Housing Starts Bounce Back in February

- Housing starts increased 11.2% to 1.501 million SAAR, though the previous two months’ starts were slightly revised lower.

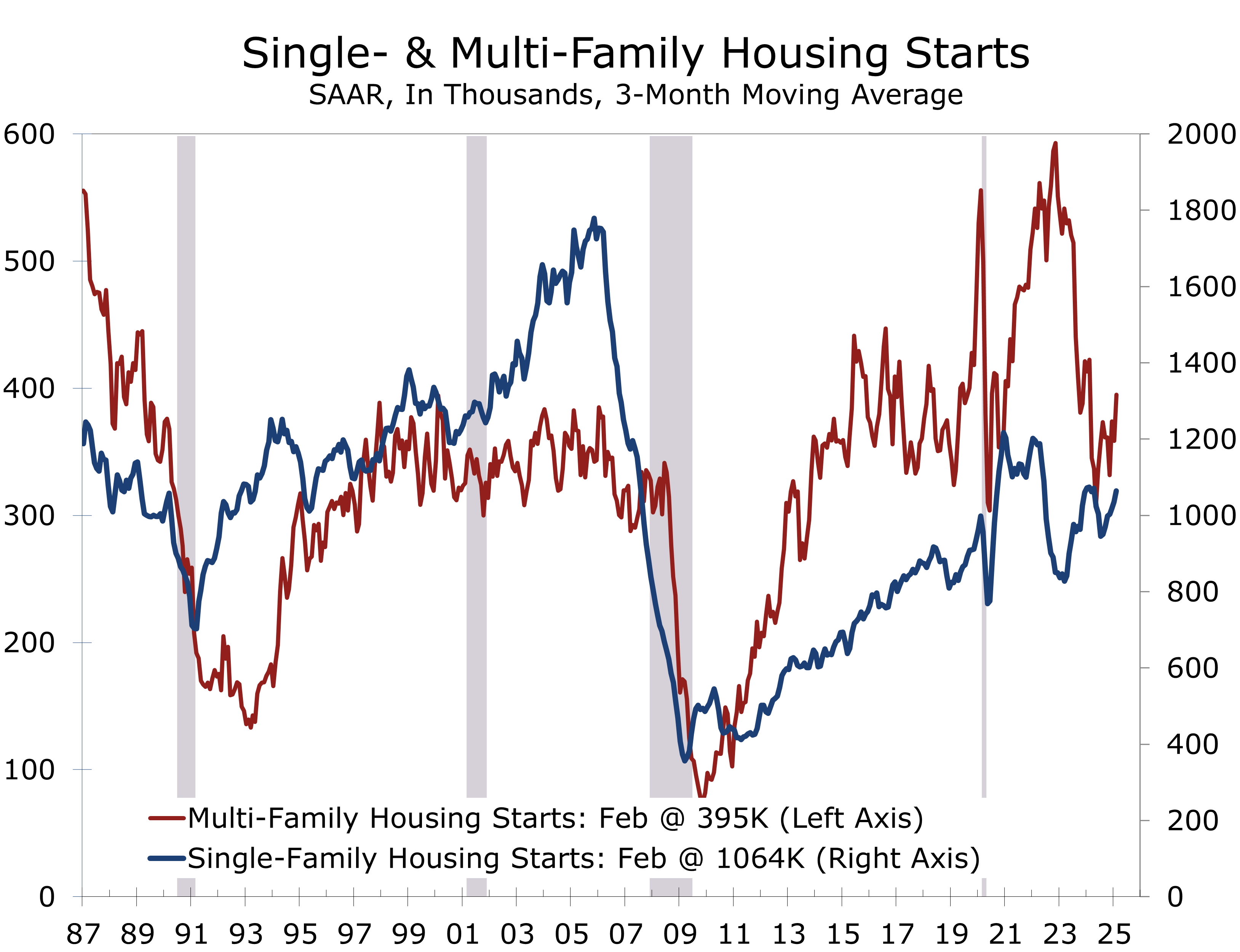

- Single-family starts rose 11.4% to a 1.108 million unit pace, the highest level since February 2024. Multifamily starts increased 10.7% to a 393,000 unit pace.

