More of a Touch and Go Rather Than a Typical Soft Landing

- After a volatile first half marked by rapid tariff escalation and market swings, the reciprocal tariff regime is now largely in place. Early progress in trade negotiations with key allies suggests uncertainty could ease later this year and into 2026, reducing market risk premiums and supporting a more stable investment environment.

- Strong productivity gains, driven in part by AI adoption, and tighter immigration enforcement are reshaping labor supply and demand. This is producing a bifurcated labor market—tight for blue-collar and service roles, yet increasingly slack in many white-collar professions—creating complex challenges for wage growth and policy decisions.

- Consumer spending is slowing as softer job and income growth collide with higher prices for imported goods. Tariff pass-through is expected to increase in the second half, shifting spending toward essentials and putting added pressure on lower-income households, while higher-income consumers remain relatively resilient.

- Capital spending, previously delayed by policy uncertainty, is showing signs of acceleration. Clearer trade rules are unlocking postponed projects, with reshoring, supply chain diversification, and strategic infrastructure—including data centers and energy investments—set to drive business investment into 2026.

- While higher interest rates and tariff uncertainty have temporarily slowed momentum, the economy is positioned to regain altitude, supported by a backlog of capital projects, easing financial conditions, and a likely September Fed rate cut. However, the total number of cuts may be fewer than markets anticipate.

- Geopolitical developments—including the Alaska summit on Ukraine, the escalation in Gaza, and the expiration of the U.S.–China tariff truce—are key variables for markets. Alliance cohesion and trade negotiation outcomes will shape risk sentiment and global trade flows in the coming months.

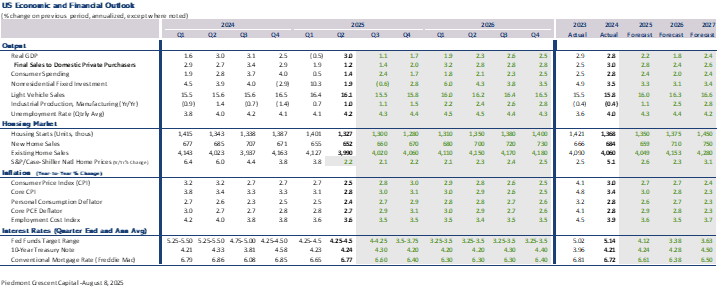

- Outlook: We expect U.S. GDP growth to moderate to 1.3% in 2025 before reaccelerating to 2.3% in 2026 and 2.6% in 2027 (Q4/Q4). Growth will increasingly be driven by business investment, with housing and trade gradually improving as interest rates and policy clarity provide lift.

Macro Outlook – Something Beyond a Typical Soft Landing

The U.S. economy enters the second half of 2025 with momentum slowing but not stalling. After turbulence in April and May—marked by volatile markets, trade policy uncertainty, and softer consumer spending—conditions have steadied. Recession risk has eased, replaced by a more nuanced outlook: a brief deceleration followed by a cautious reacceleration as clarity improves on multiple fronts.

Rather than a smooth soft landing, the path ahead resembles a “touch and go.” In aviation, this maneuver involves landing and immediately taking off without coming to a full stop—a staple of naval carrier practice and an occasional necessity for commercial pilots when margins narrow. For the economy, the analogy fits: a short slowdown under the weight of higher interest rates and policy uncertainty, followed by renewed lift from capital investment, clearer trade rules, and a long-anticipated easing in monetary policy.

One of the largest sources of uncertainty earlier this year—the rapid escalation and down-to-the-wire negotiations over tariffs—has shifted into a more stable phase. After sending the economy on a wild ride in the first half, the reciprocal tariff regime is now largely in effect. We expect agreements with China and other key nations to emerge later this year or in early 2026. The initial adjustment period produced sharp swings in trade flows—import frontloading in Q1 subtracted about five percentage points from GDP growth, only to reverse in Q2 and add a comparable boost as imports normalized. Beneath this volatility, core domestic demand expanded just 1.2% in Q2, its slowest pace since late 2022.

