A Narrow Path to a Soft Landing

- While inflation has firmed slightly, tariff passthrough has been less than feared. Meanwhile, higher interest rates are exacting a heavier toll on the real economy—dragging down homebuilding, commercial construction, and big-ticket consumer spending. The labor market is also softening beneath the surface. Despite a low unemployment rate and subdued weekly claims, stress is mounting. Tighter immigration enforcement and accelerating Baby Boomer retirements may be masking deeper labor market slack.

- Trade policy volatility remains elevated, with proposed baseline tariff hikes, sector-specific duties, and the threat of secondary sanctions on Russia impacting a wide range of countries. New trade deals continue to trickle in, with Indonesia the latest to strike an agreement. President Trump has reaffirmed the August 1 deadline for reciprocal tariffs, though he also hinted at flexibility for nations actively negotiating. The endgame appears to mirror the Vietnam and Indonesia deals: a 20% base tariff, and a higher 40% rate on Chinese goods transshipped through those countries.

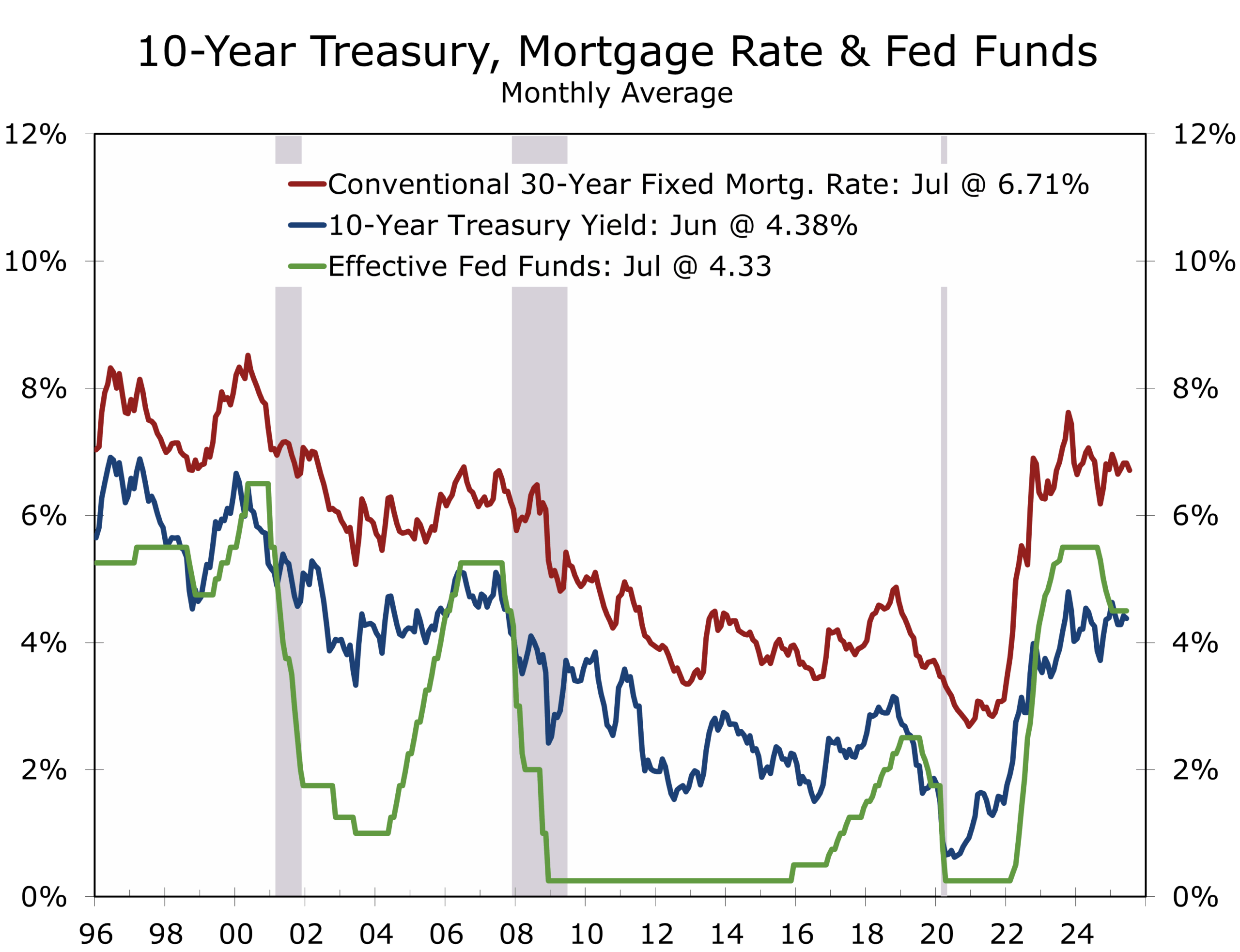

- Home sales and new construction have slowed to a crawl as affordability concerns and higher interest rates push buyers to the sidelines. Construction employment has held up for now, supported by a large backlog of projects. But inventories are rising, pressuring prices. Existing home prices are rising more slowly—and declining outright in a growing number of markets.

- Fiscal dominance concerns are rising as growing debt burdens collide with monetary policy decisions, renewing questions about Fed independence. Some degree of coordination between the Treasury and the Fed now appears inevitable. We do not expect President Trump to fire Chair Powell—it would likely prove counterproductive to his own economic objectives.

- Geopolitical risk is rising again, with the Russia–Ukraine conflict escalating and the Middle East remaining a persistent flashpoint. Both theaters carry the potential to disrupt global trade, energy markets, and investor confidence.

