Prices Are Likely Bolstering Core Retail Sales

-

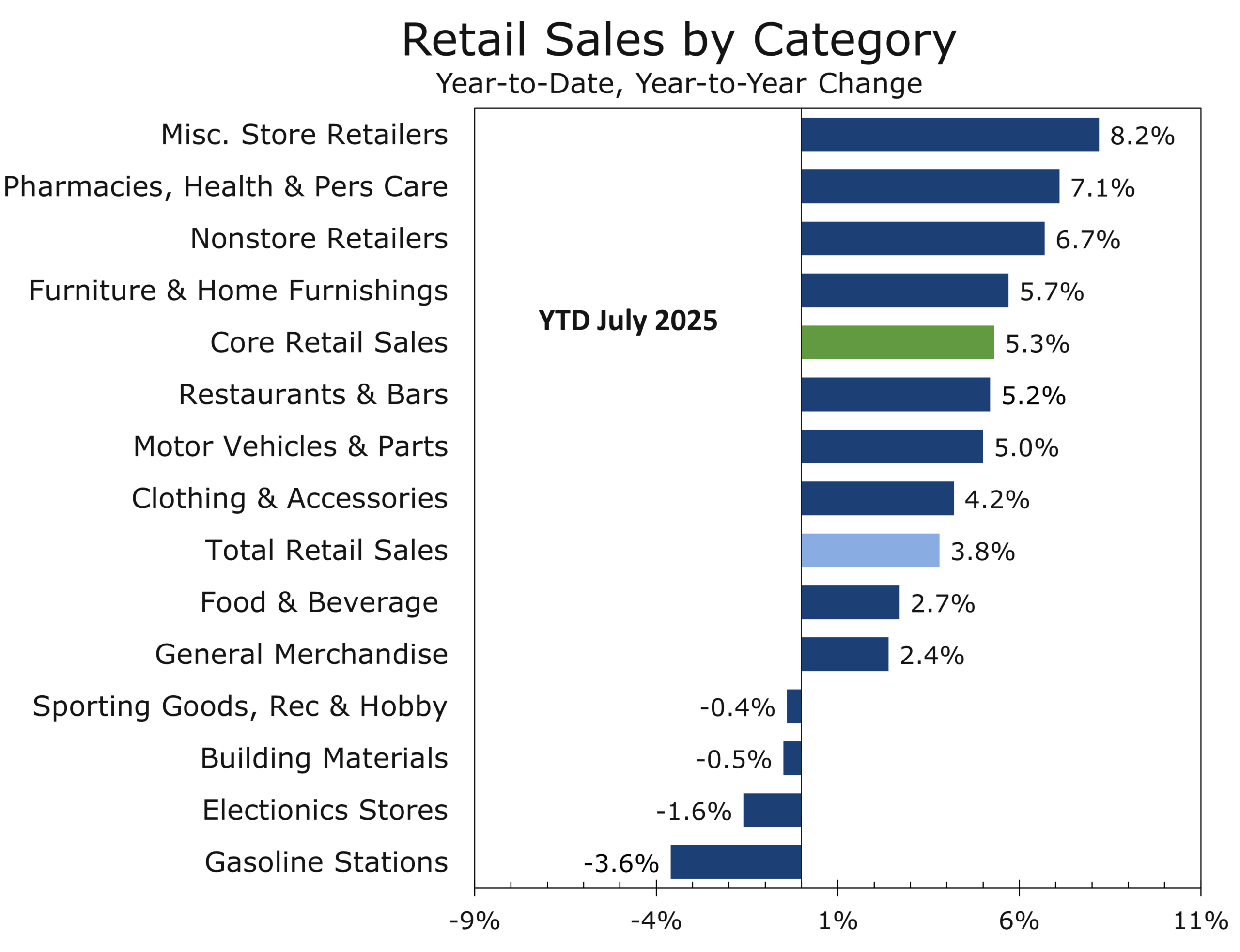

- Headline retail & food services sales rose 0.5% m/m in July and 3.9% y/y; June was revised up to +0.9% m/m.

