Tariff Clouds Keep Inflation Fears Aloft

- Both the headline and the core CPI rose just 0.1% in May—well below expectations.

- Year-over-year, the CPI rose to 2.4%, while the core CPI held steady at 2.8%.

- Over the past three months, the CPI has decelerated to just a 1.0% annualized pace; the core CPI has slowed to 1.7%, the lowest since July 2024.

- Core goods prices slipped, including both new and used vehicles, but early signs of tariff pass-through are appearing in apparel, vehicle parts, and tech goods.

- Discretionary services prices—including airfare, lodging, and recreation—are moderating or outright declining.

- Real average hourly and weekly earnings rose 0.3% in May and are up 1.4% and 1.5% respectively year-over-year.

- The Fed is expected to hold rates steady next week, but tariff-driven inflation is likely to rise this summer. Producer prices will be more impacted by tariffs—suggesting margin compression. As tariffs erode consumer purchasing power, price gains in non-traded sectors may stall unless the Fed loosens policy more aggressively.

May’s CPI print offers the Fed at least a brief moment to exhale. Both headline and core prices rose just 0.1%, undershooting consensus forecasts for a fourth straight month. The annualized core inflation rate has decelerated to 1.7% over the past three months—the clearest sign yet that disinflationary momentum is holding despite tariffs.

Year-over-year, the CPI nudged higher to 2.4%, while the core CPI was unchanged at 2.8%. The short-run trend shows even more progress, with the headline CPI advancing at just 1.0% pace the past three months, and the supercore—which strips out food, energy, and shelter—rising at only 0.1% pace over the same period and falling to just 2.8% year-to-year.

Real average hourly earnings rose 0.3% in May and are up 1.4% year-to-year. Weekly earnings improved by 1.5%. Higher real incomes are supporting consumer resilience against earlier price hikes for key necessities.

While prices are rising for some imported goods, tariffs have yet to show up in the inflation data.

Core goods prices fell again in May, with new vehicles down 0.3% and used vehicles falling 0.5%. Apparel prices—widely expected to rise due to tariffs—surprisingly fell 0.4%. In contrast, prices firmed for tech products, household appliances, and motor vehicle parts, suggesting early-stage pressures are building beneath the surface. Inventories are tightening, particularly for autos, and restocking at higher input costs may push goods prices higher later this year.

We have emphasized repeatedly that inflation is, at its core, a monetary phenomenon. Tariffs are likely to raise prices on tradable goods, especially those lacking viable substitutes. However, if consumers are forced to spend more on higher-priced imports, they will have less discretionary income for other goods and services—unless the Federal Reserve eases aggressively. So far, the Fed has remained cautious, and money growth has stayed modest. That restraint helps explain the better-than-expected inflation data.

If consumers spend more on higher-priced imports, they will have less to spend elsewhere.

Moderating prices for groceries and gasoline are helping to offset tariff-related pressures. Energy prices fell 1.0% in May, driven by a 2.6% decline in gasoline. West Texas Intermediate crude briefly dropped to $60 per barrel last month but has since rebounded on rising Mideast tensions. As such, the relief from lower gas prices seen this spring may fade this summer.