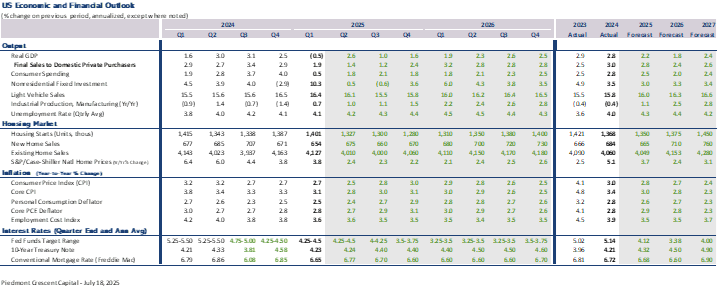

- After wide swings in Q1 and Q2—driven by tariff front-running, inventory volatility, and erratic consumer spending—we expect the economy to stabilize in the second half of the year. Disinflationary trends remain intact, and the labor market is cooling beneath the surface. Barring a major geopolitical or financial shock, we anticipate the Federal Reserve will begin a gradual easing cycle, with 25-basis-point cuts at the September, October, and December FOMC meetings. Fed officials are increasingly signaling readiness to pivot as inflation expectations anchor and downside risks to growth accumulate. The rate path beyond December remains data-dependent, but we expect the Fed to maintain a dovish bias heading into 2026.

Trade & Tariffs: Delay, Double Down, Distort

The next wave of tariffs has been delayed until August 1, but the structure is largely set. A 10% global baseline anchors U.S. trade policy, layered with 20% to 60% sector-specific duties on Chinese goods—targeting critical minerals, semiconductors, EV components, and medical supplies. The regime will cover nearly $2 trillion in annual imports.

Washington is leaning hard into tariff-first diplomacy—using trade barriers to accelerate reshoring, pressure adversaries, and rewire global supply chains. Inflation impacts remain modest. We estimate only 20% of tariff costs have been passed to consumers, with the rest absorbed via margin compression, efficiency gains, and supplier concessions. Durable goods have seen more pricing pressure; commoditized goods less so.

That cushion is unlikely to hold. As tariffs become a permanent feature of trade policy, passthrough will rise. Transshipping restrictions are tightening, targeting Chinese goods routed through third countries like Vietnam and Indonesia, where blended tariff rates now approach 40%. Compliance is no longer optional.

