Tariff Fears Fuel Big-Ticket Purchases

- Retail sales rose 1.4% in March, fueled by a 5.3% surge in motor vehicle sales.

- Excluding autos, sales rose 0.5%, with gains reported in 10 of 12 major categories.

- Gas station sales fell 2.5% due to lower prices; ex-gasoline, sales advanced a solid 1.7%.

- Gains were broad based, with building materials, recreation and sport stores, and electronics stores all posting solid gains. Online sales were soft, however, and furniture stores saw sales drop 0.7%.

- Core retail sales (control group) posted a softer-than-expected 0.4% gain, though upward revisions to prior months signal firmer underlying strength.

- March retail sales should alleviate some of the darker fears about the outlook. While the data preceded April’s tariff turmoil, the underlying trend is stronger than earlier thought and the first quarter ended on a strong note that should carry over into the current quarter.

U.S. retail sales rebounded sharply in March, rising 1.4% and marking a welcome turnaround after two consecutive weak prints. While the rise was broadly in line with expectations, the underlying details point to consumer spending than previously assumed. Auto sales surged 5.3%, a move widely attributed to front-loaded purchases ahead of anticipated tariffs. Combined with upward revisions to prior months, the data ease concerns that the economy is on the edge of, or already in, recession. Real personal consumption now appears on pace for a 1% annualized gain in Q1 — a clear deceleration from the prior quarter’s 4% pace, but materially better than earlier estimates.

Beyond the tariff-driven dynamics, several temporary factors likely provided a meaningful boost. The rebound from weather‑related disruptions and illness earlier in the quarter helped unlock pent‑up demand. In addition, the peak of tax‑refund disbursements in late February and early March temporarily lifted disposable income. The distribution of retroactive Social Security payments during the month also added modest incremental support to household cash flow.

This year’s extremely late Easter may have also provided an unexpected boost. Retail sales are adjusted for seasonal, holiday, and trading‑day differences, occasionally resulting in head‑scratching reports. When Easter comes late, the Census Bureau smooths retail sales by pulling some of the sales it expects to occur in April into March. The opposite adjustment applies in years when Easter falls early.

March retail sales also likely benefited from improving weather, following a colder and wetter‑than‑usual winter and a particularly severe flu season.

Looking beyond temporary distortions, the underlying data highlight a remarkably resilient U.S. consumer. History reminds us to never underestimate the American consumer’s willingness to spend, even as economic headwinds gather. Control group sales — the core input for the most discretionary components of the Bureau of Economic Analysis’ personal consumption calculations — advanced a solid 0.4% in March. Upward revisions to the two prior months underscore the firmer underlying trend.

Never underestimate the American consumer, even when economic headwinds gather.

Incorporating the stronger data, we have revised our Q1 real personal consumption growth estimate to a 1.2% annualized rate, up from 0.9%. While some forecasts are likely to come in higher, we expect unseasonably mild March weather to suppress utility use, limiting the upside for services spending.

