A View from the Piedmont

Our Weekly Commentary on Money, Credit, Exchange Rates and Geopolitics

Highlights of the Week

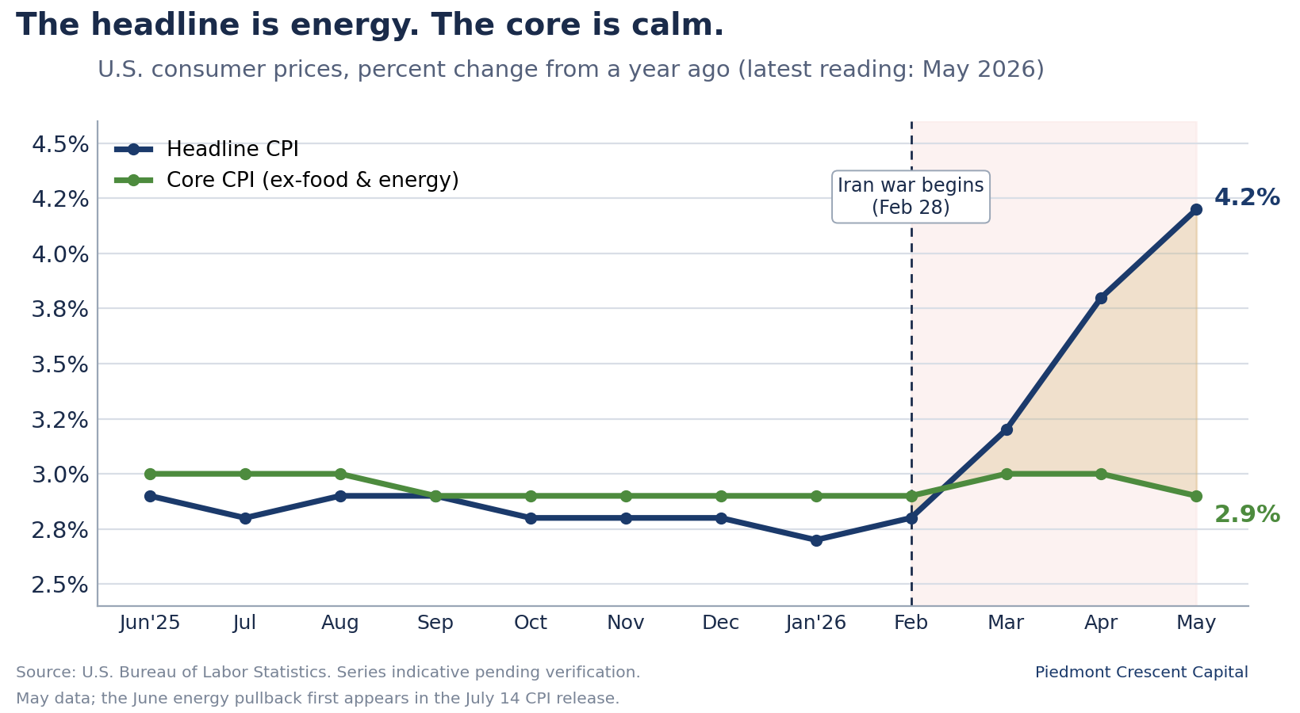

- Inflation: May CPI rose 0.5% on the month and 4.2% over the year, a three-year high. Soaring energy prices drove better than sixty percent of the gain, while core rose only 0.2%. Imported.

- Pipeline: Producer prices climbed 6.5% year on year, the most since 2022, with goods posting a record monthly jump. AI hardware is now a second engine.

- Labor: Payrolls rose 172,000 versus 80,000 expected, with 93,000 in upward revisions. Part of the beat might be pre-World Cup hiring that reverses in August.

- Capital cycle: Manufacturing has turned up and the build-out is broadening from AI to Boeing, defense replenishment, and reshored pharma, steel, and chips.

