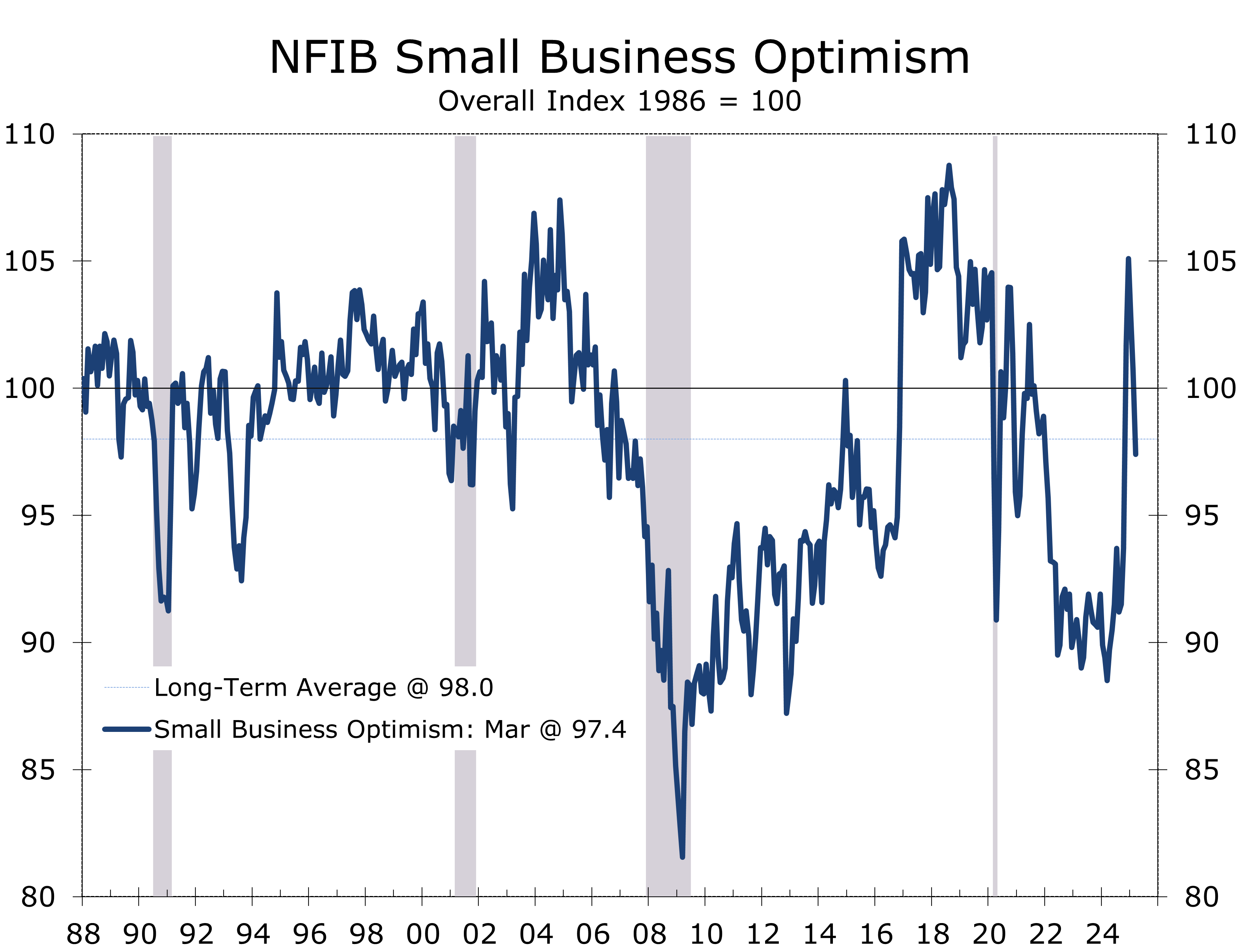

Sentiment Falters Amid Renewed Uncertainty

- The NFIB Small Business Optimism Index declined 3.3 points to 97.4 in March, its largest drop since June 2022, and is now slightly below its long-term average of 98.

