Housing Starts Decline Modestly in January

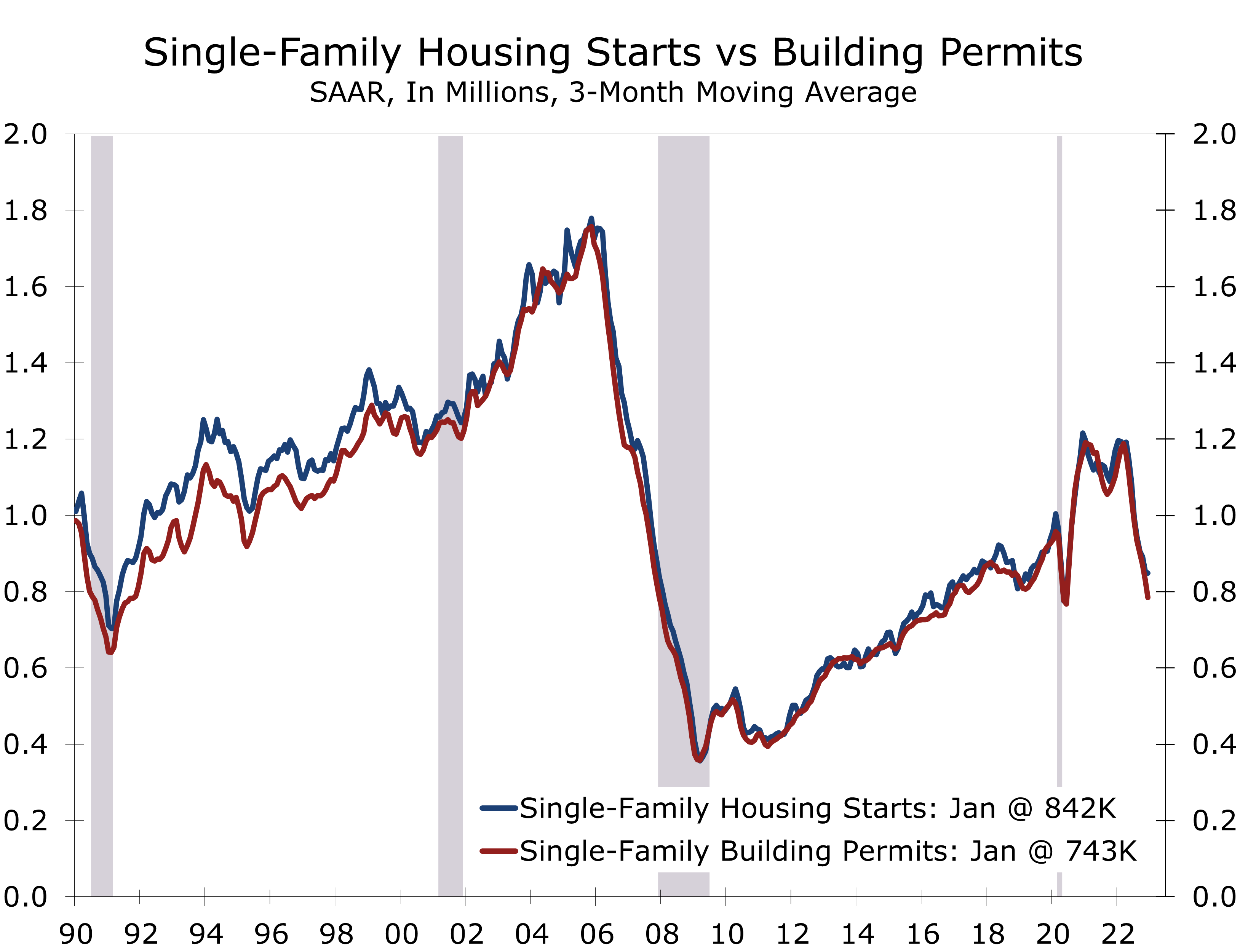

- Housing starts fell 4.5% to a 1.309-million unit pace. Single-family starts fell 4.5% to an 841,000 unit pace, while multi-family starts fell 4.9% to a 468,000-unit pace.

