Highlights of the Week

- July CPI was relatively benign, raising hopes that tariffs would not bite as hard as feared and spurred talk of a half-point cut in September.

- More recent data told a different story: headline PPI surged 0.9%, core PPI rose 0.4%, and import prices climbed 0.4%, all pointing to stubborn inflation pressures and putting the kibosh on a half-point cut.

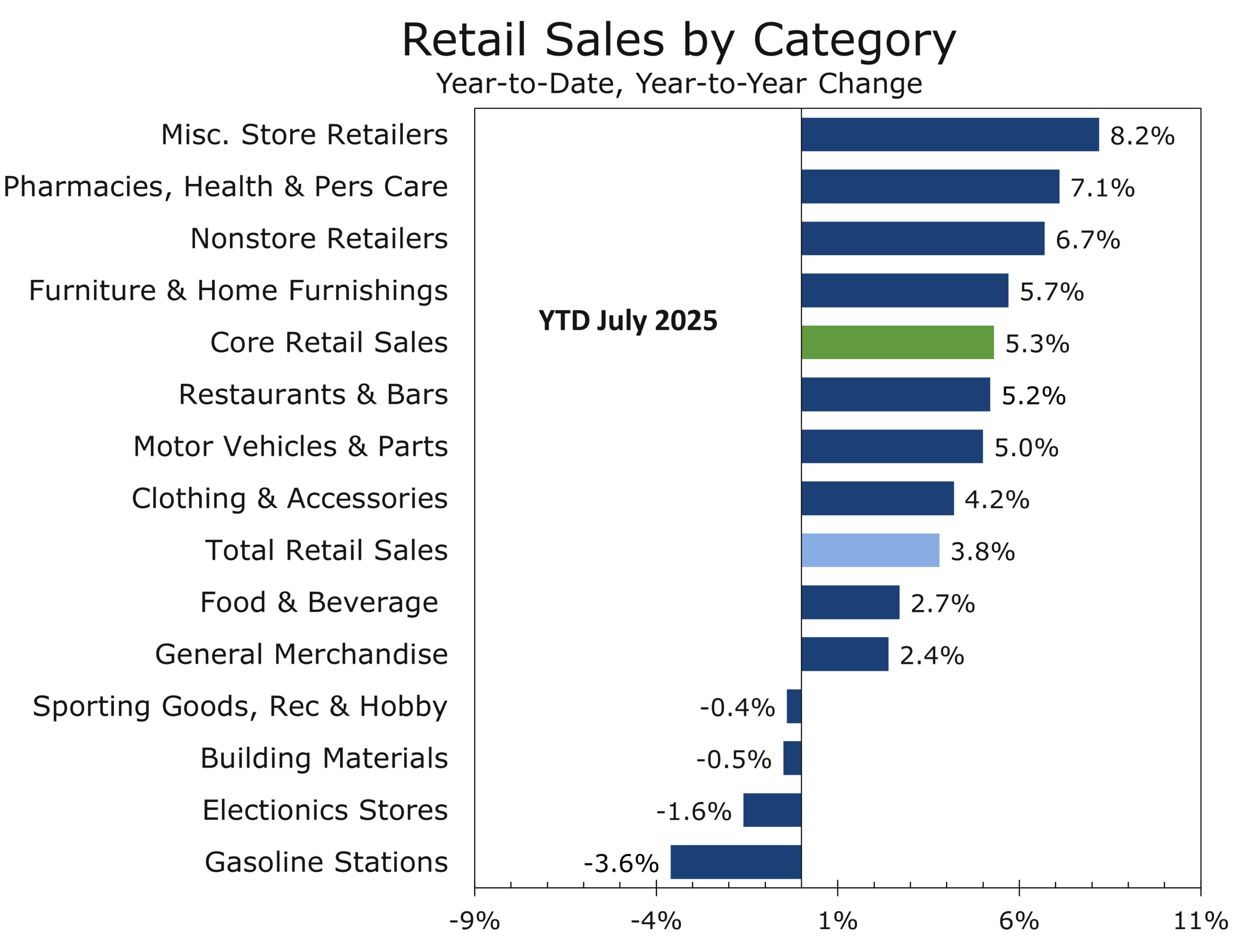

- Retail sales strengthened in July, with control group sales up 0.5% and previous data were revised higher, lifting Q3 GDP baseline estimates.