- Expectations took a big hit, with the share expecting better business conditions plunging 16 points to 21% and real sales expectations tumbling 11 points to 3%.

- Uncertainty remains historically high at 96, despite an 8-point drop in March.

- Job openings rose to 40%, led by gains in construction and transportation, but net hiring plans fell to a one-year low.

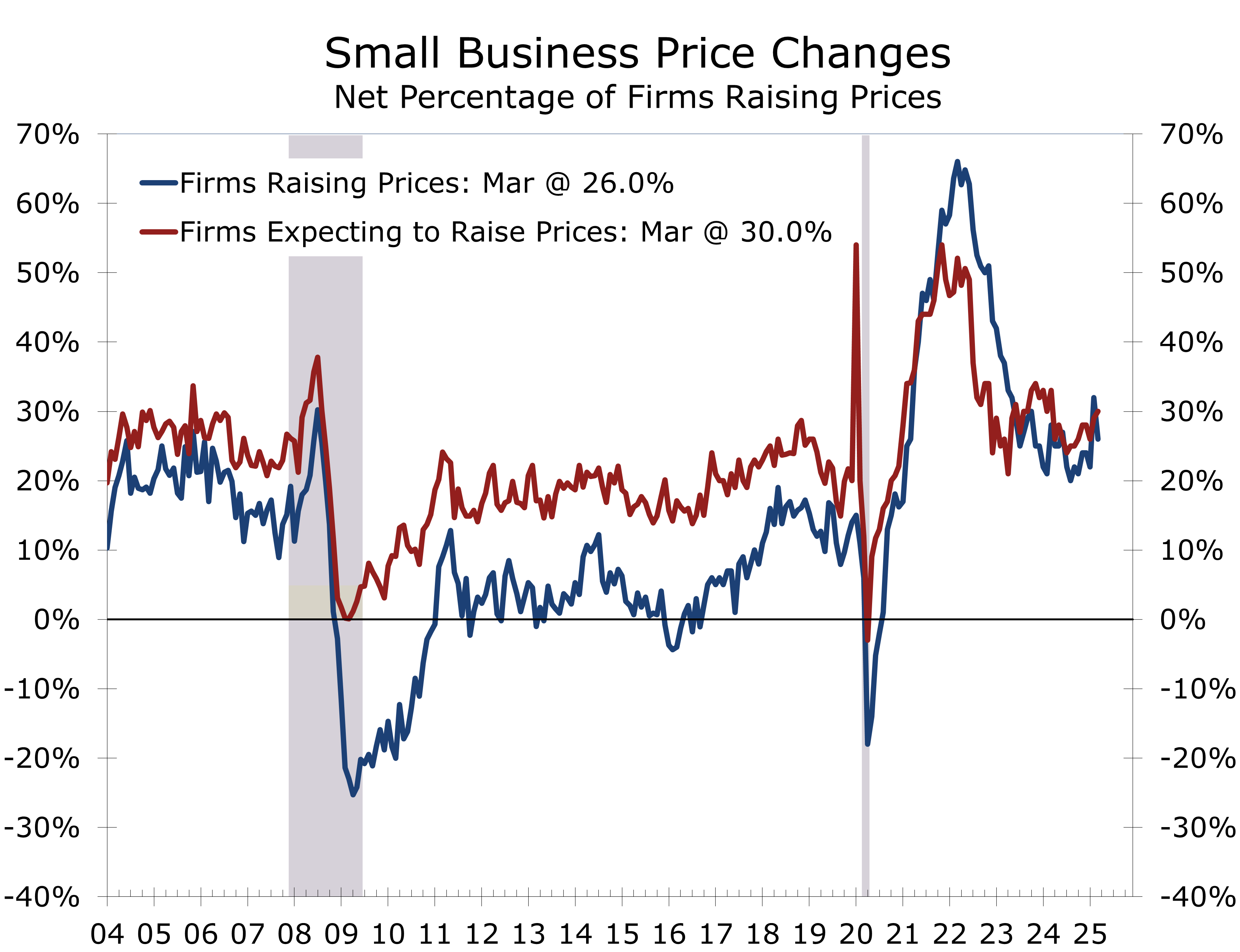

- Twenty-six percent of firms increased their prices, a figure still well above historical averages. Wage increases were widespread, and margin pressure is intensifying.

