Inflation Surprises to the Downside in March

- The headline CPI fell 0.1% in March, driven by a sharp decline in energy prices (-2.4%) that more than offset a 0.4% rise in food prices. The core CPI rose 0.1%, which was also well below expectations.

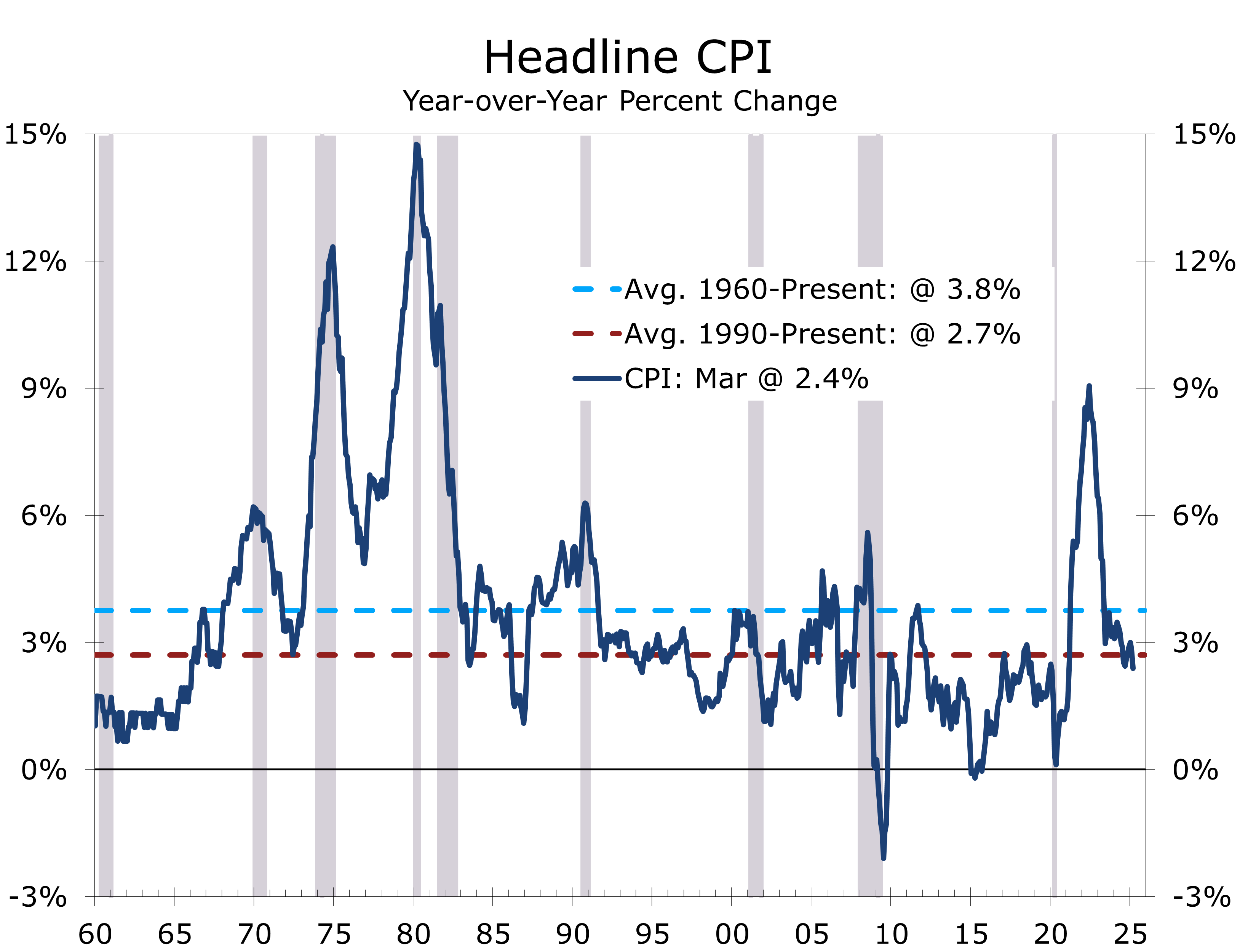

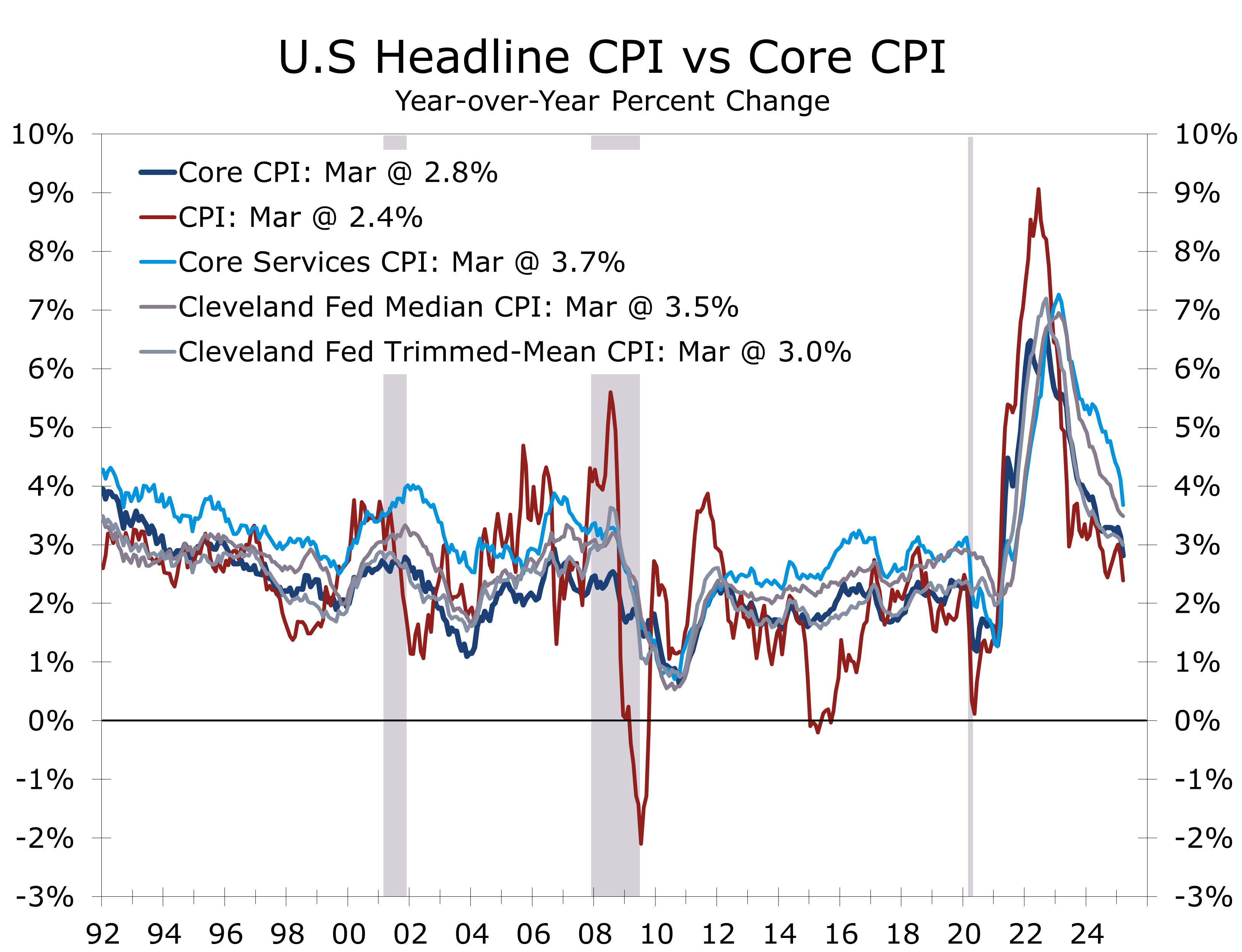

- Year-over-year headline CPI fell to 2.4%, its lowest since February 2021, while core CPI held at 2.8%, the smallest 12-month gain since March 2021.