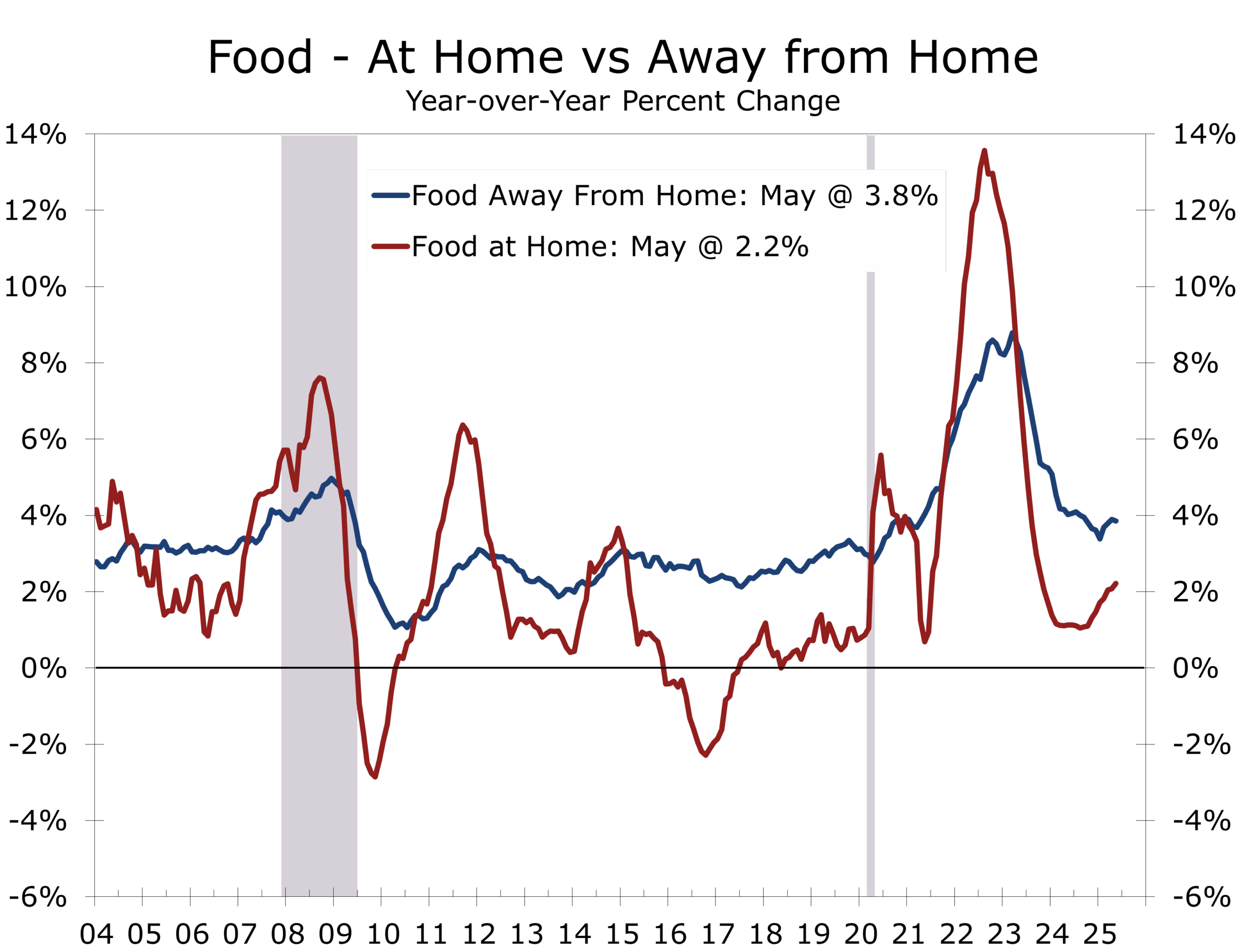

Food prices rose 0.3% in May after a 0.1% dip in April. Grocery inflation was mixed: three of six major food-at-home categories rose, led by cereals and bakery products (+1.1%) and “other food at home” (+0.7%), while prices for meats, poultry, fish, and eggs fell 0.4%—driven by a 2.7% drop in egg prices. Restaurant inflation remained steady, with both full-service and limited-service meals up 0.3%. On a year-over-year basis, prices at the grocery store are up 2.2%, while the costs of dining out continues to rise faster, climbing 3.8%.

Discretionary Services Lead the Decline

Core services inflation slowed again. Airline fares fell 2.7%, hotel prices dipped 0.1%, and recreation services declined for a second month. Medical care costs also moderated. These categories are most likely to soften if consumers shift spending toward higher-priced imports. The drop in discretionary services may reflect front-loaded purchases of imported big-ticket items ahead of tariff hikes, reducing spending—and price pressure—elsewhere.