- Tightening credit conditions are evident as concerns about loan access have surged and short-term interest rates have climbed to 8.9%, suggesting increased financing constraints for small businesses.

- Small business owners were already on edge before unexpectedly large tariffs were announced on April 2. Small businesses have fewer options to offset the impact of tariffs and will likely curtail investment and hiring.

The NFIB Small Business Optimism Index fell 3.3 points to 97.4 in April, the largest monthly pullback since June 2022. The index has now fallen below its 51-year average of 98, retreating further from December’s recent cycle high of 105.1. The March reading underscores a broad-based deterioration, with business owners citing elevated uncertainty tied to domestic policy changes, the rollout of tariffs, and slower-than-expected regulatory relief under President Trump’s second term. While the Uncertainty Index edged down from a near-record 104 to 96, it remains significantly above the long-term norm, reflecting Main Street’s growing unease.

Small Businesses were cautious ahead of the introduction of surprisingly large tariffs in April.

The most significant driver of the headline decline was a 16-point drop in the net percentage of owners expecting better business conditions, now at 21%. Real sales expectations also fell 11 points to 3%. These reversals mark a swift erosion in confidence following December’s surge in optimism. The net percentage of owners viewing the present as a good time to expand fell to 9% (down 3 points), and business health perceptions weakened, with a 2-point decline in those rating conditions as “good.” The sharp pivot highlights how policy signals—especially around trade and regulation—can create rapid sentiment reversals.

Labor demand remains robust. Job openings rose 2 points to 40%, with notable strength in construction (+10 points m/m; +12 y/y) and transportation (+23 points to 53%). Manufacturing openings remained steady, while agriculture and wholesale trade remain softer. Openings for skilled workers rose to 33%, while unskilled job openings remained unchanged at 13%.

While job openings have remained high, actual hiring has slowed and should slow further.

While job openings remained high, actual hiring softened: 14.4% of firms reduced headcount, while just 9.6% added staff. Net hiring plans slipped 3 points to 12%, the lowest level in nearly a year. Compensation pressures remain acute, with 38% of firms raising wages (up 5 points), and 19% planning further hikes.