While the U.S. effective tariff rate has climbed above 15%, the latest measures spared China from new penalties, limiting the risk of major supply disruptions. Financial markets have taken the changes in stride, and some uncertainty has given way to greater policy clarity. Early progress in trade talks suggests the policy backdrop could become less volatile later this year and into 2026. Markets now appear to have a better read on the administration’s trade strategy and are pricing in a potential deal with China and other major partners within the next year.

High tariffs will continue to act as a “tax-like” constraint on consumers and certain industries, but the near-term bite has been milder than feared. Much of the initial impact on prices was muted as businesses stockpiled goods ahead of implementation, absorbed costs through lower margins, and cut expenses. Those buffers are now largely exhausted, and more tariff impact is likely to pass through to prices in the second half, potentially pushing inflation back toward—or slightly above—3%.

Economic growth is expected to run below potential in the second half—around 1.3% annualized—as weaker real income growth, persistent housing market softness, and lingering policy uncertainty offset tailwinds from inventory restocking and a narrowing trade gap. Still, with the tariff regime more predictable, financial conditions easing, and the prospect of Fed rate cuts ahead, the runway for a late-2025 or early-2026 pickup in growth is beginning to clear. Lower interest rates should help ensure a safe climb-out.

Productivity Gains and Tighter Immigration Enforcement Reshape the Labor Market

The July employment report confirmed that the labor market is slowing more decisively. Nonfarm payrolls rose just 73,000, and downward revisions erased a combined 258,000 jobs from May and June. Over the past three months, job growth has averaged only 35,000—a pace well below replacement levels. The unemployment rate ticked up to 4.2% (4.24% unrounded), but this masks underlying weakness: labor force participation fell to 62.2%, the lowest since the economy’s initial ascent from the pandemic, and the employment-population ratio slipped to 59.6%. Long-term unemployment rose by 179,000 to 1.8 million, now nearly one-quarter of total unemployed.

