ECONOMIC INDICATOR REPORT · EMPLOYMENT SITUATION, MAY 2026

Resilient and Broadening

Hiring Firms Across More Industries: Good for Growth, but Awkward for a Fed Boxed In by Inflation

EARLY SIGNAL

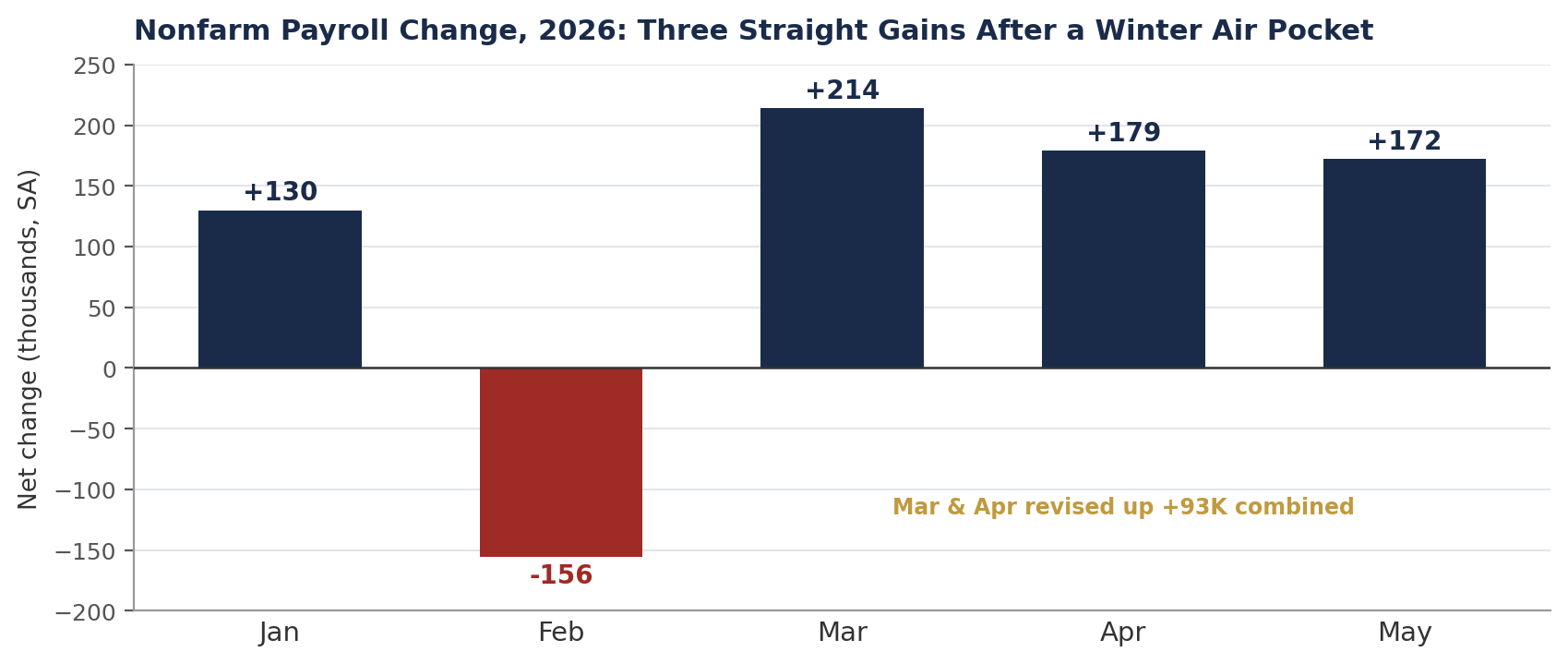

- May payrolls surprised sharply to the upside, rising 172,000, roughly double the consensus call of around 85,000 net new jobs and the third consecutive outsized monthly gain, the first such streak in about a year.

- March and April were revised up a combined 93,000 (to 214,000 and 179,000), reversing the persistent downward-revision pattern of late 2025.

- The unemployment rate held at 4.3% for a fourth straight month, with household employment growth outpacing labor force growth.