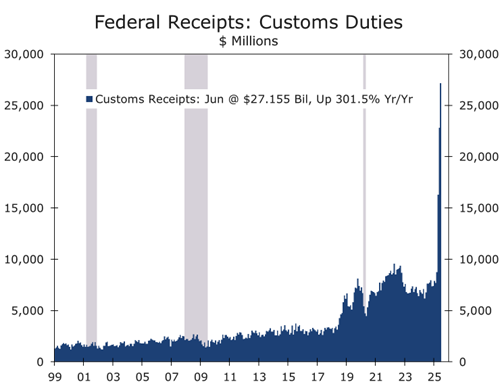

Tariff revenues are surging, providing Treasury with a growing source of funding. Collections have reached their highest level since the original China tariffs in 2018 and are poised to rise further as enforcement expands. While tariffs won’t erase the deficit, they will meaningfully offset shortfalls from the recently enacted budget deal—which notably excluded tariff revenues from its projections.

The Indonesia deal exemplifies this new model: a 19% base tariff with partial relief tied to mineral quotas and investment thresholds. The earlier Vietnam agreement, with its 17% floor and more lenient terms, now looks like an outlier. The message is clear: tariff relief must be earned, not assumed.

While some foreign policy experts remain puzzled by Trump’s trade strategy, we view it as the next evolution of globalization—an explicit response to China’s rise as an economic competitor and geopolitical threat.

Meanwhile, secondary sanctions on countries continuing trade with Russia—including India, Brazil, and parts of Europe—remain under active consideration, threatening to upend global sourcing and raise compliance costs.

Bottom line: Tariff volatility is no longer background noise—it is policy. The delayed inflation impact will not last. Slower trade, higher costs, and deeper fragmentation are reshaping business strategy and narrowing the Fed’s margin for maneuver.

