Manufacturers Are Playing Defense

-

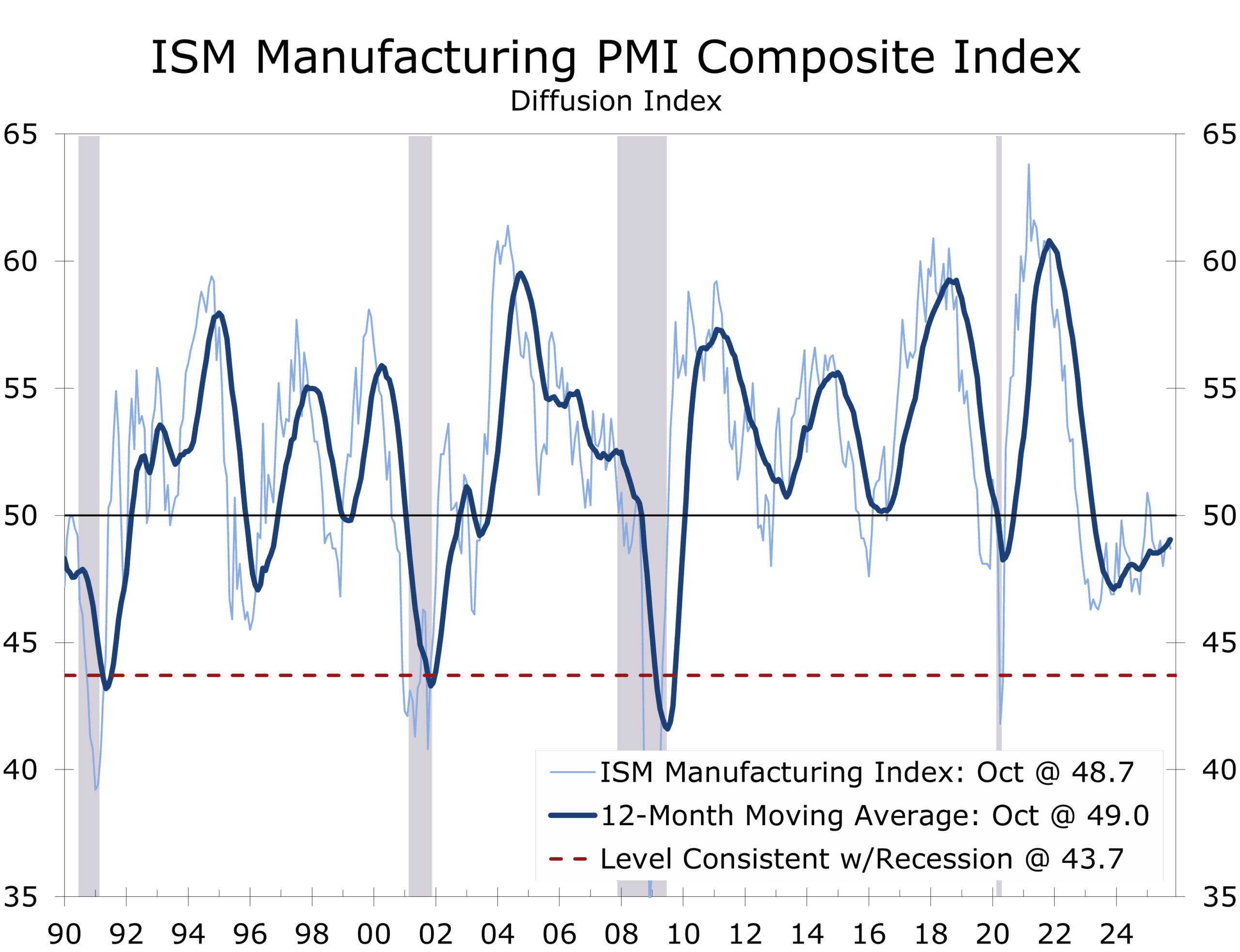

- ISM Manufacturing Index: 48.7 (–0.4) — signals the eighth straight month of contraction and a widening breadth of weakness across U.S. manufacturing.

- Production: 48.2 (down from 51.0) — slipped back into contraction after a brief September rebound.

- New Orders: 49.4 (up from 48.9) — second straight month below 50, still reflecting soft demand.