- Consumer sentiment dipped in August, ending a four-month streak of improvement, underscoring fragile household finance.

- Trump’s Aug. 15 Anchorage summit with Putin signaled a precarious shift in U.S. posture toward Ukraine; Zelensky meets Trump August 18, in Washington with many European leaders traveling along for support.

- Equities hit record highs while Treasurys diverged, with a steepening curve on firmer PPI/import price data; markets still price around 80% odds of a September Fed cut.

- Markets remain calm and complacent via the swings in sentiment on growth and inflation ahead of Powell’s Jackson Hole keynote on Aug. 22, but risks are mounting.

Dog Days, Lingering Pressures

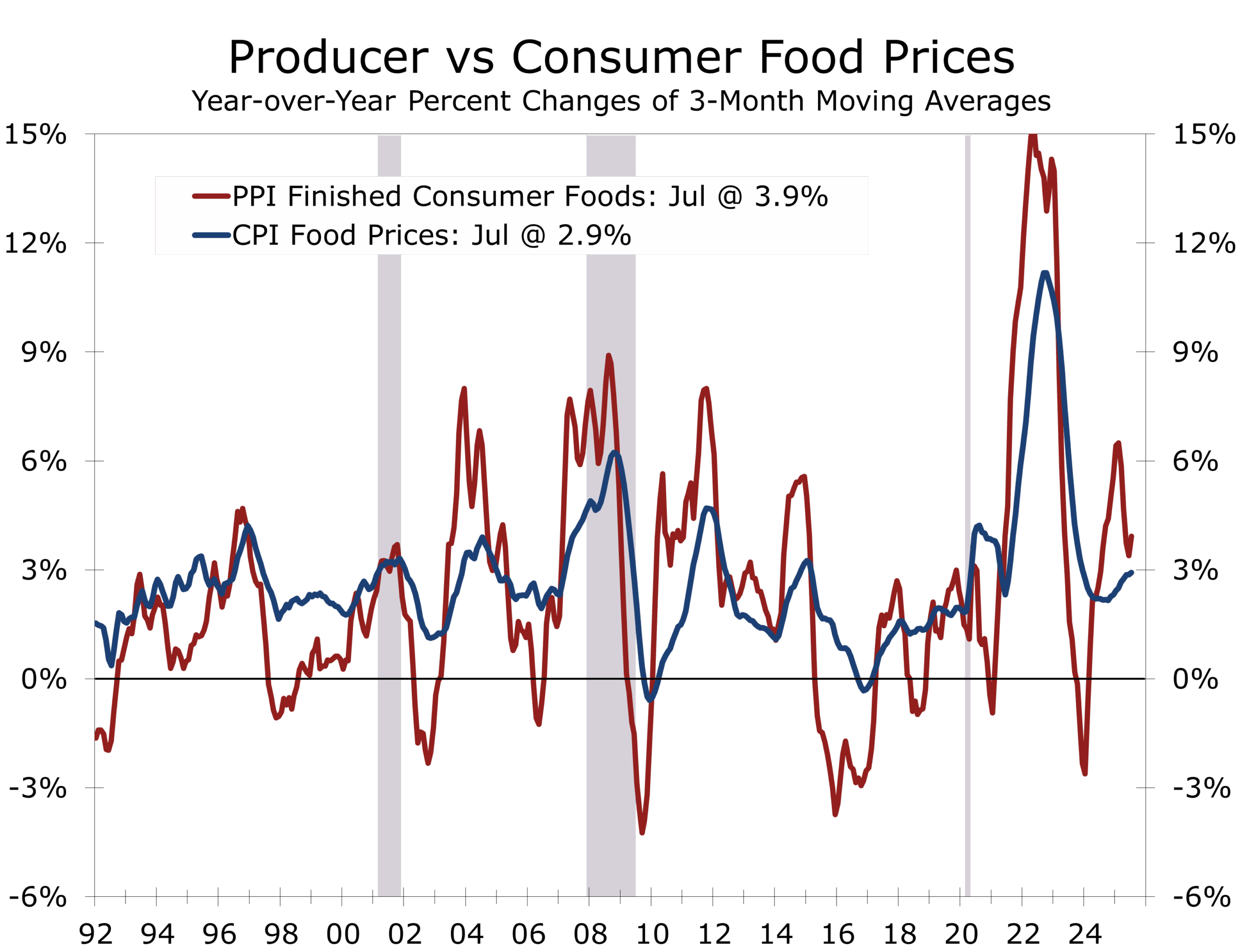

The dog days of summer have brought record equity highs and a veneer of calm. July’s CPI—headline inflation steady at 2.7% y/y with shelter easing—further fueling hopes that tariffs would not bite as hard as feared. But those hopes proved short-lived.

The headline PPI surged 0.9% in July, the largest monthly increase since early 2022. Core PPI rose 0.4%, double expectations, signaling stronger pipeline pressures. Import prices also came in firmer, climbing 0.4% versus 0.1% expected, with industrial supplies and consumer goods leading gains. Take together, the data suggest core PCE rose 0.3% in July, or 2.9% year-to-year—less benign than CPI alone implied. Some of July’s spikes likely reflect catchup in purchases of industrial supplies and materials stockpiled ahead of tariffs. The replenishing of those stocks boosted demand and helped pull prices higher.

Tariffs did not deliver an immediate inflation shock but are now seeping into supply chains.