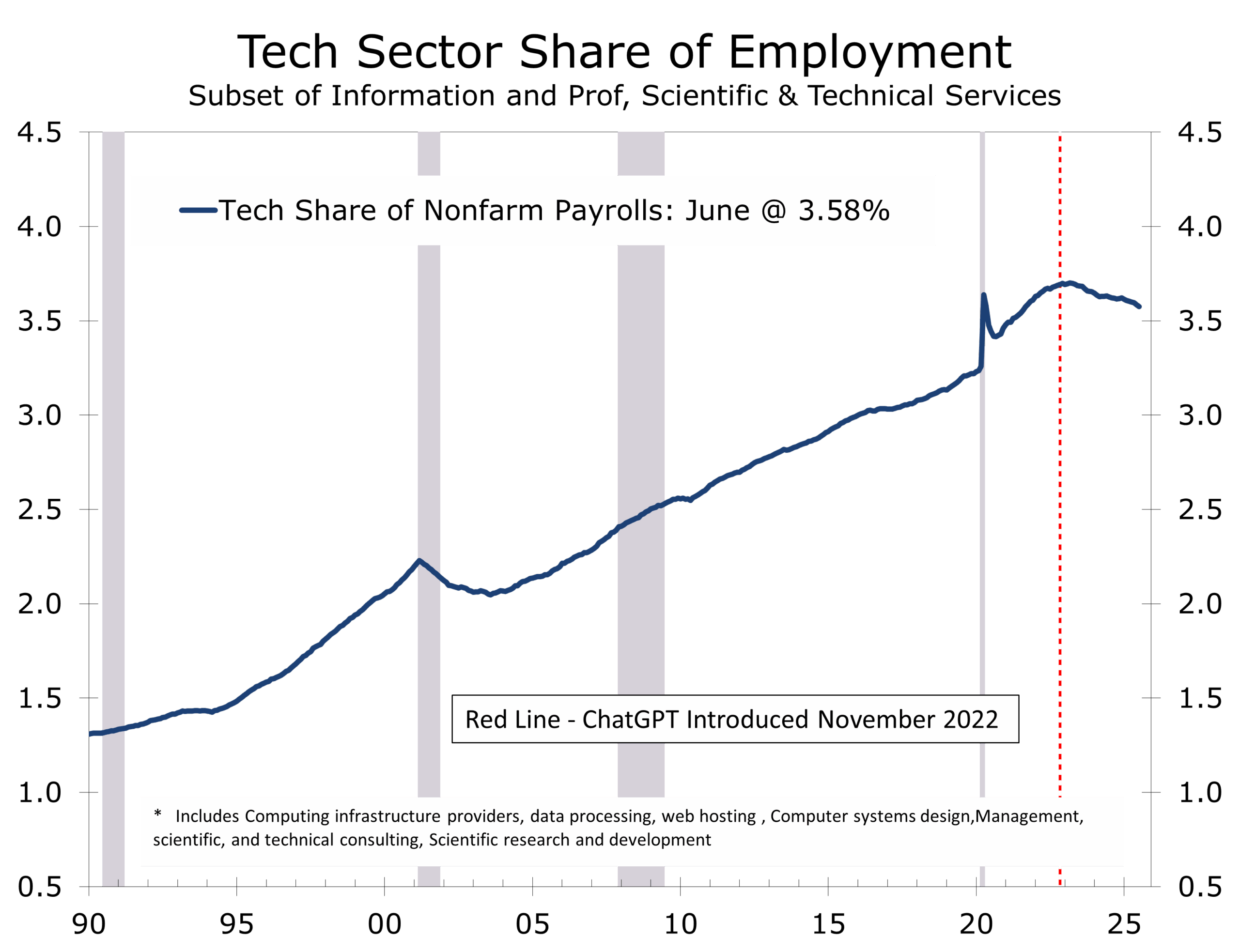

Layoffs are edging higher but remain historically low. Instead, the market is characterized by unusually low turnover—fewer firings but also fewer hirings. Productivity gains, partly driven by increased AI use, are contributing to this dynamic. Nonfarm productivity grew at a 2.4% annualized pace in Q2. Employment in a narrow set of information technology industries has fallen sharply, losing 12,300 jobs in June and seeing its share of nonfarm employment decline steadily since ChatGPT debuted in November 2022.

Hiring in sectors such as tech, finance, and business services is flat or contracting, leaving many new graduates facing an unexpectedly tough job market. By contrast, blue-collar and service roles remain tight, particularly in construction, manufacturing, logistics, and healthcare. Stricter immigration enforcement and accelerating retirements are constraining labor supply in these sectors, keeping wage pressures elevated despite slower overall hiring.

Wages remain firm, rising 0.3% in July and 3.9% year-over-year, with stronger gains in lower-paying, labor-intensive industries. This divergence—slack in white-collar work alongside persistent shortages in blue-collar roles—marks a reversal from prior labor cycles. We expect businesses to accelerate investment in automation and training programs to offset constrained labor supply in trade and service occupations, reshaping the job market in the second half of the decade.

The unevenly cooling labor market also creates a dilemma for policymakers. Easing wage pressures in white-collar sectors provide some room to cut interest rates, but sustained inflation risk from persistent blue-collar shortages limits how aggressive the Fed can be. The challenges to living standards also raise important questions for elected officials and are helping drive populist sentiment across the political spectrum.

Consumer Spending – Losing Altitude Amid Higher Prices and Softer Incomes

Consumer spending is losing momentum as softer job and income growth collide with persistently high prices for imported goods. Employment concerns are building as hiring plans slow across a wide range of industries, leaving middle- and lower-income households squeezed by tighter budgets, reduced discretionary outlays, and a growing reliance on savings or consumer credit to maintain basic consumption. Rising credit utilization in these groups signals that the cushion from pandemic-era savings has largely been depleted.

The strain is uneven across the income distribution. High-income households—buoyed by strong equity market gains, rising home values, and relatively secure employment—still account for more than half of total consumer spending. Lower-income families face greater exposure to tariff-driven price increases on necessities, thinner savings buffers, and reduced government support, such as cuts to nutrition assistance programs. The result is a bifurcated spending environment: affluent households continue to drive demand in premium goods, travel, and high-end services, while lower-income households cut back in discretionary retail, dining, and entertainment.

