Still Dancing but to a Softer Tune

-

- Personal income rose 0.4%, with after-tax income also up 0.4%, led by healthy gains in wages & salaries, which jumped 0.6% on broad-based strength.

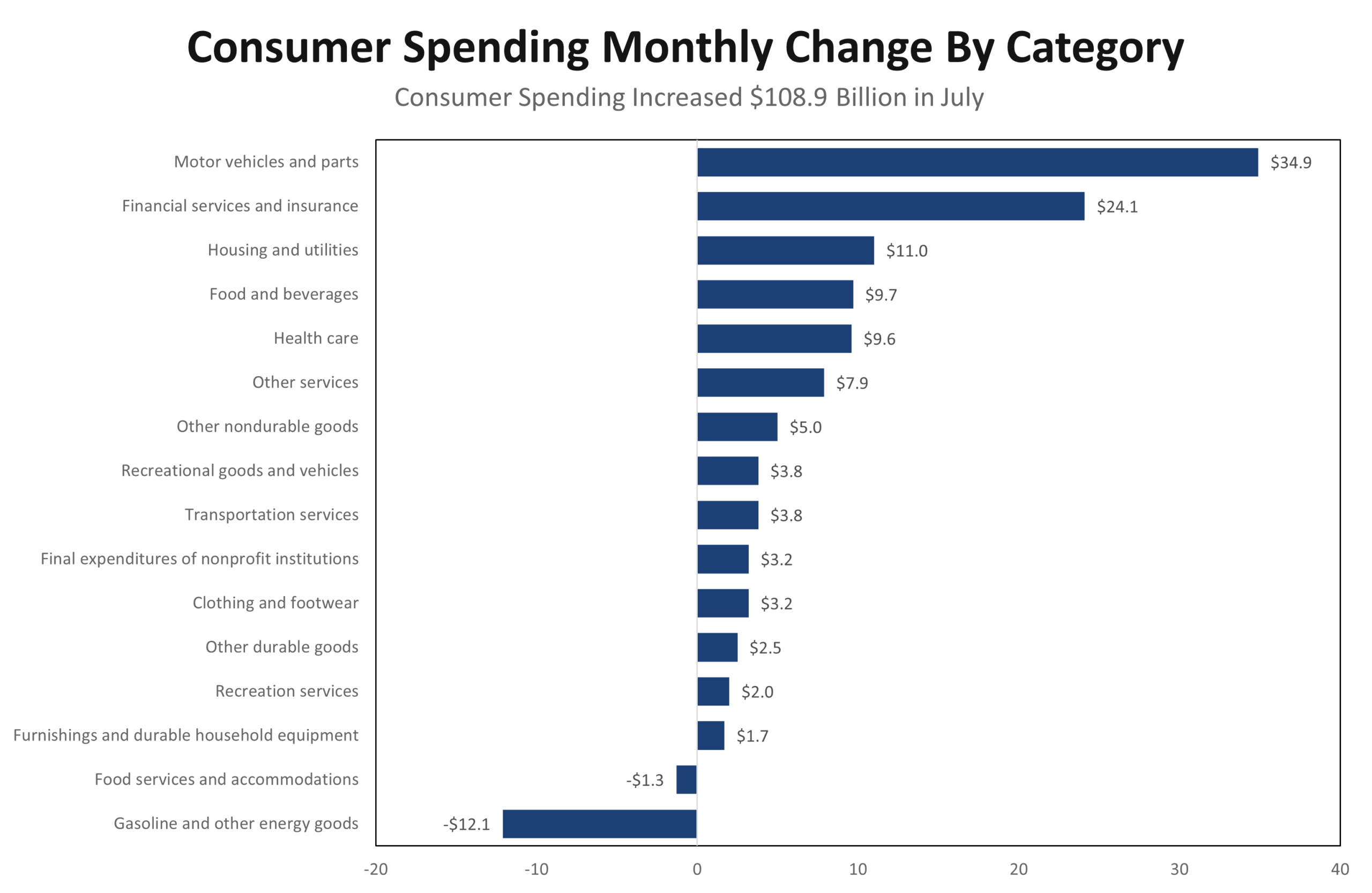

- Consumer spending rose 0.5% nominal, 0.3% real. Goods purchases solid — particularly durables (+2.0%) — while services slowed.

- PCE inflation rose 2% and is up 2.6% y/y, slightly softer than expected. Core PCE rose 0.3% and is up 2.9% y/y, broadly in line with expectations.

