This essay expands on themes from the January 20, 2026 A View from the Piedmont. An earlier version, published last week, was inadvertently deleted.

Echoes of Jimmy Carter: Credit Controls Revisited

When affordability becomes a political flashpoint, the temptation to act visibly is powerful. High credit card interest rates are easy to see, easy to criticize, and easy to promise to cap. President Trump’s proposal to limit credit card APRs to 10% for one year fits squarely in that tradition.

The policy was announced on January 9 via Truth Social. The stated aim is straightforward: relieve consumers facing average credit card rates north of 20%. The mechanics, however, echo a policy experiment that ended badly and was abandoned just as quickly.

The closest historical parallel remains President Jimmy Carter’s 1980 credit controls. Those controls were not about affordability. They were explicitly designed to fight inflation by restricting consumer borrowing. The logic was simple. Less credit meant less spending. Less spending meant less inflation.

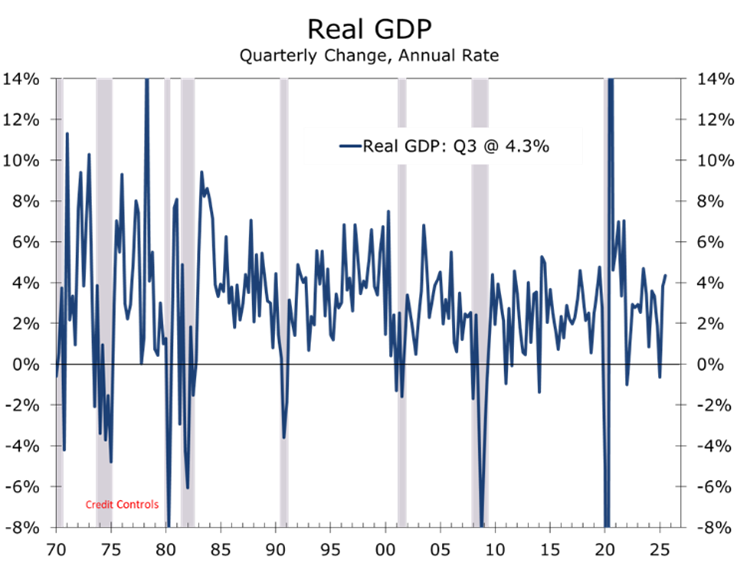

The outcome was equally simple and far more damaging. Credit availability collapsed almost overnight. Consumer spending retrenched sharply. The economy fell into a short but violent recession. Real GDP contracted at an 8% annual rate in the second quarter of 1980, a decline rivaled only by the worst quarters of the Global Financial Crisis and the COVID shock. Inflation, meanwhile, barely budged. That should not have surprised anyone. Inflation is a monetary phenomenon. It was not caused by credit cards and could not be cured by choking off consumer lending.

Trump’s proposal differs in motivation but not in transmission. Credit cards are unsecured, high-risk products. A 10% cap does not eliminate that risk. It forces lenders to ration credit instead of pricing it. Underwriting standards tighten. Credit limits shrink. Marginal borrowers are pushed out entirely.

1980 set the template: Credit controls collapsed lending first, spending second, and growth almost immediately. The policy was abandoned once the damage became undeniable.

Recent analyses reflect that tradeoff clearly. Estimates from former Consumer Financial Protection Bureau officials suggest consumers could save as much as $100 billion annually in interest costs. Those same analyses also conclude that access to credit would fall sharply for borrowers with fair or poor credit scores. Rewards programs would be curtailed or eliminated. Co-branded airline and retail cards would suffer. The headline savings come paired with a quieter contraction in credit availability.

Markets grasped that immediately. Bank stocks sold off sharply following the announcement. The Bank Policy Institute called the proposal “devastating” for families and small businesses, warning it would drive borrowers toward less regulated and more expensive alternatives such as payday lending. Capital One CEO Richard Fairbank was more blunt. Speaking on a January 22 earnings call, he warned that price controls would force banks to slash credit lines, restrict accounts, and limit new originations. In his words, banks do not lend at a loss. The result would be an engineered contraction in consumer credit with recessionary consequences.

The burden would fall where it always does. Lower-income households. Younger borrowers. Consumers who rely on revolving credit to smooth cash flow rather than finance discretionary excess. These groups have the highest marginal propensity to spend. Pulling credit here does not cool inflation at the margin. It pulls demand out at the core.

Credit rationing hits the economy’s pressure points: The borrowers most dependent on revolving credit also drive the highest marginal spending. When credit disappears, growth follows.

Implementation remains uncertain. Trump initially floated the idea as a voluntary gesture by banks. Advisors later encouraged congressional action. Kevin Hassett suggested lenders might offer voluntary “Trump Cards.” Banks have largely ignored the call. That response underscores the core problem. Credit price controls are easy to announce and hard to enforce without distorting the system.

This proposal fits a broader governing style. Bold ideas. Rapid testing. A willingness to experiment under pressure. It has drawn bipartisan curiosity, with nods from both Senator Sanders and Senator Hawley. But history suggests the same arc as before. Credit contracts. Spending falls. Political support erodes. The policy snaps back.

A higher cap, perhaps in the 15% to 18% range, would still compress excesses while allowing risk to be priced rather than rationed. That is where most expert modeling lands. A 10% ceiling, by contrast, revives a lesson from 1980 that the economy already learned the hard way.

Credit controls do not bend cycles. They break them.

.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 20, 2026

Mark Vitner, Chief Economist

Piedmont Crescent Capital