Tariffs Cast a Cautious Shadow Over The U.S. Economy

- The implementation of larger-than-expected tariffs has led the Federal Reserve and most private forecasters to sharply lower their projections for economic growth this year. The tariffs are not only higher and more broad-based than anticipated but are also now expected to be more enduring and more disruptive to both U.S. and global economic growth.

- Tensions between President Trump and Fed Chair Jerome Powell raise concerns about potential monetary policy missteps in 2025. Powell, cautious after the Fed’s 2021-2022 misjudgment of inflation as “transitory,” may resist pressure to ease rates aggressively. Meanwhile, Trump has criticized the Fed’s 2017-2019 rate hikes for slowing growth and its limited easing in 2019 for leaving the economy unnecessarily vulnerable before the pandemic.

- The absence of a flight to safety following the early April tariff announcements has been viewed by some as a sign of diminishing U.S. exceptionalism. The larger-than-expected tariffs come amid inconsistent messaging on Russia-Ukraine conflict and NATO leadership. While we share some sympathy for these perspectives, we believe the weaker dollar and rising Treasury yields signal expectations of deeper trade dispute impacts—specifically, a shift in production to developing economies and heightened competition for global savings—mirroring dynamics preceding the late 1990s emerging market crises and the collapse of Long-Term Capital Management (LTCM).

- The soft data from various surveys continue to flash warnings signs that the U.S. economy is slowing significantly, while the hard data remain consistent with slower but still solid economic growth. We are closely watching the higher frequency data for clues that the economy’s underlying momentum and continue to hold the view that a recession will be narrowly averted.

- Geopolitical risks remain high on a number of fronts aside from tariffs. Russia appears to be taking advantage of Trump’s negotiating posture and has been racing to push Ukraine out if Kursk region and solidly gains in eastern Ukraine, while maintaining unrealistic objectives for a lasting peace. U.S. attacks on Houthi infrastructure have intensified but will likely need to go further to dissuade attacks on shipping or influence demands on Iran’s nuclear program.