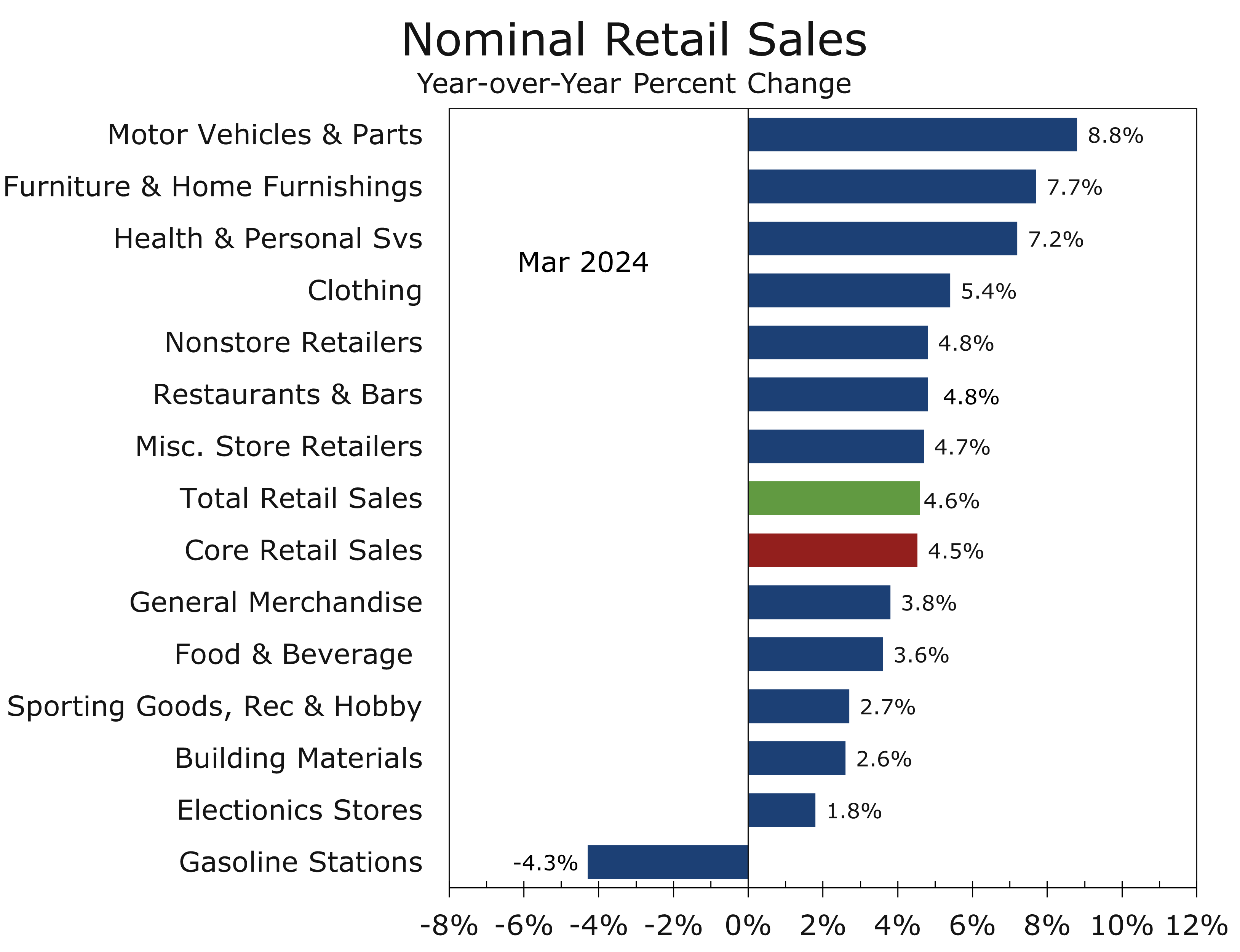

Retail sales look meaningfully stronger following March’s strong retail sales report. Year-over-year comparisons highlight a resilient consumer, with furniture sales up 7.7%, health and personal care stores rising 7.2%, clothing advancing 5.4%, nonstore sales up 4.8%, and restaurants up 4.8%. That said, core retail sales have been tempered by continued softness at department stores, sporting goods, and electronics.

