Housing politics in a supply-constrained economy

Executive takeaway

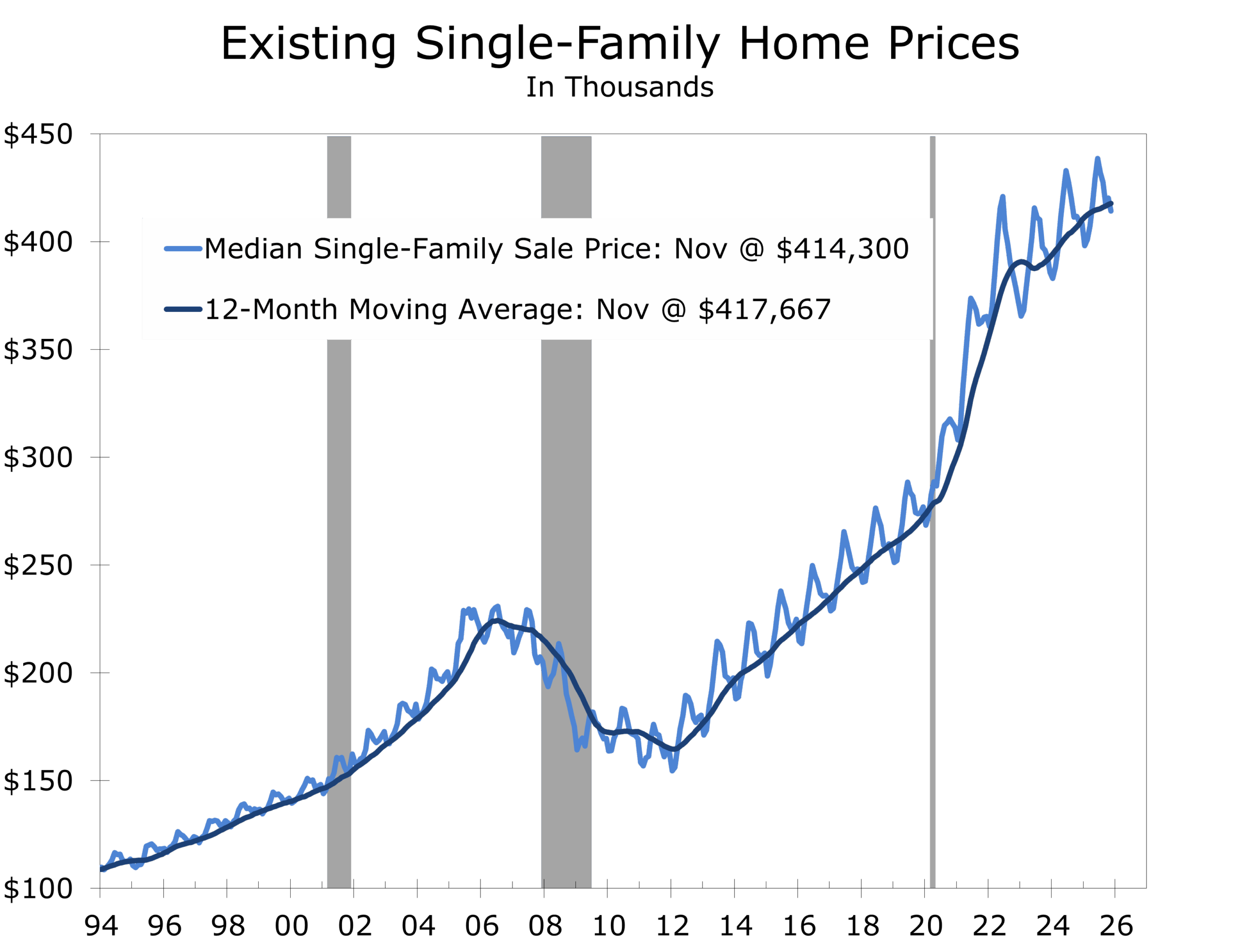

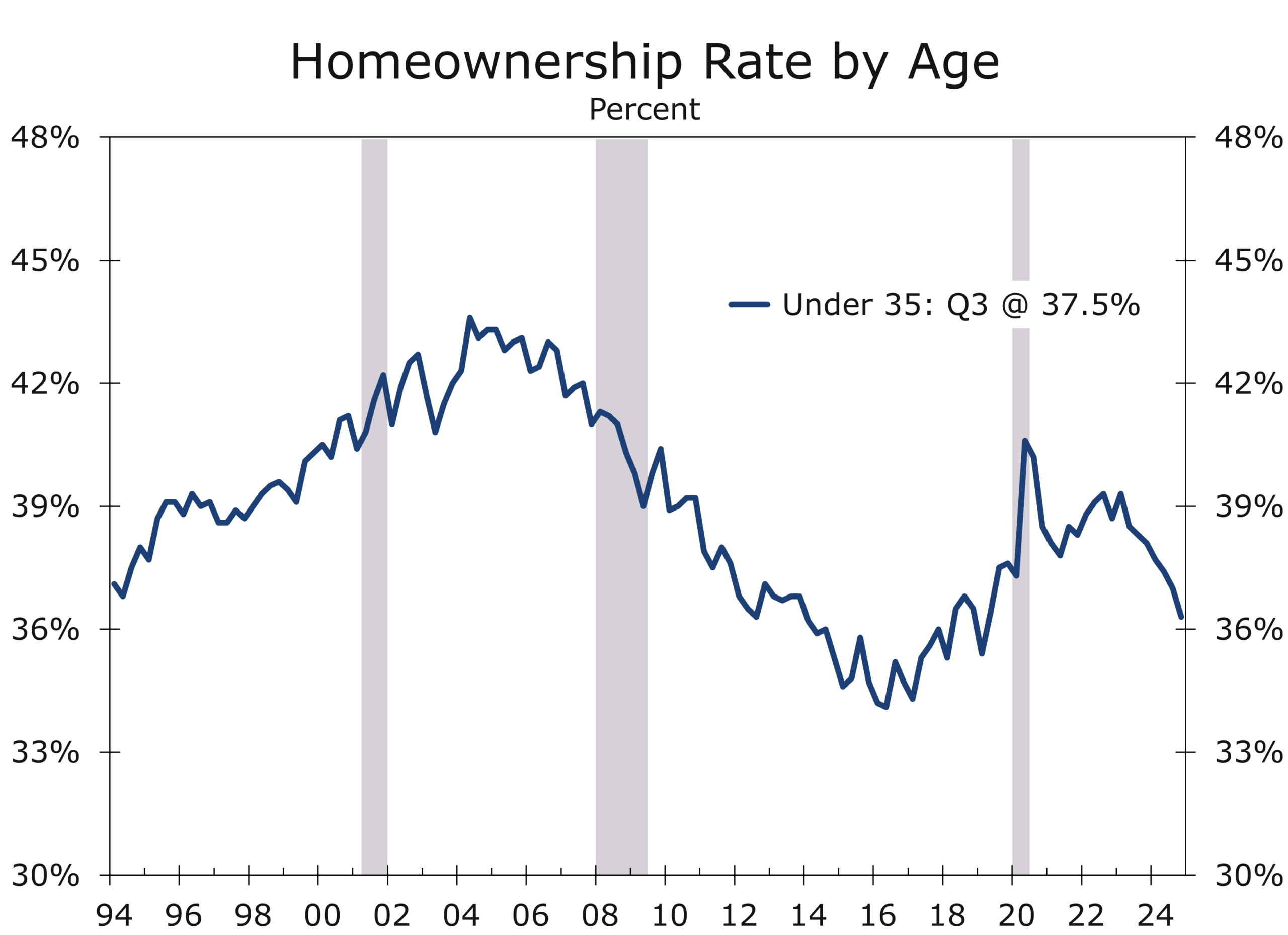

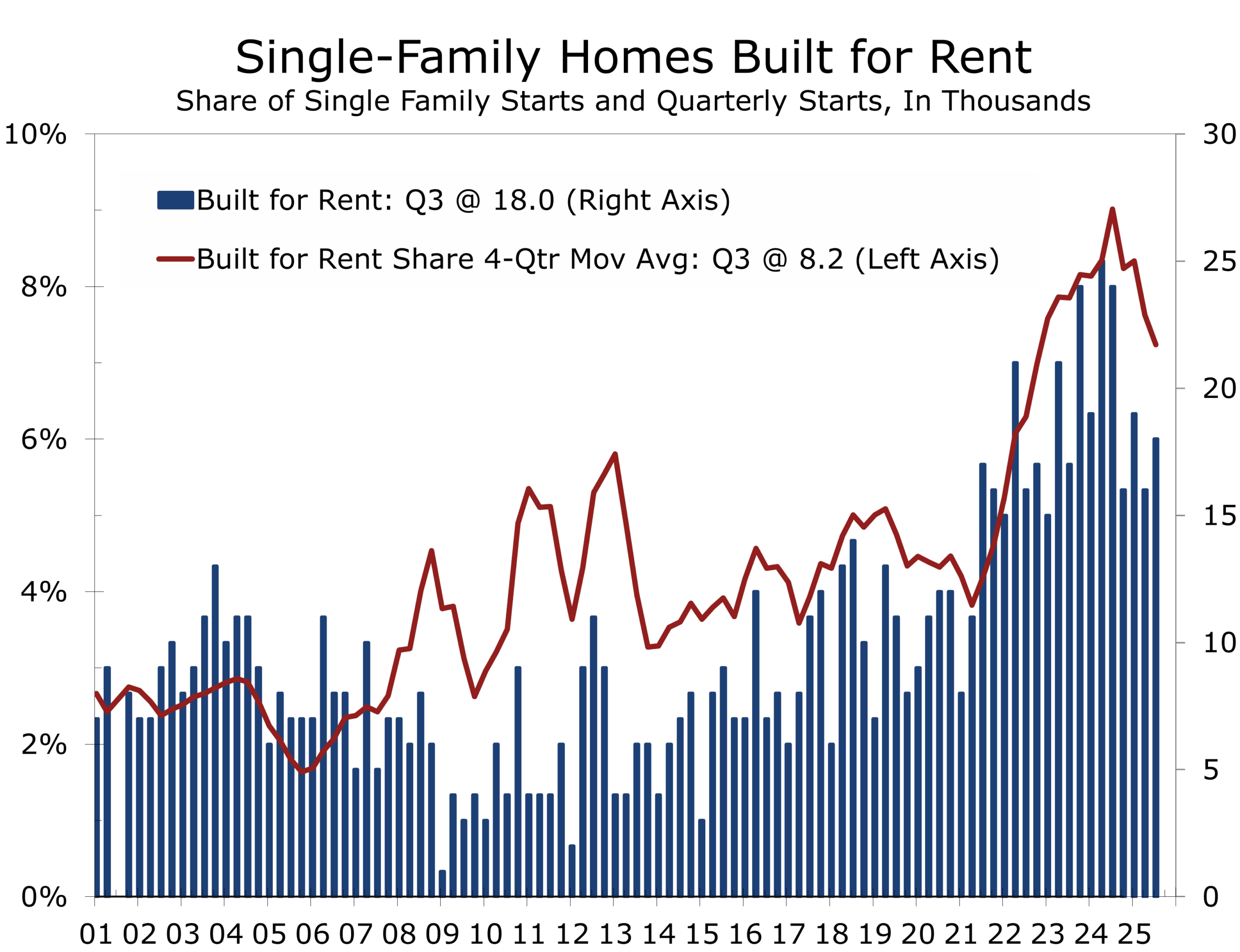

Proposals to limit institutional purchases of single-family homes reflect real frustration over housing affordability, but they misdiagnose the problem. Large institutions own only a small share of the U.S. housing stock and cannot explain the national rise in home prices; where they matter is at the margin, in supply-constrained metros where purchase flows can amplify price pressures and reduce entry points for first-time buyers. Even there, institutional activity is a second-order effect layered on top of a much deeper structural shortage driven by years of underbuilding, restrictive zoning, rising construction costs, and strong in-migration. Recent data show institutions already slowing acquisitions and shifting toward build-to-rent, helping expand rental supply rather than crowd it out. Framing affordability as a battle between households and institutions may be politically appealing, but durable relief will come from expanding housing capacity—faster permitting, zoning reform, and infrastructure investment—not from constraining capital in an already undersupplied market.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 12, 2026

Mark Vitner, Chief Economist

Piedmont Crescent Capital