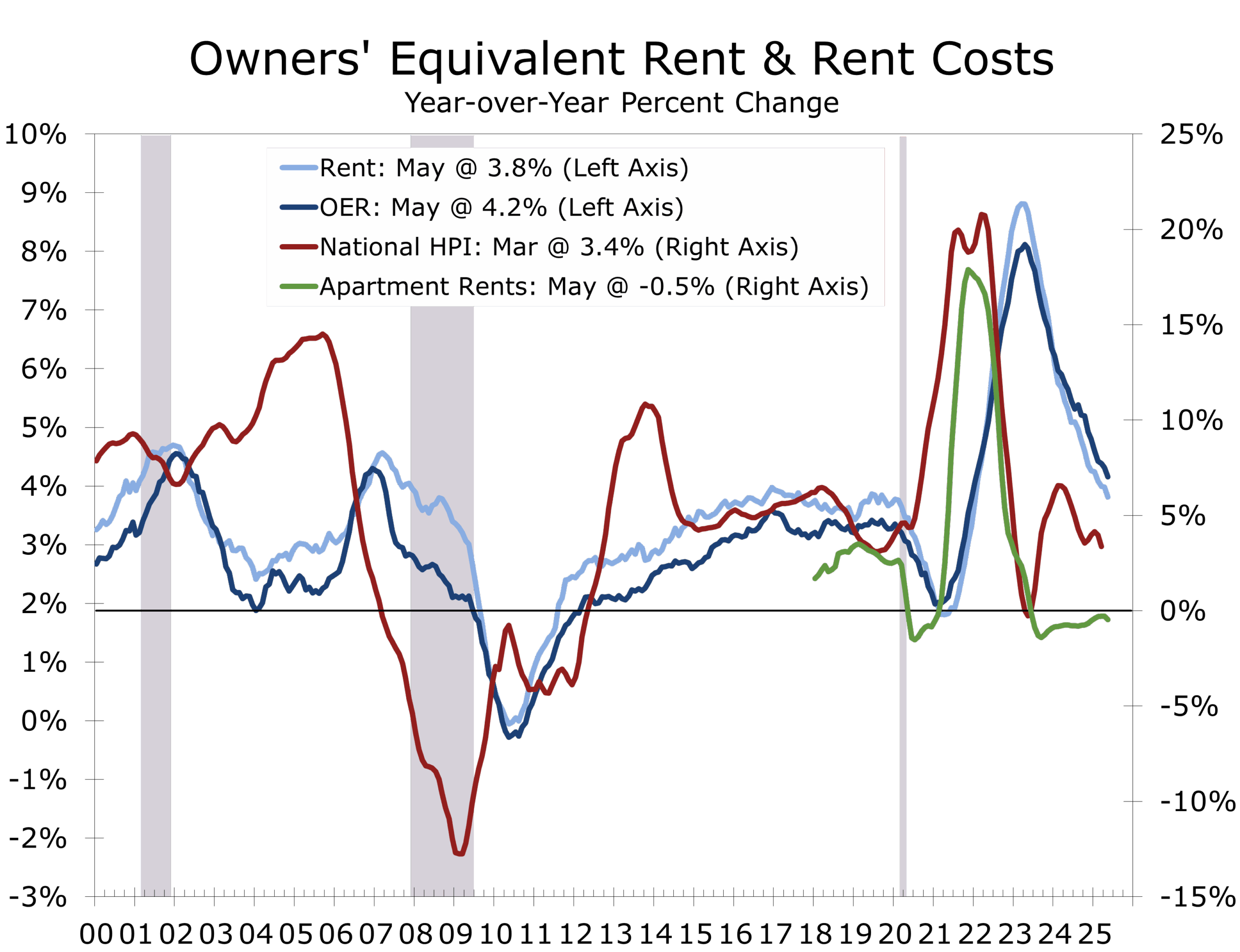

Shelter remains sticky—owners’ equivalent rent (OER) and primary rent each rose 0.3%—but signs of moderation are emerging. A surge in apartment completions has cooled rent growth, while rising for-sale inventories have helped ease home price gains.

