Shelter and Core Inflation Continue to Cool

-

- Headline CPI rose 2% over the two-month period (September–November), with year-over-year inflation slowing to 2.7%, down from 3.0% in September.

- Core CPI increased 0.2% over two months, leaving core inflation at 2.6% y/y, the lowest reading of this cycle.

- Shelter inflation continued to decelerate, rising just 0.2% over two months and slowing to 3.0% y/y.

- Energy prices rebounded, lifting headline inflation, but remain a volatile rather than structural driver.

- Food inflation eased further, particularly at grocery stores, while restaurant inflation remained elevated but stable.

- Data caveat: October CPI data were not collected due to the federal government shutdown, compressing two months of inflation into a single report.

- Policy signal: Despite plenty of data distortions, the direction of travel is clear; inflation is cooling, reinforcing the Fed’s ability to continue easing.

The Big Picture: Two-Months of CPI in One-Month

November’s CPI report is unusual, but its message is unmistakable. Because the federal government shutdown halted data collection in October, the Bureau of Labor Statistics reported two months of price changes in a single release. That complicates month-to-month comparisons, but it does not obscure the underlying trend.

Inflation is moderating.

Headline CPI rose 0.2% from September to November, while year-over-year inflation declined to 2.7%, its lowest level since early 2021. The year-to-year change in the CPI is now back to its average since 1990. Core CPI followed the same trajectory, rising 0.2% over two months and decelerating to 2.6% y/y. Even with imperfect data, the signal is clear: underlying inflation pressures continue to fade.

The CPI was the only major piece of federal government data released during the shutdown; reflecting its outsized influence.

Core Inflation: Cooling, Even Through the Noise

Core inflation rose at an annualized pace well below the Fed’s comfort threshold. A two-month increase of 0.2% implies roughly 0.10% per month, a pace consistent with inflation settling near target once shelter completes its normalization. We have taken a simple average of the September and November data to impute the missing monthly data for October to allow continuity with our charts. This was done all series where no October data was available.

