Liberation Day Tariffs & Implications

- President Trump’s “Liberation Day” initiative places a 10% tariff on all U.S. imports, with additional reciprocal tariffs of up to 49% targeting trade deficit-heavy nations.

- The administration aims to reduce the trade deficit, reshore manufacturing, and enhance national security by reducing reliance on foreign supply chains in critical industries.

- Early indicators suggest economic fallout, rising inflation, and declining business confidence, with reduced expectations for growth amid fears of retaliatory tariffs.

- Our initial analysis is that tariffs will be more disruptive to the U.S. economy and will likely prompt a response from key trading partners.

- We have further reduced our forecast for 2025 economic growth and raised our inflation forecast. The impact on consumer prices is likely to be less than feared, however.

- We remain optimistic that current trade turbulence will drive a necessary update to the post-World War II trading system and a reworking of NAFTA/USMCA to ensure a better deal for the U.S., Canada and Mexico.

President Trump’s “Liberation Day” tariff initiative represents a major shift in U.S. trade policy. Implemented under the International Emergency Economic Powers Act (IEEPA), the plan declares a national emergency to address unfair trade practices and persistent trade imbalances. The policy establishes a minimum 10% tariff on all U.S. imports, while additional reciprocal tariffs of up to 49% target countries with substantial trade surpluses with the U.S., including Cambodia (49%), South Korea (25%), and the European Union (20%).

Additional executive actions include:

- A 25% tariff on light vehicles (effective April 3).

- A 20% tariff on Chinese imports.

- 25% tariffs on steel and aluminum, with tariffs on key auto parts phased in by July.

Liberation Day is aimed at correcting the nation’s large structural trade imbalance.