- Control group (ex‑autos, gas, building materials, and food services) rose 0.5%; June’s was revised up about 0.4 ppts, implying the consumer spending has stronger underlying momentum.

- Gains were driven by stronger auto sales and solid gains in clothing, sporting goods, and general merchandise stores. Spending was down at home improvement stores and restaurants, however, reflecting continuing weakness in housing and a further pullback in spending for discretionary services.

- Prime Day–style promotions and extended online sales boosted nonstore activity, potentially beyond seasonal adjustments.

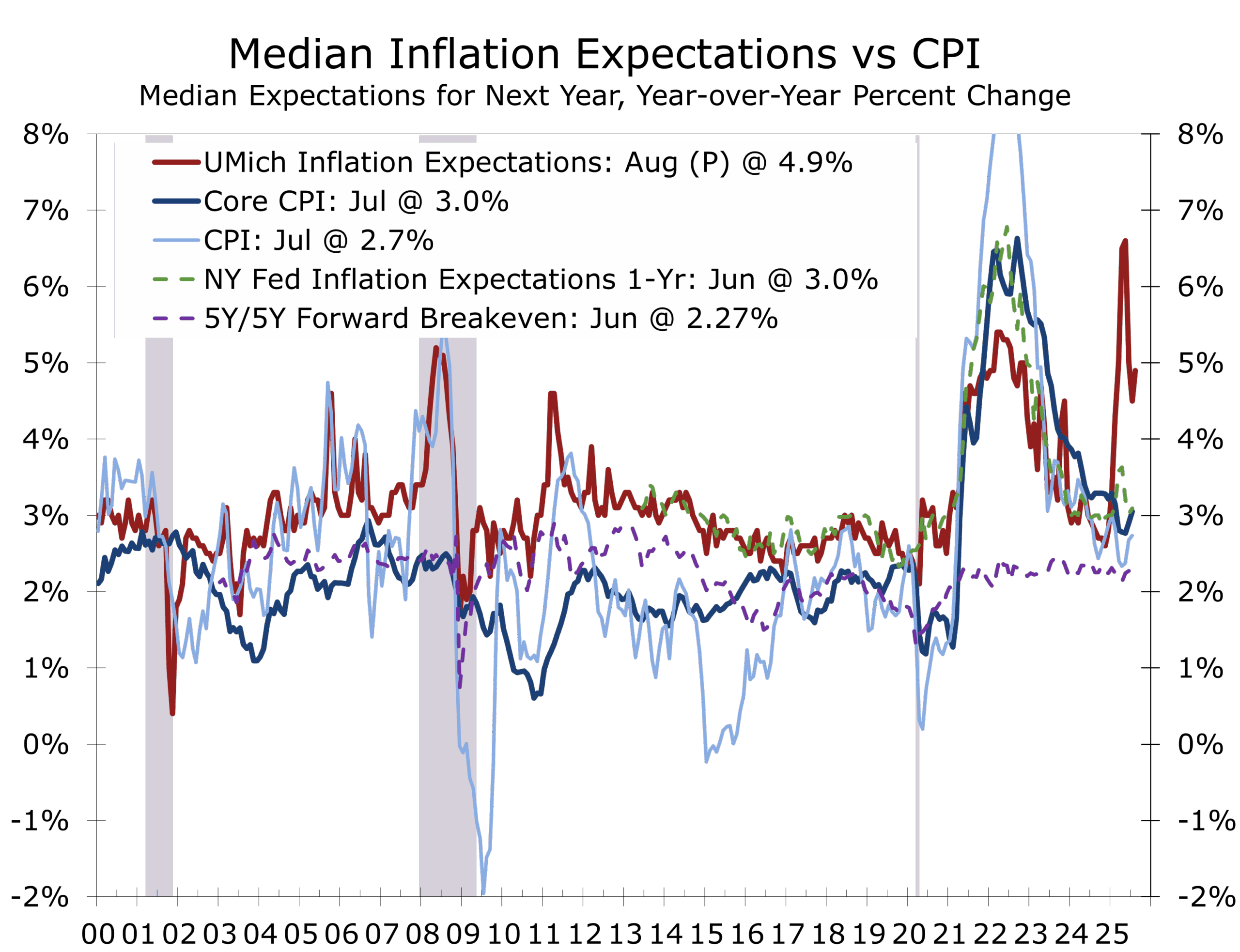

- University of Michigan sentiment fell to 58.6, with 1-year inflation expectations up to 4.9% and long-run to 3.9%.