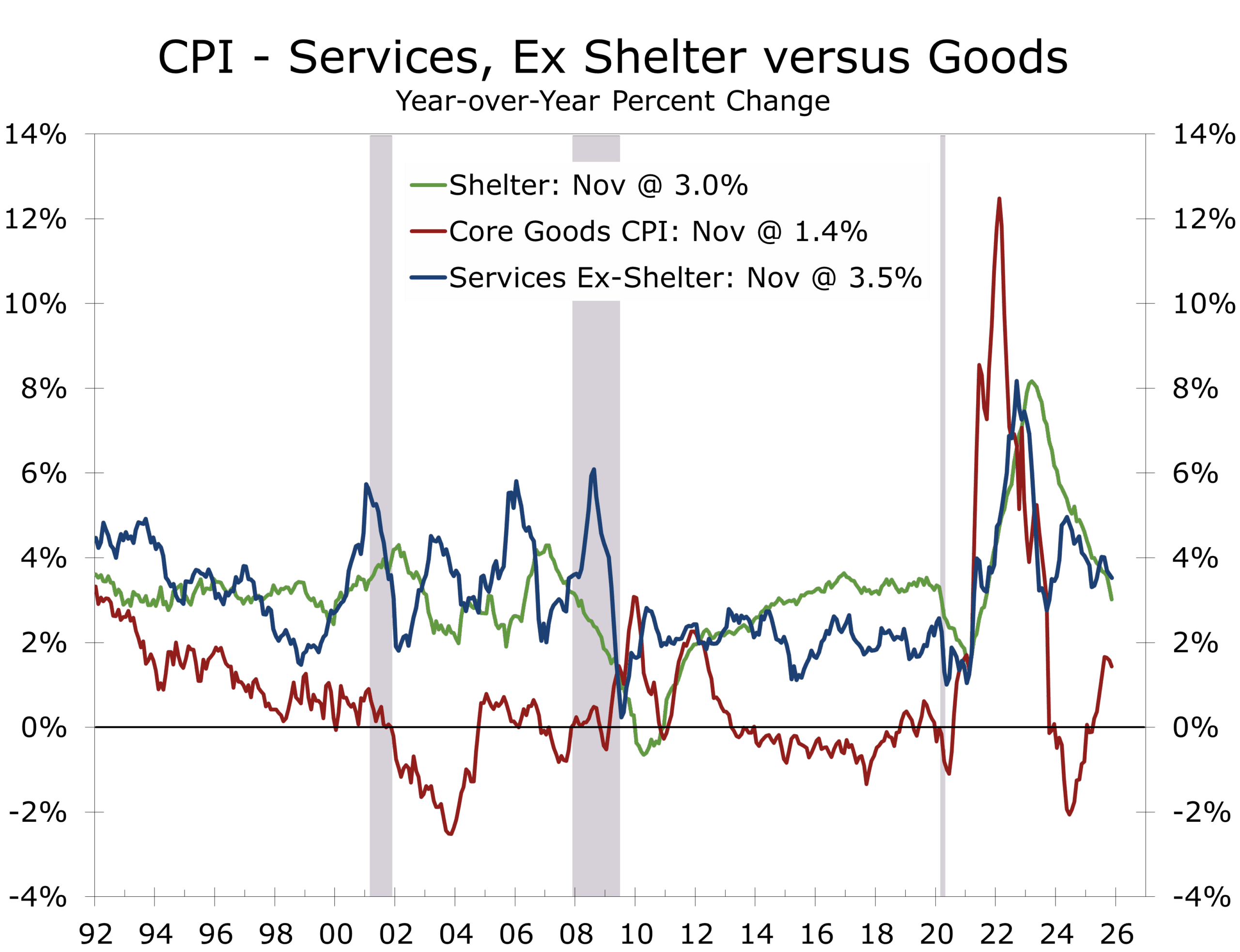

Core services excluding energy rose 3.0% y/y, down materially from earlier in the cycle, while core goods inflation remained contained at 1.4% y/y despite ongoing tariff uncertainty and a weaker dollar. The slight improvement suggests the bulk of the tariff impact is now behind us. Used vehicle prices edged higher but remain far removed from their pandemic-era surge.

With the worst of tariff impacts behind us, inflation pressures are narrowing.