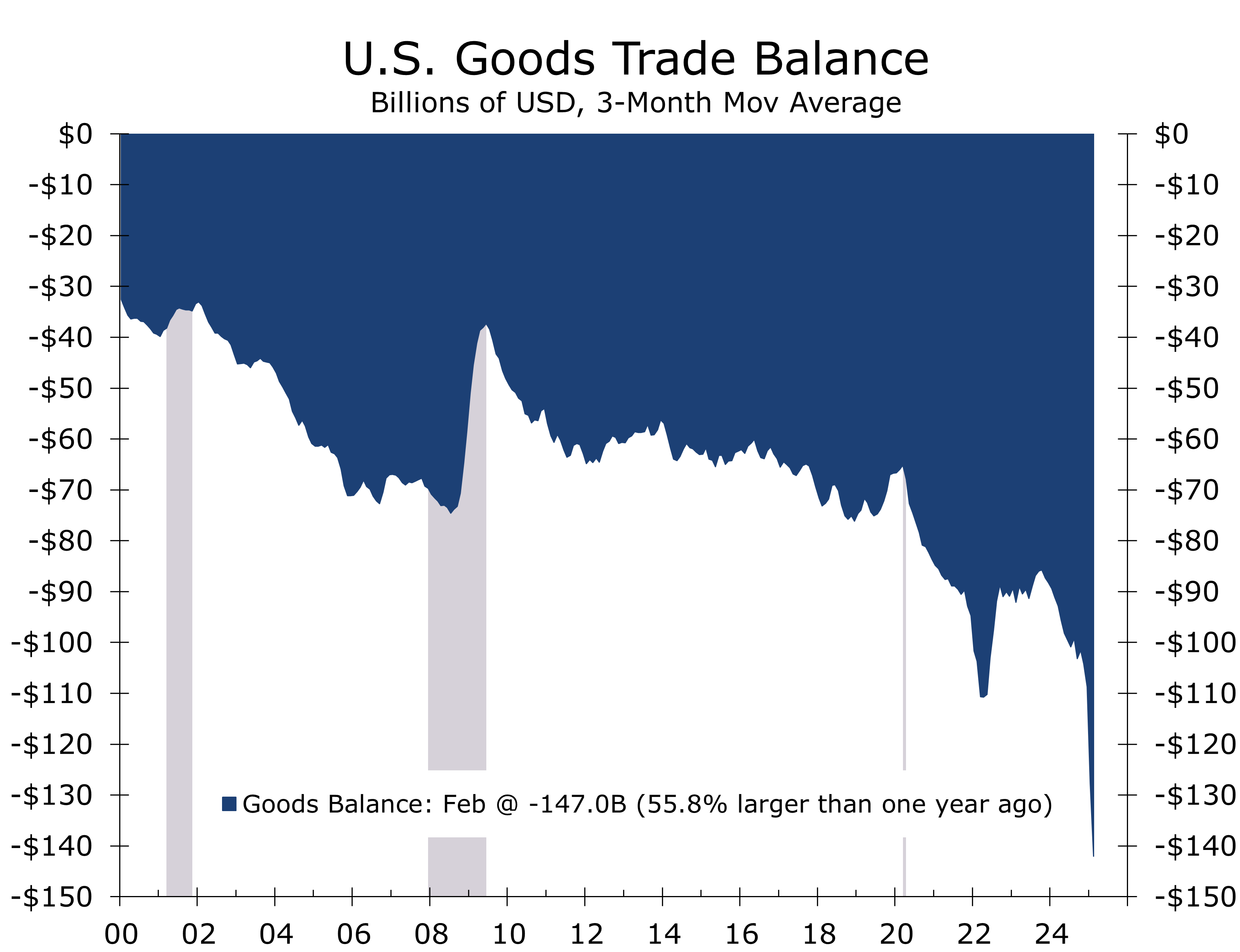

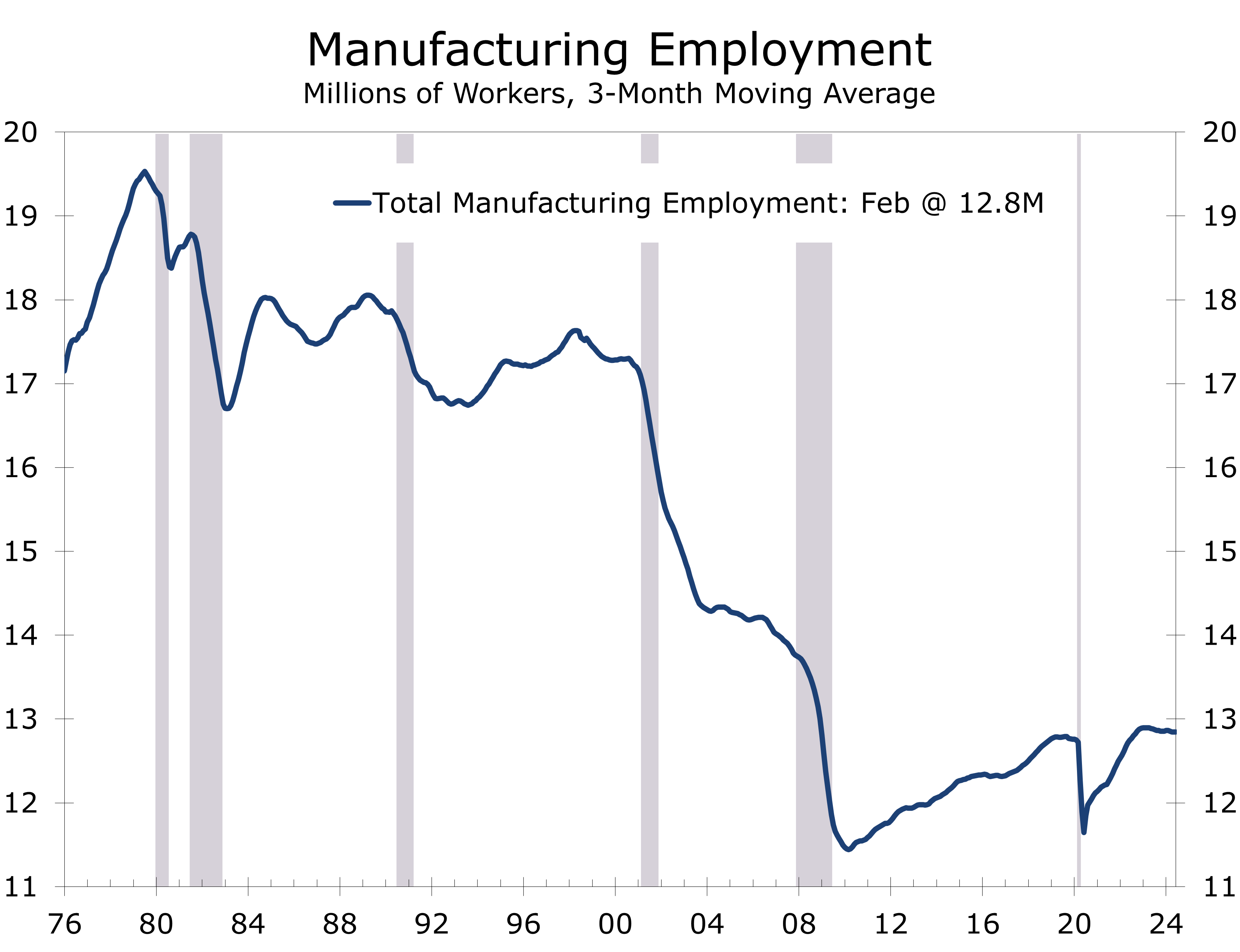

“Liberation Day” is aimed at correcting the nation’s structural trade imbalances. The U.S. trade deficit in goods reached $1.2 trillion in 2024, and manufacturing’s share of GDP declined from 28.4% in 2001 to 17.4% in 2023, contributing to the loss of 5 million manufacturing jobs since 1997. The auto sector alone posted a $93.5 billion trade deficit in 2024, underscoring the push for reshoring production.

The initiative also aims to promote fair trade by addressing tariff disparities, such as the U.S. 2.5% tariff on passenger vehicles compared to the EU’s 10% and India’s 70%. Eliminating these gaps could increase U.S. exports to India by $5.3 billion and generate $18 billion annually in remanufactured goods.

National security concerns also factor into the policy. The administration aims to reduce reliance on foreign supply chains in critical sectors such as autos, pharmaceuticals, and microelectronics. The U.S. auto industry is operating at just 68.4% capacity, below its historical average of 74.9%. Other concerns include counterfeit goods, which cost the U.S. economy between $225 billion and $600 billion annually, and unfair trade practices such as currency manipulation and value-added tax (VAT) policies, which purportedly cost U.S. firms over $200 billion per year.

We remain optimistic that the current trade turbulence will prompt a much-needed update to the post-World War II trading system. The world is currently navigating a post-Cold War era under an outdated framework designed reflecting a different economic landscape. NAFTA and the USMCA, originally established to create a competitive trading bloc in response to China’s rise, must be reworked to prevent China from benefiting more than the U.S., Canada, and Mexico. Additionally, a robust strategy to address steel transshipments must be developed and enforced.

