FOMC REACTION · JUNE 17, 2026

A Hawkish Hold, a Quieter Fed

Warsh holds at 3.50%–3.75%, the dots split nine-to-nine, and the new Chair orders a top-to-bottom review of the institution.

Download the PDFEarly Signals

- A hawkish hold. The Committee left the funds rate at 3.50%–3.75%, stripped the easing bias from the statement, and shortened the statement itself. No cut, as we have argued all year.

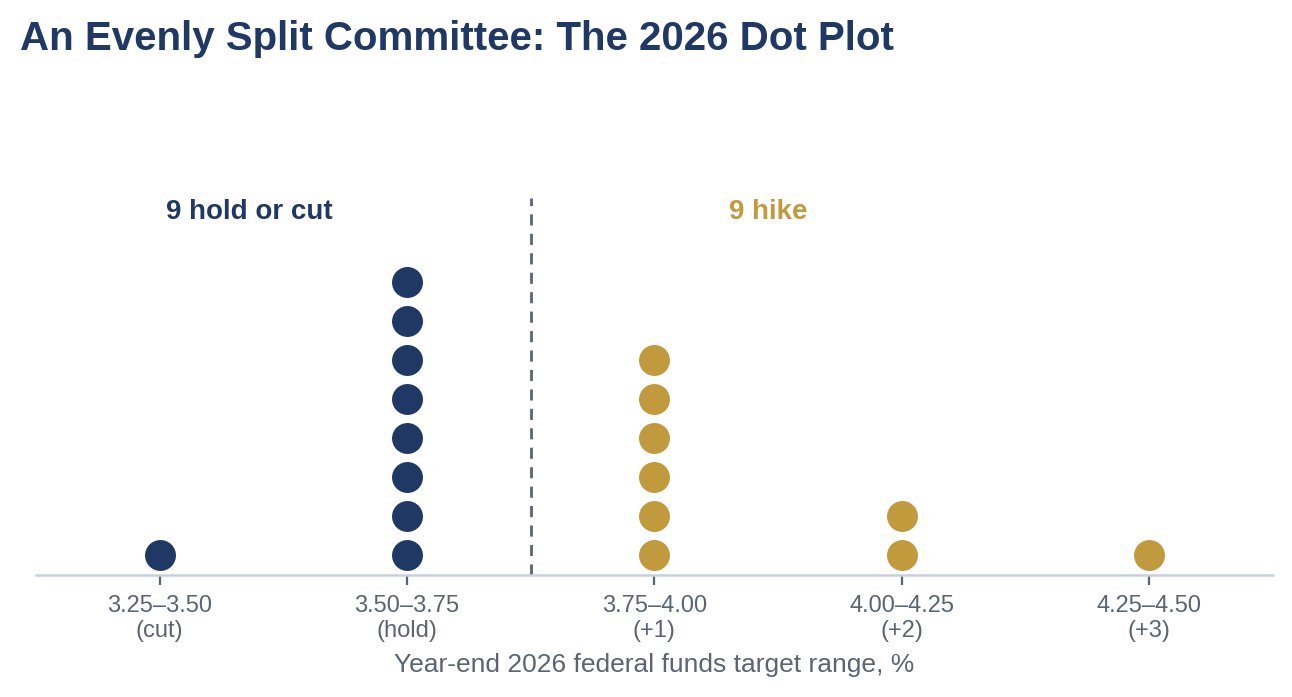

- The dots flipped. Nine of eighteen submitting participants now project at least one 2026 hike. Warsh’s decision not to submit a dot left a clean nine-to-nine split, and the 2027 core PCE median was marked up to 2.5%.

- A wider target, by design. Warsh said he focuses on the left of the decimal point, which we read as any reading that rounds to 2%, roughly 1.51% to 2.49%. That range has always made more sense to us than a hard 2% target, and it buys room to hold as long as inflation is drifting toward that pace.

- A Fed under review. Five new task forces and a wholesale re-examination of the post-2008 operating model signal patience now and a rethink of the framework for an AI-era economy.

