Housing Hits a Wall—But the Foundation Holds

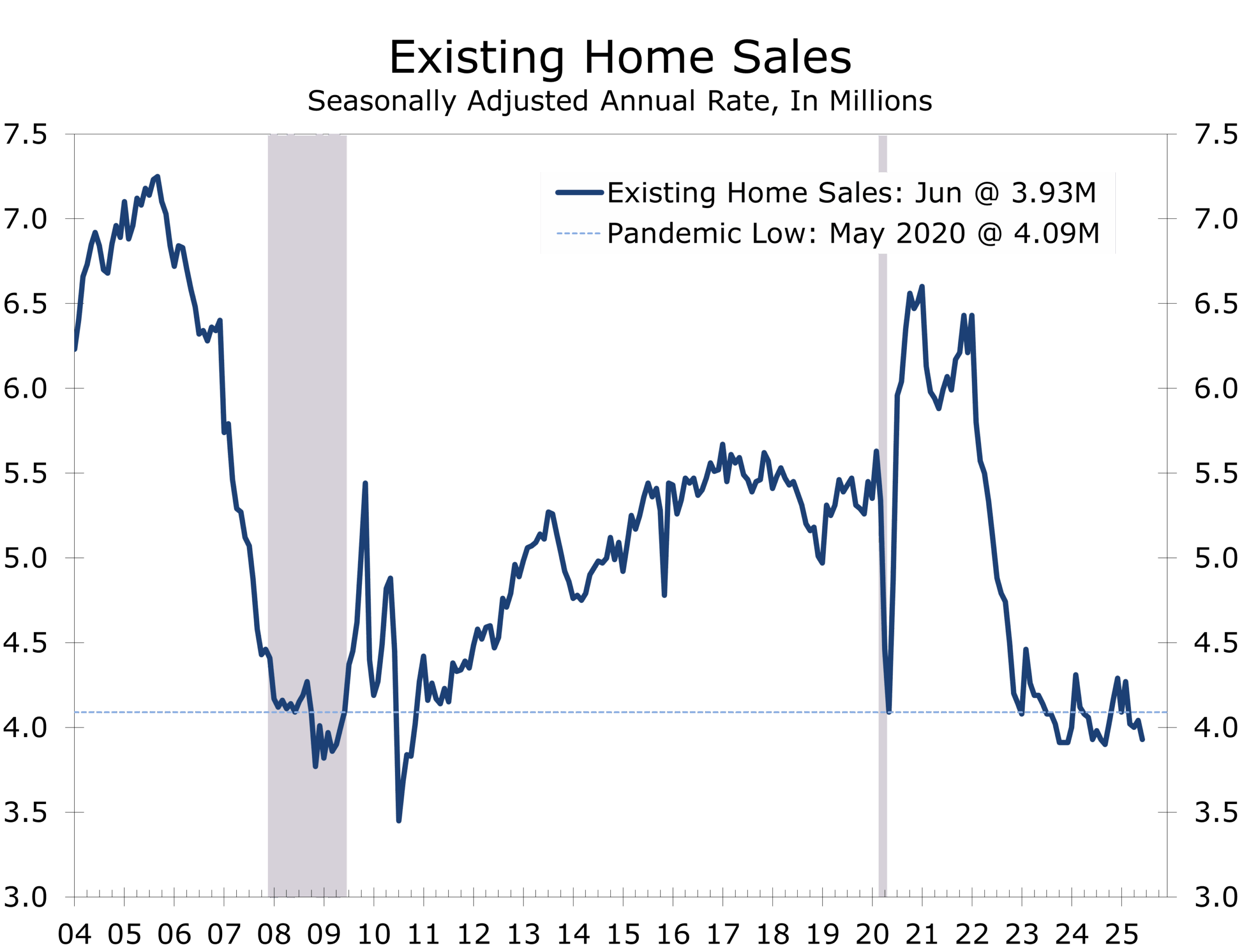

- Existing home sales fell 2.7% in June to a 3.93 million unit annualized pace—below expectations.

