An Energy Headline, a Paycheck Problem

Early Signals

- Energy did the damage. Headline CPI rose 0.5% in May, with energy contributing more than sixty percent of the increase. Gasoline jumped 7.0% on the month and is up 40.5% over the year.

- Core stayed contained. The 0.2% core gain kept the annual rate at 2.9%, and the trend stripped of shelter and energy is running near 2.4%.

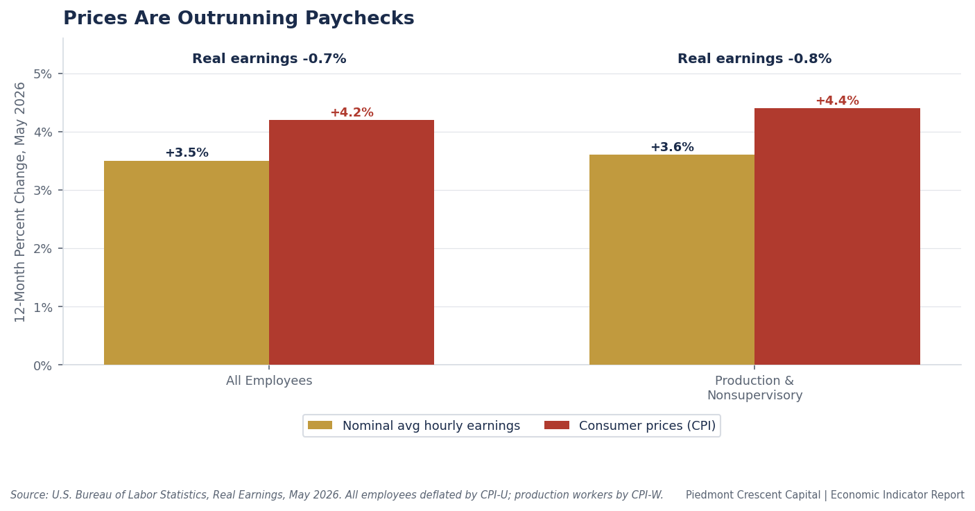

- Paychecks lost ground. Real average hourly earnings fell 0.1% in May and are down 0.7% over twelve months, with production workers off 0.8%.

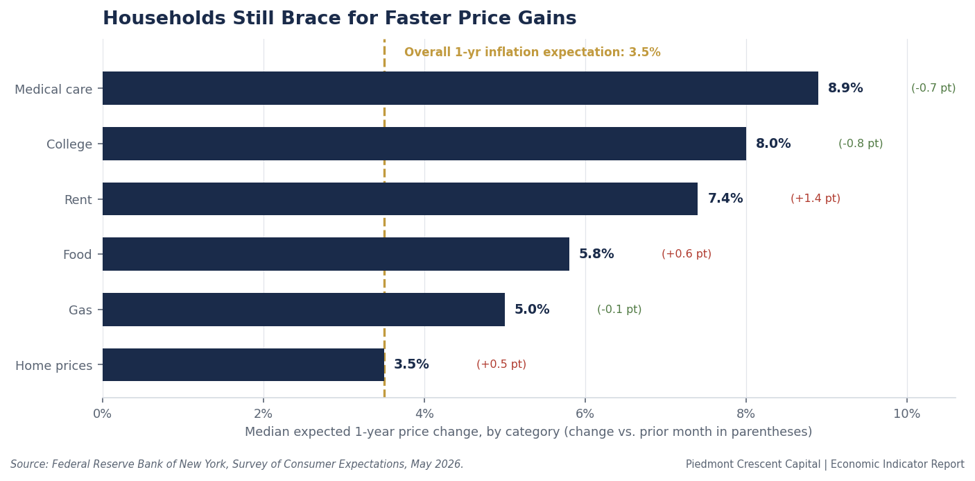

- Expectations held, but high. The New York Fed’s one-year inflation expectation eased to 3.5%, while household finances and labor confidence deteriorated.

