Manufacturing Cools but Remains Resilient

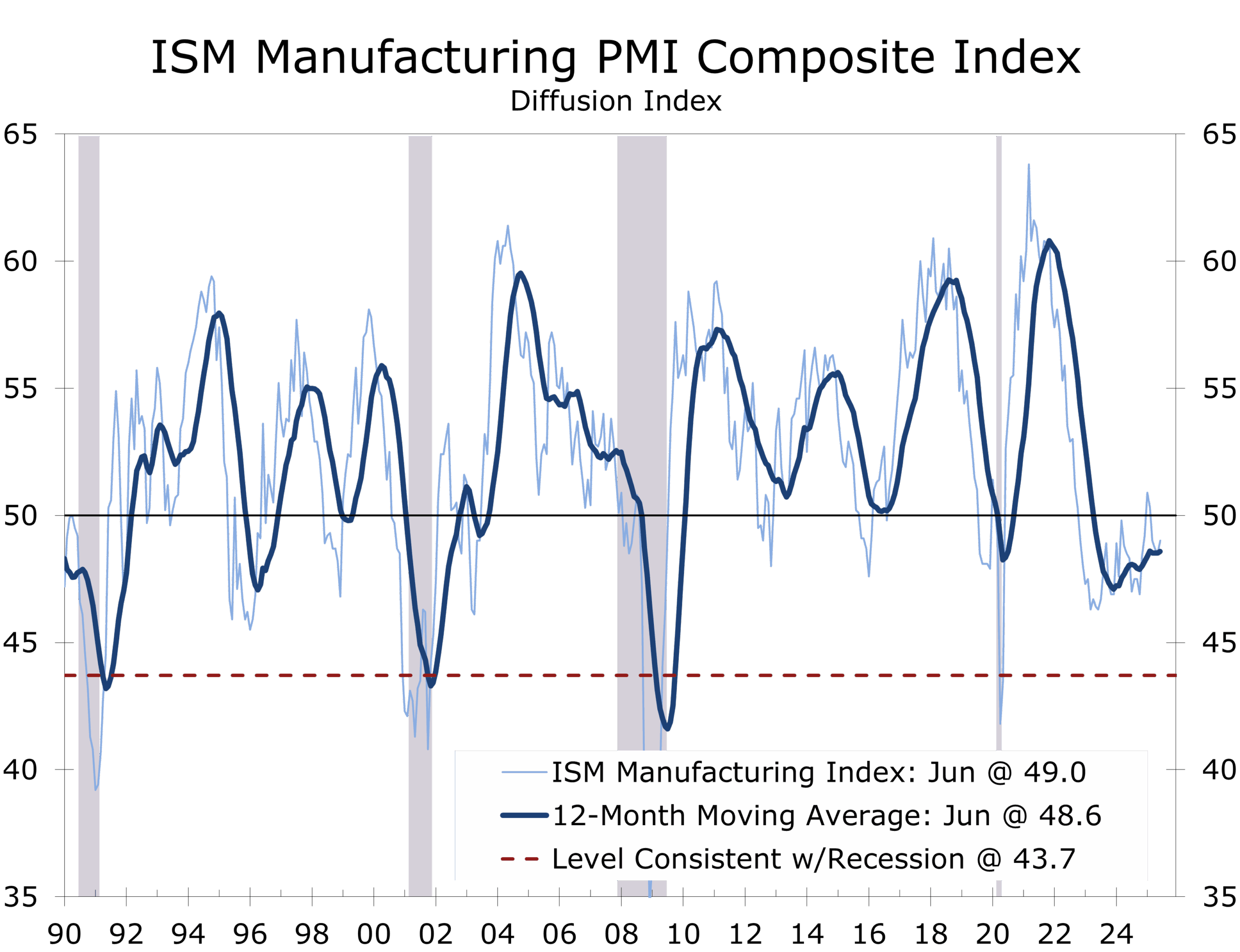

- The ISM Manufacturing PMI rose slightly to 49.0 in June, marking its fourth straight month below 50 but showing continued stabilization.

