A View from the Piedmont

Our Weekly Commentary on Money, Credit, Exchange Rates and Geopolitics

Two Markets, Two Americas, One Unsigned Deal

Three things defined the week: a data-heavy run that mostly confirmed our priors, a burst of US–Iran diplomacy that has yet to close, and the opening days of the Warsh Fed. The data showed a Q1 that was softer than first reported and a Q2 shaping up considerably stronger, with capital spending again carrying the load. While headline measures have spiked, underlying inflation keeps drifting sideways. The labor market is still in its low-hire, low-fire holding pattern. The capital-cycle thesis remains intact.

The week’s most uncomfortable number came from the New York Fed’s Q1 Household Debt and Credit Report, and it landed on the front page of the Wall Street Journal. Credit card delinquency of 90 days or more rose to 13.1%, the highest since 2011. Serious auto-loan delinquency is running near 5.4%, not far from financial-crisis levels. Aggregate delinquency, at 4.8%, looks calm, but the average hides the split underneath. The recovery, the capital cycle, and record margins now sit next to a lower-tier consumer who is falling behind. Both are true at once. The market is pricing only the first.

On geopolitics, the week ended unresolved but closer to a deal. The U.S. and Iran reached a tentative memorandum of understanding on Thursday to extend the ceasefire 60 days, reopen the Strait of Hormuz, and restart nuclear talks. President Trump left a two-hour Situation Room meeting on Friday without a final call, citing language on uranium disposition and Hormuz tolling. The deal is close. It is not signed.

What follows walks through the week’s data, the New York Fed credit picture, the Warsh Fed’s first public comments, the state of the Iran talks, a short Ukraine update, and Treasury Secretary Bessent’s Reagan Forum speech on reshoring. We close with the scenario framework and an updated forecast table.

The Macro Backdrop: Revisions Down, Nowcast Up

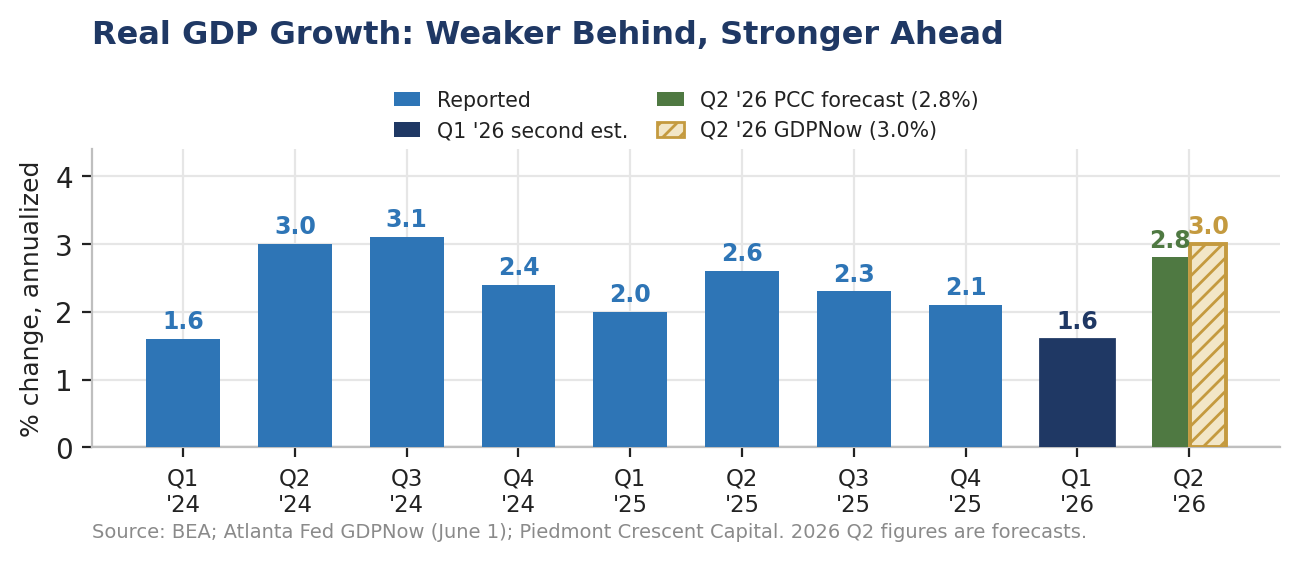

It was a busy week for economic data. The second estimate of Q1 GDP landed, April durable goods orders printed, the April Personal Income and Outlays report carried the PCE inflation read, and the Consumer Confidence Index for May rounded out the week. The Atlanta Fed cut its Q2 GDPNow estimate to 3.0% in today’s update, down sharply from 3.8% last week and now within two-tenths of our own forecast. The picture is familiar: weaker in the rearview mirror, stronger through the windshield, with the capital cycle still in the driver’s seat.