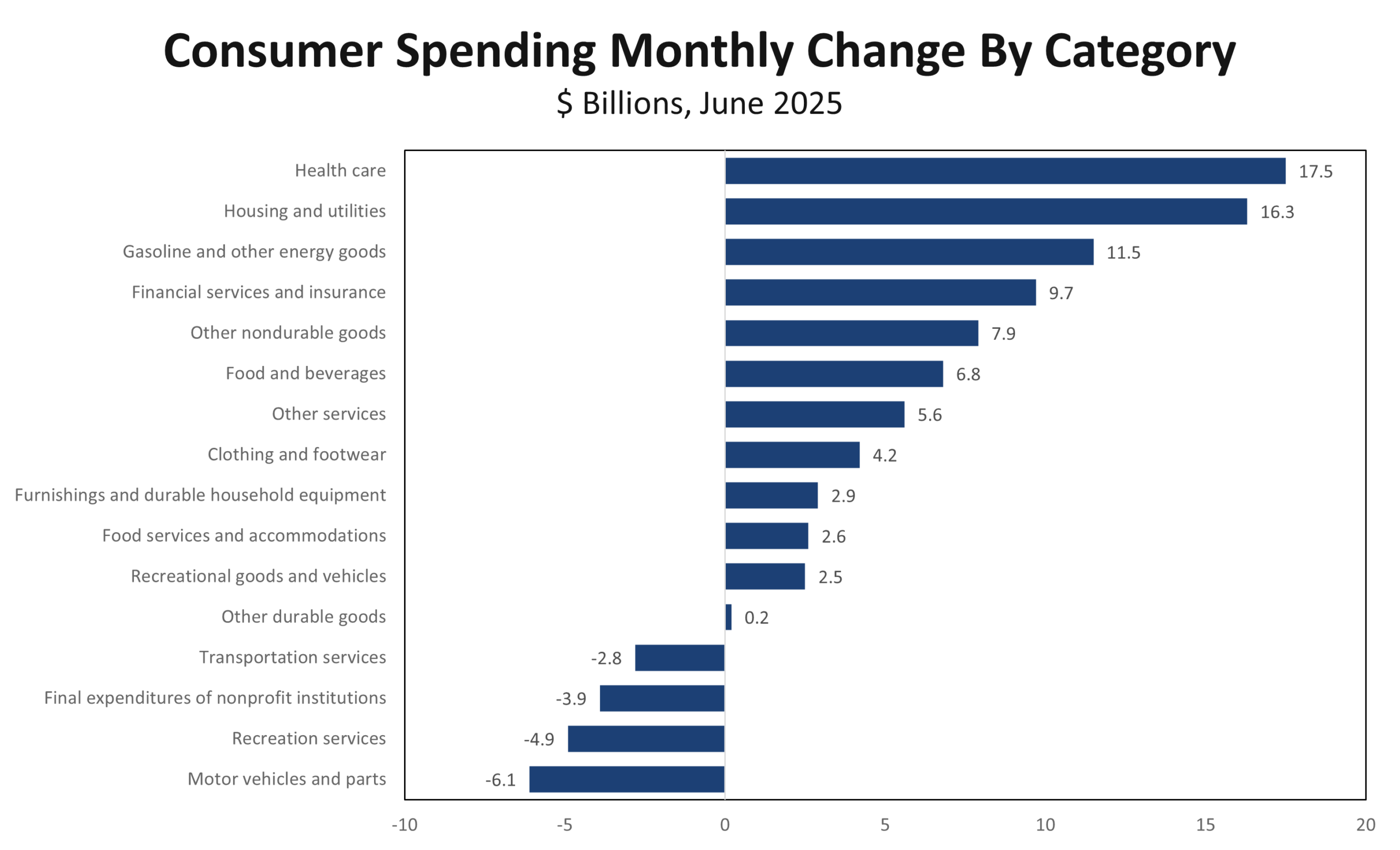

Tariffs are amplifying the pressure. Early mitigation—via import frontloading, margin compression, and cost cuts—has largely run its course, raising the likelihood of more direct pass-through to consumer prices in the second half. With goods inflation poised to edge back toward or slightly above 3%, households are shifting spending toward staples and away from non-essentials. Recent retail and services data confirm the pivot, with grocery and household goods outperforming, while apparel, electronics, and other discretionary categories lag.

