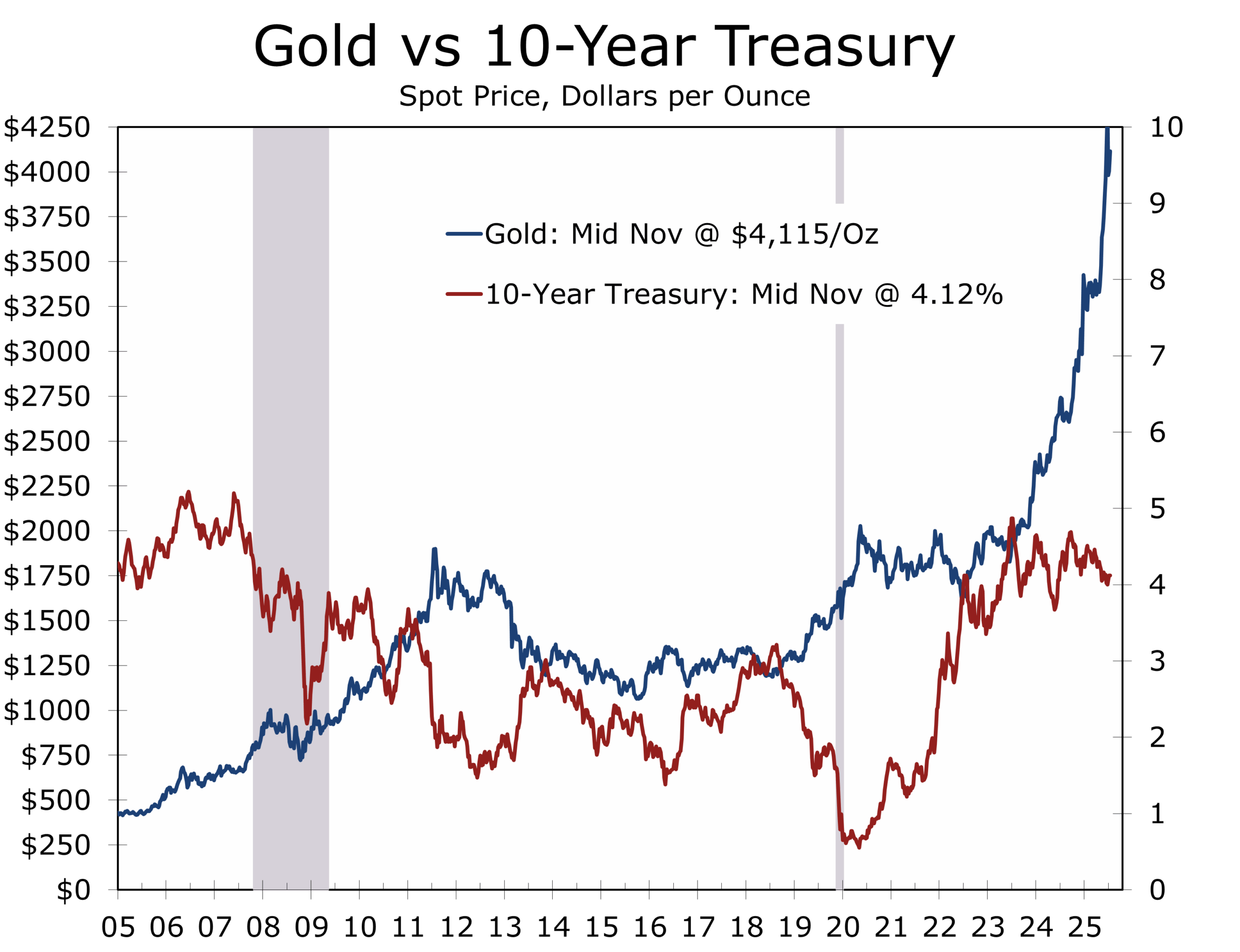

- Gold is signaling deep doubts about fiscal sustainability, institutional credibility, and the viability of aging, deficit-heavy advanced economies.