- Single-family home sales fell 3.0% to 3.57 million; median price rose 2.0% y/y to $441,500.

- Condo and co-op sales were flat at 360,000; median price rose 0.8% y/y to $374,500.

- Median price for all existing homes hit a record $435,300 (+2.0% y/y), 24th consecutive annual gain.

- Inventory declined 0.6% m/m but is up 15.9% y/y—rising but still skewed to higher-end single-family units or condominiums.

- The market remains gridlocked by affordability, high mortgage rates, and persistent undersupply of affordable homes.

- Housing’s multiplier effect remains powerful—policy support may be necessary to reignite activity. Further inaction risks deepening housing’s drag on labor mobility, GDP, and inflation rebalancing.

Existing home sales fell 2.7% in June to a 3.93 million unit annualized pace, disappointing consensus and underscoring the persistent paralysis in housing. Sales were flat versus a year ago, but structural cracks are widening. High borrowing costs, anemic affordable supply, and declining participation continue to weigh on turnover.

Single-family sales fell 3.0% to a 3.57 million rate, though modestly higher (+0.6%) from last June. The median price for single-family homes rose 2.0% y/y to $441,500. Condominium and co-op sales held steady at 360,000 units, down 5.3% year-over-year. Condo prices edged up 0.8% to $374,500. The divergence reflects the same pattern seen across the broader market—tight inventory at the low end, modest activity at the high end.

Record prices mask a market paralyzed by high rates and locked-in equity.