Labor Market: A Shaky Foundation

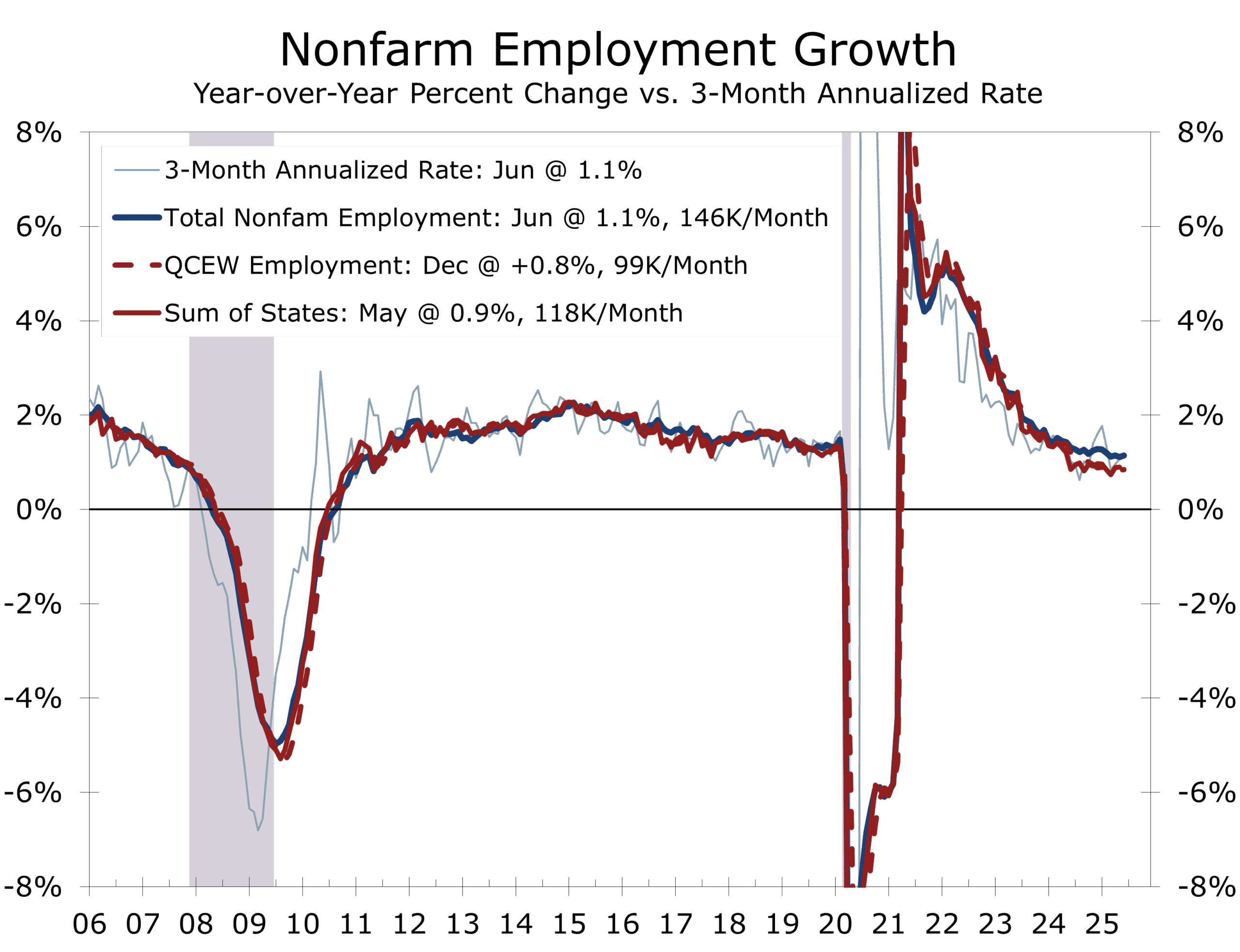

The U.S. labor market remains caught in a slow-motion deceleration. Employers added just 150,000 jobs a month over the past 3 months, down from 168,000 a month in 2024 and 220,000 jobs a month in 2023. Not only has hiring slowed but it is also much more narrowly based. Health care, leisure and hospitality, and state and local government have accounted for the bulk of job gains this past year, and there is growing evidence that these gains have been overstated.

We have long warned that the monthly nonfarm payroll series is overstating job growth, and recent data continue to support that assessment. The Quarterly Census of Employment and Wages (QCEW)—which underpins the BLS’s annual benchmark revisions—and state employment data, which integrate those figures more quickly, both suggest that job gains have been overstated by as much as one-third. These more comprehensive datasets, drawn from actual UI tax filings, point to a labor market that is far weaker beneath the surface than the monthly headlines imply.

The latest ADP private payrolls report, which posted its first decline in several months, offers additional confirmation. While official payroll data show private-sector job gains of 1.8 million over the past year, nearly half of that—878,000 jobs—comes from education and health care. Yet ADP data show that the same sectors accounted for just 13% of its measured payroll gains. This glaring discrepancy underscores how concentrated—and potentially overstated—hiring has become.

The divergence between headline strength and underlying softness is also evident in the unemployment claims data. Initial claims remain relatively low, but continuing claims have climbed to post-pandemic highs, indicating that displaced workers are struggling to find new jobs. The labor market is transitioning from one defined by robust churn to one marked by stagnation—less hiring, less firing, and fewer opportunities for job seekers.