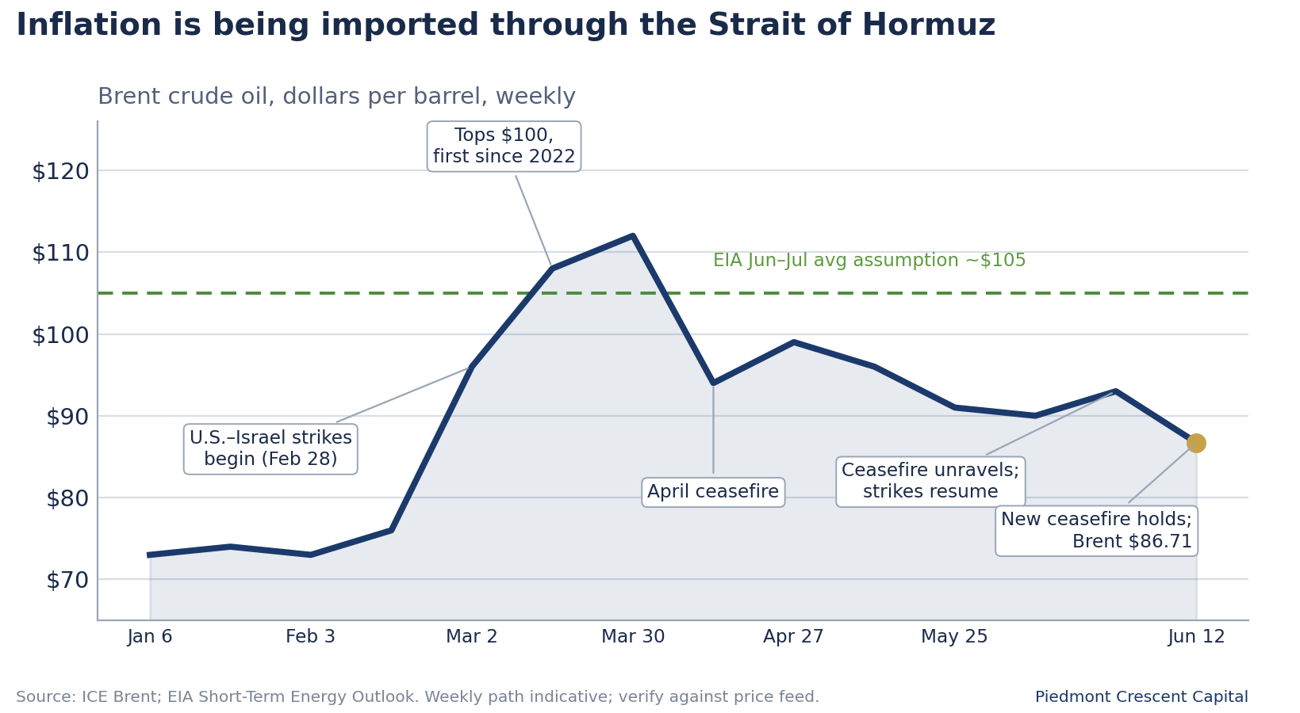

- Geopolitics: A reported fourteen-point draft would reopen the Strait of Hormuz, though a full physical reopening looks more like late summer than the thirty days. Crude is down about a quarter from its March peak with the strait still shut.

- Global: The World Bank cut 2026 world growth to 2.5%, the weakest since the pandemic, while holding the US at 2.2%, far ahead of Europe and Japan.

- Fed: Warsh chairs his first FOMC June 16 to 17. We expect a hold, no 2026 cut, and the next Fed move to be a hike. The consensus is now converging on the no-cut call, while the ECB hikes and the Bank of Japan looks set to follow.

- Our view: Stay constructive on the expansion, cautious on duration, and selective on the capital-investment trade driving both growth and volatility.

The Tanker and the Server

The hiring rebound reflects genuine strength, and the inflation spike is essentially an imported tax. The way to deal with a supply shock is to allow supply to increase, not implement a slowdown the economy does not need.