- Fed Nears End of Runoff: Powell’s tone suggests a pivot to growth management, with two more rate cuts likely this year.

- Seven Years’ War fiscal dynamics are reemerging, with major powers overspending into demographic headwinds, rising tax burdens, and broadening generational doubts about capitalism. Stalin’s line—“There are decades where nothing happens, and weeks where decades happen”—feels uncomfortably relevant.

- Geopolitics remain tense but contained, with slow-motion diplomacy between Saudi Arabia and Israel, persistent risks around Iran, and a fragile equilibrium across the China–Taiwan Strait. Russia continues pressing against Ukraine, increasingly targeting civilian infrastructure to break morale or provoke retaliation that could erode Western support for Zelensky.

- Domestic political undercurrents are shifting, with cities such as New York and Seattle electing young, inexperienced Democratic Socialist mayors—reflecting rising generational discontent. This dynamic is already shaping early 2026 political currents, including left-wing pressure on Minority Leader Hakeem Jeffries within his Brooklyn district.

THE FOG BEGINS TO LIFT

The six-week government shutdown severed the economy from its statistical nerve center. Without the jobs report, inflation, income, spending, or productivity data, markets were forced to navigate with one eye closed. For much of that period, the absence of data created more uncertainty than any single release likely would have.

Now, the fog is beginning to thin. The return of the September employment report offers the first hard anchor in more than a month, and expectations point to modest job gains—precisely what private-sector trackers indicated before the shutdown. September is likely to show an economy that lost some momentum but remained fundamentally consistent with its pre-shutdown profile.

October will be murkier. Survey windows were missed, responses were delayed, and parts of the dataset may require reconstruction. Private-sector proxies, including ADP’s 42,000 job gain, slowing weekly job data, and rising layoff announcements—indicate softer conditions with higher downside risks, but not an unraveling.

A newly published ADP weekly series paints a more cautious picture: in the four weeks ending October 25, firms shed an average of 11,250 jobs per week, suggesting that job growth was inconsistent and late-month momentum faded. Layoff announcements continue to rise, and other proxies point to softer hiring, higher downside risk—but at this stage, the signal is of deceleration, not collapse. Still, early estimates for the October employment data call for a net decline in payrolls, as DOGE-era retirements lead to a drop in federal payrolls that will easily swamp what now looks like a modest rise in private payrolls.

Inflation appears to be following a similar arc. Tariffs pushed some goods prices higher, but broader pricing power is fading. Rents and home prices are decelerating. Core services inflation, while elevated, shows renewed signs of slowing. When CPI and PCE return, they are likely to confirm that the tariff-driven bump has largely run its course and that underlying inflation continues to cool.

The fog is clearing—but as it lifts, long-standing vulnerabilities that were hidden in the haze are coming back into view. The softer pace of job growth and easing underlying inflation will inevitably shape policy, increasing the likelihood of selective tariff rollbacks and reinforcing the case for additional interest-rate cuts.