- The monthly housing starts data are extremely volatile during the winter months, when swings in weather conditions can lead to wide month swings.

- Weather appears to have influenced the data, with starts plunging 42.2% in the Northeast and 25.9% in the Midwest but rising 7.3% in the South and 5.5% out West.

- Permits are less impacted by the weather and were little changed in January.

- Last year’s slide in housing starts may be subsiding. The NAHB Home Builders’ Survey improved for a second month in February, reflecting a rise in present sales.

- Home builders continue to work down their backlog of work in process, with many making a concerted effort to get lean.

January’s 4.5% decline in housing starts broke a nascent string of improving reports for the housing sector. Home builders have reported a rise in buyer traffic in recent months and pending home sales and mortgage demand had shown some promise. Our sense is the pullback in mortgage rates brought some buyers back to the market that had canceled deals or put off home purchases when mortgage rate were closer to 7%. Those buyers came back in when rates fell back closer to 6%. Many builders also offered incentives to buy down mortgage rates.

While we would like to join the rising chorus of analysts expressing optimism about the housing market, we remain more cautious. Affordability remains extremely challenging and we have only seen a modest rebound in buyer traffic. Home builders have a huge backlog of single-family homes under construction and are actively working to reduce their inventory of completed homes and work-in-process.

Starts and permits still appear to be trending lower, as builders work to reduce inventory.

Housing starts are extremely volatile during the winter, particularly single-family starts, which rose 8.9% in December. Most of that rise was in the Northeast, where starts nearly doubled. Starts plummeted back to their prior trend in the Northeast in January but jumped to their highest level since June in the South, where weather was unusually mild. Permits are less influenced by the weather and do not show these wide swings. Starts and permits are both trending lower on a three-month moving average basis.