— Vitner, on an economy strong enough to carry a war premium

Three threads ran through the week. Two inflation reports that looked alarming on the surface but milder underneath; which followed reports of a labor market that ran hotter than almost anyone expected; and a war that, after a hundred days, may have finally started its turn toward a deal. The economy is absorbing two supply shocks at once. The first is transmitted via tanker traffic, or the lack thereof, as a closed strait keeps Gulf crude bottled up and explains most of a 4.2 percent headline CPI spike. The second is transmitted over optical fiber via servers, as the build-out of artificial-intelligence infrastructure tightens the market for chips and electronics the way a war tightens the market for diesel. The first is a supply shock, which monetary policy can do little about. The second is a demand shock, driven primarily by the relative ease with which AI firms are raising capital in the private and public markets. Higher interest rates would dampen this trend but would also weigh heavily on other parts of the economy where demand is not nearly as strong. What is new in our view is a focus on the latter. The economy beyond these price shocks is strengthening, not weakening, and that changes the direction of the next policy move. We expect a hold in June and at least through the midterms. After that, and we now see the next move as more likely a hike.

What follows walks through the May price reports, the labor beat, which was flattered by a big surge in hospitality hiring, the broadening capital cycle, Chairman Warsh’s first FOMC meeting, the reported Iran framework and the Hormuz hangover behind it, and another volatile week in the financial markets, which included the long anticipated SpaceX IPO. We close with the CFO corner, the scenario framework, and our forecast update.

The Inflation Reports: Imported, Not a Spiral

The CPI report looks worse than it is. Headline inflation rose half a percent in May and sits at 4.2 percent over the past year, the fastest pace in three years. Open it up and the level of concern fades a bit. Energy rose nearly four percent in a single month and accounted for more than sixty percent of the all-items gain, with gasoline up better than forty percent from a year ago. Strip the war out and core prices rose two-tenths of a percent, the mildest reading in months, and core goods actually fell. The tariff pass-through that so many braced for is not showing up at the register. What is showing up is a fuel surcharge on the whole economy, and fuel surcharges are not what monetary policy is built to fight.

The producer report adds a second engine. Wholesale prices jumped 1.1 percent on the month and 6.5 percent over the year, the steepest annual climb since late 2022, with goods posting their largest monthly gain on record. The breadth runs wider than oil. Diesel lifted freight, fertilizer ran up sharply and will eventually extend to the grocery aisle, but only partially and with a lag. Core goods climbed above five percent as memory chips and electronics tightened on AI demand. We feel the Fed will treat the war-related runup as close to cresting and view the technology line as more durable. The first will ease when the tankers move again. The second is the price of a building boom we would rather have than not, that is largely being financed by private capital and generous public valuations.

The Labor Market: Firm, with a World Cup Asterisk

The beat was real but partly borrowed. Employers added 172,000 jobs in May, more than double what was penciled in, and March and April were revised up a combined ninety-three thousand. The unemployment rate held at 4.3 percent. Some of that strength, though, reflects an earlier than usual Memorial Day, which likely pulled summertime hiring forward. The World Cup also likely bolstered hospitality payrolls. Business-services hiring in the host metros ran well ahead of the rest of the country as cities staffed up for the tournament, and the leisure and hospitality lift will build through June and July before giving back in August. We read the underlying trend as genuinely improving, but modestly so, and we would discount the next two payroll reports and warn readers not to mistake an early summer and packed sporting calendar for an acceleration.

The distortion cuts both ways, and the runway is long. The eleven host metros span the country and account for about a third of national output, so the lift shows up in the national aggregates, hot in the summer and soft in the fall. Some of these markets could use the lift. Atlanta is a clear example, hit hard this year by federal job cuts, and its hospitality sector has made significant investments ahead of the games, so the tournament arrives there as a welcome offset rather than a distortion to discount. The events are not a one-summer affair. The World Cup this year, the nation’s two hundred fiftieth anniversary alongside it, and the Los Angeles Olympics in 2028 give the hospitality and travel sector a multiyear runway of marquee demand that few other parts of the consumer economy can claim. Moreover, Memorial Day fell early this year, while Labor Day will come relatively late. The calendar works nicely for an economy where Americans are staying close to home this year and larger numbers of international travelers are coming to the U.S. for the World Cup and Olympics.