Tariffs did not deliver an immediate inflation shock, but their effects are seeping into supply chains. And with ground beef prices rising ahead of Labor Day, households feel inflation’s persistence more acutely than headline figures suggest. The persistence of inflation, particularly for everyday items, is emerging as the key issue for this year’s off-year elections, which are typically seen as a harbinger for the mid-terms.

Consumers: Still Resilient, But Uneasy

Retail sales rose 0.5% in July, which is a shoulder month for most retailers and makes up a relatively small proportion of their overall sales. Control group sales, or what we often call core retail sales, also rose 0.5%, and prior months’ data were revised higher. Autos (+1.6%) and online retailers (+0.8%) led gains, supported by extended Prime Day promotions and competitive discounts. Furniture, clothing, and sporting goods also posted solid advances, while housing-linked segments most closely tied to housing appreciation, including building materials, hardware, and home improvement centers (-1.0%) and restaurants (-0.4%) lagged. Real core sales point to slightly stronger Q3 personal consumption, once again emphasizing one of our most often refrains about the U.S. economy, which is to never underestimate the capabilities of the U.S. consumer.

Confidence is historically weak, however, and is wavering. The University of Michigan’s preliminary August sentiment index slipped to 58.6 from 61.7, ending a four-month streak of improvement. One-year inflation expectations rose to 4.9% and long-run expectations to 3.9%, reversing recent progress. While the link between sentiment and spending has weakened since the pandemic, the deterioration reflects growing household unease over inflation, tariffs, and labor market conditions. The contrast between solid spending and softening sentiment underscores the precarious balance sustaining growth.