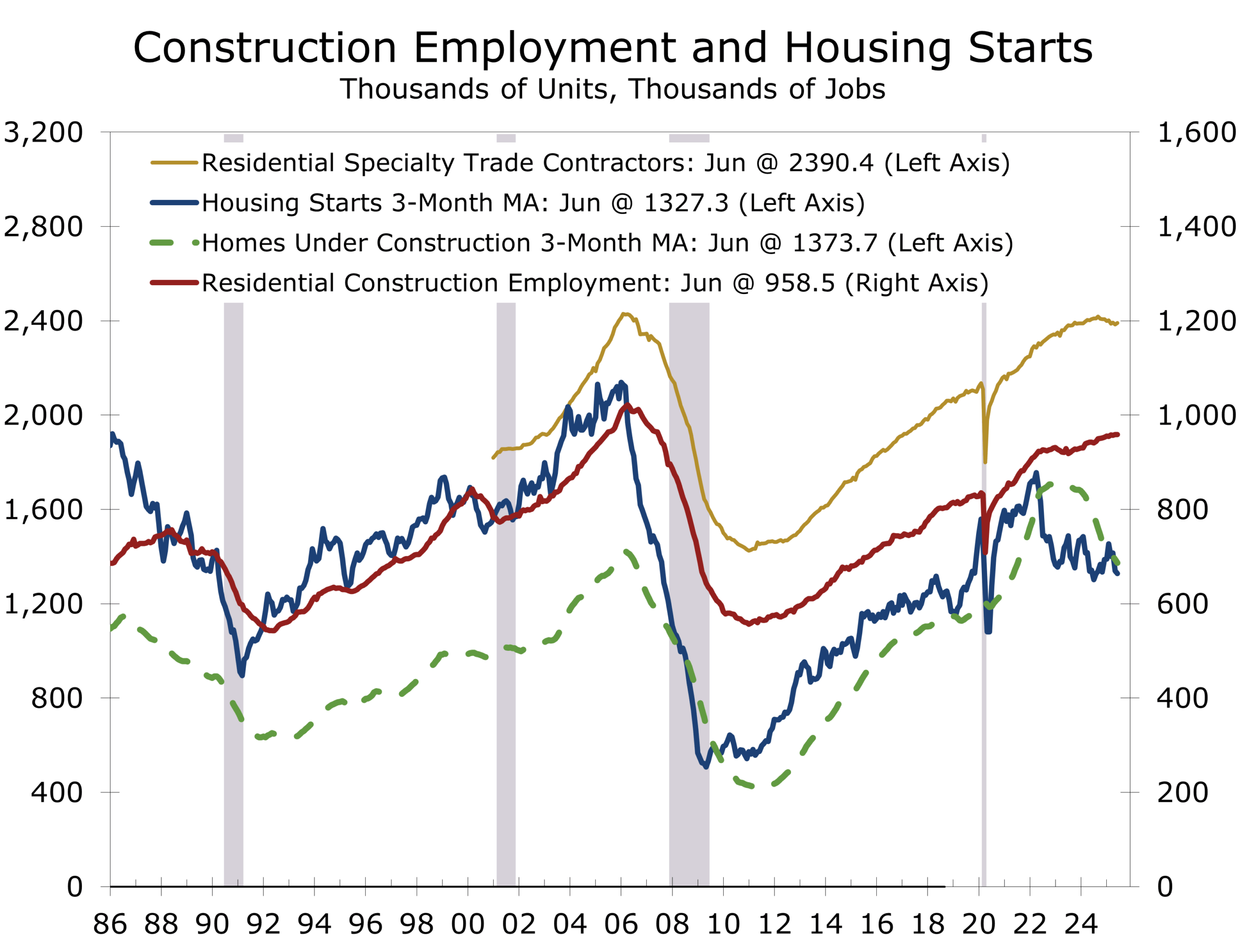

We believe the labor market is on the verge of a more pronounced downshift and that the FOMC would do well to heed the warnings recently made by Kevin Warsh and Fed Governor Waller. Key sectors that fueled the post-COVID recovery—warehousing, e-commerce, and residential construction—are now paring headcount. The lagged effects of tighter monetary policy and front-loaded hiring are beginning to show in other areas, including construction and consumer spending on big-ticket items. The pull-forward in demand from tariff-related inventory building and a massive construction backlog have masked much of the weakness. But those tailwinds are fading, and with them, the scaffolding supporting labor demand.