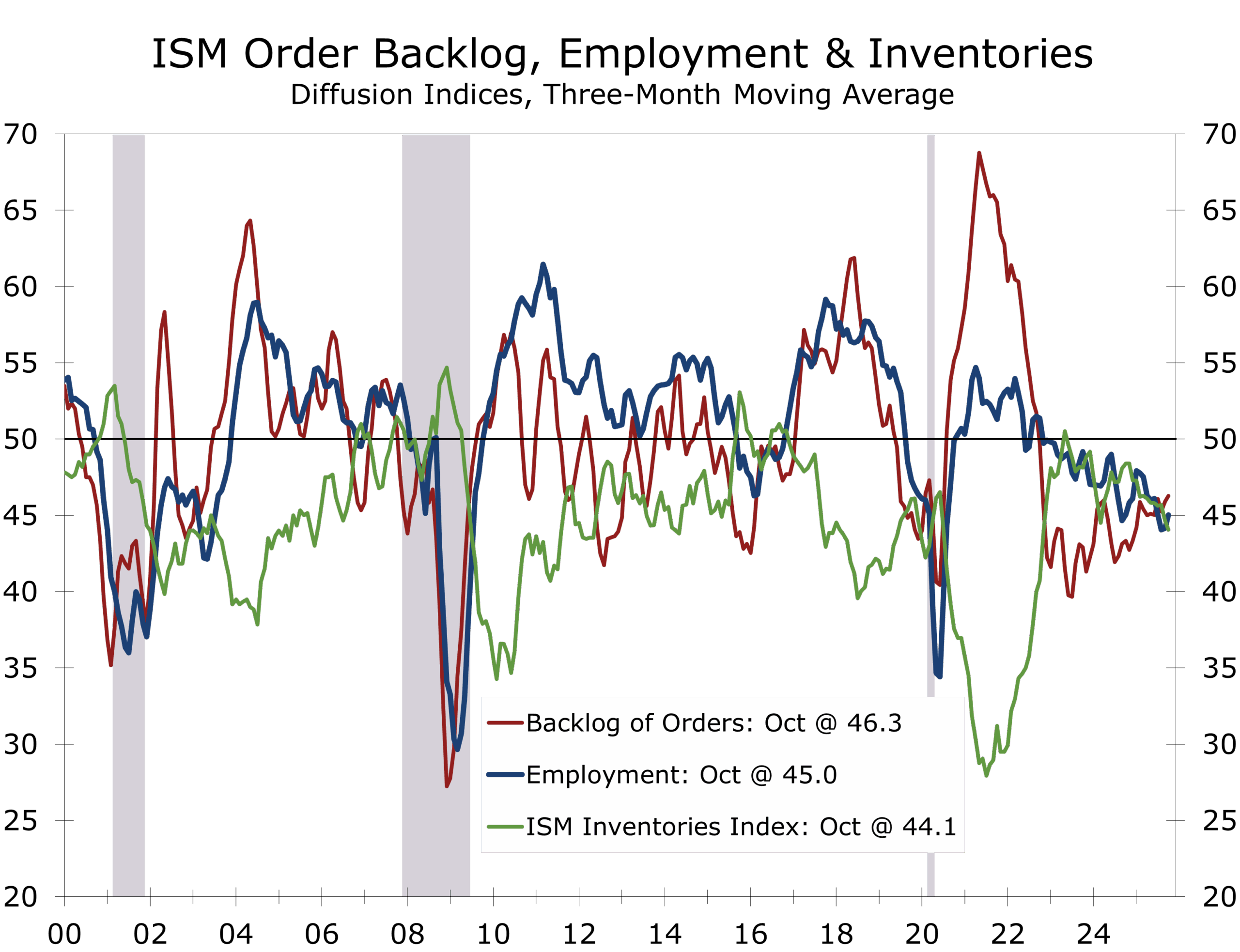

- Employment: 46.0 (+0.7) — ninth month of contraction as manufacturers continue managing headcount leanly.