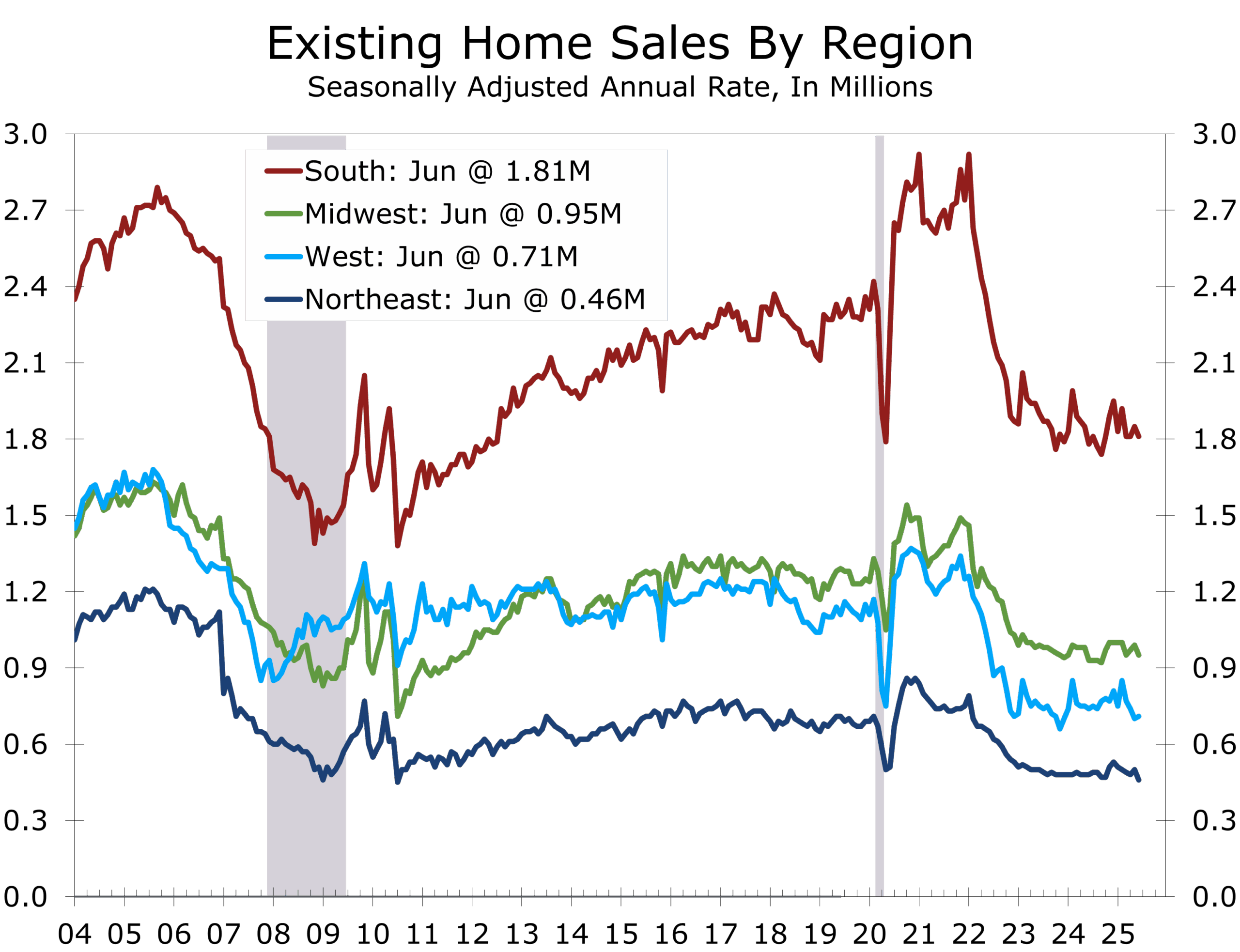

Across all housing types, the median price rose to a record $435,300, up 2.0% year-to-year. That marks the 24th straight annual gain, driven less by demand strength and more by supply distortions and a skewed sales mix. With higher-end properties accounting for a growing share, prices are rising even as unit volume remains muted. The small rise in sales in the West, which has the highest median home prices in the nation, also pulled prices higher. Home sales fell in the Midwest and South, where the median price is lower.

NAR estimates the average homeowner has gained $140,900 in equity over the past five years, but that wealth is locked in place by the “golden handcuff” of 3% mortgages.

Inventory slipped 0.6% in June to 1.53 million units, though levels remain 15.9% above a year ago. At 4.7 months of supply, the market is at its most balanced since 2016—but the relief is concentrated in higher-end and newly built homes. Entry-level supply remains structurally scarce.

Regionally, only the West posted a gain (+1.4%). Sales dropped sharply in the Northeast (-8.0%) and declined in the Midwest (-4.0%) and South (-2.2%). The South—home to nearly half of all sales—is seeing price growth stall, while the West continues to cool off its pandemic peak.

Participation remains narrow. First-time buyers held steady at 30%. Investors and second-home buyers fell to 14%, the lowest share since 2022. Cash buyers accounted for 29%—underscoring the outsized role of equity-rich households and institutional buyers in affordable submarkets in high-growth metro areas.

While housing directly accounts for less than 4% of GDP, its multiplier is far greater. Each sale fuels demand for everything from appliances and furniture to lending, legal, and moving services. That flywheel has slowed. Retail activity tied to housing—especially in furnishings and home improvement—remains weak. Labor mobility is constrained, weighing on productivity and wage growth.