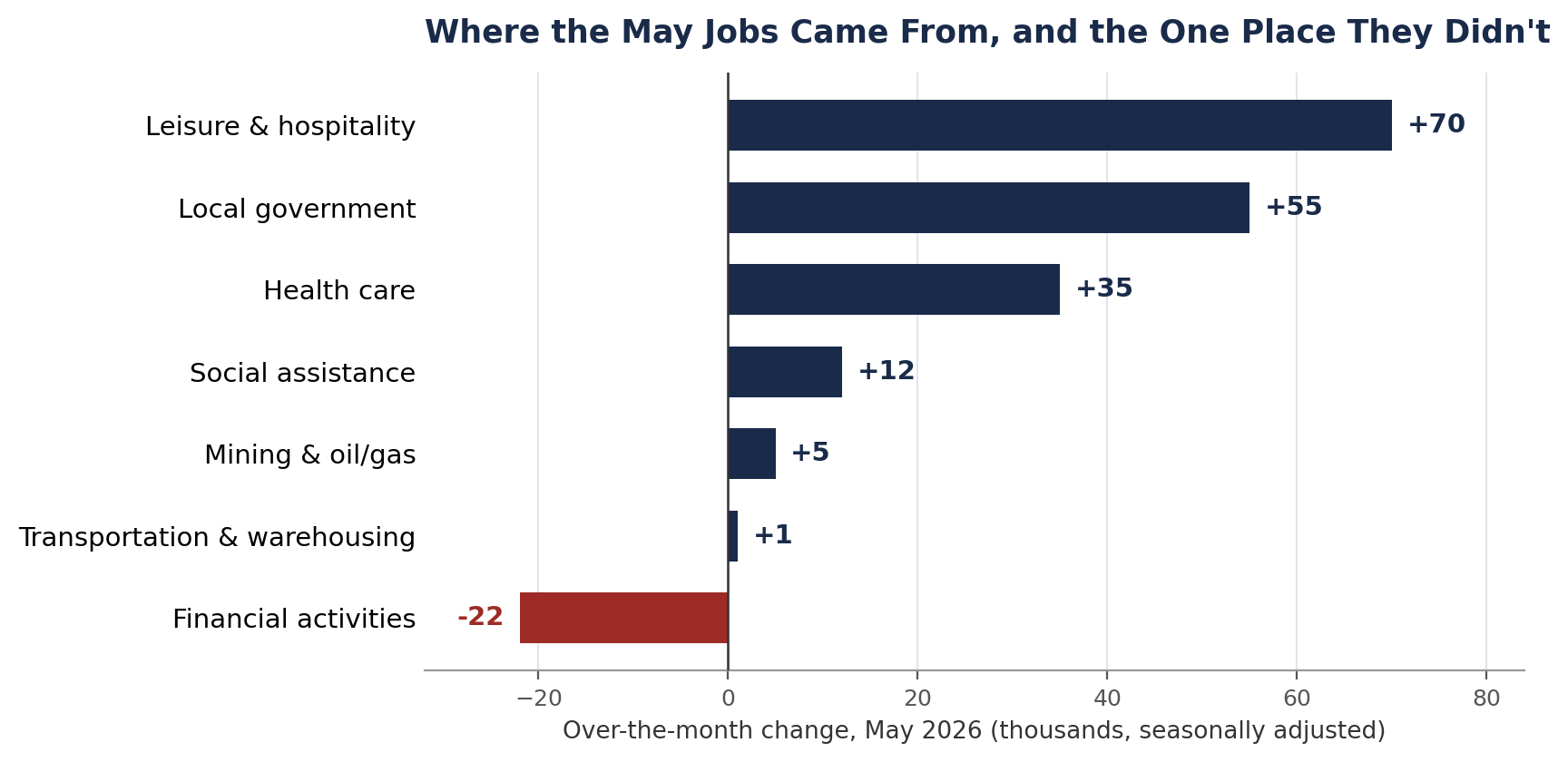

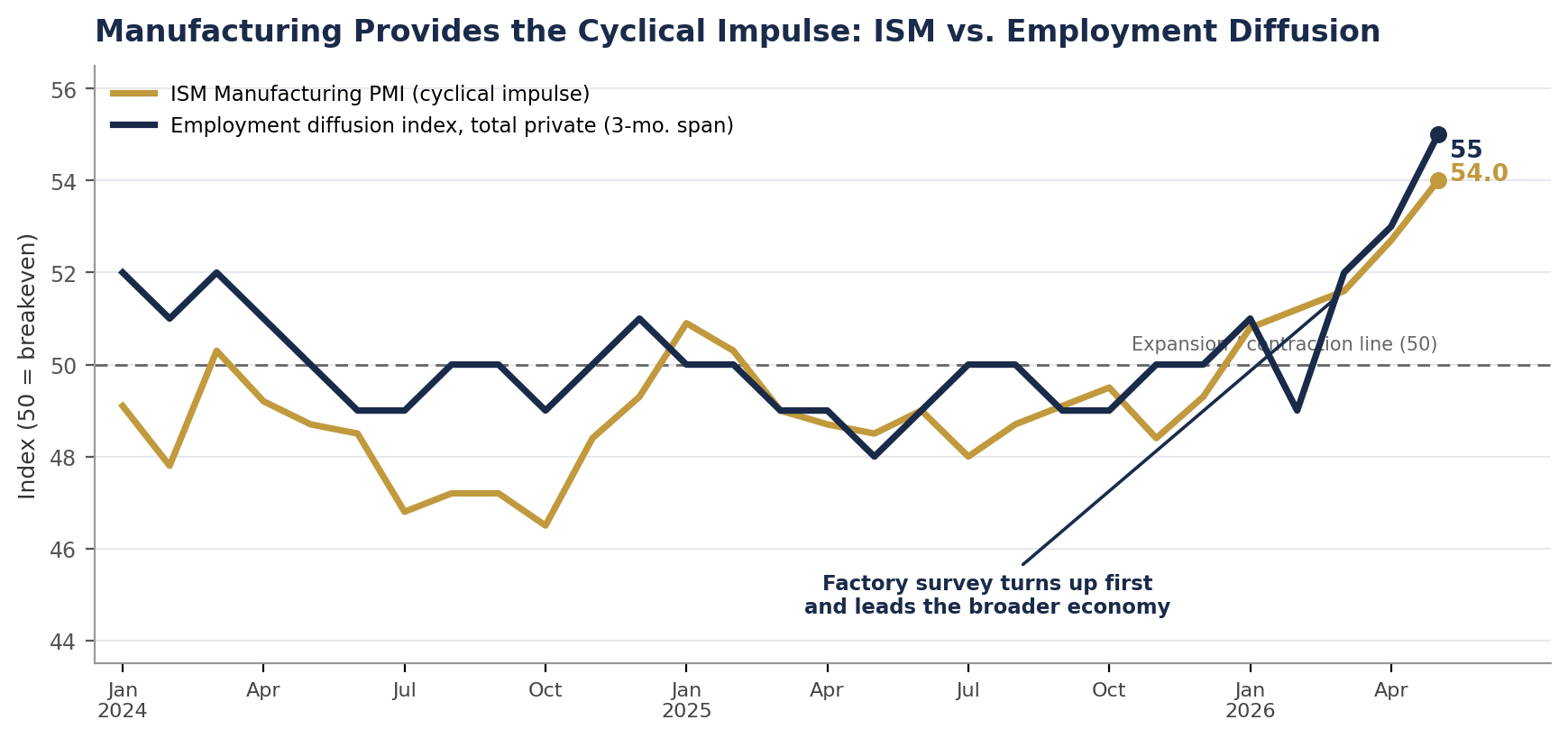

- Job growth is broadening, not narrowing. Although the bulk of the gain came in leisure and hospitality, local government, health care, and social services, the one-month diffusion index rose on both a total private and a manufacturing basis, confirming the firmer ISM manufacturing survey.

- Manufacturing is turning, and energy is ramping. The May ISM Manufacturing PMI hit a four-year high of 54.0% with 16 of 18 industries expanding, and oil and gas extraction added jobs again (up 5,000, and up 10,000 since February).

- Aggregate hours are rising. With the workweek steady at 34.3 hours and payrolls climbing, aggregate hours worked are tracking at roughly a 2% annualized pace in Q2 over Q1, consistent with our forecast for 2.8% real GDP growth for the quarter.

- Financial services is the one clear weak link, down 22,000, reflecting sluggish housing, rising consumer-credit delinquencies, slower light-vehicle sales, and cost-cutting pressure. Insurance, which lost 10,700 jobs, was a notable soft spot in May.

- Wage growth of 3.4% remains below inflation, leaving real average hourly earnings negative and the household squeeze intact.

A HEADLINE THE FED CANNOT IGNORE

May payroll growth blew past expectations. Employers added 172,000 net new jobs, roughly twice the consensus of around 85,000 and the third straight monthly gain, the first such streak in about a year. Coming on the heels of an upwardly revised 179,000 in April, the report reinforces a theme we have flagged repeatedly this spring, namely that the labor market appears to be firming amid a modest broadening in job growth. While the same group of industries (health care, social services, and leisure and hospitality) accounts for the bulk of the gain, the number of industries reducing employment has fallen, and manufacturing, logistics, and even some technology areas thought to be weighed down by AI are now seeing hiring firm up.