Crosscurrents Beneath the Surface

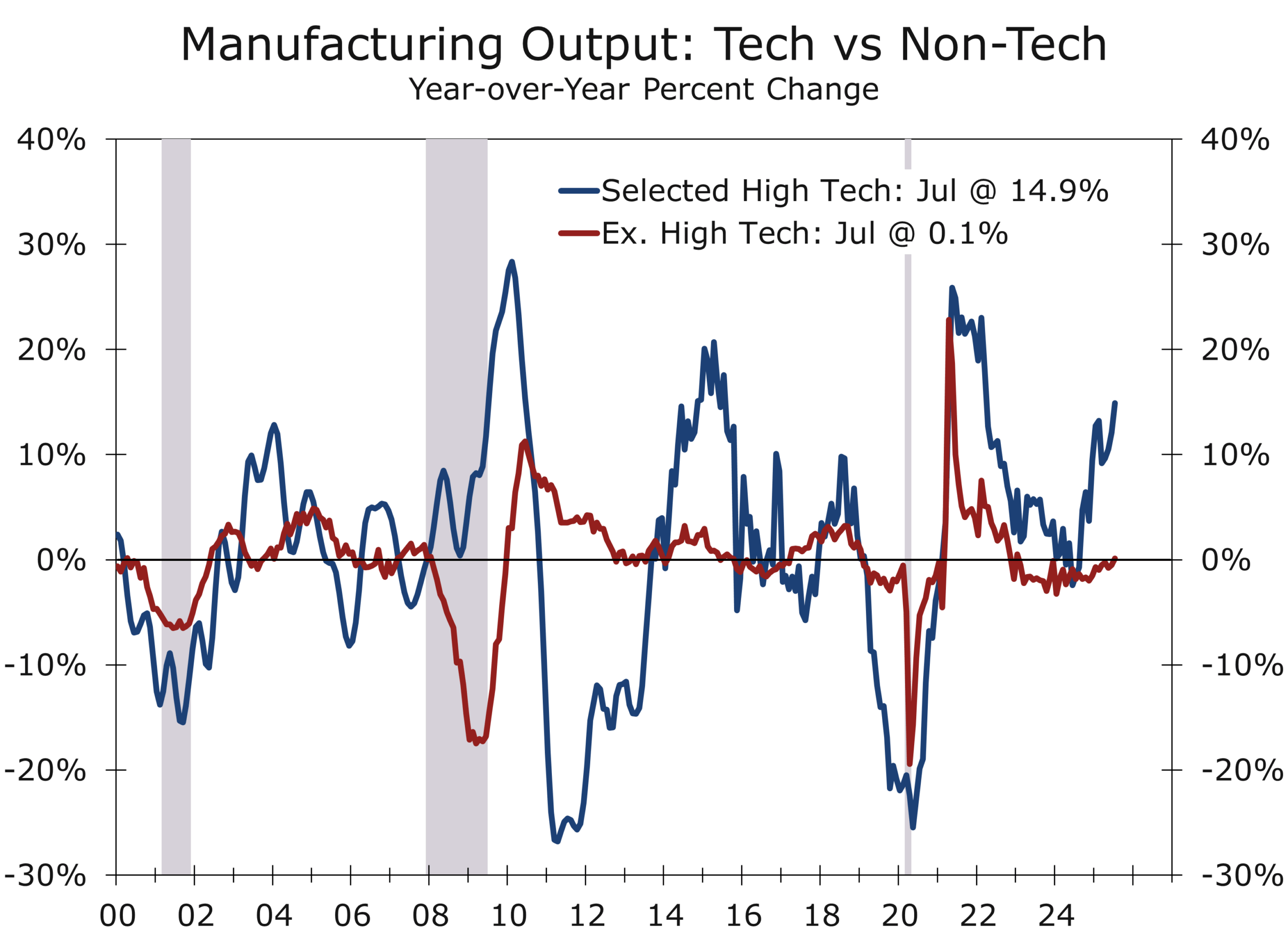

Industrial production slipped 0.1% in July, its first decline in four months, as weakness in utilities (-0.2%) and mining (-0.4%) offset resilience elsewhere. Manufacturing output was flat overall, though auto production fell 0.4%, reflecting tariff-related pressures and affordability headwinds.

Production of high-tech equipment is up 14% y/y; aerospace is surging as Boeing ramps up.

Not all the details were negative. High-tech equipment output rose 1.4% in July and is up 14% year-over-year, fueled by AI and semiconductor investment as new plants ramp production. Overall business equipment saw output rise 0.5% in July and production has grown at an 11% annualized pace over the past six months. Aerospace also stands out: Boeing is boosting 737 Max output and raising 787 assemblies, steadily working to keep pace with its historic backlog.

Elsewhere, output of consumer goods edged higher (+0.1%), with gains in tariff-sensitive categories such as furniture and wood products, which are benefiting from some reshoring of upholstered furniture. These improvements may prove fleeting, however, given sluggish new and existing home sales and weakening homebuilding. Steel and aluminum production held steady, supported by industrial demand, though higher input costs remain a constraint.