- New orders softened to 46.4, pointing to ongoing weakness in underlying demand.

- Production ticked up to 50.3, just above breakeven, driven by easing supply chain bottlenecks.

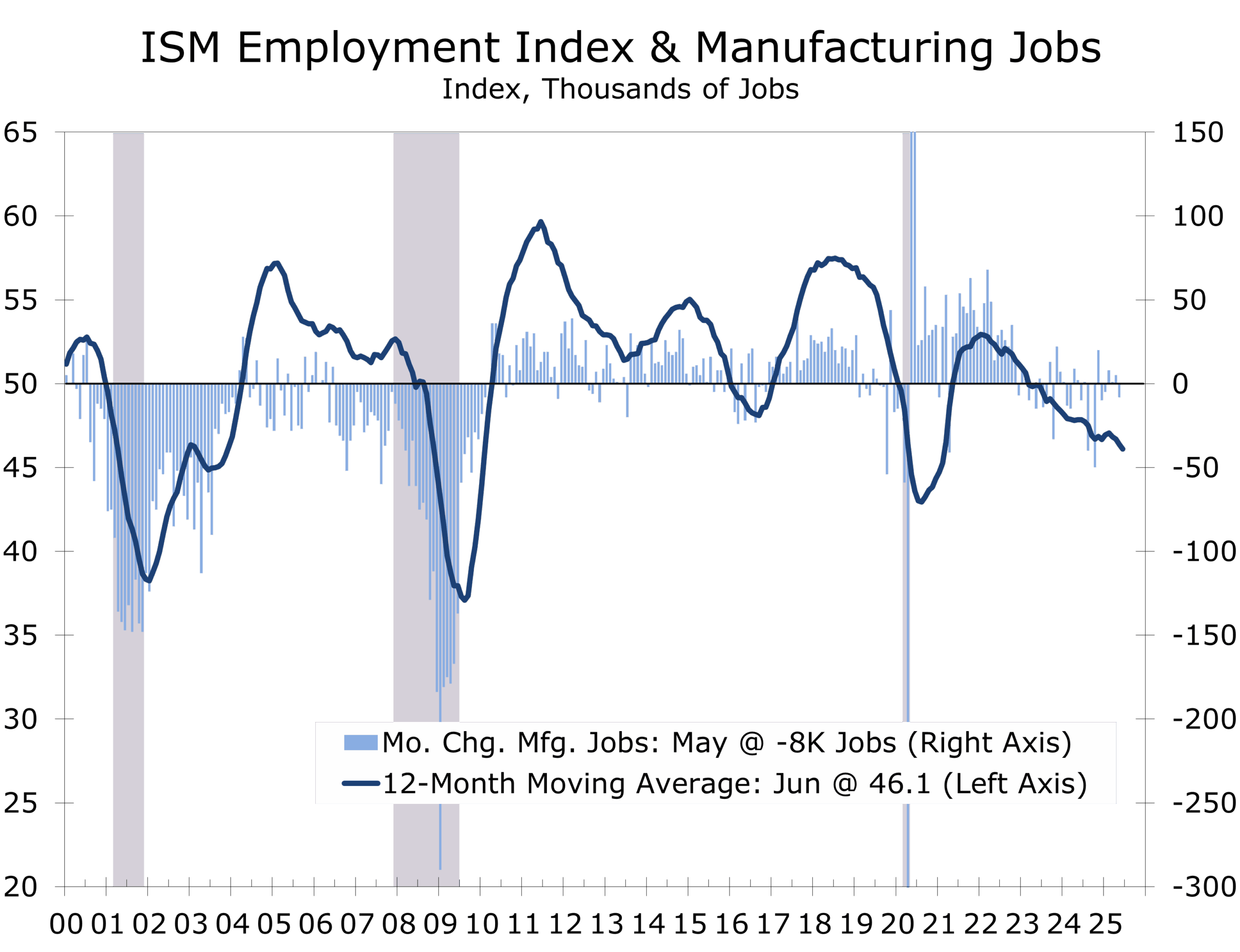

- Employment fell to 45.0 as firms remain cautious about hiring and leave positions open to help curb costs.