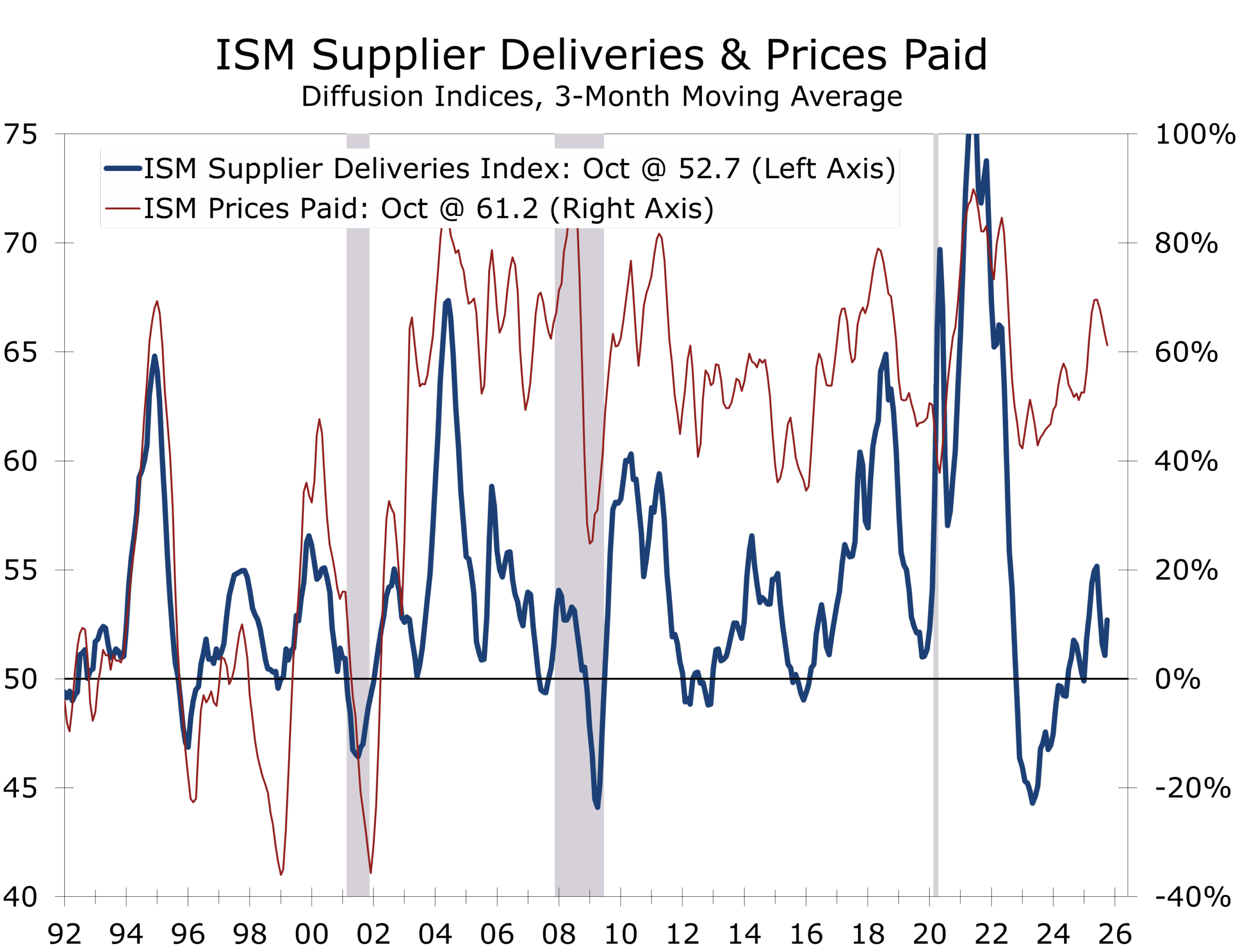

- Supplier Deliveries: 54.2 (+1.6) — slower deliveries for a third month, consistent with stabilized but subdued activity.

- Customers’ Inventories: 43.9 (+0.2) — still “too low,” implying potential for restocking once confidence improves.

- Prices Paid: 58.0 (–3.9) — still elevated but easing from September’s 61.9, indicating slower input cost inflation.

- Exports: 44.5 (+1.5) — contracting for an eighth consecutive month.

- Imports: 45.4 (+0.7) — seventh month of contraction as tariff pricing dampens activity.

- Backlog of Orders: 47.9 (+1.7) — modest improvement, but still in contraction.

The ISM Manufacturing PMI® registered 48.7 in October, down 0.4 points from September, marking the eighth consecutive month of contraction following a brief reprieve earlier this year. As a diffusion index, readings below 50 mean that more firms report worsening rather than improving conditions — a measure of breadth, not magnitude.

Production fell 2.8 points to 48.2, returning to contraction territory—meaning more firms reported output decelerating rather than accelerating—after just one month of growth. New Orders (49.4) and Employment (46.0) both edged higher but remained below 50, indicating continued weakness in order flow and hiring. Inventories were drawn down more sharply, while supplier deliveries lengthened modestly. Notably, all four demand components—New Orders, New Export Orders, Order Backlogs, and Customers’ Inventories—improved slightly, though each remains in contraction. Overall, the index remains consistent with modest economic growth, and we believe it is uncertainty, more than demand softness, that is weighing on manufacturer sentiment.