Markets: Calm at the Highs

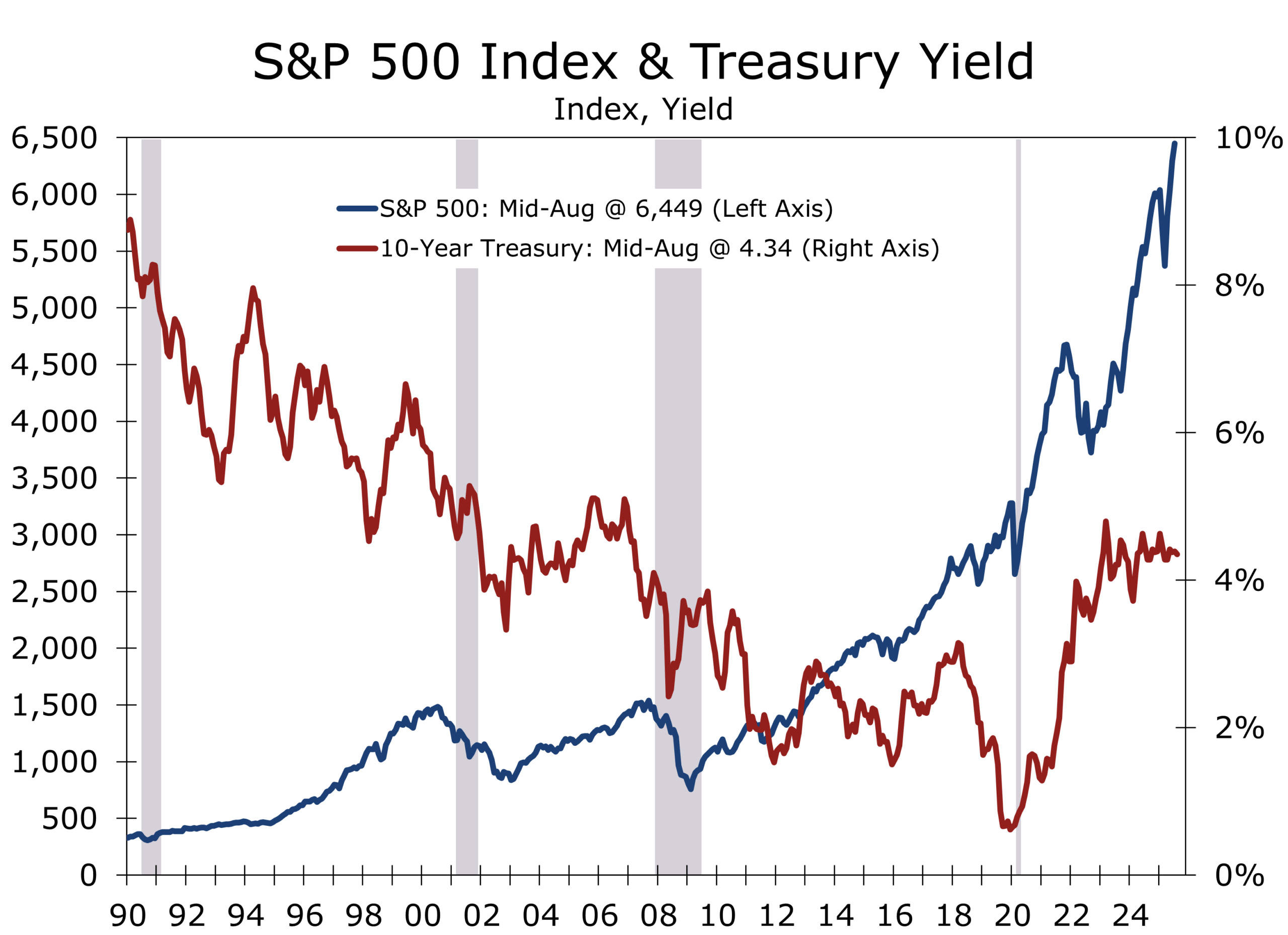

Despite firmer inflation, equities pushed higher this past week, with the Dow at record highs and the S&P 500 close behind. Treasurys told a different story: the yield curve steepened as the long-end backed up on the hotter PPI and import price data. The front end held relatively steady, with traders still assigning around an 80% probability to a September cut. Talk of a half point cut has vanished.