- Travel-related costs (gasoline, airfares, lodging away from home) weakened, partly due to this year’s late Easter.

- Core goods prices remained flat in March and are down 0.6% year-to-year. Tariffs on Chinese imports are expected to reverse this trend; apparel (+0.4%) and furniture (+0.6% NSA) already may be feeling the impact.

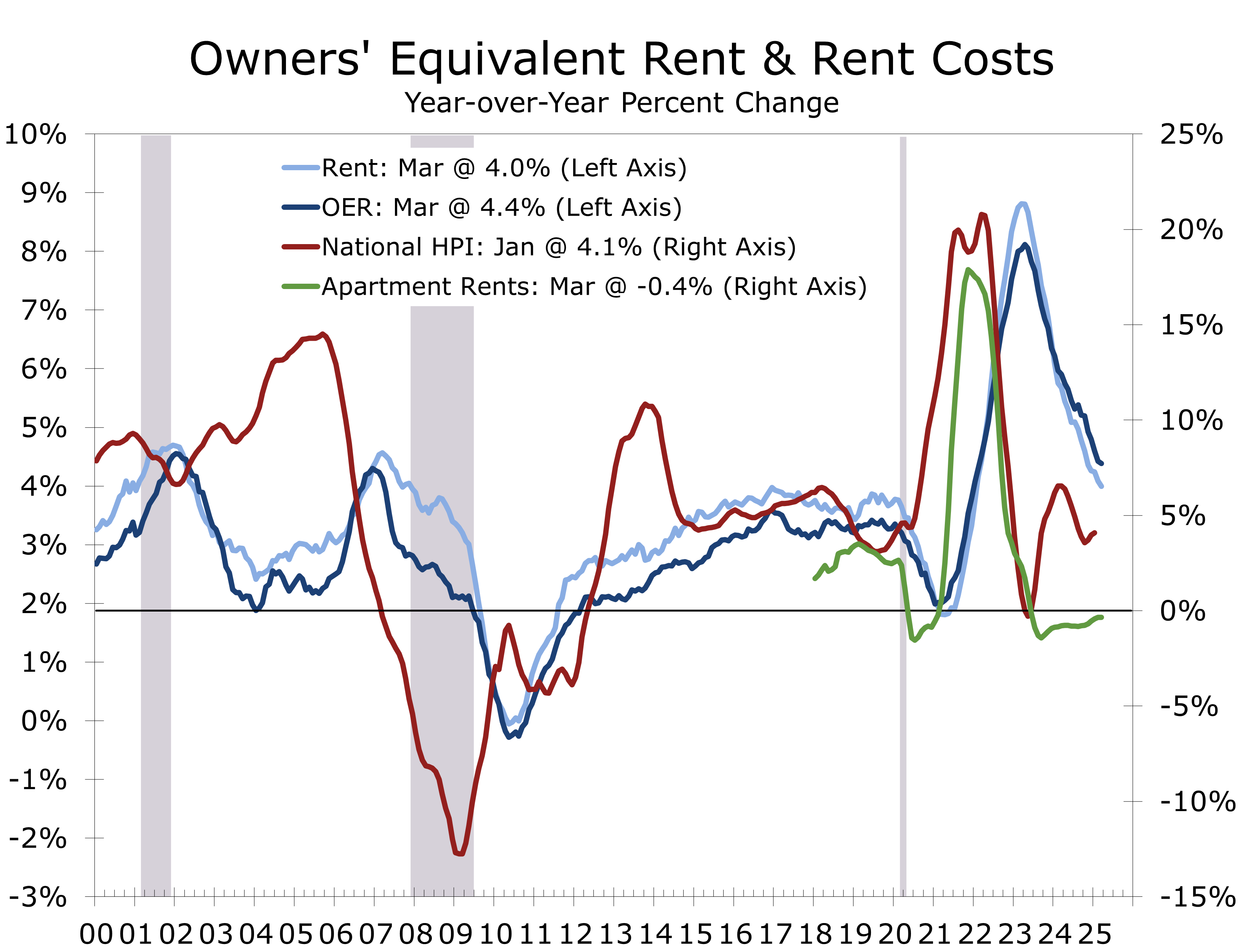

- Shelter costs increased, with rent up 0.3% and owners’ equivalent rent (OER) up 0.4%. Motor vehicle insurance fell 0.8%, a rare decline, though still up 7.5% year-over-year.