The Real Economy: A Broadening Capital Cycle

The productive core is gaining strength. Manufacturing has turned the corner, with the factory diffusion index back above the waterline and payrolls in the sector adding rather than shedding, the kind of cyclical impulse that tends to lead rather than lag broader economic strength. The capital cycle behind it is broadening well beyond the data centers. Boeing is ramping production in the Pacific Northwest and South Carolina, the defense base is replenishing munitions stocks on multiyear contracts across a dozen states, the Space race is in full force, driving economies across the South, and the reshoring of pharmaceuticals, steel, and semiconductors is putting shovels in the ground from Arizona and central Texas to Ohio, Georgia, and the Carolinas. Business fixed investment is running better than six percent with equipment in double digits. The economy is getting its calories primarily from protein and vegetables, which should keep it lean. Persistent inflation comes from easy money that fuels consumer spending, something that is not in place today.

The consumer is squeezed but cushioned. Real hourly pay slipped again in May as prices outran wages, which is why two-thirds of Americans now call inflation a very big problem. Yet the consumer has not buckled. Tax refunds are still flowing, including the tariff refunds reaching companies and households after last winter’s court ruling, household equity wealth sits near records, and a restocking inventory cycle is adding to growth. Step back and the contrast is stark. The World Bank cut its 2026 world growth forecast this week to the weakest since the pandemic, with the euro area barely positive and Japan softer still, while holding the United States near its prior pace. The war is a tax on everyone. The American economy, with its outsized energy sector, is simply better built to pay it.

The Warsh Fed: A Hold, and a Tilt Toward a Hike

The center holds and watches. Chairman Warsh chairs his first meeting on the seventeenth, and the Committee will in all likelihood stand pat. The case for holding is now nearly unanimous among officials who describe themselves as well positioned and content to watch how the conflict and the data evolve. Cutting rates into a four-percent CPI print with payrolls running this hot would invite the one outcome a central bank cannot tolerate, which is a public that comes to expect higher prices as a matter of course.

The minority has turned toward tightening. A widening group worries that inflation is not heading the right way, that price pressures outside housing have been stuck for two years where neither tariffs nor energy is the obvious cause, and that waiting for proof of embedded inflation only guarantees a larger adjustment later. President Collins put it best when she described her patience for looking through yet another supply shock as worn thin after five years of above-target inflation, and this from an official who still hopes to ease before year-end. Europe’s central bank raised rates the same week, the first major authority to tighten into the war’s inflation. We see no cut in 2026, a hold next week, and the next move, when it comes, more likely a hike than a cut. That hike might not come until late 2027 or early 2028, by when conditions could very well change.

We were early, and the consensus is catching up. We removed the last 2026 cut from our base case two weeks ago, when the prevailing forecast still carried a September move. Since then, the major houses have fallen into line, either calling for hikes or pushing their final cuts deep into 2027 and conceding that core inflation will sit above target all year. We are comfortable a step ahead of that crowd, and a notch more hawkish than where it has landed, because the resilient activity data and a core still north of three percent tilt the risk toward a hike rather than a cut. We do not expect any move this year, however. It is worth adding that the Fed is now the outlier among major central banks, holding while Europe raises rates and Japan prepares to. A central bank that stands pat while its peers tighten is, at the margin, importing a softer currency and a little more inflation, which only reinforces the case against easing.

Geopolitics: A Draft Deal, and the Hormuz Hangover

The tanker may be turning toward home, but slowly. The escalation was real at midweek, a second round of strikes and counterstrikes against Gulf bases and then a threat to seize Iran’s oil. Then the tone changed. Iranian state media circulated a reported fourteen-point draft that would lift oil sanctions, release frozen funds, withdraw US forces, commit Tehran to forgo a nuclear weapon, and reopen the strait within thirty days, with the President suggesting it could be signed at the summit of major economies in Europe this weekend. Crude broke lower in a big way, with both benchmarks closing at three-month lows. We would read the thirty-day timeline as a diplomatic number rather than a physical one. Getting Gulf exports back to normal looks more like a mid- to late summer endeavor, and even that requires flows through the strait to climb back toward seventy percent of their pre-war level alongside the workarounds already running through Yanbu, Fujairah, and Ceyhan. Some of the more extreme takes on this have oil prices elevated well into 2027, as facilities are repaired and oil importers rebuild stockpiles. All of that can happen with lower oil prices, however, as production limits will likely be ignored and non-OPEC gains in output are likely to remain in place.