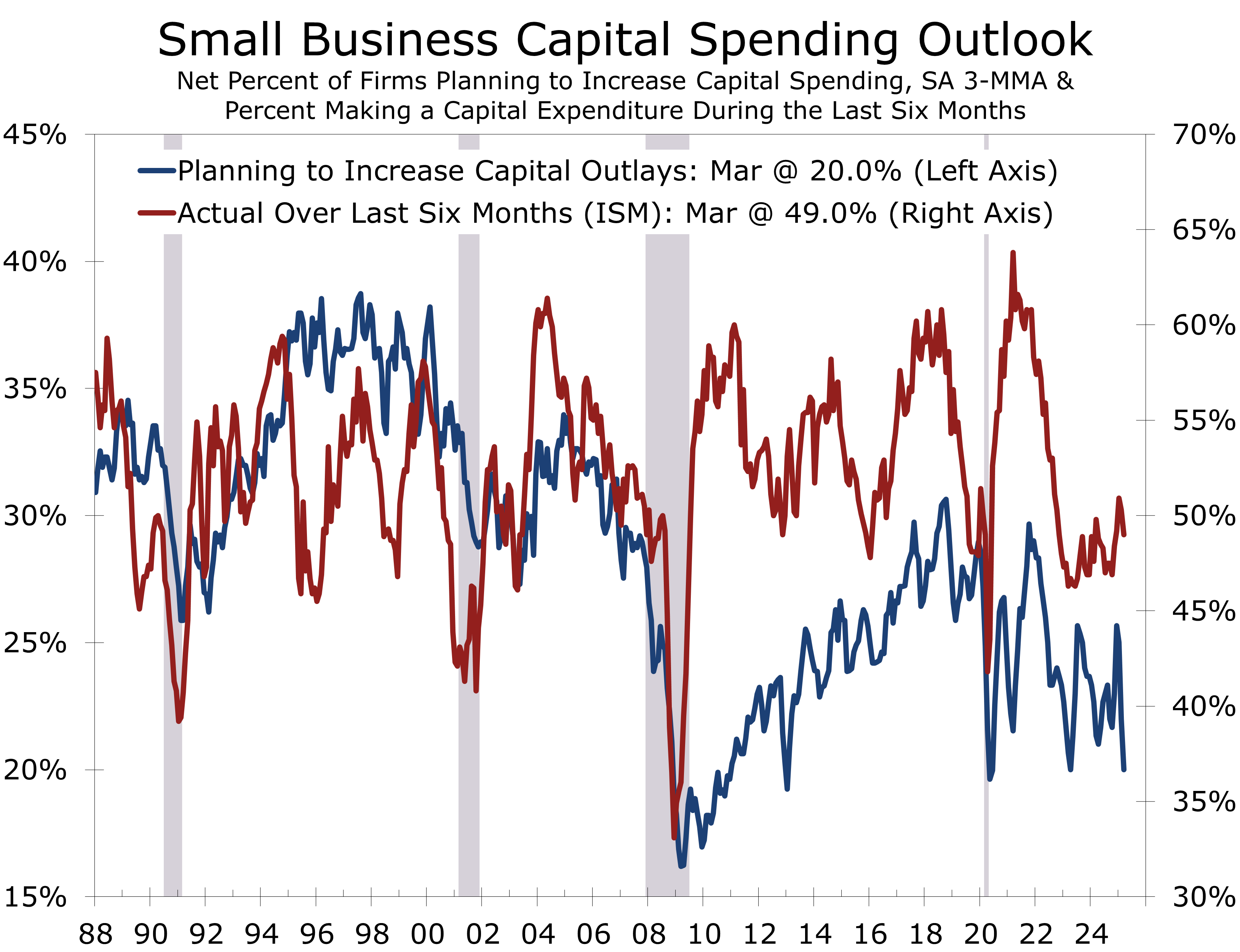

Capital expenditures saw a slight improvement, with 59% of firms reporting spending in the last six months (a 1-point increase). This was driven by a 6-point rise in equipment purchases and a 3-point rise in facility improvements. Vehicle purchases fell 3 points. Future capital spending plans remain cautious, rising 2 points to a historically low 21%. Inventory data also indicates weakness: with a net -3% adding to inventory, and a net -7% stating their current inventory are too low. Planned inventories remained unchanged, aligning with expectations of slowing sales.

While headline inflation has recently retreated, small business owners continue to pass along their higher cost. In March, 26% of firms raised prices (down 6 points), but this remains well above the 8% pre-2020 average. Planned price hikes increased to 30% (up 1 point), but a rising share of firms (10%) cut prices, suggesting some sector-specific softness and providing some early indication of the limits of pricing power.

Small business owners are having difficulty passing along their higher operating costs.

Credit conditions are tightening. The percentage of firms reporting difficulty accessing credit increased 4 points to 6%—the largest monthly rise since September 2023. The average short-term loan rate reached 8.9%, its highest level since early 2007. Despite financing being a top concern for only 3%, tighter credit and higher interest rates are hindering investment and impacting housing-sensitive sectors.

The latest NFIB data aligns with a slowing economy. Business owners were reporting diminished pricing power prior to the unveiling of tariffs. Consequently, investment and hiring are expected to slow, weighing on economic growth this spring and summer.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

April 8, 2025

Mark Vitner, Chief Economist

Piedmont Crescent Capital

(704) 458-4000