Financial market valuations reflect precarious complacency heading into fall.

This disconnect—stocks at record highs, real yields rising, inflation proving stubborn—captures the precarious complacency of late summer. Investors have shed some of their long-held skepticism about tariffs and appear to view labor risks as temporary. It is still early innings on both fronts, however, and upcoming releases on employment and inflation will carry a great deal of weight this fall.

Geopolitics: Anchorage and Beyond

On August 15, Trump met Putin in Anchorage. The summit ended without a deal but marked a clear shift in U.S. posture toward Ukraine. Trump dropped his demand for an immediate cease-fire, opening the door to a broader settlement more favorable to Moscow—recognition of Crimea, neutrality, and frozen front lines in Donbas and the south. Stalled on the battlefield, Putin is seeking to secure diplomatically what he could not by force. Anchorage was not Reykjavik; it looked far more like Munich 1938.

Now the spotlight shifts to Washington, where Zelensky met with Trump on August 18, joined by leaders from the U.K., France, Germany, Italy, Finland, and the EU, along with NATO Secretary-General Mark Rutte. Their task: preserve Western unity, keep Trump focused on Putin as the aggressor, and prevent a rift that could fracture Ukraine’s support. Early reports showed Trump and European leaders were closely aligned.

The divide is stark. Security guarantees—once a flashpoint between Trump and Zelensky—are now under discussion, potentially modeled on NATO’s Article 5 but issued bilaterally by the U.S. and European states. Yet the territorial issue remains a chasm. Putin’s terms for Ukraine to cede Donetsk in exchange for a frozen conflict elsewhere are a constitutional nonstarter for Kyiv and overwhelmingly opposed by the Ukrainian public. Analysts warn that conceding hardened defenses would most certainly invite future Russian offensives.

The Stakes in Anchorage Echo Munich, Not Reykjavik. Let’s Hope the Outcome is Different.

At a minimum, Trump would do well to demand the withdrawal of Russian forces from Transnistria in Moldova as part of any settlement, removing a threat to Ukraine’s southwestern flank. Otherwise, the outcome risks echoing the 1938 Munich Agreement, when Hitler was granted the German-speaking Sudetenland of Czechoslovakia under the promise of peace. Within months, he struck a separate deal with Slovakia, encircled what remained of Czechoslovakia, and effortlessly swallowed the rest. Conceding Donetsk without removing Russia’s forward positions in Moldova could set up a similarly perilous dynamic, inviting Moscow to return later and complete the conquest from a position of even greater advantage.

Trump’s rhetoric has added pressure, suggesting Zelensky “can end the war almost immediately if he wants to.” Meanwhile, Russian drone strikes—including one in Kharkiv this morning that killed four civilians—underscore Moscow’s unwillingness to halt the war. Markets may briefly rally on cease-fire talk, but appeasement would deepen long-term risks, embolden adversaries from Beijing to Tehran, and raise doubts about Western resolve. For Trump, the political stakes are equally high. Biden’s presidency never recovered from Afghanistan; a perceived capitulation in Ukraine could be more damaging still, with potential to reopen the GOP field for 2028, which had recently consolidated around J.D. Vance.

The consequences extend far beyond Europe. If Washington is seen conceding territory under pressure, the message to other adversaries will be unmistakable. Xi Jinping could interpret it as a green light to test U.S. resolve in the South China Sea or accelerate plans for Taiwan. Tehran and Pyongyang would likewise conclude that coercion pays. Trade and tariff deals would also likely prove even harder to reach, particularly with India and China, as Trump would be viewed as a far less strong leader than he has proven so far.

Russia is betting heavily that U.S. security guarantees will prove as hollow as those given to Ukraine in 1994, when Kyiv surrendered its nuclear arsenal. Moscow is also amplifying far-right narratives in the U.S. against “forever wars,” aiming to erode bipartisan consensus on supporting Ukraine. These fringe movements have a small but committed following that are likely unwittingly being supported by Russian intelligence.