The more telling fact is why crude fell at all. Oil is down about a quarter from its March peak with the strait still largely shut, which should not happen if the price were only a war premium waiting on a ceasefire. The deficit during the disruption has been far smaller than feared, on the order of five to six million barrels a day against a hit to Gulf production more than twice that size, and the gap has been filled by demand that simply went away. Much of it is China, where the shift into electric vehicles has accelerated since the war began. That is the part the cheering misses. Lower oil is a genuine relief for the American consumer, but the reason it is falling is weak global demand as much as the prospect of peace, and weak demand is not an unmixed blessing. More supply also appears to be reaching markets around the world, including increased shipments from the U.S. and Latin America as well as tankers clandestinely escorted out of the Persian Gulf.

Even a reopening leaves a higher floor. Clearing the mines, repositioning the hundreds of stranded tankers, restarting shut-in production, and refilling the inventory hole the closure dug takes months, not days, and runs well into the autumn. And when it is done, the war will have left a mark. Depleted stockpiles and a market that now prices a premium for the risk of the next disruption keep a floor under crude even against a record surplus building for next year. The surplus caps the ceiling. The security premium lifts the floor. We are nudging our own base case up, toward Brent near ninety dollars into year-end rather than the mid-eighties we had carried, with a long tail toward triple digits if the draft falls apart. We are still calling for lower oil prices than the current consensus. Markets do a good job of deciphering all the conflicting information and are more attuned to new supply developments.

None of it changes the policy call. Lower oil takes the sting out of the headline and makes May the likely peak for top-line inflation, the closest thing to a tax cut this economy has had all year. It does not pull the Fed toward a cut. Our case for a hold now and a hike next rests on the part of the economy that has nothing to do with the strait, the firming labor market, the manufacturing turn, the broadening capital cycle, and a core that has been stuck for two years. On the relief, yields slipped and the market pared a little of its hawkishness, the reflex on every de-escalation day. We would fade that move and keep our duration short until the tankers actually move.

Markets & Financial Conditions

The bond market keeps duration short, and here we part ways with the consensus. The long-bond reopening drew soft demand and tailed by the widest margin since late 2024, with dealers left holding more than they wanted amid worries about the deficit, inflation, and oil all at once. The two-year sits at its highest in sixteen months and the ten-year near four and a half percent. The prevailing view looks for the ten-year to drift lower into year-end as the energy spike fades. We are not in that camp. The term premium, fed by the deficit, heavy issuance, a tightening bias, and an energy security premium, keeps the long end sticky, and the asymmetry in long yields is to the upside. A price shock with no clear end date, set against a central bank whose next step is more likely up than down, is not the backdrop for reaching out the curve in search of yield.

Equities are earnings-led, and not yet at a peak. This year’s gains have tracked earnings revisions rather than expanding multiples, a healthier footing than a melt-up on hope. The features that marked past market tops, speculative mania, a deteriorating growth backdrop, a flood of new issuance, and a tightening Fed, are mostly absent today, even if a little closer than at the start of the year, and the better gauges of speculative trading sit well below their 2000 and 2021 extremes. That argues the bull market has further to run, with the broad index able to grind higher into year-end on profits rather than euphoria. What we watch is not the level but the breadth. Not at a peak is not the same as without air pockets. The leadership is narrow, the volatility is real, and a market this concentrated in one theme can correct hard without the economy doing anything wrong.

Piedmont Perspective: The Capital Cycle Comes Home

There is a temptation, when a single category of spending grows large enough to bend a national price index, to call it a bubble and move on. We think that misreads what is happening, and the misreading matters because it would steer capital away from the most productive investment cycle the country has seen in a generation. We find it instructive to remember that capital always seeks its highest risk-adjusted rate of return. Right now, that is in AI and all things associated with the AI buildout. Will it get overdone? Microeconomic theory says yes. Just when, however, is nearly impossible to tell just yet.