Labor force participation has plateaued, while demographic trends—particularly the retirement of baby boomers—and more stringent immigration enforcement are muting labor supply. These shifts help suppress the unemployment rate, giving a false sense of resilience even as underlying slack builds across the economy.

Housing Outlook: The Inventory Illusion Meets the Vanishing Dream

The U.S. housing market is increasingly defined by contradiction. Existing home supply remains tight, as owners cling to ultra-low mortgage rates secured during the pandemic. Meanwhile, inventories of unsold new homes are rising, especially in high-growth markets like Texas, Florida, and the Carolinas—where 7%+ mortgage rates are eroding demand.

The divergence between new and existing homes is distorting market signals. Builder incentives are widespread: 62% offered concessions in July, and 38% cut prices—the highest share since tracking began in 2022. Absorption remains weak. Builder sentiment edged up following passage of the One Big Beautiful Bill Act, which aims to ease regulatory hurdles and support affordable housing. But the NAHB/Wells Fargo Index remains deeply negative at 33—its 15th straight month below neutral.

As backlogs clear and permits decline, housing starts—particularly single-family—are expected to fall in H2 2025. Labor demand is already softening, especially in markets tied to new construction. The shift may ease shelter inflation in CPI and PCE data but won’t resolve the broader affordability crisis. Most new supply still targets mid-tier and upscale buyers, leaving few options for first-time homeowners.

That dream is slipping further out of reach. First-time homebuyers fell to just over 1.1 million in 2024, the lowest since NAR began tracking in 1989. The average age of a first-time buyer is now 38, up from the late 20s in the 1980s—delaying wealth accumulation, retirement, and financial security.

Affordability metrics tell the story. The median price of a single-family home hit $427,800 in May, up from $357,100 in 2021. Buyers now need to earn $126,700 annually, up from $79,300 just three years ago. Mortgage rates remain double their 2020 lows, while real incomes lag. Even stable prices can’t offset these financing costs.

Renting has become the default. John Burns Research reports that entry-level homes now cost double the price of renting, a gap last seen in 2006. That spread is freezing mobility and inventory alike.

Homeownership remains a core aspiration, but for millions—especially younger Americans—it’s becoming a distant hope. Without a shift in policy, financing, and land use, the housing ladder may remain out of reach—and the fallout could extend well beyond the housing market.

Geopolitical Risk: Ukraine Escalates, Syria Ignites

Geopolitical tensions are intensifying on two fronts—Eastern Europe and the Middle East—adding complexity to an already fragile global backdrop. A more aggressive Russian offensive and an unexpected Israel–Syria flare-up threatens to derail ceasefires, rewire trade alignments, and disrupt capital flows.

Russia has ramped up its summer offensive with deeper drone and missile strikes on Kyiv and Kharkiv. The Kremlin is betting on fading Western support. In response, President Trump reaffirmed U.S. backing for Ukrainian sovereignty while threatening secondary tariffs on nations trading with Russia. This would mark a major policy shift and could force countries like India, Brazil, and Turkey to rethink ties with Moscow.

Markets have yet to fully price in the threat. Strategic decoupling is accelerating, with “friend-shoring” replacing global integration as the dominant model.

While Gaza ceasefire talks grind on, Israel’s northern border with Syria has erupted. After attacks on Syria’s Druze minority, hundreds of Israeli Druze crossed into Syria to defend family members. Israel responded with precision strikes on Syrian Army positions, killing at least 350 and reactivating a once-dormant front.

The intervention—officially humanitarian but strategically aimed at Iranian militias—complicates Israeli politics and undermines prospects for a Syria-Israel agreement. Netanyahu’s coalition has lost its majority, with early elections in 2026 increasingly likely.

Meanwhile, Houthi missile strikes from Yemen continue to target southern Israel, widening the conflict and highlighting Iran’s proxy reach.