Tighter credit conditions are compounding the slowdown. While an expected Fed rate cut later this year should lower borrowing costs, banks are raising lending standards, especially for households with weaker credit profiles. Credit card delinquency rates are climbing, led by younger borrowers and lower-income households. Mortgage refinancing could provide some relief, but the benefits are concentrated among middle- and upper-income households with strong equity positions—leaving the most financially vulnerable with limited options.

Taken together, the consumer sector is transitioning from broad-based strength to a more fragile and uneven footing. Continued resilience among high-income households should prevent a sharp collapse in aggregate spending, but persistent drag from middle- and lower-income groups will weigh on consumption growth through year-end. For policymakers, the challenge will be ensuring that rate cuts, while supportive, do not disproportionately benefit those least constrained, leaving the regressive impact of tariffs and inflation largely intact for the households that feel it most.

Capital Spending – From Standby to Full Throttle

After a year of hesitation, capital spending appears set to regain altitude as clarity on trade policy begins to filter through the corporate sector. The reciprocal tariff regime, now largely in place, has reduced the day-to-day policy uncertainty that kept many projects on hold through the first half of 2025. With the rules of engagement more clearly defined—and early signs of progress in negotiations with key allies—firms are dusting off deferred investment plans, particularly in sectors where long lead times make planning stability essential.

Manufacturers are at the forefront. Reshoring and supply chain diversification efforts, accelerated by recent geopolitical tensions, have sparked renewed investment in domestic production capacity. Industrial construction pipelines are filling, driven primarily by the need to build massive data centers to support the accelerating rollout of AI and by restructuring projects tied to defense and national security. Energy projects are also moving forward, with natural gas viewed as the fastest option to ramp up output. Small modular nuclear reactors are generating significant interest and investment, but working models remain years away. Wind and solar projects are progressing more cautiously and must stand on their own to a greater degree than in the past.

