Economic Indicator Report · ISM Manufacturing PMI, June 2026

Building Without Hiring

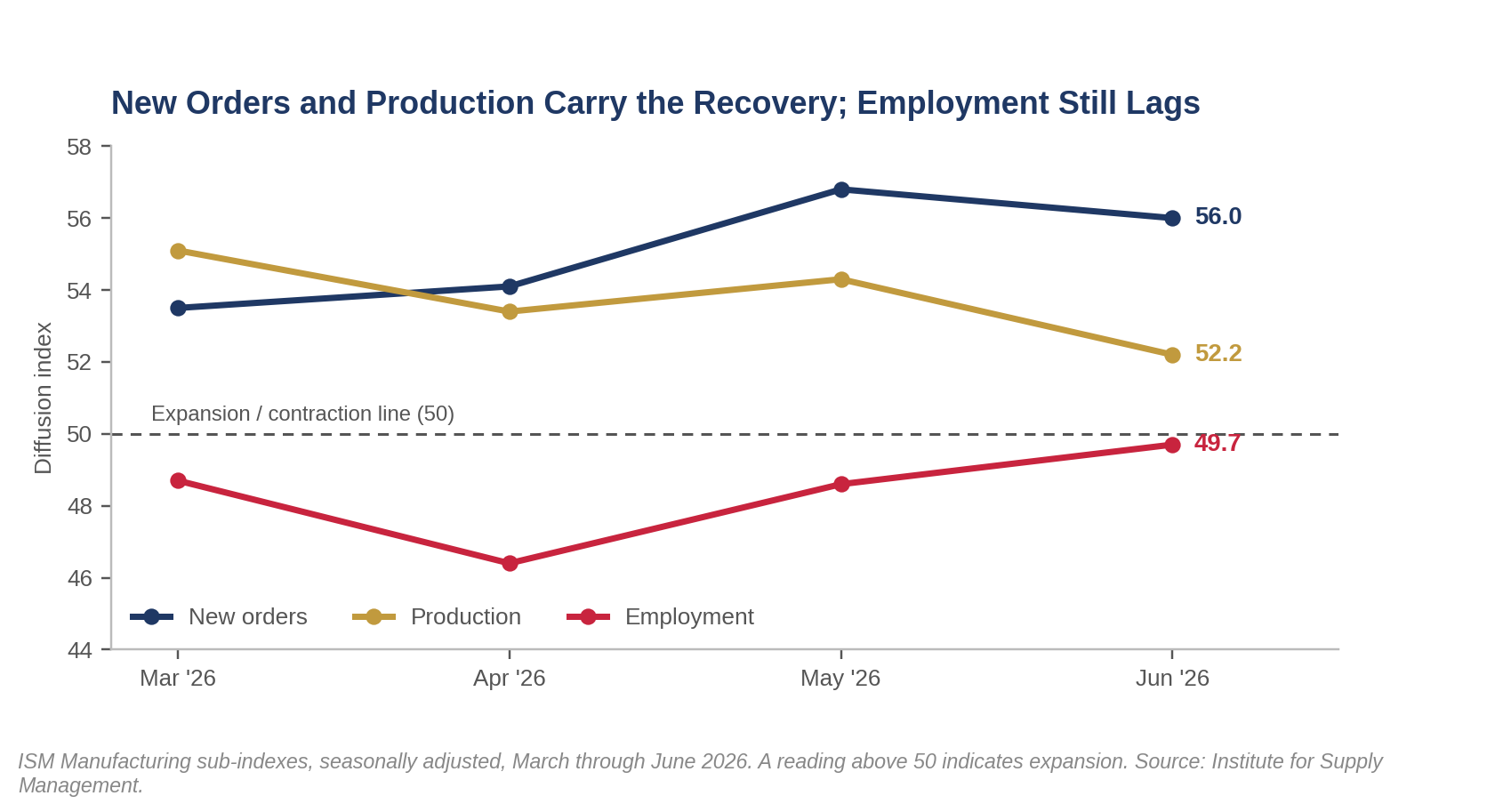

New Orders and Production Are Carrying the Factory Recovery While Employment Contracts for a 33rd Straight Month, the Capital Led Pattern Our Productivity Work Anticipated