Q1 GDP revised down to 1.6%. The Bureau of Economic Analysis (BEA) cut its Q1 2026 growth estimate to a 1.6% annual rate on Thursday, May 28, down from the 2.0% advance reading, mostly on softer investment and consumer spending. The PCE price index held at 4.5% for the quarter; core PCE was nudged up a tenth to 4.4%. Real gross domestic income rose 0.9%, and the average of GDP and GDI, which some view as a steadier signal than either alone, came in at 1.3%. Corporate profits from current production rose $40.4 billion, a sharp slowdown from the $246.9 billion fourth-quarter gain. The revision itself matters less than the timing: the Q1 softness was front-loaded into the weeks before the war intensified, and the energy shock runs mainly through Q2 and beyond.

Durable goods jumped on aircraft; core capex slipped following strong earlier gains. April durable goods orders surged 7.9% to $346.0 billion, well past the 4.0% consensus and the largest monthly gain since last May, with new orders up 17.2% from a year earlier. Transportation drove it, rising 21.5% on a wave of nondefense aircraft orders. Excluding transportation, orders rose 1.1%. Core capital goods orders, which strip out defense and aircraft and are a proxy for business investment, fell 1.1% in nominal terms and 1.45% after adjusting for prices. Shipments rose 0.5%, unfilled orders 1.7%, inventories 0.3%. The aircraft surge will flatter second-quarter investment in the GDP accounts even as the underlying capex signal cooled. Whether that cooling is the war weighing on investment decisions or simply payback for earlier strength should show up in the May and June data. We lean toward the former and expect the capex trend to remain in place.

