Downward Revisions Soften a Soft May Report

- Nonfarm payrolls rose by 139,000 in May, a soft print made softer by 95,000 in downward revisions to March and April.

- Unemployment held steady at 4.2%, but the employment-population ratio fell to 59.7%, the lowest in eight months.

- Labor force participation declined to 62.4%, with household survey data showing subtle but broad-based weakness.

- Health care (+62,000) and leisure & hospitality (+48,000) led job creation; federal payrolls shrank by 22,000.

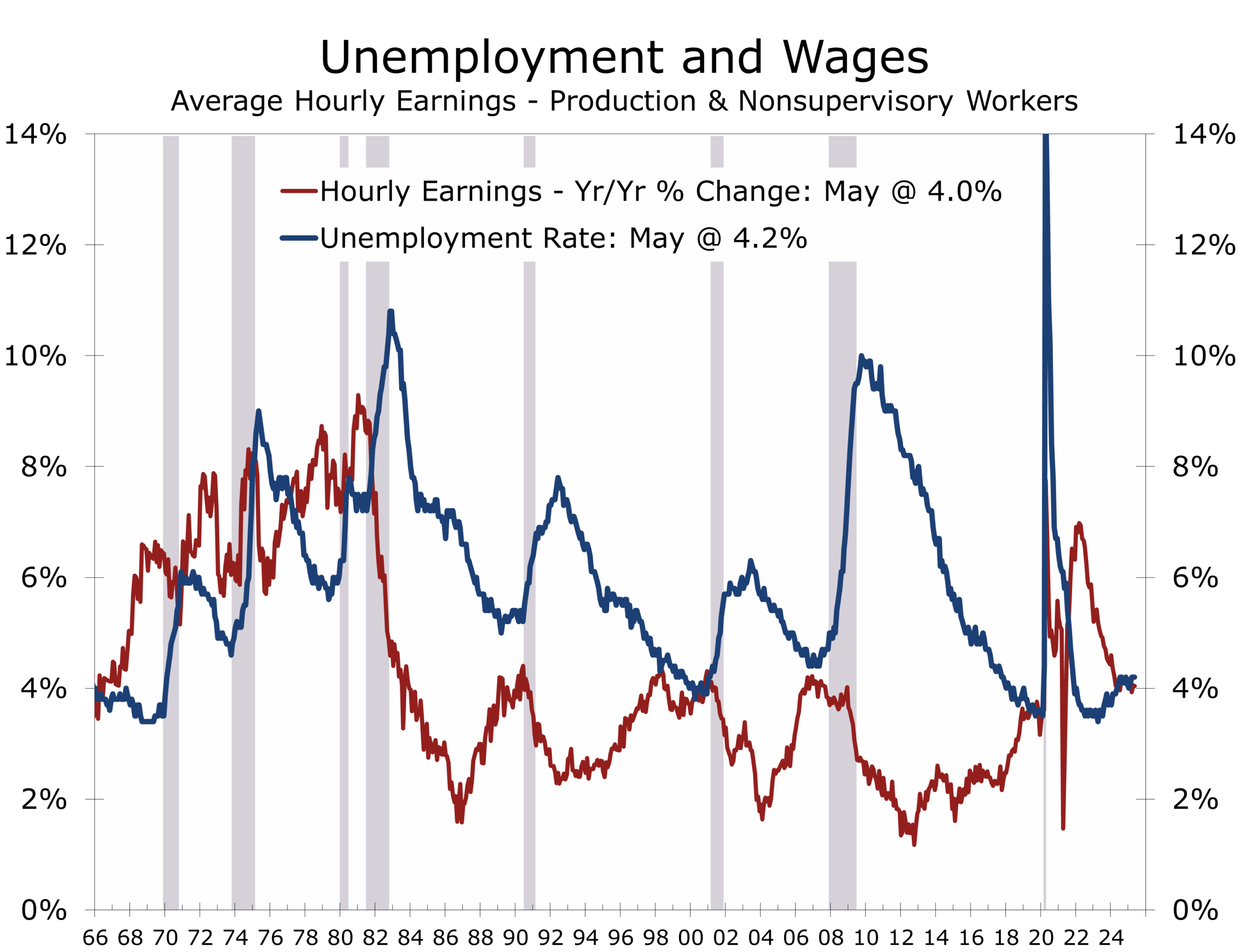

- Average hourly earnings rose 0.4%, lifting the year-over-year pace to 9%, slightly above April’s 3.8%.

- The workweek remained unchanged at 34.3 hours, with manufacturing overtime stable at 2.9 hours. Aggregate hours rose slightly.

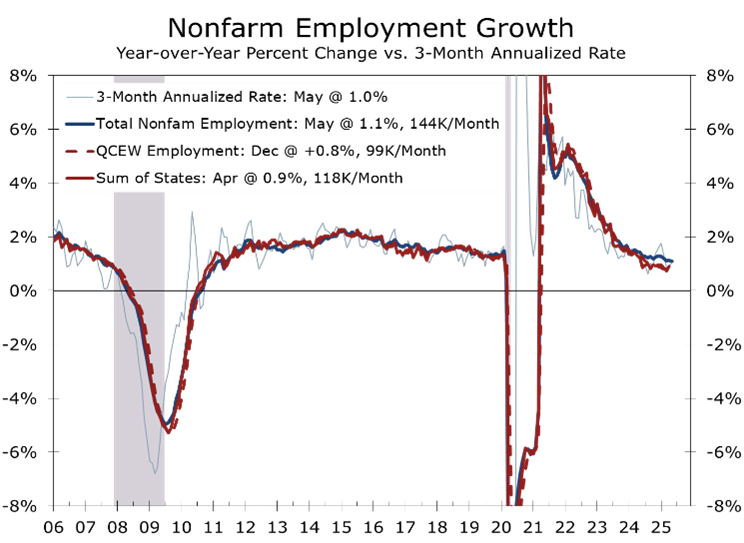

- The labor market continues to lose altitude quietly but steadily. Nonfarm payrolls have grown at a 135,000 monthly pace over the past three months—well below the 12MMA of 149,000. Moreover, the latest QCEW data suggest job growth may be overstated by as much as 558K positions, reinforcing concerns that recent momentum is weaker than it appears.