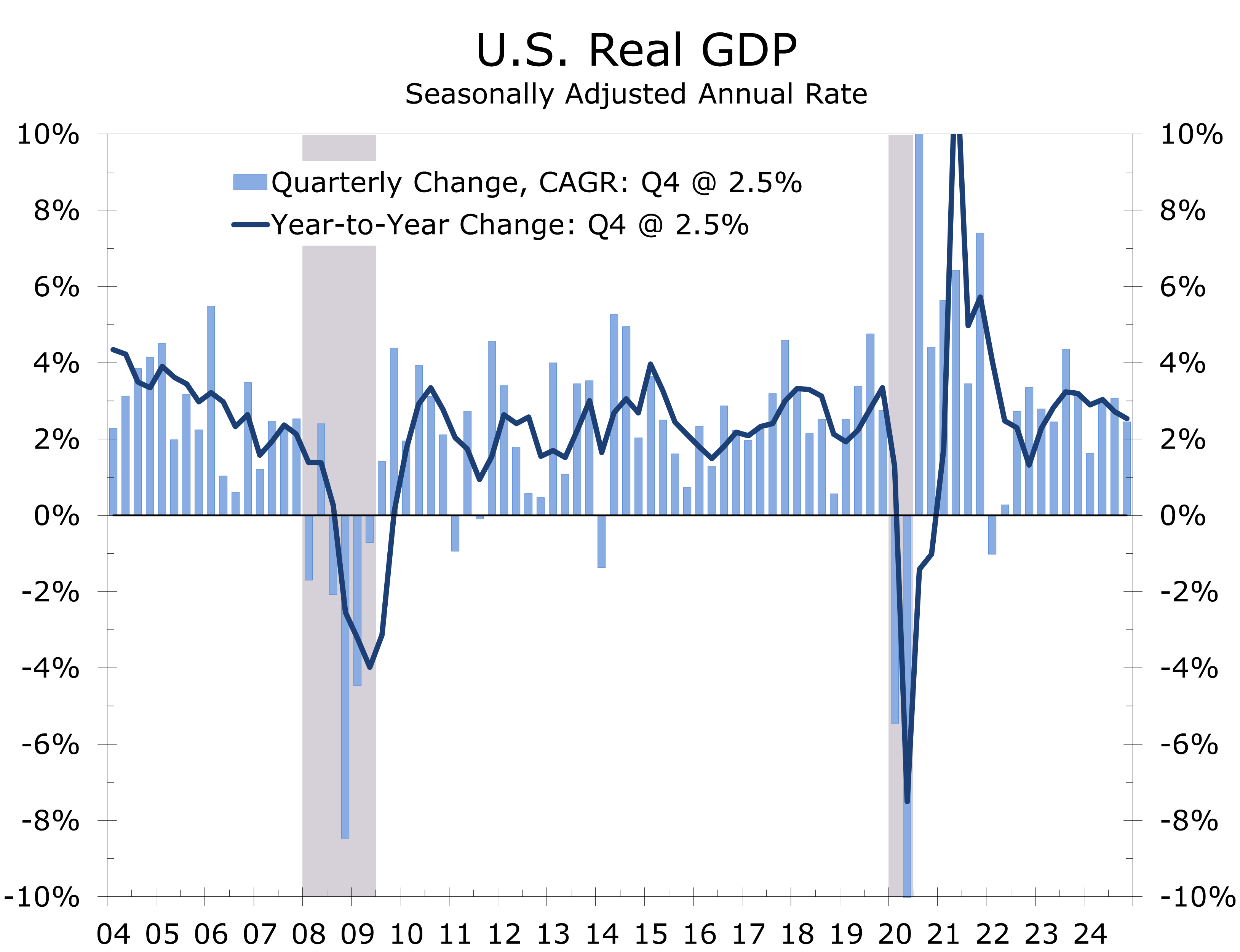

- The front-loading of imports ahead of tariffs will lead to wide swings in GDP during the first half of this year, a time of the year when GDP growth has tended to be weak in recent years. While jobless claims remain exceptionally low, we expect nonfarm payroll growth to moderate this year and look for the Federal Reserve to cut interest rates 2 or 3 times this summer and fall.

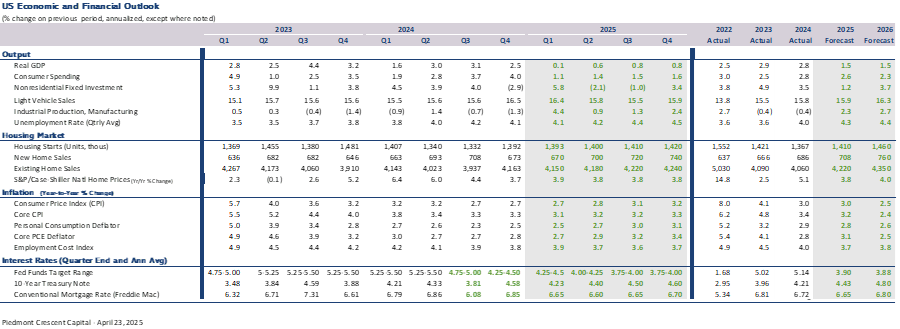

The implementation of larger-than-expected tariffs in 2025 has significantly altered the economic landscape, leading both the Federal Reserve and private forecasters to sharply revise downward their projections for U.S. economic growth. The tariffs, which are broader and more enduring than initially anticipated, are expected to disrupt both U.S. and global economic growth. The cumulative effect of all tariffs enacted in 2025 is projected to reduce U.S. real GDP growth by 1.5 percentage points in 2025 from what it otherwise would have been.

The moderation in growth is due to heightened uncertainty surrounding tariffs, which reduces hiring and business fixed investment, and slower real income growth, resulting from weaker job growth and higher prices. Moreover, the front-loading of imports ahead of tariffs will result in wide swings in real GDP growth, further fueling uncertainty and increasing the risk of a policy mistake. Following the pandemic, economic growth has shown a tendency to come below expectations during the first half of the year, including a decline in the first quarter of 2022 followed by a scant 0.3% rise the following quarter.

The latest wave of tariffs has pushed the average effective tariff rate to 22.5% — the highest since 1909 — amplifying price pressures on imported goods and adding fuel to broader inflation risks. The larger-than-expected scope of the tariffs triggered a front-loading of shipments ahead of implementation, driving up import prices and signaling further price increases in the pipeline. The inflationary impact is expected to weigh heavily on household budgets. The Yale Budget Lab estimates tariffs will cost U.S. consumers an average of $3,800 per household, with middle- and lower-income families bearing a disproportionate share of the burden.