Markets will oscillate between optimism over the possibility of a cease-fire and anxiety that appeasement only defers larger conflicts. Energy prices may ease on signs of progress, while defense stocks could see near-term pressure but retain longer-term support. The euro remains vulnerable if Europe is perceived as conceding leverage to Moscow, while the dollar continues to benefit from safe-haven flows. Treasurys, as ever, will mirror risk appetite—steepening on real progress, flattening if talks collapse.

Bottom line: Putin is using negotiation and flattery to extract what his army could not achieve by force. Financial markets, which are forward-looking, would quickly see through a bad deal—shrugging off near-term relief about the absence of secondary sanctions on India and China and instead pricing in greater instability for the U.S. and Western democracies in the years ahead, amidst what would be a diminished and politically weakened U.S. presidency. We expect Trump to work out a good deal that ends the war and provides durable security guarantees that fall just short of immediate NATO membership for Ukraine.

High-Stakes, High Altitude: Jackson Hole 2025

This week, global policymakers converge at the Jackson Lake Lodge in Wyoming for the Kansas City Fed’s annual Jackson Hole Symposium, August 21–23, under the theme “Labor Markets in Transition.” With only about 120 attendees, the event is one of the most exclusive global economic forums. For Chair Powell—likely his last appearance before his term ends next May—the stakes are high: the Fed is deeply divided between those urging preemptive cuts and those worried about additional inflationary pressures from tariffs. Easing when inflation is rising requires a great deal of clarity in the Fed’s messaging.

Markets enter the week focused squarely on Powell’s Friday remarks. Futures currently price around an 80% probability of a quarter-point September cut, but weak July payrolls and large downward revisions to the two prior months’ data have sharpened attention on the Fed’s employment mandate. Based on our analysis of the Quarterly Census of Employment and Wages series, the state employment data and data from private sources, we estimate nonfarm payroll growth is currently running at just 60,000–80,000 jobs per month. That may be enough to hold the unemployment rate steady, given reduced immigration flows—or at least limit how much it rises.