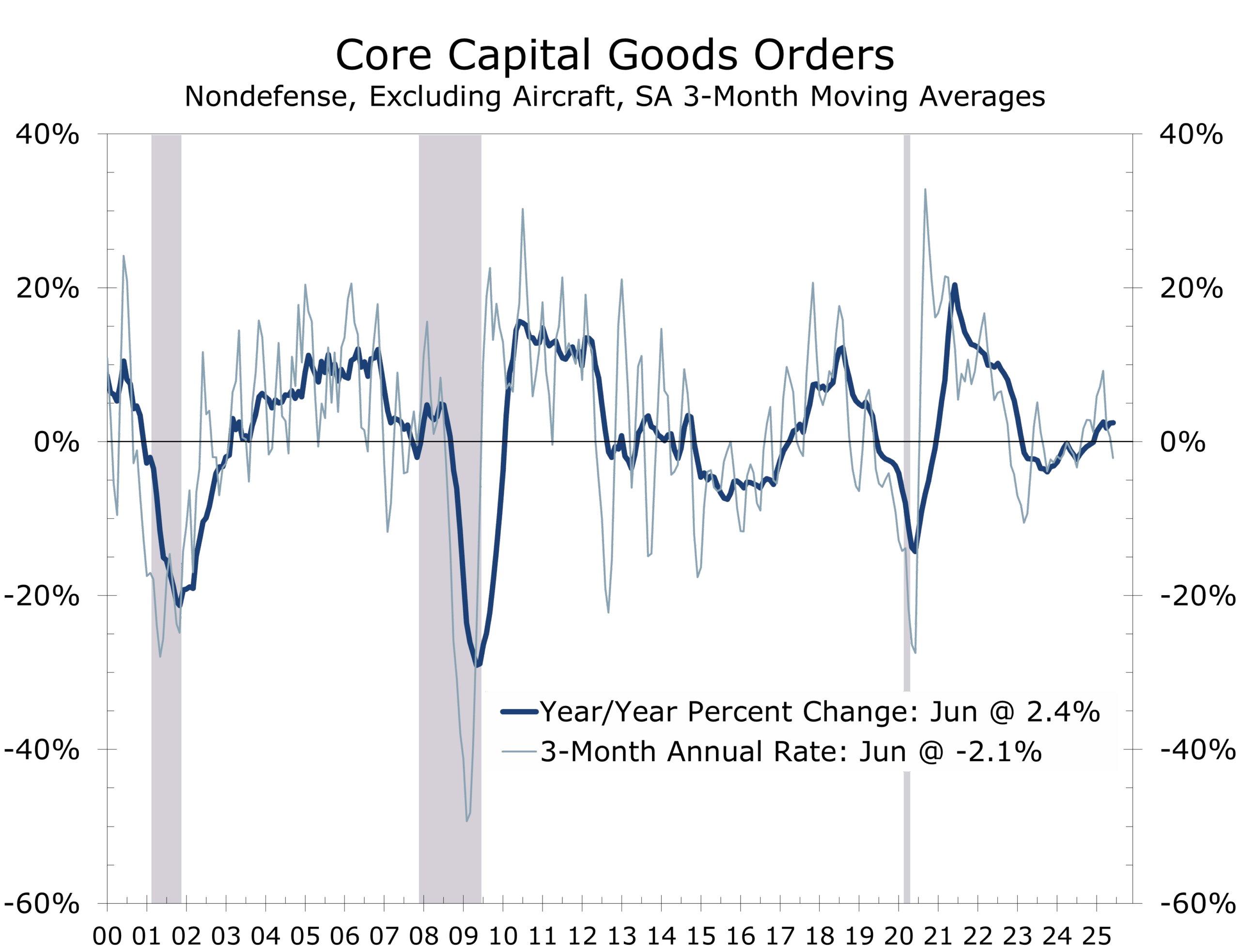

The thaw is not limited to heavy industry. Technology, logistics, and advanced manufacturing firms are expanding capacity to capture market share in growth segments—semiconductors, AI-driven data infrastructure, and electric vehicle supply chains. Commercial equipment orders, which flattened earlier this year, are expected to rebound in the second half as companies position for strengthening demand in 2026 and beyond. Clearer trade rules have improved supply chain predictability, reducing risk premiums in project budgets and freeing capital for deployment.

While elevated interest rates and a strong dollar had been drags on investment, both headwinds are easing. Treasury yields have drifted lower in anticipation of a September Fed rate cut, and corporate bond spreads remain tight, offering favorable financing conditions for well-rated issuers. For small and mid-sized firms, credit remains tighter, but even here the prospect of lower rates and clearer trade policy is helping restore confidence.

Taken together, these shifts suggest the capital spending cycle is moving from standby into taxiing for takeoff—a stage where project pipelines are being reactivated, contracts are being signed, and financing is being secured, but full-scale execution is still a few months ahead. The combination of a backlog of deferred projects, targeted reshoring initiatives, and improving financing conditions should carry this momentum into a more robust expansion phase beginning in late 2025 and into 2026. With corporate balance sheets generally healthy and supply chain bottlenecks easing, the next leg of the expansion will be driven less by the consumer and more by strategic capital deployment across key sectors—echoing the tech boom of the late 1990s.

Monetary Policy – Cleared for Landing, but a Short Runway Ahead

The Fed appears increasingly likely to begin its descent from restrictive policy at the September FOMC meeting. Softer labor market readings and a loss of altitude in consumer spending have brought rate cuts onto the active flight plan. Market pricing now implies near-certainty of a quarter-point move, with many forecasters expecting five or six cuts over the next year. We see a shorter flight path—three or four cuts at most—as inflation remains above target, tariff-related price pressures are still ahead, and the economy, while slowing, is not yet in a hard-landing trajectory.