Globally, escalating tariffs have triggered a wave of retaliatory measures, further deepening uncertainty around the economic outlook. China, for example, has raised its retaliatory tariffs on U.S. imports to as high as 125% and suspended exports of critical minerals and magnets — a move that threatens to further strain global supply chains. Several other trading partners have followed suit, either threatening or enacting countermeasures of their own, pushing the global economy closer to a broad-based trade war.

The International Monetary Fund highlighted the growing risks from prolonged trade tensions, estimating a universal 10% increase in U.S. tariffs — accompanied by full retaliation — could cut U.S. GDP by roughly 1% and global GDP by 0.5% through 2026. The IMF also warned that the indirect effects on business sentiment and investment could compound these losses, especially if tariffs remain in place or expand further.

Federal Reserve Chair Jerome Powell stated similar concerns, noting persistent trade policy uncertainty has become “a notable headwind” for both U.S. and global growth. Powell specifically flagged the disruption to supply chains and the rising cost of intermediate goods as critical channels through which tariffs are now impacting decision-making. His remarks echoed the findings of the First Quarter 2025 CFO Survey, which showed over 30% of firms citing trade and tariffs as their top concern, highlighting a growing fear that production costs will continue to climb, and strategic investment will be deferred as long as trade tensions remain unresolved.

.

The strained relationship between President Donald Trump and Federal Reserve Chair Jerome Powell has become an increasingly destabilizing force in the 2025 economic landscape. The feud has escalated well beyond a political drama to a real threat toward the Fed’s independence and credibility. With tariffs driving inflation higher and growth slowing, the widening gap between the White House’s push for rate cuts and the Fed’s cautious stance is adding to market uncertainty.

A core principle of monetary policy is to ensure price stability — famously defined by Alan Greenspan as an environment where inflation is no longer a factor in business decisions. Yet the Fed’s dual mandate also obliges it to support full employment, placing Powell in a difficult balancing act as tariff-driven price pressures mount.

Trump intensified his attacks on Powell, stating his “termination cannot come fast enough” and accusing the Fed of “playing politics” by not cutting rates. Powell has signaled no intention of stepping down before his term ends in May 2026, reaffirming the Fed’s commitment to price stability over politically expedient easing.

At the core of the standoff is a fundamental policy divide. Trump is seeking rate cuts to cushion the impact of his trade agenda, while Powell remains wary of repeating the Fed’s 2021–2022 misstep of underestimating inflation risks, particularly related to supply chain risks. Speaking in Chicago, Powell warned tariffs were “highly likely” to trigger at least a temporary inflation spike, with the potential for more persistent effects if costs pass-throughs proves stickier than expected.

Markets have started to price-in political risk. Betting platforms now place the odds of Powell leaving before year-end at roughly 25% — nearly double from a month ago — as investors recalibrate expectations for both Fed policy and the broader stability of U.S. economic governance.

Powell’s removal remains unlikely given the legal and institutional hurdles. Trump’s sharp rhetoric appears aimed less at undermining Fed independence and more at shifting blame should the economy slip into recession from the trade war. Even if Powell were replaced — with Kevin Warsh rumored as a frontrunner — markets expect little immediate change in policy. The broader risk, however, is clear: a more politicized Fed only deepens the challenges of navigating a fragile economy, where fiscal and monetary authorities are increasingly at odds and more likely to make a mistake. Such an environment would further fuel financial market volatility. Asset prices would fall given the higher perceived risks that would be present in the U.S. and global economies.

Financial markets responded harshly to the introduction of tariffs. Global equities tumbled in early April, with the S&P 500 falling nearly 5% on April 3 — its steepest single-day drop since June 2020 — and the Nasdaq sliding roughly 6%. Gold prices surged, Treasury yields initially dipped on risk-off flows, and the Chinese yuan sank to a seven-week low. Crude oil prices also retreated on fears of slowing global growth. Stock markets have since rebounded, after some tariffs were later delayed but bond yields have only fallen back modestly.