Key Takeaways

| Key Concept | Findings |

|---|---|

| Decision | Held the federal funds target range at 3.50%–3.75%, removed the language pointing toward eventual cuts, and trimmed the statement to a leaner document. The hold surprised no one, but the message around it did. |

| The Dots | Nine of the eighteen participants who submitted projections now pencil at least one hike in 2026. Because Warsh chose not to submit a dot, the result is a clean nine-to-nine split between the hike camp and those projecting an unchanged or lower rate. |

| Projections | The 2027 Q4/Q4 core PCE median was lifted to 2.5%, a sign participants read the energy-driven firmness as having a longer tail. Markets repriced hawkish, roughly +20bp on the end-2026 path and +11bp on end-2027. |

| Warsh’s Band | The Chair said he watches the left of the decimal point. We read that as any reading that rounds to 2%, roughly 1.51% to 2.49%, which gives him more room to navigate. |

| Five Task Forces | Reviews of communications and the SEP, the balance sheet, the Fed’s data sources, productivity and jobs in “an era of transformation,” and the inflation framework. Functionally a patience mechanism that buys time. |

| Policy Signal | A hawkish hold rather than a hike. The next move is more likely up, but the energy de-escalation, the task-force timetable, and Warsh’s wider band push it into 2027. |

The Overview

Kevin Warsh’s first meeting in the chair delivered the outcome we expected on the policy rate and a genuine surprise nearly everywhere else. The Committee held at 3.50%–3.75%, removed the language that had pointed toward eventual cuts, and pared the post-meeting statement to a leaner document, a first concrete sign of the communications philosophy the new Chair brings with him. With the hold itself never in doubt, the meeting that mattered played out in the dots and at the podium.

Read in full, this was a hawkish hold. The Committee has not merely paused. It has removed easing from the near-term menu and put the question of a hike squarely back on the table, and the June dots have now caught up to a view we have held for some time, that the next move is more likely up than down. What is new is how many participants want to act this year rather than later, and, against that, how much latitude the new Chair has quietly given himself to wait.

The Dots Flipped Toward Hikes

The headline sits in the dots. Nine participants now project at least one rate hike in 2026, a far more hawkish tally than the Street expected, and because Warsh chose not to submit his own projection, the result is a clean nine-to-nine split between the hike camp and those projecting an unchanged or, in a single case, lower rate. Half of the committee that submitted dots is now signaling that the next move, if it comes this year, is up.

The economic projections carried the same message. The median 2027 core PCE forecast was lifted to 2.5%, a meaningful upward revision that says participants increasingly read the recent firmer inflation, driven in part by the energy cost shock from the Iran conflict, as having a longer tail than a one-off price-level bump. Markets took the cue, with pricing for the funds rate at the end of 2026 rising roughly 20 basis points and end-2027 pricing rising about 11 across the projections and the press conference.

Warsh and the Left of the Decimal Point

Warsh’s own stance was deliberately balanced. He allowed that policy is probably restraining housing while declining to say the same of financial conditions, and he leaned on the price-stability mandate in a way that would make him sympathetic to a hike if the next several inflation prints disappoint. He also flagged that market prices are among the most important signals a central banker has, which could mean he reads the market’s own move toward a higher path as corroborating evidence.

The most useful tell was his comment that on inflation he watches the left side of the decimal point. Some will read that as treating anything with a two in front of it as at target, but we believe he meant any reading that rounds to 2%. That makes intuitive sense, because under a hard 2% target a 0.2% rise in the CPI would count as above target and a 0.1% rise as below it, distinctions too fine to manage. The CPI has averaged 2.7% since 1990. We do not see this as a major change for the Fed, since Warsh reiterated several times that the FOMC remains committed to returning inflation to its 2% target.