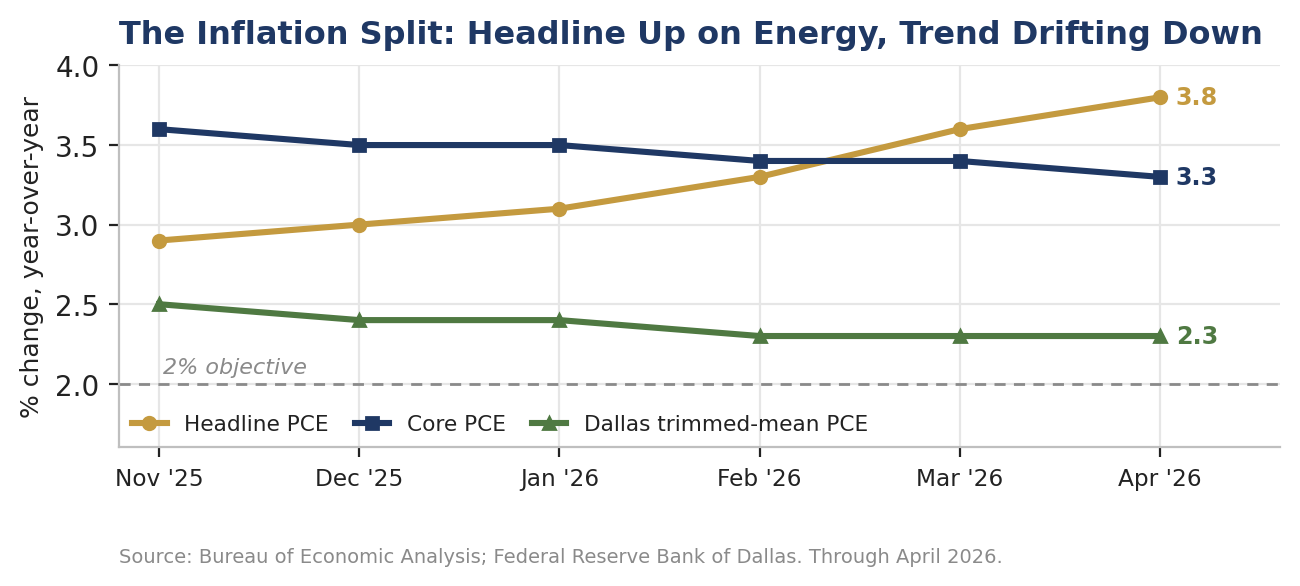

April PCE inflation came in about as expected. Core PCE rose 0.2% on the month and 3.3% from a year earlier, in line with consensus and a tenth below the prior monthly pace. Headline PCE rose 0.4% and 3.8% year over year, the energy pass-through doing the work. Personal income was roughly flat. The Dallas Fed’s trimmed-mean PCE rate, which Chairman Warsh singled out in his Senate testimony as a cleaner gauge of underlying pressure, held at 2.3% over twelve months. The read is unchanged: oil is pushing the headline around while the trend measures stay contained and point lower. Treating the war as a one-time supply shock rather than a new inflation regime remains the most defensible interpretation, although price increases appear to us to be a bit broader than the trimmed-mean PCE deflator suggests.

Atlanta GDPNow cut to 3.0% for Q2; our call is 2.8%. The Atlanta Fed’s nowcast was cut to 3.0% in today’s update, down from 3.8% last week and a 4.3% peak on May 21. The path tells the story: 3.7% at the start of May, 4.3% mid-month, 3.8% after the GDP revision and durable goods print, and now 3.0% as the model digests the softer underlying data. That move brings the nowcast within two-tenths of our own 2.8% forecast, which we have held for weeks. We had argued the higher prints were flattered by the aircraft-driven jump in durable goods and a likely inventory build, while the cleaner signal from core capital goods orders softened and consumer spending lost momentum. Today’s revision is the model catching down to that view rather than the other way around. Either way the message holds: capital spending and government outlays are running hot, the top of the income distribution is steady, and the bottom is softening. The still-firm Q2 headline conceals that split.

Consumer credit, plainly. The New York Fed’s Q1 2026 Household Debt and Credit Report is the most uncomfortable read we have seen in a while. Total household debt edged up 0.1% to $18.8 trillion. Credit card balances fell seasonally by $25 billion to $1.25 trillion, yet the serious delinquency rate, which are accounts 90 days or more past due, rose to 13.1%, the highest since 2011. Auto balances climbed to $1.69 trillion with serious delinquency near 5.4%, close to financial-crisis levels. Student loan balances were flat at $1.66 trillion, with serious delinquency up to 10.3% from 9.6% in Q4 as repayment strains persist. Mortgages remain in good shape: HELOC balances keep expanding and overall mortgage delinquencies sit near historic lows. Aggregate delinquency, at 4.8%, is little changed. But the K-shape is now obvious, and the stress is concentrated among lower- and middle-income households. This is not a recession signal by itself; the mortgage book is too clean and the labor market too steady for that. It is, though, a real constraint on discretionary spending as the year wears on, and the first place to watch if hiring falters.

Piedmont Perspective: Two Americas, One Economy

S&P 500 net profit margins hit 13.4% in Q1, the highest since FactSet began tracking the series in 2009. Information Technology led at 29.1%, up from 25.4% a year earlier. Across the index, 84% of companies beat EPS estimates, and earnings ran 18.2% above forecasts against a five-year average of 7.3%. Capital deployed well is earning returns at a breadth we have not seen since the late 1990s.

Over the same stretch, credit card delinquency reached 13.1%, also a post-2011 high, and auto stress is brushing financial-crisis levels. Aggregate delinquency looks stable at 4.8% only because the mortgage book is so clean and roughly two-thirds of household debt sits in mortgages, where the prevalence of low fixed-rate mortgages and equity cushions are providing a powerful offset. The rise in auto delinquency rates is another headwind for light vehicle sales, which remain under pressure from payback for the COVID-era surge sales that occurred at or above the sticker price then and have left many car owners with negative equity now.

Two nearly identical numbers, pointing in opposite directions. The asset-owning, equity-holding economy is having a banner year. The wage-dependent, revolving-credit economy is sinking. The labor market sits in between, in its low-hire, low-fire stall, masking the gap for as long as layoffs stay low. The risk we care most about is not inflation, the war, or the Fed. It is whether the bottom half of the income distribution can hold on long enough for the capital cycle to feed through into wages. That has historically taken several quarters of sustained capital deepening, and it is the reason we stay constructive on the medium term even as we flag the near-term risks to household finances.

