The Fed Looks Set to Lean into the Wind

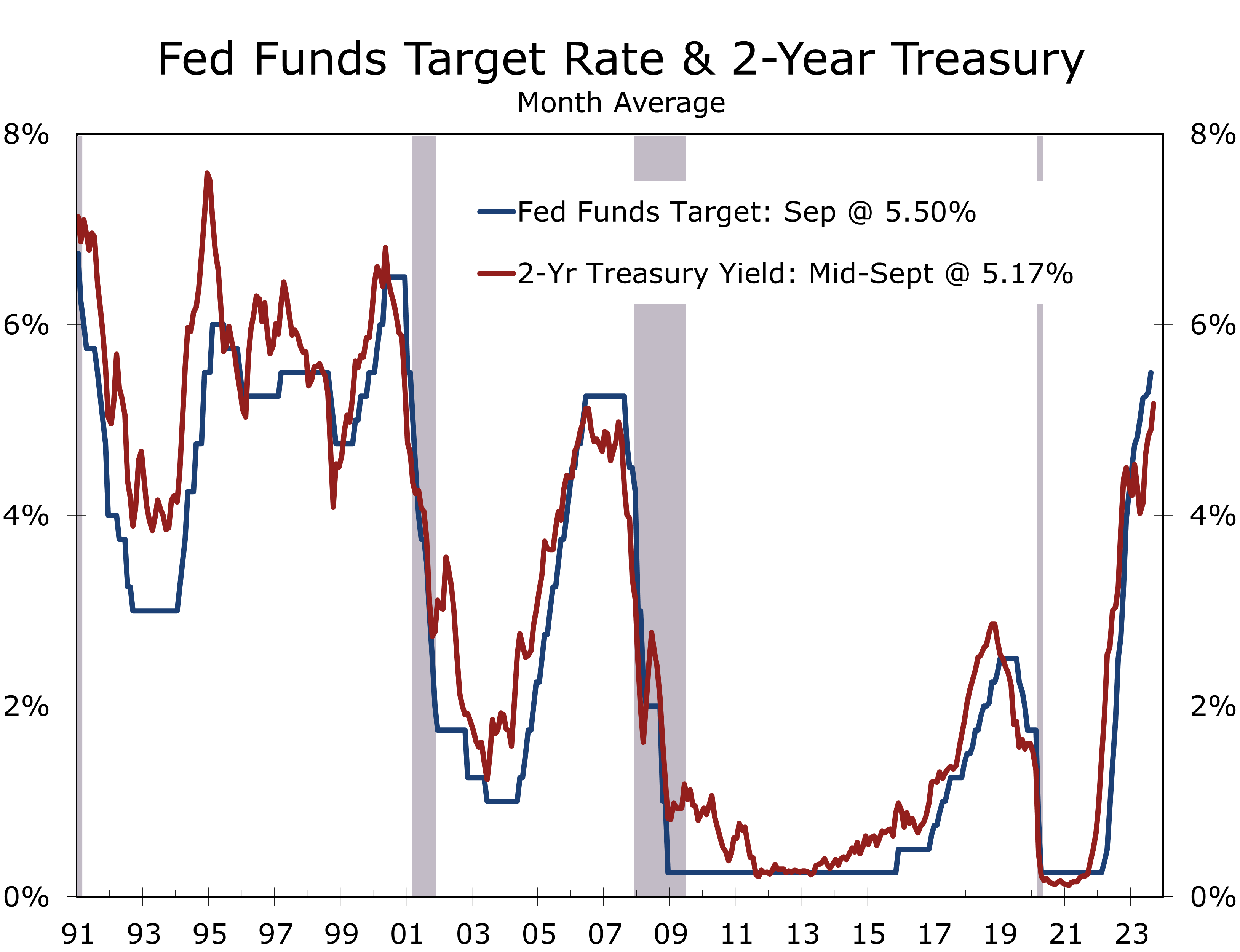

- The Federal Reserve left its federal funds rate target unchanged at 5.25-5.50%.