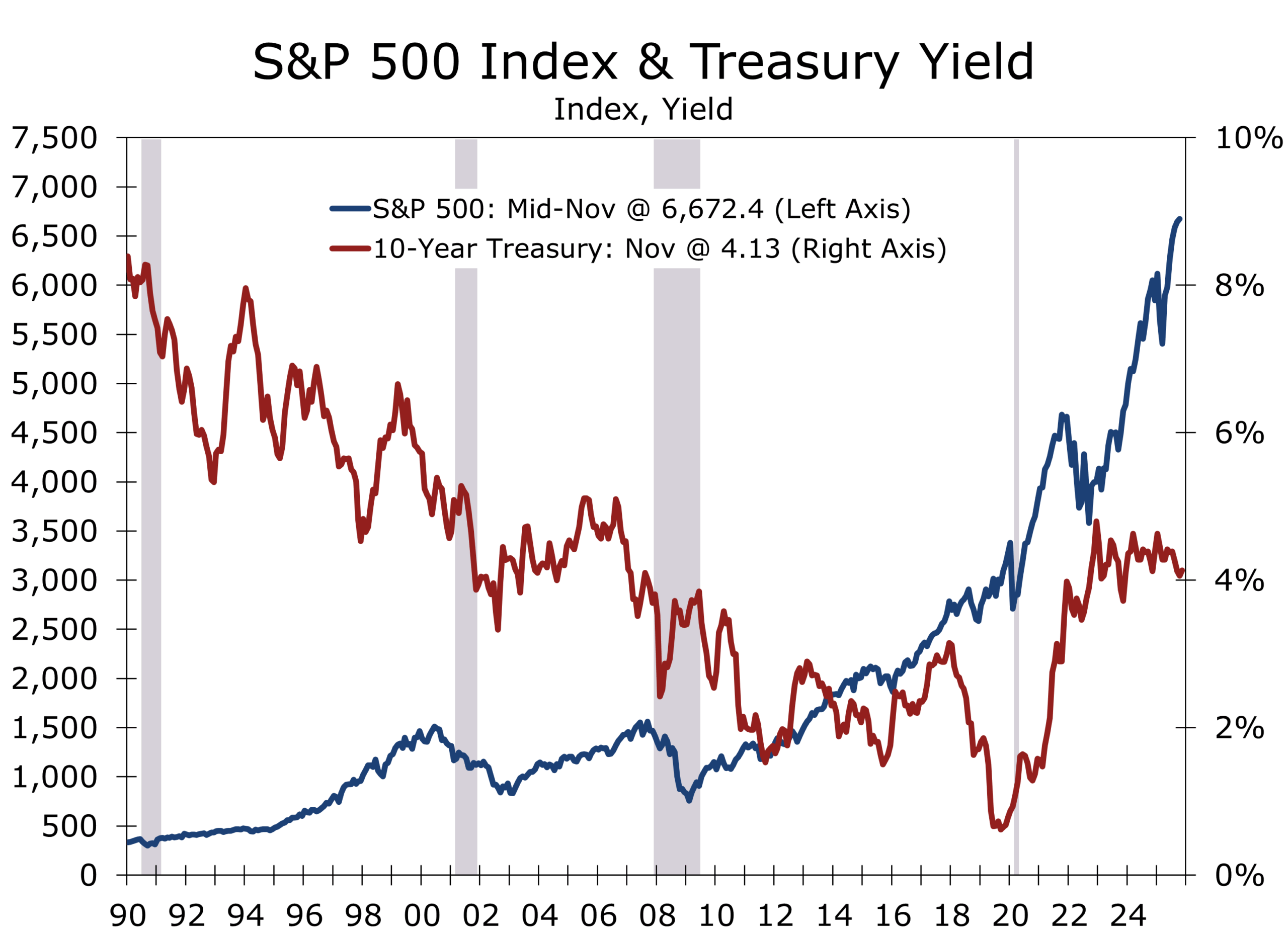

MARKETS: A CORRECTION AND A REORIENTATION, NOT A BUST

Markets remain cautious. The AI complex—once a runaway locomotive—is now moving more like a heavily loaded freight train cresting a grade: powerful, but deliberate, and increasingly sensitive to inclines. Recent selling has been concentrated in mega-cap tech, while cyclicals and defensives have held up better, signaling rotation rather than retreat.

AI skepticism has resurfaced, driven less by current fundamentals and more by the long shadow of the dot-com bust. The comparison, however, is superficial. Balance sheets are strong, leverage is minimal, earnings are rising, and capex remains tightly linked to real demand for computing power rather than speculative excess. IPO volumes are modest, and valuation expansion has been concentrated, not universal. A bubble requires broad exuberance and financial overextension; while markets have shown pockets of enthusiasm—especially as indices pushed to new highs—the underlying numbers do not support the excesses that typify true bubbles.

Even so, investors are on edge. The Economist’s warning that “the markets could topple the global economy” sharpened anxieties—especially among those who lived through 2000–2002 and 2008–2009. In this environment, sentiment reacts violently to uncertainty, even when fundamentals argue for a normal correction and continued sector rotation away from the most fully valued parts of the tech complex.