The absence of a traditional “flight to safety” following the early April tariff announcements has sharpened doubts about U.S. exceptionalism and the dollar’s role as the world’s reserve currency. Markets appear to be pricing in not only the immediate trade disruptions but also deeper structural risks — including shifting global production patterns and intensifying competition for capital — reminiscent of the environment that existed prior to to the late-1990s Asian Financial Crisis (1997) and Russia Debt default (1998) which led to the collapse of Long-Term Capital Management (LTCM) and a flight to safety to U.S. dollar assets. The influx of global savings drove U.S. interest rates down and fueled bubbles in tech stocks, housing, and other assets.

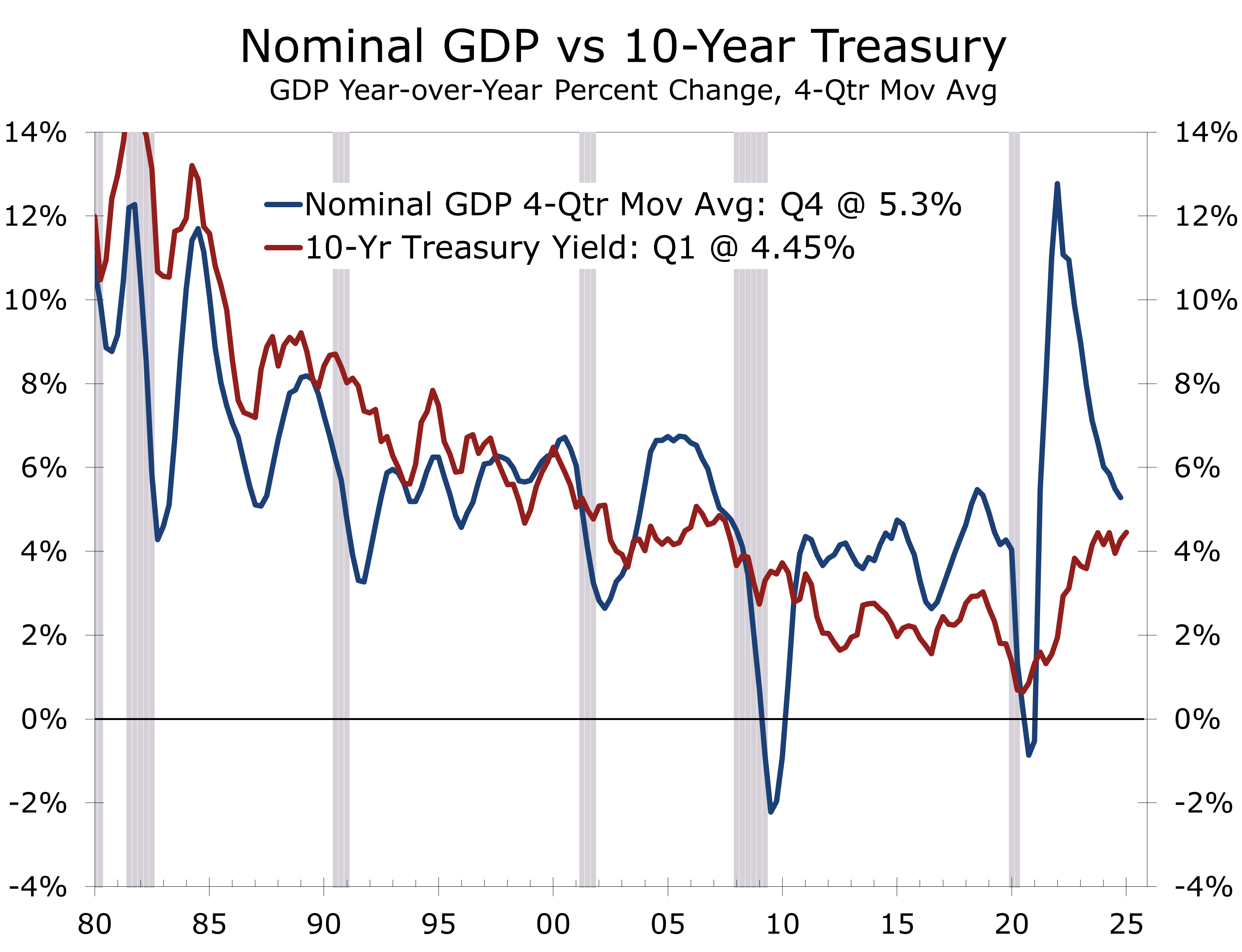

Today, a weaker dollar and rising Treasury yields suggest investors are bracing for lasting economic dislocations rather than a short-lived trade skirmish. Higher yields also reflect expectations of reduced foreign demand for Treasuries, as Trump’s tariff strategy aims to narrow the U.S. trade deficit, and capital reallocates toward emerging markets poised to absorb displaced production. Prior to the collapse of LTCM, the yield on the 10-Year Treasury Note consistently remained above nominal GDP growth – which would put it over 5.0% today.

