Cooling Without Cracking

-

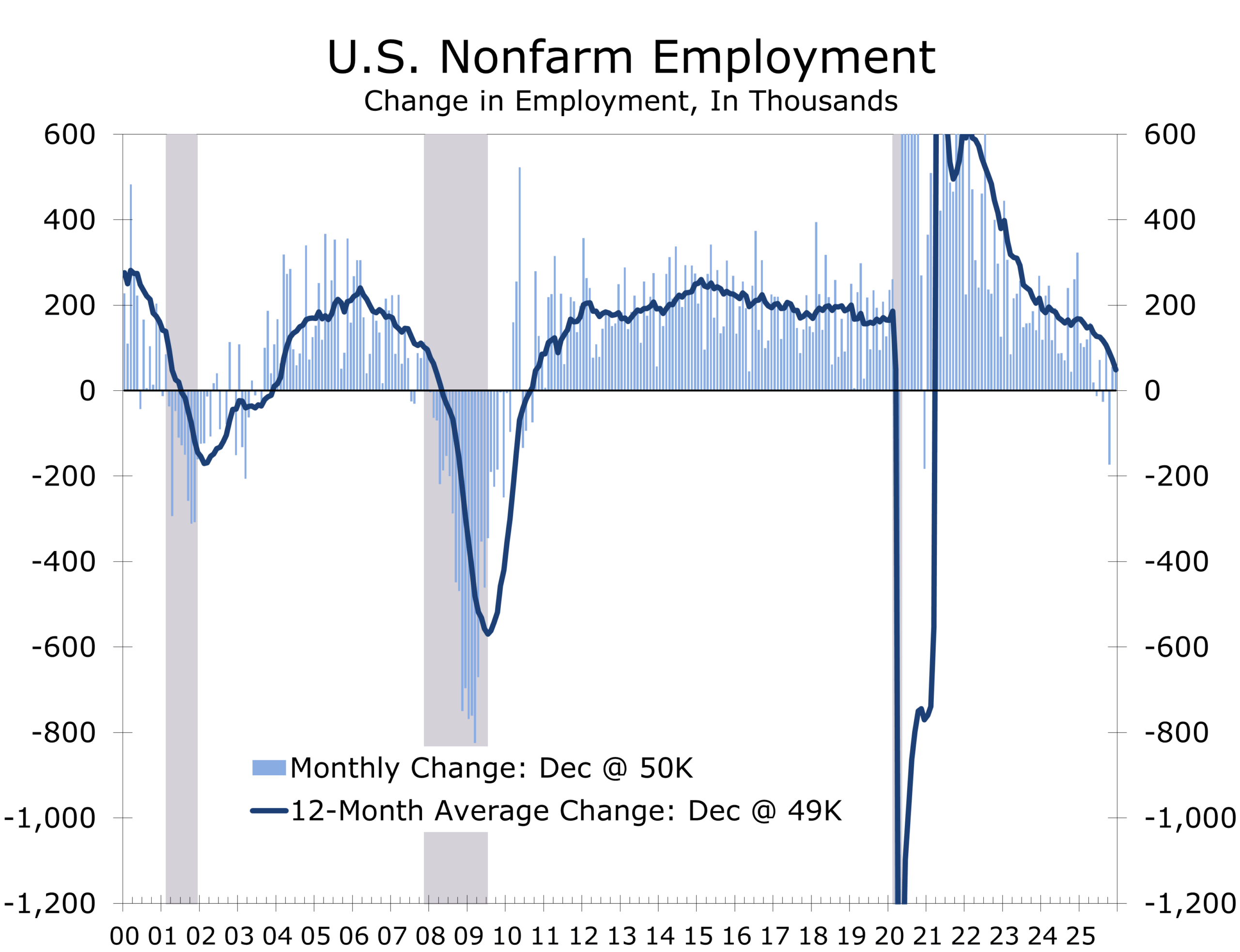

- Payroll growth remains subdued. Nonfarm payrolls rose 50,000 in December, extending the stall-speed pace of job growth that has prevailed through much of the second half of 2025.