- Building permits declined 1.2% to 1.456 million units, with single-family permits nearly flat at 992,000 units (down 0.2%) and multifamily falling 3.1% to 464,000 units.

- Weather impacts were evident across the country, with starts soaring in the Northeast (+47.4%) and South (+18.3%), rising solidly in the West (+5.9%), but tumbling in the Midwest (-24.9%).

- Housing completions fell 4.0%, with single-family completions rising 7.1% and multifamily completions falling 20.8%.

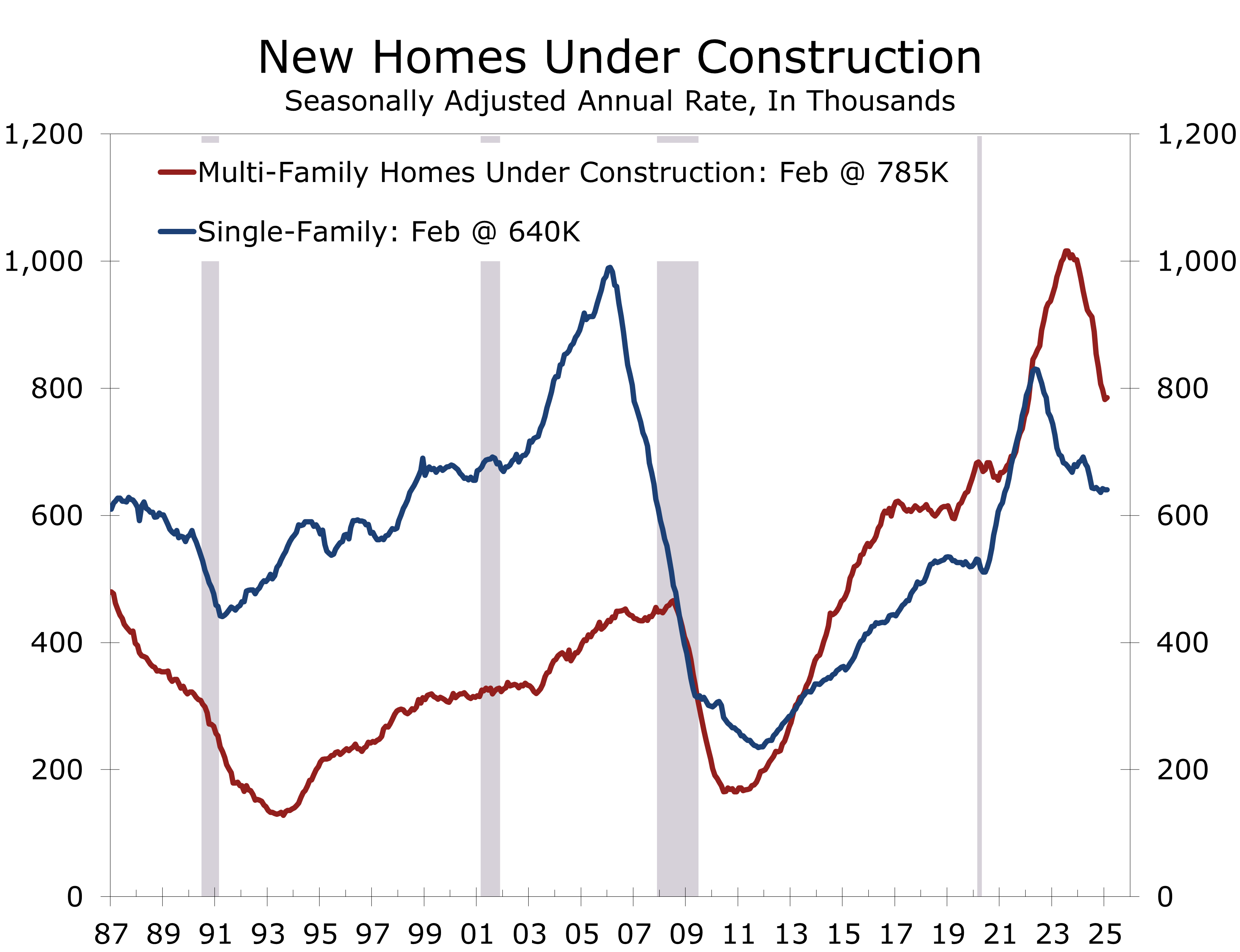

- Units under construction edged up 0.1%, with single-family units flat and multifamily units up 0.3%.