Geopolitical tensions remain elevated, compounding concerns over U.S. leadership. Russia continues to exploit perceived U.S. foreign policy divisions, rejecting ceasefire overtures while regaining all Ukrainian-held territory in the Kursk region. Rising Ukrainian casualties and stalled diplomacy suggest Moscow is using negotiation talk to consolidate further gains.

In the Middle East, U.S. airstrikes on Houthi targets have escalated, yet Red Sea shipping disruptions persist. Meanwhile, Iran shows no signs of moderating its nuclear ambitions, raising the risk of broader regional conflict.

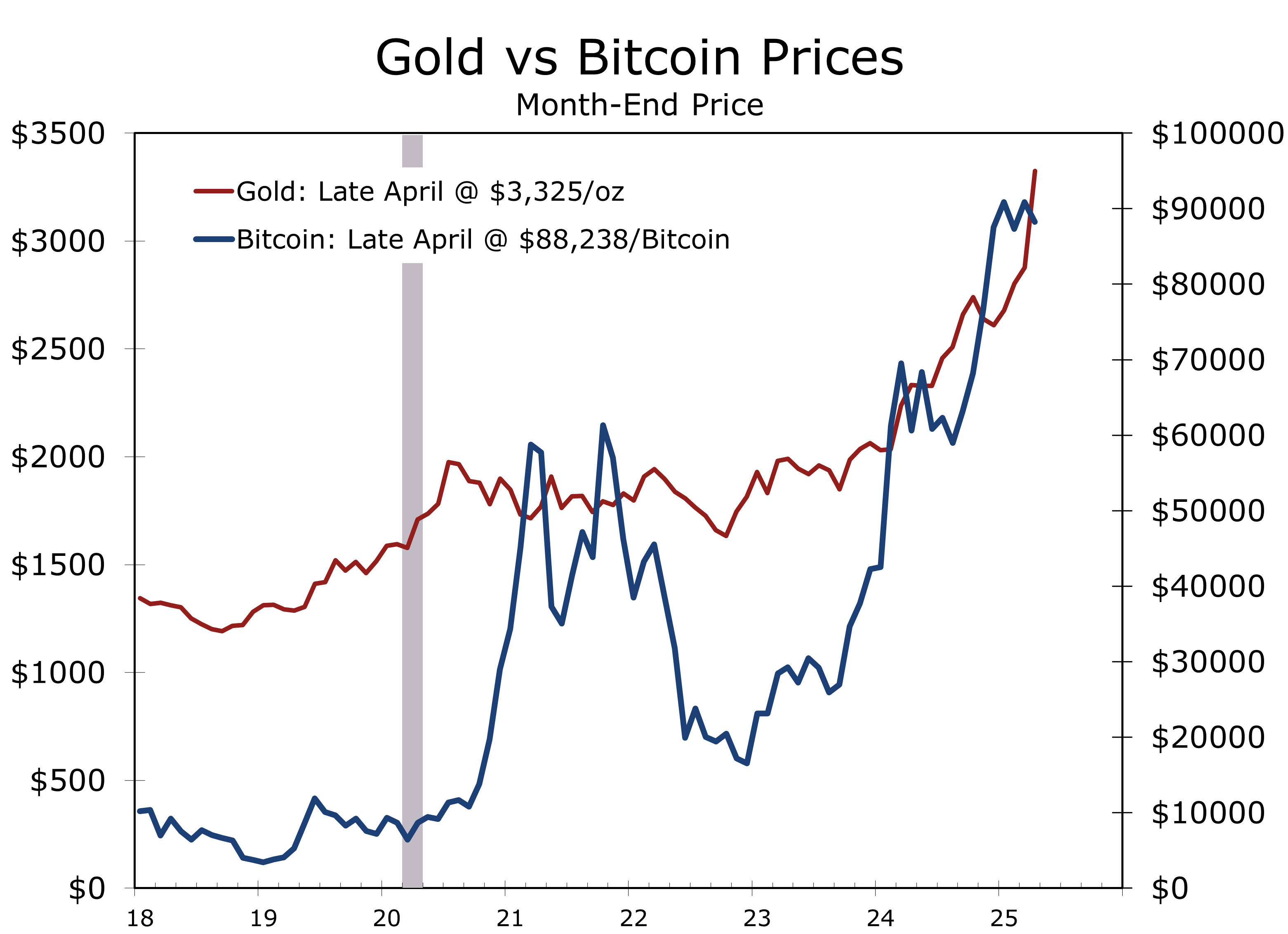

Economic and geopolitical stress points are converging in a rare and destabilizing fashion. While the U.S. dollar remains the global reserve currency by default, its primacy is being tested. Gold has emerged as a relative safe haven, outperforming Bitcoin and other crypto assets in the current crisis environment.

.

One of the clearest byproducts of tariff-driven uncertainty is the widening gap between soft and hard economic data. The divergence appears rooted in the Trump Administration’s shifting — and at times contradictory — tariff strategy. Multiple rounds of tariffs have been introduced, each with differing and sometimes overlapping objectives, leaving businesses and households to navigate an unusually opaque policy landscape.

Some tariffs have been explicitly framed as tools to curb the flow of illicit fentanyl, targeting specific chemical imports and manufacturers in China and Mexico. Others are aimed at what the administration describes as “unfair” trade practices, designed to shield U.S. manufacturers from subsidized foreign competition, particularly in heavy industry and advanced technology. A third category of tariffs appears driven by fiscal objectives — boosting government revenues to help finance a restructuring of the U.S. tax system.