- Inflation fears continue to outpace the data. July’s hotter than expected PPI report and today’s slightly faster rise in import prices likely reflect some catch-up with tariffs.

July Retail Sales—What Stood Out

U.S. consumer prices increased moderately in July. The July retail sales report shows more resiliency. Headline sales rose 0.5% m/m and are up 3.9% y/y, and the prior month’s gain was revised higher to a 0.9% gain. Those revisions nudge the level of activity up heading into the third quarter and should cause forecasters to slightly increase their estimate for Q3 growth.

Under the hood, vehicles sales rebounded 1.6% m/m and nonstore (e‑commerce) climbed 0.8%, consistent with extended summer discount events. Part of the strength in vehicle sales is likely higher prices, with prices of maintenance and repairs climbing rapidly the past few months. Sales also rose solidly at furniture (+1.4%), clothing (+0.7), sporting goods (0/8%), and department stores (0.9%). Nonstore retailers, which includes online retailers, rose 0.8%.

Housing Weakness, Higher Prices Squeeze Services

Sales at home improvement and hardware stores fell 1.0%—reflecting the recent swing of weak home sales, as well as some softening in home prices. Restaurant sales dipped 0.4%, which is consistent with our thesis that with consumers spending more for higher priced imported goods, they will have less to spend on discretionary services, including dining out. The weaker numbers are consistent with recent earnings reports from restaurant chains.

From a GDP-relevant perspective, control group sales rose an estimated 0.5% in July, and June’s level was revised up by 0.4 ppts. The stronger data indicate consumer spending had more momentum heading into Q3, making it easier for consumption to contribute meaningfully to real GDP growth. We have been looking for real consumption to rise at a 2.4% pace in Q3 and the upward revisions will help reach that mark. Higher prices, however, are padding core retail sales.

Consumer sentiment slipped in August as inflation and job worries grew.