- The FOMC policy statement acknowledges moderating job growth but continues to emphasize inflation remains elevated.

- FOMC members are in a wait and see mode on growth and inflation but continue to lean toward hiking rates at least one more time.

- The Summary of Economic Projections now calls for 2.1% real GDP growth this year, up a full percentage point from their June.

- Powell’s press conference contained few surprises. He acknowledge household balance were stronger than initially thought, which contributed to the economy’s resilience.

- Powell stressed the Fed would proceed carefully, suggesting an awareness of the risk over overtightening.

- Bottom line: The Fed left the door open for an additional rate hike but also noted they would likely lower rates more slowly. We expect the Fed to lean into the wind as the economic growth slows and pressure builds to cut interest rates.

The FOMC left its target range for the federal funds rate unchanged at 5.25-5.50% at its September FOMC meeting. The overwhelming majority of market participants expected the Fed to remain on hold and the bulk of the interest today was whether there would be any changes to their policy statement and the updated Summary of Economic Projections (SEP).

Changes to the policy statement were minimal. The Fed’s assessment of economic activity was upgraded from ‘moderate’ in July to ‘solid’ today. The move makes sense, given the upgrade to the Fed’s real GDP forecast for 2023, which was raised to 2.1% from 1% in June. Real GDP is expected to rise 1.5% in 2024, up from 1.1% earlier, and grow 1.8% in both 2025 and 2026, which is close to the CBO’s estimate of potential GDP growth.

The Fed’s economic forecast now calls for a prolonged soft landing. Slower economic growth over the next year is expected to nudge the unemployment rate up from 3.8% this year to 4.1% in 2024 and 2025. That is slightly lower than the Fed projected in June and suggest FOMC members expect labor markets to remain tight over the forecast period.

A prolonged soft landing means interest rates will likely remain higher for longer.

A prolonged soft landing means interest rates will likely remain higher for longer. The SEP has the federal funds rate ending this year a quarter percentage point higher than it is currently. The biggest change is the FOMC now only sees a cumulative cut of half a percentage point in 2024, versus a full point cut earlier.

Despite maintaining an unemployment rate near the mid-point of the range of forecasts for ‘full employment’, core inflation is expected to be slightly lower this year and about the same as it was previously projected for 2024 and 2025. Core inflation is expected to return to 2.0 in 2026 and remain there over the long run.

The benign inflation environment combined with the higher projected path for the federal funds rate means the real federal funds rate (federal fund rate minus core PCE inflation) is half a percentage point higher for 2024 and 0.4 percentage points higher for 2005. Even in 2026, the real federal funds rates is 90 basis points, which is at the high end of rising estimates for the neutral federal funds rate.

Higher projections for the real federal funds rate suggest policy will remain tight well into 2025.

The higher projections for the real federal funds rate suggest monetary will remain tight well after the Fed begins to cut interest rates next year. This part of the Fed’s forecast is a nod to recent discussion suggesting the neutral federal funds rate has risen. The median forecast for the federal funds rate at the end of 2026 is 2.9%, which is well above the median estimate for the long-term federal funds rate, which was unchanged at 2.5%.

We expect estimates for the long-term federal funds rate to gradually edge higher to 2.9%. Seven of the 19 FOMC participants currently have projections above 2% and average forecast derived from longer-run federal funds rate dot-plot works out to 2.76%.

Taken together, the policy statement, Powell’s press conference and the Summary of Economic Projections make a compelling case that interest rates are likely to rise a bit higher than previously thought and remain for longer. We expect the Fed to cut rates begrudgingly, to bring inflation back down to their 2% target.

A prolonged soft landing means interest rates will likely remain higher for longer.

The Fed’s updated forecast might stem some of the criticism from congress that the Fed was pursuing a policy that would send the economy into recession. The environment the Fed now envisions is a near picture perfect soft landing. Whether an economy growing this modestly can successfully navigate the shocks from periodic government shutdowns, labor strikes and unforeseen geopolitical events is an open question but for now the Fed appears set on a credible course to a soft landing.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.