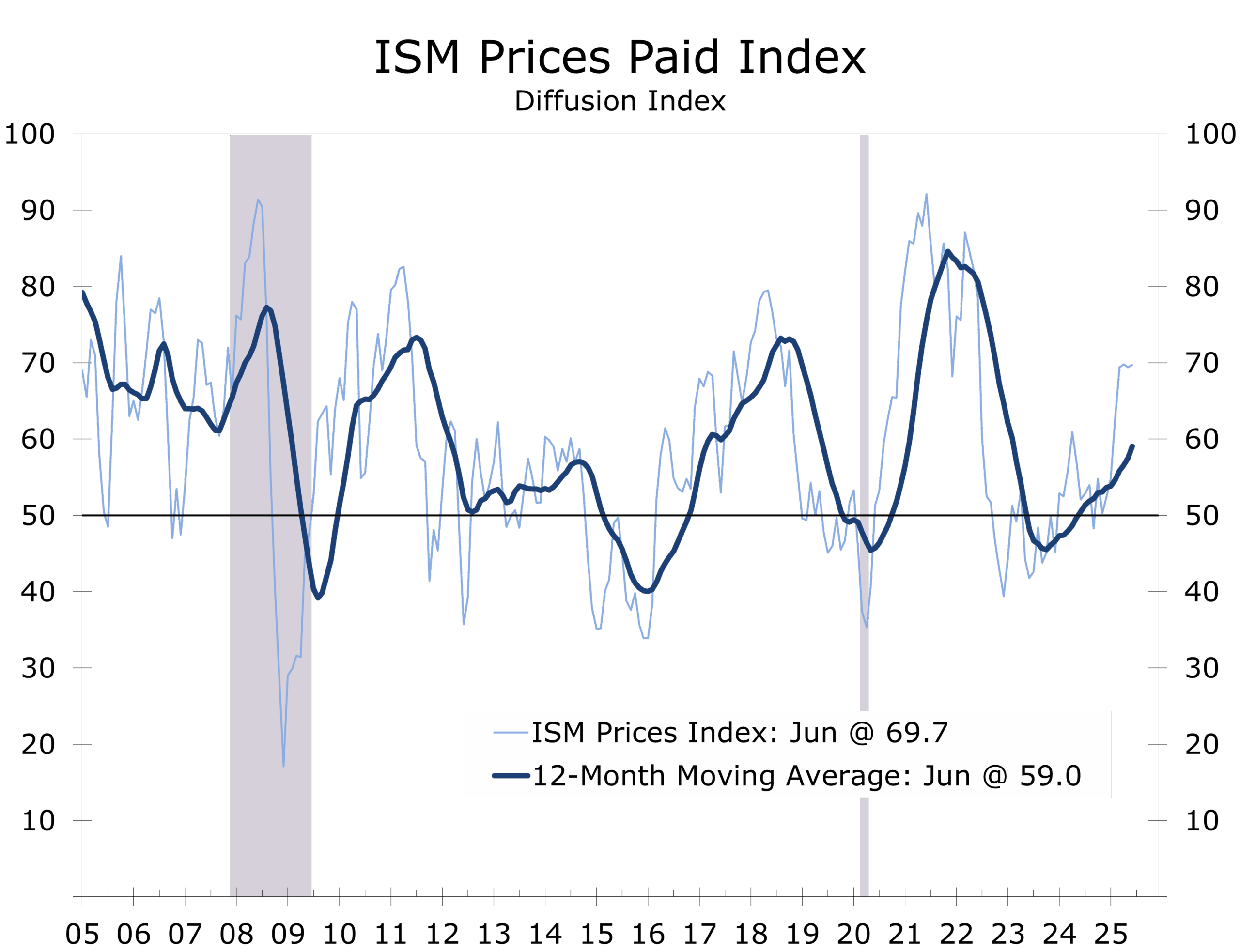

- Prices paid rose to 69.7, reflecting intensifying input cost pressures.