Sentiment Apparently Softens on Inflation Fears

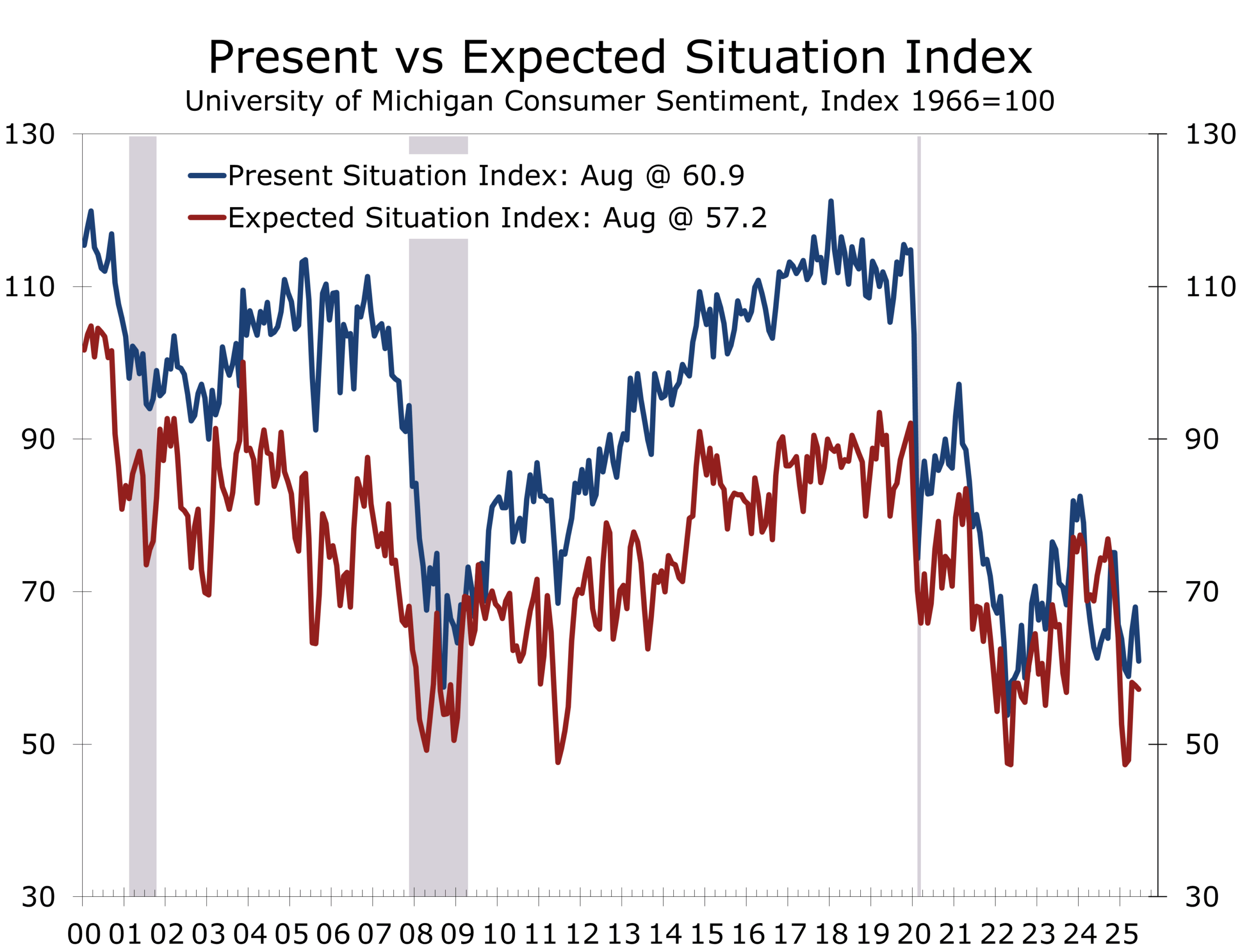

The preliminary University of Michigan Consumer Sentiment Index slipped to 58.6 in August from 61.7, ending a string of four consecutive modest improvements. Consumers appear to be increasingly concerned about inflation and a softening labor market. One-year inflation expectations rose to 4.9% and long-run expectations to 3.9%, reversing recent improvements. Both measures are well above market-implied levels and the inflation expectations reported in the Federal Reserve Bank of New York’s survey.

While the link between sentiment and spending has weakened since the pandemic, elevated inflation expectations and growing anxiety about the labor market can weigh on big-ticket purchases and are likely to constrain consumer spending in the coming months. The latest drop was largely concentrated in consumers’ assessment of the present situation,which fell 7.9 points to 60.9. The expectations series, which is much more closely correlated with spending, fell just 0.5 points to a still low 57.2.

We continue to expect below-trend but positive real consumption growth in Q3, supported by autos and value-oriented online promotions, with housing-related categories lagging. Spending on discretionary goods and services will likely slow or even decline modestly, which should help contain overall inflation, as services account for the bulk of consumer expenditures and the CPI and PCE price measures.

Policy & Market Implications

The retail data do not materially change the growth narrative: consumption is slowing but showing more resilience. The softer sentiment and higher inflation expectations argue for caution, but with labor data softening and core PCE still drifting lower on trend, the bar for a near‑term policy pivot remains a function of employment prints, which are weakening, as much as inflation. We see risk management dominating the Fed’s tone over the next few weeks as officials weigh still‑moderate demand against sticky goods prices and expectations.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

August 15, 2025

Mark Vitner, Chief Economist

(704) 458-4000