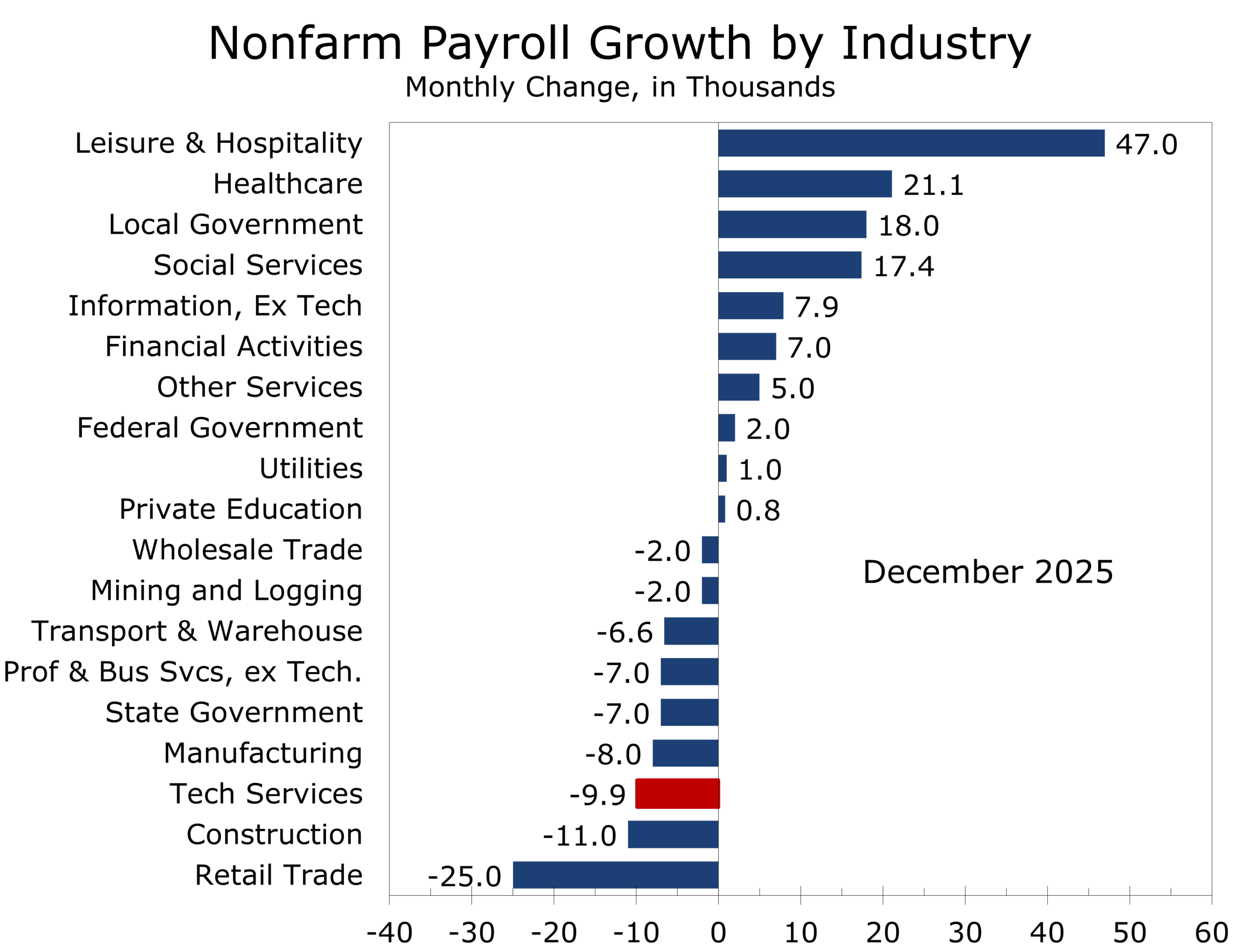

- Job gains remain narrowly concentrated in health care, social assistance, and food services. Most other major sectors showed little or no change.