Which Gauge? Reading Across the Measures

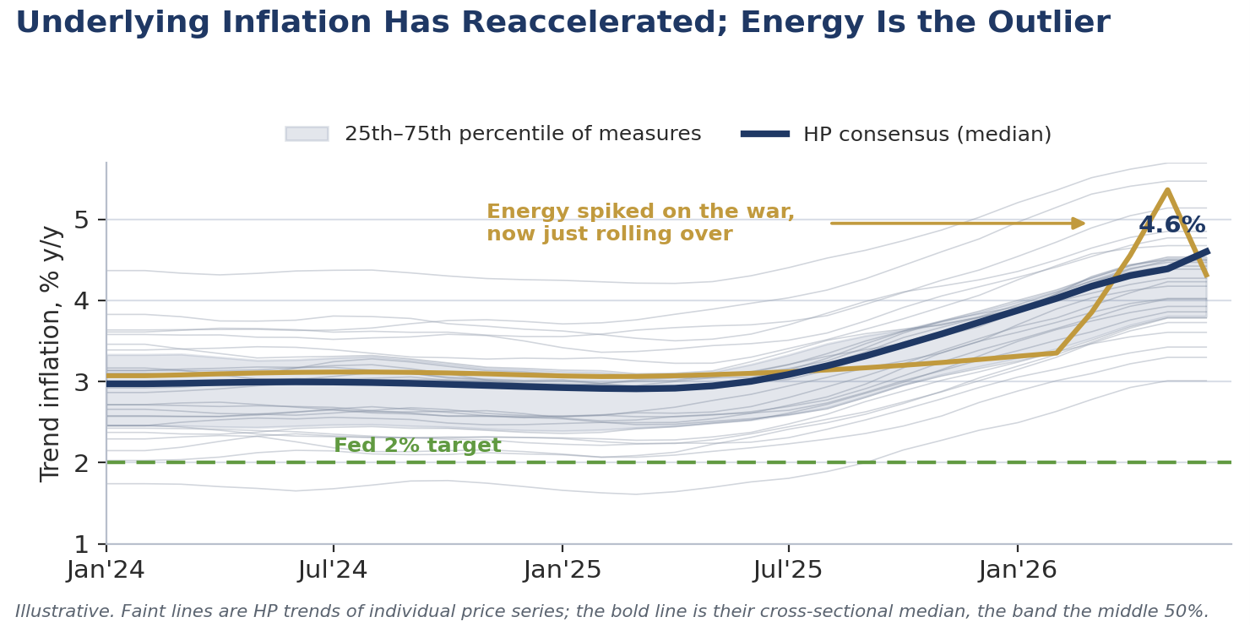

The choice of inflation gauge has quietly become its own debate. Warsh has pointed to Federal Reserve research showing that the trimmed-mean CPI tends to forecast where headline inflation is heading better than the traditional core, and he has argued that policymakers should weight it more heavily as a signal rather than leaning primarily on the core PCE deflator, the Fed’s current preferred measure. He is not proposing any change to how inflation is officially calculated. The point is about which gauge best anticipates the trend, which matters because policy acts with long and variable lags, so getting the forward read right is most of the job. The counterargument is about timing rather than principle. Trimmed-mean measures smooth by design and are slow to register abrupt moves, the twelve-month window still carries the distortions of last fall’s government shutdown, and with the PCE deflator having jumped from roughly 2.5% to 3.8%, some at the Fed, including the Dallas Fed’s Lorie Logan, have cautioned against putting too much weight on soft trimmed-mean readings just now. The cautionary tale of 2021 sits underneath it all, when a gauge favored because it confirmed a prior proved a credibility risk rather than a forecast.

Our own practice sidesteps the contest between any two gauges. Headline inflation is, and always will be, the Fed’s ultimate target, and the various core and trimmed measures matter only to the extent they forecast it. Rather than crown one, we examine the full range of price series and focus on where they agree and where they diverge, treating statistical outliers as more likely transitory than representative of the trend. To formalize that, we run a Hodrick-Prescott filter across dozens of individual price series, extract each one’s underlying trend, and take the cross-sectional consensus, a median resistant to outliers that we report alongside its dispersion and the outliers themselves. The current read is consistent. The consensus underlying pace has reaccelerated over the past three months across most measures, the breadth is real rather than the work of a few categories, and energy stands out as the principal outlier. That last point is also where the relief lies, since softer energy should help ease headline readings in the second half even as the underlying consensus stays firm.

Five Task Forces and the Time They Buy

Warsh announced five task forces, to be staffed with Fed economists and outsiders, including non-economists. They will reconsider Fed communications, with particular focus on the Summary of Economic Projections and the dot plot and a hint that press conferences may not follow all eight meetings; the balance sheet; the Fed’s use of and reliance on its existing data sources; productivity and jobs in “an era of transformation”; and the inflation framework itself.