Early Signals

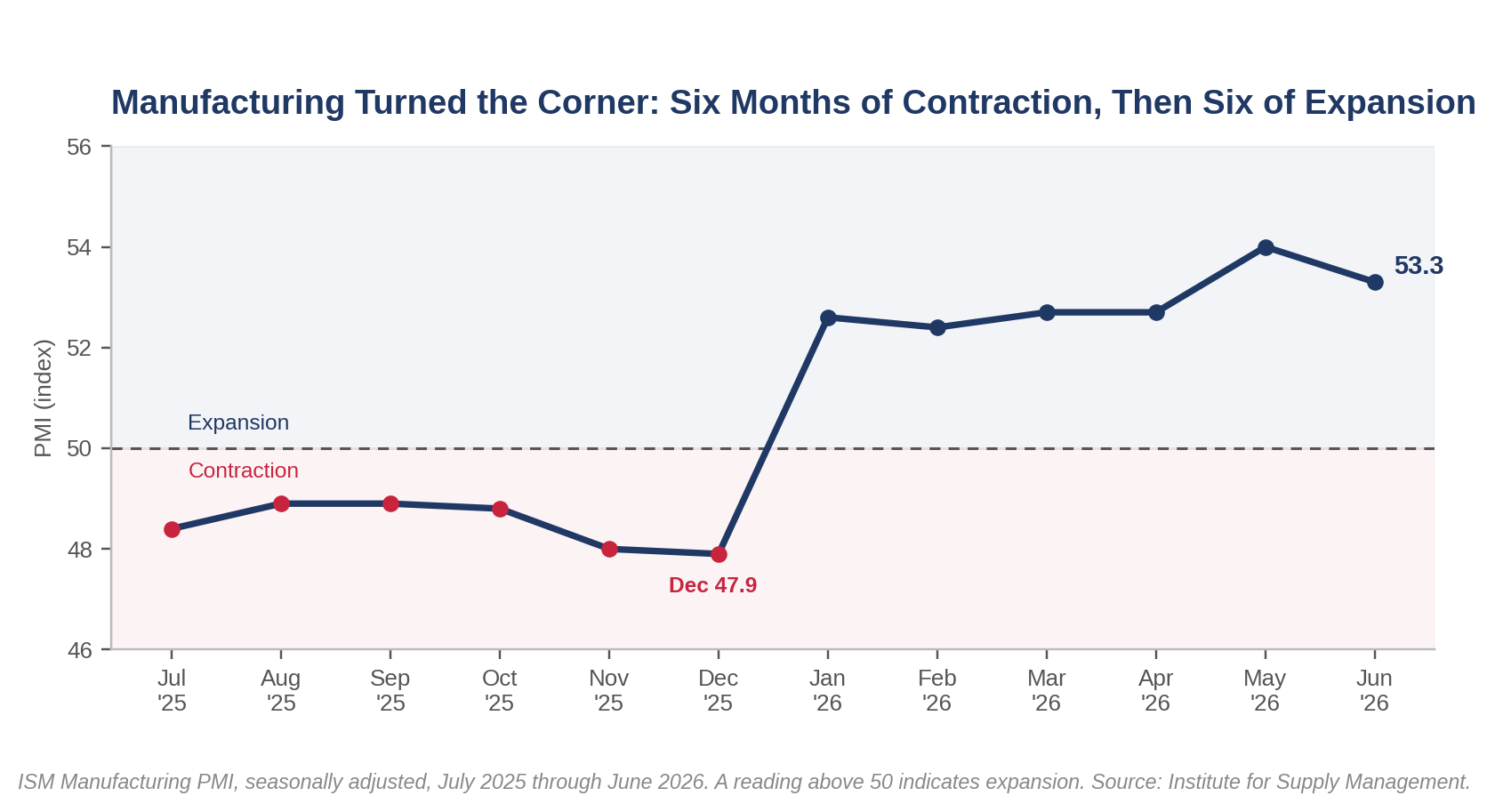

- The expansion held even as the headline eased. The Manufacturing PMI slipped 0.7 point to 53.3, a sixth straight month above 50 after a ten-month contraction, and the level remains consistent with the overall economy growing for a 20th consecutive month.