- The unemployment rate held at 4.4%, unchanged on the month, but measures of labor underutilization continue to creep higher.

- Wage growth continues to cool. Average hourly earnings rose 0.3% in December and are up 3.8% year over year, consistent with a disinflationary labor market.

- Unemployment is drifting higher—but unevenly. The jobless rate rose to 4.6%, the highest since October 2021, driven largely by labor-force reentrants and concentrated among younger workers.

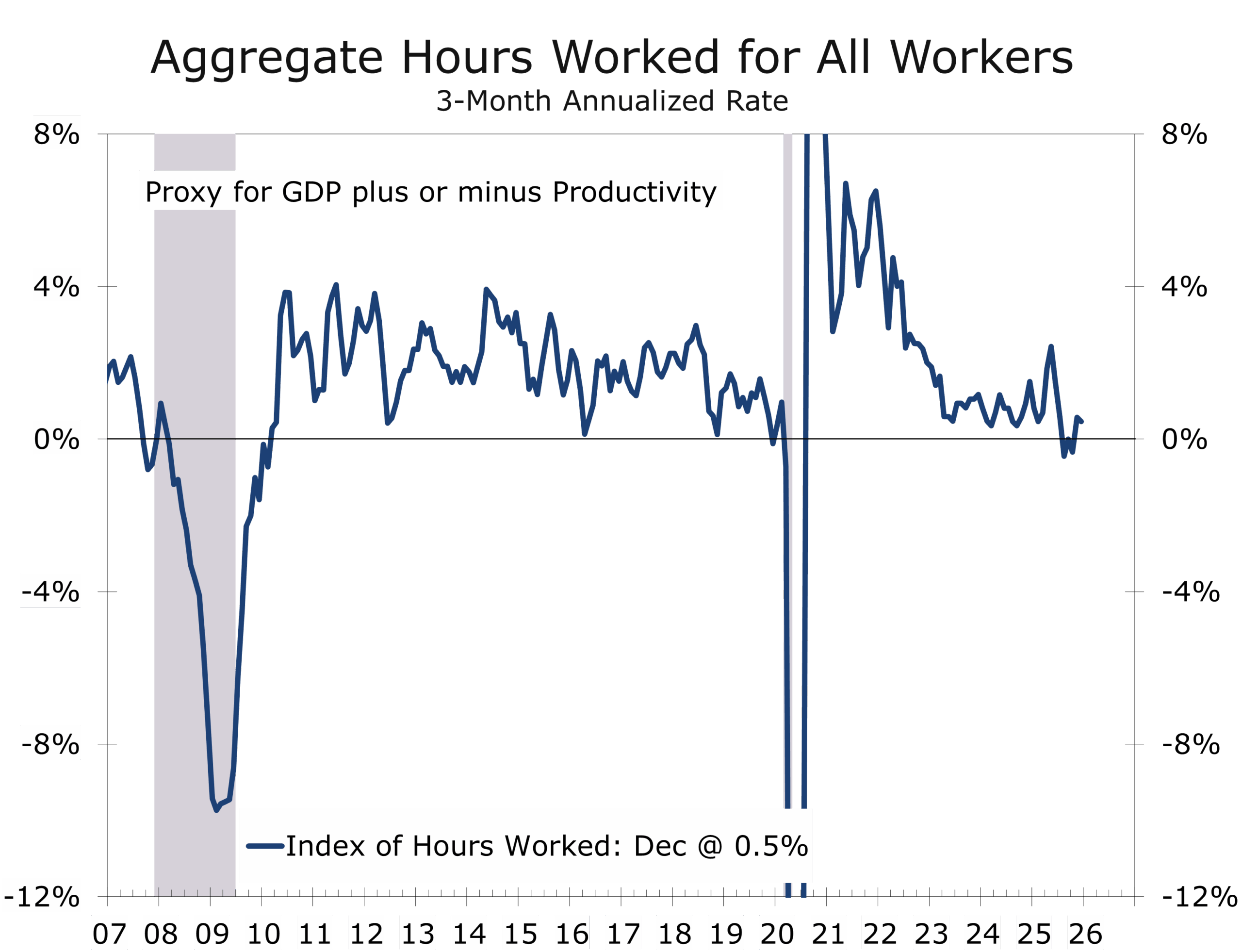

- Hours worked declined again. Firms continue to manage labor input through hours rather than headcount, a classic late-cycle adjustment.