- Alan Greenspan once called the ISM his favorite economic indicator, praising its timeliness and ability to capture cyclical inflection points. The latest reading suggests we are not yet at such a juncture, and the Fed can afford to wait for greater clarity on the evolving tariff landscape and fiscal policy mix. While still soft, the PMI remains closer to expansion territory (50+) than to levels typically associated with recession (43.7 or lower).

Modest Uptick Masks Crosscurrents Beneath the Surface

As we expected, the ISM Manufacturing Index remained just below the key 50-breakeven level in June, rising to 49.0 from 48.5 in May. As a diffusion index, the ISM measures the breadth of change rather than magnitude—so while more firms reported weakening conditions than improving, the reading remains well above the 43.7 mark that historically signals a broad-based recession.

Production rose for a second straight month and eked into expansion territory, reflecting slightly better delivery times and inventory normalization. Businesses are holding off major commitments but with lean customer inventories and solid order backlogs, production should hold up reasonably well. The resilience in production, however, was offset by a decline in new orders, which fell 1.2 points to 46.4—marking a renewed pullback in forward demand.

The employment index slipped to 45.0, indicating increased hesitation among firms to bring on new staff. Most survey respondents noted they are controlling costs via hiring freezes and reduced overtime, rather than mass layoffs. That aligns with broader labor market trends: manufacturing job growth is flat, but layoffs remain contained. The latest JOLTS data show 414,000 job openings in manufacturing as of May, which is up slightly from April but down from 576,000 openings a year ago.

Tariffs Recede, But Price Pressures Reemerge

The headline narrative has shifted from tariffs to margin pressure. With input costs rising and end demand soft, many firms find themselves caught in a vice. Prices Paid rose 0.3 points to 69.7—driven by higher metals, chemicals, and shipping costs—while supplier delivery times increased slightly, complicating production planning. The Prices Index has increased 17.2 percentage points over the past six months, with the past three months readings marking the index’s highest since June 2022

Fading tariff concerns in the financial markets have not brought relief to manufacturers. Survey comments indicate that sourcing frictions and price mismatches persist, especially for intermediate goods. Manufacturers are facing a tougher environment for passing through price increases, with customer resistance growing amid slower final demand. Geopolitical uncertainty has also stifled demand overseas.

Trade and Inventory Signals Remain Mixed

Export orders rose 6.2 points to 46.3, benefitting from recent reprieves on tariffs with major trading companies. Companies are still awaiting greater clarity on trade deals, which we expect to see in the second half of this year. Imports edged down, partly due to deliberate efforts to trim inventory risk. Customer inventories rose 2.2 points by remain in relatively good shape at 46.7, suggesting some room for future restocking if demand firms and tariff uncertainty gives way more rapidly. Backlogs continue to decline, falling 2.8 points to 44.3, reflecting a softening production pipeline, which will keep managers cautious.

Outlook & Policy Implications

The June report confirms that manufacturing remains in a cautious holding pattern. Businesses are navigating a complex mix of excruciating slowly fading tariff threats, resurfacing cost pressures, and lackluster demand. That triple squeeze is forcing firms to cut costs, delay hiring, and tighten capex plans.

For policymakers, the ISM data signal ongoing fragility rather than crisis. Factory activity is soft, but not recessionary. The Fed is likely to interpret this as another argument for patience—watching how pricing power and demand evolve in the second half of the year before cutting rates. We still expect the next cut to come in September and now expect successive quarter point cuts at the three meetings afterward.

Former Fed Chair Alan Greenspan once said the ISM “tells you where the turning points are,” and right now, the signal is: we are not there yet. The squeeze manufacturers are dealing with is painful but is also the reason why higher import prices have not spilled more forcefully over into consumer prices. We expect to see a little more spillover this summer but look for slower economic growth to limit inflation and for lower interest rates, trade deals and tax incentives for capital spending to drive growth in the spring and summer of next year.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 1, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

704-458-4000