- Homebuilding faces a challenging year. High home prices, elevated mortgage rates, a weakening labor market, persistent inflation and policy uncertainty are keeping many potential buyers on the sidelines.

Home building rebounded in February, with housing starts surging 11.2% to a 1.51 million unit seasonally adjusted annual rate (SAAR). This increase exceeded expectations for a modest rebound following January’s weather-related slowdown. Building permits—which tend to lead starts by 1 to 2 months and are less influenced by weather distortions—dipped 1.2% to a 1.456 million-unit pace. While the stronger February housing starts data is a rare bit of good news, we doubt it reflects a momentum shift for the sector, which faces persistent headwinds from tariffs, labor shortages, and sagging consumer sentiment.

The jump in housing starts was broad-based, driven by an 11.4% increase in single-family starts to a 1.108 million unit pace and a 10.7% rise in multifamily starts to 393,000 units. The rebound reflects a normalization after January’s severe winter weather disrupted construction, particularly in the Northeast and South.

February’s stronger housing starts likely does not signal a momentum shift for home building.

Starts averaged 1.426 million units the past 2 months, close to the recent trend in permits and consistent with our 2025 forecast for 1.445 million starts. Building permits fell 1.2% and have averaged 1.465 million units the past two months. Single-family held steady at 992,000 units, while multifamily fell 3.1%, reflecting uneasiness about the torrent of new supply.