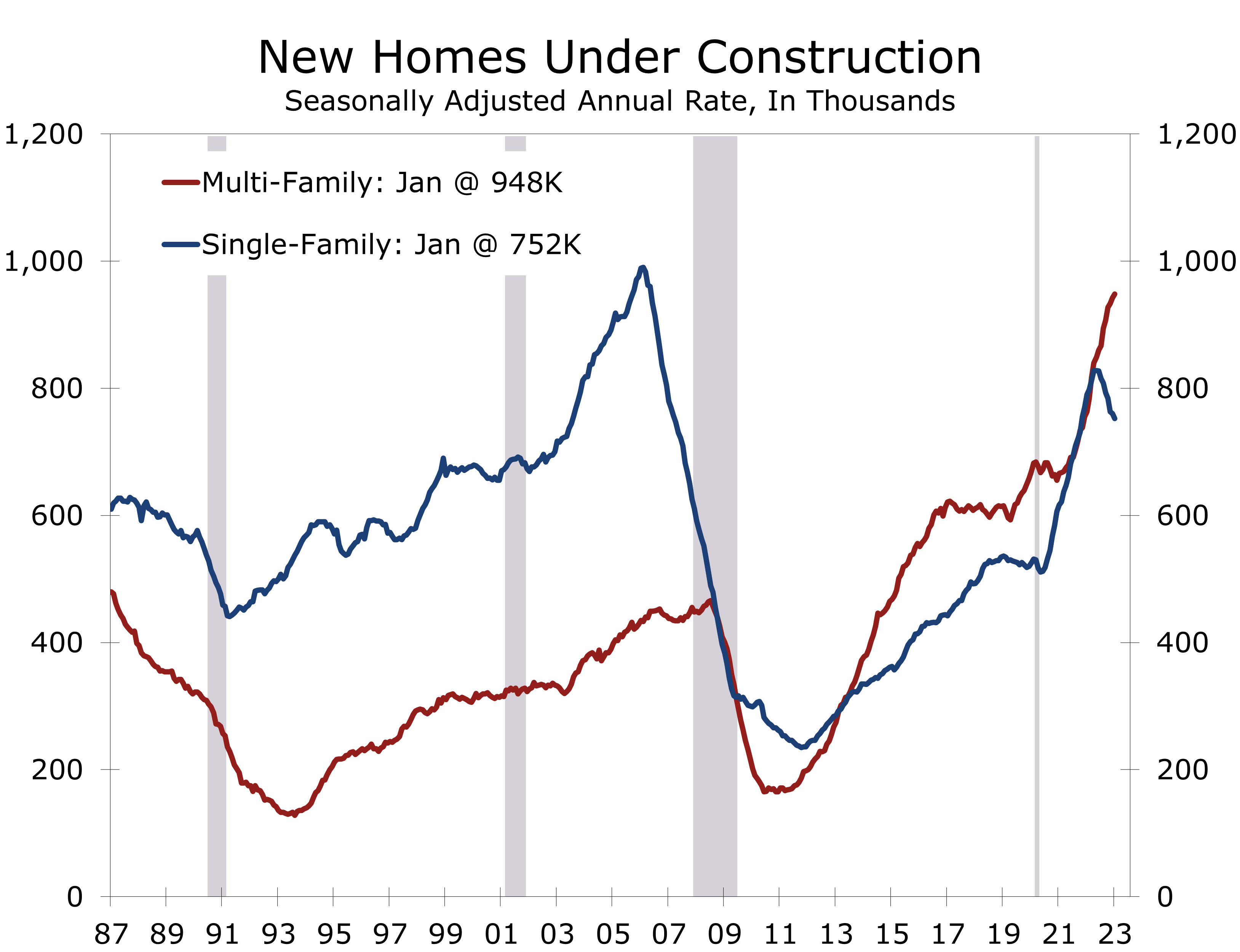

Multi-family starts fell 4.9% in January, while permits rose 2.5%. Both starts and permits are trending lower on a three-month moving average, however, as apartment developers appear to have their hands full with projects currently underway.

Shortage of materials and workers and the preponderance of mid-rise and high-rise apartment projects has stretched out the timeline for completing apartment developments. The number of multi-family units under construction, the overwhelming majority of which are apartments rose by 6,000 in January to a 948,000-unit pace, which is the highest since 1974. The number of authorized multi-family permits that have not been started also continues to trend higher.

Rents have been falling the past few months and lenders have tightened underwriting.

Demand for apartments has weakened in recent months, largely reflecting affordability issues. Rents have been declining the past few months and lenders have tightened underwriting standards for new developments. All signs point to fewer new multi-family projects entering the pipeline until the backlog of developments begins to clear and participants have a better sense of how demand is holding up. We are looking for around a 15% pullback in multi-family starts this year, and about a 20% drop in permits.