The immediate market read should be that these reviews buy time. A Chair who has just commissioned a year of study on how the institution thinks, talks, and measures is not in a hurry to move in the interim, and the task forces function as a patience mechanism. Combined with the at-target-band framing and a cooling energy shock, they make a 2026 move unlikely in our base case.

The Bigger Story: A Reset of the Post-2008 Fed

Step back, and the task forces are not five separate housekeeping items but the scaffolding of a single project. Warsh is signaling a wholesale review of an operating model the Fed has run essentially unchanged since the 2008 crisis: the communications apparatus, the ample-reserves balance-sheet regime, the data it leans on, and the inflation framework. The question underneath all five is whether the old benchmarks still hold.

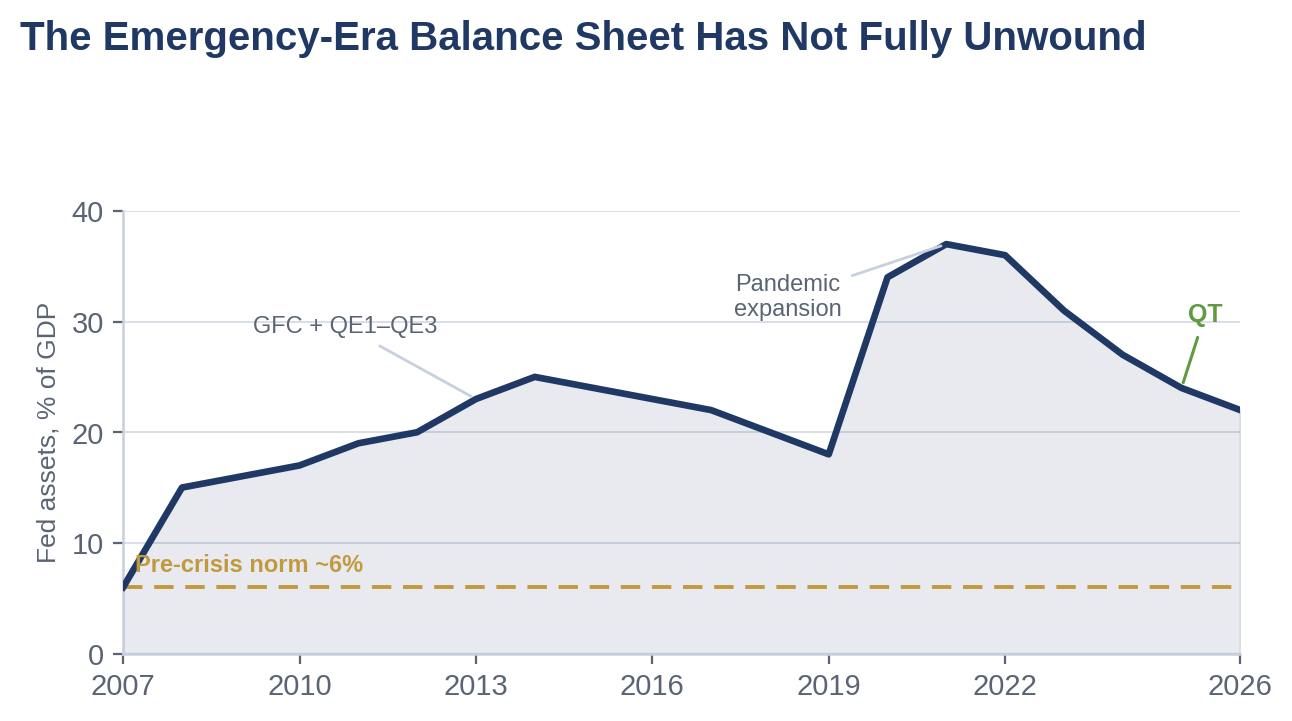

The starting point for that review is a judgment the new Chair has come close to making explicit, that the extraordinary policies assembled after the 2008 financial crisis, and again during the pandemic, are no longer appropriate for the economy we actually have. Zero rates, successive rounds of quantitative easing, and a balance sheet that swelled from roughly 6% of GDP before the crisis to nearly 37% at its pandemic peak were emergency responses to a world short of demand and stuck below the inflation target, conditions that no longer hold. Even after several years of runoff, the balance sheet remains far above its pre-crisis footprint, and the question Warsh is forcing is whether tools designed to fight deflation still belong in a cycle whose problem is the opposite.