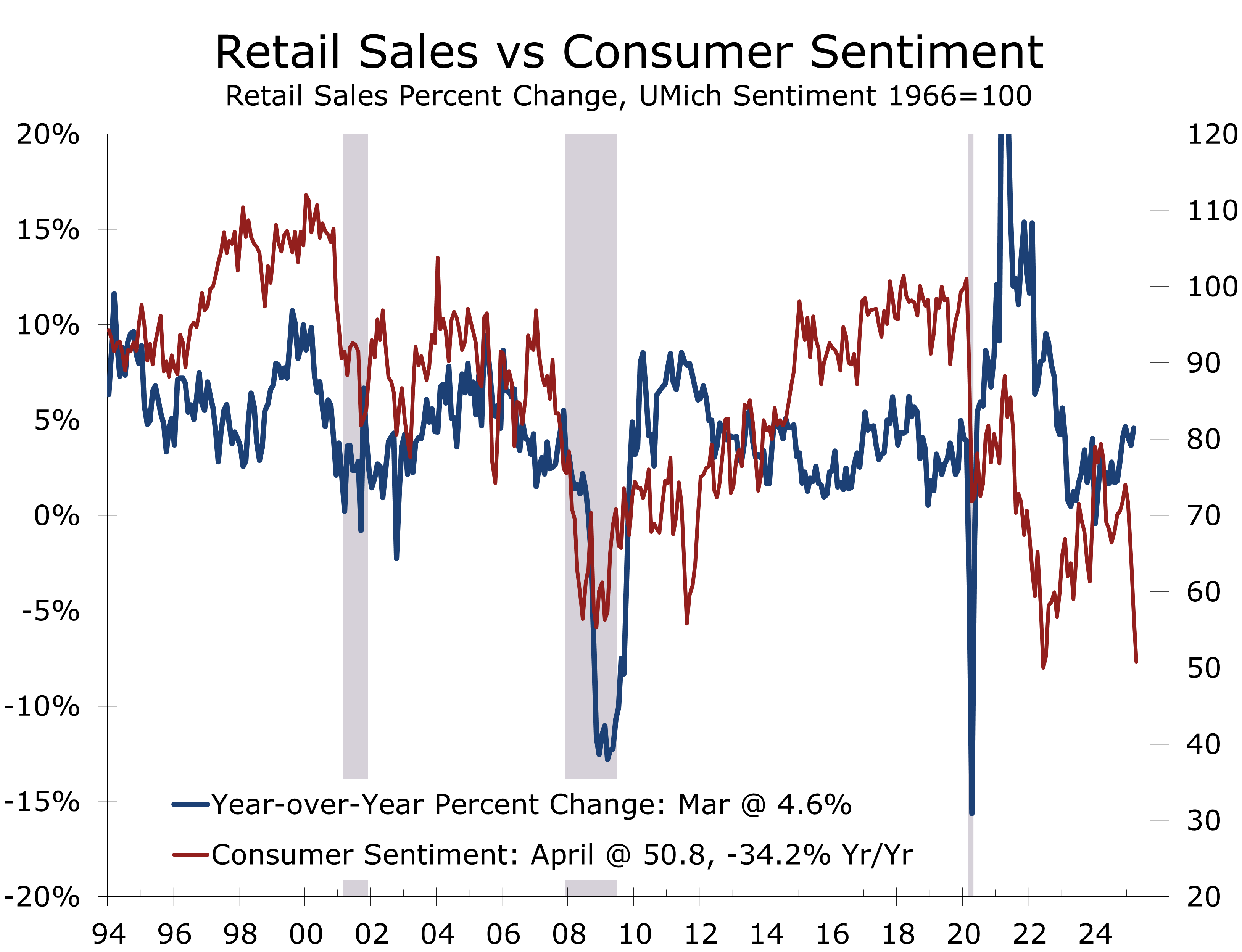

For markets, businesses, and consumers alike, the mix of motives — economic, geopolitical, and fiscal — makes it exceptionally difficult to discern which tariffs are intended as short-term negotiating levers and which are likely to become permanent fixtures of U.S. trade policy. One question repeatedly raised across boardrooms and trading desks is: “Where’s the off-ramp?” That uncertainty has weighed heavily on sentiment, forcing many firms to slow hiring, delay investment, and shift their focus toward short-term risk management — a dynamic reflected in the persistent weakness across business and consumer surveys, including the NFIB Small Business Optimism Index, ISM PMIs, and the Conference Board’s Consumer Confidence Index.

The tariff uncertainty is also distorting business activity in real time. Firms are stockpiling inventories ahead of scheduled tariff increases, diverting time and capital away from growth initiatives. Consumers, too, are adjusting their behavior, pulling forward big-ticket purchases — particularly for new and used vehicles and large appliances — on expectations that prices will climb once tariffs take effect.

Tariffs, and the threat of tariffs, are being used to meet multiple objectives and the process has been messy. Until it becomes clearer how much of the tariffs are a temporary bargaining tool and how much marks a permanent shift in U.S. trade policy, the gap between soft and hard economic data is likely to persist. Businesses are already pricing in this risk, even as consumers continue to spend. But the longer the uncertainty drags on, the greater the odds that caution will spill over into actual hiring, investment, and growth.