- New orders and production are doing the lifting. New orders, the most-leading component of the survey, held at 56.0, a sixth month of growth. Production expanded for an eighth straight month at 52.2. Demand and output are leading the recovery, employment is lagging.

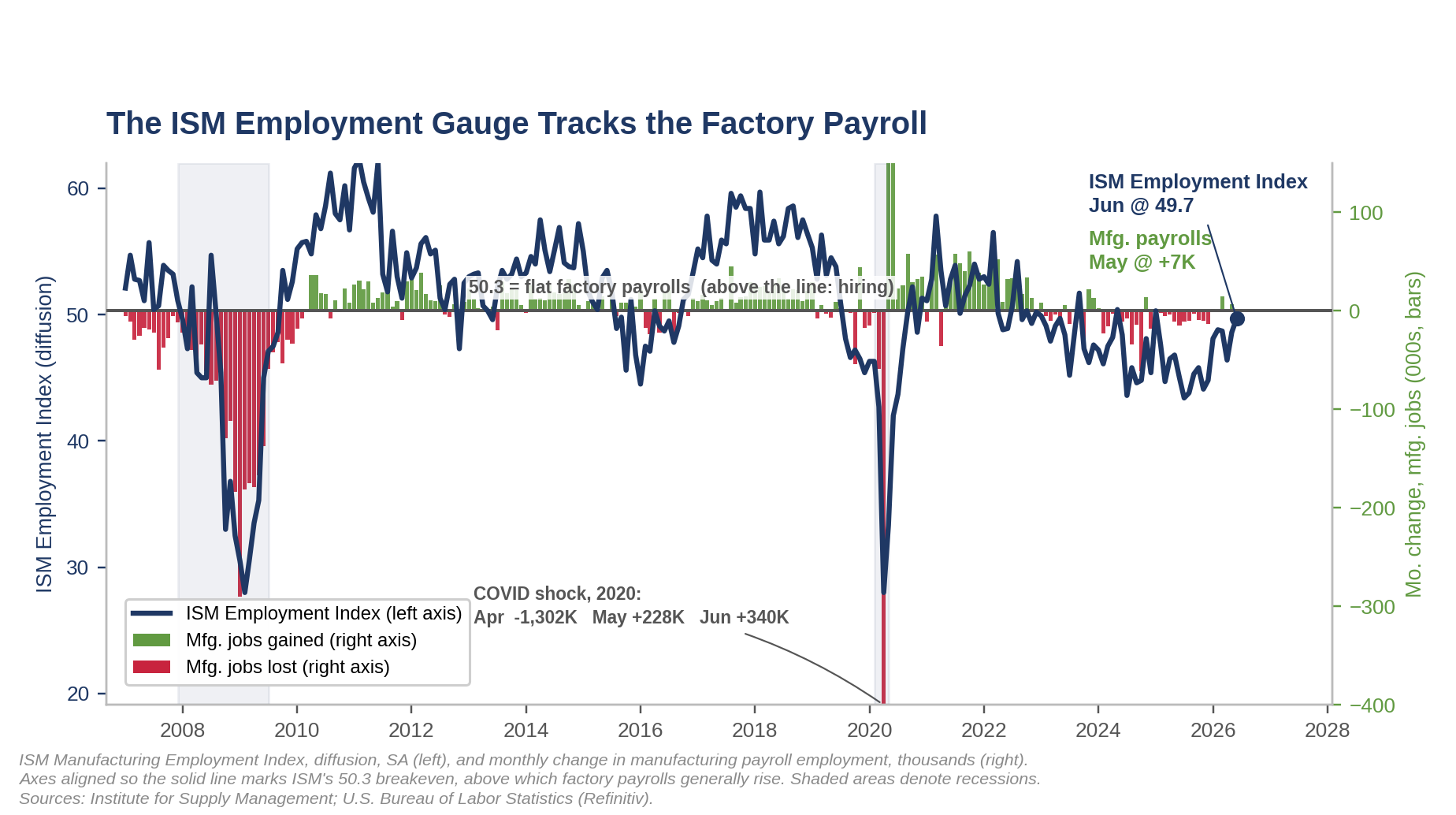

- Employment is again the laggard. The Employment Index rose 1.1 points to 49.7 but remained in contraction for a 33rd consecutive month.

- That gap is the signature of a capital-led recovery. Rising output on flat-to-falling hours worked is productivity, not weakness. The factory floor that sat out the 2023 to 2025 productivity boom is finally delivering through capital and automation rather than hiring.