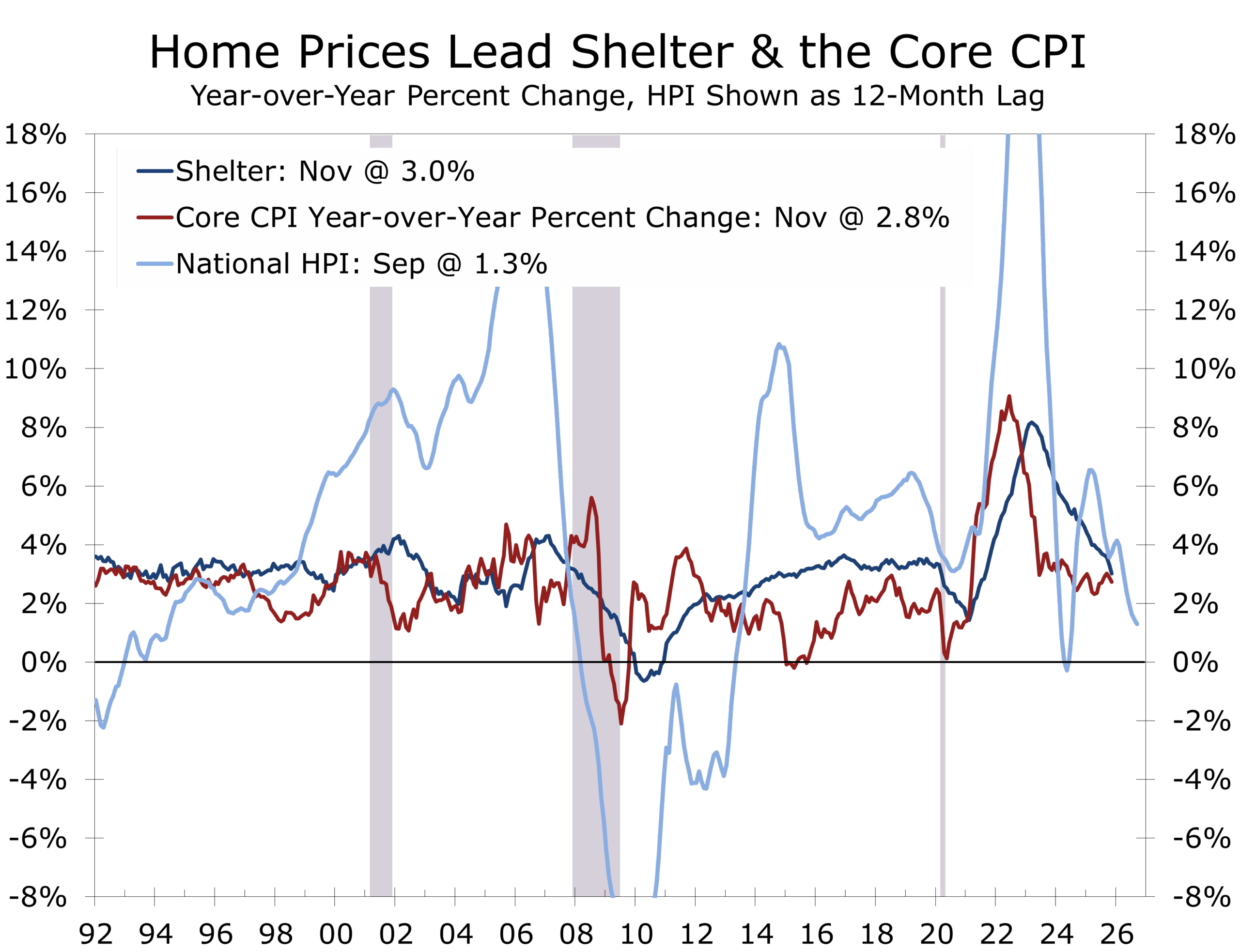

Shelter: The Heavy Lifting Continues

Shelter remains the key variable in the CPI narrative. November delivered further confirmation that this component is finally bending lower, which confirms earlier private sector reports of falling home prices and declining rents.

Shelter prices rose just 0.2% over two months, pulling year-over-year shelter inflation down to 3.0%, a dramatic deceleration from the 6%+ pace seen earlier in the cycle. This reflects a confluence of forces: a surge in multifamily supply, widespread rent concessions, and lease renewals resetting at lower rates, particularly across the Sun Belt. Home prices also declined for five months in a row earlier this year and are currently up just 1.3% year-to-year.

Given that shelter accounts for roughly 44% of core CPI, its deceleration is doing most of the work in pushing inflation lower.

Energy: Volatile, Not Structural

Energy prices rose 1.1% over the two-month period, lifting the energy index to 4.2% y/y. Gasoline prices increased modestly, while electricity and natural gas costs remain elevated on a year-over-year basis.

The inflation problem is shifting from grocery stores to more slowly moderating services.

Still, energy continues to behave as a swing factor rather than a structural inflation driver. Absent a sustained surge that feeds into wages or expectations, energy-driven volatility does little to alter the disinflation trend. Moreover, oil prices have weakened recently, and natural gas prices are expected to decline over the next year, slowing gains in electricity costs.