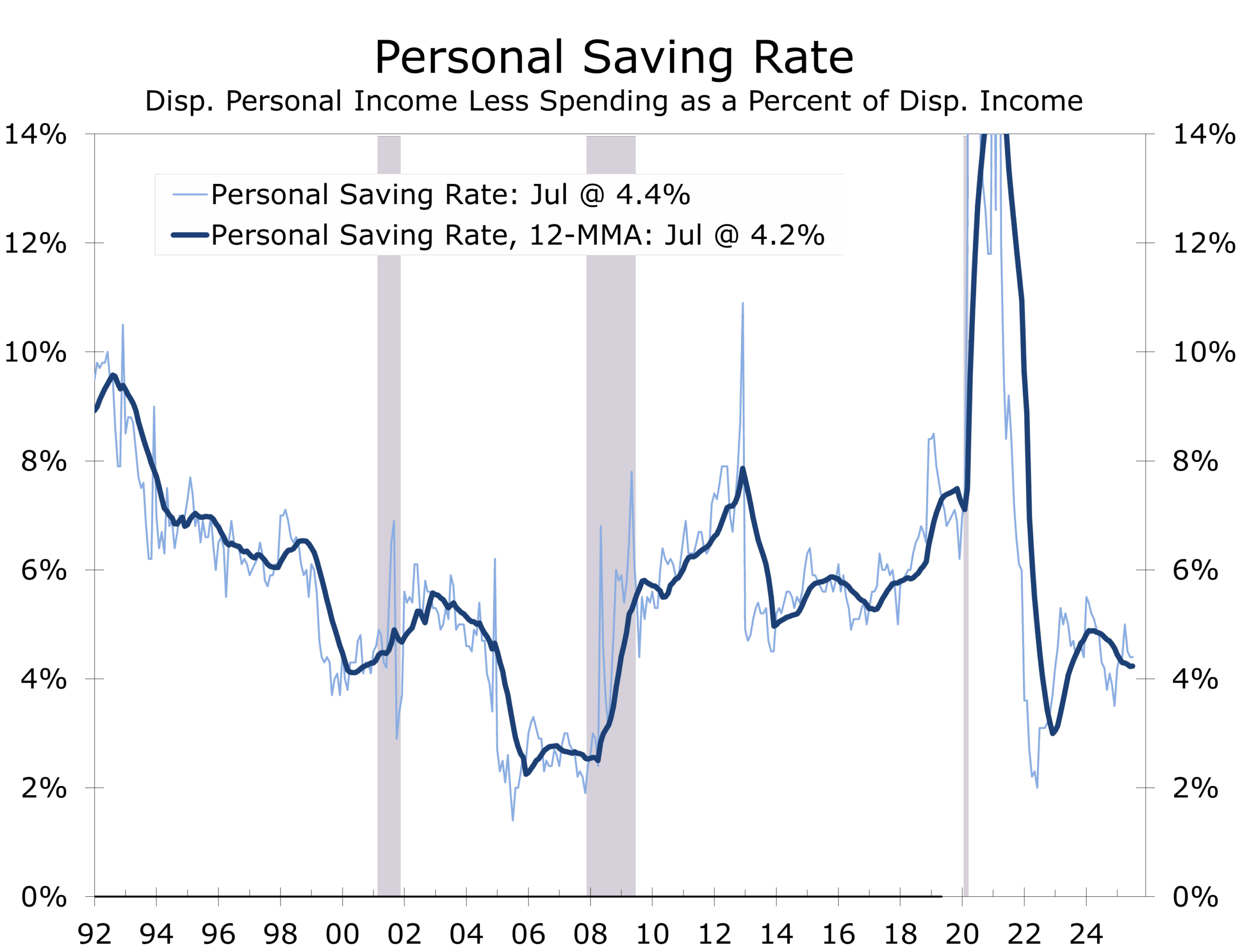

- The personal saving rate slipped to 4%, still well above the 2023 low of 3.5%, when recession fears were widespread.

- Consumer sentiment slipped in August, as inflation expectations edged higher despite softer PCE readings

- The latest data point to greater economic resilience heading into Q3, with optimism around back-to-school spending. A rate cut looks likely in September, but there is less urgency for the Fed to cut as aggressively as markets have priced in. Delivering fewer cuts could help bend the long end of the yield curve lower and provide more relief to housing.