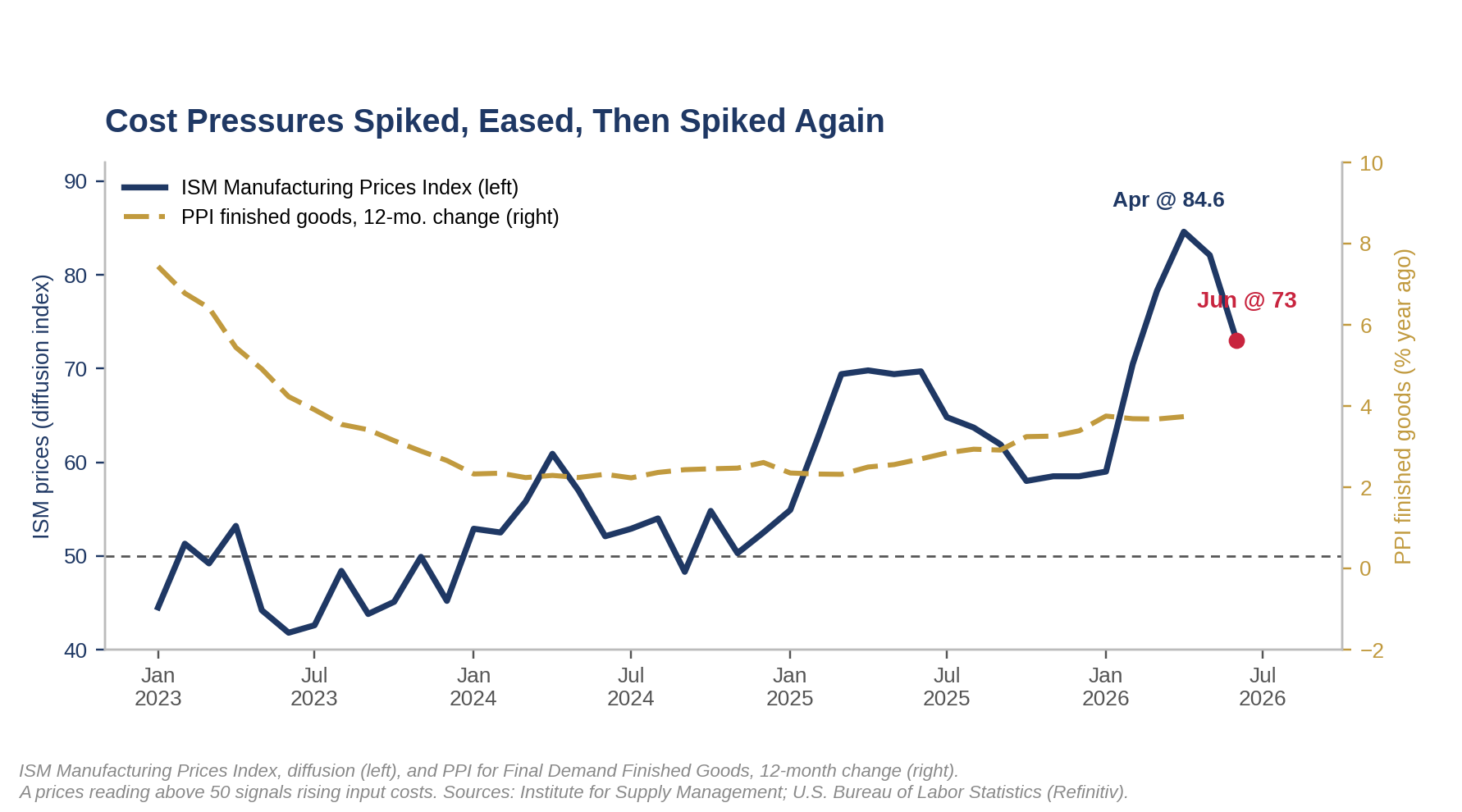

- Price pressure cooled sharply but did not clear. The Prices Index fell 9.1 points to 73.0, the largest drop since July 2022, yet still marks a 21st straight month that more managers reported rising input costs than reported falling costs. Some of the most persistent price pressures have been driven by steel and aluminum tariffs and Middle East oil.

- Geopolitics remains the swing factor. The Iran conflict surfaced in 31 percent of negative comments and tariffs in 17 percent, with half of panelists citing pricing volatility. A reopening of the Strait of Hormuz would ease the cost overhang substantially.

A Headline That Undersells the Story

The June PMI headline reads like a mild deceleration, but the more important signal is the regime change that came before it. The index eased to 53.3 from 54.0. Remember the ISM is a diffusion index. Any reading above 50 is consistent with improvement in the factory sector, while a reading below 50 is consistent with weakening conditions. The internals softened at the margin, with the New Orders and Production sub-indexes posting narrower gains than in May. Even so, four of the five components that feed the PMI were in expansion in June, one more than in May, and the composite remains consistent with real GDP rising at roughly a 2 percent annual pace. The larger picture is the one our first chart below tells. Manufacturing spent the back half of 2025 in a shallow contraction, bottoming at 47.9 in December, then flipped to six consecutive expansion readings in the low-to-mid 50s. A few tenths of wobble inside that new expansion is noise. The turn itself is the story.

Momentum is steady rather than accelerating, and that distinction matters. The share of firms reporting higher new orders fell to 22 percent from 31 percent, and the net new-orders reading dropped to plus 9 from plus 17, even as the index held near 56. In plain terms, the expansion is broad but no longer broadening. That is an early-to-mid cycle profile, not a boom, and it fits our view of a capital-led recovery that grinds higher without the vertical takeoff of a demand-driven cycle.