The timing of the dampening near-term effects on employment and income and intermediate to long-term productivity-enhancing effects puts the Fed in a bind. Cutting harder might ease the strain on indebted households, but the better inflation gauges are not yet at target, and the capital cycle does not need help. Remaining restrictive keeps inflation moving the right way but allows the credit stress to compound. The Warsh framework, leaning on trimmed-mean measures and a structural optimism about productivity, can sit still for a while. The political pressure to cut, already building before the war, will be back as soon as the war recedes.

The Warsh Fed’s First Week of Commentary

Chairman Warsh was sworn in on May 22 and elected FOMC chairman by the Committee the same day, succeeding Chair Powell, whose term as chair ended May 15. Minutes of the April 28–29 meeting, released May 20 ahead of the handover, showed the 8–4 split we covered last week. This week brought the first substantive remarks under Warsh, from Vice Chair Jefferson, Governor Cook, and Vice Chair for Supervision Bowman, plus Governor Waller and Powell himself in his final public appearance.

Jefferson (May 27, Tokyo). Speaking at a Bank of Japan conference, Jefferson said the global inflation impulse from the Iran shock is large but so far concentrated in energy and energy-adjacent categories, with longer-run expectations still anchored across major economies. His tone was measured, with no near-term policy signal. What stood out was his focus on the cross-border transmission of the shock and the implications for the trade-weighted dollar, an increasing concern for the Treasury market as deficits stay wide.

Cook (May 27, Stanford). Cook addressed AI, the economy, and the financial system. She acknowledged that AI is delivering measurable productivity gains today and is likely to compound, while flagging the financial-stability risks of the capex boom, particularly the private-credit channels funding data-center and power buildout. The mix of optimism on potential and caution on financing tracks Warsh’s framework closely. The Fed looks increasingly comfortable with the productivity story and increasingly attentive to how it is being financed.

Bowman (May 29, Reykjavík). Bowman focused on conducting policy under uncertainty, arguing that any easing should be gradual and data-dependent, with attention to whether the trend measures keep drifting lower despite the energy-driven headline. No near-term preference, but a reinforcement of the Committee consensus: patience, data dependence, and explicit caution about the war’s distortion of the headline.

Waller (May 22 Frankfurt, May 31 Dubrovnik). Waller spoke on the outlook in Frankfurt and on stablecoins in Dubrovnik on Sunday. The Frankfurt remarks were the week’s most substantive: the labor market is roughly in balance, the war’s inflation impulse should fade through the back half of the year, and the run-rate of underlying inflation, on the Dallas trimmed mean, is consistent with the Fed’s longer-run goal. That reads more dovish than the rest, though Waller stopped short of calling for cuts.

Powell (May 31, Boston). Powell delivered acceptance remarks for the John F. Kennedy Profile in Courage Award on Sunday, reflective rather than forward-looking on policy. His term as Governor runs through January 2028, and he has not said whether he will stay on the Board. The market assumes he will, which matters for the internal balance of the Committee even with Warsh in the chair.

Net read. The opening week was patient and data-dependent, consistent with our view that the next move is more likely a cut than a hike, with the timing firmly in the back half of the year. We still expect the first cut in September if the trend on inflation cooperates and the labor market holds. A second cut in December is plausible but increasingly hinges on the consumer-credit picture not deteriorating.

Geopolitics: Iran Close, Not Done; Ukraine Attritional

Iran and Hormuz: a tentative MOU awaiting signature. The week’s biggest development was a tentative U.S.–Iran memorandum of understanding to extend the ceasefire 60 days, reopen the Strait of Hormuz, end the U.S. blockade of Iranian ports, and reopen nuclear talks. Trump sketched the outline on May 23, saying a deal had been “largely negotiated” pending sign-off from several Gulf states and Israel. The two sides reached the tentative framework on Thursday, May 28, with Treasury Secretary Bessent calling it the “makings of a deal.” On Friday, Trump entered the Situation Room to make a final determination, attaching two key conditions: Iran’s highly enriched uranium “unearthed by the United States” and destroyed, the strait reopening with no tolls. He left after two hours without an announcement. As of Sunday, no signature is confirmed.

The mechanics matter. The framework sets a 60-day ceasefire window: the strait reopens toll-free, Iran clears deployed mines within 30 days, the U.S. lifts the blockade, and nuclear talks resume. Sanctions relief and the unfreezing of certain assets are flagged for negotiation during the window, contingent on the strait operating normally. Kazakhstan has publicly offered to take Iran’s enriched-uranium stockpile, one route to settling the disposition question. The IRGC, Hezbollah, and Iranian hardliners continue to object to the main terms. The administration says Iran reneged on earlier uranium commitments, and the Pentagon reported Thursday that Iran fired a ballistic missile toward Kuwait and moved drones around the strait. So we are closer to a deal but not done.