Softening Beneath the Surface

The May jobs report paints a mixed picture of the labor market. Nonfarm payrolls rose a moderate 139,000—just below the 12-month average of 149,000—but the signal softened considerably after downward revisions of 95,000 to March and April. The three-month average has now slipped to just 135,000. While the unemployment rate held at 4.2%, that stability masks a 0.2-point decline in labor force participation and a 0.3-point drop in the employment-population ratio—early signs slack is quietly accumulating.

The underlying trend of job growth is likely slower than recent data suggest.

The underlying trend is likely weaker than headline data suggest. Job gains remained narrowly concentrated in health care (+62,000), leisure and hospitality (+48,000), and social assistance (+16,000). Health hiring was led by hospitals (+30,000) and ambulatory services (+29,000), while restaurants and bars added 30,000 jobs. Federal government payrolls, however, fell by another 22,000 in May and are down 59,000 year to date—continuing a clear policy-driven unwind centered in Washington.

The recent trend may also be overstated. Newly released QCEW data for Q4 2024 show payrolls grew just 0.88% last year—roughly 0.35 percentage points, or 558,000 jobs, below current estimates. Preliminary state payroll data for Q1 2025 echo this pattern, pointing to further downside revisions.

Job gains are becoming less broad-based, a sign consistent with a decelerating labor market. The payroll diffusion index for private-sector employment fell 1.8 points to 50.0, while the manufacturing diffusion index dropped 2.7 points to 41.7. This narrowing breadth reflects the disproportionate impact of tariffs and elevated interest rates. Retailers cut 6,500 jobs in May after losing 2,700 in April, as they continue to seek efficiencies to avoid passing the full cost of tariffs on to consumers. Meanwhile, temporary staffing firms shed 20,700 jobs, likely reflecting pressure on margins and increased caution.

Tariffs and higher interest rates are clearly weighing on job growth.Top of Form

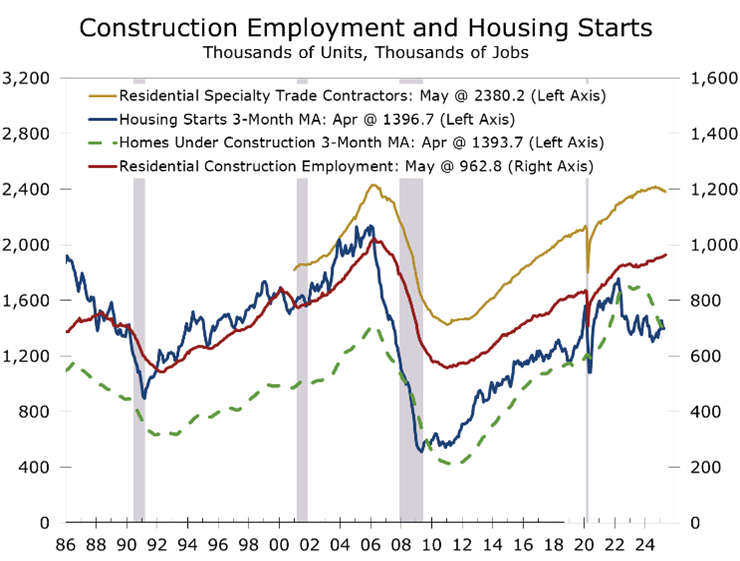

Elsewhere, job growth was notably absent. Construction, manufacturing, transportation, professional and business services, and financial activities all saw little or no change. Higher interest rates continue to weigh on home sales and mortgage activity. Homebuilding is also showing signs of strain, with residential specialty contractors cutting 11,000 jobs in May. We expect further reductions in the second half of the year as both single-family and multifamily starts continue to slide.

Wages rose more briskly in May. Average hourly earnings increased 0.4% to $36.24, lifting the year-over-year gain to 3.9%—a modest acceleration that may catch the Fed’s attention if it persists.

The unemployment rate was unchanged at 4.2% but the household survey still raised some red flags. The labor force participation rate fell 0.2 points to 62.4%, and the employment-population ratio slipped to 59.7%. The number of people unemployed for less than five weeks rose by 264,000, while long-term unemployment declined—possibly due to labor force exits. Part-time for economic reasons remained elevated at 4.6 million, and discouraged workers hovered at 381,000. Household employment adjusted to a nonfarm basis fell an outsized 762,000 in May, widening the gap between the two series.

The household data were than the headlines suggest, with most key metrics weakening.

The May jobs data reinforce the Fed’s recent stance—patience over panic. While wage pressures picked up, the broader slowdown in job growth and accumulation of slack indicators provide ample justification for holding rates steady and also support the market’s recent tilt toward earlier rate cuts. The downward revisions are especially significant, and call into question the labor market’s underlying strength. While a soft landing remains likely, the economy’s ability to weather a shock is considerably limited.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

June 6, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000