Policy Implications

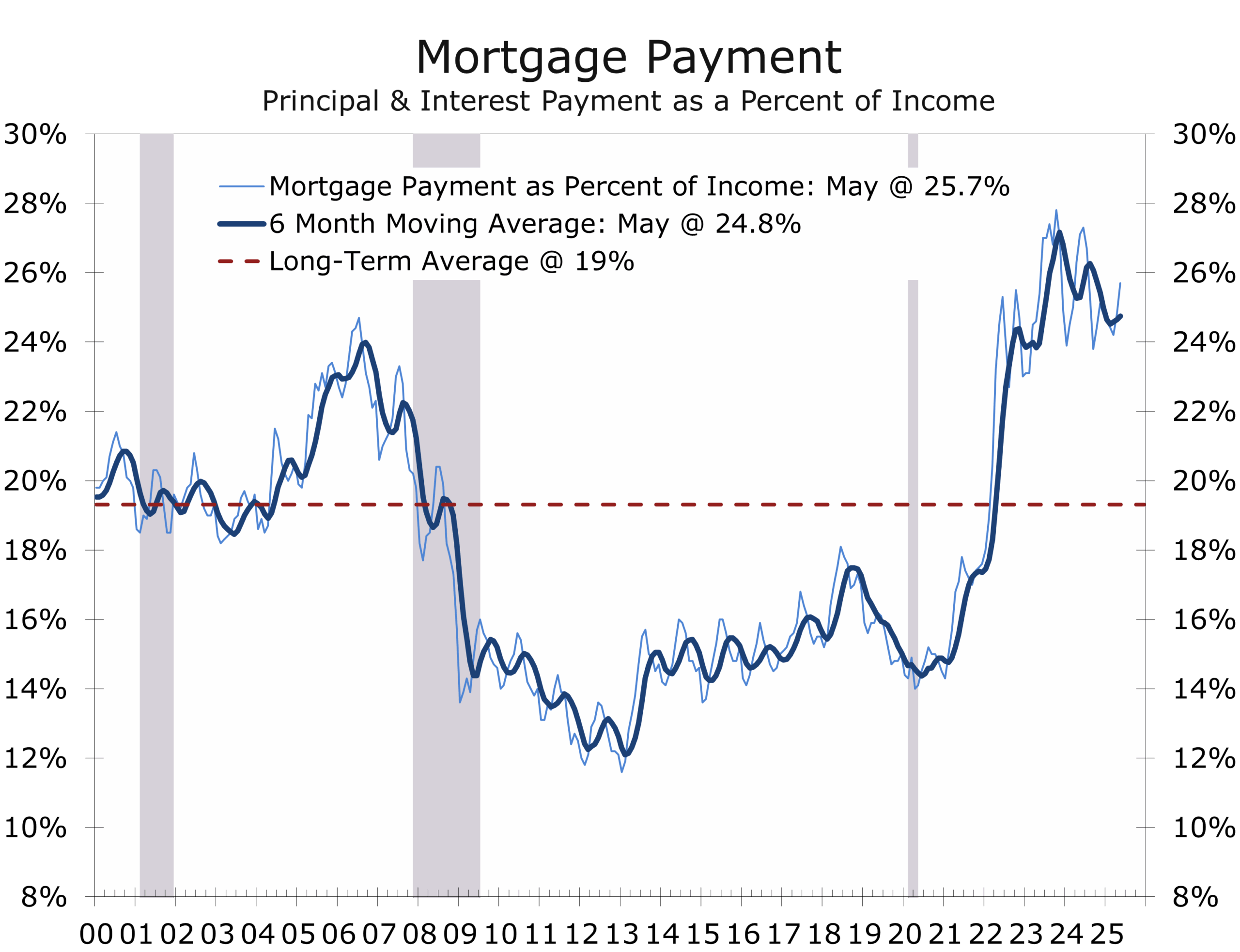

June’s weak sales underscore housing’s role as a growing policy bottleneck. For a median-income household putting 10% down on a median-priced home, principal and interest now consume over 25% of income—well above historical norms. With turnover frozen, lower rates are not translating into broader economic momentum. A drop toward 6% could spur some demand, but structural constraints run deeper.

Years of underbuilding, restrictive zoning, and limited entry-level supply continue to suppress market access. Fiscal tools like down payment assistance, first-time buyer credits, and portable subsidies can help on the margin. But real relief depends on zoning reform, faster permitting, and incentives for infill—none of which are quick fixes or politically easy.

Housing’s stagnation is no longer just a sectoral issue; it is a macro headwind. It is curbing labor mobility, dampening inflation adjustment, and weakening the impact of monetary easing. The shelter component of CPI remains sticky in part because turnover is too low.

Housing is not collapsing—but it is not healing either. Without improved affordability and stronger policy support, it will continue to drag on growth and limit the effectiveness of Fed rate cuts.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 23, 2025

Mark Vitner, Chief Economist

(704) 458-4000