New Orders and Production Are Carrying the Recovery

The demand side of this report is doing its job. New orders expanded for a sixth month at 56.0, production for an eighth at 52.2, and both have sat comfortably above 50 all year. Backlogs are only barely positive at 50.5, but customers’ inventories remain deep in too-low territory at 42.3, a 21st month, a condition that historically foreshadows restocking and future production. Supplier deliveries slowed for a seventh straight month, a pattern that usually accompanies firming demand, though tariff friction and disruptions tied to the Iran conflict are behind much of the lengthening.

What the chart makes plain is the split between output and labor. New orders and production have held in the 52 to 57 band for four months while employment has sat below 50 the entire time. The lines do not converge. Orders and production are pulling the sector forward, and employment is trailing well behind. The divergence is not unusual at pivot points. The road to recovery in the factory sector is typically led by new orders, rising production, increased order backlogs and eventually rising employment. Uncertainty surrounding tariffs and the Iran War has likely made employers a bit more hesitant to add staff.

Employment Is Soft, and That Is the Point

The soft employment reading is not a crack in the recovery; it is the fingerprint of a capital-led one. The Employment Index registered 49.7, its 33rd consecutive month of contraction, and it has now contracted in 41 of the past 42 months. Because a reading near 50.3 is the level consistent with rising factory payrolls, June’s 49.7 implies manufacturing employment is still edging lower even as output climbs. Producing more with the same or fewer hours is the definition of rising productivity, and it is exactly what a sector leaning on recently installed plant, equipment, and automation looks like.