The hyperscalers are on course to spend on the order of three-quarters of a trillion dollars on AI infrastructure this year, and the consensus for next year may still be too low. This is a capital cycle in the older and more honest sense of the term, the kind that lays down physical plant, draws on real power and steel and labor, and leaves behind productive capacity rather than a pile of marked-up paper. And AI is the largest strand but not the only one. Boeing is climbing back toward full production, the defense base is replenishing depleted stocks, there is boom in the Space industry and the reshoring of pharma, steel, and semiconductors is adding plant and payroll in places that spent a generation losing both. What looks like a technology story is better understood as a broad re-industrialization.

The cycle is now reaching the wellhead. After a decade of starving themselves of reinvestment in order to return cash to shareholders, oil and gas producers are being rewarded for spending again, and energy capex looks set to return to double-digit growth next year. This is not a coincidence sitting beside the AI story. It is the same story. The server drives power demand, power demand drives the grid, and the grid and the data center together drive the wellhead. Even the coal industry is looking more promising, boosting prospects for railroads and utilities that now have an extended window to operate depreciated facilities. The capital cycle that began in the data center now runs through the energy patch, the transmission line, and the turbine yard, which is one more reason we think it has staying power.

The closest analog is the late 1990s, and it is instructive in both directions. That decade’s investment in fiber was real and raised productivity for years, and it also outran near-term demand badly enough to punish the firms that financed it on credit. The lesson is that the capital cycle and the equity cycle are different animals. Today’s spending is funded largely out of the deepest cash flows in corporate America, a sturdier base than the telecom debt of twenty-five years ago, but the valuations have run and the dispersion of returns is enormous. Some of these companies are building the railroad. Others are selling tickets to a destination that may not generate the traffic the price implies.

The footprint is national, reshaping regional economies that had little to do with technology a decade ago, from Northern Virginia and central Texas to Arizona, Ohio, Georgia, and the Carolina Piedmont, with grid strain from the PJM mid-Atlantic to the Texas interconnection. The particulars differ by region. The pattern does not. It is protein, not carbohydrates. It compounds. We would own the cycle but would be choosy about how.

CFO & Treasurer Corner: What This Means for Corporate Finance

Funding and liquidity. With the ten-year near 4.55 percent and the next policy move more likely up than down, the case for opportunistic fixed-rate issuance is stronger, not weaker. Floating-rate borrowers should stress coverage on a ten-year at or above 4.50 percent and a policy rate unchanged through at least the November midterms.

Energy and input costs. Crude has broken to three-month lows, but the relief builds gradually. The physical reopening of the strait looks like late summer, not thirty days, and a security premium is likely to keep a floor under oil even after it clears. Firms exposed to freight, logistics, or petrochemical inputs should plan for energy costs that ease through the third quarter rather than collapse and should not bank on a deal that is not signed and lived up to.

Labor and wages. Discount the next two payroll and retail reports for the World Cup, hot in summer and soft in the fall. World Cup watching parties will provide a lift to bars across the country. The underlying hiring trend is improving, and wage pressure is easing at the margin, which helps the cost line. Firms relying on slack to refill roles cheaply should not assume it.

Cost of capital. Gains are earnings-led, but leadership is narrow and volatility is real. Treasurers planning equity-linked issuance or buybacks should assume more two-way volatility and a higher cost of equity than the spring’s calm implied. The fixed-rate funding case is stronger now that the near-term cut is off the table.

Capital allocation. The capital-cycle thesis holds. Commitments tied to AI, power, grid, and reshoring remain on plan, and the market continues to reward credible productivity narratives over undisciplined spending. The bar for capex without a clear margin path keeps rising.

Planning assumption. Our base case is a prolonged Fed hold with no cut in 2026 and the next move a hike, an Iran framework that reopens Hormuz by late summer rather than in thirty days, Brent settling near ninety dollars into year-end with a security premium under it, and full-year US growth near 2.5 percent led by capital spending. Boards should model the no-cut case as central and keep a deal-collapse case, with oil back toward triple digits, live for the third quarter.