This market is undergoing a pivot—part correction, part rotation, part repricing—not a systemic breakdown. The path forward will depend on how quickly the data restore visibility. As the economic fog lifts and the trajectory of growth becomes clearer, we expect markets to stabilize and leadership to broaden beyond the narrow handful of AI-driven names that have dominated much of the past year.

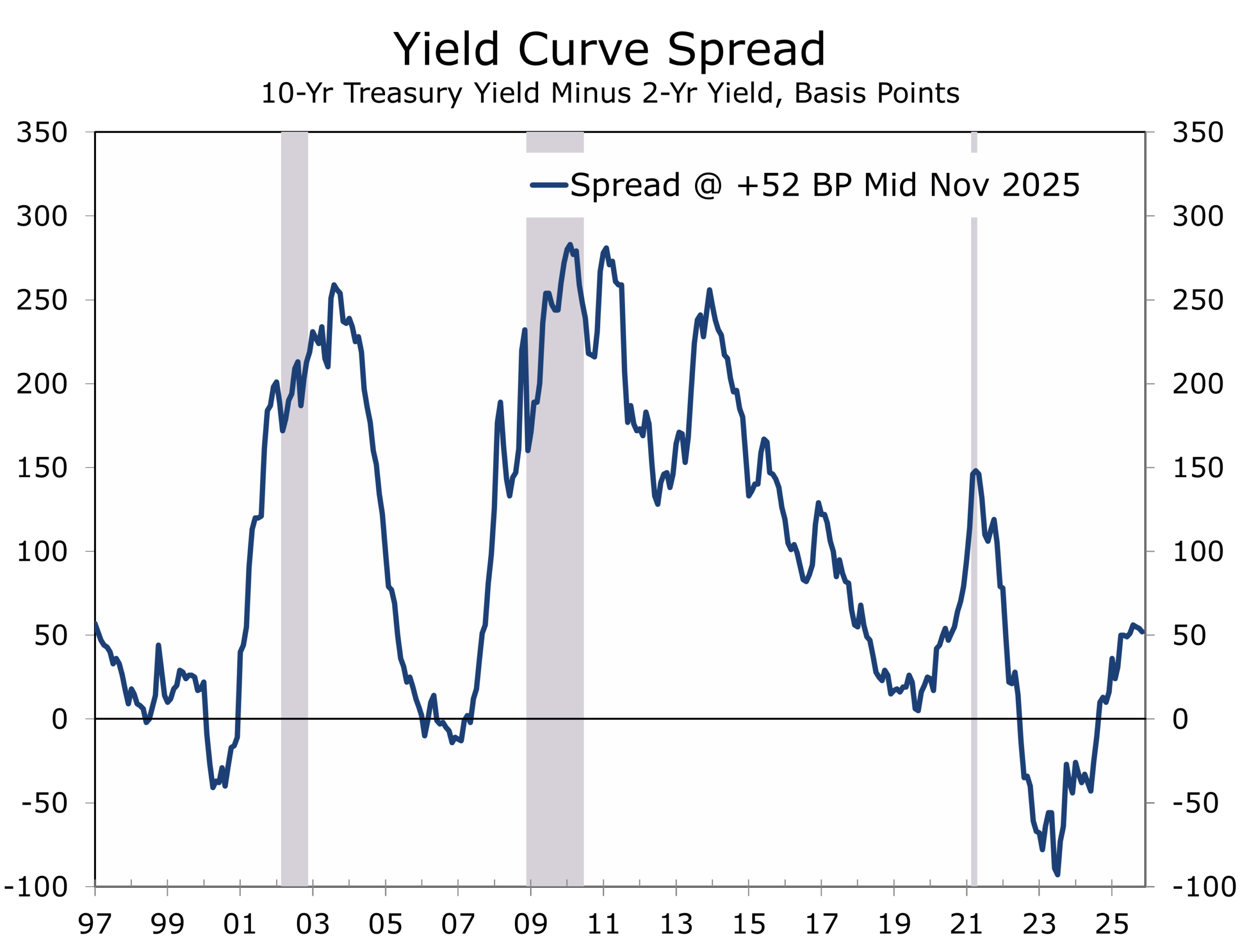

RATES & THE CURVE: ORDERLY NORMALIZATION, LATE-1990s PARALLELS

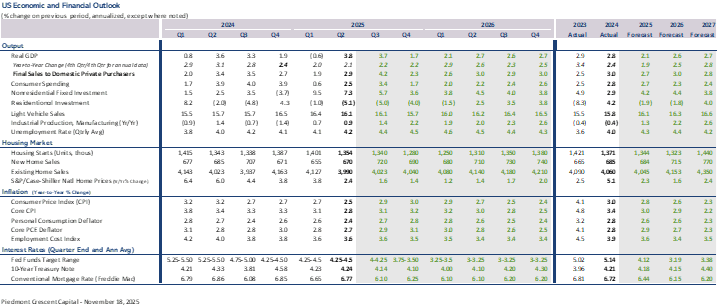

The yield curve has remained modestly positive for much of the year—a stark departure from the deep and persistent inversions of 2022–23. A drifting lower 2-year reflects expectations for at least one more cut in the federal funds rate, while the 10-year remains elevated due to firmer term premiums and large Treasury issuance. Together, they point to normalization rather than stress and reinforce our forecast for stronger growth in the second half of 2026 following a near pause in growth during the current quarter and Q1 2026.

Kevin Warsh and Kevin Hassett argue that today’s macro backdrop echoes aspects of the late 1990s: an early-stage productivity upswing driven by AI, hardened supply chains, and an investment-led expansion that could ultimately allow short-term rates to settle below what the forward curve implies. They view the present moment as closer to Internet 1.0 and the Y2K investment cycle than to any inflationary replay of the 1970s.

Christopher Waller—now widely seen as a leading contender for Fed Chair—takes a more incrementalist approach. He argues for refining the current framework rather than redesigning it and has signaled that another quarter-point cut in December will likely be appropriate. Waller has underscored that “easier financial conditions” reflected in markets earlier this fall were not being felt by middle-income households facing intense affordability pressures. He has also noted that the labor market is losing momentum and that tariff-related inflation noise is already fading, leaving core inflation “close to 2 percent.”