As is often the case, the revisions to prior months matter as much as the headline. The revisions run to the upside now, which is consistent with the firmer Q4 QCEW data reported earlier this week. March was revised up by 29,000 to 214,000 and April by 64,000 to 179,000, leaving the prior two months a combined 93,000 stronger than first reported. That is a clean break from the downward-revision pattern that dogged the data through late 2025, and it tells the Federal Reserve that the underlying pace of hiring has been firmer than real-time prints suggested. The private payroll processor ADP corroborated the direction, reporting 122,000 private jobs added, just above the 120,000 increase that had been anticipated.

CONCENTRATED BY VOLUME, BROADENING BY BREADTH

The bulk of the May gain came from a familiar set of sectors. Leisure and hospitality added 70,000 jobs, local government 55,000 (almost entirely outside education), health care 35,000, and social assistance another 12,000. On their own, those categories more than account for the headline. But the more important story this month is what is happening beneath that concentration, where hiring is beginning to broaden. The one-month employment diffusion index rose on both a total private and a manufacturing basis, meaning a wider share of industries added workers than in recent months, and that improvement lines up with a firming ISM manufacturing survey.

The manufacturing signal is the clearest evidence. The May ISM Manufacturing PMI climbed to 54.0%, its highest reading in four years, with new orders jumping to 56.8% and 16 of 18 industries reporting expansion. Factory employment within the survey rose more than two points. Manufacturing payrolls in the establishment data have not yet caught up, but employment historically follows sustained improvement in new orders and production with a lag of one to three months, precisely the sequence we described in January. Energy is adding to the breadth as well. Mining, quarrying, and oil and gas extraction added 5,000 jobs in May and is up 10,000 since February, a rational supply response to elevated crude and a sector that touches industrial activity across the Gulf Coast and Mountain West.

Manufacturing is a small share of total payrolls, but it punches well above its weight as a cyclical bellwether. Factory activity tends to turn before the broader economy, and it provides the cyclical impulse that pulls services hiring along behind it. Chart 3 shows the employment diffusion index moving in step with the ISM manufacturing gauge, with the factory survey turning up first and the broader labor market following.

AGGREGATE HOURS: THE GROWTH SIGNAL

Average hourly earnings rose 12 cents, or 0.3%, to $37.53, while the average workweek held at 34.3 hours and manufacturing held at 40.4 hours. A steady workweek combined with a rising headcount means aggregate hours worked, the broadest real-time gauge of labor input into the economy, continued to climb in May. Employers typically lengthen the workweek before adding to payrolls, so firm hours alongside firmer hiring is an encouraging sign for the months ahead.

That matters for the growth outlook. By our tracking, aggregate hours worked are running at roughly a 2% annualized rate in the second quarter relative to the first, and when paired with the strong productivity trend underlying this capital-intensive expansion, that pace is consistent with solid real GDP growth. The Atlanta Fed's GDPNow model has been tracking Q2 real GDP around a 3% annual rate. Rising aggregate hours support household income and consumption even without a wage-growth acceleration, and they argue against any narrative of an economy losing momentum heading into the summer. Q2 real GDP could bring an upside surprise, and we will likely bump up our 2.8% forecast for the quarter.

THE ONE WEAK LINK: FINANCIAL SERVICES

If the breadth of hiring is encouraging, financial activities is the conspicuous exception. The sector shed 22,000 jobs in May and is now down 107,000 from its May 2025 peak, with May's losses concentrated in insurance carriers, down 11,000, and commercial banking, down 3,000. In our view, this is not random noise. It reflects a cluster of interest-rate-sensitive pressures bearing down on the industry at once. Housing activity remains sluggish, holding down mortgage origination and related employment. Consumer-credit delinquencies are rising, pushing lenders toward caution and loss mitigation rather than expansion. Light-vehicle sales have slowed, weighing on auto-finance volumes. And across the industry, firms are under visible pressure to cut costs as net interest margins and fee income come under strain.

Transportation and warehousing tells a milder version of the same story, essentially flat in May and still 92,000 below its February 2025 peak. Together, these pockets are a reminder that the rate-sensitive corners of the economy are still absorbing the cost of restrictive policy, even as the broader hiring picture firms. Beneath the steady 4.3% unemployment rate, there is also a subtle lengthening of jobless spells. The long-term unemployed are up 524,000 over the year and now make up 27.5% of all unemployed, even as short-duration unemployment fell sharply in May. The increase is consistent with some skill obsolescence tied to the rollout of AI.