Markets are underpricing escalation risk. In Ukraine, secondary sanctions could redraw trade lanes and rekindle energy price volatility. In the Middle East, a hot Syria front likely puts the brakes any chance of normalization with Israel under the Abraham Accords. For the U.S., this means deeper reengagement in global security and more pressure on fiscal policy. For the Fed, geopolitical risk raises inflation tail.

Investors should brace for volatility. These simultaneous flashpoints are not isolated—they are pressure points in a rapidly shifting global order.

Between the Fed and a Fiscal Place

Fiscal dominance—where high government debt constrains central bank policy, effectively forcing interest rates lower to manage borrowing costs—is no longer theoretical. It’s shaping monetary and fiscal decisions in real time. Elevated long-term yields are pressuring both Treasury and the Fed to act—balancing funding needs against credibility and independence.

At Treasury, yield curve control is quietly returning in softer form. While formal caps remain unlikely, issuance is tilting toward shorter maturities, buybacks are expanding, and long-end debt is being selectively absorbed during market stress. The goal: shape the curve without triggering alarm. With net issuance climbing and foreign demand retreating, crowding out is no longer a risk—it’s a present reality.

The Fed’s bind is subtler but increasingly urgent. Governor Christopher Waller became the first senior Fed official to back a July rate cut, citing disinflation in core services and mounting labor market slack. He argued that acting now would support a soft landing without undermining credibility—framing the move as data-driven, not political. Governor Adriana Kugler echoed similar concerns, warning that delay could create asymmetric risks—overcorrecting on inflation while ignoring real economic strain.

Former Governor Kevin Warsh, a possible successor to Chair Powell, added institutional context with a call for a new Fed–Treasury accord modeled on the 1951 Agreement. His aim: shrink the Fed’s $6.7 trillion balance sheet and restore monetary autonomy through coordination with the Treasury. Warsh floated a hybrid strategy—pairing rate cuts with accelerated asset runoff—to balance near-term easing with long-term fiscal discipline. His proposal highlights how rising debt and political volatility are narrowing the Fed’s policy space.

Politics are muddying the waters. Trump’s handwritten accusation that Powell is “costing the USA a fortune” has put monetary policy on the campaign trail. Yet delay risks deepening the downturn, while action risks appearing compromised. The Fed is walking a narrowing tightrope, with stakes rising weekly.

Liquidity risks are resurfacing too. Standing repo facilities and broader collateral eligibility are back on the table as buffers against tariff shocks or geopolitical jolts to Treasury markets. Coordinated, clearly signaled action may be the only way to steady yields and preserve room to maneuver as risks converge.

Soft Landing, Touch and Go, or Another Go-Around?

The outlook has steadied. After two rocky quarters, Q3 is starting with firmer footing—retail sales have normalized, manufacturing has stabilized, and ISM indexes are no longer slipping. But fragilities remain. Consumer credit is tightening, delinquencies are inching higher, and business investment is weak.

A soft landing is still within reach, but the approach vector is narrow. The Fed must pivot preemptively while avoiding the perception of political capitulation. Treasury must finance larger deficits without destabilizing the long end of the curve. And Trump’s tariff-first diplomacy must avoid choking off supply chains or igniting retaliatory measures.

We anticipate three 25-basis-point rate cuts—September, October, and December—with a possible fourth in Q1 2026. Powell is unlikely to be replaced in the near term; doing so would expose Trump to blame if the economy stumbles. Still, Powell must communicate any cuts as economically warranted—not politically motivated.

A more volatile glidepath is forming. Each new shock—tariffs, sanctions, oil disruptions, or a credit crunch—narrows the Fed’s window and complicates execution. A misstep could stall growth or reignite inflation.

Homebuilders, manufacturers, and financial markets are bracing for a “touch and go” landing—where easing helps, but momentum fades. Until policy coordination improves and global tensions ease, investors should keep seat belts fastened and stay near the exit row.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 18, 2025

Mark Vitner, Chief Economist

704-458-4000