This debate highlights a deeper reality: high structural deficits are narrowing the Fed’s room to maneuver. Interest expense is consuming a growing share of federal revenues, Treasury issuance is lifting term premiums, and fiscal policy is exerting a growing pull on the long end of the curve. Monetary and fiscal tools—long treated as separate levers—are beginning to intersect in ways not seen in decades.

LABOR MARKETS: SOFTENING, BUT STRUCTURALLY SUPPORTED

Labor markets continue to cool. Hiring has slowed, job postings have eased, and layoff announcements are rising. Challenger’s October tally was the highest for that month since 2003 and WARN notices in several large states have moved higher. The pattern is eerily similar to the early stages of past recessions, where firms begin trimming headcounts well before claims rise. The trend is also broadening. Verizon announced the largest layoff in its history this past week, with plans to eliminate 13,000 positions—an unusually large move for a company that typically adjusts costs more gradually.

Despite the tide of announcements, weekly jobless claims remain low. Two structural dynamics explain the apparent contradiction. First, the gig economy now acts as a shock absorber, allowing displaced workers to pivot quickly into rideshare, delivery, freelance, or digital task-based income. This was evident during the shutdown, when furloughed federal workers immediately turned to gig work to bridge income gaps. The availability of flexible, on-demand earnings blunts the impact of layoffs and suppresses claims.

Second, accelerating Baby Boomer retirements continue to thin the labor force even as demand softens. This demographic shift reduces measured slack, supports wage stability, and prevents the kind of sharp unemployment spikes seen in previous downturns. Many firms are eliminating positions that might previously have gone to younger workers rather than laying off incumbents.