Key Takeaways

| Key Concept | Findings |

|---|---|

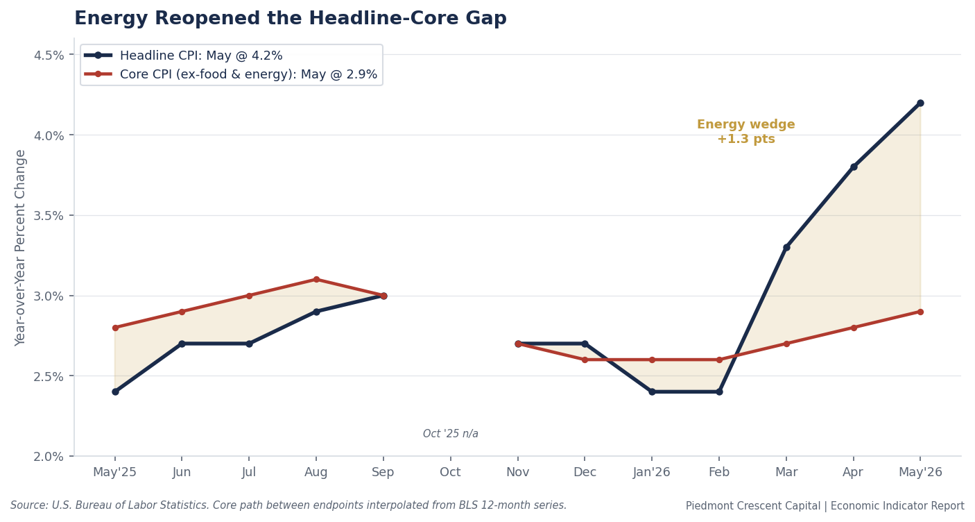

| Headline CPI | Rose 0.5% in May after 0.6% in April, lifting the 12-month rate to 4.2% from 3.8%. The third straight month in which energy did most of the lifting. |

| Energy | Up 3.9% on the month and 23.5% over the year, with gasoline alone up 7.0% in May and 40.5% over twelve months. Energy accounted for more than sixty percent of the monthly increase. |

| Core CPI | A contained 0.2% monthly gain held the core rate at 2.9%. Stripping shelter and energy, the underlying trend is running near 2.4%. The breadth of inflation is not widening. |

| Shelter | Up 0.3% as owners’ equivalent rent and primary rent each advanced gradually. Year-over-year shelter has eased to 3.4% and remains the slow-moving anchor under core. |

| Real Earnings | Real average hourly earnings fell 0.1% on the month and are down 0.7% over the year. For production workers the annual decline is 0.8%. Paychecks are losing ground to prices. |

| Policy Signal | A fourth consecutive firm headline keeps a 2026 cut off the table. We hold our no-cut base case, with the risk skewed toward a hike rather than an ease. |

The Overview

The May inflation report is best read as the third installment of a single story. For three consecutive months, a swing in energy prices has done most of the work in the headline, while the underlying trend has changed far less. The Consumer Price Index rose 0.5% in May after gains of 0.6% in April and 0.9% in March, and the twelve-month rate has climbed from 2.4% as recently as February to 4.2% in May. That is a meaningful move, and it is almost entirely an energy move.

We would caution against reading the four handle as evidence that inflation is reigniting across the economy. The pieces of the index that the Federal Reserve watches most closely behaved well. Core prices advanced a modest 0.2%, and the measures that strip out the noisiest categories point to an underlying pace closer to the high twos than the low fours. What changed in May was the price of a gallon of gasoline, not the price of services.

Energy Did the Lifting

The energy index rose 3.9% in May and is up 23.5% over the year, the steepest twelve-month pace since 2022. Gasoline did most of the work, climbing 7.0% on a seasonally adjusted basis and 40.5% over the trailing year. Energy alone accounted for more than sixty percent of the monthly all-items increase, which is why the headline can run hot while the core sits quietly underneath it.

This is the most regressive form of inflation. Households do not get to substitute away from the commute or the grocery run, and the bill lands hardest on the families that can least absorb it. That distributional reality matters more for the consumer outlook than the headline number itself, and it frames much of what follows.

Core Inflation Stayed Contained

Core CPI, which excludes food and energy, rose 0.2% in May and held its annual rate at 2.9%. The internals were reassuring. Communication prices jumped 1.3%, airline fares rose 2.7%, and personal care advanced 1.0%, but those gains were offset by outright declines in motor vehicle insurance, down 1.7%, household furnishings, off 0.6%, and new vehicles, lower by 0.3%. Medical care firmed 0.3% as hospital services rose, while prescription drugs fell. The give and take is the signature of an inflation pulse that is normalizing rather than broadening.