Beneath the sub-50 headline, though, the labor picture is quietly turning. The Employment Index improved 1.1 points, and the ratio of panelists hiring to those merely managing head counts flipped to 1.8-to-1, with 64 percent hiring, a near-reversal of the 1-to-2 ratio that prevailed at the start of the year. The recovery began with capital and is only now beginning to pull in labor. Gains in factory payrolls would significantly broaden the recovery and help make the rebound self-reinforcing.

Why the Floor Struggled, and Why This Time Looks Different

This is the pattern our productivity report focused on this past week. That report showed the factory floor sitting out the productivity boom, with total factor productivity falling in 70 of 86 manufacturing industries in 2023, a third straight broad-based down year, while the economy-wide engine of software, information, and data centers powered ahead. Our estimates for the two following years based on output by industry, employment and hours data suggest the data for subsequent two years were no better, with output rising in only 19 of 85 industries and hours falling in most. That was the 2024 and 2025 struggle in a sentence: weak output, shrinking hours, and productivity gains confined to a sliver of the sector.

The difference now is that the capital is finally showing up in output. Those productivity figures were a photograph of the old regime, taken before the reshoring and AI-driven capital build hit its stride in 2025. What the June ISM, and data for the first half of 2026 in general, capture is the handoff. The plant and automation put in place over the past two years are beginning to convert into rising orders and production, without a matching rise in payrolls. The factory floor is starting to earn the capital deepening it absorbed. Protein for the platforms through 2025, and the production line is finally being fed in 2026. Look for employment to rise after order backlogs improve a bit further.

Prices, Tariffs, and the Fed

The price relief is real, but it is relief from a very high level. The Prices Index dropped 9.1 points to 73.0, the sharpest fall since July 2022, and the share of firms paying more fell to 55 percent from 66 percent. June marked the 21st consecutive month of rising input costs, and any reading above roughly 53 is consistent with a rising producer price index. The cooldown owes much to retreating oil, with crude now listed among the commodities falling in price as the war premium fades, and to the disappearance of European energy surcharges. What has not gone away is the structural layer. Section 232 steel and aluminum tariffs continue to lift costs across the value chain, and panelists again flagged tariffs and pricing volatility as their dominant concerns.

For the Fed, a single sharp drop in a still-elevated prices gauge does not open the door to easing. Pair a firming, capital-led industrial recovery with input costs that remain well above their historical norm, and the case for a near-term cut weakens rather than strengthens. We continue to carry no 2026 rate reduction in our base case, and we still judge the next policy move as more likely up than down, in 2027 or 2028. New export orders slipping back into contraction at 48.5 is a reminder that tariffs cut both ways, but it does not change the domestic inflation math the Fed is watching.

Our Call

The June ISM confirms two things at once, and they point the same way. The manufacturing recovery is real, durable and, on a six-month view, still strengthening. The improvement is being delivered through output and productivity rather than job growth. A firming factory economy layered on a prices index still in the 70s does not give the Fed any room to cut but it does not demand a rate hike either. Our 2026 base case has the Fed on hold until at least December and likely well into 2027, when the next move is more likely to be a rate hike. That is typically what the Fed has done when manufacturing accelerates after a mid-cycle pause and the labor market is near full employment.

For positioning, we would stay with the capital-led expansion rather than fade it. The equipment, automation, power, and semiconductor supply chains doing the work in this recovery remain the place to be, and the soft factory-employment reading is a reason to lean into the productivity leaders, not away from the sector. With input costs still elevated and the long end still under-compensated for fiscal and geopolitical risk, we remain cautious on duration.

This report is produced by Piedmont Crescent Capital for informational purposes only and does not constitute investment, legal, or tax advice or a recommendation to buy or sell any security. Views are as of the date of publication and are subject to change without notice. Underlying data are from the Institute for Supply Management Manufacturing PMI report for June 2026 and from the U.S. Bureau of Labor Statistics. Past performance is not indicative of future results.