Labor markets are bending, not breaking. The still low unemployment rate likely overstates strength, while the surge in layoff announcements likely overstates weakness. The truth lies somewhere in between—a cooler, more cautious labor market with meaningful pockets of resilience, with payroll gains averaging 75,000 a month.

CONSUMERS: AFFORDABILITY IS THE PRESSURE POINT

Consumers remain far more anxious about affordability than about job loss. Rents, insurance, utilities, medical services, auto repairs, and debt service continue to compress budgets. This explains why the University of Michigan’s Index of Consumer Sentiment remains historically weak while the Conference Board’s Consumer Confidence Index remains consistent with moderate growth.

High-frequency spending data show a cooler but still expanding consumer backdrop. Lower-income households face the most intense pressure, with rising delinquencies, heavier Buy Now–Pay Later usage, thinning liquidity buffers—but overall spending remains positive.

HOUSING: THE PARADOX THAT DEFINES THE CYCLE

Housing remains the clearest example of structural imbalance. The existing home market is historically undersupplied. Millions of owners with sub-5% mortgages remain unwilling to list, creating structural scarcity and a durable price floor. By contrast, the new home market is working through the tail end of the pandemic-era pipeline. Builders in the Southeast and Mountain West are sitting on elevated completed inventories, the highest since the housing bubble—leading to aggressive incentives and rate buydowns to support absorption.

While new home inventories are the highest since the housing bust, this is not a replay of 2005–2007. While some formerly red-hot markets, most notably Central and Southern Florida, are seeing widespread declines, most markets are seeing only modest price adjustment and overall home prices are still running about 1.5% above their year ago level. The tight resale market prevents builders from slashing prices too much without triggering appraisal failures, cancellations, and margin deterioration. Moreover, Millennials and Gen Z continue to age into peak household-formation years, supporting underlying demand.

One way that consumers are adjusting is by migrating to parts of the country where housing is relatively more affordable. Texas, the Carolinas, Georgia, Tennessee, Arizona and Alabama are the big winners in this trend.

Gold, Deficits, and the New Age of Policy Doubt

Gold is rallying not because of near-term inflation jitters but because investors are questioning the durability of fiscal and geopolitical strategy itself. Structural deficits continue to widen, aging populations are colliding with rising interest burdens, and political systems across advanced economies remain unwilling—or unable—to confront basic fiscal arithmetic. The result is a growing search for assets immune to policy drift. Gold has become less an inflation hedge and more a hedge against eroding fiscal capacity across the U.S., Europe, Japan, and increasingly China, where demographic decline and debt saturation present challenges just as severe.

Layered onto these pressures is the intensifying U.S.–China microchip rivalry—a technological arms race reshaping global power dynamics and straining national budgets. Washington’s CHIPS incentives and export controls, combined with Beijing’s massive state-backed subsidies, have set off a costly contest for semiconductor self-sufficiency. That competition is cascading through the rest of the world: developed economies in Europe and East Asia are being pulled into subsidy battles to protect their own chip ecosystems, while developing economies—from Vietnam and Malaysia to Mexico and India—are absorbing new investment flows as supply chains reroute. The race for technological sovereignty is becoming a fiscal challenge as much as a strategic one, amplifying the sense that traditional policy frameworks are no longer fit for the era.

The historical rhyme is unmistakable. The Seven Years’ War drained the treasuries of the world’s major powers as they chased geopolitical advantage, triggering fiscal crises, heavier taxes, and rising public frustration—conditions that helped set the stage for the American Revolution. Today’s environment carries a similar echo: mounting fiscal stress, institutional fatigue, and a generational skepticism that the existing economic model can still deliver upward mobility or broad-based prosperity.

Stalin’s stark warning captures the moment: “There are decades where nothing happens; and there are weeks where decades happen.” After years in which deeper structural issues could be deferred, the combination of deficits, demographics, and dual-use technology competition has pushed them to the forefront. Gold’s strength is not about the next CPI print—it reflects rising concern over what the next decade will demand from fiscal and monetary systems already stretched to their limits.