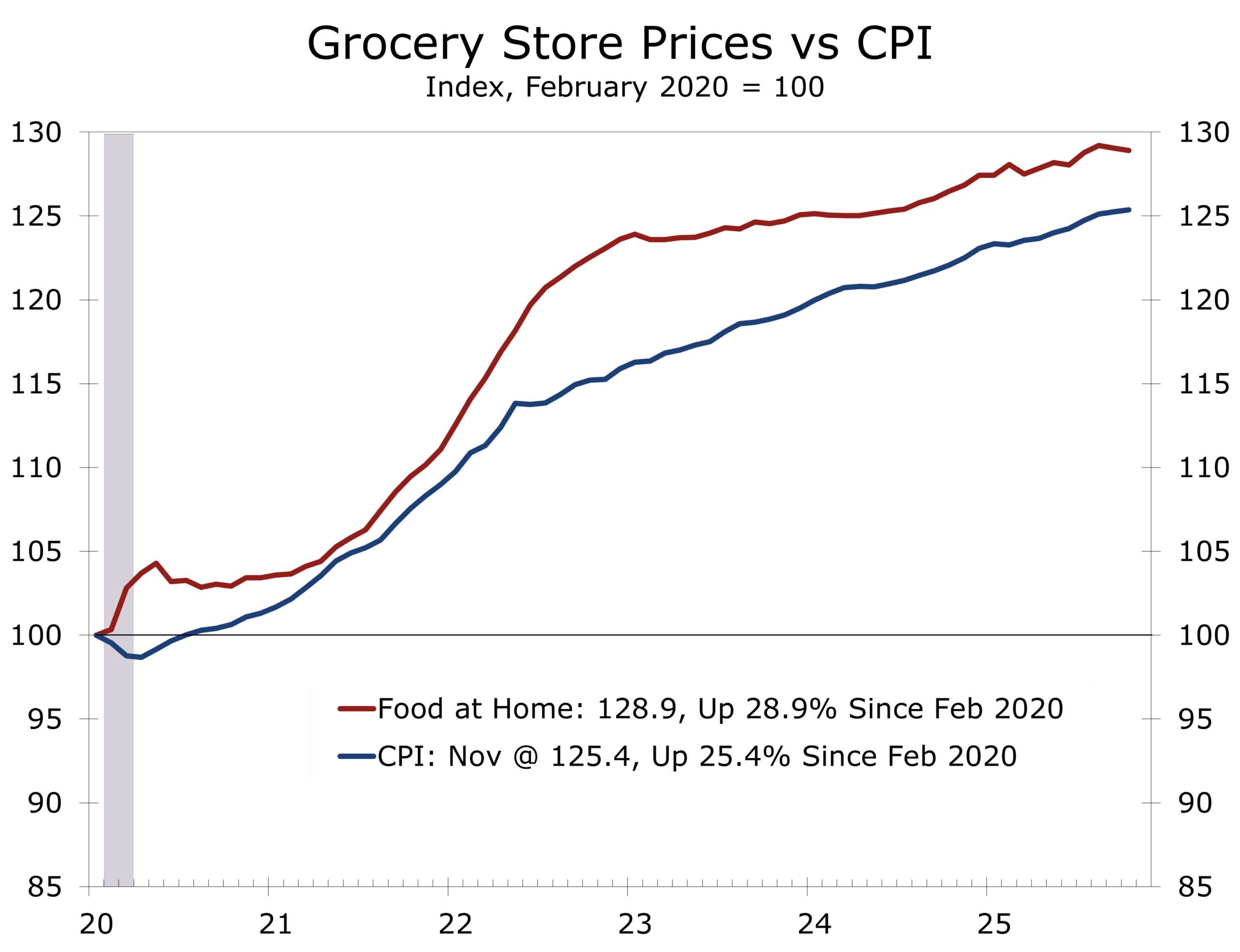

Food: Cooling at Home, less so at Restaurants

Food inflation continues to decelerate, led by groceries. Food at home rose just 1.9% y/y, with dairy prices falling and produce inflation essentially flat. In contrast, food away from home rose 3.7% y/y, reflecting still-elevated labor and occupancy costs.

Restaurant pricing remains one of the last pockets of persistence, but even here momentum is no longer accelerating. Promotions, menu simplification, and growing consumer price sensitivity are limiting further pass-through. Beef is a clear exception to the moderating trend and is rising due to structural factors, not monetary policy. Higher beef prices will slow the moderation in grocery store prices and also squeeze restaurant margins.

Surprise and Doubts

The improvement in CPI may ring hollow for many consumers, particularly those still grappling with elevated grocery bills. While inflation has slowed, prices are not falling. The post-pandemic inflation surge was the product of a policy era marked by massive federal spending and a Federal Reserve that was slow to withdraw accommodation as the economy roared back to life.

Flush with stimulus-era savings, consumers bid up prices for key necessities, including groceries and housing, at a pace well above the overall inflation rate. Although price increases have since moderated, grocery prices remain roughly 29% higher than before the pandemic. Much of that increase is now embedded in labor costs, which rose even faster and are unlikely to reverse. Adding to the strain, beef prices are poised to rise further before improving, reinforcing consumer frustration. Chicken and pork prices should be less affected and may provide some relief at the margins—but for many households, the sticker shock is here to stay.

Shutdown Distortions: Timing Changed, Trend Intact

The federal shutdown introduces important caveats. The BLS did not collect survey data in October and was unable to retroactively recover those observations. As a result, this report reflects a combination of two months of survey-based data and non-survey sources where available.

Even so, the shutdown distorted timing, not direction. Despite compressed reporting and missing seasonal detail, the underlying trend points decisively toward slower inflation.

Policy Implications: The Fed’s Job Has Changed

This report reinforces a clear shift in the Fed’s reaction function. Inflation is no longer the dominant risk. With headline CPI at 2.7%, core CPI at 2.6%, and shelter inflation decelerating rapidly, policymakers have room to pivot their focus toward emerging labor-market softening and broader financial-conditions stability.

The inflation fight is not over, but it no longer requires highly restrictive policy.

Rate cuts at this stage are best viewed as insurance, not stimulus—designed to guard against a policy-induced or needlessly severe downturn in employment while inflation continues its gradual glide lower. Monetary policy is working, and at current levels the federal funds rate remains modestly restrictive. Calls for sharply lower rates are premature unless economic growth weakens materially.

Strip away the shutdown noise, and the message is straightforward: inflation is cooling, shelter is leading the way, and price pressures are becoming increasingly concentrated rather than broad-based. While it is too soon for a victory lap, the latest CPI data provide important confirmation that the disinflation process is durable enough for the Fed to remain focused on stabilizing growth and employment as 2026 approaches, providing the incoming Fed Chair greater policy latitude.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 18, 2025

Mark Vitner, Chief Economist

(704) 458-4000