Markets have moved. Brent eased toward $95 by Friday, well off the mid-May high near $119, on deal optimism. U.S. retail gasoline has retraced toward $4.20 a gallon, still above pre-war levels but off the peak. The World Bank, IMF, and IEA issued a joint statement Friday warning that if shipping does not normalize soon, the continued rapid drawdown of global oil inventories ahead of peak summer demand would raise risks to fuel security and broader resilience. The timing was deliberate: the institutions want closure before the driving season.

Our read: the deal probably gets done, with edits. The framework is close enough that both sides can sell it as a win. Trump can say Iran’s nuclear program will be dealt with over the next 60 days; Iran can point to sanctions relief and a lifted blockade in exchange for safe passage. The sticking points: the uranium-destruction and Hormuz-tolling language are exactly the pieces each side needs for its domestic story. We expect an announcement this week, possibly with further textual edits or side letters that paper over the gaps. The risk is that hardliners or the IRGC derail it first, or that another incident kills the moment. We raise our base-case probability that the strait reopens by mid-summer to 55% from 50% and hold the downside at 30% because the deal is not done.

Ukraine: attritional, with new NATO friction. The Institute for the Study of War describes a grinding rather than turning conflict. Russia is preparing another large aerial strike. Ukrainian forces hit a Russian Iskander system in Rostov Oblast overnight on May 29–30 and continue to remote-mine supply lines in occupied territory. The more consequential event for NATO was a Russian Geran-2 drone strike on an apartment building in Galati, Romania, on the night of May 28–29. Moscow is running a two-track response, deflecting blame onto Ukraine while laying groundwork to absolve itself of future strikes against Moldova (read our previous research on Moldova). The pattern is familiar, and the implications for the Article 4 and Article 5 thresholds are material. Ukraine continues to burn through Russian materiel faster than Moscow can replace it, though when that constraint binds is still unclear. Putin’s approval slipped again in state polling, a series we treat skeptically, and Russia is reportedly letting private firms buy air-defense and counter-drone systems, a sign the federal supply squeeze is real.

Policy: Bessent at the Reagan Forum and the Reshoring Trade

Treasury Secretary Scott Bessent used the Reagan National Economic Forum in Simi Valley on Friday to lay out the administration’s economic-security doctrine in an address titled “While America Slept,” followed by a fireside chat with Larry Kudlow. The title is a nod to Churchill’s 1940 wartime address “While England Slept.” We flag it because the framing provides insight into the priority the Administration places on this issue and provides an idea where tariffs, procurement, and investment are headed. This matters more for the medium-term capital cycle than any single data point this week.

Bessent’s thesis is that decades of optimizing supply chains for cost and efficiency hollowed out domestic capacity in the industries that matter most in a crisis: semiconductors, rare earths, pharmaceuticals, and defense goods; and that this is a national-security problem, not merely an economic one. “We mistook comfort for strength,” Bessent said, faulting a generation of policy that treated efficiency as a substitute for resilience and consumption as the measure of prosperity. He organized the agenda around three pillars: industrial dominance, domestic investment, and preparedness. The bottom line, however, is building resilience.

What it implies for trade policy. The direction is clear. Expect tariffs aimed specifically at imports from adversarial nations rather than uniformly across partners, paired with a willingness to use the federal balance sheet directly: Bessent floated taking equity stakes in strategic sectors such as rare earths and pharmaceuticals to offset what he framed as non-market competition from state-subsidized foreign producers. The throughline is selective decoupling from rivals, China in particular, and a tighter weld between trade policy and national security, with semiconductors and U.S. reliance on Taiwan singled out as the priority vulnerability. This is a more surgical, more interventionist trade posture than a simple tariff wall, and a less predictable one for firms whose supply chains run through targeted countries.

What it implies for reshoring. Continuity, with acceleration. The speech reinforces the capital-cycle thesis at the center of this report: federal policy is now actively subsidizing and protecting domestic capacity in chips, critical minerals, pharma, and defense, which underwrites multi-year capex in exactly those areas. The cost is a structurally higher price level, as resilience is more important than efficiency, and more supply-chain friction for import-dependent businesses. Net, it is constructive for domestic industrial capex and the companies building it, and a margin-and-complexity headwind for firms sourcing through rival nations. It also fits the week’s other threads: the same logic that wants chips and minerals onshore is the logic behind the financial pressure on Iran that Bessent and Kudlow discussed.