GEOPOLITICS: SLOW MOVES, SHARP UNDERCURRENTS

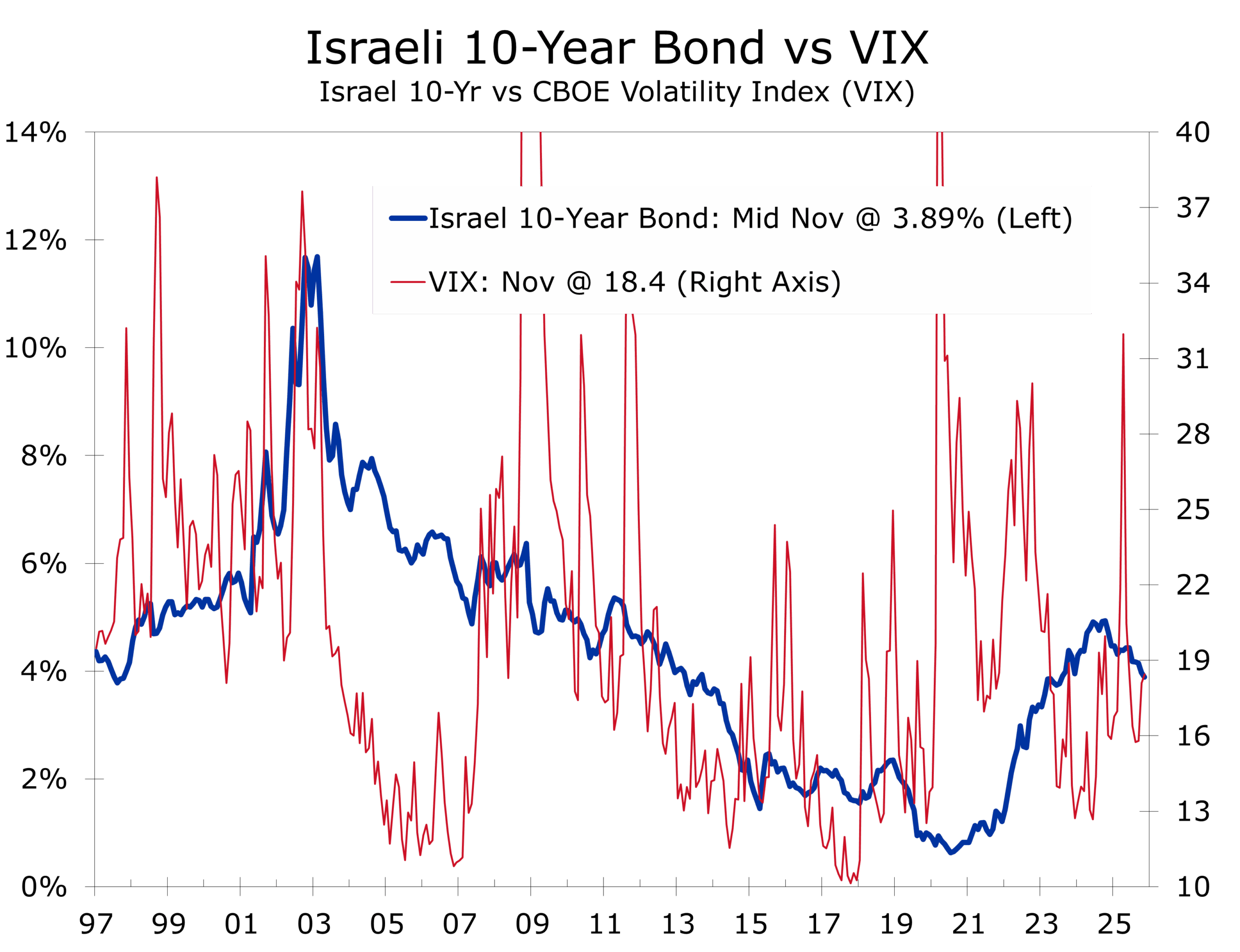

The Middle East tail risk has fallen sharply. The decisive ceasefire that took effect on October 10 has held and the UN Security Council’s unanimous November 17 endorsement of the Trump 20-point Gaza plan—backed by Saudi Arabia and the UAE—has dramatically raised the odds of Saudi-Israeli normalization at some point in 2026. Riyadh’s asks (U.S. defense treaty, civilian nuclear program, tangible Palestinian progress) are steep but now within reach. Credit markets have already responded: S&P shifted Israel’s outlook to stable on November 7, Israeli 10-year yields have dropped 45 bps since early October, and Gulf sovereign spreads are at two-year tights.