That question lands with particular force in an AI-era economy. The “productivity and jobs in an era of transformation” task force is the explicit hook, and it dovetails with the framework we have used all year, a capital-led, investment-driven expansion that rhymes with the late-1990s capex cycle. If productivity is structurally faster, the neutral rate, the slope of the Phillips curve, and the speed limit on growth may all sit somewhere other than the post-crisis playbook assumes. A Fed that takes that seriously may keep policy higher for longer, not because it fears overheating but because the old framework no longer fits the economy it faces.

A Different Set of Challenges

If the old emergency tools no longer fit, neither do the old problems. The challenges that now dominate the economic conversation are not the deficient-demand, debt-deflation risks of 2009 but distributional ones. Income and wealth inequality have widened as asset holders compounded through a decade and more of cheap money and rising markets, while wage earners relied on paychecks that have only intermittently kept pace with prices. This is the two-speed, K-shaped economy we have described all year, with the top half insulated by asset values and capital income and the bottom half exposed to the day-to-day cost of living.

Housing affordability sits at the center of the strain. A long stretch of suppressed rates inflated home prices, and the post-pandemic surge pushed the median home well out of reach for first-time buyers even before mortgage rates normalized. The result is a widening divide between those who own and those locked out, with the rental market absorbing the overflow. Monetary policy built around the price of credit has limited reach here, because lower rates tend to capitalize into higher prices rather than better affordability, which is precisely why the problem resists the Fed’s blunt instruments.