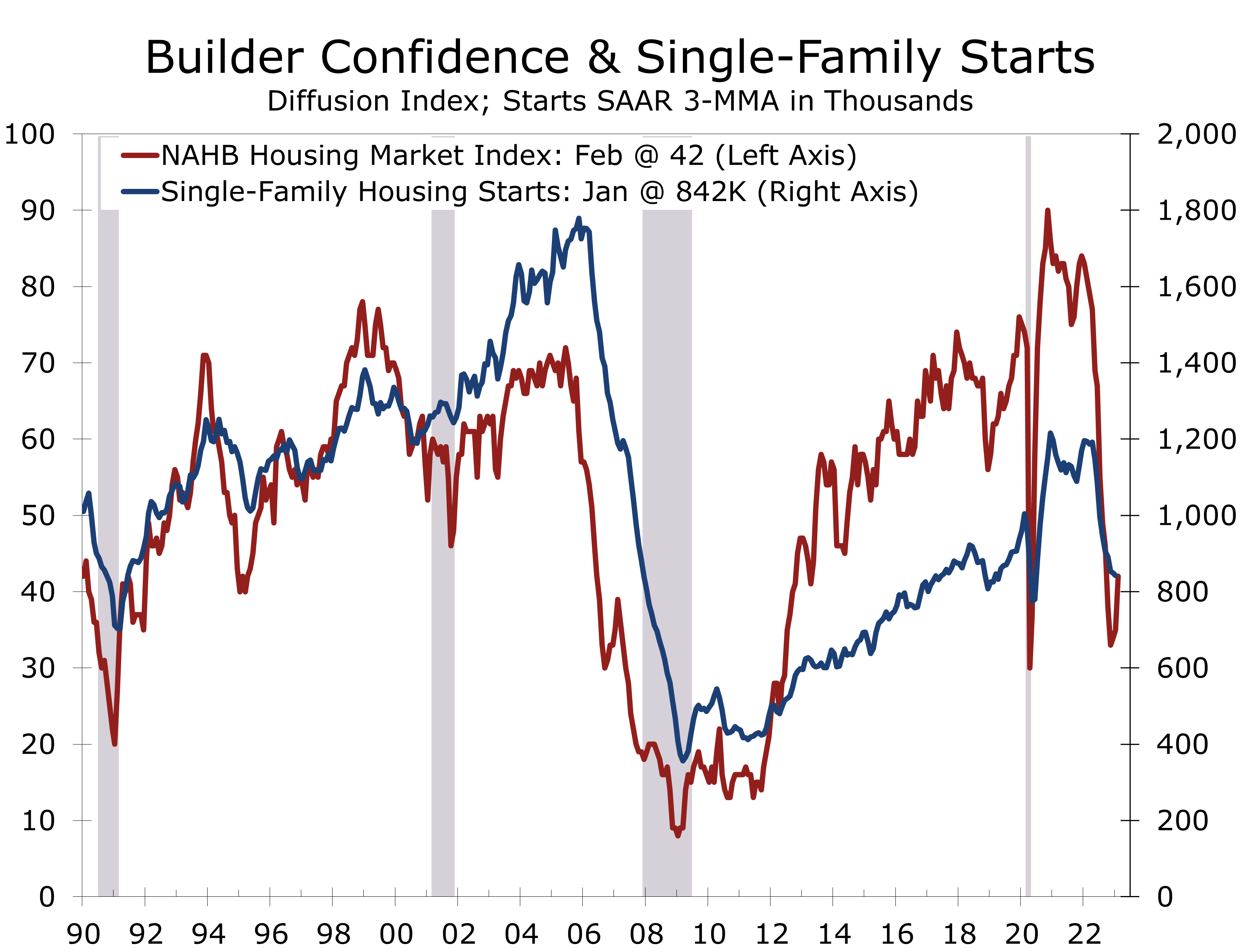

Back-to-back improvements in the NAHB/Wells Fargo Housing Market Index (HMI) boosted optimism ahead of January housing starts. The HMI jumped 7 points in February to 42, after rising 4 points in January. Any reading below 50 means more builders see conditions deteriorating than see them improving.

We suspect new home sales rose in January, confirming the improvement in builder sentiment.

The present sales index rose 6 points to 46, after rising 4 points in January. Expected sales over the next six months rose 9 points to 48, while prospective buyer traffic rose 6 points to 29. We suspect new home sales rose in January, reflecting lower mortgage rates and various incentives by builders to bring buyers back to the table. Builders have mostly been buying down mortgage rates, to reduce the sting from rising rates.

We feel it would be a mistake to interpret the bounce in builder confidence as a sign the housing market is stabilizing. Housing starts are almost certainly headed lower, as interest rates remain higher for longer. Builders will concentrate on clearing their construction backlog and will discount prices to point. Other than lumber, however, raw material prices are still rising.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.