Iran remains the principal residual wildcard. Proxy forces are subdued but not disarmed, missile and cyber programs advance unchecked, and domestic pressure could still trigger asymmetric retaliation if Tehran feels encircled by a formal anti-Iran axis. Base case is further de-escalation.

China continues tightly calibrated gray-zone pressure on Taiwan while closing the military gap at pace. TSMC-centric exposures carry explicit invasion pricing—keep rotating to on-shored and diversified-node semis.

Russia systematically strikes Ukrainian civilian infrastructure while baiting Kyiv into responses on Russian soil that would erode international support. European utilities, grains, and freight remain vulnerable; energy prices appear too low given the risk set—stay long hard-currency energy.

U.S. generational backlash is accelerating, amplified by documented PRC, Russian, and Iranian social-media influence operations. DSA mayors hold New York and Seattle; Hakeem Jeffries and Governor Kathy Hochul face credible 2026 left-wing primaries. Favor investments in red states, particularly Texas; raise hurdles for duration and illiquid credit in progressive jurisdictions.

Mexico’s Gen Z protests have escalated into the most sustained and geographically widespread unrest since 1994. Triggered by collapsing real wages, cartel violence spilling into urban areas, and anger at perceived judicial capture under the outgoing administration, demonstrations have paralyzed major cities and forced repeated highway blockades. President-elect Sheinbaum has responded with a mix of concessions and force, but confidence in public security remains at multi-decade lows. Near-shoring beneficiaries with more than 30% Mexico revenue exposure (auto parts, electronics assembly, logistics) now trade with a visible political-risk discount. Selectively underweight or hedge that exposure; favor exporters with U.S.-centric or multi-Latin American footprints.

Risk premiums are easing but not gone. Favor gold, short-dated T-bills, defense, energy, commodity-exposed investment, and a neutral-to-modest overweight on Israeli and Gulf credits. Watch Saudi normalization triggers closely—upside surprises are now the higher-probability outcome. Position defensively but opportunistically.

Outlook – The Fog is Thinning, Albeit Unevenly

U.S. growth has proven far more resilient than nearly anyone expected at mid-year. The Atlanta Fed GDPNow has consistently tracked at or above the high end of consensus, and even after the prolonged government shutdown shaved Q4 estimates, the underlying pace remains robust. Beneath the noise lies the same structural shift we have highlighted all year: an economy increasingly powered by capital-intensive, high-productivity sectors—AI infrastructure, aerospace, defense, and advanced manufacturing—rather than traditional labor-driven expansion. Productivity is quietly rebuilding the foundation for durable growth.

Layoffs have spiked but remain concentrated in a handful of over-extended sectors and have not yet triggered broader contagion. Housing continues to restrain momentum yet does not pose systemic risk; new-home inventories are rising, existing-home supply remains tight, and prices are adjusting modestly. The housing drag is now unambiguously disinflationary, giving the Fed additional latitude to ease.

We still expect the Fed to accomplish more by doing less—no more than three additional 25 bp cuts in the base case. A weakening labor market, the recent equity correction, and the Fed’s upcoming leadership transition introduce modest downside risks, but nothing that derails the expansion. Markets have begun pricing exactly this scenario. Not a boom, nor a bust, but a resilient gradual reacceleration that becomes visible by mid-2026.

The shutdown and layoff headlines generated fog, yet the core pillars: innovation, secure property rights, and trusted capital markets remain unshaken. The fog is thinning, unevenly but unmistakably. We expect growth to surprise to the upside once again in 2026.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 18, 2025

Mark Vitner, Chief Economist

704-458-4000