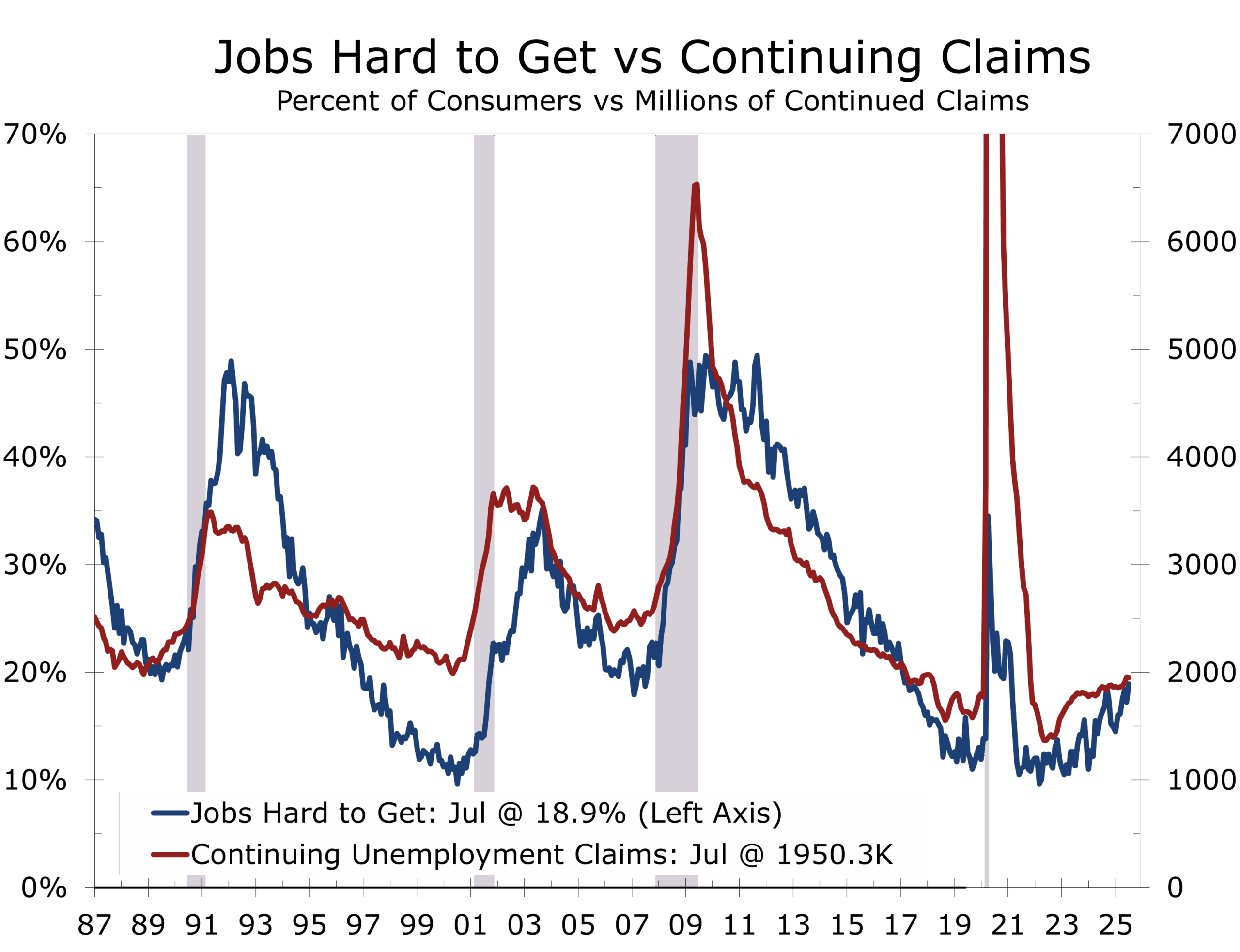

At the same time, a rising number of consumers report that jobs are harder to get, coinciding with broader weakness in sentiment. Consumers are equally worried about higher prices, particularly for necessities such as housing, groceries, and transportation—not only the cost of new and used vehicles, but also higher maintenance and insurance costs.

The optics also amplify the risk: Powell’s final Jackson Hole appearance comes as equities trade at stretched valuations near 24x forward earnings. Markets have climbed the wall of worry largely on expectations of Fed easing and resilient corporate earnings. That leaves them highly sensitive to Powell’s message. A hawkish guardrail could unsettle risk assets, while dovish reassurance may extend the rally in equities, Treasuries, and a weakening dollar. Either way, Powell’s tone will set the trajectory heading into this fall.

Looking Ahead: Light on Data, Heavy on Stakes

It is a relatively light week for economic reports, but a heavy one for monetary policy and geopolitics:

Tuesday, August 19 – Housing Starts & Permits Expected to slip below 1.3M. New home inventories remain elevated (511,000 in June, +8.5% y/y), with completed homes up 21%. Rising supply is weighing on builder sentiment and slowing new construction.

Wednesday, August 20 — FOMC Minutes

Will offer details on the July debate, though they predate the unexpectedly weak jobs report and firmer July inflation data.

Leading Economic Index (July)

The consensus is looking for a 0.1 point drop.

Thursday-Saturday August 21-23 — Jackson Hole Symposium – Powell’s keynote (Aug 22) is the highlight. Markets expect a dovish tilt, but stubborn inflation may force a more cautious tone.

Friday, August 22 — Existing Home Sales

Forecast to rise slightly to 3.95M. Affordability remains tight. The rising supply of homes for sale is providing some support for sales, particularly at the upper end. With sales skewed toward higher priced homes, the median sales price has risen to all-time highs.

Final Thoughts: Calm with Fault Lines

This week may feel light on data, but it is heavy with risk. Powell’s Jackson Hole remarks and Zelensky’s White House visit are set to define the narrative far more than the economic data. Beneath the calm of record equity highs lie clear warning signs: producer prices are accelerating, consumer sentiment is slipping, the LEI is flashing red, and geopolitics and public policy remain on edge.

The dog days may feel slow and tranquil, but as Powell speaks at Jackson Hole and Zelensky negotiates in Washington, complacency could quickly give way to volatility this fall.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

August 18, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000