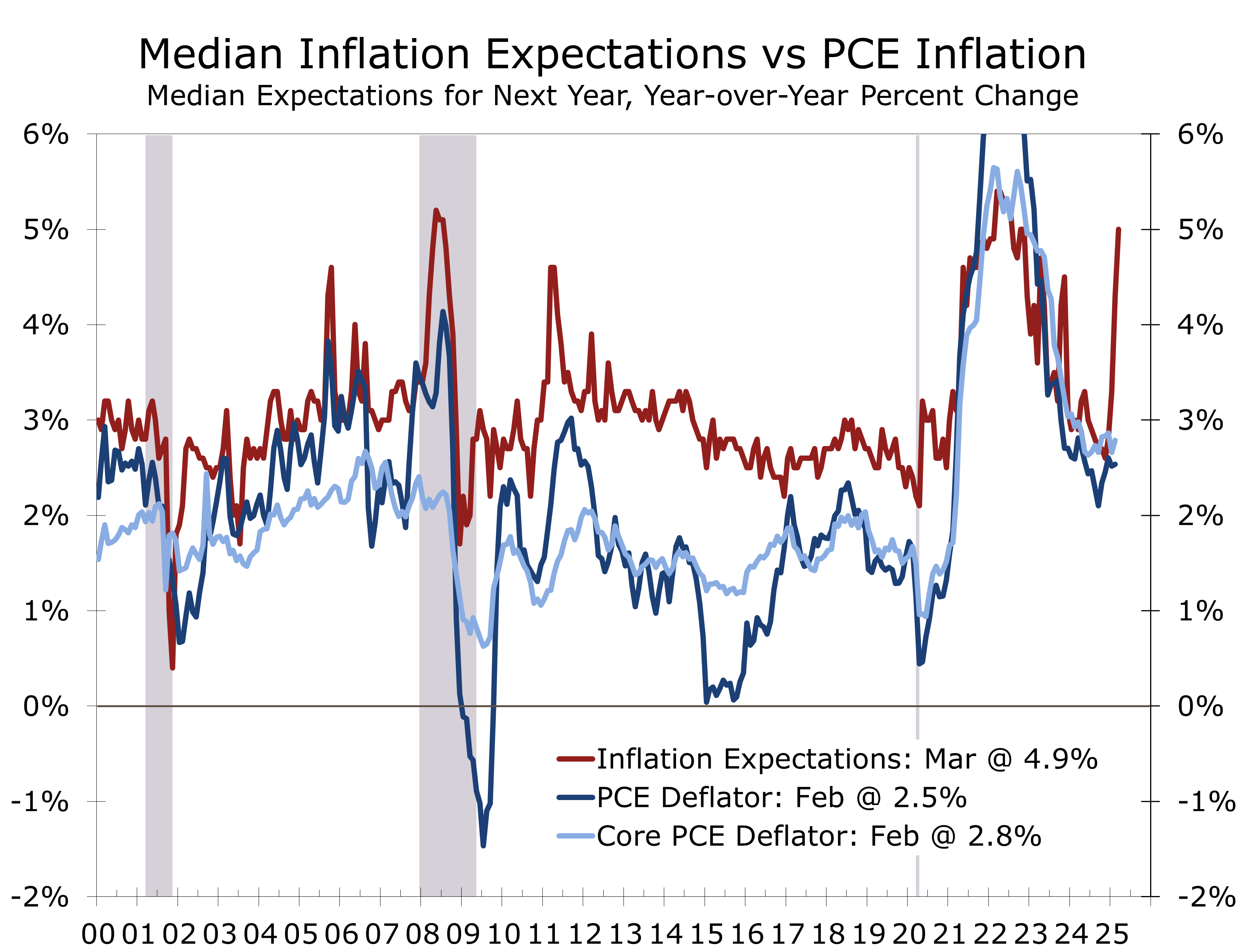

The economic fallout from “Liberation Day” is already evident. Despite contested studies predicting stronger GDP growth and job creation, early signs show negative implications. The Federal Reserve lowered its economic outlook in March, while boosting their inflation projections. Consumer and business confidence have also dropped sharply due to concerns over retaliatory tariffs and supply chain disruptions, while inflation expectations have spiked.

Our analysis indicates that the new tariff structure may be more disruptive than expected. The higher-than-anticipated tariff rates, even with exemptions, could burden the U.S. economy. Reshoring production will take time, causing short-term cost increases before domestic industries can scale up. Moreover, the uneven treatment of trade partners and targeted measures against China and the EU raise the risk of escalatory responses.