The Uncertainty and policy volatility, not collapsing demand, continue to weigh on manufacturing.

Manufacturing weakness in October was broad-based but not especially severe, with about 58% of manufacturing GDP contracting and 41% in strong contraction (PMI® ≤ 45).

Panelists repeatedly described a cautious tone. Two-thirds of respondents indicated they are still managing headcount, not hiring. Most are adjusting production schedules to match slower demand and are reluctant to rebuild inventories or add capacity. Even as backlogs ticked up, they remain historically low — a sign that order pipelines are not refilling.

Firms are operating in risk-management mode, focused on flexibility, liquidity, and cost control.

Tariffs and Policy Volatility Weighing on Risk Taking

Uncertainty appears to be weighing on a growing proportion of manufacturers. ISM respondents cited the tariff environment, the recent government shutdown, and heightened geopolitical and policy uncertainty as key factors shaping business behavior.

Companies report cancelled or reduced orders due to shifting trade policies and reciprocal actions from China, such as export controls on rare earths and semiconductors. Firms in machinery, chemical products, and fabricated metals highlighted how the unpredictability of tariffs is disrupting cost planning, margin management, and investment decisions.

This climate has fostered a “wait-and-see” mindset. As one respondent put it, “Money is sitting tighter, and geopolitical changes add to the uncertainty/risk factor.” Across multiple industries, that sentiment is translating into leaner operations, reduced overtime, and tighter working-capital discipline.

.

Input Prices Remain Elevated but Easing

The Prices Paid Index fell 3.9 points to 58.0, marking the 13th consecutive month of increases but at a slower rate. Price pressure remains concentrated in metals — particularly steel, aluminum, and copper — and in tariff-affected imports. Fewer respondents reported rising costs (27 percent versus 33 percent in September), suggesting that input inflation is decelerating, even as overall price levels remain high.

This backdrop supports ISM’s observation that cost stickiness and margin compression continue to weigh on capital spending and hiring. Manufacturers are prioritizing balance sheet preservation over expansion.

Manufacturers are preserving liquidity and awaiting policy clarity before restocking or rehiring.

Inventories and Demand Indicators: “Too Low,” Yet Still Too Risky to Rebuild

Customer inventories stayed in “too low” territory at 43.9, which historically signals potential for future restocking. However, panelists remain hesitant to respond — instead choosing to operate lean amid uncertain end-market demand.

Inventories fell more sharply (45.8), and order backlogs, while modestly higher, remain in contraction. These dynamics reinforce a theme of defensive stock management rather than preparation for renewed growth. Until confidence strengthens, restocking may continue to lag underlying consumption.

Sector Breadth and Structural Takeaways

Only Food, Beverage & Tobacco Products and Transportation Equipment expanded in October, reflecting stable consumer demand, and solid aerospace activity and defense orders. Most other industries — including machinery, chemicals, fabricated metals, and electronics — saw broad-based declines, confirming that the softness is systemic rather than isolated.

The ISM estimates that the October PMI corresponds to roughly +1.8% annualized real GDP growth, indicating that while manufacturing is contracting, it has not dragged the broader economy into decline. Still, the diffusion of weakness across 12 industries warrants close monitoring as policymakers balance corralling inflation with sustaining growth momentum.

The October ISM Manufacturing Index reinforces our assessment that policy uncertainty—not just soft demand—is the primary headwind facing U.S. manufacturing. The latest data show a sector leaning hard on cost control and liquidity preservation as confidence remains clouded by tariffs, fiscal volatility, and geopolitical friction.

Customers and producers alike are running lean and deferring restocking or rehiring until visibility improves. While the index does not point to a collapse in output, the breadth of contraction has widened, signaling a slow, grinding adjustment phase rather than an outright downturn.

The combination of lean inventories, early signs of easing price pressures (-3.9 points to 58.0 in October), and pent-up replacement demand suggests the groundwork for eventual stabilization. For now, however, the prevailing mood is caution. Unless the policy environment steadies, manufacturers are likely to remain defensive through year-end, waiting for clearer signals before committing to renewed production growth.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 3, 2025

Mark Vitner, Chief Economist

(704) 458-4000