- The December jobs report supports a policy pause: Federal job cuts and reduced hours mask private-sector resilience, while cooling wages and solid productivity argue for the Fed to hold rates steady in January rather than respond to labor-market stress.

Momentum Fades as Slack Continunes to Gradually Build

December’s employment report confirms that the U.S. labor market is no longer tightening and is instead operating in a lower-growth, mid-cycle equilibrium. Payroll gains of 50,000 were modest, and downward revisions to October and November subtracted a combined 76,000 jobs, reinforcing the view that underlying momentum has been softer than initially reported.

Employers added just 584,000 net new jobs in 2025, a sharp deceleration from the 2.0 million job gain in 2024. Hiring is no longer keeping pace with prior expansionary norms, but neither is it collapsing. This is an economy cooling without breaking.

Job growth has slowed to a pace that barely offsets labor-force growth.

Job Growth Barely Offsets Labor Force Expansion

The unemployment rate remained at 4.4%, with 7.5 million unemployed, little changed on the month. The labor force participation (62.4%) and the employment-population rate (59.7%) were also stable, suggesting that headline labor market conditions remain resilient amidst a lingering hiring slowdown.

Beneath the surface, however, slack continues to accumulate. Long-term unemployment rose to 1.9 million, accounting for 26% of all unemployed, and is up nearly 400,000 over the year. This reflects a labor market where re-employment is becoming more difficult at the margin.

At the same time, part-time employment for economic reasons climbed to 5.3 million, nearly 1 million higher than a year ago, indicating that firms are increasingly trimming hours rather than payrolls.

Underemployment is rising even as the headline unemployment rate remains stable.

Hiring Remains Narrow and Service-Sector Heavy

Sectoral detail underscores the late-cycle character of the labor market. Food services and drinking places added 27,000 jobs. Health care employment rose by 21,000, led by hospitals. Social assistance increased by 17,000, primarily in individual and family services. These categories account for virtually all net job creation in December.

Elsewhere, hiring stalled. Manufacturing, construction, professional and business services, financial activities, information, wholesale trade, and transportation and warehousing all showed little or no change. Hiring within the tech sector is a notable soft spot, with tech employers cutting 9,900 jobs in December and 61,000 jobs over the past 12 months.

Retail trade lost 25,000 jobs, concentrated in general merchandise and grocery stores. This appears structural rather than cyclical, reflecting productivity gains, automation, and ongoing shifts in retail formats rather than a sudden pullback in consumer demand. The drop was also exaggerated by seasonal factors.

Federal government employment was little changed in December but remains a significant drag. Since peaking in January, federal payrolls are down 277,000 jobs, or 9.2%, reflecting post-pandemic normalization and DOGE-related retirements. These cuts continue to distort headline payroll growth and mask modest private-sector resilience.

Average hourly earnings rose 0.3% in December and are up 3.8% year over year, a pace consistent with the Federal Reserve’s inflation objective when paired with productivity growth. The average workweek edged down to 34.2 hours, while the manufacturing workweek slipped to 39.9 hours. Overtime hours were unchanged, and aggregate hours worked fell 0.3% in December and rose at just a 0.5% annualized pace in the fourth quarter.

The adjustment continues to occur through hours rather than headcount, signaling caution without distress. Productivity remains sufficient to support real GDP growth near 2.5% in the fourth quarter.

This is not a collapsing labor market. It is a rebalancing one. Hiring has slowed materially, wage growth is cooling, and underutilization is rising at the margins. Yet layoffs remain contained, participation is stable, and service-sector demand continues to absorb labor.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 9, 2026

Mark Vitner, Chief Economist

(704) 458-4000