Tariffs are a blunt and infrequently used economic tool, often offering short-term benefits that fail to address underlying structural competitive issues. While unfair trade practices exist, they are not the primary cause of the U.S. trade imbalance. The Trump administration views the tariff rates as a negotiation tactic to secure lower tariffs through bilateral agreements, but this outcome seems overly optimistic, contributing to global market volatility and increased economic uncertainty.

The 10% minimum tariff is designed to be permanent and potentially could generate $300 billion annually. Imports will likely fall, however, so the tariff duties would likely be less. The revenue would help reduce the deficit or provide tax relief and can be at least somewhat justified, given the U.S. Navy’s outsized role in protecting global trade routes, ensuring freedom of navigation that otherwise would be more uncertain and costly to transit.

Tariffs are based on the dutiable value, which is typically much lower than the retail price.

Tariff Impact on Consumer Goods:

It is essential to note that tariffs apply to the landed value of imports, excluding shipping, insurance, and financing costs. For clothing, the dutiable value typically represents only 10% of the retail price, while for automobiles, it accounts for about 65%.

For a $50,000 imported car subject to a 25% tariff:

- The dutiable value is approximately $32,500 ($50,000 × 0.65).

- The tariff adds $8,125 ($32,500 × 25%).

- If fully passed on, the price could rise to $58,125, a 16.25% increase.

However, the actual impact may be lower. Some consumers may shift to domestic models, while others may delay purchases, waiting for market conditions to stabilize. Additionally, manufacturers and dealers might absorb part of the cost, making actual price increases more variable.

For smartphones, where tariffs on Chinese and Vietnamese imports were unexpectedly high, the dutiable value is typically $350–$400 per unit (about 50% of retail price). A 46% tariff would add approximately $175 to an $800 smartphone if fully passed on.

Revised Economic Outlook:

Ultimately, we remain optimistic that the current trade turbulence will prompt a much-needed update to the post-World War II trading system. We have long argued that the world is navigating a post-Cold War era under an outdated framework designed for a different economic landscape. NAFTA and the USMCA, originally established to create a competitive trading bloc in response to China’s rise, must be reworked to prevent China from benefiting more than the U.S., Canada, and Mexico. Additionally, a robust strategy to address steel transshipments must be developed and strictly enforced.

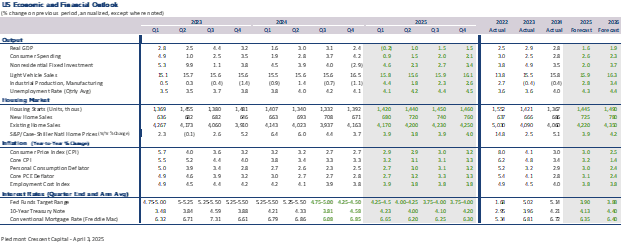

Given February’s soft consumer spending data and the continued decline in consumer confidence, we now forecast Q1 2025 real GDP to contract by 0.2%. The Atlanta Fed’s GDPNow model projects a 0.5% decline (gold-adjusted basis), with surging gold imports exaggerating the trade deficit’s drag. Imports of consumer goods and industrial materials have surged more than 55% over the past year, with much of that increase in the past three months – which may slice as much as 3 points off Q1 GDP growth.

For 2025, we have lowered our 2025 GDP growth forecast to 1.1% on a Q4-to-Q4 basis, 0.5 percentage points below the Fed’s latest projection. This implies a 0.5 percentage point rise in the unemployment rate. Inflation is also expected to run 0.5 percentage points higher, with the core PCE deflator projected to rise 3.3% in 2025. Despite higher inflation, we still expect the Federal Reserve to cut rates three times this year. We assign a 35% probability of recession—more than one in three, but still below an even likelihood.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

April 3, 2025

Mark Vitner, Chief Economist

Piedmont Crescent Capital

(704) 458-4000