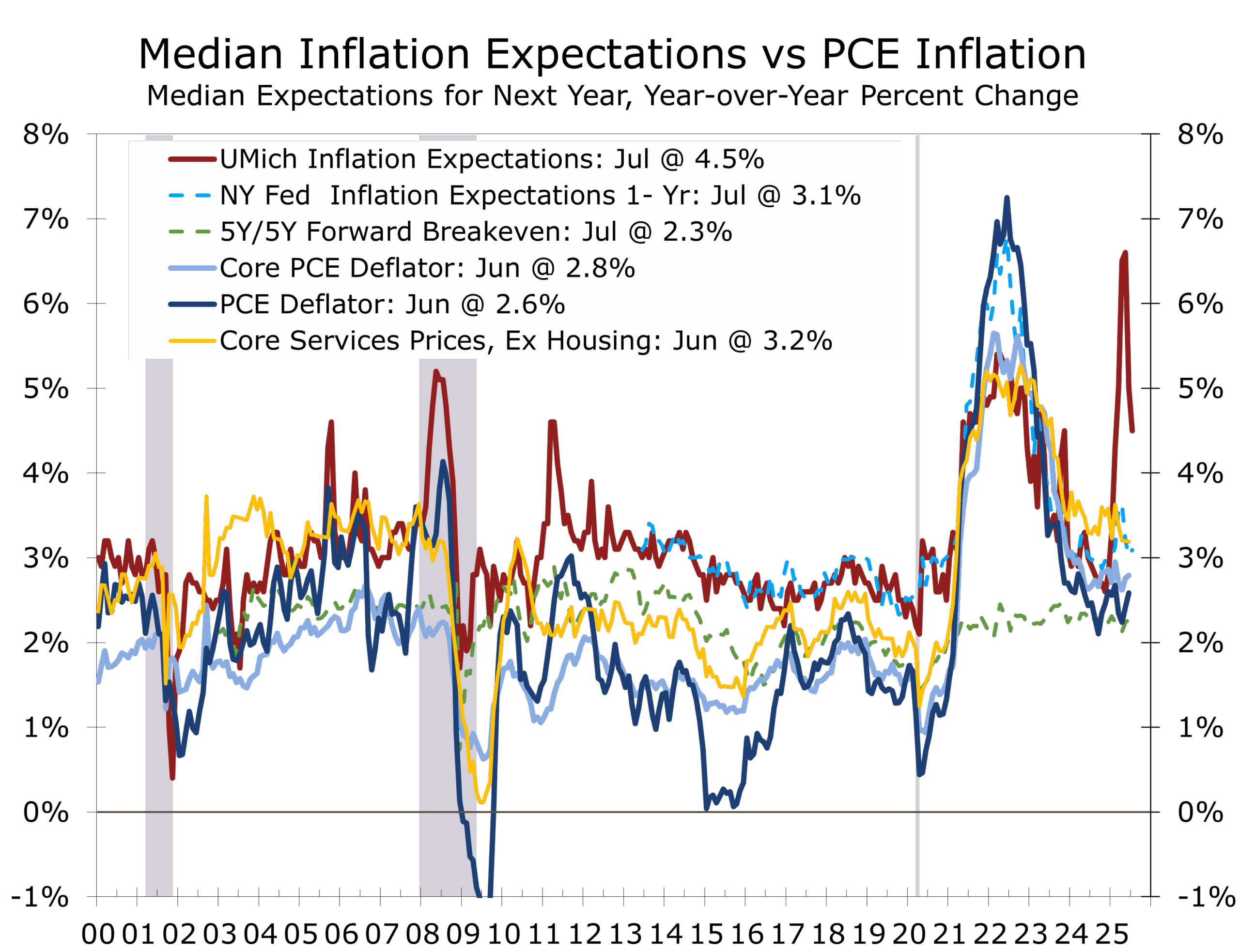

Recent inflation readings underscore the Fed’s balancing act. Core PCE rose to 2.8% year-over-year in June, up from its spring lows, and is likely to edge above 3% before leveling off. This uptick should be temporary, but it comes at a politically sensitive moment—much like hitting turbulence on approach—complicating the optics of easing. Goods prices in tariff-exposed categories such as electronics, autos, and apparel are climbing, while consumers have responded by pulling back on discretionary services, helping to cool inflation there. Wage growth, though down from its peak, remains firm at 3.9%, adding lift to inflation pressures. Productivity gains, now picking up, may give the Fed a little more room to maneuver.

From the Fed’s perspective, the runway is visible but with uncertain crosswinds. Financial conditions have already eased on expectations of a September cut, with Treasury yields drifting lower and equity markets climbing. Housing could be an early beneficiary: with the share of mortgages above 6% roughly doubling since 2021, even a modest rate drop could spur refinancing and sales. Credit-sensitive sectors such as autos and consumer durables could also see a tailwind, though tighter lending standards will keep some households grounded.