Fed Outlook: Steady for Now, but Cuts are Coming

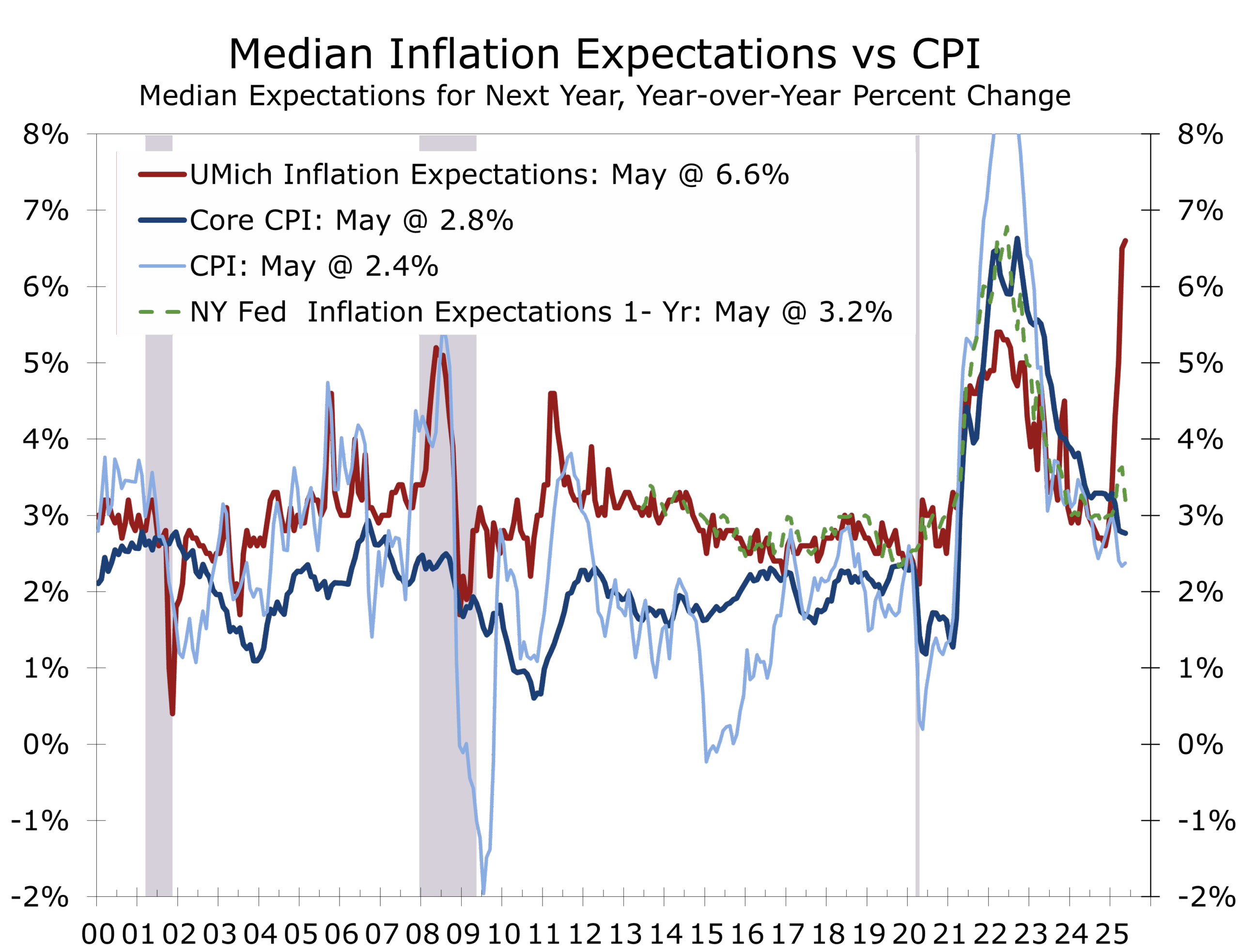

The Federal Reserve is expected to hold rates steady at its June meeting. While tariffs have not yet driven broad inflation, base effects will fade by July, and seasonal demand combined with tightening vehicle inventories could push prices higher. Tariff impacts may appear first in producer prices, but the Federal Reserve will take comfort in the latest inflation data. Still, policymakers want to see heightened inflation expectations ease before cutting interest rates.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

June 11, 2025

Mark Vitner, Chief Economist

704-458-4000