Markets & Financial Conditions

Equities still take the constructive view. The S&P 500 finished near record highs on deal optimism and the breadth of Q1 earnings. The 10-year Treasury yields about 4.45%, the 2-year 3.84%, and the curve is positively sloped by roughly 61 basis points. The long end has eased on de-escalation hopes, but term premium keeps rebuilding on heavy issuance, and a growth backdrop the bond market increasingly accepts.

Brent settled near $95 Friday, off the $119 mid-May peak but still well above pre-war levels. Commercial stocks are tight: the IEA puts Persian Gulf production losses near 14 million barrels a day, and U.S. refined-product stocks have drawn for thirteen straight weeks on gasoline and ten on distillates. The supply math stays tight even with the diplomacy. A clean strait reopening in June would point Brent toward $80 by year-end, risks two-sided. A collapse puts $120 back in play.

Credit has widened modestly over the past two weeks on the consumer story, with high-yield spreads roughly 25 basis points wider to Treasuries and BB paper a bit more. It is not yet stressful, but it shows the market starting to absorb the New York Fed report. Investment grade remains tight.

CFO & Treasurer Corner: What This Means for Corporate Finance

Funding & liquidity. The fixed-rate window is open but unlikely to improve much soon. With the 10-year near 4.45% and term premium rebuilding, keep locking fixed-rate funding opportunistically, and pull forward 2027 and 2028 maturities where the trade-off allows. Floating-rate borrowers should stress interest coverage assuming the 10-year holds at or above 4.40% through year-end.

Energy & input costs. Brent at $95 beats $119 but is still elevated, and diesel and middle distillates remain the choke point. Firms exposed to freight, logistics, or petrochemical inputs should keep stress tests on 2026 cost assumptions in place. The hedging window may widen if the deal closes cleanly, but do not count on it.

Consumer exposure. The New York Fed credit data belongs in board discussions, particularly with the recent weakness in real incomes. Businesses serving lower- and middle-income households should model demand sensitivity to rising card delinquencies; auto-related firms should model further weakness in lower-tier credit; and anyone in subprime-adjacent lines should revisit reserve assumptions.

Capital allocation. The capital-cycle thesis continues to hold. Commitments tied to AI, power generation, grid, and reshoring are on plan or accelerating, and the market keeps rewarding credible productivity narratives; the Alphabet-versus-Meta divergence earlier this season is the cleanest illustration. The bar for capex without a clear margin path is rising.