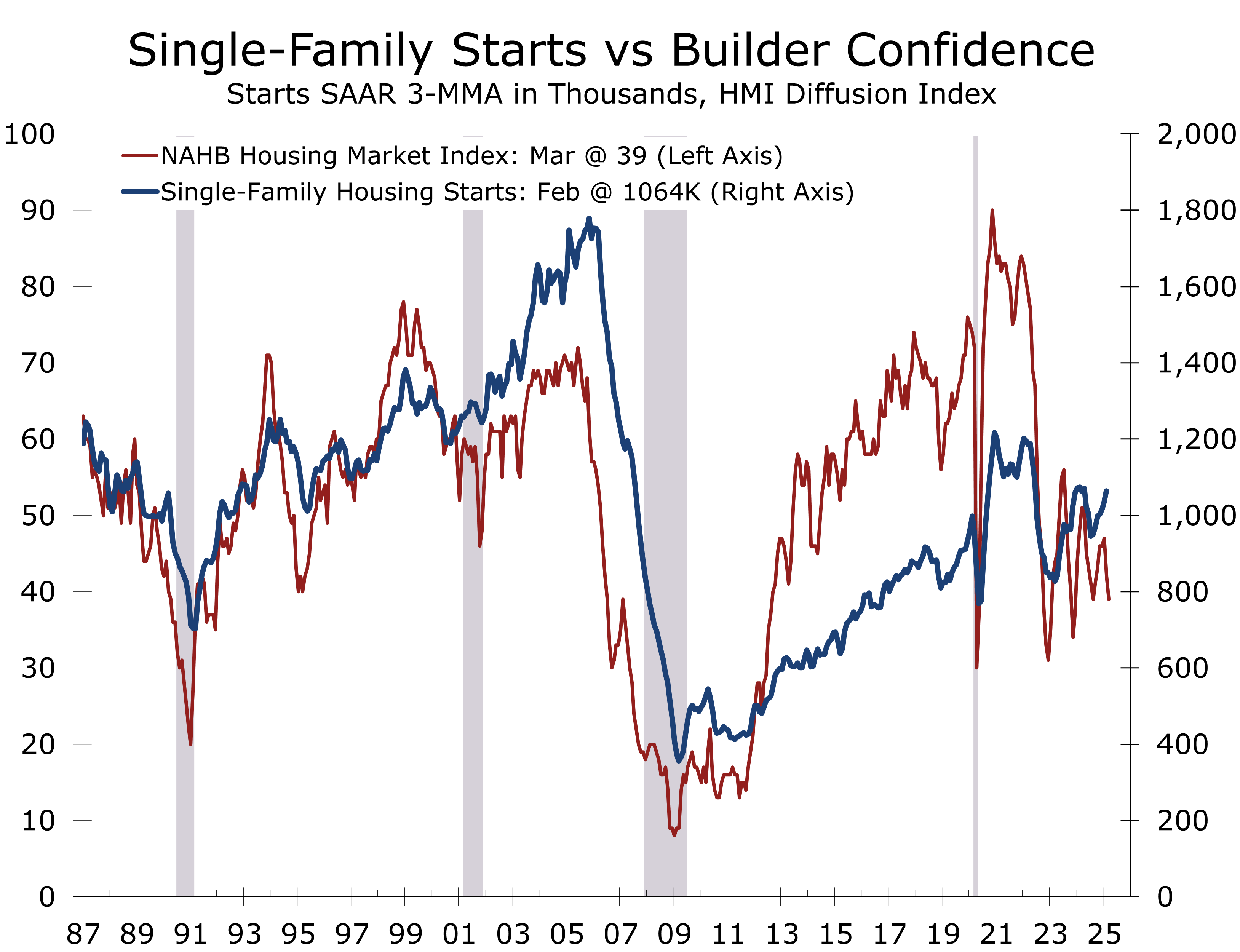

Builder sentiment, as measured by the National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI), fell to 39 in March—its lowest since August 2024. Homebuilders cited potentially higher input costs from tariffs and worsening labor shortages tied to immigration policies under President Trump. Despite a 40-basis-point decline in mortgage rates since January, builders noted growing buyer caution and weaker prospective buyer traffic. Prospective buyer traffic tumbled 5 points in March to 24, its lowest level in 15 months.

Builders remain exceptionally cautious, reflecting uncertainty and weak buyer traffic.

February’s rise in housing starts was concentrated in the Northeast (+47.4%) and South (+18.3%), which both rebounded from unseasonably cold winter weather in January. By contrast, starts rose a more modest 5.9% in the West and plunged 24.9% in the Midwest.

Permits were also mixed, with the Midwest posting an +8.9% rise. The South (+1.0%) also posted a modest gain, while permits fell in the Northeast (-15.3%) and West (-7.6%). Despite the drop, the West is proving resilient, following a 42.3% surge in January. The Midwest’s volatility underscores disparities driven by weather, economic conditions, and supply constraints.

Housing completions dipped 4.0%, primarily due to a 20.8% drop in multifamily units. Single-family completions rose 7.1%. Units under construction saw a negligible increase, yet remain down for the quarter, which will weigh on residential investment and is consistent our forecast for just 1.2% Q1 GDP growth.

While the quarter was soft, February’s stronger data provide a glimmer of optimism. The January-February average of 1.426 million starts, coupled with steady permits, suggesting a possible floor for home building. Sustaining this momentum faces significant hurdles, however. Tariffs are inflating input costs, labor shortages are intensifying, and economic uncertainty is eroding both builder and buyer confidence. While recent mortgage rate declines offer some relief, buyer wariness persists, as evidenced by the NAHB survey, casting doubt on the spring selling season.

The housing sector’s significance to the broader economy remains paramount. The Federal Reserve possesses levers to stimulate construction, notably by cutting short-term rates and narrowing the substantial spread between 30-year mortgages and 10-year Treasuries. Ending quantitative tightening would provide additional relief.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

March 18, 2025

Mark Vitner, Chief Economist

Piedmont Crescent Capital

(704) 458-4000