From recession fears to resilience

In both 2022 and 2023, personal income and spending reports were read through the lens of imminent recession. Income growth was soft, often just +0.2% per month, as government transfer payments fell and disposable income stalled. The saving rate collapsed to 3.5% in July 2023, down sharply as consumers dipped into reserves to fund discretionary outlays on travel, concerts, and entertainment. Inflation, though moderating, remained sticky — core PCE was 4.2% y/y in July 2023, well above the Fed’s target.

By contrast, July 2025 shows the economy on a firmer footing. Income gains are broader, wages are accelerating, and real disposable income is rising modestly. Spending is advancing without relying heavily on saving drawdowns, and the saving rate — while still below pre-pandemic averages — is demonstrating resilience. Consumers are still dancing, but this time the floor feels steadier beneath their feet.

With the saving rate at 4.4% vs. 3.5% in July 2023, households appear less vulnerable.

With much of consumers’ pandemic-era savings drawn down, spending now more closely tracks wages and salaries, which are up a respectable 6.2% over the past year. Even factoring in 4% inflation, real consumption should remain solidly positive, providing some cushion against a likely slowdown in job growth. While hiring has slowed, firms are holding onto workers.

Spending headed into Q3: less boom, more balance

Real consumer spending rose +0.3% in July, led by durables (+2.0%). In 2023, spending was juiced by one-off events like Amazon Prime Day, blockbuster movie releases, and record travel demand. Today’s picture is steadier, with optimism around the back-to-school season giving Q3 momentum. That steadiness lowers the risk of an abrupt pullback and raises hopes for a solid holiday season.

Q3 consumer spending is tracking a 1.5% annualized rate, above earlier forecasts.

Motor vehicles and parts were a major contributor to July’s gains, and their tracking suggests real consumer spending could rise at a 1.5% annualized pace in Q3, versus their baseline of 1%. Part of July’s big increases was likely due to higher prices, however, with tariffs boosting new car prices, repair costs, and also the prices for major household appliances, such as washing machines. While one month doesn’t make a quarter, the stronger start lends upside risk to growth forecasts.

Inflation: better than expected, but risks ahead

The July PCE deflator rose +0.2% m/m, slightly below consensus, while the core deflator increased +0.3%, in line with expectations. Both headline and core are running in the “2s,” a marked improvement from 2022–2023, when core was above 4%.

Goods prices were generally flat-to-lower in July, helped by a sharp drop in energy. Services rose 0.3%, led by a jump in financial services tied to strong equity market gains. For now, consumers are enjoying an easier rhythm.

Yet tariffs are still widely expected to push the core PCE deflator back above 3% later this year. That looming shift tempers today’s relief and ensures the Fed will tread cautiously.

Consumers’ fears of inflation are much worse than actual inflation or the market expectations.

Consumers’ view: sentiment lags the data

Even with firmer income growth and softer inflation readings, the public mood remains dour. The latest University of Michigan survey shows consumer sentiment slipping, with inflation expectations ticking higher. Consumers’ fears of inflation are much worse than actual inflation or the market’s expectations.

Consumers are likely taking note of their reduced purchasing power from earlier price hikes. Higher prices for necessities — housing, groceries, new and used cars, and the ongoing increases in operating expenses like maintenance, repairs, and insurance — has left households with less discretionary income. While forecasters see resilience, households feel squeezed, which explains why recession fears remain elevated even as the data point to stability.

Fed outlook and the yield curve

Annual revisions, due September 26, will carry unusual weight. If wages and salaries are truly growing as solidly as July’s report suggests, the Fed has justification to take more time before cutting rates. A September cut is still expected, but after that officials may skip meetings or signal fewer cuts than markets currently anticipate.

One way to bring the long end of the yield curve down more sustainably might be to deliver fewer cuts in the near term. This approach could ease financial conditions in housing and other rate-sensitive sectors without stoking renewed inflation pressure.

Bottom line

Compared with the heightened fears of 2022–2023, today’s landscape looks sturdier. Consumers are spending steadily, wages are supporting growth, inflation is easing more than expected, and the saving rate is healthier. Recession worries remain high among households, but forecasters see an economy that is a little further from the edge — and a Fed that can adjust the tempo of easing with less urgency.

Consumers remain on the dance floor, and while the music may have slowed, the steps are steadier and more sustainable.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

August 29, 2025

Mark Vitner, Chief Economist

(704) 458-4000