Looking Ahead

| When | Release / Event | Why It Matters for CFOs & Markets |

|---|---|---|

| Mon–Wed | Summit of major economies (France) | Iran tops the agenda. Watch for a signed framework and a firm Hormuz reopening timeline. A signing would confirm the oil-down, risk-on read; a collapse would reverse it. |

| Tuesday | FOMC begins; Retail Sales (May) | Energy will distort the sales headline, and the World Cup will begin to pad the numbers in June. Watch the control group for the true consumer read. |

| Wednesday | FOMC decision; Industrial Production (May) | A hold is near-certain. The story is the dot plot and whether the language tilts toward a hike. IP is a clean look at the manufacturing turn. |

| Thursday | Housing Starts (May); Initial Claims; LEI | Starts test how four-and-a-half-percent yields bite. We will be looking for confirmation that the recent rise in claims is seasonal noise, not a trend. |

Scenario Framework

| Scenario | Macro & Market Implications | Corporate Finance Action |

|---|---|---|

| Base Case55% | The framework holds and Gulf exports normalize by late summer; Brent settles near ninety dollars into year-end as inventories slowly refill, with a security premium under the price. Labor stays firm and broadening once the World Cup noise clears. The Warsh Fed holds in June with no cut in 2026 and a tightening bias. The 10-year holds 4.40% but trades as high as 4.70%. | Lock fixed-rate funding opportunistically. Stay with productivity-led capex. Model a no-cut-in-2026 path. Treat equity concentration as a conditions risk. |

| Benign20% | Exports normalize by late July, demand stays soft, and supply runs strong; Brent eases toward seventy dollars. Energy disinflation lets the trend gauges resume their drift lower and pulls displaced workers back in. The Fed gains room for one late-year cut. | Step up productivity-led capex. Open the refinancing window. Lean into an energy-sensitive demand recovery. |

| Adverse25% | The draft collapses or a fresh incident keeps the strait shut into the autumn; Brent averages above $110, and a closure dragging through 2027 points toward $140. Headline CPI re-accelerates and the better gauges follow, validating the hike bet. The Warsh Fed weighs a hike into a falling market; narrow equity leadership unwinds. | Stress-test floating-rate exposure and covenant headroom. Build liquidity. Defer non-essential capex. Hedge energy and freight. |

Forecast Update

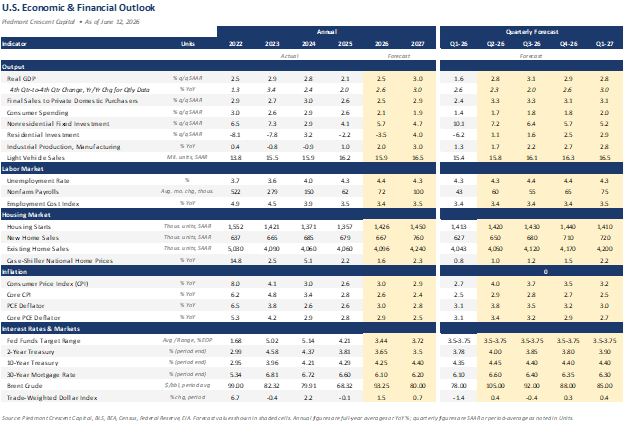

Our full US economic and financial outlook is below, updated for this week’s data and the revised policy path. The headline change remains the rate trajectory: with the labor market firmer, the capital cycle broadening, and core inflation sticky, we carry no 2026 cut in the base case and see the next move as a hike, a call the broader consensus has now moved toward. We mark the oil track to a late-summer reopening, with Brent near ninety dollars into year-end and a security premium beneath it, a benign path toward seventy dollars on faster normalization, and an adverse path above one hundred ten dollars if the strait stays shut. We hold the line where we differ from consensus, looking for the ten-year to stay near four and a half percent rather than drift lower. Cross-checks worth noting: US growth near 2.5 percent, a broad-equity path consistent with an S&P 500 near 8,000 on earnings, and gold marked sharply higher on the same security bid. Forecast values are shown in the shaded cells.

This commentary reflects the views of the author as of the date noted and is provided for informational purposes only. It does not constitute investment advice or a recommendation to buy or sell any security. Information has been obtained from sources believed to be reliable, but accuracy and completeness are not guaranteed. Past performance is not indicative of future results. © 2026 Piedmont Crescent Capital.

Piedmont Crescent Capital | A View from the Piedmont