Trump’s aggressive tariffs have clouded the outlook, pushing inflation expectations higher while placing downward pressure on real income and business investment. While recession risks remain elevated, current labor market trends and resilient consumer spending suggest a narrow path to avoiding a full-blown contraction still exists. That path, however, hinges on a meaningful de-escalation of trade tensions. After teetering on the edge of a global trade war, recent developments suggest a tentative step back from the brink.

The bulk of the most recent hard data show the economy continuing to grow modestly. Consumer spending surprised to the upside in March, supported by lower gasoline prices and solid outlays on motor vehicles, furniture, and household appliances. In addition, the production and shipment of commercial and defense aircraft picked up, likely boosting Q1 equipment investment.

Despite this strength, Q1 real GDP growth is expected to be tepid, with most forecasts, including ours, hovering near zero, with risks stacked to the downside depending on how the Bureau of Economic Analysis (BEA) estimates data not yet available. At best, the economy appears to be skirting the edge of recession, and we expect that fragility to become increasingly visible in the employment and income data.

The ongoing public feud between President Trump and Federal Reserve Chair Jerome Powell may complicate efforts to ease rates, particularly in the lead-up to the summer. Nevertheless, we continue to expect a 25-basis-point rate cut in June. Labor market softening—likely to show up in claims and payrolls data ahead of the June 14 FOMC meeting—should provide the necessary pretext. Inflation is likely to remain elevated but broadly in line with expectations. The Fed has room to ease policy, and even three quarter-point cuts would leave the federal funds rate in restrictive territory relative to trend nominal GDP growth and neutral funds rate estimates.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

April 25, 2025

Mark Vitner, Chief Economist

704-458-4000