The Fed’s challenge will be to manage descent speed. Move too quickly and it risks reigniting inflation expectations; too slowly, and growth could stall before the aircraft is aligned with the runway. Unless incoming data show a sharper slowdown in jobs or inflation, the Fed is likely to keep subsequent cuts data-dependent rather than pre-set.

In short, September looks like the “cleared for landing” moment for rate cuts, but we expect the touchdown to be brief—three or four cuts at most—before the economy gains altitude again in 2026, propelled by capital spending, reshoring of critical industries, and a modest rebound in housing.

Geopolitics – Summits, Sieges, and Shifting Leverage

The mid-August Alaska summit is shaping up as a critical waypoint in the Ukraine war. Moscow’s floated ceasefire would freeze the front lines and cement Russian territorial gains, but Ukraine and its European allies countered on August 9 with a proposal that any talks begin only after a ceasefire or reduction in hostilities—starting from current front lines—and include robust security guarantees. The U.S. has signaled openness to a trilateral meeting including Zelensky, though Putin has resisted direct talks. The Kremlin’s strategy appears aimed at dividing Washington from Europe, portraying Ukraine and the EU as obstacles to peace while refusing to compromise on core war aims.

In the Middle East, Israel’s cabinet approval of a Gaza City seizure marks an aggressive escalation in the Gaza campaign. Prime Minister Netanyahu frames the move as decisive in defeating Hamas, but European and UN leaders have condemned it as worsening a humanitarian crisis. Germany has suspended certain arms exports, and a bloc of European UNSC members has reiterated calls for a halt to hostilities. The U.S. remains firmly in Israel’s corner—reinforcing perceptions that Washington will fly solo when strategic imperatives outweigh multilateral alignment.

These parallel conflicts intersect with U.S.–China trade negotiations. The 90-day tariff truce expires August 12, just days before the Alaska summit. Beijing is watching closely to see if the U.S. maintains coordinated allied altitude or drifts toward transactional, bilateral deals. A U.S.–Russia arrangement that sidelines Europe, or growing isolation over Gaza, could embolden China to demand more favorable terms, delay market access, or resist export controls. Conversely, disciplined allied formation on Ukraine would strengthen Washington’s negotiating position.

Policy Watch – Industrial Policy for a China 2.0 World

Nvidia and AMD will remit 15% of China-related AI-chip revenue to the U.S. in exchange for export licenses—an unprecedented blend of export control and fiscal capture. The move could trim gross margins and pressure both stocks, while aligning with the administration’s broader shift toward state capitalism with American characteristics.

The U.S. response to China’s rise is moving beyond traditional free-market playbooks toward a more direct state role in steering capital, shaping industries, and linking economic policy to geopolitical goals. Unlike the Cold War, this is not a binary contest between capitalism and communism. China is the world’s second-largest economy, firmly in the communist camp politically, but using capitalist tools to generate growth.

The U.S., by contrast, remains a capitalist system increasingly willing to use the state as a strategic instrument. Tariffs, investment controls, sovereign wealth funding, and corporate leverage are now policy tools aimed at securing strategic advantage. This shift will likely endure and may define how market economies contend with China’s command-and-control model.

Economic Outlook – Touch and Go Landings Require a Skilled Pilot

With tariffs now largely finalized with many trade partners, we expect a base tariff of between 10% and 15%, with higher rates on China and on goods transshipped through third countries by China. An updated USMCA is likely next year, strengthening the North American trade alliance. The effective U.S. tariff rate should settle between 15% and 20%, with China’s near 35%.

Comparisons to the 1930s Smoot-Hawley tariffs are overstated. Goods account for only about one-third of consumption today versus 75% then, reducing the economy-wide impact. Still, greater tariff pass-through in the second half will push headline inflation higher, complicating the Fed’s balancing act. We expect quarter-point cuts at the September, October, and December FOMC meetings, with a possible January cut if growth disappoints.

By spring, stronger economic growth should emerge, increasingly driven by business fixed investment. Home sales and construction should see a modest rebound once mortgage rates fall near 6%. We project real GDP growth of 1.3% in 2025, 2.3% in 2026, and 2.6% in 2027, measured from Q4 to Q4.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

August 12, 2025

Mark Vitner, Chief Economist

704-458-4000