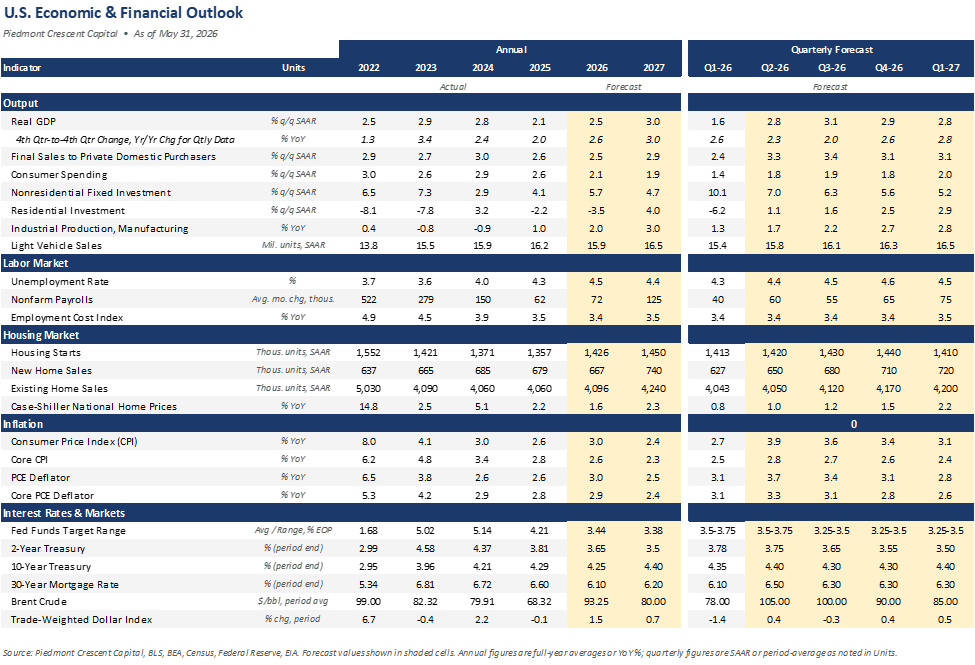

Planning assumption. Our base case has the strait reopening by mid-summer, the MOU signed within two weeks, and Brent retracing toward $80 by year-end. Full-year GDP near 2.5%, led by capital spending. The Warsh Fed cuts 25 bps in September, with a December cut conditional on labor and credit holding up. With the downside at 30% and consumer credit a fresh risk, boards should model both a war-escalation case and a deepening-consumer-credit case for Q3.

Looking Ahead

| Day | Release / Event | Why It Matters for CFOs & Markets |

|---|---|---|

| Monday | ISM Manufacturing (May); Construction Spending (April); Atlanta Fed GDPNow update | ISM is the cleanest read on whether the energy-cost impulse is still squeezing margins; watch the prices and employment indices. The GDPNow update folds in the durable goods and PCE prints and resets the Q2 picture. |

| Tuesday | JOLTS (April); Factory Orders (April); Total Vehicle Sales (May) | Job openings have drifted lower for months; another step down strengthens the case for a September cut. Vehicle sales will reveal more about dealer mindsets. |

| Wednesday | ADP Employment (May); ISM Services (May); Beige Book | ADP provides the best private-payroll assessment ahead of Friday. ISM Services has now expanded for 23 straight months. The Beige Book adds regional color on labor and prices. Look for signs of resilience or firming demand. |

| Thursday | Trade Balance (April); Initial Claims; Productivity & Unit Labor Costs (Q1 revised) | Trade has been volatile throughout the war. Claims remain the highest-frequency labor signal and remain near historic lows. The productivity revision speaks to the AI story that anchors the Warsh framework. |

| Friday | Employment Situation (May) | The main event. Consensus is roughly 90,000 payrolls with unemployment at 4.3%. Watch wage growth, breadth (which has been improving), and revisions. A clean print holds the low-hire, low-fire read; a soft one with rising unemployment pulls rate cuts forward. |

The open questions for the week: whether the Iran deal closes, whether the May payroll print holds or breaks the low-hire, low-fire equilibrium, and whether the consumer-credit stress in the Q1 New York Fed data kept building through April and May. How the numbers are read will matter more than the headlines.

Scenario Framework

| Scenario | Macro & Market Implications | Corporate Finance Action |

|---|---|---|

| Base Case55% | US–Iran MOU signed in early June; Hormuz reopens by mid-summer; Brent retraces toward $80 by Q4. Capital cycle runs on; Q2 GDP near 2.8% (in line with the 3.0% nowcast), full year around 2.5%. Labor stays low-hire, low-fire with unemployment 4.3–4.5%. Consumer credit stress is contained but persistent. Warsh Fed cuts 25 bps in September, possibly again in December. 10-year holds 4.30–4.60%. | Lock fixed-rate funding opportunistically. Stay with productivity-led capex. Build modest buffers on energy-sensitive inputs. Model lower-tier consumer softness in revenue. |

| Upside15% | Deal signs cleanly; Hormuz reopens faster than expected with mines cleared by July. Brent back to $70–75 by Q3. Capital cycle accelerates. Consumer credit stabilizes as gasoline slips below $3.50. Fed cuts 50 bps in H2. | Step up productivity-led capex. Shift working capital toward growth. Open the refinancing window wider. |

| Downside30% | Deal collapses or stalls in implementation; hardliners or the IRGC trigger a fresh Hormuz incident; Brent back above $120. Headline CPI re-accelerates above 4%. Consumer credit stress deepens. Fed on hold indefinitely. Credit spreads widen 50–100 bps. GDP slows toward 1.5% in H2. | Stress-test floating-rate exposure. Build liquidity. Defer non-essential capex. Hedge energy and freight. Review covenant headroom. |

Forecast Update

This commentary reflects the views of the author as of the date noted and is provided for informational purposes only. It does not constitute investment advice or a recommendation to buy or sell any security. Information has been obtained from sources believed to be reliable, but accuracy and completeness are not guaranteed. Past performance is not indicative of future results. © 2026 Piedmont Crescent Capital.

Piedmont Crescent Capital | A View from the Piedmont | June 1, 2026