The cleanest read on the underlying trend is the index that removes food, shelter, and energy together. It rose just 0.1% in May and is running near 2.4% over the year. Strip away the volatile and the lagging, and what remains looks like an economy whose price pressures are close to target, not one accelerating away from it.

Shelter Keeps Cooling, Slowly

Shelter rose 0.3% in May, with owners’ equivalent rent up 0.3% and primary rent up 0.4%. The twelve-month shelter rate has eased to 3.4%, continuing a patient descent that has further to run as new-lease data flows through the index with its customary lag. Because shelter carries the largest weight in the core, its gradual moderation remains the most important disinflationary force in the report, quietly doing more for the trend than any single month of energy can undo.

Food Was Quiet, With Familiar Crosscurrents

Food rose 0.2% on the month and 3.1% over the year. Groceries were nearly flat, up 0.1%, as cheaper dairy and a continued collapse in egg prices, down more than thirty percent from a year ago, offset gains in beef and coffee. Food away from home rose 0.3%. There is little here to alarm, and the category is no longer the source of pressure it was two years ago, though the cumulative price level still weighs on household budgets.

Real Earnings: The Paycheck Problem

The companion release tells the part of the story that the headline obscures. Real average hourly earnings fell 0.1% in May and are down 0.7% over the past year, as a 0.3% nominal wage gain was overwhelmed by the 0.5% rise in consumer prices. Real weekly earnings fell 0.2%. For production and nonsupervisory workers, the squeeze is sharper still, with real hourly pay down 0.3% on the month and 0.8% over the year.

When prices outrun paychecks, the cost-of-living gain is not a statistic on a page. It is a smaller cart at the register and a thinner cushion at the end of the month. This is the mechanism behind the strain we have flagged all year, and it is why we treat the composition of this report as more consequential than its headline.

What Households Expect: The New York Fed Survey

The New York Fed’s May Survey of Consumer Expectations, released June 8, offers a useful read on whether the energy shock is changing the way households think about the future. The encouraging signal is that it is not, at least not yet. The median one-year inflation expectation eased a tenth to 3.5%, and the three- and five-year expectations were steady at 3.1% and 3.0%. Expectations remain anchored, which is exactly what the Fed needs to see when the pump price is doing what it did in May.

The less encouraging signal is the texture beneath that number. Households now expect rent to rise 7.4% over the year ahead, up more than a point, and food to climb 5.8%. Home price growth expectations jumped to 3.5%, the highest reading since 2022. Just as telling, the survey’s measures of household finances deteriorated broadly. The share of households reporting a worse financial situation than a year ago reached its highest level since early 2023, the perceived odds of missing a debt payment rose, and labor market confidence softened as layoff fears increased and the perceived ease of finding a new job fell. Expectations are holding, but the ground beneath them is less steady.

Four point two percent is an energy headline, not a broadening of inflation. Strip out the gasoline surge and the underlying trend is firmer than it was in the winter but still a long way from a reacceleration. Core sits at 2.9%, and the cleanest cut of the data, all items less food, shelter, and energy, is running near 2.4%. The breadth of price pressure is not widening, and shelter, the largest and slowest-moving piece of core, continues its patient descent toward 3%.

The composition is where the discomfort lives. An energy and grocery bill is a regressive tax, and it is landing on households whose real paychecks just turned negative. Real hourly earnings are down 0.7% over the year, and the squeeze is deeper for production workers. This is the two-Americas economy we have described all year: asset holders are insulated, while wage earners absorb the cost of living through the gas pump and the checkout line. Consumer expectations confirm the strain, with the New York Fed’s measures of household finances and labor market confidence both deteriorating in May.

For the Warsh Fed, this is a credibility test rather than a reacceleration scare. Longer-run inflation expectations remain anchored, but they are anchored at three percent, not two. A fourth consecutive firm headline removes any remaining case for a 2026 cut, and the second-round risk, energy bleeding into airfares, transport, and services, argues for patience over generosity. We retain our no-cut base case for the year, with the tail skewed toward a hike, and we continue to favor caution on duration as the term premium rebuilds.