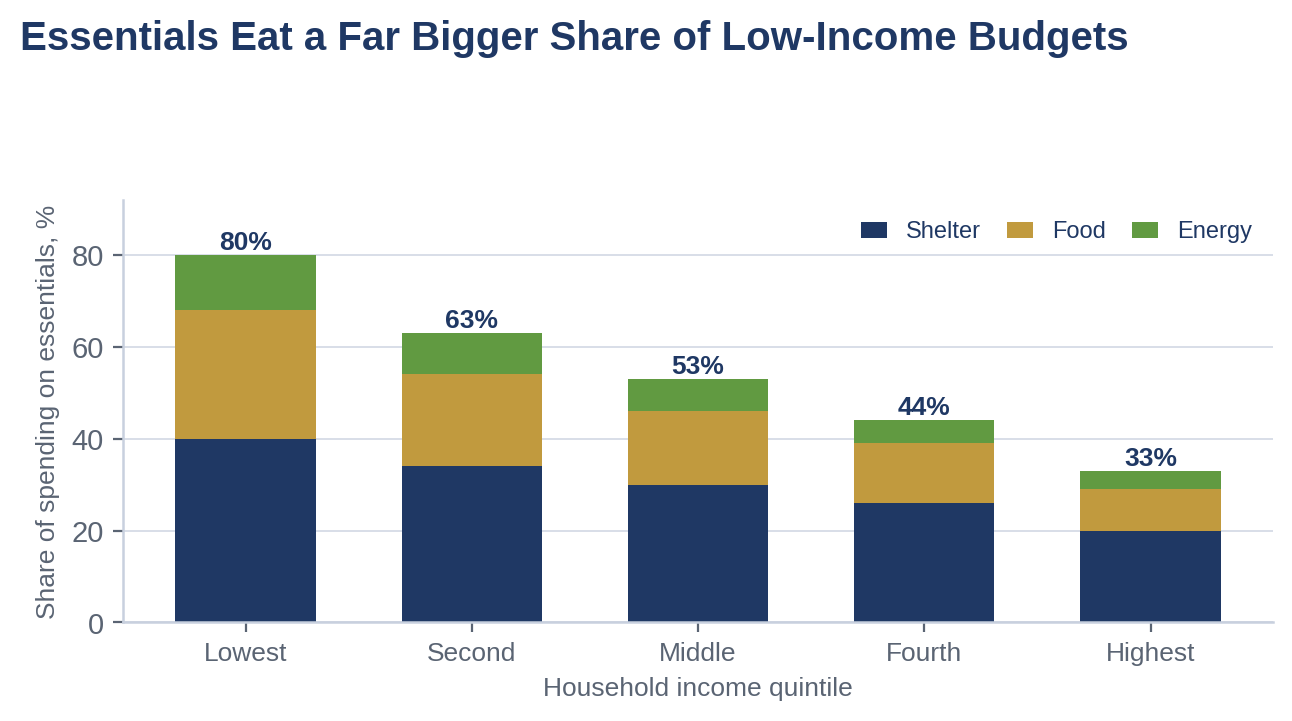

Inflation itself lands unevenly, and that is the part the headline average obscures. The categories running hottest, namely energy, food, and shelter, are the essentials, and they consume a far larger share of a low-income household’s budget than a high-income one. A burst of energy- and grocery-led inflation therefore works as a regressive tax, falling hardest on the families least able to substitute away from the commute or the checkout line. A central bank that targets an economy-wide average will, by construction, understate the burden carried at the bottom.

None of these problems, whether inequality, affordability, or the distributional bite of inflation, is one the Federal Reserve can solve with the funds rate, and Warsh has been careful not to claim otherwise. They are instead the backdrop against which the post-2008 framework now looks mismatched. A toolkit and a communications style built for a low-inflation, demand-short decade are being asked to govern an economy with the opposite ailments, and that mismatch, as much as any single inflation print, is what the five task forces are really being convened to confront.

Why We Still See No Move in 2026

Three things keep us at no hike this year despite the dots. First, the energy shock is de-escalating. News of a deal with Iran and the reopening of the Strait of Hormuz removes the most acute source of upside inflation risk, and if trade resumes, today’s hawkish projections could look stale within a quarter or two. Warsh underscored as much when he noted that his colleagues do not feel bound by their dots in a fast-changing world. Second, the voters lean less hawkish than the room. The dots reflect all nineteen participants, but only twelve vote, and we suspect a majority of those twelve still prefer to wait. Third, the Chair has given himself latitude through the left-of-the-decimal framing and the task-force timetable. The direction of travel is nonetheless clear, with the next move more likely a hike than a cut, even if we do not expect it before 2027.

Market Implications

A Fed on hold with a hawkish dot split, a Chair tolerant of a wider inflation band, and a quieter communications posture argues for front-end yields anchored higher for longer, a flatter curve as residual cut expectations are squeezed out, and a firmer dollar. The larger repricing risk sits in the Fed put itself, since a Warsh-led committee that telegraphs less, studies more, and re-benchmarks the whole framework sets a higher bar for the rescue that risk markets habitually assume, and we would be cautious about extrapolating the old reaction function into the new regime.

Our Call

OUR CALL

This was a hawkish hold rather than the start of a hiking cycle. The Committee removed the easing bias and half the dot submitters now see a 2026 hike, but the level held at 3.50%–3.75% and the new Chair built himself room to wait, so the next move points up while the timing looks like 2027 in our base case.

Warsh’s band is the quiet dovish offset to the hawkish dots. Watching the left of the decimal point means any reading that rounds to 2%, roughly 1.51% to 2.49%, counts as at target. That latitude, the five task forces, and a de-escalating energy shock together make a 2026 move unlikely even as the projections turn.

The real story is the reset. Five task forces amount to a top-to-bottom review of the post-2008 Fed, spanning communications, the balance sheet, the data, productivity, and the inflation framework, and they start from the premise that the emergency tools of the crisis and pandemic no longer fit the economy we have. The problems that dominate now are distributional, including inequality, housing affordability, and the regressive bite of inflation, none of which the funds rate can fix. This is the two-speed, capital-led expansion we have described all year, now meeting a central bank willing to question its own map. We retain our no-cut base case for 2026, with the tail skewed toward a hike, and we continue to favor caution on duration as the term premium rebuilds.

Mark P. Vitner

Chief Economist, Piedmont Crescent Capital

mark.vitner@piedmontcrescentcapital.com · (704) 458-4000

Disclaimer: This report is provided for informational purposes only and does not constitute investment, legal, tax, or accounting advice, nor an offer or solicitation to buy or sell any security. Information is drawn from sources believed to be reliable, including publicly reported FOMC materials and meeting coverage, but its accuracy and completeness are not guaranteed. Statement, projection, and market-pricing figures should be verified against source data before publication. Views expressed are those of the author as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

© 2026 Piedmont Crescent Capital · For informational purposes only.