- Tariff concerns overshadowed a better-than-expected CPI report. Price pressures are cooling in core services and energy, which may help offset the sting of higher tariffs.

Concerns over the persistence of higher-than-expected tariffs—particularly with China—have overshadowed any relief from the better-than-expected March Consumer Price Index (CPI) report. Headline CPI fell 0.1% in March after rising 0.2% in February, defying expectations for a modest increase. The decline was largely driven by a 2.4% drop in energy prices, including a sharp 6.3% fall in gasoline.

Core CPI, which excludes food and energy, rose just 0.1%, down from 0.2% in February. This brought the year-over-year increase down to 2.8%, the smallest annual gain since March 2021. Meanwhile, headline CPI slowed to 2.4% year-over-year, the lowest reading since February 2021.

While the Fed continues to favor the core PCE deflator as its primary inflation gauge, the headline CPI is now well below its long-term average. Notably, much of the recent disinflation has come from core services—an area less susceptible to tariff-related pressures. Moreover, the recent slide in energy prices should help stem both the slide in consumer sentiment and rise in inflation expectations.

The year-to-year change in the headline CPI is now well below its long-run average.

The headline CPI is now running below its long-run average. Most alternative inflation measures show similar improvement, albeit from slightly higher levels.

Energy prices fell sharply in March, with gasoline tumbling 6.3%. Gasoline prices usually perk up in spring, as driving increases along with evening daylight and springtime travel. Easter comes exceptionally late this year, however, which has weighed on travel and driving. The effects extended to other travel-related categories. Airline fares declined 5.3% (following a 4.0% drop in February) and lodging costs fell 3.5%.

Partially offsetting lower energy prices, food prices rose 0.4%. Grocery prices increased 0.5%, led by a 5.9% spike in eggs and a 1.3% rise in meats, poultry, fish, and eggs. Restaurant prices rose 0.4%, with full-service meals up 0.6%. Over the past year, food prices rose 3.0%, with egg prices up 60.4%—continuing to strain household budgets, especially for middle- and lower-income families. Relief is in the pipeline, however, as wholesale egg prices have plummeted in recent weeks.

Inflation is easing across most measures and tariffs may not upend this as much as feared.

One of the more encouraging aspects of the inflation data has been the sharp slide in core services’ prices. The improvement is backed up by the continued deceleration in both the Median and Trimmed-Mean CPI, which exclude many of the more volatile components, like used cars, that exaggerated the swings in both the headline and core CPI.

Residential rent and owners’ equivalent rent have been key contributors to the recent moderation in core inflation. Shelter costs rose just 0.2% in March, with owners’ equivalent rent up 0.4% and rent up 0.3%. Lodging costs fell 3.5%. Over the past year, residential rent growth has slowed by 1.7 percentage points to 4.0%, down 4.1 points from its peak two years ago. Owners’ equivalent rent has decelerated by 1.5 points to 4.4%, down 3.7 points from its April 2023 high.

Market-based measures of apartment rents, home prices, and single-family rents have slowed even more than the Bureau of Labor Statistics’ official housing cost data. As official figures catch up with market trends, residential rent and owners’ equivalent rent are likely to continue easing into 2025. Given housing’s outsized weight in both the economy and inflation metrics, this moderation should help cushion some of the impact from higher tariffs.

We raised our 2025 inflation forecast in response to the rollout of significantly larger-than-expected tariffs. We now project headline CPI to rise 3.4% and core CPI to increase 3.5%. Tariffs apply to the dutiable value of imported goods—typically tied to production costs and represent a relatively small share of retail prices.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

April 10, 2025

Mark Vitner, Chief Economist

Piedmont Crescent Capital

(704) 458-4000