WAGES AND THE REAL-INCOME SQUEEZE

The critical wage comparison is to prices. Nominal average hourly earnings rose 3.4% over the year, below the most recent 3.8% headline CPI reading for April, which means real average hourly earnings remain negative, continuing the squeeze we documented in detail following the April inflation reports. We will not have the cleanest read until the May CPI lands on June 11, but the direction is clear, as workers' paychecks are still losing ground to the cost of living. Crucially, wage growth running below inflation is the strongest evidence that this is not a wage-price spiral. Workers are not driving inflation by extracting outsized raises. An energy- and supply-driven cost shock is eroding their real incomes.

WHAT IT MEANS FOR THE FED

This is the report the hawks wanted and the doves feared. With inflation reaccelerating, with April core CPI at 0.4%, the Cleveland Fed's trimmed mean near 4.4% annualized, and producer prices up 6.0% year over year, the labor market was the one piece of the puzzle that might have argued for patience tilting toward easing. It did not cooperate. A third straight solid payroll gain, upward revisions, broadening industry breadth, a four-year high in the ISM, and a steady 4.3% unemployment rate remove any labor-market justification for a near-term cut and strengthen the hand of the two FOMC members who dissented in favor of a tightening bias on April 29. While we do not see a rate hike this year, we are warming to the idea that the next Fed move will likely be in that direction.

Incoming Chair Kevin Warsh inherits this configuration at his first meeting on June 16 and 17. The data give him cover to hold without appearing to bow to either side, but they do nothing to resolve the deeper tension. Inflation is demanding patience at minimum, the economy and labor market are offering no offsetting weakness, and the White House is demanding cuts. Markets that briefly flirted with pricing a year-end hike will read this report as validating that risk rather than retiring it.

We continue to expect a hold at the June meeting, with the statement shifting toward explicitly two-sided risk language. Our base case still allows for a 25 basis-point cut in September, but that path remains conditional on Hormuz normalization, energy prices receding materially by mid-summer, and shelter disinflation reasserting itself. A strong, broadening jobs report does not advance that timeline. If anything, it removes the labor-market urgency that would have argued for moving sooner. The live risk we flagged after the April inflation data, that the FOMC debate shifts from when to cut to whether to hike, is not retired by this report. It is reinforced, and we are warming to the idea that the next Fed move, at some point in 2027, will be a rate hike. There is an awful lot of economic and geopolitical ground to cover before then, however.

BOTTOM LINE

May's employment report is strong where it is easy to see and, for the first time in a while, encouraging beneath the surface as well. The headline, the upward revisions, the steady unemployment rate, broadening industry breadth, a four-year high in the ISM, and rising aggregate hours together describe a labor market that is not just holding up but firming. This is the cyclical lift we anticipated in January, now beginning to supplement the structural, capital-intensive expansion. The one genuine soft spot is financial services, where sluggish housing, rising credit delinquencies, slower vehicle sales, and cost pressures are converging.

For the Fed, that strength is a double-edged sword. A broadening, resilient labor market is good for growth and for households' nominal incomes. But against a backdrop of reaccelerating inflation and still-negative real wages, it removes the last excuse for easing and keeps the central bank boxed in. The June meeting will be one of the most consequential in years.

WHAT WE ARE WATCHING

- May CPI (June 11): The most important print before the FOMC. A second consecutive firm core reading would materially raise the hike probability and confirm the real-wage squeeze.

- Warsh's first FOMC and press conference (June 16 and 17): Watch his framing on whether the spring inflation is a supply shock or a broadening trend, and what conditions he sets for any future cut.

- Manufacturing follow-through: Whether the four-year-high ISM and improving diffusion translate into actual factory payroll gains over the next one to three months, confirming the breadth signal.

- Financial services and the rate-sensitive complex: Housing activity, consumer-credit delinquencies, and light-vehicle sales, the channels driving the sector's job losses.

- Aggregate hours and real wages: Whether hours sustain their Q2 pace and whether nominal wage growth can close the gap with inflation into the summer.

Chief Economist, Piedmont Crescent Capital

mark.vitner@piedmontcrescentcapital.com · (704) 458-4000

Sources: U.S. Bureau of Labor Statistics, Employment Situation, May 2026 (June 5, 2026), and employment diffusion indexes (3-month span, total private); ADP National Employment Report; Institute for Supply Management, Manufacturing PMI, May 2026; Federal Reserve Bank of Atlanta, GDPNow; CME FedWatch; Dow Jones consensus surveys; Federal Reserve Bank of Cleveland; Piedmont Crescent Capital, April Inflation Reports Top Expectations (May 13, 2026).

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation, offer, or solicitation with respect to the purchase or sale of any security or other financial product, nor does it constitute investment advice.