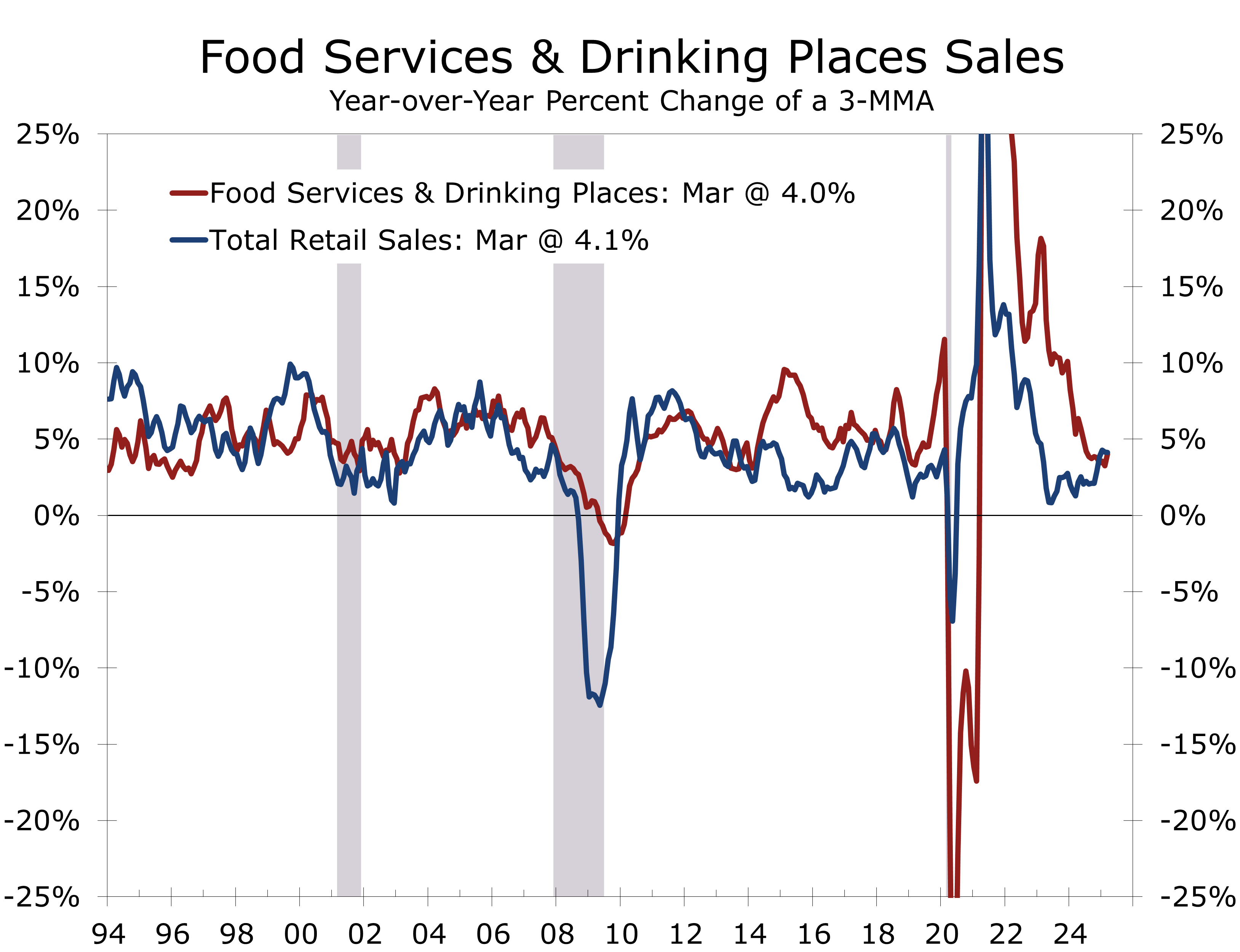

Calendar dynamics provided a notable tailwind to the foodservice sector. OpenTable data indicated a significant surge in Valentine’s Day dining, with reservations trending higher than in 2024, partly due to the date falling on a Friday this year. While sales experienced a brief dip following the April 2 tariff announcements, they have since rebounded, particularly in popular spring‑break destinations. The unusually late Easter has extended the spring‑break season, boosting foodservice‑related sales.

The unusually late Easter holiday has extended the spring break season.

Another trend boosting restaurants is the return to the office, which is driving lunchtime and after-work business. Office employment is now back near its pre-pandemic peak in most major MSAs. Other retailers that cater to the office workforce, dry cleaners, shoe shops and miscellaneous retail, are also benefiting.

The latest retail sales data push back at the notion that the economy is either in recession or soon will be. While growth has clearly slowed and the risks have clearly increased, we still see a better-than-even chance of the economy avoiding recession in 2025.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

April 16, 2025

Mark Vitner, Chief Economist

(704) 458-4000